Exhibit (a)(1)(B)

NOTICE OF INTENT TO TENDER

REGARDING

SHARES

OF

AB PRIVATE CREDIT INVESTORS CORPORATION

Tendered Pursuant to the Offer to Purchase Dated August 30, 2024

THE OFFER AND WITHDRAWAL RIGHTS WILL EXPIRE AT, AND THIS NOTICE OF INTENT TO TENDER MUST BE RECEIVED BY, 5:00 P.M. EASTERN TIME ON SEPTEMBER 30, 2024 (THE “EXPIRATION DATE”), UNLESS THE OFFER IS EXTENDED.

Complete this Notice of Intent to Tender and return or deliver it to your Bernstein advisor.

If you do not have a Bernstein advisor, you may return it to:

1345 Avenue of the Americas, Attn: Private Client, 40th Floor,

New York, New York, 10105; or fax it to (212) 407-5850.

For additional information, call your Bernstein advisor.

You may also direct questions to the main office of Bernstein at (212) 486-5800.

AB Private Credit Investors Corporation

The undersigned hereby tenders to AB Private Credit Investors Corporation, an externally managed, non-diversified, closed-end management investment company that has elected to be regulated as a business development company under the Investment Company Act of 1940, as amended (“AB PCIC” or the “Fund”), shares of the Fund’s common stock, par value $0.01 per shares (the “Shares”), held by the undersigned, described and specified below, on the terms and conditions set out in the Offer to Purchase, dated August 30, 2024 (the “Offer to Purchase”), receipt of which is hereby acknowledged, and in this Notice of Intent to Tender. THE OFFER AND THIS NOTICE OF INTENT TO TENDER ARE SUBJECT TO ALL THE TERMS AND CONDITIONS SET OUT IN THE OFFER TO PURCHASE INCLUDING, BUT NOT LIMITED TO, THE ABSOLUTE RIGHT OF THE FUND OR ITS AGENTS TO REJECT ANY AND ALL TENDERS DETERMINED BY IT, IN ITS SOLE DISCRETION, NOT TO BE IN THE APPROPRIATE FORM.

The undersigned hereby sells to the Fund the Shares tendered pursuant to this Notice of Intent to Tender. The undersigned warrants that it has full authority to sell the Shares tendered hereby and that the Fund will acquire good title to the Shares, free and clear of all liens, charges, encumbrances, conditional sales agreements or other obligations relating to this sale, and not subject to any adverse claim, when and to the extent the Shares are purchased by the Fund. Upon request, the undersigned will execute and deliver any additional documents necessary to complete the sale in accordance with the terms set out in the Offer to Purchase.

The undersigned recognizes that under certain circumstances set out in the Offer to Purchase, the Fund may not be required to purchase the Shares tendered hereby.

Until cash payment has been made, a non-interest bearing, non-transferable promissory note for the purchase price will be held in an account for the undersigned with AllianceBernstein Investor Services, Inc., the Company’s transfer agent and agent designated for this purpose. A copy may be requested by calling your Bernstein advisor and, upon request, will be provided to the undersigned at the email address on record with the Fund, or by mail at the address of the undersigned as maintained in the Fund’s records. Subsequently, cash payment of the purchase price for the Shares tendered by the undersigned will be made as instructed in Part 3 of this Notice of Intent to Tender. The undersigned understands that the purchase price will be based on the unaudited net asset value per Share as of September 30, 2024. All authority conferred or agreed to be conferred in this Notice of Intent to Tender will survive the death or incapacity of the undersigned and the obligation of the undersigned hereunder will be binding on the heirs, personal representatives, successors and assigns of the undersigned. Except as stated in the Offer to Purchase, this tender is irrevocable.

PLEASE FAX, MAIL OR EMAIL THIS NOTICE OF INTENT TO TENDER TO YOUR BERNSTEIN ADVISOR NO LATER THAN 5:00 P.M. EASTERN TIME ON THE EXPIRATION DATE. IF YOU DO NOT HAVE A BERNSTEIN ADVISOR, THIS NOTICE OF INTENT TO TENDER MUST BE RECEIVED IN GOOD ORDER, NO LATER THAN 5:00 P.M. EASTERN TIME ON THE EXPIRATION DATE, BY THE COMPANY’S TRANSFER AGENT, ALLIANCEBERNSTEIN INVESTOR SERVICES, INC., AT THE FOLLOWING ADDRESS: ALLIANCEBERNSTEIN L.P., 1345 AVENUE OF THE AMERICAS, ATTN: PRIVATE CLIENT, 40TH FLOOR, NEW YORK, N.Y. 10105; OR BY FAX TO (212) 407-5850. FOR ADDITIONAL INFORMATION CONTACT YOUR BERNSTEIN ADVISOR OR BERNSTEIN’S MAIN OFFICE AT (212) 486-5800.

PART 1 Stockholder Information:

| Name of Stockholder: (account name) |

| Account Number: |

PART 2 Shares Being Tendered: (specify one)

| ☐ | All of the undersigned’s Shares. |

Effect on Remaining Capital Commitment: By electing this option, stockholders that entered into a Capital Commitment (as defined in the Offer to Purchase) on or before September 30, 2021 will be released from such Capital Commitment and, if all Shares are accepted, will no longer be stockholders in the Fund.

Dividend Reinvestment Plan Election: If a stockholder has not opted in to the Dividend Reinvestment Plan, no action is necessary.

For stockholders that entered into a Capital Commitment on or before September 30, 2021, by virtue of delivery of this Notice of Intent to Tender, the election to tender all of the undersigned’s Shares shall be deemed an instruction to the Fund to notify State Street Bank and Trust Company (the administrator of the Fund’s Dividend Reinvestment Plan) of a change of election to have all dividends of the Fund paid in cash to the stockholder beginning with dividends payable on or after September 30, 2024.

