Exhibit 99.1

© 2016 Majesco. All rights reserved 1 Majesco Investor Day Ketan Mehta, CEO and Co - Founder May 11, 2016

© 2016 Majesco. All rights reserved 2 2 Cautionary Language Concerning Forward - Looking Statements This presentation contains forward - looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act . These forward - looking statements are made on the basis of the current beliefs, expectations and assumptions of management, are not guarantees of performance and are subject to significant risks and uncertainty . These forward - looking statements should, therefore, be considered in light of various important factors, including those set forth in Majesco’s reports that it files from time to time with the Securities and Exchange Commission and which you should review, including those statements under “Item 1 A – Risk Factors” in Majesco’s Annual Report on Form 10 - K . Important factors that could cause actual results to differ materially from those described in forward - looking statements contained in this presentation include, but are not limited to : integration risks ; changes in economic conditions, political conditions, trade protection measures, licensing requirements and tax matters ; technology development risks ; intellectual property rights risks ; competition risks ; additional scrutiny and increased expenses as a result of being a public company ; the financial condition, financing requirements, prospects and cash flow of Majesco ; loss of strategic relationships ; changes in laws or regulations affecting the insurance industry in particular ; restrictions on immigration ; the ability and cost of retaining and recruiting key personnel ; the ability to attract new clients and retain them and the risk of loss of large customers ; continued compliance with evolving laws ; customer data and cybersecurity risk ; and Majesco’s ability to raise capital to fund future growth . These forward - looking statements should not be relied upon as predictions of future events and Majesco cannot assure you that the events or circumstances discussed or reflected in these statements will be achieved or will occur . If such forward - looking statements prove to be inaccurate, the inaccuracy may be material . You should not regard these statements as a representation or warranty by Majesco or any other person that we will achieve our objectives and plans in any specified timeframe, or at all . You are cautioned not to place undue reliance on these forward - looking statements, which speak only as of the date of this presentation . Majesco disclaims any obligation to publicly update or release any revisions to these forward - looking statements, whether as a result of new information, future events or otherwise, after the date of this press release or to reflect the occurrence of unanticipated events, except as required by law

© 2016 Majesco. All rights reserved 3 Majesco Investor Day • Welcome • Agenda for the Day • Majesco Update – Ketan Mehta 30 Minutes • Insurance Industry View – Denise Garth 20 Minutes • Customer Panel – 45 Minutes • Ed Ossie, COO Majesco • Ernie Garateix, COO Heritage Insurance • Gregg Nickerson, CIO Mapfre Insurance US • Patrick Hesidence, VP Billing Erie Insurance • Break / Solution Showcase 20 Minutes • P&C Business Update – Prateek Kumar 20 Minutes • L&A Business Update – Chad Hersh 20 Minutes • Product Update – Manish Shah 20 Minutes • Financial Update – Farid Kazani 20 Minutes • Wrap - up and Q&A 15 Minutes • Cocktail Reception

© 2016 Majesco. All rights reserved 4 Majesco Overview and Performance of 2015 - 16

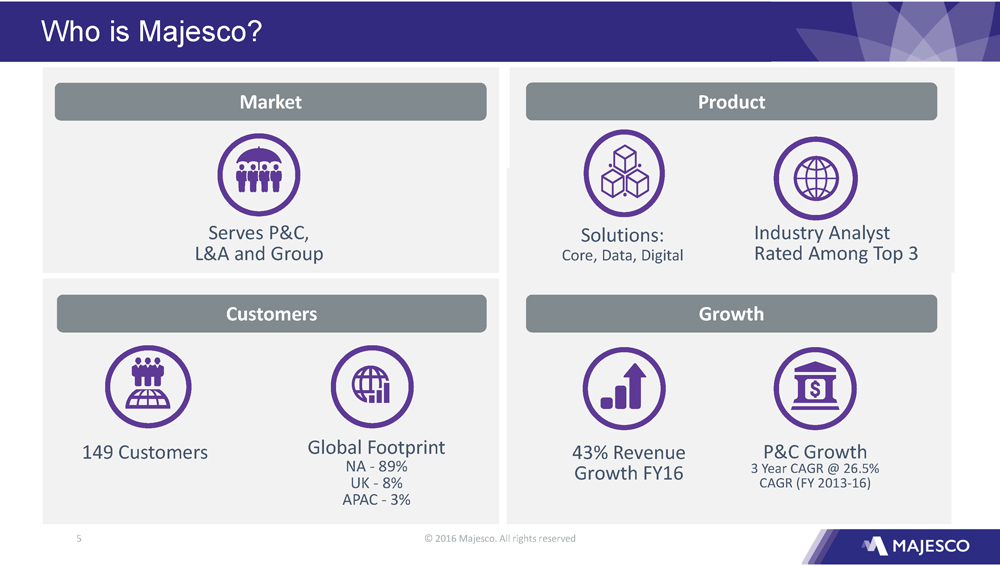

© 2016 Majesco. All rights reserved 5 Who is Majesco? 5 Industry Analyst Rated Among Top 3 149 Customers Serves P&C, L&A and Group 43% Revenue Growth FY16 Global Footprint NA - 89% UK - 8% APAC - 3% P&C Growth 3 Year CAGR @ 26.5% CAGR (FY 2013 - 16 ) Product Solutions: Core, Data, Digital Customers Growth Market

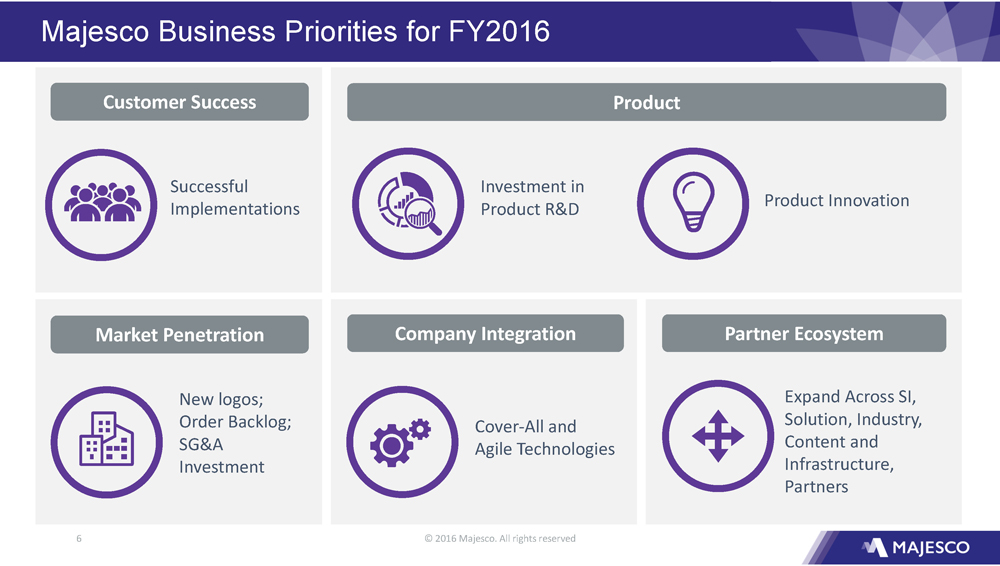

© 2016 Majesco. All rights reserved 6 Majesco Business Priorities for FY2016 Customer Success Product Investment in Product R&D Product Innovation Market Penetration New logos; Order Backlog; SG&A Investment Company Integration Partner Ecosystem Cover - All and Agile Technologies Expand Across SI, Solution, Industry, Content and Infrastructure, Partners Successful Implementations

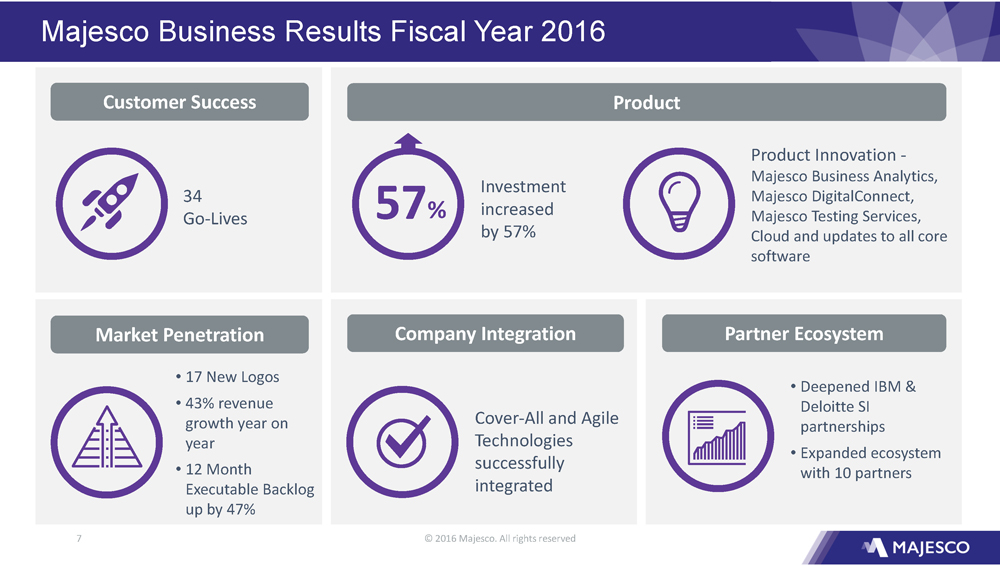

© 2016 Majesco. All rights reserved 7 Majesco Business Results Fiscal Year 2016 Customer Success 34 Go - Lives Product Investment increased by 57% Product Innovation - Majesco Business Analytics, Majesco DigitalConnect, Majesco Testing Services, Cloud and updates to all core software Market Penetration • 17 New Logos • 43% revenue growth year on year • 12 Month Executable Backlog up by 47% Company Integration Partner Ecosystem Cover - All and Agile Technologies successfully integrated • Deepened IBM & Deloitte SI partnerships • Expanded ecosystem with 10 partners 57 %

© 2016 Majesco. All rights reserved 8 Insurance Industry Dynamics

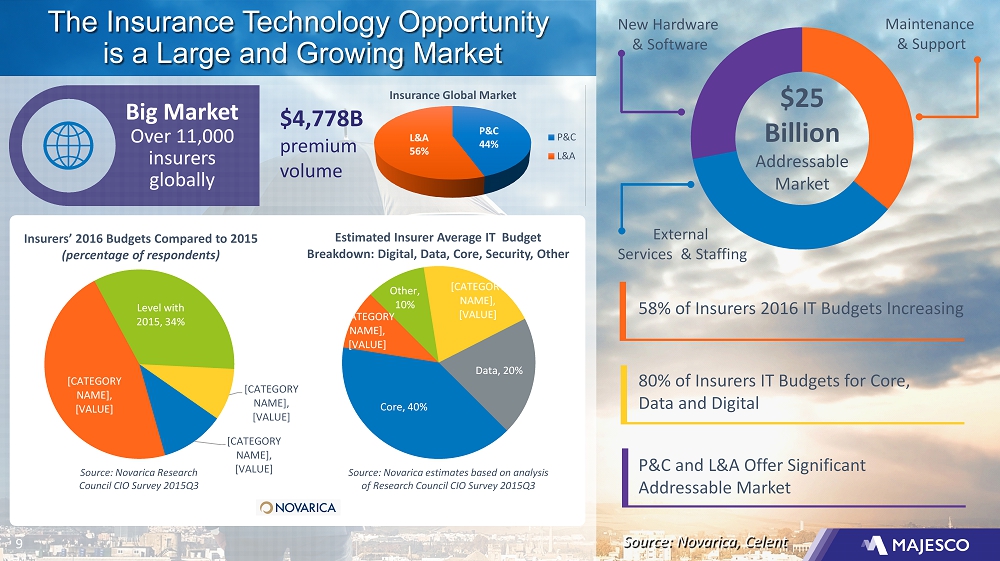

© 2016 Majesco. All rights reserved 9 The Insurance Technology Opportunity is a Large and Growing Market Source: Novarica, Celent 9 New Hardware & Software Maintenance & Support External Services & Staffing $25 Billion Addressable Market 80% of Insurers IT Budgets for Core, Data and Digital P&C and L&A Offer Significant Addressable Market 58% of Insurers 2016 IT Budgets Increasing Big Market Over 11,000 insurers globally $4,778B premium volume P&C 44% L&A 56% Insurance Global Market P&C L&A Core, 40% [CATEGORY NAME] , [VALUE] Other, 10% [CATEGORY NAME] , [VALUE] Data, 20% Estimated Insurer Average IT Budget Breakdown: Digital, Data, Core, Security, Other Source: Novarica estimates based on analysis of Research Council CIO Survey 2015Q3 [CATEGORY NAME] , [VALUE] [CATEGORY NAME] , [VALUE] Level with 2015, 34% [CATEGORY NAME] , [VALUE] Insurers’ 2016 Budgets Compared to 2015 (percentage of respondents) Source: Novarica Research Council CIO Survey 2015Q3

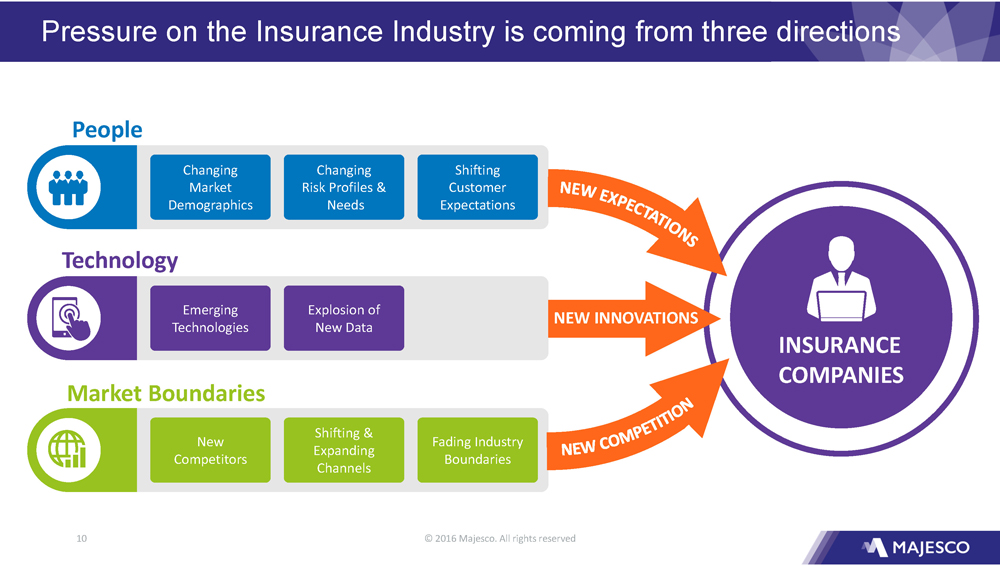

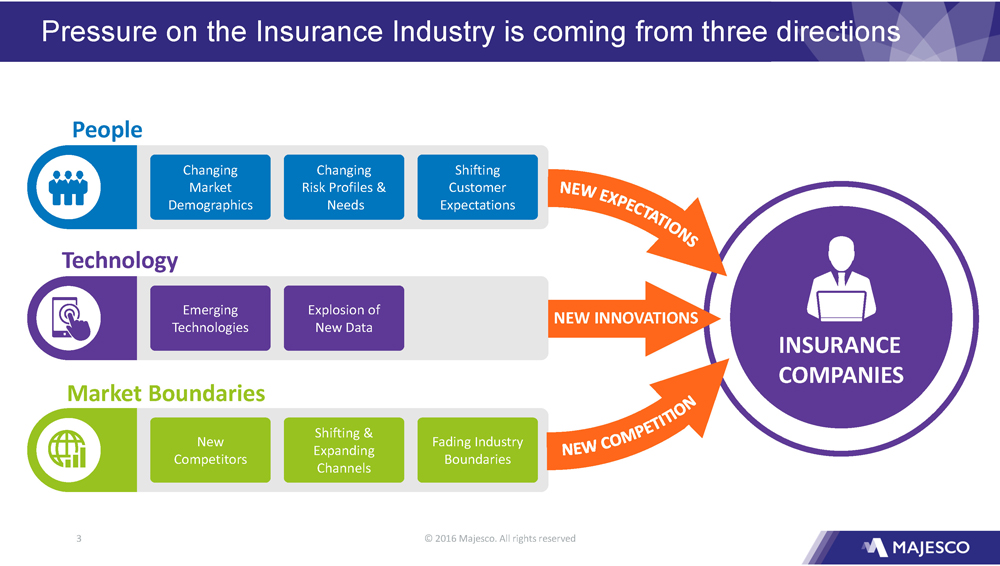

© 2016 Majesco. All rights reserved 10 INSURANCE COMPANIES Pressure on the Insurance Industry is coming from three directions People Changing Market Demographics Changing Risk Profiles & Needs Shifting Customer Expectations Emerging Technologies Explosion of New Data Technology New Competitors Shifting & Expanding Channels Fading Industry Boundaries Market Boundaries NEW INNOVATIONS

