As filed with the Securities and Exchange Commission on September 24, 2015

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Bioceres S.A.

(Exact name of Registrant as Specified in its Charter)

Not Applicable

(Translation of Registrant’s name into English)

| Republic of Argentina | 2870 | Not Applicable |

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

Bioceres S.A.

Ocampo 210 bis

Predio CCT, Rosario, Santa Fe, Argentina

Tel: +54 (341) 486-1100

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

National Corporate Research, Ltd.

10 E. 40th Street, 10th Floor

New York, NY 10016

Tel.: +1 (212) 947-7200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Conrado Tenaglia, Esq. Matthew S. Poulter, Esq. Linklaters LLP 1345 Avenue of the Americas New York, New York 10105 Phone: +1 (212) 903-9000 Fax: +1 (212) 903-9100 | Michael K. Coddington, Esq. Faegre Baker Daniels LLP 2200 Wells Fargo Center, 90 South Seventh St. Minneapolis, MN 55402 Phone: +1 (612) 766-7000 Fax: +1 (612) 766-1600 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Calculation of Registration Fee

| Title of each Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price(1)(2)(3) | Amount of Registration Fee | ||||

| Ordinary Shares, nominal value AR$2 per share(4)(5) | $ | 80,500,000.00 | $ | 9,354.10 | ||

| (1) | Estimated solely for purposes of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes the aggregate offering price of additional shares that may be purchased by the international underwriters. |

| (3) | Translated into dollars based on the exchange rate of AR$9.09 per $1.00 reported by the Central Bank of Argentina on June 30, 2015. |

| (4) | The ordinary shares may initially be represented by the registrant’s American Depositary Shares, or ADSs, each of which represents ordinary shares. A separate registration statement on Form F-6 will be filed for the registration of ADSs issuable upon deposit of the ordinary shares registered hereby. |

| (5) | Includes ordinary shares which the underwriters may purchase solely to cover over-allotments, if any, and ordinary shares which are to be offered outside the United States but which may be resold from time to time in the United States in transactions requiring registration under the Securities Act, including ordinary shares which the registrant may sell to current shareholders pursuant to preemptive rights and accretion rights. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the Securities and Exchange Commission declares our registration statement effective. This preliminary prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS

Subject to completion, dated September 24, 2015

| Bioceres S.A. (incorporated in Argentina) |

Ordinary Shares

represented by

American Depositary Shares

$ per American Depositary Share

This is the initial public offering of the ordinary shares of Bioceres S.A., or Bioceres. We are offering ordinary shares in a global offering. The ordinary shares will be offered in the form of American Depositary Shares, or ADSs, in the United States and other countries outside of Argentina through the international underwriters named in this prospectus. Each ADS represents ordinary shares. We refer to this offering of ordinary shares in the form of ADSs, as the “international offering.” We are concurrently offering ordinary shares in Argentina through the Argentine underwriter under a Spanish-language offering document, which we refer to as the “Argentine offering.” The total number of ordinary shares in the international and Argentine public offerings is subject to reallocation between these offerings. Prior to this offering, there has been no public market in the United States for our ordinary shares or ADSs. All of the ADSs and ordinary shares to be sold in the global offering are being sold by us.

All of our existing shareholders have a preferential right, including preemptive rights and accretion rights, to subscribe to our capital increase resulting from the global offering. Certain of our shareholders have assigned their preferential rights to the underwriters for the international offering and the Argentine offering, who can then exercise the underlying right to purchase the shares to be sold by Bioceres S.A. in the global offering. The remaining ordinary shares are available for subscription by our remaining shareholders in Argentina. The preferential subscription period will expire on or about , 2015. Subject to certain conditions, the ordinary shares that have not been subscribed in the global offering, if any and by minority shareholders pursuant to their preferential rights will be offered in Argentina by the Argentine underwriter after the preferential subscription period.

The estimated initial public offering price per ADS is between $ and $ .

We have applied to list our ADSs in the United States on the New York Stock Exchange, or NYSE, under the symbol “BIOX”. We have applied to list our ordinary shares in Argentina on the Mercado de Valores de Buenos Aires, or MERVAL.

We are an “emerging growth company” as defined in Section 2(a)(19) of the Securities Act of 1933, as amended, and, as such, are allowed to provide in this prospectus more limited disclosures than an issuer that would not so qualify. In addition, for as long as we remain an emerging growth company, we will qualify for certain limited exceptions from the Sarbanes-Oxley Act of 2002. Please see “Risk Factors—Risks Related to Our ADSs and the Offering—We are an “emerging growth company” and we cannot be certain whether the reduced requirements applicable to emerging growth companies will make our ADSs less attractive to investors” and “Summary—JOBS Act.”

Investing in our shares and the ADSs involves risks. See “Risk Factors” beginning on page 16 of this prospectus.

Per ADS | Total | |||||

| Public offering price | $ | $ | ||||

| Underwriting discounts and commissions(1) | $ | $ | ||||

| Proceeds, before expenses, to Bioceres S.A. | $ | $ | ||||

(1)See “Underwriting” beginning on page 154 for additional information regarding underwriting compensation.

The international underwriters expect to deliver the ADSs to purchasers on or about , 2015 through the book-entry facilities of The Depository Trust Company Americas.

We have granted the international underwriters the option for a period of days to purchase up to an additional ADSs, representing ordinary shares, at the initial public offering price less the underwriting discount to cover over-allotments, if any. Certain of our shareholders have assigned their preferential rights to the international underwriters, who can then exercise the underlying right to purchase the shares to be sold by Bioceres S.A. under this option. New shareholders will not have preemptive or accretion rights with respect to the ordinary shares offered pursuant to the over-allotment option.

Neither the Securities and Exchange Commission, nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Global coordinators and joint book-running managers

| Piper Jaffray | Itaú BBA |

Co-manager

Raymond James

The date of this prospectus is , 2015.

TABLE OF CONTENTS

This prospectus has been prepared by us solely for use in connection with the proposed offering of ordinary shares, including in the form of ADSs, in the United States and elsewhere outside Argentina. Piper Jaffray & Co. and Itau BBA USA Securities, Inc. will act as representatives of the international underwriters with respect to the offering of the ADSs. The offices of Piper Jaffray & Co. are located at 800 Nicollet Mall, 10th Floor, J10N01, Minneapolis, MN 55402. The offices of Itau BBA USA Securities, Inc. are located at 767 Fifth Avenue #50, New York, NY 10153. The offices of Raymond James & Associates, Inc. are located at 880 Carillon Parkway, St. Petersburg, FL 33716.

Neither we nor the international underwriters have authorized anyone to provide information different from that contained in this prospectus, any amendment or supplement to this prospectus or in any free writing prospectus prepared by us or on our behalf. When you make a decision about whether to invest in our ordinary shares in the form of ADSs, you should not rely upon any information other than the information in this prospectus and any free writing prospectus prepared by us or on our behalf. Neither the delivery of this prospectus nor the sale of our ordinary shares in the form of ADSs means that information contained in this prospectus is correct after the date of this prospectus. This prospectus is not an offer to sell or the solicitation of an offer to buy our ordinary shares or ADSs in any circumstances under which such offer or solicitation is unlawful. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or when any sale of ordinary shares in the form of ADSs occurs.

i

This prospectus includes statistical, market and industry data and forecasts which we have obtained from publicly available information and independent industry publications and reports that we believe to be reliable sources. These publicly available industry publications and reports generally state that they obtain their information from sources that they believe to be reliable, but they do not guarantee the accuracy or completeness of the information. Although we believe that these sources are reliable, we have not independently verified the information contained in such publications. Certain estimates and forecasts involve uncertainties and risks and are subject to change based on various factors, including those discussed under the headings “Special Note Regarding Forward-Looking Statements” and “Risk Factors” in this prospectus.

This offering is being made in the United States and elsewhere outside of Argentina solely on the basis of the information contained in this prospectus. The concurrent offering of our ordinary shares is being made in Argentina by a prospectus in Spanish that has been filed with the Argentine Securities Commission (Comisión Nacional de Valores), or CNV. The prospectus for the Argentine offering, although in a different format in accordance with CNV regulations, contains substantially the same information as contained in this prospectus. To satisfy CNV regulatory requirements, we have furnished the CNV with our financial statements as of and for the years ended December 31, 2013 and 2012, prepared in accordance with Argentine GAAP and presented in Argentine pesos, and which have not been included in this prospectus. The Argentine public offering of the ordinary shares was approved by the CNV on by Resolution No. .

Certain figures included in this prospectus have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not be an arithmetic aggregation of the figures that precede them.

ii

This summary highlights selected information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our ADSs. Before investing in our ADSs, you should read carefully this entire prospectus for a more complete understanding of our business and this offering, including the sections entitled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements included elsewhere in this prospectus.

Overview

We are a fully-integrated agricultural technology company with a strong leadership position in South America and access to global agricultural markets through our direct distribution channel and industry-leading partners. We believe we have a distinct multifaceted approach to the commercialization of our products, of which our proprietary distribution channel forms an important part. Our ability to deliver multiple, value-creating technologies, including seed biotechnology and agro-industrial biotechnology, to customers globally mitigates risks that channel partnerships may create. We work with global agricultural firms and researchers to create, develop, deregulate and commercialize technologies suited for our targeted high-growth markets in agricultural and industrial biotechnology. We anticipate that our first commercialized trait technology will be HB4, our yield-enhancement technology through abiotic stress-tolerance, which in April 2015 received biosafety regulatory approval in Argentina with respect to soybeans through a joint venture entity. Recently, the U.S. Food and Drug Administration, or U.S. FDA, completed its Early Food Safety Evaluation process for the plant protein responsible for the HB4 stress tolerance trait, or HB4 Protein. We believe we have created a platform for the delivery of numerous products in multiple large and high-growth end-markets.

