UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-23161

Nushares ETF Trust

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Diana R. Gonzalez

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: July 31

Date of reporting period: July 31, 2021

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

Nuveen Exchange-Traded

Funds

| Fund Name | | Listing Exchange | Ticker Symbol | |

| Nuveen Enhanced Yield U.S. Aggregate Bond ETF | | NYSE Arca | NUAG | | |

| Nuveen Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF | | NYSE Arca | NUSA | | |

| Nuveen ESG High Yield Corporate Bond ETF | | NYSE Arca | NUHY | | |

| Nuveen ESG U.S. Aggregate Bond ETF | | NYSE Arca | NUBD | | |

As permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds' annual and semi-annual shareholder reports will not be sent to you by mail unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds' website (www.nuveen.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

You may elect to receive shareholder reports and other communications from the Funds electronically at any time by contacting the financial intermediary (such as a broker-dealer or bank) through which you hold your Fund shares.

You may elect to receive all future shareholder reports in paper free of charge at any time by contacting your financial intermediary. Your election to receive reports in paper will apply to all funds held in your account with your financial intermediary.

Life is Complex.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your e-mail!

www.investordelivery.com

If you receive your Nuveen Fund distributions and statements from your financial professional or brokerage account.

or

www.nuveen.com/client-access

If you receive your Nuveen Fund distributions and statements directly from Nuveen.

Must be preceded by or accompanied by a prospectus.

NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE

Chair’s Letter to Shareholders

Dear Shareholders,

More than a year has passed since the World Health Organization declared COVID-19 a global pandemic in March 2020, resulting in a year marked by a global economic downturn, financial market turbulence and some immeasurable losses of life. Although the health crisis persists, with the widespread distribution of vaccines in the U.S. and extraordinary economic interventions by governments and central banks around the world, we collectively look forward to what our “new normal” might be.

Rebounding global economic activity has driven both gross domestic product growth and inflation higher, especially in the U.S. Vaccinations have enabled a further reopening of economies while governments and central banks have taken extraordinary measures to support the recoveries. Since the crisis began, the U.S. government has enacted six relief measures totaling $5.3 trillion to support individuals and families, small and large businesses, state and local governments, education, public health and vaccinations. Currently, Congress is working on an infrastructure spending plan, although its final shape and whether it passes remains to be seen. The U.S. Federal Reserve (Fed) and other central banks around the world have acknowledged the economic progress to date but remain committed to sustaining the recovery by maintaining accommodative monetary conditions. However, as economies have reopened, the surge in consumer demand has outpaced supply chain capacity, resulting in a jump in inflation indicators in recent months. Whether inflation persists is a subject of debate by economists and some market observers, while the Fed and other central banks believe it to be more transitory. Additionally, the recent impact of the COVID-19 delta variant is likely to be factored into central bank forecasts, which could complicate the timing of monetary policy changes.

While the markets’ longer-term outlook has brightened, we expect intermittent bouts of volatility to continue. There are some signs that the first economies to recover – including China, the U.S. and Europe not far behind – have reached their growth peaks and are moving toward stabilization, while the delta variant is adding caution to the growth outlook. Markets are closely monitoring central bank signals, particularly if inflation remains elevated, as a sooner-than-expected shift to monetary tightening could slow the economic recovery. Additionally, as more virulent strains of COVID-19 such as the delta variant have spread, both case counts and hospitalizations are rising again, and vaccination rollouts have been uneven around the country and around the world. The recovery hinges on controlling the virus, and estimates vary considerably on when economic activity might be fully restored and what level of public inoculation would be sufficient to contain the spread of the virus, particularly in light of new variants. On the political front, the Biden administration’s full policy agenda and the potential for Congressional gridlock remain to be seen, either of which could cause investment outlooks to shift. Short-term market fluctuations can provide your Fund opportunities to invest in new ideas as well as upgrade existing positioning while providing long-term value for shareholders. For more than 120 years, the careful consideration of risk and reward has guided Nuveen’s focus on delivering long-term results to our shareholders.

If you have concerns about what’s coming next, it may be an opportune time to assess your portfolio. We encourage you to review your time horizon, risk tolerance and investment goals with your financial professional.

On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Terence J. Toth

Chair of the Board

September 24, 2021

Portfolio Managers’

Comments

Nuveen Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

Nuveen Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (NUSA)

Nuveen ESG High Yield Corporate Bond ETF (NUHY)

Nuveen ESG U.S. Aggregate Bond ETF (NUBD)

These Funds feature portfolio management by Teachers Advisors, LLC, an affiliate of Nuveen Fund Advisors, LLC. Portfolio managers include Lijun (Kevin) Chen, CFA, and Yong (Mark) Zheng, CFA. Kevin has managed the Funds since their inceptions and Mark was added as a portfolio manager in June 2018.

Here the portfolio management team discusses U.S. economic and market conditions, key investment strategies and the performance of the Funds for the twelve-month reporting period ended July 31, 2021. For more information on each Fund’s investment objectives and policies, please refer to each Fund’s prospectus.

What factors affected the U.S. economy and the bond market during the twelve-month annual reporting period ended July 31, 2021?

Supported by massive fiscal and monetary stimulus and economic reopening, the U.S. economy rebounded more quickly than expected from the deep downturn caused by the COVID-19 crisis and containment measures. The federal government’s relief measures have totaled approximately $5.3 trillion across six aid packages that have allocated direct payments to individuals and families, expanded unemployment insurance, provided loans to large and small businesses, funded hospitals and health agencies, and supported state and local governments, education and public health/vaccination. (Additionally, in August 2021, after the close of this reporting period, the Senate approved a $1 trillion infrastructure and jobs plan, which moves to the House for consideration.) The U.S. Federal Reserve (Fed) has maintained short-term interest rates near zero and enacted credit facilities to help keep the financial system stable, lowering borrowing costs for businesses and individuals. Gross domestic product (GDP) expanded at an annualized rate of 6.3% in the first quarter and 6.5% in the second quarter, according to the “advance” estimate released by the Bureau of Economic Analysis, after shrinking 3.5% (annualized) in 2020 compared to 2019’s annual level.

By the start of this reporting period, markets had largely stabilized from the initial health crisis shock. In March 2020, equity and commodity markets sold off and safe-haven assets rallied as countries initiated quarantines, restricted travel and shuttered factories and businesses, while an ill-timed oil price war between the Organization of the Petroleum Exporting Countries (OPEC) and non-OPEC member Russia amplified price volatility. In late 2020, the announcement of high efficacy rates in several COVID-19 vaccine trials, fol-

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Each Fund uses credit quality ratings for its portfolio securities provided by Moody’s, S&P and Fitch. For NUAG and NUSA, if all three of Moody’s, S&P, and Fitch provide a rating for a security, an average of the ratings is used; if two of the three agencies rate a security, an average of the two is used; and if only one rating agency rates a security, that rating is used. For NUHY and NUBD, if all three of Moody’s, S&P, and Fitch provide a rating for a security, the middle rating is used; if two of the three agencies rate a security, the lower rating is used; and if only one rating agency rates a security, that rating is used. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC/CC/C and D are below-investment grade ratings. Credit ratings are subject to change. U.S. Treasury, U.S. Agency, and U.S. Agency mortgage-backed securities are included in the U.S. Treasury/Agency category.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Portfolio Managers’ Comments (continued)

lowed by regulatory authorizations and public vaccination drives across Western countries, improved the outlook for 2021, which contributed to risk-on sentiment in the markets. Increasing vaccination rates and certain surprisingly strong economic readings in the first few months of 2021 led to rising inflation concerns. However, recent Fed commentary pointed to Fed Fund rate hikes by 2023, calming market fears of inaction.

The improving economy and rising inflation pressures steepened the yield curve and drove interest rates higher. Rates had peaked in the first quarter of 2021 then partially retreated by the end of the reporting period. As of July 31, 2021, yields on U.S. Treasuries with 1-year maturities fell to 0.07% (from 0.11% as of July 31, 2020), 5-year Treasury yields rose to 0.69% (from 0.22%), 10-year yields rose to 1.23% (from 0.54%) and 30-year yields rose to 1.90% (from 1.20%). While government bond performance was negative for the reporting period, spread sectors (non-governmental fixed income investments with higher yields at greater risk than governmental investments) generally outperformed as credit spreads continued to narrow. Demand for incremental yield remained strong, with risk appetite supported by economic and vaccine optimism, accommodative monetary policy signals from the Fed and anticipated fiscal stimulus from the Biden administration.

Nuveen Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

What key strategies were used to manage the Fund during the six-month reporting period and how did these strategies influence performance?

The Fund employs a passive management (or “indexing”) approach, seeking to track the investment results, before fees and expenses, of the ICE BofA Enhanced Yield U.S. Broad Bond Index (the “NUAG Enhanced Index”). The NUAG Enhanced Index is designed to broadly capture the U.S. investment grade fixed income market and uses a rules-based weighting methodology that seeks to enhance yield while maintaining comparable risk. The NUAG Enhanced Index is primarily comprised of U.S. government securities, debt securities issued by U.S. corporations, residential and commercial mortgage-backed securities, asset-backed securities and U.S. dollar-denominated debt securities issued by non-U.S. corporations that are publicly offered for sale in the U.S. The NUAG Enhanced Index selects from the securities included in the ICE BofA U.S. Broad Market Index (the “Base Index”), which consists of U.S. dollar-denominated, investment grade taxable debt securities with fixed rate coupons that have at least one year to final maturity.

