| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-180779-15 | ||

|  |

MSBAM 2015-C22

Free Writing Prospectus

Structural and Collateral Term Sheet

$1,107,324,016

(Approximate Total Mortgage Pool Balance)

$950,914,000

(Approximate Offered Certificates)

Morgan Stanley Capital I Inc.

as Depositor

Morgan Stanley Mortgage Capital Holdings LLC

Bank of America, National Association

CIBC Inc.

Starwood Mortgage Funding III LLC

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2015-C22

March 30, 2015

| MORGAN STANLEY | BofA MERRILL LYNCH |

Co-Lead Bookrunning Manager CIBC World Markets | Co-Lead Bookrunning Manager Drexel Hamilton |

| Co-Managers | |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the SEC (File Number 333-180779) for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC web site at www.sec.gov. Alternatively, the depositor or any underwriter or any dealer participating in the offering will arrange to send you the prospectus if you request it by calling toll free 1-866-718-1649 or by email to prospectus@ms.com.

| This is not a research report and was not prepared by any Underwriter’s research department. It was prepared by the Underwriters’ sales, trading, banking or other non-research personnel. Please see additional important information and qualifications at the end of this Term Sheet. |

Neither this Term Sheet nor anything contained herein shall form the basis for any contract or commitment whatsoever. The information contained herein is preliminary as of the date hereof. This Term Sheet is subject to change, completion or amendment from time to time. The information contained herein will be superseded by similar information delivered to you as part of the Free Writing Prospectus. The information contained herein supersedes any such information previously delivered. The information contained herein should be reviewed only in conjunction with the entire Free Writing Prospectus. All of the information contained herein is subject to the same limitations and qualifications contained in the Free Writing Prospectus. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described in the Free Writing Prospectus and the Prospectus attached thereto as Exhibit A. The information contained herein will be more fully described in the Free Writing Prospectus. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Free Writing Prospectus in its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this Term Sheet is truthful or complete. Any representation to the contrary is a criminal offense.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of, or attached to, the email communication to which this Term Sheet may have been attached are not applicable to this Term Sheet and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of this Term Sheet having been sent via Bloomberg or another email system.

IMPORTANT NOTICE REGARDING THE CONDITIONS FOR THIS OFFERING OF ASSET-BACKED SECURITIES

THE ASSET-BACKED SECURITIES REFERRED TO IN THIS TERM SHEET ARE BEING OFFERED WHEN, AS AND IF ISSUED. IN PARTICULAR, YOU ARE ADVISED THAT THE ASSET-BACKED SECURITIES, AND THE ASSET POOL BACKING THEM, ARE SUBJECT TO MODIFICATION OR REVISION (INCLUDING, AMONG OTHER THINGS, THE POSSIBILITY THAT ONE OR MORE CLASSES OF SECURITIES MAY BE SPLIT, COMBINED OR ELIMINATED), AT ANY TIME PRIOR TO ISSUANCE OR AVAILABILITY OF A FINAL PROSPECTUS. AS A RESULT, YOU MAY COMMIT TO PURCHASE SECURITIES THAT HAVE CHARACTERISTICS THAT MAY CHANGE, AND YOU ARE ADVISED THAT ALL OR A PORTION OF THE SECURITIES MAY NOT BE ISSUED THAT HAVE THE CHARACTERISTICS DESCRIBED IN THIS TERM SHEET. OUR OBLIGATION TO SELL SECURITIES TO YOU IS CONDITIONED ON THE SECURITIES AND THE UNDERLYING TRANSACTION HAVING THE CHARACTERISTICS DESCRIBED IN THIS TERM SHEET. IF WE DETERMINE THAT THE FOREGOING CONDITION IS NOT SATISFIED IN ANY MATERIAL RESPECT, WE WILL NOTIFY YOU, AND NEITHER THE ISSUING ENTITY NOR ANY UNDERWRITER WILL HAVE ANY OBLIGATION TO YOU TO DELIVER ALL OR ANY PORTION OF THE SECURITIES WHICH YOU HAVE COMMITTED TO PURCHASE, AND THERE WILL BE NO LIABILITY BETWEEN US AS A CONSEQUENCE OF THE NON-DELIVERY.

This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

T-1

MSBAM 2015-C22 | Structural Overview |

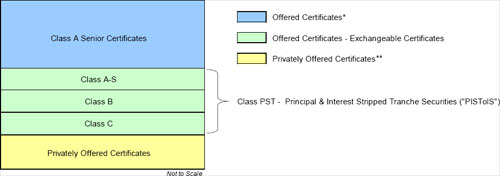

Offered Certificates

| Class | Expected Ratings (Moody’s/Fitch/KBRA)(1) | Approximate Initial Certificate Principal Balance or Notional Amount(2) | Approximate Initial Credit Support(3) | Pass-Through Rate Description | Expected Weighted Average Life (Years)(5) | Principal Window (Months)(5) | Certificate Principal UW NOI Debt Yield(6)(8) | Certificate Principal to Value Ratio(7)(8) | ||||||||

| Class A-1 | Aaa(sf)/AAAsf/AAA(sf) | $55,100,000 | 30.000% | (4) | 2.78 | 1-59 | 14.3% | 47.2% | ||||||||

| Class A-2 | Aaa(sf)/AAAsf/AAA(sf) | $66,500,000 | 30.000% | (4) | 4.92 | 59-60 | 14.3% | 47.2% | ||||||||

| Class A-SB | Aaa(sf)/AAAsf/AAA(sf) | $84,700,000 | 30.000% | (4) | 7.33 | 60-115 | 14.3% | 47.2% | ||||||||

| Class A-3 | Aaa(sf)/AAAsf/AAA(sf) | $250,000,000 | 30.000% | (4) | 9.78 | 115-119 | 14.3% | 47.2% | ||||||||

| Class A-4 | Aaa(sf)/AAAsf/AAA(sf) | $318,826,000 | 30.000% | (4) | 9.90 | 119-120 | 14.3% | 47.2% | ||||||||

| Class X-A | Aa2(sf)/AAAsf/AAA(sf) | $836,029,000(9) | N/A | Variable IO(10) | N/A | N/A | N/A | N/A | ||||||||

Class A-S(11) | Aa2(sf)/AAAsf/AAA(sf) | $60,903,000 | 24.500% | (4) | 9.98 | 120-120 | 13.2% | 51.0% | ||||||||

Class B(11) | NR/AA-sf/AA(sf) | $63,671,000 | 18.750% | (4) | 9.98 | 120-120 | 12.3% | 54.8% | ||||||||

Class PST(11) | NR/A-sf/A-(sf) | $175,788,000 | 14.125% | (4) | 9.98 | 120-120 | 11.6% | 58.0% | ||||||||

Class C(11) | NR/A-sf/A-(sf) | $51,214,000 | 14.125% | (4) | 9.98 | 120-120 | 11.6% | 58.0% |

Privately Offered Certificates(12)

| Class | Expected Ratings (Moody’s/Fitch/KBRA)(1) | Approximate Initial Certificate Principal Balance or Notional Amount(2) | Approximate Initial Credit Support(3) | Pass-Through Rate Description | Expected Weighted Average Life (Years)(5) | Principal Window (Months)(5) | Certificate Principal UW NOI Debt Yield(6) | Certificate Principal to Value Ratio(7) | ||||||||

| Class X-B | NR/AA-sf/AAA(sf) | $63,671,000(9) | N/A | Variable IO(10) | N/A | N/A | N/A | N/A | ||||||||

| Class D | NR/BBB-sf/BBB-(sf) | $62,287,000 | 8.500% | (4) | 9.98 | 120-120 | 10.9% | 61.8% | ||||||||

| Class E | NR/BB-sf/BB(sf) | $26,299,000 | 6.125% | (4) | 9.98 | 120-120 | 10.7% | 63.4% | ||||||||

| Class F | NR/B-sf/B+(sf) | $13,841,000 | 4.875% | (4) | 9.98 | 120-120 | 10.5% | 64.2% | ||||||||

| Class G | NR/NR/B-(sf) | $17,994,000 | 3.250% | (4) | 9.98 | 120-120 | 10.3% | 65.3% | ||||||||

| Class H | NR/NR/NR | $35,989,016 | 0.000% | (4) | 9.98 | 120-120 | 10.0% | 67.5% |

| (1) | Ratings shown are those of Moody’s Investors Service, Inc., Fitch Ratings, Inc. and Kroll Bond Rating Agency, Inc. Certain nationally recognized statistical rating organizations that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended, or otherwise to rate the certificates. There can be no assurance as to what ratings a non-hired nationally recognized statistical rating organization would assign. See “Risk Factors—Risks Related to the Offered Certificates—Ratings of the Offered Certificates Do Not Represent Any Assessment of the Yield to Maturity That a Certificateholder May Experience and Such Ratings May Be Reviewed, Revised, Suspended, Downgraded, Qualified or Withdrawn By the Applicable Rating Agency” and “Ratings” in the other free writing prospectus, which is expected to be dated March 30, 2015 (the “Free Writing Prospectus”), to which the prospectus dated October 1, 2013 (the “Prospectus”) is attached as Exhibit A. Capitalized terms used but not defined herein have the meanings assigned to such terms in the Free Writing Prospectus. |

