SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a)

of the Securities Exchange Act of 1934

Filed by the Registrant¨

Filed by a Party other than the Registrantþ

Check the appropriate box:

| o | Preliminary Proxy Statement |

| o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| o | Definitive Proxy Statement |

| þ | Definitive Additional Materials |

| o | Soliciting Material Under Rule 14a-12 |

Immunomedics, Inc.

(Name of Registrant as Specified In Its Charter)

venBio Select Advisor LLC

Behzad Aghazadeh

Scott Canute

Peter Barton Hutt

Khalid Islam

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (check the appropriate box):

| þ | No fee required. |

| | |

| o | Fee computed on table below per Exchange Act Rule 14a-6(i)(4) and 0-11. |

| | 1) | Title of each class of securities to which transaction applies: |

| | | |

| | | |

| | | |

| | 2) | Aggregate number of securities to which transaction applies: |

| | | |

| | | |

| | 3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act |

| Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| | | |

| | | |

| | 4) | Proposed maximum aggregate value of transaction: |

| | | |

| | | |

| | | |

| | 5) | Total fee paid: |

| | | |

| | | |

| | | |

| o | Fee paid previously with preliminary materials. |

| o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the |

| filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| | 1) | Amount Previously Paid: |

| | | |

| | | |

| | | |

| | 2) | Form, Schedule or Registration Statement No.: |

| | | |

| | | |

| | | |

| | 3) | Filing Party: |

| | | |

| | | |

| | | |

| | 4) | Date Filed: |

On January 26, 2017, venBio Select Advisor LLC (“venBio”) issued a press release (the “Press Release”) to stockholders of Immunomedics, Inc. (the “Company”) concerning venBio’s presentation to representatives of Institutional Shareholder Services Inc. regarding the Company (the “ISS Presentation”), made on January 24, 2017. A copy of the Press Release is filed herewith asExhibit 1 and a copy of the ISS Presentation is filed herewith asExhibit 2.

Exhibit 1

venBio Releases Presentation Detailing Urgent Case for Change at Immunomedics

Outlines Strategic Plan to Maximize Value and Improve Corporate Governance

Reveals Interconnectedness of Newly-Appointed Immunomedics Board and Lack of Qualifications of Appointees to Reverse Strategic Missteps

Urges Stockholders to Support venBio’s Board Nominees, Who Possess the Necessary Skillset and Experience to Maximize the Value of Immunomedics

NEW YORK(January 26, 2017) – venBio Select Advisor LLC (“venBio”), the beneficial owner of approximately 10.5 million shares, or 9.9%, of Immunomedics, Inc. (NASDAQ: IMMU) (“Immunomedics” or the “Company”) and its largest stockholder, today released a presentation: titled “The Case for Change at Immunomedics, Inc.” This presentation can be found at: http://www.okapivote.com/immunomedics.

In this presentation, venBio highlights the Company’s decades-long value destruction and underperformance and discusses how the Board of Directors and management have failed to advance the best interests of stockholders, especially due to the Company’s failure to form a strategic partnership to bring to market the Company’s promising Triple Negative Breast Cancer drug, IMMU-132. venBio strongly believes that it is crucial to provide experienced and competent oversight to realize the significant potential of IMMU-132. In venBio’s view, the Company’s leadership and newly-configured Board lack the independence and experience needed to right the course of Immunomedics and to maximize the value of the Company’s assets.

Highlights of venBio’s presentation and strategic plan for Immunomedics include:

| · | In venBio’s view, Immunomedics’ newly-appointed Board members lack the manufacturing, regulatory, and pharmaceutical deal experience that is vital to reverse the string of strategic missteps at the Company.Furthermore, this group is highly interconnected and lacks the independence to adequately oversee the Company. |

| · | Newly-appointed Vice-Chairman Jason Aryeh does not have the necessary skillset or experience to position the Company for success, and has a history of overpromising, under-delivering and destroying stockholder value. Boards in which Aryeh is a director have experienced share price decline and loss of key stockholders, likely due to his history of failing to execute on promises and acting on behalf of the best interests of stockholders. His Board experience to date has been characterized by inability to complete promised acquisitions, failure to generate public market interest and poor financial performance under his oversight. In addition, while Aryeh is currently on five different Boards, none of these have relevance to Immunomedics’ core business. |

| · | The current Immunomedics management team that has overseen decades-long value destruction and underperformance – while simultaneously enriching themselves – will retain control with the new Board structure. Failure to execute on striking a pharma partnership in order to advance IMMU-132 threatens to add it to the long list of drug failures that have taken place at the Company under the current management team. Even with the recent success of IMMU-132, the stock price continues to underperform, in our view, largely due to |

management missteps. Despite poor company performance, management continues to generously reward themselves at the expense of stockholders.

| · | venBio’s nominees have defined a 100-day plan with clear objectives.These include moving quickly to evaluate strategic options for Immunomedics while advancing IMMU-132 towards the market, bolstering corporate governance to rebuild confidence among key stakeholders, and improving operations and financial management of the Company. |

| · | venBio’s four highly-qualified nominees possess the necessary qualities to restore independent and competent governance and to maximize value for stockholders. venBio believes its nominees – Scott Canute, Peter Barton Hutt, Dr. Khalid Islam, and Dr. Behzad Aghazadeh – have the right pharmaceutical development background, commercial manufacturing expertise and pharmaceutical partnering/deal making experience needed to advance IMMU-132, build stockholder value and position the Company for long-term value creation. |

We believe urgent change is necessary at Immunomedics in order to advance the IMMU-132 drug and to ultimately maximize value for all stockholders. Your vote is critical to electing a Board with the right capabilities necessary to advance the best interests of stockholders.