Our agricultural technologies and products are focused on enhancing yields for several core global crops, including wheat, soybean, corn and alfalfa. Field trial data to date in wheat, soybean and corn have shown yield improvements attributable to our HB4 trait of greater than 10%, without adversely impacting yields in optimal growing conditions. For example, soybean plants with our HB4 trait, tested in independent field trials from 2012 to 2014 under normal growing conditions with sporadic drought episodes, had an average yield improvement of up to 14% compared to controls. We integrate our proprietary trait technologies into proprietary, proven germplasms to provide a complete and effective agronomic solution for our customers. In order to drive continual improvement through our subsidiaries and joint ventures, we have ongoing soybean and wheat breeding programs producing varieties that are now under registration. In addition, we have access to elite alfalfa genetics through our third party collaborators. In the future, we plan to develop or acquire corn germplasm assets in order to provide a comprehensive solution in all four of our core crops.

In addition to crop genetics, we further apply our technology sourcing and product development, or TS&PD, capabilities to develop and integrate agricultural biological inputs to create the agronomic solutions our customers are seeking. Our EcoSeedPack products, which will provide customized seed treatments that complement our traits and germplasms, are an example of our platform’s capabilities. We are leveraging our TS&PD capabilities to extend our reach into agro-industrial biotechnology opportunities, including the production of enzymes and fermentation solutions for the production of high-value compounds. We currently have 26 seed biotechnology and agro-industrial products in the proof of concept phase of development or later. Of these, 24 are being developed by us or through one of our joint ventures. The remaining products, including HB4 technology for sugarcane and non-proprietary corn, are being developed by third party collaborators. In respect of 12 of these products we have demonstrated efficacy in field trials, and five of these products are undergoing regulatory reviews or registration processes. Our chymosin enzyme produced through our SPC platform is currently being commercialized at pre-launch volumes.

We currently generate revenues primarily through the sale of seeds and the provision of research and development services through our subsidiaries to our joint ventures and other product development partnerships. As the technologies under development by our joint ventures or other partners receive regulatory approvals and are commercialized, we anticipate that our primary source of revenues will be derived from the sale of seeds that contain our biotech traits or are treated with our seed treatments, including royalty payments and license fees, and to a lesser extent, the commercialization of enzymes and other agro-industrial biotechnology solutions.

1

We believe we are strongly positioned to develop and implement technologies for the global agricultural markets given our leading market position in Argentina, where some of our technologies have been validated in the field and are currently being commercialized. The biosafety approval in April 2015 of the use of HB4 in soybeans in Argentina through one of our joint ventures is the world’s first regulatory approval of an abiotic stress tolerance trait in soybeans, which we believe is an important initial step in pursuing additional regulatory approvals in multiple geographies globally. With proven products in Argentina, one of the leading markets for agricultural technologies, we believe we can quickly expand into other Latin American markets, such as Brazil, Uruguay and Paraguay, as well as into additional key agricultural markets, including the United States.

Our direct access to our grower-shareholders is attractive to our commercial partners as they understand the value that access to growers provides. Our grower-shareholders include the founding members of AAPRESID, an Argentine farmers’ organization known for its international leadership in the adoption of new agricultural technologies in Argentina, which has historically experienced faster agricultural technology adoption rates than other countries. Some of our shareholders also include large agricultural cooperatives and agro-industrial processors, and the leading members of AACREA, an organization representing some of the largest farm operations in the region. A number of our shareholders are key influencers in the agricultural technology market. We believe our relationship with our grower-shareholders facilitates our ability to bring to market technologies that have been vetted, thereby driving successful adoption of our products.

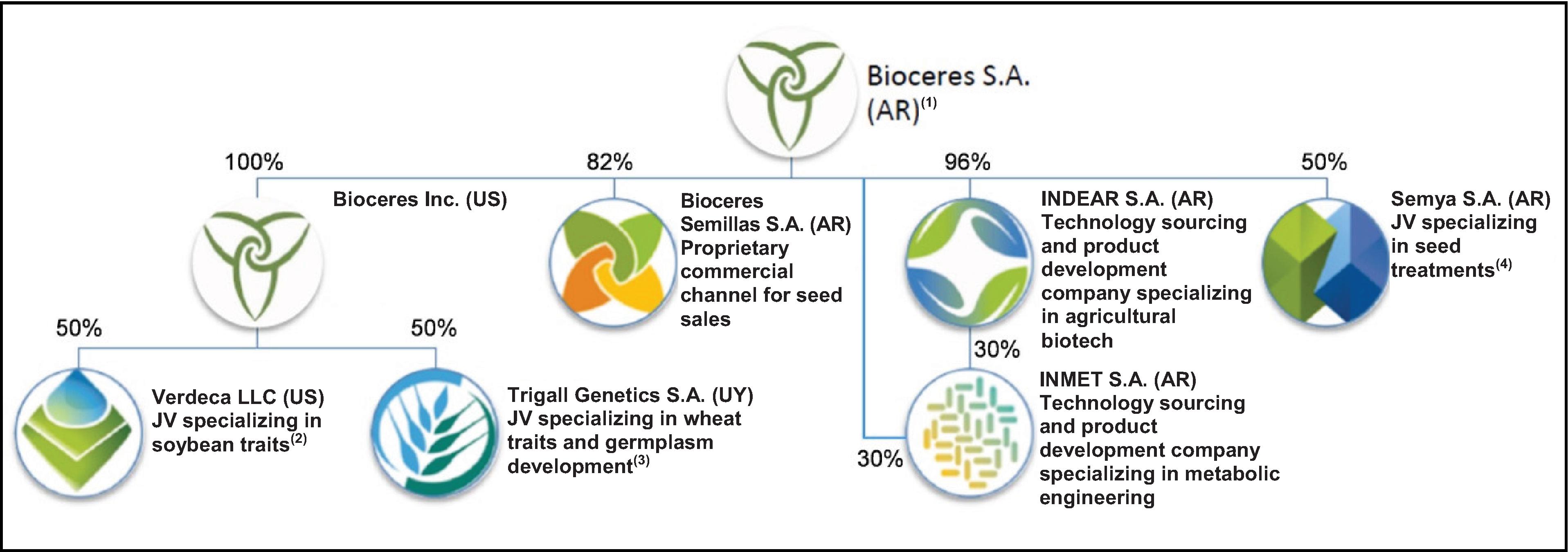

Our Operations and Pipeline

We operate in multiple business segments, including seed biotechnology and agro-industrial biotechnology, to provide value to customers around the world. Below is a chart showing our organizational structure:

Notes:

(1)AR means Argentina. US means the United States. UY means Uruguay.

(2)In Verdeca, our JV partner is Arcadia Biosciences Inc., or Arcadia Biosciences, a U.S. company that commercializes agriculture-based technologies.

(3)In Trigall Genetics, our JV partner is FD Admiral SAS, or Florimond Desprez, a French company specializing in wheat breeding, among other crops.

(4)In Semya, our JV partner is Rizobacter Argentina S.A., or Rizobacter, an Argentine company that focuses on research, development, production and commercialization of biological agents used in agriculture.

We use both GM and non-GM technologies to develop our traits, enabling us to select the approach best suited for a particular trait, crop or market. Our agricultural productivity traits are designed to increase crop yields, leading to increased growers’ income. Our existing portfolio of agricultural productivity traits concentrates on solutions to improve the tolerance of crops to drought and soil salinity, and increases in yield through improved nutrient use and/or water use efficiencies. Field trial results have demonstrated significant yield improvements resulting from our agricultural productivity traits in multiple crops and geographies. We have a secondary focus on traits that improve quality, such as delayed senescence technology in alfalfa, and we also work on herbicide tolerance traits for weed management.

