Exhibit 2.1

ANNUAL INFORMATION FORM

For the twelve-month period ended March 31, 2014

June 30, 2014

TABLE OF CONTENTS

| FORWARD-LOOKING INFORMATION | 1 |

| CORPORATE STRUCTURE | 3 |

| GENERAL DEVELOPMENT OF THE BUSINESS | 4 |

| DESCRIPTION OF THE BUSINESS | 7 |

| DIVIDENDS | 20 |

| DESCRIPTION OF SHARE CAPITAL | 21 |

| MARKET FOR SECURITIES | 22 |

| ESCROWED SECURITIES AND SECURITIES SUBJECT TO RESTRICTION ON TRANSFER | 23 |

| GOVERNANCE OF THE CORPORATION | 23 |

| CONFLICTS OF INTEREST | 28 |

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS | 29 |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 29 |

| REGISTRAR AND TRANSFER AGENT | 29 |

| INTERESTS OF EXPERTS | 29 |

| MATERIAL CONTRACTS | 30 |

| ADDITIONAL INFORMATION | 30 |

FORWARD-LOOKING INFORMATION

This annual information form (“AIF”) contains “forward-looking information” within the meaning of applicable Canadian securities legislation and United States securities laws. Forward-looking information may include, but is not limited to, statements regarding future operations and results, anticipated business prospects and financial performance of Ceres Global Ag Corp. (“Ceres” or the “Corporation”) and its subsidiaries, expectations or projections about the future, strategies and goals for growth, anticipated capital projects, construction and completion dates, including the plans, costs, timing and capital for the development of the Northgate Commodities Logistics Centre (the “NCLC”), operating and financial results, critical accounting estimates and the expected financial and operational consequences of future commitments. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “scheduled”, “intends”, “anticipates” or “does not anticipate”, “believes” or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, or “will be taken”, “occur”, or “be achieved”. Forward-looking information is based on the opinions and estimates of management at the date the information is available, and is based on a number of assumptions and subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking information.

Key assumptions upon which such forward-looking information is based include, but are not limited to, the following (i) expected transition towards a more integrated North American grain commodity market as a result of the deregulation and privatization of the Canadian Wheat Board, which has effectively dismantled the monopoly in marketing wheat crops in Canada enabling farmers to gain more direct access to the open market; (ii) volume and quality of grain held on-farm by producers in North America are expected to increase as a result of the opening up of the Canadian grain market; (iii) no material change in the regulatory environment in Canada and the United States; (iv) supply and demand factors as well as the pricing environment for grains and other agricultural commodities; (v) fluctuation of currency and interest rates; (vi) general financial conditions for Western Canadian and American agricultural producers; (vii) market share that will be achieved by the Corporation; (viii) Riverland Ag’s ability to maintain existing customer contracts and relationships; (ix) expected increase in the utilization of Riverland Ag’s facilities; (x) continued compliance by Riverland Ag with its loan covenants; (xi) successful financing and completion of NCLC and all required regulatory permits and approvals; (xii) ability of Riverland Ag to successfully plan, design, build and operate the Northgate grain elevator as well as its ability to realize the economic benefits resulting from the synergies with NCLC; (xiii) successful internalization of Ceres’ management, processes and procedures; (xiv) Ceres’ ability to obtain financing on acceptable terms; (xv) successful negotiation of competitive rail freight agreements with Burlington Northern Santa Fe Railway at Northgate; (xvi) ability of Stewart Southern Railway Inc. to continue its growth in grain and oil shipments by rail, without service disruption; and (xvii) the outcome of the claim by The Scoular Company.

Many such assumptions are based on factors and events that are not within the control of Ceres and there is no assurance they will prove to be correct. Factors that could cause actual results to vary materially from results anticipated by such forward-looking information include, among others, risks related to weather, politics and governments, changes in environmental and other laws and regulations, competitive factors in agricultural, food processing and feed sectors, construction and completion of capital projects, labour, equipment and material costs, access to capital markets, interest and currency exchange rates, technological developments, global and local economic conditions, the ability of Ceres to successfully implement strategic initiatives and whether such strategic initiatives will yield the expected benefits, the operating performance of the Corporation’s assets, the availability and price of commodities and regulatory environment, processes and decisions. Although Ceres has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking information, there may be other factors that cause actions, events or results that are not anticipated, estimated or intended. There can be no assurance that forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Ceres undertakes no obligation to update forward-looking information if circumstances or management's estimates or opinions should change, except as required by applicable securities laws. The reader is cautioned not to place undue reliance on forward-looking information.

___________

- 2 -

In this AIF, unless otherwise indicated, all dollar amounts are expressed in Canadian dollars, references to “$” are to Canadian dollars and references to “U.S.$” are to United States dollars.

This AIF is dated June 30, 2014. Unless otherwise indicated, the information contained in this AIF is current as of March 31, 2014.

- 3 -

CORPORATE STRUCTURE

Name, Address and Incorporation

Ceres Global Ag Corp. was incorporated under the Business Corporations Act (Ontario) (the “OBCA”) by articles of incorporation dated November 1, 2007. Pursuant to articles of amendment dated December 6, 2007, the share transfer restrictions applicable to the Corporation were removed. On April 1, 2013, the Corporation amalgamated with Corus Land Holding Corp. under the OBCA. The Corporation’s registered and head office is located at 1920 Yonge Street, Suite 200, Toronto, ON M4S 3E2.

Intercorporate Relationships

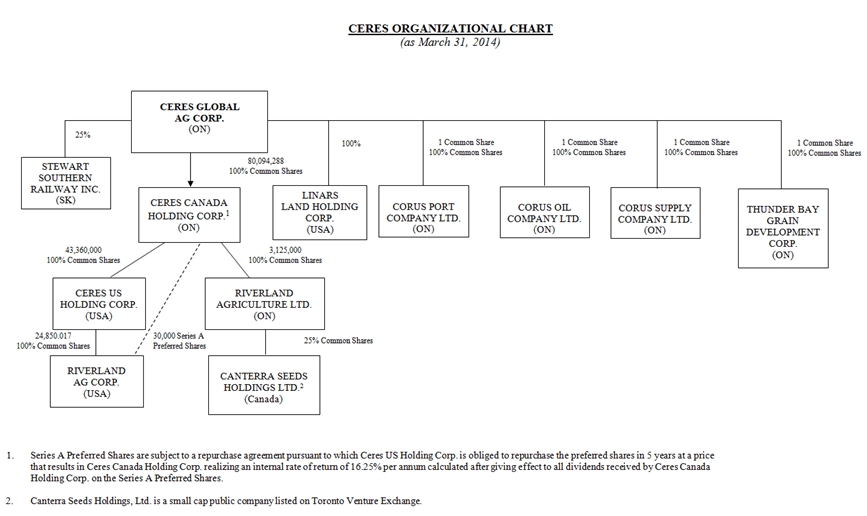

The Corporation has nine wholly-owned subsidiaries: Ceres Canada Holding Corp. (Ontario), Ceres U.S. Holding Corp. (Delaware), Riverland Ag Corp. (Delaware), Riverland Agriculture, Ltd. (Canada) (“Riverland Canada” and together with Riverland Ag Corp. (“Riverland AG”), Canterra Seeds Holdings Ltd. (Canada), Corus Port Company Ltd. (Ontario), Corus Oil Company Ltd. (Ontario), Corus Supply Company Ltd. (Canada) and Linars Land Holding Corp (USA). Unless the context otherwise requires, all references to the “Corporation” refer to the Corporation and its subsidiaries. Set out below is the corporate structure of the Corporation and its subsidiaries as at the date hereof.