The Fund generally invests in a sample of the securities in the NUAG Enhanced Index whose risk, return and other characteristics resemble the risk, return and other characteristics of the NUAG Enhanced Index. Under normal market conditions, the Fund invests at least 80% of its assets, exclusive of collateral held from securities lending, in component securities of the NUAG Enhanced Index. To the extent the NUAG Enhanced Index concentrates (i.e., holds 25% or more of its total assets) in the securities of companies in a particular industry or group of industries, the Fund will concentrate its investments to approximately the same extent as the NUAG Enhanced Index. The Fund rebalances its holdings monthly in response to the monthly NUAG Enhanced Index rebalances. During the reporting period, the Fund has remained fully invested within its allocation targets to track the NUAG Enhanced Index.

How did the Fund perform during the twelve-month reporting period ended July 31, 2021?

The Fund’s total returns at net asset value (NAV) are compared with the performance of the NUAG Enhanced Index, which the Fund is designed to track. The Fund’s total return underperformed the NUAG Enhanced Index during the reporting period. The relative underperformance is mainly attributable to the representative sampling process, primarily within the securitized sector, that utilizes a subset of Index securities in an effort to provide exposure similar to that of the NUAG Enhanced Index, which leads the Fund to be overweight and underweight (and, in some cases, not invested at all in) certain securities as compared to the Index, transaction costs related to the Fund’s acquisition of portfolio securities, and the fees and expenses incurred by the Fund that are not incurred by the NUAG Enhanced Index. The NUAG Enhanced Index is unmanaged and therefore its returns do not reflect any fees or expenses, which would detract from its performance. You cannot invest directly in an index.

Nuveen Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (NUSA)

What key strategies were used to manage the Fund during the twelve-month reporting period and how did these strategies influence performance?

The Fund employs a passive management (or “indexing”) approach, seeking to track the investment results, before fees and expenses, of the ICE BofA Enhanced Yield 1-5 Year U.S. Broad Bond Index (the “NUSA Enhanced Index”). The NUSA Enhanced Index is designed to broadly capture the 1-5 year U.S. investment grade fixed income market and uses a rules-based weighting methodology that seeks to enhance yield while maintaining comparable risk. The NUSA Enhanced Index is primarily comprised of U.S. government securities, debt securities issued by U.S. corporations, residential and commercial mortgage-backed securities, asset-backed securities and U.S. dollar-denominated debt securities issued by non-U.S. corporations that are publicly offered for sale in the U.S. The NUSA Enhanced Index selects from the securities included in the ICE BofA 1-5 Year U.S. Broad Market Index (the “Base Index”), which consists of U.S. dollar-denominated, investment grade taxable debt securities with a remaining term to final maturity, or an average life, of less than five years.

The Fund generally invests in a sample of the securities in the NUSA Enhanced Index whose risk, return and other characteristics resemble the risk, return and other characteristics of the NUSA Enhanced Index. Under normal market conditions, the Fund invests at least 80% of its assets and the amount of any borrowings for investment purposes in component securities of the NUSA Enhanced Index. To the extent the NUSA Enhanced Index concentrates (i.e., holds 25% or more of its total assets) in the securities of companies in a particular industry or group of industries, the Fund will concentrate its investments to approximately the same extent as the NUSA Enhanced Index. The Fund rebalances its holdings monthly in response to the monthly NUSA Enhanced Index rebalances. During the reporting period, the Fund has remained fully invested within its allocation targets to track the NUSA Enhanced Index.

How did the Fund perform during the twelve-month reporting period ended July 31, 2021?

The Fund’s total returns at net asset value (NAV) are compared with the performance of the NUSA Enhanced Index, which the Fund is designed to track. For the reporting period, the Fund’s total return underperformed that of the NUSA Enhanced Index. The relative underperformance is mainly attributable to the representative sampling process, primarily within the securitized sectors, that utilizes a sub-set of Index securities in an effort to provide exposure similar to that of the NUSA Enhanced Index, which leads the Fund to be overweight and underweight (and, in some cases, not invested at all in) certain securities as compared to the Index, transaction costs related to the Fund’s acquisition of portfolio securities, and the fees and expenses incurred by the Fund that are not incurred by the NUSA Enhanced Index. The NUSA Enhanced Index is unmanaged and therefore its returns do not reflect any fees or expenses, which would detract from its performance. You cannot invest directly in an index.

Nuveen ESG High Yield Corporate Bond ETF (NUHY)

What key strategies were used to manage the Fund during the twelve-month reporting period and how did these strategies influence performance?

The Fund employs a passive management (or “indexing”) approach, investing in a diversified portfolio of U.S. dollar-denominated, high yield, fixed-rate corporate bonds that satisfy certain environmental, social and governance (“ESG”) criteria. The Fund seeks to track the investment results, before fees and expenses, of the Bloomberg MSCI U.S. High Yield Very Liquid ESG Select Index (“the NUHY Select Index”). The NUHY Select Index is composed of U.S. dollar-denominated below investment grade corporate bonds with above average liquidity that satisfy certain ESG and low-carbon criteria. Below investment grade bonds are commonly referred to as “high yield” or “junk” bonds. The NUHY Select Index selects from the securities included in the Bloomberg U.S. High Yield Very Liquid Index (the “Base Index”), which is designed to broadly capture the U.S. dollar-denominated, high yield, fixed-rate corporate bond market.

The Fund generally invests in a sample of the securities in the NUHY Select Index whose risk, return and other characteristics resemble the risk, return and other characteristics of the NUHY Select Index. Under normal market conditions, the Fund invests at least 80% of the sum of its net assets and the amount of any borrowings for investment purposes in component securities of the NUHY Select Index. To the extent the NUHY Select Index concentrates (i.e., holds 25% or more of its total assets) in the securities of companies in a

Portfolio Managers’ Comments (continued)

particular industry or group of industries, the Fund will concentrate its investments to approximately the same extent as the NUHY Select Index. The Fund rebalances its holdings monthly in response to the monthly NUHY Select Index rebalances. During the reporting period, the Fund sought to fully invest within its allocation targets to track the NUHY Select Index.

How did the Fund perform during the twelve-month reporting period ended July 31, 2021?

The Fund’s total returns at net asset value (NAV) are compared with the performance of the NUHY Select Index, which the Fund is designed to track. For the reporting period, the Fund’s total return underperformed that of the NUHY Select Index. The relative underperformance is mainly attributable to the transaction costs related to the Fund’s acquisition of portfolio securities, as well as fees and expenses incurred by the Fund that are not incurred by the NUHY Select Index. The NUHY Select Index is unmanaged and therefore its returns do not reflect any fees or expenses, which would detract from its performance. You cannot invest directly in an index.

Nuveen ESG U.S. Aggregate Bond ETF (NUBD)

What key strategies were used to manage the Fund during the twelve-month reporting period and how did these strategies influence performance?

The Fund employs a passive management (or “indexing”) approach, investing in a diversified portfolio of U.S. investment grade bonds that satisfy certain environmental, social and governance (“ESG”) criteria. The Fund seeks to track the investment results, before fees and expenses, of the Bloomberg MSCI U.S. Aggregate ESG Select Index (“the NUBD Select Index”). The NUBD Select Index is composed of U.S. investment grade fixed income securities that satisfy certain ESG and low-carbon criteria, including U.S. government securities, debt securities issued by U.S. corporations, residential and commercial mortgage-backed securities, asset-backed securities and U.S. dollar-denominated debt securities issued by non-U.S. corporations that are publicly offered for sale in the U.S. The NUBD Select Index selects from the securities included in the Bloomberg U.S. Aggregate Bond Index (the “Base Index”), which is designed to broadly capture the U.S. investment grade, taxable fixed income market.

The Fund generally invests in a sample of the securities in the NUBD Select Index whose risk, return and other characteristics resemble the risk, return and other characteristics of the NUBD Select Index. Under normal market conditions, the Fund invests at least 80% of the sum of its net assets and the amount of any borrowings for investment purposes in component securities of the NUBD Select Index. To the extent the NUBD Select Index concentrates (i.e., holds 25% or more of its total assets) in the securities of companies in a particular industry or group of industries, the Fund will concentrate its investments to approximately the same extent as the NUBD Select Index. The Fund rebalances its holdings monthly in response to the monthly NUBD Select Index rebalances. During the reporting period, the Fund remained fully invested within its allocation targets to track the NUBD Select Index.

How did the Fund perform during the twelve-month reporting period ended July 31, 2021?

The Fund’s total returns at net asset value (NAV) are compared with the performance of the NUBD Select Index, which the Fund is designed to track. For the reporting period, the Fund’s total return underperformed that of the NUBD Select Index. The relative underperformance is mainly attributable to the representative sampling process, primarily within the securitized sector, that utilizes a subset of Index securities in an effort to provide exposure similar to that of the NUBD Select Index, which leads the Fund to be overweight and underweight (and, in some cases, not invested at all in) certain securities as compared to the Index, transaction costs related to the Fund’s acquisition of portfolio securities, and the fees and expenses incurred by the Fund that are not incurred by the NUBD Select Index The NUBD Select Index is unmanaged and therefore its returns do not reflect any fees or expenses, which would detract from its performance. You cannot invest directly in an index.

Risk Considerations and Dividend Information

Nuveen Enhanced Yield U.S. Aggregate Bond ETF

Investing involves risk; principal loss is possible. This is no guarantee the Fund's investment objective will be achieved. An exchange-traded fund seeks to generally track the investment results of an index; however the Fund may underperform, outperform or be more volatile than the referenced index. Interest rate risk occurs when interest rates rise causing bond prices to fall. Credit risk arises from an issuer's ability to make interest and principal payments when due, as well as the prices of bonds declining when an issuer's credit quality is expected to deteriorate. These and other risk considerations are described in detail in the Fund's prospectus.