2

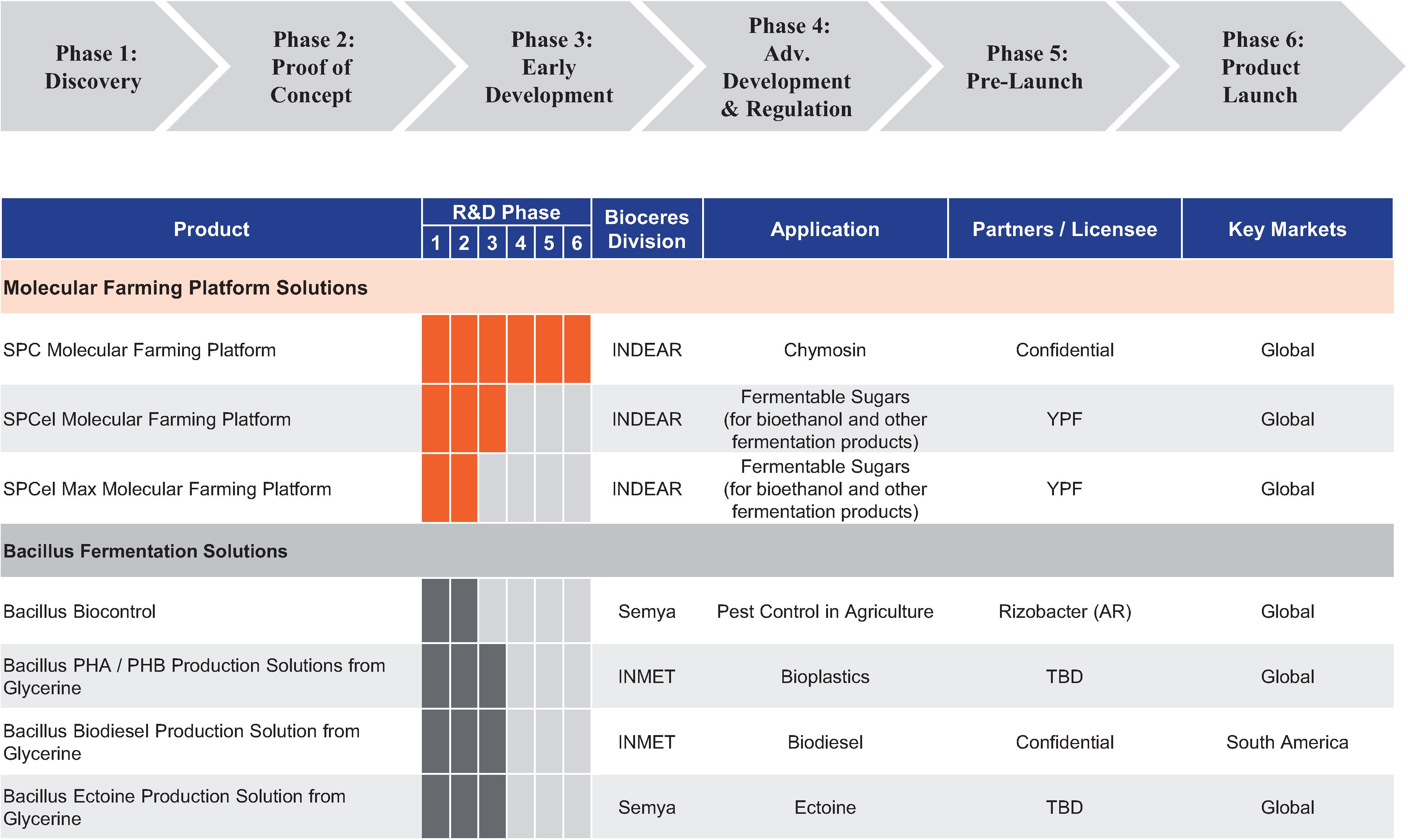

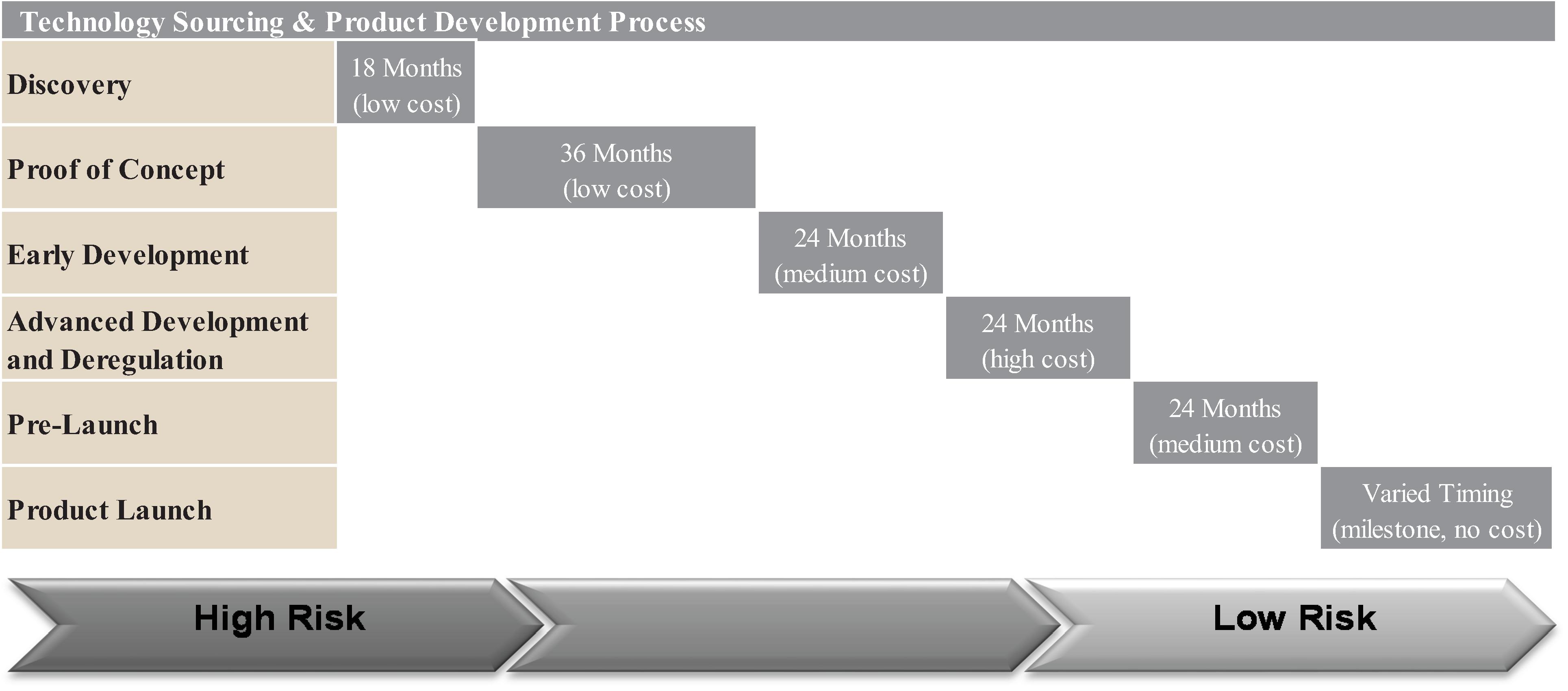

The following chart sets forth the various stages of the research and development process.

The following table summarizes our current products and our pipeline of products in development at the proof of concept stage or higher, including products under development by our joint ventures, and does not include products that are being developed by third party collaborators.

Notes:—

(1)Germplasms are categorized by maturity groups. MG III to MG VIII germplasms are short to long term maturity groups. Non-elite germplasms are williams and jack soybean varieties or B73 corn inbred. Spring and winter germplasms refer to short and long cycle wheat elite lines and varieties. Temperate germplasms are corn hybrids adapted to temperate climates. Non-dormant germplasms are alfalfa elite breeding materials without winter dormancy. A. cruentus germplasms are amaranth varieties of the A. cruentus species.

(2)GT/BT means glyphosate tolerance and insect tolerance. GT means glyphosate tolerance. GGT means glyphosate and glufosinate tolerance. GluT means glufosinate tolerance. GluT/BT means glufosinate tolerance and insect tolerance. Genuity is the glyphosate tolerance technology developed by Monsanto and Forage Genetics International, or FGI, for alfalfa. PPO means PPO-inhibitor herbicide tolerance. ALS means ALS-inhibitor herbicide tolerance.

(3)HarvXtra is the reduced lignin technology developed by Monsanto and FGI and de-regulated by us in Argentina. LXR is a delayed-senescence technology used in multiple crops, shown to improve quality and forage productivity in alfalfa.

(4)UY means Uruguay. PY means Paraguay. SA means South Africa. AR means Argentina. ROW means rest of world. US means the United States. AU means Australia.

3

The following table summarizes our current agro-industrial biotechnology pipeline of products in the proof of concept stage or higher.

Seed Biotechnology

Our seed biotechnology segment commercializes leading crop genetics across the wheat, soybean, corn and alfalfa seed markets. In order to quickly and cost-effectively deliver our products to market, we have created distinct companies or joint ventures:

| • | INDEAR: Launched in 2004, INDEAR represents our research and development services arm. Formed through a strategic alliance with CONICET, the Argentine National Research Council employing about 2,700 scientists in the life sciences. INDEAR constitutes the core of our TS&PD efforts, which we believe is the leading agricultural biotechnology platform in Latin America. INDEAR’s personnel are engaged in various collaborations within our technology focus areas. |

| • | Bioceres Semillas: Launched in 2009, Bioceres Semillas is our proprietary commercial sales channel for seeds. Bioceres Semillas develops and brings to market our latest crop innovations. |

| • | Verdeca: Launched in 2012, Verdeca is our U.S.-based joint venture with Arcadia Biosciences created to develop and deregulate soybean varieties with next-generation agricultural technologies. |

| • | Trigall Genetics: Launched in 2013, Trigall Genetics is our Uruguay-based joint venture with Florimond Desprez focused on developing and commercializing conventional as well as next-generation biotechnology wheat varieties for the South American market. |

| • | Semya: Launched in 2012, Semya is our Argentina-based joint venture with Rizobacter focused on the research and development for commercialization of seed treatments and agricultural biological input applications for the soybean, wheat, corn and alfalfa markets. |

Agro-Industrial Biotechnology

Our agro-industrial biotechnology segment focuses on the production of industrial enzymes and fermentation technologies to convert sugars and oils to high-value molecules or compounds. Our agro-industrial biotechnology business segment is undertaken through INDEAR and INMET, which was launched in 2013 to develop and commercialize fermentation solutions for environmentally-friendly production of high-value compounds by converting low-cost raw materials using genetically optimized bacteria.

4

We currently generate a majority of our agro-industrial biotechnology revenues through our production and sale of chymosin, an enzyme used to make cheese. We intend to scale-up production of chymosin and to accelerate development of commercial technologies that rely on bacterial fermentation for bio-conversions of soy glycerin to be used for the production of biofuels, bio-chemicals and bioplastics.

Our Competitive Strengths

Our diversified platform generates revenues through multiple technologies, customers and end-markets, providing us with a profitable growth trajectory. Our competitive strengths include:

Delivery of Multiple Value Enhancing Agricultural Technologies

Since our formation in 2001, we have pursued an approach based on identifying, developing and commercializing multiple technologies addressing growers’ demands for higher yields on the acre or conversion pathways to expand feedstock applications. Our proprietary solutions enable growers to meet their needs through technologies that provide additional value, drive customer demand and preserve the environment.

Strong Relationship with Shareholder Base Facilitates Early Technology Adoption and Influences Broader Market Adoption

Our major customers and influencers are our current investors. Our current investors include 252 growers, which include some of the largest farm operators, processors and early agricultural technology adopters in South America, a leading agricultural region in the world. Our grower-shareholders also include the founding members of AAPRESID and leading members of AACREA. These relationships enable us to quickly deliver our technologies to the operations of our grower-shareholders.

