UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

¨REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

xANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2015

OR

¨TRANSITIONAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

¨TRANSITIONAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report _________

For the transition period from _________ to __________

Commission file number 001-37655

CHINA CUSTOMER RELATIONS CENTERS, INC.

(Exact Name of registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

British Virgin Islands

(Jurisdiction of incorporation or organization)

c/o Shandong Taiying Technology Co., Ltd.

1366 Zhongtianmen Dajie, Xinghuo Science and Technology Park, Hugh-tech Zone, Taian City, Shandong Province,

People’s Republic of China 27100

(Address of principal executive offices)

Zhili Wang

c/o Shandong Taiying Technology Co., Ltd.

1366 Zhongtianmen Dajie, Xinghuo Science and Technology Park, Hugh-tech Zone, Taian City, Shandong Province,

People’s Republic of China 27100

Tel: (+86) 538 691 8899

Email:ir@ccrc.com

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | | Name of Exchange on which registered |

| Common Shares, $0.001 par value per share | | The Nasdaq Capital Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act:None

Securities for which there is a reporting obligation pursuant to Section 15(d):None

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report:18,329,600 outstanding common shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Not Applicable.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See the definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer¨ | Accelerated filer¨ | Non-accelerated filerx |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAPx | International Financial Reporting Standards as issued | Other¨ |

| | By the International Accounting Standards Board¨ | |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17¨Item 18¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes¨Nox

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13, or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes¨No¨

Table of Contents

Defined Terms and Conventions

Except where the context otherwise requires and for purposes of this annual report on Form 20-F only:

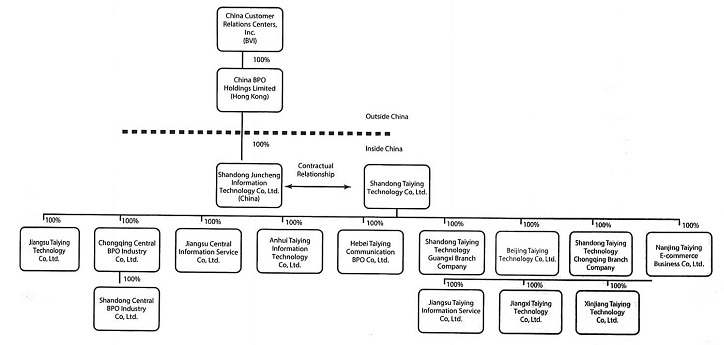

| ● | The terms “we,” “us,” “company” “our company,” and “our” refer to China Customer Relations Centers, Inc. and its wholly-owned subsidiaries and its affiliated entities, including our variable interest entities and their subsidiaries; |

| ● | China Customer Relations Center, Inc., a British Virgin Islands company (“CCRC” |

when referring solely to our British Virgin Islands listing company);

| ● | China BPO Holdings Limited, a Hong Kong company wholly-owned by CCRC (“CBPO”); |

| ● | Shandong Juncheng Information Technology Co., Ltd., a Chinese company wholly-owned by CBPO (“WFOE”); |

| ● | Shandong Taiying Technology Co., Ltd., an affiliated Chinese company that WFOE controls by virtue of contractual arrangements (“Taiying”); |

| ● | Chongqing Central BPO Industry Co., Ltd., a wholly-owned subsidiary of Taiying (“Central BPO”); |

| | | |

| | ● | Jiangsu Taiying Technology Co., Ltd., a wholly-owned subsidiary of Taiying (“JTTC”); |

| ● | Hebei Taiying Communication BPO Co., Ltd., a wholly-owned subsidiary of Taiying (“HTCC”); |

| ● | Shandong Central BPO Industry Co., Ltd., a wholly-owned subsidiary of Taiying (“SCBI”); |

| ● | Jiangsu Central Information Service Co., Ltd., a wholly-owned subsidiary of Taiying (“JCBI”); |

| ● | Anhui Taiying Information Technology Co., Ltd., a wholly-owned subsidiary of Taiying (“ATIT”); |

| ● | Shandong Taiying Technology Guangxi Branch Company, a wholly-owned branch company of Taiying (“STTGB”); |

| ● | Shandong Taiying Technology Chongqing Branch Company, a wholly-owned branch company of Taiying (“STTCB”); |

| ● | Hebei Taiying Technology Yanjiao Branch Company, a wholly-owned branch company of HTCC (“HTTYB”); |

| ● | Jiangsu Taiying Information Service Co., Ltd., a wholly-owned subsidiary of Taiying (“JTIS”); |

| | | |

| | ● | Jiangxi Taiying Technology Co., Ltd., a wholly-owned subsidiary of Taiying (“JXTT”); |

| ● | Xinjiang Taiying Technology Co., Ltd., a wholly-owned subsidiary of Taiying (“XTTC”); |

| ● | Nanjing Taiying E-Commerce Business Co., Ltd., a wholly-owned subsidiary of Taiying (“NTEB”); |

| | | |

| | ● | Beijing Taiying Technology Co., Ltd., a wholly-owned subsidiary of Taiying (“BTTC”); |

| | | |

| | ● | “shares” and “common shares” refer to our common shares, $0.001 par value per share; |

| ● | “Operating Companies” or “Operating Company” refer to, collectively or individually, as the case may be, to Taiying, Central BPO, BTTC, JTTC, HTCC, SCBI, JCBI, NTEB, STTGB, STTCB, JTIS, JXTT and XTTC; |

| ● | “China” and “PRC” refer to the People’s Republic of China, excluding, for the purposes of this annual report only, Macau, Taiwan and Hong Kong; |

| | | |

| | ● | “BPO” refers to business process outsourcing; |

| ● | “tier 1 cities” are to the term used by the National Bureau of Statistics of China and refer to Beijing, Shanghai, Shenzhen and Guangzhou; |

| ● | “tier 2 cities” are the 32 major cities, other than tier 1 cities, as categorized by the National Bureau of Statistics of China, including provincial capitals, administrative capitals of autonomous regions, direct-controlled municipalities and other major cities designated as “municipalities with independent planning” by the State Council; |

| ● | “MVAS” refers to mobile value-added services, such as weather, health, education and farming related products to targeted telecommunications subscribers; and |

| ● | all references to “RMB,” and “Renminbi” are to the legal currency of China, and all references to “USD,” and “U.S. Dollars” are to the legal currency of the United States. |

We refer to Taiying by name in discussing the entity that conducts our day-to-day BPO business in China and refer to “our company” when discussing our strategies, business plans, organization and other decision-making focused matters. Because we control Taiying by virtue of our ownership of WFOE and WFOE’s contractual rights to control the day-to-day operations and corporate activities of Taiying, we believe it would be misleading in most cases to discuss the business decisions of Taiying as though Taiying were at arm’s-length from our company.

For the sake of clarity, this annual report follows the English naming convention of first name followed by last name, regardless of whether an individual’s name is Chinese or English. For example, the name of our chief executive officer will be presented as “Gary Wang” or “Zhili Wang”, even though, in Chinese, his name would be presented as “Wang Zhili”.

FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements. All statements contained in this annual report other than statements of historical fact, including statements regarding our future results of operations and financial position, our business strategy and plans, and our objectives for future operations, are forward-looking statements. The words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” and similar expressions are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and trends that we believe may affect our financial condition, results of operations, business strategy, short-term and long-term business operations and objectives, and financial needs. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described in the “Risk Factors” section. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties and assumptions, the future events and trends discussed in this annual report may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements.

You should not rely upon forward-looking statements as predictions of future events. The events and circumstances reflected in the forward-looking statements may not be achieved or occur. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, or achievements. We are under no duty to update any of these forward-looking statements after the date of this annual report or to conform these statements to actual results or revised expectations.

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable for annual reports on Form 20-F.

Item 2. Offer Statistics and Expected Timetable

Not applicable for annual reports on Form 20-F.

Item 3. Key Information

| A. | Selected Financial Data. |

In the table below, we provide you with summary financial data of our company. The selected consolidated statement of income and other comprehensive income data for the years ended December 31, 2013, 2014 and 2015 and the selected consolidated balance sheet data as of December 31, 2014 and 2015 are derived from our audited consolidated financial statements, which are included elsewhere in this annual report. The selected consolidated statement of income and comprehensive income data for the year ended December 31, 2012 and the selected consolidated balance sheet data as of December 31, 2012 and 2013 are derived from our audited consolidated financial statements, which are not included in this annual report. The selected consolidated statement of income and other comprehensive income data for the year ended December 31, 2011 and the selected consolidated balance sheet as of December 31, 2011 have been derived from our unaudited consolidated financial statements not included in this annual report. Historical results are not necessarily indicative of the results that may be expected for any future period. When you read this historical selected financial data, it is important that you read it along with the historical statements and notes and “Operating and Financial Review and Prospects” included elsewhere in this annual report.

Selected Consolidated

Statement of Income and Other | | For The Years Ended December 31, | |

| Comprehensive Income Data | | 2015 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| (In U.S. dollars) | | | | | | | | | | | | | | | |

| Total revenues | | $ | 59,350,721 | | | $ | 42,673,139 | | | $ | 28,130,305 | | | $ | 21,780,782 | | | $ | 14,335,679 | |

| Cost of revenues | | | 46,891,617 | | | | 35,188,331 | | | | 23,757,669 | | | | 19,436,755 | | | | 12,882,355 | |

| Gross profit | | | 12,459,104 | | | | 7,484,808 | | | | 4,372,636 | | | | 2,344,027 | | | | 1,453,324 | |

| Total operating expenses | | | 7,250,331 | | | | 5,779,600 | | | | 3,085,437 | | | | 2,649,439 | | | | 2,412,171 | |

| Income (loss) from operations | | | 5,208,773 | | | | 1,705,208 | | | | 1,287,199 | | | | (305,412 | ) | | | (958,847 | ) |

| Other income and (expenses) | | | | | | | | | | | | | | | | | | | | |

| Government grants | | | 1,027,581 | | | | 1,439,186 | | | | 2,714,026 | | | | 1,152,983 | | | | 967,176 | |

| Other income | | | 225,306 | | | | 64,873 | | | | 112,140 | | | | 85,802 | | | | 10,273 | |

| Other expense | | | (133,421 | ) | | | (238,413 | ) | | | (101,034 | ) | | | (137,451 | ) | | | (58,911 | ) |

| Interest expense | | | (278,363 | ) | | | (552,894 | ) | | | (468,823 | ) | | | (517,400 | ) | | | (295,130 | ) |

| Total other income | | | 841,103 | | | | 712,752 | | | | 2,256,309 | | | | 583,934 | | | | 623,408 | |

| Income before provision for income taxes | | | 6,049,876 | | | | 2,417,960 | | | | 3,543,508 | | | | 278,522 | | | | (335,439 | ) |

| Income tax provision | | | 1,275,633 | | | | 635,859 | | | | 594,240 | | | | (35,066 | ) | | | (55,934 | ) |

| Net income (loss) | | | 4,774,243 | | | | 1,782,101 | | | | 2,949,268 | | | | 313,588 | | | | (279,505 | ) |

| Earnings per common share – basic and fully diluted | | $ | 0.30/0.30 | | | $ | 0.11/0.11 | | | $ | 0.19/0.19 | | | $ | 0.02/0.02 | | | $ | (0.02)/(0.02) | |

| | | As of December 31, | |

| Selected Balance Sheet Data | | 2015 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| (In U.S. dollars) | | | | | | | | | | | | | | | |

| Cash | | $ | 13,623,849 | | | $ | 5,097,010 | | | $ | 5,714,563 | | | $ | 2,218,473 | | | $ | 980,306 | |

| Total current assets | | | 25,384,834 | | | | 16,149,427 | | | | 13,448,808 | | | | 8,090,493 | | | | 5,646,138 | |

| Total non-current assets | | | 5,624,155 | | | | 3,715,981 | | | | 3,795,375 | | | | 3,425,107 | | | | 3,167,957 | |

| Total assets | | | 31,008,989 | | | | 19,865,408 | | | | 17,244,183 | | | | 11,515,600 | | | | 8,814,095 | |

| Total current liabilities | | | 9,245,474 | | | | 10,684,120 | | | | 14,391,502 | | | | 8,508,025 | | | | 7,086,700 | |

| Total non-current liabilities | | | - | | | | 4,450 | | | | - | | | | - | | | | - | |

| Total liabilities | | | 9,245,474 | | | | 10,688,570 | | | | 14,391,502 | | | | 8,508,025 | | | | 7,086,700 | |

| Total shareholders’ equity | | | 21,763,515 | | | | 9,176,838 | | | | 2,852,681 | | | | 3,007,575 | | | | 1,727,395 | |

| Total liabilities and shareholders’ equity | | $ | 31,008,989 | | | $ | 19,865,408 | | | $ | 17,244,183 | | | $ | 11,515,600 | | | $ | 8,814,095 | |

We have presented earnings per share in CCRC after giving retroactive effect to the reorganization of our company that was completed on September 3, 2014, upon Taiying’s execution of control agreements with its sole shareholder, Beijing Taiying Anrui Holding Co., Ltd. (“Beijing Taiying”), and WFOE. This information is pro forma because the 15,929,600 CCRC common shares did not exist prior to the formation of CCRC in 2014.

Exchange Rate Information

Our business is conducted in China, and the financial records of WFOE and Taiying are maintained in RMB, their functional currency. However, we use the U.S. dollar as our reporting currency; therefore, periodic reports made to shareholders will include current period amounts translated into U.S. dollars using the then-current exchange rates, for the convenience of the readers. Our financial statements have been translated into U.S. dollars in accordance with Accounting Standards Codification (“ASC”) 830-10, “Foreign Currency Matters.” We have translated our asset and liability accounts using the exchange rate in effect at the balance sheet date. We translated our statements of operations using the average exchange rate for the period. We reported the resulting translation adjustments under other comprehensive income. Unless otherwise noted, we have translated balance sheet amounts with the exception of equity at December 31, 2015 at RMB 6.4907 to $1.00 as compared to RMB 6.1460 to $1.00 at December 31, 2014. The average translation rates applied to income statement accounts for the years ended December 31, 2015, 2014 and 2013 were RMB 6.2175, RMB 6.1457 and RMB 6.1905, respectively.

