UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| x | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended _______________

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number: ___________

Profound Medical Corp.

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

Ontario, Canada

(Jurisdiction of incorporation or organization)

2400 Skymark Avenue, Unit 6, Mississauga, Ontario L4W 5K5

(Address of principal executive offices)

Aaron Davidson, Chief Financial Officer and Senior Vice-President of Corporate Development; Tel (647) 476-1350; Fax (647) 847-3739

2400 Skymark Avenue, Unit 6, Mississauga, Ontario L4W 5K5

(Name, Telephone, E-mail, and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of Each Class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common Shares | | PROF (reserved) | | Nasdaq Capital Market (proposed) |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: N/A.

Indicate by check mark whether Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No ¨

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ¨ No ¨

Indicate by check mark whether Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “accelerated filer”, “large accelerated filer”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated Filer ¨ | Accelerated Filer ¨ | Non-accelerated Filer x | Emerging growth company x |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark which basis of accounting the Registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ¨ | International Financial Reporting Standards as issued by the International Accounting Standards Board x | Other ¨ |

If “Other” has been check in response to the previous question, by check mark which financial statement item Registrant has elected to follow. Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ¨

TABLE OF CONTENTS

TABLE OF CONTENTS

(continued)

GENERAL MATTERS

In this Registration Statement on Form 20-F (this “Registration Statement”), all references to “Profound” are to Profound Medical Corp., and all references to the “Company”, “our”, “us” or “we” refer to Profound Medical Corp. and its consolidated subsidiaries, unless the context clearly requires otherwise. Certain terms used herein are defined in the text and others are included in the glossary of terms. See “Glossary of Terms” below.

We report under International Financial Reporting Standards, as issued by the International Accounting Standards Board (“IFRS”). None of our financial statements were prepared in accordance with generally accepted accounting principles in the United States (“U.S. GAAP”).

We use the Canadian dollar as our reporting currency. All references to “C$” are to Canadian dollars and references to “US$” are to United States dollars. On August 28, 2019 the daily average exchange rate for the conversion of Canadian dollars into U.S. dollars as reported by the Bank of Canada was C$1.00 = US$0.7518. See also Item 3, “Key Information” for more detailed currency and conversion information.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Registration Statement includes certain statements that are “forward-looking statements” within the meaning of applicable securities laws. All statements in this Registration Statement, other than statements of historical facts, are forward-looking statements. These statements appear in a number of different places in this Registration Statement and can be identified by words such as “anticipates”, “estimates”, “projects”, “expects”, “intends”, “believes”, “plans”, “will”, “could”, “may”, or their negatives or other comparable words. Such forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements. Examples of such forward-looking statements include, but are not limited to:

| · | our expectations regarding commercializing our approved products (particularly the TULSA-PRO system following FDA clearance) and our ability to generate revenues and achieve profitability; |

| · | our expectations regarding the safety, efficacy and advantages of our products over our competitors and alternative treatment options; |

| · | our expectations regarding our products fulfilling unmet clinical needs and achieving market acceptance among patients, physicians and clinicians; |

| · | our expectations regarding reimbursement for our approved products from third-party payers; |

| · | our expectations regarding our relationships with Philips and Siemens, and our ability to achieve compatibility of our systems with MRI scanners produced by other manufacturers; |

| · | our ability to attract, develop and maintain relationships with other suppliers, manufacturers, distributors and strategic partners; |

| · | our expectations regarding our pipeline of product development, including expanding the clinical application of our products to cover additional indications; |

| · | our expectations regarding current and future clinical trials, including the timing and results thereof; |

| · | our expectations regarding receipt of additional regulatory approvals for our products and future product candidates; |

| · | our mission and future growth plans; |

| · | our ability to attract and retain personnel; |

| · | our expectations regarding our competitive position for each of our products in the jurisdictions where they are approved; |

| · | our ability to raise debt and equity capital to fund future product development, pursue regulatory approvals and commercialize our approved products; and |

| · | anticipated trends and challenges in our business and the markets in which we operate. |

In evaluating forward-looking statements, current and prospective shareholders should specifically consider various factors, including the risks outlined herein under the heading “Risk Factors” in Item 3.D. of this Registration Statement. Some of these risks and assumptions include, among others:

| · | risks related to our limited operating history and history of net losses; |

| · | risks related to our ability to commercialize our approved products, including expanding our sales and marketing capabilities, increasing our manufacturing and distribution capacity, increasing reimbursement coverage for our approved products and achieving and maintaining market acceptance for our products; |

| · | risks related to the regulation of our products, including in connection with obtaining regulatory approvals as well as post-marketing regulation; |

| · | risks related to our successful completion of clinical trials with respect to our products and future product candidates; |

| · | risks related to managing growth, including in respect of obtaining additional funding and establishing and maintaining collaborative partnerships, to achieve our goals; |

| · | risks related to competition that may impact market acceptance of our products and limit our growth; |

| · | risks relating to fluctuating input prices and currency exchange rates; |

| · | risks related to the reimbursement models in relevant jurisdictions that may not be advantageous; |

| · | risks related to reliance on third parties, including our collaborative partners, manufacturers, distributors and suppliers, and increasing the compatibility of our systems with MRI scanners; |

| · | risks related to intellectual property, including license rights that are key to our business; and |

| · | risks related to the loss of key personnel. |

Should one or more of these risks or uncertainties, or a risk that is not currently known to us, materialize, or should assumptions underlying those forward-looking statements prove incorrect, actual results may vary materially from those described herein. These forward-looking statements are made as of the date of this Registration Statement and we do not intend, and do not assume any obligation, to update these forward-looking statements, except as required by applicable securities laws. Investors are cautioned that forward-looking statements are not guarantees of future performance and are inherently uncertain. Accordingly, investors are cautioned not to put undue reliance on forward-looking statements.

We caution you that these cautionary remarks expressly qualify in their entirety all forward-looking statements attributable to us or persons acting on our behalf.

TRADEMARKS

The “Profound Medical” name and design logo are our registered trademarks. Solely for convenience, the trademarks, service marks, and trade names referred to in this Registration Statement are without the ® and TM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks and trade names. This Registration Statement contains additional trademarks, service marks and trade names of others, which are the property of their respective owners. All trademarks, service marks and trade names appearing in this Registration Statement are, to our knowledge, the property of their respective owners. We do not intend our use or display other companies’ trademarks, service marks or trade names to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

MARKET AND INDUSTRY DATA

This Registration Statement includes statistics and other data relating to markets, market sizes and other industry data pertaining to our business that we have obtained from industry publications and surveys and other information available to us. Industry publications and surveys generally state that the information contained therein has been obtained from sources believed to be reliable. Market data and statistics are inherently predictive and speculative and are not necessarily reflective of actual market conditions. Such statistics are based on market research, which itself is based on sampling and subjective judgments by both the researchers and the respondents, including judgments about what types of products and transactions should be included in the relevant market. In addition, the value of comparisons of statistics for different markets is limited by many factors, including that (i) the markets are defined differently, (ii) the underlying information was gathered by different methods and (iii) different assumptions were applied in compiling the data. Accordingly, the market statistics included in this prospectus should be viewed with caution. We believe that information from these industry publications included in this Registration Statement is reliable.

