Exhibit 99.2

TILL CAPITAL LTD.

MANAGEMENT’S DISCUSSION AND ANALYSIS

FOR THE NINE MONTHS ENDED SEPTEMBER 30, 2015 AND THE

TEN MONTHS ENDED SEPTEMBER 30, 2014

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

| BACKGROUND AND CORE BUSINESS | 2 |

| COPORATE DEVELOPMENTS, SIGNIFICANT TRANSACTIONS AND FACTORS AFFECTING RESULTS OF OPERATIONS | | 3 |

| • U.S. listing | 3 |

| • Change of presentation currency | 3 |

| • Acquisition of Omega | | | 3 |

| • Reinsurance agreements | | | 4 |

| • Changes to the Company's officers and board of directors | | | 4 |

| • Coeur Communications retained as investor relations firm | | | 5 |

| • Taussig Capital Ltd. engagement agreement | | | 5 |

| • Exiting the resource sector | | | 5 |

| • Assets held for sale | | | 5 |

| • Revision of SPD Promissory Note | | | 5 |

| • Loan to SPD | | | 5 |

| • Revision of GPY Promissory Note | | | 5 |

| • Normal course issuer bid | | | 6 |

| • GPY share options | | | 6 |

| REVIEW OF INVESTMENTS AND INVESTMENT PERFORMANCE | 6 |

| • Investment policy and strategy | | | 6 |

| • Investments | | | 6 |

| • Investment performance | | | 7 |

| OUTLOOK | | | 7 |

| SELECTED FINANCIAL INFORMATION | | | 8 |

| • Results of operations for the three months ended September 30, 2015 compared to the three months ended September 30, 2014 | 8 |

| • Results of operations for the nine months ended September 30, 2015 compared to the ten months ended September 30, 2014 | 8 |

| • Cash flows for the nine months ended September 30, 2015 compared to the ten months ended September 30, 2014 | 9 |

| • Summary of quarterly results | | 9 |

| • Financial position | | 10 |

| LIQUIDITY AND CAPITAL RESOURCES | | | 10 |

| OUTSTANDING SHARE DATA | | | 10 |

| OFF BALANCE SHEET ARRANGEMENTS | | | 10 |

| RELATED PARTY TRANSACTIONS | | | 11 |

| CRITICAL ACCOUNTING ESTIMATES | | | 11 |

| CHANGES TO ACCOUNTING STANDARDS | | | |

| RISKS | | | 13 |

| DISCLOSURE CONTROLS & PROCEDURES AND INTERNAL CONTROL PROCEDURES OVER FINANCIAL REPORTING | | 15 |

| INFORMATION REGARDING FORWARD LOOKING STATEMENTS | | | 16 |

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

The following management’s discussion and analysis ("MD&A") of the activities, results of operations and financial position of Till Capital Ltd. ( the "Company” or “Till”) should be read in conjunction with the interim condensed consolidated financial statements for the nine months ended September 30, 2015 and the audited consolidated financial statements for the ten months ended December 31, 2014 and related notes that have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). All amounts in this MD&A are stated in United States dollars unless otherwise indicated.

Additional information related to the Company, and its subsidiaries, including their Annual Information Forms can be found on SEDAR at www.sedar.com and EDGAR at www.sec.gov/edgar ..

The Company’s website is www.tillcap.com.

BACKGROUND AND CORE BUSINESS

Till Capital Ltd. ("the Company" or "Till") was incorporated under the laws of Bermuda on August 20, 2012 under the name Resource Holdings Ltd. On March 19, 2014, the Company changed its name to Till Capital Ltd. in accordance with the Company's bye-laws and section 10 of the Bermuda Companies Act 1981, as amended (the "Companies Act"). Till is an exempted holding company with its principal place of business at Continental Building, 25 Church Street, Hamilton HM12, Bermuda. Till's registered office is Crawford House, 50 Cedar Avenue, Hamilton HM 11, Bermuda and its registered agent is Compass Administration Services Ltd.

On April 17, 2014, the Company completed a reorganization plan (the “Reorganization”) whereby shares of Americas Bullion Royalty Corp. (“AMB”) were exchanged on a 100:1 ratio for shares of Till. Upon completion of the Reorganization, the Company’s shares commenced trading as Till Capital Ltd. (symbol TIL) on the TSX Venture Exchange(“TSXV”) and AMB’s shares were delisted from the Toronto Stock Exchange (“TSX”). The Company filed a Registration Statement with the United States Securities and Exchange Commission that became effective May 12, 2015 and its shares commenced trading on Nasdaq on May 26, 2015.

As part of the Reorganization, AMB sold the majority of its mining and mineral assets to Silver Predator Corp.(“SPD”) and Golden Predator Mining Corp. ("GPY"), formerly Northern Tiger Resources Inc., in return for controlling interests, collateralized notes, and royalty interests.

On September 2, 2015, the Company entered into a separation agreement with Mr. Sheriff, a former officer and director, whereby 7,100,000 shares of the Company's controlled subsidiary GPY were transfered to Mr. Sheriff. As a result, as of September 30, 2015, the Company no longer has a controlling interest in GPY, but maintains significant influence in GPY as a result of holding more then 20% of GPY's voting power. Accordingly, the Company consolidated GPY through September 30, 2015 and recognized a loss in the amount of $291,641 during the period ended September 30, 2015. The remaining shares of GPY shares were reported at their fair value as investment in associate at September 30, 2015. As at September 30, 2015, the Company owns approximately 36% of the outstanding shares of GPY. The financial statements of SPD are consolidated in the Company's financial results.

Till was formed to respond to the market need for more capacity for certain types of insurance and reinsurance. Till conducts its reinsurance business through Resource Re Ltd. (“RRL”), a wholly-owned subsidiary of Till that was incorporated in Bermuda on August 20, 2012 and licensed as a Class 3A insurance company in Bermuda by the Bermuda Monetary Authority (“BMA”) on August 28, 2013. RRL operates through the Multi-Strat Re Ltd. ("MSRE") program as a global property and casualty reinsurer to acquire medium to long-term customized reinsurance contracts with capped liabilities and diversification in specialty property and casualty lines. MSRE is a Bermuda based privately-held reinsurance company.

RRL's business strategy is to produce both underwriting profits from reinsurance policies and investment returns by investing reinsurance premiums and corporate capital. RRL generates underwriting income by offering reinsurance coverage to a select group of insurance companies, captive insurers that wish to redeploy capital more productively, profitable privately-held insurers with capital constraints that limit growth or wish to redeploy capital more productively, and insurers and reinsurers that are under regulatory, capital, or ratings stress. RRL's investment team has extensive experience in finance, trading, and operations.

On May 15, 2015, the Company acquired all of the issued and outstanding shares of Omega Insurance Holdings, Inc. (“Omega”), a privately-held Toronto, Canada based insurance provider, including its subsidiaries, Omega General Insurance Company (a fully licensed insurance company) and Focus Group, Inc. Omega’s mission is to offer secure, innovative, and customized solutions for insurers/reinsurers exiting the market and organizations with unique insurance needs in a cost effective manner. Omega’s expertise in both the Canadian run-off phase and the Canadian start-up phase for a foreign insurance company gives Omega a strategic advantage in its two main target markets:

| • | To provide those insurers wishing to access the Canadian market an ability to do so in an efficient manner through fronting arrangements and other means. |

| • | To provide those insurers wishing to exit Canada, through a dedicated company with experience in handling run-off business, an ability to facilitate such an exit so that their financial, legal, and moral obligations are met on a continuing basis, while being able to repatriate surplus capital in a more timely fashion. |

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

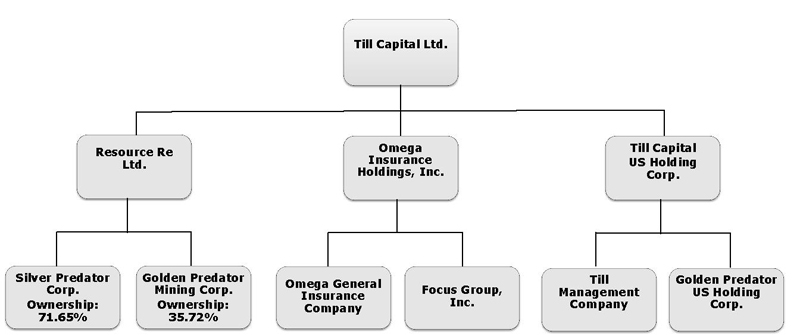

A summary of the Company’s legal structure at the date of filing this report is summarized in the following chart:

In conjunction with the Reorganization, the Company changed its year end from February 28, which was the year end of AMB, to December 31 to synchronize its financial reporting with that of comparable companies within the insurance industry. Pursuant to IFRS, AMB was the accounting acquirer in the Reorganization transaction; therefore, historical comparative results presented herein include those of AMB.