For stockholders that have made Capital Commitments after September 30, 2021, the delivery of this Notice of Intent to Tender and tender of all of the undersigned’s Shares shall not be deemed an instruction to the Fund to notify State Street Bank and Trust Company of a change of election under the Fund’s dividend reinvestment plan, unless this box is checked to opt out of the Fund’s dividend reinvestment plan: ☐

| ☐ | A portion of the undersigned’s Shares expressed as the following percentage of current shareholdings: %. |

Effect on Remaining Capital Commitment:

Stockholders that entered into a Capital Commitment (as defined in the Offer to Purchase) on or before September 30, 2021 will be released from such Capital Commitment unless they elect to keep their Capital Commitment in effect by selecting an option below:

| ☐ | Maintain such Capital Commitment. |

| ☐ | Release from such Capital Commitment (Default election if no election is made). |

| ☐ | The following number of Shares: . |

Effect on Remaining Capital Commitment:

Stockholders that entered into a Capital Commitment (as defined in the Offer to Purchase) on or before September 30, 2021 will be released from such Capital Commitment unless they elect to keep their Capital Commitment in effect by selecting an option below:

| ☐ | Maintain such Capital Commitment. |

| ☐ | Release from such Capital Commitment (Default election if no election is made). |

PART 3 Payment:

If you want to request that 100% of the cash payment of the note be sent to a single destination, please check one option below and provide the relevant information:

| ☐ | Journal to Bernstein Account Number: |

| ☐ | Check Payable to: |

Mailing Address:

| ☐ | Wire or ACH Transfer (circle one) |

Destination Bank:

ABA Routing Number or BIC/SWIFT:

Mailing Address:

Recipient Institution:

Account Number:

Recipient/For Credit to: (Account Title)

Account Number: (if applicable)

Alternatively, if you want to request that cash payment of the note be divided among two or more destinations, please provide the relevant instructions in this section, specifying amounts and percentages as needed:

PART 4 Signature(s)

By signing below, you acknowledge that you have received and reviewed the Offer to Purchase and that the Fund will execute your tender request as detailed in Parts 1-3 unless a Notice of Withdrawal is properly submitted prior to the Expiration Date outlined in the Offer to Purchase.

