February 4, 2015

Larry Spirgel

Assistant Director

Division of Corporation Finance

Securities and Exchange Commission

Washington, D.C. 20549

| Re: | Videocon d2h Limited Draft Registration Statement on Form F-4 Submitted December 31, 2014 |

Comment Letter Dated January 27, 2015

CIK No. 0001629220

Dear Mr. Spirgel:

This letter is in response to the comment letter of the Staff of the Securities and Exchange Commission dated January 27, 2015 (the “Comment Letter”) regarding the draft Registration Statement on Form F-4 of Videocon d2h Limited (the “Company”) (the “Form F-4”).

We have addressed each of the Staff’s comments in the order presented in the Comment Letter. For ease of reference, we have included each Staff comment in bold and inserted our response after each comment.

General

| 1. | We note references to third-party market data throughout the prospectus. Please provide us with copies of any materials that support third-party statements, clearly cross-referencing a statement with the underlying factual support. Confirm for us that these documents are publicly available. To the extent any of these reports have prepared specifically for this filing, file a consent from the party. |

Response: The Company has made references in the Form F-4 to"Indian DTH Market Overview — Key Dynamics & Future Outlook 2014," a report prepared by Media Partners Asia, Ltd ("MPA"), an independent provider of information services, focusing on media, communications, and entrainment industries (the "MPA Report"). The report is not publicly available and was prepared for the Company for the purposes of filing the Form F-4. A consent has been obtained from Media Partners Asia, Ltd regarding inclusion of the MPA Report in the F-4 and has been filed as Exhibit 23.3 to the Amendment to Form F-4. The MPA report is attached here as Annex A.

The following statements made by the Company in the Form F-4 are supported by the relevant sections in the MPA Report:

| · | Statements on page 14 of the Form F-4: "Videocon d2h is the fastest growing direct-to-home, or DTH provider in India by acquisition of new subscribers, adding approximately 9.0 million gross subscribers during the period from April 2011 through September 2014 across India". (Reference: "Exhibit 18: Operator Share of Gross Subs" on page 25 of the MPA Report). |

| · | Statements on page 31 of the Form F-4: "Videocon d2h's gross DTH subscriber base has increased from approximately 0.44 million as of March 31, 2010 to 11.82 million as of September 30, 2014..." (Reference: "Exhibit 17: Operator Share of Gross Subs" on page 25 of the MPA Report). |

| · | Statement on page 149 of the Form F-4: "It has grown its subscriber base from 0.44 million gross subscribers as of March 31, 2010, representing approximately 1.9% of the total DTH gross subscriber base in India to 10.45 million gross subscribers as of March 31, 2014, representing approximately 15.7% of the total DTH gross subscriber base inIndia…" (Reference: "Exhibit 17: Operator Share of Gross Subs" on page 25 of the MPA Report). |

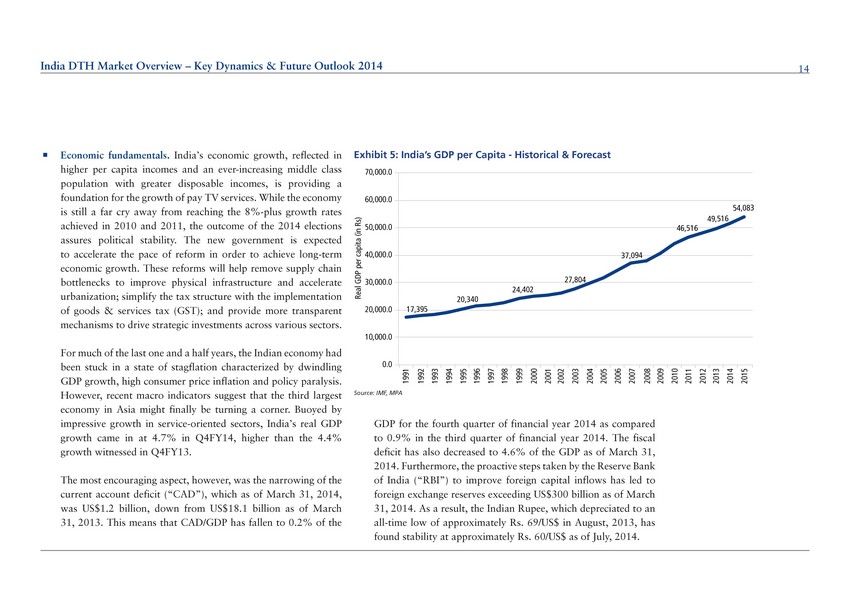

| · | Statement on page 128 of the Form F-4: Recently, economic growth in India has decreased from the 8% rates achieved in 2010 and 2011. Please see page 14 of the MPA Report. |

| · | Statement on page 128 of the Form F-4: The outcome of the 2014 elections has increased political stability in India. Please see page 14 of the MPA Report. |

| · | Statement on page 128 of the Form F-4:In recent times, the Indian economy had stagnant GDP growth, high consumer price inflation and policy paralysis, but recent macro indicators suggest that India’s economy may be recovering.Please see page 14 of the MPA Report. |

| · | Statement on page 128 of the Form F-4:India’s real GDP growth was 4.7% in the fourth quarter of the financial year 2014, an increase fromthe 4.4% growth for the fourth quarter of the financial year 2013.Please see page 14 of the MPA Report. |

| · | India hadreduction of the current account deficit (‘‘CAD’’) to which US$1.2 billion as of March 31, 2014 from US$18.1 billion as of March 31, 2013. This means that AD has fallen 0.2% of the GDP for the fourth quarter of financial year 2014 compared to 0.9% in the third quarter of financial year 2014.Please see page 14 of the MPA Report. |

| · | Statement on page 128 of the Form F-4:The fiscal deficit has also decreased to 4.6% of the GDP as of March 31, 2014. |

| · | Statement on page 128 of the Form F-4:The proactive steps taken by the Reserve Bank of India (“RBI”) to improve foreign capital inflows has led to foreign exchange reserves exceeding US$300 billion as of March 31, 2014.Please see page 14 of the MPA Report. |

Videocon d2h Limited

(formerly Bharat Business Channel Limited

Corporate Office: 1st floor, Techweb Center, New link Road, Oshiwara, Mumbai-400102, India

Ph: 91-22-4255 5000 ; Fax - 91-22-4255 5050

Registered office : Auto Cars Compound, Adalat Road, Aurangabad – 431 005. Maharashtra.

Ph: 91-240-2320750 ; Fax - 91-240 233575

www.videocon.d2h.com

CIN : U92100MH2002PLC137947

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 1

| · | Statement on page 128 of the Form F-4:The Indian Rupee, which depreciated to an all-time low of approximately Rs.69/US$ in August 2013, has foundstability at approximately Rs.60/US$ as of July 2014.Please see page 14 of the MPA Report. |

| · | Statement on page 128 of the Form F-4:Equity markets in India have witnessed a revival on account of the improved macro environment. During the financial year 2014, Foreign Institutional Investors (“FIIs”) invested a net amount of Rs.797.1 billion into Indian equities.As a result,India’s benchmark equity indices, Sensex and Nifty, reached historical highs.Please see page 15 of the MPA Report. |

| · | Statement on page 128 of the Form F-4:Foreign Direct Investment (“FDI”) continued to exhibit growth in India. According to the United Nations Conference on Trade and Development (“UNCTAD”), FDI flows into India grew by 17.0% over the financial year 2013 to US$28 billion.Please see page 15 of the MPA Report. |

| · | Statement on page 128 of the Form F-4:Business confidence in India has also improvedin recent months on hopes of greater political stability after the Union elections.Please see page 15 of the MPA Report. |

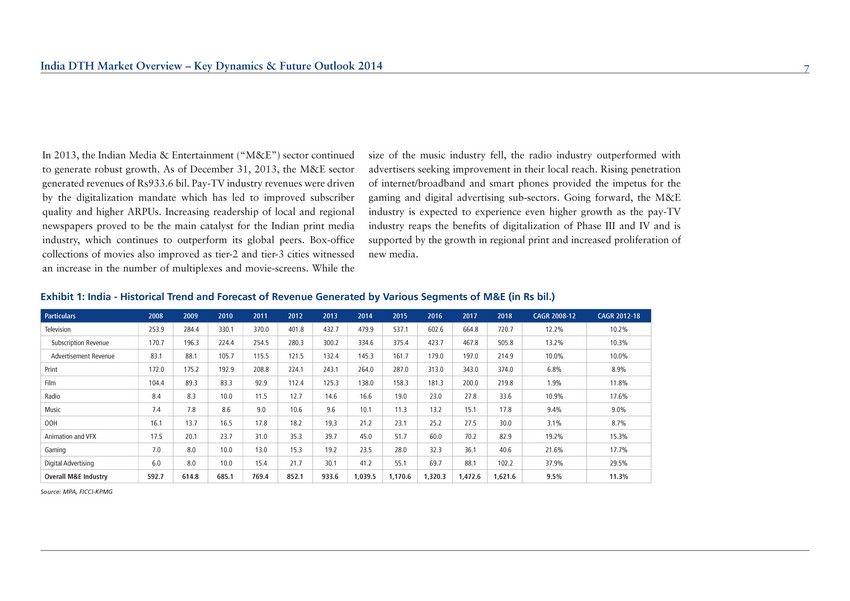

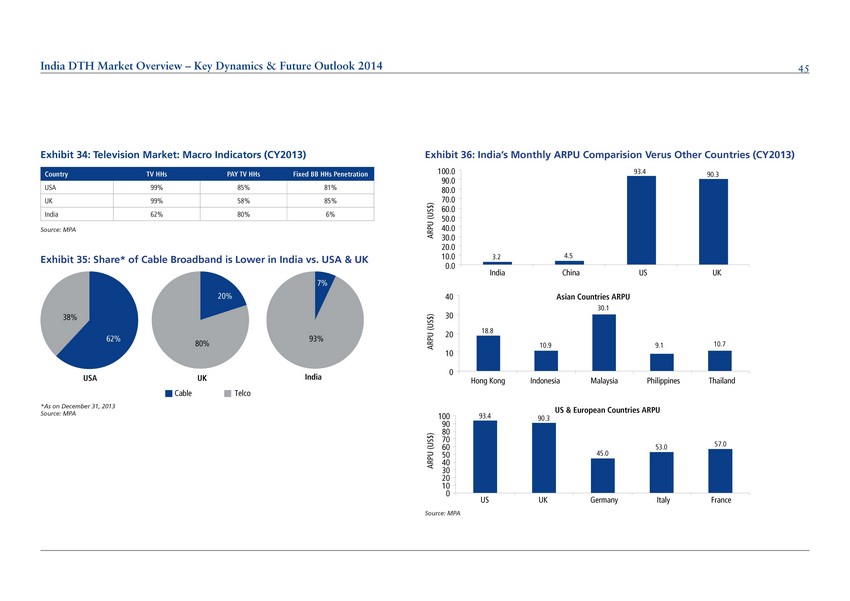

| · | Statement on page 129 of the Form F-4:In 2014, the Indian Media & Entertainment (“M&E”) sector continued to exhibit growth. In the year ended December 31, 2013, the M&E sector generated revenues of Rs.933.6 billion. Pay-TV industry revenues were driven by the digitalization mandate which has led to improved subscriber quality and higher Average Revenue Per User (“ARPU”).Please see page 7 of the MPA Report. |

| · | Statement on page 129 of the Form F-4:An increase in the readership of local and regional newspapers was a key driver for the Indian print media industry, which continues to outperform its global peers.Please see page 7 of the MPA Report. |

| · | Statement on page 129 of the Form F-4:Box-office collections of movies in India also improved as tier-2 and tier-3 cities experienced an increase in the number of multiplexes and movie-screens.Please see page 7 of the MPA Report. |

