DIRECTDIAL +852 3740 4863 DIRECTFAX +852 3910 4863 EMAILADDRESS JULIE.GAO@SKADDEN.COM

PARTNERS JOHN ADEBIYI¿ CHRISTOPHER W. BETTS EDWARD H.P. LAM¿* HAIPING LI * CLIVE W. ROUGH¿ JONATHAN B. STONE * ALEC P. TRACY * ¿ (ALSO ADMITTED IN ENGLAND & WALES) * (ALSO ADMITTEDIN NEW YORK)

REGISTERED FOREIGN LAWYERS WILL H. CAI (CALIFORNIA) Z. JULIE GAO (CALIFORNIA) BRADLEY A. KLEIN (ILLINOIS) RORY MCALPINE (ENGLAND & WALES) GREGORY G.H. MIAO (NEW YORK) ALAN G. SCHIFFMAN (NEW YORK) | SKADDEN, ARPS, SLATE, MEAGHER & FLOM

42/F, EDINBURGH TOWER, THE LANDMARK 15 QUEEN’S ROAD CENTRAL, HONG KONG

______

TEL: (852) 3740-4700 FAX: (852) 3740-4727 www.skadden.com

CONFIDENTIAL

August 7, 2015 |

AFFILIATE OFFICES

---------

BOSTON CHICAGO HOUSTON LOS ANGELES NEW YORK PALO ALTO WASHINGTON, D.C. WILMINGTON

---------

BEIJING BRUSSELS FRANKFURT LONDON MOSCOW MUNICH PARIS SÃO PAULO SEOUL SHANGHAI SINGAPORE SYDNEY TOKYO TORONTO | ||||||

Dietrich King, Assistant Director

David Lin, Staff Attorney

Amit Pande, Accounting Branch Chief

Benjamin Phippen, Staff Accountant

Division of Corporation Finance

Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549

| Re: | Yirendai Ltd. (CIK No. 0001631761) |

| Response to the Staff’s Comment Letter Dated July 24, 2015 |

Dear Mr. King, Mr. Lin, Mr. Pande and Mr. Phippen:

On behalf of our client, Yirendai Ltd., a foreign private issuer organized under the laws of the Cayman Islands (the “Company”), we submit to the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) this letter setting forth the Company’s responses to the comments contained in the Staff’s letter dated July 24, 2015. Concurrently with the submission of this letter, the Company is submitting a revised draft registration statement on Form F-1 (the “Revised Draft Registration Statement”) and certain exhibits via EDGAR to the Commission for confidential non-public review pursuant to the Jumpstart Our Business Startups Act.

The Staff’s comments are repeated below in bold and are followed by the Company’s responses. We have included page references in the Revised Draft Registration Statement where the language addressing a particular comment appears. Capitalized terms used but not otherwise defined herein have the meanings set forth in the Revised Draft Registration Statement.

Securities and Exchange Commission

August 7, 2015

Page 2

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Key Factors Affecting Our Results of Operations – Effectiveness of Risk Management, page 77

| 1. | We note your disclosure on page 121 that the actual amount to be set aside in the risk reserve fund is continuously monitored and calculated based on an analysis of both your historical charge-off rates and a charge-off forecast for your target borrower group. In addition, we note your disclosure linking collection efforts and triggering events, such as loan aging and default, with the withdrawals from the risk reserve fund. Given the significance of the underlying loan data and statistics to your operating performance, please revise your disclosure to include additional detailed information for the underlying loan portfolio such as aging / delinquency data and historical charge-offs for both the online channels such as the internet and mobile applications, as well as offline sources such as referrals from CreditEase’s on-the-ground sales network. |

In response to the Staff’s comment, the Company has expanded its disclosure on pages 77, 78 and 79 of the Revised Draft Registration Statement to include loan delinquency and historical charge-off information by channel.