GLOSSARY OF TERMS

As used in this Registration Statement, the following terms have the respective meaning as specified below:

| 2016 Bought Deal | has the meaning given under the heading Item 5.B, “Liquidity and Capital Resources—Recent Sources and Uses of Financing—Bought Deals”. |

| | |

| 2017 Bought Deal | has the meaning given under the heading Item 5.B, “Liquidity and Capital Resources—Recent Sources and Uses of Financing—Bought Deals”. |

| | |

| 2018 Bought Deal | has the meaning given under the heading Item 5.B, “Liquidity and Capital Resources—Recent Sources and Uses of Financing—Bought Deals”. |

| 3D | means three-dimensional. |

| | |

| ablation | means to remove or destroy tissue. |

| | |

| ACA | means the 2010 Affordable Care Act and the Health Care and Education Affordability Reconciliation Act of 2010. |

| | |

| ADT | means androgen deprivation therapy. |

| | |

| Articles | means our Articles of Incorporation, as amended. |

| | |

| Audit Committee | has the meaning given under the heading Item 6.C, “Directors, Senior Management and Employees—Board Practices—Audit Committee”. |

| | |

| BDC Capital | means BDC Capital Inc. |

| | |

| Board | means the Board of Directors of Profound Medical Corp. |

| | |

| Bought Deals | means the 2016 Bought Deal, the 2017 Bought Deal and/or the 2018 Bought Deal, as the context may require. |

| | |

| BPH | means benign prostatic hyperplasia, a condition where the prostate gland is enlarged and not cancerous. |

| | |

| brachytherapy | means the precise placement of short-range radiation-sources (radioisotopes) directly at the site of the cancerous tumor. |

| | |

| Canada MDR | means the Medical Devices Regulations issued by Health Canada’s Therapeutic Products Directorate. |

| | |

| CE Mark | means “Conformité Européenne” and is affixed to a medical device in the European Union by its manufacturer or his authorized representative to declare that the medical device complies with the essential requirements of the Medical Device Directive (Council Directive 93/42/EEC, “MDD”) and that the appropriate related conformity assessment procedure as provided in the MDD and its annexes has been conducted. |

| | |

| CIBC | means Canadian Imperial Bank of Commerce. |

| | |

| CIBC Loan | means the initial gross proceeds of C$12,500,000, maturing on July 29, 2022, with an interest rate based on prime plus 2.5%, pursuant to the CIBC Loan Agreement. |

| | |

| CIBC Loan Agreement | means the loan agreement entered into on July 30, 2018 between PMI, as borrower; Profound, Profound Medical (U.S.) Inc and Profound Medical GmbH, as guarantors; and CIBC, as lender. |

| | |

| Common Shares | means the common shares in the capital of Profound Medical Corp. |

| | |

| cryoablation | means a therapy that uses extreme cold temperature to destroy benign and malignant tissue by crystallizing it. |

| | |

| de novo classification | means the submission of a petition to the FDA to reclassify a novel non-predicated Class III device as a Class I or II device pursuant to Section 513(f)(2) of the United States Federal Food, Drug and Cosmetic Act. |

| | |

| EBRT | means external beam radiation therapy. |

| | |

| EPIC | means the Expanded Prostate Cancer Index Composite. |

| | |

| Essential Requirements | has the meaning given under the heading Item 4.B, “Information on the Company—Business Overview—Regulation—European Union”. |

| European Union or EU | means an organization created in 1993 with the aim of achieving closer economic and political union between the member states of Europe and currently comprising Austria, Belgium, Bulgaria, Croatia, Cyprus, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, and the United Kingdom. |

| | |

| Executive Employment Agreements | has the meaning given under the heading Item 6.B., “Compensation—Executive Compensation—Executive Employment Agreements – Termination and Change of Control Benefits.” |

| | |

| False Claims Act | means the U.S. False Claims Act, 31 U.S.C. §§ 3729-3733. |

| | |

| FCPA | means the U.S. Foreign Corrupt Practices Act of 1977, as amended. |

| | |

| FDA | means the United States Food and Drug Administration. |

| Federal Economic Development Agency Loan | has the meaning given under the heading Item 5.B, “Liquidity and Capital Resources—Recent Sources and Uses of Financing—Federal Economic Development Agency Loan”. |

| | |

| FFDCA | means the Federal Food, Drug and Cosmetic Act, 21 U.S.C. § 301 et seq., as amended. |

| | |

| FSCAs | means Field Safety Corrective Actions. |

| | |

| Genesys | means Genesys Ventures II LP. |

| | |

| Gleason Score | means the histological assessment of prostate tissue using a tumor grading system which describes how aggressive a prostate cancer is on a scale from 1 (least aggressive) to 5 (most aggressive). The Gleason score is a combination of the two most common growth patterns observed in a biopsy specimen. |

| | |

| Gn-RH | means gonadotrophin-releasing hormone. |

| | |

| HDR | means high dose radiation. |

| | |

| Health Technology Exchange Loan | has the meaning given under the heading Item 5.B, “Liquidity and Capital Resources—Recent Sources and Uses of Financing—Health Technology Exchange Loan”. |

| | |

| HIFU | means high intensity focus ultrasound. |

| | |

| HIPAA | means Health Insurance Portability and Accountability Act of 1996. |

| | |

| IDE | means an investigational device exemption under the FFDCA and FDA regulations. |

| | |

| IFRS | means the International Financial Reporting Standards as issued by the International Accounting Standards Board. |

| | |

| IIEF | means the International Index of Erectile Function. |

| | |

| income test | has the meaning given under the heading Item 10.E, “Additional Information—Taxation—Certain U.S. Federal Income Tax Considerations”. |

| Insider Participation Limits | has the meaning given under the heading Item 6.B., “Compensation—Executive Compensation—Share Option Plan.” |

| | |

| IRB | means an institutional review board. |

| | |

| JOBS Act | means the Jumpstart Our Business Startups Act of 2012, as amended. |

| | |

| Knight | means Knight Therapeutics Inc. |

| | |

| Knight Loan | means the secured loan of C$4,000,000 bearing interest at 15% per annum provided by Knight pursuant to the Knight Loan Agreement. |

| | |

| Knight Loan Agreement | means the loan agreement entered into on April 30, 2015 between PMI and Knight. |

| | |

| MDB | means Medical Devices Bureau of Health Canada. |

| | |

| Medical Devices Directive | means the Council Directive 93/42/EEC concerning medical devices. |

| | |

| Medical Device License | means the license for marketing approval of a medical device in Canada. |

| | |

| MHLW | means Japan’s Pharmaceutical and Medical Device Agency. |

| | |

| Mira | has the meaning given under the heading Item 4.A.1, “History and Development of the Company—Name, Address and Incorporation; Trading Market”. |

| | |

| Mira Subco | has the meaning given under the heading Item 4.A.1, “History and Development of the Company—Name, Address and Incorporation; Trading Market”. |

| | |

| MR | means magnetic resonance. |

| | |

| MR-HIFU | means magnetic resonance guided high intensity focused ultrasound. |

| | |

| MRI | means magnetic resonance imaging. |

| | |

| Nasdaq | means the Nasdaq Stock Market LLC (a U.S. national securities exchange). |

| | |

| New Siemens Agreement | has the meaning given under the heading Item 10.C, “Additional Information—Material Contracts. |

| | |

| New EU MDR | has the meaning given under the heading Item 4.B, “Business Overview—Regulatory—European Union Regulation”. |

