SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

For the month of | August | 2015 | |

Commission File Number | 001-37410 | ||

ESSA Pharma Inc. | |||

| (Translation of registrant’s name into English) | |||

Suite 720, 999 West Broadway, Vancouver, British Columbia, Canada, V5Z 1K5 | |||

| (Address of principal executive offices) | |||

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F | X | Form 40-F |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

DOCUMENTS INCLUDED AS PART OF THIS REPORT

| Document | |

| 1 | ESSA Pharma Inc. Reports Third Quarter 2015 Financial Results |

| 2 | ESSA Pharma Inc. Third Quarter 2015 Financial Results |

| 3 | ESSA Pharma Inc. Third Quarter 2015 Management Discussion and Analysis |

DOCUMENT 1

ESSA PHARMA INC. REPORTS THIRD QUARTER 2015 FINANCIAL RESULTS

Vancouver, Canada, and Houston, Texas, August 17, 2015 - ESSA Pharma Inc. (”ESSA” or the “Company”) (TSX: EPI, NASDAQ: EPIX) today reported financial results for the third quarter and three months ended June 30, 2015. Amounts, unless specified otherwise, are expressed in Canadian dollars and in accordance with International Financial Reporting Standards (“IFRS”).

Summary Results

ESSA recorded a net loss of $6.2 million ($0.35 per common share) for the quarter ended June 30, 2015 (Q3-2015), compared to a net loss of $1.0 million ($0.07 per common share) for the quarter ended June 30, 2014 (Q3-2014).

Research and Development (“R&D”) expenditures for Q3-2015 were $3.1 million compared to $0.7 million for Q3-2014. The increase was primarily due to increased R&D activity related to preclinical work on the clinical candidate EPI-506 in support of the Investigational New Drug application (the “IND”) to the U.S. Food and Drug Administration.

General and administration expenditures for Q3-2015 were $1.2 million compared to $0.3 million for Q3-2014. The increase was primarily due to increased activity as a corporate entity as the Company successfully completed a listing on the TSX Venture Exchange in January 2015, and a filing of a registration statement on Form 20-F with the United States Securities and Exchange Commission in July 2015 and a listing on the Nasdaq Capital Market (the “Nasdaq”) in July 2015.

Liquidity and Outstanding Share Capital

At June 30, 2015, ESSA had cash and cash equivalents of $7.7 million which included net proceeds of $14.2 million from the issuance of special warrants of the Company in January 2015 (the “2015 Special Warrants”). Working capital as at June 30, 2015 was $8.0 million, which the Company believes is sufficient, together with the anticipated CPRIT advance of US$3.7 million to be received upon clearance of the IND in the fourth fiscal quarter of 2015, to finance operational and capital needs for the following six months.

As of June 30, 2015, the company had 18,332,536 common shares issued and outstanding, 4,283,634 special warrants (“2015 Special Warrants”), 1,768,550 common shares issuable upon the exercise of outstanding stock options at a weighted-average exercise price of $1.33 per share, and 285,590 common shares issuable upon the exercise of outstanding warrants at a weighted-average exercise price of $3.29 per share.

As a result of the Company’s listing on the Nasdaq on July 9, 2015, the 2015 Special Warrants were exercised, without payment of any additional consideration, on July 10, 2015.

Change in Escrow Release Schedule

The Company also announced that as a result of the Company’s listing on the Toronto Stock Exchange in July, 2015, ESSA became an “established issuer” pursuant to the terms of an escrow agreement entered into with Computershare Investor Services Inc. on January 20, 2015 (the “Escrow Agreement”). The Escrow Agreement provides for an early release of ESSA common shares subject to escrow (the “Escrow Shares”) upon the company becoming an “established issuer”, with the following release schedule: ¼ of Escrow Shares released on the original listing date on a Canadian exchange, ¼ released six months after the listing date, ¼ released 12 months after the listing date and the final ¼ released 18 months after the listing date. Pursuant to the new release schedule, 281,256 Escrow Shares are to be released from escrow for the first release date under the new release schedule, being the release which is to occur on the date that is six months from the date the Company listed on the TSX Venture Exchange. The Escrow Shares remain subject to the terms of the Escrow Agreement.

Contact Information:

David Wood

Chief Financial Officer, ESSA Pharma Inc.

T: 778-331-0962

E: dwood@essapharmaceuticals.com

About ESSA Pharma Inc.

ESSA Pharma is a development-stage pharmaceutical company focused on developing novel and proprietary therapies for the treatment of castration resistant prostate cancer (“CRPC”) in patients whose disease is progressing despite treatment with current therapies. ESSA believes that its product candidate, EPI-506, can significantly expand the interval of time in which patients suffering from CRPC can benefit from hormone-based therapies. Specifically, EPI-506 acts by disrupting the androgen receptor (“AR”) signaling pathway, which is the primary pathway that drives prostate cancer growth. We have shown that EPI-002, the primary metabolite of EPI-506, prevents AR activation by binding selectively to the N-terminal domain (“NTD”) of the AR. A functional NTD is essential for activation of the AR. Blocking the NTD prevents activation of the AR by all of the three known mechanisms of activation. In pre-clinical studies, blocking the NTD has demonstrated the capability to overcome the known AR-dependent mechanisms of CRPC. ESSA was founded in 2009 and is headquartered in Vancouver, British Columbia, Canada.

About Prostate Cancer

Prostate cancer is the second-most commonly diagnosed cancer among men and the fifth most common cause of male cancer death worldwide (Globocan, 2012). Adenocarcinoma of the prostate is dependent on androgen for tumour progression and depleting or blocking androgen action has been a mainstay of hormonal treatment for over six decades. Although tumours are often initially sensitive to medical or surgical therapies that decrease levels of testosterone (for example, ADT), disease progression despite castrate levels of testosterone generally represents a transition to the lethal variant of the disease (mCRPC) and most patients ultimately succumb to the illness. The treatment of mCRPC patients has evolved rapidly over the past five years; despite these advances, additional treatment options are needed to improve clinical outcomes in patients, particularly those who fail existing treatments including abiraterone or enzalutamide, or those that have contraindications to receive those drugs. Over time, patients with mCRPC generally experience continued disease progression, worsening pain, leading to substantial morbidity and limited survival rates. In both in vitro and in vivo studies, ESSA's novel approach to blocking the androgen pathway has been shown to be effective in blocking tumour growth when current therapies are no longer effective.

Forward-Looking Statement Disclaimer

This release contains certain information which, as presented, constitutes "forward-looking information" within the meaning of applicable Canadian securities laws. Forward-looking information involves statements that relate to future events and often addresses expected future business and financial performance, containing words such as "anticipate", "believe", "plan", "estimate", "expect", and "intend", statements that an action or event "may", "might", "could", "should", or "will" be taken or occur, or other similar expressions and includes, but is not limited to, statements about the implementation of the Company’s business model and strategic plans.

Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of ESSA to control or predict, and which may cause ESSA’s actual results, performance or achievements to be materially different from those expressed or implied thereby. Such statements reflect ESSA’s current views with respect to future events, are subject to risks and uncertainties and are necessarily based upon a number of estimates and assumptions that, while considered reasonable by ESSA as of the date of such statements, are inherently subject to

significant medical, scientific, business, economic, competitive, political and social uncertainties and contingencies. In making forward looking statements, ESSA may make various material assumptions, including but not limited to (i) obtaining positive results of clinical trials; (ii) obtaining regulatory approvals; and (iii) general business, market and economic conditions.

Forward-looking information is developed based on assumptions about such risks, uncertainties and other factors set out herein and in ESSA’s prospectus dated December 5, 2014 under the heading “Risk Factors”, a copy of which is available on ESSA’s profile at the SEDAR website at www.sedar.com, and as otherwise disclosed from time to time on ESSA’s SEDAR profile. Forward-looking statements are made based on management's beliefs, estimates and opinions on the date that statements are made and ESSA undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change, except as may be required by applicable Canadian securities laws. Readers are cautioned against attributing undue certainty to forward-looking statements.

DOCUMENT 2

CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS

(Unaudited)

(Expressed in Canadian dollars)

FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014

ESSA PHARMA INC.

