UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

[ ] REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year endedDecember 31, 2015

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________________to ____________________

OR

[ ] SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number: 000-55324

Till Capital Ltd.

(Exact name of Registrant as specified in its charter)

Bermuda

(Jurisdiction of incorporation or organization)

Continental Building

25 Church Street

Hamilton, HM12, Bermuda

(Address of principal executive offices)

Brian P. Lupien

Continental Building

25 Church Street

Hamilton, HM12, Bermuda

(208) 635-5415, (208) 635-5465 Fax

(Name, Telephone, E-Mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:None

| Title of each class | | Name of each exchange on which registered |

| Restricted voting shares, par value $0.001 | | The NASDAQ Capital Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act:None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:3,429,284 restricted voting shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [ ] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See the definition of “accelerated filer” and “large accelerated filer” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] | Non-accelerated filer [X] |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP [ ] | International Financial Reporting Standards as issued By the International Accounting Standards Board [X] | Other [ ] |

| | | |

If “Other” has been checked in response to previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 [ ] Item 18 [ ]

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [X]

TABLE OF CONTENTS

EXPLANATORY NOTE

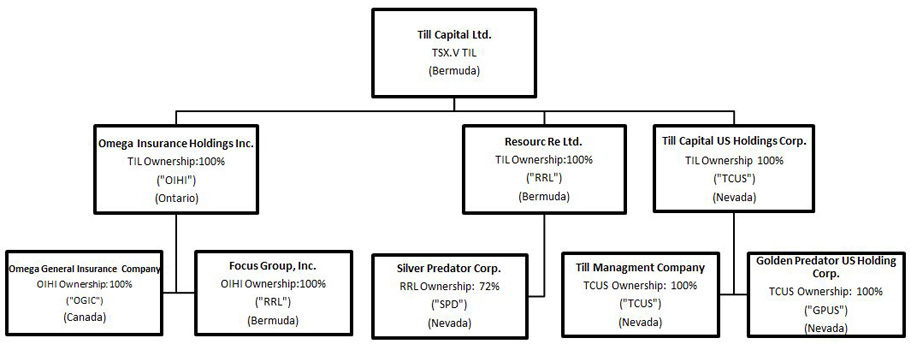

On April 17, 2014, Till Capital Ltd. (the “Company,” “Till,” “we,” “us” or “our”) acquired Americas Bullion Royalty Corp. (“AMB”) in a reverse takeover by way of a plan of arrangement (the “Arrangement”) under the British Columbia Business Corporations Act (the “BCBCA”) pursuant to the Arrangement Agreement dated as of February 18, 2014 between AMB and Resource Holdings Ltd. Pursuant to the International Financial Reporting Standards, as issued by the International Accounting Standards Board (“IFRS”), AMB was the acquirer in the Arrangement. Accordingly, the financial statements and disclosures related thereto contained in this Annual Report on Form 20-F reflect AMB as the acquirer.

Following completion of the Arrangement, we began to transition our business to primarily conduct reinsurance business through Resource Re Ltd. (“RRL”), our wholly-owned subsidiary. In support of this transition, through the Arrangement, we acquired an investment portfolio of cash, marketable securities and illiquid securities from Kudu Partners L.P. (“Kudu”). Before completion of the Arrangement, AMB was an exploration and development junior natural resource and mining company with royalty and exploration property holdings and the Company was an exempted holding company with no operations.

On May 15, 2015, Till acquired all of the issued and outstanding shares of Omega Insurance Holdings, Inc. (“Omega”), a privately held insurance provider based in Toronto, Canada, including its subsidiaries, Omega General Insurance Company (a fully licensed insurance company) and Focus Group, Inc. Omega’s mission is to offer secure, innovative, and customized solutions for insurers/reinsurers exiting the market and organizations with unique insurance needs in a cost effective manner. Omega’s expertise in both the Canadian run-off phase and the Canadian start-up phase for a foreign insurance company gives Omega a strategic advantage in its two main target markets:

| · | To provide those insurers wishing to access the Canadian market an ability to do so in an efficient manner through fronting arrangements and other means. |

| · | To provide those insurers wishing to exit Canada, through a dedicated company with experience in handling run-off business, an ability to facilitate such an exit so that their financial, legal, and moral obligations are met on a continuing basis, while being able to repatriate surplus capital in a more timely fashion. |

CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS

This Annual Report contains "forward-looking statements" within the meaning of theUnited States Private Securities Litigation Reform Act of 1995, as amended, that are based on expectations, estimates and projections as at the date of this Annual Report. These forward-looking statements include, but are not limited to, statements and information concerning: the Arrangement; the potential benefits of the Arrangement; statements relating to the business and future activities of, and developments related to the Company after the date of this Annual Report; the Company’s market position and future financial or operating performance; and goals; strategies; future growth; and other events or conditions that may occur in the future.

Any statements that involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often but not always using phrases such as "expects" or "does not expect", "is expected", "anticipates" or "does not anticipate", "plans", "budget", "scheduled", "forecasts", "estimates", "believes" or "intends" or variations of such words and phrases or stating that certain actions, events or results "may", "could", "would", "might" or "will" be taken to occur or be achieved) are not statements of historical fact and may be forward- looking statements and are intended to identify forward-looking statements, which include statements relating to, among other things, our ability to successfully compete in the market.

These forward-looking statements are based on the beliefs of our management, as well as on assumptions which such management believes to be reasonable, based on information currently available at the time such statements were made. However, there can be no assurance that forward-looking statements will prove to be accurate. Such assumptions and factors include, among other things, general business and economic conditions; that the anticipated benefits of the Arrangement will be achieved; market competition; currency exchange rates, tax benefits and tax rates.

By their nature, forward-looking statements are based on assumptions and involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Forward-looking statements are subject to a variety of risks, uncertainties and other factors which could cause actual events or results to differ from those expressed or implied by the forward-looking statements, including, without limitation: general business, economic, competitive, political, regulatory and social uncertainties; mineral price volatility; risks related to competition; risks related to factors beyond our control; risks and uncertainties associated with the mining industry; risks related to our lack of an operating history; risks related to our investment portfolio not being widely diversified; risks related to the cyclical nature of the reinsurance industry; risks related to our ability to structure our investments in relation to our anticipated liabilities under reinsurance and insurance contracts; risks related third party rating agencies assessments of our reinsurance business; dependence on key management, employees, consultants, and skilled personnel; the global economic climate; exchange rate fluctuations; the execution of strategic growth plans; dilution; market reaction to the Arrangement; risks related to the integration of AMB's and our operations; insurance risks; and litigation.

This list is not exhaustive of the factors that may affect any of our forward-looking statements. Forward-looking statements are statements about the future and are inherently uncertain. Actual results could differ materially from those projected in the forward-looking statements as a result of the matters set out in this Annual Report generally and certain economic and business factors, some of which may be beyond our control. Some of the important risks and uncertainties that could affect forward-looking statements are described further under the heading "Risk Factors" in this Annual Report. We do not intend, and do not assume any obligation, to update any forward-looking statements, other than as required by applicable law. For all of these reasons, you should not place undue reliance on forward-looking statements.

NOTE REGARDING DIFFERENCES IN REPORTING PRACTICES

The financial statements included in this Annual Report have been prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board, which differ from United States generally accepted accounting principles in certain material respects, and thus they may not be comparable to financial statements of U.S. companies.