| | |

| NMPA | National Medical Products Administration of China. |

| | |

| non-resident holder | has the meaning given under the heading Item 10.E, “Additional Information—Taxation—Canadian Federal Income Taxation”. |

| | |

| OBCA | means the Business Corporations Act (Ontario), as amended, together with all regulations promulgated pursuant thereto. |

| | |

| Old PMI | has the meaning given under the heading Item 4.A.1, “History and Development of the Company—Name, Address and Incorporation; Trading Market”. |

| | |

| Original Siemens Agreement | has the meaning given under the heading Item 4.B, “Information on the Company—Business Overview—Alliances and Partnerships—Siemens”. |

| Philips | means Koninklijke Philips N.V. |

| | |

| Philips Confidentiality Agreement | has the meaning given under the heading Item 10.C, “Additional Information—Material Contracts”. |

| | |

| Philips Medical | has the meaning given under the heading Item 10.C, “Additional Information—Material Contracts”. |

| | |

| Philips Resale Purchasing Agreement | has the meaning given under the heading Item 10.C, “Additional Information—Material Contracts”. |

| | |

| Philips Share Purchase Agreement | has the meaning given under the heading Item 10.C, “Additional Information—Material Contracts”. |

| | |

| Philips Supply Agreement | has the meaning given under the heading Item 10.C, “Additional Information—Material Contracts”. |

| | |

| PIRADS | means Prostate Imaging Reporting and Data System. |

| | |

| PMA | means the Pre-Market Approval application process for marketing approval of medical devices in the United States. |

| | |

| PMD Act | means Japan’s Pharmaceutical and Medical Device Act. |

| | |

| PMDA | means Japan’s Pharmaceutical and Medical Device Agency. |

| | |

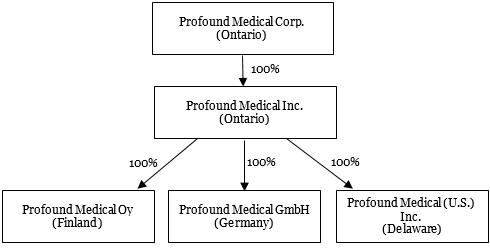

| PMI | means Profound Medical Inc., an OBCA corporation and Profound’s 100%-owned direct subsidiary, which serves as the holding subsidiary of our operating subsidiaries. |

| | |

| Profound | means Profound Medical Corp., an OBCA corporation and our TSX-traded holding company and registrant for purposes of this Registration Statement. |

| | |

| PSA | means prostate specific antigen. |

| | |

| QMS | means quality management system. |

| | |

| QSR | means the FDA’s Quality System Regulation. |

| | |

| radical prostatectomy | means a surgical procedure that involves the removal of the whole prostate gland. |

| | |

| Registration Statement | means this registration statement on Form 20-F. |

| | |

| Sarbanes-Oxley | means the Sarbanes-Oxley Act of 2002, as amended. |

| | |

| SEC | means the U.S. Securities and Exchange Commission. |

| | |

| SEDAR | means the Canadian System for Electronic Document Analysis and Retrieval. |

| | |

| Share Consolidation | has the meaning given under the heading Item 4.A.1, “History and Development of the Company—Name, Address and Incorporation; Trading Market”. |

| | |

| Share Option Plan | means our amended and restated share option plan dated July 13, 2018. |

| | |

| Siemens | means Siemens Healthcare GmbH. |

| | |

| Sonalleve | means the technology acquired from Philips in 2017 underlying our Sonalleve system, which combines real-time MRI and thermometry with focused ultrasound delivered from the outside to the patient to enable precise and incision-free ablation of diseased tissue. |

| Sonalleve system | means our system utilizing Sonalleve technology. |

| | |

| Sonalleve Transaction | means the transaction with Philips on July 31, 2017, where we entered into the Philips Share Purchase Agreement with Philips in order to expand the existing collaboration and acquire the Sonalleve technology, which we use in our Sonalleve system. |

| | |

| Sunnybrook | means the Sunnybrook Health Sciences Centre. |

| | |

| Sunnybrook License | has the meaning given under the heading Item 10.C, “Additional Information—Material Contracts”. |

| | |

| TACT or TACT Pivotal Clinical Trial | means our TULSA-PRO Ablation Clinical Trial, a prospective, open-label, single-arm pivotal clinical study of our TULSA-PRO system. |

| | |

| TPD | means Health Canada’s Therapeutic Products Directorate. |

| | |

| TSX | means the Toronto Stock Exchange. |

| | |

| TSX-V | means the TSX Venture Exchange. |

| | |

| TULSA | means transurethral ultrasound ablation. |

| | |

| TULSA-PRO | means our TULSA technology, which is used in our TULSA-PRO systems. |

| | |

| TULSA-PRO system | means our leading product, which combines real-time MRI, robotically-driven transurethral sweeping action/thermal ultrasound and closed-loop temperature feedback control, and is comprised of two categories of components: disposables and the capital equipment used in conjunction with a customer’s MRI scanner. |

| | |

| TURP | means a transurethral resection of the prostate, a surgical procedure that removes portions of the prostate gland via the urethra. |

| | |

| UA | means ultrasound applicator. |

| | |

| urinary rectal fistula | means an abnormal channel between the bladder and rectum resulting in the potential for leakage of urine from the urinary tract into surrounding tissues. |

| | |

| USPTO | means the United States Patent and Trademark Office. |

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

A. Directors and Senior Management

For the names, business addresses and functions of our directors and senior management, see Item 6.A, “Directors and Senior Management” and Item 6.C, “Board Practices”.

B. Advisors

Our principal legal advisers are Torys LLP, 79 Wellington St. W., 33rd Floor, TD South Tower, Toronto, Ontario, Canada M5K 1N2.

C. Auditors

PricewaterhouseCoopers LLP audited our consolidated financial statements for the fiscal years ended December 31, 2018, 2017 and 2016. The address of PricewaterhouseCoopers LLP is PwC Centre, 354 Davis Road, Suite 600, Oakville, Ontario, Canada L6J 0C5.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. Selected Financial Data

The following table sets forth selected consolidated financial information for the periods indicated, prepared in accordance with IFRS. The selected consolidated statements of operations data and balance sheet data as of and for the years ended December 31, 2018, 2017 and 2016 are derived from our audited consolidated financial statements set forth elsewhere in this Registration Statement. The selected consolidated statements of operations data for the three and six months ended June 30, 2019 and 2018 and selected consolidated balance sheet data as of June 30, 2019 are derived from our unaudited consolidated financial statements included elsewhere in this Registration Statement.