Vote FOR all four of venBio’s nominees on the GOLD Proxy Card today.

About venBio Select Advisor LLC

venBio Select Advisor LLC (“venBio Select”) is the SEC registered investment manager for venBio’s public markets strategy and its main equity investment vehicle – the venBio Select Fund – which primarily invests across the biotechnology and therapeutics sector. The venBio Select Fund is managed by Dr. Behzad Aghazadeh, supported by a team of seasoned professionals with advanced medical and scientific backgrounds, and extensive investment experience in the biopharmaceutical industry. The investment and business operations for venBio Select are based in New York. venBio’s separate venture capital team operates and manages their funds from San Francisco, partnering with industry leaders to build biotechnology companies with a focus on novel therapeutics for unmet medical needs.

Investor Contact

Okapi Partners LLC

Bruce H. Goldfarb /Lydia Mulyk, (212)-297-0720 or Toll-free (855) 305-0857

info@okapipartners.com

Media Contact

Sloane & Company

Dan Zacchei / Joe Germani, 212-486-9500

dzacchei@sloanepr.com /jgermani@sloanepr.com

About the Proxy Solicitation

venBio Select Advisor LLC, Behzad Aghazadeh, Scott Canute, Peter Barton Hutt and Khalid Islam (collectively, the “Participants”) have filed with the Securities and Exchange Commission (the “SEC”) a definitive proxy statement and accompanying form of proxy to be used in connection with the solicitation of proxies from the stockholders of Immunomedics (the “Company”). All stockholders of the Company are advised to read the definitive proxy statement and other documents related to the solicitation of proxies by the Participants, as they contain important information, including additional information related to the Participants. The definitive proxy statement and an accompanying proxy card is being furnished to some or all of the Company’s stockholders and is, along with other relevant documents, available at no charge on the SEC website at http://www.sec.gov/ or from Okapi Partners at 212-297-0720 or info@okapipartners.com.

Information about the Participants and a description of their direct or indirect interests by security holdings is contained in the definitive proxy statement on Schedule 14A filed by the Participants with the SEC on December 6, 2016. This document is available free of charge from the sources indicated above.

Warning Regarding Forward Looking Statements

THIS PRESS RELEASE CONTAINS FORWARD LOOKING STATEMENTS. FORWARD LOOKING STATEMENTS CAN BE IDENTIFIED BY USE OF WORDS SUCH AS "OUTLOOK", "BELIEVE", "INTEND", "EXPECT", "POTENTIAL", "WILL", "MAY", "SHOULD", "ESTIMATE", "ANTICIPATE", AND DERIVATIVES OR NEGATIVES OF SUCH WORDS OR SIMILAR WORDS. FORWARD LOOKING STATEMENTS IN THIS PRESS RELEASE ARE BASED UPON PRESENT BELIEFS OR EXPECTATIONS. HOWEVER, FORWARD LOOKING STATEMENTS AND THEIR IMPLICATIONS ARE NOT GUARANTEED TO OCCUR AND MAY NOT OCCUR AS A RESULT OF VARIOUS RISKS, REASONS AND UNCERTAINTIES. EXCEPT AS REQUIRED BY LAW, VENBIO AND ITS AFFILIATES AND RELATED PERSONS UNDERTAKE NO OBLIGATION TO UPDATE ANY FORWARD LOOKING STATEMENT, WHETHER AS A RESULT OF NEW INFORMATION, FUTURE DEVELOPMENTS OR OTHERWISE.

Exhibit 2

The Case for Change at Immunomedics , Inc. (IMMU)

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 2 Disclosures/Disclaimer venBio Select Advisor LLC, (" venBio ") Behzad Aghazadeh, Scott Canute, Peter Barton Hutt and Khalid Islam (collectively, the “Participants”) have filed with the Securities and Exchange Commission (the “SEC”) a definitive proxy statement and accompanying form of proxy to be used in connection with the solicitation of consents from the stockholders of Immunomedics , Inc. (the “Company”). All stockholders of the Company are advised to read the definitive proxy statement and other documents related to the solicitation of proxies by the Participants, as they contain important information, includ ing additional information related to the Participants. The definitive proxy statement and an accompanying proxy card are being furnished to some or all of the Company’s stockholders and are, along with other relevant documents, available at no charge on the SEC website at http://www.sec.gov/ or from Okapi Partners at 212 - 297 - 0720 or info@okapipartners.com. Information about the Participants and a description of their direct or indirect interests by security holdings is contained in the definitive proxy statement on Schedule 14A filed by the Participants with the SEC on December 6, 2016. This document is available free of charge from the sources indicated above. venBio has not sought or obtained consent from any third party to use any statements or information indicated herein as having been obtained or derived from statements made or published by third parties. Any such statements or information should not be viewed as indicating the support of such third party for the views expressed herein. No warranty is made that data or information, whether derived or obtained from filings made with the SEC or from any third party, is accurate. Warning Regarding Forward Looking Statements THIS PRESENTATION CONTAINS FORWARD LOOKING STATEMENTS. FORWARD LOOKING STATEMENTS CAN BE IDENTIFIED BY USE OF WORDS SUCH AS "OUTLOOK", "BELIEVE", "INTEND", "EXPECT", "POTENTIAL", "WILL", "MAY", "SHOULD", "ESTIMATE", "ANTICIPATE", AND DERIVATIVES OR NEGATIVES OF SUCH WORDS OR SIMILAR WORDS. FORWARD LOOKING STATEMENTS IN THIS PRESENTATION ARE BASED UPON PRESENT BELIEFS OR EXPECTATIONS. HOWEVER, FORWARD LOOKING STATEMENTS AND THEIR IMPLICATIONS ARE NOT GUARANTEED TO OCCUR AND MAY NOT OCCUR AS A RESULT OF VARIOUS RISKS, REASONS AND UNCERTAINTIES. EXCEPT AS REQUIRED BY LAW, VENBIO AND ITS AFFILIATES AND RELATED PERSONS UNDERTAKE NO OBLIGATION TO UPDATE ANY FORWARD LOOKING STATEMENT, WHETHER AS A RESULT OF NEW INFORMATION, FUTURE DEVELOPMENTS OR OTHERWISE .

