INTRODUCTION

This Management’s Discussion and Analysis dated April 11, 2022 (this “MD&A”), should be read in conjunction with the condensed consolidated interim financial statements (the “Interim Financial Statements”) of Organigram Holdings Inc. (the “Company” or “Organigram”) for the three and six months ended February 28, 2022 (“Q2 Fiscal 2022”) and the audited consolidated financial statements for the year ended August 31, 2021 (the “Annual Financial Statements”), including the accompanying notes thereto, which have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

Financial data in this MD&A is based on the Interim Financial Statements of the Company for the three and six months ended February 28, 2022, and has been prepared in accordance with International Accounting Standard ("IAS") 34 Interim Financial Reporting as issued by the IASB, unless otherwise stated. All financial information in this MD&A is expressed in thousands of Canadian dollars (“$”), except for share and per share calculations, references to $ millions and $ billions, per gram (“g”) or kilogram (“kg”) of dried flower and per milliliter (“mL”) or liter (“L”) of cannabis oil calculations.

This MD&A contains forward-looking information within the meaning of applicable securities laws, and the use of non-IFRS measures. Refer to “Cautionary Statement Regarding Forward-Looking Information” and “Cautionary Statement Regarding Certain Non-IFRS Measures” included within this MD&A.

The financial data in this MD&A contains certain financial and operational performance measures that are not defined by and do not have any standardized meaning under IFRS but are used by management to assess the financial and operational performance of the Company. These include, but not limited to, the following:

•Yield per plant (in grams);

•Target production capacity;

•Average net selling price per gram and per unit;

•Adjusted gross margin; and

•Adjusted EBITDA.

The Company believes that these non-IFRS financial measures and operational performance measures, in addition to conventional measures prepared in accordance with IFRS, enable investors to evaluate the Company’s operating results, underlying performance and prospects in a similar manner to the Company’s management. The non-IFRS financial performance measures are defined in the sections in which they appear. Adjusted gross margin and adjusted EBITDA are reconciled to IFRS in the “Financial Review and Discussion of Operations” section of this MD&A.

As there are no standardized methods of calculating these non-IFRS measures, the Company’s approaches may differ from those used by others, and the use of these measures may not be directly comparable. Accordingly, these non-IFRS measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

The Company’s wholly-owned subsidiary, Organigram Inc., is a licensed producer of cannabis and cannabis derived products (a “Licensed Producer” or “LP”) under the Cannabis Act (Canada) and the Cannabis Regulations (Canada) (together, the “Cannabis Act”) and regulated by Health Canada. The Company’s wholly-owned subsidiaries, The Edibles and Infusions Corporation (“EIC”) and Laurentian Organic Inc. ("Laurentian") are also licensed under the Cannabis Act as described below.

The Company’s head and registered office is located at 35 English Drive, Moncton, New Brunswick, E1E 3X3. The Company’s common shares (“Common Shares”) are listed under the ticker symbol “OGI” on both the Nasdaq Global Select Market (“NASDAQ”) and on the Toronto Stock Exchange (“TSX”). Any inquiries regarding the Company may be directed by email to investors@organigram.ca.

Additional information relating to the Company, including the Company’s most recent annual information form (the “AIF”), is available under the Company’s issuer profile on the Canadian Securities Administrators’ System for Electronic Document Analysis and Retrieval (“SEDAR”) at www.sedar.com. The Company’s reports and other information filed with or furnished to the United States Securities and Exchange Commission (“SEC”) are available on the SEC’s Electronic Document Gathering and Retrieval System (“EDGAR”) at www.sec.gov.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 1

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

Certain information herein contains or incorporates comments that constitute forward-looking information within the meaning of applicable securities legislation (“forward-looking information”). Forward-looking information, in general, can be identified by the use of forward-looking terminology such as “outlook”, “objective”, “may”, “will”, “could”, “would”, “might”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “plan”, “continue”, “budget”, “schedule” or “forecast” or similar expressions suggesting future outcomes or events. They include, but are not limited to, statements with respect to expectations, forecasts or other characterizations of future events or circumstances, and the Company’s objectives, goals, strategies, beliefs, intentions, plans, estimates, projections and outlook, including statements relating to the Company’s plans and objectives, or estimates or predictions of actions of customers, suppliers, partners, distributors, competitors or regulatory authorities; and statements regarding the Company’s future economic performance. These statements are not historical facts but instead represent management beliefs regarding future events, many of which by their nature are inherently uncertain and beyond management control. Forward-looking information has been based on the Company’s current expectations about future events.

Certain forward-looking information in this MD&A includes, but is not limited to the following:

•Moncton Campus (as defined herein), Winnipeg facility (as defined herein) and Laurentian Facility (as defined herein) licensing and target production capacity and timing thereof;

•Expectations regarding production capacity, facility size, THC (as defined herein) content, costs and yields;

•Expectations regarding the prospects of the Company’s collaboration with a wholly-owned subsidiary of British American Tobacco plc (together, "BAT");

•Expectations regarding the prospects for the Company’s subsidiary EIC;

•Expectations regarding the prospects for the Company's newly acquired subsidiary Laurentian;

•The ongoing impact of the current global health crisis caused by COVID-19 (as defined below);

•Expectations around demand for cannabis and related products, future opportunities and sales, including the relative mix of medical versus adult-use recreational products, the relative mix of products within the adult-use recreational category including wholesale, the Company’s financial position, future liquidity and other financial results;

•Legislation of additional cannabis types and forms for adult-use in Canada including regulations relating thereto and the implementation thereof and our future product forms;

•Expectations around branded products and derivative-based products with respect to timing, launch, product attributes, composition and consumer demand;

•Strategic investments and capital expenditures, and expected related benefits;

•Expectations regarding the resolution of litigation and other legal proceedings;

•The general continuance of current, or where applicable, assumed industry conditions;

•Changes in laws, regulations and guidelines, including those relating to the recreational and/or medical cannabis markets domestically and internationally;

•The price of cannabis and derivative cannabis products;

•Expectations around the availability and introduction of new genetics including consistency and quality of plants and the characteristics thereof;

•The impact of the Company’s cash flow and financial performance on third parties, including its supply partners;

•Fluctuations in the price of Common Shares and the market for the Common Shares;

•The treatment of the Company’s business under governmental regulatory regimes and tax laws, including the Excise Act (as defined herein) and the renewal of the Company’s licenses thereunder and the Company’s ability to obtain export licenses from time to time;

•The Company’s growth strategy, targets for future growth and forecasts of the results of such growth;

•Expectations concerning access to capital and liquidity and the Company’s ability to access the public markets to fund operational activities and growth;

•The Company’s ability to remain listed on the TSX and NASDAQ and the impact of any actions it may be required to take to remain listed;

•The ability of the Company to generate cash flow from operations and from financing activities;

•The competitive conditions of the industry, including the Company’s ability to maintain or grow its market share;

•Moncton Campus and Laurentian Facility expansion plans, capital expenditures, current and targeted production capacity and timing thereof; and

•Expectations concerning Fiscal 2022 performance including with respect to revenue, adjusted gross margins and SG&A.

Forward-looking information is provided for the purposes of assisting the reader in understanding the Company and its business, operations, risks, financial performance, financial position and cash flows as at and for the periods ended on certain dates, and to present information about management’s current expectations and plans relating to the future, and the reader is cautioned that such statements may not be appropriate for other purposes. In addition, this MD&A may contain forward-looking information attributed to third party industry sources. Undue reliance should not be placed on forward-looking

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 2

information, as there can be no assurance that the plans, intentions or expectations upon which they are based will occur. Forward-looking information does not guarantee future performance and involves known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in the forward-looking information. By its nature, forward-looking information involves numerous assumptions, known and unknown risks and uncertainties, both general and specific, that contribute to the possibility that the expectations, predictions, forecasts, projections and conclusions will not occur or prove accurate, that assumptions may not be correct, and that objectives, strategic goals and priorities will not be achieved. These and other factors that may cause actual results or events to differ materially from those anticipated in the forward-looking information.