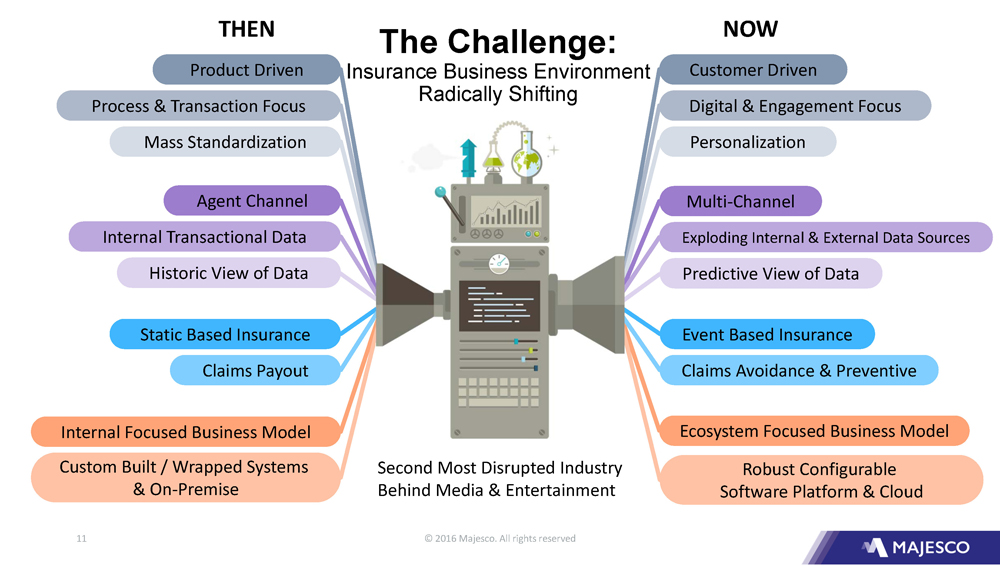

© 2016 Majesco. All rights reserved 11 The Challenge: Insurance Business Environment Radically Shifting Agent Channel Mass Standardization Product Driven Historic View of Data Internal Transactional Data Static Based Insurance Process & Transaction Focus Claims Payout Custom Built / Wrapped Systems & On - Premise Internal Focused Business Model Multi - Channel Personalization Customer Driven Predictive View of Data Exploding Internal & External Data Sources Event Based Insurance Digital & Engagement Focus Claims Avoidance & Preventive Robust Configurable Software Platform & Cloud Ecosystem Focused Business Model THEN NOW Second Most Disrupted Industry Behind Media & Entertainment

© 2016 Majesco. All rights reserved 12 Evolution of Technology Underpins the Insurance Industry Challenge 12 Effectiveness: Agent Automation Agility Innovation Speed Enabling Insurers: Optimization: E - Business & Engagement Efficiency: Operational Automation Innovation: New Business Models

© 2016 Majesco. All rights reserved 13 Market Dynamics Driven by Customer Demands Strong preference to buy vs. build Digital and Data strategies drive need to improve customer experience and insights Channel strategies demand distribution and digital solutions Demand for fewer trusted partners with size and scale Top 5 software suite vendors get majority of new deals Source: SMA Research; Novarica Increased adoption of cloud for core and more for innovation and speed

© 2016 Majesco. All rights reserved 14 Majesco Offerings

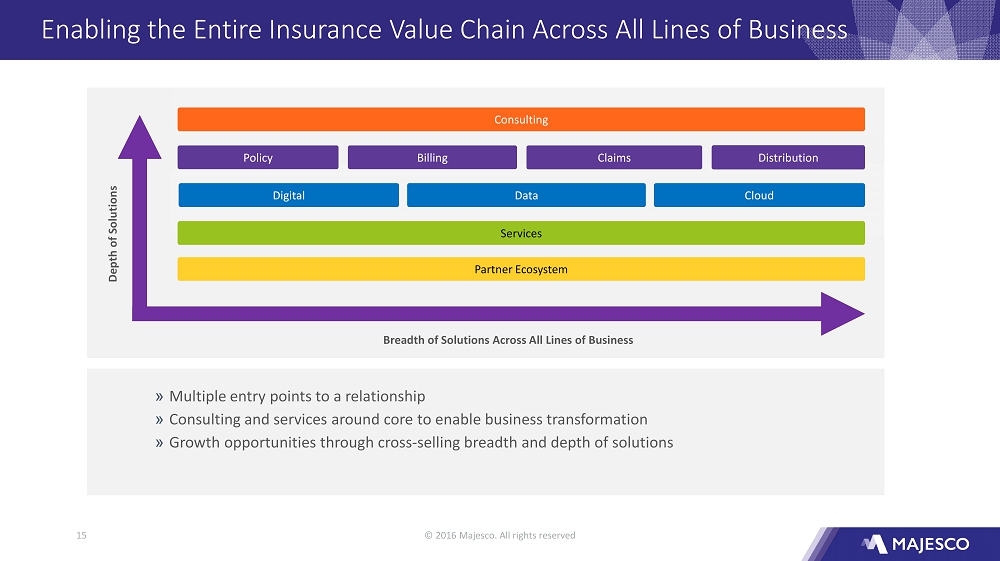

© 2016 Majesco. All rights reserved 15 Enabling the Entire Insurance Value Chain Across All Lines of Business Consulting Policy Billing Claims Digital Data Cloud Services Partner Ecosystem Breadth of Solutions Across All Lines of Business Depth of Solutions » Multiple entry points to a relationship » Consulting and services around core to enable business transformation » Growth opportunities through cross - selling breadth and depth of solutions Distribution

© 2016 Majesco. All rights reserved 16 Expanding Partner Ecosystem Majesco System Integrators Niche Solutions Industry Technology Content Deloitte IBM Pitney Bowes Appulate Splice Elagy Blueprint IBM Oracle Microsoft ISO NAMIC IASA ACORD LIMRA LOMA MGA

© 2016 Majesco. All rights reserved 17 Cloud Market Opportunity 13 Attractive to Greenfields, Start - ups and Incubators Market Opportunity Speed to Value Variable cost model Lower total cost of ownership

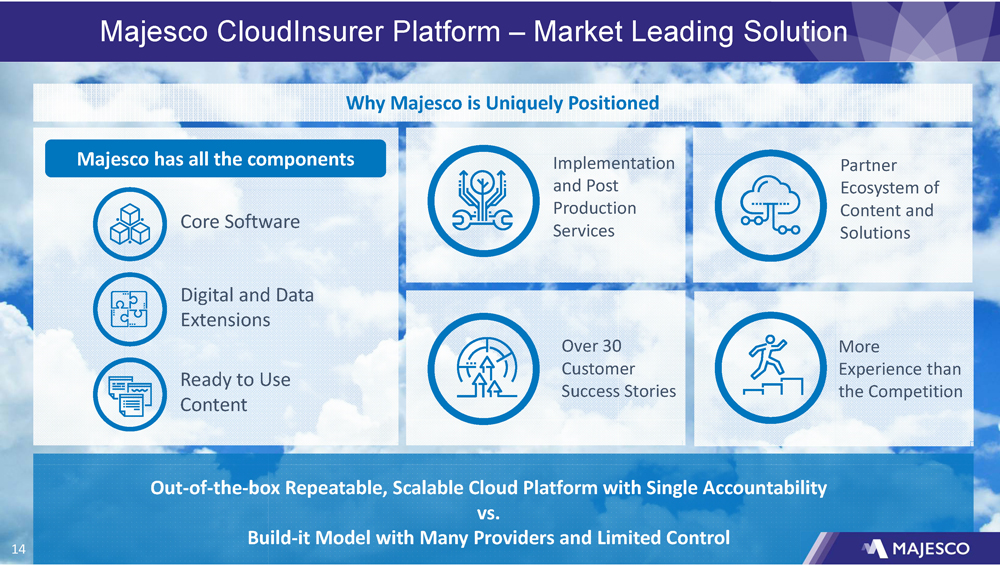

© 2016 Majesco. All rights reserved 18 Majesco CloudInsurer Platform – Market Leading Solution 14 Why Majesco is Uniquely Positioned Partner Ecosystem of Content and Solutions Implementation and Post Production Services Over 30 Customer Success Stories More Experience than the Competition Out - of - the - box Repeatable, Scalable Cloud Platform with Single Accountability vs. Build - it Model with Many Providers and Limited Control Majesco has all the components Digital and Data Extensions Core Software Ready to Use Content

© 2016 Majesco. All rights reserved 19 Our Customers We serve 149 clients globally

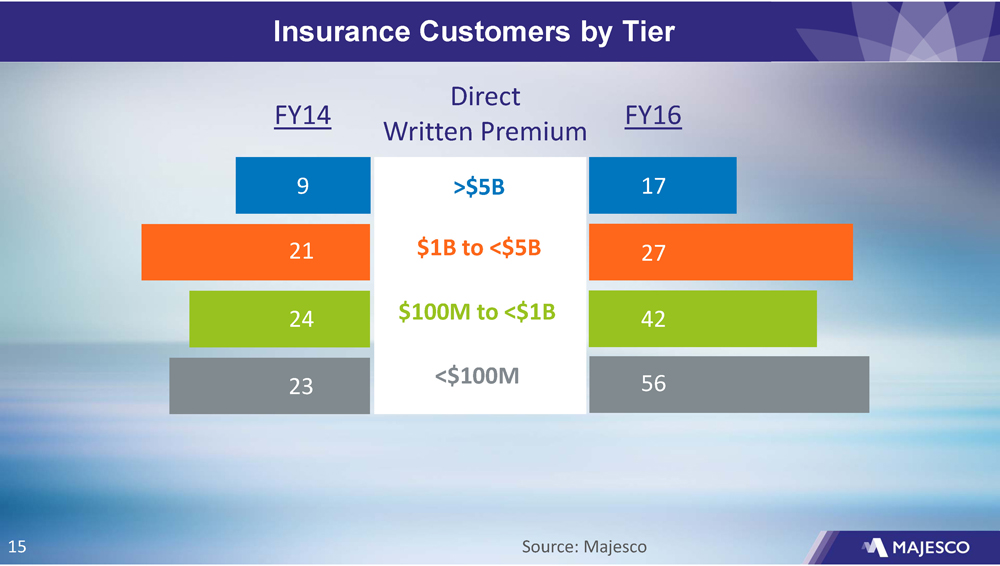

© 2016 Majesco. All rights reserved 20 Insurance Customers by Tier FY14 FY16 >$5 B 9 17 $1B to <$5B 21 27 24 $100M to <$1B 42 23 <$100M 56 15 Source: Majesco Direct Written Premium

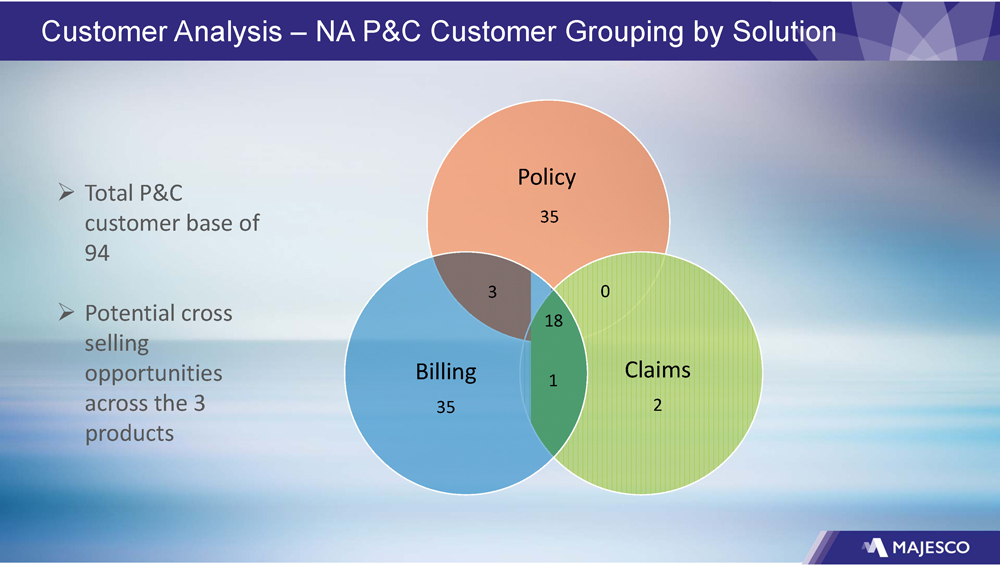

© 2016 Majesco. All rights reserved 21 Customer Analysis – NA P&C Customer Grouping by Solution Policy Billing Claims 35 3 18 0 35 1 2 » Total P&C customer base of 94 » Potential cross selling opportunities across the 3 products

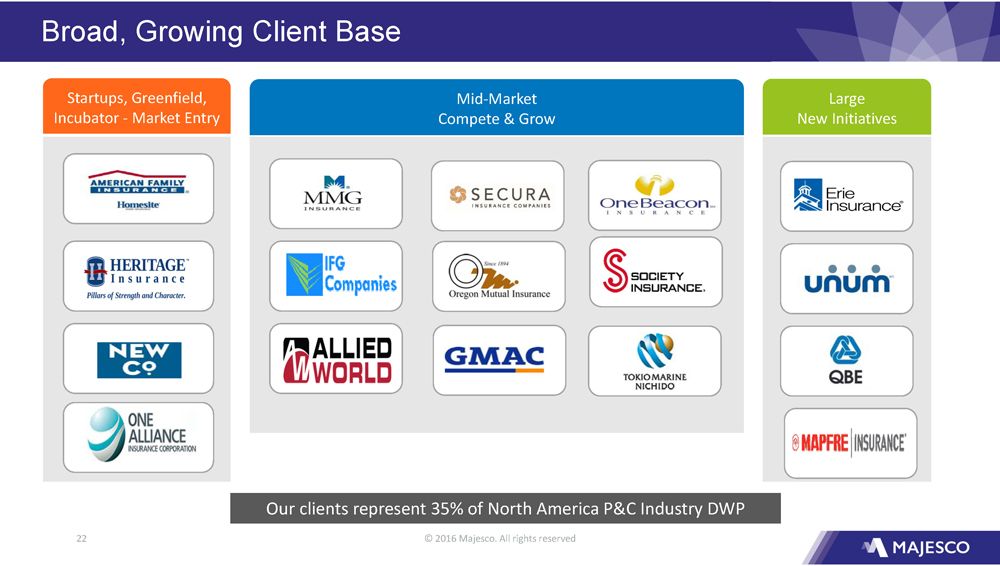

© 2016 Majesco. All rights reserved 22 Broad, Growing Client Base Startups, Greenfield, Incubator - Market Entry Mid - Market Compete & Grow Large New Initiatives Our clients represent 35% of North America P&C I ndustry DWP

© 2016 Majesco. All rights reserved 23 Growth strategy

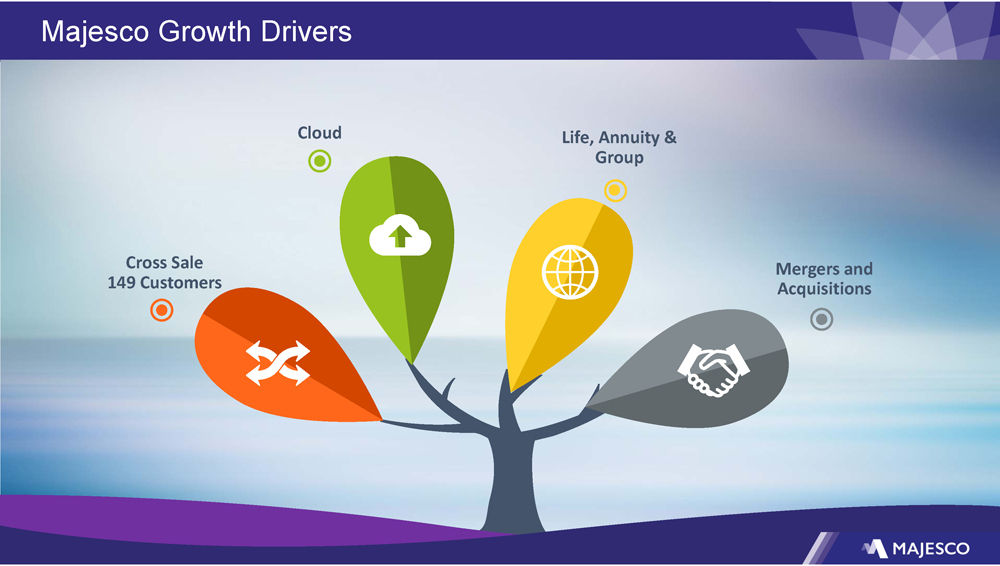

© 2016 Majesco. All rights reserved 24 Majesco Growth Drivers 24 Cross Sale 149 Customers Cloud Life, Annuity & Group Mergers and Acquisitions

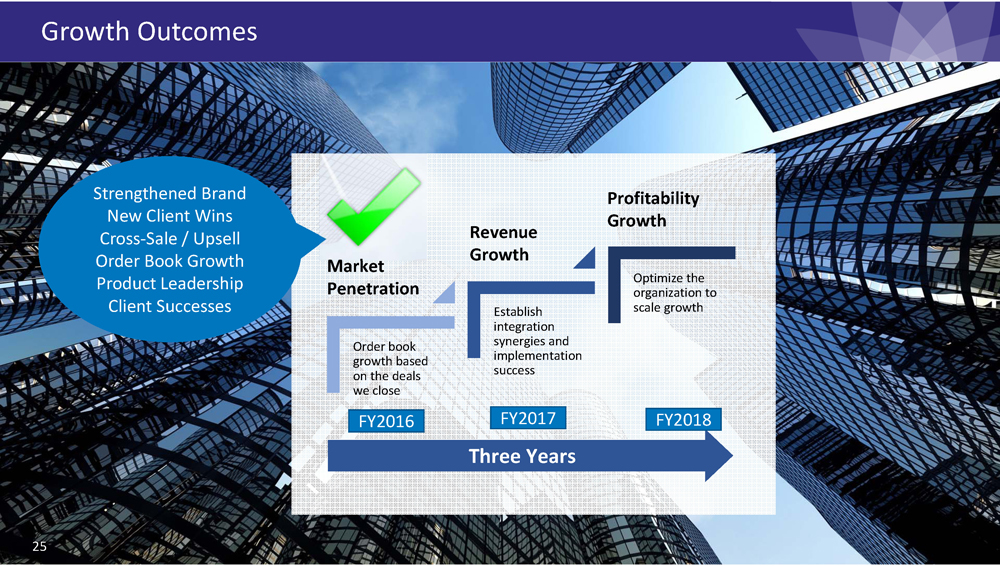

© 2016 Majesco. All rights reserved 25 Strengthened Brand New Client Wins Cross - Sale / Upsell Order Book Growth Product Leadership Client Successes Revenue Growth Market Penetration 25 Order book growth based on the deals we close Establish integration synergies and implementation success Optimize the organization to scale growth Profitability Growth Three Years Growth Outcomes FY2016 FY2017 FY2018

© 2016 Majesco. All rights reserved 26 Experienced Leadership Team Ketan Mehta Chief Executive Officer & Co - Founder Integrated four acquisition and executed insurance focus strategy. Farid Kazani Chief Financial Officer & Treasurer Deep experience in strategic technology mergers and acquisitions. Manish Shah Executive Vice President - Products Former CEO of Cover - All Technologies with over 15 years of insurance technology experience. Edward Ossie Chief Operating Officer Former President of Innovation Group and Director of Corum Technologies. Prateek Kumar Executive Vice President & P&C Industry Leader 12 years of experience in insurance technology. Tilakraj Panjabi Executive Vice President - P&C Delivery Over 26 years of experience in IT industry and majority of his experience is in insurance and retail banking domains. Chad Hersh Executive Vice President - L&A Business Ex - Managing Director, Novarica’s Insurance Practice and Ex - Senior Analyst, Celent. Bill Freitag Executive Vice President - Consulting Founder of Agile Technologies, insurance focused consulting company. Denise Garth Senior Vice President – Strategic Marketing & Innovation Insurance Company and ACORD executive; Head of Innovation and Ex - Partner, Strategy Meets Action.