- 4 -

GENERAL DEVELOPMENT OF THE BUSINESS

Three Year History

Northgate Commodities Logistics Centre

On February 5, 2013, the Corporation announced it had acquired approximately 1,300 acres of land at Northgate, Saskatchewan, where it is constructing a new commodities logistics centre (the “NCLC”) that utilizes high-efficiency rail loops, capable of handling unit trains of up to 120 railcars. A grain handling and shipping facility is expected to be the initial focus, potentially followed by an oil and natural gas supply logistics centre to facilitate exports from Saskatchewan’s and Western Canada’s energy sector, and a frac sand, pipe and cement unloading centre to bring these products in from the United States to service Western Canada’s energy drilling industry. As of the date hereof, site preparation at NCLC is 80% complete and Ceres has installed 1,150 meters of rail track running north from the Canada-U.S. border into the site, connected to Burlington Northern Santa Fe Railway (“BNSF Railway”). The NCLC is expected to be developed in conjunction with potential energy partners. Construction of NCLC is expected to continue through 2014 and 2015.

Following the completion of a comprehensive strategic review that was launched in September of 2013, Ceres decided to continue the development of the grain facility at the NCLC without the involvement of The Scoular Company (“Scoular”). Accordingly, in January 2014, Ceres terminated its arrangements and ongoing discussions with Scoular with respect to the development and construction by Scoular of a grain facility at the NCLC. On June 12, 2014, The Scoular Company initiated an action against Ceres for injunctive relief and unspecified damages relating to such termination. See “Legal Proceedings and Regulatory Actions”.

On May 9, 2014, Ceres announced the formation of a special committee comprised of five directors of the Corporation to lead the review process to explore the financing alternatives for an appropriate capital structure to fund the development of NCLC. The Corporation has retained a financial advisor to assist with the process.

See “Description of Business – The Northgate Commodities Logistics Centre” for further details.

Transition to Internal Management

On February 25, 2013, Ceres received a requisition from VN Capital Management LLC (the “VN Capital”) to hold a special meeting of shareholders to consider, and if thought fit, to pass certain resolutions to terminate the management agreement (the “Management Agreement”) between Ceres and Front Street Capital 2004 (“Front Street”) and transition to an internal management structure. A special committee of independent directors (the “Independent Committee”) was established and the special meeting of shareholders took place on July 24, 2013 where in excess of two-thirds of the common shares of the Corporation (the “Common Shares”) that were voted and held by shareholders not affiliated with Front Street were voted in favour of the termination of the Management Agreement. Through further negotiations among the Independent Committee, Front Street and certain shareholder groups, including VN Capital and Whitebox Advisors LLC (“Whitebox”), an Agreement Among Shareholders was agreed on, pursuant to which VN Capital, Whitebox and Front Street presented (i) a Management Agreement Early Termination and Management Internalization Agreement (the “Transition Agreement”), (ii) a proposed new slate of nominees for the Board and (iii) a proposal for a transition into a new management structure which, subject to the approval of the Board, they would be willing to support. On August 23, 2013, guided by the recommendation of the Independent Committee, the Corporation announced that it had entered into the Transition Agreement with Front Street, which provided, among other things, for the early termination of the Management Agreement effective November 30, 2013. The Transition Agreement was approved by the shareholders at the annual and special meeting held on September 27, 2013.

Under the terms of the Transition Agreement, among other things:

| · | the Management Agreement terminated effective November 30, 2013; |

- 5 -

| · | the monthly management fee payments to Front Street ceased at the end of September 2013 and a one-time termination payment of $5.0 million (plus taxes) was paid to Front Street on October 1, 2013; |

| · | Front Street will be paid an additional $1.0 million if the five-day volume weighted average price of the Corporation’s common shares on the TSX (the “5-day VWAP”) reaches $10.00 within 5 years, and a further $1.0 million if the 5-day VWAP reaches $11.00 (these payments will become immediately payable if there occurs prior the fifth anniversary of the date of the Transition Agreement either a change in control or a going private transaction at a price in excess of $7.85 per share); |

| · | the Corporation will deposit into an escrow fund 1/20th of any net sale proceeds (being gross sale proceeds in excess of net book value and direct transaction costs) from the sale of any of the Corporation’s assets, to a maximum amount of $1.0 million and such escrow fund shall be paid to Front Street if the 5-day VWAP does not reach $10.00 within five years; |

| · | Michael Detlefsen was appointed President and Chief Executive Officer, with a mandate to work with an expanded Board of Directors to facilitate a strategic review of the Corporation, develop and implement the resulting strategic plan, and develop and implement a new, permanent management structure for the Corporation, with the shared goal of a seamless transition and continuity in the business; |

| · | until November 30, 2013, Front Street continued to provide services and support to the Corporation, with no additional management fee payable to Front Street after September 30, 2013; and until March 31, 2014, Front Street continued to provide the services of Jason Gould as Interim Chief Financial Officer; and |

| · | the Corporation agreed to certain cost reimbursements for Front Street and VN Capital. |

Adoption of Advance Notice Bylaw

At the annual and special meeting of shareholders held on September 27, 2013, Ceres shareholders voted to ratify the adoption of the Amended and Restated By-Law No. 1, which, among other things, includes a provision requiring that advance notice be given to the Corporation in connection with shareholders intending to nominate directors for election to the Board (the “Advance Notice Provision”).

In particular, the Advance Notice Provision sets forth a procedure requiring advance notice to the Corporation by any shareholder who intends to nominate any person for election as director of the Company other than pursuant to (i) a requisition of a meeting made pursuant to the provisions of the OBCA, or (ii) a shareholder proposal made pursuant to the provisions of the OBCA. Among other things, the Advance Notice Provision fixes a deadline by which shareholders must submit a notice of director nominations to the Corporation prior to any annual or special meeting of shareholders where directors are to be elected and sets forth the information that a shareholder must include in the notice for it to be valid.

The Advance Notice Provision ensures an orderly nomination process and that all shareholders of Ceres are properly and adequately informed in advance of an election of directors. The Advance Notice Provision adopted by the Board provides a reasonable time frame for shareholders to notify the Corporation of their intention to nominate directors and requires the disclosure of information concerning the proposed nominees that is consistent with applicable securities laws.

Riverland AG

On July 12, 2011, the two-year revolving line of credit facility in place at Riverland Ag was increased from US$115 million to US$180 million, and an additional financial institution was brought to the lenders’ syndicate. Furthermore, on December 14, 2011, Riverland Ag modified a secured term loan agreement and entered into a 10-year term loan agreement in the amount of US$40.5 million. As part of the modification, Riverland Ag repaid the remaining principal on an existing secured term loan agreement, which then had a principal balance owing of US$19.2 million. In addition, management negotiated a reduction in the interest rate from 6.25% to 5.35%.

Since being acquired by the Corporation in June 2010, Riverland Ag has undergone efforts to increase its storage capacity. Two facilities in Wyoming were purchased from Busch Agricultural Resources, Inc. (“BARI”), adding 2.1 million bushels of storage. An expansion of the Shakopee facility was completed during the quarter ended March 31, 2011, which added 2.3 million bushels of storage. This facility is strategically located close to one of the largest

- 6 -

malting plants in North America and is positioned near several major milling companies. During the quarter ended March 31, 2011, Riverland Ag completed construction on a 2.3-million bushel expansion of its Malt One facility sited in an intermodal rail facility in downtown Minneapolis.

In August 2011, Riverland Ag acquired the Manitowoc grain storage and malting facility from Anheuser-Busch InBev of Leuven, Belgium. The Manitowoc facility includes 4.5 million bushels of grain storage capacity, with access to marine, rail and trucking modes of transportation.