| · | Statement on page 129 of the Form F-4:While the size of the music industry decreased, the radio industry increased with advertisers expanding their local reach.Please see page 7 of the MPA Report. |

| · | Statement on page 129 of the Form F-4:The growing penetration of internet, broadband and smart phones provided the impetus for the gaming and digital advertising sub-sectors.Please see page 7 of the MPA Report. |

| · | Statement on page 129 of the Form F-4:In the future, the M&E industry is expected to experience higher growth as the pay-TV industry benefits from the government's digitalization initiative.Please see page 7 of the MPA Report. |

| · | Statement on page 132 of the Form F-4:Increasing purchasing power is expected to result in a higher number of homes with TVs in India.Please see page 15 of the MPA Report. |

| · | Statement on page 132 of the Form F-4:Pay-TVpenetration in households will also grow in India.Please see page 15 of the MPA Report. |

| · | Statement on page 132 of the Form F-4:By 2023, it is estimated that 70.0% of the pay-TV market in India will be digitalized.Please see page 15 of the MPA Report. |

| · | Statement on page 132 of the Form F-4:The Indian government’s mandate to digitalize the cable TV market using Digital Addressable Cable TV System ("DAS") will be a catalyst to future growth of the pay-TV market in India.Please see page 15 of the MPA Report. |

| · | Statement on page 132 of the Form F-4:Between 2015 and 2017, subscriber growth is expected to be strong given the government's implementation of the DAS mandate.Please see page 15 of the MPA Report. |

| · | Statement on page 132 of the Form F-4:After 2017, digital pay-TV subscriber growth is expected todecrease as consolidation and monetization of the industry will take priority.Please see page 15 of the MPA Report. |

| · | Statement on page 132 of the Form F-4:In terms of revenue, televisionrepresented approximately 46.0% of India’s total media industry in 2013.Please see Exhibit 2 on page 8 of the MPA Report. |

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 2

| · | Statement on page 132 of the Form F-4:In 2012, the television industry in India was estimated at Rs.401.8 billion and is expected to grow at aCAGR of 10.2% between 2012 and 2018, to reach Rs.720.7 billion in 2018. Please see Exhibit 1 on page 7 of the MPA Report. |

| · | Statement on page 132 of the Form F-4: Subscription charges, as a portionof total industry revenue, are expected to increase from 67.2% in 2008 to 70.2% in 2018. These percentages are calculated from the data provided inExhibit 1 on page 7 of the MPA Report. |

| · | Statement on page 133 of the Form F-4:Despite the recent increase in production costs, digitalization of the TV industry in India continues to create new opportunities for content producers. Content producers now focus on improving the quality of content, targeting specific demographics through localized content and niche offerings.Please see page 13 of the MPA Report. |

| · | Statement on page 133 of the Form F-4:Ownership of intellectual propertyrights has enabled content providers to grow and attain better monetization.Please see page 13 of the MPA Report. |

| · | Statement on page 134 of the Form F-4: Broadcasters have benefited most from digitalization as it has resulted in improved addressability and higher yields. The revenue mix continues to be dominated by advertising revenue. Please see page 13 of the MPA Report. |

| · | Statement on page 134 of the Form F-4: In the future, subscription fee growth is expected to outpace that of advertising. Please see page 13 of the MPA Report. |

| · | Statement on page 134 of the Form F-4: Improved addressability in cable and |

CPS-linked deals with higher consumer ARPU will be long-term growth drivers for pay-TV channel subscription revenues. Please see page 13 of the MPA Report.

| · | Statements on page 134 of the Form F-4: Two key regulatory developments, the cap on commercial advertisement inventory and the unbundling of channel aggregators, will determine the future course of the industry. Please see page 13 of the MPA Report. |

| · | Statements on page 134 of the Form F-4: These regulations adversely impact the economics of smaller or standalone players. The industry is expected to consolidate and a more level playing field is expected to develop. Please see page 13 of the MPA Report. |

| · | Statements on page 134 of the Form F-4: In 2013, the industry added 5.4 million net new subscribers, taking the overall industry base to 135 million, 80.0% penetration of TV homes, including multiple subscriptions. Much of this growth has been driven by DTH satellite, which had a 66.0% share of net new additions in 2013. Please see page 15 of the MPA Report. |

| · | Statement on page 134 of the Form F-4: Cable TV subscribers numbered 97.6 million in 2013, a 72.0% market share, with 27.9 million gross digital subscribers. Please see page 15 of the MPA Report. |

| · | Statements on page 134 of the Form F-4:Phases III and IV of the DAS program will be critical for growth in overall digital penetration. DTH in particular is expected to play a key role in adding net new subscribers. Without monetization, digitalization is meaningless and cable multi-system operators (‘‘MSOs’’) may need to increase billing, packaging and revenue collections in Phases I and II of the DAS program, a trend that began in the first quarter of 2014.Please see page 15 of the MPA Report. |

| · | Statements on page 134 of the Form F-4:A notable driver of TV industry value has been the advent of digital TV services, spurred largely by a well-organized and highly competitive DTH industry. DTH subscription revenues accounted for 33.5% of total pay-TV subscription revenues generated in India, and 23.5% of total TV industry revenues.Please see page 9 of the MPA Report. |

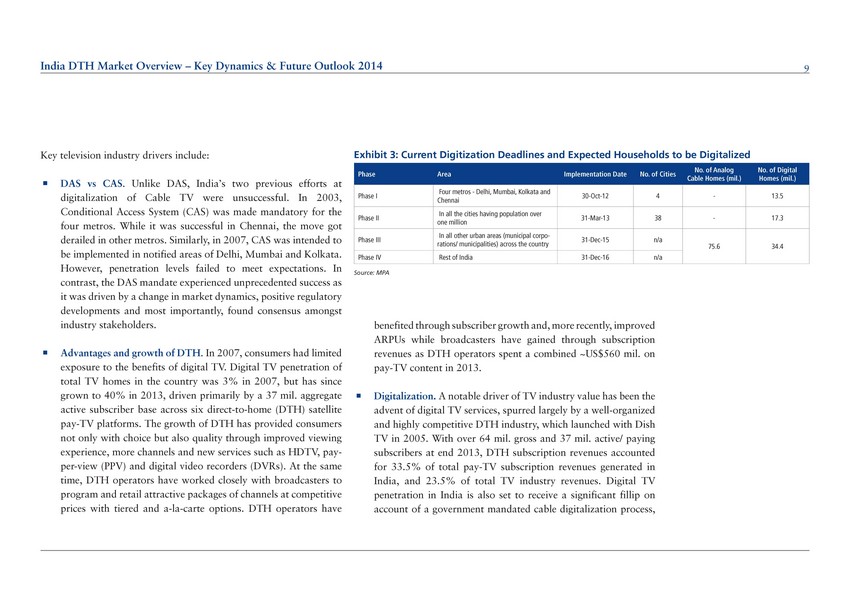

| · | Statements on pages 134-135 of the Form F-4: Digital TV penetration in India is also expected to increase on account of the government mandated cable digitalization process, which accelerated after November 1, 2012. Phases III and IV will be rolled out on December 31, 2015 and December 31, 2016, respectively, and will be comprised of all other regions in the country. Please see pages 9 - 10 of the MPA Report. |

| · | Statement on page 135 of the Form F-4: In November 2012, DAS Phase I was successfully implemented. The rollout was opposed by certain LCO groups and local political parties. However, despite the conflicting opinions from certain sections of the industry, the Phase I rollout was reasonably successful in Delhi, Mumbai and Kolkata. It is estimated that the top five MSOs deployed approximately 9 million STBs in Phase I markets. However, these are gross subscriptions and the platform has yet to test its initial churn numbers. Net-ARPUs to MSOs have started to see improvement as operators implement gross billing and roll out packages. Please see page 10 of the MPA Report. |

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 3

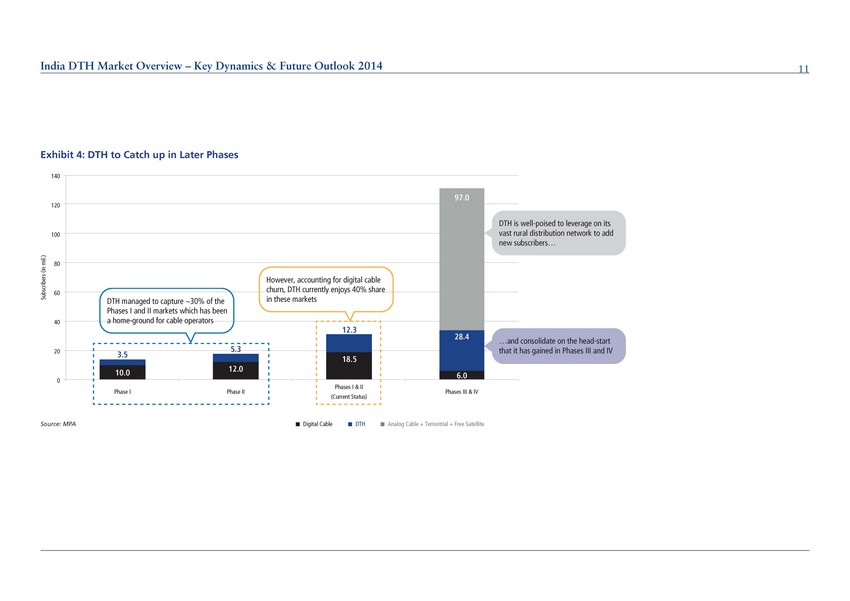

| · | Statements on page 135 of the Form F-4: Phase II has been a success in terms of digital deployment. Cable operators deployed 12 million STBs in these markets, although on-ground collections have remained below par. Digital cable managed to retain a little over 70.0% market share in DAS Phases I and II combined. The stronger presence of MSOs in Phases I and II markets enabled them to gain higher share against DTH. However, making inroads to Phases III and IV will be challenging for cable as this remains a dominant market for DTH, which has the benefit of an established distribution network spread across a much wider geography. Please see page 10 of the MPA Report. |

| · | Statements on page 136 of the Form F-4: In 2007, consumers had limited exposure to the benefits of digital TV. In 2007, digital TV penetration of total TV homes in the country was 3.0%, but has since increased to 40.0% in 2013. This increase was driven primarily by a 37 million aggregate active subscriber base across six DTH satellite pay-TV platforms. Please see page 9 of the MPA Report. |

| · | Statements on page 136 of the Form F-4: The growth of DTH has provided consumers with greater choice and quality through an improved viewing experience, more channels and new services such as HDTV, pay-per-view and DVRs. DTH operators have worked closely with broadcasters to program and retail attractive packages of channels at competitive prices with tiered and a-la-carte options. Please see page 9 of the MPA Report. |

| · | Statements on page 136 of the Form F-4: DTH operators have benefited through subscriber growth and, more recently, improved ARPUs while broadcasters have gained through subscription revenues as DTH operators spent a combined approximately US$560 million on pay-TV content in 2013. Please see page 9 of the MPA Report. |

| · | Statements on page 136 of the Form F-4: Unlike DAS, India’s two previous efforts at digitalization of Cable TV were unsuccessful. In 2003, Conditional Access System (‘‘CAS’’) was made mandatory for Delhi, Mumbai, Kolkata and Chennai. While it was successful in Chennai, the move experienced problems in other cities. Similarly, in 2007, CAS was intended to be implemented in notified areas of Delhi, Mumbai and Kolkata. However, penetration levels failed to meet expectations. By contrast, the DAS mandate has witnessed unprecedented success, driven by changes in market dynamics, positive regulatory developments and, most importantly, consensus amongst stakeholders. Please see page 9 of the MPA Report. |

| · | Statements on page 136 of the Form F-4: Digitalization has improved addressability for broadcasters thus enabling monetization of subscriptions and has also led to rationalization of distribution costs. Digitalization has also led to improvement in the quality of content, content production and transmission. Most channels in key genres such as Hindi GECs, movies, sports and infotainment now offer HD feed. This has increased the number of HD subscribers for operators, while also improving their blended yields. The next wave of growth is expected to come from HD feeds for regional content; however, with the exception of Sun TV in south India, this has not been explored. Additionally, subsidized HD offerings will also act as a key differentiator for DTH players as cable is yet to roll out packages and push HD services across broader markets. Please see page 13 of the MPA Report. |