Factors that could cause actual results to differ materially from those set forth in forward-looking information include, but are not limited to: financial risks; dependence on senior management, the board of directors of the Company (the “Board of Directors”), consultants and advisors; availability and sufficiency of insurance including continued availability and sufficiency of director and officer and other forms of insurance; the Company and its subsidiaries being able to, where applicable, cultivate cannabis pursuant to applicable law and on the currently anticipated timelines; industry competition; general economic conditions and global events, including COVID-19 retail store closures or reduced sales at retail stores or otherwise due to COVID-19; heightened economic and industry uncertainty as a result of COVID-19 and governmental action in respect thereto, including with respect to impacts on production, operations, product development, new product launches, disclosure controls and procedures or internal control over financial reporting, including as they may be impacted by delays in remediation due to work from home policies and other COVID-19 impacts, demand for products and services, third-party suppliers or service providers, and any existing or new international business partnerships; production facilities running at less than full capacity due to reduced workforce for reasons related to COVID-19 (as described herein) and market demand; potential supply chain and distribution disruptions; product development, facility and technological risks; changes to government laws, regulations or policy, including environmental or tax, or the enforcement thereof; agricultural risks; ability to maintain any required licenses or certifications; supply risks; product risks; construction delays or postponements; packaging and shipping logistics; expected number of medical and adult-use recreational cannabis users in Canada and internationally; potential time frame for the implementation of legislation to legalize cannabis internationally; the Company’s, its subsidiaries' and its investees’ ability to, where applicable, obtain and/or maintain their status as Licensed Producers (as defined herein) or other applicable licenses; risk factors affecting its investees; availability of any required financing on commercially attractive terms or at all; the potential size of the regulated adult-use recreational cannabis market in Canada; demand for and changes in the Company’s cannabis and related products, including the Company’s derivative products (as defined herein), and the sufficiency of the retail networks to supply such demand; ability to enter and participate in international market opportunities; general economic, financial market, regulatory, industry and political conditions affecting the Company; the ability of the Company to compete in the cannabis industry and changes in the competitive landscape; a material decline in cannabis prices; the Company’s ability to manage anticipated and unanticipated costs; the Company’s ability to implement and maintain effective internal control over financial reporting and disclosure controls and procedures; and, other risks and factors described from time to time in the documents filed by the Company with securities regulators in Canada and the United States. Material factors and assumptions used in establishing forward-looking information include that construction and production activities will proceed as planned, and demand for cannabis and related products will change in the manner expected by management, in each case after taking into account any impacts related to COVID-19 that are currently known or predicted by management based on the limited information available and the fluidity and uncertainty of the crisis. All forward-looking information is provided as of the date of this MD&A.

The Company does not undertake to update any such forward-looking information whether as a result of new information, future events or otherwise, except as required by law.

ADDITIONAL INFORMATION ABOUT THE ASSUMPTIONS, RISKS AND UNCERTAINTIES OF THE COMPANY’S BUSINESS AND MATERIAL FACTORS OR ASSUMPTIONS ON WHICH INFORMATION CONTAINED IN FORWARD-LOOKING INFORMATION IS BASED IS PROVIDED IN THE COMPANY’S DISCLOSURE MATERIALS, INCLUDING IN THIS MD&A UNDER “RISK FACTORS” AND THE COMPANY’S CURRENT AIF UNDER “RISK FACTORS”, FILED WITH THE SECURITIES REGULATORY AUTHORITIES IN CANADA AND AVAILABLE UNDER THE COMPANY’S ISSUER PROFILE ON SEDAR AT WWW.SEDAR.COM, AND FILED WITH OR FURNISHED TO THE SEC AND AVAILABLE ON EDGAR AT WWW.SEC.GOV. ALL FORWARD-LOOKING INFORMATION IN THIS MD&A IS QUALIFIED BY THESE CAUTIONARY STATEMENTS.

CAUTIONARY STATEMENT REGARDING CERTAIN NON-IFRS MEASURES

This MD&A contains certain financial and operational performance measures that are not recognized or defined under IFRS (“Non-IFRS Measures”). As there are no standardized methods of calculating these Non-IFRS Measures, the Company's approaches may differ from those used by others, and, this data may not be comparable to similar data presented by other licensed producers of cannabis and cannabis companies. For an explanation of these measures to related comparable financial information presented in the Interim Financial Statements prepared in accordance with IFRS, refer to the discussion below.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 3

The Company believes that these Non-IFRS Measures are useful indicators of operating performance and are specifically used by management to assess the financial and operating performance of the Company. These Non-IFRS Measures include, but are not limited, to the following:

•Net revenue represents revenue from the sale of cannabis and non-cannabis products. Net revenue is further broken down as follows:

◦Medical net revenue represents Canadian net revenue for medical cannabis sales direct to patient and to Canadian medical wholesale only.

◦Recreational net revenue represents net revenue for recreational consumer sales only.

◦International and Wholesale net revenue represents cannabis net revenue from international and domestic wholesale bulk cannabis only.

◦Other net revenue represents non-cannabis net revenue for other support functions only.

Management believes the net revenue measures provide more specific information about the net revenue purely generated from its core cannabis business and by market type.

•Average net selling price per gram and per unit are calculated by taking net revenue, which is then divided by total grams or total units sold in the period. Average net selling price per gram and per unit is further broken down as follows:

◦Average net selling price per gram of dried flower represents the average net selling price per gram for dried flower sales only, including medical sales, domestic and international wholesale bulk cannabis sales in the period.

Management believes the average net selling price per gram or per unit provide more specific information about the pricing trends over time by product type.

•Yield per plant in grams is calculated by taking the total amount of grams of dried flower harvested, excluding trim, and dividing it by the total number of plants harvested.

Management believes that yield per plant in grams provides a useful measure about the efficiencies gained through its operating activities.