FINANCIAL INFORMATION AND EXCHANGE RATES

In this Annual Report, unless otherwise specified, all dollar amounts are expressed in U.S. Dollars (“US$” or “$”). The following table sets forth the rate of exchange for the Canadian Dollar (“Cdn”) at the end of each month for the previous six months and at the end of the five most recent fiscal years, the average rates for each period, the high and low exchange rates for these periods and the exchange rate as of the last day of these periods. For purposes of this table, the exchange rate means the Bank of Canada noon rate. The table sets forth the number of Canadian Dollars required to buy one U.S. dollar. The average exchange rate means the average of the exchange rates on the last day of each month during the period.

| Period | | Average | | High | | Low | | Close |

| Year Ended December 31, 2015 | | $ | 1.2785 | | | $ | 1.3990 | | | $ | 1.1728 | | | $ | 1.3870 | |

| Ten Months Ended December 31, 2014 | | $ | 1.1054 | | | $ | 1.1656 | | | $ | 1.0639 | | | $ | 1.1627 | |

| Year Ended February 28, 2014 | | $ | 1.0461 | | | $ | 1.1171 | | | $ | 1.0023 | | | $ | 1.1133 | |

| Year Ended February 28, 2013 | | $ | 0.9988 | | | $ | 1.0418 | | | $ | 0.9710 | | | $ | 1.0285 | |

| Year Ended February 29, 2012 | | $ | 0.9914 | | | $ | 1.0604 | | | $ | 0.9449 | | | $ | 0.9886 | |

| Year Ended February 28, 2011 | | $ | 1.0205 | | | $ | 1.0778 | | | $ | 0.9739 | | | $ | 0.9739 | |

| April 2016 | | | | | | $ | 1.3136 | | | $ | 1.2534 | | | $ | 1.2554 | |

| March 2016 | | | | | | $ | 1.3468 | | | $ | 1.2962 | | | $ | 1.2971 | |

| February 2016 | | | | | | $ | 1.4040 | | | $ | 1.3523 | | | $ | 1.3523 | |

| January, 2016 | | | | | | $ | 1.4589 | | | $ | 1.3969 | | | $ | 1.4080 | |

| December 2015 | | | | | | $ | 1.3980 | | | $ | 1.3360 | | | $ | 1.3840 | |

| November 2015 | | | | | | $ | 1.3360 | | | $ | 1.3095 | | | $ | 1.3333 | |

On May 10, 2016, the exchange rate was Cdn$1.2959 to US$1.

PART I

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| A. | Selected Financial Data |

The following tables summarize selected financial data of the Company for the year ended December 31, 2015, for the ten months ended December 31, 2014 and for the years ended February 28, 2014, February 28, 2013 and February 29, 2012. The information in the tables was extracted from the detailed financial statements and related notes which were prepared in accordance with IFRS and should be read in conjunction with such financial statements and with the information appearing under the heading,“Item 5. Operating and Financial Review and Prospects.”

| | | Till Capital Ltd. | | Americas Bullion Royalty Corp. |

| | | | | | | Year Ended |

| | | Year | | Ten Months | | | | | | |

| | | Ended | | Ended | | | | | | |

| | | December 31, | | December 31, | | February 28, | | February 28, | | February 29, |

| Consolidated Statements of Loss and | | 2015 | | 2014(1) | | 2014 | | 2013 | | 2012 |

| Comprehensive Loss | | (US$) | | (US$) | | (US$) | | (US$) | | (US$) |

| Net Investment Income | | | (1,165,612 | ) | | | 605,989 | | | | (4,343 | ) | | | - | | | | - | |

| Expenses | | | (9,624,185 | ) | | | (15,277,229 | ) | | | (18,908,387 | ) | | | (49,698,707 | ) | | | (9,732,593 | ) |

| Other items | | | - | | | | - | | | | - | | | | (7,161,633 | ) | | | (1,243,553 | ) |

| Loss before income taxes | | | (15,610,735 | ) | | | (8,192,249 | ) | | | (18,894,952 | ) | | | (56,860,340 | ) | | | (10,976,146 | ) |

| Net loss attributable to shareholders of Till Capital Ltd | | | (13,988,085 | ) | | | (5,000,555 | ) | | | (20,699,612 | ) | | | - | | | | - | |

| Net loss attributable to Non-controlling interests | | | (1,644,729 | ) | | | (807,037 | ) | | | - | | | | - | | | | - | |

| Loss | | | (15,632,814 | ) | | | (5,807,592 | ) | | | (20,699,612 | ) | | | (48,399,389 | ) | | | (11,877,068 | ) |

| Comprehensive loss | | | (16,431,581 | ) | | | (5,114,775 | ) | | | (21,090,033 | ) | | | (48,070,186 | ) | | | (12,517,537 | ) |

| Basic and diluted loss per common share | | | (4.05 | ) | | | (1.50 | ) | | | (11.89 | ) | | | (0.33 | ) | | | (0.10 | ) |

| (1) | Due to the change in our fiscal year end to December 31, the result of this period are for the ten months ended December 31, 2014. |

| | | | | | | |

| | | Till Capital Ltd. | | Americas Bullion Royalty Corp. |

| | | As at | | | | As at | | |

| | | December 31 | | December 31 | | February 28, | | February 28, | | February 29, |

| Consolidated Statements of Financial | | 2015 | | 2014(1) | | 2014 | | 2013 | | 2012 |

| Position | | (US$) | | (US$) | | (US$) | | (US$) | | (US$) |

| Assets | | | 51,262,639 | | | | 52,816,013 | | | | 34,039,205 | | | | 58,362,042 | | | | 88,879,534 | |

| Total liabilities | | | 24,981,798 | | | | 7,988,661 | | | | 4,659,646 | | | | 12,790,591 | | | | 8,487,599 | |

| Shareholders' equity | | | 26,280,841 | | | | 44,827,352 | | | | 29,379,559 | | | | 45,571,451 | | | | 80,391,935 | |

| Share capital (2) | | | 3,429 | | | | 3,569 | | | | 115,600,198 | | | | 110,971,769 | | | | 101,827,619 | |

| Deficit | | | (14,672,446 | ) | | | (684,361 | ) | | | (94,359,330 | ) | | | (73,403,323 | ) | | | (27,467,133 | ) |

| Weighted average number of common shares outstanding | | | 3,454,207 | | | | 3,329,269 | | | | 174,066,463 | | | | 147,035,728 | | | | 120,502,303 | |

| (1) | Due to the change in our fiscal year end to December 31, the results of this period are for the ten months ended December 31, 2014. |

| (2) | We completed a quasi-reorganization effective December 31, 2014 to restate our share capital to an amount equal to our then issued and outstanding shares multiplied by the par value per share of $0.001, or $3,569. Because assets had been stated at approximate fair values, the quasi-reorganization had no effect on recorded assets. |

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

Risks Relating to Insurance and Reinsurance

The insurance and reinsurance markets are cyclical and we are subject to their cycles.