CONDENSED CONSOLIDATED INTERIM STATEMENTS OF FINANCIAL POSITION

(Unaudited)

(Expressed in Canadian dollars)

AS AT

June 30, 2015 | September 30, 2014 | |||||||

| ASSETS | ||||||||

| Current | ||||||||

Cash | $ | 7,739,769 | $ | 4,146,938 | ||||

Receivables | 47,231 | 72,295 | ||||||

Prepaids (Note 4) | 1,351,434 | 69,946 | ||||||

| 9,138,434 | 4,289,179 | |||||||

Equipment (Note 5) | 149,119 | 15,806 | ||||||

Intangible assets (Note 6) | 385,437 | 404,430 | ||||||

| Total assets | $ | 9,672,990 | $ | 4,709,415 | ||||

| LIABILITIES AND SHAREHOLDERS' EQUITY | ||||||||

| Current | ||||||||

Accounts payable and accrued liabilities | $ | 1,432,206 | $ | 658,305 | ||||

Derivative liability (Note 8) | 2,796,853 | - | ||||||

Product development and relocation grant (Note 16) | - | 1,838,507 | ||||||

| 4,229,059 | 2,496,812 | |||||||

| Shareholders' equity | ||||||||

Share capital (Note 9) | 9,165,328 | 4,240,917 | ||||||

Preferred shares (Note 9) | - | 3,090,345 | ||||||

Special warrants (Note 9) | 12,763,885 | - | ||||||

Reserves (Note 10) | 1,999,698 | 1,004,467 | ||||||

Accumulated other comprehensive income (loss) | (152,705 | ) | 6,477 | |||||

Deficit | (18,332,275 | ) | (6,129,603 | ) | ||||

| 5,443,931 | 2,212,603 | |||||||

| Total liabilities and shareholders’ equity | $ | 9,672,990 | $ | 4,709,415 | ||||

| On behalf of the Board on August 14, 2015 | ||||||

| “Robert Rieder” | Director | “Franklin Berger” | Director | |||

The accompanying notes are an integral part of these condensed consolidated interim financial statements.

ESSA PHARMA INC.

CONDENSED CONSOLIDATED INTERIM STATEMENTS OF LOSS AND COMPREHENSIVE LOSS

(Unaudited)

(Expressed in Canadian dollars)

Three months ended June 30, 2015 | Three months ended June 30, 2014 | Nine months ended June 30, 2015 | Nine months ended June 30, 2014 | |||||||||||||

| OPERATING EXPENSES | ||||||||||||||||

Research and development, net of recoveries (Note 17) | $ | 3,108,000 | $ | 653,681 | $ | 6,950,487 | $ | 832,685 | ||||||||

Financing costs | 72,748 | 51,938 | 126,021 | 60,896 | ||||||||||||

General and administration, net of recoveries (Note 17) | 1,219,442 | 335,308 | 3,631,102 | 541,061 | ||||||||||||

| Total operating expenses | (4,400,190 | ) | (1,040,927 | ) | (10,707,610 | ) | (1,434,642 | ) | ||||||||

Foreign exchange | (257,941 | ) | (6,142 | ) | 971,362 | (11,465 | ) | |||||||||

Interest income | 185 | - | 185 | 227 | ||||||||||||

Loss on derivative liability (Note 8) | (1,685,743 | ) | - | (2,466,609 | ) | - | ||||||||||

| Net loss for the period | (6,343,689 | ) | (1,047,069 | ) | (12,202,672 | ) | (1,445,880 | ) | ||||||||

| OTHER COMPREHENSIVE INCOME (LOSS) | ||||||||||||||||

Cumulative translation adjustment | 140,773 | 77 | (159,182 | ) | 77 | |||||||||||

| Comprehensive loss for the period | $ | (6,202,916 | ) | $ | (1,046,992 | ) | $ | (12,361,854 | ) | $ | (1,445,803 | ) | ||||

| Basic and diluted loss per common share | $ | (0.35 | ) | $ | (0.07 | ) | $ | (0.71 | ) | $ | (0.09 | ) | ||||

Weighted average number of common sharesoutstanding | 18,163,071 | 15,687,534 | 17,070,193 | 15,687,534 | ||||||||||||

The accompanying notes are an integral part of these condensed consolidated interim financial statements.

| ESSA PHARMA INC. |

| CONDENSED CONSOLIDATED INTERIM STATEMENTS OF CASH FLOWS |

| (Unaudited) |

| (Expressed in Canadian dollars) |

| FOR THE NINE MONTHS ENDED JUNE 30, |

| 2015 | 2014 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES | ||||||||

Loss for the period | $ | (12,202,672 | ) | $ | (1,445,880 | ) | ||

Items not affecting cash: | ||||||||

Accrued interest expense | - | 24,986 | ||||||

Amortization | 28,604 | 18,993 | ||||||

Loss on derivative liability | 2,466,609 | - | ||||||

Product development and relocation grant | (1,894,263 | ) | - | |||||

Unrealized foreign exchange | 704,136 | - | ||||||

Share-based payments (Note 10) | 1,070,889 | 170,062 | ||||||

Changes in non-cash working capital items: | ||||||||

Receivables | 25,064 | (14,104 | ) | |||||

Prepaid expenses | (1,229,392 | ) | (1,260 | ) | ||||

Accounts payable and accrued liabilities | 784,267 | 363,220 | ||||||

Net cash used in operating activities | (10,246,758 | ) | (883,983 | ) | ||||

| CASH FLOWS FROM INVESTING ACTIVITIES | ||||||||

Acquisition of equipment | (136,178 | ) | - | |||||

Net cash used in investing activities | (136,178 | ) | - | |||||

| CASH FLOWS FROM FINANCING ACTIVITIES | ||||||||

Proceeds on private placement | 15,574,435 | - | ||||||

Issuance costs | (1,022,035 | ) | - | |||||

Convertible debenture issued | - | 1,000,000 | ||||||

Financing costs | - | (23,541 | ) | |||||

Options exercised | 96,760 | - | ||||||

Warrants exercised | 203,377 | - | ||||||

Net cash provided by financing activities | 14,852,537 | 976,459 | ||||||

| Effect of foreign exchange on cash | (876,770 | ) | - | |||||

| Change in cash for the period | 3,592,831 | 92,476 | ||||||

| Cash, beginning of period | 4,146,938 | 232,093 | ||||||

| Cash, end of period | $ | 7,739,769 | $ | 324,569 | ||||

Supplemental Cash Flow Information (Note 11)

The accompanying notes are an integral part of these condensed consolidated interim financial statements.

ESSA PHARMA INC.

CONDENSED CONSOLIDATED INTERIM STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY

(Unaudited)

(Expressed in Canadian dollars)

| Reserves | ||||||||||||||||||||||||||||||||||||

| Share capital | Preferred shares | Special warrants | Convertible debenture | Share-based payments | Warrants | Cumulative translation adjustment | Deficit | Total | ||||||||||||||||||||||||||||

| Balance, September 30, 2013 | $ | 4,240,917 | $ | - | $ | - | $ | - | $ | 419,991 | $ | - | $ | - | $ | (4,168,097 | ) | $ | 492,811 | |||||||||||||||||

Issuance of convertible debenture | - | - | - | 1,000,000 | - | - | - | - | 1,000,000 | |||||||||||||||||||||||||||

Financing costs – issuance | - | - | - | (39,935 | ) | - | 16,394 | - | - | (23,541 | ) | |||||||||||||||||||||||||

Financing costs | - | - | - | 24,986 | - | - | - | - | 24,986 | |||||||||||||||||||||||||||

Share-based payments | - | - | - | - | 170,062 | - | - | - | 170,062 | |||||||||||||||||||||||||||

Loss for the period | - | - | - | - | - | - | 77 | (1,445,880 | ) | (1,445,803 | ) | |||||||||||||||||||||||||

| Balance, June 30, 2014 | $ | 4,240,917 | $ | - | $ | - | $ | 985,051 | $ | 590,053 | $ | 16,394 | $ | 77 | $ | (5,613,977 | ) | $ | 218,515 | |||||||||||||||||

Financing costs | - | - | - | 10,014 | - | - | - | - | 10,014 | |||||||||||||||||||||||||||

Conversion of debenture | - | 995,065 | - | (995,065 | ) | - | - | - | - | - | ||||||||||||||||||||||||||

Private placement (Note 9(c)) | - | 2,370,800 | - | - | - | - | - | - | 2,370,800 | |||||||||||||||||||||||||||

Share issue costs | - | (275,520 | ) | - | - | - | 50,004 | - | - | (225,516 | ) | |||||||||||||||||||||||||

Share-based payments | - | - | - | - | 348,016 | - | - | - | 348,016 | |||||||||||||||||||||||||||

Loss for the period | - | - | - | - | - | - | 6,400 | (515,626 | ) | (509,226 | ) | |||||||||||||||||||||||||

| Balance, September 30, 2014 | $ | 4,240,917 | $ | 3,090,345 | $ | - | $ | - | $ | 938,069 | $ | 66,398 | $ | 6,477 | $ | (6,129,603 | ) | $ | 2,212,603 | |||||||||||||||||