Capital-Efficient, Risk-Mitigated Focus on Later Stage Development and Partnership Model to Commercialize Technology

Our business model is focused on efficiently bringing to market technologies by minimizing the typically high cost and high risk associated with technology discovery and development. In order to avoid the higher risk and capital expense of biotechnology discovery, we leverage the discovery efforts of leading global research institutions and scientists with whom we have strong relationships, to identify and access promising early stage agricultural and agro-industrial biotechnologies. Upon technology validation, we partner with internationally recognized entities to further develop our technologies into products, as our joint venture Verdeca recently did with Dow AgroSciences LLC in respect of traits in soybeans. We commercialize these products through third party or proprietary channels.

Early Market Access Position with HB4 and Other Technologies

Our HB4 technology is in advanced stages of regulatory approval in Argentina, including having obtained biosafety approval in April 2015 in Argentina through a joint venture entity for the use of HB4 in soybeans, which we believe positions us to be the first company to provide the Argentine market with drought tolerant soybeans and wheat. We plan to leverage our initial entry into the Argentine market to expand into other key global agricultural markets with this technology. Our HB4 technology provides demonstrated yield enhancement in normal growing conditions with sporadic drought episodes by an average of 7% to 14% without adversely impacting yields in optimal growing conditions, which is not often seen with drought tolerance traits. We are incorporating HB4 technology into other core crops such as corn and alfalfa, as well as into various secondary crops through our third party collaborators. We are leveraging our germplasm assets, particularly in soybean and wheat, in the development of our integrated EcoSeedPack products, our customized seed treatments that complement our traits and germplasms.

Deep Executive Team with Unique Blend of Technical and Commercialization Experience

We believe our management team’s experience will enable us to be highly successful in implementing our technologies and delivering them to the field. Our leaders are able to integrate our team’s strong experience in technology sourcing and product development, regulatory, business development, commercialization, distribution and intellectual property to quickly deliver leading products into the market successfully.

5

Industry Overview

Agriculture

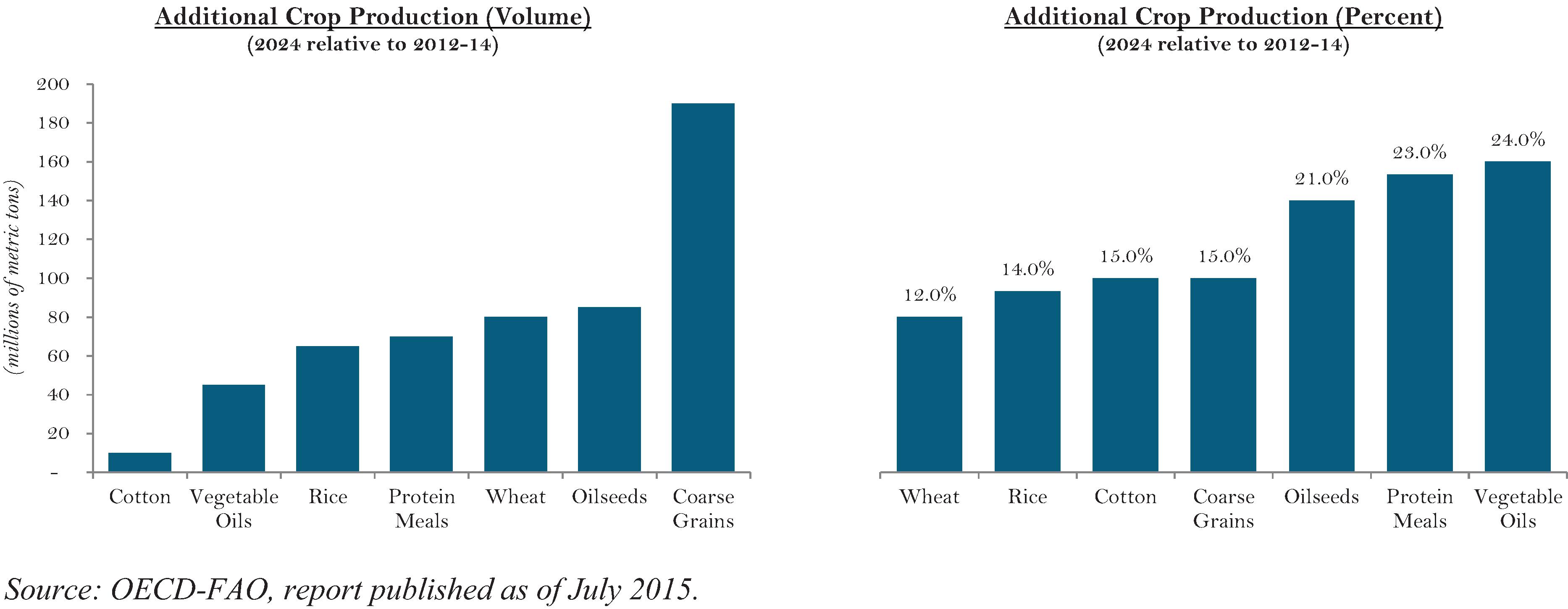

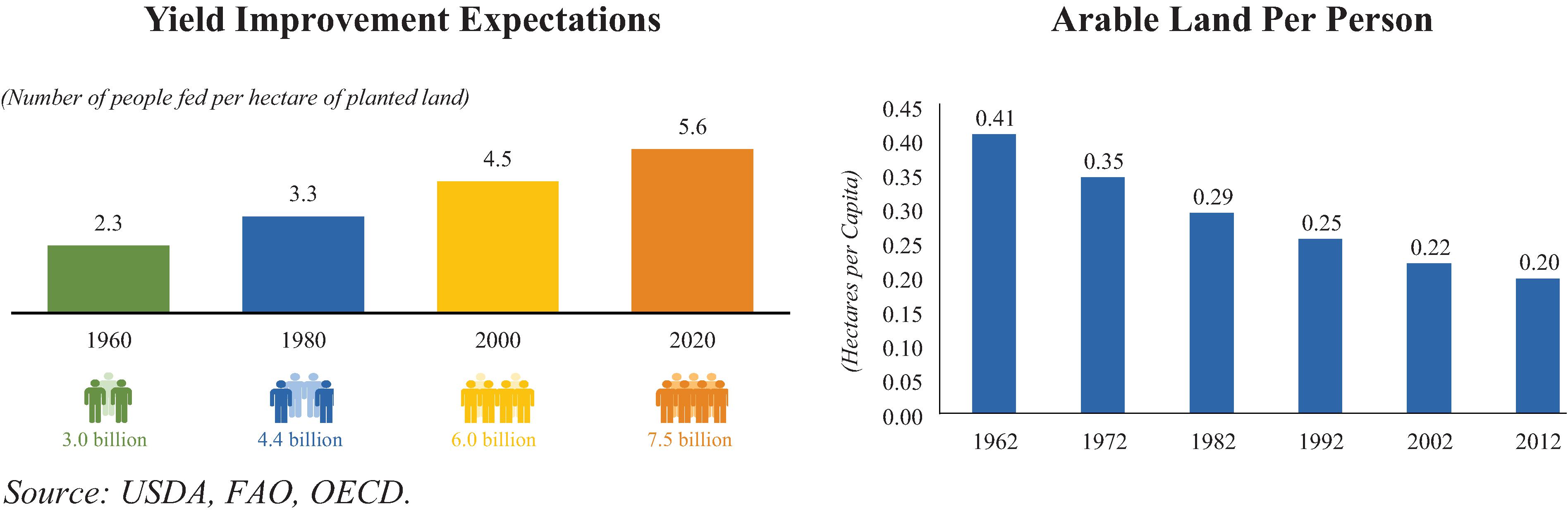

Across the world, growers are facing increasing demand for food, feed and fuel. According to the United States Department of Agriculture, or USDA, global demand for grain has increased over 50% from 1.4 billion metric tons in 1980 to 2.2 billion metric tons in 2010 and is expected to increase another 20% by 2020. This increasing demand is driven primarily by a rising global population and an expanding middle class in certain regions. As household income rises, the demand for protein-rich diets often increases, which drives underlying demand for grain. As global demand for agricultural outputs rises, a concurrent trend toward urbanization is causing a large reduction in the amount of arable land per capita available. The Food and Agriculture Organization of the United Nations, or FAO, data reveal that the ratio of arable land to population steadily declined by over 50% from 1962 to 2012.

Faced with increasing demand and limited supply in addition to climate variability and unfavorable natural events, growers are seeking to improve crop productivity through a number of technologies. Agricultural biotechnology has and will represent a significant source of innovation for increasing crop yields through improving performance of seeds while often reducing potentially environmentally harmful and costly inputs. The benefits of increased productivity have been well established, as growers who adopt GM crops earn 69% higher profits than non-adopting growers, according to a study published in 2014 in the Public Library of Science One on the impacts of GM crops.