Key Components of Results of Operations – Net Revenues – Transaction fees, page 79

| 2. | You disclose that revenue is recognized net and that in January 2015 you recognize the amount of the transaction fee collected upfront upon completion of the loan facilitation services and the remainder when the fees are collected. You also state that the amount of transaction fee paid upfront is sufficient to provide cash for the risk reserve fund. Please confirm that the average transaction fee rates disclosed on page 80 includes the amount collected for the risk reserve fund, which currently is 6%. |

The Company respectfully confirms that the average transaction fee rates disclosed on page 81 of the Revised Draft Registration Statement include the amounts collected for the risk reserve fund.

| 3. | You disclose separately the amount of loans originated and the sales and marketing expenses by online channels and offline channels. You also disclose on page 111 that you pay CreditEase a referral fee for |

Securities and Exchange Commission

August 7, 2015

Page 3

| those borrowers you acquire through their extensive on-the-ground sales network and that the average size of loans sourced through offline channels tends to be larger than that of loans sourced through online channels. Please clarify whether your offline channels include only the referrals from CreditEase and therefore, the referral fee paid to CreditEase is only associated with these channels. Also tell us if there are other differences in the investor or borrower base for the offline channel versus online channel (e.g. concentration in pricing grid or fees). |

The Company advises the Staff that the Company’s offline channels include only referrals from CreditEase and that the referral fee paid to CreditEase is only associated with these offline channels. In response to the Staff’s comment, the Company has revised its disclosure on page 83 of the Revised Draft Registration Statement to include the relevant clarification.

The Company advises the Staff that investors acquired through offline channels typically invest larger sums through the Company’s platform as compared with investors acquired through online channels. Similarly, borrowers acquired through offline channels tend to receive approvals to borrow larger sums as compared with borrowers acquired through online channels. In addition, borrowers acquired through offline channels are typically grouped into the Grade A or D segments, while borrowers acquired through online channels are grouped into the Grade A, B, C or D segments.

Critical Accounting Policies, Judgments and Estimates

Revenue Recognition, page 84

| 4. | You disclose on page 85 that you recognize revenue on the upfront transaction fee upon completion of the service of facilitating loan origination only to the extent the upfront fee exceeds the stand-ready liability related to the risk reserve fund. We also note your risk reserve fund rollforward on page F-37 and that during the three months ended March 31, 2015 you recorded a provision of $15.7 million related to the liability. Please address the following related to your accounting for the risk reserve fund: |

| • | Tell us what service(s) you provide, other than facilitation of the loan, to the borrow that relate to the transaction fee; |

The Company respectfully advises the Staff that other than the facilitation of the loan, the Company also provides risk reserve fund

Securities and Exchange Commission

August 7, 2015

Page 4

services and other miscellaneous services such as sending payment reminder text messages to borrowers during the first fourteen days of loan delinquency, and instructing third-party payment platforms to transfer principal repayment and interest payment.

With the launching of investor protection service in January 2015, in accordance with ASC 460-10-55-23 (b), the Company allocates the upfront transaction fee from the borrower to offset the stand-ready liability related to the risk reserve fund, which is recorded at the estimated fair value of the guarantee according to ASC 460-10-30-2 (b). Thus the revenue on the upfront transaction fee is recognized only to the extent the upfront fee exceeds the stand-ready liability. In response to the Staff comment, the Company has revised its disclosure on page F-37 of the Revised Draft Registration Statement to more accurately describe the US$15.7 million as “upfront fees allocated” rather than as a “provision.”

| • | Explain in greater detail how you account for your guarantee of principal and accrued interest to an investor once a loan is originated and the accounting guidance you apply (e.g. ASC 460); |

The Company respectfully advises the Staff that once a loan is originated, the Company recognizes a stand-ready liability related to the risk reserve fund service as the higher of the fair value of the future repayments and the probable contingent liability amount required to be recognized at inception of the guarantee, in accordance with ASC 460-10-30-3. The Company estimates the fair value of the future repayments as 6% of the total loan facilitation amount, which equals the risk reserve fund set aside by the Company. Please refer to Note 3 on page F-39 of the Revised Draft Registration Statement for an explanation of the determination of the fair value of the future repayment. The probable contingent liability amount (which is covered by guidance from ASC 450-20) is also equal to the risk reserve fund set aside by the Company, as management believes the payment of the full risk reserve amount is probable at the inception of each loan.

As a result, the stand-ready liability is recognized as the full risk reserve amount, with the offsetting entry being the debit for the cash received from the transaction fees upfront in accordance with ASC 460-10-55-23 (b).