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 3 Executive Summary 1. venBio is IMMU’s largest stockholder (9.9% of shares outstanding); our interests are aligned with other stockholders to maximize value 2. IMMU’s management and board have overseen decades of value destruction; recent management missteps have further penalized stockholders and impeded patient access to promising therapy 3. Early data for company’s lead product candidate IMMU - 132 promises significant potential, but requires competent oversight to prevent repeat of missteps leading to further value destruction 4. venBio strongly believes there is a limited window to realizing value, which requires structural changes within the board a) Assembled team of industry veterans to oversee transformational period at IMMU b) Developed robust 100 - day plan to critically evaluate IMMU assets and capabilities, to formulate winning strategy for long - term value creation

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 4 venBio Select Advisor • Public market investment fund focused on innovation within biotechnology sector – Fund launched in 2010 – Team of seasoned investment professionals with medical/scientific backgrounds – IMMU is venBio's f irst activist situation; activism not regular component of our investment strategy – venBio Select is based in New York and independent of venBio venture capital business (based in San Francisco) • As IMMU’s largest stockholder, we are seeking change due to concerns over company’s ability to execute and deliver value to stockholders – Followed company for many years and holder of 9.9% of outstanding shares – Over 18 months held numerous one - on - one meetings with management over phone / email, medical meetings, investor conferences, and site visit at IMMU headquarters – Decided to actively pursue change, in light of major concerns for company’s ability to realize potential of IMMU - 132 and bring this important medicine to patients – IMMU's dilutive financing in October, with stock already trading near 52 - week lows and down >50% from yearly highs, added to our concerns compelling us to seek urgently needed change

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” IMMU’s track record of destroying stockholder value while enriching management 5

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 6 Early data of lead drug candidate IMMU - 132 supports a significant opportunity • IMMU - 132 is being studied for the treatment of Triple Negative Breast Cancer (“TNBC ”) • Most aggressive form of breast cancer • significant unmet need • The FDA granted Breakthrough Designation – recognition of compelling early data • 30% tumor shrinkage vs 10 - 15% expected (“response rate”) • Disease progression at 6 mos vs 2 - 3mos expected (“progression free survival”) • Time to death ~19mos vs 9 - 11mos expected (“median survival”) Source: Company R&D Day presentation, Slide 54, January 18, 2017 Early success of lead drug candidate is IMMU - 132 Additional indications with early promising data could materially add to the potential of the product

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 7 IMMU has a history of drug f ailures and value destruction AMGN licenses Epratuzumab Epratuzumab fails again Nycomed licenses Veltuzumab Veltuzumab fails UCB licenses Epratuzumab Epratuzumab fails for the first time Clivatuzumab fails ‘132 Ejected from ASCO (*): Based on closing price 11/15/16; day prior to venBio 13D filing (106M shares outstanding ) (**): SEC Filings (***): 1/1/00 – 11/15/16 Founded 1982 Market cap $294M* Accumulated deficit $389M** Drugs on market 0 CSO tenure 32 years CEO tenure 15 years Nasdaq Comp: +33% Nasdaq Biotech Index: +273% IMMU : - 65% ***

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” IMMUFPRXBPMCARRYSGENXNCRIMGNTSROCLVSMGNXCTMX Oncology aaaaaaaaaaa Antibody Engineering aa r r aaa r r aa Platform Technology aaa a aaa r r aa First in Class aaa r a r a r r r r Positive Results (Lead Program) a r r a r r r aa r r Breakthrough Designation (FDA) a r r r a r r r a r r Regulatory Clarity a r r a r r r aa r r Technology Clinical Progress 8 Despite the recent clinical success of IMMU - 132, the stock has significantly underperformed IMMU - 132 has enjoyed major clinical progress compared to peers … … yet IMMU’s stock continues to underperform** (*): CTMX IPO Oct 2015; BPMC IPO June 2015 (**): All returns calculated through 11/15/16, the day before we filed our proxy. This represents the company’s own independ ent efforts. 1 year 2 year 3 year IMMU -10% -27% -27% FPRX 71% 285% 500% BPMC 79% ARRY 64% 93% 23% SGEN 65% 101% 73% XNCR 110% 139% IMGN -82% -77% -85% TSRO 173% 337% 247% CLVS 18% -33% -30% MGNX -5% 34% 14% CTMX -10% Average (ex-IMMU) 48% 110% 106% Reference from 11/15/16 (*) Our peer group consists of small - and mid - cap biotechnology companies developing oncology drugs and possessing novel platform technologies