The Company completed a quasi-reorganization effective December 31, 2014 to restate its share capital to an amount equal to its then issued and outstanding shares multiplied by the par value per share of $0.001, or $3,569. The quasi-reorganization also eliminated the Company's historical deficit and increased contributed surplus. Because assets had been stated at approximate fair values, the quasi-reorganization had no effect on recorded assets.

A quasi-reorganization is an accounting process and transaction that results in the elimination of the accumulated deficit in retained earnings. This accounting process and transaction is limited to a reclassification of accumulated deficits as a reduction of share capital. The Company implemented the quasi-reorganization effective December 31, 2014 upon completion of the Company's revised business strategy and operating plans, and as a result thereof entering into the insurance and reinsurance business.

CORPORATE DEVELOPMENTS, SIGNIFICANT TRANSACTIONS, AND FACTORS AFFECTIING RESULTS OF OPERATONS

U.S. listing

To provide the Company with timely access to public capital markets should it require additional capital for insurance and reinsurance programs, capital expenditures, acquisitions or other general corporate purposes, the Company completed a U.S. exchange listing to broaden its access to capital markets. The Company's Registration Statement, filed with the United States Securities and Exchange Commission (“SEC”) on Form 20-F as a Foreign Private Issuer, became effective on May 12, 2015 and the Company's shares commenced trading on Nasdaq on May 26, 2015.

Change of presentation currency

The Company anticipates raising capital primarily in the U.S. market. Accordingly, the Company’s board of directors made a decision to change the Company’s financial statements’ presentation currency from Canadian dollars to U.S. dollars starting with the second quarter of 2015 so that investors in the U.S can better understand the Company’s financial results and financial position and so that the financial statements are more comparable to other companies in the U.S. market.

The unaudited interim condensed consolidated financial statements have been prepared in U.S. dollars as if the U.S. dollars had been the presentation currency since January 1, 2015, and all of the comparative prior period financial statements have been restated to U.S. dollars in accordance with International Accounting Standard (“IAS”) 21,"The Effect of Changes in Foreign Exchange Rates" ("IAS 21").

Acquisition of Omega

On May 15, 2015, the Company completed the acquisition of Omega Insurance Holdings, Inc., a privately-held Toronto, Canada based insurance provider, including its subsidiaries, Omega General Insurance Company (a fully licensed insurance company) and Focus Group Inc.

The purchase price of $14,042,084 represents 1.2 times the book value as of the closing date, and includes an additional amount of $730,994 for pending insurance transactions in process. The Company paid $12,262,988 on May 15, 2015 and $392,587 in June 2015. One of the two pending insurance transactions closed in August 2015, for which the Company paid $215,859 on August 31, 2015. The other insurance transaction was closed in October 2015, for which the Company paid $346,751 on October 30, 2015. All payments are subject to a 5% hold-back of approximately $700,000 to be paid to Omega shareholders on or about March 1, 2016 based on 2015 year-end results, and adjusted to give effect to any adverse development above 10% in claim reserves calculated from the closing date until December 31, 2015.

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

Reinsurance agreements

On February 17, 2015, the Company announced that its wholly owned subsidiary, RRL, entered into its first reinsurance policy effective as of December 31, 2014, arranged through MRSE, for $5.05 million of net premium with a claim liability cap of $6.49 million.

On August 28, 2015, the Company announced that it has novated its two reinsurance contracts held by its wholly-owned subsidiary, RRL. The total dollar value of the novated agreements is $5.3 million. The novation releases RRL from its liabilities under these reinsurance contracts.

Changes to the Company's officers and board of directors

On September 2, 2015, the Company announced Mr. William Sheriff (Mr. Sheriff) resigned as Chairman and Chief Executive Officer ("CEO") of the Company and from all of his board and executive positions with the Company and all of its wholly-owned subsidiaries as of September 1, 2015. The Board appointed Mr. William A. Lupien, a Director of the Company and it's Chief Investment Officer, to serve as Interim CEO of the Company while it pursues the recruitment of a CEO having a strong reinsurance/insurance background.

For over 50 years, Mr. Lupien has been an innovator in the public financial markets. His career in the securities business began at the California-based brokerage firm of Mitchum, Jones & Templeton (MJT), Inc. in 1965, where he eventually served as President. In 1983, as CEO and Chairman of Instinet Corporation, he successfully expanded the market reach of the world's first electronic stock trading system. As Chairman and CEO of OptiMark Technologies Inc., he co-invented the OptiMark trading system designed for stock markets around the world. From 2005 to 2014, Mr. Lupien served as the investment manager of Kudu Partners LP. Mr. Lupien currently serves as Chief Investment Officer of Till Management Company, a wholly-owned subsidiary of Till. Mr. Lupien previously served on the Securities and Exchange Commission's Advisory Committee dedicated to the development of a national market system, and also served as a Governor of the Pacific Stock Exchange. He had previously served as Chairman of Instinet (1983 - 1989), MJT (1989 - 1996), and Optimark US Equities Inc. (1996 - 2001), and as Director of Energy Metals Corp., Gold One International Ltd., Uranium One Inc., and Midway Gold Corp. He is the co-author, with Mr. David Nassar, of the book Market Evaluation and Analysis for Swing Trading, and is a co-author of several papers on trading technology and early-stage company evaluation. Mr. Lupien is also a co-inventor on multiple patents related to electronic securities trading. He is a graduate of San Diego State University. Mr. Lupien was appointed as the Company's Director on June 14, 2015.

Dr. John T. (Terry) Rickard was appointed as the Company's Director on August 3, 2015. Dr. Rickard has 44 years of experience in advanced technology and financial organizations, all of it in management, oversight, and technology development positions. He has been an executive and a director of several private companies and one public reporting company. He was President and later Chief Scientific Officer of OptiMark Technologies, Inc. and served on its board. He was a co-inventor of the OptiMark transaction matching system and was instrumental in the development of that company from a start-up enterprise to an operating entity on the Pacific Stock Exchange, the Nasdaq market and the Osaka Securities Exchange, including the securing of over $350 million in investment capital from major investors in the U.S. and internationally. Prior to that, he was President of the brokerage firm Mitchum, Jones & Templeton. He has authored/co-authored over 70 refereed technical publications in engineering, electronic market structure, matching algorithms, and trading strategies, and has co-authored 11 issued patents. He has also served as an expert witness in multiple intellectual property litigations involving financial markets. He received a Ph.D. degree in Engineering Physics from the University of California, San Diego, in 1975. As the Director of Quantitative Research for Till Management Company, a wholly-owned subsidiary of Till, Dr. Rickard is responsible for designing computationally intelligent systems for automated trading and investment due diligence.