The insurance and reinsurance markets are cyclical and subject to unforeseen developments which may affect our results. These include trends of courts granting increasingly larger awards for certain damages, natural disasters, fluctuations in interest rates, changes in laws, changes in the investment environment that affect market prices of investments, inflationary pressures and other events that affect the size of premiums or losses companies and primary insurers experience. Demand for insurance and reinsurance is influenced significantly by prevailing economic conditions. The supply of reinsurance is related to prevailing prices, the levels of insured losses, and the levels of industry surplus which, in turn, may fluctuate in response to changes in rates of return on investments being earned in the reinsurance industry. Furthermore, weak economic conditions may adversely affect (among other aspects of our business) the demand for and claims made under our products, the ability of clients, counterparties and others to establish or maintain their relationships with us, our ability to access and efficiently use internal and external capital resources and our investment.

Our results of operations fluctuate from period to period and may not be indicative of our long-term prospects.

The performance of our reinsurance operations and investment portfolio fluctuates from period to period. Fluctuations result from a variety of factors, including: reinsurance contract pricing; our assessment of the quality of available reinsurance opportunities; the volume and mix of reinsurance products underwritten; loss experience on our reinsurance liabilities; the performance of our investment portfolio; and our ability to assess and integrate our risk management strategy properly.

We face numerous competitors, many of which are more experienced and better capitalized than us.

We compete with major global insurance and reinsurance companies. These companies may have extensive experience in insurance and reinsurance and have greater financial resources available to them. We may also face competition in the future from new entrants that provide products similar to those we provide. Competition could result in less business being available to us, lower premium rates, investment credits, and less favorable retrocession coverage, which could adversely impact our growth and profitability. Our competitors include, among others, Watford Re Ltd., Third Point Reinsurance Ltd. and Hamilton Re, Ltd. and traditional reinsurers, including ACE Ltd., Everest Re, General Re Corporation, Hannover Re Group, Munich Reinsurance Company, Partner Re Ltd., Swiss Reinsurance Company and Transatlantic Reinsurance Company, which are dominant companies in our industry. Although we seek to provide coverage where capacity and alternatives are limited, we directly compete with these larger companies due to the breadth of their coverage across the property and casualty market in substantially all lines of business. We also compete with smaller companies and other niche reinsurers.

Further, our ability to compete may be harmed if insurance industry participants consolidate. Consolidated entities may try to use their enhanced market power to negotiate price reductions for our products and services. If competitive pressures reduce our prices, we would expect to write less business. As the insurance industry consolidates, if at all, competition for customers may become more intense, and the importance of acquiring and properly servicing each customer may become greater. We could incur greater expenses relating to customer acquisition and retention, further reducing our operating margins. In addition, insurance companies that merge may be able to spread their risks across a consolidated, larger capital base so that they require less reinsurance. The number of companies offering retrocessional reinsurance may decline. Reinsurance intermediaries could also consolidate, potentially adversely impacting our ability to access business and distribute our products. We could also experience more robust competition from larger, better capitalized competitors. Any of the foregoing could significantly, and negatively, affect our business or our results of operation.

When we choose to purchase reinsurance, we may be unable to do so, and if we successfully purchase reinsurance, we may be unable to collect the amounts due from such reinsurers.

We may purchase reinsurance for our own account in order to mitigate the volatility of losses upon our financial condition. A reinsurer’s insolvency, or inability or refusal to make payments under the terms of its reinsurance agreement with us, could have a material adverse effect on us because we will remain liable to the insured.

From time to time, market conditions have limited, and in some cases have prevented, insurers and reinsurers from obtaining the types and amounts of reinsurance that they consider adequate for their business needs. Accordingly, we may not be able to obtain our desired amounts of reinsurance or retrocessional reinsurance. In addition, even if we were able to obtain such reinsurance or retrocessional reinsurance, we may not be able to negotiate terms that we deem appropriate or acceptable or obtain such reinsurance or retrocessional reinsurance from entities with satisfactory creditworthiness.

There are numerous counterparty risks associated with the insurance and reinsurance businesses.

We may suffer investment losses due to defaults by others, including issuers of investment securities, reinsurance and derivative counterparties. Issuers or borrowers whose securities we hold, reinsurers, clearing agents, clearing houses and other financial intermediaries may default on their obligations due to bankruptcy, insolvency, lack of liquidity, adverse economic conditions, fraud or other reasons. Our investment portfolio may include investment securities or other assets of the type that have recently experienced defaults. All or any of these types of default could have a material adverse effect on our results of operations, financial condition and liquidity.

In addition, our reinsurance transactions may expose us to credit and counterparty risks of certain parties, such as intermediaries and trustees, in addition to risks relating to such ceding insurers’ underwriting practices. Although we intend to operate our business in a manner that should limit and manage these risks, there can be no assurance that we will not be adversely affected as a result of our exposure to such risks.

For example, in accordance with industry practice, we may pay amounts owed under our policies to reinsurance intermediaries or brokers, who in turn pay these amounts to the ceding insurer. In some jurisdictions, if the intermediary or broker fails to make such an onward payment, we might remain liable to the ceding insurer for the deficiency. Conversely, the ceding insurer may pay premiums to the intermediary or broker, for onward payment to us in respect of reinsurance policies we issued. In certain jurisdictions, these premiums are considered to have been paid to us at the time that payment is made to the intermediary or broker, and the ceding insurer will no longer be liable to us for those amounts, whether we have or have not actually received the premiums. We may not be able to collect all premiums receivable due from any particular intermediary or broker at any given time.

We also may hold a substantial portion of our reserves with third party custodians to secure letters of credit for the benefit of the related cedant, and our access to these amounts would be limited. As a result, we may be exposed to the risk of operational errors or delays at applicable trustees in addition to credit risk with respect to such parties. The terms of applicable custody and letter of credit agreements are generally expected to provide, and depending on the cedant’s jurisdiction, may be required to provide, certain protections against such risks, but there can be no assurance that we will not be adversely affected as a result of our exposure to such risks.

There are numerous operational risks associated with the insurance and reinsurance businesses that could adversely affect our business.

Operational risks and losses can result from many sources, including fraud, errors by employees, failure to document transactions properly or to obtain proper internal authorization, failure to comply with regulatory requirements or information technology failures.

We believe our information technology and application systems are critical to our business and reputation and ability to compete successfully. In addition to our own systems, we are dependent on those of others, including those licensed from our service providers. We cannot be certain that we will continue to have access to these, or comparable service providers and information and technology application systems, or that existing systems will continue to operate as intended. A major defect or failure in our internal controls or information technology and application systems could result in management distraction, harm to our reputation, a loss or delay of revenues or increased expense.

There are ever changing legal and regulatory developments in the insurance and reinsurance industries that could adversely affect our business.

The insurance industry has experienced substantial volatility as a result of litigation, investigations and regulatory activity by various insurance, governmental and enforcement authorities concerning certain practices within the insurance industry. These practices include the accounting treatment for finite reinsurance or other non-traditional or loss mitigation insurance and reinsurance products.

These investigations have resulted in changes in the insurance and reinsurance markets and industry business practices. We cannot predict the potential effects, if any, that future litigation, investigations and regulatory activity may have upon the reinsurance industry.

The effect of emerging claim and coverage issues on our business is uncertain.

As industry practices and legal, judicial and regulatory conditions change, unexpected issues related to claims and coverage may emerge. Various provisions of our contracts, such as limitations or exclusions from coverage or choice of forum, may be difficult to enforce in the manner we intend, due to, among other things, disputes relating to coverage and choice of legal forum. These issues may adversely affect our business by either extending coverage beyond the period that we intended or by increasing the number or size of claims. In some instances, these changes may not manifest themselves until many years after we have issued insurance or reinsurance contracts that are affected by these changes. As a result, we may not be able to ascertain the full extent of our liabilities under our insurance or reinsurance contracts for many years following the issuance of our contracts. The effects of unforeseen development or substantial government intervention could adversely impact our ability to adhere to our goals.