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 9 Management’s missteps directly contributed to this underperformance Source: Thestreet.com, Bloomberg.com, Firstwordpharma.com ASCO selects IMMU - 132 for press briefing pack Stock declined 62% by the end of June vs. pre - ejection share price ASCO ejects IMMU for violation of data embargo 6/3/16 IMMU s tock price surrounding ASCO conference 6/3/16 Key Takeaway Last night it was reported that IMMU and their anticipated 132 data in TNBC was removed from ASCO 2016. Later confirmed by the company, ASCO determined that the data had previously been presented at another conference (PEGS Boston), which was a violation of embargo policy. In our view, this is a function of stricter ASCO policies and pot'l poor mgmt decision, rather than a negative reflection on '132. 6/21/16 IMMU: Downgrading Rating To Market Perform We are downgrading our rating on shares of IMMU to Market Perform (from Outperform) and reducing our valuation range to $1.75 to $2.25 (from $8 - $9) following today’s news and a series of management missteps that have shaken our confidence in IMMU’s ability to create sustainable shareholder value

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 10 Management has failed to execute on main corporate goal: striking a pharma partnership to enable approval and advancement of ‘132 to market Source: Clinicaltrials.gov, C ompany reports & filings Earnings call transcripts Partnering Updates Development Updates Delays have hurt patients and destroyed stockholder value Company announces FDA grants SPA (Special Protocol Assessment) for phase 3 trial 12/’15 FY Q4‘16 earnings call: Plan to initiate phase 3 by the end of 2016 8/’16 8/’15 FY Q4’15 earnings call: Manufacturing preparations to complete by Jun 2016; Phase 3 to initiate thereafter FY Q1’17 earnings call: Believe first patient/first visit to occur (by/)in March ‘17 11/’16 Company will seek accelerated approval; requires Phase 3 to be underway at time of filings 6/’16 FY Q4‘16 earnings call: - Work with outside advisory group for partnering continues - “We already have term sheets” 4/’16 Sol Barer joins as special advisor to strengthen Company’s business and commercial development activities FY Q4’15 earnings call: IMMU not capable to take on phase 3 trial without a partner IMMU hires advisory firm, Greenhill & Co, to assist in its ongoing efforts to out - license IMMU - 132; Sol Barer steps down as advisor 10/’16 R&D Day: Phase 3 start in late Q1/early Q2 1/’17 TODAY • Still no partner • Insufficient funds to run Phase 3 trial • Ongoing delays in manufacturing and Phase 3 start Program Timelines at Risk

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 11 IMMU has been unable to retain independent & competent partners Richard L. Sherman DID NOT STAND FOR RE - ELECTION to the board at 2015 stockholders meeting Lasted 2 years 2 months Arthur Kirsch STEPPED DOWN from the board of directors Lasted 1 year 2 months Chief Medical Officer Dr. Francois Wilhelm RESIGNED Lasted 1 year 5 months Chief Financial Officer Peter Pfreundschuh RESIGNED Lasted 2 years 9 months Senior Advisor Dr. Sol Barer RESIGNED Lasted 2 months UCB TERMINATED licensing agreement with Immunomedics Bayer TERMINATED licensing agreement with Immunomedics 2017 2015 Mary Paetzold , Donald Stark RELPACED from the BoD in response to venBio contest Lasted 15 years and 11 years, respectively 2016 Long serving “Independent” board members jettisoned shortly after we filed our proxy Source: Company Filings

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 12 Source: Immunomedics R&D Day, slide 71,January 18 th , 2017 Our experts are skeptical of IMMU’s communicated manufacturing strategy and timelines IMMU cannot manufacture their product without world - class CMC (Chemistry , Manufacturing & Controls ) operating flawlessly, which they likely do not have Impossible to validate multi - component pharmaceutical products in parallel as this suggests Each component must be validated individually before any product can be evaluated Each site must coordinate across the globe before final assembly, complicating logistics even for most experienced teams Suggestion of multiple runs in parallel before a single one is validated i s ill - conceived Best case scenario, ready mid - 2Q17, making 2Q17 trial start unlikely Immunomedics Manufacturing Plan Communicated 1/18/2017 No details given on completed steps despite importance to overall plan Antibody manufacture in - house suggests scale - up/ out - sourcing challenges

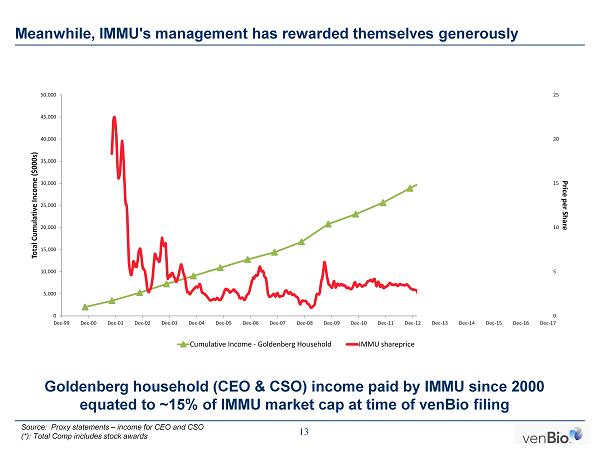

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 13 Meanwhile, IMMU's management has rewarded themselves generously Source: Proxy statements – income for CEO and CSO (*): Total Comp includes stock awards Goldenberg household (CEO & CSO) income paid by IMMU since 2000 equated to ~15% of IMMU market cap at time of venBio filing 0 5 10 15 20 25 0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000 Dec-99 Dec-00 Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17 Price per Share Total Cumulative Income ($000s) Cumulative Income - Goldenberg Household IMMU shareprice