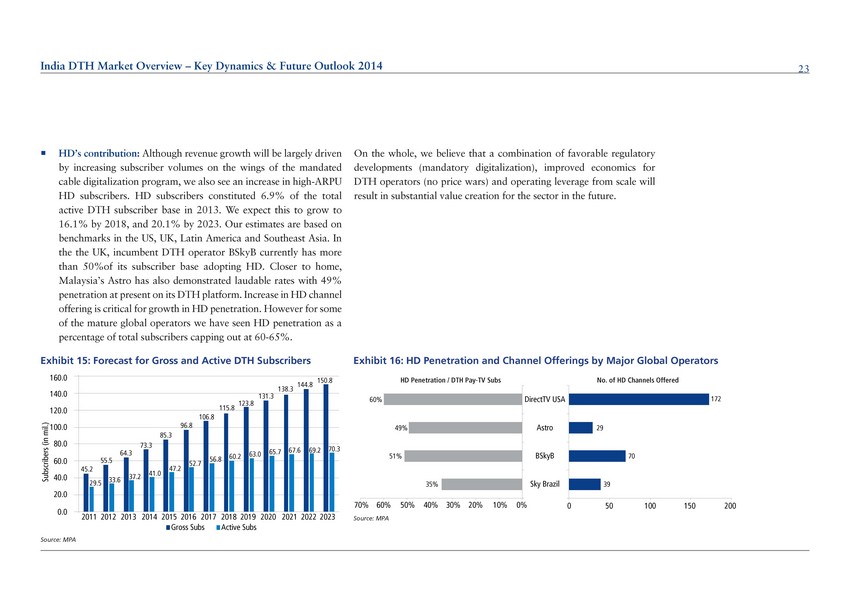

| · | Statements on page 136 of the Form F-4: HD is expected to contribute to the industry. Although revenue growth is expected to be driven by increasing subscriber numbers as a result of the mandated cable digitalization program, an increase in high-ARPU HD subscribers is also expected. Please see page 23 of the MPA Report. |

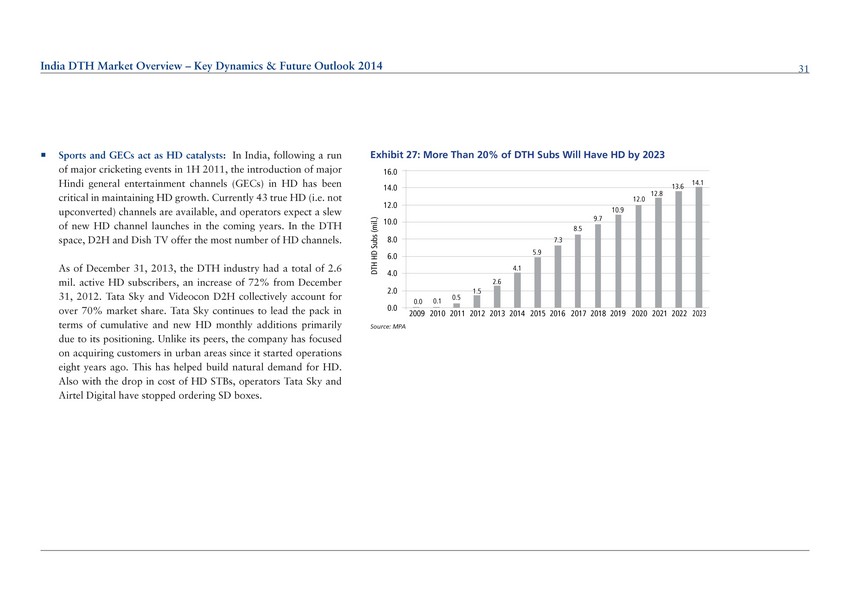

| · | Statements on page 136 of the Form F-4: It is expected that HD penetration will grow significantly in the future, rising from less than 7.0% of active DTH subscribers currently, to over 20.0% by 2020, based on benchmarks in the United States, United Kingdom, Latin America and Southeast Asia. In the United Kingdom, incumbent DTH operator BSkyB currently has more than 50.0% of its subscriber which has adopted HD. Malaysia’s Astro has also demonstrated strong rates with 49.0% penetration at present on its DTH platform. An increase in HD channel offerings is critical for growth in HD penetration. However, for some mature global operators, HD penetration as a percentage of total subscribers is limited between 60.0% and 65.0%. Please see page 23 of the MPA Report. |

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 4

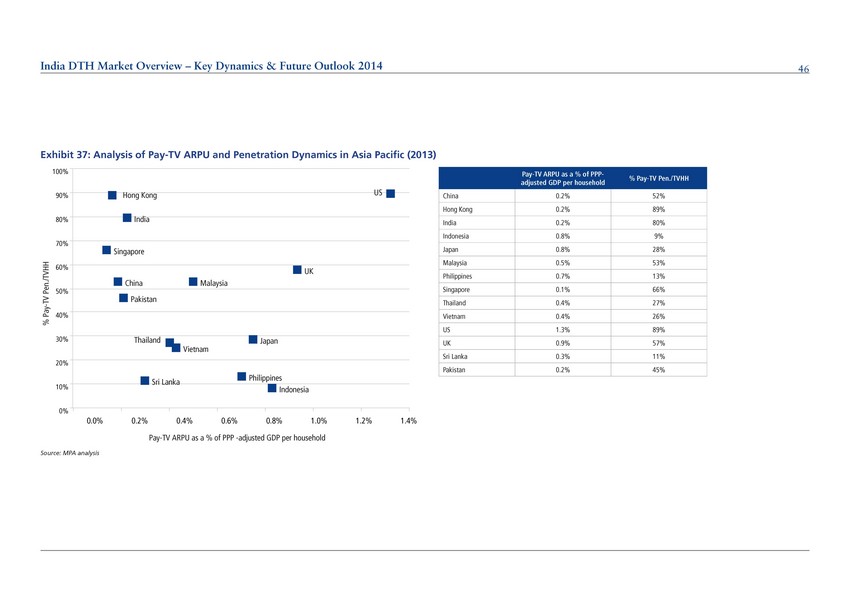

| · | Statements on page 137 of the Form F-4: Although India’s pay TV ARPUs remain one of the lowest in the world at US$3.2 per month, it has been showing improvements in recent years as a direct result of digitalization, smarter packaging of content and channels and the provision of value added services, such as HD and DVR. Further improvements from rational DTH and digital cable pricing and the growth of premium pay-TV are expected in the next few years. Please see page 12 of the MPA Report. |

| · | Statement on page 139 of the Form F-4:Over the past eight years, the Indian television industry has experienced significant growth in theadoption of DTV services, driven by DTH.Please see page 20 of the MPA Report. |

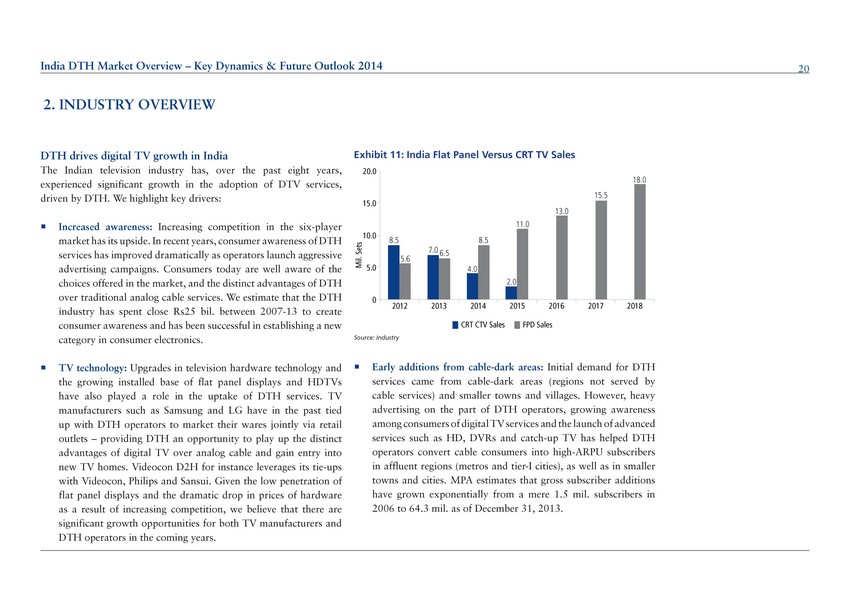

| · | Statements on page 139 of the Form F-4:Increasing competition in the six-player market has certain advantages. In recent years, consumer awareness of DTH services has improved as operators launch aggressive advertising campaigns. Consumers today are more aware of the choices available in the market and the distinct advantages of DTH over traditional analog cable services. Between 2007 and 2013, it is estimated that the DTH industry spent approximately Rs.25 billion to create consumer awareness and establish a new category in consumer electronics.Please see page 20 of the MPA Report. |

| · | Statements on page 139 of the Form F-4: Upgrades in television hardware technology and the growing installed base of flat panel displays and HDTVs have also played a role in the uptake of DTH services. TV manufacturers such as Samsung and LG have in the past partnered with DTH operators to market their wares jointly through retail outlets. This marketing strategy provided DTH an opportunity to play up the distinct advantages of digital TV over analog cable and gain entry into new TV homes. Videocon d2h leverages its tie-ins with Videocon, Philips and Sansui. Given the low penetration of flat panel displays and the dramatic drop in prices of hardware as a result of increasing competition, there are growth opportunities for both TV manufacturers and DTH operators in the coming years. Please see page 20 of the MPA Report. |

| · | Statements on page 139 of the Form F-4: Initial demand for DTH services came from cable-dark areas (regions not served by cable services) and smaller towns and villages. However, advertising on the part of DTH operators, growing awareness among consumers of digital TV services and the launch of advanced services such as HD, DVRs and catch-up TV has helped DTH operators convert cable consumers into high-ARPU subscribers in affluent regions (metropolitan regions and tier-1 cities), as well as in smaller towns and cities. It is estimated that gross subscriber additions have grown from approximately 1.5 million subscribers as of December 31, 2006 to 64.3 million as of December 31, 2013. Please see page 20 of the MPA Report. |