Neither ASC 460 nor ASC 450-20 provides explicit guidance on the interaction between ASC 460 and ASC 450-20 after initial recognition. Accordingly, entities should establish a systematic and

Securities and Exchange Commission

August 7, 2015

Page 5

rational method with a reasonable basis for support for subsequent accounting. According to ASC 460-10-35-1, the liability that the guarantor initially recognized would typically be reduced (by a credit to earnings) as the guarantor is released from risk under the guarantee. And normally, the recognition of a contingent liability results in the recognition of expenses in earnings. In the Company’s case, the estimated stand-ready liability equals the estimated contingent liability. As there is no specific authoritative guidance addressing the day-two income statement presentation for financial guarantee the Company considered that netting the changes in the guarantee is more representative of the Company’s obligation, therefore no separate guarantee revenue or guarantee provision expense have been recognized in the Consolidated Statement of Operations.

The stand-ready liability is reduced when the Company makes payments to investors.

In response to the Staff’s comment, Note 2 of the Unaudited Condensed Consolidated Financial Statements for the three-month period on page F-37 has been revised to clarify the subsequent accounting of the guarantee liability.

| • | Tell us where the provision related to the risk reserve fund liability is recorded on the Consolidated Statement of Operations; and |

The Company respectfully advises the Staff that, as explained in the preceding response, the net impact of the guarantee obligation on the Consolidated Statement of Operations was nil.

| • | Explain how you subsequently measure the risk reserve fund liability. |

The Company respectfully advises the Staff that the stand-ready liability represents the opening balance of the fund plus risk reserve funds set aside from new loans facilitated and collections of default payments and penalties (if any) during the period less payments for defaulted loan principal and interest for the specific period.

Liabilities from risk reserve fund and servicing, page 86

| 5. | You disclose that you guarantee the principal and accrued interest repayment of a defaulted loan up to a cap. The cap is currently set at 6% of the total loan facilitation amount. You also disclose on page 114 that you will withdraw funds from the risk reserve fund to repay |

Securities and Exchange Commission

August 7, 2015

Page 6

| the principal and accrued interest for a defaulted loan. Please tell us whether the agreement with the investor discloses the cap on the guarantee repayment of a defaulted loan and your ability to change this cap in the future. In addition, confirm, if true, and revise your risk reserve fund disclosures throughout the filing to clearly state that the amount of principal and accrued interest to be repaid and withdrawn from the risk reserve fund for any defaulted loan is only 6% of that defaulted loan due to the cap. |

The Company respectfully advises the Staff that the investor protection service arrangement was launched in January 2015 and has only been in operation for eight months. As a result, some of the terms of the arrangement are being refined. For example, although the Company sets aside a certain amount of the fees it collects in the risk reserve fund, it does not disclose in the agreements with investors that it currently sets asides 6% of each loan for the risk reserve fund, or it may change this percentage in the future. To mitigate this, in early August 2015, the Company added a statement on its website clarifying that 6% of each loan is set aside in the risk reserve fund. The Company discloses to the public the balance of the risk reserve fund at the end of every month.

Currently, the Company does not expect that the 6% set aside to change in the near term, but the Company has the right to change it in the future. Under the current risk reserve fund agreement entered into between the investors and the Company, the investors are aware of and inherently exposed to the risk of not receiving the full amount of the defaulted loan from the risk reserve fund.

The Company respectfully advises the Staff that the amount of principal and accrued interest to be repaid and withdrawn from the risk reserve fund for any individual defaulted loan is not caped at only 6% of that particular defaulted loan, as the repayment of the defaulted loans is on a portfolio basis, not on an individual loan basis. Therefore, when an individual loan defaults, as long as the risk reserve fund balance is sufficient, the amount of principal and accrued interest will be paid in full to the investor. In other words, the Company sets aside a fund from fees collected that would cover the investors for credit losses on their loans up to a cap equal to the risk reserve fund balance. The Company has revised its disclosure on pages 87 and F-37 of the Revised Draft Registration Statement to further clarify this.

Securities and Exchange Commission

August 7, 2015

Page 7

Business

Our Platform and the Transaction Process, page 114

| 6. | You disclose on page 116 that funds are withdrawn from a custody account managed by China Guangfa Bank and disbursed to the borrower once the loan is fully subscribed or funded by an investor. Please tell us what rights or risks (e.g. interest income) you have related to the investor funds held in the custody account before being disbursed to the borrower. |

The Company respectfully advises the Staff that, with respect to custody accounts managed by China Guangfa Bank, the rights it has with regard to undisbursed investor funds consist solely of the right to instruct China Guangfa Bank to distribute such funds to a borrower. The Company receives no interest income on investor funds held in such custody accounts.

| 7. | We note in your “Stage 5” disclosures on page 116 that you must authorize the transfer of loan repayments to the investor and you are involved in the collection process for delinquent loans. However, you then disclose that you outsource all stages of the collections process to CreditEase. Please revise your disclosures to clarify what day-to-day activities related to the loans and the collection process you perform versus CreditEase. Clarify also who makes the decisions for default services and / or any remediation processes such as restructurings of loans. |

In response to the Staff’s comment, the Company has revised its disclosure on page 117 of the Revised Draft Registration Statement.