|

|

|

| ||

| Print Signatory Name and Title (if any) | Signature | Date | ||

|

|

|

| ||

| Print Signatory Name and Title (if more than one) | Signature | Date | ||

|

|

|

| ||

| Print Signatory Name and Title (if more than one) | Signature | Date | ||

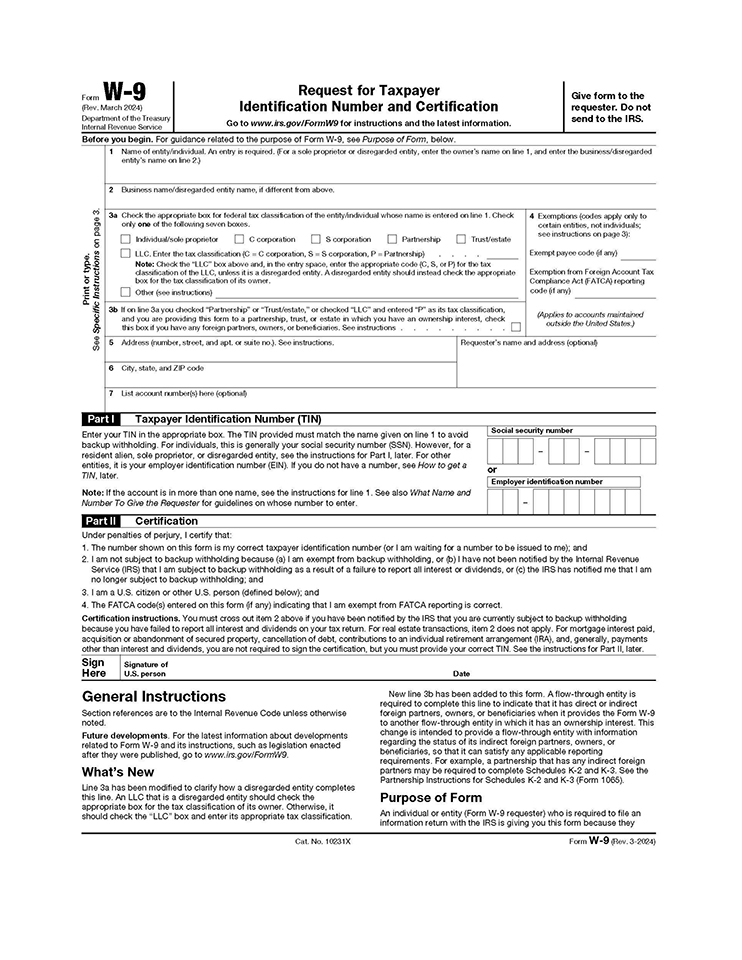

W-9 March 200 Dupetent of the Truy Request for Taxpayer Identification Number and Certification Go to www.is.gov/Form/9 for instructions and the latest information. Before you begin. For guidance related to the purpose of Form W-B, see Purpose of Form, below Give form to the requester. Do not send to the IRS. 1 Name of entity individuel. An entry is requirol, for a sole proprati or daregarded entity, onke the owner’s namo on Ine 1, and on for the besmens/dorogordoll Print or type. See Specific Instructions on page 3 of the Tollowing neven ent from dove Exmptune codas apply only t sec instructions on page India/sole propatetor Cccepionation Trust take LLC. Enter the tax classification (CC corporation, 8 & corporation, P-Partne Note: Check the “C” box above and in the entry space, onben the sapropriisto code, or for the tank dassification of the LLC, unless it is a disregan led ently, A disregarded endity should instead check the appropriate box for the box clacedication of Esoxa If online you chechal Parhnutslip on “Trustotale,” or chacked “LLC” wd enhed as its tax chatice and you arm providing this form to a partnership, truck, or estate a wibinh you have box if you foreign partners, owners, or benefits. See intructions ownership evtreet, check ã,³ Addres, shoot, and apt, or sullen. Sou lostudiom Requestor’s Exemp Account Tex Compliores Act (FATCA) raporting codo any Apolles to accours outside the Leuted State) adde foptiona City, state, and ZIP code List sccount numbaris been optal Parti Taxpayer Identification Number (TIN) Enter your TIN in the appropriate box: The TIN provided must match the name given on line 1 to avoid backup withholding. For indi liviclusis, this is generally your social security number (38) However for a resident alien, sole the instructions for Part I, later. For other entities, it is your employer identification number (EIN). If you do not have a number, see How to get a TIN lator Laten, sole proprietor, or disregarded entity, see Note: If the account is in more than one name, ses the instuctione for line 1. See also What Name and Number To Give the Requester for guidelines on whose number to enter Part II Certification Under penalties of perjury, I certify that Soolul security number 1. The number shown on this form le my correct taxpayer identification number for I am waiting for a number to be lasued to me and 2. I am not subject to backup withholding because (a) I am sxemat from hackup withholding, or (b) I have not been notified by the intemal Revenue Service (RS) that I am subject to backup withholding as a result of a fallure to report all interest or dividends, or (c) the RS has notified me that i am no longer subject to beckup withholding, and 3. I am a US citizen or other U.S. person idefined below); and 1. The FATCA code(s) entered on this form if any) indicating that I am exempt from FATCA reporting is correct. Certification instructions. You must cross out Item 2 above If you have been notified by the IRS that you are currently subject to backup withholding because you have fallet to report all interest and dividends on your tex maturn. For real estats transactions, item 2 does not apply. For mortgage interest paid, acquisition or or solandonment it of secured property, cancellationc nof debt, contributions to an individual retirement arrangement (RA), and, generally, payments other than interest and dividends, you are not required to sign the certification, but you must provide your correct T TIN See the instructions for Part I later Sign Here Signature of U.S. person General Instructions Section references are to the Intema Ravenue Code unless othenstoe noted Future developments. For the latest information about developments Form W-9 and ite instructions, such as legislation enacted published go to www.in.gov/Form related Neted to to Form after they What’s New Line 3a has been modified to clarify how a disregarded entity completes thie then the An LLC that is a disregarded entity should check the appropriate box for ropriate box fox classification of its owner Otherwise the fox classification of its owner. Otherwise, it classification should check the “LLC” box and enter its appropriate Date New line 3b has been added to this form. A flow-through entity is required to complete this line to indicate that it has direct or indirect foreign partners, owners, or beneficiaries when it provides the Form W-9 to another flow-through entity in which it has an ownership interest. This change is intended to provide a flow-through entity with Information regarding the status of its indirect foreign partners owners, or beneficianes, so that it can satisfy any applicable reporting requirements. For example, a partnership that has any indirect foreign partners may be required to complete Schedules K-2 and K-3 See the Partnership Instructions for Schedules K-2 and K-3 (Form 1085) Purpose of Form An individual or entity (Form W-9 requester) who is required to file an information return with the IRS is giving you this form because they Cat. No. 10231X Form W-93-200