Nuveen Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF

Investing involves risk; principal loss is possible. There is no guarantee the Fund's investment objectives will be achieved. This ETF seeks to generally track the investment results of an index; however the Fund may underperform, outperform or be more volatile than the referenced index. Interest rate risk is the risk that the value of the Fund's portfolio will decline because of rising interest rates. Credit Risk is the risk that an issuer of a debt security may be unable or unwilling to make interest and principal payments when due and the related risk that the value of a debt security may decline because of concerns about the issuer's ability or willingness to make such payments. These and other risk considerations are described in detail in the Fund's prospectus.

Nuveen ESG High Yield Corporate Bond ETF

Investing involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. This ETF seeks to generally track the investment results of an index; however the Fund may underperform, outperform or be more volatile than the referenced index. In addition, because the Index selects securities for inclusion based on environmental, social, and governance (ESG) criteria, the Fund may forgo some market opportunities available to funds that don’t use these criteria. Investments in below investment grade or high yield securities are subject to liquidity risk and heightened credit risk. Credit risk arises from an issuer’s ability to make interest and principal payments when due, as well as the prices of bonds declining when an issuer’s credit quality is expected to deteriorate. The Fund is subject to interest rate risk; as interest rates rise, bond prices fall. These and other risk considerations, such as call, concentration and income risks, are described in detail in the Fund’s prospectus.

Nuveen ESG U.S. Aggregate Bond ETF

Investing involves risk; principal loss is possible. There is no guarantee the Fund's investment objectives will be achieved. An exchange-traded fund seeks to generally track the investment results of an index; however the Fund may underperform, outperform or be more volatile than the referenced index. Because the Index selects securities for inclusion based on environmental, social, and governance (ESG) criteria, the Fund may forgo some market opportunities available to funds that don't use these criteria. Interest rate risk occurs when interest rates rise causing bond prices to fall. Credit risk arises from an issuer's credit quality is expected to deteriorate. These and other risk considerations are described in detail in the Fund's prospectus.

Dividend Information

Each Fund seeks to pay monthly dividends out of its net investment income. Monthly distributions are not expected to be a level amount from period-to-period. Each Fund will, over time, pay all its net investment income as dividends to shareholders.

All monthly dividends paid by each Fund during the current reporting period were paid from net investment income. If a portion of the Fund's monthly distributions is sourced or comprised of elements other than net investment income, including capital gains and/or a return of capital, shareholders will be notified of those sources. For financial reporting purposes, the per share amounts of each Fund's dividends for the reporting period are presented in this report's Financial Highlights. For income tax purposes, distribution information for NUAG, NUSA, NUHY and NUDB as of their most recent tax year end is presented in Note 6 - Income Tax Information within the Notes to Financial Statements of this report.

Fund Performance and Expense Ratios

The Fund Performance and Expense Ratios for each Fund are shown within this section of the report.

Fund Performance

Returns quoted represent past performance, which is no guarantee of future results. Investment returns and principal value will fluctuate so that when shares are sold, they may be worth more or less than their original cost. Current performance may be higher or lower than the performance shown.

Total returns for a period of less than one year are not annualized (i.e. cumulative returns). Returns assume reinvestment of dividends and capital gains. Market price returns are based on the closing market price as of the end of the reporting period. For performance current to the most recent month-end visit nuveen.com or call (800) 257-8787.

Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares.

Expense Ratios

The expense ratios shown are as of each Fund's most recent prospectus. The expense ratios shown reflect total operating expenses (before fee waivers and/or expense reimbursements, if any). The expense ratios include management fees and other fees and expenses. Refer to the Financial Highlights later in this report for each Fund's expense ratios as of the end of the reporting period.

Fund Performance and Expense Ratios (continued)

Nuveen Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance and Expense Ratio

| | Total Returns as of July 31, 2021 | |

| | | Average Annual | |

| | Inception

Date | 1-Year | Since

Inception | Expense

Ratios |

| NUAG at NAV | 9/14/16 | (0.81)% | 3.40% | 0.20% |

| NUAG at Market Price | 9/14/16 | (0.64)% | 3.40% | - |

| ICE BofA Enhanced Yield U.S. Broad Bond Index | - | (0.01)% | 3.78% | - |

| ICE BofA U.S. Broad Market Index | - | (0.82)% | 3.38% | - |

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

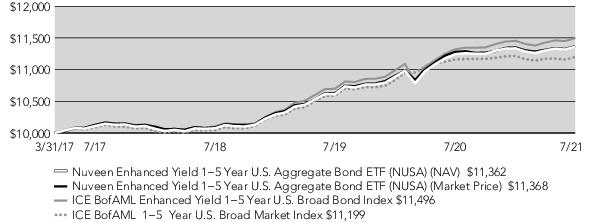

Nuveen Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (NUSA)

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance and Expense Ratio

| | Total Returns as of July 31, 2021 | |

| | | Average Annual | |

| | Inception

Date | 1-Year | Since

Inception | Expense

Ratios |

| NUSA at NAV | 3/31/17 | 1.03% | 2.99% | 0.20% |

| NUSA at Market Price | 3/31/17 | 0.80% | 3.00% | - |

| ICE BofA Enhanced Yield 1-5 Year U.S. Broad Bond Index | - | 1.53% | 3.27% | - |

| ICE BofA 1-5 Year U.S. Broad Market Index | - | 0.34% | 2.65% | - |

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

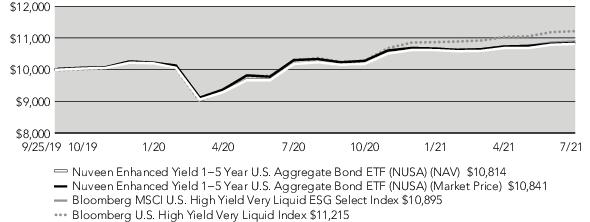

Nuveen ESG High Yield Corporate Bond ETF (NUHY)

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance and Expense Ratio

| | Total Returns as of July 31, 2021 | |

| | | Average Annual | |

| | Inception

Date | 1-Year | Since

Inception | Expense

Ratios |

| NUHY at NAV | 9/25/19 | 6.32% | 4.37% | 0.35% |

| NUHY at Market Price | 9/25/19 | 5.25% | 4.48% | - |

| Bloomberg MSCI U.S. High Yield Very Liquid ESG Select Index | - | 6.83% | 4.75% | - |

| Bloomberg U.S. High Yield Very Liquid Index | - | 9.05% | 6.40% | - |

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

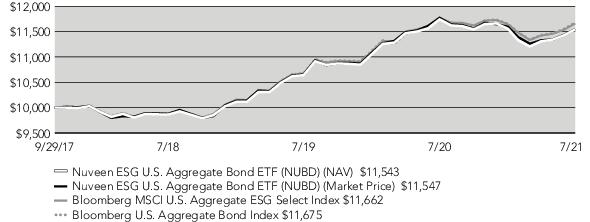

Nuveen ESG U.S. Aggregate Bond ETF (NUBD)

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance and Expense Ratio

| | Total Returns as of July 31, 2021 | |

| | | Average Annual | |

| | Inception

Date | 1-Year | Since

Inception | Expense

Ratios |

| NUBD at NAV | 9/29/17 | (1.72)% | 3.81% | 0.20% |

| NUBD at Market Price | 9/29/17 | (1.90)% | 3.81% | - |

| Bloomberg MSCI U.S. Aggregate ESG Select Index | - | (0.95)% | 4.09% | - |

| Bloomberg U.S. Aggregate Bond Index | - | (0.70)% | 4.12% | - |

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Yields as of July 31, 2021

Dividend Rate is the average dividend per share for the current reporting period divided by the offering price per share at period end.

The SEC 30-Day Yield is a standardized measure of a fund’s yield that accounts for the future amortization of premiums or discounts of bonds held in the fund’s portfolio. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. Dividend Rate may differ from the SEC 30-Day Yield because the fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium.

Nuveen Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

| | |

| Dividend Rate | 2.54% |

| SEC 30-Day Yield | 1.16% |

Nuveen Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (NUSA)

| | |

| Dividend Rate | 2.13% |

| SEC 30-Day Yield | 0.61% |

Nuveen ESG High Yield Corporate Bond ETF (NUHY)

| | |

| Dividend Rate | 4.59% |

| SEC 30-Day Yield | 3.48% |

Nuveen ESG U.S. Aggregate Bond ETF (NUBD)

| | |

| Dividend Rate | 1.94% |

| SEC 30-Day Yield | 1.04% |

Holding Summaries as of July 31, 2021

This data relates to the securities held in each Fund's portfolio of investments as of the end of this reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

Each Fund uses credit quality ratings for its portfolio securities provided by Moody's, S&P and Fitch. For NUAG and NUSA, if all three of Moody's S&P, and Fitch provide a rating for a security, an average of the ratings is used; if two of the three agencies rate a security, an average of the two is used; and if only one rating agency rates a security, that rating is used. For NUHY and NUBD, if all three of Moody's S&P, and Fitch provide a rating for a security, the middle rating is used; if two of the three agencies rate a security, the lower rating is used; and if only one rating agency rates a security, that rating is used. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC/CC/C and D are below-investment grade ratings. Credit ratings are subject to change. U.S. Treasury, U.S. Agency, and U.S. Agency mortgage-backed securities are included in the U.S. Treasury/Agency category.