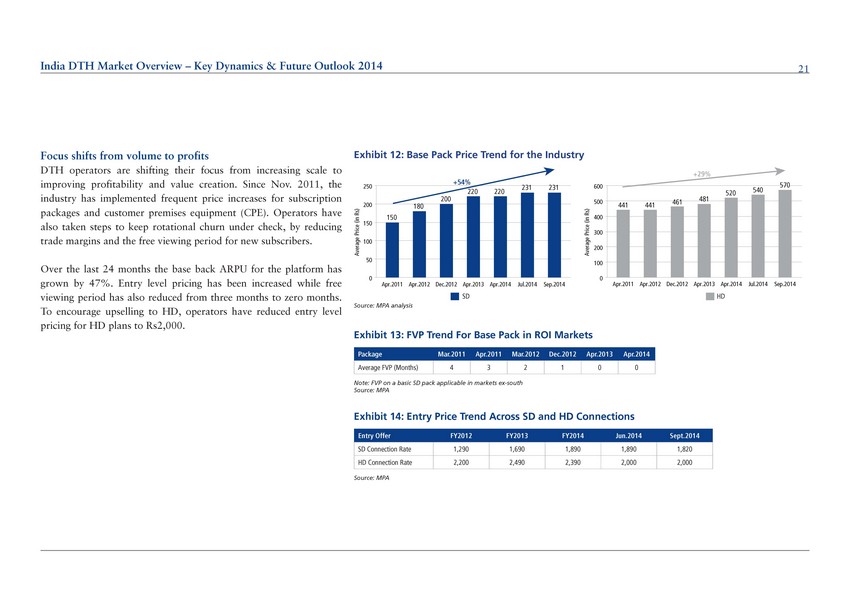

| · | Statements on page 139 of the Form F-4: Over the last 24 months, the base back ARPU for the platform has increased by 47.0%. Entry level pricing has been increased while the free viewing period has also been reduced from three months to zero months. Please see page 21 of the MPA Report. |

| · | Statements on page 140 of the Form F-4: DTH operators are shifting their focus from increasing scale to improving profitability and value creation. Since November 2011, the industry has implemented frequent price increases for subscription packages and customer premises equipment (‘‘CPE’’). Operators have also taken steps to keep rotational churn under check, by reducing trade margins and the free viewing period for new subscribers. Please see page 21 of the MPA Report. |

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 5

| · | Statements on page 140 of the Form F-4: In the future, gross subscriber additions will gain momentum as mandatory cable digitization is implemented. The quality of subscriber additions is expected to be superior, as the switch-off of analog signals will allow DTH to further develop within urban areas and target high-ARPU subscribers, while at the same time managing churn rates. The recent increase in entry prices will also help control industry churn levels. Please see page 22 of the MPA Report. |

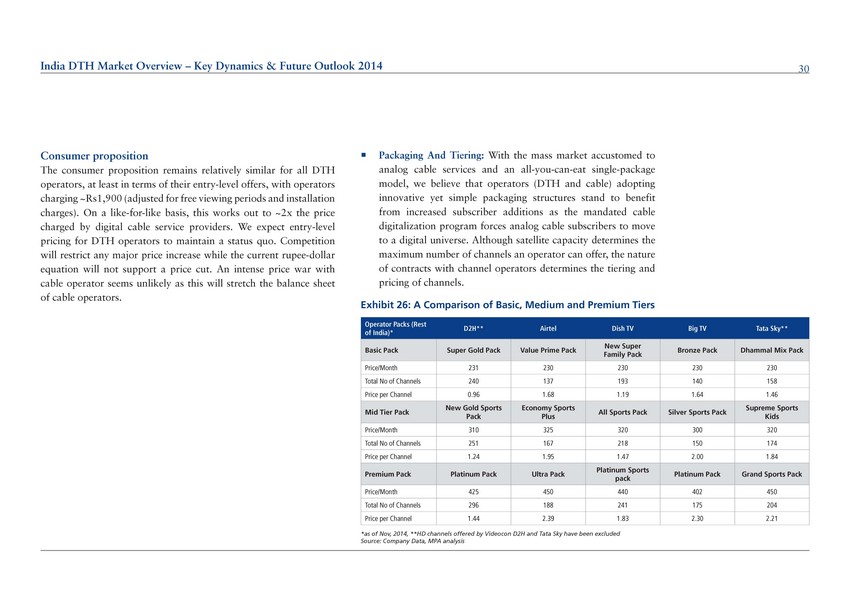

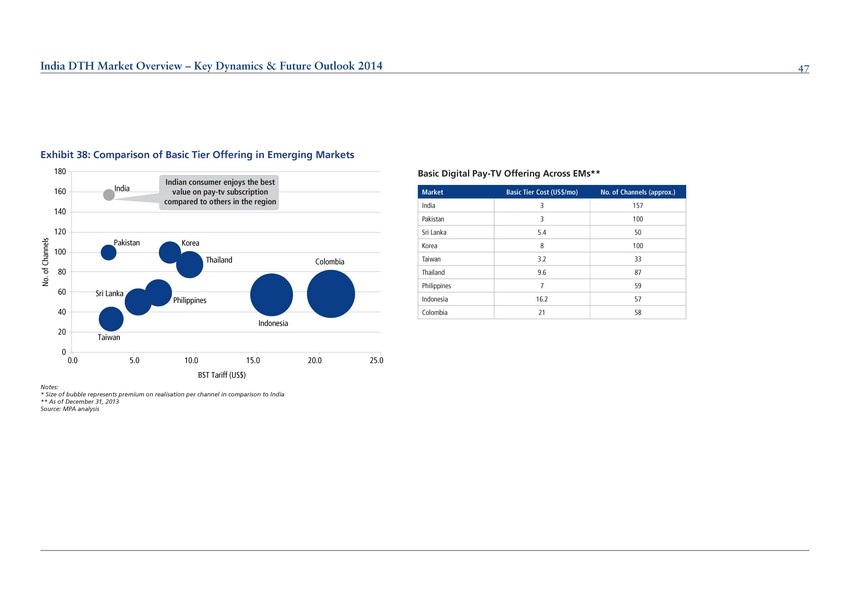

| · | Statements on page 141 of the Form F-4: The consumer proposition remains relatively similar for all DTH operators, at least in terms of their entry-level offers, with operators charging approximately Rs.1,900. This is approximately two times the price charged by digital cable service providers. Entry-level pricing for DTH operators is expected to maintain a status quo. Competition will restrict any major price increase while the current rupee-dollar equation will not support a price cut. An intense price war with cable operators seems unlikely as this will stretch the balance sheet of cable operators which have already been under pressure. Please see page 30 of the MPA Report. |

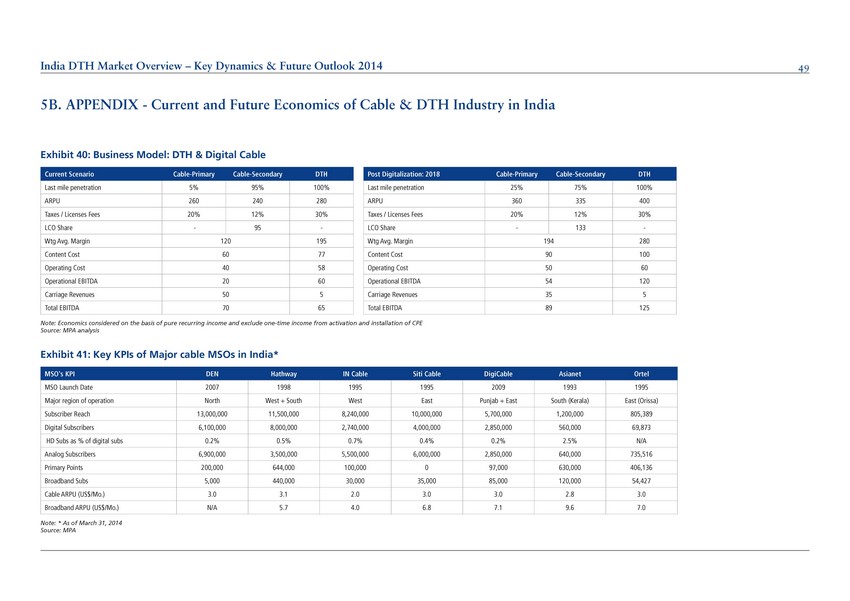

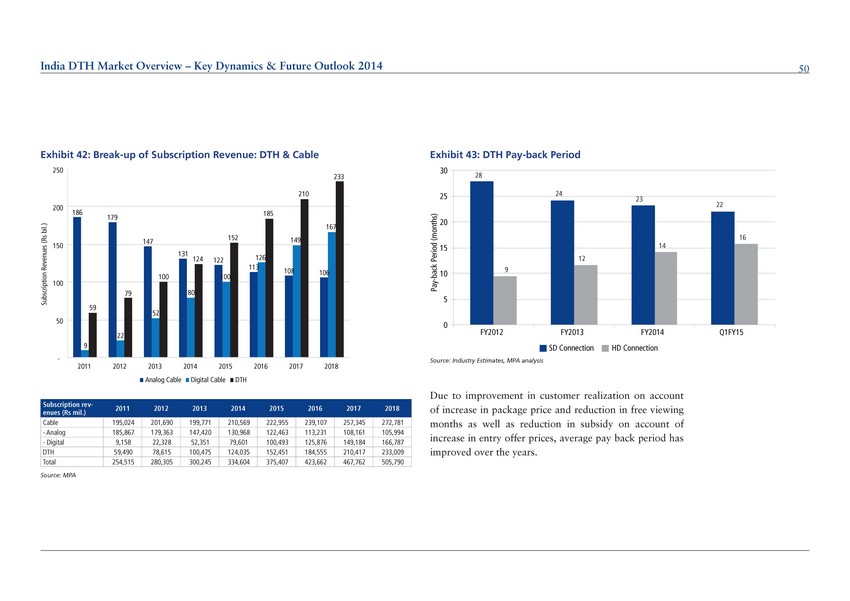

| · | Statements on page 141 of the Form F-4:Due to improvement in customer realization on account of increase in package price and reduction in free viewing months as well as reduction in subsidy on account of increase in entry offer prices, average pay-back period has improved over the years.Please see page 50 of the MPA Report. |

| · | Statements on page 144 of the Form F-4:Sports and general entertainment channels (‘‘GECs’’) act as HD catalysts: In India, following a run of major cricketing events in early 2011, the introduction of major Hindi GECs in HD has been critical in maintaining HD growth. Currently, 43 true HD (i.e. not up-converted) channels are available, and operators expect several new HD channel launches in the coming years. In the DTH space, Videocon d2h and Dish TV offer the most number of HD channels.Please see page 31 of the MPA Report. |

| · | Statement on page 144 of the Form F-4:Due to a lack of transponders in India, many operators are struggling to increase channel availability and provide new channels.Please see page 24 of the MPA Report. |

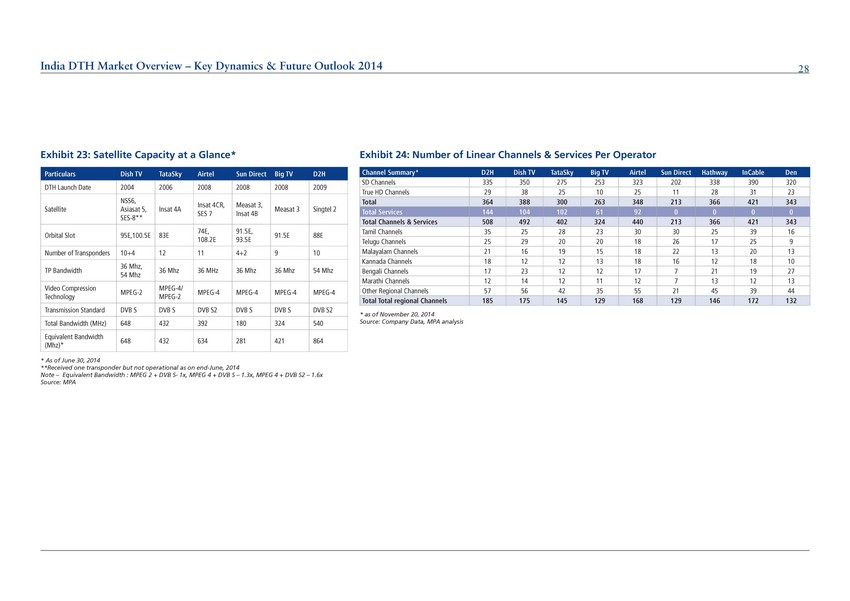

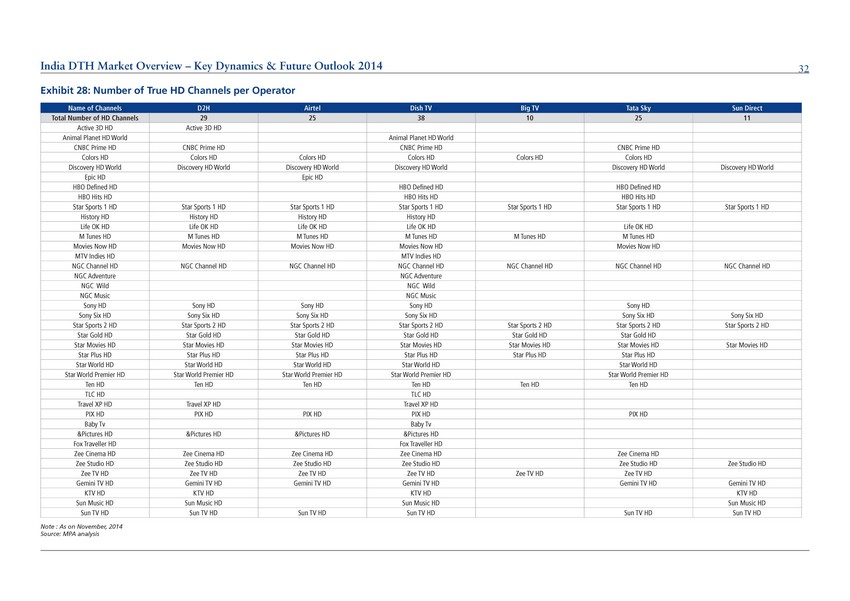

| · | Statement on page 144 of the Form F-4:Videocon d2h offers over 500 channels and services, the highest in the industry (including the highest number of regional channels), followed by Dish TV, which offers 492 channels and services.Please see exhibit 24 on page 28 of the MPA Report. |