Private placement (Note 9(b)) | - | - | 1,359,280 | - | - | - | - | - | 1,359,280 | |||||||||||||||||||||||||||

Issuance costs | - | - | (193,921 | ) | - | - | 49,960 | - | - | (143,961 | ) | |||||||||||||||||||||||||

Conversion of special warrants | - | 1,165,359 | (1,165,359 | ) | - | - | - | - | - | - | ||||||||||||||||||||||||||

Private placement (Note 9(a)) | - | - | 14,215,155 | - | - | - | - | - | 14,215,155 | |||||||||||||||||||||||||||

Issuance costs | - | - | (1,212,470 | ) | - | - | - | - | - | (1,212,470 | ) | |||||||||||||||||||||||||

Conversion of preferred shares | 4,255,704 | (4,255,704 | ) | - | - | - | - | - | - | - | ||||||||||||||||||||||||||

Conversion of special warrants | 238,800 | - | (238,800 | ) | - | - | - | - | - | - | ||||||||||||||||||||||||||

Options exercised | 159,094 | - | - | - | (62,334 | ) | - | - | - | 96,760 | ||||||||||||||||||||||||||

Warrants exercised | 270,813 | - | - | - | - | (63,284 | ) | - | - | 207,529 | ||||||||||||||||||||||||||

Share-based payments | - | - | - | - | 1,070,889 | - | - | - | 1,070,889 | |||||||||||||||||||||||||||

Loss for the period | - | - | - | - | - | - | (159,182 | ) | (12,202,672 | ) | (12,361,854 | ) | ||||||||||||||||||||||||

| Balance, June 30, 2015 | $ | 9,165,328 | $ | - | $ | 12,763,885 | $ | - | $ | 1,946,624 | $ | 53,074 | $ | (152,705 | ) | $ | (18,332,275 | ) | $ | 5,443,931 | ||||||||||||||||

The accompanying notes are an integral part of these condensed consolidated interim financial statements.

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

1. NATURE AND CONTINUANCE OF OPERATIONS

ESSA Pharma Inc. (the “Company”) was incorporated under the laws of the Province of British Columbia on January 6, 2009. The Company’s head office address is Suite 720 – 999 West Broadway, Vancouver, BC, V5Z 1K5. The registered and records office address is the 26th Floor at 595 Burrard Street, Three Bentall Centre, Vancouver, BC, V7X 1L3. In the period ended September 30, 2013, the Company modified its fiscal year end from December 31 to September 30.

The Company is focused on the development of small molecule drugs for the treatment of prostate cancer. The Company has acquired a license to certain patents (the “NTD Technology”) which were the joint property of the British Columbia Cancer Agency and the University of British Columbia. As at June 30, 2015, no products are in commercial production or use.

These financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) assuming the Company will continue on a going-concern basis. The Company has incurred losses and negative operating cash flows since inception. The Company incurred a loss of $12,202,672 during the period ended June 30, 2015 and has an accumulated deficit of $18,332,275. The ability of the Company to continue as a going concern in the long-term depends upon its ability to develop profitable operations and to continue to raise adequate financing. As at June 30, 2015, the Company has not advanced its research into a commercially viable product. The Company’s continuation as a going concern is dependent upon the successful development of its NTD Technology to a commercial standard. Management continues to seek sources of additional financing which would assure continuation of the Company’s operations and research programs.

2. BASIS OF PRESENTATION

Statement of Compliance

These condensed consolidated interim financial statements, including comparatives, have been prepared in accordance with International Accounting Standards (“IAS”) 34 ‘Interim Financial Reporting’ (“IAS 34”) using accounting policies consistent with International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”) and Interpretations of the International Financial Reporting Interpretations Committee (“IFRIC”).

The condensed consolidated interim financial statements do not include all the information and disclosures required in the annual consolidated financial statements and should be read in conjunction with the Company’s annual consolidated financial statements for the year ended September 30, 2014.

Estimates

The Company makes estimates and assumptions about the future that affect the reported amounts of assets and liabilities. Estimates and judgments are continually evaluated based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances. In the future, actual experience may differ from these estimates and assumptions.

The effect of a change in an accounting estimate is recognized prospectively by including it in comprehensive income in the period of the change, if the change affects that period only, or in the period of the change and future periods, if the change affects both. Significant assumptions about the future and other sources of estimation uncertainty that management has made at the statement of financial position date, that could result in a material adjustment to the carrying amounts of assets and liabilities, in the event that actual results differ from assumptions that have been made, relate to the following key estimates:

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

2. BASIS OF PRESENTATION (cont’d…)

Estimates (cont’d…)

Intangible Assets – impairment

The application of the Company’s accounting policy for intangible assets expenditures requires judgment in determining whether it is likely that future economic benefits will flow to the Company, which may be based on assumptions about future events or circumstances. Estimates and assumptions may change if new information becomes available. If, after expenditures are capitalized, information becomes available suggesting that the recovery of expenditures is unlikely, the amount capitalized is written off in profit or loss in the period the new information becomes available.

Intangible Assets – useful lives

Following initial recognition, the Company carries the value of intangible assets at cost less accumulated amortization and any accumulated impairment losses. Amortization is recorded on a straight-line basis based upon management’s estimate of the useful life and residual value. The estimates are reviewed at least annually and are updated if expectations change as a result of technical obsolescence or legal and other limits to use. A change in the useful life or residual value will impact the reported carrying value of the intangible assets resulting in a change in related amortization expense.

Product development and relocation grant

Pursuant to the terms of the Company’s grant from the Cancer Prevention Research Institute of Texas (“CPRIT”), the Company must meet certain terms and conditions to qualify for the grant funding. The Company has assessed its performance relative to these terms as detailed in Note 16 and has judged that there is reasonable assurance the Company will meet the terms of the grant and qualify for the funding. The Company has therefore taken into income a portion of the grant that represents expenses the Company has incurred to date under the grant parameters. The expenses are subject to assessment by CPRIT for compliance with the grant regulations which may result in certain expenses being denied and incurred in a future period.

Share-based payments and compensation

The Company has applied estimates with respect to the valuation of shares issued for non-cash consideration. Shares are valued at the fair value of the equity instruments granted at the date the Company receives the goods or services.

The Company measures the cost of equity-settled transactions with employees by reference to the fair value of the equity instruments at the date at which they are granted. Estimating fair value for share-based payment transactions requires determining the most appropriate valuation model, which is dependent on the terms and conditions of the grant. This estimate also requires determining the most appropriate inputs to the valuation model including the fair value of the underlying common shares, the expected life of the share option, volatility and dividend yield and making assumptions about them. Prior to listing on the TSX-V, the fair value of the underlying common shares was assessed as the most recent issuance price per common share for cash proceeds. Following listing on the TSX-V, the Company makes reference to prices quoted on the TSX-V. The assumptions and models used for estimating fair value for share-based payment transactions are discussed in Note 10.

Derivative financial instruments

Certain broker’s warrants are treated as derivative financial liabilities. The estimated fair value, based on the Black-Scholes model, is adjusted on a quarterly basis with gains or losses recognized in the statement of net loss and comprehensive loss. The Black-Scholes model is based on significant assumptions such as volatility, dividend yield and expected term (Note 8).

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

3. SIGNIFICANT ACCOUNTING POLICIES

The accounting policies adopted in the preparation of the condensed consolidated interim financial statements are consistent with those followed in the preparation of the Company’s annual consolidated financial statements for the year ended September 30, 2014, except for the adoption of new standards and interpretations effective as of October 1, 2014.

Embedded derivatives

Derivatives may be embedded in other financial instruments (the “host instrument”). Embedded derivatives are treated as separate derivatives when their economic characteristics and risks are not clearly and closely related to those of the host instrument, the terms of the embedded derivative are the same as those of a stand-alone derivative, and the combined contract is not held for trading or designated at fair value. These embedded derivatives are measured at fair value with subsequent changes recognized in gains or losses on derivative instruments in the statement of loss and comprehensive loss.

New standards, interpretations and amendments adopted

The following standards, amendments to standards and interpretations have been adopted for the fiscal year beginning October 1, 2014:

| ● | IFRS 2 (Amendment) | Revised definitions for ‘vesting conditions’ and ‘market condition’ related to share based compensation | |||

| ● | IFRS 13 (Amendment) | Revised disclosure requirements for contracts under the scope of IFRS 9/IAS 39 | |||

| ● | IAS 24 (Amendment) | New definitions for ‘related party’ encompassing key management personnel | |||

| ● | IAS 38 (Amendment) | Revised valuation methods for the ‘revaluation model’ for intangible assets | |||

| ● | IAS 39 | New standard for financial instruments including embedded derivatives |

The application of these standards, amendments and interpretations has not had a material impact on the results and financial position of the Company.