© 2016 Majesco. All rights reserved 27 $4.6 Trillion market in the midst of major disruption and need for modern technology adoption Multiple growth drivers for P&C, L&A and Group Among top 3 in Core Systems, Distribution, Data, Digital and Cloud Revenue growth target of $200 to $225 M with 12% to 14% EBITDA by 2017 - 18 Track record of M&A integration with additional opportunities Majesco Strong Growth Opportunity Successful track record of growth in last year at 48.8% and last 4 years at XX%

© 2016 Majesco. All rights reserved 28 Thank You

© 2016 Majesco. All rights reserved 1 Change. Disruption. Facing the Four Realities of the Changing Industry Landscape Denise Garth, SVP

© 2016 Majesco. All rights reserved 2 2 Cautionary Language Concerning Forward - Looking Statements This presentation contains forward - looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act . These forward - looking statements are made on the basis of the current beliefs, expectations and assumptions of management, are not guarantees of performance and are subject to significant risks and uncertainty . These forward - looking statements should, therefore, be considered in light of various important factors, including those set forth in Majesco’s reports that it files from time to time with the Securities and Exchange Commission and which you should review, including those statements under “Item 1 A – Risk Factors” in Majesco’s Annual Report on Form 10 - K . Important factors that could cause actual results to differ materially from those described in forward - looking statements contained in this presentation include, but are not limited to : integration risks ; changes in economic conditions, political conditions, trade protection measures, licensing requirements and tax matters ; technology development risks ; intellectual property rights risks ; competition risks ; additional scrutiny and increased expenses as a result of being a public company ; the financial condition, financing requirements, prospects and cash flow of Majesco ; loss of strategic relationships ; changes in laws or regulations affecting the insurance industry in particular ; restrictions on immigration ; the ability and cost of retaining and recruiting key personnel ; the ability to attract new clients and retain them and the risk of loss of large customers ; continued compliance with evolving laws ; customer data and cybersecurity risk ; and Majesco’s ability to raise capital to fund future growth . These forward - looking statements should not be relied upon as predictions of future events and Majesco cannot assure you that the events or circumstances discussed or reflected in these statements will be achieved or will occur . If such forward - looking statements prove to be inaccurate, the inaccuracy may be material . You should not regard these statements as a representation or warranty by Majesco or any other person that we will achieve our objectives and plans in any specified timeframe, or at all . You are cautioned not to place undue reliance on these forward - looking statements, which speak only as of the date of this presentation . Majesco disclaims any obligation to publicly update or release any revisions to these forward - looking statements, whether as a result of new information, future events or otherwise, after the date of this press release or to reflect the occurrence of unanticipated events, except as required by law

© 2016 Majesco. All rights reserved 3 INSURANCE COMPANIES Pressure on the Insurance Industry is coming from three directions People Changing Market Demographics Changing Risk Profiles & Needs Shifting Customer Expectations Emerging Technologies Explosion of New Data Technology New Competitors Shifting & Expanding Channels Fading Industry Boundaries Market Boundaries NEW INNOVATIONS

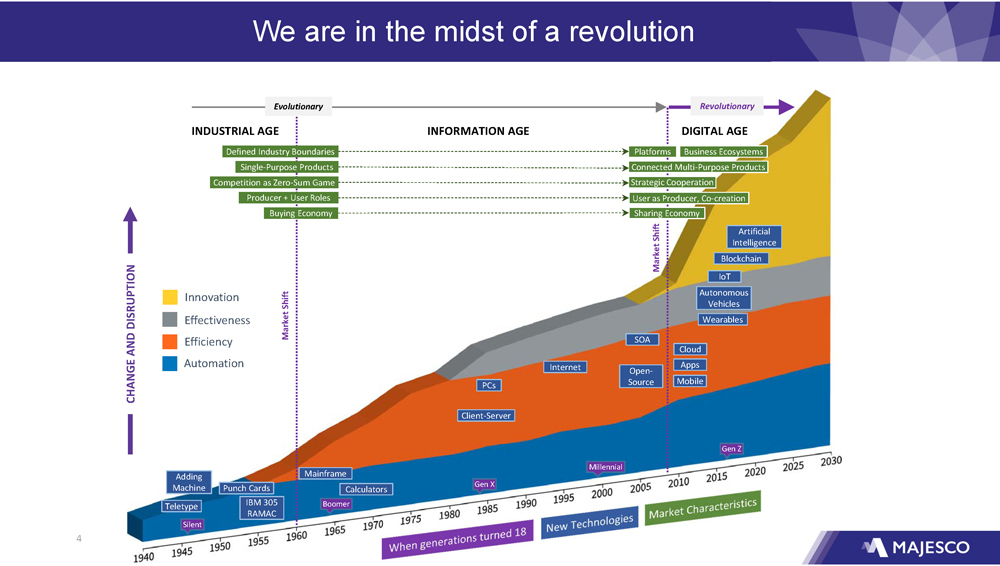

© 2016 Majesco. All rights reserved 4 We are in the midst of a revolution Silent Boomer Gen X Millennial Gen Z INDUSTRIAL AGE INFORMATION AGE DIGITAL AGE Mainframe Client - Server PCs Internet SOA Open - Source Cloud Mobile Apps IoT Wearables Autonomous Vehicles Blockchain Artificial Intelligence Teletype Adding Machine Punch Cards IBM 305 RAMAC Calculators Defined Industry Boundaries Single - Purpose Products Competition as Zero - Sum Game Producer + User Roles Business Ecosystems Platforms Connected Multi - Purpose Products Strategic Cooperation User as Producer, Co - creation Buying Economy Sharing Economy Revolutionary CHANGE AND DISRUPTION Evolutionary Market Shift Market Shift Innovation Effectiveness Efficiency Automation

© 2016 Majesco. All rights reserved 5 People

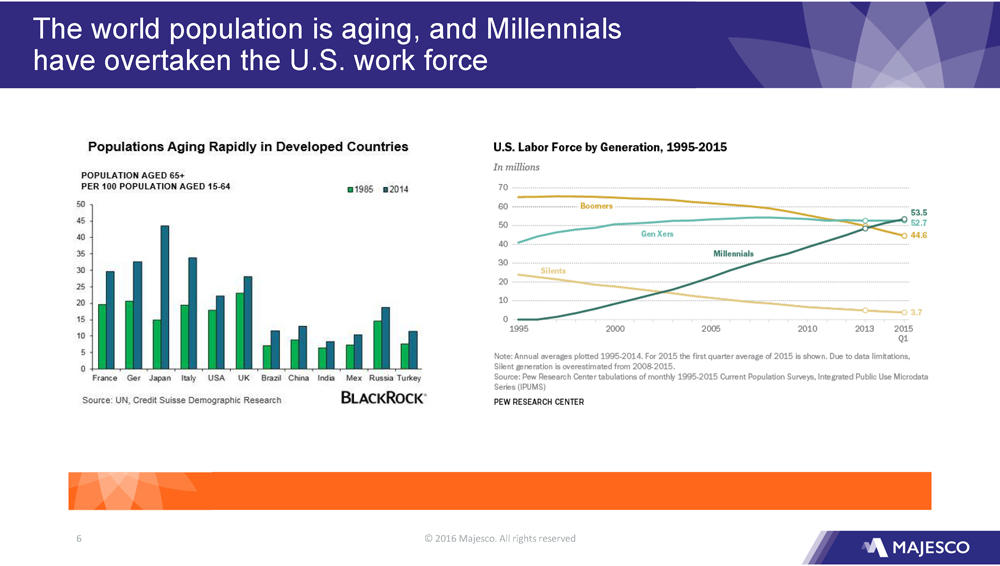

© 2016 Majesco. All rights reserved 6 The world population is aging, and Millennials have overtaken the U.S. work force

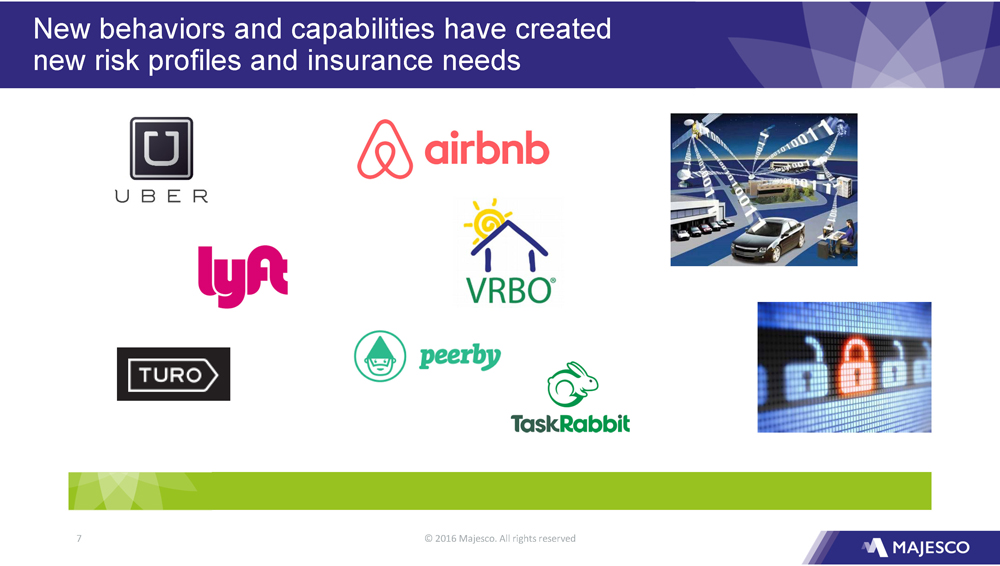

© 2016 Majesco. All rights reserved 7 New behaviors and capabilities have created new risk profiles and insurance needs

© 2016 Majesco. All rights reserved 8 Customers’ expectations are being set by non - insurance companies

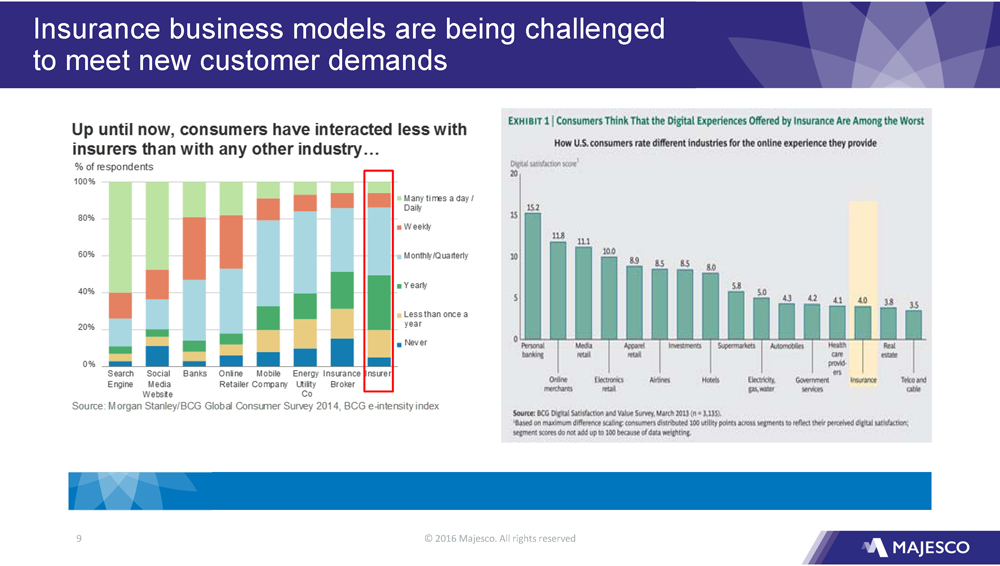

© 2016 Majesco. All rights reserved 9 Insurance business models are being challenged to meet new customer demands

© 2016 Majesco. All rights reserved 10 Technology

© 2016 Majesco. All rights reserved 11 Advances in technology and data create new capabilities – and new insurance needs and opportunities

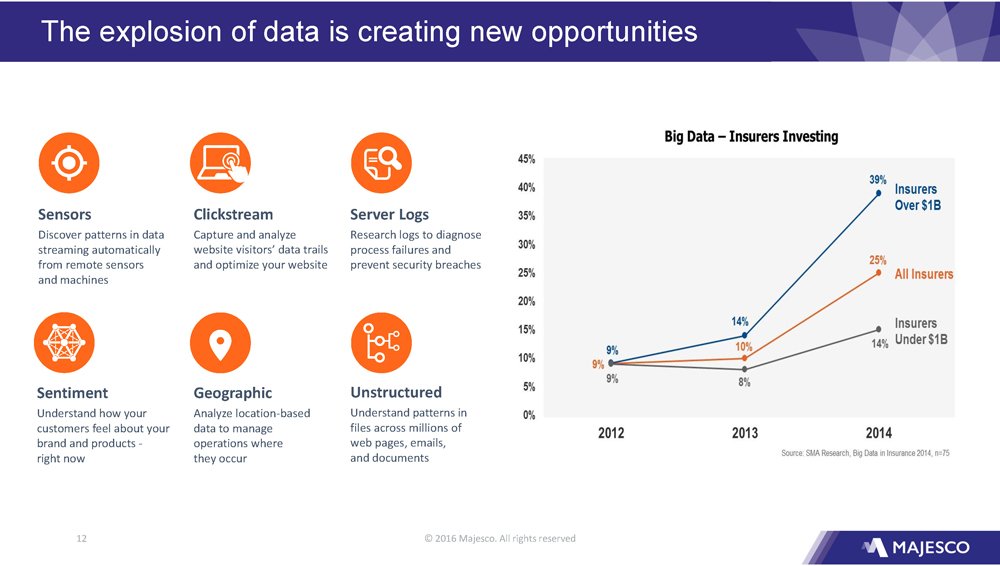

© 2016 Majesco. All rights reserved 12 The explosion of data is creating new opportunities Sensors Discover patterns in data streaming automatically from remote sensors and machines Geographic Analyze location - based data to manage operations where they occur Server Logs Research logs to diagnose process failures and prevent security breaches Unstructured Understand patterns in files across millions of web pages, emails, and documents Sentiment Understand how your customers feel about your brand and products - right now Clickstream Capture and analyze website visitors’ data trails and optimize your website

© 2016 Majesco. All rights reserved 13 Market Boundaries

© 2016 Majesco. All rights reserved 14 New and established companies are creating innovative new business models and products

© 2016 Majesco. All rights reserved 15 New companies are leveraging expectations and capabilities to disrupt the insurance value chain Berkshire Hathaway Direct

© 2016 Majesco. All rights reserved 16 Non - insurance brands are leveraging expectations and capabilities to disrupt the insurance value chain +