Nuveen Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

Fund Allocation

(% of net assets) | |

| Securitized | 38.6% |

| U.S. Treasury | 29.7% |

| Corporate Debt | 24.9% |

| Government Related - Long-Term | 6.1% |

| Investments Purchased with Collateral from Securities Lending | 0.9% |

| U.S. Government and Agency Obligations | 25.3% |

| Other Assets Less Liabilities1 | (25.5)% |

| Net Assets | 100% |

Corporate Debt: Industries

(% of total corporate debt

holdings) | |

| Industrial | 60.2% |

| Financials | 14.6% |

| Utility | 25.2% |

| Total | 100% |

Portfolio Credit Quality

(% of total investments) | |

| U.S. Treasury/Agency | 71.4% |

| AAA | 1.1% |

| AA | 1.2% |

| A | 1.8% |

| BBB | 21.4% |

| N/R | 2.4% |

| N/A (not applicable) | 0.7% |

| Total | 100% |

| 1 | Includes payable for investments purchased on a when issued/delayed delivery basis as reported on the Statement of Assets and Liabilities. | |

Holding Summaries as of July 31, 2021 (continued)

Nuveen Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (NUSA)

Fund Allocation

(% of net assets) | |

| Corporate Debt | 43.0% |

| Securitized | 30.0% |

| U.S. Treasury | 26.2% |

| Investments Purchased with Collateral from Securities Lending | 0.7% |

| U.S. Government and Agency Obligations | 1.8% |

| Other Assets Less Liabilities | (1.7)% |

| Net Assets | 100% |

Corporate Debt: Industries

(% of total corporate debt

holdings) | |

| Industrial | 22.4% |

| Financials | 48.4% |

| Utility | 29.1% |

| Total | 100% |

Portfolio Credit Quality

(% of total investments) | |

| U.S. Treasury/Agency | 43.3% |

| AAA | 11.4% |

| AA | 2.6% |

| A | 15.2% |

| BBB | 27.5% |

| Total | 100% |

Nuveen ESG High Yield Corporate Bond ETF (NUHY)

Fund Allocation

(% of net assets) | |

| Corporate Debt | 97.7% |

| Investments Purchased with Collateral from Securities Lending | 2.0% |

| U.S. Government and Agency Obligations | 0.2% |

| Other Assets Less Liabilities | 0.1% |

| Net Assets | 100% |

Corporate Debt: Industries

(% of total corporate debt

holdings) | |

| Industrial | 90.8% |

| Financials | 7.9% |

| Utility | 1.3% |

| Total | 100% |

Portfolio Credit Quality

(% of total investments) | |

| U.S. Treasury/Agency | 0.2% |

| BBB | 2.8% |

| BB or Lower | 97.0% |

| Total | 100% |

Holding Summaries as of July 31, 2021 (continued)

Nuveen ESG U.S. Aggregate Bond ETF (NUBD)

Fund Allocation

(% of net assets) | |

| U.S. Treasury | 36.7% |

| Securitized | 29.8% |

| Corporate Debt | 27.0% |

| Government Related - Long-Term | 5.7% |

| Investments Purchased with Collateral from Securities Lending | 0.5% |

| U.S. Government and Agency Obligations | 0.7% |

| Other Assets Less Liabilities | (0.4)% |

| Net Assets | 100% |

Corporate Debt: Industries

(% of total corporate debt

holdings) | |

| Industrial | 60.3% |

| Financials | 31.3% |

| Utility | 8.4% |

| Total | 100% |

Portfolio Credit Quality

(% of total investments) | |

| U.S. Treasury/Agency | 61.8% |

| AAA | 8.5% |

| AA | 2.6% |

| A | 13.9% |

| BBB | 12.4% |

| N/R (not rated) | 0.8% |

| Total | 100% |

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including brokerage commissions on purchases and sales of Fund shares, and (2) ongoing costs, including management fees and other applicable Fund expenses. The Examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other funds.

The Examples below are based on an investment of $1,000 invested at the beginning of the period and held through the period ended July 31, 2021.

The beginning of the period is February 1, 2021.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your Fund in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance” provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Nuveen Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

| Actual Performance | |

| Beginning Account Value | $1,000.00 |

| Ending Account Value | $ 999.80 |

| Expenses Incurred During Period | $ 0.99 |

Hypothetical Performance

(5% annualized return before expenses) | |

| Beginning Account Value | $1,000.00 |

| Ending Account Value | $1,023.80 |

| Expenses Incurred During the Period | $ 1.00 |

Expenses are equal to the Fund's annualized net expense ratio of 0.20% multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Expense Examples (continued)

Nuveen Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (NUSA)

| Actual Performance | |

| Beginning Account Value | $1,000.00 |

| Ending Account Value | $1,002.00 |

| Expenses Incurred During Period | $ 0.99 |

Hypothetical Performance

(5% annualized return before expenses) | |

| Beginning Account Value | $1,000.00 |

| Ending Account Value | $1,023.80 |

| Expenses Incurred During the Period | $ 1.00 |

Expenses are equal to the Fund's annualized net expense ratio of 0.20% multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Nuveen ESG High Yield Corporate Bond ETF (NUHY)

| Actual Performance | |

| Beginning Account Value | $1,000.00 |

| Ending Account Value | $1,019.00 |

| Expenses Incurred During Period | $ 1.75 |

Hypothetical Performance

(5% annualized return before expenses) | |

| Beginning Account Value | $1,000.00 |

| Ending Account Value | $1,023.06 |

| Expenses Incurred During the Period | $ 1.76 |

Expenses are equal to the Fund's annualized net expense ratio of 0.35% multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Nuveen ESG U.S. Aggregate Bond ETF (NUBD)

| Actual Performance | |

| Beginning Account Value | $1,000.00 |

| Ending Account Value | $ 998.90 |

| Expenses Incurred During Period | $ 0.99 |

Hypothetical Performance

(5% annualized return before expenses) | |

| Beginning Account Value | $1,000.00 |

| Ending Account Value | $1,023.80 |

| Expenses Incurred During the Period | $ 1.00 |

Expenses are equal to the Fund's annualized net expense ratio of 0.20% multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Trustees of

Nushares ETF Trust:

Opinion on the Financial Statements

We have audited the accompanying statements of assets and liabilities of Nuveen Enhanced Yield U.S. Aggregate Bond ETF, Nuveen Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF, Nuveen ESG High Yield Corporate Bond ETF and Nuveen ESG U.S. Aggregate Bond ETF (four of the funds comprising Nushares ETF Trust) (the Funds), including the portfolios of investments, as of July 31, 2021, the related statements of operations for the year then ended, the statements of changes in net assets for each of the years in the two year period then ended (the one-year period then ended and the period from September 25, 2019 (commencement of operations) to July 31, 2020 for Nuveen ESG High Yield Corporate Bond ETF), and the related notes (collectively, the financial statements) and the financial highlights for each of the years in the four year period then ended and the period from September 14, 2016 (commencement of operations) to July 31, 2017 for Nuveen Enhanced Yield U.S. Aggregate Bond ETF, the four-year period then ended and the period from March 31, 2017 (commencement of operations) to July 31, 2017 for Nuveen Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF, the one-year period then ended and the period from September 25, 2019 to July 31, 2020 for Nuveen ESG High Yield Corporate Bond ETF, and the three-year period then ended and the period from September 29, 2017 (commencement of operations) to July 31, 2018 for Nuveen ESG U.S. Aggregate Bond ETF. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Funds as of July 31, 2021, the results of their operations for the year then ended, the changes in their net assets for each of the years in the two-year period then ended (the one-year period then ended and the period from September 25, 2019 to July 31, 2020 for Nuveen ESG High Yield Corporate Bond ETF), and the financial highlights for each of the years in the four year period then ended and the period from September 14, 2016 to July 31, 2017 for Nuveen Enhanced Yield U.S. Aggregate Bond ETF, the four-year period then ended and the period from March 31, 2017 to July 31, 2017 for Nuveen Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF, the one-year period then ended and the period from September 25, 2019 to July 31, 2020 for Nuveen ESG High Yield Corporate Bond ETF, and the three-year period then ended and the period from September 29, 2017 to July 31, 2018 for Nuveen ESG U.S. Aggregate Bond ETF in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Funds in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Such procedures also included confirmation of securities owned as of July 31, 2021, by correspondence with custodians and brokers or other appropriate auditing procedures. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. We believe that our audits provide a reasonable basis for our opinion.

/s/ KPMG LLP

We have served as the auditor of one or more Nuveen investment companies since 2014.