The selected consolidated financial information should be read in conjunction with the financial statements and accompanying notes thereto contained elsewhere in this Registration Statement and discussions in Item 5, “Operating and Financial Review and Prospects”. The selected consolidated financial information set out below may not be indicative of our future performance.

| | | Three Months

Ended June 30, | | | Six Months

Ended June 30, | | | Year Ended

December 31, | |

| | | 2019 | | | 2018 | | | 2019 | | | 2018 | | | 2018 | | | 2017 | | | 2016 | |

| | | | (Unaudited) | | | | (Unaudited) | | | | | | | | | | | | | |

| Figures in C$ unless otherwise stated Consolidated Statements of Operations Data: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Revenues | | | 574,109 | | | | 213,343 | | | | 2,049,897 | | | | 589,678 | | | | 2,602,278 | | | | 4,904,550 | | | | - | |

| Cost of sales | | | 244,066 | | | | 126,259 | | | | 777,422 | | | | 357,334 | | | | 1,778,501 | | | | 3,032,208 | | | | - | |

| Gross profit | | | 330,043 | | | | 87,084 | | | | 1,272,475 | | | | 232,344 | | | | 823,777 | | | | 1,872,342 | | | | - | |

| Expenses: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Research and development expenses | | | 3,186,355 | | | | 2,347,909 | | | | 5,864,101 | | | | 4,864,690 | | | | 10,265,388 | | | | 9,638,190 | | | | 9,988,693 | |

| General and administrative expenses | | | 1,586,323 | | | | 2,236,529 | | | | 3,100,436 | | | | 3,539,733 | | | | 6,656,723 | | | | 5,935,215 | | | | 4,369,288 | |

| Selling and distribution expenses | | | 1,154,869 | | | | 1,113,225 | | | | 625,524 | | | | 2,060,127 | | | | 4,091,347 | | | | 3,925,804 | | | | 1,282,433 | |

| Total expenses | | | 5,927,547 | | | | 5,697,663 | | | | 9,590,061 | | | | 10,464,550 | | | | 21,013,458 | | | | 19,499,209 | | | | 15,640,414 | |

| Finance costs | | | 337,220 | | | | 313,606 | | | | 651,905 | | | | 633,569 | | | | 826,312 | | | | 1,249,084 | | | | 829,899 | |

| Financial income | | | (110,790 | ) | | | (117,357 | ) | | | (252,671 | ) | | | (157,161 | ) | | | (483,788 | ) | | | (127,732 | ) | | | (157,598 | ) |

| Net finance costs | | | 226,430 | | | | 196,249 | | | | 399,234 | | | | 476,408 | | | | 342,524 | | | | 1,121,352 | | | | 672,301 | |

| Loss before income taxes | | | 5,823,934 | | | | 5,806,828 | | | | 8,716,820 | | | | 10,708,614 | | | | 20,532,205 | | | | 18,748,219 | | | | 16,312,715 | |

| Income tax expense | | | 20,200 | | | | 24,200 | | | | 54,000 | | | | 60,600 | | | | 230,784 | | | | 74,123 | | | | 14,054 | |

| Net loss attributable to shareholders for the period | | | 5,844,134 | | | | 5,831,028 | | | | 8,770,820 | | | | 10,769,214 | | | | 20,762,989 | | | | 18,822,342 | | | | 16,326,769 | |

| Other comprehensive income | | | (11,843 | ) | | | 57,943 | | | | (58,232 | ) | | | 14,695 | | | | 29,226 | | | | (69,245 | ) | | | 11,316 | |

| Net loss and comprehensive loss for the period | | | 5,832,291 | | | | 5,888,971 | | | | 8,712,588 | | | | 10,783,909 | | | | 20,792,215 | | | | 18,753,097 | | | | 16,338,085 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Loss per share: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Basic and diluted weighted average shares outstanding | | | 108,061,539 | | | | 107,727,319 | | | | 108,058,221 | | | | 92,614,640 | | | | 100,395,649 | | | | 61,404,141 | | | | 41,510,145 | |

| Basic and diluted | | | 0.05 | | | | 0.05 | | | | 0.08 | | | | 0.12 | | | | 0.21 | | | | 0.31 | | | | 0.39 | |

| | | As of

June 30, | | | As of

December 31, | |

| | | 2019 | | | 2018 | | | 2017 | |

| | | (Unaudited) | | | | | | | |

| Consolidated Balance Sheet Data: | | | | | | | | | | | | |

| Cash(1) | | C$ | 20,493,470 | | | C$ | 30,687,183 | | | C$ | 11,103,223 | |

| Total assets | | | 37,862,711 | | | | 46,549,872 | | | | 27,879,379 | |

| Total liabilities | | | 19,443,184 | | | | 19,923,538 | | | | 13,738,240 | |

| Deficit | | | (119,644,062 | ) | | | (111,033,661 | ) | | | (90,270,672 | ) |

| Total shareholders’ equity | | | 18,419,527 | | | | 26,626,334 | | | | 14,141,139 | |

| (1) | Following FDA clearance of our TULSA-PRO system in August 2019, we paid a C$250,000 milestone payment to Sunnybrook under the Sunnybrook License. See Item 4.B, “Business Overview—Intellectual Property—Licenses”. |

B. Capitalization and Indebtedness

The following table sets forth our capitalization as of June 30, 2019. You should read this information together with our historical financial information and other information provided in this Registration Statement, including Item 5, “Operating and Financial Review and Prospects” and our unaudited consolidated financial statements as of and for the three months ended June 30, 2019 and 2018, including the notes thereto, set forth elsewhere in this Registration Statement.

| | | As of June 30,

2019 | |

| | | (Unaudited) | |

| Figures in C$ unless otherwise stated | | | | |

| Long-Term Debt | | | | |

| Long-term bank loan (secured) (non-current portion)(1) | | $ | 8,562,737 | |

| Total long-term debt | | | 8,562,737 | |

| | | | | |

| Equity | | | | |

| Share capital | | | 120,942,408 | |

| Contributed surplus | | | 17,208,040 | |

| Accumulated other comprehensive loss | | | (86,935 | ) |

| Deficit | | | (119,644,062 | ) |

| Total equity | | | 18,419,527 | |

| | | | | |

| Total Capitalization (long-term debt and equity) | | $ | 26,982,264 | |

| (1) | Excludes current portion of C$3,475,358. |

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

An investment in the Common Shares involves a high degree of risk and should be considered highly speculative due to the nature and present early stage of our business. The following risks are the material risks that we face; however, the risks below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we believe to be immaterial may also adversely affect our business. If any of the following risks occur, our business, financial condition and results of operations could be seriously harmed and you could lose all or part of your investment. Before deciding to invest in any Common Shares, investors should carefully consider the risk factors described below.

Risk Factors Relating to Our Operating History and Financial Condition

We have a limited operating history and history of operating losses.

We commenced operations in June 2008 and have only begun generating revenues in 2017. As of June 30, 2019, we had an accumulated deficit of C$119,644,062 and had cash and cash equivalents of approximately C$20.5 million. Since inception, we have incurred significant losses each year. For the six months ended June 30, 2019, we recorded a net loss of C$8,770,820, and for the year ended December 31, 2018, we recorded a net loss of C$20,762,989. We expect to incur significant operating losses even as we begin to commercialize the TULSA-PRO system in the United States following our recent FDA clearance, which will require significant expenditures to increase our sales and marketing capabilities and expand our manufacturing and distribution capacity, as well as other expenses related to increasing reimbursement coverage and gaining market acceptance among patients, physicians/clinicians and others in the medical community. In addition, we plan to continue product research and development and clinical trials and may pursue additional regulatory approvals. There is no assurance that we will ever successfully commercialize our systems, generate significant revenues from our approved products or achieve profitability. Even if profitability is achieved, we may not be able to sustain or increase profitability. Our failure to achieve or maintain profitability could negatively impact the value of the Common Shares.

Our business is capital intensive and requires significant investment to increase our commercial capacity for our approved products, and the resources to do so may not be available in amounts or on terms acceptable to us, if at all.