© 2016 Majesco. All rights reserved 17 The Four Realities

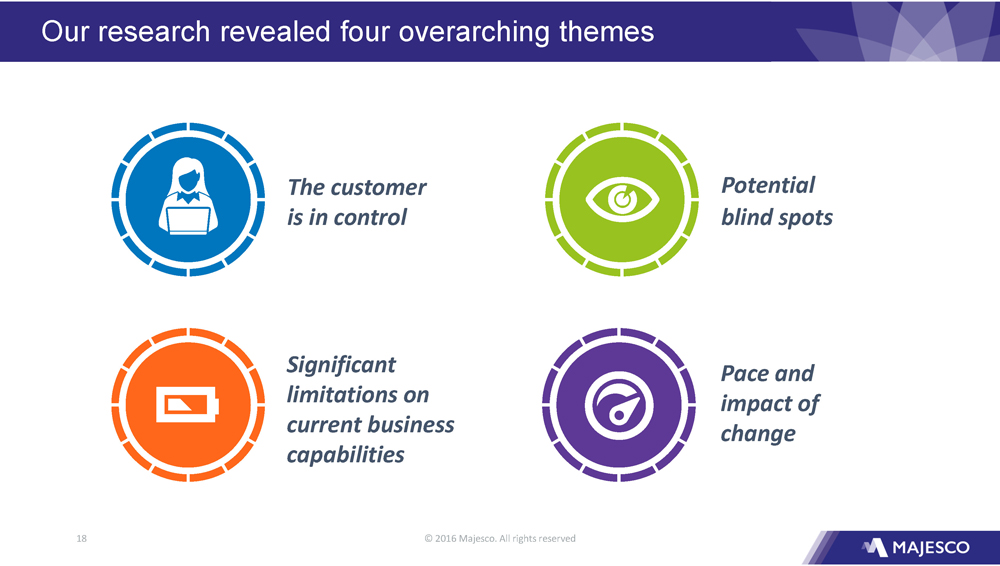

© 2016 Majesco. All rights reserved 18 Our research revealed four overarching themes The customer is in control Significant limitations on current business capabilities Pace and impact of change Potential blind spots

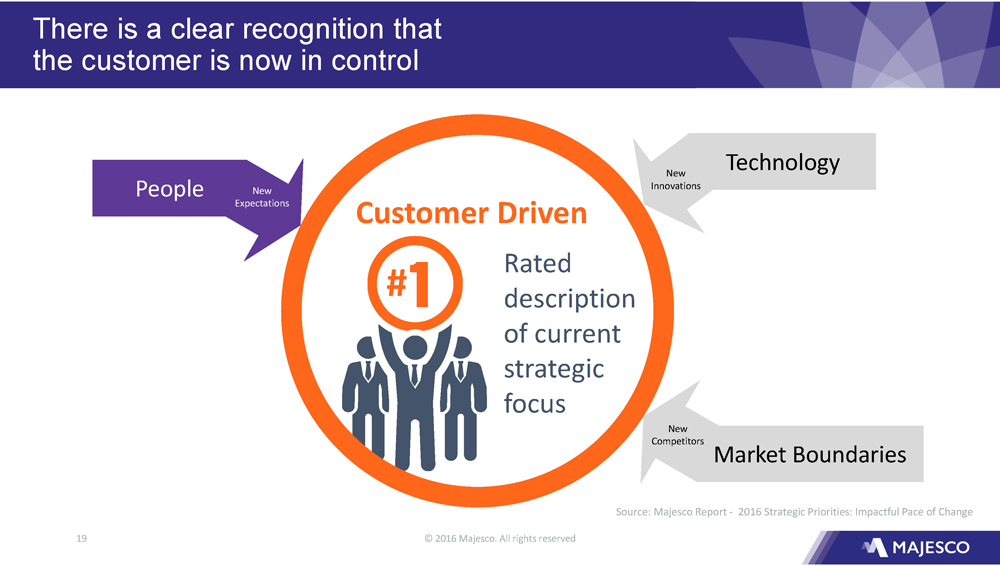

© 2016 Majesco. All rights reserved 19 There is a clear recognition that the customer is now in control Customer Driven Rated description of current strategic focus # Technology New Innovations Market Boundaries New Competitors People New Expectations Source: Majesco Report - 2016 Strategic Priorities: Impactful Pace of Change

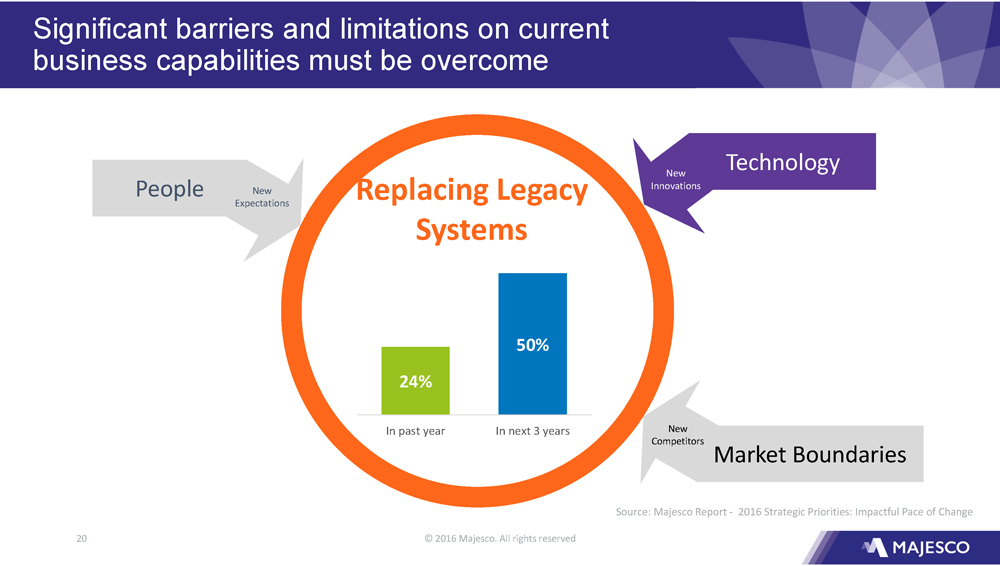

© 2016 Majesco. All rights reserved 20 Significant barriers and limitations on current business capabilities must be overcome Replacing Legacy Systems Technology New Innovations Market Boundaries New Competitors People New Expectations 24% 50% In past year In next 3 years Source: Majesco Report - 2016 Strategic Priorities: Impactful Pace of Change

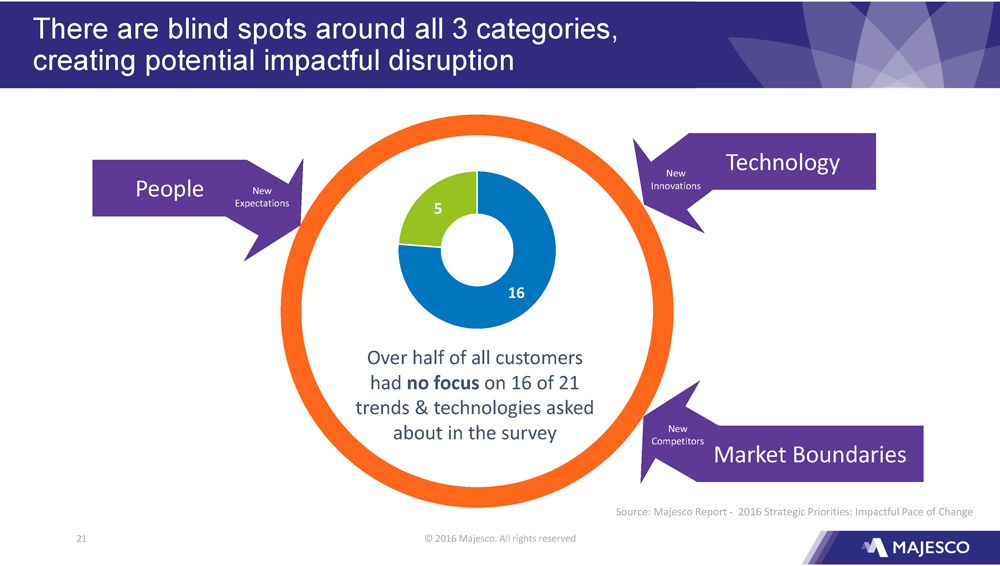

© 2016 Majesco. All rights reserved 21 There are blind spots around all 3 categories, creating potential impactful disruption Technology New Innovations Market Boundaries New Competitors People New Expectations 16 5 Over half of all customers had no focus on 16 of 21 trends & technologies asked about in the survey Source: Majesco Report - 2016 Strategic Priorities: Impactful Pace of Change

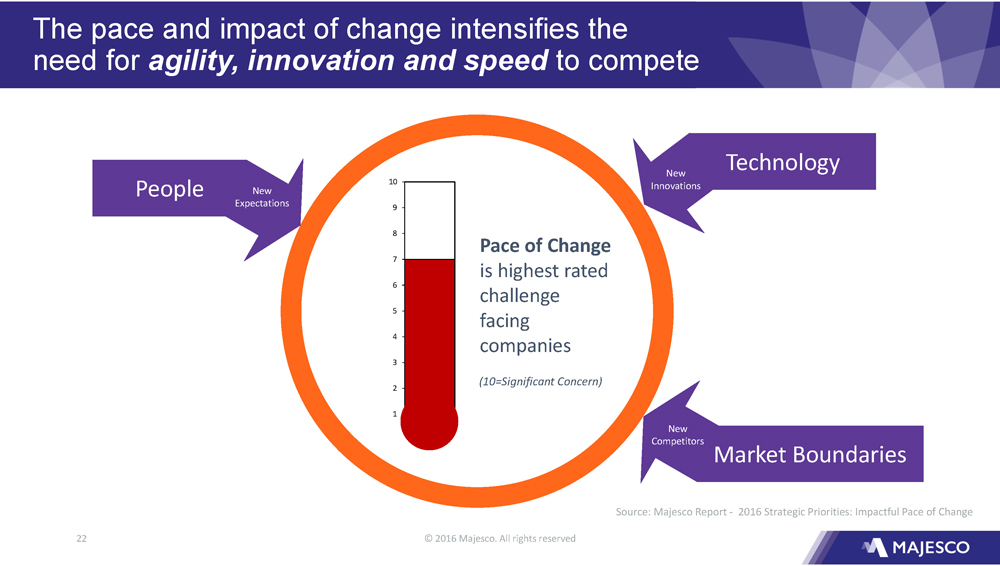

© 2016 Majesco. All rights reserved 22 The pace and impact of change intensifies the need for agility, innovation and speed to compete Technology New Innovations Market Boundaries New Competitors People New Expectations Pace of Change is highest rated challenge facing companies (10=Significant Concern) 1 2 3 4 5 6 7 8 9 10 Source: Majesco Report - 2016 Strategic Priorities: Impactful Pace of Change

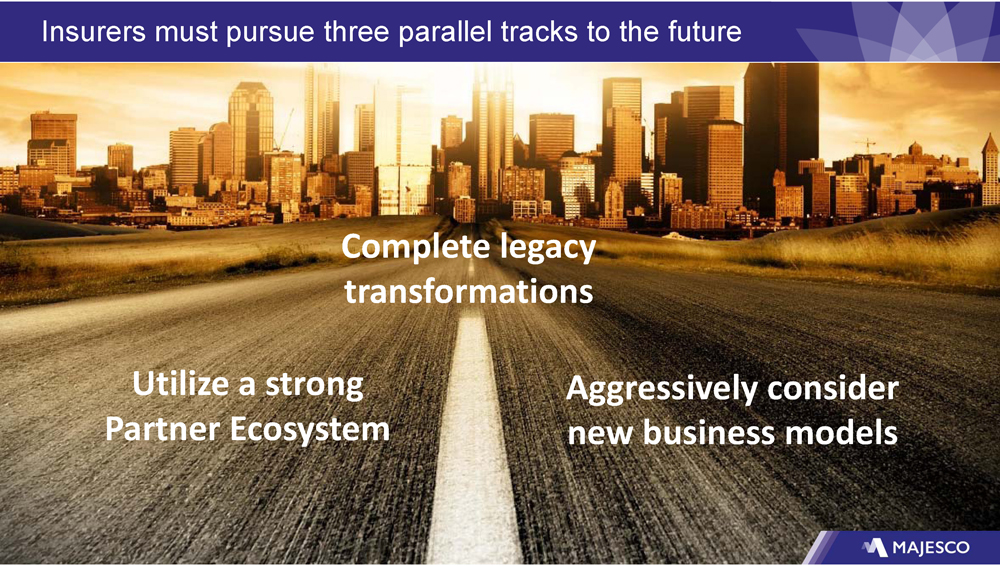

© 2016 Majesco. All rights reserved 23 Insurers must pursue three parallel tracks to the future Complete legacy transformations U tilize a strong Partner E cosystem Aggressively consider new business models

© 2016 Majesco. All rights reserved 24 www.majesco.com

© 2016 Majesco. All rights reserved 1 Customer Panel Ed Ossie, COO Moderator

© 2016 Majesco. All rights reserved 2 2 Cautionary Language Concerning Forward - Looking Statements This presentation contains forward - looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act . These forward - looking statements are made on the basis of the current beliefs, expectations and assumptions of management, are not guarantees of performance and are subject to significant risks and uncertainty . These forward - looking statements should, therefore, be considered in light of various important factors, including those set forth in Majesco’s reports that it files from time to time with the Securities and Exchange Commission and which you should review, including those statements under “Item 1 A – Risk Factors” in Majesco’s Annual Report on Form 10 - K . Important factors that could cause actual results to differ materially from those described in forward - looking statements contained in this presentation include, but are not limited to : integration risks ; changes in economic conditions, political conditions, trade protection measures, licensing requirements and tax matters ; technology development risks ; intellectual property rights risks ; competition risks ; additional scrutiny and increased expenses as a result of being a public company ; the financial condition, financing requirements, prospects and cash flow of Majesco ; loss of strategic relationships ; changes in laws or regulations affecting the insurance industry in particular ; restrictions on immigration ; the ability and cost of retaining and recruiting key personnel ; the ability to attract new clients and retain them and the risk of loss of large customers ; continued compliance with evolving laws ; customer data and cybersecurity risk ; and Majesco’s ability to raise capital to fund future growth . These forward - looking statements should not be relied upon as predictions of future events and Majesco cannot assure you that the events or circumstances discussed or reflected in these statements will be achieved or will occur . If such forward - looking statements prove to be inaccurate, the inaccuracy may be material . You should not regard these statements as a representation or warranty by Majesco or any other person that we will achieve our objectives and plans in any specified timeframe, or at all . You are cautioned not to place undue reliance on these forward - looking statements, which speak only as of the date of this presentation . Majesco disclaims any obligation to publicly update or release any revisions to these forward - looking statements, whether as a result of new information, future events or otherwise, after the date of this press release or to reflect the occurrence of unanticipated events, except as required by law

© 2016 Majesco. All rights reserved 3 Customer Profiles Ernie Garateix , Chief Operating Officer Heritage Insurance Patrick Hesidence , Vice President of Billing Erie Insurance Gregg Nickerson , Chief Information Officer Mapfre Insurance US

© 2016 Majesco. All rights reserved 4 Thank you

© 2016 Majesco. All rights reserved 1 Property & Casualty Business Prateek Kumar, EVP

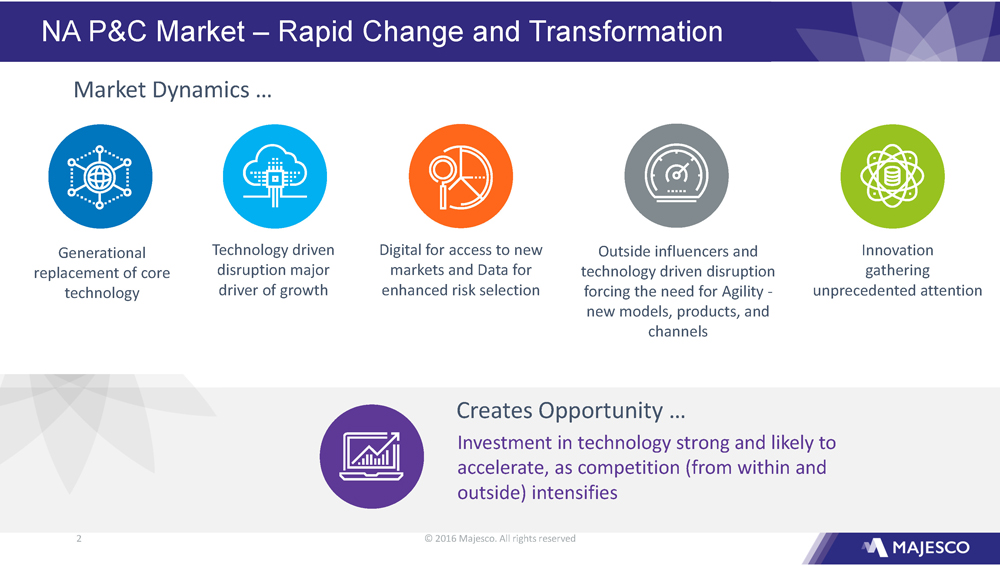

© 2016 Majesco. All rights reserved 2 NA P&C Market – Rapid Change and Transformation Generational replacement of core technology Technology driven disruption major driver of growth Digital for access to new markets and Data for enhanced risk selection Outside influencers and technology driven disruption forcing the need for Agility - new models, products , and channels Investment in technology strong and likely to accelerate, as competition (from within and outside) intensifies Innovation gathering unprecedented attention Market Dynamics … Creates Opportunity …

© 2016 Majesco. All rights reserved 3 The Market Opportunity 3 Combined business demands creates greater market opportunity today and in future E merging Greenfields, Start - ups & Incubator Business Models Traditional business core system transformation continues ▪ Growing gap between IT and Business ▪ Focus on NEW business vs. replace old ▪ Shift from “build to specifications” to “ready to use” ▪ “Solution as a Service” gaining momentum