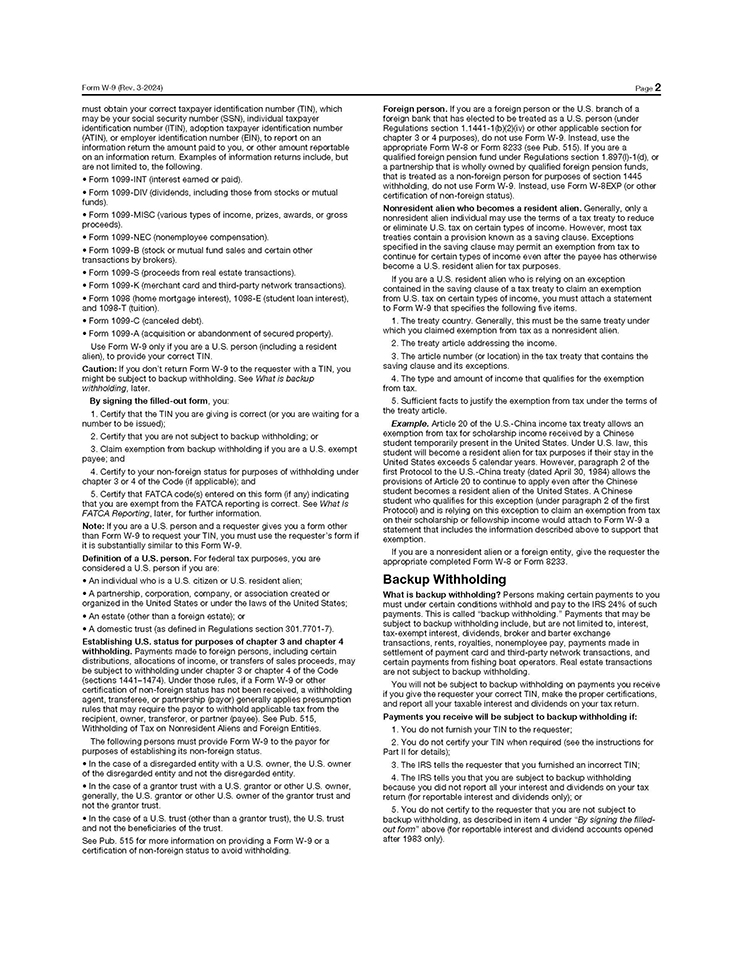

Fiem W F3-2004) must obtain your corect taxpayer identification number (TIN), which may be your social security number (SSN), individual taxpayer Identification number (ITIN), adoption taxpayer identification number (ATIN), or employer identification number (EIN), to report on an Information return the e an amount mount paid p to you or other amount amount reportable on an information retum. Examples of information returns include, but are not limited to, the following Form 1099-INT (Interest earned or paid). Form 1099-DIV (dividends, induding those from stocks or mutusk funds Form 1099-MISC (various types of income, prizes, awards, or grose8 proceeds) Form 1098-NEC (nonemployee compensation) Form 1000-B (stock or mutual fund sales and certain other transactions by brokers) Form 1099-5 (procoads from real estate transactions Form 1000-K (merchant card and third-party network transactione) Farm 1098 ihome mortgage interest). 1096-E (student loan interest), and 1098-T tuition) Form 1098-C canceled debt Form 1099-A(acquisition or abandonment of secured property). Use Form W-9 only if you are a US. person including a resident alien), to provide your correct TIN Caution: If you don’t return Form W-9 to the requester with a TIN, you might be subject: to beckup withholding hholding. See withholding What re backup By signing the filled-out form, you 1. Certify that the TIN you are giving is correct for you are waiting for a number to be issued 2. Certify that you are not subject to backup withholding, or 3. Claim exemption from backup withholding if payse, and you are a U.S. exempt 4. Certify to your non-foreign statue for purposes of withholding under chapter 3 or 4 of the Code of applicable and 5. Certify that FATCA code(s) entered on this form (if any) indicating that you are exempt from the FATCA reporting is correct. See What is FATCA Reporting, later, for further information Note: If you are a US person and a requester gives you a form other than Form W-9 to request your TIN, you must use the requester’s form if it is substantially similar to this Form W-9. Definition of a U.S. person, For federal tax purposes, you are considered a US person if you are: An individual who is a US citizen or US resident aller A partnership, corporation, company, or assocation created or organized in the United States or under the laws of the United States; An estate (other than a foreign estate); Adomestic trust (as defined in Regulations section 301.7701-7) Establishing U.S. status for purposes of chapter 3 and chapter 4 withholding. Payments made to foreign persons, including certain distributions, allocations of income, or transfers of sales proceeds, may be subject to withholding under chapter 3 or chapter 4 of the Code 1441-1474 Under 1441-147- 4 Under those rules if if a Form Form W-B or other (sectione 1 certification of non-foreign status has not been received, a withholding agent transferee, or partnership (payori generally applies presumption rules that may require the payor to withhold applicable tax from the recipient, owner, transteror, or partner (payee) See Pub. 515 Withholding of Tax on Nonresident Allens and Foreign Entitice. The following persons must provide Form W-9 to the payor for purposes of establishing its non-t foreign statua in the case of a disregarded entity with a U.S. owner, the U.S. owner of the disregarded entity and not the disregarded entity. In the case of a grantor trust with a U US grantor generally, the U.S. grantor or other US owner of not the grantor trust. owner, or other US owner, the grantor trust and In the case of a U.S. trust (other than a grantor trust, the US trust and not the beneficiaries of the trust. See Pub, 516 for more information on providing a Form W-9 or a certification of non-foreign status to avoid withholding. Page 2 Foreign person. If you are a foreign person or the U.S. branch of a foreign bank that has elected to be treated as a U.S. person (under Regulations section 1.1441-1bx230V) or other applicable section for chapter 3 or 4 purposes) do not use Form W-9 Instead, use the appropriate Form W-B or Form 8233 (see Pub. 515) If you are a qualifi fied foreign pension fund under Regulations section 1.897(0-1)d, or a partnership that is wholly owned by qualified foreign pension funds, that is treated as a non-foreign person for purposes of section 1445 withhsking, do not use Form W-9, Instead, use Form W-BEXP (or other certification of non-foreign status) Nonresident allen who becomes a resident alien. Generally, only a nonresident allen individual may use the terms of a tax Tax treaty to reduce Income How’s However or most tax or eliminate US tax on certain types of income. Ho treaties contain a provision known as a saving clause. Exceptions specified in the saving disuse may permit an exemption from tax to continue certain types of income even after the payee has become US resident alien for tax purposes. If you are a U.S. resident alien who is relying on an exception use of tax treaty to deim an exemption contained in the saving cau on certain types of income, you must attach a statement from US from US to Farm W- that specifies the following five items 1. The treaty country, Generally, this must be the same treaty under which you claimed exemption from tax 2. The treaty article addressing the income. nonresident alion 3. The article number for location in the tax treaty that contains the saving clause and its exceptions 4. The type and amount of income that qualifies for the exemption fron tax 5. Sufficient facts to justify the exemption from tax under the terme of the treaty article Example. Article 20 of the US China Income tax treaty allows an exemption from tax for scholarship income received by a Chinese student temporarily present in the United States. Under U.S. law, this student will become a resicient allen for tax purposes if their stay in the United States exceeds 5 calendar years. However, paragraph 2 of the first Protocol to the U.S.-China treaty (dated April 30, 1984) allows the provisions of Article 20 to continue to apply even after the Chinese student becomes a resickent allen of the United States. A Chinese student who qualifies for this exception (under paragraph 2 of the first Protocol) and is relying on this exception to claim an exemption from tax on their scholarship or fellowship income would attach on their scholarship ip or telowship in e would attach to to Farm W- statement that includes the information described above to support that exemption If you are a nonresident allen or a foreign entity, give the requester the appropriate completed Form W-B or Form 8233 Backup Withholding What is backup withholding? Persons making certain payments to you must under certain conditions withhold and pay to the IRS 24% of such payments. This is called backup withholding. Payments that may be subject to backup withholding include, but are not limited to, interest, tax-exempt interest, dividends, broker and barter exchange transactione, rents, royalties, nonemployee pay, payments made in from fishing boat operate perators. rators. Real estate tramactions tra are not subject to backup withholding. settlement of payment card and third-party network transactions, and certain payments from fishing boat ope You will not be subject to backup withholding on payments you receive If you give the requester your correct TIN, make the proper certifications and report all your taxable dividends on your tax return Payments you receive will be subject to backup withholding if 1. You do not fumish your TIN to the requester 2. You do not certify your TIN when required see Part for details 3. The IFRS tells the requester that you furished an incorrect TIN. the instructions for 4. The IRS tells you that you are subject to backup withholding because you did not report all your interest and dividends on your tax retum for reportable interest and dividends only): . You do not certify to cester that you not subject to 5 backup withholding, as described in item 4 under “By signing the filed out form sbove for reportable interest and dividend accounts opened