| · | Statement on page 144 of the Form F-4:Having a clear road map for building satellite capacity is critical for DTH operators to ensure long term competitiveness. Restricted by the spectrum crunch and the falling reliabilityof INSAT satellites have resulted in instances where India’s DTH operators are migrating to foreign satellites. In 2010, Sun Direct shifted several channels to Measat after INSAT 4B, which hosted its channels, encountered a major technical problem. Likewise, in 2011, Airtel Digital had to transition subscribers from Insat 4CR to SES 7.Please see page 27 of the MPA Report. |

| · | Statement on page 144 of the Form F-4:Tata Sky, which until recently was behind in terms of channel offerings, is upgrading its subscribers from MPEG-2 to MPEG-4 STBs. This will enable the company to substantially expand its channel suite, especially in HD. However, it will cost Tata Sky Rs.9 billion to complete this exercise. Tata Sky has already added a number of SD and HD channels in the last few months.Please see page 27 of the MPA Report. |

| · | Statement on page 145 of the Form F-4:Dish TV has been the most efficient at managing satellite capacity, enabling it to carry the highestnumber of channels. Its 350 SD channels include 59 channels offered as pass through from DD Freedish, which will expand to 120 channels by CY 2014 as DD Freedish expands its capacity. The successful SES-8 satellite launch in December 2013 will enable Dish TV to further augment its capacity. Dish TV aims to completely shift to MPEG-4 compression at some point, since the STBs for its new subscribers support MPEG-4.Please see page 27 of the MPA Report. |

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 6

| · | Statement on page 145 of the Form F-4:Already supporting MPEG-4 compression and DVB-S2 transmission, Videocon d2h offers the highest number of regional channels, which is a strong driver of monthly subscriber additions. The improved efficiency of these compression standards has enabled Videocon d2h and Airtel Digital to offer more interactive services. Please see page 27 of the MPA Report. |

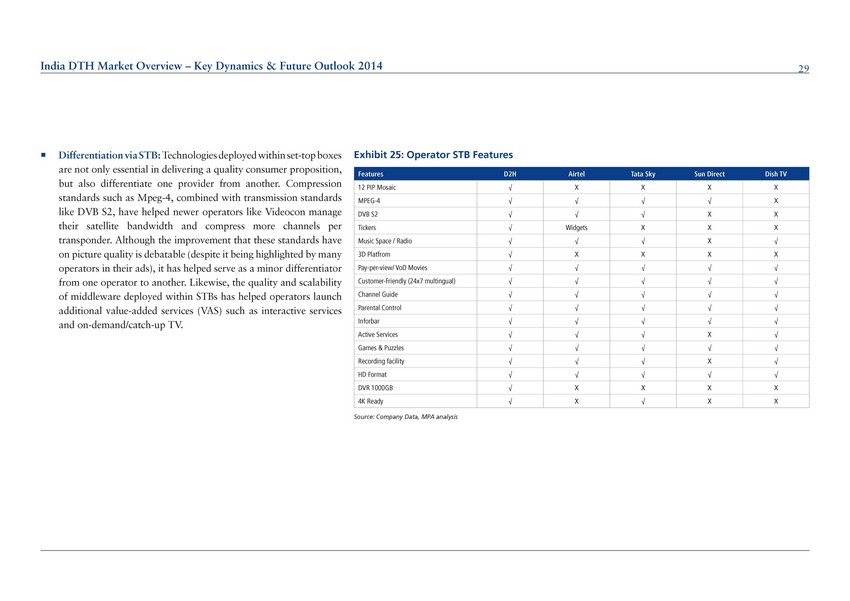

| · | Statement on page 145 of the Form F-4:Technologies deployed within set-top boxes are essential in delivering a quality consumer proposition and also differentiate one provider from another. Compression standards such as MPEG-4, combined with transmission standards like DVB S2, have helped newer operators like Videocon d2h manage their satellite bandwidth and compress more channels per transponder. Although the improvement that these standards have on picture quality is debatable (despite it being highlighted by many operators in their advertising), it has helped serve as a minor differentiator from one operator to another. Likewise, the quality and scalability of middleware deployed within STBs has helped operators launch additional value-added services (VAS) such as interactive services and on-demand and catch-up TV. Please see page 29 of the MPA Report. |

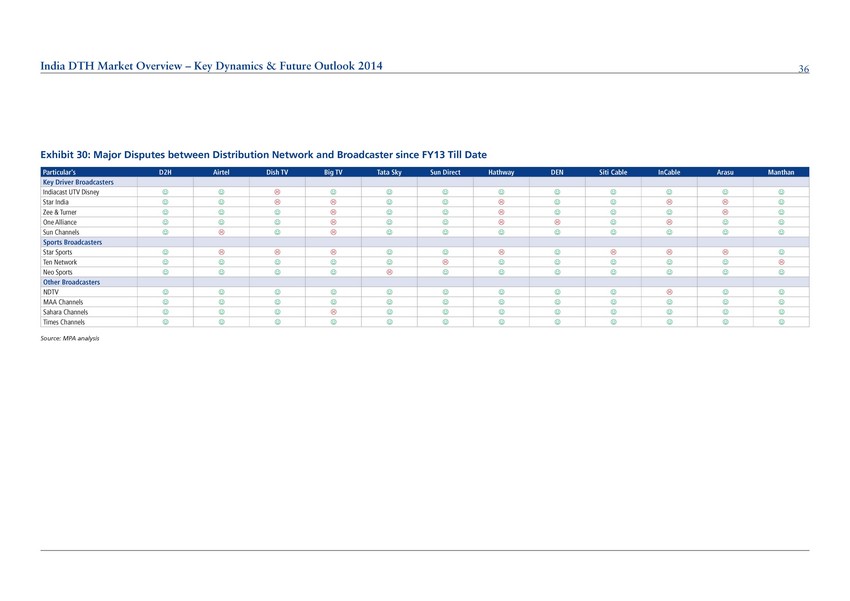

| · | Statement on page 146 of the Form F-4:To keep up with evolving technology, which has been rapidly changing consumers’ viewing habits, choice and delivery of content, collaboration between broadcasters and operators becomes highly critical in the overall pay-TV ecosystem. Operators which enjoy strong and cordial relationships with broadcasters are thus better placed for long term monetization of subscription revenues, both in terms of volume and value share. In India, the regulators have intervened previously to ensure that there is a balance between the operators and broadcasters. Please see page 35 of the MPA Report. |

| · | Statements on page 146 of the Form F-4:In February 2014, Telecom Regulatory Authority of India issued new regulations to significantly limit the role of channel aggregators. The new regulations prevent aggregators from: (1) publishing reference interconnect offers (‘‘RIO’’, which form the basis of wholesale bouquet/channel agreements), and (2) entering into agreements with distributors. These functions will only be assumed by broadcasters directly. Aggregators can continue to exist as authorized agents, but only in the name and on behalf of the broadcaster. The broadcaster must ensure that the aggregator does not alter the bouquet of channels stipulated in its RIO. Significantly, the aggregator cannot bundle channels and bouquets of multiple broadcasters. Please see page 35 of the MPA Report. |

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 7

| · | Statements on page 146 of the Form F-4:The one exception is that broadcasters belonging to the same promoter group can bundle their channels. This potentially benefits domestic incumbents such as Star and Zee. However, more significantly, the new guidelines allow for distribution platforms to negotiate rates with broadcasters which are mutually acceptable and closer to market reality. Please see page 35 of the MPA Report. |

| · | Statements on page 146 of the Form F-4: Over 2013 and 2014, the industry experienced several disputes between broadcasters and aggregators and platforms which forced several operators to carry individual channels on an à-la-carte basis at RIO rates. For cable, frequent black outs of channels may upset end-subscribers and the LCO who might decide to move its entire network to a competing MSO, leading to the swapping of STBs. With regard to DTH, which offers several channel packages, frequent switch offs might result in higher churn or on a sustained basis and may weaken the consumer proposition for a given tier, thereby having an adverse impact on its new subscriber additions. Procuring channels on RIO is an expensive proposition due to TRAI’s stipulated two-part rate increase, a 15.0% increase effective April 1, 2014 and a further 12.5% increase to take effect from January 1, 2015). Please see page 35 of the MPA Report. |

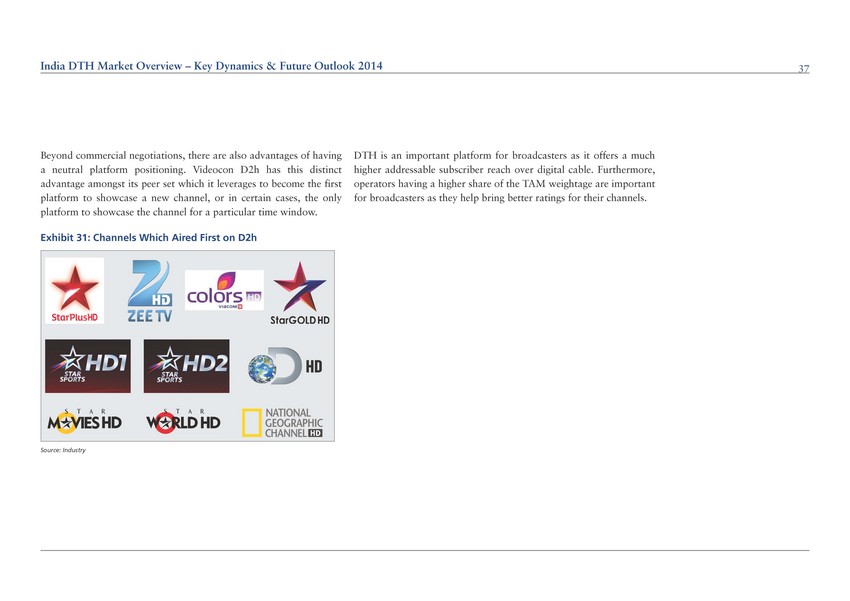

| · | Statements on page 146 of the Form F-4: Videocon d2h was the first platform for several HD channels in India. Some key channels which Videocon d2h first brought to consumers include: Star Plus HD, Zee TV HD, Colors HD, Star Gold HD, Star Sports HD-1, Star Sports HD-2, Star world HD, Star Movies HD, Discovery HD and National Geographic Channel HD. Please see page 37 of the MPA Report. |

| 2. | Please update your financial statements to include interim financial statements for at least the first six months of your fiscal year. |

Response: The Company has revised the Form F-4 to include the interim financial statements for the six-month period ended September 30, 2014 and 2013.