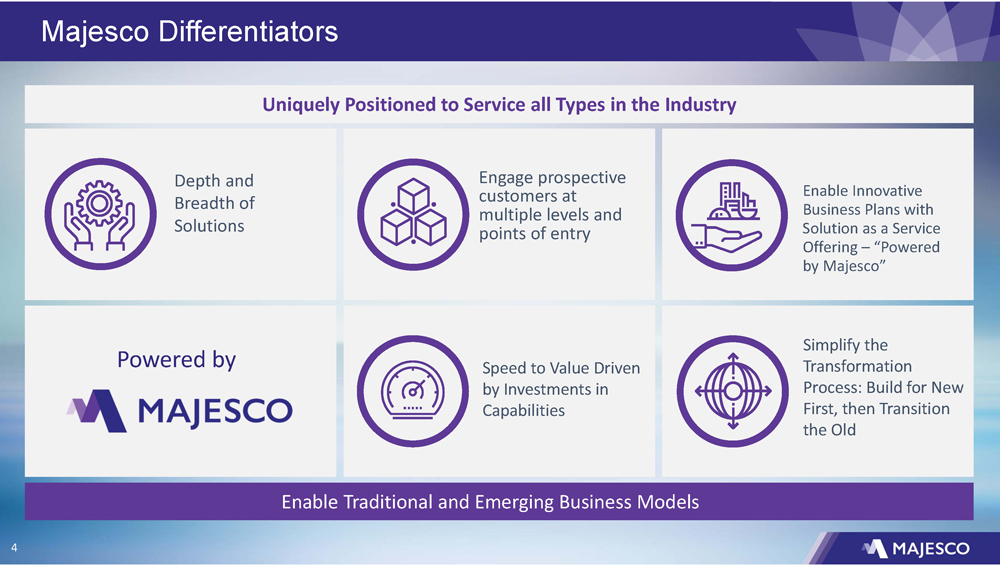

© 2016 Majesco. All rights reserved 4 Majesco Differentiators 4 Uniquely Positioned to Service all Types in the Industry Enable Traditional and Emerging Business Models Depth and Breadth of Solutions Engage prospective customers at multiple levels and points of entry Speed to Value Driven by Investments in Capabilities Powered by Enable Innovative Business Plans with Solution as a Service Offering – “Powered by Majesco” Simplify the Transformation Process: Build for New First, then Transition the Old

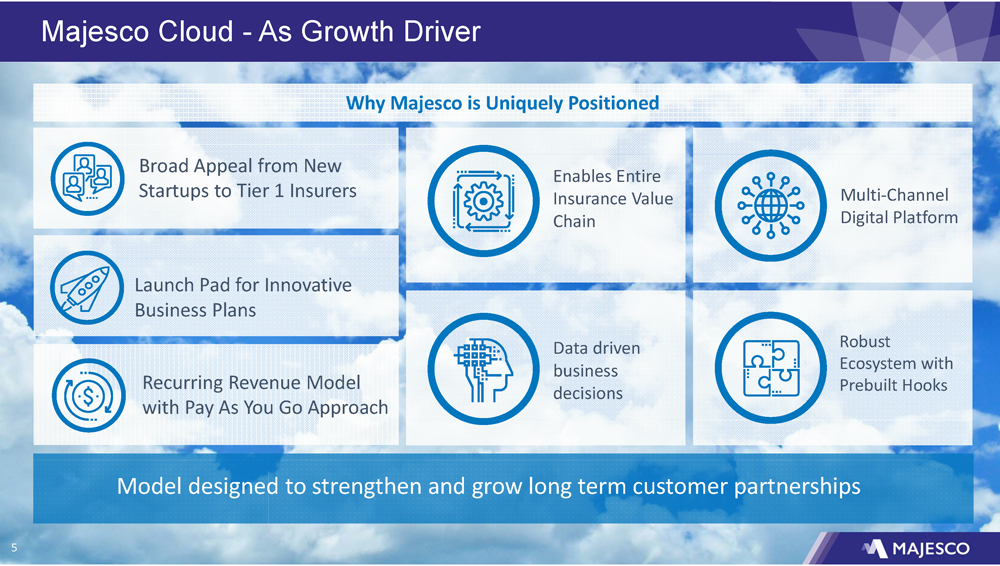

© 2016 Majesco. All rights reserved 5 Majesco Cloud - As Growth Driver 5 Why Majesco is Uniquely Positioned Multi - Channel Digital Platform Enables Entire Insurance Value Chain Robust Ecosystem with P rebuilt Hooks Data driven business decisions Model designed to strengthen and grow long term customer partnerships Launch Pad for Innovative Business Plans Broad Appeal from New S tartups to Tier 1 Insurers Recurring Revenue Model with Pay As You Go Approach

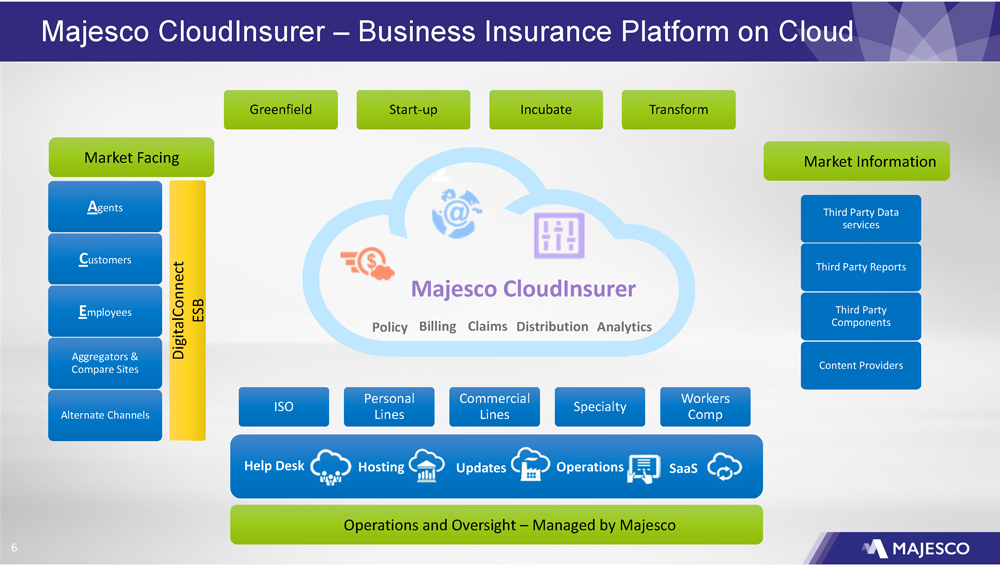

© 2016 Majesco. All rights reserved 6 Majesco CloudInsurer – Business Insurance Platform on Cloud 6 Greenfield Start - up Incubate Transform A gents C ustomers E mployees Aggregators & Compare Sites Alternate Channels Market Facing DigitalConnect ESB ISO Personal Lines Commercial Lines Specialty Workers Comp Market Information Policy Majesco CloudInsurer Billing Claims Distribution Analytics Help Desk Hosting Updates SaaS Operations Third Party Data services Third Party Reports Third Party Components Content Providers Operations and Oversight – Managed by Majesco

© 2016 Majesco. All rights reserved 7 Thank You

© 2016 Majesco. All rights reserved 1 Life, Annuities, and Group Chad Hersh, EVP

© 2016 Majesco. All rights reserved 2 2 Cautionary Language Concerning Forward - Looking Statements This presentation contains forward - looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act . These forward - looking statements are made on the basis of the current beliefs, expectations and assumptions of management, are not guarantees of performance and are subject to significant risks and uncertainty . These forward - looking statements should, therefore, be considered in light of various important factors, including those set forth in Majesco’s reports that it files from time to time with the Securities and Exchange Commission and which you should review, including those statements under “Item 1 A – Risk Factors” in Majesco’s Annual Report on Form 10 - K . Important factors that could cause actual results to differ materially from those described in forward - looking statements contained in this presentation include, but are not limited to : integration risks ; changes in economic conditions, political conditions, trade protection measures, licensing requirements and tax matters ; technology development risks ; intellectual property rights risks ; competition risks ; additional scrutiny and increased expenses as a result of being a public company ; the financial condition, financing requirements, prospects and cash flow of Majesco ; loss of strategic relationships ; changes in laws or regulations affecting the insurance industry in particular ; restrictions on immigration ; the ability and cost of retaining and recruiting key personnel ; the ability to attract new clients and retain them and the risk of loss of large customers ; continued compliance with evolving laws ; customer data and cybersecurity risk ; and Majesco’s ability to raise capital to fund future growth . These forward - looking statements should not be relied upon as predictions of future events and Majesco cannot assure you that the events or circumstances discussed or reflected in these statements will be achieved or will occur . If such forward - looking statements prove to be inaccurate, the inaccuracy may be material . You should not regard these statements as a representation or warranty by Majesco or any other person that we will achieve our objectives and plans in any specified timeframe, or at all . You are cautioned not to place undue reliance on these forward - looking statements, which speak only as of the date of this presentation . Majesco disclaims any obligation to publicly update or release any revisions to these forward - looking statements, whether as a result of new information, future events or otherwise, after the date of this press release or to reflect the occurrence of unanticipated events, except as required by law

© 2016 Majesco. All rights reserved 3 The North American L&A and Group Market – A Rapidly Changing Landscape Underinvestment in Technology Overcoming legacy challenges has been put off by many carriers Limited Competition Few modern solutions offered with little competition compared to P/C Technology Investment Stagnation The financial crisis brought L&A technology investment to a screeching halt in 2007 Lack of Modern, Compelling Software Options Most vendors limited investments for many years, creating a void of modern software options for insurers Market Dynamics … Creates Opportunity … The net result is tremendous pent - up demand for modern core systems

© 2016 Majesco. All rights reserved 4 Majesco Market Opportunity More RFI/RFP activity in Group than seen in years due to selection by a Top 5 Group insurer, strengthening our market visibility Fewer competitors in Group than Individual and P/C; Offers opportunity to rapidly achieve market - leading position Growing interest with Individual L&A insurers looking to modernize, especially those expanding to Group Increasing demand for distribution management and digital solutions due to a changing market landscape Majesco L&A North America Market Opportunity Potential to dominate Group market in UK where two of our clients represent 42% of group protection market Additional growth potential in Australia / NZ for individual and group products Provides gateway to the APAC market that needs combined Individual , Group , and Health products Expanding opportunities in Latin and South America for modern core software solutions Majesco International Market Opportunity

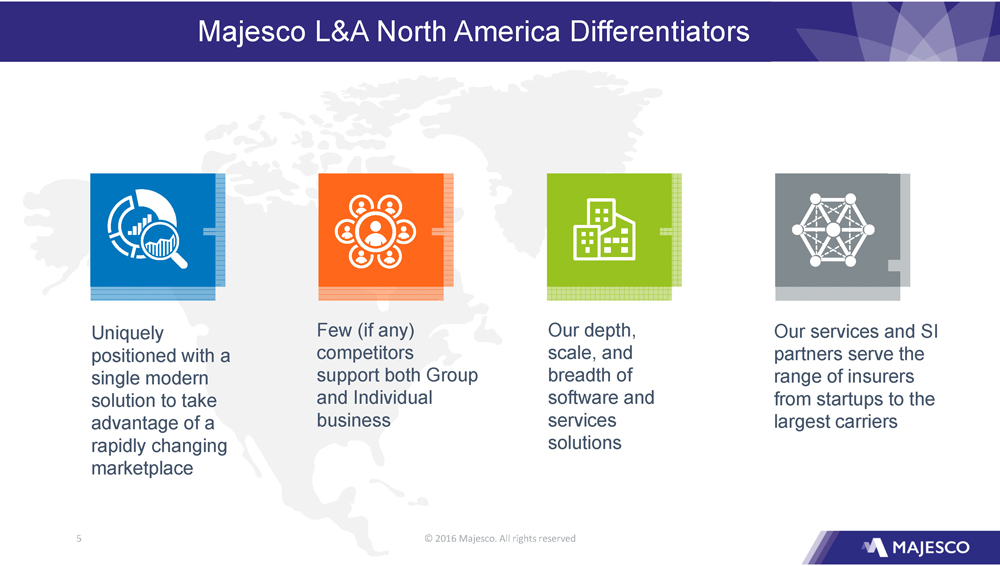

© 2016 Majesco. All rights reserved 5 Majesco L&A North America Differentiators Uniquely positioned with a single modern solution to take advantage of a rapidly changing marketplace Few (if any) competitors support both Group and I ndividual business Our depth, scale, and breadth of software and services solutions Our services and SI partners serve the range of insurers from startups to the largest carriers

© 2016 Majesco. All rights reserved 6 L&A and Group As Growth Driver Potential to grow significantly over the next few years Opportunity to be the Group market leader Aim to be a top 3 North America vendor for Individual L&A Internationally, strong market activity for Group and Individual Shift to market acceptance of annual license fees and cloud to grow recurring revenues 6

© 2016 Majesco. All rights reserved 7 Thank you

© 2016 Majesco. All rights reserved 1 Majesco Analysts Day Product Update Manish Shah, EVP

© 2016 Majesco. All rights reserved 2 2 Cautionary Language Concerning Forward - Looking Statements This presentation contains forward - looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act . These forward - looking statements are made on the basis of the current beliefs, expectations and assumptions of management, are not guarantees of performance and are subject to significant risks and uncertainty . These forward - looking statements should, therefore, be considered in light of various important factors, including those set forth in Majesco’s reports that it files from time to time with the Securities and Exchange Commission and which you should review, including those statements under “Item 1 A – Risk Factors” in Majesco’s Annual Report on Form 10 - K . Important factors that could cause actual results to differ materially from those described in forward - looking statements contained in this presentation include, but are not limited to : integration risks ; changes in economic conditions, political conditions, trade protection measures, licensing requirements and tax matters ; technology development risks ; intellectual property rights risks ; competition risks ; additional scrutiny and increased expenses as a result of being a public company ; the financial condition, financing requirements, prospects and cash flow of Majesco ; loss of strategic relationships ; changes in laws or regulations affecting the insurance industry in particular ; restrictions on immigration ; the ability and cost of retaining and recruiting key personnel ; the ability to attract new clients and retain them and the risk of loss of large customers ; continued compliance with evolving laws ; customer data and cybersecurity risk ; and Majesco’s ability to raise capital to fund future growth . These forward - looking statements should not be relied upon as predictions of future events and Majesco cannot assure you that the events or circumstances discussed or reflected in these statements will be achieved or will occur . If such forward - looking statements prove to be inaccurate, the inaccuracy may be material . You should not regard these statements as a representation or warranty by Majesco or any other person that we will achieve our objectives and plans in any specified timeframe, or at all . You are cautioned not to place undue reliance on these forward - looking statements, which speak only as of the date of this presentation . Majesco disclaims any obligation to publicly update or release any revisions to these forward - looking statements, whether as a result of new information, future events or otherwise, after the date of this press release or to reflect the occurrence of unanticipated events, except as required by law

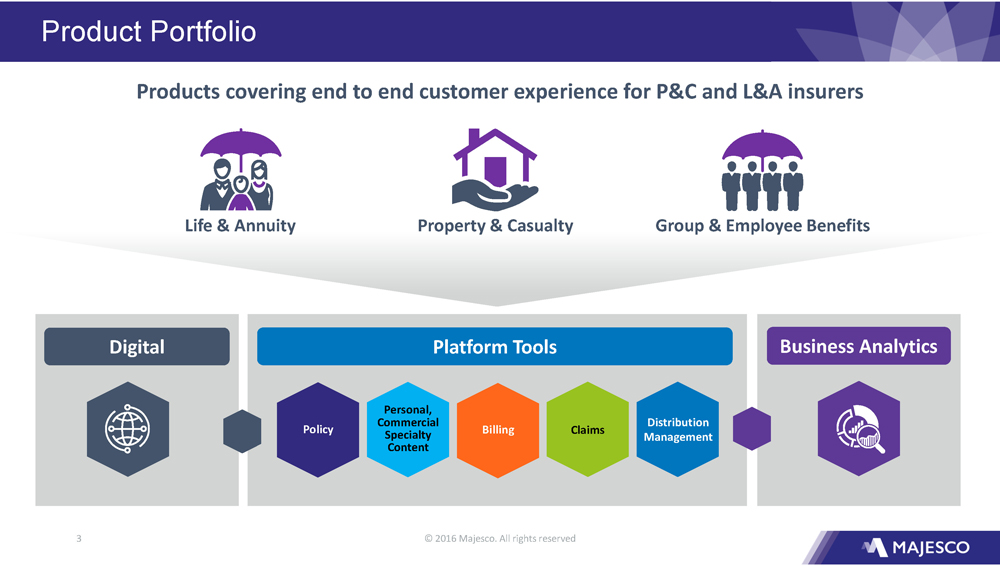

© 2016 Majesco. All rights reserved 3 Product Portfolio Digital Business Analytics Platform Tools Billing Policy Personal, Commercial Specialty Content Claims Distribution Management Property & Casualty Life & Annuity Group & Employee Benefits Products covering end to end customer experience for P&C and L&A insurers