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” • Additional salary from IBC, a wholly owned subsidiary • 20%+ royalty on partnership fee 14 The founder/ CSO also benefits from extraordinary self - enrichment arrangements David Goldenberg, CSO, Additional Compensation • 0.75% of 3 rd party transaction $ • 1.5 % of annual net revenue* • $150k/ yr minimum payment as credit against special incentive programs** Source: IMMU proxy statement (*): in years with positive income (**): in years when company posts no profit Product royalties Partnership royalties Additional Salaries

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 15 … Including ownership in IMMU’s IBC subsidiary that enriches him over IMMU stockholders … while he owns 18.3% of IBC vs. 6.8% of IMMU Source: IMMU proxy statement, R&D Day slides David Goldenberg decides IMMU product ownership rights … Certain members of our senior management and Board of Directors have relationships and agreements, both with us as well as among themselves and their respective affiliates, which create the potential for both real, as well as perceived, conflicts of interest. These include Dr. David M. Goldenberg, our Chairman, Chief Scientific Officer, and Chief Patent Officer, Ms. Cynthia L. Sullivan, our President and Chief Executive Officer (who is also the wife of Dr. Goldenberg) , and certain companies with which we do business, including the Center for Molecular Medicine and Immunology and the Garden State Cancer Center (which operated as the clinical arm of CMMI to facilitate the translation of CMMI’s research efforts in the treatment of patients), collectively defined as CMMI. For example, Dr. Goldenberg was the President and a Trustee of CMMI, a not - for - profit cancer research center that we used to conduct certain research activities. CMMI has ceased operations. Dr. Goldenberg is also a minority stockholder, director and officer of our majority - owned subsidiary, IBC Pharmaceuticals, Inc. Dr. Goldenberg is the primary inventor of new intellectual property for Immunomedics and IBC and is largely responsible for allocating ownership between the two companies . Dr. Goldenberg also has primary responsibility for monitoring the market for incidences of potential infringement of the Company’s intellectual property by third parties. As of June 30, 2016, the shares of IBC were held as follows: Stockholder Holdings % of Tot Immunomedics , Inc. 5.6M shrs Ser A pref 73.5% Third Party Investors 0.6M shrs Ser B pref 8.2% Goldenberg Mill. Trust 1.4M shrs Ser C pref 18.3% • 143 FTEs; 54 MD/PhD/other advanced degrees • funded by IMMU shareholders • UNUSUAL for Goldenberg to be named “PRIMARY INVENTOR OF ALL INTELLECTUAL PROPERTY” Goldenberg has perverse incentives in allotting ownership of new inventions

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 16 Management sells shares ahead of a dilutive financing; dilution that failed to raise the cash needed to fund the required phase 3 study Between 6/6 and 6/13, David and Cynthia Goldenberg sold 1,006,832 options, with strike prices of $2.50 & $2.63 Source: Nasdaq, Company's SEC filings IMMU stock price Jun - Nov 2016 $30M raise equates to <2 quarters of runway based on most recent burn rate June 6 - 13 insider selling Goldenberg/Sullivan sell >1M shares average price $3.63 ($4.27 - $3.02) October 5, 2016 Financing Terms: $3/share; 100% warrants Close 10/4: $3.28 Close 10/5: $2.50 ( 1 - day decline of 24% )

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” IMMU’s response to venBio filing: a newly appointed equally unqualified and self - serving BoD 17

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 18 In response to our proxy filing, IMMU reconstituted its board with a closely linked group that is affiliated with the IMMU board and banker IMMU Board of Directors as of 1/9/2017 David Goldenberg, CSO Cynthia Sullivan, CEO Brian Markinson 12 - years on the board Jason Aryeh Robert Forrester Geoffrey Cox Bob Oliver New IMMU Board announced January 12 th , 2017 MULTIPLE CURRENT & PRIOR BUSINESS RELATIONSHIPS

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 19 Jason Aryeh Geoffrey Cox Robert Forrester David Goldenberg Brian A. Markison Cynthia Sullivan Husband and Wife Appointed CEO Hired as Financial Advisor Banking Relationships The newly appointed IMMU board is highly inter - connected with multiple current and past relationships with Aryeh at the center (*): Aryeh and Markison directly negotiated a transaction involving Avinza in 2006 per ( https://goo.gl/9YXOr8 )

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 20 QLT: Case study of Aryeh’s failed chairmanship • Phase - 3 ready ophthalmology compound (1) QLT press release 11/20/13 (2) Auxilium acquired by Endo; Insite Vision acquired by Sun Pharma (3) QLT press release 6/08/15 and 2/05/16 (4) Aralez webpage (5) SEC Filings (6) QLT press release 2/21/16 (7) QLT press release 11/29/16 • Still awaiting trial start despite 11/20/13 statement that: ‘close to finalizing a pivotal trial protocol ’ (1) • Proposed 2 inversions • Company failed to close on either (2) • Acquired shares in Aralez Pharma • Initially proposed investment at $7.20/ Aralez share; lowered to $ 6.25 (3) • Currently trading at $ 4.25 • “Optimize the allocation of QLT’s excess cash” yet concurrently proposed $20M equity financing • Became Aralez board member at close (2/5/16) (4) • Lost confidence of significant QLT shareholders who exited (5) • Distributed Aralez Shares • Cash election over - subscribed • QLT Shareholders received Aralez shares against their will (6) • Proposed Merger • Aegerion merger closed 11/29/16 (7) • PPS down ~50% since Aryeh became chairma n IMMU does NOT NEED a chairman with the credentials of Aryeh X X X - 30% - 50% Aryeh Appointed Chairman of QLT mid - 2012