| (2) | The certificate principal balances and notional amounts are approximate and on the closing date may vary by up to 5%. Mortgage loans may be removed from or added to the mortgage pool prior to the closing date within the same maximum permitted variance. Any reduction or increase in the aggregate principal balance of mortgage loans within these parameters will result in changes to the initial certificate principal balance or notional amount of each class of certificates shown in the table above and to the other statistical data contained herein and in the Free Writing Prospectus. In addition, the notional amounts of the Class X-A and Class X-B Certificates may vary depending upon the final pricing of the classes of certificates and/or trust components whose certificate principal balances comprise such notional amounts, and, if as a result of such pricing the pass-through rate of the Class X-A or Class X-B Certificates, as applicable, would be equal to zero, such class of certificates will not be issued on the closing date of this securitization. |

| (3) | The percentages indicated under the column “Approximate Initial Credit Support” with respect to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates represent the approximate credit support for the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates in the aggregate. The percentage indicated under the column “Approximate Initial Credit Support” with respect to the Class C Certificates and the Class PST Certificates represents the approximate credit support for the underlying Class C trust component. |

| (4) | The Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-S, Class B, Class C, Class D, Class E, Class F, Class G and Class H Certificates will, at all times, accrue interest at a per annum rate equal to (i) a fixed rate, (ii) a fixed rate subject to a cap equal to the weighted average of the net interest rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of 12 30-day months) or (iii) a rate equal to the weighted average of the net interest rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of 12 30-day months) less a specified percentage, which percentage may be zero. The Class PST Certificates will not have a pass-through rate, but will be entitled to receive the sum of the interest distributable on the Class PST components. The pass-through rates for the Class A-S Certificates, the Class A-S trust component and the Class PST Component A-S will, at all times, be the same. The pass-through rates for the Class B Certificates, the Class B trust component and the Class PST Component B will, at all times, be the same. The pass-through rates for the Class C Certificates, the Class C trust component and the Class PST Component C will, at all times, be the same. |

| (5) | The principal window is expressed in months following the closing date and reflects the period during which distributions of principal would be received under the assumptions set forth in the following sentence. The expected weighted average life and principal window figures set forth above are based on the following assumptions, among others: (i) no defaults or subsequent losses on the mortgage loans; (ii) no extensions of maturity dates of the mortgage loans; (iii) payment in full on the stated maturity date or, in the case of any mortgage loan having an anticipated repayment date, on the anticipated repayment date; and (iv) no prepayments of the mortgage loans prior to maturity or, in the case of a mortgage loan having an anticipated repayment date, prior to such anticipated repayment date. See the structuring assumptions set forth under “Yield, Prepayment and Maturity Considerations—Weighted Average Life” in the Free Writing Prospectus. |

| (6) | Certificate Principal UW NOI Debt Yield for any class of principal balance certificates (other than the Exchangeable Certificates) is calculated as the product of (a) the weighted average UW NOI Debt Yield for the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial principal balance of all the principal balance certificates (other than the Exchangeable Certificates) and trust components, and the denominator of which is the total initial principal balance of the subject class of principal balance certificates and all other classes of principal balance certificates (other than the Exchangeable Certificates) and trust components, if any, that are senior to such class. The Certificate Principal UW NOI Debt Yields of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are calculated in the aggregate for those classes as if they were a single class. |

| (Footnotes continued on next page) |

This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

T-2

MSBAM 2015-C22 | Structural Overview |

| (7) | Certificate Principal to Value Ratio for any class of principal balance certificates (other than the Exchangeable Certificates) is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio of the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial principal balance of the subject class of principal balance certificates and all other classes of principal balance certificates (other than the Exchangeable Certificates) and trust components, if any, that are senior to such class, and the denominator of which is the total initial principal balance of all the principal balance certificates (other than the Exchangeable Certificates) and trust components. The Certificate Principal to Value Ratios of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are calculated in the aggregate for those classes as if they were a single class. |

| (8) | Certificate Principal UW NOI Debt Yield for the Class A-S, Class B and Class C Certificates is calculated as the product of (a) the weighted average UW NOI Debt Yield for the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial principal balance of all the principal balance certificates (other than the Exchangeable Certificates) and trust components, and the denominator of which is the total initial principal balance of the Class A-S trust component, the Class B trust component or the Class C trust component, as applicable, and all other classes of principal balance certificates (other than the Exchangeable Certificates) and trust components that are senior to such trust component. Certificate Principal to Value Ratio for the Class A-S, Class B and Class C Certificates is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio of the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial principal balance of the Class A-S trust component, the Class B trust component or the Class C trust component, as applicable, and all other classes of principal balance certificates (other than the Exchangeable Certificates) and trust components that are senior to such trust component, and the denominator of which is the total initial principal balance of all the principal balance certificates (other than the Exchangeable Certificates) and trust components. The Certificate Principal UW NOI Debt Yield and Certificate Principal to Value Ratio of the Class PST Certificates are equal to the respective amounts for the Class C Certificates. |

| (9) | The Class X-A and Class X-B Certificates (collectively, “the Class X Certificates”) will not have certificate principal balances and will not be entitled to receive distributions of principal. Interest will accrue on the Class X-A and Class X-B Certificates at their respective pass-through rates based upon their respective notional amounts. The notional amount of the Class X-A Certificates will equal the aggregate certificate principal balance of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates and the Class A-S trust component outstanding from time to time. The notional amount of the Class X-B Certificates will equal the certificate principal balance of the Class B trust component outstanding from time to time. |

| (10) | The pass-through rate on the Class X-A Certificates will generally be equal to the excess, if any, of (a) the weighted average of the net interest rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of 12 30-day months), over (b) the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates and the Class A-S trust component as described in the Free Writing Prospectus. The pass-through rate on the Class X-B Certificates will generally be equal to the excess, if any, of (a) the weighted average of the net interest rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of 12 30-day months), over (b) the pass-through rate of the Class B trust component as described in the Free Writing Prospectus. |

| (11) | The Class A-S, Class B, Class PST and Class C Certificates are “Exchangeable Certificates.” On the closing date, the upper-tier REMIC of the issuing entity will issue the Class A-S, Class B and Class C trust components (each a “trust component”), which will have outstanding principal balances on the closing date of $60,903,000, $63,671,000 and $51,214,000, respectively. The trust components will be held in the grantor trust for the benefit of the holders of the Class A-S, Class B, Class PST and Class C Certificates. The Class A-S, Class B, Class PST and Class C Certificates will, at all times, represent undivided beneficial ownership interests, held through the grantor trust, in one or more of such trust components. Each class of the Class A-S, Class B and Class C Certificates will, at all times, represent an undivided beneficial ownership interest in a percentage of the outstanding certificate principal balance of the trust component with the same alphabetical class designation. The Class PST Certificates will, at all times, represent an undivided beneficial ownership interest in the remaining percentages of the outstanding certificate principal balances of the Class A-S, Class B and Class C trust components, and such portions of those trust components are respectively referred to in this Term Sheet as the Class PST Component A-S, Class PST Component B and Class PST Component C (collectively, the “Class PST Components”). Following any exchange of Class A-S, Class B and Class C Certificates for Class PST Certificates or any exchange of Class PST Certificates for Class A-S, Class B and Class C Certificates as described in the Free Writing Prospectus, the percentage interests of the outstanding certificate principal balances of the Class A-S, Class B and Class C trust components that are represented by the Class A-S, Class B, Class PST and Class C Certificates will be increased or decreased accordingly. The initial certificate principal balance of each class of the Class A-S, Class B and Class C Certificates shown in the table represents the maximum certificate principal balance of such class without giving effect to any exchange. The initial certificate principal balance of the Class PST Certificates shown in the table is equal to the aggregate of the initial certificate principal balances of the Class A-S, Class B and Class C Certificates shown in the table and represents the maximum certificate principal balance of the Class PST Certificates that could be issued in an exchange; such initial certificate principal balance is not included in the aggregate certificate principal balance of the offered certificates set forth on the cover page of this Term Sheet. The certificate principal balances of the Class A-S, Class B and Class C Certificates to be issued on the closing date will be reduced, in required proportions, by an amount equal to the certificate principal balance of the Class PST Certificates issued on the closing date. Distributions and allocations of payments and losses with respect to the Exchangeable Certificates are described in this Term Sheet under “Allocations and Distributions on the Exchangeable Certificates” and under “Description of the Offered Certificates—Distributions” in the Free Writing Prospectus. |

|

* For purposes of the foregoing chart, the Class A-Senior Certificates include the Class X-A Certificates, which are also offered certificates, in regards to payments of interest. |

| ** For purposes of the foregoing chart, the Class X-B Certificates have the same payment priority as the Class A Senior Certificates in regards payments of interest. The foregoing chart does not address the Class V Certificates (which represent interests in excess interest in respect of any anticipated repayment date loans). |

| (12) | Not offered pursuant to the Prospectus, the Free Writing Prospectus or this Term Sheet. Information provided in this Term Sheet regarding the characteristics of these certificates is provided only to enhance your understanding of the offered certificates. The privately offered certificates also include the Class V and Class R Certificates, which do not have a certificate principal balance, notional amount, pass-through rate, rating or rated final distribution date, and which are not shown in the chart. The Class V Certificates represent a beneficial ownership interest held through the grantor trust in certain excess interest in respect of mortgage loans having anticipated repayment dates, if any. The Class R Certificates represent the beneficial ownership of the residual interest in each of the real estate mortgage investment conduits, as further described in the Free Writing Prospectus. |