Our failure to maintain sufficient letter of credit (“LOC”) facilities or to increase our LOC capacity on commercially acceptable terms as we grow could significantly and negatively affect our ability to implement our business strategy.

We are not licensed or admitted as a reinsurer in any jurisdiction other than Bermuda and Canada. Certain jurisdictions, including the United States, do not permit ceding insurers to take credit on their statutory financial statements for reinsurance obtained from unlicensed or non-admitted insurers unless the reinsurer posts a LOC or provides other collateral. Further, our license from the Bermuda Monetary Authority (“BMA”) requires that it post collateral equal to the limit of each contract of reinsurance written. Consequently, certain clients require us to deliver a LOC or provide other collateral through funds withheld or trust arrangements. When a reinsurer obtains a LOC facility, the reinsurer is typically required to provide collateral to the LOC provider in order to secure the obligations under the facility. Our ability to provide collateral, and the costs at which we provide collateral, are primarily dependent on the composition of our investment portfolio.

Typically, LOCs are collateralized with fixed-income securities. Banks may be willing to accept our investment portfolio as collateral, but on terms that may be less favorable to us than reinsurance companies that invest solely or predominantly in fixed-income securities. The inability to renew, maintain or obtain LOCs collateralized by our investment portfolio has limited the amount of reinsurance we can write and may require us to modify our investment strategy.

We may utilize margin loans from prime brokers to provide cash to support the LOC arrangements. The potential for margin loan capacity to be reduced or withdrawn may negatively impact our ability to obtain, renew, maintain or increase LOCs.

If we are unable to obtain, renew, maintain or increase LOC facilities or are unable to do so on commercially acceptable terms, we may need to liquidate all or a portion of our investment portfolio and invest in a fixed-income portfolio or other forms of investment acceptable to our clients and banks as collateral, which could significantly and negatively affect our ability to implement our business strategy.

We depend on our clients’ evaluations of the risks associated with their insurance underwriting, which may subject us to reinsurance losses.

In some of our proportional reinsurance business, in which we assume an agreed percentage of each underlying insurance contract being reinsured, or quota share contracts, we do not separately evaluate each of the original individual risks assumed under these reinsurance contracts. Therefore, we are largely dependent on the original underwriting decisions made by ceding companies. We would be subject to the risk that the clients may not have adequately evaluated the insured risks and that the premiums ceded may not adequately compensate us for the risks we assume. We also do not separately evaluate each of the individual claims made on the underlying insurance contracts under quota share contracts. Therefore, we are dependent on the original claims decisions made by our clients.

We could face unanticipated losses from political instability which could have a material adverse effect on our financial condition and results of operations.

We could be exposed to unexpected losses on our reinsurance contracts resulting from political instability and other politically driven events globally. These risks are inherently unpredictable and recent events may indicate an increased frequency and severity of losses. It is difficult to predict the timing of these events or to estimate the amount of loss that any given occurrence will generate. To the extent that losses from these risks occur, our financial condition and results of operations could be significantly and negatively affected.

Any suspension or revocation of RRL’s reinsurance license or Omega’s insurance license would materially impact our ability to do business and implement our business strategy.

RRL is presently licensed as a reinsurer only in Bermuda and Omega is presently licensed as an insurance provider only in Canada. The suspension or revocation of RRL’s or Omega’s license to do business as a reinsurance or insurance company in either of these jurisdictions for any reason would mean that RRL or Omega would not be able to enter into any new reinsurance or insurance contracts until the suspension ended or until RRL or Omega became licensed in another jurisdiction. Any such suspension or revocation of either RRL’s or Omega’s license could negatively impact RRL’s or Omega’s reputation in the reinsurance or insurance marketplace and could have a material adverse effect on our results of operations.

We are subject to the risk of possibly becoming an investment company under U.S. federal securities law.

In the United States, the Investment Company Act of 1940, as amended (the “Investment Company Act”) regulates certain companies that invest in or trade securities. For United States investments, we rely on an exemption under the Investment Company Act for an entity organized and regulated as a foreign insurance company which is engaged primarily and predominantly in the reinsurance of risks on insurance agreements. The law in this area is subjective and there is a lack of guidance as to the meaning of ‘‘primarily and predominantly’’ under the relevant exemption to the Investment Company Act. For example, there is no standard for the amount of premiums that need to be written relative to the level of an entity’s capital in order to qualify for the exemption. If this exemption were deemed inapplicable, we would have to register under the Investment Company Act as an investment company, unless another exemption is available. Registered investment companies are subject to extensive, restrictive and potentially adverse regulation relating to, among other things, operating methods, management, capital structure, leverage, dividends and transactions with affiliates. Registered investment companies are not permitted to operate their business in the manner in which we operate our business, nor are registered investment companies permitted to have many of the relationships that we have with our affiliated companies.

If at any time it were established that we had been operating as an investment company in violation of the registration requirements of the Investment Company Act, there would be a risk, among other material adverse consequences, that we could become subject to monetary penalties or injunctive relief, or both, or that we would be unable to enforce contracts with third parties or that third parties could seek to obtain rescission of transactions with us undertaken during the period in which it was established that we were an unregistered investment company.

To the extent that the laws and regulations change in the future so that contracts we write are deemed not to be reinsurance contracts, we will be at a greater risk of not qualifying for the Investment Company Act exception. Additionally, it is possible that our classification as an investment company would result in the suspension or revocation of our reinsurance license.

Insurance regulations to which we are, or may become, subject, and potential changes thereto, could have a significant and negative effect on our business.

We currently are admitted to do business in Bermuda and Canada. Our operations in these jurisdictions are subject to regulation and supervision. We conduct our business in a manner such that we expect that it will not be subject to insurance and/or reinsurance licensing requirements or regulations in any jurisdiction other than Bermuda and Canada. Although we do not currently intend that we, RRL or Omega will engage in activities which would require an entity to comply with insurance and reinsurance licensing requirements outside of Bermuda or Canada, should we choose to engage in activities that would require us to become licensed in such jurisdictions, we cannot assure investors that we will be able to do so or to do so in a timely manner. Furthermore, the laws and regulations applicable to direct insurers could indirectly affect us, such as collateral requirements in various U.S. states to enable such insurers to receive credit for reinsurance ceded to us. Also, we cannot assure investors that insurance regulators in the United States or elsewhere will not review our activities and claim that we are subject to such jurisdiction’s licensing requirements. In addition, we are subject to indirect regulatory requirements imposed by jurisdictions that may limit our ability to provide reinsurance. For example, our ability to write reinsurance may be subject, in certain cases, to arrangements satisfactory to applicable regulatory bodies, and proposed legislation and regulations may have the effect of imposing additional requirements upon, or restricting the market for, non-U.S. reinsurers, with whom domestic companies may place business. We do not know of any such proposed legislation pending at this time.