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 21 As a board member, Jason Aryeh has overseen value destruction and underperformance Source: SEC filings, Bloomberg Ligand, Myrexis relative performance vs. IBB from Aryeh joining BoD to end of tenure/current (*) Ligand assumed that special dividend is reinvested in security Jason Aryeh joins BoD PPS under - performed by ~ 90 % PPS down ~50 % PPS under - performed by ~50 %* PPS down ~ 90%

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 22 Geoffrey Cox has NOT had successful development experience since 1997 Cox disappointing leadership PPS DOWN 51% 2010 - Present 1984 - 1997 2001 - 2010 1997 - 2001 Declining Pharmaceutical development relevance … Beacon Street Advisors, LLC Cox manufacturing experience is irrelevant Source: Bloomberg

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 23 Robert Forrester has failed in the C - suite Forrester appointed CEO Lead drug fails PPS DOWN ~90 % $100 $80 $60 $40 $20 $0 $120 $140 CombinatoRx Nasdaq NBI PPS DOWN ~90% 112/06 12/07 12/08 12/09 11/05 - 12/05 Lead drug fails again Lead drug fails CEO of Verastem (2012 - present) COO of CombinatorX (2005 - 2009) Source: Verastem Bloomberg; CombinatorX SEC 10k

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 24 Geoffrey Cox Robert Forrester David Goldenberg Brian A. Markinson Cynthia Sullivan Husband and Wife Yet they always get paid: e.g., Jason Aryeh … “Chairman Package” Jason Aryeh IMMU does NOT NEED ANOTHER board with these credentials

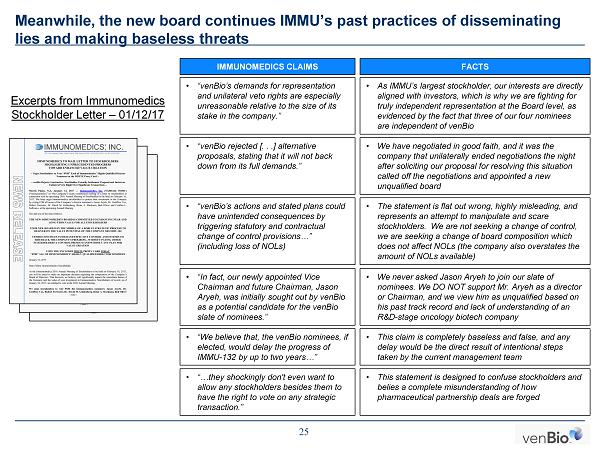

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 25 Meanwhile, the new board continues IMMU’s past practices of disseminating lies and making baseless threats • “ venBio’s demands for representation and unilateral veto rights are especially unreasonable relative to the size of its stake in the company .” • “ venBio’s actions and stated plans could have unintended consequences by triggering statutory and contractual change of control provisions…” (including loss of NOLs) • “ We believe that, the venBio nominees, if elected, would delay the progress of IMMU - 132 by up to two years…” • “ venBio rejected [. . .] alternative proposals, stating that it will not back down from its full demands .” • “ In fact, our newly appointed Vice Chairman and future Chairman, Jason Aryeh , was initially sought out by venBio as a potential candidate for the venBio slate of nominees.” • “… they shockingly don't even want to allow any stockholders besides them to have the right to vote on any strategic transaction.” • As IMMU’s largest stockholder, our interests are directly aligned with investors, which is why we are fighting for truly independent representation at the Board level, as evidenced by the fact that three of our four nominees are independent of venBio • The statement is flat out wrong , highly misleading, and represents an attempt to manipulate and scare stockholders. We are not seeking a change of control, we are seeking a change of board composition which does not affect NOLs (the company also overstates the amount of NOLs available) • This claim is completely baseless and false, and any delay would be the direct result of intentional steps taken by the current management team • We have negotiated in good faith, and it was the company that unilaterally ended negotiations the night after soliciting our proposal for resolving this situation called off the negotiations and appointed a new unqualified board • We never asked Jason Aryeh to join our slate of nominees. We DO NOT support Mr. Aryeh as a director or Chairman, and we view him as unqualified based on his past track record and lack of understanding of an R&D - stage oncology biotech company • This statement is designed to confuse stockholders and belies a complete misunderstanding of how pharmaceutical partnership deals are forged IMMUNOMEDICS CLAIMS FACTS Excerpts from Immunomedics Stockholder Letter – 01/12/17

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” venBio’s proposed plan and board expertise 26

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 27 There is a short window for value creation and the right team is needed – the market has responded favorably to venBio’s proposal • Critical path involves securing Accelerated Approval (AA) • IMMU’s capabilities remain unproven in key areas, posing risks to timelines – No prior experience assembling a drug application – Never manufactured a complex biologic therapeutic at commercial sale – Co - development agreement has yet to materialize – Unable to launch a global phase 3 program • High cash burn - rate with few financing options – Insufficient cash to complete manufacturing, or run phase 3 trial – High emphasis on early - stage research, despite lack of visibility to funding – Low credibility with Wall Street to raise additional funding – Excessive management compensation Source: SEC filings; Nasdaq Path to Value Creation Market reaction to venBio Filing 11/16/16 venBio 13D filing

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 28 • Identify key IMMU personnel and ensure continuity – develop working relationship with management • Bring in as needed additional resources and expertise to ensure smooth transition • Understand key open items – Manufacturing – Clinical – Regulatory submission Our nominees are prepared to assume oversight immediately and maintain momentum while driving to a clear vision for the future of IMMU • Evaluate strategic options to advance ‘132 as rapidly as possible – Secure funding – Secure partnerships – Establish manufacturing relationships • Implement CEO succession plan – Profile subject to outcome of strategic review Internally Oriented Activities Externally Oriented Activities Strategic Direction to Maximize Stockholder Value