This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

T-3

MSBAM 2015-C22 | Structural Overview |

Issue Characteristics

| Offered Certificates: | $950,914,000 (approximate) monthly pay, multi-class, commercial mortgage pass-through certificates, consisting of nine principal balance classes (Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-S, Class B, Class PST and Class C) and one interest-only class (Class X-A) | |

| Co-Lead Bookrunning Managers: | Morgan Stanley & Co. LLC and Merrill Lynch, Pierce, Fenner & Smith Incorporated | |

| Co-Managers: | CIBC World Markets Corp. and Drexel Hamilton, LLC | |

| Mortgage Loan Sellers: | Morgan Stanley Mortgage Capital Holdings LLC, Bank of America, National Association, CIBC Inc. and Starwood Mortgage Funding III LLC | |

| Rating Agencies: | Moody’s Investors Service, Inc., Fitch Ratings, Inc. and Kroll Bond Rating Agency, Inc. | |

| Master Servicer: | Wells Fargo Bank, National Association | |

| Special Servicer: | Midland Loan Services, a Division of PNC Bank, National Association | |

Certificate Administrator/ Certificate Registrar/Custodian: | Wells Fargo Bank, National Association | |

| Trustee: | Wilmington Trust, National Association | |

| Trust Advisor: | Park Bridge Lender Services LLC | |

Initial Controlling Class Representative: | DoubleLine Capital LP or its affiliate | |

| Cut-off Date: | April 1, 2015. For purposes of the information contained in this term sheet (this “Term Sheet”), scheduled payments due in April 2015 with respect to mortgage loans not having payment dates on the first day of each month have been deemed received on April 1, 2015, not the actual day on which such scheduled payments were due | |

| Expected Pricing Date: | Week of April 6, 2015 | |

| Expected Closing Date: | Week of April 20, 2015 | |

| Determination Dates: | The 11th calendar day of each month (if the 11th calendar day is not a business day, the next succeeding business day), commencing in May 2015 | |

| Distribution Dates: | The 4th business day following the Determination Date in each month, commencing in May 2015 | |

| Rated Final Distribution Date: | The Distribution Date in April 2048 | |

| Interest Accrual Period: | Preceding calendar month | |

| Payment Structure: | Sequential pay | |

| Tax Treatment: | REMIC, except that the Class A-S, Class B, Class PST and Class C Certificates will evidence an interest in the grantor trust | |

| Optional Termination: | 1.00% clean-up call | |

| Minimum Denominations: | $10,000 for each class of Offered Certificates (other than Class X-A); $100,000 for the Class X-A Certificates | |

| Settlement Terms: | DTC, Euroclear and Clearstream | |

| Legal/Regulatory Status: | Each class of Offered Certificates is expected to be eligible for exemptive relief under ERISA. No class of Offered Certificates is SMMEA eligible. | |

| Analytics: | The certificate administrator is expected to make available all distribution date statements, CREFC® reports and supplemental notices received by it to certain modeling financial services as described in the Free Writing Prospectus. | |

| Bloomberg Ticker: | MSBAM 2015-C22 <MTGE><GO> | |

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. SEE THE “RISK FACTORS” SECTION OF THE FREE WRITING PROSPECTUS AND THE “RISK FACTORS” SECTION OF THE PROSPECTUS. |

This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

T-4

MSBAM 2015-C22 | Structural Overview |

Structural Overview

| Accrual: | Each class of Offered Certificates will accrue interest on a 30/360 basis. | |

| Amount and Order of Distributions: | On each distribution date, certificateholders will be entitled to receive distributions of interest and principal from funds received with respect to the mortgage loans and available for distribution. Funds available for distribution on the certificates will be net of excess interest, excess liquidation proceeds and specified trust expenses, including, without limitation, all advance reimbursements (with interest) and all servicing fees and expenses, certificate administrator fees (including trustee fees and custodian fees) and expenses, special servicer compensation, trust advisor fees (together with certain trust advisor consulting fees), CREFC® License Fees and expenses as set forth below. Distributions to certificateholders on each distribution date out of payments (or advances in lieu thereof) and other collections on the mortgage loans will be in an amount equal to each class’s interest and principal entitlement, subject to: (i) payment of the respective interest entitlement for any other class of certificates bearing an earlier alphanumeric designation (except (x) in respect of the distribution of interest among the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class X-A and Class X-B Certificates, which will have the same senior priority and be distributed pro rata, and (y) in respect of the distribution of interest among the Class A-S, Class B, Class PST and Class C Certificates as described below under “Allocations and Distributions on the Exchangeable Certificates”); (ii) if applicable, payment of the respective principal entitlement for the distribution date to the outstanding classes of principal balance certificates, first, to the Class A-SB Certificates, until the principal balance of such class has been reduced to the planned principal balance for the related distribution date set forth on Appendix VII to the Free Writing Prospectus, then, to the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB Certificates, in that order (or pro rata among such classes if the principal balance of all other classes of certificates has been reduced to zero as a result of the allocation of mortgage loan losses or trust advisor expenses to such other classes, or if the aggregate appraisal reduction equals or exceeds the aggregate principal balance of the Class A-S through Class H Certificates (including the Class PST Certificates)), until the principal balance of each such class has been reduced to zero, then, to the Class A-S, Class B, Class PST and Class C Certificates as described below under “Allocations and Distributions on the Exchangeable Certificates” until the principal balance of each such class has been reduced to zero, and then to the Class D, Class E, Class F, Class G and Class H Certificates, in that order, until the principal balance of each such class has been reduced to zero; and (iii) the allocation of trust advisor expenses, (a) first, to reduce payments of interest on the Class D Certificates, the Class C trust component and the Class B trust component, in that order, (b) second, to reduce payments of principal on the Class D Certificates, the Class C trust component, the Class B trust component and the Class A-S trust component, in that order, and (c) third, to reduce payments of principal on the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates on a pro rata basis. No trust advisor expenses (which do not include the trust advisor fee) will be allocated to or otherwise borne by the Control Eligible Certificates. As a result, none of the classes of such certificates will provide protection to the more senior classes of certificates for the purposes of allocating losses based on trust advisor expenses. Trust advisor expenses allocated to the Class A-S trust component, the Class B trust component and the Class C trust component will be allocated to the Class A-S, Class B, Class PST and Class C Certificates as described below under “Allocations and Distributions on the Exchangeable Certificates.” | |

| Interest and Principal Entitlements: | Interest distributable on any class of certificates (other than the Exchangeable Certificates and the Class V and Class R Certificates) or trust component on any distribution date, with various adjustments described under “Description of the Offered Certificates—Distributions” in the Free Writing Prospectus, represents all unpaid interest accrued with respect to that class of certificates or trust component through the end of the interest accrual period that corresponds to that distribution date. Interest accrues with respect to each such interest-bearing certificate and each trust component during each interest accrual period at the applicable pass-through rate for, and on the principal balance or notional amount, as applicable, of that certificate or trust component outstanding immediately prior to, the distribution date that corresponds to that interest accrual period. However, as described in “Description of the Offered Certificates—Distributions” in the Free Writing Prospectus, there are circumstances relating to the timing of prepayments in which the interest entitlement with respect to any certificate or trust component for a distribution date could be less than one full month’s interest at the pass-through rate on the certificate’s or trust component’s principal balance or notional amount. In addition, certain specified trust fund expenses, the right of the master servicer, the special servicer and the trustee to reimbursement for payment of advances (with interest thereon), and the rights of such parties and of the certificate administrator, the custodian and, subject to certain limitations, the trust advisor to the payments of compensation and reimbursement of certain costs and expenses will be prior to a certificateholder’s right to receive distributions of principal or interest. In addition, the right of the trust advisor to receive reimbursement of trust advisor expenses will be prior to the right of the holders of the Class B, Class PST, Class C and Class D Certificates to receive payments of interest, and to the right of the holders of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-S, Class B, Class PST, Class C and Class D Certificates to receive payments of principal. The amount of principal available to be distributed on the classes entitled to principal on a particular distribution date will, in general, be equal to the sum of: (i) the principal portion of all scheduled payments, other than balloon payments, to the extent received during the related collection period or advanced by the |