New standards not yet adopted

IFRS 9 Financial Instruments

IFRS 9 was issued by the IASB in October 2010. It incorporates revised requirements for the classification and measurement of financial liabilities and carrying over the existing derecognition requirements from IAS 39 Financial instruments: recognition and measurement. The revised financial liability provisions maintain the existing amortized cost measurement basis for most liabilities. New requirements apply where an entity chooses to measure a liability at fair value through profit or loss – in these cases, the portion of the change in fair value related to changes in the entity's own credit risk is presented in other comprehensive income rather than within profit or loss. IFRS 9 is effective for annual periods beginning on or after January 1, 2018. The impact of IFRS 9 on the Company’s consolidated financial instruments has not yet been determined.

IFRS 15 Revenue from Contracts with Customers

IFRS 15 establishes a single five-step model framework for determining the nature, amount, timing and uncertainty of revenue and cash flows arising from a contract with a customer. The standard is effective for annual periods beginning on or after January 1, 2018, with early adoption permitted. The change in accounting standard is unlikely to have a significant impact on the Company’s consolidated financial statements.

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

4. PREPAIDS

June 30, 2015 | September 30, 2014 | |||||||

| Clinical program deposit | $ | 1,271,865 | $ | - | ||||

| Other deposits and prepaid expenses | 79,569 | 69,946 | ||||||

| Balance | $ | 1,351,434 | $ | 69,946 | ||||

During the period ended June 30, 2015, the Company paid $1,271,865 (US$1,018,307) as an initial deposit under a clinical research services agreement with a third party in relation to the Company’s clinical trial activities.

5. EQUIPMENT

Office equipment | ||||

| Cost | ||||

| Balance, September 30, 2013 | $ | - | ||

Additions | 15,806 | |||

| Balance, September 30, 2014 | 15,806 | |||

Additions | 136,178 | |||

Net exchange differences | 7,122 | |||

| Balance, June 30, 2015 | 159,106 | |||

| Accumulated Amortization | ||||

| Balance, September 30, 2013 and 2014 | $ | - | ||

Amortization expense | 9,611 | |||

Net exchange differences | 376 | |||

| Balance, June 30, 2015 | 9,987 | |||

| Net Book Value | ||||

| Balance, September 30, 2014 | $ | 15,806 | ||

| Balance, June 30, 2015 | $ | 149,119 | ||

Amortization expense for the period ended June 30, 2015 has been recorded in “general and administrative expenses” in the statement of loss and comprehensive loss.

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

6. INTANGIBLE ASSETS

NTD Technology | June 30, 2015 | September 30, 2014 | ||||||

| Cost | ||||||||

Balance, beginning and end of period | $ | 500,017 | $ | 500,017 | ||||

| Accumulated amortization | ||||||||

Balance, beginning of period | 95,587 | 70,264 | ||||||

Amortization | 18,993 | 25,323 | ||||||

Balance, end of period | 114,580 | 95,587 | ||||||

Net book value, end of period | $ | 385,437 | $ | 404,430 | ||||

Amortization expense for the period ended June 30, 2015 and year ended September 30, 2014 has been recorded in “general and administrative expenses” in the statement of loss and comprehensive loss.

The NTD Technology is held under a License Agreement signed in fiscal 2010. As consideration for the License Agreement, the Company issued common shares of the Company. The License Agreement contains an annual royalty as a percentage of annual net revenue and a percentage of any annual sublicensing revenue earned with respect to the NTD Technology. The License Agreement stipulates certain minimum advance royalty payments of $40,000 for 2013 and escalating to $85,000 by 2017. In addition, there are certain cumulative milestone payments totaling $2,400,000 for the first compound, to be paid in stages at the start of Phase II and Phase III clinical trials, at application for marketing approval, and with further milestone payments on the second and additional compounds.

In order to maintain the License Agreement in good standing, the Company is required to spend $5,000,000, in cash or in kind, in connection with the commercialization of the NTD Technology by December 20, 2015. This expenditure commitment was completed in the year ended September 30, 2014.

7. DEBENTURE

In April 2014, the Company issued a convertible debenture to the Bloom Burton Healthcare Structured Lending Fund LP (“the Lender”) for $1,000,000. The convertible debenture terms include interest of 12% per annum payable at maturity (24 months from closing), as secured by various security agreements. The Company incurred transaction costs of $23,541 and issued 25,000 warrants to the Lender valued at $16,394, each exercisable into one common share at a price of $2.00 for a period of five years. The warrants were valued using the Black-Scholes model with a risk-free interest rate of 1.63%, term of 5 years, volatility of 80%, and dividend rate of 0%.

The principal and accrued interest are convertible into common shares of the Company at maturity at a conversion price of $1.20 unless the Company opts to settle the balance in cash. The terms of the debenture maintained control of the conversion option in the hands of the Company; therefore, the instrument has been recorded as equity in the statement of financial position.

The Company and Lender agreed to proceed with early conversion of the debenture, including accrued interest, into 517,500 preferred shares of the Company upon the closing of the financing completed in July 2014 (Note 9(c)).

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

7. DEBENTURE (cont’d…)

| Amount | ||||

| Balance, September 30, 2013 | $ | - | ||

| Proceeds on issuance of convertible debenture | 1,000,000 | |||

| Issuance costs | (39,935 | ) | ||

| Interest accrued | 35,000 | |||

| Conversion to preferred shares | (995,065 | ) | ||

| Balance, September 30, 2014 and June 30, 2015 | $ | - | ||

8. DERIVATIVE LIABILITY

In connection with the 2015 Special Warrant financing in January 2015 (Note 9(a)), the Company issued 257,018 broker warrants. Each broker warrant is exercisable to purchase one common share until January 16, 2017 at a price of US$2.75 per broker warrant.

As these broker warrants are denominated in US dollars and are exercisable into the Company’s common shares which are listed in Canadian dollars, the instrument contains an embedded derivative liability. In accordance with IFRS, an obligation to issue shares for a price that is not fixed in the Company’s functional currency, and that does not qualify as a rights offering, must be classified as a derivative liability and measured at fair value with changes recognized in the statement of loss and comprehensive loss as they arise. The embedded derivative is designated as a financial liability carried at fair value through profit and loss.

On issuance of the broker warrants, the Company recorded a derivative liability of $334,396 using the Black-Scholes model (Note 9). During the period ended June 30, 2015, 655 of the broker warrants were exercised, reducing the derivative liability by $4,152. As at June 30, 2015, the derivative liability had a fair value of $2,796,853, using the Black-Scholes model with a risk-free interest rate of 0.49%, term of 1.55 years, volatility of 80.0%, and dividend rate of 0%. The Company has recorded the resulting change in fair value of $2,466,609 in the statement of loss and comprehensive loss for the period ended June 30, 2015.

| Amount | ||||

| Balance, September 30, 2014 | $ | - | ||

| Derivative liability on issuance of broker warrants | 334,396 | |||

| Exercise of broker warrants | (4,152 | ) | ||

| Change in fair value | 2,466,609 | |||

| Balance, June 30, 2015 | $ | 2,796,853 | ||

9. SHAREHOLDERS’ EQUITY

Authorized:

Unlimited common shares, without par value.

Unlimited preferred shares, without par value.

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

9. SHAREHOLDERS’ EQUITY (cont’d…)

| Share capital | Preferred shares | Special warrants | ||||||||||||||||||||||

| Number | Amount | Number | Amount | Number | Amount | |||||||||||||||||||

| Balance, September 30, 2013 and June 30, 2014 | 15,687,534 | $ | 4,240,917 | - | $ | - | - | $ | - | |||||||||||||||

| Balance, September 30, 2014 | 15,687,534 | $ | 4,240,917 | 1,702,900 | $ | 3,090,345 | - | $ | - | |||||||||||||||

Private placement (Note 9(b)) | - | - | - | - | 679,640 | 1,359,280 | ||||||||||||||||||

Financing costs | - | - | - | - | - | (193,921 | ) | |||||||||||||||||

Conversion of special warrants | - | - | 679,640 | 1,165,359 | (679,640 | ) | (1,165,359 | ) | ||||||||||||||||

Private placement - (Note 9(a)) | - | - | - | - | 4,363,634 | 14,215,155 | ||||||||||||||||||

Financing costs | - | - | - | - | - | (1,212,470 | ) | |||||||||||||||||

Conversion of preferred shares | 2,382,540 | 4,255,704 | (2,382,540 | ) | (4,255,704 | ) | - | - | ||||||||||||||||

Conversion of special warrants | 80,000 | 238,800 | - | - | (80,000 | ) | (238,800 | ) | ||||||||||||||||

Options exercised | 81,200 | 159,094 | - | - | - | - | ||||||||||||||||||

Warrants exercised | 101,262 | 270,813 | - | - | - | - | ||||||||||||||||||

| Balance, June 30, 2015 | 18,332,536 | $ | 9,165,328 | - | $ | - | 4,283,634 | $ | 12,763,885 | |||||||||||||||

Listing on the TSX-V

The Company completed its listing on the TSX-V on January 27, 2015 (“Date of Listing”) and began trading under the symbol “EPI”.