We may not be able to comply fully with, or obtain desired exemptions from, statutes, regulations and policies that currently, or may in the future, govern the conduct of our business. Failure to comply with, or to obtain desired authorizations and/or exemptions under, any applicable laws could result in restrictions on our ability to do business or undertake activities that are regulated in one or more of the jurisdictions in which we operate and could subject us to fines and other sanctions. In addition, changes in the laws or regulations to which our subsidiaries are subject or may become subject, or in the interpretations thereof by enforcement or regulatory agencies, could have a material adverse effect on our business.

The insurance and reinsurance regulatory framework of Bermuda recently has become subject to increased scrutiny in many jurisdictions, including the United States. In the past, there have been Congressional and other initiatives in the United States regarding increased supervision, regulation and taxation of the insurance industry, including proposals to supervise and regulate offshore reinsurers. Government regulators are generally concerned with the protection of policyholders rather than other constituencies, such as our shareholders. We are unable to predict the future impact on our operations of changes in the laws and regulations to which we are or may become subject.

We are subject to regulations in Canada through our acquisition of Omega. As a participant in the Canadian insurance industry, Omega is subject to significant regulations of the Canadian federal and provincial governments, including capital and solvency standards, restrictions on certain types of investments and periodic market conduct and financial examinations by regulators. Future changes to Canadian regulations may limit Omega’s ability to adjust prices, adjudicate claims or take other actions that would enhance operating results. Omega mitigates these risks through regular discussions with regulators and industry groups to ensure it is aware of proposed changes and to provide feedback on proposed changes.

Complex and changing U.S. government regulations could impact our business and results of operations.

In July 2010, the U.S. government passed the Dodd-Frank Wall Street Reform and Consumer Protection Act, or “Dodd-Frank Act,” one of the most sweeping financial reforms in decades. The legislation is expected to affect virtually every segment of the financial services industry, including the insurance and reinsurance industry in the United States.

Among other things, the Dodd-Frank Act created the Federal Insurance Office (the “FIO”) to be located within the U.S. Treasury department, with the authority to monitor all aspects of the insurance industry (except health insurance), and changes the regulatory framework for non-admitted insurance and reinsurance. The FIO recently issued a report with recommendations on how to modernize and improve the system of insurance regulation in the United States. Many of the provisions of the Dodd-Frank Act and the recommendations of the FIO require substantial rulemaking within the federal government. Consequently, the ultimate impact of any of these provisions on our operations, financial results or capital resources is currently indeterminable. We intend to monitor the impact of the Dodd-Frank Act on our business.

Risks Relating to the Investment Strategy

We may change our investment strategy at any time.

Till will continually assess the extent of investment allocation in the mining industry and may sell assets as part of its investment strategy. In 2015, we announced our intention to pursue an investment strategy that focuses up to 30% of our investment portfolio in long term (1-3 year) investments. As of December 31, 2015, approximately 9% of our investment portfolio consisted of long term investments. We may change our investment strategy again at any time. Any change in investment strategy could expose us to different risks than those described in this section entitled “Risk Factors.”

We may effectuate short sales of securities that subject us to unlimited loss potential.

We may enter into transactions in which we sell a security we do not own, which we refer to as a short sale, in anticipation of a decline in the market value of the security. Short sales for our account theoretically will involve unlimited loss potential since the market price of securities sold short may continue to increase.

We may buy and sell derivatives which may increase the risk of our investment portfolio.

We may buy and sell derivative instruments, or derivatives, including futures, options, swaps, structured securities and other instruments and contracts that derive their value from one or more underlying securities, financial benchmarks, currencies, commodities or indices. We have made the determination that we qualify for an exemption from the registration requirements as a commodity pool operator. To the extent that we engage in derivatives trading, there are a number of risks associated therewith. Because many derivatives are leveraged, and thus provide significantly more market exposure than the money paid or deposited when the transaction is entered into, a relatively small adverse market movement may result in the loss of a substantial portion of or the entire investment, and may potentially expose us to a loss exceeding the original amount invested. Derivatives may also expose us to liquidity and counterparty risk. There may not be a liquid market within which to close or dispose of outstanding derivatives contracts. In the event of the counterparty’s default, we would generally only rank as an unsecured creditor and risk the loss of all or a portion of the amounts we were contractually entitled to receive.

Our representatives’ service on boards and committees may place trading restrictions on our investments and may subject us to indemnification liability.

We may from time to time place representatives or representatives of our affiliates on creditors’ committees and/or boards of certain companies in which we have invested. While such representation may enable us to enhance the sale value of our investments, it may also place trading restrictions on our investments and may subject us to indemnification liability.

Risks Relating to the Company

We have a limited history of operating results.

We have limited operations in the reinsurance business to date and no long term financial results on which potential investors may base their investment decision or compare our results with other investment opportunities. Because we are still in the early stage of development, we face substantial business and financial risks and may suffer significant losses. We must successfully develop business relationships, establish operating procedures, hire staff, install management information and other systems and complete other tasks necessary to conduct our intended business activities. We are attempting to successfully develop and maintain business relationships, establish operating procedures, and complete other tasks appropriate for the conduct of our intended business activities. In particular, our ability to implement successfully our strategy depends on, among other things:

| • | our ability to establish relationships with insurance brokers and reinsurance intermediaries to develop premiums; |

| • | our ability to secure our insurance or reinsurance obligations; and |

| • | our ability to manage our investments. |

It is possible that we will not be successful in implementing our business strategy or accomplishing these necessary tasks.

Additionally, because our business model and investment strategies differ from those of other insurers and reinsurers, investors may not be able to compare our business or prospects to those of other property and casualty reinsurers because, among other things:

- RRL intends to focus on reinsurance contracts that have average or above frequency and low severity claims where risks are generally more predictable than compared to reinsurance contracts where claims are expected to be less frequent but more severe (i.e., catastrophic risks). Profit or loss of reinsurers who assume more predictable risks is generally less volatile and less profitable than the profit or loss of reinsurers who assume catastrophic risks. Our underwriting profit may therefore not be as profitable compared to reinsurers who assume catastrophic risks, and conversely, our underwriting losses may not be as large as reinsurers who assume catastrophic risks.

- RRL intends to focus on reinsurance contracts that have longer periods for loss development (i.e., run-off) where premiums collected on the contracts may be held, and invested, for longer periods than reinsurance contracts where claims are expected to develop and be paid more quickly. Our investment income may therefore be higher compared to the investment income of reinsurers with contracts that have shorter loss development periods.

- RRL intends to maintain a high capital ratio to support claim liabilities and may therefore enter into fewer reinsurance contracts than other reinsurers who may maintain a lower level of capital to support claim liabilities. As such, our underwriting profit or loss may be less than the underwriting profit or loss compared to reinsurers who maintain a lower level of capital to support claim liabilities. Conversely, our investment income may be higher compared to reinsurers who maintain a lower level of capital to support claim liabilities.

- RRL intends to rely significantly on third-party contractors to whom we will pay commissions and incentives to evaluate and secure reinsurance contracts. Our underwriting costs may therefore be higher, and our underwriting profit lower, compared to reinsurers who do not rely on third-party contractors to evaluate and secure reinsurance contracts.

- In addition to the availability of RRL’s assets to settle claims, RRL expects to further support a substantial amount of its insurance risks with letters of credit (“LOCs”). We will incur costs to maintain LOCs. Other established reinsurers may not enhance their claims-paying ability with LOCs. Our underwriting costs may therefore be higher compared to reinsurers who do not support their claims-paying ability with LOCs.