Our business requires substantial capital investment in order to commercialize our approved products, in particular to expand our sales and marketing capabilities and increase our manufacturing capacity, as well as to conduct research and development and to obtain regulatory approvals for existing products and future product candidates. We will likely need additional capital to fund our current and planned business activities and to fund any significant expansion of operations. In order to secure financing, if available, it is likely that we would need to sell additional Common Shares and/or securities that are exchangeable for or convertible into Common Shares, incur additional indebtedness and/or enter into development, manufacturing, distribution and/or licensing relationships. Any future equity financing may be dilutive to existing shareholders. Any future debt financing arrangements we enter into (like our CIBC Loan Agreement as described below) would likely contain restrictive covenants that would impose significant operating and, if any, financial restrictions on us. The availability of equity or debt financing will be affected by, among other things, our commercial progress and market acceptance in respect of the TULSA-PRO system and other approved products, as well as the results of our research and development, our ability to obtain regulatory approvals, the state of the capital markets generally, strategic alliance agreements, and other relevant considerations.

Any additional financing may not be obtained on favorable terms, if at all. If we cannot obtain adequate funding on reasonable terms, we may not be able advance our business strategy and/or the commercialization of our approved products, and we may need to terminate or delay clinical trials, curtail significant regulatory initiatives, and/or sell, license or assign rights to our technologies, products or product candidates.

Our cash outflows are expected to consist primarily of expenditures to increase our commercial capacity, particularly in sales and marketing, as well as in manufacturing and distribution. In addition, we intend to continue internal and external research and development efforts to develop and expand our product pipeline, as well as incur general and administrative expenditures to support our corporate infrastructure. If we do not obtain sufficient additional capital, there may be substantial doubt about our ability to continue as a going concern and realize assets and pay liabilities as they become due. Depending upon the results of our research and development programs and the availability of financial resources, we could decide to accelerate, terminate or reduce certain projects, or commence new ones. Any failure on our part to raise additional funds on terms favorable to us, or at all, may require us to significantly change or curtail current or planned operations in order to conserve cash until such time, if ever, that sufficient proceeds from operations are generated, and could result in us not taking advantage of business opportunities, in the termination or delay of clinical trials for one or more of our product candidates, in curtailment of our product development programs designed to identify new product candidates, and/or in the sale or assignment of rights to our technologies, products or product candidates. Any of the foregoing could have a material adverse effect on our business, financial condition and results of operations.

Our CIBC Loan Agreement contains financial and non-financial covenants that may impact how we operate our business. In addition, failure to comply with any of these covenants could have a material adverse effect on our business.

Our CIBC Loan Agreement contains financial and non-financial covenants, including a requirement that our unrestricted cash is at all times greater than our operating cash expenditures during any trailing three month period. Complying with such covenants may at times necessitate that we must forego other favorable business opportunities. Moreover, our failure to comply with any of these covenants would likely constitute a default under any other similar facilities and agreements that we may enter into in the future, and could give rise to an acceleration of some, if not all, of our other then outstanding indebtedness, if any, which would have a material adverse effect on our business. Our indebtedness may grow as our business grows and/or we make acquisitions. If our income from operations underperforms, we may have to utilize cash flow or capital resources to fund our debt service payments. If our cash flow and capital resources are insufficient to service amounts owed under our current or any future indebtedness, we may be forced to reduce or delay capital expenditures, dispose of assets, license or assign the rights to our technology, issue equity or incur additional debt to obtain necessary funds, or restructure our debt, any or all of which could have a material adverse effect on our business, financial condition and results of operations. In addition, we cannot guarantee that we would be able to take any of these actions on terms acceptable to us, or at all; that these actions would enable us to continue to satisfy our capital requirements; or that these actions would be permitted under the terms of our debt agreements. In particular, the CIBC Loan Agreement contains covenants with respect to capital expenditures and other indebtedness, maintaining minimum cash balances at all times and certain financial covenants. We have granted a security interest over all of our assets (including the shares of our subsidiaries owned by us). Events of default under the CIBC Loan Agreement include among other things, any covenant breach (subject, in certain instances, to a cure period), insolvency of Profound or its subsidiaries, the occurrence of certain events which would have a material adverse effect, cross defaults to other agreements, a failure to comply with certain financial tests, and a change of control of Profound or its subsidiaries. The enforcement by CIBC of its rights and remedies pursuant to the terms of the CIBC Loan Agreement and associated documentation could result in CIBC, its agent or any third party purchaser thereof owning all of our assets, including the shares of our subsidiaries.

We are exposed to foreign currency risk, which exposure will increase as we commercialize our approved products in the United States; to date, we have not hedged against risk associated with foreign exchange rate exposure.

As we commercialize our approved products, in particular our TULSA-PRO system in the United States, we expect that a significant portion of our revenues, expenses, current assets and current liabilities will be denominated in United States dollars, Euros and other foreign currencies. Currently, our financial statements are expressed in Canadian dollars. A decrease in the value of such foreign currencies relative to the Canadian dollar could result in decreases in revenues from currency exchange rate fluctuations. To date, we have not hedged against risk associated with foreign exchange rate exposure. Consequently, our results of operations may be negatively affected by foreign currency exchange rate fluctuations, which could have a negative impact on the market price of our Common Shares.

Risks Related to Our Business and Growth Strategy

We may not achieve our commercialization and future product development goals in the time frames expected, or at all.

We may set goals for and makes public statements regarding the timing of the accomplishment of objectives material to our success, such as the timing and extent of product launches in the jurisdictions where they are approved for marketing and sale, in particular our expected commercialization of the TULSA-PRO system following our recently obtained FDA clearance in the United States; third-party reimbursement for our approved products; the timing and terms of any collaborations, partnerships, licenses, acquisitions or other agreements; the commencement and completion of clinical trials, including follow-up data on our TACT Pivotal Clinical Trial; and anticipated regulatory submission and approval dates for our products in additional jurisdictions, and for future product candidates. The actual timing of these events can vary dramatically due to factors such as the uncertainties inherent in the arrangements sufficient to commercialize our products, including in respect of manufacturing, distribution and marketing, as well as market competition and adverse results from our clinical trials, and other factors and described herein, many of which are beyond our control. There can be no assurance that we will achieve our commercialization goals in respect of the TULSA-PRO system in the United States, or that future efficacy and safety results from our TACT Pivotal Clinical Trial will be favorable. If we fail to commercialize the TULSA-PRO system in the United States or any other approved products in the time frame and to the extent that we anticipate, our business, results of operations and financial condition may be materially adversely affected, and the price of the Common Shares could decline.

Our products, including the TULSA-PRO system, may not achieve or maintain expected levels of market acceptance.