Mr. Roger Loeb was appointed as the Company's Director on August 17, 2015. Mr. Loeb has been consulting to senior executive management for over 30 years, following a career as a senior corporate executive, where he held both technology strategy and line management responsibilities. He is President and CEO of The MarTech Group, Inc., Parker, CO, an organizational transformation and strategic technology consulting company he founded in 1984. Mr. Loeb and two partners are currently engaged by NeuStar, Inc. (NYSE:NSR) to guide the transition of the telephone Local Number Portability Administration service to a new provider. From 2008 to 2014, Mr. Loeb was engaged by the Deputy Chief Information Officer ("DCIO")(G6) of the Department of the Army for whom he provided “reality check” and “best practices” oversight of various high-profile enterprise-scale information technology implementations. The DCIO team’s most notable achievement during this period was the Army’s successful migration to a single email service from roughly 1,000 separate email server instantiations. From 2003 to 2008 Mr. Loeb was engaged exclusively by the Office of the Chief Technology Officer, IBM Federal, holding the title of Executive Consultant, Strategic Transformation, and providing technology strategy counsel to senior executives of the U.S. Department of Defense and Intelligence agencies. Mr. Loeb has been a significant contributor to the creation or improvement of industry-leading, technology-based service businesses in domains as diverse as commercial software, healthcare, nonprofit membership associations, publishing, insurance, direct marketing, credit decisioning and risk assessment, customer relationship management, venture capital startups, stock trading, employee selection, commercial printing management, transportation, travel booking, advertising, and defensive cyber security. He has also served as an expert witness in successful lawsuits over failed software development projects. Prior to founding The MarTech Group, Mr. Loeb was employed for 17 years by the A.C. Nielsen Co., Neodata Services Division, where he retired as Vice-President and Chief Information Officer. His innovations at Neodata were acknowledged to have completely transformed circulation management for the consumer magazine publishing industry. Mr. Loeb holds a B.S. degree in mathematics from the University of Wisconsin.

Mr. Alan S. Danson was appointed as the Company's Director on August 21, 2015 and was elected as non-executive chairman of the Board on September 2, 2015. Mr. Danson is currently a private investor and volunteer board member of several non-profit organizations. During his career, he worked as an attorney in a Wall Street law firm, an investment banker on Wall Street, an investment manager and investment banker in Mexico City, a partner in a venture capital firm in Denver and an entrepreneurial manager in Colorado. Mr. Danson has served on boards of directors of private companies, public companies and a regulated entity. Mr. Danson served, for 19 years, as an independent director of Dreyfus Founders Funds, a Denver-based family of actively managed equity mutual funds, becoming chairman of the board in 2008. The fund family was acquired by Bank of New York Mellon and later was rolled into its Dreyfus family of funds. Between September 1995 and December 1999, Mr. Danson was an investor in and served as a board member of OptiMark Technologies, Inc., a developer of electronic markets, he held the title of Senior Vice President and was instrumental in crafting several offering circulars and raising the company’s initial rounds of investment capital. From 1986 to 1995, Mr. Danson served as a board member and, through 1989, as President, of Integrated Medical Systems, Inc., a start-up provider of health care information and marketing services. The company was sold to Eli Lilly & Co. in December 1995. Between 1983 and 1986, Mr. Danson was a general partner of The Centennial Funds, the largest venture capital management company in the Rocky Mountain region. Mr. Danson was active on both the fund-raising and investment sides of the business. From 1972 to 1982, Mr. Danson lived and worked in Mexico, where he was a founding partner of a startup brokerage and investment firm, Acciones y Valores de Mexico (“Accival”), he helped the firm capture and manage pension funds from Mexican subsidiaries of US companies, and he helped a variety of Mexican companies with their public offerings in Mexico. Accival was ultimately acquired by CitiGroup. Between 1966 and 1972, Mr. Danson worked as an investment banker on Wall Street, first for Bear, Stearns & Co. and subsequently for Wertheim & Co. Mr. Danson began his career as an attorney with the Wall Street law firm Winthrop Stimson Putnam & Roberts.

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

On October 15, 2015, the Company held its Annual General and Special Meeting in Las Vegas, Nevada. All of the proposed candidates, Alan S. Danson, William A. Lupien, Wayne Kauth, Roger M. Loeb, and John T. Rickard were duly elected as directors for the ensuing year.

The following former Directors resigned from the Company's Board of Directors: Barry Rayment on June 14, 2015, David Atkins on July 31, 2015, Blair Shilleto on August 5, 2015, William Harris on August 17, 2015, Thomas Skimming on August 18, 2015, Joseph Taussig on September 2, 2015.

Ms. Janet Lee-Sheriff resigned as Executive Vice President on July 31, 2015.

Coeur Communications retained as investor relations firm

The Company has retained the services of Coeur Communications as the Company’s investor relations firm effective August 19, 2015. Coeur Communications is an investor relations and corporate governance solutions firm based in Coeur d’Alene, Idaho. Led by Monique Hayes, who has over 25 years combined experience in marketing, corporate governance, and investor relations for small public reporting companies, Coeur Communications’ goal is to provide the core elements for small public companies to communicate their story to shareholders. Coeur Communications replaces the Company's previous investor relations firm Sard Verbinnen.

Taussig Capital Ltd. engagement agreement

In July 2015, the Company entered into a non-exclusive engagement agreement (the "Agreement") between the Company and Taussig Capital Ltd. ("TCL"), a company incorporated in Bermuda. Pursuant to the Agreement and subsequent amendment, TCL serves as a non-exclusive advisor to the Company in connection with a proposed financing of no less than $50 million in equity capital from strategic investors (the "Proposed Financing") on a best efforts basis.

The Agreement also provides that, after completion of the Proposed Financing, the strategic investors, who may themselves be asset managers, will be allowed to manage 100% of their invested capital as part of the Company’s reinsurance related assets.

Mr. Joseph Taussig, a principal of TCL, is also a principal of MSRE with whom the Company’s wholly-owned reinsurance subsidiary, RRL, has previously entered into a separate agreement for underwriting and related services in support of its reinsurance business.

Exiting the resource sector

On September 2, 2015, the Company announced its desire to exit its involvement in the resource sector, with the corresponding financial commitments, and to devote its future efforts and attention to its reinsurance/insurance businesses.

Assets held for sale

In the second quarter of 2015, SPD announced its intention to realize value from assets by initiating the process to sell all, or part, of the tangible and intangible assets at some of its properties in Nevada. There is an active program in place to sell these assets, and active negotiations are being held with potential buyers. It is expected the sale will be completed within one year. Pursuant to IFRS 5, Non-current Assets Held for Sale and Discontinued Operations(“IFRS 5”), the associated assets and liabilities are classified as assets held for sale and liabilities held for sale.

Revision of SPD Promissory Note

In August 2015, SPD’s Board of Directors approved making a full cash payment of its $4.5 Million Promissory Note to the Company, plus accrued interest, upon receipt of the proceeds from the sale of SMC. SPD's Board of Directors also agreed to negotiate in good faith with the Company to settle on a cash price for the existing 2.0% Net Smelter Royalty on the Springer property to the Company. The agreed upon dollar amount would be paid in cash by SPD in exchange for the Company extinguishing the royalty on the property.

Loan to SPD

On August 28, 2015, the Company announced that it has signed a Promissory Note (the "Note") issued by SPD to the Company, in conjunction with which the Company advanced $235,000 of the Note principal to SPD during the period ended September 30, 2015. The principal on the Note is limited to $275,000, which amount represents the maximum that SPD may borrow, but is not obligated to do so. The annual interest rate on any balance on the Note is 12% and, in addition to other repayment provisions, the Note must be repaid in its entirety by December 31, 2015.

Revision of GPY Promissory Note

On September 2, 2015, the Company announced that it renegotiated the terms of a Promissory Note from GPY that it currently holds, to require payment in cash only, removing GPY’s current right to pay with shares of GPY valued at $0.35 CDN per share, and securing repayment of the note against GPY’s Brewery Creek and 3 Aces properties. In return for these changes, the Company has agreed to: (a) an extended repayment schedule, with the first payment due to the Company on June 1, 2016, and consisting of $500,000 CDN, plus any then-outstanding accounts payable owed by GPY to the Company, plus accrued interest, and with subsequent annual payments of principal plus accrued interest extending to June 1, 2019; (b) a transfer to GPY of the Company’s 0.5% net smelter royalty (“NSR”) on GPY’s Brewery Creek property and its 1% NSR on GPY’s Sonora Gulch property; and (c) for a period of 18 months, vote in favor of management’s slate of directors for the GPY Board and not exercise its voting rights in regard to any financing(s) of GPY. The renegotiated terms of this Promissory Note are in keeping with the Company’s desire to exit the resource sector by requiring payment in cash rather than in shares of GPY and by transferring these royalties to GPY.