Letter to Silver Eagle Acquisition Corp. Stockholders and Public Warrantholders

| 3. | We note your disclosure that Videocon d2h is the fastest “direct-to-home service provider.” Please specify that Videocon d2h is a pay TV provider. |

Response:The Company confirms that it is a pay TV provider operating in India. The Company has included that clarification on the Form F-4 on page 26.

Industry and Market Data, page v

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 8

| 4. | You state certain industry and market data contained in this prospectus has not been “independently verified.” Under the federal securities laws, you are responsible for all information contained within your registration statement and you should not include language that suggests otherwise. Please delete this statement. |

Response:The Company has deleted the relevant statement in the Form F-4 on page v.

Questions and Answers…, page 1

| 5. | Please add a question and answer on whether Silver Eagle obtained a fairness opinion in connection with the Contribution. |

Response:The Company has added a question-and-answer on page 5 of the Form F-4 addressing whether Silver Eagle has obtained a fairness opinion.

Q: Why is Silver Eagle holding a special meeting of public warrantholders, page 2

| 6. | Please explain the treatment of the warrants in the transaction if the shareholders do not approve the exchange. |

Response:The Company has revised the Form F-4 on page 3 to disclose that if the Warrant Amendment is not approved but the Business Combination Proposal and the Plan of Dissolution Proposal are both approved then all unexercised warrants will remain outstanding and Silver Eagle will dissolve and distribute any remaining assets it has.

Q: What equity stake will current Silver Eagle stockholders hold in Videocon d2h after the closing, page 3

| 7. | Please disclose the ADS price targets for the up to 3.88% of earn-out shares that may be issued to the current Videocon d2h shareholders after closing. |

Response:The Company has revised the Form F-4 on pages 3 and 4 to include the ADS price targets for the up to 11.68 million earn-out shares that may be issued to the current Videocon d2h shareholders after closing. The Company has also removed references throughout the Form F-4 to the earn-out shares constituting 3.88% of the equity share capital of Videocon d2h.

Q: How will founder shares be treated in the Transaction, page 4

| 8. | For illustrative purposes, please provide tabular disclosure regarding the number of shares to be issued to the founders based on different contribution levels. In addition, please provide tabular disclosure of the potential forfeiture of shares based on the post-closing ADS prices. |

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 9

Response: The Company has revised the Form F-4 on page 5 to provide tabular disclosure regarding the number of shares to be issued to the founders based on different contribution levels.

Q: Why is Silver Eagle proposing the Plan of Dissolution, page 4

| 9. | Disclose that, prior to the effectiveness of the Form F-4, Videocon d2h, together with the depositary, will file a Form F-6 to register the ADSs with the Commission. Further, disclose that the Form F-6 will include a copy of the deposit agreement that sets forth the rights of ADS holders and explains certain other matters, including the procedures to be followed for the distribution of the ADSs. |

Response:The Company has revised the Form F-4 on page 6 to disclose that, prior to the effectiveness of the Form F-4, the Company and the depositary will file a Form F-6 to register the ADSs and that the Form F-6 will include as an exhibit a copy of the deposit agreement that sets forth the rights of the ADS holders. The deposit agreement will not address the distribution; these procedures are set out on page 6. Silver Eagle and the Company anticipate that Silver Eagle’s transfer agent will receive the ADSs and distribute them to Sliver Eagle’s shareholders in the same manner it would a dividend payment.

How will Silver Eagle’s Sponsor, directors and officers vote, page 6

| 10. | We note your disclosure that 16,250,001 of the 32,500,000 outstanding public warrants must approve the Warrant Amendment Proposal. However, elsewhere you disclose that approval by 65% of the outstanding warrants is required. Please reconcile. |

Response: The Company has revised the Form F-4 on pages 7, 55 and 89 to indicate that the favorable vote of 21,125,000 public warrants is required for the approval of the Warrant Amendment Proposal.

What happens to the funds held in the trust account…, page 8

| 11. | To the extent known, please quantify the fees listed in this answer. |

Response:The Company has revised the Form F-4 on page 9 to quantify the estimated fees listed in this answer.

When is the transaction expected to be completed, page 9

| 12. | Please disclose any regulatory approvals that you must obtain prior to closing. |

Response: The Company has revised the Form F-4 on page 10 to disclose the regulatory approvals required to be obtained prior to closing under applicable Indian law.

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 10

What will happen if I abstain from voting or fail to vote at the applicable special meeting, page 10

| 13. | In your answer to this question, you state “[f]or purposes of approval, an abstention or failure to vote will have no effect on the Business Combination Proposal.” Yet on page 16, you state “a stockholder’s failure to vote by proxy or to vote in person at the special meeting of stockholders, an abstention from voting or a broker non-vote will have the same effect as a vote “AGAINST” the Business Combination Proposal…” Revise or advise accordingly. |

Response: The Company has revised the Form F-4 on pages 10-11 to indicate that a stockholder’s failure to vote by proxy or to vote in person at the special meeting of stockholders, an abstention from voting or a broker non-vote will have the same effect as a vote “AGAINST” the Business Combination Proposal.

Summary of the Proxy Statement/Prospectus, page 13

| 14. | Please disclose the extent and amount of Videocon d2h’s indebtedness and the amount of such debt that will be repaid out of the proceeds of this offering. |

Response: The Company has revised the Form F-4 on page 14 to include this information.

Reasons for the Transaction, page 15

| 15. | Please revise your disclosure to provide the basis for the statement “Silver Eagle’s management team has extensive experience operating media businesses and leading transactions in high growth international markets, including India.” |

Response:The Company has revised the disclosure on pages 16 and 17 of the F-4 to provide the basis for the referenced statement.

Risk Factors, page 18

| 16. | Please expand your disclosure to address the “seasonal factors” affecting your business, including the relative rise in revenues and/or subscribers during cricket season, as your recognize on page 141 that becoming the Title Sponsor of the Kings XI Punjab cricket team and sports HD channels favorable influence the amount of subscribers. |

Response: The Company has revised the Form F-4 on page 31 to include this information.

Videocon d2h’s indebtedness could adversely affect its financial health…, page 18

| 17. | This risk factor appears to address several different risks, including debt burden, potential breaches and restrictive covenants. Please separate these risks into separate risk factors. |

Response: The Company has revised the Form F-4 on page 19 to separate the risk factors.

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 11

| 18. | Please clarify whether you are currently in default under any of your outstanding indebtedness and, if so, disclose the nature of the breach. |

Response: The Company has revised the Form F-4 on pages 19, 20 to include disclosure relating to the terms of its financing arrangements that it is currently not in compliance with. As stated in the disclosure, it is clarified that the lenders have neither enforced any security nor have accelerated repayment of the loans for any such non-compliance.

| 19. | Please explain your affiliation with Videocon Industries. |

Response: Videocon d2h is controlled by Mr. Saurabh Pradipkumar Dhoot, while Videocon Industries Limited (the flagship entity of the Videocon Group) is controlled by other members of the Dhoot family. Videocon d2h is affiliated with the Videocon Group, including on account of (i) use of the brand name “Videocon”, which has been licensed to it by an entity belonging to a Videocon Group; (ii) a number of its secured loans being either guaranteed or supported through undertakings by Videocon Industries Limited; and (iii) having received unsecured loans from Videocon Industries Limited from time to time. However, Videocon d2h and Videocon Industries Limited are each controlled and managed by different member(s) of the Dhoot family, with no overlapping management control or rights.

| 20. | Please clarify whether your must seek your lender’s consent for this transaction. |

Response: In accordance with the terms of its financing arrangements, Videocon d2h is required to obtain prior consents from certain lenders for any issuance of equity shares, including pursuant to the Transaction. Videocon d2h is presently in the process of obtaining such consents and is expected to receive such consents prior to closing of the Transaction. The requirement of Videocon d2h’s lenders’ consent is disclosed in the Form F-4 on page 20.

Videocon d2h’s failure to adhere to the terms and conditions contained in the DTH License Agreement…, page 19

| 21. | Please clarify whether this transaction requires approval from the MIB. |

Response:As disclosed on pages 20 and 21 of the Form F-4, in order to consummate the Transaction, Videocon d2h will be required to obtain prior approvals from the MIB for (i) issuance of equity shares underlying the Videocon d2h ADSs; and (ii) security clearances in respect of Mr. Jeff Sagansky and Mr. Harry E. Sloan, in respect of their appointment on the Company’s board of directors, which is a condition to closing of the Transaction.

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 12

Videocon d2h’s leased satellite ST-2 is subject to operational, lease and environmental risks…, page 20

| 22. | Please provide us with the status of your negotiations to extend your lease with Department of Space, which expires on February 28, 2015. |

Response:As disclosed on page 22 of the Form F-4, the Department of Space, Government of India tenders transponder capacity by entering into lease agreements with satellite owners (SingTel, in this case) and the Department of Space enters into back-to-back lease agreements with persons seeking to lease such space segment capacity for periods of up to three years. The Company has made an application to the Department of Space seeking renewal of the Ku-Band Lease Agreement which expires on February 28, 2015.

In addition, the Company has had a discussion with Antrix Corporation, the commercial division of the Department of Space, for renewal of the agreement. The Company have been informed that Antrix has send a request for proposal to SingTel for the purpose of renewing the Company's lease with the Department of Space and a response is currently awaited from SingTel. Once SingTel responds the Company will enter into a three year lease with Antrix.

Videocon d2h’s business is regulated and failure to obtain required regulatory approvals…, page 24

| 23. | We note that each of your directors must obtain security clearance from MIB. Please disclose whether Messrs. Sloan and Sagansky have obtained such clearance. |

Response:The Company is presently in the process of obtaining security clearances from the MIB for Messrs. Sloan and Sagansky. In accordance with the terms of the Contribution Agreement, such clearances will be obtained prior to closing of the Transaction. The Company has revised the Form F-4 on page 26 to include disclosure regarding the requirement that Messrs. Sloan and Sagansky obtain MIB clearance.

As a foreign private issuer, Videocon d2h is permitted, and Videocon d2h will, follow certain home country corporate governance practices in lieu of certain NASDAQ requirements applicable to U.S. issuers..., page 32

| 24. | Clarify how the Nasdaq Listing Rules applicable to U.S. issuers (e.g., Nasdaq Listing Rule 5605(b) and (c)) regarding the independence of members of the board of directors and of the Nomination and Remuneration Committee differ from the comparable Indian Companies Act requirements. |

Response:The Company has revised the Form F-4 on page 34 to clarify how theNasdaq Listing Rules applicable to U.S. issuers regarding the independence of members of the board of directors and of the Nomination and Remuneration Committee differ from the comparable Indian Companies Act requirements.

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 13

Videocon d2h may be classified as a passive foreign investment company. . ., page 36

| 25. | In this risk factor, disclose that Videocon d2h does not intend to provide the information that would enable investors to take a qualified electing fund (“QEF”) election that could mitigate the adverse U.S. federal income tax consequences should it be classified as a PFIC. |

Response:The Company has revised the Form F-4 on pages 38-39 to indicate that Videocon d2h does not intend to provide the information that would enable investors to take a QEF election that could mitigate the adverse U.S. federal income tax consequences should it be classified as a PFIC.

NASDAQ recently delisted Silver Eagle’s securities…, page 40

| 26. | Please specify why Silver Eagle’s securities were delisted. |

Response:The Company has revised the Form F-4 on page 42 to disclose why Silver Eagle's securities were delisted.