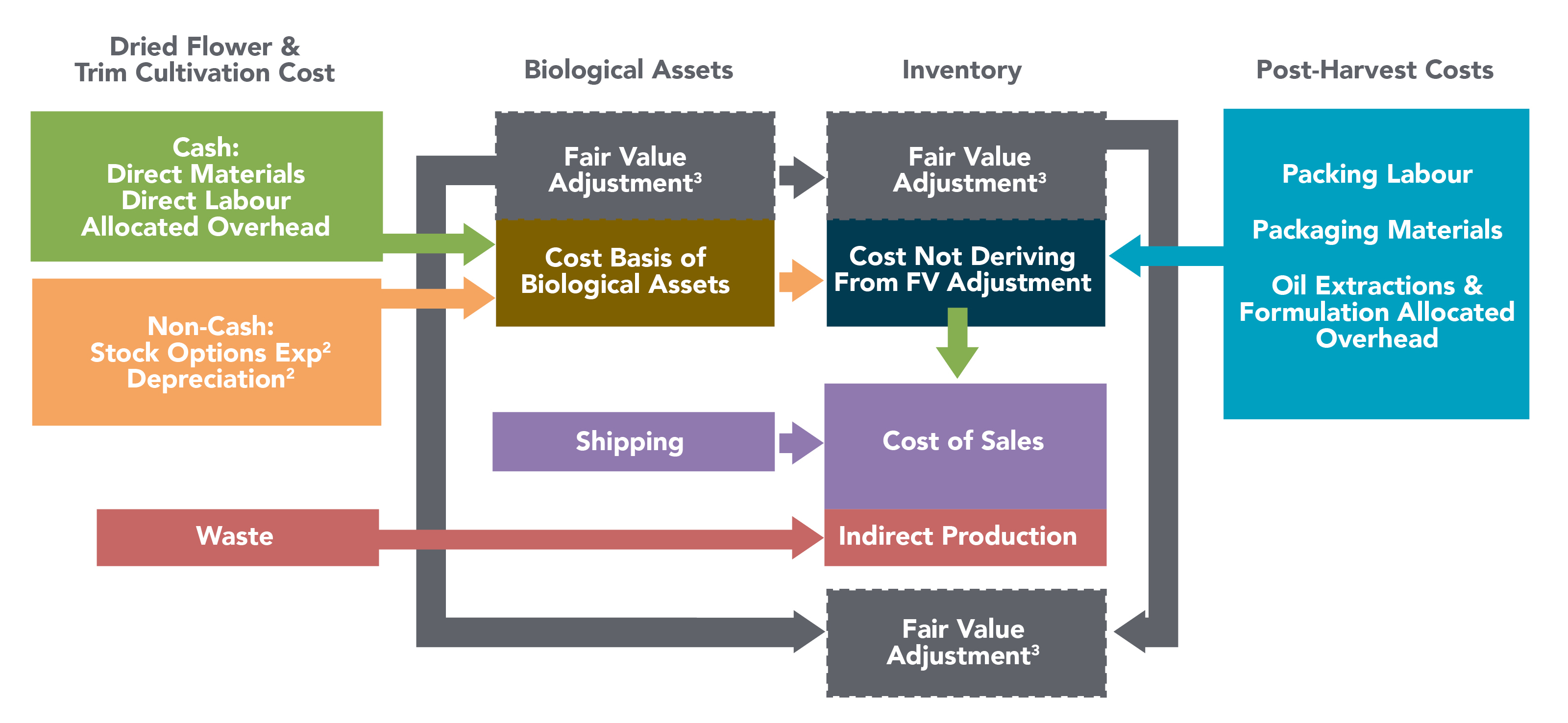

•Gross margin before fair value adjustments is calculated by subtracting cost of sales, before the effects of unrealized gain (loss) on changes in fair value of biological assets, realized fair value on inventories sold and other inventory charges from total net revenue. Gross margin before fair value adjustments percentage is calculated by dividing gross profit before fair value adjustments (defined above) divided by net revenue.

Management believes that these measures provide useful information to assess the profitability of our cannabis operations as it excludes the effects of non-cash fair value adjustments on inventory and biological assets, which are required by IFRS.

•Adjusted gross margin is calculated by subtracting cost of sales, before the effects of (i) unrealized gain (loss) on changes in fair value of biological assets; (ii) realized fair value on inventories sold and other inventory charges; (iii) provisions and impairment of inventories and biological assets; (iv) provisions to net realizable value; (v) COVID-19 related charges; and (vi) unabsorbed overhead relating to underutilization of the production facility grow rooms and manufacturing equipment, most of which is related to non-cash depreciation expense, from net revenue. Adjusted gross margin percentage is calculated by dividing adjusted gross margin by net revenue. Adjusted gross margin is reconciled to IFRS in the "Financial Review and Discussion of Operations" section of this MD&A.

Management believes that these measures provide useful information to assess the profitability of our operations as it represents the normalized gross margin generated from operations and excludes the effects of non-cash fair value adjustments on inventories and biological assets, which are required by IFRS. The most directly comparable measure to adjusted gross margin calculated in accordance with IFRS is gross margin before fair value changes to biological assets and inventories sold.

•Adjusted EBITDA is calculated as net income (loss) excluding: financing costs, net of investment income; income tax expense (recovery); depreciation, amortization, reversal of/or impairment, gain (loss) on disposal of property, plant and equipment (per the condensed consolidated interim statement of cash flows); share-based compensation (per the condensed consolidated interim statement of cash flows); share of loss and impairment loss from loan receivable and investments in associates; change in fair value of contingent consideration; change in fair value of derivative liabilities; expenditures incurred in connection with research & development activities; unrealized gain (loss) on changes in fair value of biological assets; realized fair value on inventories sold and other inventory charges;

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 4

provisions to net realizable value of inventories; COVID-19 related charges; government subsidies; legal provisions; incremental fair value component of inventories sold from acquisitions; transaction costs; and share issuance costs. Adjusted EBITDA is reconciled to IFRS in the "Financial Review and Discussion of Operations" section of this MD&A.

Adjusted EBITDA is intended to provide a proxy for the Company’s operating cash flow and derive expectations of future financial performance for the Company, and excludes adjustments that are not reflective of current operating results. The most directly comparable measure to adjusted EBITDA calculated in accordance with IFRS is net income (loss).

Non-IFRS Measures should be considered together with other data prepared in accordance with IFRS to enable investors to evaluate the Company’s operating results, underlying performance and prospects in a manner similar to the Company’s management. Accordingly, these non-IFRS measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

BUSINESS OVERVIEW

NATURE AND HISTORY OF THE COMPANY’S BUSINESS

The Company’s wholly-owned subsidiary Organigram Inc. is a Licensed Producer of cannabis under the Cannabis Act.

The Company conducts most of its operations at its facility located in Moncton, New Brunswick. The Company has expanded its main facility over time to create additional production capabilities by strategically acquiring land and buildings adjacent to the main facility (together, the “Moncton Campus”), including to add capacity for the manufacture of derivative products allowed for legal sale by Licensed Producers under amendments to the Cannabis Act.

Patients order medical cannabis dried flower and cannabis derivative-based products from the Company primarily through the Company’s online store or by phone. Medical cannabis dried flower and cannabis derivative-based products are delivered by secure courier or other methods permitted by the Cannabis Act. The Company’s prices may vary based on grow time, strain yield, THC level, terpene profile and market conditions.

The Company is also authorized for wholesale shipping of cannabis plant cuttings, dried flower, blends, pre-rolls and cannabis derivative-based products to approved retailers and wholesalers for adult-use recreational cannabis under the individual provincial and territorial regulations as per the Cannabis Act.

In March 2021, the Company formed a Product Development Collaboration ("PDC") with BAT, a leading, multi-category consumer goods business, and established a "Centre of Excellence" (the "CoE") to focus on the next generation of cannabis products with an initial focus on CBD. The CoE is established at the Company's Moncton Campus, which holds the Health Canada licenses required to conduct research and development activities with cannabis products. Both companies contributed scientists, researchers, and product developers to the CoE which is governed and supervised by a steering committee consisting of an equal number of senior members from both companies. Under the terms of the PDC Agreement, both Organigram and BAT have access to certain of each other’s intellectual property (“IP”) and, subject to certain limitations, have the right to independently, globally commercialize the products, technologies and IP created by the CoE pursuant to the PDC Agreement.

During April 2021, the Company expanded its manufacturing and production footprint with the acquisition of EIC (the "Winnipeg Facility"), located in Winnipeg, Manitoba. The Winnipeg Facility holds a research license and standard processing license under the Cannabis Act and is in the process of completing its application to add the sale of derivative products, including cannabis edibles, to its standard processing license. As a wholly-owned subsidiary, EIC enables the Company to penetrate a new product category and gain access to its leadership's expertise in the confectionary space. The Winnipeg Facility also provides the Company with a share of the cannabis infused gummies market.

The Company has additional cannabis production capacity at its new wholly-owned subsidiary, Laurentian, located in Lac-Supérieur, Quebec (the "Laurentian Facility"), acquired on December 21, 2021. The Laurentian Facility has a cultivation focus on artisanal craft flower and on the production of hash, a cannabis derivative. Laurentian provides the Company with a foothold in the important Quebec market, and also adds to the Company's premium product portfolio, providing further opportunities for margin expansion. Laurentian holds a standard processing and cultivation license under the Cannabis Act.

STRATEGY

Organigram’s strategy is to leverage its broad brand and product portfolio and culture of innovation to increase market share, drive profitability and grow into an industry leader that delivers long-term shareholder value.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 5

The pillars of the Company’s strategy are:

1.Innovation

2.Consumer Focus

3.Efficiency

4.Market Expansion

1. Innovation

Meeting the demands of a fast-growing industry with changing consumer preferences requires the ability to innovate and create breakthrough products that are embraced by the market and establish a long-term competitive advantage.

The Company is committed to maintaining a culture of innovation and has established a track record of introducing differentiated products that are able to quickly capture market share, specifically:

•SHRED X Kief-Infused Blends: an innovative milled flower product with a 50%/50% kief and flower combination that delivers convenience and flavour with high potency;

•SHRED: the first milled flower product, blended to create curated flavour profiles; and

•Edison JOLTS: Canada’s first flavoured high-potency lozenge with 100 mg of THC per package.

Consistent with its innovation culture, in Fiscal 2021, the Company announced the launch of its CoE as part of its PDC with BAT, a leading multi-category consumer goods business. The CoE focuses on research and development to develop the next generation of cannabis products, with an initial focus on CBD.