Chicago, Illinois

September 28, 2021

Nuveen Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

Portfolio of Investments July 31, 2021

| Principal Amount (000) | | Description (1) | Coupon | Maturity | Ratings (2) | Value |

| | | LONG-TERM INVESTMENTS – 99.3% | | | | |

| | | SECURITIZED – 38.6% | | | | |

| $ 400 | | BANK 2021-BNK33 | 2.021% | 5/15/64 | Aaa | $409,318 |

| 150 | | Benchmark 2021-B27 Mortgage Trust | 2.703% | 7/15/54 | A- | 152,190 |

| 250 | | COMM 2015-LC19 Mortgage Trust | 3.527% | 2/10/48 | Aa1 | 268,901 |

| 594 | | Fannie Mae Pool AL9125 | 4.000% | 10/01/43 | N/R | 651,150 |

| 274 | | Fannie Mae Pool AS6302 | 3.500% | 12/01/45 | N/R | 294,698 |

| 394 | | Fannie Mae Pool AX4887 | 4.000% | 12/01/44 | N/R | 430,540 |

| 1,636 | | Fannie Mae Pool FN MA4356 | 2.500% | 6/01/51 | N/R | 1,705,013 |

| 37 | | Fannie Mae Pool MA1489 | 3.000% | 7/01/43 | Aaa | 39,156 |

| 323 | | Fannie Mae Pool MA2929 | 3.500% | 3/01/47 | Aaa | 345,546 |

| 3,157 | | Fannie Mae Pool MA3120, (DD1) | 3.500% | 9/01/47 | Aaa | 3,362,876 |

| 119 | | Fannie Mae Pool MA3211 | 4.000% | 12/01/47 | Aaa | 128,285 |

| 213 | | Fannie Mae Pool MA3239 | 4.000% | 1/01/48 | Aaa | 229,275 |

| 285 | | Fannie Mae Pool MA3276 | 3.500% | 2/01/48 | Aaa | 303,174 |

| 73 | | Fannie Mae Pool MA3277 | 4.000% | 2/01/48 | N/R | 77,767 |

| 145 | | Fannie Mae Pool MA3305 | 3.500% | 3/01/48 | N/R | 153,865 |

| 48 | | Fannie Mae Pool MA3306 | 4.000% | 3/01/48 | N/R | 51,325 |

| 150 | | Fannie Mae Pool MA3332 | 3.500% | 4/01/48 | Aaa | 159,155 |

| 89 | | Fannie Mae Pool MA3383 | 3.500% | 6/01/48 | Aaa | 94,159 |

| 707 | | Fannie Mae Pool MA3416 | 4.500% | 7/01/48 | Aaa | 762,011 |

| 89 | | Fannie Mae Pool MA3467 | 4.000% | 9/01/48 | Aaa | 95,520 |

| 99 | | Fannie Mae Pool MA3663 | 3.500% | 5/01/49 | Aaa | 104,618 |

| 136 | | Fannie Mae Pool MA3744 | 3.000% | 8/01/49 | N/R | 142,902 |

| 154 | | Fannie Mae Pool MA3774 | 3.000% | 9/01/49 | Aaa | 161,160 |

| 204 | | Fannie Mae Pool MA3905 | 3.000% | 1/01/50 | N/R | 213,723 |

| 1,430 | | Fannie Mae Pool MA4209, (WI/DD) | 1.500% | 12/01/50 | N/R | 1,415,329 |

| 1,321 | | Fannie Mae Pool MA4256 | 2.500% | 2/01/51 | N/R | 1,376,479 |

| 689 | | Fannie Mae Pool MA4304 | 1.500% | 4/01/51 | N/R | 681,941 |

| 1,837 | | Fannie Mae Pool MA4307 | 3.000% | 4/01/51 | N/R | 1,937,387 |

| 4,171 | | Fannie Mae Pool MA4355 | 2.000% | 6/01/51 | N/R | 4,254,448 |

| 9,968 | | Fannie Mae Pool MA4398, (WI/DD) | 2.000% | 8/01/51 | N/R | 10,166,215 |

| 6,971 | | Fannie Mae Pool MA4399, (WI/DD) | 2.500% | 8/01/51 | N/R | 7,263,606 |

| 4,971 | | Fannie Mae Pool MA4400, (WI/DD) | 3.000% | 8/01/51 | N/R | 5,243,131 |

| 282 | | Freddie Mac Gold Pool G08797 | 4.000% | 1/01/48 | N/R | 303,383 |

| 125 | | Freddie Mac Gold Pool G08800 | 3.500% | 2/01/48 | N/R | 133,036 |

| 350 | | Freddie Mac Multifamily Structured Pass-Through Certificates | 0.861% | 6/25/27 | Aaa | 350,912 |

| 214 | | Freddie Mac Multifamily Structured Pass-Through Certificates | 1.760% | 3/25/28 | Aaa | 222,298 |

| Principal Amount (000) | | Description (1) | Coupon | Maturity | Ratings (2) | Value |

| $ 199 | | Freddie Mac Multifamily Structured Pass-Through Certificates | 1.353% | 11/25/30 | Aaa | $202,995 |

| 349 | | Ginnie Mae II Pool G2 MA7418 | 2.500% | 6/20/51 | N/R | 362,684 |

| 30 | | Ginnie Mae II Pool MA2149 | 4.000% | 8/20/44 | N/R | 32,858 |

| 315 | | Ginnie Mae II Pool MA3310 | 3.500% | 12/20/45 | Aaa | 335,767 |

| 95 | | Ginnie Mae II Pool MA3311 | 4.000% | 12/20/45 | Aaa | 102,837 |

| 108 | | Ginnie Mae II Pool MA3874 | 3.500% | 8/20/46 | Aaa | 114,993 |

| 71 | | Ginnie Mae II Pool MA3937 | 3.500% | 9/20/46 | Aaa | 75,463 |

| 155 | | Ginnie Mae II Pool MA4900 | 3.500% | 12/20/47 | Aaa | 164,632 |

| 120 | | Ginnie Mae II Pool MA4962 | 3.500% | 1/20/48 | Aaa | 127,527 |

| 130 | | Ginnie Mae II Pool MA5875 | 3.500% | 4/20/49 | Aaa | 136,411 |

| 216 | | Ginnie Mae II Pool MA6283 | 3.000% | 11/20/49 | N/R | 225,838 |

| 224 | | Ginnie Mae II Pool MA6338 | 3.000% | 12/20/49 | N/R | 234,120 |

| 222 | | Ginnie Mae II Pool MA6474 | 3.000% | 2/20/50 | N/R | 232,546 |

| 927 | | Ginnie Mae II Pool MA6994 | 2.000% | 11/20/50 | N/R | 950,177 |

| 496 | | Ginnie Mae II Pool MA7366 | 2.000% | 5/20/51 | N/R | 508,751 |

| 1,984 | | Ginnie Mae II Pool MA7367 | 2.500% | 5/20/51 | N/R | 2,062,577 |

| 495 | | Ginnie Mae II Pool MA7368 | 3.000% | 5/20/51 | N/R | 519,646 |

| 349 | | Ginnie Mae II Pool MA7417 | 2.000% | 6/20/51 | N/R | 357,707 |

| 3,988 | | Ginnie Mae II Pool MA7471, (WI/DD) | 2.000% | 7/20/51 | N/R | 4,087,216 |

| 3,987 | | Ginnie Mae II Pool MA7472, (WI/DD) | 2.500% | 7/20/51 | N/R | 4,145,580 |

| 3,487 | | Ginnie Mae II Pool MA7473, (WI/DD) | 3.000% | 7/20/51 | N/R | 3,670,256 |

| 3,488 | | Ginnie Mae II Pool MA7474, (WI/DD) | 3.500% | 7/20/51 | N/R | 3,711,246 |

| 230 | | GS Mortgage Securities Trust 2013-GC16 | 5.161% | 11/10/46 | Aa1 | 245,992 |

| 233 | | GS Mortgage Securities Trust 2016-GS4 | 3.178% | 11/10/49 | Aaa | 249,893 |

| 250 | | Morgan Stanley Capital I Trust 2021-L5 | 1.518% | 5/15/54 | AAA | 252,467 |

| 250 | | Wells Fargo Commercial Mortgage Trust 2014-LC16 | 4.020% | 8/15/50 | Aa2 | 261,796 |

| $ 64,453 | | Total Securitized (cost $66,631,913) | | | | 67,056,467 |

| Principal Amount (000) | | Description (1) | Coupon | Maturity | Ratings (2) | Value |

| | | U.S. TREASURY – 29.7% | | | | |

| $ 13 | | United States Treasury Note/Bond | 1.750% | 6/15/22 | AAA | $13,189 |

| 2,243 | | United States Treasury Note/Bond | 0.125% | 12/31/22 | AAA | 2,243,088 |

| 9,950 | | United States Treasury Note/Bond | 0.125% | 4/30/23 | AAA | 9,943,781 |

| 840 | | United States Treasury Note/Bond | 0.125% | 5/31/23 | AAA | 839,442 |

| 1,200 | | United States Treasury Note/Bond, (3) | 0.125% | 6/30/23 | AAA | 1,199,156 |

| 1,183 | | United States Treasury Note/Bond | 1.250% | 2/28/25 | AAA | 1,210,311 |

| 634 | | United States Treasury Note/Bond | 0.375% | 4/30/25 | AAA | 630,954 |

| 2,208 | | United States Treasury Note/Bond | 0.250% | 9/30/25 | AAA | 2,177,899 |

| 2,695 | | United States Treasury Note/Bond | 0.250% | 10/31/25 | AAA | 2,655,628 |

| 425 | | United States Treasury Note/Bond | 0.375% | 1/31/26 | AAA | 420,102 |

| 425 | | United States Treasury Note/Bond | 0.750% | 3/31/26 | AAA | 426,826 |

Nuveen Enhanced Yield U.S. Aggregate Bond ETF (NUAG) (continued)