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” a a a a a a a a a a a a a a a a 29 Our Board Nominees and Advisors provide the necessary expertise to position the company for long - term value creation • Behzad Aghazadeh, PhD – Biotech / Capital Markets Expertise – Portfolio Manager & Managing Partner, venBio Select Advisor – Formerly Principal Booz Allen (general management consultant/healthcare) • Scott Canute – Manufacturing Expertise – Former President, Global Manufacturing and Corporate Operations, Genzyme – Former President, Global Manufacturing Operations , Eli Lilly • Peter Barton Hutt – Regulatory Expertise – Senior Counsel; Covington & Burling LLP – Former FDA Chief Counsel • Khalid Islam, PhD – Clinical/Corporate Governance Expertise – Co - Founder and Partner Sirius Healthcare Partners; Founder/Owner Life Sciences Management; Founder PrevABR – Former CEO Gentium (acquired by Jazz Pharmaceuticals) • Richard Heyman , PhD – Clinical/Corp Governance/Strategic Advisor – CEO Seragon Pharma (acquired by Roche /Genentech) – C EO Aragon Pharma (acquired by Johnson & Johnson) – Executive Chairman, Metacrine – Former Receptos BoD (acquired by Celgene) Additional strong advisory network that can be drawn upon a a a a a

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 30 We have a defined plan with clear objectives … Function Objective Governance • Restore independent & competent governance • Serve fiduciary responsibility to stockholders • Rebuild confidence & credibility with stakeholders Strategy • Evaluate strategic options for IMMU - 132 development • Asset and capability evaluation & prioritization • Resource allocation & portfolio optimization Organization / Talent • Evaluate and identify key talent to focus on IMMU - 132 • Highlight and fill key talent & capability gaps • Put in place high - touch reporting to BoD Operations • Evaluate key operating processes – clinical, manufacturing, regulatory, commercial, etc. • Put in place best - in - class, scalable, & efficient processes Finance • Audit and evaluate finances, budgets, & resource allocation • Evaluate financing needs and options • Determine new budget & resource allocation

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 31 … and identified key steps to maximize the potential for IMMU - 132 Organizational GAP analysis Audit Finances Clinical Development Plan and Detailed Budget Decision to partner or go - it - alone New corporate communication plan Characterize key processes Validate process repeatability GMP performance Pre - approval inspection readiness Governance systems Review FDA interactions Identify FDA counterpart Validate accelerated approval pathway Plan additional indication pathway Internal regulatory affairs NDA Submission Plan Clinical/Organizational – Khalid Islam/ Behzad Aghazadeh & Advisory Network Manufacturing/CMC – Scott Canute Regulatory – Peter Barton Hutt

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” Appendix 32

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 33 Appendix: Board Nominee Bio – Behzad Aghazadeh, PhD Dr. Behzad Aghazadeh – Dr. Aghazadeh is a Managing Partner and Portfolio Manager of the venBio Select Fund. He brings more than 20 years of experience in the biopharmaceutical industry, including more than 10 years as an institutional investor and previously six years at Booz Allen as a general management consultant to senior executive teams in the healthcare sector. Dr. Aghazadeh holds a Master’s in Physics from the Ludwig - Maximilians - University (Munich, Germany) and a PhD in Biochemistry & Biophysics from Cornell University. We believe that Dr. Aghazadeh’s extensive experience working on strategic initiatives for executive management teams and boards of directors of numerous companies in the biopharmaceutical industry, as well as his considerable experience as an investor in emerging companies in the sector, make him well - qualified to serve as a director of Immunomedics .

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 34 Appendix: Independent Board Nominee Bio – Khalid Islam, PhD Dr. Khalid Islam – Dr. Islam has over 29 years of experience in the pharmaceutical and biotechnology industry and currently serves as the Managing Director of Life Sciences Management GmbH. He also co - founded Sirius Healthcare Partners, a Swiss life sciences company, and PrevABR LLC, an American clinical - stage therapeutics company. Dr. Islam also previously served as Chairman and CEO of Gentium S.p.A., a Nasdaq - listed pharmaceutical company. Dr. Islam graduated from Chelsea College and received his PhD from Imperial College, University of London. In our view, Dr. Islam’s extraordinary board experience, deep knowledge of business development and collaboration, and outstanding leadership position him well to be a Board member at Immunomedics .

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 35 Appendix: Independent Board Nominee Bio – Peter Barton Hutt Peter Barton Hutt – Mr. Hutt is a renowned expert in food and drug law and currently serves as Senior Counsel at Covington & Burling LLP. He began his law practice with the firm in 1960 and has remained at the firm with the exception of serving as Chief Counsel for the Food and Drug Administration from 1971 until 1975. He has been recognized by The Washingtonian magazine as one of Washington’s 50 best lawyers and one of the 40 best health care lawyers in the U.S. by the National Law Journal. He holds a B.A. from Yale University, an LL.B. from Harvard Law School, and an LL.M. from the New York University School of Law. We believe that Mr. Hutt’s expertise in the US and EU regulatory frameworks including successful interactions with both the FDA and the EMA as well as his service on a wide range of Boards of Directors in the biotechnology and pharmaceutical industries, make him very well qualified for the Board of Immunomedics .