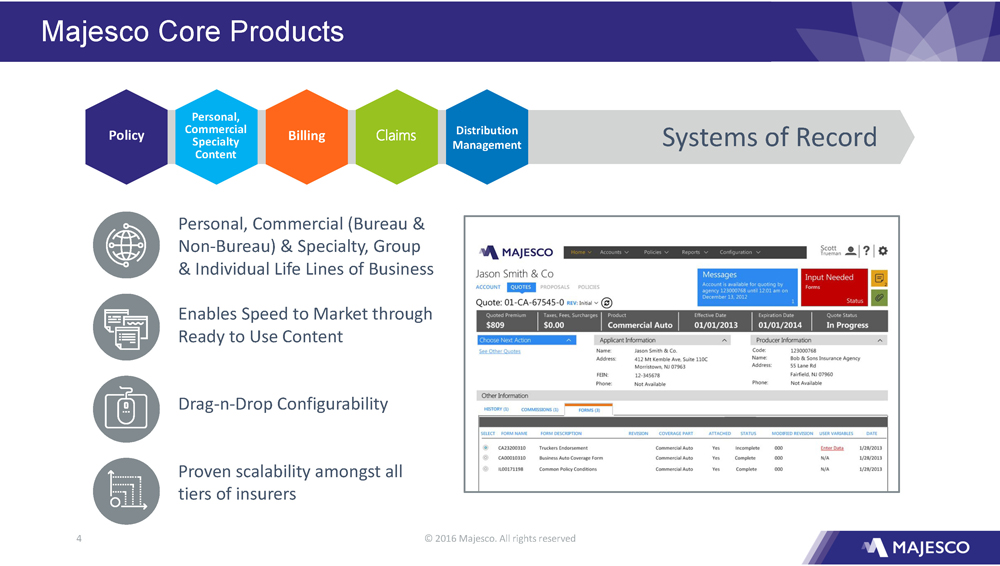

© 2016 Majesco. All rights reserved 4 Majesco Core Products Systems of Record Billing Policy Personal, Commercial Specialty Content Distribution Management Claims Personal, Commercial (Bureau & Non - Bureau) & Specialty, Group & Individual Life Lines of Business Enables Speed to Market through Ready to Use Content Drag - n - Drop Configurability Proven scalability amongst all tiers of insurers

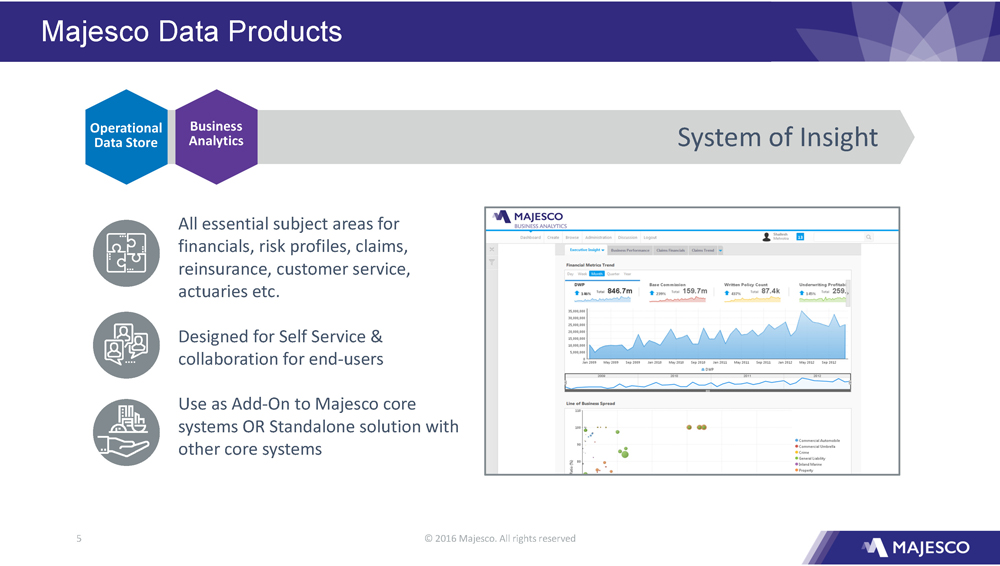

© 2016 Majesco. All rights reserved 5 Majesco Data Products System of Insight Operational Data Store Business Analytics All essential subject areas for financials, risk profiles, claims, reinsurance, customer service, actuaries etc. Designed for Self Service & collaboration for end - users Use as Add - On to Majesco core systems OR Standalone solution with other core systems

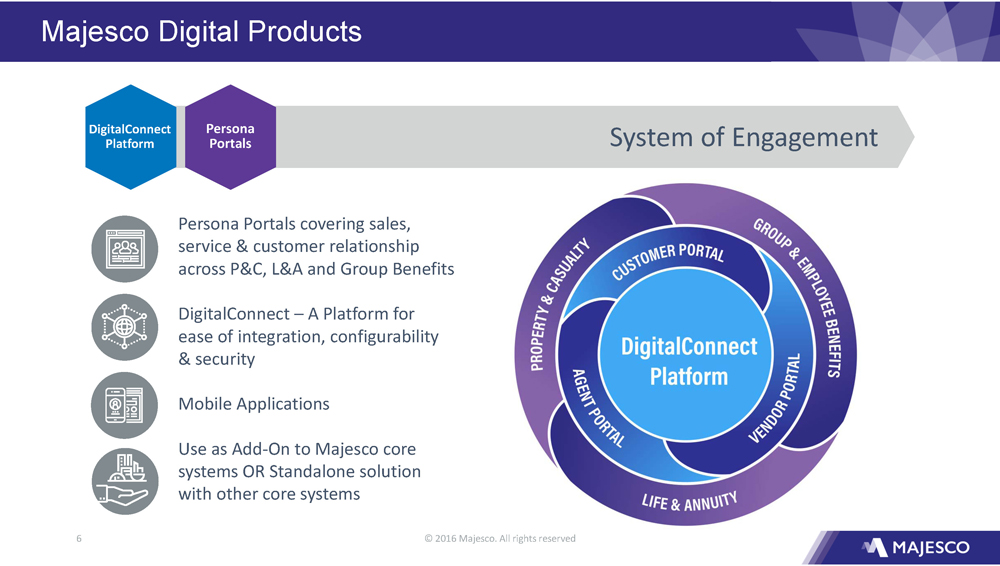

© 2016 Majesco. All rights reserved 6 Majesco Digital Products System of Engagement DigitalConnect Platform Persona Portals Persona Portals covering sales, service & customer relationship across P&C, L&A and Group Benefits DigitalConnect – A Platform for ease of integration, configurability & security Mobile Applications Use as Add - On to Majesco core systems OR Standalone solution with other core systems

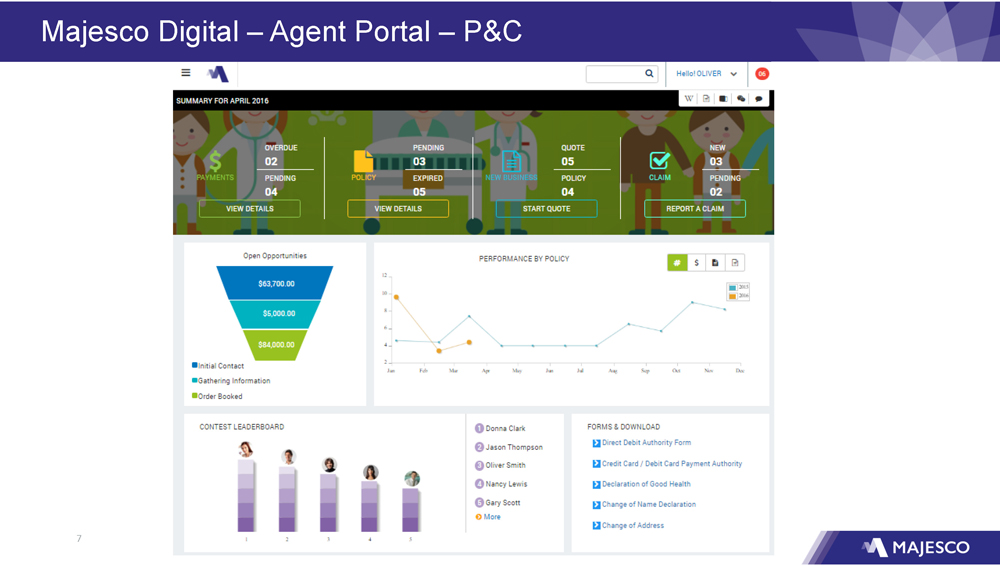

© 2016 Majesco. All rights reserved 7 Majesco Digital – Agent Portal – P&C Life & Annuity

© 2016 Majesco. All rights reserved 8 Majesco Digital – Customer Portal – L&A Life & Annuity

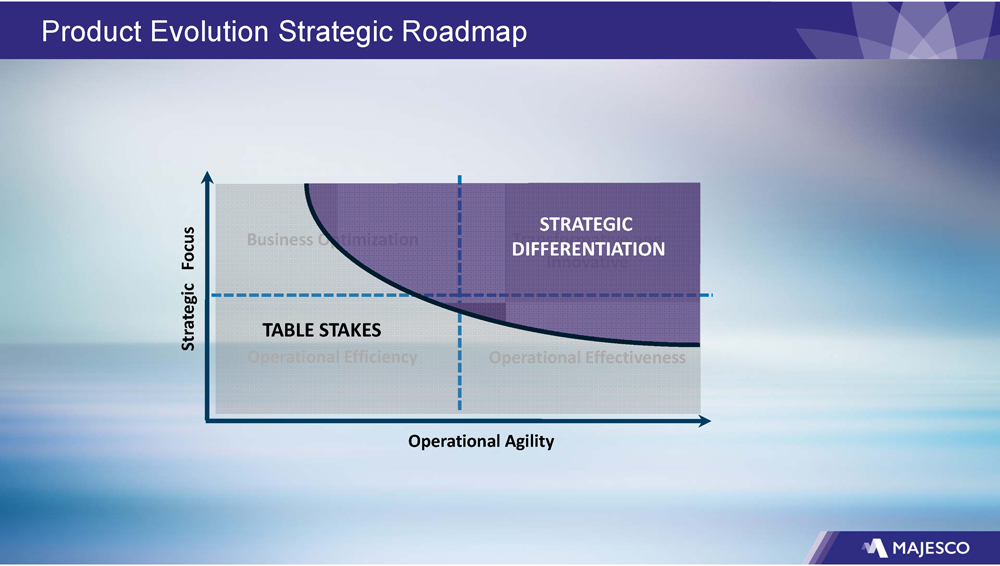

© 2016 Majesco. All rights reserved 9 Product Evolution Strategic Roadmap Strategic Focus Operational Agility Operational Effectiveness Transformative and Innovative Business Optimization Operational Efficiency TABLE STAKES STRATEGIC DIFFERENTIATION

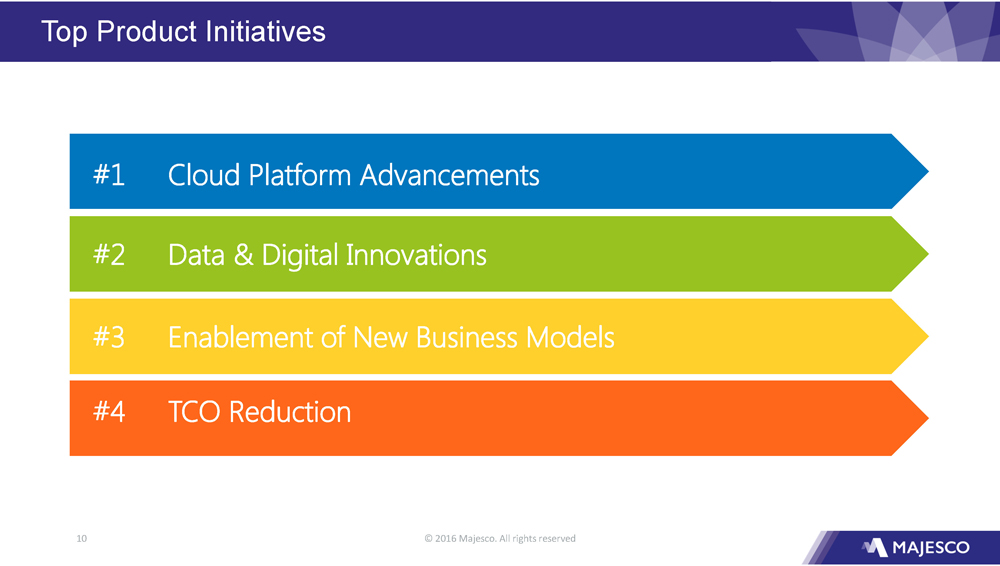

© 2016 Majesco. All rights reserved 10 Top Product Initiatives #1 Cloud Platform Advancements #2 Data & Digital Innovations #3 Enablement of New Business Models #4 TCO Reduction

© 2016 Majesco. All rights reserved 11 #1 Cloud Platform Advancements CLOUD INVESTMENT BY INSURERS Majesco Cloud SOFTWARE ANALYTICS DATA CENTERS CONTENT TOOLS INTEGRATION PERFORMANCE SECURITY ADMINISTRATION PARTNER SERVICES SUPPORT SERVICES AGENT SELF SERVICE CUSTOMER SELF SERVICE UNDERWRITING OMNI CHANNELS INSIGHTS & INTELLIGENCE

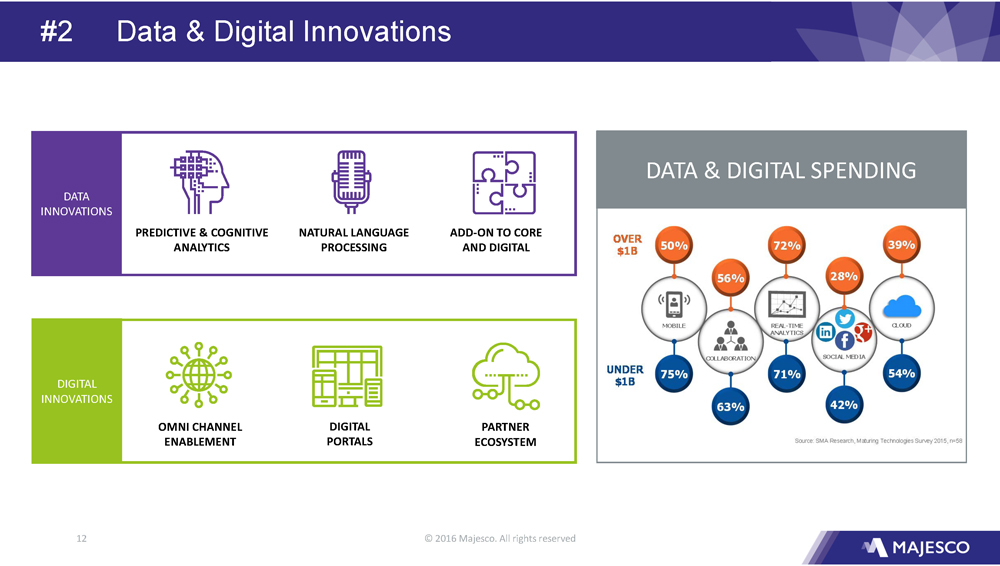

© 2016 Majesco. All rights reserved 12 #2 Data & Digital Innovations PREDICTIVE & COGNITIVE ANALYTICS DIGITAL PORTALS ADD - ON TO CORE AND DIGITAL NATURAL LANGUAGE PROCESSING OMNI CHANNEL ENABLEMENT PARTNER ECOSYSTEM DATA INNOVATIONS DIGITAL INNOVATIONS OVER $1B UNDER $1B COLLABORATION REAL - TIME ANALYTICS SOCIAL MEDIA CLOUD MOBILE 50% 56% 72% 28% 39% 75% 63% 71% 42% 54% Source: SMA Research, Maturing Technologies Survey 2015, n=58 DATA & DIGITAL SPENDING

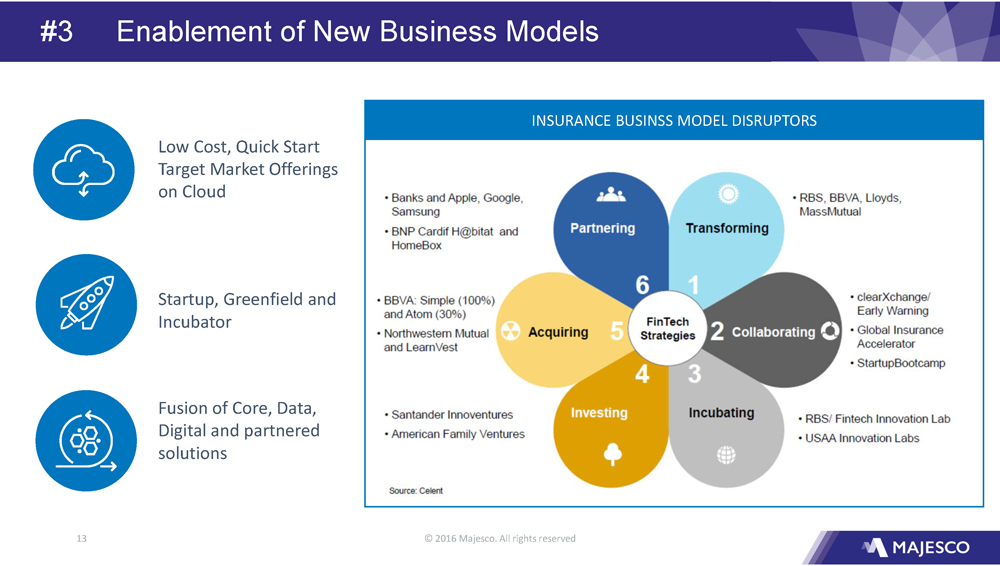

© 2016 Majesco. All rights reserved 13 #3 Enablement of New Business Models Low Cost, Quick Start Target Market Offerings on Cloud Startup, Greenfield and Incubator Fusion of Core, Data, Digital and partnered solutions INSURANCE BUSINSS MODEL DISRUPTORS