On March 15, 2013, the Corporation entered into a strategic sourcing relationship with Briess Industries Inc. (“Briess”). As part of the strategic sourcing relationship, Briess acquired the Ralston elevator facility and the Powell, Wyoming seed plant for US$12.4 million. Riverland Ag will manage the facility on behalf of Briess for a minimum of three years. The majority of the facility’s barley shipments will be to Briess, with the balance being sold to the facility’s other existing customers. Riverland Ag will receive a monthly management fee and a contingency payment of between US$1.125 million and US$1.5 million in 2016 subject to certain performance targets being met. Processing of sales to the facilities’ other customers will be to the account of Riverland Ag. Briess assumes the working capital obligations of the facility, and will continue to be an important customer of Riverland Ag’s U.S. Upper Midwest facilities. On the sale of the two facilities in Q4 2013, Ceres recognized a gain of $9.6 million.

On March 20, 2014, the Corporation announced that Riverland AG Corp. had entered into an agreement to sell its Manitowoc, Wisconsin grain storage facility to Briess Malt and Ingredients Company of Chilton, Wisconsin. On May 23, 2014, the Corporation, through Riverland Ag, closed the sale of the Manitowoc grain storage facility. The gross proceeds from the sale were US$6.2 million. Pursuant to the purchase and sales agreement, Riverland Ag will lease back from the purchaser one million bushels of storage capacity at the Manitowoc grain facility for a three-year term.

On March 31, 2014, the Corporation announced that it had entered into an agreement to sell its Savage, Minnesota grain storage facility to Consolidated Grain and Barge Co., a wholly-owned subsidiary of CGB Enterprises, Inc., headquartered in Mandeville, Louisiana. On June 5, 2014, the Corporation announced that both parties agreed to terminate their agreement on the sale of the Corporation’s grain storage facility at Savage.

Normal Course Issuer Bids

On October 8, 2010, the Corporation commenced a normal course issuer bid for the purpose of providing the Corporation with a mechanism to decrease the potential spread between the trading price and the net asset value per common share of the Corporation (“Common Share”), as deemed necessary by the Corporation at the time when the Corporation operated as an investment company. Under the bid, the Corporation purchased a total of 276,021 Common Shares, for an aggregate consideration of $2.1 million. The bid concluded on October 5, 2011.

On October 17, 2011, the Corporation commenced another normal course issuer bid. Under the bid, the Corporation purchased a total of 373,796 Common Shares, for an aggregate consideration of $2.0 million. The bid concluded on March 31, 2012.

On July 11, 2013, the Corporation commenced a further normal course issuer bid. As of the date hereof, the Corporation purchased a total of 126,020 Common Shares, for an aggregate consideration of $1.0 million. The Corporation made no purchases after October 15, 2013.

All Common Shares purchased by the Corporation in connection with the normal course issuer bids above were cancelled.

- 7 -

DESCRIPTION OF THE BUSINESS

The Corporation

The Corporation is a Toronto-based agriculture and commodity logistics company with two main investment areas: (1) its Grain Storage, Handling and Merchandising unit, anchored by its 100% ownership of Riverland Ag; and (2) its Commodity Logistics unit, containing its 25% interest in Stewart Southern Railway Inc. (“SSR”) and its development of NCLC located in Northgate, Saskatchewan.

Ceres commenced business following its initial public offering on December 21, 2007. The Corporation is focused on acquiring control or significant influence positions in operating investments with a focus on the agricultural industry and related infrastructure industries. Prior to November 30, 2013, under the Management Agreement, Ceres had retained Front Street to manage and administer its day-to-day business and affairs. Ceres transitioned into an internal management structure in 2013 after the termination of the Management Agreement with Front Street. See “General Development of the Business – Transition to Internal Management”.

Riverland Ag

Riverland Ag engages in cereal grain storage, customer-specific procurement and “process-ready” cleaning of specialty grains such as oats, barley, rye and durum wheat. It offers a comprehensive range of services to its customers to help manage the risks associated with the price, quality, and availability of these critical food grains.

As of the date hereof, Riverland Ag owns and operates nine grain storage and handling facilities in the American states of Minnesota, North Dakota, New York and Wisconsin, and the Canadian province of Ontario. Riverland Ag also manages two facilities in Wyoming on behalf of its customer-owner. Riverland Ag’s facilities are strategically located, with excellent rail, truck and ship transportation logistics and close proximity to major grain-processing facilities in the United States. Many of the grain storage facilities are located at deep-water ports in the Great Lakes and along the upper Mississippi River, allowing access for lakers and barges, and enabling the efficient global import and export of grains.

The majority of Riverland Ag’s facilities are qualified as “regular for delivery” locations for certain futures contracts on the Minneapolis and Chicago exchanges, allowing Riverland Ag to earn carrying charges against grain stored for delivery to the exchanges by matching deliverable cash inventories with futures contracts. This delivery mechanism helps to mitigate risk for Riverland Ag and it is an important component of its credit facilities, as it provides Riverland with the option of delivering certain grain against futures contracts and enhances overall liquidity.

The majority of Riverland Ag’s current storage space is utilized to benefit from grain trading, arbitrage and merchandising opportunities. Management determines which of Riverland Ag’s facilities to be employed for the storage or throughput of a particular grain shipment based on the source of the grain shipment, the elevator location relative to the end customer(s), the cost of logistics to transport the grain, and the availability of space in the intended elevator.

Riverland Ag focuses on the storage, handling, trading and merchandising of cereal grains with particular emphasis on wheat, oats, barley and rye. In the case of wheat and oats, there are futures markets which it uses to hedge its inventories. For barley and rye, where no futures markets exist, Riverland Ag stores the grain under contract with end users.

Grains purchased by Riverland are primarily bought from third-party grain companies in the United States and Canada, although Riverland Ag has an ever-expanding direct-to-farmer purchase program that is expected to become increasingly important as the industry consolidates. Grains are usually sold to grain processing and milling companies along with food and beverage companies and livestock-related businesses, as well as delivered into the futures markets.

- 8 -

The nature and location of Riverland Ag’s assets allow it to be flexible in different types of grain markets, but typically Riverland Ag has performed best in an environment of strong production, resulting in surplus grains that need to be stored, combined with a futures market in contango (as further described below). The multiple inversions of the wheat and oats markets have posed significant challenges to Riverland Ag in the past two years. In addition, the Dodd-Frank legislation in the United States significantly reduced futures market activities as financial institutions retreated from the sector. This resulted in an excess in storage capacity at Riverland Ag, with corresponding low capacity utilization rates. Riverland Ag responded to this market development by selling non-core assets and entering into strategic partnerships with key customers. Going forward, management expects to continue the process of optimizing its grain elevator capacity and will likely pursue strategic partnerships and longer-term storage agreements with key cereal grain customers to raise capacity utilization and enhance profitability. With NCLC, management expects Riverland Ag to: (i) gain access to key origination markets, such as Western Canada; (ii) implement its direct-from-farmer buying programs to purchase grain at wholesale prices; (iii) attract additional downstream customers which will translate to elevator utilization improvement; and (iv) ultimately improve profit margin.

Historically, Riverland Ag made the majority of its revenues and profits from a ‘contango’ business model, in which it purchased grain inventories futures, earning a net carry charge that covered the costs of storage and interest, plus a profit margin. During the period from 2010 to early 2012, this strategy was highly profitable, given the large crop surpluses, significant participation in the long futures markets by a variety of financial players and a widening benchmark storage rate. Since that period, the market dynamics have changed substantially, with the financial players dropping out as counterparties in the futures market (driven primarily by provisions of the Dodd-Frank legislation in the United States), several crop years of production rebalancing grain market inventories and the more gradual than expected opening of the North American grain markets with the deregulation of the Canadian Wheat Board, such that the contango business model alone is no longer sufficiently profitable to generate sufficient returns on Riverland Ag’s invested capital.