This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

T-5

MSBAM 2015-C22 | Structural Overview |

master servicer or other party (in accordance with the pooling and servicing agreement) in respect of such distribution date; (ii) all principal prepayments and the principal portion of balloon payments received during the related collection period; (iii) the principal portion of other collections on the mortgage loans received during the related collection period, for example liquidation proceeds, condemnation proceeds, insurance proceeds and income on other “real estate owned” (“REO”); and (iv) the principal portion of proceeds of mortgage loan repurchases received during the related collection period; subject to certain adjustments described in the Free Writing Prospectus relating to the payment or reimbursement of nonrecoverable advances, workout-delayed reimbursement amounts and trust advisor expenses, and exclusive of any late collections of principal received during the related collection period for which there is an outstanding advance. The Class V, Class R, Class X-A and Class X-B Certificates will not be entitled to principal distributions. | ||

| Allocations and Distributions on the Exchangeable Certificates: | On the closing date, the upper-tier REMIC of the issuing entity will issue the Class A-S, Class B and Class C trust components (each a “trust component”), which will have outstanding principal balances on the closing date of $60,903,000, $63,671,000 and $51,214,000, respectively. The trust components will be held in the grantor trust for the benefit of the holders of the Class A-S, Class B, Class PST and Class C Certificates. Each class of the Class A-S, Class B and Class C Certificates will, at all times, represent an undivided beneficial ownership interest, held through the grantor trust, in a percentage of the outstanding principal balance of the trust component with the same alphabetical class designation. The Class PST Certificates will, at all times, represent an undivided beneficial ownership interest, held through the grantor trust, in the remaining percentages of the outstanding principal balances of the Class A-S, Class B and Class C trust components, which portions of these trust components are respectively referred to in this Term Sheet as the “Class PST Component A-S,” “Class PST Component B” and “Class PST Component C” (collectively, the “Class PST Components”). Distributions of principal and interest will be made sequentially with respect to the trust components in alphabetic order of class designation after all required distributions of interest and principal have been made with respect to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class X-A and Class X-B Certificates. Interest, principal, prepayment premiums, yield maintenance charges, voting rights and any losses (including, without limitation, as a result of trust advisor expenses) or collateral support deficits that are allocated to the Class A-S, Class B or Class C trust component will be distributed or allocated, as applicable, as between the Class A-S, Class B or Class C Certificates, as applicable, on the one hand, and Class PST Component A-S, Class PST Component B or Class PST Component C, as applicable (and correspondingly, the Class PST Certificates), on the other hand, pro rata, based on their respective percentage interests in the Class A-S, Class B or Class C trust component, as applicable. For a complete description of the allocations and distributions with respect to the Class A-S trust component, the Class B trust component and the Class C trust component (and correspondingly the Class A-S, Class B, Class PST and Class C Certificates and the Class PST Component A-S, Class PST Component B and Class PST Component C), see “Description of the Offered Certificates” in the Free Writing Prospectus. See “Material Federal Income Tax Consequences” in the Free Writing Prospectus for a discussion of the tax treatment of the Exchangeable Certificates. | |

| Exchanges of Exchangeable Certificates: | If you own Class A-S, Class B and Class C Certificates, you will be able to exchange them for a proportionate interest in the Class PST Certificates, and vice versa, as described in the Free Writing Prospectus. You can exchange your Exchangeable Certificates by notifying the certificate administrator. Holders of Class PST Certificates will be entitled to receive principal and interest that would otherwise be payable on the applicable proportion of the Class A-S, Class B and Class C Certificates exchangeable therefor. Any such allocations of principal and interest as between classes of Exchangeable Certificates will have no effect on the principal or interest entitlements of any other class of certificates. The Free Writing Prospectus describes the available combinations of Exchangeable Certificates eligible for exchange. | |

| Special Servicer Compensation: | The special servicer is entitled to a special servicing fee payable from general collections on the mortgage loans (and any related B note or serviced companion loan). The special servicing fee for each distribution date is calculated based on the outstanding principal balance of each mortgage loan (other than any non-serviced mortgage loan) that is a specially serviced mortgage loan (and any related B note or serviced companion loan) or as to which the related mortgaged property has become an REO property at the special servicing fee rate, which will be 0.25% per annum. Any primary servicing fee or sub-servicing fee will be paid by the special servicer out of the fees described above. The special servicer is also entitled to additional fees and amounts, including, without limitation, income on the amounts held in certain permitted investments. The special servicer will also be entitled to (i) liquidation fees generally equal to 1.0% of liquidation proceeds in respect of a specially serviced mortgage loan (and any related B note or serviced companion loan) or REO property and (ii) workout fees generally equal to 1.0% of interest and principal payments made in respect of a rehabilitated mortgage loan (and any related B note or serviced companion loan), subject to a cap with respect to each such fee of $1,000,000 with respect to any mortgage loan, loan pair, non-serviced loan combination, A/B whole loan or REO property and subject to certain adjustments and exceptions as described in the Free Writing Prospectus under “Servicing of the Mortgage Loans—The Special Servicer—Special Servicer Compensation.” With respect to any non-serviced mortgage loan, the related special servicer under the related other pooling and servicing agreement pursuant to which such mortgage loan is being serviced will be entitled to similar compensation as that described above with respect to such non-serviced mortgage loan under such other pooling and servicing agreement as further described in the Free Writing Prospectus, although any related fees may accrue at a different rate and there may be a higher (or no) cap on liquidation and workout fees. |

This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

T-6

MSBAM 2015-C22 | Structural Overview |

| Prepayment Premiums/Yield Maintenance Charges: | On any distribution date, prepayment premiums or yield maintenance charges collected in respect of each mortgage loan during the related collection period will be distributed by the certificate administrator on the classes of certificates or trust components as follows: to each class of principal balance certificates (other than the Exchangeable Certificates and the Class E, Class F, Class G and Class H Certificates) and each trust component then entitled to distributions of principal on such distribution date, an amount equal to the product of (a) a fraction, the numerator of which is the amount distributed as principal to that class or trust component on that distribution date, and the denominator of which is the total amount distributed as principal to all classes of principal balance certificates (other than the Exchangeable Certificates) and trust components on that distribution date, (b) the Base Interest Fraction for the related principal prepayment and that class or trust component and (c) the amount of the prepayment premium or yield maintenance charge collected in respect of such principal prepayment during the one month period ending on the related determination date. Any prepayment premiums or yield maintenance charges relating to the mortgage loans collected during the related collection period and remaining after those distributions described above (as to the applicable distribution date, the “Class X YM Distribution Amount”) will be distributed to the holders of the Class X Certificates, as follows: first, to holders of the Class X-A Certificates in an amount equal to the product of (a) a fraction, the numerator of which is the total amount of principal distributed on the applicable distribution date with respect to the class(es) of certificates and/or trust component(s) whose certificate principal balances comprise the notional amount of such class of Class X Certificates, and the denominator of which is the total amount of principal distributed on the applicable distribution date with respect to all classes of principal balance certificates (other than the Exchangeable Certificates) and trust component(s), multiplied by (b) the Class X YM Distribution Amount for the applicable distribution date; and second, to the holders of the Class X-B Certificates in an amount equal to the portion of the Class X YM Distribution Amount remaining after the distributions to the holders of the Class X-A Certificates. Distributions of prepayment premiums and yield maintenance charges made on the Class A-S trust component, the Class B trust component and the Class C trust component will be distributed to the Class A-S, Class B and Class C Certificates and the Class PST Components (and correspondingly the Class PST Certificates) as described above in “Allocations and Distributions on the Exchangeable Certificates.” No prepayment premiums or yield maintenance charges will be distributed to holders of the Class E, Class F, Class G, Class H, Class V or Class R Certificates. The “Base Interest Fraction,” with respect to any principal prepayment of any mortgage loan that provides for payment of a prepayment premium or yield maintenance charge, and with respect to any class of principal balance certificates (other than the Exchangeable Certificates and the Class E, Class F, Class G and Class H Certificates) or trust component, is a fraction (A) whose numerator is the greater of (x) zero and (y) the difference between (i) the pass-through rate on that class of certificates or trust component, as applicable, and (ii) the applicable discount rate and (B) whose denominator is the difference between (i) the mortgage interest rate on the related mortgage loan and (ii) the applicable discount rate; provided that under no circumstances will the Base Interest Fraction be greater than one. If the discount rate referred to above is greater than or equal to the mortgage interest rate on the related mortgage loan, then the Base Interest Fraction will equal zero; provided that if the discount rate referred to above is greater than or equal to the mortgage interest rate on the related mortgage loan, but is less than the pass-through rate on the subject class of certificates or trust component, the Base Interest Fraction shall be equal to 1.0. Consistent with the foregoing, the Base Interest Fraction is equal to: |

| (Pass-Through Rate – Discount Rate) | |||

| (Mortgage Rate – Discount Rate) |

Collateral Support Deficits: | On each distribution date, immediately following the distributions made to the certificateholders on that date, the certificate administrator will be required to calculate the amount, if any, by which (1) the aggregate stated principal balance of pool of the mortgage loans, including any mortgage loans as to which the related mortgaged properties have become REO properties, expected to be outstanding immediately following that distribution date, is less than (2) the aggregate principal balance of the principal balance certificates after giving effect to distributions of principal on that distribution date and the allocation of any excess trust advisor expenses to reduce the principal balances of the principal balance certificates that are not Control Eligible Certificates on that distribution date (any such deficit, a “Collateral Support Deficit”). On each distribution date, the certificate administrator will be required to allocate any Collateral Support Deficit to the respective classes of principal balance certificates (other than the Exchangeable Certificates) and the trust components in the following order: to the Class H Certificates, the Class G Certificates, the Class F Certificates, the Class E Certificates, the Class D Certificates, the Class C trust component, the Class B trust component, and the Class A-S trust component, in that order, in each case in reduction of and until the remaining principal balance of that class of certificates or trust components has been reduced to zero. Following the reduction of the principal balances of all such classes of certificates to zero, the certificate administrator will be required to allocate the Collateral Support Deficit to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates, pro rata (based upon their respective principal balances), until the remaining principal balances of those classes of certificates have been reduced to zero. Any Collateral Support Deficit allocated to a class of certificates will be allocated to the respective certificates of such class in proportion to the percentage interests evidenced by the respective certificates. Any such Collateral Support Deficit allocated to the Class A-S, Class B and Class C trust components will, in turn, be allocated to the Class A-S, Class B, Class PST and Class C Certificates as described above in “Allocations and Distributions on the Exchangeable Certificates.” | |