- Depending on the amount and types of business made available to RRL, RRL does not initially expect to have an aged block of diversified insurance risks, either by line of business, geographic area, producer, etc. Most traditional reinsurers would have such diversity embedded in to their overall book of business and, accordingly, may not be exposed to single events and one-time loss occurrences.

- RRL does not have a long history of operations, and that absence of a long operating history may affect our ability to execute our strategies and operating philosophies.

We cannot assure investors that there will be sufficient demand for the insurance and reinsurance products we plan to write to support our planned level of operations, or that we will succeed in implementing our business strategy.

Our operational structure is currently being developed and implemented.

We continue to develop and implement our operational structure and enterprise risk management framework, including exposure management, financial reporting, information technology and internal controls, with which we will conduct our business activities. There can be no assurance that the development of our operational structure or the implementation of our enterprise risk management framework will proceed smoothly or on our projected timetable.

Forward-looking statements may prove inaccurate.

The analysis of our business contains forward-looking statements, which include information concerning our possible future results, as well as other expressions of belief, expectation or anticipation. The forward-looking statements included in our analysis are based on a limited history and current expectations and are subject to uncertainty including the risk that the assumptions on which they are based prove to be inaccurate. Shareholders are cautioned that many factors could affect the our future results and, as a result, contribute to our actual results being materially different from those results expressed in, or implied by, the forward-looking statements contained herein. Because we are a newly formed company, most of the statements relating to us and our business, including statements relating to our competitive strengths and business strategies, are forward-looking statements.

There are limitations for financial projections, especially for a new company.

We have a limited operating history in the reinsurance business. There can be no assurance that policyholders or cedants will transact with us. Moreover, insurance and reinsurance risks we assume and expenses may leave us exposed to liabilities in excess of premiums and investment income, resulting in a demand on our capital base, and there can be no assurance that losses exceeding our total resources will not occur.

RRL is unrated and the markets rely heavily on ratings so RRL may not be able to generate premiums.

Third party rating agencies assess and rate the claims paying ability of insurers and reinsurers based on criteria established by such rating agencies. The claims paying ability ratings assigned by rating agencies to insurance and reinsurance companies represent independent opinions of financial strength and ability to meet policyholder obligations, and are not directed toward the protection of investors. Insured parties and brokers/intermediaries use these ratings as one measure by which to assess the financial strength and quality of insurers and reinsurers. These ratings are often a key factor in the decision by an insured or a broker/intermediary of whether to place business with a particular insurance or reinsurance provider. RRL hopes to secure an “A-(Excellent)” or better rating from A.M. Best Company (“A.M. Best”), a company which provides credit ratings services for the insurance industry, and apply for a rating as soon as practicable. However, there is no guarantee that such a rating, or a comparable rating from any rating agency, will be obtained, or that if any such rating is obtained, that it will be maintained. Other than A.M. Best, the rating agencies may not rate RRL for some time because RRL lacks an operating history. Although we believe our strong financial position will be sufficient to attract a sufficient volume of business, there can be no assurance that the lack of a rating will not adversely affect the volume and quality of business available to RRL.

We expect to rely on Multi-Strat Re Ltd., brokers, and other reinsurance intermediaries, which may be unwilling or unable to produce business for us.

We expect to rely primarily on Multi-Strat Re Ltd. (“Multi-Strat Re”) for the business we will receive. We expect that a large portion of our business will come from a limited number of intermediaries. We have entered into agreements with Multi-Strat Re pursuant to which we have written limited amounts of reinsurance business through the Multi-Strat Re platform. Multi-Strat Re is licensed as a Class 3A insurer under Insurance Act of 1978, as amended and its related regulations (the “Insurance Act”) but has a limited history of operations. We understand that Multi-Strat Re is the process of sourcing insurance business and is in regular contact with the BMA about the status of such business. It is possible that the BMA will not approve certain insurance business proposed by Multi-Strat Re, in which case Multi-Strat Re will not be able to write such insurance business, and we will not be able to source such insurance business through the Multi-Strat Re platform. Loss of the Multi-Strat Re business could adversely affect our results.

We may not be able to locate, bind, or profitably underwrite insurance and reinsurance underwriting risks.

Our successful operations rely on our ability to find, select, monitor and control the reinsurance risks we are assuming. To the extent that the developing nature of this market, together with the volatility of both spreads in capital markets and of low treasury returns, cause such risks to be more volatile than projected or less profitable, poor implementation or selection of underwriting criteria could result in material deterioration in earnings or shareholder’s equity in future periods.

The concentration of our insurance and reinsurance clients could adversely affect us.

Due to the limited number of potential insurance and reinsurance clients, we expect that a few of these potential clients will account for a high percentage of our revenues for the foreseeable future. If we fail to attract or retain business from one or more of these potential clients, we would be adversely affected. Also, the loss of a significant client in the future could adversely affect us.

If interest rates increase significantly, they could hurt us.

If interest rates move upward significantly, we could be adversely affected in two ways. First, competitors could become more aggressive in their pricing, making up for any increase in underwriting losses with higher investment gains. Second, cedants could insist on higher claims limits to compensate for the opportunity cost of investing the funds that they are using to pay the premiums to RRL.

If our loss reserves are inadequate, we could suffer additional reductions in earnings.

We will establish loss reserves to cover the payment of all losses incurred with respect to the business we write. Reserves are estimates involving actuarial and statistical projections at a given time to quantify our expectation of ultimate settlement and administration of claims costs and the timing thereof. The establishment of an appropriate level of reserves is an inherently uncertain process. Moreover, the estimation of reserves for new insurers, such as us, is inherently less reliable than the reserve estimations for an insurer with a longer operating history because such newer companies do not yet have an established loss history. Actual losses and loss adjustment expenses we incur may deviate, perhaps substantially, from initial estimates. If our reserves in respect of business written should be inadequate, we may be required to increase reserves, causing a corresponding reduction in our net income in the period in which the deficiency is identified. There can be no assurance that losses will not exceed our reserves and have a material adverse effect on our financial condition or results of operations in a particular period. If actual claims exceed our loss reserves, our financial results could be significantly adversely affected.

Fixed overheads could adversely affect our expense ratio.

Our overhead will not necessarily vary in proportion to the volume and profitability of the business we write, which is expected to fluctuate. As a result, our expense ratio may become disproportionately high during periods in which we write a lower volume of business.

We are dependent on outsourcing and any inability to do so or failure by an outsourcer could adversely affect us.

Until dedicated management is retained, our success will largely be dependent on the efforts of our service providers, particularly with respect to obtaining premiums, insurance underwriting, and/or raising capital. If we fail to meet expectations in underwriting, we could suffer financially.

We may not be able to recruit the quality or quantity of full-time management necessary to make us successful.

While outsourcing makes sense when we are our current size, our expansion plans may require us to recruit full-time management.

If we are unable to do so, we could fail to grow, and our results of operations could be adversely affected.

We are reliant on key employees.

Various aspects of our business will depend on the services and skills of key personnel, including our Chief Executive Officer, Chief Investment Officer and key management personnel of Omega. There can be no assurance that we will be able to attract and retain key personnel. We currently have employment contracts with Phil Cook and Matthew Cook, the senior managers of Omega.

There are limitations in using predictive models.