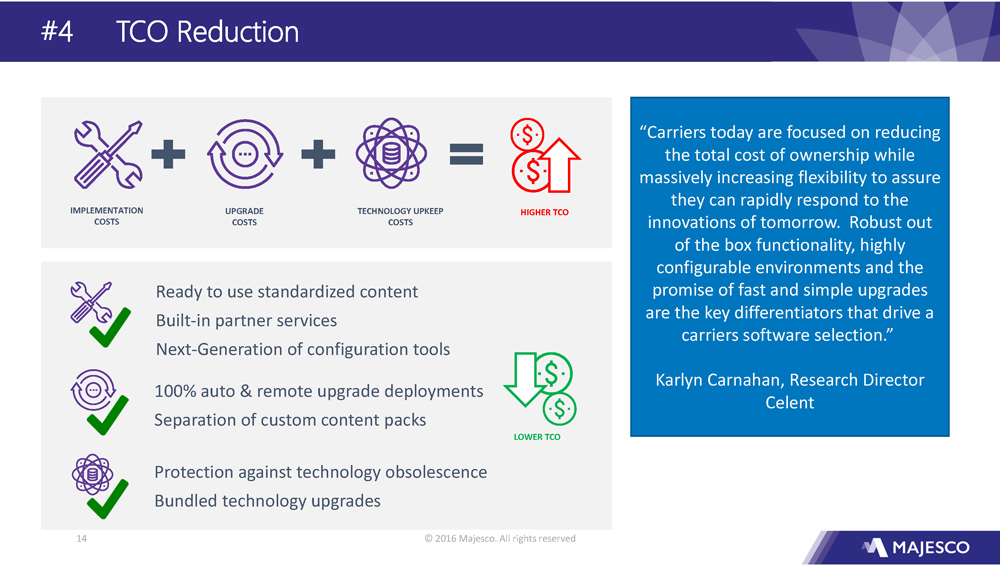

© 2016 Majesco. All rights reserved 14 #4 TCO Reduction “Carriers today are focused on reducing the total cost of ownership while massively increasing flexibility to assure they can rapidly respond to the innovations of tomorrow. Robust out of the box functionality, highly configurable environments and the promise of fast and simple upgrades are the key differentiators that drive a carriers software selection .” Karlyn Carnahan, Research Director Celent IMPLEMENTATION COSTS UPGRADE COSTS TECHNOLOGY UPKEEP COSTS HIGHER TCO Ready to use standardized content Built - in partner services Next - Generation of configuration tools 100% auto & remote upgrade deployments Separation of custom content packs Protection against t echnology obsolescence Bundled technology upgrades LOWER TCO

© 2016 Majesco. All rights reserved 15 Thank You

© 2016 Majesco. All rights reserved 1 Majesco Financials Farid Kazani, CFO

© 2016 Majesco. All rights reserved 2 2 Cautionary Language Concerning Forward - Looking Statements This presentation contains forward - looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act . These forward - looking statements are made on the basis of the current beliefs, expectations and assumptions of management, are not guarantees of performance and are subject to significant risks and uncertainty . These forward - looking statements should, therefore, be considered in light of various important factors, including those set forth in Majesco’s reports that it files from time to time with the Securities and Exchange Commission and which you should review, including those statements under “Item 1 A – Risk Factors” in Majesco’s Annual Report on Form 10 - K . Important factors that could cause actual results to differ materially from those described in forward - looking statements contained in this presentation include, but are not limited to : integration risks ; changes in economic conditions, political conditions, trade protection measures, licensing requirements and tax matters ; technology development risks ; intellectual property rights risks ; competition risks ; additional scrutiny and increased expenses as a result of being a public company ; the financial condition, financing requirements, prospects and cash flow of Majesco ; loss of strategic relationships ; changes in laws or regulations affecting the insurance industry in particular ; restrictions on immigration ; the ability and cost of retaining and recruiting key personnel ; the ability to attract new clients and retain them and the risk of loss of large customers ; continued compliance with evolving laws ; customer data and cybersecurity risk ; and Majesco’s ability to raise capital to fund future growth . These forward - looking statements should not be relied upon as predictions of future events and Majesco cannot assure you that the events or circumstances discussed or reflected in these statements will be achieved or will occur . If such forward - looking statements prove to be inaccurate, the inaccuracy may be material . You should not regard these statements as a representation or warranty by Majesco or any other person that we will achieve our objectives and plans in any specified timeframe, or at all . You are cautioned not to place undue reliance on these forward - looking statements, which speak only as of the date of this presentation . Majesco disclaims any obligation to publicly update or release any revisions to these forward - looking statements, whether as a result of new information, future events or otherwise, after the date of this press release or to reflect the occurrence of unanticipated events, except as required by law

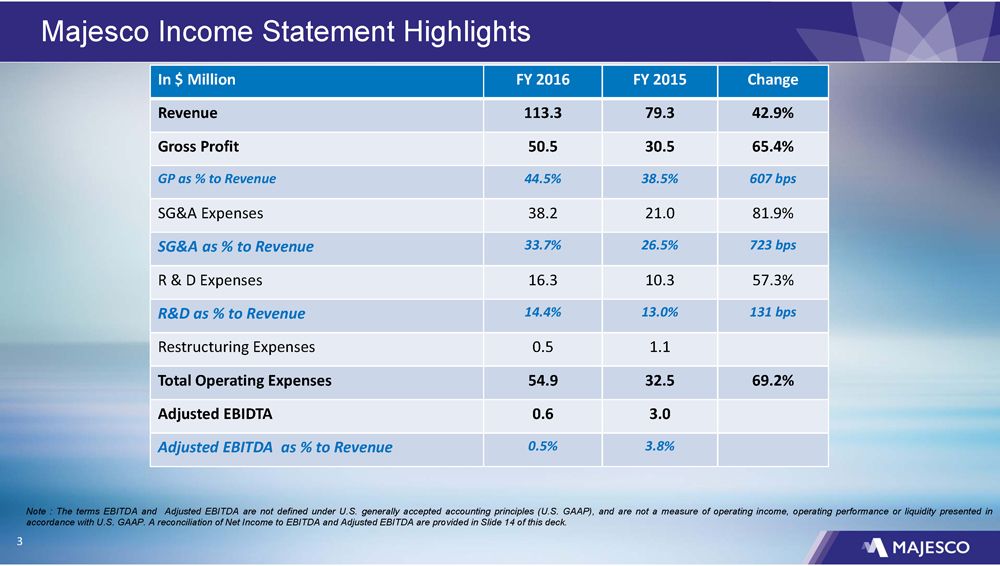

© 2016 Majesco. All rights reserved 3 Majesco Income Statement Highlights 3 In $ Million FY 2016 FY 2015 Change Revenue 113.3 79.3 42.9% Gross Profit 50.5 30.5 65.4% GP as % to Revenue 44.5% 38.5% 607 bps SG&A Expenses 38.2 21.0 81.9% SG&A as % to Revenue 33.7% 26.5% 723 bps R & D Expenses 16.3 10.3 57.3% R&D as % to Revenue 14.4% 13.0% 131 bps Restructuring Expenses 0.5 1.1 Total Operating Expenses 54.9 32.5 69.2% Adjusted EBIDTA 0.6 3.0 Adjusted EBITDA as % to Revenue 0.5% 3.8% Note : The terms EBITDA and Adjusted EBITDA are not defined under U . S . generally accepted accounting principles (U . S . GAAP), and are not a measure of operating income, operating performance or liquidity presented in accordance with U . S . GAAP . A reconciliation of Net Income to EBITDA and Adjusted EBITDA are provided in Slide 14 of this deck .

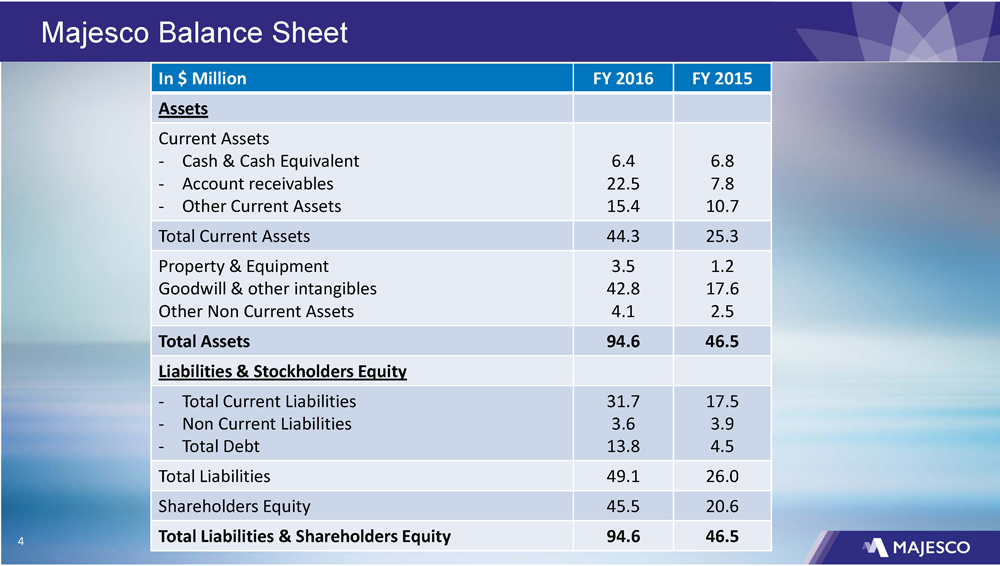

© 2016 Majesco. All rights reserved 4 Majesco Balance Sheet 4 In $ Million FY 2016 FY 2015 Assets Current Assets - Cash & Cash Equivalent - Account receivables - Other Current Assets 6.4 22.5 15.4 6.8 7.8 10.7 Total Current Assets 44.3 25.3 Property & Equipment Goodwill & other intangibles Other Non Current Assets 3.5 42.8 4.1 1.2 17.6 2.5 Total Assets 94.6 46.5 Liabilities & Stockholders Equity - Total Current Liabilities - Non Current Liabilities - Total Debt 31.7 3.6 13.8 17.5 3.9 4.5 Total Liabilities 49.1 26.0 Shareholders Equity 45.5 20.6 Total Liabilities & Shareholders Equity 94.6 46.5

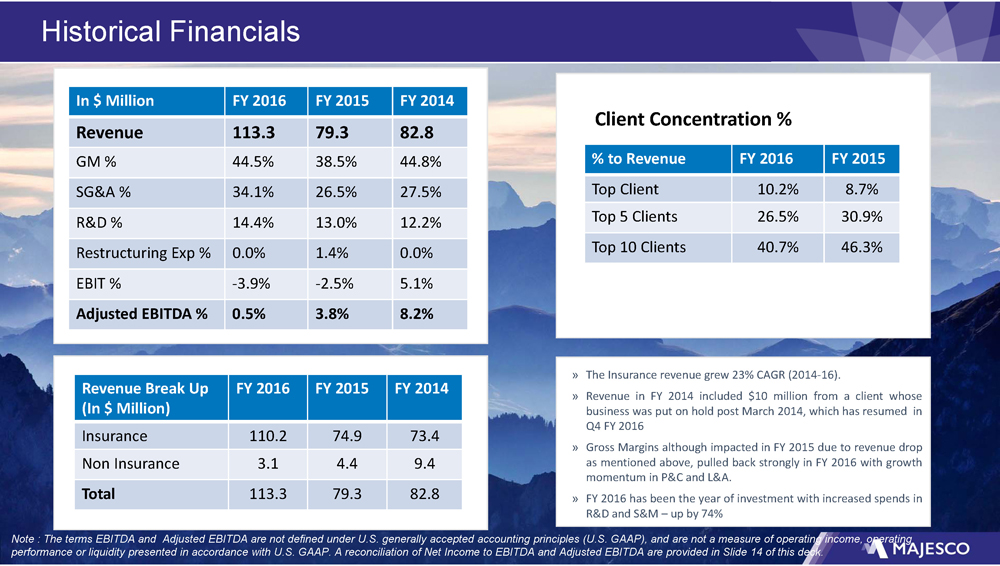

© 2016 Majesco. All rights reserved 5 Historical Financials » The Insurance revenue grew 23 % CAGR ( 2014 - 16 ) . » Revenue in FY 2014 included $ 10 million from a client whose business was put on hold post March 2014 , which has resumed in Q 4 FY 2016 » Gross Margins although impacte d in FY 2015 due to revenue drop as mentioned above, pulled back strongly in FY 2016 with growth momentum in P&C and L&A . » FY 2016 has been the year of investment with increased spends in R&D and S&M – up by 74 % % to Revenue FY 2016 FY 2015 Top Client 10.2% 8.7% Top 5 Clients 26.5% 30.9% Top 10 Clients 40.7% 46.3% Client Concentration % Revenue Break Up (In $ Million) FY 2016 FY 2015 FY 2014 Insurance 110.2 74.9 73.4 Non Insurance 3.1 4.4 9.4 Total 113.3 79.3 82.8 In $ Million FY 2016 FY 2015 FY 2014 Revenue 113.3 79.3 82.8 GM % 44.5% 38.5% 44.8% SG&A % 34.1% 26.5% 27.5% R&D % 14.4% 13.0% 12.2% Restructuring Exp % 0.0% 1.4% 0.0% EBIT % - 3.9% - 2.5% 5.1% Adjusted EBITDA % 0.5% 3.8% 8.2% Note : The terms EBITDA and Adjusted EBITDA are not defined under U.S. generally accepted accounting principles (U.S . GAAP), and are not a measure of operating income, operating performance or liquidity presented in accordance with U.S. GAAP. A reconciliation of Net Income to EBITDA and Adjusted EBITDA are provided in Slide 14 of this deck.

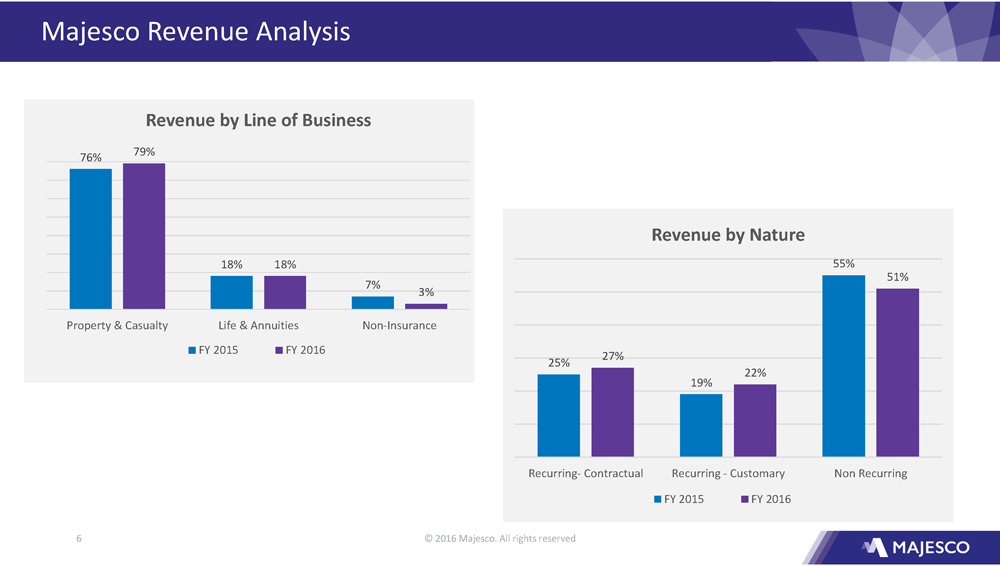

© 2016 Majesco. All rights reserved 6 Majesco Revenue Analysis 76% 18% 7% 79% 18% 3% Property & Casualty Life & Annuities Non-Insurance Revenue by Line of Business FY 2015 FY 2016 25% 19% 55% 27% 22% 51% Recurring- Contractual Recurring - Customary Non Recurring Revenue by Nature FY 2015 FY 2016

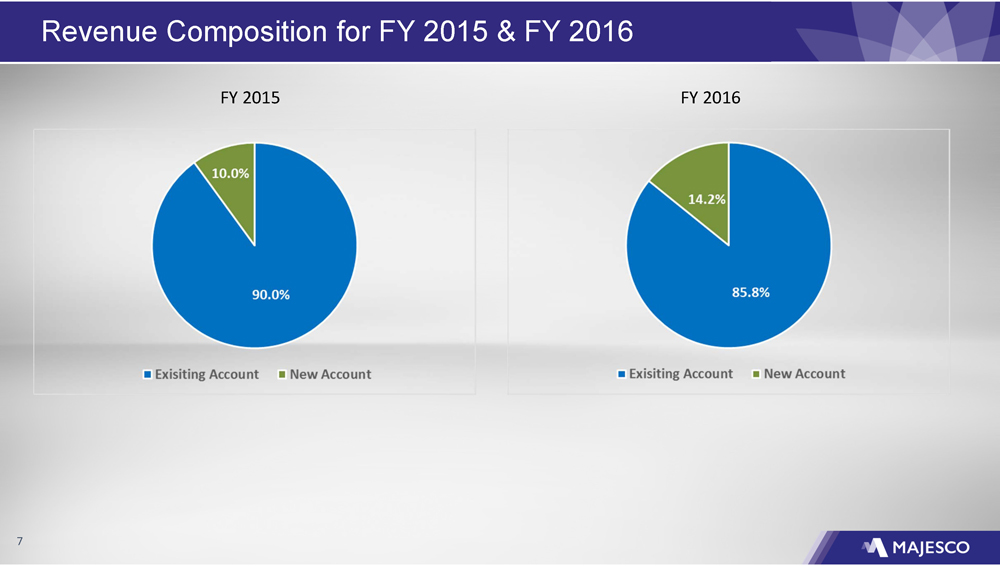

© 2016 Majesco. All rights reserved 7 7 Revenue Composition for FY 2015 & FY 2016 FY 2015 FY 2016

