INTRODUCTION

This Management’s Discussion and Analysis dated January 11, 2023 (this “MD&A”), should be read in conjunction with the unaudited condensed consolidated interim financial statements (the “Interim Financial Statements”) of Organigram Holdings Inc. (the “Company” or “Organigram”) for the three months ended November 30, 2022 (“Q1 Fiscal 2023”) and the audited annual consolidated financial statements for the year ended August 31, 2022 (the "Annual Financial Statements"), including the accompanying notes thereto.

Financial information in this MD&A is based on the Interim Financial Statements of the Company for the three months ended November 30, 2022, and has been prepared in accordance with International Accounting Standard 34 Interim Financial Reporting as issued by the International Accounting Standards Board (“IASB”), unless otherwise stated. All financial information in this MD&A is expressed in thousands of Canadian dollars (“$”), except for share and per share calculations, references to $ millions and $ billions, per gram (“g”) or kilogram (“kg”) of dried flower and per milliliter (“mL”) or liter (“L”) of cannabis extracts calculations.

This MD&A contains forward-looking information within the meaning of applicable securities laws. Refer to “Cautionary Statement Regarding Forward-Looking Information” included within this MD&A.

The financial information in this MD&A also contains certain financial and operational performance measures that are not defined by and do not have any standardized meaning under IFRS but are used by management to assess the financial and operational performance of the Company. These include, but not limited to, the following:

•Yield per plant (in grams);

•Average net selling price per gram and per unit;

•Target production capacity;

•Gross margin before fair value adjustments;

•Adjusted gross margin; and

•Adjusted earnings before interest, taxes, depreciation and amortization ("Adjusted EBITDA").

The Company believes that these non-IFRS financial measures and operational performance measures, in addition to conventional measures prepared in accordance with IFRS, enable investors to evaluate the Company’s operating results, underlying performance and prospects in a similar manner to the Company’s management. The non-IFRS financial performance measures are defined in the sections in which they appear. Adjusted gross margin and Adjusted EBITDA are reconciled to IFRS in the “Financial Review and Discussion of Operations” section of this MD&A.

As there are no standardized methods of calculating these non-IFRS measures, the Company’s approaches may differ from those used by others, and the use of these measures may not be directly comparable. Accordingly, these non-IFRS measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Refer to "Cautionary Statement Regarding Certain Non-IFRS Measures" included within this MD&A.

The Company’s wholly-owned subsidiary, Organigram Inc., is a licensed producer of cannabis and cannabis derived products (a “Licensed Producer” or “LP”) under the Cannabis Act (Canada) and the Cannabis Regulations (Canada) (together, the “Cannabis Act”) and regulated by Health Canada. The Company’s wholly-owned subsidiaries, The Edibles and Infusions Corporation (“EIC”) and Laurentian Organic Inc. ("Laurentian") are also licensed under the Cannabis Act.

The Company’s head office is located at 1250-333 Bay Street, Toronto, Ontario, M5H 2R2. The Company's registered office is located at 35 English Drive, Moncton, New Brunswick, E1E 3X3. The Company’s common shares (“Common Shares”) are listed under the ticker symbol “OGI” on both the Nasdaq Global Select Market (“NASDAQ”) and on the Toronto Stock Exchange (“TSX”). Any inquiries regarding the Company may be directed by email to investors@organigram.ca.

Additional information relating to the Company, including the Company’s most recent annual information form (the “AIF”), is available under the Company’s issuer profile on the Canadian Securities Administrators’ System for Electronic Document Analysis and Retrieval (“SEDAR”) at www.sedar.com. The Company’s reports and other information filed with or furnished to the United States Securities and Exchange Commission (“SEC”) are available on the SEC’s Electronic Document Gathering and Retrieval System (“EDGAR”) at www.sec.gov.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 1

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

Certain information herein contains or incorporates comments that constitute forward-looking information within the meaning of applicable securities legislation (“forward-looking information”). Forward-looking information, in general, can be identified by the use of forward-looking terminology such as “outlook”, “objective”, “may”, “will”, “could”, “would”, “might”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “plan”, “continue”, “budget”, “schedule” or “forecast” or similar expressions suggesting future outcomes or events. They include, but are not limited to, statements with respect to expectations, forecasts or other characterizations of future events or circumstances, and the Company’s objectives, goals, strategies, beliefs, intentions, plans, estimates, projections and outlook, including statements relating to the Company’s plans and objectives, or estimates or predictions of actions of customers, suppliers, partners, distributors, competitors or regulatory authorities; and statements regarding the Company’s future economic performance. These statements are not historical facts but instead represent management beliefs regarding future events, many of which by their nature are inherently uncertain and beyond management control. Forward-looking information has been based on the Company’s current expectations about future events.

Certain forward-looking information in this MD&A includes, but is not limited to the following:

•Moncton Campus (as defined herein), Winnipeg Facility (as defined herein) and Lac-Supérieur Facility (as defined herein) licensing and target production capacity and timing thereof;

•Expectations regarding production capacity, facility size, THC (as defined herein) content, costs and yields;

•Expectations regarding the prospects of the Company’s collaboration with a wholly-owned subsidiary of British American Tobacco p.l.c. ("BAT");

•Expectations regarding the prospects for the Company’s subsidiaries EIC and Laurentian;

•The ongoing impact of the current global health crisis caused by COVID-19 (as defined below);

•Expectations around demand for cannabis and related products, future opportunities and sales, including the relative mix of medical versus adult-use recreational cannabis products, the relative mix of products within the adult-use recreational category including wholesale, the Company’s financial position, future liquidity and other financial results;

•Legislation of additional cannabis types and forms for adult-use recreational cannabis in Canada including regulations relating thereto, the timing and the implementation thereof and our future product forms;

•Expectations around branded products and derivative-based products with respect to timing, launch, product attributes, composition and consumer demand;

•Strategic investments and capital expenditures, and expected related benefits;

•Expectations regarding the resolution of litigation and other legal proceedings;

•The general continuance of current, or where applicable, assumed industry conditions;

•Changes in laws, regulations and guidelines, including those relating to the recreational and/or medical cannabis markets domestically and internationally;

•The price of cannabis and derivative cannabis products;

•Expectations around the availability and introduction of new genetics including consistency and quality of plants and the characteristics thereof;

•The impact of the Company’s cash flow and financial performance on third parties, including its supply partners;

•Fluctuations in the price of Common Shares and the market for Common Shares;

•The treatment of the Company’s business under governmental regulatory regimes and tax laws, including the Excise Act (as defined herein) and the renewal of the Company’s licenses thereunder and the Company’s ability to obtain export licenses from time to time;

•The Company’s growth strategy, targets for future growth and forecasts of the results of such growth;

•Expectations concerning access to capital and liquidity and the Company’s ability to access the public markets to fund operational activities and growth;

•The Company’s ability to remain listed on the TSX and NASDAQ and the impact of any actions it may be required to take to remain listed;

•The ability of the Company to generate cash flow from operations and from financing activities;

•The competitive conditions of the industry, including the Company’s ability to maintain or grow its market share;

•Lac-Supérieur Facility expansion plans, capital expenditures, current and targeted production capacity and timing thereof; and

•Expectations concerning Fiscal 2023 performance including with respect to revenue, adjusted gross margin, selling, general and administrative expenses ("SG&A") and Adjusted EBITDA.

Forward-looking information is provided for the purposes of assisting the reader in understanding the Company and its business, operations, risks, financial performance, financial position and cash flows as at and for the periods ended on certain dates, and to present information about management’s current expectations and plans relating to the future, and the reader is cautioned that such statements may not be appropriate for other purposes. In addition, this MD&A may contain forward-looking information attributed to third party industry sources. Undue reliance should not be placed on forward-looking

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 2

information, as there can be no assurance that the plans, intentions or expectations upon which they are based will occur. Forward-looking information does not guarantee future performance and involves known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in the forward-looking information. By its nature, forward-looking information involves numerous assumptions, known and unknown risks and uncertainties, both general and specific, that contribute to the possibility that the expectations, predictions, forecasts, projections and conclusions will not occur or prove accurate, that assumptions may not be correct, and that objectives, strategic goals and priorities will not be achieved. These and other factors that may cause actual results or events to differ materially from those anticipated in the forward-looking information.

This MD&A contains information concerning our industry and the markets in which we operate, including our market position and market share, which is based on information from independent third-party sources. Although we believe these sources to be generally reliable, market and industry data is inherently imprecise, subject to interpretation and cannot be verified with complete certainty due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process, and other limitations and uncertainties inherent in any statistical survey or data collection process. We have not independently verified any third-party information contained herein.