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

Normal course issuer bid

On September 25, 2015, the Company announced that it has initiated a new normal course issuer bid ("NCIB"). Under the new NCIB, the Company intends to bid for up to 265,502 common shares, representing 10% of the 2,655,025 shares forming Till's public float. The board of directors of the Company believes that the current and recent market prices for the Company's common shares do not give full effect to their underlying value and that, accordingly, the purchase of common shares under the NCIB will increase the proportionate share interest of, and be advantageous to, all remaining shareholders. The Company also believes the NCIB purchases will provide increased liquidity to current shareholders who would like to sell their shares. Purchased shares will be returned to treasury and canceled. Purchases subject to the bid will be carried out pursuant to open market transactions through the facilities of the TSXV/Nasdaq by Canaccord Genuity on behalf of Till.

Under a prior NCIB, which commenced on September 23, 2014 and expired on September 23, 2015, Till purchased 183,400 common shares through open market purchases, all of which have been returned to treasury and canceled.

GPY share options

As part of the separation agreement between the Company and Mr. Sheriff, the Company granted Mr. Sheriff two assignable options, each with a term of 18 months, to purchase the balance of the Company’s 11,812,154 GPY shares. The first option is to purchase up to 5,500,000 of the Company’s GPY shares according to a staggered schedule and price as follows: a) if exercised by September 30, 2015, at $0.11 CDN per share, b) if exercised by October 31, 2015, at $0.12 CDN per share, c) if exercised by November 30, 2015, at $0.13 CDN per share, d) if exercised by December 23, 2015, at $0.14 CDN per share, e) if exercised after December 23, 2015 and before March 1, 2017, at $0.15 CDN per share. The second option is to purchase up to 6,312,154 of the Company’s GPY shares at $0.15 CDN per share. The Company can accelerate the expiry of either option to a date 45 days after it gives notice to the holder at any time after the ten-day volume-weighted average price (“VWAP”) of the GPY shares is at or above $0.25 CDN per share. The closing price of GPY share on September 30, 2015 was $0.12 CDN. Thus, the derivative liability associated with the remaining options was immaterial as at September 30, 2015. Through the date of the filing of this Management's Discussion and Analysis, Mr. Sheriff has exercised a total of 1,300,000 GPY share options. The first transaction was completed on September 30, 2015 for 500,000 shares at an exercise price of $0.11 CDN per share and the second transaction was completed on October 30, 2015 for 800,000 shares at an exercise price of $0.12 CDN per share. The Company currently owns approximately 34% of the outstanding shares of GPY.

REVIEW OF INVESTMENTS AND INVESTMENT PERFORMANCE

Investment policies and strategy

The Company’s overall portfolio includes the portfolios of both of its wholly-owned subsidiaries, Omega and RRL. As previously announced, the Company is pursuing the divestiture of its current resource sector investments in the RRL portfolio. Going forward, investments in both portfolios will be principally allocated to one of the following two strategies:

Highly Liquid Investments - Investments in highly liquid securities with a maturity of less than 30 days or that can be converted to cash within 10 days. The percentage of Company investments allocated to highly liquid investments is expected to range between 70% and 100%.

Long-Term Opportunities - Longer-term opportunistic investments where the Company expects to achieve asymmetrical returns and disposition optionality; these may include equity investments, debt financing arrangements, and other structured investments. Holding periods are expected to be one to three years. The percentage of Company investments allocated to long-term opportunities is expected to range between 0% and 30%.

Investments

The Company’s investments at September 30, 2015 (excluding cash of $8,966,401) totaled $24,814,657, and are primarily made up of marketable securities.

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

Investments in securities as of September 30, 2015:

| Government bonds & guaranteed investment certificates | | $ | 19,434,131 | |

| Public companies – natural resource sector | | | 3,030,293 | |

| Public companies – all other sectors | | | 1,323,925 | |

| Private companies – natural resource sector | | | 926,308 | |

| Private companies – all other sectors | | | 100,000 | |

| | | $ | 24,814,657 | |

On September 2, 2015, the Company announced its intent to exit the resource sector and to divest or dispose of its investments in natural resource companies and assets.

Investment performance

For the nine months ended September 30, 2015, total loss on investments, before net investment expenses of $745,398, was $124,577, as summarized in the following table:

| Security | | Realized Gain (Loss) | | Unrealized Gain (Loss) | | Total |

| Equities | | $ | (986,361 | ) | | $ | 379,138 | | | $ | (607,223 | ) |

| Options, warrants and futures | | | (63,789 | ) | | | 418,318 | | | | 354,529 | |

| Bonds | | | (42,579 | ) | | | 10,417 | | | | (32,162 | ) |

| Gold bullion | | | (19,542 | ) | | | - | | | | (19,542 | ) |

| Foreign currencies | | | 132,327 | ) | | | 47,494 | | | | 179,821 | |

| TOTAL | | $ | (979,944 | ) | | $ | 855,367 | | | $ | (124,577 | ) |

The precious metals markets were down in the first three quarters of 2015. The Market Vectors Junior Gold Miners ETF (GDXJ) closed at 23.93 on December 31, 2014, and at 19.59 on September 30, 2015, a decrease of 18.14%. The Market Vectors Gold Miners ETF (GDX) closed at 18.38 on December 31, 2014, and at 13.73 on September 30, 2015, a decrease of 25.3%. In spite of these performances, the Company's core positions (a significant portion of which are in junior mining stocks) gained 12.22% for the nine months ending September 30, 2015; however, the gains from these positions were more than offset by losses in the Company's active trading program.

The Company's active trading program yielded a loss in large part due to the unusual intraday stasis of the market during much of the first three quarters of 2015. The nine month period ended September 30, 2015 has been characterized by exceptionally low intraday volatility, with a daily price range frequently less than 0.5%, a range that is not conducive to active trading. The Company's trading strategy generally has avoided holding overnight positions that have substantially higher risk due to the potential for gaps in price. Thus, the market has provided little opportunity to produce significant profits during this period.

OUTLOOK

The Company's shares began trading on the Nasdaq stock exchange on May 26, 2015. The Company expects that the listing of its shares in the U.S. will broaden its access to capital markets and intends to pursue the issuance of additional share capital in the near term to expand its underwriting capacity, fund purchases of additional insurance and reinsurance contracts, consider acquisitions in the insurance/reinsurance industry, and for general corporate purposes. The Company has entered into an engagement agreement with Taussig Capital Ltd. to raise no less than $50 million in equity capital, which agreement is more fully described herein under Corporate Developments, Significant Transactions, and Factors Affecting Results of Operations. There can be no assurance that the Company and Taussig Capital Ltd. will be successful in raising additional equity capital.

The insurance markets in which the Company operates have historically been cyclical. During periods of excess underwriting capacity, as defined by the availability of capital, competition can result in lower pricing and less favorable policy terms and conditions for insurers and reinsurers. The Company has entered the reinsurance business at a time when the reinsurance capital is at its highest, and, as such, the margins that can be earned on some reinsurance programs are now at low levels. The Company expects to find its own market niche in acquisitions such as Omega and agreements with MSRE to generate underwriting income. Historically, underwriting capacity has been affected by several factors, including industry losses, the impact of catastrophes, changes in legal and regulatory guidelines, new entrants, investment results (including interest rate levels), and the credit ratings and financial strength of competitors. Resource Re anticipates writing new reinsurance premiums to modestly outpace claims paid in an effort to grow the business. The Company realizes that, in the early years, the possibility of “netting” whereby new premiums are used to pay outstanding claims within the same period is unlikely. As such, the Company intends to maintain flexibility in the liquidity of investable assets and/or excess capacity in letters of credit to maintain sufficient available assets to cover claim payments.