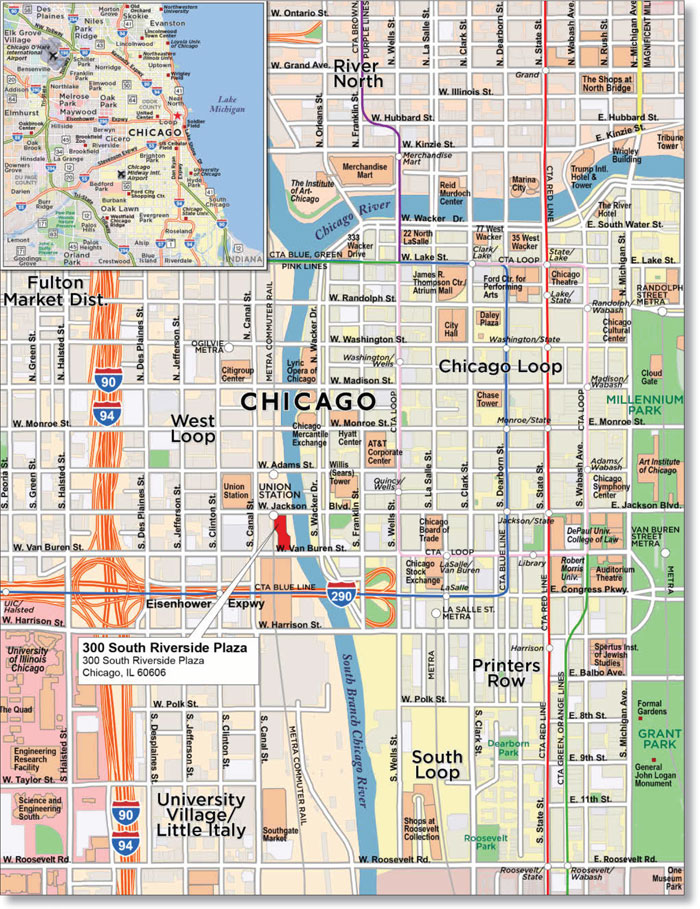

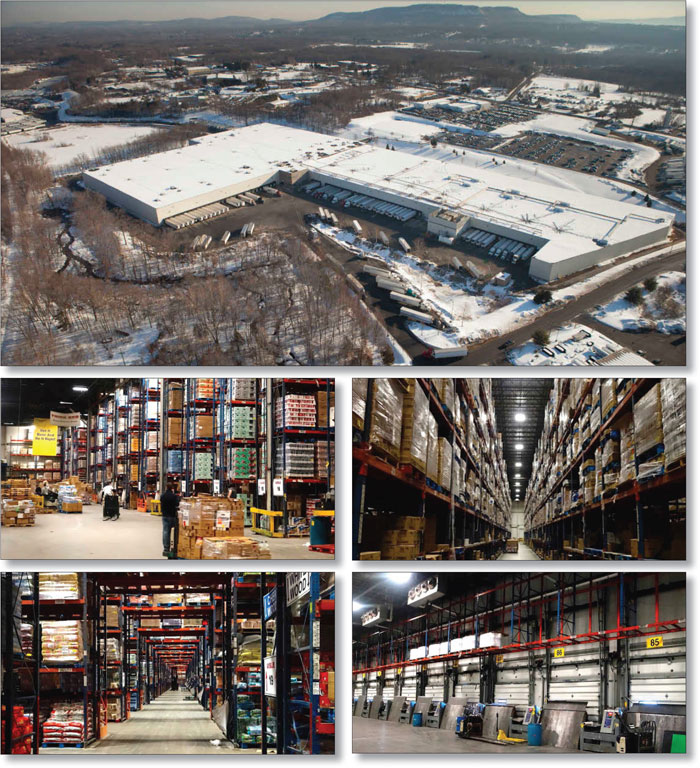

| A/B Whole Loans and Loan Pairs: | The mortgaged property identified on Appendix I to the Free Writing Prospectus as 300 South Riverside Plaza Fee secures on a pari passu basis (i) a mortgage loan (the “300 South Riverside Plaza Fee mortgage loan”) |

This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

T-7

MSBAM 2015-C22 | Structural Overview |

with an outstanding principal balance as of the cut-off date of $100,000,000, representing approximately 9.0% of the initial pool balance, and (ii) a pari passu promissory note that has an outstanding principal balance as of the cut-off date of $67,000,000 (the “300 South Riverside Plaza Fee serviced companion loan” and a “serviced companion loan”) that is not part of the mortgage pool and that is currently held by Morgan Stanley Bank, N.A. The 300 South Riverside Plaza Fee mortgage loan and the 300 South Riverside Plaza Fee serviced companion loan together constitute the “300 South Riverside Plaza Fee loan pair” and a “loan pair,” are pari passu in right of payment and will be serviced pursuant to the related intercreditor agreement and the pooling and servicing agreement for this transaction. With respect to the 300 South Riverside Plaza Fee mortgage loan, any holder of the 300 South Riverside Plaza Fee serviced companion loan will have certain consultation rights under the pooling and servicing agreement with respect to certain major decisions and other matters related to the 300 South Riverside Plaza Fee loan pair. | ||

