Cassidy & Associates

Attorneys at Law

9454 Wilshire Boulevard

Beverly Hills, California 90212

Email: CassidyLaw@aol.com

| Telephone: 949/673-4510 | Fax: 949/673-4525 |

December 18, 2015

Securities and Exchange Commission

Division of Corporation Finance

100 F Street, NE

Attn: Pamela Long, Assistant Director (Office of Manufacturing and Construction)

Washington, D.C. 20549

| RE: | Fuda Group (USA) Corporation |

Registration Statement on Form S-1

Filed November 17, 2015

File No. 333-208078

Dear Ms. Long:

Please find attached for filing with the Securities and Exchange Commission (the “Commission”) the amendments to the S-1 (filed November 17, 2015) for Fuda (USA) Corporation (the “Company”).

The following responses address the comments of the reviewing staff of the Commission as set forth in the comment letter dated November 30, 2015 (the “Comment Letter”) in response to the filing of the Form S-1 in November 2015. The comments and our responses below are sequentially numbered (based on the numbering sequence and text of the comments issued per the Comment Letter) and the answers herein refer to each of the comments by number and by citing if the response (if applicable) thereto results in revisions being made to the Form S-1.

General

1. Please revise your registration statement to provide updated financial statements and related disclosures for the interim period ending September 30, 2015 as required by Rule 8-08 of Regulation S-X.

Response: The Company is including its consolidated financial statements as of September 30, 2015 in the amended S-1 filed herewith.

2. You disclose that on February 23, 2015 the Company issued 61,000,000 shares of common stock to Lianing Fuda Mining Company. Further explain this transaction and how this related or impacted the transaction between Liaoning Fuda Mining and Marvel in September 2015.

Response: The Company’s initial intention on or about February 21, 2015 was to complete a direct merger with Liaoning Fuda Mining Company (“Liaoning Fuda”). However, upon further consultation with professional advisors, the Company determined that this structure was not most suitable. The interplay of Chinese (PRC) and domestic U.S. laws was something that professional advisors helped the Company to consider the better way to structure the transaction and that was later what was used in the mergers and acquisitions completed in 2015.

Accordingly, the following transactions/events transpired during 2015:

On February 21, the Company issued 61 million shares to Liaoning Fuda.

On February 28, there was an Equity Transfer Agreement made between Liaoning Fuda and Marvel whereby Liaoning Fuda agreed to transfer 100% of its shares and its assets to Marvel. The effective date of this agreement was June 30, 2015.

On July 1 through September 2015, through the Consent of Board via a Board Resolution, the Company redeemed all shares issued on February 21 (including those issued to Liaoning Fuda) and reissued them to another set of parties (Liaoning Fuda was not included).

The Company also used these redeemed shares to perform a share exchange merger to acquire Marvel (62 million shares issues) and Fuda UK (50 million shares issued).

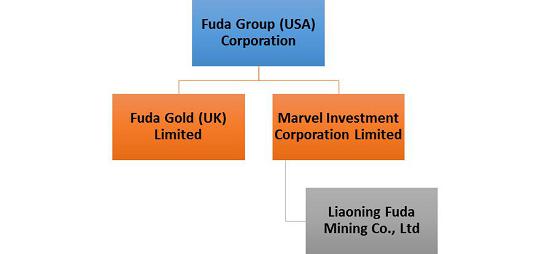

These various transactions were consummated in order for Fuda USA to become the parent company of Liaoning Fuda. Initially, the Company planned to achieve this goal by issuing 61 million shares to Liaoning Fuda in exchange for 100% of the shares of Liaoning Fuda, directly making the Company the parent company of Liaoning Fuda. The original and initial structure of the transactions is depicted below:

After this transaction was closed, the Company realized, upon consultation with professional advisers in PRC, that the Company could not directly acquire shares of a Chinese company under SAFE circulars. In order to undo this transaction, on July 1, 2015, the Company redeemed various shares that were originally issued in February 2015.

In order for the Company to become the parent company of Liaoning Fuda, the Company then used the second method: First, Marvel became the parent company of Liaoning Fuda on June 30, 2015 under an Equity Transfer Agreement. Under PRC law, Marvel, a company incorporated in Hong Kong would be treated as an on-shore company allowing the transaction to proceed as a VIE transaction

The Company then used the redeemed shares to perform a share exchange merger to (i) acquire 100% of Marvel’s shares for 62 million of the Company’s shares and (ii) acquire 100% of Fuda UK’s shares for 50 million of the Company’s shares. These transactions (which are illustrated in the structure below) allowed the Company to then become the parent company of Marvel and Fuda UK and the indirect parent company of Liaoning Fuda Mining.