We will utilize predictive models to underwrite our insurance and reinsurance business and manage our reserves successfully. Any substantial or repeated failures in the accuracy or reliability of such models could have a material adverse effect on our business, financial condition and results of operation.

We may be unable to retrocede risk and might suffer severe losses as a result.

We may seek to limit our risk by purchasing retrocessional protection for our business. However, we believe that access to retrocession will be limited. There can be no assurance that retrocession will be available to us in the future. If retrocession is available, there can be no assurance that it will be on terms we deem to be appropriate or acceptable or from entities with satisfactory creditworthiness. We have not arranged for any retrocession to date.

We may be unsuccessful in making acquisitions or strategic investments.

We may pursue growth through acquisitions and/or strategic investments in new businesses. The negotiation of potential acquisitions or strategic investments as well as the integration of an acquired business or new personnel could result in a substantial diversion of management resources. Acquisitions could involve numerous additional risks such as potential losses from unanticipated litigation or levels of claims and inability to generate sufficient revenue to offset acquisition costs. Our ability to manage our growth through acquisitions or strategic investments will depend, in part, on our success in addressing these risks. Any failure by us to effectively implement our acquisitions or strategic investment strategies could have a material adverse effect on our business, financial condition or results of operations.

Our financial results are likely to be very volatile, which could diminish valuations of our shares.

Insurance and reinsurance risks and investing can be volatile. We expect to mitigate insurance and reinsurance volatilities by adhering to strict underwriting guidelines restricting the volatility of risks being assumed and/or through further retrocessions pursuant to which we will cede our own risks to other assuming companies.

Furthermore, our investment results could also be volatile. Investors must be prepared for the possibility of losing their entire investment.

We may require additional capital, which may be unavailable when we need it.

Our future capital requirements depend on many factors, including our ability to establish reserves at levels sufficient to cover losses. We may need to raise additional funds through financings or curtail our growth and reduce our assets. Any equity or debt financing, if available at all, may be on terms that are not favorable to us. In the case of equity financings, dilution to our shareholders could result. In addition, one or more investors may fail to purchase the full amount of shares such investor committed to purchase under its subscription agreement. If we cannot obtain adequate capital, our business, results of operations and financial condition could be adversely affected. We may require additional capital in the future, which may not be available or may only be available on unfavorable terms.

U.S. persons who own our shares may have more difficulty in protecting their interests than U.S. persons who are shareholders of a U.S. corporation.

Our bye-laws call for all shareholder suits to be adjudicated in Bermuda and all shareholders agree to this as a condition of purchasing shares. Bermuda does not permit its attorneys to act on behalf of clients on a contingency fee basis, so any shareholder or combination of shareholders must pay legal fees to press any grievance against us or our directors in a Bermuda court of law. Furthermore, Bermuda’s legal system requires the non-prevailing party to pay legal fees of the prevailing party.

The rights of shareholders under Bermuda law are also not as extensive as the rights of shareholders under legislation or judicial precedent in many Canadian or United States jurisdictions. For example, class actions and derivative actions are generally not available to shareholders under the laws of Bermuda. However, the Bermuda courts ordinarily would be expected to follow English case law precedent, which does permit a shareholder to commence an action in the name of a company to remedy a wrong done to the company where the act complained of (i) is alleged to be beyond the corporate power of the company; (ii) is illegal; or (iii) would result in the violation of the company’s Memorandum of Association or Bye-laws. Furthermore, consideration would be given by the court to acts that are alleged to constitute a fraud against the minority shareholders or where an act requires the approval of a greater percentage of the company’s shareholders than actually approved it. The winning party in such an action would generally be able to recover a portion of attorneys’ fees incurred in connection with such action. Our bye-laws provide that shareholders waive all claims or rights of action that they might have, individually or in the right of the Company, against any director or officer for any act or failure to act in the performance of such director’s or officer’s duties, except with respect to any fraud or dishonesty of such director or officer.

We are subject to the jurisdiction of Bermuda work eligibility laws which may limit our ability to employ key employees.

We may also be affected by Bermuda laws requiring work permits for certain employees. Under Bermuda law, non-Bermudians (other than spouses of Bermudians) may not engage in any gainful occupation in Bermuda without an appropriate governmental work permit. Our success may depend in part upon the continued services of key employees and contractors in Bermuda. A work permit may be granted or renewed upon showing that, after proper public advertisement, no Bermudian (or spouse of a Bermudian or a holder of a permanent resident’s certificate or holder of a working resident’s certificate) is available who meets the minimum standards reasonably required by the employer. The Bermuda government’s policy no longer places a term limit on individuals with work permits. A work permit is issued with an expiry date (up to five years) and no assurances can be given that any work permit will be issued or, if issued, renewed upon the expiration of the relevant term. If work permits are not obtained, or are not renewed, for our principal employees and contractors, we would lose their services, which could materially affect our business.

There could be changes of law in Bermuda that could adversely affect us.

Because we are organized in Bermuda, we will be subject to changes of law or regulation in such jurisdiction that may have an adverse impact on our operations overall, including imposition of tax liability or increased regulatory supervision. In addition, we will be exposed to changes in the political environment in Bermuda.

Risks Relating to our Shares.

Our shares have limited voting rights.

No holder or combination of holders who attribute beneficial ownership to one another may hold more than 9.9% of the voting power of the Company, regardless of whether they hold substantially more than 9.9% of the votes attaching to our issued and outstanding shares. However, if any one person (within the meaning of the United States Internal Revenue Code of 1986, as amended) owns in excess of 50% of our shares, then the restriction on voting power will cease to apply. While this structure is in place to avoid inadvertent taxation of U.S. shareholders under the controlled foreign corporation U.S. taxation rules, it also limits the abilities of shareholders to combine to enforce changes in our practices.

There are restrictions on dividends.

We are a holding company and therefore cannot conduct a reinsurance or insurance business on our own. Dividends and other permitted payments from RRL and Omega are expected to be our primary source of funds to pay expenses and dividends, if any. Although we may declare dividends to our shareholders, it is uncertain when, if ever, such dividends will be declared, and the Class 3A insurance license of RRL also prohibits RRL from declaring and/or paying any dividends and/or making any capital contributions to RRL’s parent, shareholders or affiliates without the obtaining prior written approval of the BMA. During the early years of operations, we expect that RRL will retain virtually all profit (if any), other than that necessary to pay our expenses, to provide capacity to write reinsurance and to accumulate reserves and surplus for the payment of claims. In addition, the payment of dividends by RRL to Till is limited under Bermuda law and regulations, and may be limited by the terms of RRL’s agreements with its cedants.

Warrants and options will dilute shareholders.

We have issued warrants and will issue further warrants and options to our officers, directors and certain business partners. Our shareholders will experience dilution upon the exercise of the warrants, with the scope of such dilution dependent on the number of fully diluted shares of the Company outstanding as of such time.

We have adopted a stock option plan, and as options are granted and exercised thereunder, our shareholders will experience dilution upon the exercise of such options, with the scope of such dilution dependent on the number of fully diluted shares outstanding as of such time. In addition, although the size of the option pool will be determined by our senior management and approved by our Board, no assurance can be given that the size of the option pool will be adequate to retain and properly incentivize our management. As a result, additional options or other equity awards may be granted in the future, resulting in additional dilution to our shareholders.