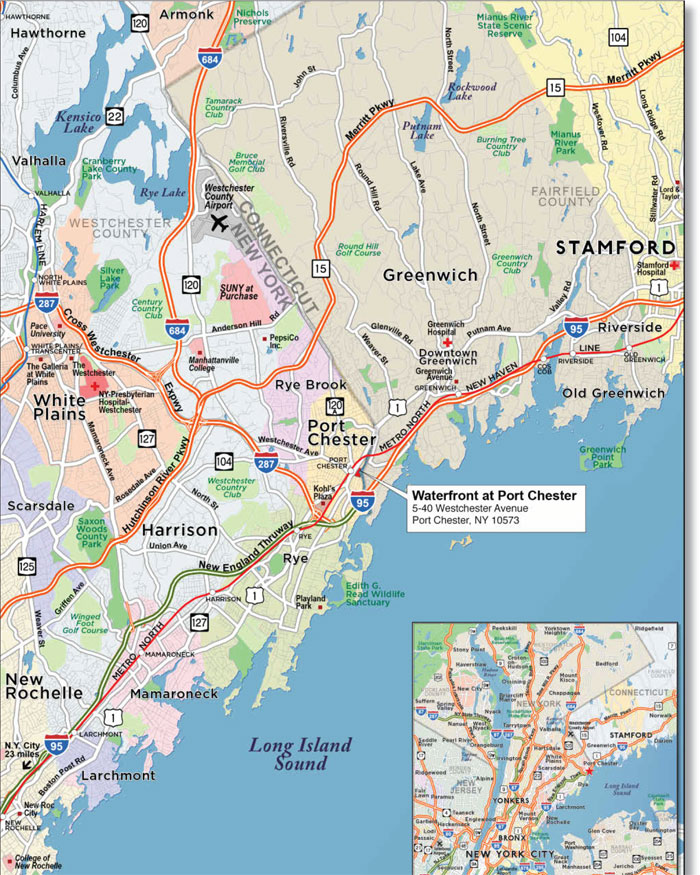

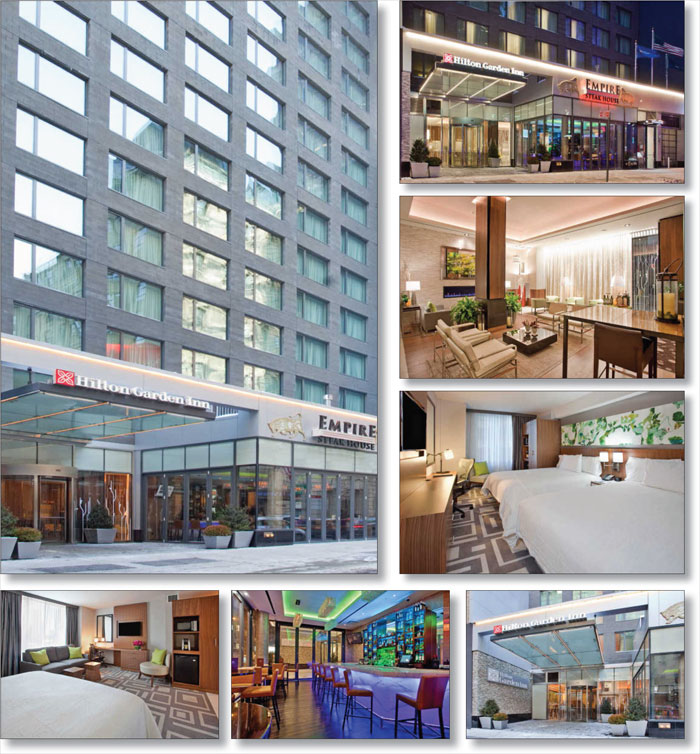

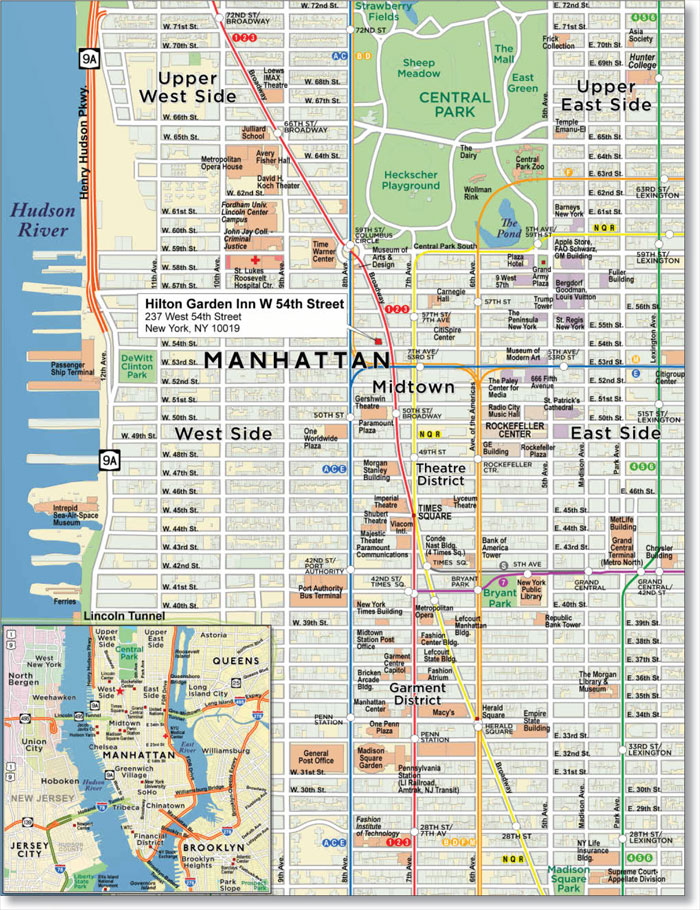

The mortgaged property identified on Appendix I to the Free Writing Prospectus as Waterfront at Port Chester secures on a pari passu basis (i) a mortgage loan (the “Waterfront at Port Chester mortgage loan”) with an outstanding principal balance as of the cut-off date of $80,000,000, representing approximately 7.2% of the initial pool balance, and (ii) a pari passu promissory note that has an outstanding principal balance as of the cut-off date of $53,500,000 (the “Waterfront at Port Chester serviced companion loan” and a “serviced companion loan”) that is not part of the mortgage pool and that is currently held by Morgan Stanley Bank, N.A. The Waterfront at Port Chester mortgage loan and the Waterfront at Port Chester serviced companion loan together constitute the “Waterfront at Port Chester loan pair” and a “loan pair,” are pari passu in right of payment and will be serviced pursuant to the related intercreditor agreement and the pooling and servicing agreement for this transaction. With respect to the Waterfront at Port Chester mortgage loan, any holder of the Waterfront at Port Chester serviced companion loan will have certain consultation rights under the pooling and servicing agreement with respect to certain major decisions and other matters related to the Waterfront at Port Chester loan pair. The mortgaged property identified on Appendix I to the Free Writing Prospectus as Hilton Garden Inn W 54th Street secures (i) on a generally senior pari passu basis (a) a mortgage loan (the “Hilton Garden Inn W 54th Street mortgage loan”) with an outstanding principal balance as of the cut-off date of $75,000,000, representing approximately 6.8% of the initial pool balance, and (b) two pari passu promissory notes (collectively, the “Hilton Garden Inn W 54th Street serviced companion loan” and a “serviced companion loan”) with an aggregate outstanding principal balance as of the cut-off date of $80,000,000, which promissory notes are pari passu in right of payment with the Hilton Garden Inn W 54th Street mortgage loan, are not included in the issuing entity and are currently held by Morgan Stanley Bank, N.A., (ii) on a generally subordinate basis relative to the Hilton Garden Inn W 54th Street mortgage loan and the Hilton Garden Inn W 54th Street serviced companion loan, a subordinate promissory note (the “Hilton Garden Inn W 54th Street B note” and a “B note”) with an outstanding principal balance as of the cut-off date of $20,000,000, which promissory note is not included in the issuing entity and is currently held by Morgan Stanley Bank, N.A. The Hilton Garden Inn W 54th Street mortgage loan, the Hilton Garden Inn W 54th Street serviced companion loan and the Hilton Garden Inn W 54th Street B note are collectively referred to herein as the “Hilton Garden Inn W 54th Street loan pair” and a “loan pair.” The Hilton Garden Inn W 54th Street loan pair will be serviced pursuant to the related intercreditor agreement and the pooling and servicing agreement for this transaction. There are no other “loan pairs,” and there are no “A/B whole loans,” related to the issuing entity. See “Description of the Mortgage Pool—The A/B Whole Loans and the Loan Pairs” in the Free Writing Prospectus. With respect to any mortgage loan that is part of a loan pair, unless otherwise indicated, all LTV, DSCR and Debt Yield calculations herein include the related pari passu serviced companion loan (and in the case of the Hilton Garden Inn W 54th Street mortgage loan, such calculations exclude the Hilton Garden Inn W 54th Street B note). | ||

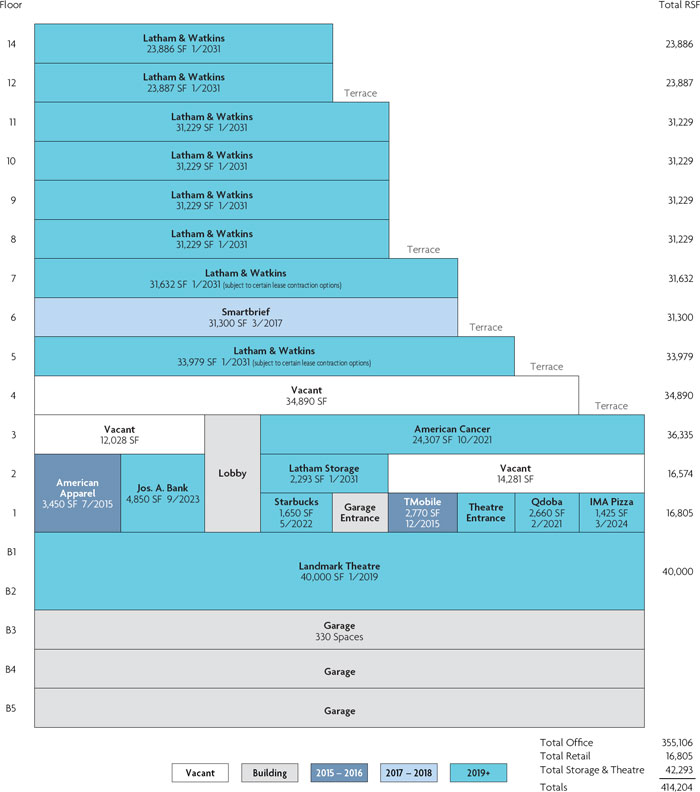

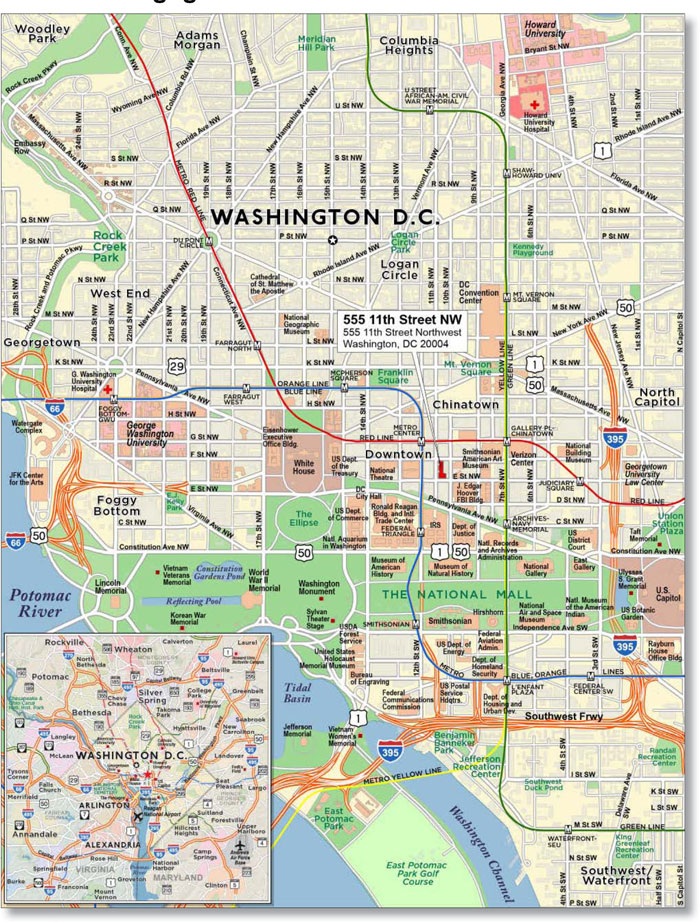

| Non-Serviced Loan Combinations: | The mortgaged property identified on Appendix I to the Free Writing Prospectus as 555 11th Street NW secures (1) on a generally senior pari passu basis (a) a mortgage loan (the “555 11th Street NW mortgage loan”) with an outstanding principal balance as of the cut-off date of $30,000,000, representing approximately 2.7% of the initial pool balance, and (b) one pari passu promissory note that has an outstanding principal balance as of the cut-off date of $60,000,000 (the “555 11th Street NW non-serviced companion loan” and a “non-serviced companion loan”), which promissory note is pari passu in right of payment with the 555 11th Street NW mortgage loan, is not included in the issuing entity and is currently held by the MSBAM 2015-C21 securitization trust, and (2) on a generally subordinate basis relative to the 555 11th Street NW mortgage loan and the 555 11th Street NW non-serviced companion loan, (a) a subordinated promissory note with an outstanding principal balance as of the cut-off date of $30,000,000 (the “555 11th Street NW MSBAM 2015-C21 trust B note” and a “B note”), which 555 11th Street NW MSBAM 2015-C21 trust B note is, in general, subordinate in right of payment to the 555 11th Street NW mortgage loan and the 555 11th Street NW non-serviced companion loan and, in general, senior in right of payment to the 555 11th Street NW non-securitized B note, is not included in the issuing entity and is currently held by the MSBAM 2015-C21 securitization trust, and (b) two subordinated promissory notes with an aggregate outstanding principal balance as of the cut-off date of $57,000,000 (collectively, the “555 11th Street NW non-securitized B note” and a “B note” and, together with the 555 11th Street MSBAM 2015-C21 trust B note, the “555 11th Street NW B note”), which 555 11th Street NW non-securitized B note is, in general, subordinate in right of payment to the 555 11th Street NW mortgage loan, the 555 11th Street NW non-serviced companion loan and the 555 11th Street NW MSBAM 2015-C21 trust B note, is not included in the issuing entity or mortgage pool and is currently held by Principal Life Insurance Company. The 555 11th Street NW mortgage loan, the 555 11th Street NW non-serviced companion loan and the 555 11th Street NW B note are collectively referred to herein as the “555 11th Street NW non-serviced loan combination” and a “non-serviced loan combination.” The 555 11th Street NW non-serviced loan combination will be serviced pursuant to the related intercreditor agreement and the MSBAM 2015-C21 pooling and servicing agreement. |