Risk Management – Proprietary Credit Scoring Model and Loan Qualification System, page 117

| 8. | We note your disclosure on page 79 that net revenues include transaction fees, service fees and other revenues and that the amount of transaction fee charged is based upon the pricing and amount of the underlying loan. We also note your disclosure on page 80 detailing the average transaction fee rate for each of the pricing grades A through D, which range from 6.2% to 28.7%. On page 119, you disclose the APRs that correspond to these same four segments ranging from 16.9% to 39.5%, which includes both a fixed interest rate and a transaction fee rate for the services offered to borrowers. In order to provide additional clarity surrounding these disclosures, please revise your disclosure on page 119 to state, if true, that the |

Securities and Exchange Commission

August 7, 2015

Page 8

| difference between the average transaction fee rates on page 80 and the APR rates on page 119 is the fixed interest rates for the corresponding pricing grades. |

In response to the Staff’s comment, the Company has revised its disclosure on page 120 of the Revised Draft Registration Statement.

Consolidated Financial Statements

Notes to Consolidated Financial Statements

Note 1. Organization and Principal Activities, page F-8

| 9. | We note your response to comment 8 of our letter dated April 27, 2015 and that Heng Cheng was established on September 15, 2014. You state that Heng Cheng is a variable interest entity (“VIE”) that should be consolidated by the CreditEase group before and after the signing of the VIE arrangement in February 2015. In order to more fully understand your analysis and conclusion, please address the following: |

| • | Describe, in detail, the structure of Heng Cheng including the organization chart, whether there were VIE arrangements between a subsidiary of CreditEase and Heng Cheng, terms for distributions, rights of the three shareholders, etc. |

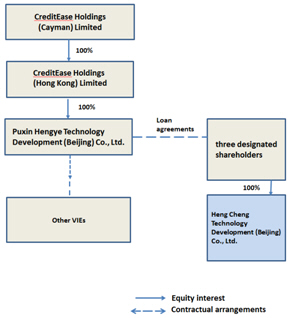

The Company respectfully advises the Staff that the organization chart for Heng Cheng Technology Development (Beijing) Co., Ltd. (“Heng Cheng”) within the CreditEase group is as follows:

Securities and Exchange Commission

August 7, 2015

Page 9

The only agreements in place before February 2015 were the loan agreements between Puxin Hengye Technology Development (Beijing) Co., Ltd. (“Puxin Hengye”), a 100% owned subsidiary of CreditEase, and the three designated shareholders of Heng Cheng. The loan agreements between each of the three designated shareholders and Puxin Hengye stipulated that the sole purpose of the loans was to provide funds to inject into Heng Cheng as capital in the name of the three designated shareholders on behalf of CreditEase, and that Puxin Hengye had the right to request the three designated shareholders transfer a portion or all of the equity ownership of Heng Cheng to Puxin Hengye or any third party designated by it with no consideration.

Based on the loan agreements, the three designated shareholders of Heng Cheng lack the character of being obliged to absorb the expected losses of Heng Cheng, as the cash was provided by Puxin Hengye. As a result, Heng Cheng should be regarded as a VIE according to ASC 810-10-15-14 (b)(2). Furthermore, the three designated shareholders are considered de facto agents of CreditEase under ASC 810-10-25-43, as their equity interests in Heng Cheng were received through a loan extended by CreditEase, and two of the designated shareholders, Mr. Ning Tang and Mr. Fanshun Kong, are a director and an employee of the CreditEase group, respectively. CreditEase and the three designated shareholders, as a group, held the

Securities and Exchange Commission

August 7, 2015

Page 10

power to direct the activities of Heng Cheng that most significantly impact its economic performance, and had the obligation to absorb the losses of Heng Cheng that could potentially be significant. As a result, according to ASC 810-10-25-44, CreditEase should consolidate Heng Cheng, as CreditEase was the principal in the de facto agency relationship with the three designated shareholders.