Portfolio of Investments July 31, 2021

| Principal Amount (000) | | Description (1) | Coupon | Maturity | Ratings (2) | Value |

| $ 9,200 | | United States Treasury Note/Bond | 0.750% | 4/30/26 | AAA | $9,236,656 |

| 2,565 | | United States Treasury Note/Bond | 0.750% | 5/31/26 | AAA | 2,573,416 |

| 5,500 | | United States Treasury Note/Bond | 0.875% | 6/30/26 | AAA | 5,548,555 |

| 976 | | United States Treasury Note/Bond | 3.125% | 11/15/28 | AAA | 1,119,541 |

| 483 | | United States Treasury Note/Bond | 2.375% | 5/15/29 | AAA | 529,470 |

| 557 | | United States Treasury Note/Bond | 1.625% | 8/15/29 | AAA | 579,541 |

| 2,432 | | United States Treasury Note/Bond | 0.625% | 5/15/30 | AAA | 2,319,900 |

| 1,383 | | United States Treasury Note/Bond | 0.875% | 11/15/30 | AAA | 1,342,158 |

| 3,320 | | United States Treasury Note/Bond | 1.625% | 5/15/31 | AAA | 3,437,756 |

| 2,700 | | United States Treasury Note/Bond | 1.875% | 2/15/51 | AA+ | 2,677,641 |

| 420 | | United States Treasury Note/Bond | 2.375% | 5/15/51 | AAA | 465,741 |

| $ 51,352 | | Total U.S. Treasury (cost $51,609,352) | | | | 51,590,751 |

| Principal Amount (000) | | Description (1) | Coupon | Maturity | Ratings (2) | Value |

| | | CORPORATE DEBT – 24.9% | | | | |

| | | Financials – 3.6% | | | | |

| $ 22 | | AerCap Ireland Capital DAC / AerCap Global Aviation Trust | 3.875% | 1/23/28 | BBB- | $23,776 |

| 20 | | Aetna Inc | 4.750% | 3/15/44 | BBB | 25,348 |

| 13 | | Air Lease Corp | 3.875% | 7/03/23 | BBB | 13,781 |

| 30 | | Air Lease Corp | 3.625% | 4/01/27 | BBB | 32,624 |

| 10 | | Air Lease Corp | 3.000% | 2/01/30 | BBB | 10,325 |

| 130 | | Alexandria Real Estate Equities Inc | 1.875% | 2/01/33 | BBB+ | 125,657 |

| 131 | | American International Group Inc | 4.200% | 4/01/28 | BBB+ | 151,496 |

| 153 | | Anthem Inc, (3) | 2.875% | 9/15/29 | BBB+ | 164,796 |

| 100 | | Anthem Inc | 3.125% | 5/15/50 | BBB+ | 104,633 |

| 132 | | Aon Corp | 3.750% | 5/02/29 | BBB+ | 149,734 |

| 2 | | Arch Capital Group US Inc | 5.144% | 11/01/43 | BBB+ | 2,665 |

| 10 | | Ares Capital Corp | 2.150% | 7/15/26 | BBB- | 10,075 |

| 10 | | Ares Capital Corp | 2.875% | 6/15/28 | BBB- | 10,310 |

| 10 | | Assurant Inc | 2.650% | 1/15/32 | BBB- | 10,108 |

| 122 | | Athene Holding Ltd | 6.150% | 4/03/30 | BBB+ | 156,441 |

| 27 | | AXIS Specialty Finance PLC | 4.000% | 12/06/27 | BBB+ | 30,168 |

| 11 | | BankUnited Inc | 5.125% | 6/11/30 | Baa3 | 12,951 |

| 250 | | Barclays PLC | 5.088% | 6/20/30 | BBB | 293,063 |

| 10 | | Blackstone Secured Lending Fund | 2.750% | 9/16/26 | Baa3 | 10,246 |

| 100 | | Blackstone Secured Lending Fund, 144A | 2.125% | 2/15/27 | Baa3 | 98,740 |

| 75 | | Boston Properties LP | 3.400% | 6/21/29 | BBB+ | 82,501 |

| 34 | | Brighthouse Financial Inc | 5.625% | 5/15/30 | BBB | 41,789 |

| 100 | | Brixmor Operating Partnership LP | 4.125% | 5/15/29 | BBB- | 114,049 |

| 134 | | Capital One Financial Corp | 3.800% | 1/31/28 | BBB+ | 151,237 |

| 100 | | Capital One Financial Corp | 2.359% | 7/29/32 | BBB | 100,801 |

| Principal Amount (000) | | Description (1) | Coupon | Maturity | Ratings (2) | Value |

| | | Financials (continued) | | | | |

| $ 10 | | CI Financial Corp | 4.100% | 6/15/51 | BBB | $10,554 |

| 65 | | Citigroup Inc | 1.122% | 1/28/27 | A- | 64,440 |

| 140 | | Citigroup Inc | 1.462% | 6/09/27 | A- | 140,123 |

| 9 | | Citigroup Inc | 4.450% | 9/29/27 | BBB | 10,379 |

| 17 | | Citizens Financial Group Inc | 2.500% | 2/06/30 | BBB+ | 17,631 |

| 32 | | CNA Financial Corp | 3.900% | 5/01/29 | BBB+ | 36,473 |

| 20 | | Cooperatieve Rabobank UA | 3.750% | 7/21/26 | BBB+ | 22,115 |

| 150 | | Deutsche Bank AG/New York NY | 3.547% | 9/18/31 | BBB- | 161,924 |

| 17 | | Digital Realty Trust LP | 4.450% | 7/15/28 | BBB | 19,948 |

| 150 | | Discover Financial Services | 4.100% | 2/09/27 | BBB | 170,272 |

| 10 | | Duke Realty LP | 1.750% | 7/01/30 | BBB+ | 9,761 |

| 11 | | Duke Realty LP | 3.050% | 3/01/50 | BBB+ | 11,118 |

| 100 | | Equitable Holdings Inc | 4.350% | 4/20/28 | BBB | 115,501 |

| 280 | | Essex Portfolio LP | 2.550% | 6/15/31 | BBB+ | 290,068 |

| 122 | | Fairfax Financial Holdings Ltd | 4.625% | 4/29/30 | BBB- | 141,525 |

| 100 | | Federal Realty Investment Trust | 3.500% | 6/01/30 | BBB+ | 111,040 |

| 100 | | Fidelity National Financial Inc | 3.400% | 6/15/30 | BBB | 109,210 |

| 14 | | Fifth Third Bancorp | 3.950% | 3/14/28 | BBB+ | 16,253 |

| 100 | | First American Financial Corp | 2.400% | 8/15/31 | BBB | 98,892 |

| 66 | | GATX Corp | 4.550% | 11/07/28 | BBB | 77,263 |

| 40 | | GE Capital Funding LLC | 4.550% | 5/15/32 | BBB+ | 48,294 |

| 285 | | GE Capital International Funding Co Unlimited Co | 4.418% | 11/15/35 | BBB+ | 349,249 |

| 15 | | Goldman Sachs Group Inc | 2.615% | 4/22/32 | A- | 15,511 |

| 100 | | Goldman Sachs Group Inc | 2.383% | 7/21/32 | A- | 101,477 |

| 100 | | Golub Capital BDC Inc | 2.050% | 2/15/27 | BBB- | 98,998 |

| 17 | | Hartford Financial Services Group Inc | 6.100% | 10/01/41 | BBB+ | 24,763 |

| 20 | | Healthcare Trust of America Holdings LP | 3.100% | 2/15/30 | BBB | 21,573 |

| 100 | | Healthpeak Properties Inc | 2.875% | 1/15/31 | BBB+ | 106,604 |

| 5 | | Highwoods Realty LP | 3.050% | 2/15/30 | BBB | 5,379 |

| 20 | | HSBC Holdings PLC | 0.976% | 5/24/25 | A | 20,051 |

| 30 | | Humana Inc | 3.850% | 10/01/24 | BBB | 32,595 |

| 100 | | Humana Inc | 2.150% | 2/03/32 | BBB | 100,316 |

| 15 | | Huntington Bancshares Inc/OH | 4.000% | 5/15/25 | BBB+ | 16,698 |

| 22 | | Jefferies Financial Group Inc | 5.500% | 10/18/23 | BBB | 23,539 |

| 10 | | JPMorgan Chase & Co | 2.069% | 6/01/29 | A | 10,182 |

| 4 | | JPMorgan Chase & Co | 3.702% | 5/06/30 | A | 4,496 |

| 100 | | KeyCorp | 2.550% | 10/01/29 | BBB+ | 105,961 |

| 22 | | Kimco Realty Corp | 4.250% | 4/01/45 | BBB+ | 25,909 |

| 17 | | Lazard Group LLC | 4.500% | 9/19/28 | BBB | 19,779 |

| 150 | | Lincoln National Corp | 3.625% | 12/12/26 | BBB+ | 167,277 |

| 12 | | Manulife Financial Corp | 4.061% | 2/24/32 | BBB+ | 13,178 |

Nuveen Enhanced Yield U.S. Aggregate Bond ETF (NUAG) (continued)