Videocon d2h has not previously operated as a foreign private issuer. . ., page 44

| 27. | Briefly describe the exemptions from the audit committee member independence requirements applicable to foreign private issuers that were added under the Sarbanes-Oxley Act (see Exchange Act Rule 10A-3(b)(1)(iv)(C), (D), and (E)). Then clarify whether any of Videocon d2h’s audit committee members are, or are expected to be, exempt from the independence requirements pursuant to those provisions. |

Response: The Company has revised the Form F-4 on page 46 to include additional disclosure about the exemptions from the audit committee independence standards available for foreign private issuers.

Background of the Transaction, page 71

| 28. | Please provide us with any analyses, reports, presentation, or similar materials, including projections and board books, provided to or prepared by Deutsche Bank in connection with the transaction with Videocon d2h. We may have further comment upon receipt of these materials. |

Response: The Company respectfully advises the Staff that Deutsche Bank did not prepare any analyses, reports, presentation or similar materials, including projections and board books in connection with the Transaction, other than (i) presentation of publicly available information and (ii) presentation of information and data formatted by Deutsche Bank personnel specifically as directed by the Company, with all content solely determined by and sole responsibility of the Company.

| 29. | Please note that the disclosure of financial forecasts prepared by management may be required if the forecasts were provided to third parties, including a third party’s financial advisor. Accordingly, please disclose all material projections that Videocon d2h provided to Silver Eagle and/or its financial advisor or advise us why they are not material. Also, disclose the bases for and the nature of the material assumptions underlying the projections. |

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 14

Response: The Company has revised page 77 to expand the discussion of the specific projections for fiscal 2015 that Videocon d2h provided to Silver Eagle and its financial advisor and Silver Eagle’s consideration thereof. Specifically, Videocon d2h provided Silver Eagle and its advisors with its budget for F2015 gross revenues, EBITDA (a non-GAAP financial metric), gross and net subscribers and ARPU at various times during 4Q 2014, which forecasts were subsequently confirmed by Videocon d2h to Silver Eagle and its advisors on February 3, 2015, and again will be subject to bring down due diligence around the time of the effective date of the Form F-4.

| 30. | Please revise the disclosure on pages 72 – 73 to clarify that Mr. Dhoot is also the largest shareholder of Videocon d2h. |

Response: The Company has revised the Form F-4 on pages 75-76 to disclose that Mr. Dhoot is the Company’s largest shareholder.

| 31. | Please expand your discussion of the parties’ negotiation of key aspects of the proposed deal, including, but not limited to: |

| · | The determination of the final structure of the proposed transactions; |

| · | The determination of the ratios resulting in the post-closing equity ownership of Silver Eagle; |

| · | The earn-out that will be paid to current Videocon d2h shareholders; and |

| · | The amount to be paid to Silver Eagle’s directors and officers in connection with the transaction. |

Response: The Company has revised pages 74-78 to expand the discussion of the parties’ negotiation of key aspects of the Transaction, including to discuss the final structure of the proposed Transaction, the determination of the ratios resulting in the post-closing equity ownership of Silver Eagle, the earnout that will be paid to current Videocon d2h shareholders, and the amount to be paid to Silver Eagle directors and officers in connection with the Transaction.

Critical Accounting Policies, page 162

| 32. | Your discussion of critical accounting policies on page 162 substantially duplicates your footnote disclosure. Please revise this section to provide greater insight into the quality and variability of your estimates. For example, you should describe how these estimates and related assumptions were derived, how accurate those estimates / assumptions have been in the past, and whether the estimates / assumptions are reasonably likely to change in the future. You should provide quantitative as well as qualitative information when information is reasonably available. Tell us what consideration you gave to providing these disclosures for each of the accounting policies described. |

Response:The Company has revised the Form F-4 on page 170 to provide the requested information. In addition,the Company makes estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities. The Company bases its estimates on historical experience and various assumptions that it believes to be reasonable under the circumstances, the results of which form its basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources.

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 15

Revenue recognition, page 162

| 33. | Please expand your revenue recognition policy as it relates to subscription revenue from DTH services to specify how you are able to recognize revenue "on an accrual basis on rendering of the services." Discuss if estimates are used when recognizing revenue. If estimates are used, disclose the accuracy of those estimates. Also, disclose if subscribers enter contracts in order to receive these services. Disclose the average contract term for these contracts. |

Response:The Company has revised the Form F-4 on page 171 to provide the requested information.

Arrangements with multiple deliverables, page 162

| 34. | You state that management makes the determination of the amount assigned to activation revenue, installation revenue, and lease rental of set-top box and out-door unit and its accessories. In this regard, please disclose how management determines the value of each item in a multiple element arrangement. |

Response:The Company has revised the Form F-4 on page 171 to provide the requested information.

Income Tax Expense, page 168

| 35. | We note your statement that, “The carrying amount of deferred tax assets and liabilities are reviewed at each balance sheet date and recognized and carried forward only to the extent that there is areasonable certaintythat the asset will be realized in future.” Please tell us how your statement reconciles to guidance in paragraph 56 of IAS 12. |

Response: Paragraph 56 of IAS 12 states that amount of deferred tax assets carried forward must be reviewed at the end of each reporting period and the amount carried forward must be reduced to the extent that it is no longer probable that sufficient taxable profits are available to allow the benefit of part or all of that deferred tax asset to be utilized.

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 16

Under the provisions of Indian Tax laws, business losses are allowed to be carried forward for a period of 8 years and unabsorbed depreciation can be carried forwarded for an infinite period.

The Company has had an accumulated loss and unabsorbed depreciation amounting to Rs. 10,090.04 million and 11,217.34 million as of March 31, 2014, respectively. The Company's management believes with reasonable certainty that the profits in the next 5-6 years will be sufficient to allow the benefit of the deferred tax assets carried forward for the accumulated losses and unabsorbed depreciation as of March 31, 2014.

As an illustration: If during fiscal year 2010 the Company incurs a loss under income tax of Rs. 200 including Rs. 100 of unabsorbed depreciation, the Company would be allowed to set-off unabsorbed loss of Rs. 100 until fiscal year 2017-18, whenever profit arises to the Company for more than or equal to Rs. 100. Similarly, unabsorbed depreciation can be carried forward for an infinite period.

Certain Key Measures of Financial Performance, page 168

| 36. | We note that your metric called "subscription revenue and activation revenue" “includes margins provided to distributors for distribution of subscriptions and consumer premises equipment.” Please explain this statement and why these margins are included in revenue. Referring to your basis in accounting literature, tell us how you account for these margins. Also, please reconcile this metric to subscription revenue shown on page 165. |

Response: The term ‘subscription revenue and activation revenue’ used on page 178 of the Form F-4 is specific for calculation of Average Revenue Per User (ARPU). ARPU is a common terminology used in the pay TV industry worldwide to measure the operational performance of company. Here the subscription revenue and activation revenue are considered on a gross basis without netting off the margins or discounts provided to the distributors according to the industry practice.

In preparation of the financial statements under IFRS, the subscription and activation revenue are netted with such margins or discounts provided to the distributor network, which includes our distributors, direct dealers and sub-dealers. We draw your attention to our accounting policy relating to revenue recognition particularly for subscription revenue and activation revenue, stating that these metrics are net of discounts provided to the distributor network.

The "Subscription revenue" metric presented on pages 178-179 of the Form F-4 is an extract from the financial statements and is presented net of margins and discounts.

Fiscal year 2014 Compared to Fiscal year 2013, page 169

| 37. | We note your subscription revenue increased significantly between the 2014 fiscal year and the 2013 fiscal year, primary as a result of an increase in the total number of gross subscribers and an increase in ARPU. As such, please expand your analysis to explain the underlying reason for the increase in subscribers and ARPU. Also, quantify what portion of the increase was due to volume versus price increases. |

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 17

Response:The Company has revised the Form F-4 on page 180 to provide the requested information.

| 38. | We note your statement that, “other income increased by 379.44% to Rs.17.26 million for the fiscal year 2014 from Rs.3.60 million for the fiscal year 2013, as a result of an increase in liabilities/provisions no longer written back which represented Rs.15.41 million for the fiscal year 2014 as compared to Rs.2.52 million for the fiscal year 2013 as a result of greater recoveries of advances to subscribers whose subscriptions were expiring through subsequent recharges.” Please explain these liabilities / provisions and how your accounting for them. Refer to your basis in accounting literature. |

Response:The Company has revised the Form F-4 on page 181 to provide the requested information.

Administrative and Other Expenses, page 170

| 39. | We note that you transitioned from a service franchisee model to providing customer service through direct service centers. In this regard, please explain to us both models and your accounting for each model. Tell us how you accounted for the transition to the new model. Also, in addition to disclosing the effect on rent expense, disclose other material effects to your financial statements as a result of this transition. |

Response: Under the service franchisee model, third party contractors provide customer support services to the Company on a fixed fee basis as stipulated in an agreement. The Company had entered into such an agreement with third party contractors for installation work and service and repairs. The Company pays these third party contractor fees at an agreed contractual rate. The payments made to the third party contractors are shown under "Operating Expenses" as “Installation and service expenses” (See Note 9 of the financial statement).

Under the direct service center model, the Company operates its own customer service and support centers and contracts with third parties for the provision of persons to staff these service centers. The Company incurs expenses including rent, electricity expenses, communication expenses and certain administrative expenses, in addition to third party contract employee fees. These expenses are shown under "Administrative and other expenses" as “Rent”, “Power and Fuel”, “Communication Expenses” and “Office and General Expenses” (See Note 11 of the financial statements). The third party contract employee are accounted as “Installation and Service Charges” as shown under schedule No. 9 of “Operating Expenses” of the financial statement.

Currently the Company uses both models for its operations and intends to open more direct service centers to ensure higher quality and timely provision of support services to its customers.

The accounting would be treated as per the paragraphs above. There were no transition expenses other than as noted above.

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 18

The Company stated on page 181 of the Form F-4 that its rent cost, which forms part of the Administrative and Other Expenses, increased due to the transition from a service franchisee model to a direct service center model, this was offset by a decrease in installation and service expenses resulting in no major impact with respect to the transition. The increase in the other expenses were not material.

Financial Condition, Liquidity and Sources of Capital, page 171

| 40. | Please provide prominent disclosure, in the opening paragraphs of your Financial Conditions, Liquidity and Sources of Capital section of your MD&A, regarding your auditors going concern opinion, your debt defaults, and your ability to meet short term and long terms liquidity needs. This discussion should be detailed, specifying why your debt is in default and how you plan to improve your liquidity outlook in the future. |

Response:The Company has revised the Form F-4 on page 182 to provide the requested information.

| 41. | Your discussion of net cash provided by operating activities does not appear to contribute substantively to an understanding of your historical cash flows. When preparing the discussion and analysis of operating cash flows, you should address material changes in the underlying drivers that affect these cash flows. These disclosures should include a discussion of the underlying reasons for changes in working capital accounts that affect operating cash flows. |

Response:The Company has revised the Form F-4 on page 182 to provide the requested information.

Contractual Obligations, page 172

| 42. | You state that the contractual obligations "table does not include payments required to be made in future under the terms of Videocon d2h’s Ku-Band Lease Agreement, contracts for provision of programming content or lease rental amounts. The table below also does not include payments to be made to content providers as these will depend on the number of subscribers from time to time." We also note that interest appears to not be included in your contractual obligations table. Since these payments are material to your cash flows, it appears you should include the scheduled and/or expected payments in the table. Please revise accordingly and if you continue to omit, explain to us how they are variable and therefore the future obligation is unknown to management. |

Response:The Company has revised the contractual obligations table on page 184 to include the requested information.