The Company has also made a strategic investment in Hyasynth Biologicals Inc. ("Hyasynth"), a biotechnology company that is deploying proprietary technology to develop cannabinoids using biosynthesis. During the quarter, the Company made an additional investment in Hyasynth as described herein.

2. Consumer Focus

The Company seeks to address the changing needs of the adult cannabis consumer through its broad product portfolio with offerings in the most popular categories and price points. Based on ongoing consumer research, the portfolio is refreshed frequently with different flower strains, new package formats and new product introductions. The Company’s alignment with consumers is evidenced by its growing market share and category leadership:

•SHRED Tropic Thunder and Funk Master: #1 and #2 top selling flower products1;

•Edison JOLTS: #1 position for ingestible extracts2; and

•SHRED’ems gummies: among the top-selling gummies in Canada and provide the Company with a #3 share in the gummies category1.

In addition to third-party and direct consumer research, the Company maintains close contact with consumers through an active social presence and has established the Cannabis Innovators Panel. This online panel engages with up to 2,500 cannabis consumers across Canada on a regular basis and helps to inform the Company on product development and brand initiatives.

3. Efficiency

From its inception, the Company has remained committed to being an efficient operator.

The Company’s growing facility in Moncton, New Brunswick utilizes three-tier cultivation technology to maximize square footage. The facility has a proprietary information technology in place to track all aspects of the cannabis cultivation and harvest process. The Company maintains a continuous improvement program to maximize harvest yield while reducing operating costs. This is complemented by the introduction of automation in post-harvest production, including two pre-roll machines.

The Company’s Winnipeg Facility is highly-automated and able to efficiently handle both small-batch artisanal manufacture of edibles as well as large-scale nutraceutical-grade production. The facility provides the Company with the unique ability to produce a wide range of high-quality edible products at attractive price points.

The Company's Laurentian Facility, houses a cultivation and derivatives processing facility. The Company has committed $11 million in growth capital expenditures based on current expectations for the cost of expanding the facility to increase capacity, processing and storage space and deliver on automation.

1 Hifyre data extract from March 25, 2022

2 Edison JOLTS was recorded as the most sold item in the capsules and mints category, Hifyre data extract from March 25, 2022

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 6

Key efficiency milestones achieved or planned in Fiscal 2022 include:

•Significant reduction in cultivation costs, to achieve a 25% cost decrease from Fiscal 2021's average amount (Q2 2022 year to date was a 42% reduction from the prior years comparison six month period);

•Doubling the harvest volume exceeding THC levels of 22% compared to Fiscal 2021;

•Adding two pre-roll machines at the Moncton Campus; and

•Commissioning high-speed pouch packing lines for SHRED and Big Bag O' Buds products.

4. Market Expansion

The Company is committed to expanding its market presence by adding to its product offering and enhancing its geographical presence. This strategy is enabled by strategic merger and acquisition opportunities and assessing expansion into international markets.

Recent examples of market expansion include:

•December 2021 acquisition of Laurentian which adds craft cultivation and hash to the Company's product portfolio and increases its presence in Quebec;

•Shipments to Canndoc in Israel and Cannatrek in Australia to supply bulk cannabis into these markets generating $4.4 million in net revenue during Q2 2022;

KEY QUARTERLY FINANCIAL AND OPERATING RESULTS

| Q2-2022 | Q2-2021 | CHANGE | % CHANGE | ||||||||||||||||||||

| Financial Results | |||||||||||||||||||||||

| Gross revenue | $ | 43,934 | $ | 19,292 | $ | 24,642 | 128 | % | |||||||||||||||

| Net revenue | $ | 31,836 | $ | 14,643 | $ | 17,193 | 117 | % | |||||||||||||||

| Cost of sales | $ | 24,955 | $ | 31,146 | $ | (6,191) | (20) | % | |||||||||||||||

| Gross margin before fair value adjustments and other charges | $ | 6,881 | $ | (16,503) | $ | 23,384 | nm | ||||||||||||||||

Gross margin % before fair value adjustments and other charges(1) | 22 | % | (113) | % | 135 | % | nm | ||||||||||||||||

| Operating expenses | $ | 18,019 | $ | 12,077 | $ | 5,942 | 49 | % | |||||||||||||||

Adjusted EBITDA(2) | $ | 1,556 | $ | (7,840) | $ | 9,396 | (120) | % | |||||||||||||||

| Net loss | $ | (4,047) | $ | (66,389) | $ | 62,342 | nm | ||||||||||||||||

| Net cash used in operating activities | $ | (803) | $ | (10,430) | $ | 9,627 | nm | ||||||||||||||||

Adjusted Gross Margin(3) | $ | 8,255 | $ | (680) | $ | 8,935 | nm | ||||||||||||||||

Adjusted Gross Margin %(3) | 26 | % | (5) | % | 31 | % | (620) | % | |||||||||||||||

| Financial Position | |||||||||||||||||||||||

Working capital(4) | $ | 189,597 | $ | 112,398 | $ | 77,199 | 69 | % | |||||||||||||||

| Inventories and biological assets | $ | 56,187 | $ | 43,374 | $ | 12,813 | 30 | % | |||||||||||||||

| Total assets | $ | 585,102 | $ | 392,764 | $ | 192,338 | 49 | % | |||||||||||||||

| Operating Results | |||||||||||||||||||||||

| Kilograms harvested - dried flower | 10,037 | 4,467 | 5,570 | 125 | % | ||||||||||||||||||

| Kilograms sold - dried flower | 11,785 | 3,688 | 8,097 | 220 | % | ||||||||||||||||||

Note 1: Equals gross margin before fair value adjustments (as reflected in the Interim Financial Statements) divided by net revenue.

Note 2: Adjusted EBITDA is a non-IFRS measure that the Company defines as net income (loss) before: financing costs, net of investment income; income tax expense (recovery); depreciation, amortization, reversal of/or impairment, gain (loss) on disposal of property, plant and equipment (per the statement of cash flows); share-based compensation (per the statement of cash flows); share of loss and impairment loss from loan receivable and investments in associates; change in fair value of contingent consideration; change in fair value of derivative liabilities; expenditures incurred in connection with research & development activities; unrealized gain (loss) on changes in fair value of biological assets; realized fair value on inventories sold and other inventory charges; provisions to net realizable value of inventories; impairment of biological assets; COVID-19 related charges; government subsidies; legal provisions; incremental fair value component of inventories sold from acquisitions; transaction costs; and share issuance costs. See the cautionary statement regarding non-IFRS financial measures in the “Introduction” section at the beginning of this MD&A and the reconciliation to IFRS measures in the "Financial Results and Review of Operations" section of this MD&A.

Note 3: Adjusted gross margin is a non-IFRS measure that the Company defines as net revenue less: (i) cost of sales, before the effects of unrealized gain (loss) on changes in fair value of biological assets, realized fair value on inventories sold and other inventory charges; excluding (ii) provisions and impairment of inventories and biological assets; (iii) provisions to net realizable value; (iv) COVID-19 related charges; and (v) unabsorbed overhead relating to underutilization of the production facility and equipment, most of which is related to non-cash depreciation expense. See the cautionary statement regarding non-IFRS financial measures in the “Introduction” section at the beginning of this MD&A and the reconciliation to IFRS measures in the "Financial Results and Review of Operations section of this MD&A. Adjusted gross margin % equals adjusted gross margin divided by net revenue.

Note 4: Equals current assets less current liabilities (as reflected in the Interim Financial Statements).

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 7

REVENUE

For the three months ended February 28, 2022, the Company reported $31,836 in net revenue. Of this amount $24,887 (78%) was attributable to sales to the adult-use recreational market, $4,437 (14%) to the international market, $1,920 (6%) to the medical market and $592 (2%) to other revenues. Q2 Fiscal 2022 net revenue increased 117%, or $17,193, from the prior year comparative period’s net revenue of $14,643, primarily due to an increase of $12,899 in adult-use recreational revenue, an increase in international revenue by $4,363, partly offset by the $(141) decrease in medical revenue. Net revenue from the adult-use recreational market was higher by $12,899 (108%), generated from a significant increase in sales volumes from value oriented product sold in Q2 2022, which also carry a lower average selling price.