Portfolio of Investments July 31, 2021

| Principal Amount (000) | | Description (1) | Coupon | Maturity | Ratings (2) | Value |

| | | Financials (continued) | | | | |

| $ 7 | | Markel Corp | 5.000% | 5/20/49 | BBB | $9,310 |

| 11 | | Mid-America Apartments LP | 2.750% | 3/15/30 | BBB+ | 11,659 |

| 19 | | Morgan Stanley | 4.350% | 9/08/26 | BBB+ | 21,631 |

| 100 | | Morgan Stanley | 1.512% | 7/20/27 | A | 100,810 |

| 100 | | National Retail Properties Inc | 2.500% | 4/15/30 | BBB+ | 103,485 |

| 160 | | Natwest Group PLC | 5.076% | 1/27/30 | BBB+ | 191,673 |

| 34 | | Nomura Holdings Inc | 2.679% | 7/16/30 | BBB+ | 34,793 |

| 10 | | Old Republic International Corp | 3.850% | 6/11/51 | BBB | 10,859 |

| 22 | | Omega Healthcare Investors Inc | 4.750% | 1/15/28 | BBB- | 25,154 |

| 10 | | Owl Rock Capital Corp | 2.625% | 1/15/27 | BBB- | 10,115 |

| 30 | | Prudential Financial Inc | 5.375% | 5/15/45 | BBB+ | 33,091 |

| 100 | | Prudential Financial Inc | 3.700% | 10/01/50 | BBB+ | 105,591 |

| 17 | | Regency Centers LP | 4.400% | 2/01/47 | BBB+ | 20,387 |

| 18 | | Reinsurance Group of America Inc | 4.700% | 9/15/23 | BBB+ | 19,533 |

| 28 | | Santander Holdings USA Inc | 3.244% | 10/05/26 | BBB | 30,120 |

| 20 | | Spirit Realty LP | 2.100% | 3/15/28 | BBB | 20,218 |

| 20 | | SVB Financial Group | 1.800% | 2/02/31 | BBB+ | 19,432 |

| 23 | | Synchrony Financial | 3.950% | 12/01/27 | BBB- | 25,712 |

| 25 | | UDR Inc | 3.000% | 8/15/31 | BBB+ | 26,811 |

| 13 | | Unum Group | 4.500% | 12/15/49 | BBB- | 14,016 |

| 122 | | Ventas Realty LP | 4.750% | 11/15/30 | BBB+ | 147,463 |

| 100 | | VEREIT Operating Partnership LP | 3.100% | 12/15/29 | BBB | 108,613 |

| 84 | | Wachovia Corp | 5.500% | 8/01/35 | BBB+ | 110,861 |

| 100 | | Welltower Inc | 2.800% | 6/01/31 | BBB+ | 105,587 |

| 140 | | Westpac Banking Corp | 1.150% | 6/03/26 | AA- | 141,358 |

| 11 | | Willis North America Inc | 4.500% | 9/15/28 | BBB | 12,806 |

| 5,757 | | Total Financials | | | | 6,334,721 |

| | | Industrial – 15.0% | | | | |

| 150 | | AbbVie Inc | 3.200% | 11/21/29 | BBB | 164,520 |

| 230 | | AbbVie Inc | 4.050% | 11/21/39 | BBB | 270,796 |

| 159 | | AbbVie Inc | 4.625% | 10/01/42 | BBB | 199,590 |

| 12 | | Altria Group Inc | 3.400% | 5/06/30 | BBB+ | 12,933 |

| 147 | | Altria Group Inc | 5.800% | 2/14/39 | BBB+ | 184,387 |

| 100 | | Altria Group Inc | 3.875% | 9/16/46 | BBB+ | 101,187 |

| 6 | | Altria Group Inc | 5.950% | 2/14/49 | BBB+ | 7,805 |

| 20 | | Amcor Flexibles North America Inc | 2.690% | 5/25/31 | BBB | 20,864 |

| 213 | | American Tower Corp | 2.100% | 6/15/30 | BBB | 212,981 |

| 30 | | AmerisourceBergen Corp | 2.700% | 3/15/31 | BBB+ | 31,332 |

| 100 | | Amgen Inc, (3) | 2.300% | 2/25/31 | BBB+ | 103,099 |

| 224 | | Amgen Inc | 3.150% | 2/21/40 | BBB+ | 239,367 |

| Principal Amount (000) | | Description (1) | Coupon | Maturity | Ratings (2) | Value |

| | | Industrial (continued) | | | | |

| $ 17 | | Amgen Inc | 5.150% | 11/15/41 | BBB+ | $22,794 |

| 209 | | Anheuser-Busch Cos LLC / Anheuser-Busch InBev Worldwide Inc | 4.900% | 2/01/46 | BBB+ | 267,680 |

| 83 | | Anheuser-Busch InBev Worldwide Inc | 4.000% | 4/13/28 | BBB+ | 95,228 |

| 282 | | Anheuser-Busch InBev Worldwide Inc | 4.350% | 6/01/40 | BBB+ | 341,171 |

| 145 | | Anheuser-Busch InBev Worldwide Inc | 4.600% | 6/01/60 | BBB+ | 181,818 |

| 279 | | AT&T Inc | 2.750% | 6/01/31 | BBB | 293,998 |

| 296 | | AT&T Inc | 4.850% | 3/01/39 | BBB | 362,928 |

| 150 | | AT&T Inc | 3.500% | 6/01/41 | BBB | 159,171 |

| 145 | | AT&T Inc | 4.900% | 6/15/42 | BBB | 180,137 |

| 19 | | AutoNation Inc | 4.500% | 10/01/25 | BBB- | 21,185 |

| 10 | | AutoZone Inc | 3.750% | 4/18/29 | BBB | 11,297 |

| 50 | | AutoZone Inc | 4.000% | 4/15/30 | BBB | 57,636 |

| 117 | | Barrick North America Finance LLC | 5.700% | 5/30/41 | BBB | 162,987 |

| 100 | | BAT Capital Corp | 3.557% | 8/15/27 | BBB | 108,203 |

| 209 | | BAT Capital Corp | 4.390% | 8/15/37 | BBB | 229,526 |

| 27 | | Baxter International Inc | 3.500% | 8/15/46 | A- | 30,586 |

| 100 | | Becton Dickinson and Co | 1.957% | 2/11/31 | BBB- | 99,076 |

| 32 | | Becton Dickinson and Co | 4.685% | 12/15/44 | BBB- | 40,721 |

| 30 | | Bell Telephone Co of Canada or Bell Canada | 4.464% | 4/01/48 | BBB+ | 37,469 |

| 100 | | Biogen Inc | 5.200% | 9/15/45 | BBB+ | 133,632 |

| 10 | | Block Financial LLC | 2.500% | 7/15/28 | BBB- | 10,217 |

| 84 | | Boeing Co | 6.125% | 2/15/33 | BBB- | 108,226 |

| 35 | | Boeing Co, (3) | 3.300% | 3/01/35 | BBB- | 35,703 |

| 150 | | Boeing Co | 3.500% | 3/01/39 | BBB- | 153,512 |

| 24 | | Boeing Co | 5.875% | 2/15/40 | BBB- | 31,659 |

| 209 | | Boeing Co | 5.705% | 5/01/40 | BBB- | 271,295 |

| 18 | | BorgWarner Inc | 4.375% | 3/15/45 | BBB+ | 21,192 |

| 100 | | Boston Scientific Corp | 4.550% | 3/01/39 | BBB | 123,926 |

| 15 | | BP Capital Markets America Inc | 3.379% | 2/08/61 | A | 15,577 |

| 200 | | British Telecommunications PLC | 5.125% | 12/04/28 | BBB | 237,908 |

| 130 | | Broadcom Corp / Broadcom Cayman Finance Ltd | 3.500% | 1/15/28 | BBB- | 142,606 |

| 282 | | Broadcom Inc | 4.750% | 4/15/29 | BBB- | 330,865 |

| 10 | | Broadridge Financial Solutions Inc | 2.600% | 5/01/31 | BBB+ | 10,387 |

| 74 | | Canadian Natural Resources Ltd | 5.850% | 2/01/35 | BBB- | 97,006 |

| 12 | | Canadian Natural Resources Ltd | 6.750% | 2/01/39 | BBB- | 17,068 |

| 30 | | Canadian Pacific Railway Co | 2.050% | 3/05/30 | BBB | 30,255 |

| 100 | | Canadian Pacific Railway Co | 4.800% | 8/01/45 | BBB | 130,957 |

| 30 | | Cardinal Health Inc | 4.500% | 11/15/44 | BBB | 35,373 |

| 154 | | Carrier Global Corp | 2.722% | 2/15/30 | BBB- | 162,959 |

| 100 | | Cenovus Energy Inc | 5.250% | 6/15/37 | BBB- | 120,560 |

Nuveen Enhanced Yield U.S. Aggregate Bond ETF (NUAG) (continued)

Portfolio of Investments July 31, 2021

| Principal Amount (000) | | Description (1) | Coupon | Maturity | Ratings (2) | Value |

| | | Industrial (continued) | | | | |

| $ 250 | | Charter Communications Operating LLC / Charter Communications Operating Capital | 5.375% | 4/01/38 | BBB- | $310,909 |

| 155 | | Charter Communications Operating LLC / Charter Communications Operating Capital | 5.375% | 5/01/47 | BBB- | 191,585 |

| 11 | | Choice Hotels International Inc | 3.700% | 1/15/31 | BBB- | 12,062 |

| 21 | | Cigna Corp | 4.500% | 2/25/26 | BBB+ | 23,981 |

| 209 | | Cigna Corp | 4.900% | 12/15/48 | BBB+ | 277,049 |

| 10 | | Cimarex Energy Co | 4.375% | 6/01/24 | BBB- | 10,865 |

| 10 | | CNH Industrial Capital LLC | 1.450% | 7/15/26 | BBB- | 10,058 |

| 100 | | CommonSpirit Health | 2.782% | 10/01/30 | BBB+ | 105,633 |

| 100 | | Conagra Brands Inc | 4.850% | 11/01/28 | BBB- | 120,058 |

| 20 | | Conagra Brands Inc | 5.300% | 11/01/38 | BBB- | 25,789 |

| 11 | | ConocoPhillips, 144A | 2.400% | 2/15/31 | A- | 11,469 |

| 100 | | Constellation Brands Inc | 5.250% | 11/15/48 | BBB- | 137,434 |

| 100 | | Corning Inc | 3.900% | 11/15/49 | BBB+ | 114,995 |

| 180 | | Crown Castle International Corp | 2.500% | 7/15/31 | BBB | 184,276 |

| 18 | | CSX Corp | 4.250% | 3/15/29 | BBB+ | 21,103 |

| 156 | | CSX Corp | 3.800% | 4/15/50 | BBB+ | 184,363 |

| 100 | | CVS Health Corp | 1.750% | 8/21/30 | BBB | 97,821 |

| 222 | | CVS Health Corp | 4.875% | 7/20/35 | BBB | 276,080 |

| 227 | | CVS Health Corp | 4.780% | 3/25/38 | BBB | 284,386 |

| 100 | | Danaher Corp | 4.375% | 9/15/45 | BBB+ | 128,290 |

| 77 | | Dell International LLC / EMC Corp | 6.200% | 7/15/30 | BBB- | 99,685 |

| 25 | | Dell International LLC / EMC Corp | 8.350% | 7/15/46 | BBB- | 41,398 |

| 70 | | Deutsche Telekom International Finance BV | 8.750% | 6/15/30 | BBB+ | 105,748 |