3. Where you provide projections, please disclose the assumptions underlying them and other information to facilitate investor understanding of the basis for and limitations of these projections. Please specifically address the significant difference in your historical revenue and market share from you future projections, including those that are multiple years into the future.See Item 10(b) of Regulation S-K.

Response: For reasons unrelated to this comment from the Staff, the Company has decided to remove future projections from the Form S-1 in order to allow prospective investors to make their own judgments about the Company and its future. However, for purposes of this response letter to comments, the Company notes below the following for the Staff’s reference as related to the prior comment:

(a) Revenue assumptions for graphite business: These assumption for the current business were based off of historical trends (1994-2010) and previous business financials. These items include graphite & marble and graphite & fluorite segments. The Company assumed that growth will stabilize at an 8% year-over-year growth rate (in the past, the rate has been somewhat lower, at 4% to 6% annual growth; however, additional growth is expected from BRIC countries as well as advances in high technology uses of graphite). In making its estimates and basing its assumption, the Company reviewed a report from Industrial Alliance Securities Inc. that was published in 2012 discussing the graphite market.

(b) Franchising assumptions: The Company assumed royalty fees for franchisees at a rate of 5%, which is based on industry standards in this particular sector of the Company’s business. The Company looked at publicly-available research, such as from KPMG, regarding customary royalty rates and projections across various industries. The Company also consulted other business and entrepreneurial publications in making its estimates and assumptions that underlie the projections that it previously offered in the prior S-1 filing.

(c) Mining assumptions: The Mining assumptions were based off of current gold values and market trends including IBIS World paid research for futures and gold for precious metal mining. This methodology includes an average reserve volume based on speculation and average costs of mines.

(d) Gold prices: The Company had made assumptions about gold prices based on the prices of spot gold over the last 90 days (during this time, for example, the price of gold was approximately $1,150).

(e) Scrap gold: The Company relied on assumptions from other public estimates regarding gold wastage. While making gold jewelry, some percentage of gold is often lost. Hence, jewelries often charge the cost of the lost gold to buyers (the cost usually ranges from 10% to 35% of the cost of gold, based on the complexity of making the specific jewel).

(f) The Company made various other general assumptions.

Finally, the Company understands that, if it chooses to include projections in a future S-1 filing, the Company would need to include more disclosure in the body of the S-1 regarding financial and other assumptions to facilitate a more thorough understanding of the basis for and limitations of these assumptions. The discussion above regarding certain specific assumptions is provided only for discussion purposes and to better inform the Staff as to the bases for the prior set of projections were included in the prior version of the Form S-1 that was filed by the Company in November 2015.

Unaudited Pro-Forma Condensed Combined Financial Information, page 116

4. You state that your pro forma income statement financial information are presented as if the acquisition of Marvel and Fuda UK had occurred on December 31, 2014. Please revise your pro forma financial information to present information as if the transaction occurred at the beginning of the fiscal year presented in accordance with Rule 11-02(b)(6) of Regulation S-X.

Response: The Company is including its consolidated financial statements as of September 30, 2015 in the amended S-1 filed herewith.

In summary of the foregoing responses to your comments, we trust that the responses above as a whole and the revised Form S-1 filed herewith address the recent comments in the Comment Letter. We trust that we have responded satisfactorily to the comments issued by the Commission regarding the Form S-1. Hence, we hope that we will be in a position to request for acceleration of the Form S-1 in the near future once the Staff has completed its review of the instant amendment to the Form S-1 and these accompanying comment responses.

If you have any questions or concerns, please do not hesitate to contact Lee W. Cassidy at (949) 673-4510 or the undersigned at (310) 709-4338. In addition, we would request in the future that electronic copies of any comment letters or other correspondence from the Commission sent to the Company also be simultaneously copied to bothlwcassidy@aol.com andtony@tonypatel.com.

| Sincerely, | |

| /s/ Anthony A. Patel | |

| Anthony A. Patel, Esq. | |

| Cassidy & Associates |