We make no representation that any RMB or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or RMB, as the case may be, at any particular rate, or at all. The Chinese government imposes control over its foreign currency reserves in part through direct regulation of the conversion of RMB into foreign exchange and through restrictions on foreign trade. The company does not currently engage in currency hedging transactions.

The following table sets forth information concerning exchange rates between the RMB and the U.S. dollar for the periods indicated.

Forex Exchange Rate

| | | | (RMB per U.S. Dollar) | |

| | | | Period End | | | Average | |

| | | | | | | | |

| 2010 | | | | 6.6018 | | | | 6.7696 | |

| 2011 | | | | 6.3585 | | | | 6.4640 | |

| 2012 | | | | 6.3086 | | | | 6.3116 | |

| 2013 | | | | 6.1104 | | | | 6.1905 | |

| 2014 | | �� | | 6.1460 | | | | 6.1457 | |

| 2015 | | | | 6.4907 | | | | 6.2175 | |

| January 2016 | | | | 6.6046 | | | | 6.5668 | |

| February 2016 | | | | 6.5535 | | | | 6.5486 | |

| March 2016 | | | | 6.4479 | | | | 6.5036 | |

| April 2016 (through April 28th) | | | | 6.4831 | | | | 6.4774 | |

| B. | Capitalization and indebtedness. |

Not applicable for annual reports on Form 20-F.

| C. | Reasons for Offer and use of Proceeds. |

Not applicable for annual reports on Form 20-F.

Risks Related to Our Business

We are likely to depend on third-party software, systems and services and an interruption in the services could have a material adverse effect on our business, financial condition and results of operations.

Our business and operations rely on China Telecom and China Mobile and may rely on other third parties to provide services, such as IT services, or shipping and transportation services. We may experience operational problems attributable to the installation, implementation, integration, performance, features or functionality of third-party software, access to communication networks and fiber optics, hosted environments, systems and services. Any interruption in the availability or usage of the services provided by China Mobile or China Telecom or other third parties could have a material adverse effect on our business, financial condition and results of operations.

Unexpected network interruptions, security breaches or computer virus attacks could have a material adverse effect on our business, financial condition and results of operations.

Our business depends on the performance and reliability of the mobile telecommunications network of China Mobile or China Telecom, as the case may be. We may not have access to alternative networks in the event of disruptions, failures or other problems with China Mobile or China Telecom’s wireless infrastructure.

Any failure to maintain the satisfactory performance, reliability, security and availability of our network infrastructure may cause significant harm to our reputation and our ability to attract and maintain clients. Major risks involved in such network infrastructure include, among others, any breakdowns or system failures resulting in a prolonged shutdown of all or a material portion of our servers, including failures which may be attributable to sustained power outages, or effort to gain unauthorized access to our systems causing loss or corruption of data or malfunctions of software or hardware.

Our network systems are vulnerable to damage from fire, flood, power loss, telecommunications failures, computer viruses, hackings and other similar events. Any network interruption or inadequacy that causes interruptions in the availability of our services or deterioration in the quality of access to our services could reduce our user satisfaction and our competitiveness. In addition, any security breach caused by hacking, which involves effort to gain unauthorized access to information or systems, or to cause intentional malfunctions or loss or corruption of data, software, hardware or other computer equipment, and the inadvertent transmission of computer viruses could have a material adverse effect on our business, financial condition and results of operations. We do not maintain insurance policies covering losses relating to our systems and we do not have business interruption insurance. See “Risk Factors - We have limited business insurance coverage. Any future business liability, disruptions or litigation we experience might divert management focus from our business and could significantly impact our financial results.”

Our business is dependent upon the reliability and accessibility of China’s telecommunications and Internet infrastructure and if they become nonfunctional our operational results could suffer as a result.

We render our services via telecommunications and Internet networks, and therefore our ability to fulfill our contracts and generate revenue and profits is dependent on those systems remaining available and accessible with minimal disruption or interruption. Just as we are dependent on the reliability of our software and systems and the telecommunications networks of our principal clients, we are also dependent on the operational reliability and capacity of China’s overall telecommunications and Internet infrastructure. Should this infrastructure or key portions of it be disabled or become nonfunctional, we may not be able to secure alternate means of communication or alternate means of accessing needed information. Our operational results could suffer as a result.

Our revenues are highly dependent on a limited number of industries and any decrease in demand for outsourced services in these industries could reduce our revenues and adversely affect our results of operations.

For the years ended December 31, 2015, 2014 and 2013, a majority of our net revenues were derived from clients in the telecommunications industry. The success of our business largely depends on continued demand for our services from clients in the telecommunications industry, as well as on trends in the telecommunications industry to outsource customer relation management services. A downturn in any of our targeted industries, particularly the telecommunications, a slowdown or reversal of the trend to outsource customer relation management services in any of these industries or the introduction of regulations that restrict or discourage companies from outsourcing could result in a decrease in the demand for our services, which in turn could harm our business, results of operations and financial condition. Any significant reduction in or the elimination of the use of the services we provide within any of these industries would result in reduced revenues and harm our business. Our clients may experience rapid changes in their prospects, substantial price competition and pressure on their profitability. This, in turn, may result in increasing pressure on us from clients in these key industries to lower our prices, which could negatively affect our business, results of operations and financial condition.

We depend on the provincial subsidiaries of China Mobile and China Telecom for a significant portion of our revenues, and this dependency is likely to continue. Any deterioration of such relationships may result in severe disruptions to our business operations and the loss of the majority of our revenues.

We have derived, and believe that in the foreseeable future we will continue to derive, a significant portion of our revenues from a limited number of clients. In 2015, the provincial subsidiaries of China Mobile and China Telecom accounted for 10% or more of our net revenues, and in the aggregate accounted for 64% of our net revenues. In 2014, the provincial subsidiaries of China Mobile and China Telecom accounted for 10% or more of our net revenues, and in the aggregate accounted for 74% of our net revenues. In 2013, the provincial subsidiaries of China Mobile and China Telecom accounted for 10% or more of our net revenues, and in the aggregate accounted for 78% of our net revenues. Our top five clients accounted for approximately 78%, 84% and 88% of our net revenues in 2015, 2014 and 2013, respectively.

We operate under non-exclusive revenue sharing arrangements with the provincial subsidiaries of China Mobile and China Telecom for inbound and outbound callings. We generally do not have long-term commitments from any of our clients to purchase our services. Our agreements with provincial subsidiaries of China Mobile and China Telecom generally have one-year terms and they do not have automatic renewal provisions. A number of factors other than our performance could cause the loss of or reduction in business or revenue from a client and these factors are not predictable. A client may demand price reductions, change its outsourcing strategy, switch to another outsourcing service provider or return work in-house. For example, if the provincial subsidiaries of China Mobile or China Telecom are unwilling to continue our business relationships, we will face significant loss of business. The loss, cancellation, deferral or renegotiation of our arrangements with the provincial subsidiaries of China Mobile or China Telecom could have a material adverse effect on our financial condition and results of operations. Our ability to maintain close relationships with these clients is essential to the growth and profitability of our business.

The alteration of the revenue sharing percentage in our cooperation agreements with the provincial subsidiaries of China Mobile and China Telecom or termination of these agreements could materially and adversely impact our business operations and financial conditions.