The commercial success of our approved products, including the TULSA-PRO system which was recently FDA-cleared in the United States, is dependent upon achieving and maintaining market acceptance. New medical devices that appear promising in development may fail to reach the market or may have only limited or no commercial success. Levels of market acceptance for our products could be impacted by several factors, many of which are not within our control, including but not limited to:

| · | safety, efficacy, convenience and cost-effectiveness of our systems as a method of ablation of prostate tissue, uterine fibroids, bone metastases compared to products of our competitors or other forms of treatment; |

| · | scope of approved uses and marketing approval or clearance; |

| · | timing of market entry of our products versus those of our competitors; |

| · | difficulties in, or excessive costs required in the process of, manufacturing our products; |

| · | expanding compatibility of our systems to work with MRI scanners other than those made by Philips and Siemens, and maintaining our existing relationships with Philips and Siemens; |

| · | infringement or alleged infringement of the patents or intellectual property rights of others; |

| · | acceptance of the price of our products relative to those of our competitors; |

| · | acceptance and adoption of our products by patients, physicians/clinicians and the medical community; |

| · | the availability of training necessary for proficient use of our products, as well as willingness of physicians and technicians to participate in such training; |

| · | the perceived risks generally associated with the use of new products and procedures; |

| · | the placement of our products in treatment guidelines published by leading medical organizations; |

| · | the size and growth rate of the market for our products in the major geographies in which we operate or intend to operate, in particular in the United States; and |

| · | acceptance of our products by government and third-party payers for adequate reimbursement coverage. |

In addition, the success of any new product will depend on our ability to either successfully build our in-house sales and marketing capabilities or to maintain or secure new, or to realize the benefits of existing or future arrangements with, third-party marketing or distribution partners. See “—We intend to rely primarily on our in-house sales and marketing capabilities for our commercialization strategy, which will require substantial build-up and commitment of resources” and “—We currently rely on our collaborative partners, and we may rely on additional collaborative partnerships, to assist in the sales and marketing and/or distribution of our approved products” below. If we are unable to commercialize new products successfully, whether through a failure to achieve market acceptance, a failure to build our own in-house sales and marketing capabilities, a failure to maintain or secure new or existing marketing partners or to realize the benefits of our arrangements with our marketing and distribution partners, there may be a material adverse effect on our business, financial condition and results of operations and it could cause the market value of our Common Shares to decline.

Market acceptance of our approved products also depends on our ability to identify and address the relevant market. For example, our TULSA-PRO system is FDA-cleared in the United States for transurethral ultrasound ablation (“TULSA”) of prostate tissue, and is not specific to any particular condition or disease. For more information, see “We may be subject to fines, penalties or injunctions if we are determined to be promoting the use of our products for unapproved or “off-label” uses or engaged in false or misleading promotion.” below. Furthermore, our estimates of the number of patients who have received or might have been candidates to use a specific product may not accurately reflect the true market or market prices for such products or the extent to which such products will actually be used by patients. Our failure to successfully introduce and market our approved products could have a material adverse effect on our business, financial condition, and results of operations.

Successful commercialization of our approved products, including the TULSA-PRO system, and future product development depends upon our maintaining strong working relationships with physicians/clinicians.

If we fail to maintain positive working relationships with physicians/clinicians, our approved products, including our TULSA-PRO system, may not achieve the level of market acceptance sufficient for successful commercialization of the products. It is important for us to market our approved systems successfully to physicians/clinicians who we expect will use our approved products, and we depend on our sales and marketing personnel (and those of our collaborative partners, e.g., Philips and Siemens) to do so in an effective manner. We can provide no assurance that physicians/clinicians will prescribe or otherwise utilize our TULSA-PRO systems based on our existing clinical data (such as our TACT data) or the results of any future clinical trials, or at all. See “—Data from our clinical trials may not support regulatory approvals or clearances and/or reimbursement coverage for our products” below. We also rely on our relationships with physicians/clinicians to further develop our existing products and develop future product candidates in line with the clinical needs and expectations of the professionals who we expect will use and support the devices. These development efforts are similarly dependent upon us and our collaborative partners maintaining working relationships with physicians/clinicians.

In addition, we rely on physicians/clinicians to provide considerable knowledge and experience that assists us in the marketing and sale of our approved products and development of our products and product candidates. Physicians/clinicians assist us as researchers, marketing and product consultants, inventors and public speakers. If we are unable to maintain strong relationships with these professionals and continue to receive their advice and input, the development and marketing of our products could suffer, which could have a material adverse effect on our business, financial condition and operating results.

Physicians/clinicians misuse could result in negative publications, negative sentiment or adverse events, thereby limiting market acceptance and future sales of our products.

There is a risk that physicians/clinicians may misuse our products, such as not following the instructions for use, not using our products on the intended patient population, using our products with unapproved or modified hardware or software, or misuse by inadequately trained staff. Physicians/clinicians may also initiate their own clinical studies which may be poorly designed or controlled, and may result in adverse safety or efficacy results. Any of the foregoing could result in negative publications, negative sentiment or adverse events or regulatory actions in respect of our products, thereby limiting market acceptance and sales of our products, which could have a material adverse effect on our business, financial condition and results of operations.

We rely on the compatibility of our products with MRI scanners in the successful commercialization of our products.

We have designed our TULSA-PRO system to be capable of integration with some of the MRI scanners from two of the major MRI manufacturers (Philips and Siemens), and the Sonalleve system with one MRI manufacturer (Philips). Although we believe that our approved products can be used by the vast majority of hospitals and treatment facilities, not all such facilities utilize MRI scanners that are compatible with the TULSA-PRO and Sonalleve systems, and such facilities would be required to acquire (or outsource to other facilities that already have) compatible MRI equipment, which may increase their costs and which could restrict or delay utilization of our systems by such facilities. Accordingly, we intend to expand compatibility of the systems with other MRI scanners in the future, which would require design changes to our systems, collaboration with the manufacturer of the MRI scanner and may require additional regulatory approvals. We may be unsuccessful in making the necessary design changes and, if required, receiving the necessary regulatory approvals for such changes, and the terms of any such arrangements that we may enter into in the future with the MRI scanner manufacturers may not be on as favorable terms. Accordingly, we can provide no assurance that we will be successful in any such expansion of the compatibility of our products to other MRI scanners.

Successful commercialization of our approved products will also depend on the cost of the system and the availability of coverage and adequate reimbursement coverage from third-party payers.

Successful commercialization of our approved products, including our TULSA-PRO system, depends largely upon the cost of the system and the availability of coverage and adequate reimbursement for the system, and the medical procedure associated with its use, from third-party payers, such as government healthcare programs, private health insurers and other organizations, such as health maintenance organizations and managed care organizations. We expect that our systems will be purchased by health-care providers, including clinics and hospitals that use MRI scanners that are compatible with our systems, and that these providers will subsequently bill various third-party payers or will be responsible for covering the costs of the system through the provider’s operating budget. Although we expect there to be an out-of-pocket market for our approved products, an out-of-pocket market alone is unlikely to be sufficient to support successful commercialization of our products. To date we have not secured significant coverage or reimbursement for any of our products from government or third-party payors in the jurisdictions where we have regulatory approvals, including our TULSA-PRO system in the United States. We can provide no assurance that third-party payers will provide coverage and adequate reimbursement for our TULSA-PRO system to treat our targeted indications based on our existing clinical data (such as our TACT data) or the results of any future clinical trials, or at all. See “—Data from our clinical trials may not support regulatory approvals or clearances and/or coverage and reimbursement for our products” below. Accordingly, we likely will need to conduct additional research and successfully complete additional clinical trials in order to obtain such coverage (e.g., follow-up data from our TACT Pivotal Clinical Trial). Such additional research and clinical trials may require significant time and resources, and may not be successful, which could result in the postponement of or inability to obtain coverage and reimbursement for our approved products, which could significantly delay or otherwise negatively affect our commercialization strategy. Any of the foregoing could, in turn, have a material adverse effect on our business, results of operations and financial condition.