Immediately prior to the listing, all of the Company’s 2,382,540 issued and outstanding Preferred Shares were converted into common shares.

Escrow, Lock-Up, and Supplementary Lock-Up Restrictions

The Company’s 15,687,534 common shares outstanding at September 30, 2014 are subject to various trading restrictions.

As at September 30, 2014, 5,092,000 common shares of the Company were subject to a voluntary lock-up agreement. 712,950 common shares were released on the Date of Listing, 763,872 common shares were released on March 5, 2015, and the remaining shares will be released in increments of 875,910 common shares every 3 months beginning October 27, 2015. As at June 30, 2015, 3,615,678 common shares remained subject to lock-up restrictions.

As at September 30, 2014, the remaining 10,595,034 common shares of the Company were subject to an Escrow Agreement with the TSX-V, whereby 10% of the common shares subject to escrow were released upon the Date of Listing with the remaining common shares to be released in 15% increments every 6 months thereafter. Of these common shares, 9,470,000 common shares are subject to supplementary lock-up restrictions, whereby increments of 14%, 11%, and 15% will be released 6, 9, and 12 months after the Date of Listing, respectively, and increments of 15% every 6 months thereafter. As at June 30, 2015, 9,535,530 common shares were held in escrow; however, 947,000 of the common shares released from escrow remained subject to supplementary lock-up restrictions.

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

9. SHAREHOLDERS’ EQUITY (cont’d…)

Private placements:

a) January 2015 Special Warrant Financing

In January 2015, the Company issued 4,363,634 special warrants (the “2015 Special Warrants”) at a price of US$2.75 per 2015 Special Warrant for gross proceeds of approximately US$12,000,000. Each 2015 Special Warrant is exercisable for, without payment of any additional consideration, one common share at any time by the holder thereof and all of the 2015 Special Warrants will be deemed to be exercised on the earlier of: (i) October 16, 2015 and (ii) the date on which the common shares first begin to trade on either (i) the Nasdaq Global Select Market, the Nasdaq Global Market or the Nasdaq Capital Market securities trading platforms of the NASDAQ Stock Market or (ii) the NYSE MKT securities trading platform of the New York Stock Exchange (the “U.S. Listing Date”). Should the U.S. Listing Date not occur on or prior to October 16, 2015, instead of one common share, each 2015 Special Warrant shall entitle the holder thereof to receive 1.5 common shares upon exercise or deemed exercise thereof.

In connection with the 2015 Special Warrant financing, Bloom Burton & Co. and Roth Capital Partners, LLC, as Agents, and selling group members, received cash commission equal to approximately US$706,800 and 257,018 broker warrants. Each broker warrant is exercisable to purchase one common share until January 16, 2017 at a price of US$2.75 per broker warrant. The warrants were valued at $334,396 using the Black-Scholes model with a risk-free interest rate of 0.87%, term of 2 years, volatility of 72.3%, and dividend rate of 0%, and have been recorded as a derivative liability (Note 8).

b) October 2014 Special Warrant Financing

In October 2014, the Company issued 679,640 special warrants (the “2014 Special Warrants”) at a price of $2.00 per 2014 Special Warrant for gross proceeds of $1,359,280. Each 2014 Special Warrant was deemed exercised for, without payment of any additional consideration, one Class A Preferred share in the capital of the Company (each a “Preferred Share”) on December 15, 2014, being the fifth business day after the date on which a receipt for the final prospectus of the Company qualifying the distribution of the Preferred Shares issuable on exercise of the 2014 Special Warrants had been issued. During the period ended June 30, 2015, the Preferred Shares were converted into common shares of the Company.

In connection with the 2014 Special Warrant financing, the Company paid agent and finders’ fees at 7% of proceeds raised by those parties being $40,361, a cash fee to the Agent of $30,000 plus applicable taxes and estimated other expenses of $70,594. In addition, the Agent, and associated selling group, were issued 22,675 special broker warrants (the “Special Broker Warrants”), representing 7% of the number of 2014 Special Warrants sold by the Agent and the finders were issued 2,680 Special Broker Warrants, representing 7% of the number of 2014 Special Warrants sold to purchasers introduced to the Company by such finders. Each Special Broker Warrant was deemed exercised for, without payment of any additional consideration, one broker warrant (the “Broker Warrants”). Each Broker Warrant is exercisable to acquire one common share, subject to adjustment in certain circumstances, at a price of $2.00 until October 22, 2015. The Special Broker Warrants were valued at $49,960 using the Black-Scholes model with a risk-free interest rate of 1.00%, term of 1 year, volatility of 80% and dividend rate of 0%.

c) July 2014 Preferred Shares Financing

On July 29, 2014, the Company completed a brokered private placement of 1,185,400 Preferred Shares at a price of $2.00 per Preferred Share for aggregate gross proceeds of $2,370,800. During the period ended June 30, 2015, the Preferred Shares were converted into common shares of the Company.

In conjunction with the private placement, the Company issued 79,479 warrants to Bloom Burton, the Company’s advisor, and other finders exercisable at a price of $2.00 for a period of one year. The warrants were valued at $50,004 using the Black-Scholes model with a risk-free interest rate of 1.08%, term of 1 year, volatility of 80% and dividend rate of 0%. The Company paid finders’ fees of $158,956 and other share issue costs of $66,560.

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

10. RESERVES

Stock options

The Company has adopted a Stock Option Plan which is a rolling stock option plan whereby a maximum of 10% of the issued shares will be reserved for issuance under the plan. The Stock Option Plan is consistent with the policies and rules of the TSX-V.

Stock option transactions are summarized as follows:

Number of Options | Weighted Average Exercise Price | |||||||

| Balance, September 30, 2013 | 1,119,250 | $ | 0.73 | |||||

Options granted | 1,950,469 | 1.80 | ||||||

| Balance, September 30, 2014 | 3,069,719 | 1.41 | ||||||

Options granted | 425,000 | 4.20 | ||||||

Options exercised | (81,200 | ) | (1.19 | ) | ||||

| Balance outstanding, June 30, 2015 | 3,413,519 | $ | 1.76 | |||||

Balance exercisable, June 30, 2015 | 1,768,550 | $ | 1.33 | |||||

At June 30, 2015, options were outstanding enabling holders to acquire common shares as follows:

| Exercise price | Number of options | Weighted average remaining contractual life (years) | ||||

| $ | 0.50 | 261,000 | 0.86 | |||

0.80 | 1,128,300 | 2.93 | ||||

2.00 | 1,899,219 | 4.17 | ||||

4.65 | 10,000 | 4.60 | ||||

5.15 | 10,000 | 4.68 | ||||

5.35 | 50,000 | 9.68 | ||||

14.90 | 55,000 | 9.53 | ||||

| 3,413,519 | 3.68 | |||||

Escrow, Lock-Up, and Supplementary Lock-Up Restrictions

The Company’s stock options exercisable at $0.50 and $0.80 and 150,000 stock options exercisable at $2.00 are subject to various exercise restrictions.

As at September 30, 2014, 330,500 stock options exercisable at $0.50 and $0.80 were subject to pooling restrictions. 66,100 options were released on the Date of Listing, and the remaining options will be released in increments of 66,100 common shares every 3 months thereafter. As at June 30, 2015, 198,300 options remained subject to pooling restrictions. Subsequent to June 30, 2015, 66,100 options were released.

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

10. RESERVES (cont’d…)

Escrow, Lock-Up, and Supplementary Lock-Up Restrictions (cont’d…)

As at September 30, 2014, 1,110,000 stock options exercisable at $0.50 and $0.80 were subject to an Escrow Agreement with the TSX-V, whereby 10% of the options subject to escrow were released upon the Date of Listing with the remaining options to be released in 15% increments every 6 months thereafter. Of these options, 915,000 options are also subject to lock-up and supplementary lock-up restrictions, whereby increments of 14%, 11%, and 15% will be released 6, 9, and 12 months after the Date of Listing, respectively, and increments of 15% every 6 months thereafter. As at June 30, 2015, 1,090,500 options remained subject to escrow, lock-up, and supplementary lock-up restrictions. Subsequent to June 30, 2015, 206,100 options were released.