We have limited negotiating leverage with the provincial subsidiaries of China Mobile or China Telecom. Our revenues and profitability could be materially and adversely affected if the provincial subsidiaries of either China Mobile or China Telecom decide to materially increase its revenue sharing percentage. In addition, the provincial subsidiaries of China Mobile or China Telecom could impose monetary penalties upon us or even terminate cooperation agreements with us, for a variety of reasons, including without limitation, the following:

| ● | if the provincial subsidiaries of China Mobile or China Telecom receive a high level of customer complaints about our call center service; or |

| ● | if we fail to meet the performance standards established by the provincial subsidiaries of China Mobile or China Telecom from time to time. |

Significant changes in the policies or guidelines of the provincial subsidiaries of China Mobile or China Telecom with respect to services provided by us may materially adversely affect our financial condition and results of operations.

Any of the provincial subsidiaries of China Mobile or China Telecom may from time to time issue certain operating policies or guidelines, requesting or stating preferences for certain actions to be taken by all MVAS providers using their networks. Due to our reliance on the provincial subsidiaries of China Mobile and China Telecom, a significant change in the policies or guidelines of these clients may result in lower revenues or additional operating costs to us. We cannot assure that our financial condition and results of operations will not be materially adversely affected by a change in policies or guidelines by the provincial subsidiaries of either China Mobile or China Telecom.

Our clients may adopt technologies that decrease the demand for our services, which could harm our business, results of operations and financial condition.

We target clients that need our BPO services, and we depend on their continued need for our services. However, over time, our clients may adopt new technologies that decrease the need for live customer interaction, such as interactive voice response, web-based self-help and other technologies used to automate interactions with customers. The adoption of these technologies could reduce the demand for our services, create pricing pressure and harm our business, results of operations and financial condition.

Failure to attract and retain telecommunications operators to work with us will negatively affect our ability to grow revenues and market share.

The amount of fees we can charge the provincial subsidiaries of China Mobile or China Telecom depends upon the size of potential customers, the outbound cold calling success rate, and the quality of our data mining work. Telecommunications operators choose us to provide BPO services in part because of the effectiveness and quality of the services we offer. If we fail to maintain or increase the satisfaction level of our customers, or fail to solidify our brand name and reputation as a quality provider of call center services and content services, telecommunications operators may be unwilling to pay the fees at a level necessary for us to remain profitable.

Changes in the regulation of the Chinese telecommunications industry could result in new burdens and expenses on service providers like us.

Our principal customers are telecommunications companies that operate in a highly regulated environment. Major telecommunications companies in China are state-owned or controlled, and their business decisions and strategies are affected by government budgeting and spending plans. In addition, in December 2001, the Ministry of Industry and Information Technology of China promulgated a set of regulations governing telecommunications providers, and these regulations were augmented in 2003 with a classification system that covers, among other things, Type 2 (hereafter defined) value added service providers such as us. Changes in the regulatory system may impose new costs and burdens on us, or affect us indirectly by imposing new burdens and obligations onto our customers that, in turn, may be passed on to us under our agreements with customers. If such changes occur, our financial performance may be adversely affected.

Further restructuring of China’s telecommunications sector may have an adverse impact on our business prospects and results of operations.

Historically, China’s telecommunications sector has been subject to a number of state-mandated restructurings. For example, in 2002 China Telecom was split geographically into a northern division (consisting of 10 provinces) and a southern division (consisting of 21 provinces).

In May 2008, China announced a new restructuring plan for the country’s telecommunications carriers. This restructuring plan reorganized the operations of Chinese telecommunications carriers, creating three major carriers that have both mobile and fixed-line services. Moreover, in 2013, the Chinese government started to permit mobile virtual network operators to lease and repackage mobile services for sale to end customers. Such changes will lead to further intensified competition in China’s telecommunications industry. As a result, more call center outsourcing solution providers will be competing for projects and telecommunications carriers may be able to exact lower prices for our solutions and services. If we cannot effectively compete with our competitors, our profit margin will be reduced, and our results of operations may be materially and adversely affected. Furthermore, telecommunications carriers may also find it more cost-effective to keep or establish their own BPO operations, instead of outsourcing to third-party providers. If the outsourcing of such services is reduced or reversed, our financial condition and results of operations may be materially and adversely affected.

Call center services, particularly telemarketing services, may fall into disfavor among the public, reducing demand for our services.

Telemarketing services, particularly outbound call center services, may fall into public disfavor if the recipients of calls find them annoying, burdensome or otherwise overbearing. While we strive to render our services in a professional, polite and courteous manner, we cannot control the public perception of telemarketing generally. Moreover, we do not always have control over the nature or subject matter of outbound calls that our customers require us to make. Public hostility to telemarketing services generally, or to the particular types of calls our customers would like us to make, could result in decreased demand for such services, and thus be detrimental to our revenues and profits.

The growth of our business may be adversely affected due to public concerns over the security and privacy of confidential user information.

The growth of our business may be inhibited if public concerns over the security and privacy of confidential user information transmitted over the Internet and wireless networks are not adequately addressed. Our services may decline and our business may be adversely affected if significant breaches of network security or user privacy occur.

The intellectual property of our customers may be damaged, misappropriated, stolen or lost while in our possession, subjecting us to litigation and other adverse consequences.

In the course of providing services to our clients, we may have possession of or access to their intellectual property, including databases, software, certificates of authenticity and similar valuable items of intellectual property. If our clients’ intellectual property is damaged, misappropriated, stolen or lost, we could suffer adverse impacts to our business, including but not limited to:

| ● | claims under client agreements or applicable law, or other liability for damages; |

| ● | delayed or lost revenue due to adverse client reaction; |

| ● | litigation that could be costly and time-consuming. |

Our limited operating history makes it difficult to evaluate our future prospects and results of operations.

We have a limited operating history. Taiying was established in 2007, CBPO, WFOE and CCRC were established in 2014. As our operating history is limited, the revenues and income potential of our business and markets are unproven. Our limited operating history and the early stage of development of the industry in which we operate makes it difficult to evaluate our business and future prospects. Although we expect our revenues to grow, we cannot assure that we will maintain our profitability or that we will not incur net losses in the future. Any significant failure to realize anticipated revenue growth could result in significant operating losses. Accordingly, you should consider our future prospects in light of the risks and uncertainties experienced by early stage companies in evolving markets such as the growing market for call center services in the PRC. In addition, we face numerous risks, uncertainties, expenses and difficulties frequently encountered by companies at an early stage of development. We will continue to encounter risks and difficulties in implementing our business model, including (among other risks and difficulties) potential failure to:

| ● | offer additional call center services to attract and retain a larger customer base; |

| ● | increase our revenue and market share by targeting specific markets with positive consumer demographics; |

| ● | expand our operations and service network to other provinces; |

| ● | attract additional customers and increase spending per customer; |

| ● | attract a wider client base and explore new mobile marketing opportunities to target segmented consumer groups; |

| ● | increase visibility of our brand and maintain customer loyalty; |

| ● | respond to competitive market conditions; |

| ● | anticipate and adapt to changing conditions in the markets in which we operate as well as changes in government regulations, mergers and acquisitions involving our competitors, technological developments and other significant competitive and market dynamics; |

| ● | manage risks associated with intellectual property rights; |

| ● | maintain effective control of our costs and expenses; |

| ● | raise sufficient capital to sustain and expand our business; |

| ● | attract, train, retain and motivate qualified personnel, continue to train, motivate and retain our existing employees, attract and integrate new employees, including into our senior management; and |

| ● | upgrade our technology to support additional research and development of new call center services. |

We cannot predict whether we will be successful in addressing any or all of these risks. If we are unsuccessful in addressing these risks and uncertainties, our business, financial condition and results of operation may be materially and adversely affected.