Factors that could cause actual results to differ materially from those set forth in forward-looking information include, but are not limited to: financial risks; dependence on senior management and other key personnel, the board of directors of the Company (the “Board of Directors”), consultants and advisors; availability and sufficiency of insurance including continued availability and sufficiency of director and officer and other forms of insurance; the Company and its subsidiaries being able to, where applicable, cultivate cannabis pursuant to applicable law and on the currently anticipated timelines and in anticipated volumes; industry competition; general economic conditions and global events, including heightened economic and industry uncertainty as a result of COVID-19 and governmental action in respect thereto, including with respect to impacts on production, operations, disclosure controls and procedures or internal control over financial reporting, supply chain and distribution disruptions; facility and technological risks; changes to government laws, regulations or policy, including environmental or tax, or the enforcement thereof; agricultural risks; ability to maintain any required licenses or certifications; supply risks; product risks; construction delays or postponements; packaging and shipping logistics; inflationary risk, expected number of medical and adult-use recreational cannabis users in Canada and internationally; potential time frame for the implementation of legislation to legalize cannabis internationally; the Company’s, its subsidiaries' and its investees’ ability to, where applicable, obtain and/or maintain their status as Licensed Producers (as defined herein) or other applicable licenses; risk factors affecting its investees; availability of any required financing on commercially attractive terms or at all; the potential size of the regulated adult-use recreational cannabis market in Canada; demand for and changes in the Company’s cannabis and related products, including the Company’s derivative products (as defined herein), and the sufficiency of the retail networks to supply such demand; ability to enter and participate in international market opportunities; general economic, financial market, regulatory, industry and political conditions affecting the Company; the ability of the Company to compete in the cannabis industry and changes in the competitive landscape; a material decline in cannabis prices; the Company’s ability to manage anticipated and unanticipated costs; the Company’s ability to implement and maintain effective internal control over financial reporting and disclosure controls and procedures; the timing for the implementation of the Company's ERP system (as hereinafter defined) and, other risks and factors described from time to time in the documents filed by the Company with securities regulators in Canada and the United States. Material factors and assumptions used in establishing forward-looking information include that construction and production activities will proceed as planned, and demand for cannabis and related products will change in the manner expected by management. All forward-looking information is provided as of the date of this MD&A.

The Company does not undertake to update any such forward-looking information whether as a result of new information, future events or otherwise, except as required by law.

ADDITIONAL INFORMATION ABOUT THE ASSUMPTIONS, RISKS AND UNCERTAINTIES OF THE COMPANY’S BUSINESS AND MATERIAL FACTORS OR ASSUMPTIONS ON WHICH INFORMATION CONTAINED IN FORWARD-LOOKING INFORMATION IS BASED IS PROVIDED IN THE COMPANY’S DISCLOSURE MATERIALS, INCLUDING IN THIS MD&A UNDER “RISK FACTORS” AND THE COMPANY’S CURRENT AIF UNDER “RISK FACTORS”, FILED WITH THE SECURITIES REGULATORY AUTHORITIES IN CANADA AND AVAILABLE UNDER THE COMPANY’S ISSUER PROFILE ON SEDAR AT WWW.SEDAR.COM, AND FILED WITH OR FURNISHED TO THE SEC AND AVAILABLE ON EDGAR AT WWW.SEC.GOV. ALL FORWARD-LOOKING INFORMATION IN THIS MD&A IS QUALIFIED BY THESE CAUTIONARY STATEMENTS.

CAUTIONARY STATEMENT REGARDING CERTAIN NON-IFRS MEASURES

This MD&A contains certain financial and operational performance measures that are not recognized or defined under IFRS (“Non-IFRS Measures”). As there are no standardized methods of calculating these Non-IFRS Measures, the Company's approaches may differ from those used by others, and, this data may not be comparable to similar data presented by other

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 3

Licensed Producers of cannabis and cannabis companies. For an explanation of these measures to related comparable financial information presented in the Financial Statements prepared in accordance with IFRS, refer to the discussion below.

The Company believes that these Non-IFRS Measures are useful indicators of operating performance and are specifically used by management to assess the financial and operating performance of the Company. These Non-IFRS Measures include, but are not limited, to the following:

•Yield per plant in grams is calculated by taking the total amount of grams of dried flower harvested, excluding trim, and dividing it by the total number of plants harvested.

Management believes that yield per plant in grams provides a useful measure about the efficiencies gained through its operating activities.

•Average net selling price per gram and per unit are calculated by taking net revenue, which is then divided by total grams or total units sold in the period.

Management believes the average net selling price per gram or per unit measures provide more specific information about the pricing trends over time by product type.

•Gross margin before fair value adjustments is calculated by subtracting cost of sales, before the effects of unrealized gain on changes in fair value of biological assets, realized fair value on inventories sold and other inventory charges from total net revenue. Gross margin before fair value adjustments percentage is calculated by dividing gross margin before fair value adjustments (defined above) divided by net revenue.

Management believes that these measures provide useful information to assess the profitability of our cannabis operations as it excludes the effects of non-cash fair value adjustments on inventory and biological assets, which are required by IFRS.

•Adjusted gross margin is calculated by subtracting cost of sales, before the effects of: (i) unrealized gain on changes in fair value of biological assets; (ii) realized fair value on inventories sold and other inventory charges; (iii) provisions (recoveries) and impairment of inventories and biological assets; (iv) provisions to net realizable value; (v) COVID-19 related charges; and (vi) unabsorbed overhead relating to underutilization of the production facility grow rooms and manufacturing equipment, most of which is related to non-cash depreciation expense, from net revenue. Adjusted gross margin percentage is calculated by dividing adjusted gross margin by net revenue. Adjusted gross margin is reconciled to IFRS in the "Financial Review and Discussion of Operations" section of this MD&A.

Management believes that these measures provide useful information to assess the profitability of our operations as they represent the normalized gross margin generated from operations and exclude the effects of non-cash fair value adjustments on inventories and biological assets, which are required by IFRS. The most directly comparable measure to adjusted gross margin calculated in accordance with IFRS is gross margin before fair value.

•Adjusted EBITDA is calculated as net income (loss) excluding: financing costs, net of investment income; income tax expense (recovery); depreciation, amortization, reversal of/or impairment, (gain) loss on disposal of property, plant and equipment (per the consolidated statement of cash flows); share-based compensation (per the consolidated statement of cash flows); share of loss from investments in associates and impairment loss from loan receivable; unrealized loss (gain) on changes in fair value of contingent consideration; change in fair value of derivative liabilities; expenditures incurred in connection with research and development activities (net of depreciation); unrealized (gain) loss on changes in fair value of biological assets; realized fair value on inventories sold and other inventory charges; provisions and impairment of inventories and biological assets; provisions to net realizable value of inventories; COVID-19 related charges, net of government subsidies and insurance recoveries; legal provisions (recoveries); incremental fair value component of inventories sold from acquisitions; ERP implementation costs; transaction costs; and share issuance costs. Adjusted EBITDA is reconciled to IFRS in the "Financial Review and Discussion of Operations" section of this MD&A.

Adjusted EBITDA is intended to provide a proxy for the Company’s operating cash flow and derives expectations of future financial performance for the Company, and excludes adjustments that are not reflective of current operating results. The most directly comparable measure to Adjusted EBITDA calculated in accordance with IFRS is net income (loss).

Non-IFRS Measures should be considered together with other data prepared in accordance with IFRS to enable investors to evaluate the Company’s operating results, underlying performance and prospects in a manner similar to the Company’s

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 4

management. Accordingly, these non-IFRS measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

BUSINESS OVERVIEW

NATURE AND HISTORY OF THE COMPANY’S BUSINESS

The Company’s wholly-owned subsidiary Organigram Inc. is a Licensed Producer of cannabis under the Cannabis Act.

The Company is authorized for wholesale shipping of cannabis plant cuttings, dried flower, blends, pre-rolls and cannabis derivative-based products to approved retailers and wholesalers for adult-use recreational cannabis under the individual provincial and territorial regulations as per the Cannabis Act.

The Company is also authorized to distribute cannabis for medical use. In Fiscal 2022, Organigram made a strategic decision to shift its medical distribution fulfillment approach from direct shipment to patients from the Company to fulfillment via Medical Cannabis by Shoppers Drug Mart. The Company continues to be committed to medical patients via its Shoppers Drug Mart relationship and will also continue to bring new innovations to this channel. In Q1 of Fiscal 2023, the company introduced 26 new SKUs to Medical Cannabis by Shoppers Drug Mart.