Risks Relating to Taxation

U.S. holders who hold our shares may be subject to adverse U.S. tax consequences if we are considered to be a passive foreign investment company for U.S. federal income tax purposes.

If we are considered to be a passive foreign investment company (“PFIC”) for U.S. federal income tax purposes, a U.S. Holder (as defined below) who owns any of our shares may be subject to adverse U.S. federal income tax consequences, including a greater tax liability than might otherwise apply and an interest charge on certain taxes that are deferred by virtue of our non-U.S. status. In general, either we would be a PFIC for a tax year if: (i) 75% or more of our income constitutes “passive income” or (ii) 50% or more of our assets (by value) produce or were held to produce “passive income,” based on the quarterly average of the fair market value of such assets. Passive income generally includes interest, dividends and other investment income but does not include income derived in the active conduct of an insurance business by a corporation predominantly engaged in an insurance business. This exception for insurance companies is intended to ensure that a bona fide insurance company’s income is not treated as passive income, except to the extent such income is attributable to financial reserves in excess of the reasonable needs of the insurance business. However, there is very little authority as to what constitutes the active conduct of an insurance business for purposes of the PFIC rules. The IRS has notified taxpayers in IRS Notice 2003-34 that it intends to scrutinize the activities of certain insurance companies located outside of the United States, including reinsurance companies that invest a significant portion of their assets in alternative investment strategies, to determine whether such companies qualify for the active insurance company exception in the PFIC rules.

We do not believe that we are classified as a PFIC for our tax years ended December 31, 2014 and 2015. No opinion of legal counsel or ruling from the IRS concerning our status as a PFIC has been obtained or is currently planned to be requested. Whether we will be classified as a PFIC in our current tax year ending December 31, 2016 or subsequent tax years will depend, in part, on whether we continue to be actively engaged in insurance activities that involve sufficient transfer of risk and whether our financial reserves are consistent with industry standards and are not in excess of the reasonable needs of our insurance business during such years. Accordingly, we cannot assure you that we will not be a PFIC in our current tax year or future tax years or that the IRS will agree with any determination by us that we are not a PFIC. Prospective investors are urged to consult their own tax advisors to assess their tolerance of this risk.

The IRS recently proposed U.S. Treasury Regulations concerning the active insurance company exception. The proposed regulations provide that the active conduct of an insurance business must include the performance of substantial managerial and operational services by an insurance company’s own employees and officers. The activities of independent contractors and employees of affiliates are not sufficient to satisfy this requirement. The proposed regulations also clarify that income from investment assets held by an insurance company to meet its obligations under insurance and annuity contracts will not be treated as passive income for PFIC purposes. However, the IRS did not propose a specific method for determining the portion of an insurance company’s assets that are held to meet obligations under insurance and annuity contracts, and solicited comments on appropriate approaches. At this time it is unclear whether final regulations will include a specific methodology and how any such methodology would apply to us. At this time, it is uncertain whether such proposed U.S. Treasury Regulations will become effective and whether the final U.S. Treasury Regulations will contain provisions different than those set forth in such proposed U.S. Treasury Regulations.

Recently proposed legislation introduced by Senate Finance Committee ranking minority member Ron Wyden would modify the insurance exception to apply to a company only if (i) the company would be taxed as an insurance company were it a U.S. corporation and (ii) either (A) loss and loss adjustment expenses and certain reserves constitute more than 25% of the company’s gross assets for the relevant year or (B) loss and loss adjustments expenses and certain reserves constitute more than 10% of the company’s gross assets for the relevant year and, based on the applicable facts and circumstances, the company is predominantly engaged in an insurance business and the failure of the company to satisfy the preceding 25% test is due solely to temporary circumstances involving the insurance business. Similarly, Senate Finance Committee then-Chairman Max Baucus had previously released several tax reform discussion drafts on international tax issues and, in early 2014, House Ways and Means Committee then-Chairman Dave Camp had published a tax reform proposal, that would modify or eliminate the application of the insurance exception. If any such legislation were enacted in its current form, no assurance can be given that we would be able to operate in a manner to satisfy these requirements in any given year. No assurance can be given as to whether such legislation will be adopted and if so, in what form. Moreover, as discussed above, there can be no assurance as to what methodologies the proposed U.S. Treasury Regulations will adopt for determining the portion of an insurance company’s assets that are held to meet obligations under insurance and annuity contracts, or whether the proposed U.S. Treasury Regulations will be enacted in their current form.

If a U.S. Holder holds our shares during any tax year in which we are treated as a PFIC, such shares will generally be treated as stock in a PFIC for all subsequent years. The consequences of us being treated as a PFIC and certain elections designed to mitigate such consequences, including a “Protective QEF Election,” are discussed in more detail under the heading “Certain United States Federal Income Tax Considerations”. If you are a United States person, we advise you to consult your own tax advisor concerning the potential tax consequences to you under the PFIC rules and to assess your tolerance of this risk.

We may be subject to U.S. federal income tax, which would have an adverse effect on our financial condition and results of operations and on an investment in our shares.

If any of the Company, Omega or RRL were considered to be engaged in a trade or business in the United States, we could be subject to U.S. federal income and additional branch profits taxes on the portion of our earnings that are effectively connected to such U.S. business or in the case of RRL or Omega, if it is entitled to benefits under the United States income tax treaty with Bermuda and if it were considered engaged in a trade or business in the United States through a permanent establishment, RRL or Omega could be subject to U.S. federal income tax on the portion of its earnings that are attributable to its permanent establishment in the United States, in which case its results of operations could be materially adversely affected. The Company, Omega and RRL are Bermuda companies. We intend to manage our business so that each of these companies should operate in such a manner that neither of these companies should be treated as engaged in a U.S. trade or business and, thus, should not be subject to U.S. federal taxation (other than the U.S. federal excise tax on insurance and reinsurance premium income attributable to insuring or reinsuring U.S. risks and U.S. federal withholding tax on certain U.S. source investment income). However, there can be no assurance that the IRS will not contend that the Company, Omega or RRL are engaged in a trade or business in the United States. If the Company, Omega or RRL were so engaged, it would be subject to U.S. income tax at regular corporate rates on its taxable income that is effectively connected with the conduct of such trade or business as well as a 30% branch profits tax in certain circumstances.

Certain gain on investments we make may be subject to U.S. federal income tax under FIRPTA.

Under the Foreign Investment in Real Property Tax Act (“FIRPTA”), gain or loss of a foreign corporation on the disposition of a “United States real property interest” is treated as if it were effectively connected with the conduct of a U.S. trade or business of such corporation. United States real property interests include interests other than as a creditor in a “United States real property holding corporation” (“USRPHC”). A USRPHC is any corporation, subject to a limited exception for a corporation whose stock is regularly traded on an established securities market, if the fair market value of its United States real property interests on any applicable determination date equals or exceeds 50% of the fair market value of the sum of its United States real property interests, its interests in real property outside of the United States and any other of its assets which are used or held for use in a trade or business. We intend to retain oversight over our investments and may impose guidelines from time to time designed to provide for an overall earnings or risk profile for us. Although nonexistent at present, such guidelines may limit the extent to which we may invest in USRPHCs and/or other United States real property interests. The Company indirectly hold interests in USRPHCs and United States real property interests.

We may become subject to U.S. withholding and information reporting requirements under the Foreign Account Tax Compliance Act (“FATCA”) provisions.