Sale of flower from all product categories and distribution channels comprised 77% of net revenue in the quarter. The average net selling price ("ASP") of flower decreased to $2.08 per gram than as compared to $2.99 per gram for Q2 Fiscal 2021, as both the Company and the Canadian cannabis industry continued to experience general price compression in the adult-use recreational and medical markets as these markets matured, and the customer and product mix evolved to focus more on value offerings. Selling prices are prone to fluctuation and there may be further price compression if the market remains oversupplied. The Company is committed to refining its product mix as customer preferences evolve and it continues to revitalize its higher margin Edison branded flower products.

The volume of flower sales in grams increased 220% to 11,785 kg in Q2 Fiscal 2022 compared to 3,688 kg in the prior year comparative quarter, primarily as a result of the market shift towards large format value products and the success of the Company's products in these brands and formats.

COST OF SALES

Cost of sales for the three months ended February 28, 2022 decreased to $24,955 compared to $31,146 in the prior year comparative period, primarily as a result of $12,838 reduction in inventory provisions and net realizable adjustments to cost of inventory in the current period, compared to the prior period comparative, offset by an increase in sales volume in the adult-use recreational market. Included in Q2 Fiscal 2022 cost of sales are $711 of inventory provisions related to provisions for unsaleable inventories and to reflect an estimated decline in selling prices. Additionally, $nil was incurred with respect to unabsorbed fixed overhead costs as a result of improved operating production volumes at the Moncton Campus. The prior fiscal year’s comparative period had inventory provisions and net realizable value adjustments of $13,549, as well as unabsorbed fixed overhead costs of $2,274.

GROSS MARGIN BEFORE FAIR VALUE ADJUSTMENTS AND ADJUSTED GROSS MARGIN

The Company realized gross margin before fair value adjustments for the three months ended February 28, 2022 of $6,881, or 22% as a percentage of net revenue, compared to $(16,503), or (113)%, in the prior year comparative period. The increase in gross margin before fair value adjustments as a percentage of net revenue is largely due to higher net revenue, reduction in both inventory provisions and unabsorbed overhead costs and lower cost of sales per unit sold in Q2 Fiscal 2022.

Adjusted gross margin3 for the three months ended February 28, 2022 was $8,255, or 26% as a percentage of net revenue, compared to $(680), or (5)%, in the prior year comparable quarter. This was largely due to the current period's lower cost of sales combined with a higher overall sales volumes, net of the impact of the lower ASP from the shift in the sales mix to value priced products and brands. Please refer to the “Financial Review and Discussion of Operations” section of this MD&A for a reconciliation of adjusted gross margin to net revenue.

OPERATING EXPENSES

Operating expenses include: General and administrative; sales and marketing; research and development; share-based compensation expenses; along with impairment on property, plant and equipment and intangible assets. During Q2 Fiscal 2022, the operating expenses were $18,019, which is an increase from the prior year comparative amount to $12,077, primarily due to the higher employee costs from the growth of the team, higher trade and marketing spend, an increase in technology spend, research and development costs as well as a $2,000 impairment charge relating to the decommissioned Moncton chocolate line (as part of the Company's review of efficiencies between sites, chocolate will now be produced from the Winnipeg Facility).

General and administrative expenses of $10,581 increased from the prior year's comparison quarter of $7,188, primarily due to an increase in general office expenses as a result of the Company's growth, an increase in employee costs, an increase to technology costs, and also for one-time transaction and on-going costs from the acquisition of Laurentian.

Sales and marketing expenses of $3,417 increased from the prior year's comparative quarter of $3,141, primarily due to higher advertising and promotion costs, and marketing initiatives related to the launch of the Company's new products.

3 Adjusted gross margin is a non-IFRS financial measure. See the cautionary statement regarding non-IFRS financial measures in the “Introduction” section of this MD&A, and the discussion under the heading “Adjusted EBITDA” and the reconciliation to IFRS measures in the "Financial Results and Review of Operations" section of this MD&A.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 8

Research and development costs of $1,184 increased from the prior year's comparative quarter of $802, primarily due to the current periods' cost for the CoE.

ADJUSTED EBITDA

Positive adjusted EBITDA4 was $1,556 in Q2 Fiscal 2022 compared to negative adjusted EBITDA of $7,840 in Q2 Fiscal 2021. The $9,396 increase in adjusted EBITDA is primarily attributed to the increase in adjusted gross margins due to the higher volume of products sold, the impact of lower production costs that decreased cost of sales per unit sold, offset by the impact of lower ASP from higher quantities of value brands sold and by the increase in general and administrative expenses during Q2 Fiscal 2022. Please refer to the “Financial Review and Discussion of Operations” section of this MD&A for a reconciliation of adjusted EBITDA to net gain.

NET LOSS

The net loss was $4,047 in Q2 Fiscal 2022 compared to a net loss of $66,389 in Q2 Fiscal 2021. The decrease in net loss was primarily attributed to higher gross margin as described above and the $10,633 impact of the change in the fair value of derivative liabilities compared to Q2 Fiscal 2021.

FINANCIAL POSITION

Working capital as at February 28, 2022 decreased to $189,597 from $234,349 as at August 31, 2021 mainly due to the purchase of property, plant and equipment of $15,708, the acquisition of Laurentian for cash consideration of $7,000, increased investment in Hyasynth of $2,595 and cash used in operating activities of $10,144.

KEY DEVELOPMENTS DURING THE QUARTER AND SUBSEQUENT TO FEBRUARY 28, 2022

On December 21, 2021, the Company announced the acquisition of Laurentian, a Quebec-based licensed producer of artisanal craft cannabis and hash for $36 million, net of working capital adjustments, plus earnout share consideration, if any. The acquisition is expected to be accretive, adds more premium products to the Company's portfolio and strengthens its presence in the province of Quebec.

On December 22, 2021, the Company announced that it had made an additional $2.5 million investment in Hyasynth. The Company has to date invested $10 million in Hyasynth, a pioneer in the field of cannabinoid science and biosynthesis. The investment positions the Company to benefit from advances in cannabinoid technology and deploy new active ingredients for consumer products in the health and wellness and recreational spaces.

On February 24, 2022, the Company announced the election of its Board of Directors, and the appointment of BAT's nominee Simon Ashton to the Board.

On March 1, 2022, the Company announced that BAT had invested $6.3 million to exercise its rights pursuant to an Investor Rights Agreement to enhance its equity ownership position in the Company to 19.4% (as at December 31, 2021) from 18.8%. The Investor Rights Agreement was entered into between the Company and BAT in connection with the formation of the PDC between the two companies and the strategic investment of $221 million made by BAT in March 2021.

On March 17, 2022, the Company launched its social impact strategy, Organigram Operating for Good, joining the Pledge 1% movement by donating up to 1% of employee time towards causes aimed at "Building Healthy Communities Where We Live and Work."

OPERATIONS AND PRODUCTION

Moncton Cultivation Campus

While the vast majority of incremental production capacity in the initial period of recreational legalization by the Company’s competitors was generated from greenhouse (not indoor) production, Organigram focused on a core competency of controlling conditions in precisely built indoor environments with a commitment to continuous improvement and investment in information technology.

4 Adjusted EBITDA is a non-IFRS financial measure. See the cautionary statement regarding non-IFRS financial measures in the “Introduction” section of this MD&A, and the discussion under the heading “Adjusted EBITDA” and the reconciliation to IFRS measures in the "Financial Results and Review of Operations" section of this MD&A.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 9

The Company continually assesses the critical facets of the lighting and environmental elements in its facilities in an effort to drive maximum quality and yield in the plants it cultivates. It is the Company’s intention to continually improve and refine its cultivation and post-harvesting practices in an effort to achieve a competitive advantage in the space.

In Fiscal 2021, as part of its continuous improvement program, the Company implemented various new initiatives at the Moncton Campus such that the average THC content per plant and average yield per plant both increased in the second half of Fiscal 2021. "THC" refers to tetrahydrocannabinol, the principal psychoactive compound in cannabis. Higher THC content continues to be desired by consumers and the higher yield per plant combined with greater economies of scale on ramping up cultivation capacity has resulted in lower cultivation costs per gram and ultimately benefits adjusted gross margins when the product is sold. The Company continues to believe it is well-positioned and supported by the flexibility of the facility at the Moncton Campus to continue to see improvement in these areas. As the Company works with a number of different genetics and cultivars this process of improvement may not be linear or consistent across plants.