As at June 30, 2015, 150,000 stock options exercisable at $2.00 are subject to lock-up and supplementary lock-up restrictions, whereby increments of 14% and 32.2% will be released 6 and 9 months after the Date of Listing, respectively, and increments of 17.2% every 3 months thereafter. Subsequent to June 30, 2015, 21,000 options were released.

Share-based compensation

During the period ended June 30, 2015, the Company granted 425,000 (2014 – 850,469) stock options with a weighted average fair value of $2.67 (2014 – $0.43). The Company recognized share-based payments expense of $1,070,889 (2014 - $170,062) for options granted and vesting during the period.

Share-based payments expense for the nine months ended June 30, 2015 and 2014 is allocated to its functional expense as follows:

| 2015 | 2014 | |||||||

| Research and development expense (Note 17) | $ | 621,363 | $ | 92,723 | ||||

| Financing costs | 69,508 | 35,833 | ||||||

| General and administrative (Note 17) | 380,018 | 41,506 | ||||||

| $ | 1,070,889 | $ | 170,062 | |||||

The following weighted average assumptions were used for the Black-Scholes option-pricing model valuation of stock options granted during the period:

| 2015 | 2014 | |||||||

| Risk-free interest rate | 1.43 | % | 1.35 | % | ||||

| Expected life of options | 5.28 years | 5.00 years | ||||||

| Expected annualized volatility | 79.47 | % | 80.0 | % | ||||

| Dividend | - | - | ||||||

Expected annualized volatility was determined through the comparison of historical share price volatilities used by similar publicly listed companies in the pharmaceuticals / biotechnology industry. The companies chosen for comparison were, Cipher Pharmaceuticals Inc. (June 30, 2015 – 74.57% volatility), Oncolytics Biotech Inc. (June 30, 2015 – 71.05%), Helix BioPharma Corp. (June 30, 2015 – 75.82% volatility), and Cardiome Pharma Corp. (June 30, 2015 – 78.57% volatility). As the Company is less established than these comparable companies, the Company’s stock price is expected to be slightly more volatile than the average of the companies analyzed. As such, the Company used an average annualized volatility of 75%-80%. This is consistent with estimates provided in the period ended June 30, 2015 and provides a reasonable trend for the Company’s expected volatility.

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

10. RESERVES (cont’d…)

Warrants

Warrant transactions are summarized as follows:

Number of Warrants | Weighted Average Exercise Price | |||||||

| Balance, September 30, 2013 | - | $ | - | |||||

Warrants granted | 104,479 | 2.00 | ||||||

| Balance, September 30, 2014 | 104,479 | 2.00 | ||||||

Warrants granted | 282,373 | 3.18 | ||||||

Warrants exercised | (101,262 | ) | 2.01 | |||||

| Balance outstanding and exercisable, June 30, 2015 | 285,590 | $ | 3.29 | |||||

Warrants exercisable in US dollars as at June 30, 2015 are translated at current rates to reflect current weighted average exercise price in Canadian funds for all outstanding warrants.

At June 30, 2015, warrants were outstanding enabling holders to acquire common shares as follows:

Number of Warrants | Exercise Price | Expiry Date | |||

| 25,000 | $ 2.00 | April 15, 2019 | |||

| 1,589 | 2.00 | July 29, 2015* | |||

2,638 | 2.00 | October 22, 2015** | |||

256,363 | US$2.75 | January 16, 2017 | |||

| 285,590 | |||||

* 1,589 warrants were exercised subsequent to June 30, 2015

** 1,512 warrants were exercised subsequent to June 30, 2015

11. SUPPLEMENTAL DISCLOSURE WITH RESPECT TO CASH FLOWS

During the period ended June 30, 2015, the Company:

| (a) | Accrued purchases of equipment of $19,204 through accounts payable and accrued liabilities. |

| (b) | Issued agent warrants valued at $49,960 (Note 9). |

| (c) | Recognized a derivative liability of $334,396 on the issuance of broker warrants denominated in US dollars (Note 8). |

There were no significant non-cash investing and financing transactions for the period ended June 30, 2014.

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

12. RELATED PARTY TRANSACTIONS

Key management personnel of the Company include the Chief Executive Officer, Chief Financial Officer, Chief Medical Officer, Executive VP of Research and Development, and Directors of the Company. Compensation paid to key management personnel for the nine months ended June 30, 2015 and 2014 are as follows:

| 2015 | 2014 | |||||||

| Salaries, consulting fees, and director fees | $ | 1,757,341 | $ | 240,000 | ||||

| Share-based payments | 851,615 | 117,594 | ||||||

| Total compensation | $ | 2,608,956 | $ | 357,594 | ||||

During the nine months ended June 30, 2015, the Company granted 250,000 options (2014 – 270,000) to key management personnel. The vesting of these options and options granted to key management personnel in prior periods were recorded as share-based payments expense in the statement of loss and comprehensive loss at a value of $851,615 (2014 - $117,594).

Included in accounts payable and accrued liabilities at June 30, 2015 is $99,592 (September 30, 2014 – $24,331) due to related parties with respect to key management personnel compensation and expense reimbursements. Amounts due to related parties are non-interest bearing, with no fixed terms of repayment.

Commitments

The CEO is entitled to a payment of one year of base salary upon termination without cause, increasing to two years if the termination without cause occurs after a change of control event or within 60 days prior to a change of control event where such event was under consideration at the time of termination. The CFO is entitled to a payment of one year of base salary upon termination without cause, whether or not the termination was caused by a change of control event. Stock options held by the CEO and CFO vest immediately upon a change of control.

13. SEGMENTED INFORMATION

The Company works in one industry being the development of small molecule drugs for prostate cancer. The Company’s equipment is located in the USA.

14. CAPITAL MANAGEMENT

The Company considers its capital to be the components of shareholders’ equity. The Company’s objective when managing capital is to maintain adequate levels of funding to support the development of its business and maintain the necessary corporate and administrative functions to facilitate these activities. This is done primarily through equity financing.

Future financings are dependent on market conditions and the ability to identify sources of investment. There can be no assurance the Company will be able to raise funds in the future.

There were no changes to the Company’s approach to capital management during the period. The Company is not subject to externally imposed capital requirements.

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

15. FINANCIAL INSTRUMENTS AND RISK

The Company’s financial instruments consist of cash, receivables, accounts payable and accrued liabilities and derivative liability. Cash is measured based on level 1 inputs of the fair value hierarchy. The fair value of receivables and accounts payable and accrued liabilities approximates their carrying values due to their short term to maturity. The derivative liability is measured using level 3 inputs.

Fair value estimates of financial instruments are made at a specific point in time, based on relevant information about financial markets and specific financial instruments. As these estimates are subjective in nature, involving uncertainties and matters of judgement, they cannot be determined with precision. Changes in assumptions can significantly affect estimated fair values.

Financial risk factors

The Company’s risk exposures and the impact on the Company’s financial instruments are summarized below:

Credit risk

Financial instruments that potentially subject the Company to a significant concentration of credit risk consist primarily of cash and receivables. The Company’s receivables are primarily due from refundable GST/HST and investment tax credits. The Company limits its exposure to credit loss by placing its cash with major financial institutions. Credit risk with respect to investment tax credits and GST/HST is minimal as the amounts are due from government agencies.

Liquidity risk

The Company’s approach to managing liquidity risk is to ensure that it will have sufficient liquidity to meet liabilities when due. As at June 30, 2015, the Company had a cash balance of $7,739,769 to settle current liabilities of $1,432,206. All of the Company’s current financial liabilities have contractual maturities of 30 days or due on demand and are subject to normal trade terms. The Company does not generate revenue and will be reliant on equity financing and proceeds from the CPRIT grant to fund operations. Equity financing is dependent on market conditions and may not be available on favorable terms. The CPRIT grant is dependent on the Company completing all the milestones (Note 16).

Market risk

Market risk is the risk of loss that may arise from changes in market factors such as interest rates, and foreign exchange rates.

(a) Interest rate risk

The Company has cash balances and no interest-bearing debt and therefore is not exposed to risk in the event of interest rate fluctuations. Interest income is not significant to the Company’s projected operational budget.