In response to changing grain environment, Riverland Ag’s strategy focused on these platforms:

| · | A merchandising trading deck matching customer demand with supply chain efficiencies; |

| · | Maximizing carrying charges in commodities deliverable against futures where we are “regular” for delivery; and |

| · | Maximizing third-party storage income. |

With the deregulation and privatization of the Canadian Wheat Board, management expects this to strengthen Riverland Ag’s position in the spring wheat delivery market. NCLC is strategically located to facilitate the southbound grain movement and as such can enhance Riverland Ag’s potential profitability.

Stewart Southern Railway (SSR)

Ceres owns a 25% interest in the SSR, a 132-kilometre (82-mile) short-line railway that extends from Richardson, Saskatchewan (just southeast of Regina) to Stoughton, Saskatchewan. The SSR was purchased in 2010 from Canadian Pacific Railway, with which the SSR has a five-year haulage agreement that runs through mid-2015.

Historically, the SSR only shipped grain and, in 2010 and 2011, was challenged by low local production caused by excessive moisture. In February 2012, the SSR began shipping oil from the Stoughton area and monthly volumes have grown steadily. The Stoughton oil trans-loading facility now has a capacity of over 45,000 barrels per day (“bpd”) of production, and has become one of the largest crude oil by rail loading sites in Western Canada.

In April 2014, Crescent Point Energy opened a direct pipeline connection between its Viewfield, Saskatchewan storage complex and its Stoughton, Saskatchewan loading facility, enhancing the flows and reducing volume fluctuations caused by weather and local road bans. In addition, the SSR has recently been successful in developing a rail car storage program for shippers, which has broadened its revenue and earnings profile. Finally, with the strong 2013 harvest, sizeable grain volumes have returned to the SSR. Management expects that the SSR will transport as many as 18,000 railcars in the 2014 fiscal year, up from just over 1,000 in SSR’s first year of operation.

- 9 -

Having successfully absorbed this initial level of significant growth, the SSR is aggressively looking for increased shipment opportunities in oil, grain and other commodities.

The Northgate Commodities Logistics Centre (NCLC)

Ceres owns approximately 1,300 acres of land at Northgate, Saskatchewan and Northgate, North Dakota, where it is constructing a new commodity logistics centre that is designed to utilize high-efficiency rail loops, capable of handling unit trains of up to 120 railcars. A grain handling and shipping facility is expected to be the initial focus, followed by an oil and natural gas supply logistics centre to facilitate exports from Saskatchewan’s and Western Canada’s energy sector, and a frac sand, pipe and cement unloading centre to bring these products in from the United States to service Western Canada’s energy drilling industry.

NCLC’s direct connection to the 32,000-mile BNSF network is expected to give shippers direct access to customers in 28 American states, to numerous Pacific and Gulf ports, and to Mexico, including over 45 crude-by-rail destinations. Access to many other strategic interior locations in the Eastern U.S. and at Atlantic ports are also available through BNSF’s interline rail connections, providing new options to Canadian farmers and oil exporters.

Initially, Ceres intended to partner with a major U.S. based agricultural supply-chain company to develop the grain facility at NCLC. Following the completion of a comprehensive strategic review that was launched in September, 2013, Ceres decided to continue the development of the grain facility at NCLC without the involvement of a partner. Accordingly, in January 2014, Ceres terminated its arrangements and ongoing discussions with the proposed partner and announced the following plans with respect to NCLC:

| · | To complete the remaining site preparation and the installation of rail and associated infrastructure for NCLC to allow manifest and unit trains to cross the border into Canada and to facilitate the transloading of agricultural, petroleum and other bulk commodity products; |

| · | To use its 100% owned subsidiary, Riverland Ag, to bring in-house the design and development of the proposed grain facility at NCLC; and |

| · | To spend up to an additional $15.2 million of capital during the 2014 construction season for the planning and design of the grain facility and the planning, design and initial construction of the oil and natural gas liquids transload facilities at NCLC. |

As at March 31, 2014, Ceres has incurred $14.8 million of capital costs (2013 - $5.0 million) for the Canadian portion of NCLC, including land acquisition costs, environmental costs, mass grading and site preparation costs and initial rail costs. Ceres proposes to finance the remaining NCLC site development and construction costs with a combination of cash flows from operations, proceeds from the sale of selected non-core assets debt and equity financing.

The fully-completed grain facility at NCLC is expected to include a 2.2 million bushel high-speed shuttle grain loading facility capable of loading a unit train of 120 railcars within 12 hours to be operated by Riverland Ag and to provide substantial grain origination opportunities and have significant synergies with the remaining Riverland Ag assets. The NCLC elevator is expected to become a significant contributor to Riverland Ag, both as a Canadian-based originator of cereal grains from Western Canada, direct from farmers, and as a feeder to the downstream improvement of Riverland Ag’s existing storage assets. Management expects that the NCLC elevator will serve as a powerful catalyst to accelerate the repositioning and turnaround of Riverland Ag, as well as serve as the linchpin of NCLC. At full capacity, management believes that NCLC will significantly enhance the profitability of Riverland Ag by lowering grain purchase costs, increasing throughput and inventory turns, and improving capacity utilization.

To take advantage of the current logistics bottleneck and the upcoming harvest, the Corporation expects to install a temporary grain transloading facility over the summer so that grain can be shipped in the fall of 2014, while the permanent elevator is under construction. This temporary facility is expected to be able to load up to 72 grain car loads per week, serviced by the BNSF’s manifest local service 2-3 times per week.

- 10 -

Significant upgrades made by the BNSF to its network on the U.S. side of the border, required to support NCLC, have neared completion with the rail and bed in place, and recently connected to the Canadian side of the project. Currently, site preparation grading at NCLC is 80% completed and Ceres has installed 1,150 metres out of anticipated 12,552 metres of rail track running north from the Canada-U.S. border into the site. Construction of the remaining site infrastructure and rail is expected to continue over the summer, with track completion expected in early fall of 2014. In February 2014, the Corporation received approval from Canadian and U.S. customs authorities on the border crossing with the tracks connected across the border in early May 2014. The timing for initial rail shipments and the overall completion of the NCLC transloading project will depend on the Corporation obtaining appropriate financing.

Principal Business Activities

Ceres is focused in the following business areas:

Grain Storage and Handling

Riverland Ag enters third party storage contracts with food and beverage companies where the third-party owns the inventory or reimburses the interest cost of ownership and pays Riverland Ag for storage and elevation. It specializes in food grains that are marked by a diversity of species and that are differentiated by quality variables. The prescribed supply of these identity-preserved grains is critical to food and beverage companies. The specific physical aspects of individual grain shipments have an important effect on the processing performance and the resulting nutritional value of end products. Riverland Ag’s customers often seek greater quantities of ever more specific types of grains. The majority of grain suppliers tend to focus on lower-margin (higher-volume), homogenous feed grain aggregation terminals designed to serve markets such as livestock that are less quality discerning. See “General Description of Business – Riverland Ag”.

Grain Merchandising and Arbitrage

Riverland Ag also pursues arbitrage and merchandising opportunities. Most of Riverland Ag’s grain storage locations are deliverable on futures markets. Riverland Ag can match deliverable cash inventories with futures contracts. Matching cash grain to futures markets reduces basis risk, counterparty risk, and financing requirements. Its locations and equipment allow it to select among various transportation alternatives to source and/or deliver grain to markets to capture opportunities. Riverland Ag can capitalize on logistics efficiencies by utilizing 100-car unit trains from the Canadian Prairies and load grain onto even more efficient barge or ship for delivery to world markets. See “General Description of Business – Riverland Ag”.

Commodity Logistics

SSR operates a short line railway based in southeastern Saskatchewan involved primarily in the transportation of grain and oil. Ceres also owns approximately 1,300 acres of land at Northgate, Saskatchewan and Northgate, North Dakota, where it is constructing NCLC. See “Description of Business – Stewart Southern Railway” and “–The Northgate Commodities Logistics Centre”.