| • | In your response you state that the capital injection loan was from Puxin Hengye, a subsidiary of CreditEase, to the three designated shareholders (Mr. Ning Tang, Mr. Fanshun Kong and Ms. Yan Tian). However, on page 68 you disclose that the loan was between Heng Ye and the shareholders of Heng Cheng. Explain the discrepancy between your response and the disclosure on which entity lent the funds for Heng Cheng’s capital. |

The Company respectfully advises the Staff that in December 2014 the first batch of capital injected in the amount of RMB 5.5 million (US$887 thousand) into Heng Cheng by the three designated shareholders was provided by CreditEase through loans extended by Puxin Hengye. In February 2015, after the establishment of Heng Ye on January 8, 2015, Puxin Hengye transferred all rights and obligations under the loan agreements with the three designated shareholders to Heng Ye, and thus was released from the loan agreements.

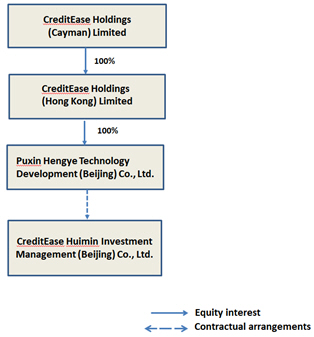

| • | Provide us with a chart of CreditEase’s corporate structure, similar to the one on page 5, before the contribution of assets to Heng Cheng and identify the subsidiaries or possibly VIEs that were contributed assets to Heng Cheng. |

The Company respectfully advises the Staff that the organization chart of CreditEase is as follows, with Puxin Hengye and CreditEase Huimin Investment Management (Beijing) Co., Ltd. (“CreditEase Huimin”) being the subsidiary and the VIE in the CreditEase group that contributed assets to Heng Cheng:

Securities and Exchange Commission

August 7, 2015

Page 11

| • | Tell us when assets were contributed to Heng Cheng and the terms of the contribution. |

The Company respectfully advises the Staff that Puxin Hengye and its VIE*, CreditEase Huimin, transferred assets and liabilities related to the Yirendai business (the “Yirendai Business”) as of March 31, 2015 to Heng Cheng as a contribution.

The key terms of the asset transfer agreement are set forth below:

| • | The date of asset transfer was March 31, 2015. |

| • | The online peer-to-peer lending business will be run solely by Heng Cheng after the transfer, and Puxin Hengye and CreditEase Huimin will no longer operate such business. |

| • | All the assets and liabilities of Puxin Hengye and CreditEase Huimin that were related to the online peer-to-peer lending business transfer to Heng Cheng as contribution. |

| • | All the employees of Puxin Hengye and CreditEase Huimin that worked for the online peer-to-peer lending business cease their existing employment contracts and sign new employee contacts with Heng Cheng, with no change in the terms of the contracts. |

*Note: A series of VIE agreements were also entered into, including exclusive business cooperation agreement, equity interest pledge agreement, exclusive option agreement, and power of attorney between Puxin Hengye and shareholders of CreditEase Huimin. Through the VIE agreements, Puxin Hengye holds the power to direct the activities that most significantly affect the economic performance of CreditEase Huimin and receives the economic benefits of CreditEase Huimin that could be significant to CreditEase Huimin.

| • | Tell us how the net assets contributed to Heng Cheng were initially measured (i.e. fair value or carrying value) and the accounting guidance relied upon for their measurement and presentation by Heng Cheng. |

The Company advises the Staff that the net assets contributed to Heng Cheng were initially measured at carrying amount, as Heng Cheng and the entities from which the assets were contributed is a consolidated subsidiary and/or are VIEs of CreditEase and therefore

Securities and Exchange Commission

August 7, 2015

Page 12

are under the common control of CreditEase. According to ASC 805-50-30-5, when accounting for a transfer of assets or exchange of shares between entities that are under common control, the entity that receives the net assets or the equity interests should initially measure the recognized assets and liabilities transferred at their carrying amounts in the accounts of the transferring entity at the date of transfer.

| • | Tell us whether CreditEase or one of its subsidiaries consolidated Heng Cheng before the 2015 reorganization and if a subsidiary, which one. |