On May 15, 2015, the Company acquired Omega Insurance Holdings, Inc for approximately $14.1 million. Omega has a history of profitable operations and the Company expects Omega will continue to generate operating income that will be consolidated with the Company's financial results going forward.

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

The Company's investment strategies will be a key aspect for generating future profitability. The Company has announced its intent to exit the resource sector and to divest or dispose of its investments in natural resource companies and assets. Omega's investment strategy has previously been focused exclusively in Canadian federal and provincial government bonds that historically have provided stable but low returns. Omega expects to make revisions to its investment policy to enhance future investment returns.

The Company's Registration Statement with the United States Securities and Exchange Commission ("SEC") that became effective May 12, 2015 was filed on Form 20-F as a Foreign Private Issuer. The Company expects that its status as a Foreign Private Issuer may change in 2016, and, if the status changes, the Company will begin reporting in accordance with SEC rules and regulations applicable to United States domestic issuers.

SELECTED FINANCIAL INFORMATION

Results of operations for the three months ended September 30, 2015 compared to the three months ended September 30, 2014

The loss for the current 2015 period was $5,710,014 (prior period - loss of $3,608,810). Individual items contributing to this increase in the loss are as follows:

| • | Premiums earned were $901,155 from Omega (prior period - $nil) as a result of the Company acquiring Omega on May 15, 2015. |

| • | As a result of RRL's insurance contracts novation, the Company reversed premium revenue of $5,246,208 (prior period - $nil) and reversed claims and claims adjustment expenses of $5,133,010 (prior period - $nil). |

| • | Net investment loss was $120,339 (prior period - $1,871,408) resulting mostly from an unrealized loss in an investment in a private resource company. Investment losses were mitigated by unrealized gains in public resource company investments and net investment income from Omega. Investment losses from the prior period were primarily a result of a decrease in the market value of core positions during the three months ended September 30, 2014, as well as trading losses in an algorithmic trading system. |

| • | General and administrative expenses decreased by $153,883 to $1,051,826 (prior period - $1,205,709) due to reduced exploration and development activity by the Company's controlled subsidiaries as well as lower legal and professional expenses, partly offset by higher general and administrative expenses since the acquisition of Omega. The prior period higher legal and professional expenses were due principally to the Company's Reorganization activities. |

| • | Staff costs increased by $383,333 to $565,603 (prior period - $182,270) primarily as a result of the payment to Mr. Sheriff pursuant to the separation agreement the Company entered into with Mr. Sheriff on September 2, 2015. |

| • | Mineral property impairment was $3,380,907 (prior period - $nil). The current period impairment was primarily related to the write-down in the Taylor assets owned by the Company's controlled subsidiaries due to the re-measurement as a result of Taylor assets being classified as assets held for sale. There was no impairment to mineral properties during the prior-period. |

| • | Foreign exchange loss increased by $585,131 to $858,428 (prior period - $273,297) as a result of the weakening Canadian dollar for the three months ended September 30, 2015. Till's controlled subsidiaries are Canadian dollar reporting entities. |

| • | The Company reported a current income tax expense of $158,900 in the period related to Omega's Canadian operations. There was no current income tax expense in the prior period. |

Results of operations for the nine months ended September 30, 2015 compared to the ten months ended September 30, 2014

The loss for the current 2015 period was $12,108,786 (prior period - loss of $24,603,988). Individual items contributing to this decrease in the loss are as follows:

| • | Premiums earned were $941,077 from Omega (prior period - $nil) as a result of the Company acquiring Omega on May 15, 2015. |

| • | As a result of RRL's insurance contracts novation, the Company reversed premium revenue of $5,246,208 (prior period - $nil) and reversed claims and claims adjustment expenses of $5,133,010 (prior period - $nil). |

| • | Net investment loss was $869,975 (prior period - income of $915,561) as a result of trading expenses and losses mostly in futures contracts and equities. Active daily trading in S&P 500 and NASDAQ futures contracts resulted in losses in the current period due to abnormally low intraday volatility. Investment losses were mitigated by currency trading gains, mostly between US dollars and Canadian dollars, and net investment income from Omega. Investment gains from the prior period were primarily the result of an increase in the market value of core positions. |

| • | Other income increased by $262,699 to $312,373 (prior period - $49,674) due principally to consulting service revenue of $155,864 from Omega (since the acquisition date of May 15, 2015), other consulting service revenue of $40,870, royalty income of $40,000, and option income of $49,430 in the nine-month period ended September 30, 2015. |

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

| • | General and administrative expenses decreased by $1,107,992 to $3,253,803 (prior period - $4,361,795) due to reduced exploration and development activity by the Company's controlled subsidiaries as well as lower legal and professional expenses, partly offset by higher general and administrative expenses since the acquisition of Omega. The prior period higher legal and professional expenses were due principally to the Company's Reorganization activities. |

| • | Staff costs decreased by $726,685 to $786,550 (prior period - $1,513,235) primarily as a result of reduced exploration and development activities by the Company's controlled subsidiaries and a higher reclassification of investment-related staff costs to investment expenses of $444,855, partly offset by the payment to Mr. Sheriff according to the separation agreement the Company entered into with Mr. Sheriff on September 2, 2015. |

| • | Stock-based compensation increased by $219,971 to $453,642 (prior period - $233,671) due to the current year expense of options issued ($223,350), as well as the issuance of 171,000 warrants to MSRE ($230,302). |

| • | Mineral property impairments decreased by $13,712,695 to $4,434,158 (prior period - $18,146,853). The current period impairment was primarily related to the writedown in the Taylor assets owned by the Company's controlled subsidiary due to the re-measurement as a result of Taylor assets being classified as assets held for sale. In the prior comparative period, impairment expenses were due to impairments on property transferred from SPD and Northern Tiger Resources Inc. as part of the Reorganization; SPD also recorded writedowns and sold its interests in several properties due to poor exploration results and management's decision to cease exploration on those properties. |

| • | Write-off of property, plant and equipment decreased by $1,696,379 to $111,245 (prior period - $1,807,624). The prior period write-off was a result of impairment of assets as part of the Reorganization at SPD. |

| • | Foreign exchange loss increased by $2,137,008 to $2,514,159 (prior period - $377,151) as a result of the weakening Canadian dollar compared to the US dollar for the nine months ended September 30, 2015. Till's controlled subsidiaries are Canadian dollar reporting entities. |

Cash flows for the nine months ended September 30, 2015 compared to the ten months ended September 30, 2014

Cash flows from operating activities were $736,086 (prior period - outflow of $5,981,591). The difference was primarily due to receipt of cash in the current period for reinsurance contract receivable of $6,087,262 and lower loss adjusted for non-cash items of $992,163 due primarily to lower general and administrative expenses and lower staff costs.

Cash flows from investing activities decreased by $21,248,102 to outflows of $8,754,253 (prior period - inflows of $12,493,849) due primarily to the Omega acquisition of $12,326,571 (net of cash received) in the current period; in the prior comparative period, the Company received proceeds from sales of mineral properties and royalties of $13,109,826; partly offset by the net sales of investment of $3,870,290 in the current period compared to the net purchases of investment of $263,074 in the prior period.

For the prior ten-month period, cash flows from financing activities were $9,260,817, primarily as a result of cash received for the issuance of Company's shares as part of the Reorganization.

Summary of quarterly results

| | 2015 | 2014* | Fiscal year ended

February 28, 2014 |

| | Q3 | Q2 | Q1 | Q3 | Q2 | Q1 | Q4 | Q3 |

| Net revenues | $ | (4,384,526 | ) | $ | (217,466 | ) | $ | (260,741 | ) | $ | 6,122,643 | | $ | (1,854,131 | ) | $ | 2,641,363 | | $ | — | | $ | — | |

| Net income (loss) | (5,710,014 | ) | (3,090,770 | ) | (3,308,000 | ) | (3,808,466 | ) | (3,608,810 | ) | 1,671,833 | | (22,784,172 | ) | 11,625,631 | |

Net income (loss) for Till

shareholders | (4,507,516 | ) | (3,094,872 | ) | (2,907,332 | ) | (3,307,937 | ) | (3,456,918 | ) | 1,816,304 | | (22,784,172 | ) | 11,625,631 | |

| | | | | | | | | |

Basic and diluted Income (loss) per share of Till | $(1.31) | $(0.90) | $(0.81) | $(1.07) | $(0.96) | $0.63 | $(12.64) | $6.44 |

*In 2014, the Company changed its year end from February 28 to December 31. As a result, the Company's 2014 reporting period consists of ten months beginning March 1, 2014 and ending December 31, 2014, and the Company's prior-year first quarter reporting period consists of the four months ended June 30, 2014.