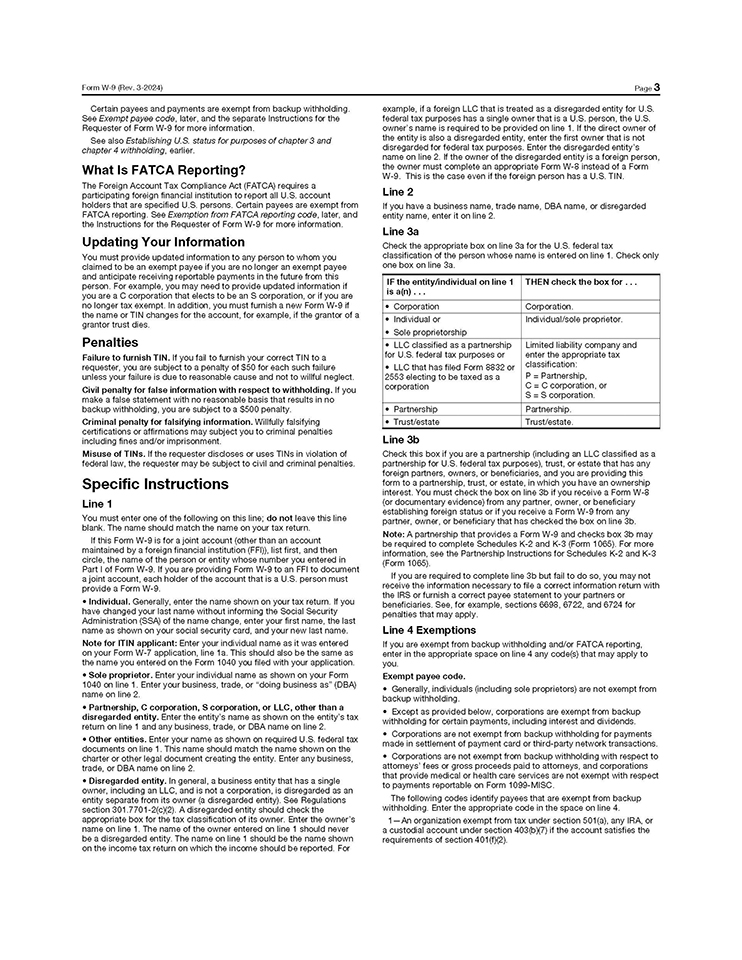

Fiem W F3-2004) Certain payees and payments are exempt from backup withholding. See Exempt payee code, later, and the separate instructions for the Requester of Form W-B for more information. See also Establishing US status for purposes of chapter 3 and chapter & withholding, earlier What Is FATCA Reporting? The Foreign Account Tax Compliance Act (FATCA) requires participating foreign financial institution to report all US account holders that are specified US persons. Certain payees are exempt from FATCA reporting. See Exemption from FATCA reporting code, luter, anci the Instructions for the Requester of Form W- for more information Updating Your Information You must provide updated information to any person to whom you claimed to be an exempt payee if you are no longer an exempt payee and anticipate reportable payments in the future from this person. For example, you may need to provide upciated information if you are a C corporation that elects to be an & corporation, or if you are no longer tax exempt in addition, you must fumish a new Form W-98 the name or TIN changes for t the account, for example, if1 rantor trust dies grantor trust dies If the grantor of a Penalties Failure to furnish TIN. If you fall to furnish your corect TiN to a requester, you are subject to a penalty of 350 for each such failure unless your fallure is due to reasonable cause and not to wiltd neglect Civil penalty for false information with respect to withholding. If you make a false statement with no reasonable basis that results in no backup withholding, you subject to a $500 penalty. y Criminal penalty for talsityi penalty for talksitying information. Withully falsifying certifications or affirmations may subject you to criminal penalties Including fines and/or imprisonment Misuse of TINs. If the requester discloses or usen TiNo in violation of federal law the requéeter may be subject to divil and criminal penalties. Specific Instructions Line 1 You must enter one of the following on this line; do not leave this fine. blank. The name should match the name on your tax return It this Form W-9 is for a joint account (other than an account maintained by a foreign financial institution (FFI) list first, and then circle, the name of the person or entity whose number you entered in Part I of Form W-0. If you are providing Form W-9 to an FFI to document a joint account, each holder of the account that is a U.S. person must provide a Form W-9 Individual, Generally, enter the name shown on your tax retum if you have changed your last name without informing the Social Security Administration (354) of the name change, enter your first name, the last name as shown on your social secunty card, and your new last name. Note for ITIN applicant: Enter your individual name as it was entered on your Form m W-7 application on, line 16. This should also be the the same as the name you entered on the Form 1040 you fled with your application Sole proprietor. Enter your individual name as shown on your Form 1040 on line 1. Enter your business, trade, or “doing businese as DBA nama on line 2 Partnership, C corporation, Scorporation, or LLC, other than a disregarded antity. Enter the entity’s name as shown on the entity’s tax return on line 1 and any business, trade, or DBA name on line 2. Other entities. Enter your name as shown on required U.S. federal tax documents on line 1.1 This name should match the name shown оп shown on the the charter rter or other legal document creating the entity. Enter Enter any any business trade, or DBA name on line li 2 Disregarded antity, in general, a business entity that has a single owner, including an LLC, and is not a corporation, is disregarded as an entity separate from its owner la dieregarded entity) See Regulations saction 301.7701-2(c)(2). A disregarded entity should check the appropriate box for the tax classification of its owner. Enter the owner’s name on the 1. The name of the comer entered onlar be a disregarded entity entity The name name on on line 1 shoul hould be the name shown on the income tax retum on which the income should be reported. For he Page 3 example, if a foreign LLC that is treated as a disregarded entity for U.S. fecleral tax purposes has a single owner that is a U.S. person, the US. owner’s name is requered to be provided on line 1. If the direct owner of the entity is siso a disregarded entity, enter the first owner that is not Enter the dlaregarded disregarde ded entity’s diaregarded dieregard for federal tax purposes. Enter the name on line 2. If the If the owner o of the disregarded 4 1 entity le a foreign person, the owner must complete an appropriate Form W-8 instead of a Form aven if the foreign person has a US TIN. W- This Line 2 If you have a business nama, trade name, DEA name, or disregarded entity name, enter it on line 2. Line 3a Check the appropriate box on line 3s for the U.S. federal tax classification of the person whose name is entered on line 1. Check only one box on line 38. IF the entity/individual online 1 THEN check the box for.... Corporation Individual or Sole proprietorship LLC classified as a partnership for U.S. federal tax purposes or LLC that has filed Form 8832 or 2553 electing to To be taxed as a corporation Partnership Trust/estate Line 3b Check this box if you are a partnership (including an LLC classified as a Corporation Individual/ssle proprietor Limited liability company and enter the appropriate tax classification Partnership, CC corporation, or SS corporation, Partnership Trust/estate partnership for U.S. federal tax purposes), trust, or estate that has any foreign partners, owners, or beneficiaries, and you are providing this form to a partnership, trust, or estate, in which you have an ownership interest. You must check the box on line 3b if you you receive s Form W-8 for documentary evidence) from any partner owner, or or beneficiary establishing foreign status or if you receive a Form W- from any partner, owner or beneficiary that has checked the box on line 35 Note: A partnership that provides a Form W-9 and checks box 35 may be required to complete Schedules K-2 and K-3 Form 1065). For more Information, see the Partnership Instructions for Schedules K-2 and K-3 (Farm 1066) If you are required to complete line 2b but fail to do so, you may not receive the information necessary to the correct information return with the IRS or furnish a correct payse statement to your partners or beneficiartes. See, for example, sections 6698,6722 penalties that may apply 6724 for Line 4 Exemptions If you are exempt from backup withholding and/or FATCA reporting enter in the appropriate space on line 4 any code(s) that may apply to you Exempt payee code. Generally, individuals (including sole proprietors) are not exempt from backup withholding. Except as provided below, corporations are exempt from backup withholding for certain payments, including interest and dividends Corporations not exempt from backup withholding for payments made in settlement of payment card or third-party network transactions Corporations are not exempt from backup withholding with respect to attorneys tees or gross proceeds paid to attorneys, and corporations that provide medical or health care services are not exempt with respect to payments reportable on Form 1099-MISC The following codes identify payees that are exempt from backup. withholding. Enter the appropriate code in the space on line 4 1-An organization exempt xempt from from tax under secte section 501( ection 501, any IRA, or a custodial account under section 403b)(7) if the gocount satisfies the requirements of section 4012)