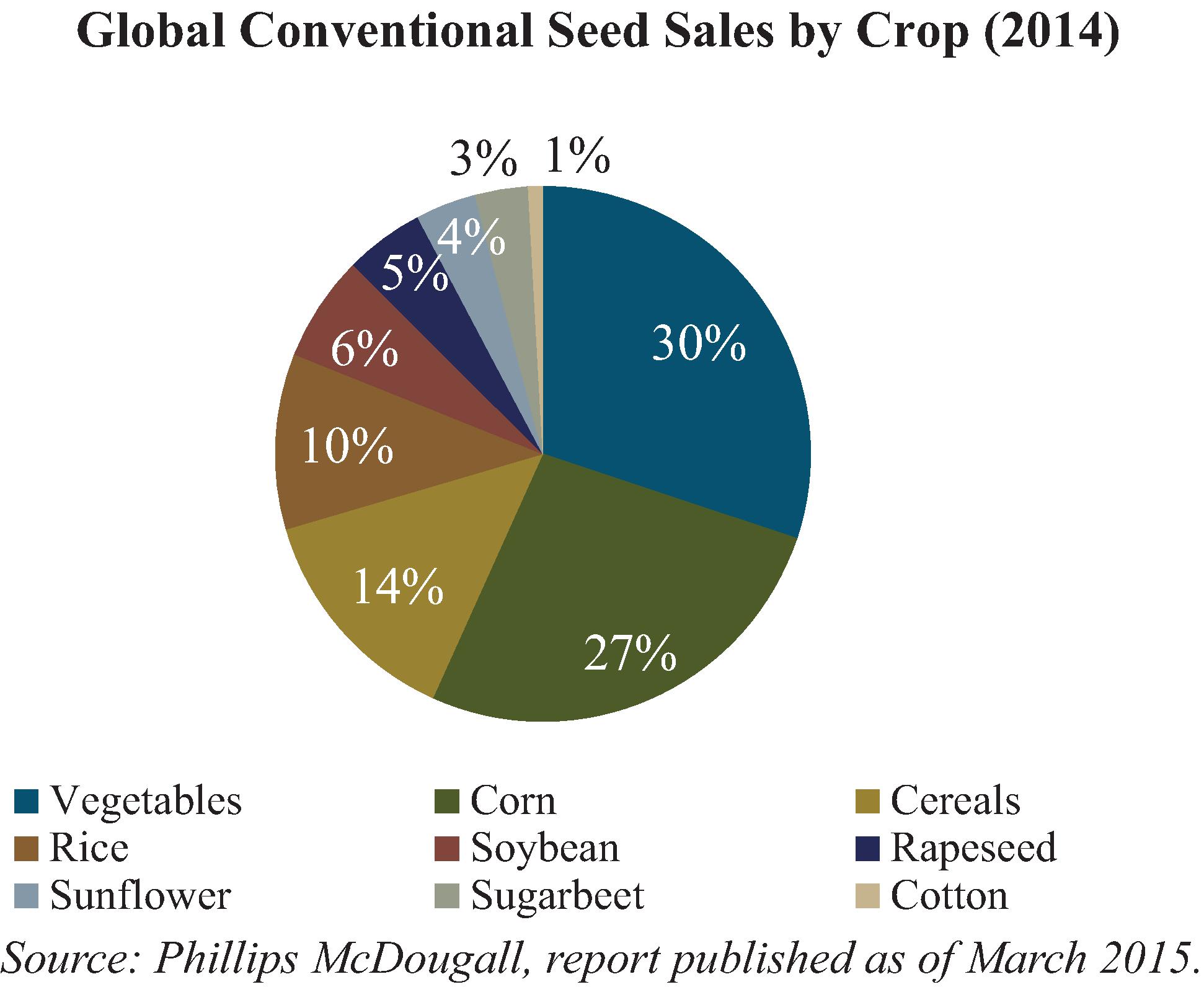

Innovative traits can provide significant additional value for farmers. Planting seed is a relatively low cost input for farmers, representing less than 10% of average total costs in 2013 according to the USDA. GM seeds can provide farmers with increased profitability at a relatively low increase in operating costs by means of increased yields, reduced costs of inputs such as chemicals and enhanced product quality. The historic success of increasing farm profits through the use of GM seeds has fueled the development of the agricultural biotechnology industry, and farmers have historically shared a portion of their economic benefit with the GM seed provider in the form of seed premiums. Because of this, large agricultural companies as well as smaller independent research firms have invested billions of dollars to identify and commercialize high-value seed traits to sell to growers. Given the ability of these products to differentiate through yield performance, these markets have demonstrated stronger growth in sales than conventional seed sales. Phillips McDougall estimates the market for GM seed to be growing at a compound annual growth rate, or CAGR, of 16.7% from $4.5 billion in representative sales in 2004 to $21.1 billion in representative sales in 2014.