Prior to 2014, AMB was involved in mining exploration and evaluation activities and previously had not generated operating revenue. It incurred administrative and other overhead expenses to support its exploration and evaluation activities, and, as such, had net losses on a quarterly basis.

In the third quarter of the fiscal year ended February 28, 2014, AMB received an option payment and sales proceeds related to the sale of 18 royalty interests for approximately $11 million and $22 million, respectively, resulting in net income for the quarter.

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

In the fourth quarter of the fiscal year ended February 28, 2014, AMB incurred impairment losses of $17 million primarily related to its Yukon properties, including the Brewery Creek and Gold Dome projects.

In the first quarter of 2014 (four months ended June 30, 2014), following the Company’s Reorganization,Till had net investment revenue of $2.6 million offset by $3.3 million in operating expenses for a net loss before tax of $0.7 million. The Company also recognized a reversal of a prior tax liability of $2.4 million that resulted in net income of $1.7 million.

In the second quarter of 2014 (three months ended September 30, 2014), the Company incurred a net investment loss of $1.8 million and operating expenses of $1.8 million, resulting in a loss of $3.6 million.

In the third quarter of 2014 (three months ended December 31, 2014), net revenue was $6.1 million as a result of the Company's entry into the reinsurance business, and a loss of $3.8 million primarily as a result of impairment charges on mineral interests of the Company's controlled subsidiaries.

In the first quarter of 2015, the Company incurred a net investment loss of $0.3 million and operating expenses of $3.0 million, resulting in a loss of $3.3 million.

In the second quarter of 2015, the Company incurred a net investment loss of $0.3 million, premiums earned and other income of $0.1 million, and operating expenses of $2.9 million, resulting in a loss of $3.1 million.

In the third quarter of 2015, the Company incurred premiums earned and other income of $1.0 million, a net investment loss of $0.1 million, a reversal of premiums earned of $5.2 million, a reversal of claims and claims adjustment expenses of $5.1 million, mineral property impairment of $3.4 million, and operating expenses of $3.1 million, resulting in a loss of $5.7 million. The reversal of premiums earned and claims and claims adjustment expenses are a result of the novation of the Company's reinsurance contracts.

Financial position

The decrease in cash of $8,068,050 to $8,966,401 during the nine months ended September 30, 2015 (December 31, 2014 - $17,034,451) is primarily due to the payment for the Omega acquisition of $12,326,571 (net of cash received), partly offset by the collection of $6,087,262 of the reinsurance contract receivable from the prior period.

Investments increased by $15,523,317 to $24,814,657 during the first three quarters of 2015 (December 31, 2014 - $9,291,340) due primarily to the acquisition of Omega in May 2015 and the inclusion of Omega's investments in the Company's investments at September 30, 2015, partly offset by trading losses during the period, changes in the fair market value of investments, and the net sales of investments during the 2015 period resulting in a decrease in investments with a corresponding increase in cash and cash equivalents, less net realized losses.

Assets held for sale were $6,257,066 (December 31, 2014 - $nil) as a result of certain assets at the Company’s controlled subsidiary SPD being classified as assets held for sale during the current period.

Investment in associate was $1,012,273 as at September 30, 2015 (December 31, 2014 - $nil) as a result of the Company no longer having a controlling interest of GPY on September 30, 2015 and measuring the remaining shares of GPY at fair value as investment in associate as at September 30, 2015.

There were no reinsurance contract receivables at September 30, 2015 (December 31, 2014 - $6,087,262) due to payment of the prior period balance in the current period, and no new contracts written in the current period. RRL's reinsurance contracts were fully novated during the current period.

At September 30, 2015, premiums and ceded claims receivable were $8,564,786 (December 31, 2014 - $nil), unpaid claims ceded were $10,863,927 (December 31, 2014 - $nil), unearned premiums ceded were $1,418,126 (December 31, 2014 - $nil), deferred policy acquisition costs were $427,049 (December 31, 2014 - $nil), claims and ceded premiums payable were $8,436,060 (December 31, 2014 - $nil), unearned premiums were $1,631,864 (December 31, 2014 - $nil), and unearned commissions were $399,711 (December 31, 2014 - $nil). These increases are all attributable to the Omega acquisition.

Insurance contract liabilities increased by $17,961,397 to $24,733,020 at September 30, 2015 (December 31, 2014 - $6,771,623) due primarily to including Omega's insurance contract liabilities of $19,508,926 from the Omega acquisition in May 2015.

LIQUIDITY AND CAPITAL RESOURCES

At September 30, 2015, the Company had working capital of $22,421,900 including cash of $8,966,401, as compared to a working capital of $25,035,568, including cash of $17,034,451 at December 31, 2014. Also included in working capital at September 30, 2015 were investments with a market value of $24,814,657 (December 31, 2014 - $9,291,340). The Company has no meaningful long-term debt.

The Company expects to invest in insurance, reinsurance, and business acquisitions that will require additional capital. The Company does not presently anticipate that it will incur any material indebtedness in the ordinary course of business other than temporary borrowings directly related to the management of the investment portfolio.

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

To provide the Company with timely access to public capital markets should it require additional capital for working capital, capital expenditures, acquisitions, or other general corporate purposes, the Company completed a U.S. exchange listing to broaden its access to capital markets. The Company's Registration Statement, filed with the United States Securities and Exchange Commission ("SEC") on Form 20-F as a Foreign Private Issuer, became effective on May 12, 2015 and the Company's shares commenced trading on Nasdaq on May 26, 2015. In July 2015, the Company entered into an engagement agreement with Taussig Capital Ltd. to raise no less than $50 million in equity capital, which agreement is more fully described herein under Corporate Developments, Significant Transactions, and Factors Affecting Results of Operations.

OUTSTANDING SHARE DATA

At September 30, 2015, Till had 3,429,284 issued and outstanding common shares, and 247,610 outstanding stock options and 179,500 outstanding warrants.

OFF BALANCE SHEET ARRANGEMENTS

At September 30, 2015, the Company had no material off-balance sheet arrangements.

RELATED PARTY TRANSACTIONS

The Company is party to service agreements with SPD whereby the Company provides accounting, corporate communications, and other management services on a cost-plus recovery basis, and was party to service agreements with GPY whereby the Company provided similar services as to SPD on a cost-plus recovery basis. The agreements with GPY were terminated on July 31, 2015. During the three months ended September 30, 2015, the Company charged SPD a total of $53,243 and GPY a total of $18,036 for those services. During the nine months ended September 30, 2015, the Company charged SPD a total of $192,836 and GPY a total of $79,376 for those services.

On August 28, 2015, the Company signed a Promissory Note (the "Note") issued by SPD to the Company. The principal on the note is limited to $275,000, which amount represents the maximum amount SPD may borrow, but is not obligated to do so. The annual interest rate on any balance on the Note is 12% and, in addition to other repayment provisions, the note must be repaid in its entirety by December 31, 2015. As of September 30, 2015, $235,000 had been loaned to SPD under the Note agreement.

CRITICAL ACCOUNTING ESTIMATES

The preparation of consolidated financial statements in accordance with IFRS requires the use of certain critical accounting estimates and judgments. It also requires management to exercise judgment in applying the Company’s accounting policies. Those judgments and estimates are based on management’s knowledge of the relevant facts and circumstances, input from certain contractors, taking into account previous experience, but actual results may differ from the amounts reported in the financial statements.