Indebtedness, page 173

| 43. | You state that you regularly experience delays in payment under your indebtedness. Please disclose why you experience these delays in payment and the specific amount of debt payment considered late as of March 31, 2004 and the date of your latest amendment. |

Response:The Company has revised the Form F-4 on pages 184-185 to provide the requested information.

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 19

| 44. | You disclose on page 173 that your debt covenants require you to maintain certain security margins and financial ratios. Given the going concern audit opinion and delays in debt payments, please disclose the terms of your debt covenants, how close you have come to meeting or failing these covenants in the past, and how you plan to meet your debt covenants in the future. |

Response:The Company has revised the Form F-4 on page 186 to provide the requested information.

Compensation of Directors and Executive Officers, page 195

| 45. | Supplementally advise, with a view to disclosure, whether Videocon d2h is required to disclose, or otherwise has disclosed, the annual compensation of its executive officers and directors on an individual basis in India for its most recently completed fiscal year.See Form 20-F Item 6.B., as referenced in Form F-4 Item 18(a)(7)(ii). |

Response: The Indian Companies Act and accounting standards issued by the Institute of Chartered Accountants of India (“ICAI”) (in accordance with which the financial statements of an Indian company are required to be prepared) do not require disclosure of the annual compensation of its executive officers and directors on an individual basis, except in the following cases:

| (i) | Compensation paid to each such employee whose compensation exceeds certain threshold limits is required to be disclosed in a report of the board of directors of the company (“Board Report”), which is annexed to such company’s annual financial statements placed before its shareholders for approval; and |

| (ii) | Transactions (including payment of compensation) with key management personnel or directors (as identified in accordance with the provisions of accounting standard 18 issued by the ICAI, relating to related party disclosures), including details of compensation paid to each such key management personnel. |

In accordance with these requirements, the Company has, in the Board Report disclosed remuneration paid in fiscal 2014 to Mr. Anil Khera (Chief Executive Officer), Mr. Rohit Jain (Deputy Chief Executive Officer) and Mr. Himanshu Patil (Chief Operating Officer), whose remuneration exceeded the prescribed thresholds. Further, the statement of related party transactions forming part of the Company’s financial statements for fiscal 2014 included disclosure of compensation paid during the year to Mr. Anil Khera (identified as the only key management personnel in terms of accounting standard 18). None of the Company’s directors were paid any compensation in fiscal 2014 (except sitting fees for attending board meetings), therefore, no disclosure was made in this respect.

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 20

Notwithstanding the above, a company proposing an initial public offering of its equity shares in order to list on a recognized stock exchange in India, is required to comply with certain disclosure requirements prescribed under the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009, as amended (“SEBI ICDR Regulations”) and file a draft offer document with SEBI, which is made available in the public domain. One such disclosure requirement requires the issuer company to disclose, on an individual basis, compensation or other benefits paid to its directors and ‘key managerial personnel’ (as defined under the SEBI ICDR Regulations, and which definition differs from that of ‘key management personnel’ as prescribed under accounting standard 18 issued by the ICAI) in the last completed financial year.

Since the Company was proposing to undertake an initial public offering in India, pursuant to which it filed a draft offer document dated September 29, 2014 with SEBI, such offer document disclosed the compensation paid to each of its directors (including sitting fees) and ‘key managerial personnel’ (identified in terms of the definition prescribed under the SEBI ICDR Regulations) in fiscal 2014. Such ‘key managerial personnel included Mr. Anil Khera, Mr. Rohit Jain, Mr. Himanshu Patil, Mr. Avanti Kanthaliya, Mr. Siddharth Kabra and Ms. Amruta Karkare.

However, such disclosure of compensation paid to each of its directors and ‘key managerial personnel’, on an individual basis, was made by the Company in its draft offer document filed with SEBI to comply with disclosure requirements that are applicable only in connection with a proposed securities offering in India and are not otherwise applicable to companies in general (except to the extent stated above under points (i) and (ii)).

Beneficial Ownership of Securities, page 234

| 46. | Provide the number of Videocon d2h’s U.S. record holders and the percentage of its equity shares held by them.See Form 20-F Item 7.A, as referenced in the instruction to Item 18(a)(5) of Form F-4. |

Response: The Company has revised the Form F-4 on page 246 to indicate that as of the record date for the special meeting of stockholders of Silver Eagle, Videocon d2h did not have any U.S. record holders of its equity shares.

Where You Can Find More Information, page 247

| 47. | Disclose, if true, that as a foreign private issuer, Videocon d2h will file its Exchange Act annual report on Form 20-F with the Commission by a date no later than 120 days following its fiscal year end. |

Response:The Company has revised the Form F-4 on page 259 to indicate that it will file its Exchange Act annual report on Form 20-F with the Commission by a date no later than 120 days following its fiscal year end.

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 21

Independent Auditor’s Report, page F-2

| 48. | We note that your auditor's report states that the audit was conducted "in accordance with auditing standards generally accepted in the United States of America." If true, please ask your auditor to revise their report to state that the audit was conducted in accordance with the standards of the Public Company Accounting Oversight Board (United States). Please refer to Auditing Standard No. |

Response: The auditor’s report has reflected the change to state that the audit was conducted in accordance with the standards of Public Company Accounting Oversight Board (United States) on page F-2 of the Form F-4.

Videocon d2h Limited — Financial Statements

Income Statement, page F-4

| 49. | Please tell us why you believe it is appropriate to present EBITDA on the face of your Income Statement. Refer to your basis in accounting literature. |

Response:IAS 1 states: “because the effects of an entity’s various activities, transactions and other events differ in frequency, potential for gain or loss and predictability, disclosing the components of financial performance assists users in understanding the financial performance achieved and in making projections of future financial performance” (IAS 1 para 86). As with the statement of financial position, additional line items, headings and sub-totals should be shown on the face of the statement of comprehensive income when such presentation is relevant to understanding the entity’s financial performance (IAS 1 para 85). Relevance is one of the qualitative characteristics of useful financial information in the IASB Framework which states: “Relevant financial information is capable of making a difference in the decisions made by users. Information may be capable of making a difference in a decision even if some users choose not to take advantage of it or are already aware of it from other sources” (Framework para QC6).

Considering, the above paragraph of IAS 1, which requires voluntary disclosure of information or line items which could be relevant in analysing the financial statements and position in more effective manner, the Company has presented EBITDA on face of the Income Statement, as we believe that EBITDA helps identify underlying trends in our business that could otherwise be distorted by the effect of the expenses that we exclude in EBITDA, and that EBITDA enhance the overall understanding of our past performance and future prospects and allow for greater visibility with respect to key metrics used by our management in its financial and operational decision-making.

In addition, the EBITDA presentation would also be helpful for investor considering the nature of this industry.

Notes to the Financial Statements for the year ended March 31, 2014, page F-8

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 22

| 50. | Please tell us how you considered the fair value disclosure requirements in paragraphs 91-99 of IFRS 13 and/or revise accordingly. |

Response:Paragraph 91 of IFRS 13 states that:

“An entity shall disclose information that helps users of its financial statements assess both of the following:

| a. | For assets and liabilities that are measured at fair value on a recurring or non-recurring basis in the statement of financial positions after initial recognition, the valuation techniques and inputs used to develop those measurement. |

| b. | For recurring fair value measurements using significant unobservable inputs (Level 3), the effect of the measurements on profit or loss or other comprehensive income for the period” |

In accordance with the above, the Company based its fair value disclosure for its assets and liabilities on the following manner;

| 1. | Currently, the Company does not have any investment and as such fair value disclosure on investments is not applicable; |

| 2. | the Company’s long term borrowings and liabilities are stated at amortized cost; and |

| 3. | the Company’s property, plant and equipment are accounted for on the cost basis. |

4. Significant accounting policies, page F-9

| 51. | Please disclose how you account for content and programming costs. If significant estimates are used in your method of accounting for programming costs and / or its impairment, please disclose those estimates and assumptions in your critical accounting estimates. |

Response:The content and programming costs are based on actual invoices the Company receives from content providers. The invoices are based on either fixed fees or based upon the average number of subscribers during the month. Since the broadcasters issue invoices for content and programming fees on a monthly actual basis no significant estimations or assumptions are used in accounting for content and programming costs.

Accordingly, the Company does not believe it is appropriate to include any additional disclosures in the financial statements.

4.3 Impairment of assets Property, plant and equipment and intangible assets, page F-11

| 52. | You state that, “If the recoverable amount of an asset is estimated to be less than its carrying amount, the carrying amount of the asset is reduced to its recoverable amount. An impairment loss is recognized as an expense immediately,unless the relevant asset is carried at a revalued amount, in which case the impairment loss is treated as a revaluation decrease.” In this regard, to help investors understand your accounting policy, please specifically disclose whether you use the cost model or the revaluation model for each class of property, plant and equipment. We refer you to paragraph 29 of IAS 16. If you do use the revaluation model, please provide disclosure in accordance with paragraph 77 of IAS 16. |

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 23

Response: The Company uses the cost model for each class of property, plant & equipment.

Particularly, for assets at the Company’s premises or in possession of the Company are tested for impairment and considering the revenue generating capacity and balance useful life, the Company determines that future profits will be sufficient to cover the written down value of these assets and hence no provision is required.

Consumer premises equipment is in in customers’ possession in order to provide DTH services. Particularly for consumer premises equipment which comprises of 85% of Videocon d2h's total Property, Plant & Equipment, the Company determines the number of subscribers who are not paying for their subscription charges. The Company provides for impairment on these assets on a cost basis.

4.4 Revenue, page F-11

| 53. | We note your discussion on 149 where you state, “As of September 30, 2014, Videocon d2h had over 2,800 distributors and direct dealers, and over 150,000 sub-dealers and recharge counters.” In this regard, please tell us in detail how the relationship between the distributors, direct dealer, sub-dealers, the end-subscribers, and yourself works. Disclose your revenue recognition as it relates to each distribution model. |

Response: The Company collectively describes its distributors, direct dealers and sub- dealers as the Company's distribution network. The Company enters into contractual agreements with its distributors to distribute our product and services. The distributors, sub-contract with the direct dealers and/or sub-dealers to retail our product and services. Ultimately the end-subscribers interact with retailers for the purpose of obtaining the Company’s product and services.

There is no difference in revenue recognition with respect to our distribution network as it forms a part of our distribution model. Any amounts received from distributors, dealers or sub- dealers (as the case may be) remain as liability under the head “Income Received in Advance” in the financial statements. The revenue in the Company’s books of accounts is recognized only upon the completion of activation by a customer, installation of set top boxes at end-subscribers’ premises. Subscription revenue is also recognized after providing the services to the subscriber.

Accordingly, the Company believes that no further disclosure is required in the financial statements. See also response to Comment 54 below.

Larry Spirgel

Division of Corporation Finance

February 4, 2015

Page 24

| 54. | We note your statement on page 150 that, “Videocon d2h operates on a prepaid model, to both distributors and, eventually, subscribers. Distributors pay in advance for subscription recharge and DTH connections.” Please disclose your revenue recognition policy as it relates to recharges and the prepaid model. Describe how the distributor(s) affect your revenue recognition policy as it relates to the recharges and the prepaid model. |

Response: Recharge is the mode of collection of money from the subscriber through the distribution network of the Company. The sale of recharge to a subscriber does not amount to revenue for the Company. The Company works on a prepaid model, i.e. the subscribers would be able to view the services as provided by the Company only if there is a credit balance in his subscription account maintained with the Company. As the recharge is the simple mode of collection and not revenue in itself it does not require any accounting policy for the same on page F-11 under. 4.4 “Revenue Recognition Policy”

The recharges are distributed to subscribers through the Company’s distribution network. The Company received in advance from distributors or direct dealers for recharge balances available for distribution to end-subscribers. The subscribers buy the recharge balance from the distribution network and recharge their DTH account with the Company.