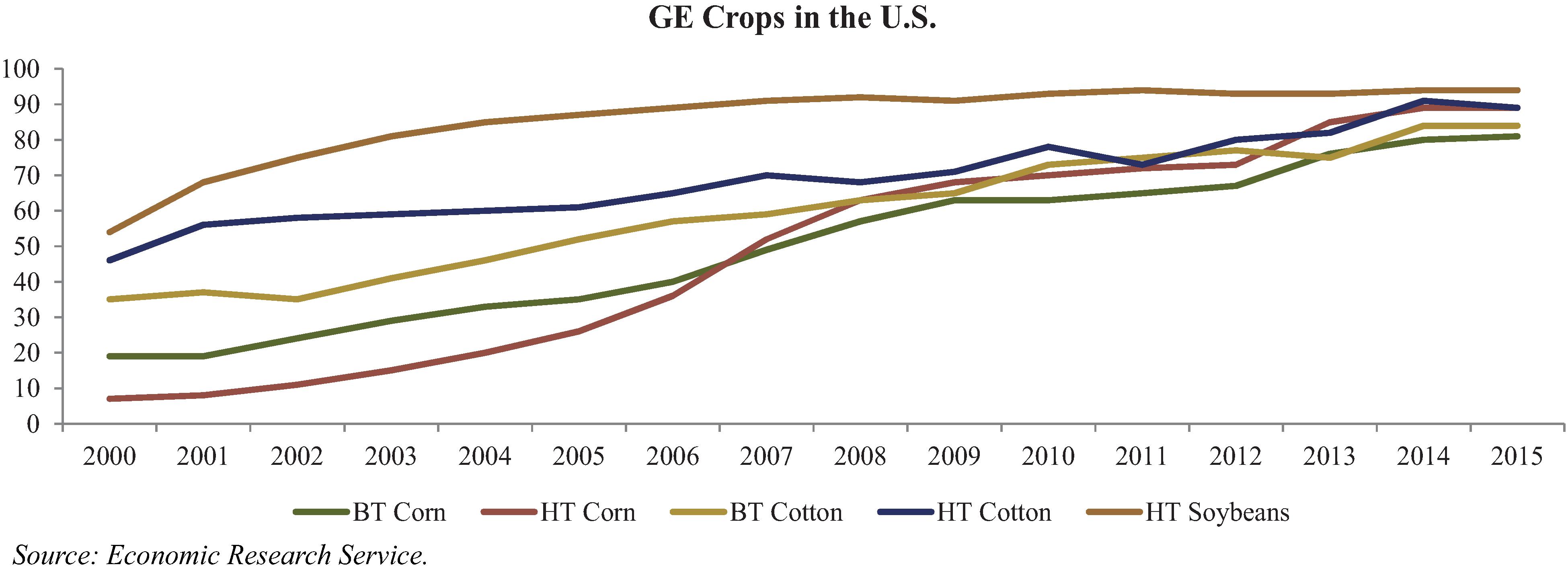

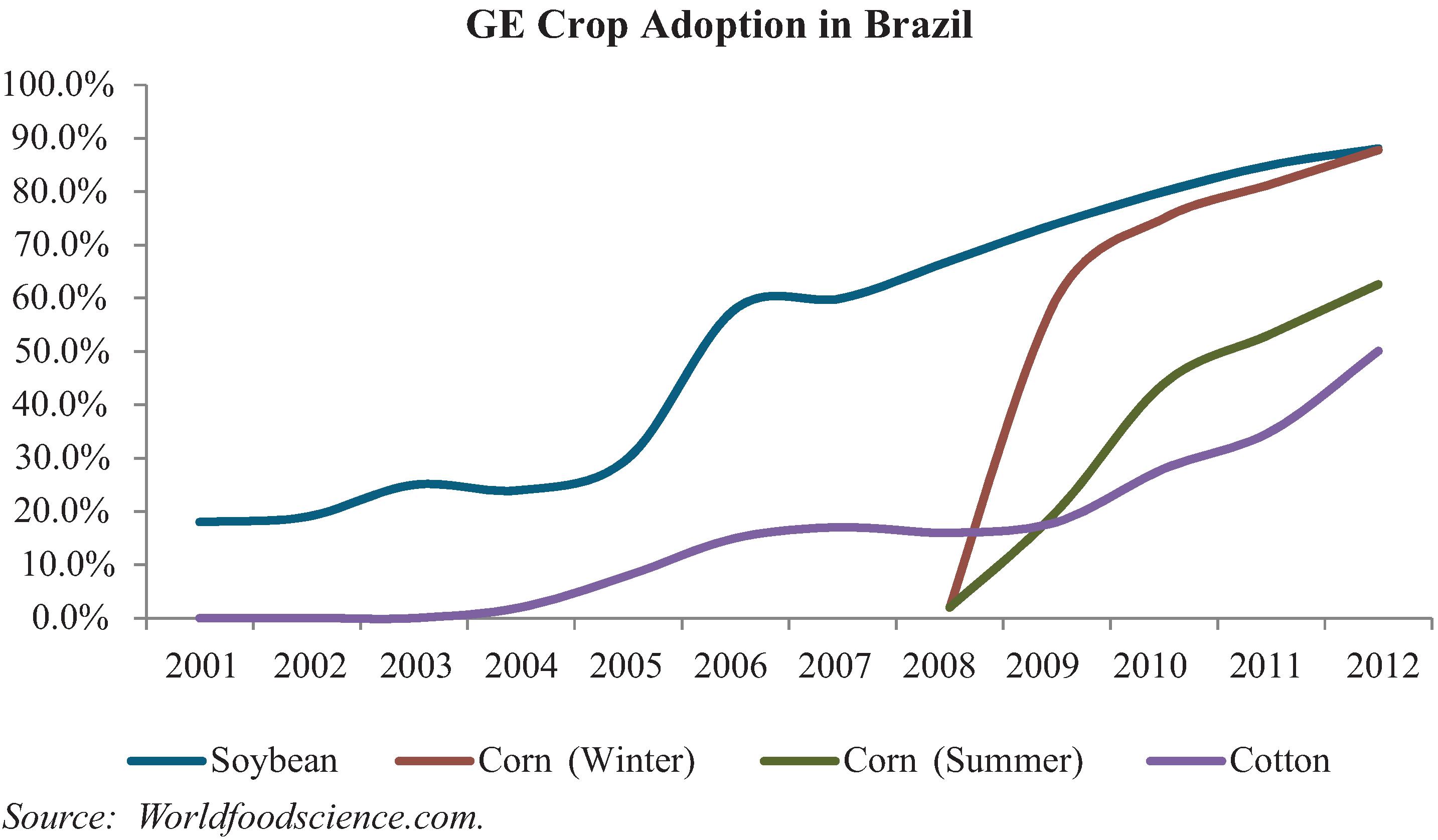

The International Service for the Acquisition of Agri-biotech Applications, or ISAAA, states that 175 million hectares were planted with GM crops in 2013. The United States, Brazil and Argentina were the top planters of biotech seeds with more than 130 million hectares under production of biotech crops in 2013, according to the ISAAA. The United States has an established history of rapid adoption rates of GM crops, typically reaching 65% to 90% peak penetration approximately ten years after introduction into the market. Argentina is the third highest producer of biotech crops, producing 14% of total global biotech crops in 2013. According to the USDA Foreign Agricultural Service, there were 24.8 million hectares of biotech crops planted in 2013 in Argentina with virtually 100% of soybean, 95% of corn and 100% of cotton hectares utilizing biotech varieties.

Biological-based Agricultural Chemicals Market

In 2013, the global agricultural chemicals market was valued at $204 billion and is expected to grow 3.6% annually from 2013 through 2018, according to Markets and Markets, an independent market research firm. The emerging biological-based sub-segment is growing at five times the rate of conventional pesticides and is expected to reach $4.4 billion by 2019. Higher growth in the biological sub-segment is driven by consistent improvements in product efficacy as well as pressure to reduce the environmental impacts of agriculture. The value of the global seed treatment market is estimated at $2.8 billion in 2014 and is projected to grow by a CAGR of 10.6% to reach $4.9 billion by 2019.

6

Our Growth Strategy

Our growth strategy is focused on identifying and accessing promising technology from third parties and forming strategic and capital-efficient partnerships that leverage our know-how and access to end-markets, through our proprietary channels and commercial partners. Our growth strategy includes the following:

Build upon Our Existing Relationships to Drive Product Sales and Adoption of Our Agricultural Technologies

Given the near-term commercialization opportunity that HB4 and many of our technologies represent, we plan to accelerate their global adoption and maximize our share of the value created on the farm. We believe we can accelerate growth through our existing direct channel access and drive faster adoption with our established partners in key markets.

Expand Our Direct Access to Grower Channels to Accelerate Adoption of New Technologies

We have the opportunity to continue to define our Bioceres brand as the technology leader in our existing geographic footprints as well as to establish and expand our reach into additional key agricultural geographies. We intend to expand upon our direct-to-grower channel leadership by offering additional in-demand technologies, including precision agriculture and direct-to-grower retail, which we believe will facilitate the adoption and subsequent sales of our products as well as achieve efficiencies to create additional value share opportunities.

Continue to Develop and Commercialize New Agricultural Biotechnology Products in Existing and New Markets

We intend to build upon our diverse portfolio of seed products by using an integrated agronomic approach leveraging our leading germplasm and trait position with the addition of EcoSeedPack, our customized, integrated seeds with treatments that we see increasingly in demand by our growers. Our track record of delivering proven technologies in Argentina allows us to credibly enter new geographies.

Further Develop Existing Agro-Industrial Biotechnology Products

Through our TS&PD activities, we intend to accelerate the cost-efficient development of commercial technologies that rely on metabolic engineering for bio-conversions of soy glycerin to produce biofuels, bio-chemicals and bioplastics as well as scale-up production of the chymosin industrial enzyme through our safflower molecular farming platform.

Pursue Strategic Collaborations and Acquisitions in Key Markets

We intend to continue collaborating with our joint venture partners and other collaborators to bring our products to customers in key markets. We may also pursue acquisition and in-licensing opportunities to gain access to later stage products and technologies that we believe would be good strategic fits for our business and would create additional value for our shareholders.

Risks Associated with Our Business

We are subject to a number of risks, including risks that may prevent us from achieving our business objectives or may materially and adversely affect our business, financial condition, results of operations, cash flows and prospects. You should carefully consider these risks, including the risks discussed in the section entitled “Risk Factors,” before investing in our ordinary shares or ADSs. Risks related to our business include, among others:

| • | if we are unsuccessful in developing biotechnologies or obtaining regulatory approvals necessary for their commercialization, in particular the HB4 technology that we co-own and license, we may face difficulties in achieving or maintaining our operations; |

| • | the agricultural biotechnology market is dominated by a relatively small number of large companies, and if we are unable to find suitable JV partners and/or collaborators, we may not succeed in developing and commercializing our existing and new technologies; |

7

| • | if, after considerable investments of time and resources, the traits and technologies that we develop do not generate revenues or royalties, then our business, financial condition and results of operations may be adversely affected; |

| • | we, our JV partners and/or our research collaborators may fail to perform our respective contractual obligations or we may have disputes with our JV partners and/or research collaborators, which may result in costly, time-consuming resolution processes; |

| • | we intend to invest significant resources, which may include a portion of the proceeds from this offering, to develop an innovative proprietary commercial channel for the distribution of our seed technologies. If we are unable to establish an effective sales and marketing platform, disrupt established market participants or maintain relationships with our existing distributors, the adoption of our products and the growth of product revenue may be slower than anticipated; |

| • | we may experience difficulties in collecting payments or royalties to which we believe we are entitled; |

| • | we depend on our key personnel and research collaborators, and we may be adversely affected if we are unable to attract and retain qualified scientific and business personnel through direct employment or technology sourcing collaborations; |

| • | our business and results of operations may be adversely affected by conditions beyond our control, such as global economic conditions, weather conditions and natural disasters; |

| • | our business is in continuous development and significant additional development may be necessary prior to achieving significant revenues or profitability; |

| • | sales of products containing traits we have engineered may be negatively impacted because of consumer and government resistance to GMOs; |

| • | if we are unable to continue to win government grants or if the Argentine government imposes sanctions and/or penalties in connection with funds from government grants, we may face difficulties in funding the development of new biotechnologies for integration into our products; |

| • | if we do not comply with various health and environmental risks associated with our use, handling and disposal of potentially toxic materials or if we sell products that are dangerous to consumers, we may be required to pay large fines or damages; |

| • | adverse economic conditions and political instability in Argentina may continue and may negatively affect our business; and |

| • | governmental intervention in the Argentine economy, particularly expropriation policies and the establishment of certain industry market conditions and prices, could adversely affect our results of operations or financial condition. |

JOBS Act

As a company with less than $1.0 billion in revenue during our last fiscal year, we qualify as an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. Section 107 of the JOBS Act provides that an emerging growth company may take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended, or the Securities Act, for complying with new or revised accounting standards. Thus, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. However, we are choosing to “opt out” of such extended transition period, and as a result, we will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for non-emerging growth companies. Section 107 of the JOBS Act provides that our decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

An emerging growth company may also take advantage of reduced reporting requirements that are otherwise applicable to public companies. If we choose to take advantage of any of these reduced reporting burdens, the information we provide to shareholders may be different from that which you may receive

8

from other public companies. Among these provisions is an exemption from the auditor attestation requirement under Section 404 of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act, in the assessment of our internal control over financial reporting. We have elected to rely on this exemption and will not provide such an attestation from our auditors.

We will remain an emerging growth company until the earliest of:

| • | the last day of our fiscal year during which we have total annual gross revenue of at least $1.0 billion; |

| • | the last day of our fiscal year following the fifth anniversary of the completion of this offering; |

| • | the date on which we have, during the previous three-year period, issued more than $1.0 billion in non-convertible debt; or |

| • | the date on which we are deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended, or the Exchange Act, which would occur if the market value of our shares that are held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter. |

Once we cease to be an emerging growth company, we will not be entitled to the exemptions provided in the JOBS Act.

Office Location

Our principal executive offices are located at Ocampo 210 bis, Predio CCT, Rosario, Santa Fe, Argentina, and our telephone number is +54 341 486-1100. We were incorporated as a sociedad anónima under the laws of Argentina on April 11, 2002 for a duration of 50 years. Our agent for service of process in the United States is National Corporate Research, Ltd., 10 E. 40th Street, 10th Floor, New York, NY 10016.

Recent Developments

On August 26, 2015, Verdeca announced it had received notification that the U.S. FDA had completed the Early Food Safety Evaluation process for the HB4 Protein, the plant protein responsible for Verdeca’s HB4 stress tolerance trait. We believe the U.S. FDA’s recent completion of its Early Food Safety Evaluation review of our joint venture’s determination that the inadvertent presence of low levels of the HB4 Protein does not raise food safety concerns is an important milestone in the development of commercial soybean seed products based on the HB4 stress tolerance trait, as well as the development of HB4-based products in other crops. The Early Food Safety Evaluation process is a preliminary, voluntary review that is commonly used by companies in order to receive from the U.S. FDA a primary safety indication of a protein. Upon the completion of our soybean regulatory field trials in the U.S., which are in advanced stages, we anticipate that we will submit the HB4 soybean event to the U.S. FDA and USDA for regulatory review.

9

Issuer.........................

Bioceres S.A.