Our dependence on the timing of the billing systems of the provincial subsidiaries of China Mobile and China Telecom may require us to estimate portions of our reported revenues and cost of revenues for our services. As a result, subsequent adjustments may have to be made to our financial statements.

It takes the provincial subsidiaries of China Mobile or China Telecom an average of 90 days to tender payment for our services after each month’s end. As a result, estimated revenues may account for a larger proportion of our reported revenues. As we do not bill our subscribers directly, we depend on the billing systems of the provincial subsidiaries of China Mobile or China Telecom to record the volume of our services provided, bill our customers, collect payments and remit to us our portion of the fees. We record revenues based on monthly statements from the provincial subsidiaries of China Mobile or China Telecom confirming the value of the services we provide that are billed by the provincial subsidiaries of China Mobile or China Telecom during the month. To the extent we have not received monthly statements from the operators, we must rely on our own internal records for a portion of our reported revenues. In such an instance, our internal estimates would be based on our own internal data of expected revenues and related fees from services provided. As a result of reliance on our internal estimates, we may overstate or understate our revenues and cost of revenues for the relevant reporting period, and may be required to make adjustments in our financial reports when we actually receive the telecommunications operators’ monthly statements for such a period. We endeavor to reduce the discrepancy between our revenue estimates and the revenues calculated by the telecommunications operators and their subsidiaries, but we cannot assure that such efforts will be successful. If we are required to make adjustments to our quarterly financial statements in subsequent quarters, it could adversely affect market sentiment toward us.

In addition, we generally do not have the ability to independently verify or challenge the accuracy of the billing systems of the telecommunications operators. We cannot assure that negotiations between us and the provincial subsidiaries of China Mobile or China Telecom to reconcile billing discrepancies would be resolved in our favor or that our results of operations would not be adversely affected as a result of such negotiations.

The markets in which we operate are highly competitive and fragmented. The competition could limit our ability to increase market share, and materially adversely affect our business operations, financial condition and results of operations.

We operate in a highly fragmented market and expect competition to persist and intensify in the future. The outsourcing industry is extremely competitive, and outsourcers have historically competed based on pricing terms. Accordingly, we could be subject to pricing pressure and may experience a decline in our average selling prices for our call center services. We compete with these companies primarily on the basis of brand, type and timing of service offerings, content, customer service, business partners and channel relationships. We also compete for experienced and talented employees. While we believe that we have certain advantages over our competitors, some of them may have greater financial, human and other resources, longer operating histories, greater technological expertise, more recognizable brand names and more established relationships than we do in the industries that we currently serve or may serve in the future. Some of our competitors may enter into strategic or commercial relationships among themselves or with larger, more established companies in order to increase their ability to address client needs. Increased competition, pricing pressure or loss of market share could reduce our operating margin, which could harm our business, results of operations and financial condition. Furthermore, our competitors may be able to develop or exploit new technologies faster than we can, or offer a broader range of services than we are presently able to offer.

We could face decreasing revenues and lower profitability if we are forced to significantly reduce the price of our services. We split a pre-determined percentage of our revenue with the provincial subsidiaries of China Mobile and China Telecom for most of our services. However, increasing competition among telecommunication companies in the PRC may lead to a reduction in telecommunication services fees that can be charged by such companies. If either the provincial subsidiaries of China Mobile or China Telecom experience a reduction in telecommunication services fees, such a reduction will negatively impact revenue generated by the provincial subsidiaries of China Mobile or China Telecom. Under such circumstances, we may be required to reduce the price of our services; or the provincial subsidiaries of China Mobile or China Telecom may demand an increase of its share of profit sharing under our agreements with their subsidiaries or seek competitors that charge less for services than we do, all or any of which could adversely affect our financial results.

If we fail to compete successfully against new and existing competitors, we may not be able to increase our market share, and our profitability may be adversely affected.

We do and will continue to face significant competition in the PRC in the BPO business. We compete for clients primarily on the basis of our brand name, delivery method, price and the range of services that we offer. We also compete for overall advertising spending with other alternative advertising media companies, such as the Internet, newspapers, television, magazines and radio.

Increased competition will provide advertisers with a wider range of media and advertising service alternatives, which could force us to offer lower prices for our services, resulting in reduced operating margins and profitability and a loss of market share. Some of our existing and potential competitors may have competitive advantages, such as significantly greater financial, marketing or other resources. We cannot assure that we will be able to successfully compete against new or existing competitors.

If we are unable to respond successfully to technological or industry developments, our business may be materially adversely affected.

Rapid advances in technology, industry standards and customer demands characterize the telecommunications industry. New technologies, industry standards or market demands may render our existing services or technologies less competitive or even obsolete. Telecommunications operators in the PRC are currently in the process of introducing 4G telecommunications services. Responding and adapting to 4G and other technological developments and standard changes in our industry may require substantial time, effort and capital investment. If we are unable to respond successfully to technology, industry and market developments, such developments may materially adversely affect our business, results of operations and competitiveness.

Our operating margin will suffer if we are not able to maintain our pricing, utilize our employees and assets efficiently or maintain and improve the current mix of services that we deliver.

Our operating margin is largely a function of the prices that we are able to charge for our services, the new programs we are able to develop, the efficient use of our assets, the utilization of our employees, and the geographical location from which we deliver services. For example, China Mobile Beijing has transferred a portion of its call center service business to our Shandong Province location in an effort to reduce costs. Our business model is predicated on our ability to objectively quantify the value that we provide to our clients. If we fail to succeed on any of these objectives, we may experience a decline in our current operating margin.

The rates we are able to charge for our services, our ability to manage our assets efficiently and the location from which we deliver our services are affected by a number of factors, including, without limitation:

| ● | our clients’ perceptions of our ability to add value through our services; |

| ● | our ability to objectively differentiate and verify the value we offer to our clients; |

| ● | the introduction of new services by us or our competitors; |

| ● | our ability to estimate demand for our services; |

| ● | our ability to control costs and improve the efficiency of our employees; and |

| ● | general economic and political conditions. |

Wage increases in China may prevent us from sustaining our competitive advantage and could reduce our profit margins.

Wage costs for our call center professionals and other employees form a significant part of our costs. For instance, in 2015, 2014 and 2013, our compensation and benefit expenses in respect of our professionals was $43.62 million, $31.62 million and $21.16 million, accounting for 73%, 74% and 75% of our total revenues, respectively. Because of rapid economic growth and increased competition for skilled employees in China, we may need to increase our levels of employee compensation more rapidly than in the past to remain competitive in retaining the quality and number of employees that our business requires. Increases in the wages and other compensations we pay our employees in China could reduce our competitive strength; especially if increase in wage costs of our call center professionals exceeds increase in our call center professionals’ billing rate, we may suffer a reduction in profit margins. In addition, the future issuance of equity-based compensation to our professional staff and other employees would also result in additional stock dilution for our shareholders.