As part of its review of the continually expanding Canadian cannabis markets, its long-term demand forecast model and its cultural commitment to continuous improvement, management is reviewing its production capacity and methodologies with a focus on cost reductions which will further improve margins over time. Management obtained approval from the Board of Directors to complete the Phase 4C expansion of its Moncton Campus which will significantly increase capacity, enabling the Company to meet the increased consumer demand for its products. The Company has also identified additional changes to its growing and harvesting methodologies, including facility design improvements that should assist the operating conditions of the Moncton Campus resulting in higher quality flower and a reduction to production costs. The current approximate annual capacity is 55,000 kg of flower as of the date of this MD&A and the increase to the number of growing rooms and yield improvements are targeted when complete to result in an approximate annual production capacity of 80,000 kg of flower. The total capacity of the Moncton Campus will continue to fluctuate as the Company further refines its growing methods and room utilization.

The Company harvested 10,037 kg of dried flower during Q2 Fiscal 2022 compared to 4,467 kg of flower in Q2 Fiscal 2021. The increase of 5,570 kg (125%) from the comparative period was primarily related to increased cultivation planting and staffing during Q4 Fiscal 2021 and Q1 Fiscal 2022, that was done in order to meet the increased demand for many of its new products as part of its product portfolio revitalization as well as the increase in industry demand on the back of the ongoing accelerated retail store build out particularly in Ontario.

Moncton Edibles and Derivatives Facility

Contained in the 56,000 square foot expansion referred to as Phase 5 of the Moncton Campus is the Company's edibles and derivative facility. This space includes, among other things, additional extraction capacity and, office space and was designed under European Union GMP (“EU GMP”) standards. EU GMP describes the minimum standard that a manufacturer must meet in its production processes. EU GMP certification is subject to inspections coordinated by the European Medicines Agency. The Company has no plans to seek certification in the immediate future but continues to evaluate paths to certification. The facility includes CO2 and Hydrocarbon Extraction equipment, as well as expanded areas for formulation including short path distillation for edibles and vape pen formulas, high speed cart filling and automated packaging. Some of this equipment remains in the commissioning and research and development phase.

Winnipeg Edibles Facility

As part of the EIC acquisition completed in Q3 Fiscal 2021, the Company now has a purpose-built, highly-automated, 51,000 square-foot manufacturing facility in Winnipeg, Manitoba which was also designed under EU GMP standards. The Company has no plans to seek certification in the immediate future but continues to evaluate paths to certification. The facility design and the equipment specifications were also designed to handle both smaller-batch artisanal manufacturing as well as large-scale nutraceutical-grade high-efficiency manufacturing and to produce highly customizable, precise, and scalable cannabis-infused products in various formats and dosages including pectin, gelatin, and sugar-free soft chews (gummies), chocolates, toffee and caramel with novel capabilities such as infusions, striping and the possibility of using fruit purees.

The Winnipeg Facility currently holds a research license and a standard processing license issued under the Cannabis Act; it is in the process of completing its application to add the activity of sale of derivative cannabis products to its Standard Processing License. Until the Winnipeg Facility receives its sales license, it is capable of manufacturing products in bulk for further processing, review and sale by Organigram or third-party Licensed Producers, for which it may provide white-label services in future. The Company commenced commercial operations during Fiscal 2021 and at this time the Winnipeg facility has 51 employees.

The Company has been reviewing the capabilities and efficiencies of the Moncton Campus and Winnipeg Facility to determine how best to allocate its resources and functions across the two sites. As part of these operational efficiency initiatives, during February the Company ceased the production of chocolates from Moncton, and has now decommissioned the Moncton Chocolate line with the intention to manufacture and sell chocolates from its Winnipeg Facility.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 10

Laurentian Facility

The Company acquired Laurentian in December 2021. The Laurentian Facility has 6,800 square feet of cultivation area, which is currently being expanded to 33,000 square feet. The Laurentian Facility is equipped to produce approximately 600 kilograms of flower and 1 million packaged units of hash annually. The expansion program currently underway is expected to increase annual capacity to 2,400 kilograms of flower and 2 million packaged units of hash. The Company has committed $10 million towards completing the expansion and management believes that there are opportunities for costs savings from further investments in automation.

CANADIAN ADULT-USE RECREATIONAL MARKET

Organigram continues to increase its focus on generating meaningful consumer insights and applying these insights to the ongoing optimization of its brand and product portfolio with a goal of ensuring that they are geared towards meeting consumer preferences. The Company aggressively and successfully revitalized its product portfolio to meet rapidly evolving consumer preferences in Fiscal 2021, and through its increased focus on insights in Fiscal 2022, will continue its expansion of brands and products aimed at driving continued momentum in the marketplace.

DRIED FLOWER AND PRE-ROLLS

Dried flower and pre-rolls remain the first and second largest product categories, respectively, in the Canadian adult-use recreational market and the Company believes that these categories will continue to dominate based on the sales history in mature legal markets in certain U.S. states as well as regulatory restrictions on other form factors (e.g. the 10 mg per package THC limit in the edibles category). While we expect consumer preferences will slowly evolve away from THC and price being the key purchase drivers, today they appear to be the most important attributes to consumers for flower products. Over time, genetic diversity and other quality related attributes such as terpene profile, bud density, and aroma, are expected to become increasingly important. While the Company’s efforts are focused on delivering on consumer expectations today, it is concurrently planning for the eventual evolution towards a more nuanced approach to cannabis appreciation through its ongoing work in genetic breeding and pheno-hunting with the goal of offering a unique and relevant assortment to consumers. Additionally, the strategic acquisition of Laurentian in December 2021 provides the Company with the opportunity to participate in the growing craft cannabis segment, through its craft facility located in the province of Quebec.

The Company's portfolio of brands continues to show strong momentum within the flower segment in Canada and as of February 2022 maintains its #1 share in the flower category5. The SHRED varieties Tropic Thunder and Funk Master were the top two flower products sold in Canada, with Gnarberry holding the #4 position5, and Big Bag O' Buds continues to see continued month over month market share momentum in the large format category. The growth and significant contribution of these dried flower value segment brands, however, has also contributed to an overall decline in margins for Organigram and many of its peers over the last number of quarters. To counteract this phenomenon, Organigram is dedicated to revitalizing the Edison brand and product portfolio, by launching new dried flower offerings with unique genetics and higher potency THC. In Q2 2022, two new strains were launched under the Edison brand to appeal to the cannabis enthusiast. The successful completion of these initiatives is expected to increase Edison sales, that have a higher ASP than value brands and therefore attract higher margins. To address the growing demand for strain differentiation in the value segment, post quarter-end, the Company introduced a new strain to its Big Bag O' Buds line to increase the SKUs in market for this product to five.

CANNABIS DERIVATIVES

While dried flower and pre-rolls are currently the largest categories in Canada, derivative cannabis products, including vapes, concentrates and edibles, are projected to continue to increase in market share over the next several years at the expense of flower.

Organigram is committed to these growing categories. The strategic acquisition of EIC in April 2021 provides the Company with the opportunity to produce high quality, edible products such as soft chews (gummies) and chocolates, at scale, positioning the Company to effectively compete in this segment. The acquisition of Laurentian in December 2021 also provides the Company with the ability to produce high-quality hash products in the growing hash segment.

In March 2022, Organigram launched SHRED X Kief-Infused Blends. This is another innovative product that combines milled flower with the cannabis derivative, kief, in a 50-50 ratio. The Company expects that providing the convenience of milled flower with the THC potency of kief will gain popularity with consumers.