Ordinary shares offered in the global offering......................

ordinary shares (or ordinary shares if the international underwriters exercise their option to purchase additional ADSs, representing ordinary shares, in full) in the international offering and the Argentine offering. We refer to the offering in the United States and in other jurisdictions outside of Argentina as the “international offering” and to the offering in Argentina as the “Argentine offering.” We refer to the international offering together with the Argentine offering as the “global offering.”

Ordinary shares offered in the international offering............

ADSs, representing ordinary shares, are being offered through the international underwriters in the United States and in other countries outside Argentina (or ADSs if the international underwriters exercise their option to purchase additional ADSs, representing ordinary shares, in full).

Ordinary shares offered in the Argentine offering..............

Concurrently with the international offering, ordinary shares are being offered in a public offering in Argentina through a Spanish-language offering document with the same date as this prospectus. The Argentine offering document, which has been filed with the Argentine National Securities Commission (Comisión Nacional de Valores), or CNV, is in a format different from that of this prospectus, consistent with CNV regulations but contains substantially the same information as contained in this prospectus.

American Depositary Shares offered...

Each ADS represents ordinary shares and may be represented by American Depositary Receipts, or ADRs. The ADSs will be issued under an ADS deposit agreement among us, Deutsche Bank Trust Company Americas, or the ADS Depositary, and the registered holders and beneficial owners from time to time of ADSs issued thereunder.

Preferential rights................

All of our existing shareholders have a preferential right, including preemptive rights and accretion rights, to subscribe for the capital increase in connection with the global offering. Certain of our shareholders have assigned preferential rights to the underwriters for the international offering and the Argentine offering to purchase ordinary shares, which the underwriters for the international offering and the Argentine offering will sell in the global offering, including in the form of ADSs. The remaining ordinary shares are available for subscription by our remaining shareholders. The preferential subscription period will expire on or about , 2015. Subject to certain conditions, the ordinary shares that have not been subscribed in the global offering, if any and by minority shareholders pursuant to their preferential rights will be offered in Argentina by the Argentine underwriter after the preferential subscription

10

period. New shareholders will not have preemptive or accretion rights in respect of ordinary shares offered pursuant to the over-allotment option of the international underwriters.

Ordinary shares to be outstanding after the global offering..............

ordinary shares (or if the international underwriters exercise their option to purchase additional ADSs in full).

Offering price...................

We expect that the offering price for the international offering will be between $ and $ per ADS.

Over-allotment option.............

We have granted the international underwriters an option to purchase up to an additional ADSs, representing of our ordinary shares. Certain of our shareholders have assigned their preferential rights to the international underwriters, who can then exercise the underlying right to purchase the shares to be sold by Bioceres S.A. under this option.

Use of proceeds..................

We intend to use the net proceeds from this offering primarily for working capital required to accelerate growth, capital expenditures and other general corporate purposes. See “Use of Proceeds.”

Listing........................

We have applied to have the ADSs approved for listing on the NYSE under the symbol “BIOX”. We have also applied to list our ordinary shares on the MERVAL.

Voting Rights...................

All holders of ordinary shares are entitled to one vote per share. Subject to Argentine corporate law, our bylaws and the terms of the deposit agreement, holders of ADSs will have the right to instruct the ADS Depositary regarding the voting of the underlying shares represented by ADSs. Ordinary shares are subject to applicable provisions of Argentine corporate law. Non-Argentine companies that own ordinary shares directly are required to register in Argentina in order to exercise their voting rights. See “Description of Share Capital” and “Description of American Depositary Shares.”

Dividends......................

Under Argentine law, the declaration, payment and amount of dividends on the ordinary shares are subject to the approval of our shareholders and to certain requirements of Argentine law. Pursuant to the deposit agreement, holders of ADSs will be entitled to receive dividends, if any, declared with respect to the underlying ordinary shares represented by such ADSs to the same extent as the holders of the ordinary shares. Also, cash dividends will be paid in Argentine pesos, although we reserve the right to pay in other currency. The ADS Depositary will convert the dividends received by the ADS Depositary in Argentine pesos to U.S. dollars pursuant to the deposit agreement and pay such amount to the holders of ADSs net of any dividend distribution fees, currency conversion expenses, depositary fees and expenses, taxes or governmental charges, if any. See “Dividends,” “Description of Share Capital,” “Description of American Depositary Shares” and “Risk Factors.”

11

Dividend Policy.................

Since our inception, we have not declared or paid any cash or other form of dividends on our ordinary shares. We intend to retain any earnings for use in our business and do not intend to pay cash dividends on our ordinary shares for the foreseeable future.

Lock-up Agreement...............

We have agreed with the international underwriters, subject to certain exceptions, not to sell or dispose of any ordinary shares or securities convertible into or exchangeable or exercisable for any ordinary shares during the period commencing on the date of this prospectus until 180 days after the completion of this offering. Members of our board of directors, our executive officers and certain of our shareholders have agreed to similar lock up provisions, subject to certain exceptions. See “Underwriting.”

ADS Depositary.................

Deutsche Bank Trust Company Americas.

Risk Factors....................

See “Risk Factors” and other information in this prospectus before investing in our ordinary shares or ADSs.

The number of ordinary shares to be outstanding after the global offering is based on 12,822,150 ordinary shares to be outstanding prior to the completion of this offering. This assumes the 50-to-1 stock split, which will occur immediately prior to the completion of the offering. See notes 10 and 11 to our consolidated annual financial statements. The number of outstanding ordinary shares excludes:

| • | 464,520 ordinary shares issuable upon the exercise of stock options that have already been approved for issuance as of the date hereof under our stock option incentive plan and under its individual option agreements expected to be entered into with certain of our key employees and members of our board of directors, with an exercise price of $15.85 per ordinary share; and |

| • | 799,480 ordinary shares reserved for future issuance consisting of 167,480 ordinary shares issuable upon the exercise of future stock option awards under our stock option incentive plan and 632,000 ordinary shares issuable pursuant to future stock grants under our stock grant incentive plan, in each case authorized by our shareholders as of the date hereof. |

For further information on our equity incentive plans, see “Management—Equity Incentive Plans.”

Unless otherwise indicated, this prospectus:

| • | reflects a 50-to-1 share split of our ordinary shares effective immediately prior to the completion of the offering; |

| • | assumes the number of ADSs sold in the international offering is the same as the number on the cover page of this prospectus; |

| • | assumes an initial public offering price of $ per ADS, the midpoint of the price range set forth on the cover of this prospectus; |

| • | assumes ordinary shares are sold in the Argentine offering; |

| • | assumes ordinary shares are sold to our existing shareholders who exercise their preemptive and accretion rights under Argentine law; and |

| • | assumes no exercise of the international underwriters’ option to purchase additional ADSs representing up to an additional ordinary shares. |

12

The following tables set forth our summary consolidated financial data. You should read the following summary consolidated financial and other data in conjunction with “Selected Financial Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our annual consolidated financial statements and unaudited interim condensed consolidated financial statements and related notes included elsewhere in this prospectus. Historical results are not necessarily indicative of the results that may be expected in the future. Our consolidated financial statements have been prepared in accordance with International Financial Reporting Standards as issued by International Accounting Standards Board, or IFRS. Our unaudited interim condensed consolidated financial statements have been prepared in accordance with International Accounting Standard 34 Interim Financial Reporting, or IAS 34.

The summary consolidated statements of profit or loss and other comprehensive income data for the years ended December 31, 2014 and 2013 and the summary consolidated statements of financial position data as of December 31, 2014 and 2013 are derived from our audited consolidated financial statements appearing elsewhere in this prospectus. The selected consolidated statement of profit or loss and other comprehensive income data for the six months ended June 30, 2015 and 2014 and the selected consolidated statement of financial position data as of June 30, 2015 are derived from our unaudited interim condensed consolidated financial statements appearing elsewhere in this prospectus. The unaudited interim condensed consolidated financial statements have been prepared on the same basis as the audited consolidated financial statements and, in the opinion of our management, include all normal recurring adjustments necessary for a fair presentation of the information set forth therein. The interim results are not necessarily indicative of results for the year ending December 31, 2015 or for any other period.

Consolidated statements of profit or loss and other comprehensive income

For the six months ended June 30, | For the year ended December 31, | |||||||||||

2015 | 2014 | 2014 | 2013 | |||||||||

| unaudited | ||||||||||||

| ($) | ($) | |||||||||||

| Revenue | 3,381,721 | 2,530,034 | 10,469,943 | 7,387,288 | ||||||||

| Government grants | 502,418 | 335,634 | 1,343,806 | 1,062,393 | ||||||||

| Total revenues | 3,884,139 | 2,865,668 | 11,813,749 | 8,449,681 | ||||||||

| Cost of sales | (1,686,699 | ) | 1,439,937 | (6,110,740 | ) | (5,519,418 | ) | |||||

| Research and development expenses | (1,377,778 | ) | 1,010,818 | (1,645,657 | ) | (1,594,382 | ) | |||||

| Selling, general and administrative expenses | (2,058,401 | ) | 1,566,230 | (3,721,511 | ) | (3,084,079 | ) | |||||

| Share of profit (or loss) of joint ventures | (279,380 | ) | (228,877 | ) | (931,076 | ) | (443,784 | ) | ||||

| Operating loss | (1,518,119 | ) | (1,380,194 | ) | (595,235 | ) | (2,191,982 | ) | ||||

| Finance income | 229,056 | 1,127,378 | 785,109 | 735,100 | ||||||||

| Finance costs | (944,954 | ) | (591,958 | ) | (680,440 | ) | (895,135 | ) | ||||

| Loss before income tax | (2,234,017 | ) | (844,774 | ) | (490,566 | ) | (2,352,017 | ) | ||||

| Income tax charge | 197,528 | (621,859 | ) | (690,040 | ) | (663,776 | ) | |||||

| Total comprehensive loss | (2,036,489 | ) | (1,466,633 | ) | (1,180,606 | ) | (3,015,793 | ) | ||||

| Total comprehensive income/(loss) attributable to: | ||||||||||||

| Equity holders of the parent | (1,860,940 | ) | (1,653,175 | ) | (1,321,310 | ) | (2,837,027 | ) | ||||

| Non-controlling interests | (175,549 | ) | 186,542 | 140,704 | (178,766 | ) | ||||||