Revenue Sources

Ceres’ revenue is 100% derived from Riverland Ag’s operations. Riverland Ag’s revenue sources are from grain storage and handling as well as grain merchandising and arbitrage. For the year ended March 31, 2014, revenue from grain merchandising and arbitrage was $227.2 million, representing 97.8% (2013 - $217.9 representing 97.7%) of the total revenue sources, while grain storage and handling was $5.2 million representing 2.2% (2013 - $5.2 million representing 2.3%) of the revenue sources.

- 11 -

Specialized Skill and Knowledge

Riverland Ag requires specific skill and knowledge in both its trading and facilities operations. In its trading operation, Riverland Ag requires and has knowledge and understanding of the global grain markets coupled with an understanding of local North American markets. Riverland Ag employs traders who are focused on each specific major grain that the company handles. With respect to facilities management, the key areas of specific skill are managing product quality control, facility safety and multiple forms of logistics, including truck, rail and water. The majority of the staff was trained at some of the largest grain companies in the world. Facilities staff are regularly updated and trained on best new practices and new regulations for facilities. In addition, with 9 separate locations as of the date of this AIF, Riverland Ag’s risk is diversified and represents a pool of experienced employees who can back fill in other locations if issues arise.

SSR requires specific skill and knowledge in the management of traffic flow and rail line safety and operation. SSR is staffed with a combination of employees and third party contractors which enable SSR to access experienced workers despite its size.

The construction of the NCLC requires specific skill and knowledge in rail construction and logistics management in commodities. The Corporation has engaged a project management firm that specializes in rail construction to management the construction of NCLC. The Corporation relies on the expertise of Riverland Ag on the management of the logistics in grain and is in the process of hiring two senior personnel to develop and manage the energy logistics business of NCLC.

Competitive Conditions

Riverland Ag operates in a fragmented market where access to grain commodities, maintenance of the quality of the grains it stores and robust futures markets are expected to ultimately determine its competiveness. Riverland Ag sources grains from a large number of suppliers and its facilities on the Great Lakes systems are able to procure on an international basis if there is no local supply. Riverland Ag sells grains to approximately 240 customers with price ultimately determined by market conditions. Riverland Ag’s facilities are tributary to many of its customers due to the location of its elevators. There are several major mills within approximately 300 miles. Mills and feed lots are tributary to Riverland Ag’s elevators due to rail logistics or water.

Given the nature of the rail line industry, SSR’s main competition is the trucking industry for grain and oil and pipeline economics in the specific case of oil. While trucking oil provides a competitive connection to pipelines or rail, management believes that it is an interim mode of transportation requiring transloading to rail (or pipelines), and is not efficient for long distance transport to most end customers.

NCLC provides Ceres with strong competitive positioning for the export of bulk commodities (grain, oil, natural gas liquids and various minerals and mineral-based products) from Saskatchewan and imports of certain specialty products including fertilizer, frac sand, condensate, etc., used by western Canadian industries. As one of the few resuscitated rail border crossings, management believes that NCLC is not only uniquely positioned to efficiently transport goods across the borders but also provides a connection to BNSF. BNSF is one of North America’s largest railways, and, according to its public disclosure, connects 28 American states including over 45 crude-by-rail destinations 32,000 miles of rails, and allowing direct access to large parts of industrial America.

New Products and Services

With the sale of the grain storage facilities in Wyoming to Briess and subsequent entering into of a facilities management agreement, Riverland Ag has expanded into supply-chain management services for its customers.

The NCLC is currently designed to transport grain, oil, natural gas and other energy products from Saskatchewan to North Dakota whereupon it is expected to link to the BNSF rail system to other parts of the United States. The NCLC is designed to include grain storage and handling facilities to service its customers in Western Canada.

- 12 -

Suppliers

Food grains, such as oats, wheat and barley, are often purchased from dealers, including those in Canada with delivery being made by truck, rail, and vessel. The purchases are typically contracted with delivery to occur within a few months of purchase depending on transportation scheduling. Riverland Ag has no long term supply agreements, although most of its customers are repeat customers. Riverland Ag’s supplier base includes major North American grain companies.

Seasonality

As a commercial grain storage company, seasonality does not materially affect the operations of Riverland Ag in the same way as a traditional grain handler that is focused on inventory turns and the annual harvest of crops; however, in certain years Riverland Ag may have fewer inventory positions in the summer months in order to take advantage of harvests in the subsequent months. Riverland Ag can take advantage of merchandising opportunities throughout the year.

Economic Dependence

Riverland Ag has approximately 240 merchandising customers drawn from approximately 50 points of origination located in 8 American states and Canadian provinces. During the year ended March 31, 2014, Riverland Ag’s largest customer contributed to approximately 11% of total revenue. The largest 20 customers constituted 70% of total revenue, a majority of them are grain processing or large grain companies. Riverland Ag has no long term supply agreements with any supplier nor any long term sales agreement with any customer.

Environmental Protection

Riverland Ag is subject to compliance of various environmental protection requirements but none are out of the ordinary for the industry. Maintaining compliance is not expected to have a material impact on earnings or capital expenditures.

NCLC will be subject to federal, provincial, municipal and local environmental laws and regulations in Canada, concerning, among other things, emissions, discharges into waters, the generation, handling, storage transportation, treatment and disposal of waste, hazardous substances and other materials, and soil and groundwater contamination.

Employees

As at March 31, 2014, the Corporation had a total of 90 employees. Riverland Ag had 89 employees. Approximately 15 are located in the head office in Minneapolis and the balance were located at the elevator locations. SSR had 19 employees and numerous third party contractor.

Foreign Operations

Riverland Ag operates primarily in the United States. As at March 31, 2014, Riverland Ag operated ten grain elevators in Minnesota (Duluth, Savage, Minneapolis and Shakopee), Buffalo, New York, Wisconsin and Ontario.

- 13 -

| Location | Storage Capacity (000 Bu) | Transportation | Construction | Deliverable |

| Duluth, MN | 12,158 | Vessel, Truck, RR-CP | Vessel Berth Concrete Loader | MGEX, CBOT |

| Duluth, MN | 4,172 | Barge, Truck RR - CP | Vessel Berth Concrete | MGEX, CBOT |

| Savage, MN | 9,276 | UP, TCWR | Barge Slip Concrete | MGEX, CBOT |

| Malt One, MN | 4,608 | Truck, RR- BNSP | Concrete/Steel | MGEX, CBOT |

| Electric Steel, MN | 4,579 | Truck, RR - CP | Steel | MGEX, CBOT |

| Calumet, MN | 1,323 | Truck, RR- UP | Concrete | MGEX, CBOT |

| Shakopee, MN | 3,380 | Truck, RR- UP | Concrete/Steel | MGEX, CBOT |

| Buffalo, NY | 4,827 | Vessel Unload RR-CSXT | Vessel Berth Concrete | |

Port Colborne, Ontario | 2,259 | Vessel, Truck, RR-CP | Vessel Berth Concrete | |

| Manitowoc, WI (1) | 4,399 | Truck/Rail RR-CN | Concrete | |

Total | 50,981 |

| (1) | Sold on May 23, 2014. See “General Development of the Business – Riverland Ag” |

Risk Factors

An investment in the securities of the Corporation is speculative and involves a number of risks. In addition to the other information contained in this AIF, the following risk factors should be considered carefully. The events arising from these risks could materially adversely affect the Corporation’s business, financial condition, revenues or profitability. The following information pertains to the outlook and conditions currently known to the Corporation that could have a material impact on the financial condition of the Corporation. Additional risks not currently known to the Corporation or are deemed to be immaterial may also impair the business operations or financial conditions of the Corporation.