SHRED'ems, the Company's cannabis-infused gummies, an extension of the popular, value-priced SHRED brand, were introduced in Q1 Fiscal 2022 and quickly gained momentum within the gummy segment. As of February 2022, all SHRED'ems SKUs were among the top 15 gummies in Canada4. Subsequent to quarter-end, the Company added two flavours to the

5 Source: Data extracted from Hifyre, March 25, 2022

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 11

SHRED'ems line and also introduced SHRED'ems POP! – gummies formulated in three soft drink flavours: Cola, Root Beer and Cream Soda. Monjour, a CBD-forward wellness brand was launched in Q1 of Fiscal 2022 with four SKUs. As of February 2022, Monjour's Berry Good Day product is among the top 20 of gummies sold in Canada. Overall, Organigram holds the #3 market share position in the gummy category5.

Edison JOLTS, mint flavoured, high potency THC lozenges that combine the benefits of sublingual oil with the convenience and portability of soft gels reached the #1 position in terms of number of items sold in the capsules and mints category6. The Company intends to build on the positive momentum of Jolts with further line extensions in the near future.

Organigram intends to leverage the capabilities of the Winnipeg Facility beyond soft chews and is working to offer new and novel chocolate and confectionary product offerings into the Canadian market during Fiscal 2022.

Organigram has renewed its focus on building share within the vape category through unique formulations, premium hardware, and high-quality inputs. Fiscal 2022 will see numerous innovative offerings in the vape segment, all geared towards building our share in this category. In March 2022, the Company launched three new vape SKUs under the SHRED X brand in the popular 510 cartridge format. These have been formulated in the flavour profiles of the SHRED milled flower products.

RESEARCH AND PRODUCT DEVELOPMENT

The Company’s management believes the cannabis industry is still in the nascent stages of product development and that product innovation backed by core fundamental research and development is necessary to establish a long-term competitive advantage in the industry. Research and development and innovation remain a hallmark of Organigram. In fact, there have been many recent efforts and investments made in Fiscal 2021 and early Fiscal 2022 which we anticipate will continue in the remainder of Fiscal 2022 and strengthen the Company's focus in this area and are expected to allow Organigram to continue to position itself to be at the forefront of launching new, innovative, differentiated products and formulations that appeal to adult consumers.

BAT Product Development Collaboration and Centre of Excellence

In early Q4 Fiscal 2021, the Company announced the successful launch of the CoE outlined in the PDC Agreement with BAT which was established to focus on research and product development activities for the next generation of cannabis products, as well as cannabinoid fundamental science, with an initial focus on CBD. The CoE is located at the Moncton Campus, which holds the Health Canada licenses required to conduct research and development activities with cannabis products. The Company and BAT have already created a number of new full-time product development, analytical science and innovation related roles which is expected to ramp up in the second phase of the CoE expansion in Fiscal 2022 when further full time employees will be added. The CoE is governed and supervised by a steering committee consisting of an equal number of senior members from each of the Company and BAT. To date, the CoE remains on schedule for staffing and project planning, and the remaining core construction projects will be completed in Q3 Fiscal 2022. The CoE includes state of the art shared research and development, Good Production Practices ("GPP") food preparation, sensory testing and bio-lab research spaces, and the strategic collaboration has already begun moving from planning to implementation.

As previously disclosed, under the terms of the PDC Agreement, both Organigram and BAT have access to certain of each other’s IP and, subject to certain limitations, have the right to independently, globally commercialize the products, technologies and IP created pursuant to the PDC Agreement. Approximately $31 million of BAT’s investment in Organigram has been reserved for Organigram’s portion of its funding obligations under a mutually agreed initial budget. Costs relating to the CoE are being funded equally by Organigram and BAT. BAT will own all IP developed under this collaboration and will grant to Organigram a royalty-free, perpetual, global license to all such IP. Each party has also agreed to grant to the other a non-exclusive, perpetual and irrevocable license to certain existing IP of such party and its affiliates for purposes of conducting the development activities and exploiting the products, technologies and IP created per the PDC Agreement, subject to certain restrictions.

Plant Science, Breeding and Genomics Research and Development in Moncton

The Company’s cultivation plans focus on developing a pipeline of unique and sought-after genetics, maximizing flower quality in terms of THC yield, terpene profiles and general plant health to meet evolving consumer demand. The Company plans to pursue the expansion of its in-house breeding program dedicating significant research and development space for breeding, phenotyping, screening and various plant science trials while prioritizing commercial cultivation capacity.

Organigram also works with a range of nurseries with different competencies and genetic portfolios in order to screen and identify the latest genetics that will resonate with consumers and grow in the Company's unique environment. The Company believes this kind of strategic and creative product development process is a key differentiator for both the Edison portfolio and the Company overall, and looks forward to introducing more new genetics over the next few quarters.

6 Source: Data extracted from Hifyre, March 25, 2022

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 12

OUTLOOK

The Company's outlook remains positive on the cannabis market both in Canada and internationally. Canada-wide recreational retail sales are expected to total $5.9 billion in calendar 2022.7

The Company believes there are a few factors creating tailwinds to facilitate further industry growth. First, the legalization in October of 2019 of cannabis derivative products has attracted consumers who were not interested in smoking or vaporizing dried flower (including pre-rolls). Newer categories such as vape pens, edibles (soft chews, chocolates), beverages and other ingestible products have significantly expanded the addressable market and proliferation of SKUs continues in these categories offering consumers a wider range of product formulations, flavours and price points. Second, the number of brick-and-mortar retail stores has increased significantly, particularly in Ontario where the number of stores surpassed 1,479 with the national count now surpassing 3,100 stores. Third, the industry as a whole has made a concerted effort to match or beat illicit market pricing, particularly on dried flower, which has helped to accelerate the conversion of consumers from illicit to legal consumption.

Notwithstanding the above, the cannabis industry in Canada remains highly competitive and generally oversupplied versus the current market demand considering both regulated Licensed Producers and the still largely unfettered operations of the illicit market including many online delivery platforms. Since adult-use recreational legalization in Canada, consumer trends and preferences have continued to evolve, including significant growth in the large format value segment, a desire for higher THC potency particularly in dried flower, as well as a penchant for newness, including new genetic strains and novel products. Organigram continues to revitalize its product portfolio to address these changing consumer trends and preferences in order to grow sales and capture market share. We have also seen supply and demand dynamics brought into a more equilibrated state as many of the larger LPs have shuttered surplus cultivation capacity including as a direct result of M&A activities. At the same time, the number of retail stores in Canada began to grow meaningfully for the first time since legalization.

Against this backdrop of strong industry growth, increased demand for the Company's products is evidenced by Organigram's growing national adult-use recreational retail market share ("market share") in Canada. The Company's market share grew from 7.6% in September 2021 to 8.4% in March 2022, ranking Organigram as the #3 licensed producer (LP) in Canada by market share8. Management believes that the Company is better equipped to fulfill demand in Q3 Fiscal 2022 with larger harvests expected as compared to Q2 Fiscal 2022. In addition to the domestic sales growth, during Q2 Fiscal 2022, Organigram completed two shipments to Canndoc Ltd. in Israel and one shipment to Cannatrek in Australia. With a full year of revenues from its Winnipeg Facility, and additional revenues from Laurentian, management expects that the Company will generate higher revenue in Fiscal 2022 as compared to Fiscal 2021.

The Company intends to continue to leverage its Moncton Campus which it believes can provide a sustainable competitive advantage over its peers as a result of having over 100 three-tiered cultivation rooms each with the ability to deliver bespoke growing environmental conditions (lighting, humidity, fertigation, plant density) tailored individually to a wide variety of genetics. With an improved genetics portfolio (including some genetics which are not widely sold in the legal market) and a higher average THC being grown than the previous year, the Company believes it is well positioned to take advantage of the dried flower and pre-roll categories which collectively represents approximately 70%8 of the Canadian legal market.

Opportunities to scale up new genetics require a patient and deliberate process where cultivation protocols are trialed for each strain and adjusted through multiple growth cycles before full roll-out to multiple rooms in the facility. The Company has successfully launched several new genetics under the Edison brand. Organigram’s commitment to invest in new genetics continues and the Company expects to launch more new high THC genetics in the near term.

In addition to traditional dried flower and pre-roll offerings, Organigram expects to be in a position to generate more revenue growth from the production of soft chews and other confectionary products with the specialized equipment in the Winnipeg Facility under the direction of leadership that brings significant expertise in confectionary manufacturing. The Company completed its first sales of Winnipeg Facility manufactured soft chews during Q4 Fiscal 2021, and with several line extensions planned for Fiscal 2022, management expects meaningful growth in this product category.