We depend on our key personnel, and our business and growth prospects may be severely disrupted if we lose their services.

Our future success depends heavily upon the continued service of our key executives. In particular, we rely on the expertise and experience of Gary Wang, our founder, chairman and chief executive officer. We rely on his industry expertise and experience in our business operations, and in particular, his business vision, management skills, and working relationship with our employees, our other major shareholders, the regulatory authorities, and many of our clients. If he became unable or unwilling to continue in his present position, or if he joined a competitor or formed a competing company in violation of his employment agreement, we may not be able to replace him easily, our business may be significantly disrupted and our financial condition and results of operations may be materially adversely affected.

We do not maintain key man life insurance on any of our senior management or key personnel. The loss of any one of them would have a material adverse effect on our business and operations. Competition for senior management and our other key personnel is intense and the pool of suitable candidates is limited. We may be unable to locate a suitable replacement for any senior management or key personnel that we lose. In addition, if any member of our senior management or key personnel joins a competitor or forms a competing company, they may compete with us for customers, business partners and other key professionals and staff members of our company. Although each of our senior management and key personnel has signed a confidentiality and non-competition agreement in connection with his employment with us, we cannot assure that we will be able to successfully enforce these provisions in the event of a dispute between us and any member of our senior management or key personnel.

In addition, we compete for qualified personnel with other call center companies, and we face competition in attracting skilled personnel and retaining the members of our senior management team. These personnel possess technical and business capabilities, including expertise relevant to the BPO market, which are difficult to replace. There is intense competition for experienced senior management with technical and industry expertise in the BPO industry, and we may not be able to retain our key personnel. Intense competition for these personnel could cause our compensation costs to increase, which could have a material adverse effect on our results of operations. Our future success and ability to grow our business will depend in part on the continued service of these individuals and our ability to identify, hire and retain additional qualified personnel. If we are unable to attract and retain qualified employees, we may be unable to meet our business and financial goals.

If we fail to attract and retain enough sufficiently trained customer service associates and other personnel to support our operations, our business, results of operations and financial condition will be seriously harmed.

We rely on large numbers of customer service associates, and our success depends to a significant extent on our ability to attract, hire, train and retain qualified customer service associates. Companies in the BPO market, including us, experience high employee attrition. Our attrition rate for our customer service associates who remained with us following a 90-day training and orientation period was on average approximately 5% per month. A significant increase in the attrition rate among our customer service associates could decrease our operating efficiency and productivity. Our failure to attract, train and retain customer service associates with the qualifications necessary to fulfill the needs of our existing and future clients would seriously harm our business, results of operations and financial condition.

Our senior management lacks experience in managing a public company and complying with laws applicable to operating as a U.S. public company domiciled in the British Virgin Islands and failure to comply with such obligations could have a material adverse effect on our business.

Prior to the completion of our initial public offering, Taiying operated as a private company located in the PRC. In connection with our initial public offering, the senior management of Taiying formed CCRC in the British Virgin Islands, CBPO in Hong Kong and made WFOE a CCRC subsidiary in the PRC. They also entered Taiying and WFOE into certain agreements that gave CCRC effective control over the operations of Taiying by virtue of its ownership of CBPO and CBPO’s ownership of WFOE. In the process of taking these steps to prepare our company for its initial public offering, Taiying’s senior management became the senior management of CCRC. None of CCRC’s senior management has experience managing a public company or managing a British Virgin Islands company.

As a result of our initial public offering, the company became subject to laws, regulations and obligations that dis not previously apply to it, and our senior management currently has limited experience in complying with such laws, regulations and obligations. For example, CCRC will need to comply with the British Virgin Islands laws applicable to companies that are domiciled in that country. The senior management is only experienced in operating the business of Taiying in compliance with Chinese laws. Similarly, by virtue of the initial public offering, CCRC is required to file annual reports in compliance with U.S. securities and other laws. These obligations can be burdensome and complicated, and failure to comply with such obligations could have a material adverse effect on CCRC. In addition, we expect that the process of learning about such new obligations as a public company in the United States will require our senior management to devote time and resources to such efforts that might otherwise be spent on the operation of our BPO business.

Our quarterly operating results are difficult to predict and may fluctuate significantly from period to period in the future.

Our quarterly operating results may differ significantly from period to period due to factors such as, without limitation:

| ● | client losses or program terminations; |

| ● | variations in the volume of business from clients resulting from changes in our clients’ operations; |

| ● | delays or difficulties in expanding our operational facilities and infrastructure; |

| ● | changes to our pricing structure or that of our competitors; |

| ● | inaccurate estimates of resources and time required to complete ongoing programs; |

| ● | inaccurate estimates of amounts billed by our clients for the services we provided during such period; |

| ● | ability to hire and train new employees; |

| ● | seasonal changes in the operations of our clients; |

| ● | a deterioration of economic conditions in the PRC; |

| ● | potential changes to the regulation of the advertising, Internet and wireless communications industries in the PRC; and |

| ● | seasonality of economic activities in the PRC, such as the anticipated decrease in outbound calling during January and February each year due to the Chinese Lunar New Year holiday, and the anticipated decrease in revenues during July and August due to overall slow commercial activities during the summer months. |

As a result, you may not be able to rely on period-to-period comparisons of our operating results as an indication of our future performance. If our revenues for a particular quarter are lower than we expect, we may be unable to reduce our operating expenses for that quarter by a corresponding amount, which would harm our operating results for that quarter relative to our operating results from other quarters.

We have limited business insurance coverage. Any future business liability, disruption or litigation we experience might divert management focus from our business and could significantly impact our financial results.

Availability of business insurance products and coverage in the PRC is limited, and most such products are expensive in relation to the coverage offered. We have determined that the risks of disruption, cost of such insurance and the difficulties associated with acquiring such insurances on commercially reasonable terms make it impractical for us to maintain such insurances. As a result, we do not have any business liability, disruption or litigation insurance coverage for our operations in the PRC. Accordingly, a business disruption, litigation or natural disaster may result in substantial costs and divert management’s attention from our business, which would have an adverse effect on our results of operations and financial condition.

We may require additional financing in the future and our operations could be curtailed if we are unable to obtain required additional financing when needed.

We may need to obtain additional debt or equity financing to fund future capital expenditures. While we do not anticipate seeking additional financing in the immediate future, any additional equity financing may result in dilution to the holders of our outstanding shares of capital stock. Additional debt financing may put us in situations that would restrict our freedom to operate our business, such as situations that:

| ● | limit our ability to pay dividends or require us to seek consent for the payment of dividends; |

| ● | increase our vulnerability to general adverse economic and industry conditions; |

| ● | require us to dedicate a portion of our cash flow from operations to payments on our debt, thereby reducing the availability of our cash flow to fund capital expenditures, working capital and other general corporate purposes; and |

| ● | limit our flexibility in planning for, or reacting to, changes in our business and our industry. |

We cannot guaranty that we will be able to obtain additional financing on terms that are acceptable to us, or any financing at all.