(b) Foreign currency risk

The Company is exposed to foreign currency risk on fluctuations related to accounts payable and accrued liabilities that are denominated in United States dollars. As at June 30, 2015, the Company had cash of US$6,004,945 and accounts payable and accrued liabilities of US$708,494. The Company anticipates that, pursuant to the product development and relocation grant disclosed in Note 16, the transactions of the Company will be increasingly subject to fluctuations in the US dollar. Additionally, the Company has broker warrants outstanding which are denominated in United States dollars (Note 8).

A 10% change in the foreign exchange rate between the Canadian and US dollar would result in a fluctuation of $601,975 in the net loss realized for the period.

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

15. FINANCIAL INSTRUMENTS AND RISK (cont’d…)

Financial risk factors (cont’d…)

Market risk (cont’d…)

(b) Foreign currency risk (cont’d…)

The Company does not currently engage in hedging activities.

(c) Price risk

The Company is exposed to price risk with respect to equity prices. The Company closely monitors individual equity movements, and the stock market to determine the appropriate course of action to be taken by the Company.

16. COMMITMENTS

The Company has the following obligations over the next five years:

Contractual obligations | 2016 | 2017 | 2018 | 2019 | 2020 | |||||||||||||||

| Minimum annual royalty per License Agreement (Note 6) | $ | 65,000 | $ | 85,000 | $ | 85,000 | $ | 85,000 | $ | 85,000 | ||||||||||

| Lease on Vancouver office space | 48,510 | 48,510 | 48,510 | 48,510 | 48,510 | |||||||||||||||

| Total | $ | 113,510 | $ | 133,510 | $ | 133,510 | $ | 133,510 | $ | 133,510 | ||||||||||

| Lease on US office space (In USD) | 241,009 | 245,690 | 250,372 | 255,053 | 57,789 | |||||||||||||||

Product Development and Relocation Grant

In February 2014 the Company received notice that it had been awarded a product development and relocation grant by the Cancer Prevention Research Institute of Texas (“CPRIT”) whereby the Company is eligible to receive up to US$12,000,000 on eligible expenditures over a three year period related to the development of the Company’s androgen receptor n-terminus blocker program for prostate cancer. The funding under CPRIT is subject to a number of conditions including negotiation and execution of an award contract which details the milestones that must be met to release the tranched CPRIT funding, proof the Company has raised the 50% matching funds to release CPRIT monies, and relocation of the project to the State of Texas such that the substantial functions of the Company related to the project grant are in Texas and the Company uses Texas-based subcontractor and collaborators wherever possible.

During the year ended September 30, 2014, the Company received US$2,793,533 as an advance on the CPRIT grant, of which US$1,153,181 in qualifying expenses was incurred in that same period. During the nine month period ended June 30, 2015, the Company incurred qualifying expenses of US$6,372,517 and has recognized a reduction in the grant liability in the statement of loss and comprehensive loss. The Company has judged there is reasonable assurance that the funds will be successfully earned under the terms of the grant.

If the Company is found to have used any grant proceeds for purposes other than intended, is in violation of the terms of the grant, or relocates its operations outside of the state of Texas, then the Company is required to repay any grant proceeds received.

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

16. COMMITMENTS (cont’d…)

Product Development and Relocation Grant (cont’d…)

Under the terms of the grant, the Company is also required to pay a royalty to CPRIT, comprised of 4% of revenues until aggregate royalty payments equal US$24,000,000, and 2% of revenues thereafter. The Company has the option to terminate the grant agreement by paying a one-time, non-refundable buyout fee, based on certain factors including the grant proceeds, and the number of months between termination date and the buyout fee payment date.

June 30, 2015 | September 30, 2014 | |||||||

| Opening balance | $ | 1,838,507 | $ | - | ||||

| Advance received | - | 3,048,694 | ||||||

| Recoveries claimed | (1,894,263 | ) | (1,256,621 | ) | ||||

| Effect of foreign exchange | 55,756 | 46,434 | ||||||

| Ending balance | $ | - | $ | 1,838,507 | ||||

Advisory Contract

In February 2014 the Company executed an Engagement Letter with Bloom Burton & Co. (“Bloom Burton”), an investment bank, to retain their services to act as its exclusive agent and financial advisor in connection with a funding strategy for the Company to involve a private financing, that is compatible with the CPRIT grant, followed by an initial public offering on a major North American stock exchange. In exchange for their services, Bloom Burton would receive a percentage of any funds raised and warrants on successful completion of the financing. The Engagement Letter was for a term of nine months and has since expired; however, Bloom Burton retains a right of first refusal on all future financings occurring up to 24 months following the Company’s initial public offering.

The July 2014 Preferred Shares financing, October 2014 Special Warrant financing, and January 2015 Special Warrant financing were completed under the terms of the Advisory Contract (Note 9).

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

17. EXPENSES BY NATURE

General and administrative expenses include the following major expenses by nature for the three and nine month periods ended June 30, 2015 and 2014:

Three months ended June 30, 2015 | Three months ended June 30, 2014 | Nine months ended June 30, 2015 | Nine months ended June 30, 2014 | |||||||||||||

| Amortization | $ | 10,644 | $ | 6,331 | $ | 28,604 | $ | 18,993 | ||||||||

| Consulting and subcontractor fees | 50,683 | 73,496 | 157,568 | 199,091 | ||||||||||||

| Director fees | 47,000 | - | 91,000 | - | ||||||||||||

| Investor relations | 86,866 | - | 174,438 | - | ||||||||||||

| Office, IT and communications | 166,529 | 21,299 | 313,771 | 27,458 | ||||||||||||

| Professional fees | 491,871 | 178,665 | 1,489,020 | 220,922 | ||||||||||||

| Regulatory fees and transfer agent | 19,998 | - | 78,747 | - | ||||||||||||

| Rent | 84,387 | 8,249 | 145,929 | 23,761 | ||||||||||||

| Salaries and benefits | 185,971 | - | 801,991 | - | ||||||||||||

| Share-based payments (Note 10) | 16,235 | 41,506 | 323,505 | 41,506 | ||||||||||||

| Travel and entertainment | 59,258 | 5,762 | 171,839 | 9,330 | ||||||||||||

| CPRIT grant claimed on eligible expenses (Note 16) | - | - | (145,310 | ) | - | |||||||||||

| Total | $ | 1,219,442 | $ | 335,308 | $ | 3,631,102 | $ | 541,061 | ||||||||

Research and development expenses include the following major expenses by nature for the three and nine month period ended June 30, 2015 and 2014:

Three months ended June 30, 2015 | Three months ended June 30, 2014 | Nine months ended June 30, 2015 | Nine months ended June 30, 2014 | |||||||||||||

| Analytical studies, formulation and testing | $ | 696,904 | $ | 153,687 | $ | 2,385,390 | $ | 261,961 | ||||||||

| Consulting | 305,129 | 132,867 | 949,187 | 216,441 | ||||||||||||

| Legal patents and license fees | 231,153 | 99,169 | 542,474 | 239,854 | ||||||||||||

| Manufacturing | 1,190,464 | 203,846 | 2,567,121 | 215,246 | ||||||||||||

| Other | 12,392 | 8,000 | 19,163 | 8,000 | ||||||||||||

| Salaries and benefits | 530,807 | 2,828 | 1,332,877 | 2,828 | ||||||||||||

| Share-based payments (Note 10) | 99,981 | 31,747 | 621,363 | 92,723 | ||||||||||||

| Travel | 105,233 | 21,537 | 345,928 | 31,102 | ||||||||||||

| SRED tax credits | (64,063 | ) | - | (64,063 | ) | (235,470 | ) | |||||||||

| CPRIT grant claimed on eligible expenses (Note 16) | - | - | (1,748,953 | ) | - | |||||||||||

| Total | $ | 3,108,000 | $ | 653,681 | $ | 6,950,487 | $ | 832,685 | ||||||||

| ESSA PHARMA INC. NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited) (Expressed in Canadian dollars) FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014 |

18. SUBSEQUENT EVENTS

Subsequent to June 30, 2015, the Company:

| (a) | Became listed on the NASDAQ Capital Market and began trading on July 9, 2015 under the symbol “EPIX”. As a result of the listing, each of the outstanding special warrants issued on January 16, 2015 was deemed to be exercised into one common share for no additional consideration on July 13, 2015. |

| (b) | Graduated to the TSX Exchange on July 28, 2015, under its existing symbol of “EPI”. |

DOCUMENT 3

FORM 51-102F1

MANAGEMENT DISCUSSION AND ANALYSIS

FOR THE NINE MONTHS ENDED JUNE 30, 2015 AND 2014

ESSA Pharma Inc. Head Office 900 West Broadway – Suite 720 Vancouver, BC V5Z 1K5 Canada | ESSA Pharmaceuticals Corp. 7505 South Main Street – Suite 250 Houston, TX 77030 USA |

1

| Management’s Discussion and Analysis | June 30, 2015 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS FOR NINE MONTHS ENDED JUNE 30, 2015 AND 2014

This management discussion and analysis (“MD&A”) of ESSA Pharma Inc. (the “Company” or “ESSA”) for the nine months ended June 30, 2015 and 2014 is as of August 17, 2015.