General

Regulatory Change

The Corporation may be affected by changes in regulatory requirements, customs, duties or other taxes. Such changes could, depending on their nature, benefit or adversely affect the Corporation. Rail operations in Canada are subject to (i) economic regulation by the Canadian Transportation Agency under the Canada Transportation Act (CTA), and (ii) safety regulation by the Federal Minister of Transport under the Railway Safety Act and certain other statues. No assurance can be given that any current or future legislative action by the federal government or

- 14 -

other future government initiatives will not materially adversely affect the Corporation’s development and future operating results of the Corporation.

General Economic, Political and Market Conditions

The success of the Corporation’s activities may be affected by general economic, political and market conditions, such as interest rates, availability of credit, inflation rates, economic uncertainty, changes in laws, and national and international political circumstances. These factors may affect the level and volatility of securities prices and the liquidity of the Corporation’s agricultural assets. Unexpected volatility or illiquidity could impair the Corporation’s profitability or result in losses.

Market Price of the Common Shares May Be Adversely Affected By Factors Beyond the Corporation’s Control

The market price of the Common Shares is expected to be based on the results of operations of the Corporation as reflected in its financial statements. The market price of the Common Shares will likely also be affected by macroeconomic developments in North America and globally and market perceptions of the attractiveness of particular industries. Other factors unrelated to the Corporation’s performance that may have an effect on the price of the Common Shares include the following: the extent of analytical coverage available to investors concerning the Corporation’s business may be limited if investment banks with research capabilities do not follow the Corporation’s securities; the lessening in trading volume and general market interest in the Corporation’s securities may affect an investor’s ability to trade significant numbers of Common Shares; and the size of the Corporation’s public float may limit the ability of some institutions to invest in the Corporation’s securities.

As a result of any of these factors, the market price of the Common Shares at any given point in time may not accurately reflect the Corporation’s long-term value. Securities class action litigation often has been brought against companies following periods of volatility in the market price of their securities. The Corporation may in the future be the target of similar litigation. Securities litigation could result in substantial costs and damages and divert management’s attention and resources.

Transition to Internal Management

Pursuant to the terms of the Transition Agreement, the Management Agreement was terminated effective November 30, 2013. In implementing its transition to internal management, the Corporation may not be able to engage the services of a senior management team on acceptable terms or with sufficient experience. If internal management is unable to manage the Corporation’s growth and projects effectively, such inability could adversely impact the Corporation’s business, financial condition and financial performance. The success of the Corporation is highly dependent on the services of certain management personnel. The loss of the services of such personnel could have an adverse effect on the Corporation. The transition may require time and attention of management and the Board that might otherwise be focused on management of the business of the Corporation. See “Recent History and Development of the Corporation – Transition to Internal Management”.

Attract and Retain Senior Management and Key Employees

The Corporation’s executives and other senior officers play a significant role in its success. The conduct of the Corporation’s business and the execution of its growth strategy rely heavily on teamwork and the Corporation’s future performance and development depend to a significant extent on the abilities, experience and efforts of its management team. The Corporation’s ability to retain its management team or attract suitable replacements should key members of the management team leave is dependent on the competitive nature of the employment market. The loss of services from key members of the management team or a limitation in their availability could adversely impact the Corporation’s prospects, financial condition and cash flow. The Corporation’s success also depends largely upon its continuing ability to attract, develop and retain skilled employees to meet its needs from time to time. Competition for skilled employees in certain geographical areas in which the Corporation operates can be significant and the Corporation may not be successful in attracting, retaining or developing such skilled employees.

- 15 -

In addition, the Corporation invests significant time and expense in training its employees, which increases their value to competitors who may seek to recruit them.

The Corporation’s Present and Potential Future Indebtedness

On March 28, 2014, Riverland Ag entered into a syndicated uncommitted US$120,000,000, 364-day revolving credit agreement, bearing interest at LIBOR plus 2.875% with interest calculated and paid monthly. Amounts under the credit agreement that remain undrawn are not subject to a commitment fee. The credit agreement is subject to borrowing base limitations. The credit facility is secured by predominantly all assets of Riverland Ag, including cash and Riverland’s Duluth Storage facility but excluding other property, plant and equipment. Obligations under this facility are guaranteed by Ceres Canada Holding Corp., Ceres U.S. Holding Corp., and Riverland Canada. As at March 31, 2014, the balance payable by Riverland Ag on this uncommitted revolving credit line (excluding the effect of unamortized financing costs) was US$65 million ($71.9 million).

New debt obligations may be incurred by the Corporation in the future, specifically with respect to the financing of NCLC. The Corporation’s present indebtedness and any additional debt it may incur in the future could have negative consequences on its business should operating cash flows be insufficient to cover debt service, which would adversely affect the Corporation’s operations and liquidity.

Currency Risk

The Corporation’s primary subsidiary, Riverland Ag, operates in United States dollars, being its reporting and functional currency. Riverland Ag does not hold material assets nor have material liabilities denominated in currencies other than United States dollars. Therefore, it is not directly exposed to currency risk in its normal operations.

A significant shift of the value of the Canadian dollar against the U.S. dollar could impact the Corporation’s profits. As the Corporation has cross-border operations, it may earn revenues and incur expenses in both U.S. dollars and Canadian dollars. Changes in the exchange rate between the Canadian dollar and U.S. dollar may make the products whose transportation the NCLC facilitates between Canada and the United States more or less competitive in the world marketplace and thereby may adversely affect the Corporation’s revenues and expenses.

Counterparty Risk

Riverland Ag uses various grain contracts as part of its overall grain merchandising strategies. Performance on these contracts is dependent on delivery of the grain or a customer buy-out. There is counterparty risk associated with non-performance, which may have the potential of creating losses for the Corporation. The Corporation’s management has assessed the counterparty risk and believes that insignificant losses, if any, would result from non-performance.

Market Price Volatility

Riverland Ag’s participation in the grain business makes it subject to market price volatility inherent in agricultural commodities. The nature of Riverland Ag’s arbitrage and merchandising business mitigates against the impact that short- and near-term price volatility would otherwise have on operating earnings. Interest costs on debt used to finance inventory fluctuates with changes in commodity prices. Riverland Ag typically builds inventory positions that bridge different crop years, which serves to mitigate against earnings volatility related to poor or bumper crop years.

Competition

The SSR faces significant competition, including from other rail carriers and other modes of transportation, and is also affected by its customers’ flexibility to select among various origins and destinations, including ports, in getting their products to market. Specifically, the SSR faces competition from long-distance trucking companies.

- 16 -

Competition is generally based on the quality and the reliability of the service provided, access to markets, as well as price. Factors affecting the competitive position of customers, including exchange rates and energy cost, could materially adversely affect the demand for goods supplied by the sources served by the Corporation and, therefore, the SSR’s volumes, revenues and profit margins. Factors affecting the general market conditions for the SSR’s customers can result in an imbalance of transportation capacity relative to demand. An extended period of supply/demand imbalance could negatively impact market rate levels for all transportation services, and more specifically the Corporation’s ability to maintain or increase rates. This, in turn, could materially and adversely affect the Corporation’s business, results of operations or financial position.

Risks Related to Commodity Markets

Commodity risk is inherent in the nature of Riverland Ag’s business, as it enters into commitments involving a degree of speculative risk. To reduce risk that might be caused by commodity market fluctuations, Riverland Ag generally follows a policy of using exchange-traded futures and options contracts to minimize its net position of merchandisable agricultural commodity inventories and forward cash purchase and sales contracts. It would also use exchange-traded futures and options contracts as components of merchandising strategies designed to enhance margins. The results of these strategies can be significantly influenced by factors such as the volatility of the relationship between the value of exchange-traded commodities futures contracts and the cash prices of the underlying commodities, and volatility of freight markets.