The Company respectfully advises the Staff that, as discussed under the bullet points above, Puxin Hengye provided the loans to the designated shareholders of Heng Cheng, and became the primary beneficiary of Heng Cheng, as Puxin Hengye was the principal in the de facto agency relationship with the three designated shareholders. As a result, Puxin Hengye consolidated Heng Cheng before the 2015 reorganization.

| 10. | You disclose that in the first quarter of 2015 your parent, CreditEase reorganized and as part of this reorganization the Yirendai Business was transferred to the “Group”. The “Group” is defined as the Company, its subsidiaries, and VIE. In your response to comment 8 of our letter dated April 27, 2015 you also state that Heng Cheng was consolidated in the financial statements before and after the signing of the new VIE arrangements. Please address the following: |

| • | Confirm that the “Group” is the Company at the consolidated level. |

The Company respectfully confirms that the “Group” means Yirendai Ltd., its subsidiaries and VIE.

| • | Describe the terms of the agreement between Heng Ye and Puxin Hengye for the assignment of the capital injection loan for Heng Cheng including the effective date of the assignment; |

The Company advises the Staff that in December 2014, the initial portion of capital injected in an amount of RMB5.5 million (US$887 thousand) into Heng Cheng by Mr. Ning Tang was provided by CreditEase through a loan extended by Puxin Hengye. In January 2015, the second portion of capital injected into Heng Cheng in amounts of RMB3.0 million (US$484 thousand) by Mr. Fanshun Kong and RMB3.0 million (US$484 thousand) by Ms. Yan Tian was

Securities and Exchange Commission

August 7, 2015

Page 13

also provided by CreditEase through loans extended by Puxin Hengye. In February 2015, after the establishment of Heng Ye on January 8, 2015, according to the loan transfer agreement dated and signed on February 22, 2015 between Puxin Hengye and Heng Ye, Puxin Hengye transferred all rights and obligations under the loan agreements with the three designated shareholders to Heng Ye, and thus was released from the loan agreements, effective from the date of signing of the loan transfer agreement. Mr. Ning Tang, chief executive officer of CreditEase, cannot change the terms of the loan without pre-approval of preferred shareholders of CreditEase Holdings (Cayman) Limited, as restricted by the preferred shareholders’ related party contract approval right.

In aggregate, Heng Ye provided loans of RMB11.5 million (US$1.8 million) to the designated shareholders of Heng Cheng solely for the capitalization of Heng Cheng up to March 31, 2015.

| • | Explain in detail how you determined that Heng Cheng should be consolidated by the Company before February 2015 if the Company did not have the power to direct the activities that most significantly affects the economic performance of the VIE or right to the economic benefits or obligation to absorb losses of Heng Cheng until 2015. |

The Company respectfully advises the Staff that according to ASC 805-50-05-5, transactions between entities under common control are accounted for in a manner similar to the pooling-of-interest method. Thus, the financial statements of the commonly controlled entities should be combined, retrospectively, as if the transaction had occurred at the beginning of the period. Further, ASC 805-50-45-5 states that prior years’ comparative information is adjusted for periods during which the entities were under common control. In addition, ASC 805-50-45-2 requires that the “effects of intra-entity transactions on current assets, current liabilities, revenue, and cost of sales for periods presented and on retained earnings at the beginning of the periods presented shall be eliminated to the extent possible.”

In addition, section 13410.1 of SEC Financial Reporting Manual, “SFAS 154 [ASC 250] requires that a change in the reporting entity or the consummation of a transaction accounted for in a manner similar to a pooling of interests (i.e., a reorganization of entities under common control) be retrospectively applied to the financial statements of all prior periods when the financial statements are issued for a period that includes the date the change in reporting entity or the transaction occurred.”

Securities and Exchange Commission

August 7, 2015

Page 14

As Heng Cheng and the Company were under common control of CreditEase for all periods presented, the comparative information was retrospectively adjusted.

According to ASC 805-50-30-5, when accounting for a transfer of assets or exchange of shares between entities under common control, the entity that receives the net assets or the equity interests should initially measure the recognized assets and liabilities transferred at their carrying amounts in the accounts of the transferring entity at the date of transfer.