This MD&A has been prepared with reference to National Instrument 51-102 “Continuous Disclosure Obligations” of the Canadian Securities Administrators. This MD&A should be read in conjunction with the unaudited condensed interim consolidated financial statements and notes thereto for the nine months ended June 30, 2015 and 2014 as well as the audited consolidated financial statements for the year ended September 30, 2014, nine months ended September 30, 2013 and year ended December 31, 2012, and the related notes thereto. The consolidated financial statements are prepared in accordance with International Financial Reporting Standards (“IFRS”).

This MD&A may contain certain “forward-looking statements” and certain “forward-looking information” as defined under applicable Canadian securities laws. Please refer to the discussion of forward-looking statements set out under the heading “Forward-Looking Statements”, located at the end of this document. As a result of many factors, our actual results may differ materially from those anticipated in these forward-looking statements.

The Company trades on the Toronto Stock Exchange (“TSX”) under the symbol “EPI” and the NASDAQ under the symbol “EPIX”.

OVERVIEW OF THE COMPANY

We are a development-stage pharmaceutical company focused on developing novel and proprietary therapies for the treatment of prostate cancer in patients whose disease is progressing despite treatment with current therapies, including abiraterone and enzalutamide. We believe our product candidate, EPI-506, can significantly expand the interval of time in which patients suffering from castration resistant prostate cancer (“CRPC”) can benefit from hormone-based therapies. Specifically, EPI-506 acts by disrupting the androgen receptor (“AR”) signaling pathway, which is the primary pathway that drives prostate cancer growth. We have shown that EPI-002, the primary metabolite of EPI-506, prevents AR activation by binding selectively to the N-terminal domain (“NTD”) of the AR. A functional NTD is essential for activation of the AR. Blocking the NTD prevents activation of the AR by all of the known mechanisms of activation. In pre-clinical studies, blocking the NTD has demonstrated the capability to prevent AR activation and overcome the known AR-dependent mechanisms of CRPC.

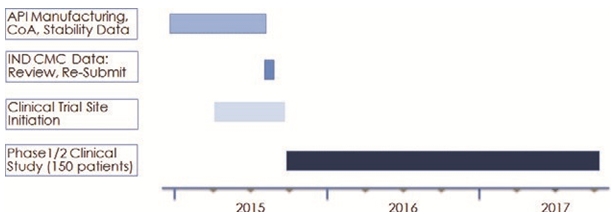

We have submitted an Investigational New Drug (“IND”) application to the U.S. Food and Drug Administration (“FDA”) for EPI-506 to begin a Phase 1/2 clinical trial. We will explore the safety, tolerability, maximum tolerated dose and pharmacokinetics of EPI-506, in addition to tumor response rates in asymptomatic or minimally symptomatic patients who are no longer responding to either abiraterone or enzalutamide treatments, or both. Efficacy endpoints include prostate specific antigen (“PSA”) reduction, as well as other progression criteria. The IND is currently on clinical hold until we provide the FDA with additional chemistry and stability information relating to EPI-506. We expect to submit this information during the third quarter of 2015.

According to the American Cancer Society, in the United States, prostate cancer is the second most frequently diagnosed cancer among men, behind skin cancer. Approximately one-third of all prostate cancer patients who have been treated for local disease will subsequently have rising serum levels of PSA, which is an indication of recurrent or advanced disease. Patients with advanced disease often undergo androgen ablation therapy using analogues of luteinizing hormone releasing hormone (“LHRH”) or surgical castration. Most advanced prostate cancer patients initially respond to androgen ablation therapy, however many experience a recurrence in tumor growth despite the reduction of testosterone to castrate levels, and at that point are considered to be suffering from CRPC. Following diagnosis of CRPC, patients are often treated with anti-androgens, which block the binding of androgens to the AR.

The growth of prostate tumors is mediated by an activated AR. Generally, there are three means of activating the AR. First, androgens such as dihydrotestosterone can activate AR by binding to its ligand-binding domain (“LBD”). Second, CRPC can be driven by constitutively-active variants of AR (“vAR”) that lack a LBD and do not require androgen for activation. The third mechanism involves certain signaling pathways that activate AR independent of androgen activity. Current drugs for the treatment of prostate cancer work by focusing on the first mechanism and preventing androgen from binding to LBD, but this approach eventually fails and may not block the other two mechanisms of AR activation. By directly and selectively blocking all known means of activating the AR, we believe EPI-506 holds the potential to be effective in cases where current therapies have failed.

2

| Management’s Discussion and Analysis | June 30, 2015 |

According to the Decision Resources Group, in 2014, there were approximately 213,000 prevalent cases of CRPC, and that prevalence is expected to increase to approximately 235,000 in 2023. We expect that EPI-506 could be effective for many of those patients. For the following reasons, we intend to first focus on patients who have failed abiraterone or enzalutamide therapies:

| · | CRPC treatment remains the prostate cancer market segment with the greatest unmet need and is therefore a potentially large market; |

| · | we believe that the unique mechanism of action of our product candidate is well suited to treat patients who have failed LBD focused therapies; and |

| · | we expect the large number of patients with unmet therapeutic needs in this area will facilitate timely enrollment in our clinical trials. |

EPI-506 is a potent pro-drug of EPI-002, a stereoisomer of our discovery compound, EPI-001. A pro-drug is a drug which after administration is converted into an active form through a normal metabolic process. Pro-drugs are typically utilized to administer and more efficiently deliver another drug, which in this case is EPI-002. We believe that EPI-506 can deliver higher concentrations of EPI-002 to the target tissue than EPI-002 itself. In our pre-clinical studies, EPI-001 has been shown to shrink benign prostate tissue in mice. The pro-drug EPI-506 has demonstrated similar biological effects at doses that are lower than those required for EPI-002.

The NTD of AR is flexible with a high degree of intrinsic disorder making it extremely difficult to be used for crystal structure-based drug design. To our knowledge, no crystal structure has been identified in the AR NTD that could facilitate development of drugs which interact with this domain. We are not currently aware of any success by other drug development companies in finding drugs that bind to this drug target.

Once we have been cleared by the FDA to commence clinical trials, we intend to initiate a Phase 1/2 clinical trial with approximately 150 patients, 30 in the Phase 1 dose-escalation group and 120 in the Phase 2 dose expansion group. Key enrollment criteria are progressive, metastatic CRPC for patients who are no longer responding to abiraterone or enzalutamide. Efficacy endpoints include PSA response and radiographic progression criteria. We will also assess biomarkers of resistance including the splice variant status of patients. A biomarker is a measurable biological or chemical change that is believed to be associated with the severity or presence of a disease or condition. If the Phase 1/2 trial is successful, we expect to seek approval from the FDA to commence a Phase 3 trial in a similar patient population.

The British Columbia Cancer Agency (“BCCA”) and the University of British Columbia (“UBC”) are joint owners of the intellectual property that constitutes our primary asset. We have entered into a joint agreement with those two institutions which provides them with exclusive access to the patent and patent applications to our EPI-series compounds, including EPI-506.

Our Strategy

Our therapeutic goal is initially to provide a safe and effective therapy for prostate cancer patients who have failed current therapies, and ultimately to treat all AR-dependent forms of recurrent or advanced prostate cancer. We intend to accomplish those objectives while maximizing shareholder value. Specific components of our strategy include:

Rapidly advancing EPI-506 through clinical development and regulatory approval in CRPC patients

Once we have been cleared by the FDA to commence clinical trials, we intend to initiate a Phase 1/2 trial to determine the safety, tolerability, maximum tolerated dose, pharmacokinetics and potential therapeutic benefits of EPI-506 in CRPC patients. We expect to complete this trial by mid-2017, depending on the FDA’s clearance of our IND. If the Phase 1/2 trial is successful and following authorization by the FDA, we expect to commence a Phase 3 trial in a similar patient population. In order to accelerate the development timeline, we intend to prepare for Phase 3 development concurrently with the execution of the Phase 1/2 trial.

3

| Management’s Discussion and Analysis | June 30, 2015 |

Developing EPI-506 as an essential component of a new standard of care for the treatment of pre-CRPC and expand usage earlier in the disease stage