This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

T-8

MSBAM 2015-C22 | Structural Overview |

No mortgage loans, other than the 555 11th Street NW mortgage loan, have a non-serviced companion loan associated with them, and all of the mortgage loans, other than the 555 11th Street NW mortgage loan, are being serviced under the pooling and servicing agreement for this transaction. Accordingly, other than with respect to the 555 11th Street NW non-serviced loan combination, there are no other “non-serviced loan combinations” with respect to the issuing entity. See “Description of the Mortgage Pool—The A/B Whole Loans and the Loan Pairs” and “—The Non-Serviced Loan Combinations” in the Free Writing Prospectus. With respect to any mortgage loan that is part of a non-serviced loan combination, unless otherwise indicated, all LTV, DSCR and Debt Yield calculations herein include the related pari passu non-serviced companion loan (and, in the case of the 555 11th Street NW mortgage loan, such calculations exclude the 555 11th Street NW B note). | ||

| Appraisal Reductions: | The occurrence of certain adverse events affecting a mortgage loan (other than a non-serviced mortgage loan) (“Appraisal Events”) will require the special servicer to obtain a new appraisal or other valuation of the related mortgaged property. In general, if the principal amount of a mortgage loan plus all other amounts due under the mortgage loan and interest on advances made with respect to the mortgage loan exceeds 90% of the value of the mortgaged property determined by an appraisal or other valuation, an appraisal reduction may be created in the amount of the excess as described in the Free Writing Prospectus. Any appraisal reduction in respect of any non-serviced mortgage loan generally will be calculated in accordance with the related non-serviced mortgage loan pooling and servicing agreement, which calculations are expected to be generally similar to those provided for in the pooling and servicing agreement for this transaction. Notwithstanding the foregoing, if an appraisal is required to be obtained in accordance with the applicable pooling and servicing agreement (including with respect to any non-serviced mortgage loan) but is not obtained within 120 days following the applicable Appraisal Event, then, until such appraisal is obtained and solely for purposes of determining the amounts of P&I advances, the appraisal reduction will equal 25% of the stated principal balance of the related mortgage loan; provided that, upon receipt of an appraisal, the appraisal reduction for such mortgage loan will be recalculated generally in accordance with the preceding paragraphs. If any mortgage loan is part of an A/B whole loan, a loan pair or a non-serviced loan combination, any appraisal reduction will be calculated in respect of such A/B whole loan, loan pair or non-serviced loan combination taken as a whole. With respect to an A/B whole loan, any such appraisal reduction will be allocated first to the related B note and then to the related A note. With respect to a loan pair or non-serviced loan combination, any such appraisal reduction will be allocated between the mortgage loan and the related serviced companion loan or non-serviced companion loan, respectively, on a pro rata basis by unpaid principal balance (provided that, in the case of (i) the Hilton Garden Inn W 54th Street loan pair, such allocation will occur after the allocation of appraisal reductions to the Hilton Garden Inn W 54th Street B note, and (ii) the 555 11th Street NW non-serviced loan combination, such allocation will occur after the allocation of appraisal reductions to the 555 11th Street NW B note). If an appraisal reduction exists for, or is allocable to, any mortgage loan, the interest portion of the amount required to be advanced on that mortgage loan will be reduced in the same proportion that the appraisal reduction bears to the stated principal balance of that mortgage loan. This will reduce the funds available to pay interest on the certificates or trust components, as applicable, then outstanding. For a discussion of how appraisal reductions are calculated and allocated, see “Description of the Offered Certificates—Appraisal Reductions” in the Free Writing Prospectus. | |

| Control Rights: | During any Subordinate Control Period, the controlling class representative will have certain consent and consultation rights under the pooling and servicing agreement with respect to certain major decisions and other matters. A “Subordinate Control Period” means any period when the aggregate principal balance of the Class E Certificates (taking into account the application of any appraisal reductions to notionally reduce the aggregate principal balance of such class) is at least 25% of the initial aggregate principal balance of that class. During any Collective Consultation Period, the controlling class representative will not have any consent rights, but the controlling class representative and the trust advisor will each have certain non-binding consultation rights under the pooling and servicing agreement with respect to certain major decisions and other matters. A “Collective Consultation Period” means any period when both (i) the aggregate principal balance of the Class E Certificates (taking into account the application of any appraisal reductions to notionally reduce the aggregate principal balance of such class), is less than 25% of the initial aggregate principal balance of the Class E Certificates and (ii) the aggregate principal balance of that class (without regard to any appraisal reductions allocable to such class), is at least 25% of the initial aggregate principal balance of that class. During any Senior Consultation Period, the controlling class representative will not have any consent or consultation rights, except with respect to any rights expressly set forth in the pooling and servicing agreement, and the trust advisor will retain certain non-binding consultation rights under the pooling and servicing agreement with respect to certain major decisions and other matters. A “Senior Consultation Period” means a period when the aggregate principal balance of the Class E Certificates (without regard to any appraisal reductions allocable to such class) is less than 25% of the initial aggregate principal balance of that class. Notwithstanding any of the foregoing to the contrary, if any mortgage loan is part of an A/B whole loan, loan pair or non-serviced loan combination, the controlling class representative’s consent and/or consultation rights with respect thereto may be limited as described in the Free Writing Prospectus. See “Servicing of the Mortgage Loans—The Controlling Class Representative” in the Free Writing Prospectus. |

This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

T-9

MSBAM 2015-C22 | Structural Overview |

| A/B Whole Loan, Loan Pair and Non-Serviced Loan Combination Control Rights: | The existence of a Subordinate Control Period, Collective Consultation Period or Senior Consultation Period will not limit any control and/or consultation rights of the holder of any related B note or companion loan. In particular, (i) with respect to the Hilton Garden Inn W 54th Street loan pair, the holder of the related B note will have certain consent and consultation rights with respect to the Hilton Garden Inn W 54th Street loan pair, and will have the right to replace the special servicer with respect to such loan pair, so long as the principal balance of such B note has not been reduced or notionally reduced, as applicable, by the application of payments, losses and appraisal reductions, below 25% of its original principal balance (as reduced by principal payments), and (ii) with respect to the 555 11th Street NW non-serviced loan combination, the holder of the B note designated as the “control note” under the related intercreditor agreement (or, if such B note is an asset of the MSBAM 2015-C21 securitization trust, the designated class of certificates under the related pooling and servicing agreement) will have certain consent and consultation rights with respect to the 555 11th Street NW non-serviced loan combination, and will have the right to replace the special servicer with respect to such non-serviced loan combination, so long as the principal balance of such B note has not been reduced or notionally reduced, as applicable, by the application of payments, losses and appraisal reductions, below 25% of its original principal balance (as reduced by principal payments). See “Risk Factors—Risks Related to the Offered Certificates—Realization on a Mortgage Loan That Is Part of an A/B Whole Loan or Loan Pair May Be Adversely Affected by the Rights of the Related Directing Holder” and “Description of the Mortgage Pool—The A/B Whole Loans and the Loan Pairs” and “—The Non-Serviced Loan Combinations” in the Free Writing Prospectus. | |

| Control Eligible Certificates: | The “Control Eligible Certificates” will be the Class E, Class F, Class G and Class H Certificates. | |

| Controlling Class Representative/ Controlling Class: | The controlling class representative will be the representative appointed by more than 50% of the Controlling Class (by principal balance). The “Controlling Class” will be the most subordinate class of Control Eligible Certificates then outstanding that has an aggregate principal balance (taking into account the application of any appraisal reductions to notionally reduce the aggregate principal balance of such class) at least equal to 25% of the initial aggregate principal balance of such class; provided that if no class of Control Eligible Certificates has an aggregate principal balance (taking into account the application of any appraisal reductions to notionally reduce the aggregate principal balance of such class) at least equal to 25% of the initial aggregate principal balance of such class, then the Controlling Class will be the most senior class of Control Eligible Certificates. A summary of the consent and consultation rights of the controlling class representative, and the limitations thereon, is set forth above under “Control Rights.” The Controlling Class on the closing date will be the Class H Certificates. The initial controlling class representative is expected to be DoubleLine Capital LP or its affiliate. | |