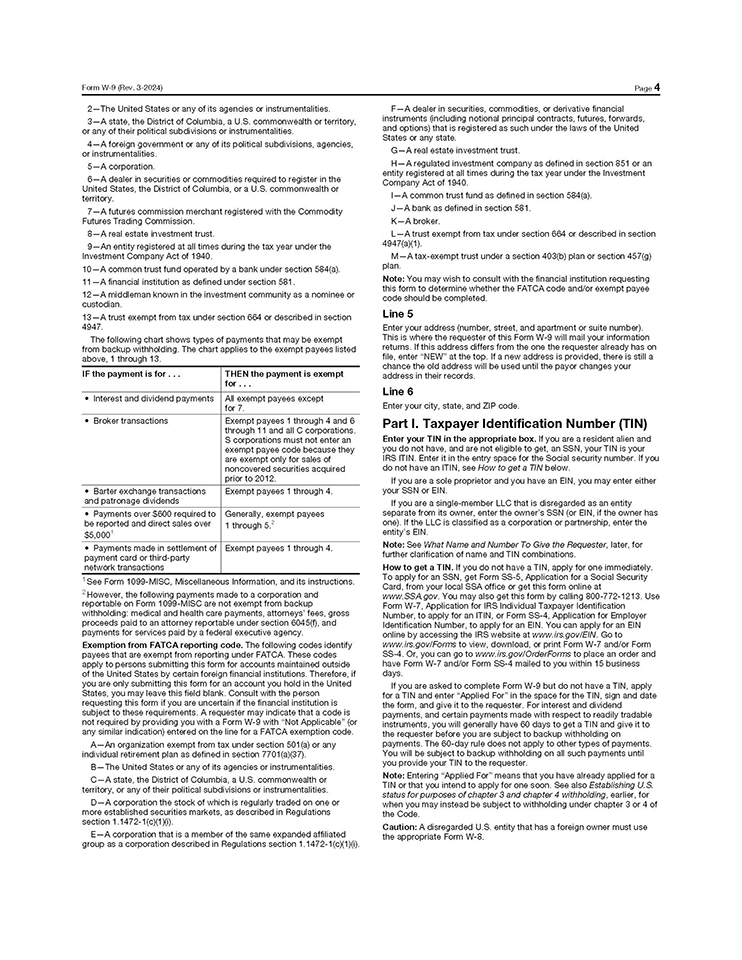

Fiem W F3-2004) 2-The United States or any of its agendes or instrumentalities 3-A state, the District of Columbia, a US commonwealth or territory, or any of their political subdivisions or instrumentalities. 4-A foreign gavemmant or any of its political subdivisions, agendes or instrumentalities. 5-A corporation. 6-A dealer in securities or commodities required to register in the United States, the District of Columbia, a U.S. commonwealth or territory 7-A futures commission merchant registered with the Commodity Futures Trading Commission B-A real estate investment trust. 9-An entity registered at all times during the tax year under the Investment Company Act of 1940. 10-A common trust fund operated by a bank under section 584(a). 11-A financial institution as defined under section 581. 12-A middleman known in the investment community as a nominee of custodian. 13-A trust exempt from tax under section 664 or described in section 4047 The following chart shows types of payrnents that may be exempt from backup withholding. The chart applies to the exempt payées listed above 1 through 13 IF the payment is for THIEN the payment is exempt for Interest and dividend payments All exempt payees except for 7. Broker transactions Barter exchange transactions and patronage dividends Payments over $600 required to be reported and direct sales over $6,000 Generally exempt payees 1 through S Exempt payees 1 through 4 and 6 through 11 and all C corporations corporations must not enter an exempt payee code because they are exempt only for sales of noncovered securities acquired prior to 2012 Exempt payees 1 through 4. Payments made in settlement of Exempt payees 1 through 4. payment card or third-party network transactions See Form 1000-MISC, Miscellaneous Information, and its instructions. However, the following payments made to a corporation and reporta on Form are not exempt backup withholding medical and health care payments, attomeys fees, gross proceeds paid to an attomey reportable under section 6045(1), and payments for services paid by a federal axecutive agency Exemption from FATCA reporting code. The following codee identify payees that exempt from reporting under FATCA These codes apply to persones submitting this form for accounts maintained outside of the United Statee by certain foreign financial institutions. Therefore, if you are only submitting this form for an account you hold in the United States, you may leave this field blank. Consult with the person requesting this form if you are uncertain if the financial institution is subject to these requirements. A requester may indicate that a code is not required by providing you with a Form W-9 with “Not Applicable for any similar indication) entered on the ine for a FATCA exemption code A-An organization exempt from tax under section 501(8) or any Individual retirement plan as defined in section 7701(0(37) B-The United States or any of its agencies or instrumentalities. C-A state, the District of Columbia, a U.S. commonwealth or territory, or any of their political subdivisions or instrumentalities. D-A corporation the stock of which is regularly traded on one more established securities securities markets, m described in Regulations section 1.1472-1(c)(1)0) E-A corporation that is a member of the same expanded affliated a corporation cribed in Regulations section 1.1472-1 (cx10) group Page 4 F-A dealer in securities, commodities, or derivative financial instruments including notional principal contracts, futures, forwarcis, and options that is registered as such under the laws of the United States or any state G-Areal estate investment trust. H-Aregulated investment company as defined in section 851 or an enbty registered at all times claring the tax year under the Investment Company Act of 1940 1-A common trust tund as defined in section 5840 J-A bank as defined in section 561 K-A broker L-A trust exempt from tax under section 664 or described in section 49478)(1) M-Atax-exempt frust under a section 403/b) plan or section 457g) plan Note: You may wish to consult with the financial institution requesting this form to to determine whether the FATCA code and/or exempt payee code should be completed Line 5 Enter your address (number, street, and apartment or suite number) This is where the requester of this Form We will mall your information returne. If this addrees differs from the one the requester already has on fils, enter “NEW” at the top. If a new acidress is provided, there is chance the old address will be used until the payor changes your address in their records Line 6 Enter your city, state, and ZIP code Part I. Taxpayer Identification Number (TIN) Enter Enter your your TIN in the appropriate box, if you are have and are not hove, and arasident allen and are not eligible to o to get, an SSN, your TIN is your IFS ITIN. Enter it in the entry spacs for the Social security number. If you do not have an ITIN, see How to get a TIN below. If you are a sole proprietor and you have an EIN, you may enter either your SSN or EIN. you are a single-member LLC that is disregarded as an entity separate from its owner, enter the owner’s SSN for EIN, if the owner has onej if the LLC is claserfied as a corporation or partnership, enter the entty’s EIN Note: See What Neme and Number To Give the Requester, later, for further carification of name and TIN combinations How to get a TIN. If you do not have a TIN, apply for one immediately. To apply for an SSN, get Form SS-5, Application for a Social Security Card, from your local SSA office or get this form online at www.SSA.gov. You may also get this form by calling 800-772-1213. Use Form W-7 Application for IRS Individual Taxpayer Identification Kumber, to apply for an ITIN, or Form SS-4, Application for Employer Identification Number, to apply for an EIN You can apply for an EIN online by accessing the IRS website at www.irs.gov/EIN Go to rs.gow/Forme to view, download, or print Form W-7 and/or and/or Form 88-4. Or, you can go to www.lis.gov/OrderForms to place an order and have Form W-7 and/or Fom 38-4 maled to you within 15 business days If you are asked to complete Form W- but do not have a TIN, apply for a TIN and enter “Applied For in the space for the TIN, sign and date e form, and give it to the requester For interest and dividend payments ints, and cartsin and catsin pay payments made with respect to readily tradable Instruments, you will generally have 60 days to get a TiN and give it to the requester before you are subject to backup withholding on syments. The 60-day rule does not apply to other types of payments. You will be subject to backup withholding on all such payments until you provide your TIN to the requester. end to apply for one a on. See also chapter 3 and chapter Note: Entering “Applied For means that you have already appited for a TIN or that you intenc intend to Establishing US status for purposes of c 4 withholding, earlier, for when you may hetead be subject to withholding under chapter 3 or 4 of the Code Caution: A disregarded U.S. entity that has a foreign owner must use the appropriate Form W-8