Laurentian was acquired in December 2021 and adds hash and artisanal craft cannabis to the Company's offering. The application of the Company's direct sales force and national distribution, along with the increased capacity from the completion of Laurentian's expansion program, is expected to generate additional revenue in Fiscal 2022.

Unabsorbed overhead costs were $nil in Q2 Fiscal 2022, a reduction from $709 in Q1 Fiscal 2022, and a significant reduction from the $2,274 in Q2 Fiscal 2021 the prior year's comparison period. The prior periods had significant unabsorbed fixed overhead costs as a consequence of the unused or idled grow rooms. With the Company's cultivation operating at capacity

7 BDSA Canada Market Forecast, January 7, 2022

8 Source: Hifyre data extract from March 25, 2022

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 13

there was no current period charge for idled or unused rooms and for the six months ended February 28, 2022, $709 of cost related to underutilization of certain derivative products manufacturing equipment. This Company does not expect to incur further expenses for unabsorbed overheads for the rest of Fiscal 2022.

The Company expects to begin to see a sequential improvement in adjusted gross margins in Q3 Fiscal 2022 largely due to lower cultivation costs from higher plant yields, and realize the benefit of several ongoing cost efficiency improvements including increased automation such as the second pre-roll machine which reduces the reliance on manual labour. The extra capacity from the phase 4c expansion, and lower production costs from operating at a larger scale are expected to start occurring during Q4 Fiscal 2022.

The overall level of Q3 Fiscal 2022 adjusted gross margins versus Q3 Fiscal 2021 adjusted gross margins will also be dependent on other factors including, but not limited to, product category and brand sales mix.

Organigram has identified the following opportunities which it believes have the potential to further improve adjusted gross margins over time:

•Economies of scale and efficiencies gained as it continues to scale up cultivation, including the grow rooms that will be available after completing the construction of Phase 4C of the Moncton Campus;

•The Company has planned for additional changes to its cultivation and harvesting methodologies and design improvements that should enhance the operating conditions of the Moncton Campus and result in higher quality flower and improved yields (which reduces production costs). See “Balance Sheet, Liquidity and Capital Resources” section of this MD&A for more detail;

•International sales have historically attracted higher margins and are expected to represent a greater proportion of the Company’s revenue. (see “International” section below);

•More sales in the vape category, that generally attract higher margins;

•Continued investment in automation is expected to drive cost efficiencies and reduce dependence on manual labour;

•The recent launches of new products such as SHRED X Kief-Infused Blends and SHRED X vapes represent new potential avenues of growth with expected attractive long-term margin profiles for the Company;

•The launch of additional products across different derivative categories;

•The margin contribution from the addition of the Laurentian portfolio of products; and

•The margin improvement to chocolates from the relocation of the production from the Moncton Campus to the Winnipeg Facility.

In Fiscal 2022, research and development activities have been shown separately from general and administrative expenses in the Interim Financial Statements, but are still be grouped with operating expenses.

Outside of Canada, the Company serves international markets (including Israel and Australia) from Canada via export permits and is looking to augment sales channels internationally over time. In early Q1 Fiscal 2021, the Israeli Ministry of Health amended its quality standards for imported medical cannabis. In June 2021, the Company received its Good Agricultural Practice certification from Control Union Certifications under the Control Union Medical Cannabis Standard (“CUMCS”) in order to permit it to continue its shipments to Israel under the amended Israeli quality standards. The Company has sought an updated certification for IMC-GMP by CUMCS to demonstrate it continues to meet the evolving Israeli quality standards. Shipments to Canndoc Ltd., resumed during Q1 Fiscal 2022 and Q2 Fiscal 2022 with expectations to continue in Fiscal 2022 subject to regulatory conditions. Future shipments are contingent upon the timing and receipt of regulatory approval from Health Canada, including obtaining an export permit, as well as timing and receipt of regulatory approval from the Israeli regulatory authority, including obtaining an import permit. Recent political changes and cannabis election ballot initiatives for both medical and recreational use in the United States suggest that the potential movements to U.S. federal legalization of cannabis (THC) have increased momentum but the timing and outcome remains difficult to predict. As the Company continues to monitor and develop a potential U.S. THC strategy, it continues to evaluate CBD entry opportunities in the United States.

With the significant capital injection from BAT and the PDC Agreement, the Company is well positioned to expand into the U.S. and further international markets at the appropriate time and subject to applicable laws. Under the PDC Agreement, the Company is granted a worldwide, royalty-free, sub-licensable, perpetual license to exploit IP developed under the PDC Agreement in any field. This license, which is non-exclusive outside of Canada and sole in Canada will also enhance Organigram’s ability to enter markets outside of Canada, including through sublicensing arrangements with established operators.

Without limiting the generality of risk factor disclosures referenced in the “Risk Factors” section of this MD&A, the expectations concerning revenue, adjusted gross margins and SG&A are based on the following general assumptions: consistency of revenue experience with indications of third quarter 2022 performance to date, consistency of ordering and return patterns or other factors with prior periods and no material change in legal regulation, market factors or general economic conditions.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE AND SIX MONTHS ENDED FEBRUARY 28, 2022 AND 2021 14

The Company disclaims any obligation to update any of the forward looking information except as required by applicable law. See cautionary statement in the “Introduction” section at the beginning of this MD&A.

MEDICAL MARKET

BDSA estimates the Canadian medical market value for calendar 2022 at $407M, an 18% year-over-year decline9. Also, the number of medical patients are projected to further decrease within the year. With this projected decline, largely due to migration to the recreational channel, Organigram has shifted its medical strategy and will focus on the important veteran community all while continuing to serve its civilian patient base with superior patient care and an ongoing portfolio optimization. The main change to the Company's strategy is the termination of its existing agreements with the majority of cannabis clinics aimed at patient acquisition.

STRATEGIC INVESTMENTS AND DEVELOPMENTS

The Company remains committed to the development and acquisition of cannabis or hemp related businesses and production assets in Canada and abroad (subject to compliance with applicable laws), intellectual properties, technologies or other assets that are synergistic to the Company’s Canadian and international strategies.

Hyasynth Strategic Investment

On September 12, 2018, the Company entered into a strategic investment to purchase an aggregate of $10,000 convertible secured debentures (the “Hyasynth Debentures”) of Hyasynth, a biotechnology company based in Montreal and pioneer in the field of cannabinoid science and biosynthesis, in three separate tranches. Organigram purchased $5,000 in secured convertible 8% Hyasynth Debentures on September 12, 2018 and advanced an additional $2,500 on October 23, 2020, as a result of Hyasynth’s achievement of the contractual production-related milestone for the second tranche (“Tranche 2”). On December 22, 2021, following the waiver of the remaining milestone, the Company acquired an additional $2,500 of Hyasynth Debentures. Additionally, the parties have amended certain terms of the Debenture Purchase Agreement governing the Debentures’ purchased by Organigram from Hyasynth in previous tranches. The Company has instituted a series of detailed milestones for Hyasynth to achieve by specified target dates. The failure to achieve any such milestone constitutes an Event of Default under the Debentures. In addition, the Company has a veto right over future financings conducted by Hyasynth. This brings the Company’s total face value of convertible debentures investment in Hyasynth to $10,000, which provides the Company with a potential ownership interest of up to 48.9% on a fully diluted basis. The Company has appointed two nominee directors to the board of Hyasynth, which currently has seven members.

Hyasynth has patent-pending enzymes, yeast strains and processes that make it possible to produce phytocannabinoids and phytocannabinoid analogues in genetically modified strains of yeast. These proprietary enzymes and yeast strains have allowed Hyasynth to produce CBG, CBD and THC for novel and specialized products such as vaporizable cannabis products and cannabis infused beverages for a fraction of the cost of traditional plant-based production. The Company anticipates that its investment in Hyasynth has the potential to provide the Company with access to what it expects to be the future of cannabinoid production. The Company expects that cost-effectiveness and scalability will be necessary to meet the needs of both the Canadian and global cannabis markets.