Potential disruptions in the capital and credit markets may adversely affect our business, including the availability and cost of short-term funds for liquidity requirements, which could adversely affect our results of operations, cash flows and financial condition.

Potential changes in the global economy may affect the availability of business and consumer credit. We may need to rely on the credit markets, particularly for short-term borrowings from banks in the PRC, as well as the capital markets, to meet our financial commitments and short-term liquidity needs if internal funds from our operations are not available to be allocated to such purposes. Disruptions in the credit and capital markets could adversely affect our ability to draw on such short-term bank facilities. Our access to funds under such credit facilities is dependent on the ability of the banks that are parties to those facilities to meet their funding commitments, which may be dependent on governmental economic policies in the PRC. Those banks may not be able to meet their funding commitments to us if they experience shortages of capital and liquidity or if they experience excessive volumes of borrowing requests from us and other borrowers within a short period of time.

Long-term disruptions in the credit and capital markets could result from uncertainty, changing or increased regulations, reduced alternatives or failures of financial institutions could adversely affect our access to the liquidity needed for our business. Any disruption could require us to take measures to conserve cash until the markets stabilize or until alternative credit arrangements or other funding for our business needs can be arranged. Such measures may include deferring capital expenditures, and reducing or eliminating discretionary uses of cash.

Continued market disruptions could cause broader economic downturns, which may lead to decreased cellular telephone usage, decreased commercial activities in general, and increased likelihood that customers will be unable to pay for our services. Further, bankruptcies or similar events by China Telecom, China Mobile, their subsidiaries or significant customers, or our other clients may cause us to incur bad debt expense at levels higher than historically experienced. These events would adversely impact our results of operations, cash flows and financial position.

Rapid growth and a rapidly changing operating environment may strain our limited resources.

We may not have adequate operational, administrative and financial resources to sustain the growth we want to achieve. Taiying was incorporated in December 2007. As of December 31, 2015, we had a total of approximately 7,799 employees. We have experienced rapid growth in our employee headcount. This expansion has resulted, and will continue to result, in substantial demands on our management resources. To manage our growth, we must develop and improve our existing administrative and operational systems and our financial and management controls and further expand, train and manage our work force. As we continue these efforts, we may incur substantial costs and expend substantial resources due to, among other things, different technology standards, legal considerations and cultural differences.

Our future success also depends on our product development, customer service, sales and marketing. If we fail to manage our growth and expansion effectively, the quality of our services and our customer support may deteriorate and our business may suffer. This could prompt either or both of the provincial subsidiaries of China Mobile or China Telecom to discontinue their respective outsourcing relationships with us. We cannot assure that we will be able to efficiently or effectively manage the growth of our operations, recruit top talent and train our personnel. Any failure to efficiently manage our expansion may materially and adversely affect our business and future growth.

Our bank accounts are not insured or protected against loss.

WFOE and the Operating Companies maintain cash accounts with various banks and trust companies located in the PRC. Such cash accounts are not insured or otherwise protected. Should any bank or trust company holding such cash deposits become insolvent, or if WFOE or an operating company of ours is otherwise unable to withdraw funds, this entity would lose the cash on deposit with that particular bank or trust company.

We may not pay dividends.

We have not previously paid any cash dividends, and we do not anticipate paying any dividends on our common shares. Although we have achieved net profitability in 2015, 2014 and 2013, we cannot assure that our operations will continue to result in sufficient revenues to enable us to operate at profitable levels or to generate positive cash flows. Furthermore, there is no assurance that our Board of Directors will declare dividends even if we are profitable. Dividend policy is subject to the discretion of our Board of Directors and will depend on, among other things, our earnings, financial condition, capital requirements and other factors. If we determine to pay dividends on any of our common shares in the future, we will be dependent, in large part, on receipt of funds from Taiying. See “Dividend Policy.”

Our growth strategy may prove to be disruptive and divert management resources, which could adversely affect our existing businesses.

Our growth strategy includes the continued expansion of Taiying’s call center operations and may include strategic acquisitions of competitive operators. We do not have any understanding, commitment or agreement in place with regard to any such acquisitions at this time. The implementation of such strategies may involve large transactions and present financial, managerial and operational challenges, including diversion of management attention from existing businesses, difficulty with integrating personnel and financial and other systems, increased expenses, including compensation expenses resulting from newly-hired employees, assumption of unknown liabilities and potential disputes. We also could experience financial or other setbacks if any of our growth strategies encounter problems of which we are not presently aware.

We expect to allocate a portion of the net proceeds from our initial public offering to such acquisitions, but we have not yet located any potential targets, and we may be unable to do so. Further, even if we find a target we believe to be suitable, we may be unable to negotiate acquisition terms that are satisfactory to us. In the event we are unable to complete acquisitions, we will reserve the right to reallocate such funds to our working capital. If this happens, we would have broad discretion over the ultimate use of such funds, and we could use such funds in ways with which investors might disagree.

Furthermore, any such acquisitions must comply with all PRC laws and regulations applicable to such transactions. The regulatory environment that governs mergers and acquisitions in the PRC has continued to evolve in recent years and remains subject to interpretation by the agencies that have responsibility for reviewing or approving such transactions. Compliance with such regulations in the process of structuring, negotiating and closing such transactions will require us to expend company resources that would otherwise be available for and used in the management and operation of the company, all of which could have an adverse effect on our operations and financial results.

We do not hold any patents or trademarks to protect our intellectual property and the misappropriation of our intellectual property could have a material adverse effect on our business, financial condition and results of operations.

Our intellectual property rights are important to our business. We rely on a combination of trade secrets, confidentiality procedures and contractual provisions to protect our intellectual property. We do not presently hold any patents or registered trademarks. However, we have been granted registered computer software ownership rights to ten pieces of intellectual property rights by the China State Copyright Bureau. In addition, we enter into confidentiality agreements with most of our employees and consultants, and control access to and distribution of our documentation and other licensed information. Despite these precautions, it may be possible for a third party to copy or otherwise obtain and use our technology without authorization, or to develop similar technology independently. Since the Chinese legal system in general, and the intellectual property regime in particular, is relatively weak, it is often difficult to enforce intellectual property rights in China. In addition, confidentiality agreements may be breached by counterparties, and there may not be adequate remedies available to us for any such breach. Accordingly, we may not be able to effectively protect our intellectual property rights or to enforce our contractual rights in China or elsewhere. In addition, policing any unauthorized use of our intellectual property is difficult, time-consuming and costly and the steps we have taken may be inadequate to prevent the misappropriation of our intellectual property. In the event that we resort to litigation to enforce our intellectual property rights, such litigation could result in substantial costs and a diversion of our managerial and financial resources. We can provide no assurance that we will prevail in such litigation. Any failure in protecting or enforcing our intellectual property rights could have a material adverse effect on our business, financial condition and results of operations.

Risks Relating to Our Corporate Structure

WFOE’s contractual arrangements with Taiying may result in adverse tax consequences to us.