The Company conducts its operations at its facilities located in Moncton, New B

runswick, Winnipeg, Manitoba and Lac-Supérieur, Quebec. The Company has expanded its main facility in Moncton over time to create additional production capabilities by strategically acquiring land and buildings adjacent to the main facility (together, the “Moncton Campus”), including to add capacity for the manufacture of derivative product forms. In Fiscal 2022, the Phase 4C expansion at Moncton was completed which increased the grow rooms available for flowering to 115 and the approximate annual capacity to 85,000 kg of flower. The total capacity of the Moncton Campus will continue to fluctuate as the Company further refines its growing methods and room utilization.

In March 2021, the Company formed a Product Development Collaboration ("PDC") with BAT, a leading, multi-category consumer goods business, and established a "Centre of Excellence" (the "CoE") to focus on the next generation of cannabis products with an initial focus on cannabidiol ("CBD"). The CoE is established at the Company's Moncton Campus, which holds the Health Canada licenses required to conduct research and development activities with cannabis products. Both companies contributed scientists, researchers, and product developers to the CoE which is governed and supervised by a steering committee consisting of an equal number of senior members from both companies. Under the terms of the PDC Agreement (as defined herein), both Organigram and BAT have access to certain of each other’s intellectual property (“IP”) and, subject to certain limitations, have the right to independently, globally commercialize the products, technologies and IP created by the CoE pursuant to the PDC Agreement.

During April 2021, the Company expanded its manufacturing and production footprint with the acquisition of Edibles and Infusion Corporation ("EIC"), located in Winnipeg, Manitoba (the "Winnipeg Facility"). The Winnipeg Facility holds a research license and standard sale and processing license under the Cannabis Act. As a wholly-owned subsidiary, EIC has enabled the Company to penetrate a new product category and gain access to its expertise in the confectionary space. The Winnipeg Facility also provides the Company with a share of the cannabis infused gummies market and other derivative products.

The Company has additional cannabis production capacity at its wholly-owned subsidiary, Laurentian, located in Lac-Supérieur, Quebec, acquired on December 21, 2021 (the "Lac-Supérieur Facility"). The Lac-Supérieur Facility has a cultivation focus on artisanal craft flower and on the production of hash, a cannabis derivative. The Lac-Supérieur Facility provides the Company with a foothold in the important Quebec market, and also adds to the Company's premium product portfolio, providing further opportunities for margin expansion. The facility holds a standard processing and cultivation license under the Cannabis Act.

STRATEGY

Organigram’s strategy is to leverage its broad brand and product portfolio and culture of innovation to increase market share, drive profitability and grow into an industry leader that delivers long-term shareholder value.

The pillars of the Company’s strategy are:

1.Innovation;

2.Consumer Focus;

3.Efficiency; and

4.Market Expansion.

1. Innovation

Meeting the demands of a fast-growing industry with changing consumer preferences requires the ability to innovate and create breakthrough products that are embraced by the market and establish a long-term competitive advantage.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 5

The Company is committed to maintaining a culture of innovation and has established a track record of introducing differentiated products that are able to quickly capture market share, specifically:

•SHRED: the first milled flower product blended to create curated flavour profiles;

•Edison JOLTS: Canada’s first flavoured high-potency lozenge with 100 mg of tetrahydrocannabinol ("THC") per package; and

•Monjour Wellness gummies: The CBD-focused wellness brand available in a large format and providing multiple flavours in one package.

Consistent with its innovation culture, in Fiscal 2021, the Company announced the launch of its CoE as part of its PDC with BAT, a leading multi-category consumer goods business. The CoE focuses on research and development to develop the next generation of cannabis products, with an initial focus on CBD.

2. Consumer Focus

The Company seeks to address the changing needs of the adult cannabis consumer through its broad product portfolio with offerings in the most popular categories and price points. Based on ongoing consumer research, the portfolio is refreshed frequently with different flower strains, new package formats and new product introductions. The Company’s alignment with consumers is evidenced by its #3 market position and category leadership:

•SHRED products have been introduced in multiple categories with the brand surpassing $150 million in retail sales and achieving a net promoter score of 77 percent1;

•HOLY MOUNTAIN: a new offering in the value sector consisting of unique flower strains and pressed hash;

•Edison JOLTS: #1 position for capsules2; and

•SHRED’ems gummies and Monjour soft chews: among the top-selling gummies in Canada which combined held the #3 market position in the gummy category2 with Monjour being the best-selling CBD only gummy.

In addition to third-party and direct consumer research, the Company maintains close contact with consumers through an active social presence and has established the Cannabis Innovators Panel. This online panel engages with up to 2,500 cannabis consumers across Canada on a regular basis and helps to inform the Company on product development and brand initiatives.

3. Efficiency

From its inception, the Company has remained committed to being an efficient operator.

The Company’s growing facility in Moncton, New Brunswick utilizes three-tier cultivation technology to maximize square footage. The facility has proprietary information technology in place to track all aspects of the cannabis cultivation and harvest process. The Company maintains a continuous improvement program to maximize harvest yield while reducing operating costs. This is complemented by the introduction of automation in post-harvest production, including high-speed pouch packing, pre-roll machines and automated excise stamping.

The Winnipeg Facility is highly-automated and is able to efficiently handle both small-batch artisanal manufacture of edibles as well as large-scale nutraceutical-grade production. The facility provides the Company with the ability to produce a wide range of high-quality edible products at attractive price points.

The Lac-Supérieur Facility houses a cultivation and derivatives processing facility. The Company has committed $13 million in growth capital expenditures based on current expectations for the cost of expanding the facility to increase capacity, processing and storage space and deliver on automation.

4. Market Expansion

The Company is committed to expanding its market presence by adding to its product offering and enhancing its geographical presence. This strategy is enabled by strategic merger and acquisition opportunities and assessing expansion into international markets.

Examples of market expansion include:

•The strategic acquisitions of EIC which added a purpose-built, highly-automated, 51,000-square-foot cannabis edibles manufacturing facility, and Laurentian, whose Lac-Supérieur Facility added craft cultivation and hash to Organigram's product portfolio and increased our presence in Quebec;

•Shipments to Canndoc Ltd. ("Canndoc") in Israel and Cannatrek Medical Pty Ltd. ("Cannatrek") and MedCan Australia Pty Ltd. ("MedCan") in Australia to supply bulk cannabis into these markets.

1 Brightfield Group

2 Hifyre data extract from December 21, 2022

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 6

KEY DEVELOPMENTS DURING THE QUARTER AND SUBSEQUENT TO NOVEMBER 30, 2022

In November 2022, the Company announced HOLY MOUNTAIN, the Company’s newest value "brand", featuring an initial lineup of legendary dried flower strains entering the market with value pressed hash. With the introduction of HOLY MOUNTAIN, Organigram now offers value-priced flower in an expanded range of sizes, starting with 3.5 gram offerings at launch.

In November 2022, the Company introduced Monjour Twilight Tranquility, sugar-free soft chews in pear, plum and lavender flavours. Each soft chew contains the cannabinoids CBD, CBN and CBG. Sold in packs of 25.

In November 2022, the Company announced that it has entered into a new multi-year agreement to supply dried flower to Canndoc, a subsidiary of InterCure Ltd. ("InterCure"), Israel's largest and most established pharmaceutical cannabis producer. The agreement provides for a commitment to supply 10,000 kg of dried flower with an option for InterCure to elect to purchase up to an additional 10,000 kg of dried flower for InterCure's international supply chain.

In November 2022, the Company introduced a number of pre-rolls infused with hash. Two examples are Edison Grape Crescendo, infused with bubble hash, and Tremblant Sweet Cherry, infused with hash.

In December 2022, the Company was awarded "Cannabis Company of the Year" by KIND Magazine.

OPERATIONS AND PRODUCTION

Moncton Cultivation Campus

At the Moncton Campus, the Company continues to make progress on its ongoing improvement program. This includes implementation of various new initiatives which have resulted in an increase in an average THC content per plant and the average yield per plant. The Phase 4C expansion at Moncton was completed in Fiscal 2022 which increased the approximate annual capacity to 85,000 kg of flower. The Company has also identified additional changes to its growing and harvesting methodologies, that should assist the operating conditions of the Moncton Campus resulting in higher quality flower and a reduction in production costs. The total capacity of the Moncton Campus will continue to fluctuate as the Company further refines its growing methods and room utilization.