Areas of estimation and judgment that have the most significant effect on the amounts recognized in the financial statements include:

Valuation of insurance and reinsurance claim liabilities and reinsurance assets

For insurance and reinsurance contract liabilities and reinsurance assets, estimates have to be made for both the expected ultimate cost of claims reported at the reporting date and for the expected ultimate cost of claims incurred but not reported ("IBNR") at the reporting date. A significant amount of time may pass before the ultimate claims cost can be established with certainty.

The ultimate cost of outstanding claims is traditionally estimated, in part, by using a range of standard actuarial claims projection techniques. The main assumption underlying those techniques is that a Company's past claims development experience can be used to project future claims development, and hence ultimate claims costs. Additional qualitative judgment is used to assess the extent to that past trends may not apply in the future to arrive at the estimated ultimate cost of claims.

The carrying value of insurance and reinsurance contract liabilities at September 30, 2015 was $26,764,595 (2014 - $6,771,623).

| | | September 30, 2015 | | December 31, 2014 |

| Provision for outstanding claims | | $ | 24,733,020 | | | $ | 6,771,623 | |

| Unearned premiums | | | 1,631,864 | | | | - | |

| Unearned commissions | | | 399,711 | | | | - | |

| Total insurance contract liabilities | | $ | 26,764,595 | | | $ | 6,771,623 | |

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

The carrying value of the reinsurance contract assets at September 30, 2015 was $12,709,102 (2014 - $0).

| | | September 30, 2015 | | December 31, 2014 |

| Unpaid claims ceded | | $ | 10,863,927 | | | $ | - | |

| Unearned premiums ceded | | | 1,418,126 | | | | - | |

| Deferred policy acquisition costs | | | 427,049 | | | | - | |

| Total insurance contract assets | | $ | 12,709,102 | | | $ | - | |

Impairment of tangible and intangible assets

The Company and its controlled subsidiaries each assess at each reporting period, in accordance with IAS 36, "Impairment of Assets"("IAS 36"), whether there is or is not an indication that an asset or group of assets may be impaired. When impairment indicators exist, the Company and its controlled subsidiaries each estimate the recoverable amount of the asset and compare it to the asset’s carrying amount. The recoverable amount is the higher of the fair value less cost to sell and the asset’s value in use. For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows (cash-generating units). If the carrying value exceeds the recoverable amount, an impairment loss is reported in the statement of loss for the period.

The Company and its controlled subsidiaries each assess mineral resource assets in accordance with IFRS 6, "Exploration for and Evaluation of Mineral Resources" ("IFRS 6"), that modifies the requirements in IAS 36 with respect to the indications of impairment; and the level at which impairment is tested. IFRS 6 applies only to exploration and evaluation (“E&E”) expenditures that are defined as expenditures incurred by an entity in connection with the exploration for and evaluation of mineral resources before the technical feasibility and commercial viability of extracting a mineral resource are demonstrable. IFRS 6 does not apply to expenditures incurred:

| • | Before the exploration for and evaluation of mineral resources, such as expenditures incurred before an entity has obtained the legal rights to explore a specific area. |

| • | After the technical feasibility and commercial viability of extracting a mineral resource are demonstrable. |

IFRS 6 requires E&E assets to be assessed for impairment when facts and circumstances suggest that the carrying amount of an E&E asset may exceed its recoverable amount. According to IFRS 6, one or more of the following facts and circumstances indicate that an entity should test E&E assets for impairment:

| • | The period for which the entity has the right to explore in the specific area has expired during the period or will expire in the near future, and is not expected to be renewed. |

| • | Substantive expenditure on further exploration for and evaluation of mineral resources in the specific area is neither budgeted nor planned. |

| • | Exploration for and evaluation of mineral resources in the specific area have not led to the discovery of commercially viable quantities of mineral resources and the entity has decided to discontinue such activities in the specific area. |

| • | Sufficient data exist to indicate that, although a development in the specific area is likely to proceed, the carrying amount of the E&E asset is unlikely to be recovered in full from successful development or by sale. |

Where indications of impairment were evident, the following key assumptions, factors, and methods in computing estimates for purposes of determining asset impairments were used:

| • | Independent evaluation of fixed asset values. |

| • | Updated metallurgical studies completed for mineral properties and royalties. |

| • | Net present value calculations related to projected production costs, commodity prices, discount rates, and other items to determine mineral property values based on future cash flows. |

| • | Estimated fair value of proceeds to be received on disposal. |

Business combinations

The Company accounts for business combinations using the guidelines specified in IFRS 3, "Business Combinations" ("IFRS 3"). The acquisition method is used in accounting for business combinations. The consideration transferred by the Company to obtain ownership of the assets is calculated as the sum of the acquisition-date fair values of assets transferred, liabilities incurred, and the equity interests issued by the Company, which amounts include the fair value of any asset or liability attributable to a contingent consideration arrangement. Acquisition costs are expensed as incurred. The Company recognized the identifiable assets acquired and liabilities assumed in a business combination, regardless of whether they have been previously recognized in the acquiree’s financial statements prior to the acquisition. Assets acquired and liabilities assumed are generally measured at their acquisition-date fair values.

The Company has not completed the process of determining the fair value of its losses and loss adjustment expense reserves acquired in the acquisition of Omega pursuant to IFRS 3. The valuation will be completed within the measurement period, which period cannot exceed 12 months from the acquisition date. As a result, the fair value reported is a provisional estimate and may be subject to adjustment. Once completed, any adjustment resulting from the valuations may impact the individual amounts reported for assets acquired and liabilities assumed.

Pro forma financial information

In Note 3 to the September 30, 2015 interim condensed consolidated financial statements, the Company presented pro forma financial information related to the Omega acquisition in accordance with IFRS 3. The unaudited pro forma financial information represents the combined results of the Company's operations as if the Omega acquisition had occurred at the beginning of the periods presented. The unaudited pro forma financial information was presented for informational purposes only and is not indicative of the results of operations that would have occurred if the acquisition had taken place at the beginning of the periods presented, nor is it indicative of future operating results.

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

Share-based compensation

The Company grants share-based awards in the form of share options in exchange for the services from certain employees, officers, and directors. The share options are equity-settled awards. The Company determines the fair value of the awards on the date of grant. This fair value is charged to loss using a graded vesting attribution method over the vesting period of the options, with a corresponding credit to contributed surplus. When the share options are exercised, the applicable amounts of contributed surplus are transferred to share capital. At the end of the reporting period, the Company updates its estimate of the number of awards that are expected to vest and adjusts the total expense to be recognized over the vesting period.

Share purchase warrants issued are accounted for using the fair value method. Under this method, the fair value of share purchase warrants is determined using the Black-Scholes valuation model. Upon exercise of a share purchase warrant, consideration paid, together with the amount previously recognized in reserves, is reported as an increase to share capital.

The key assumptions relevant to the calculation of the fair value of stock based compensation are the volatility of the share price (based on historic volatility), the expected life of the stock option (which is based on the history of stock option exercises) and the forfeiture rate of stock options (based on the history of forfeitures).

Valuation of mineral interests

Historically, the Company, from time to time, through its controlled subsidiaries, has acquired exploration and development properties. When a number of properties are acquired in a portfolio, the Company must make a determination of the fair value attributable to each of the properties within the total portfolio. When the Company conducts further exploration on acquired properties, it may determine that certain of the properties do not support the fair values applied at the time of acquisition. If such a determination is made, the property is written down, which could have a material effect on the Company's financial position and results of operations.

Income taxes

Deferred tax assets and liabilities are determined based on differences between the financial statement carrying values of assets and liabilities and their respective income tax bases (“temporary differences”), and losses carried forward.

The determination of the ability of the Company to utilize tax loss carry-forwards to offset deferred tax liabilities requires management to exercise judgment and make certain assumptions about the future performance of the Company. Management is required to assess whether it is “probable” that the Company will benefit from those prior losses and other deferred tax assets. Changes in economic conditions, metal prices, and other factors could result in revisions to the estimates of the potential benefits to be realized or the timing of utilizing the losses.