We could face material and adverse tax consequences if the PRC tax authorities determine that WFOE’s contractual arrangements with Taiying were not made on an arm’s length basis and adjust our income and expenses for PRC tax purposes in the form of a transfer pricing adjustment. A transfer pricing adjustment could result in a reduction, for PRC tax purposes, of adjustments recorded by Taiying, which could adversely affect us by increasing Taiying’s tax liability without reducing WFOE’s tax liability, which could further result in late payment fees and other penalties to Taiying for underpaid taxes, all of which could have a material adverse effect on our results of operations and financial condition.

WFOE’s contractual arrangements with Taiying may not be as effective in providing control over Taiying as direct ownership.

We conduct substantially all of our operations, and generate substantially all of our revenues, through contractual arrangements with Taiying that provide us, through our ownership of WFOE, with effective control over Taiying. We depend on Taiying to hold and maintain contracts with our customers. Taiying also own substantially all of our intellectual property, facilities and other assets relating to the operation of our business, and employ the personnel for substantially all of our business. Neither our company nor WFOE has any ownership interest in Taiying. Although we have been advised by our PRC legal counsel, that each contract under WFOE’s contractual arrangements with Taiying is valid, binding and enforceable under current PRC laws and regulations, these contractual arrangements may not be as effective in providing us with control over Taiying as direct ownership of Taiying would be. In addition, Taiying may breach the contractual arrangements. For example, Taiying may decide not to make contractual payments to WFOE, and consequently to our company, in accordance with the existing contractual arrangements. In the event of any such breach, we would have to rely on legal remedies under PRC law. These remedies may not always be effective, particularly in light of uncertainties in the PRC legal system.

PRC laws and regulations governing our businesses and the validity of certain of our contractual arrangements are uncertain. If we are found to be in violation of such PRC laws and regulations, we could be subject to sanctions. In addition, changes in such PRC laws and regulations may materially and adversely affect our business.

Foreign ownership of a call center BPO and related business, is subject to restrictions under current PRC laws and regulations. For example, foreign investors are not allowed to own more than 50% of the equity interests in a value-added telecommunication service provider and any such foreign investor must have experience in providing value-added telecommunications services overseas and maintain a good track record.

We are a BVI company and our PRC subsidiary WFOE is considered a foreign-invested enterprise. To comply with PRC laws and regulations, we conduct our business in China through WFOE, Taiying and its subsidiaries based on a series of contractual arrangements by and among WFOE, Taiying and its shareholders, which enable us to:

| ● | exercise effective control over Taiying and its subsidiaries; |

| ● | receive substantially all of the economic benefits and bear the obligation to absorb substantially all of the losses of Taiying; and |

| ● | have an exclusive option to purchase all or part of the equity interests in Taiying when and to the extent permitted by PRC law. |

Because of these contractual arrangements, we are the primary beneficiary of Taiying and hence consolidate its financial results as our variable interest entity.

In the opinion of our PRC legal counsel, (a) our current ownership structure of our WFOE and Taiying, both comply with all existing PRC laws and regulations; and (b) each of the contractual arrangements is valid, binding and enforceable in accordance with its terms and applicable PRC Laws, and will not result in any violation of PRC laws or regulations currently in effect. However, our PRC legal counsel has also advised us that there are substantial uncertainties regarding the interpretation and application of PRC Laws and future PRC Laws, and there can be no assurance that the PRC authorities may take a view that is contrary to or otherwise different from our PRC legal counsel.

It is uncertain whether any new PRC laws, rules or regulations relating to contractual arrangements structures will be adopted or if adopted, what they would provide. Further, the effectiveness of newly enacted laws, regulations or amendments may be delayed, resulting in detrimental reliance by foreign investors. If CCRC, WFOE or Taiying are found to be in violation of any existing or future PRC laws, rules or regulations, or fail to obtain or maintain any of the required permits or approvals, the relevant PRC regulatory authorities would have broad discretion to take action in dealing with such violations or failures, including, sanctions, fines, revoking the business and operating licenses of WFOE or Taiying, requiring us to discontinue or restrict our operations, restricting our right to collect revenue, requiring us to restructure our operations or taking other regulatory or enforcement actions against us. If we are not able to restructure our ownership structure and operations in a satisfactory manner, we would no longer be able to consolidate the financial results of Taiying in our consolidated financial statements. In addition, any litigation in the PRC may be protracted and result in substantial costs and diversion of resources and management attention. Any of these events would have a material adverse effect on our business, financial condition and results of operations.

The shareholder of Taiying has potential conflicts of interest with us, which may adversely affect our business.

Neither WFOE nor we own any portion of the equity interests of Taiying. Instead, we rely on WFOE’s contractual obligations to enforce our interest in receiving payments from Taiying. Conflicts of interests may arise between Taiying’s shareholder and our company if, for example, its interests in receiving dividends from Taiying were to conflict with our interest requiring these companies to make contractually obligated payments to WFOE. As a result, we have required Taiying and its sole shareholder to execute irrevocable powers of attorney to appoint the individual designated by us to be his attorney-in-fact to vote on their behalf on all matters requiring shareholder approval by Taiying and to require Taiying’s compliance with the terms of its contractual obligations. We cannot assure, however, that when conflicts of interest arise, the shareholder will act completely in our interests or that conflicts of interests will be resolved in our favor. In addition, this shareholder could violate its agreements with us by diverting business opportunities from us to others. If we cannot resolve any conflicts of interest between us and Taiying’s shareholder, we would have to rely on legal proceedings, which could result in substantial costs and diversion of management attention and resources, all of which could have a material adverse effect on our business, financial condition and results of operations.

Recent PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident shareholders to personal liability and limit our ability to inject capital into our PRC subsidiary, limit our subsidiary’s ability to increase its registered capital, distribute profits to us, or otherwise adversely affect us.

On July 4, 2014, China’s State Administration for Foreign Exchange (“SAFE”) issued the Circular of the State Administration of Foreign Exchange on Issues concerning Foreign Exchange Administration over the Overseas Investment and Financing and Round-trip Investment by Domestic Residents via Special Purpose Vehicles, or Circular 37, which became effective as of July 4, 2014. According to Circular 37, prior registration with the local SAFE branch is required for PRC residents to contribute domestic assets or interests to offshore companies, known as a special purpose vehicle (SPV). Moreover, Circular 37 applies retroactively. As a result, PRC residents who have contributed domestic assets or interests to a SPV, but failed to complete foreign exchange registration of overseas investments as required before July 4, 2014 shall send a letter to SAFE and its branches for explanation. SAFE and its branches shall, under the principle of legality and legitimacy, conduct supplementary registration, and impose administrative punishment on those in violation of the administrative provisions on the foreign exchange pursuant to the law.

We attempt to comply, and attempt to ensure that our shareholders who are subject to these rules comply, with the relevant requirements. However, we cannot provide any assurances that all of our shareholders who are PRC residents will make or obtain any applicable registrations or comply with other requirements required by Circular 37 or other related rules. The failure or inability of our PRC resident shareholders to make any required registrations or comply with other requirements may subject such shareholders to fines and legal sanctions and may also limit our ability to contribute additional capital into or provide loans to (including using the proceeds from our initial public offering) WFOE or Taiying, limiting their ability to pay dividends or otherwise distributing profits to us.

We rely on dividends paid by WFOE for our cash needs.