The Company harvested 22,138 kg of dried flower during Q1 Fiscal 2023 compared to 11,603 kg of dried flower in Q1 Fiscal 2022. The increase of 10,693 kg (92%) from the comparative period was primarily related to increased cultivation planting, staffing and environmental upgrades along with additional rooms being available that occurred over the period from Q1 Fiscal 2022 to Q1 Fiscal 2023, that was done in order to meet the increased demand for many of the Company's products.

Moncton Derivatives Facility

Contained in the 56,000 square foot expansion referred to as Phase 5 of the Moncton Campus is the Company's derivatives facility. Phase 5 includes Supercritical CO2, dry sift and cold water extraction laboratories, as well as in-house formulation and finishing of ingestibles, extracts, vape oils and concentrates, in addition to high speed cart filling, bottling and automated packaging. Some of this equipment remains in the commissioning and research and development phase.

Winnipeg Facility

The Company has a purpose-built, highly-automated, 51,000 square-foot manufacturing facility in Winnipeg, Manitoba which was also designed with reference to EU GMP (European Union good manufacturing practice) standards. The Company has no plans to seek certification in the immediate future but continues to evaluate paths to certification. The facility design and the equipment specifications were also designed to handle both smaller-batch artisanal manufacturing as well as large-scale nutraceutical-grade high-efficiency manufacturing and to produce highly customizable, precise, and scalable cannabis-infused products in various formats and dosages including pectin, gelatin, sugar-free soft chews (gummies) and lozenges with novel capabilities such as infusions, striping and the possibility of using fruit purees. Automation and efficiency investments in the facility has resulted in an increase in production. In September, 2021, the facility shipped 339,000 gummies, which increased to 2.8 million gummies in November, 2022.

The Winnipeg Facility currently holds a research license and a standard sale and processing license issued under the Cannabis Act. The Company commenced commercial operations during Fiscal 2021 and as of the date of this MD&A, the Winnipeg Facility has over 90 employees.

Lac-Supérieur Concentrates and Craft Flower Facility

The Company acquired the Lac-Supérieur Facility in December 2021. The Lac-Supérieur Facility has 6,800 square feet of cultivation area, which is currently being expanded to 33,000 square feet. The Lac-Supérieur Facility is currently equipped to

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 7

produce approximately 600 kilograms of flower and 1 million packaged units of hash annually. The expansion program currently underway is expected to increase annual capacity to 2,400 kilograms of flower and 2 million packaged units of hash once completed. The Company has committed $13 million towards completing the expansion and management believes that there may be future opportunities for cost savings from further investments in automation and increased capacity from adding staff to the packaging shifts.

CANADIAN ADULT-USE RECREATIONAL CANNABIS MARKET

Organigram continues to increase its focus on generating meaningful consumer insights and applying these insights to the ongoing optimization of its brand and product portfolio with a goal of ensuring that they are geared towards meeting consumer preferences. The Company aggressively and successfully revitalized its product portfolio to meet rapidly evolving consumer preferences and through its increased focus on insights, has continued its expansion of brands and products aimed at driving continued momentum in the marketplace.

DRIED FLOWER AND PRE-ROLLS

Dried flower and pre-rolls remain the first and second largest product categories, respectively, in the Canadian adult-use recreational cannabis market2 and the Company believes that these categories will continue to dominate based on the sales history in mature legal markets in certain U.S. states as well as regulatory restrictions on other form factors (e.g. the 10 mg per package THC limit in the edibles category). While the Company expects consumer preferences will slowly evolve away from THC and price being the key purchase drivers, today they appear to be the most important attributes to consumers for flower products. Over time, genetic diversity and other quality related attributes such as terpene profile, bud density, and aroma, are expected to become increasingly important. While the Company’s efforts are focused on delivering on consumer expectations today, it is concurrently planning for the eventual evolution towards a more nuanced approach to cannabis appreciation through its ongoing work in genetic breeding and pheno-hunting with the goal of offering a unique and relevant assortment to consumers. Additionally, the strategic acquisition of Laurentian in December 2021 allows the Company the opportunity to participate in the growing craft cannabis segment, through its craft facility located in the province of Quebec.

The Company's portfolio of brands continues to show strong momentum within the flower segment in Canada and as of November 2022 maintains a #2 share in the flower category2. The growth and significant contribution of these dried flower value segment brands, however, has contributed to overall margin pressure for Organigram and many of its peers over the last number of quarters. To counteract this phenomenon, Organigram is dedicated to revitalizing its Edison brand and product portfolio, by launching new dried flower offerings with unique genetics and higher potency THC. The completion of these initiatives is expected to increase Edison sales, that have a higher average sales price ("ASP") than value brands and therefore attract higher margins. To address the growing demand for strain differentiation in the value segment, the Company expanded the strains available in its Big Bag O' Buds line and also introduced HOLY MOUNTAIN, a value-sector brand offering hash and dry flower strains in the 3.5 gram format.

CANNABIS DERIVATIVES

While dried flower and pre-rolls are currently the largest categories in Canada, derivative cannabis products, including vapes, concentrates and edibles, are projected to continue to increase in market share over the next several years at the expense of flower.

Organigram is committed to these growing categories. The strategic acquisition of the Winnipeg Facility enabled the Company to produce high quality, edible products such as soft chews (gummies) and lozenges, at scale, positioning the Company to effectively compete in this segment. The acquisition of the Lac-Supérieur Facility provided the Company with the ability to produce high-quality products in the growing hash segment. Since the acquisition, the Company has leveraged its industry-leading national distribution and field sales network to accelerate the distribution and sale of Tremblant Cannabis, its flagship hash brand, to all provinces in Canada.

Overall, Organigram holds the number #3 position in the gummy category2.

SHRED'ems, the Company's cannabis-infused gummies, an extension of the popular, value-priced SHRED brand, were introduced in Q4 Fiscal 2021 and quickly gained momentum within the gummy segment. In Q3 Fiscal 2022, two new sour flavours were added to the product line, as well as SHRED'ems POP! – gummies formulated in three soft drink flavours: Cola, Root Beer and Cream Soda. In Q1 Fiscal 2023, SHRED'ems held the #3 market share position for net sales and #2 position by volume2.

In Q1 of Fiscal 2022, the Company launched Monjour, a CBD-focused wellness brand with four SKUs. The large format and assorted flavours proved to be disruptive to the sector and, as of November 2022, Monjour's Berry Good Day CBD gummy was in the top five of gummies sold in Canada and the leading pure CBD-infused gummy2. The Monjour product line was

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 8

further expanded in May 2022 with the introduction of CBN Bedtime Blueberry Lemon gummies, which combine the cannabinoid cannabinol ("CBN") with CBD and THC.

Edison JOLTS, high potency THC lozenges that were developed using proprietary IP, combine the benefits of sublingual oil with the convenience and portability of soft gels. JOLTS held the #1 position in net sales in the capsules and mints category in Q1 Fiscal 20232.

Organigram continues to focus on building share within the vape category through unique formulations, premium hardware, and high-quality inputs. In Fiscal 2022, the Company launched new vape SKUs under the SHRED X brand in the popular 510 cartridge format and formulated in the flavour profiles of the SHRED milled flower products.

RESEARCH AND PRODUCT DEVELOPMENT

The Company’s management believes the cannabis industry is still in the nascent stages of product development and that product innovation backed by core fundamental research and development is necessary to establish a long-term competitive advantage in the industry. Research and development and innovation remain a hallmark of Organigram. The Company has made several investments in Fiscal 2021 and Fiscal 2022 that we anticipate will continue in Fiscal 2023 and strengthen the Company's focus in this area. These efforts are expected to allow Organigram to continue to position itself to be at the forefront of launching new, innovative, differentiated products and formulations that appeal to adult consumers.

BAT Product Development Collaboration and Centre of Excellence

In early Q4 Fiscal 2021, the Company announced the successful launch of the CoE outlined in the PDC Agreement with BAT which was established to focus on research and product development activities for the next generation of cannabis products, as well as cannabinoid fundamental science, with an initial focus on CBD. The CoE is located at the Moncton Campus, which holds the Health Canada licenses required to conduct research and development activities with cannabis products.

Under the PDC Agreement, both Organigram and BAT have access to certain of each other’s IP and have the right to independently and globally commercialize the products, technologies, and IP created. Costs relating to the CoE are being funded equally by Organigram and BAT. Approximately $31 million of BAT’s investment in Organigram has been reserved for Organigram’s portion of its funding obligations.