| 17 | | Devon Energy Corp | 5.600% | 7/15/41 | BBB- | 21,186 |

| 20 | | Diamondback Energy Inc | 3.125% | 3/24/31 | BBB- | 20,973 |

| 14 | | Dignity Health | 5.267% | 11/01/64 | BBB+ | 19,780 |

| 143 | | Discovery Communications LLC | 4.000% | 9/15/55 | BBB- | 153,428 |

| 17 | | Dollar General Corp | 4.125% | 4/03/50 | BBB | 20,443 |

| 150 | | Dow Chemical Co | 4.250% | 10/01/34 | BBB | 177,626 |

| 100 | | DR Horton Inc | 1.300% | 10/15/26 | BBB | 100,098 |

| 127 | | DuPont de Nemours Inc | 5.319% | 11/15/38 | BBB+ | 169,473 |

| 10 | | Eagle Materials Inc | 2.500% | 7/01/31 | BBB | 10,098 |

| 38 | | Eaton Corp | 4.150% | 11/02/42 | BBB+ | 46,242 |

| 110 | | eBay Inc | 2.600% | 5/10/31 | BBB+ | 113,930 |

| 9 | | Electronic Arts Inc | 4.800% | 3/01/26 | BBB+ | 10,412 |

| 12 | | Enable Midstream Partners LP | 4.150% | 9/15/29 | BBB- | 13,323 |

| 22 | | Enable Midstream Partners LP | 5.000% | 5/15/44 | BBB- | 24,252 |

| 280 | | Energy Transfer LP | 5.800% | 6/15/38 | BBB- | 347,461 |

| 227 | | Enterprise Products Operating LLC | 5.750% | 3/01/35 | BBB+ | 298,068 |

| Principal Amount (000) | | Description (1) | Coupon | Maturity | Ratings (2) | Value |

| | | Industrial (continued) | | | | |

| $ 100 | | Enterprise Products Operating LLC | 3.950% | 1/31/60 | BBB+ | $112,556 |

| 140 | | Equinix Inc | 2.500% | 5/15/31 | BBB | 145,074 |

| 100 | | Expedia Group Inc | 3.800% | 2/15/28 | BBB- | 109,529 |

| 24 | | Expedia Group Inc | 3.250% | 2/15/30 | BBB- | 25,166 |

| 7 | | FedEx Corp | 3.100% | 8/05/29 | BBB | 7,657 |

| 27 | | FedEx Corp | 3.900% | 2/01/35 | BBB | 31,556 |

| 134 | | FedEx Corp | 4.050% | 2/15/48 | BBB | 155,926 |

| 100 | | Fidelity National Information Services Inc | 1.650% | 3/01/28 | BBB | 100,832 |

| 17 | | Fidelity National Information Services Inc | 4.500% | 8/15/46 | BBB | 21,692 |

| 214 | | Fiserv Inc | 4.400% | 7/01/49 | BBB | 263,434 |

| 16 | | Fortive Corp | 4.300% | 6/15/46 | BBB | 19,425 |

| 138 | | Fox Corp, (3) | 3.500% | 4/08/30 | BBB | 153,769 |

| 200 | | General Electric Co | 4.250% | 5/01/40 | BBB+ | 238,431 |

| 100 | | General Mills Inc | 4.550% | 4/17/38 | BBB | 123,387 |

| 208 | | General Motors Co | 6.600% | 4/01/36 | BBB- | 287,588 |

| 20 | | General Motors Financial Co Inc | 2.400% | 4/10/28 | BBB- | 20,516 |

| 160 | | Gilead Sciences Inc | 4.750% | 3/01/46 | BBB+ | 207,968 |

| 28 | | Global Payments Inc | 4.450% | 6/01/28 | BBB- | 32,521 |

| 100 | | Global Payments Inc | 2.900% | 5/15/30 | BBB- | 106,141 |

| 38 | | GLP Capital LP / GLP Financing II Inc | 5.300% | 1/15/29 | BBB- | 44,778 |

| 100 | | Halliburton Co | 4.850% | 11/15/35 | BBB+ | 119,351 |

| 30 | | Halliburton Co | 4.750% | 8/01/43 | BBB+ | 34,815 |

| 20 | | Hasbro Inc | 3.900% | 11/19/29 | BBB- | 22,508 |

| 131 | | HCA Inc | 4.125% | 6/15/29 | BBB- | 149,389 |

| 10 | | HCA Inc | 3.500% | 7/15/51 | BBB- | 10,315 |

| 6 | | Helmerich & Payne Inc | 4.650% | 3/15/25 | BBB+ | 6,724 |

| 35 | | Hess Corp | 4.300% | 4/01/27 | BBB- | 39,105 |

| 28 | | Hewlett Packard Enterprise Co | 6.200% | 10/15/35 | BBB | 38,828 |

| 100 | | HP Inc | 3.400% | 6/17/30 | BBB | 107,298 |

| 10 | | HP Inc, 144A | 2.650% | 6/17/31 | BBB | 10,097 |

| 17 | | HP Inc | 6.000% | 9/15/41 | BBB | 22,372 |

| 10 | | Huntsman International LLC | 2.950% | 6/15/31 | BBB- | 10,360 |

| 10 | | IDEX Corp | 2.625% | 6/15/31 | BBB | 10,379 |

| 31 | | International Paper Co | 4.800% | 6/15/44 | BBB | 40,501 |

| 27 | | International Paper Co | 4.400% | 8/15/47 | BBB | 34,257 |

| 37 | | J M Smucker Co | 4.250% | 3/15/35 | BBB | 44,188 |

| 34 | | Johnson Controls International plc | 4.625% | 7/02/44 | BBB | 42,965 |

| 6 | | Kansas City Southern | 4.300% | 5/15/43 | BBB | 7,224 |

| 100 | | Kansas City Southern | 4.700% | 5/01/48 | BBB | 127,289 |

| 24 | | Kellogg Co | 2.100% | 6/01/30 | BBB | 24,358 |

| 34 | | Keurig Dr Pepper Inc | 3.200% | 5/01/30 | BBB | 37,406 |

Nuveen Enhanced Yield U.S. Aggregate Bond ETF (NUAG) (continued)

Portfolio of Investments July 31, 2021

| Principal Amount (000) | | Description (1) | Coupon | Maturity | Ratings (2) | Value |

| | | Industrial (continued) | | | | |

| $ 100 | | Keurig Dr Pepper Inc | 4.985% | 5/25/38 | BBB | $128,807 |

| 70 | | Kinder Morgan Energy Partners LP | 6.375% | 3/01/41 | BBB | 97,952 |

| 209 | | Kinder Morgan Inc | 5.200% | 3/01/48 | BBB | 267,355 |

| 6 | | Kroger Co | 2.200% | 5/01/30 | BBB | 6,099 |

| 150 | | Kroger Co | 1.700% | 1/15/31 | BBB | 145,927 |

| 26 | | Kroger Co | 5.400% | 1/15/49 | BBB | 36,182 |

| 30 | | L3Harris Technologies Inc | 2.900% | 12/15/29 | BBB | 32,253 |

| 100 | | L3Harris Technologies Inc | 1.800% | 1/15/31 | BBB | 98,463 |

| 65 | | Laboratory Corp of America Holdings | 2.700% | 6/01/31 | BBB | 67,456 |

| 50 | | Las Vegas Sands Corp | 3.500% | 8/18/26 | BBB- | 52,649 |

| 50 | | Lear Corp | 3.500% | 5/30/30 | BBB | 54,889 |

| 224 | | Lowe's Cos Inc | 4.500% | 4/15/30 | BBB+ | 267,191 |

| 10 | | Lowe's Cos Inc | 2.625% | 4/01/31 | BBB+ | 10,505 |

| 186 | | LYB International Finance BV | 5.250% | 7/15/43 | BBB | 246,073 |

| 22 | | Magellan Midstream Partners LP | 4.200% | 3/15/45 | BBB+ | 23,709 |

| 12 | | Magellan Midstream Partners LP | 4.250% | 9/15/46 | BBB+ | 13,782 |

| 11 | | Magellan Midstream Partners LP | 3.950% | 3/01/50 | BBB+ | 12,087 |

| 17 | | Marathon Petroleum Corp | 5.000% | 9/15/54 | BBB | 20,926 |

| 50 | | Marriott International Inc/MD | 4.650% | 12/01/28 | BBB- | 57,808 |

| 27 | | Marriott International Inc/MD | 4.500% | 10/01/34 | BBB- | 30,940 |

| 16 | | Martin Marietta Materials Inc | 2.500% | 3/15/30 | BBB | 16,527 |

| 10 | | Masco Corp | 1.500% | 2/15/28 | BBB | 9,908 |

| 150 | | McDonald's Corp | 4.700% | 12/09/35 | BBB+ | 189,723 |