Fair value measurement of Level 3 investments

Level 3 investments are assets or liabilities that cannot be measured or can only be partially measured using observable market inputs. These include private and unlisted equity securities where observable inputs are not available. Fair values are derived based on unobserved inputs such as management’s assumptions developed from available information using the services of an investment adviser.

CHANGES TO ACCOUNTING STANDARDS

New standards not yet adopted

The Company is currently evaluating the impact of the following pronouncements and has not yet determined the impact on its consolidated financial statements:

IFRS 9, "Financial Instruments" ("IFRS 9"), addresses the classification, measurement, and recognition of financial assets and financial liabilities. The IASB has previously issued versions of IFRS 9 that introduced new classification and measurement requirements (in 2009 and 2010) and a new hedge accounting model (in 2013). The July 2014 publication of IFRS 9 is the complete version of the Standard, replacing earlier versions of IFRS 9 and superseding the guidance relating to the classification and measurement of financial instruments in IAS 39, "Financial Instruments: Recognition and Measurement" (“IAS 39”). Additionally, IFRS 9 introduces a new three-stage expected credit loss model for calculating impairment for financial assets, and some modifications related to hedge accounting. This final version of IFRS 9 will become effective for annual periods beginning on or after January 1, 2018, with early adoption permitted.

IFRS 15,“Revenue from Contracts with Customers”(“IFRS 15”), replaces IAS 11, “Construction Contracts”, IAS 18, “Revenue”, IFRIC 13, “Customer Loyalty Programmes”, IFRIC 15, “Agreements for the Construction of Real Estate”, IFRIC 18,“Transfer of Assets From Customers” and Standard Interpretations Committee (“SIC”) 31, “Revenue - Barter Transaction Involving Advertising Services”. IFRS 15 establishes principles for reporting the nature, amount, timing, and uncertainty of revenue and cash flows arising from an entity’s contracts with customers. This revenue standard introduces a single, principles-based, five-step model for the recognition of revenue when control of a good or service is transferred to the customer and requires the reporting entity to identify the contract(s) with the customer, identify the performance obligations in the contract, determine the transaction price, allocate the transaction price and recognize revenue when a performance obligation is satisfied. IFRS 15 is intended to enhance disclosures about revenue to help investors better understand the nature, amount, timing, and uncertainty of revenue and cash flows from contracts with customers and to improve the comparability of revenue from contracts with customers. This standard will become effective for annual periods beginning on or after January 1, 2018, with early adoption permitted.

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

RISKS

The Company is subject to a number of risks, including the risks summarized below. The risks and uncertainties summarized below are those believed to be material, but they may not be the only ones faced by the Company. If any of these risks, or any other risks and uncertainties that have not yet been identified by the Company or that the Company currently considers not to be material, actually occur or become material risks, the business, prospects, financial condition, results of operations, and cash flows of the Company could be materially and adversely affected.

Insurance risk

The Company principally issues general insurance and reinsurance contracts in the personal property, commercial property, and liability lines of business. Under these general insurance and reinsurance contracts, the Company is exposed to certain risks defined in the general insurance and reinsurance contracts.

In addition to general insurance contracts, the Company also assumes portfolios of existing claims from other insurers through assumption reinsurance transactions. These portfolios of claims could be from any line of business that the transferring insurer wrote in the past. Under these assumption reinsurance transactions, the Company is exposed to certain risks defined in the underlying insurance contracts that were originally written by the transferring insurer.

The principal risk the Company faces under both the general insurance and reinsurance contracts and assumption reinsurance contracts is that the actual claims and benefit payments, or the timing thereof, differs from the expectations used to price the general insurance and reinsurance contracts or assumption reinsurance transactions. That uncertainty results from the frequency of claims, severity of claims, emergence of unknown claims, actual benefits paid, and subsequent development of long-term claims. For long-term claims that may take years to settle, the Company is also exposed to inflation risk. The objective of the Company is to ensure that sufficient reserves are available to cover these exposures.

Risk exposure is mitigated through the use of various claim review strategies and guidelines to reduce the risk exposure for the Company. The Company purchases reinsurance as part of its risk mitigation strategies. Reinsurance is placed on both a proportional and non-proportional basis. The use of proportional and non-proportional reinsurance varies by line of business.

Liquidity risk

Liquidity risk is the risk that the Company is unable to meet its financial obligations as they come due. The Company manages this risk by management of its working capital to assess that the estimated expenditures will not exceed share capital and debt financings, or proceeds from property sales or option exercises. Omega is exposed to liquidity risk to the extent that the sale of a fixed income security prior to its maturity is required to provide liquidity to satisfy policyholder and other cash outflows. To mitigate this risk, Omega has policies to ensure that assets and liabilities are broadly matched in terms of their duration.

At September 30, 2015, the Company had a working capital balance of $22,421,900.

Credit risk

Credit risk is the risk of loss associated with a counterparty’s inability to fulfill its payment obligations. The Company's credit risk is primarily attributable to cash and cash equivalents, investments, balances receivable from policyholders and reinsurers, and reclamation bonds. To mitigate the credit risk in investment in debt securities, Omega has policies in place to limit and monitor its exposure to individual issuers and classes of issuers of debt securities that do not carry the guarantee of a national or Canadian provincial government. The Company's credit exposure to any one individual policyholder is not material. The Company's policies are distributed by brokers and agents who manage cash collection on its behalf and the Company monitors its exposure to brokers and agents. The Company has policies in place that limit its exposure to individual reinsurers and conducts regular review processes to assess the creditworthiness of reinsurers with whom it transacts business.

Reclamation bonds consist of term deposits and guaranteed investment certificates that have been invested with reputable financial institutions from which management believes the risk of loss to be minimal.

Historically cyclical business

The insurance and reinsurance business historically has been a cyclical industry characterized by periods of intense price competition due to excessive underwriting capacity, as well as periods when shortages of capacity permitted an increase in pricing and, thus, more favorable premium levels. An increase in premium levels is often, over time, offset by an increasing supply of insurance and reinsurance capacity, either from capital provided by new entrants or by additional capital committed by existing insurers or reinsurers that may cause prices to decrease. In addition, changes in the frequency and severity of losses suffered by insureds and insurers may affect the cycles of the insurance and reinsurance business significantly. Any of these factors could lead to a significant reduction in premium rates, less favorable policy terms, and fewer opportunities to underwrite insurance risks, which could have a material adverse effect on the Company’s results of operations and cash flows.

Inability to accurately assess underwriting risk

The Company’s underwriting success is dependent on its ability to accurately assess the risks associated with the business on which the risk is retained. For the RRL business, the Company relies on the experience MSRE's of underwriting staff in assessing these risks for reinsurance contracts. If the Company fails to accurately assess the risks it retains, the Company may fail to establish appropriate premium rates which, in turn, could reduce its net earnings.

Till Capital Ltd.

Management's Discussion and Analysis

For the nine months ended September 30, 2015 and ten months ended September 30, 2014

Changes in regulations and regulatory actions

The Company's insurance businesses are subject to regulation in the jurisdictions in which the Company operates. Such regulations may relate to, among other things, the types of business that can be written, the premium rates that can be charged, the level of capital that must be maintained, and restrictions on the types and size of investments that can be made. Accordingly, changes in regulations related to these or other matters or regulatory actions that impose restrictions on the Company's insurance companies may have a material adverse effect on the Company’s results of operations and cash flows.

The Company may be unsuccessful in competing against larger or more well-established businesses

The Company faces competition from other specialty insurance companies, standard insurance companies and underwriting agencies, as well as from diversified financial services companies that are larger than the Company and that have greater financial, marketing, and other resources than the Company does. Some of these competitors also have more experience and market recognition than the Company does. Furthermore, it may be difficult or prohibitively expensive for the Company to implement technology systems and processes that are competitive with the systems and processes of these larger companies. The Company cannot assure that it will maintain its current competitive position in the markets in which it operates, or that it will be able to expand its operations into new markets; if the Company fails to do so, its results of operations and cash flows could be materially adversely affected.

The Company invests a significant amount of its assets in securities that have experienced market fluctuations