The CoE development and scientific process is supporting discovery and development efforts on novel vapour ingredients, substrates and will guide the optimization of the existing traditional extract and distillate ingredients. The supporting scientific data also provides an industry leading vapour data set that will serve as part of a foundation for future development activities, including consumer safety, product quality and performance.The state-of-the-art biological experiment laboratory ("BioLab") has been operational since June 2022 and is conducting work for the CoE. It is hoped that the work being undertaken, including development of genetic toolboxes for research of key cannabis traits, will accelerate R&D activities and has already been used to support several plant science discoveries that will eventually benefit Organigram’s existing own plant portfolio and long term growing strategies.

Plant Science, Breeding and Genomics Research and Development in Moncton

Organigram’s cultivation program; a key strategic advantage for the Company has continued its expansion with the addition of a dedicated cultivation R&D space. The new space has accelerated rapid assessment and screening, delivering 20 to 30 unique cultivars every two months while freeing up rooms for commercial grow operations. The Plant Science team continues to move the garden towards unique, high terpene and high THC, in-house grown cultivars, while also leveraging the newly commissioned BioLab for ongoing plant science innovation focusing on quality, potency and disease-resistance marker discovery to enrich the future flower pipeline.

OUTLOOK

The Company's outlook remains positive on the cannabis market both in Canada and internationally. Canada-wide recreational retail sales are expected to total $5.3 billion in calendar 20263.

The cannabis industry in Canada is highly competitive and has been oversupplied versus the current market demand considering both regulated Licensed Producers and the still largely unfettered operations of the illicit market including many online delivery platforms. Consumer trends and preferences continue to evolve, including strong demand in the large format value segment, a desire for higher THC potency particularly in dried flower, as well as a penchant for newness, including new genetic strains and novel products. Organigram continues to revitalize its product portfolio to address these changing consumer trends and preferences in order to grow sales and capture market share. The Company has also seen supply and

3 BDSA Canada Market Forecast, September 2022

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 9

demand dynamics brought into a more equilibrated state as many LPs have shuttered surplus cultivation capacity including as a direct result of M&A and liquidation activities.

Against this backdrop of strong industry growth, increased demand for the Company's products is evidenced by Organigram's national adult-use recreational cannabis retail market share ("market share") in Canada. In Q1 Fiscal 2023, the Company held at the #3 position in market share with Organigram holding the #1 position in milled flower, #1 in capsules, the #3 position in gummies and the #3 position in hash nationally. Management believes that the Company is better equipped to fulfill demand in Fiscal 2023 with larger harvests, driven by stronger yields and harvests from the Moncton Phase 4C expansion coming online, compared to Fiscal 2022. With a full year of revenues from the Company's Lac-Supérieur Facility, management expects that the Company will generate higher revenue in Fiscal 2023 as compared to Fiscal 2022. In addition to the domestic sales growth, the Company expects higher international revenue under its new multi-year supply agreement with Canndoc in Israel and continued shipments to Medcan and Cannatrek in Australia.

The Company intends to continue to leverage its Moncton Campus which it believes can provide a sustainable competitive advantage over its peers as a result of having over 131 three-tiered cultivation rooms each with the ability to deliver bespoke growing environmental conditions (lighting, humidity, fertigation, plant density) tailored individually to a wide variety of genetics (115 of these rooms are used for the flowering period). With an improved genetics portfolio (including contributions from the dedicated cultivation R&D space at the newly-commissioned BioLab) and a higher average THC being grown than the previous year, the Company believes it is well positioned to take advantage of the dried flower and pre-roll categories which collectively represents approximately 70%2 of the Canadian legal market.

Opportunities to scale up new genetics require a patient and deliberate process where cultivation protocols are trialed for each strain and adjusted through multiple growth cycles before full roll-out to multiple rooms in the facility. The Company has launched several new genetics under the Edison brand. Organigram’s commitment to invest in new genetics continues and the Company expects to launch more new high THC and high terpene genetics in the near term.

In addition to traditional dried flower and pre-roll offerings, Organigram expects to be in a position to generate more revenue growth from the production of soft chews and other confectionary products with the specialized equipment at the Winnipeg Facility. The Company completed its first sales of Winnipeg Facility manufactured soft chews during Q4 Fiscal 2021, and launched several line extensions during Fiscal 2022. In Fiscal 2023, management expects continued meaningful growth in this product category.

The Lac-Supérieur Facility was acquired in December 2021 and adds hash and artisanal craft cannabis to the Company's product offerings. The application of the Company's direct sales force and national distribution has been successful at achieving national distribution for the hash products and is expected to generate additional revenues from these operations in Fiscal 2023.

Unabsorbed overhead costs were $nil in Q2, Q3 and Q4 of Fiscal 2022, a significant reduction from $1,400 in Q4 Fiscal 2021 (entire Fiscal 2021 was $8,063). The prior periods had significant unabsorbed overhead costs as a consequence of the unused or idled grow rooms. With the Company's cultivation operating at capacity, there was no current period charge for idled or unused rooms and for costs related to underutilization of certain derivative products manufacturing equipment. The Company does not expect to incur expenses for unabsorbed overheads for Fiscal 2023.

The Company's adjusted gross margin4 increased from Q4 2022's 23% to Q1 2023's 30%. This improvement was primarily due to lower cultivation costs that was the result of higher plant yields, ongoing cost efficiency improvements and the benefit of lowered per units costs that were achieved due to increased scale of operations at the Moncton facility (Phase 4C expansion was completed at the end of Q3 2022, with planting and harvests occurring over Q4 2022 and Q1 2023).

The Company expects to achieve similar adjusted gross margin rates throughout Fiscal 2023 with further cost saving initiatives being put into place to help offset anticipated price compression.

The overall level of Q2 to Q4 Fiscal 2023 adjusted gross margins will also be dependent on other factors including, but not limited to product category and brand sales mix. Organigram has identified the following sales mix opportunities which it believes have the potential to further improve adjusted gross margins over time:

•International sales, which have historically attracted higher margins and are expected to represent a greater proportion of the Company’s revenue;

•Sales from the Holy Mountain brand, which will include several product categories, in a number of higher margin formats with national distribution on most SKUs

•The launch of new products across different derivative categories with expected attractive long-term margin profiles; and

4 Adjusted gross margin is a non-IFRS financial measure. See "Cautionary Statement Regarding Certain Non-IFRS Measures".

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 10

•The larger volume of higher margin sales expected from the Lac-Supérieur Facility, achievable from the increased capacity post construction.

Outside of Canada, the Company serves international markets (mainly Israel and Australia) from Canada via export permits and is looking to augment sales channels internationally over time in other markets. The Company continues to monitor regulatory developments in other jurisdictions. In early Q1 Fiscal 2021, the Israeli Ministry of Health amended its quality standards for imported medical cannabis. In June 2021, the Company received its Good Agricultural Practice certification from Control Union Certifications under the Control Union Medical Cannabis Standard (“CUMCS”) in order to permit it to continue its shipments to Israel under the amended Israeli quality standards. The Company has sought and during May 2022 received an updated certification for IMC-GAP by CUMCS to demonstrate it continues to meet the evolving Israeli quality standards. This certification is subject to ongoing audit requirements.

Shipments to Canndoc resumed during Fiscal 2022 and on November 17, 2022, the Company entered into a multi-year agreement with Canndoc that contemplates shipping up to 20,000 kilograms of dried flower. Future shipments to Australia and Israel are contingent upon the timing and receipt of regulatory approval from Health Canada, including obtaining an export permit, as well as timing and receipt of regulatory approval from the purchaser's regulatory authority, including obtaining an import permit.

Recent political changes and cannabis election ballot initiatives for both medical and recreational use in the United States suggest that the potential movements to U.S. federal legalization of cannabis (THC) remain difficult to predict. The Company continues to monitor and develop a potential U.S. entry strategy that could include THC, CBD and other minor cannabinoids. The Company continues to monitor recreational legalization opportunities in European jurisdictions with a particular focus on German opportunities based on the size of the addressable market and recent regulatory changes.

With the significant capital injection from BAT and the PDC Agreement, the Company is well positioned to expand into the U.S. and further international markets at the appropriate time and subject to applicable laws. Under the PDC Agreement, the Company is granted a worldwide, royalty-free, sub-licensable, perpetual license to exploit IP developed under the PDC Agreement in any field. This license, which is non-exclusive outside of Canada and sole in Canada will also enhance Organigram’s ability to enter markets outside of Canada, including through sublicensing arrangements with established operators.