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 36 Appendix: Independent Board Nominee Bio – Scott Canute Scott Canute – Mr. Canute has more than 34 years of experience in the biopharmaceutical industry, having served as President, Global Manufacturing and Corporate Operations at Genzyme Corporation and previously as President of Global Manufacturing Operations at Eli Lilly and Company. He holds a B.S. in chemical engineering from the University of Michigan and an M.B.A. from Harvard Business School. Mr. Canute’s specific expertise in the area of commercial biologics manufacturing and CMC as well as his extensive Board experience with multiple pharmaceutical companies, make him well qualified to serve on the Board of Immunomedics , in our view.

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 37 Appendix: Independent Advisor Bio – Richard Heyman, PhD Dr. Richard Heyman – Dr. Heyman possesses extensive relevant experience, having served as the co - founder and Chief Executive Officer of Aragon Pharmaceuticals, which focused on androgen receptor signaling inhibitors for the treatment of prostate cancer and was acquired by Johnson & Johnson in 2013, and Seragon Pharmaceuticals, which focused on Selective Estrogen Receptor Degraders (SERDs) for the treatment of breast cancer and was acquired by Genentech in 2014. Dr. Heyman received a Ph.D. in pharmacology from the University of Minnesota and a B.S. in chemistry from the University of Connecticut.

1 2 7 3 10 6 4 5 8 9 Line Graph Color Scheme 1 2 7 3 10 6 4 5 8 9 Source: Calibri Font Size: 8 Right Alignment Horizontal: 3” Vertical: 7” Footnote: Calibri Font Size: 8 Left Alignment Horizontal: 2’” Vertical: 7” 38 Disclosures Performance Disclosures Unless otherwise indicated, the performance shown is unaudited, net of applicable management, performance and other fees, and ex penses, presumes reinvestment of earnings and excludes investor specific sales and other charges. Please refer to the Fund’s Offering Documents for more information regar din g the Fund’s fees, charges and expenses, which will reduce the Fund’s gains. Performance may vary substantially from year to year or even from month to month. An investor’s actual pe rfo rmance and actual fees may differ from the performance information shown due to, among other factors, capital contributions and withdrawals/redemptions, different share classes and el igibility to participate in “new issues.” The value of investments can go down as well as up. Certain share classes of the Fund may be closed, including the share class from which th e performance shown has been derived. Past performance is not indicative of future results. Benchmarks and financial indices are shown for illustrative purposes only and are provided for the purpose of making general mar ket data available as a point of reference only. Information related to indices and benchmarks, has been provided by and/or is based on third party sources and, although believed to be r eli able, has not been independently verified. Such benchmarks and financial indices may not be available for direct investment, may be unmanaged, assume reinvestment of income, do not ref lec t the impact of any trading commissions and costs, management or performance fees, and have limitations when used for comparison or other purposes because they, among other rea son s, may have different trading strategy, volatility, credit, or other material characteristics (such as limitations on the number and types of securities or instruments). The Fu nd’ s investment objective is not restricted to the securities and instruments comprising any one index. No representation is made that any benchmark or index is an appropriate measure for co mpa rison. Performance targets or objectives should not be relied upon as an indication of actual or projected future performance. Actu al volatility and returns will depend on a variety of factors including overall market conditions and the ability of the Investment Manager to implement the Fund’s investment process, inv est ment objectives and risk management. No representation is made that these targets or objectives will be achieved, in whole or on part, by the Fund. This information is confidential, is the property of the Investment Manager and is intended only for intended recipients and the ir authorized agents and representatives and may not be reproduced or distributed to any other person without prior written consent. Any distribution to social media is a willful vi ola tion of the confidential and regulatory strictures that govern this document. Hedge Fund Risk Disclosures Hedge Funds are unregistered private investment partnerships, funds or pools that may invest and trade in many different mark ets , strategies and instruments (including securities, non - securities and derivatives) and are NOT subject to the same regulatory requirements as mutual funds, including mutual fund re qui rements to provide certain periodic and standardized pricing and valuation information to investors. There are substantial risks in investing in Hedge Funds. You should note ca ref ully the following: Hedge Funds represent speculative investments and involve a high degree of risk. An investor could lose all or a substantial portion of his/her investment. I nve stors must have the financial ability, sophistication/experience and willingness to bear the risks of an investment in a Hedge Fund. An investment in a Hedge Fund should be discretionary cap ita l set aside strictly for speculative purposes. An investment in a Hedge Fund is not suitable or desirable for all investors. Only qualified eligible investors may invest in Hedge Funds. He dge Fund offering documents are not reviewed or approved by federal or state regulators. Hedge Funds may be leveraged (including highly leveraged) and a Hedge Fund’s performance may be vol atile. An investment in a Hedge Fund may be illiquid and there may be significant restrictions on transferring interests in a Hedge Fund. There is no secondary market for an inv est or’s investment in a Hedge Fund and none is expected to develop. A Hedge Fund may use a single advisor or employ a single strategy, which could mean a lack of diversification and hi ghe r risk. A Hedge Fund may involve a complex tax structure, which should be reviewed carefully, and may involve structures or strategies that may cause delays in important tax informati on being sent to investors. A Hedge Fund’s fees and expenses – which may be substantial regardless of any positive return – will offset the Hedge Fund’s trading profits. Hedge Funds are not required to provide periodic pricing or valuation information to investors. Hedge Funds and their managers/advisors may be subject to various conflicts of interest. The above summary is not a complete list of the risks and other important disclosures involved in investing in a Hedge Fund and is subject to the more complete disclosures contained in a Hedge Fund’s co nfidential offering documents, which must be reviewed carefully.