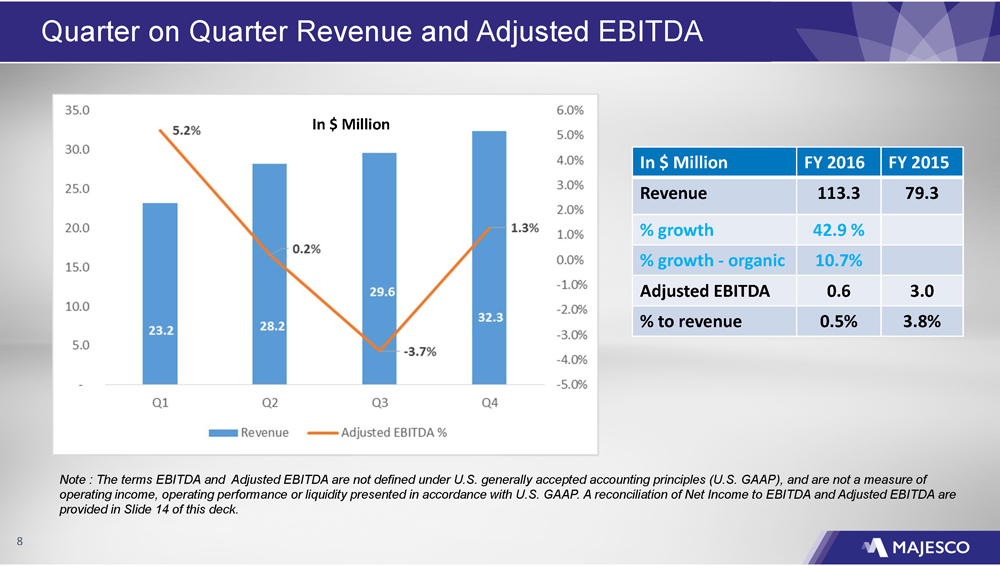

© 2016 Majesco. All rights reserved 8 Quarter on Quarter Revenue and Adjusted EBITDA Note : The terms EBITDA and Adjusted EBITDA are not defined under U.S. generally accepted accounting principles (U.S . GAAP), and are not a measure of operating income, operating performance or liquidity presented in accordance with U.S. GAAP. A reconciliation of Net Income to EBITDA and Adjusted EBITDA are provided in Slide 14 of this deck. In $ Million FY 2016 FY 2015 Revenue 113.3 79.3 % growth 42.9 % % growth - organic 10.7% Adjusted EBITDA 0.6 3.0 % to revenue 0.5% 3.8% 8 In $ Million

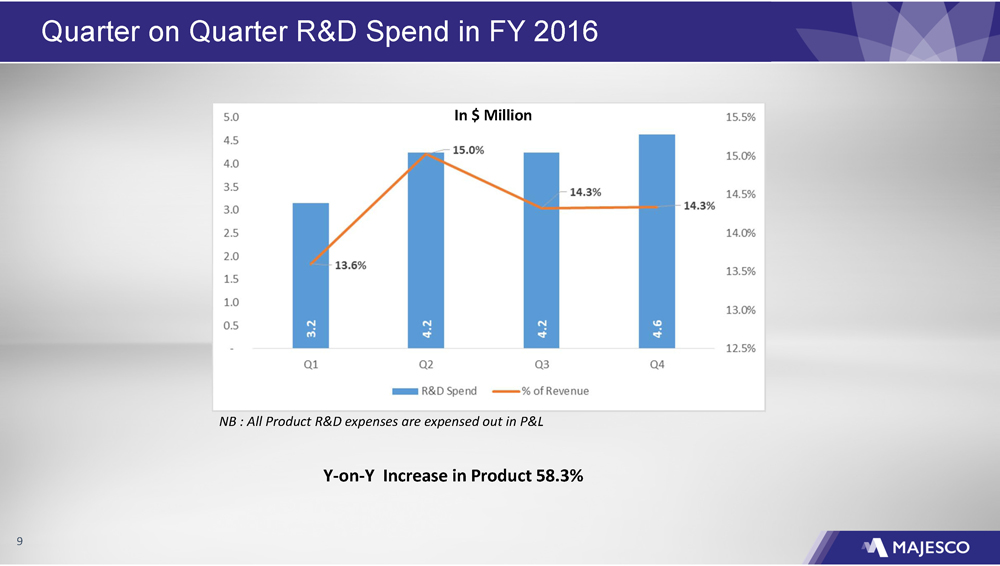

© 2016 Majesco. All rights reserved 9 Quarter on Quarter R&D Spend in FY 2016 Y - on - Y Increase in Product 58.3% NB : All Product R&D expenses are expensed out in P&L 9 In $ Million

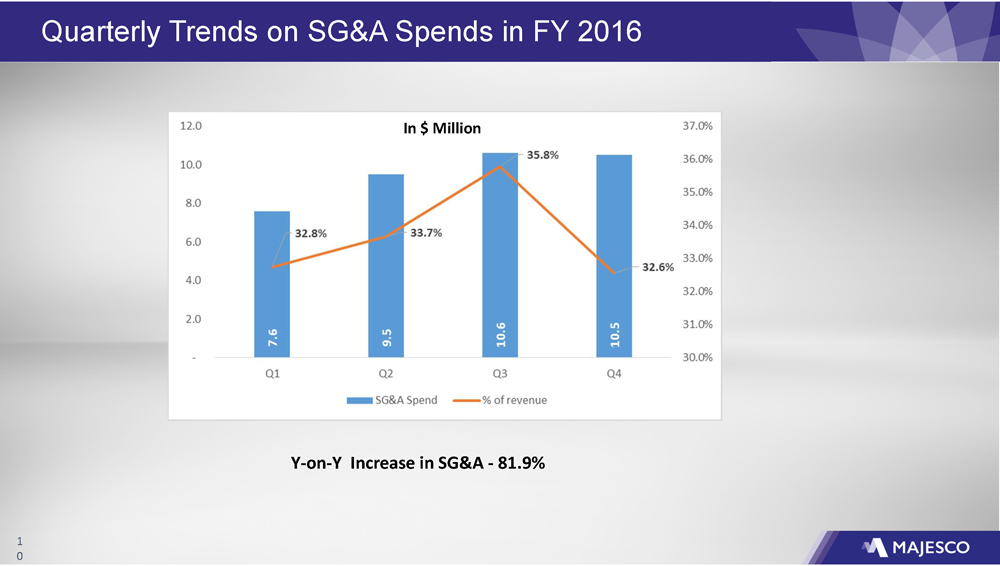

© 2016 Majesco. All rights reserved 10 1 0 Quarterly Trends on SG&A Spends in FY 2016 Y - on - Y Increase in SG&A - 81.9% In $ Million

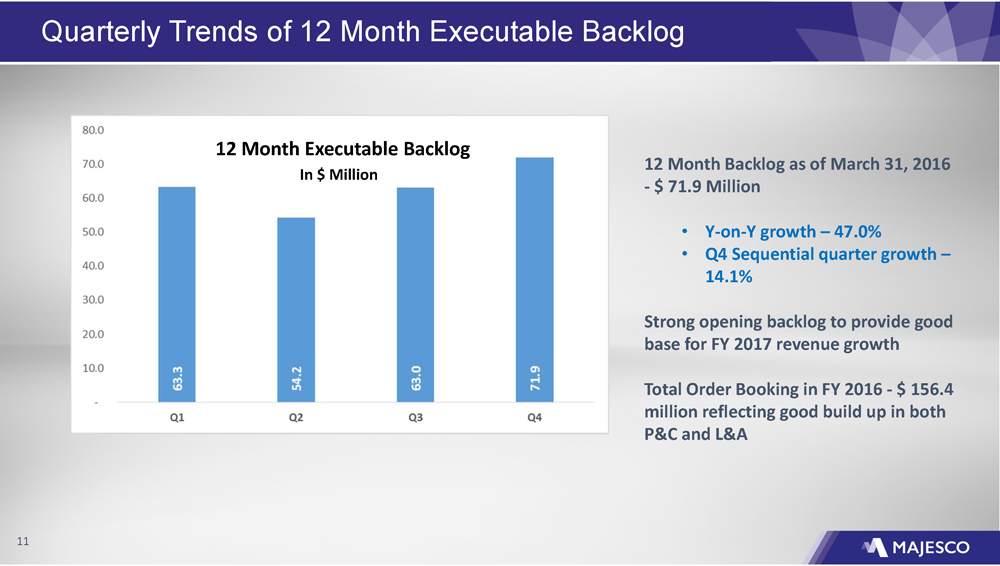

© 2016 Majesco. All rights reserved 11 11 Quarterly Trends of 12 Month Executable Backlog 12 Month Backlog as of March 31, 2016 - $ 71.9 Million • Y - on - Y growth – 47.0% • Q4 Sequential quarter growth – 14.1% Strong opening backlog to provide good base for FY 2017 revenue growth Total Order Booking in FY 2016 - $ 156.4 million reflecting good build up in both P&C and L&A 12 Month Executable Backlog In $ Million

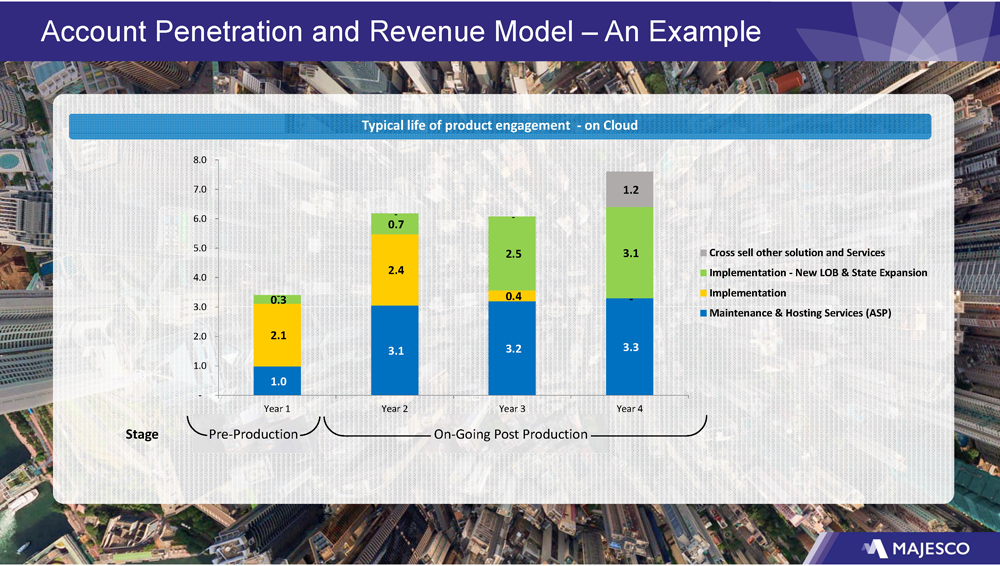

© 2016 Majesco. All rights reserved 12 Typical life of product engagement - on Cloud Stage Pre - Production On - Going Post Production Account Penetration and Revenue Model – An Example 1.0 3.1 3.2 3.3 2.1 2.4 0.4 - 0.3 0.7 2.5 3.1 - - - 1.2 - 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 Year 1 Year 2 Year 3 Year 4 Cross sell other solution and Services Implementation - New LOB & State Expansion Implementation Maintenance & Hosting Services (ASP)

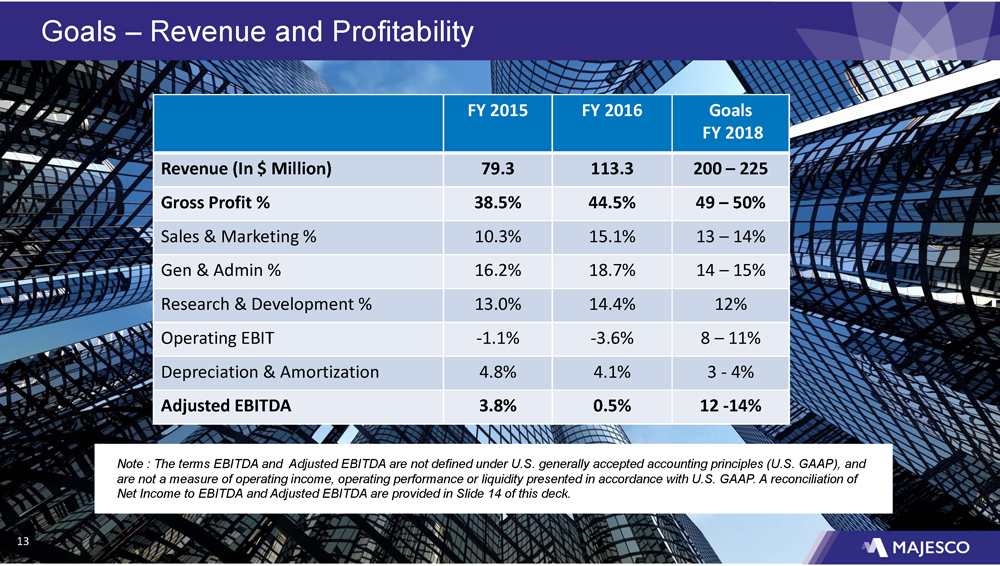

© 2016 Majesco. All rights reserved 13 Goals – Revenue and Profitability Note : The terms EBITDA and Adjusted EBITDA are not defined under U.S. generally accepted accounting principles (U.S . GAAP), and are not a measure of operating income, operating performance or liquidity presented in accordance with U.S. GAAP. A reconciliation of Net Income to EBITDA and Adjusted EBITDA are provided in Slide 14 of this deck. 13 FY 2015 FY 2016 Goals FY 2018 Revenue (In $ Million) 79.3 113.3 200 – 225 Gross Profit % 38.5% 44.5% 49 – 50% Sales & Marketing % 10.3% 15.1% 13 – 14% Gen & Admin % 16.2% 18.7% 14 – 15% Research & Development % 13.0% 14.4% 12% Operating EBIT - 1.1% - 3.6% 8 – 11% Depreciation & Amortization 4.8% 4.1% 3 - 4% Adjusted EBITDA 3.8% 0.5% 12 - 14%

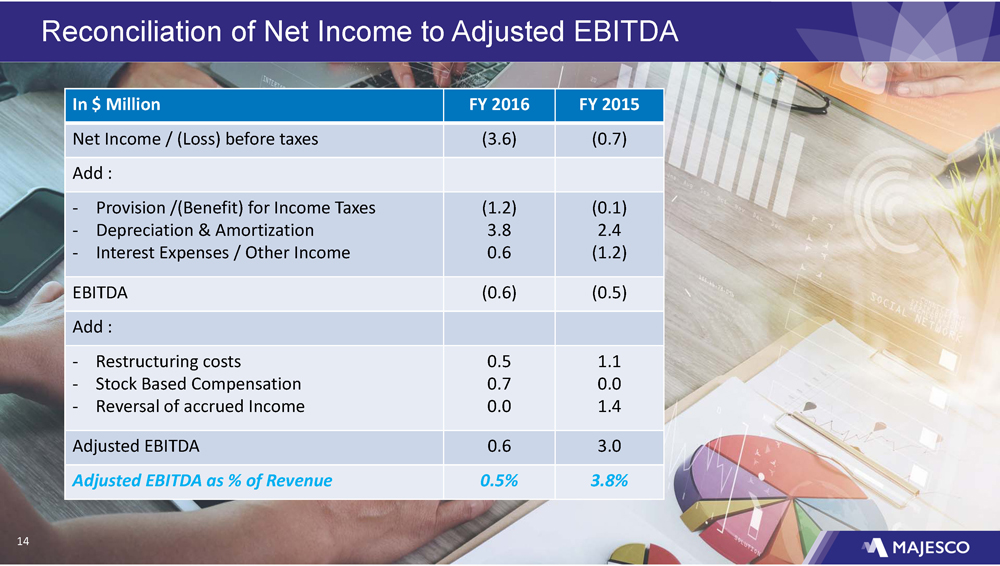

© 2016 Majesco. All rights reserved 14 14 Reconciliation of Net Income to Adjusted EBITDA In $ Million FY 2016 FY 2015 Net Income / (Loss) before taxes (3.6) (0.7) Add : - Provision /(Benefit) for Income Taxes - Depreciation & Amortization - Interest Expenses / Other Income (1.2) 3.8 0.6 (0.1) 2.4 (1.2) EBITDA (0.6) (0.5) Add : - Restructuring costs - Stock Based Compensation - Reversal of accrued Income 0.5 0.7 0.0 1.1 0.0 1.4 Adjusted EBITDA 0.6 3.0 Adjusted EBITDA as % of Revenue 0.5% 3.8%

© 2016 Majesco. All rights reserved 15 Thank You