Without limiting the generality of risk factor disclosures referenced in the “Risk Factors” section of this MD&A, the expectations concerning revenue, adjusted gross margin and SG&A (comprises of general and administrative and selling and marketing expense) are based on the following general assumptions: consistency of revenue experience with indications of performance to date, consistency of ordering and return patterns or other factors with prior periods and no material change in legal regulation, market factors or general economic conditions. The Company disclaims any obligation to update any of the forward looking information except as required by applicable law. See cautionary statement in the “Introduction” section at the beginning of this MD&A.

MEDICAL MARKET

The cannabis data company BDSA estimates that the Canadian medical market value for calendar 2022 at $320M, a 13% year-over-year decline5. Also, the number of medical patients is projected to further decrease within the year, largely due to migration to the recreational channel. In Fiscal 2022, Organigram shifted its medical strategy from direct shipment to patients to fulfillment through the Medical Cannabis by Shoppers platform offered by Shoppers Drug Mart. The Company has transitioned its patient base to the platform and continues to be committed to patients through its partnership with Shoppers Drug Mart.

5 BDSA Market Forecast, September 2022

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 11

FINANCIAL RESULTS AND REVIEW OF OPERATIONS

CAUTIONARY NOTE REGARDING NON-IFRS FINANCIAL MEASURES

The Company uses certain non-IFRS performance measures such as Adjusted EBITDA and adjusted gross margin in its MD&A and other public documents, which are not measures calculated in accordance with IFRS and have limitations as analytical tools. These performance measures have no prescribed meaning under IFRS and therefore amounts presented may not be comparable to similar data presented by other companies. The data is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance such as net income or other data prepared in accordance with IFRS. See the cautionary statement in the “Introduction” section at the beginning of this MD&A, and the following discussion.

FINANCIAL HIGHLIGHTS

Below is the quarter-over-quarter analysis of the changes that occurred for the three months ended November 30, 2022 and November 30, 2021. Commentary is provided in the pages that follow.

| Q1-2023 | Q1-2022 | $ CHANGE | % CHANGE | ||||||||||||||||||||||||||||||||

| Financial Results | |||||||||||||||||||||||||||||||||||

| Gross revenue | $ | 60,882 | $ | 44,345 | $ | 16,537 | 37 | % | |||||||||||||||||||||||||||

| Net revenue | $ | 43,321 | $ | 30,378 | $ | 12,943 | 43 | % | |||||||||||||||||||||||||||

| Cost of sales | $ | 31,621 | $ | 27,924 | $ | 3,697 | 13 | % | |||||||||||||||||||||||||||

| Gross margin before fair value adjustments | $ | 11,700 | $ | 2,454 | $ | 9,246 | 377 | % | |||||||||||||||||||||||||||

| Gross margin % before fair value adjustments | 27 | % | 8 | % | 19 | % | 238 | % | |||||||||||||||||||||||||||

| Realized fair value on inventories sold and other inventory charges | $ | (12,528) | $ | (12,313) | $ | 215 | 2 | % | |||||||||||||||||||||||||||

| Unrealized gain on changes in fair value of biological assets | $ | 24,714 | $ | 10,469 | $ | 14,245 | 136 | % | |||||||||||||||||||||||||||

| Gross margin | $ | 23,886 | $ | 610 | $ | 23,276 | 3,816 | % | |||||||||||||||||||||||||||

| Operating expenses | $ | 19,828 | $ | 14,333 | $ | 5,495 | 38 | % | |||||||||||||||||||||||||||

| Income (loss) from operations | $ | 4,058 | $ | (13,723) | $ | 17,781 | 130 | % | |||||||||||||||||||||||||||

| Other income, net | $ | (1,271) | $ | (12,418) | $ | (11,147) | (90) | % | |||||||||||||||||||||||||||

| Net income (loss) | $ | 5,329�� | $ | (1,305) | $ | 6,634 | 508 | % | |||||||||||||||||||||||||||

| Net income (loss) per common share, basic | $ | 0.017 | $ | (0.004) | $ | 0.021 | 525 | % | |||||||||||||||||||||||||||

| Net income (loss) per common share, diluted | $ | 0.017 | $ | (0.004) | $ | 0.021 | 525 | % | |||||||||||||||||||||||||||

| Net cash provided by (used in) operating activities | $ | 3,465 | $ | (9,341) | $ | 12,806 | 137 | % | |||||||||||||||||||||||||||

Adjusted Gross Margin(1) | $ | 12,829 | $ | 5,475 | $ | 7,354 | 134 | % | |||||||||||||||||||||||||||

Adjusted Gross Margin %(1) | 30 | % | 18 | % | 12% | 67 | % | ||||||||||||||||||||||||||||

Adjusted EBITDA(1) | $ | 5,577 | $ | (1,887) | $ | 7,464 | 396 | % | |||||||||||||||||||||||||||

| Financial Position | |||||||||||||||||||||||||||||||||||

| Working capital | $ | 172,920 | $ | 217,834 | $ | (44,914) | (21) | % | |||||||||||||||||||||||||||

| Inventory and biological assets | $ | 87,210 | $ | 46,420 | $ | 40,790 | 88 | % | |||||||||||||||||||||||||||

| Total assets | $ | 573,227 | $ | 545,365 | $ | 27,862 | 5 | % | |||||||||||||||||||||||||||

Non-current financial liabilities(2) | $ | 4,379 | $ | 3,074 | $ | 1,305 | 42 | % | |||||||||||||||||||||||||||

Note 1: Non-IFRS measures that have been defined and reconciled within their respective subsections in this section of the MD&A.

Note 2: Non-current financial liabilities excludes non-monetary balances related to contingent share consideration, derivative liabilities and deferred income taxes.

NET REVENUE

Net revenue for the Company is defined as gross revenue, net of customer fees, discounts, rebates, and sales returns and recoveries, less excise taxes. Revenue consists primarily of dried flower and cannabis derivative products sold to the adult-use recreational cannabis, medical cannabis, wholesale, and international cannabis marketplaces.

For the three months ended November 30, 2022, the Company recorded an increase of 43% in net revenues to $43,321 from $30,378 for the three months ended November 30, 2021. Net revenue increased in the current period primarily due to an increase in recreational revenue of $10,839 and international revenue of $2,440, partially offset by a decrease in medical sales.

For the three months ended November 30, 2022, the net ASP of recreational flower decreased to $1.82 per gram compared to $1.89 per gram for the three months ended November 30, 2021, due to a shift towards value-oriented large format products.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 12

Sales volumes of all flower in grams increased 21% to 16,148 kg for the three months ended November 30, 2022 compared to 13,336 kg in the comparative period, primarily due to an increase to sales volume, and new large-format products that have been well-received by the market.

REVENUE COMPOSITION

The Company’s revenue composition by product category was as follows for the three months ended November 30, 2022 and 2021:

| Q1-2023 | Q1-2022 | ||||||||||||||||||||||

| Recreational Flower, net of excise duty | 25,353 | 21,315 | |||||||||||||||||||||

| Recreational Vapes, net of excise duty | 875 | 1,148 | |||||||||||||||||||||

| Recreational Hash, net of excise duty | 2,165 | — | |||||||||||||||||||||

| Recreational Infused Pre-rolls, net of excise duty | 365 | — | |||||||||||||||||||||

| Recreational Edibles, net of excise duty | 4,821 | 1,888 | |||||||||||||||||||||

| Recreational Ingestible Extracts and Oil, net of excise duty | 2,280 | 669 | |||||||||||||||||||||

| Medical, net of excise duty | 1,486 | 1,908 | |||||||||||||||||||||

| International Flower and Oil | 5,869 | 3,429 | |||||||||||||||||||||

| Wholesale and Other | 107 | 21 | |||||||||||||||||||||

| Total Net Revenue | $43,321 | $30,378 | |||||||||||||||||||||

COST OF SALES AND GROSS MARGIN

The gross margin for the three months ended November 30, 2022 was $23,886, compared to $610 for the prior period. The change and significant items impacting the three months ended November 30, 2022 were primarily as a result of: (i) lower cultivation and post-harvest costs on a per unit basis; (ii) inventory provisions of excess and unsaleable inventories as well as inventory provisions to net realizable value of $1,129 compared to $2,312 in the prior period; (iii) unabsorbed overhead of $nil compared to $709 in the prior period as a result of lower production volumes in the prior period; (iv) a lower ASP from increased competition and the ongoing evolution of the customer and product mix; and (v) provisions to net realizable value relating to the fair value component of inventories (fair value loss of $1,871, compared to $3,230 in the prior period).