Third-party payers carefully review and increasingly challenge the prices charged for medical devices, procedures and services. Government healthcare programs in the United States and the European Union may reimburse certain providers at a pre-determined all-inclusive amount for all the costs associated with a particular procedure performed or course of treatment, based on such factors as the patient’s principal diagnosis, age and severity or complexity. Similarly, the surgeon or physician may be reimbursed at a pre-determined amount based on the procedure performed, and without taking into consideration the actual costs incurred, including the actual cost of the specific devices used.

New products are being increasingly scrutinized with respect to whether or not they will be covered at all by the various health plans and at what level of reimbursement. In some instances, economic research studies are and will be required to demonstrate whether our products and approach are superior from a long-term cost containment standpoint. Third-party payers may determine that our products are not medically necessary, not cost-effective, experimental, or primarily intended for non-approved indications. Such determinations could have a material adverse effect on our business, results of operations and financial condition.

Further, healthcare reform measures may be adopted in the future that may impose more rigorous coverage and reimbursement standards. We are unable to predict what, if any, additional legislation or regulation impacting the healthcare industry or third-party coverage and reimbursement may be enacted in the future, or what effect such legislation or regulation would have on our business.

We intend to rely primarily on our in-house sales and marketing capabilities for our commercialization strategy, which will require substantial build-up and commitment of resources.

We intend to rely primarily on our in-house sales and marketing capabilities in order to advance our commercialization strategy, particularly in the United States in respect of our recently FDA-cleared TULSA-PRO system. This will require a substantial commitment of time and resources in the near-term, and we may be unsuccessful in executing on this strategy, which could negatively impact our anticipated commercialization. We are in the early stages of expanding our U.S. sales and marketing capabilities and can provide no assurance that we will be successful in establishing a marketing presence and sales force sufficient to commercialize the TULSA-PRO system successfully in the United States.

In addition, by relying on an in-house sales and marketing function, we may have less visibility in the U.S. market (particularly among hospitals) than we would have if we had significant third-party distribution relationships. Any shortcomings in our in-house sales force may have a material adverse effect on our business, results of operations and financial condition.

We currently rely on our collaborative partners, and we may rely on additional collaborative partnerships, to assist in the sales and marketing and/or distribution of our approved products.

We currently rely on our collaborative partnerships for the sales and marketing and/or distribution of our approved products, in particular Philips and Siemens, who promote our systems that are compatible with the MRI scanners produced and sold by them to end users, including hospitals and clinics. In the future, we intend to enter into similar arrangements with other producers of MRI scanners to increase the compatibility of our products and to promote and increase market acceptance among hospitals, clinics and other end-users. However, we can provide no assurance that we will be successful in establishing such additional arrangements, which could negatively impact our commercialization strategy and may have a material adverse effect on our business, results of operations and financial condition. See “—We rely on the compatibility of our products with MRI scanners in the successful commercialization of our products” above.

We may also seek out, evaluate and negotiate other third-party marketing and/or distribution arrangements for our products in the jurisdictions where they are approved, which may involve the commitment of substantial time and effort and may not ultimately result in an arrangement that is favorable to our commercialization goals (e.g. if such third-party marketing or distribution partners are not as successful in promoting our products as anticipated). If any of these third party collaborators are unable or unwilling to promote and/or deliver our products to our customers in an effective manner, then our business, financial condition and operating results could be materially impacted.

Additionally, if any of our relationships with third-party collaborators is terminated, whether by us or the third party for any reason, there can be no assurance that we will be able to obtain alternative sales and marketing and/or distribution channels rapidly or effectively enough to prevent disruptions in sales generated in those markets or otherwise to ensure the success of our products in those markets. Any such termination may have material adverse impact on our business, results of operations and financial condition.

We may experience manufacturing scaling issues in connection with our commercialization strategy, as we have limited experience assembling and testing our approved products, including the TULSA-PRO system, at a significant scale.

As we implement our commercialization strategy, in particular in respect of the TULSA-PRO system in the United States, we may not be able to produce sufficient quantities of systems or maintain consistent quality control in the production of our systems. We have limited experience in assembling and testing our approved products, including our TULSA-PRO system, on a commercial scale. To commercialize our approved products successfully and become profitable, we must be able to assemble and test such in commercial quantities in compliance with applicable regulatory requirements, and at an acceptable cost. Increasing our capacity to assemble and test our products on a commercial scale will require us to improve internal efficiencies, including hiring additional experienced personnel, which may result in significant capital expenditures. We may encounter a number of difficulties in increasing our assembly and testing capacity, including:

| · | managing production yields; |

| · | maintaining quality control and assurance; |

| · | providing component and service availability; |

| · | maintaining adequate control policies and procedures; |

| · | hiring and retaining qualified personnel; and |

| · | complying with U.S. and Canadian regulations (including at the state, provincial and/or federal levels) and applicable foreign regulations. |

In particular, our ability to increase our assembly and testing capacity successfully will greatly depend on our ability to hire, train and retain an adequate number of employees, in particular employees with the appropriate level of knowledge, background and skills to assemble and test our products. We compete with several other medical device companies to hire and retain these skilled employees, and we may be unable to hire and retain such employees in numbers sufficient to increase our in-house capabilities.

We currently intend to partner with one or more additional QSR-compliant and FDA-registered contract manufacturers for our TULSA-PRO systems in the United States. However, we may not be successful in establishing or maintaining such partnerships on acceptable terms or in the timeframe necessary to commercialize our products successfully, or at all.

In addition, we may encounter difficulties in scaling our manufacturing operations, whether in-house or through third-party contract manufacturers, as a result of, among other things, quality control and quality assurance issues and availability of components and raw material supplies. Any such quality control issues may negatively affect production and sales of our products, and may require increased repair or re-engineering costs due to product returns, defects and increased expenses due to switching to alternate suppliers, and reputational damage, any of which could negatively affect our business and reputation.

If we are unable to satisfy commercial demand for our products, in particular our TULSA-PRO system in the United States, due to our inability (or the inability of any of our contract manufacturers) to assemble and test such products in sufficient quantities with consistent quality control, and in compliance with applicable regulatory requirements (and in a cost-efficient manner), our ability to commercialize such products successfully, and market acceptance of our products could be adversely affected as our target customers may instead purchase or use our competitors’ products. This, in turn, could have a material adverse effect on our business, results of operations and financial condition.

We rely on third parties to manufacture and supply components of our systems.

The TULSA-PRO and Sonalleve systems consists of common electronic components, proprietary capital equipment and proprietary disposables. We purchase standard electronic components for our systems from a number of third-party vendors. The capital equipment consists of custom system electronics, a treatment delivery console, fluid circuits and an MRI compatible robotic positioning system. Printed circuit boards and assemblies and custom mechanical parts are outsourced from approved suppliers.

We cannot be certain that manufacturing sources for all components will continue to be available or that we can continue to outsource the manufacturing of our components on reasonable or acceptable terms. If we encounter delays or difficulties with contract manufacturers, delivery of our products could be delayed. In addition, we could be forced to secure new or alternative contract manufacturers or suppliers. Securing a replacement contract manufacturer or supplier could be difficult, and we may not be able to do so in a timely manner or without significant expense. Any loss of a manufacturer or any difficulties that could arise in the manufacturing process could significantly affect our ability to supply sufficient amounts of our products to our customers on a timely basis, which may negatively affect our market share and, correspondingly, could have a material adverse effect on our business, results of operations and financial condition.