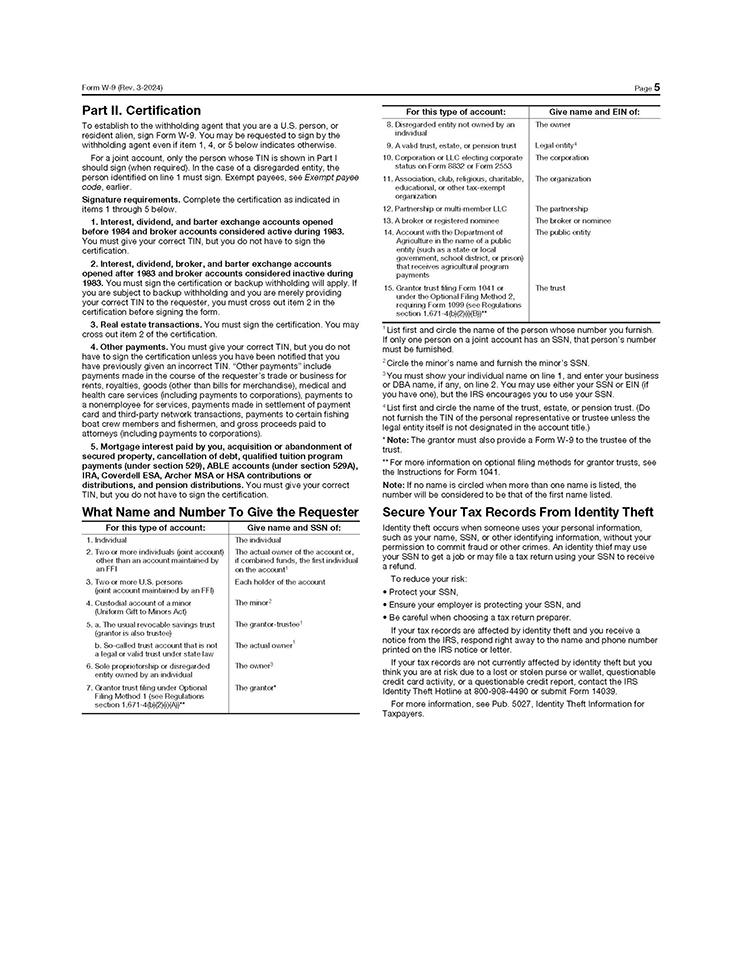

Fiem W Few 3-2004) Part II. Certification To establish to the withholding agent that you are a U.S. person, or resident alien, sign Form W-9. You may be requested to sign by the withholding agent even if Itern 1, 4 or 5 below indicates otherwise. For a joint account, only the person whose TIN is shown in Part I should sign (when required). In the case of a disregarded entity, the person identified on line 1 must sign. Exarnpt payees, see Exempt payee code, earlier Signature requirements, Complate the certification as indicated in items 1 through 5 below. 1. Interest, dividend, and berter exchange accounts opened before 1984 and broker accounts considered active during 1983. You must give certification. corect TIN, but you do no sign the 2. Interest, dividend, broker, and barter exchange accounts opened after 1983 and broker accounts considered inactiva during 1983. You must sign the certification or backup withholding will apply. If you are subject to backup withholding and you are merely providing your correct TIN to the requester, you must cross out item 2 in the certification before the form 3. Real estate transactions. You must sign the ross out item 2 of the certification. certification. You may 4. Other payments. You must give your corect TIN, but you do not have to sign certification unless you have been notified that you have previously given incorrect TIN. “Other payments” include payments made in the course of the requester’s trade or businees for rents, royalties, goods (other than bills for merchandise), medical and health care services including payments t to corpo corporations), porations), payme payments to nonemployee for services, payments made in settlement of payment card and third-party network transactions, payments to certain fishing boat crew members fishermen, and gross proceeds paid to attorneys (Including payments to corporations) 5. Mortgage Interest paid by you, acquisition abandonment of secured property, cancellation of debt, qualified tuition program ints (under section 529. ABLE accounts (under section 5294) IRA, Coverdell ESA, Archer her MSA or HSA contributions tributions distributions, and pension distributions. You must gi sign the certification. What Name and Number To Give the Requester For this type of account: 1 Give na and SSN ct: 2. Two more individual grant account odver than The actuel owner of the account o combered funds, the fast individual the account! Each holder of the scount The minc Undom Gitt to Man Act The usasi revooble savings trust The grantor-bastes b. So-called truet n a logul or valid that under state law The actuntoaner 0. Sole proprietorship or dretegarded The cur entity owned by in ind Grantor brusting under Ophonel The gombae For this type of account 8. Dieresgarded entity not owned by an Corporation or LLC slecting corpseste status on Form Form 2553 11. Association, du kom, durable, Page 5 Give name and EIN of: The owner Legal entity The corponition Tekon odunstkanal or offer tax-xompt orgarization A broker in registered nomince 14. Account with the Department of Apiculture in the name of a pubiko only couch am a state or lock povomment, school district, or person that receives agricultural program payments The perishep The broker The public entity 1041 ning Form 1099 Regulations The trust List first and cirde the name of the person whose number you furnish If only one person on a joint account has an SSN, that person’s number must be fumished. Cirde the minor’s name and furnish minor’s SSN You must show your individual name on line 1. and enter your business or DBA name, if any, on line 2. You may use either your SSN or EIN you have one, but the IRS encourages you to use your SSN. List first and cirde the name of the trust, estate or pension trust Do not furnish the TIN of the personal representative or trustee unless the legal entity itself is not designated in the account title) Note: The grantor must also provide a Form W-9 to t trust. o the trustee of the For more information on optional Bling methods for grantor trusts, s the Instructions for Form 1041. Note: If no name is