Included in gross margin are the changes in the fair value of biological assets related to IFRS standard IAS 41 Agriculture. The net increase in fair value adjustments on period-over-period basis is due to an increase in harvested and in-progress plants, combined with higher yields, resulting in an increase in fair value of biological assets of $24,714 compared to $10,469 in the prior period, which was offset by the realization of the fair value increment for inventory sold of $10,657 (November 30, 2021 – $9,083) and adjustments to the net realizable value of inventory of $1,871 (November 30, 2021 – $3,230).

Cost of sales primarily consists of the following:

•Costs of sales of cannabis (dried flower, pre-rolls, and wholesale/international bulk flower, cannabis extracts, vapes, edibles, and other wholesale formats such as extract) include the direct costs of materials and packaging, labour, including any associated share-based compensation, and depreciation of manufacturing building and equipment. This includes cultivation costs (growing, harvesting, drying, and processing costs), extraction, vape filling, quality assurance and quality control, as well as packaging and labelling;

•Costs related to other products, such as vaporizers and other accessories;

•Shipping expenses to deliver product to the customer;

•The production costs of late-stage biological assets that are disposed of, plants destroyed that do not meet the Company’s quality assurance standards, provisions for excess and unsaleable inventories and provisions related to adjustments to net realizable value that reduce the carrying value of inventory below the original production or purchase cost, and other production overhead; and

•Unabsorbed fixed overhead charges, comprised of depreciation, insurance and property taxes, resulting from the underutilization of cultivation and production capacity.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 13

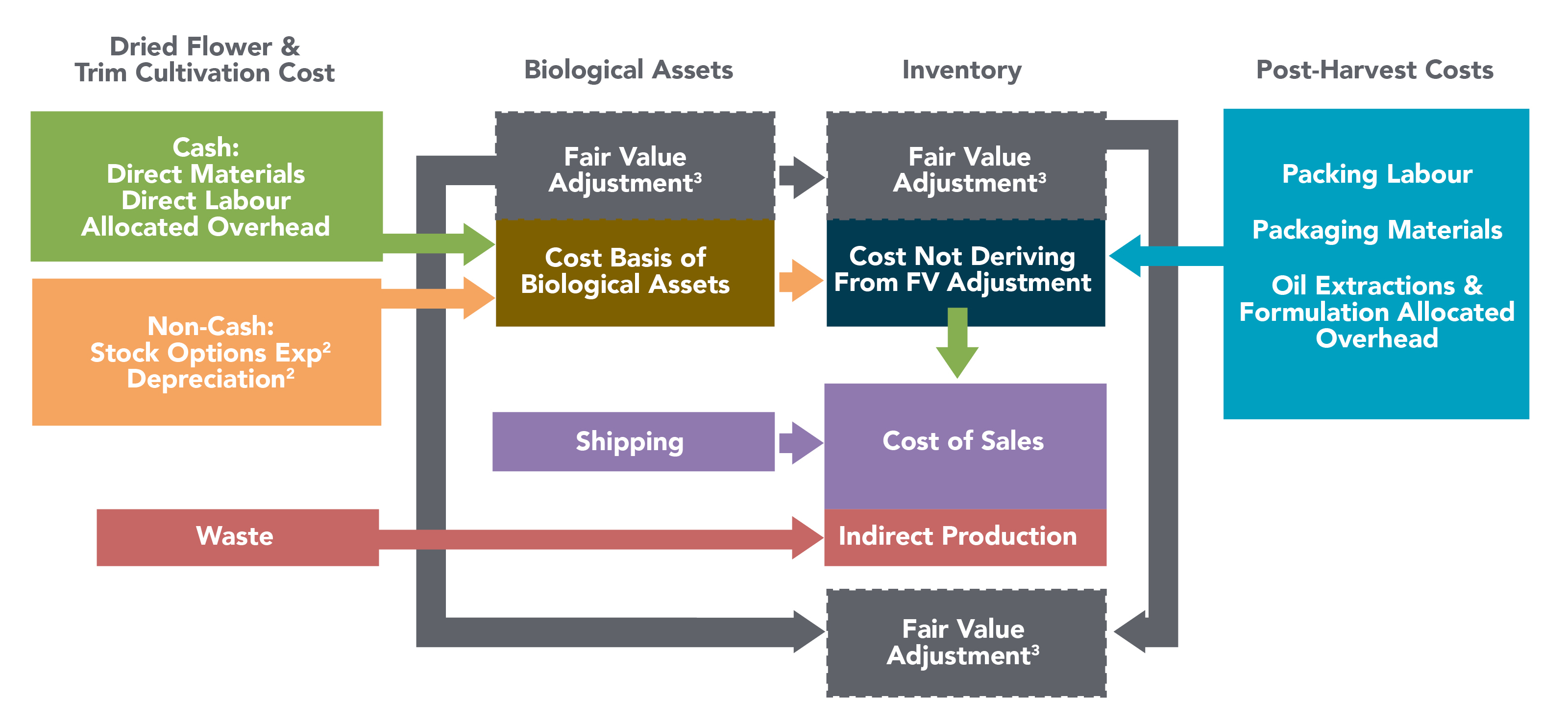

Illustrative Overview of Composition and Flow of Biological Assets, Inventories, and Cost of Sales

Note 1: The above illustration is for informational purposes only and should not be viewed as an exact representation of the actual flow of inputs and outputs. Certain items referenced above may not have a standard meaning under IFRS and therefore should be considered non-IFRS measures. Readers should refer to the notes to the Financial Statements for the official accounting policies.

Note 2: The majority of stock options and depreciation expense related to the manufacturing and operations departments are capitalized as part of cultivation and inventory production costs; however, a certain amount of these expenses that relate to overhead departments and underutilization of the Moncton Campus are expensed directly to cost of sales.

Note 3: Fair value adjustments are made to the cost basis of biological assets which collectively become the cost basis of inventories. Inventories are then carried at the lower of cost and net realizable value. When sold a portion of inventory is charged to cost of sales (actual costs) with the remainder (fair value adjustments) to “Realized fair value on inventories sold and other inventory charges” on the consolidated statements of operations and comprehensive income (loss).

Note 4: Excise taxes are excluded from this diagram and are reflected as a netting adjustment against gross revenue to arrive at net revenue for presentation purposes in the consolidated statements of operations and comprehensive income (loss).

ADJUSTED GROSS MARGIN

Adjusted gross margin is a non-IFRS measure that the Company defines as net revenue less: (i) unrealized gain on changes in fair value of biological assets; (ii) realized fair value on inventories sold and other inventory charges; (iii) provisions (recoveries) and impairment of inventories and biological assets; (iv) provisions to net realizable value; (v) COVID-19 related charges; and (vi) unabsorbed overhead relating to underutilization of the production facility grow rooms and manufacturing equipment, most of which is related to non-cash depreciation expense. Management believes that these measures provide useful information to assess the profitability of our operations as it represents the normalized gross margin generated from operations and excludes the effects of non-cash fair value adjustments on inventories and biological assets, which are required by IFRS. See the cautionary statement regarding non-IFRS financial measures in the “Introduction” section at the beginning of this MD&A and the reconciliation to IFRS measures in the “Financial Results and Review of Operations” section of this MD&A. The most directly comparable measure to adjusted gross margin calculated in accordance with IFRS is gross margin before fair value adjustments.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 14

| Q2-F21 | Q3-F21 | Q4-F21 | Q1-F22 | Q2-F22 | Q3-F22 | Q4-F22 | Q1-F23 | ||||||||||||||||||||||

| Net revenue | $ | 14,643 | $ | 20,324 | $ | 24,865 | $ | 30,378 | $ | 31,836 | $ | 38,115 | $ | 45,480 | $ | 43,321 | |||||||||||||

| Cost of sales before adjustments | 15,323 | 21,046 | 21,848 | 24,903 | 23,581 | 28,817 | 35,118 | 30,492 | |||||||||||||||||||||

| Adjusted Gross margin | (680) | (722) | 3,017 | 5,475 | 8,255 | 9,298 | 10,362 | 12,829 | |||||||||||||||||||||

| Adjusted Gross margin % | (5) | % | (4) | % | 12 | % | 18 | % | 26 | % | 24 | % | 23 | % | 30 | % | |||||||||||||

| Less: | |||||||||||||||||||||||||||||

| Provisions (recoveries) and impairment of inventories and biological assets | 10,050 | (59) | 1,997 | 1,845 | 686 | (83) | 1,600 | 1,067 | |||||||||||||||||||||

| Provisions to net realizable value | 3,499 | 669 | 622 | 467 | 25 | 6 | — | 62 | |||||||||||||||||||||

| Realized fair value on inventories sold from acquisitions | — | — | — | — | 663 | 700 | — | — | |||||||||||||||||||||

| Unabsorbed overhead | 2,274 | 1,725 | 1,400 | 709 | — | — | — | — | |||||||||||||||||||||

| Gross margin before fair value adjustments | $ | (16,503) | $ | (3,057) | $ | (1,002) | $ | 2,454 | $ | 6,881 | $ | 8,675 | $ | 8,762 | $ | 11,700 | |||||||||||||

| Gross margin % (before fair value adjustments) | (113) | % | (15) | % | (4) | % | 8 | % | 22 | % | 23 | % | 19 | % | 27 | % | |||||||||||||