Adverse Weather Conditions

Adverse weather conditions represent a very significant operating risk affecting the agricultural industry. Weather conditions affect the types of crops grown, the quality and quantity of grain production and the levels of farm inputs which, in turn, affect sales mix, grain handling volumes and the level of agricultural product sales. Adverse weather conditions, such as drought or excessive rains, can result in reduced crop production and, in turn, reduced grain handling and marketing volumes. A reduction in grain handling and/or crop input sales because of adverse weather conditions can have a material adverse effect on the Corporation’s financial results and financial condition.

The Corporation’s customers may have limited windows of opportunity to complete required tasks at each stage of crop cultivation. Should adverse weather occur during these seasonal windows, the Corporation could face the possibility of reduced revenue in those seasons without the opportunity to recover until the following season. In addition, the Corporation may face the risk of inventory carrying costs should its customers’ activities be curtailed during their normal seasons.

Weather conditions that delay or intermittently disrupt field work during the planting and growing seasons may cause agricultural customers to use different forms of grain products, which may adversely affect demand for the forms that the Corporation sells or may impede farmers form applying products handled by the Corporation until the following growing season, resulting in lower demand for products handled by the Corporation.

Adverse weather conditions following harvest may delay or eliminate opportunities to apply products handled by the Corporation in the fall. Weather can also have an adverse effect on crop yields, which could lower the income of growers and impair their ability to purchase grains stored by the Corporation. The Corporation’s quarterly financial results may vary significantly from one year to the next due to weather-related shifts in planting schedules and purchasing patterns.

Commodity Prices

Prices of agricultural commodities are influenced by a variety of regional and global factors that are beyond the control of any company in which the Corporation may invest its assets. These include various economic and weather related conditions; governmental regulation and initiatives, including domestic and foreign farm programs and policies, trade subsidies, sanctions and barriers; outbreaks of crop diseases or insect infestations; and many other factors.

- 17 -

The Corporation also has exposure to commodity prices where there is a decline in the price of the particular agricultural commodity between the time of purchase and the time of sale by the Corporation. While the Corporation may take steps to hedge this exposure, there are limitations, such as the size of forward contracts, and also the lack of a regulated futures market for any specialty crops purchased by the Corporation.

Lower or fluctuating commodity prices may have a material adverse effect on the Corporation’s financial results, business prospects and financial condition.

Political and Economic Uncertainty

The world grain market is subject to risks and uncertainties, such as global political and economic conditions that can affect the Corporation’s ability to compete in the world grain market and importing countries’ abilities to purchase grain and other agri-food products. These factors can affect export levels of all grains, which in turn could affect the Corporation’s handling volumes and could have a material adverse effect on the Corporation’s financial results, business prospects and financial condition.

International agricultural trade is affected by high levels of domestic production and global export subsidies, especially by the United States and the European Union. Such subsidies interfere with normal market demand and supply forces and generally put downward pressure on commodity prices. Tariffs and subsidies restricting access to foreign markets prevent the expansion of the Canadian agri-food processing industry and cost Canadian jobs, especially jobs in rural Canada. While not the most significant sector overall for World Trade Organization members, the agricultural sector is likely the most politicized. The political influence of the farm sector in both the European Union and the United States is very significant, and agricultural negotiations are driven as much by political needs as they are by economics. Developing nations typically have small manufacturing bases and their agricultural sectors are critical to their economies. These concerns must also be accommodated in any agreement in the agricultural sector.

Employee Relations and Collective Bargaining Agreements

There can be no assurance that labour difficulties will not arise at one or more of the companies in which the Corporation has invested or in any company upon which there is a dependence on transportation or other services. Typically, companies in the agricultural and related sectors are subject to, among other things, stringent and comprehensive labour laws and regulations in the jurisdictions in which they operate. Such laws and regulations may become more stringent and comprehensive, and may result in modifications to facilities or practices that could involve significant additional costs.

Environmental, Health and Safety Risks

The Corporation’s exposure to safety, health and environmental risk relates primarily to the possibility that a serious safety or environmental incident could occur at one of its operating facilities. Even with precautions taken, there is still a risk to the Corporation that a serious safety or environmental incident may occur, resulting in a material adverse effect on the Corporation’s financial results, business prospects and financial conditions.

In conducting business, agricultural companies must comply with various federal, provincial and municipal environmental laws and regulations. Although a company in which the Corporation invests may be in substantial compliance in all material respects, circumstances may arise in the future that cause this not to be true. New or amended environmental laws and regulations may require future expenditures by such a company to install environmental control equipment, modify operations or proceed with remediation of certain sites. Failure to comply could potentially subject such company to fines and/or penalties. There can be no assurance that it will not experience difficulties in its efforts to comply with such laws and regulations in future years, or that the costs associated with continued compliance efforts will not have a material adverse effect on such company’s financial results, business prospects and financial condition.

- 18 -

As well, certain agricultural companies in which the Corporation may invest, may have potential environmental, health and safety risks because of the transportation, storage and handling of certain hazardous substances such as certain crop protection products and fertilizers. The presence or release of hazardous substances could lead to claims by third parties as a result of the release of such substances and potentially could have a material adverse effect on a company’s financial results, business prospects and financial condition.

Product Pricing

The agricultural industry is highly competitive and sensitive to changes in commodity prices. The price of a certain commodity is affected by many factors including supply and demand, negotiations between buyers and sellers, quality and general economic conditions, all of which could have a material adverse effect on the financial condition of a company. Demand for agri-products may be subject to fluctuations resulting from adverse changes in general economic conditions, evolving consumer preferences, nutritional and health related concerns and public reaction to food spoilage or food contamination issues. General supply of product may be subject to fluctuations relating to weather, insects and plant disease. There can be no assurance that current consumption levels of a product will continue to increase or will be maintained.

Governmental Regulations

Agricultural operations are typically governed by a broad range of federal, state, provincial and local environmental, health and safety laws and regulations, permits, approvals, common law and other requirements that impose obligations relating to, among other things: worker health and safety; the release of substances into the natural environment; the production, processing, preparation, handling, storage, transportation, disposal, and management of substances (including liquid and solid, non-hazardous and hazardous wastes and hazardous materials); and the prevention and remediation of environmental impacts such as the contamination of soil and water (including groundwater). Failure by a company to comply with applicable laws, rules, regulations and policies may subject such company to civil or regulatory proceedings, including fines, injunctions, administrative orders or seizures, and may have a material adverse effect on such company’s financial condition and operations. Also, as a result of the above environmental liability (including potential civil actions, compliance or remediation orders, fines and other penalties), including with respect to the disposal of waste and the ownership, management, control or use of transport vehicles and farmland, future discovery of previously unknown environmental issues, including contamination of property underlying or in the vicinity of a company’s present or former properties or manufacturing facilities, could require such company to incur material unforeseen expenses. All of these risks and related potential expenses may have a material adverse effect on such company’s financial condition and results of operations.

Risks Associated with Cross Border Trade

Markets in Canada, the United States and other countries may be affected from time to time by trade rulings and the imposition of customs, duties and other tariffs. There can be no assurance that the financial condition and results of operations of the Corporation will not be materially adversely affected by trade rulings and the imposition of customs, duties or other tariffs in the future.

Construction of NCLC

NCLC is currently under development and construction and is subject to a variety of risks associated with the development of a large scale capital project that are beyond the Corporation’s control. The completion of NCLC remains subject to obtaining adequate financing, reaching mutually satisfactory agreements with project partners and receipt of all required governmental permits and approvals. In addition, the completion of NCLC may experience delays and unexpected developments including, without limitation, adverse and inclement weather conditions, adverse environmental and geological conditions, shortage of skilled labour, availability of materials and supplies and financing issues. Any of these issues could give rise to construction delays and construction costs exceeding the management’s expectations.