cirdied when more than name is listed, the considered to be that of the first name listect Secure Your Tax Records From Identity Theft Identity theft occurs when someone uses your personal information, such as your name, SSN. or rather identifying information, without your ather identifying information permission to commit fraud or other crimes. An identity thief may use your SSN to get a job or may file a tax return using your SSN to receive a refund To reduce your fisk Protect your SSN. Ensure your employer is protecting your SSN, and Be careful when choosing a tax retum preparer If your tax records are affected by identity theft and you receive a notice from the IFS, respond right away to the name and phone number printed on the IRS notice or letter. not currently affected by identity theft but you your tax records think you are st risk due to a lost or stolen purse or wallet, questionable credit card activity, or a questionable credit report, contact the IRS Identity Theft Hotline at 800-908-4480 or submit Form 14039. For more information, see Pub. 5027, Identity Theft Information for

Fiem W F3-2004) Victims of identity theft who are experiencing economic hamm or a systemic problem, or are seeking help in resobing tax problems that have not been resolved through normal channels, may be eligible for Taxpayer Advocate Service (TAS) assistance. You can reach TAS by Taxpayer TAS toll-free case intake line at 877-777-4778 or TTY/TDD 800-829-4060 Protect yourself from suspicious emails or phishing schemes. Phishing is the creation and use of emall and websites designed to mimic legitimate business emals and websites. The most common act is sending an email to a user falsely claiming to be an established legitimate enterprise in an attempt to soam the user into surrendering private information that will be used for identity theft The IRS does not initiate contacts with taxpayers vis emas. Also, the IRS does not request personal detailed information through email or ask taxpayers for the PIN numbers, passwords, or similar secret accees information for their credit card, bank, or other financial accounts. If you receive an unsolicited email claiming to be from the IRS forward this message to phishingtis.gov. You may also report misuse of the IRS name, logo, or other RS property to the Treasury Inspector General for Tax Administration (TIGTA) at 800-386-4484. You can forward suspicious emails to the Federal Trade Commission at spamiluce gov or report them at www.ftc.gov/complaint. You can contact the FTC at www.ftc.gov/ldtheft or 877-IDTHEFT (877-438-4338) If you have been the victim of identity theft, see www.fdentity Theft.go and Pub. 5027 Go to www.irs.gov/Identity Theft to in how to reduce your risk. bout identity theft and Page 6 Privacy Act Notice Section 6108 of the internal Fievenue Code requires you to provide your correct TIN to persons including federal agencies) who required to the information returns with the IRS to report interest, dividends, certain other Income paid to you, mortgage interest you palct, the acquisition or abandonment of secured property, the cancellation of made to an IRA. Arch MSA or HSA The person collecting this form uses the information in on on t the form to file Information retums with the IRS, reporting the above information Routine uses of this information include giving it to the Department of debt, or contributions you made to an IRA, Archer Justice for civil and criminal litigation and to cities, states, the District of Colarbia and US commonwealths and territories for use in administering their laws. The information may also be disclosed to other countries under a treaty, to federal and state agencies to enforce divil and cominal laws, or 10 federal law enforcement and intelligence agencies to combat terrorism. You must provide your TIN whether or not xu are required to file a tax ratum. Under section 3406, payors must you generally erally w withhold a percentage of taxable interest, dividends, and certain other payments to a payee who does n not give a TIN to the payor Certain penalties may also apply for providing false or fraudulent Information.