In addition, not all of our suppliers provide us with guaranteed minimum production levels, and we rely on single-source suppliers for some of our components. See “—We depend on single-source suppliers for some of the components in our systems” below. Furthermore, we do not currently have long-term supply contracts, and accordingly, our suppliers could terminate their services at any time without penalty within agreed notice periods. As a result, there can be no assurance that we will be able to obtain sufficient quantities of components in the future necessary to commercialize our approved products.

Our reliance on third-party manufacturers and suppliers involves a number of additional risks, including, among other things:

| · | contract manufacturers or suppliers may fail to comply with regulatory requirements or make errors in manufacturing that could negatively affect the efficacy or safety of our products or cause delays in shipments of products; |

| · | we or our contract manufacturers and suppliers may not be able to respond to unanticipated changes in customer orders, and if orders do not match forecasts, our suppliers may have excess or inadequate inventory of materials and components; |

| · | we or our contract manufacturers and suppliers may be subject to price fluctuations of raw materials and key components due to a lack of long-term supply arrangements for key components; |

| · | we or our contract manufacturers and suppliers may lose access to critical services and components, resulting in an interruption in the manufacture, assembly and shipment of our products; |

| · | we may experience delays in delivery by our contract manufacturers and suppliers due to changes in demand from us or our other customers; |

| · | fluctuations in demand for products that our contract manufacturers and suppliers manufacture for others may affect their ability or willingness to deliver components in a timely manner; |

| · | suppliers or contract manufacturers may wish to discontinue supplying components or services for risk management reasons; |

| · | we may not be able to find new or alternative components or reconfigure our system and manufacturing processes in a timely manner if the necessary components become unavailable; and |

| · | contract manufacturers and suppliers may encounter financial hardships unrelated to our demand, which could inhibit their ability to fulfill orders and meet our requirements. |

If any of these risks materialize, it could significantly increase costs and impact our ability to meet demand for our products, in particular in respect of our planned commercialization of TULSA-PRO in the United States. If we are unable to satisfy commercial demand for the TULSA-PRO system or other approved products in a timely manner, our ability to generate revenue could be impaired, market acceptance of our products could be adversely affected, and customers may instead purchase or use competitors’ products. As a result, our business, results of operations and financial condition may be materially adversely affected.

We depend on single-source suppliers for some of the components in our systems.

We currently rely on a single source for the manufacture of some of the components of our TULSA-PRO and Sonalleve systems. Although we intend to procure alternative supply sources for our components as our commercialization efforts increase, we can provide no assurance that we will be successful. Establishing additional or replacement suppliers for these components will take a substantial amount of time and could result in increased costs and impair our ability to produce our products. In addition, our products are highly technical and are required to meet exacting specifications, and any quality control problems that we experience from such alternative supply sources could negatively affect our reputation and market acceptance of our products.

We may also have difficulty obtaining similar components from other suppliers that are acceptable to the FDA or foreign regulatory authorities. The failure of our suppliers to comply with strictly enforced regulatory requirements could expose us to regulatory action, including warning letters, product recalls, termination of distribution, product seizures, or civil penalties. See “—Risks Relating to the Regulation of the Company and Our Products” below for more information.

If we fail to procure alternative supply sources on acceptable terms or at all, our planned commercialization of TULSA-PRO in the United States could be negatively affected, which could have a material adverse effect on our business, operating results and financial condition.

We face significant competition in the markets for our products, and in particular, there are numerous devices and procedures that compete with our TULSA-PRO system.

Our products face significant competition from currently available and future medical devices or surgical methodologies that are used in the same patient populations as our products. See Item 4.B, “Information on the Company—Business Overview—Competition”. Some of these available options are well-established, and our competitors have greater financial resources, development, selling and marketing capabilities than we do. We may face further competition from medical equipment/supply companies that focus their efforts on developing and marketing products that are similar in nature to our products, but that in some instances offer improvements over our products. Our competitors may succeed in developing technologies and products that are more effective or less expensive to use than our products. These developments could render our products uncompetitive, which would have a material adverse effect on our business, financial condition and operating results. In addition, academic institutions, government agencies and other public and private organizations conducting research may seek patent protection with respect to potentially competitive products. They may also establish exclusive collaborative or licensing relationships with our competitors.

Further, our industry is also subject to changing industry standards, market trends and customer preferences and to competitive pressures which can, among other things, necessitate revisions in pricing strategies, price reductions and reduced profit margins. Our success will depend, in part, on our ability to achieve technological superiority in our products and operations and maintain such superiority in the face of new technologies. No assurance can be given that further modification of our product offerings will not be required in order to meet demands or to make changes necessitated by developments made by competitors that might render our products less competitive. Our future success will be influenced by our ability to continue to develop, test and market our products and future product candidates, including increasing and/or maintaining their compatibility with MRI scanners. Although we have committed resources to these efforts, there can be no assurance that we will be successful.

Data from our clinical trials may not support regulatory approvals or clearances and/or reimbursement coverage for our products.

Regulatory clearances and approvals for the commercial sale of any of our product candidates require that we demonstrate through clinical trials that the product candidate is safe and effective for its intended use or, to receive 510(k) clearance in the United States, that the product candidate is substantially equivalent to an existing predicate device for its intended use. While we have obtained 510(k) clearance for TULSA-PRO, additional follow-up data from our TACT Pivotal Clinical Trial may not be consistent with our 12-month data in terms of efficacy and/or side effect profile, which in certain circumstances may result in the FDA taking regulatory actions that are adverse to us. In addition, our TACT Pivotal Clinical Trial involves a relatively small patient population. Because of the small sample size, the results may not be indicative of future results.

We believe that third-party payers, in determining reimbursement coverage for our products, including the TULSA-PRO system, generally would rely upon our clinical trial results, such as TACT, that were obtained in support of our regulatory approvals; however, we may be required to provide additional data from our existing trials and/or conduct additional clinical trials prior to obtaining reimbursement coverage for the TULSA-PRO system and other approved products, which would likely involve significant time and expense, and may have a material adverse effect on our business, results of operations and financial condition.

In the future, we may also seek regulatory approvals, which may include 510(k) clearance, for other product candidates, which likewise could be adversely affected by insufficient clinical trial results. Obtaining product clearance or approval and conducting the requisite clinical trials is a long, expensive and uncertain process and is subject to delays and failures at any stage. There can be no assurance that clinical trials will be completed successfully within any specified period of time, if at all. In addition, a regulatory authority may disagree with our interpretation of the data from our clinical trials, or may find the clinical trial data inadequate to support clearance or approval, and may require us to extend existing clinical trials and/or pursue additional clinical trials, which would increase costs and could further delay regulatory approval or clearance of our products, or cause such regulatory approvals or clearances to be denied altogether.

The data from a clinical trial may be inadequate to support clearance or approval of an application to the regulatory authorities for numerous reasons including, but not limited to:

| · | prevalence and severity of adverse events and other unforeseen safety issues; |

| · | changes in regulatory requirements, policies or guidelines; |

| · | the interim or final results are insufficient (including in respect of the time period for which results were obtained), inconclusive or unfavorable as to the safety or efficacy of the device; |