Add: Realized fair value on inventories sold and other inventory charges | $ | (7,208) | $ | (8,509) | $ | (7,286) | $ | (12,313) | $ | (5,314) | $ | (7,386) | $ | (10,191) | $ | (12,528) | |||||||||||||

| Unrealized gain (loss) on changes in fair value of biological assets | $ | 6,516 | $ | 13,685 | $ | 11,639 | $ | 10,469 | $ | 7,502 | $ | 6,353 | $ | 15,677 | $ | 24,714 | |||||||||||||

Gross margin(1) | $ | (17,195) | $ | 2,119 | $ | 3,351 | $ | 610 | $ | 9,069 | $ | 7,642 | $ | 14,248 | $ | 23,886 | |||||||||||||

Gross margin %(1) | (117) | % | 10 | % | 13 | % | 2 | % | 28 | % | 20 | % | 31 | % | 55 | % | |||||||||||||

Note 1: Gross margin reflects the IFRS measure per the Company’s Financial Statements.

The adjusted gross margin and gross margin before fair value adjustments have steadily improved over the last eight quarters. Compared to Fiscal 2021, the increase to margin has been due to the combination of higher net revenue, lower cultivation and post-harvest costs, lower inventory provisions, and lower unabsorbed overheads.

OPERATING EXPENSES

| Q1-2023 | Q1-2022 | CHANGE | % CHANGE | ||||||||||||||||||||

| General and administrative | $ | 11,211 | $ | 7,984 | $ | 3,227 | 40 | % | |||||||||||||||

| Sales and marketing | 4,491 | 4,660 | (169) | (4) | % | ||||||||||||||||||

| Research and development | 2,383 | 1,015 | 1,368 | 135 | % | ||||||||||||||||||

| Share-based compensation | 1,743 | 674 | 1,069 | 159 | % | ||||||||||||||||||

| Total operating expenses | $ | 19,828 | $ | 14,333 | $ | 5,495 | 38 | % | |||||||||||||||

GENERAL AND ADMINISTRATIVE

For the three months ended November 30, 2022, the Company incurred general and administrative expenses of $11,211 compared to $7,984 for the prior year comparative period. The increase in the current period mainly relates to higher employee costs due to more general and administrative full-time employees to support the Company's growth, higher depreciation and amortization, general wage increases, and higher technology costs which includes $1,334 (November 30, 2021: $Nil) in ERP installation costs.

SALES AND MARKETING

For the three months ended November 30, 2022, the Company incurred sales and marketing expenses of $4,491 or 10% of net revenues as compared to $4,660 or 15% of net revenues for the prior period.

RESEARCH AND DEVELOPMENT

Research and development costs of $2,383 increased from the comparative period cost of $1,015, as the Company ramps up activity under the PDC Agreement and other internal product innovation projects.

SHARE-BASED COMPENSATION

For the three months ended November 30, 2022, the Company recognized $1,743 in share-based compensation in relation to selling, marketing, general and administrative, and research and development employees, compared to $674 for the comparative period due to a greater number of equity awards issued and outstanding during Q1 Fiscal 2023 as compared to Q1 Fiscal 2022.

Total share-based compensation charges, including those related to production employees that are charged to biological assets and inventory and amounts amortized for the three months ended November 30, 2022, were $1,852, compared to $680 for the comparable period, the changes being consistent with those noted above.

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 15

For the three months ended November 30, 2022, 1,104,000 options were granted, valued at $996, compared to 520,000 options granted in the comparative period, valued at $934. Included in the three months ended November 30, 2022 were 800,000 options granted to key management personnel compared to 500,000 options granted for the three months ended November 30, 2021.

During the three months ended November 30, 2022, 1,485,239 restricted share units (“RSUs”) were granted to employees (November 30, 2021 – 391,248), of which 1,140,765 RSUs were issued to key management personnel, which includes members of the Board of Directors, compared to 361,942 issued for the three months ended November 30, 2021.

During the three months ended November 30, 2022, 846,154 performance share units (“PSUs”) were granted to employees (November 30, 2021 – 169,843), of which 547,680 PSUs were issued to key management personnel, compared to 270,877 issued for the prior year.

Share-based compensation represents a non-cash expense and was valued using the Black-Scholes valuation model for stock options and using the fair value of the shares on the date of the grant for RSUs. The fair value of PSUs was based on the Company’s share price at the grant date, adjusted for an estimate of likelihood of achievement of the defined performance criteria.

OTHER (INCOME) EXPENSES

| Q1-2023 | Q1-2022 | CHANGE | % CHANGE | ||||||||||||||||||||

| Financing costs | $ | 41 | $ | 83 | $ | (42) | (51) | % | |||||||||||||||

| Investment income | (856) | (326) | 530 | 163 | % | ||||||||||||||||||

| Share of loss from investments in associates, net | 406 | 144 | 262 | 182 | % | ||||||||||||||||||

| Impairment of loan receivable and investments in associates | — | 250 | (250) | (100) | % | ||||||||||||||||||

| Loss on disposal of property, plant and equipment | 382 | 311 | 71 | 23 | % | ||||||||||||||||||

| Change in fair value of contingent consideration | 18 | (182) | (200) | 110 | % | ||||||||||||||||||

| Change in fair value of derivative liabilities | (1,030) | (12,698) | (11,668) | 92 | % | ||||||||||||||||||

| Total other (income)/expenses | $ | (1,039) | $ | (12,418) | $ | 11,379 | (92) | % | |||||||||||||||

INVESTMENT INCOME

Investment income of $856 was earned for the three months ended November 30, 2022, compared to $326 for the three months ended November 30, 2021. The change in investment income was due to higher interest rates in the current period as compared to prior year comparative period.

INVESTMENTS IN ASSOCIATES AND CONTINGENT CONSIDERATION

During the three months ended November 30, 2022, the Company’s share of loss from investments in associates was $406, compared to a loss of $144 in the prior year comparative period.

In connection with the Company's acquisitions of EIC and Laurentian, the Company has commitments to deliver additional consideration should EIC and Laurentian achieve their milestones. There was an $18 change in the estimated fair value of these contingent liabilities for the three months ended November 30, 2022.

DERIVATIVE WARRANT LIABILITIES

As at November 30, 2022, the Company revalued the derivative warrant liabilities at an estimated fair value of $3,091. The Company recorded a decrease in the fair value of the derivative warrant liabilities of $1,047 for the three months ended November 30, 2022 (November 30, 2021 – a decrease of $(12,052)) in the statements of operations and comprehensive income (loss). There were nil exercises of warrants during the three months ended November 30, 2022, resulting in 16,943,650 warrants outstanding at November 30, 2022 (November 30, 2021 - 18,687,500).

DERIVATIVE TOP-UP RIGHTS LIABILITIES

As at November 30, 2022, the Company revalued the top-up rights at an estimated fair value of $752 (August 31, 2022 – $735). The Company recorded an increase in the estimated fair value change of the top-up rights for the three months ended November 30, 2022 of $17 (November 30, 2021 - $(646)).

MANAGEMENT’S DISCUSSION AND ANALYSIS | FOR THE THREE MONTHS ENDED NOVEMBER 30, 2022 AND 2021 16

OTHER

During the three months ended November 30, 2022, the Company recorded a loss on disposal of property, plant and equipment of $382 (November 30, 2021 - $311). During Q1 Fiscal 2023, the Company continued and completed upgrades to its growing rooms, including the installation of LED light fixtures, which are expected to further improve the operating conditions of the Moncton Campus resulting in higher quality flower and a reduction in production costs. As a result of this work, certain assets that had not yet been fully depreciated were replaced, resulting in a loss on disposal of property, plant and equipment during the current period.

NET INCOME (LOSS)