Based on the guidance above, the Company initially measured the assets and liabilities in Heng Cheng at the carrying value on Heng Cheng’s books.

| • | Tell us the accounting guidance you relied upon in determining that Heng Cheng should be consolidated by Heng Ye before February 2015 and the guidance relied upon for the initial measurement of the assets, liabilities, and noncontrolling interests in Heng Cheng when consolidated by Heng Ye. |

The Company respectfully directs the Staff to the response under the preceding bullet point for the accounting guidance references.

| • | Confirm, if true, that the Company’s financial statements for all periods presented were retrospectively adjusted for the consolidation of Heng Cheng. |

The Company respectfully confirms that the Company’s financial statements for all periods presented were retrospectively adjusted for the consolidation of Heng Cheng.

Note 2. Summary of Significant Accounting Policies – Basis of Consolidation, page F-10

| 11. | We note your response to comment 10 of our letter dated April 27, 2015. You explain that Heng Cheng did not begin to provide services until late December 2014 and that is why Heng Cheng’s total assets as of December 31, 2014 are only $2.4 million of the $64.8 million disclosed on page F-3. You also disclose on page 29 that CreditEase and the Company are under common control and therefore, your consolidated financial statements include the financial activity attributable to your business for all periods presented. Please address the following: |

Securities and Exchange Commission

August 7, 2015

Page 15

| • | Confirm, if true, that the $62.4 million difference represents assets held by the Company or one of its subsidiaries. |

The Company respectfully confirms that the US$62.4 million difference represents assets held by a subsidiary and a VIE of CreditEase which ran the Yirendai Business as of December 31, 2014, as the financial statements were prepared on a carved-out basis.

| • | Tell us whether the $62.4 million difference represents a carve-out of the Yirendai Business from CreditEase and if so, explain why this portion of the Yirendai Business was not contributed to Heng Cheng. |

The Company respectfully confirms that the US$62.4 million difference represents a carve-out of the Yirendai Business from CreditEase. These assets have not been legally transferred to Heng Cheng as of December 31, 2014.

| • | You disclose on page 75 that the online consumer finance marketplace business was commenced in March 2012. Confirm that this business was the Yirendai Business. In addition, tell us whether the Yirendai Business was presented retrospectively in Heng Cheng when the assets were contributed by CreditEase’s subsidiaries in 2014 and if so, for what periods. |

The Company respectfully confirms that the online consumer finance marketplace business commenced in March 2012 was the Yirendai Business. The Yirendai Business was presented retrospectively in Heng Cheng for all periods presented, as assets were contributed by CreditEase’s subsidiary and VIE in 2015.

| 12. | We note your disclosure on page 70 that you plan to enter into various agreements with CreditEase with respect to various ongoing relationships between your and CreditEase. These agreements include a master transaction agreement, a transitional service agreement, a non-competition agreement, a cooperation framework agreement and an intellectual property license agreement. We further note that the master transaction agreement contains provisions relating to your carve-out from CreditEase. Given that the carve-out was completed in the first quarter of 2015, please provide us with a copy of the master transaction agreement and other agreements related to the carve-out. Please also file these agreements as exhibits in your next amendment. |

Securities and Exchange Commission

August 7, 2015

Page 16

The Company respectfully advises the Staff that it plans to enter into a series of agreements with CreditEase prior to the completion of its initial public offering with respect to its ongoing relationship with CreditEase. These agreements include a master transaction agreement, a transitional service agreement, a non-competition agreement, a cooperation framework agreement and an intellectual property license agreement. In response to the Staff’s comment, the Company has filed the forms of these agreements as exhibits to the Revised Draft Registration Statement.

* * *

Securities and Exchange Commission

August 7, 2015

Page 17

If you have any questions regarding the Revised Draft Registration Statement, please contact the undersigned by phone at +852-3740-4863 or via e-mail at julie.gao@skadden.com. Questions relating to accounting and auditing matters of the Company may also be directed to Elsie Zhou, partner at Deloitte Touche Tohmatsu Certified Public Accountants LLP, by phone at +86 10 8520-7142 or via email at ezhou@deloitte.com.cn.

Very truly yours,

/s/ Z. Julie Gao

Z. Julie Gao

Enclosures

| cc: | Ning Tang, Executive Chairman, Yirendai Ltd. |

| Yu Cong, Chief Financial Officer, Yirendai Ltd. |

| Elsie Zhou, Deloitte Touche Tohmatsu Certified Public Accountants LLP |

| Chris Lin, Esq., Simpson Thacher & Bartlett LLP |