| Appraised-Out Class: | Any class of Control Eligible Certificates, the aggregate principal balance of which (taking into account the application of any appraisal reductions to notionally reduce the aggregate principal balance of such class) has been reduced to less than 25% of its initial aggregate principal balance, is referred to as an “Appraised-Out Class.” | |

| Appraisal Remedy: | The holders of the majority (by principal balance) of an Appraised-Out Class will have the right, at their sole expense, to present to the special servicer a second appraisal for any mortgage loan (other than with respect to any non-serviced mortgage loan) for which an Appraisal Event has occurred prepared by an MAI appraiser on an “as-is” basis acceptable to the special servicer in accordance with the Servicing Standard. Upon receipt of such second appraisal, the special servicer will be required to determine, in accordance with the Servicing Standard, whether, based on its assessment of such second appraisal, any recalculation of the applicable appraisal reduction is warranted and, if so warranted, will recalculate such appraisal reduction based upon such second appraisal. If required by any such recalculation, any applicable Appraised-Out Class will have its related principal balance notionally restored to the extent required by such recalculation of the appraisal reduction, and there will be a redetermination of whether a Subordinate Control Period, a Collective Consultation Period or a Senior Consultation Period is then in effect. However, until an Appraised-Out Class is restored as the Controlling Class, the next most senior class of Control Eligible Certificates that is not an Appraised-Out Class (or, if all classes of Control Eligible Certificates are Appraised-Out Classes, the most senior class of Control Eligible Certificates), if any, will be the Controlling Class. The right of any Appraised-Out Class to present a second appraisal of any mortgage loan for which an Appraisal Event has occurred is limited to one appraisal with respect to each mortgaged property relating to the affected mortgage loan, subject to certain exceptions regarding a material change in circumstance. No certificateholders of an Appraised-Out Class will have appraisal remedies in respect of a non-serviced mortgage loan under the pooling and servicing agreement for this transaction. If, as a result of an appraisal reduction, the Hilton Garden Inn W 54th Street B note is no longer the “Control Note” under the related intercreditor agreement, the holder of such B note will have a similar right to present a second appraisal of the Hilton Garden Inn W 54th Street loan pair. Any resulting recalculation of an appraisal reduction with respect to the Hilton Garden Inn W 54th Street mortgaged property may result in such B note holder remaining the directing holder with respect to the Hilton Garden Inn W 54th Street loan pair. If, as a result of an appraisal reduction, a promissory note comprising a part of the 555 11th Street NW B note is no longer the “Control Note” under the related intercreditor agreement, the holder of such B note (or, if such B note is an asset of the MSBAM 2015-C21 securitization trust, the designated class of certificates under the related pooling and servicing agreement) will have a similar right to present a second appraisal of the 555 |

This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

T-10

MSBAM 2015-C22 | Structural Overview |

11th Street NW non-serviced loan combination. Any resulting recalculation of an appraisal reduction with respect to the 555 11th Street NW mortgaged property may result in such B note holder remaining the directing holder with respect to the 555 11th Street NW non-serviced loan combination. | ||

| Sale of Defaulted Loans: | Defaulted serviced mortgage loans will be sold in a process similar to the sale process for REO property, as described under “Servicing of the Mortgage Loans—Sale of Defaulted Mortgage Loans and REO Properties” in the Free Writing Prospectus. There will be no “fair market value purchase option,” and the controlling class representative will have no right of first refusal with respect to the sale of defaulted loans. Non-serviced mortgage loans that become defaulted loans may be sold pursuant to a similar process under the related pooling and servicing agreement governing the servicing thereof. In addition, with respect to each of the 300 South Riverside Plaza Fee mortgage loan, the Waterfront at Port Chester mortgage loan and the Hilton Garden Inn W 54th Street mortgage loan, if such mortgage loan becomes a defaulted mortgage loan and the special servicer determines to sell such mortgage loan, the special servicer will be required to sell such mortgage loan together with the related serviced companion loan as one whole loan, in each case in accordance with the provisions of the related intercreditor agreement and the pooling and servicing agreement. See “Description of the Mortgage Pool—The A/B Whole Loans and the Loan Pairs—The 300 South Riverside Plaza Fee Loan Pair,” “—The Waterfront at Port Chester Loan Pair” and “—The Hilton Garden Inn W 54th Street Loan Pair” in the Free Writing Prospectus. In addition, with respect to the 555 11th Street NW mortgage loan, if such mortgage loan becomes a defaulted mortgage loan and the special servicer under the MSBAM 2015-C21 pooling and servicing agreement determines to sell the related non-serviced companion loan, such special servicer will be required to sell such non-serviced companion loan and the 555 11th Street NW mortgage loan (and will be required to sell such mortgage loan together with the 555 11th Street NW MSBAM 2015-C21 trust B note) together as one whole loan, in accordance with the provisions of the related intercreditor agreement and the MSBAM 2015-C21 pooling and servicing agreement. See “Description of the Mortgage Pool—The Non-Serviced Loan Combinations—The 555 11th Street NW Non-Serviced Loan Combination” in the Free Writing Prospectus. | |

| Appointment and Termination of Special Servicer: | The controlling class representative will appoint the initial special servicer (but not with respect to any non-serviced mortgage loan). At any time during the Subordinate Control Period, the special servicer (other than with respect to any non-serviced mortgage loan) may be replaced by the controlling class representative. During any Collective Consultation Period and any Senior Consultation Period, the special servicer (other than with respect to any non-serviced mortgage loan) will be subject to termination without cause if certificateholders evidencing not less than 25% of voting rights request a vote of certificateholders to replace the special servicer. The certificate administrator would present the proposal to all certificateholders, and replacement would be conditioned on receipt, within one hundred eighty (180) days thereafter, of approval of the termination from holders of 75% of the voting rights of the certificates. The holders initiating such vote will be responsible for the fees and expenses of the issuing entity in connection with the replacement. During any Senior Consultation Period, if the trust advisor determines that the special servicer is not performing its duties in accordance with the Servicing Standard, the trust advisor will have the right to recommend the replacement of the special servicer with respect to the applicable mortgage loan or mortgage loans. The trust advisor’s recommendation to replace the special servicer must be confirmed by an affirmative vote of holders of a majority of the voting rights of the principal balance certificates. For purposes of the voting rights described above, the Class A-S, Class B, Class PST and Class C Certificates will be allocated voting rights in accordance with their respective percentage interests in the applicable Class A-S, Class B and Class C trust components as described in the Free Writing Prospectus. If any mortgage loan is part of an A/B whole loan, a loan pair or a non-serviced loan combination, to the extent set forth in the related intercreditor agreement, the related directing holder may have the right to replace the special servicer, with respect to the related A/B whole loan, loan pair or non-serviced loan combination to the extent set forth in the related intercreditor agreement. In particular, notwithstanding any of the foregoing to the contrary, so long as the principal balance of the Hilton Garden Inn W 54th Street B note (as reduced or notionally reduced, as applicable, by the application of payments, losses and appraisal reductions) is at least 25% of its original principal balance (as reduced by principal payments), such B note holder will have the sole right to replace the special servicer with respect to the Hilton Garden Inn W 54th Street loan pair. In addition, subject to the terms of any related intercreditor agreement (including the rights of any related directing holder thereunder), with respect to any non-serviced loan combination, the related special servicer under the related other pooling and servicing agreement pursuant to which such non-serviced loan combination is being serviced may be replaced on terms set forth in such other pooling and servicing agreement that are similar to those described above for the special servicer under the pooling and servicing agreement for this transaction; provided, that in the case of the 555 11th Street NW non-serviced loan combination, (a) the holder of the B note designated as the “control note” under the related intercreditor agreement (or, if such B note is an asset of the MSBAM 2015-C21 securitization trust, the designated class of certificates under the related pooling and servicing agreement) will have the sole right to replace the special servicer with respect to such non-serviced loan combination without cause, so long as the principal balance of such B note has not been reduced or notionally reduced, as applicable, by the application of payments, losses and appraisal reductions, below 25% of its original principal balance (as reduced by principal payments) and (b) if no such B note holder is the designated “control note,” the controlling class representative under the MSBAM 2015-C21 pooling and servicing agreement may not replace the special servicer without cause during any subordinate control period unless (i) the MSBAM 2015-C21 Class E Certificates is the controlling class of certificates under the MSBAM 2015-C21 pooling and servicing agreement, (ii) LNR Partners, LLC or its affiliate is not acting as the special servicer under the MSBAM 2015-C21 pooling and servicing agreement or (iii) LNR Securities Holdings, LLC or its |

This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

T-11

MSBAM 2015-C22 | Structural Overview |

affiliate owns less than 15% of the then controlling class of certificates under the MSBAM 2015-C21 pooling and servicing agreement. See “Description of the Mortgage Pool—The A/B Whole Loans and the Loan Pairs” and “—The Non-Serviced Loan Combinations” in the Free Writing Prospectus. | ||

| Servicing Standard: | Each of the master servicer and the special servicer is obligated to service and administer the mortgage loans (and, if applicable, the related B notes and serviced companion loans) in accordance with the definition of the “Servicing Standard” described in the Free Writing Prospectus and the terms of the pooling and servicing agreement, provided that each non-serviced mortgage loan, if any, will be serviced by another master servicer or special servicer under the pooling and servicing agreement with respect to the securitization of the related companion loan or applicable portion thereof. | |