- 19 -

The foregoing conditions and circumstances could have a material adverse effect on the completion of NCLC and/or the size and scope of the project and there can be no assurance that the project can be successfully completed or meet management’s current expectations.

The Corporation’s financial exposure may be exacerbated given the significant capital costs of NCLC to be expended by the Corporation prior to obtaining all permits necessary to operate the NCLC. Governmental requirements may increase the Corporation’s costs substantially, which could have a material adverse effect on the its business, financial condition as well as its results of operations and cash flows.

The Corporation’s expansion plans may also result in other unanticipated adverse consequences, such as the diversion of management’s attention from its existing businesses and other opportunities.

Government Regulation and Border Protection

In the United States, safety matters related to security are overseen by the Transportation Security Administration, which is part of the U.S. Department of Homeland Security (“DHS”) and the Pipeline and Hazardous Materials Safety Administration, which, like the Federal Railroad Administration, is part of the U.S. Department of Transportation. Border security falls under the jurisdiction of U.S. Customs and Border protection (CBP), which is part of the DHS. In Canada, the Corporation is subject to regulation by the Canada Border Services Agency (CBSA). More specifically, the Corporation is subject to CBP’s Customs-Trade Partnership Against Terrorism and regulations imposed by the CBP requiring advance notification by all modes of transportation for all shipments into the U.S. The CBSA is also working on similar requirements for Canada-bound traffic. The Corporation is also subject to an agricultural quarantine and inspection user fee for all traffic entering the United States from Canada.

Personal Injury and Other Claims

In the normal course of business, the Corporation may become involved in various legal actions seeking compensatory and occasionally punitive damages, including actions brought on behalf of various purported classes of claimants and claims relating to employee and third-party personal injuries, occupational disease, and property damage, arising out of harm to individuals or property allegedly caused by, but not limited to, accidents relating to the Corporation. The final outcome with respect to actions outstanding or pending, or with respect to future claims, may not be predicted with certainty, and therefore there can be no assurance that their resolution will not have a material adverse effect on the Corporation’s results of operations, financial position or liquidity, in a particular quarter or fiscal year.

Fuel Costs

The SSR, like other railroads, is susceptible to the volatility of fuel prices due to changes in the economy or supply disruptions. Fuel shortages can occur due to refinery disruptions, production quota restrictions, climate, and labor and political instability. Rising fuel prices could materially adversely affect the SSR’s expenses. Increases in fuel prices or supply disruptions may materially adversely affect the SSR’s results of operations, financial position or liquidity.

Economic Conditions

The Corporation is susceptible to changes in the economic conditions of the industries and geographic areas that produce and consume the freight it stores or transports or the supplies it requires to operate. In addition, many of the goods and commodities stored or carried by the Corporation experience cyclicality in demand. Some of the bulk commodities may move offshore and be affected more by global rather than North American economic conditions. Adverse North American and global economic conditions, or economic or industrial restructuring, that affect the producers and consumers of commodities the Corporation carries, including customer insolvency, may have a material adverse effect on the Corporation’s results of operations, financial position, or liquidity.

Food Product and Safety Risk

- 20 -

The Corporation is subject to potential liabilities connected to food and feed safety and product handling as the Corporation could be vulnerable in the event of a significant outbreak of food-borne illness or increased public health concerns in connection with certain food products. This could have a material adverse effect on the Corporation’s financial results, business prospects and financial condition.

Transportation Network Disruptions and Reliance on Third Party Providers

Due to the integrated nature of the North American freight transportation infrastructure, the Corporation’s operations may be negatively affected by service disruptions of other transportation links such as trucks, ports or railroads which interchange with the Corporation. The Corporation may rely on railroad, trucking, shipping and other transportation service providers to transport products which it handles to and from its facilities. These transportation operations, equipment and services are subject to various hazards, including adverse operating conditions on any aforementioned waterways, extreme weather conditions, system failures, work stoppages, delays, accidents such as spills and derailments and other accidents and operating hazards.

In the event of a disruption of existing transportation methods for products handled by the Corporation, alternative transportation and facilities may not have sufficient capacity to fully serve all of the Corporation���s customers or facilities. An extended interruption in the delivery of our products to the Corporation’s customers could have a material adverse effect on its business, financial condition or results of operations. Furthermore, deterioration in the cooperative relationships with these third parties could directly affect the Corporation’s long term operations.

These transportation operations, equipment and services are also subject to environmental, safety, and regulatory oversight. Due to concerns related to accidents, terrorism or increasing concerns regarding transportation of potentially hazardous substances, local, state, provincial and federal governments could implement new regulations affecting the transportation of the Corporation’s products.

If transportation of products handled by the Corporation is delayed or it is unable to obtain products as a result of any third party’s failure to operate properly or the other hazards described above, or if new and more stringent regulatory requirements are implemented affecting transportation operations or equipment, or if there are significant increases in the cost of these services or equipment, the Corporation’s revenues and cost of operations could be adversely affected. In addition, increases in the Corporation’s transportation costs, or changes in such costs relative to transportation costs incurred by our competitors, could have a material adverse effect on the Corporation’s business, financial condition, results of operations and cash flow.

Potential Acts of Terrorism and Regulations to Combat Terrorism

Similar to other companies with major industrial facilities, the Corporation’s facilities may be targets of terrorist activities. The Corporation’s facilities may store materials that can be dangerous if mishandled. Any damage to infrastructure facilities, such as electric generation, transmission and distribution facilities, or injury to employees, who could be direct targets or indirect casualties of an act of terrorism, may affect the Corporation’s operations. Any disruption of the Corporation’s ability to produce or distribute its products could result in a significant decrease in revenues and significant additional costs to replace, repair or insure our assets, which could have a material adverse impact on its business, financial condition, results of operations and cash flow.

In addition, due to concerns related to terrorism, local, state, provincial, federal and foreign governments could implement new regulations impacting the security of the Corporation’s facilities or other related facilities and infrastructure. These regulations could result in higher operating costs or limitations on the Corporation and could result in significant unanticipated costs, lower revenues and reduced profit margins.

DIVIDENDS

The Corporation has not paid any dividends or distributions on its outstanding Common Shares for each of the three most recently completed financial years. As of the date hereof, the Board has no intention to change its dividend

- 21 -

policy but may, from time to time and on the basis of the Corporation’s financial performance and other relevant factors, consider paying dividends in its discretion.

DESCRIPTION OF SHARE CAPITAL

The following is a summary of the material attributes and characteristics of the share capital of the Corporation. The following summary does not purport to be complete and reference is made to the Corporation’s articles of incorporation and articles of amendment for a complete description of these securities and the full text of their provisions.

Authorized Capital

The authorized share capital of the Corporation consists of an unlimited number of Common Shares without nominal or par value. As at the date hereof, the issued and outstanding securities of the Corporation consists of 14,208,679 Common Shares.

Common Shares

Each Common Share entitles the holder thereof to receive notice of any meetings of shareholders of the Corporation, to attend and to cast one vote per Common Share at all such meetings. Holders of Common Shares do not have cumulative voting rights with respect to the election of directors and, accordingly, holders of a majority of the Common Shares entitled to vote in any election of directors may elect all directors standing for election. Holders of Common Shares are entitled to receive on a pro-rata basis such dividends, if any, as and when declared by the board of directors of the Corporation at its discretion from funds legally available there for and upon the liquidation, dissolution or winding up of the Corporation are entitled to receive on a pro-rata basis the net assets of the Corporation after payment of debts and other liabilities, in each case subject to the rights, privileges, restrictions and conditions attaching to any other series or class of shares ranking senior in priority to or on a pro-rata basis with the holders of Common Shares with respect to dividends or liquidation. The Common Shares do not carry any pre-emptive, subscription, redemption or conversion rights, nor do they contain any sinking or purchase fund provisions.

Deferred Share Unit Plan