13

Consolidated statements of financial position

As of June 30, 2015 | As of December 31, | ||||||||

2014 | 2013 | ||||||||

| unaudited | |||||||||

| ($) | ($) | ||||||||

| Current assets: | |||||||||

| Cash and cash equivalents | 100,627 | 2,249,699 | 18,156 | ||||||

| Marketable securities | 976,000 | — | — | ||||||

| Trade receivables | 4,497,966 | 5,953,882 | 3,904,526 | ||||||

| Other receivables | 3,200,632 | 2,084,775 | 792,764 | ||||||

| Income and minimum presumed income taxes recoverable | 197,349 | 54,354 | 38,045 | ||||||

| Inventories | 2,389,849 | 971,438 | 967,220 | ||||||

| Total current assets | 11,362,423 | 11,314,148 | 5,720,711 | ||||||

| Non-current assets: | |||||||||

| Other receivables | 857,803 | 627,771 | 615,180 | ||||||

| Income and minimum presumed income taxes recoverable | 213,054 | 437,427 | 290,854 | ||||||

| Deferred tax assets | 1,561,360 | 1,267,224 | 1,614,184 | ||||||

| Investments in joint ventures | 181,043 | — | — | ||||||

| Property, plant and equipment | 4,364,608 | 4,583,510 | 4,889,635 | ||||||

| Intangible assets | 1,625,354 | 1,611,030 | 1,719,247 | ||||||

| Goodwill | 536,065 | 536,065 | 536,065 | ||||||

| Total non-current assets | 9,339,287 | 9,063,027 | 9,665,165 | ||||||

| Total assets | 20,701,710 | 20,377,175 | 15,385,876 | ||||||

| Current liabilities: | |||||||||

| Trade and other payables | 4,112,483 | 4,451,520 | 5,454,038 | ||||||

| Borrowings | 1,310,678 | 730,006 | 1,373,863 | ||||||

| Employee benefits and social security | 217,315 | 296,217 | 490,068 | ||||||

| Deferred revenue and advances from customers | 214,522 | 214,173 | 382,069 | ||||||

| Income and minimum presumed income taxes payable | 128,590 | 298,244 | 258,906 | ||||||

| Other tax payables | 42,339 | 120,894 | 60,398 | ||||||

| Government grants | 178,117 | 214,808 | 202,347 | ||||||

| Investments in joint ventures | 1,057,354 | 1,364,677 | 440,900 | ||||||

| Provisions | 237,844 | 251,181 | — | ||||||

| Total current liabilities | 7,499,242 | 7,941,720 | 8,662,589 | ||||||

| Non-current liabilities: | |||||||||

| Borrowings | 962,168 | 1,134,783 | 685,913 | ||||||

| Government grants | 680,431 | 832,054 | 923,692 | ||||||

| Deferred revenue and advances from customers | 79,375 | 32,500 | 35,000 | ||||||

| Puttable instruments | 1,740,768 | 1,668,133 | — | ||||||

| Total non-current liabilities | 3,462,742 | 3,667,470 | 1,644,605 | ||||||

| Total liabilities | 10,961,984 | 11,609,190 | 10,307,194 | ||||||

| Equity: | |||||||||

| Issued capital | 6,968,538 | 6,924,146 | 6,742,969 | ||||||

| Share premium | 13,834,098 | 10,870,260 | 6,339,539 | ||||||

| Retained earnings | (11,236,760 | ) | (9,375,820 | ) | (8,054,510 | ) | |||

| Equity attributable to equity holders of the parent | 9,565,876 | 8,418,586 | 5,027,998 | ||||||

| Non-controlling interests | 173,850 | 349,399 | 50,684 | ||||||

| Total equity | 9,739,726 | 8,767,985 | 5,078,682 | ||||||

| Total equity and liabilities | 20,701,710 | 20,377,175 | 15,385,876 | ||||||

14

Business segment data

For the six months ended June 30, | For the year ended December 31, | |||||||||||

2015 | 2014 | 2014 | 2013 | |||||||||

| unaudited | ||||||||||||

| ($) | ($) | |||||||||||

| Revenue by business segment(*) | ||||||||||||

| Seed biotechnology | 1,707,152 | 1,583,813 | 6,255,438 | 5,238,579 | ||||||||

| Agro-industrial biotechnology | 114,341 | — | 2,654 | 162,496 | ||||||||

| Research & development | 2,062,646 | 1,281,855 | 5,555,657 | 3,048,606 | ||||||||

| Total revenue(*) | 3,884,139 | 2,865,668 | 11,813,749 | 8,449,681 | ||||||||

(*)Includes government grants

As of June 30, 2015 | As of December 31, | |||||||||||

2014 | 2013 | |||||||||||

| Other financial data: | ||||||||||||

| Ratio of current assets to current liabilities | 1.52 | 1.42 | 0.66 | |||||||||

| Ratio of shareholders’ equity to total liabilities | 0.89 | 0.76 | 0.49 | |||||||||

| Ratio of non-current assets to total assets | 0.45 | 0.44 | 0.63 | |||||||||

| Ratio of revenue(*) to shareholders’ equity | — | 1.35 | 1.66 | |||||||||

(*)Includes government grants

15

Investing in our shares or ADSs involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with the other information contained in this prospectus, before making any investment decision. Any of the following risks and uncertainties could have a material adverse effect on our business, prospects, results of operations and financial condition. The market price of our shares or ADSs could decline due to any of these risks and uncertainties, and you could lose all or part of your investment.

Risks Related to Our Business and Our Industry

We may not be successful in developing marketable or commercial technologies.

Our success depends in part on our ability to identify and develop high-value seed biotech and agro-industrial technologies for use in commercial products. To accomplish this, we, through our technology sourcing collaborations, JV partnerships and collaborations with third parties, commit substantial efforts and other resources to technology sourcing and product development. It may take several years, if at all, before our products complete the development process and become available for production and commercialization.

There can be no assurance that our seed biotech and agro-industrial technologies will be viable for commercial use or that we will be able to generate revenues from those technologies, in a significant manner or at all. If seeds or other products that contain our traits or technology are unsuccessful in achieving their desired effect or otherwise fail to be commercialized, we will not receive revenues from our customers or royalty payments from the commercialization of the traits and technologies we develop, which could materially and adversely affect our business, financial condition, results of operations and growth strategy.

Seeds containing the traits or biological treatments that we develop may be unsuccessful or fail to achieve commercialization for any of the following reasons:

| • | our traits or biological treatments may not be successfully validated in the target crops; |

| • | our traits or biological treatments may not have the desired effect sought by our end-market on the relevant crop; |

| • | we or our joint ventures or collaborators may be unable to obtain the requisite regulatory approvals for the seeds containing our traits or for our biological treatments; |

| • | our competitors may launch competing or more effective seed traits, biological treatments or germplasms; |

| • | a market may not exist for seeds containing our traits or biological treatments or such products may not be commercially successful; |

| • | we may be unable to patent and/or obtain breeders’ rights or any other intellectual property rights on our traits and technologies in the necessary jurisdictions; and |

| • | even if we obtain patent and/or breeders’ rights or any other intellectual property rights on our traits, such rights may be later challenged by competitors or other parties. |

Industrial enzymes, bacterial fermentation solutions and other agro-industrial biotech solutions that we develop may be unsuccessful or fail to achieve commercialization for any of the following reasons:

| • | we may not be able to effectively express or purify enzymes of interest in safflower grains; |

| • | even if we are able to express and purify enzymes of interest effectively using our safflower molecular farming technologies, these enzymes may not be effective for the industrial processes for which they were intended; |

| • | we or our collaborators may be unable to obtain the requisite regulatory approvals for safflower crop production, enzymes or by-products required or resulting from our molecular farming technologies or from the use of genetically engineered bacteria in the production of biofuels, biopolymers or higher value molecules; |

16

| • | we may not be able to effectively convert glycerin or other fermentable forms of carbon into biofuels, biopolymers or higher value molecules, such as ectoine, using our bacterial fermentation solutions; |

| • | we may not be able to effectively purify biopolymers and higher value molecules produced using our bacterial fermentation solutions; |

| • | our competitors may launch competing or more effective enzymes or agro-industrial biotech solutions; |

| • | a market may not exist for our enzymes, safflower by-products, or agro-industrial biotech solutions or such enzymes and solutions may not be commercially successful; |

| • | we may be unable to seek and obtain adequate intellectual property protection for our molecular farming or agro-industrial biotech solutions in the necessary jurisdictions; and |

| • | even if we obtain patent or other intellectual property protection for our molecular farming or agro-industrial biotech solutions, such protection may later be challenged by competitors or other parties. |

Our business and the commercialization of our products is subject to various government regulations and we or our JV partners or our other collaborators may be unable to obtain, or face delays in obtaining, necessary regulatory approvals.

Our business is generally subject to two types of regulations: (1) regulations that apply to the manner in which we operate and (2) regulations that apply to products containing or based on our technology. We are responsible for applying for and maintaining the regulatory approvals necessary for our operations, particularly those covering our field trials, bio-safety evaluations and feed and food tests. Under the terms of our joint venture agreements, we and our JV partners are jointly responsible for obtaining and maintaining the regulatory approvals necessary for the commercialization of products that contain our seed traits and other technologies in the various relevant markets. As an operational matter, however, we generally lead these processes in Argentina through our subsidiary, Instituto de Agrobiotecnologia Rosario S.A., or INDEAR, and our JV partners generally lead these efforts in the United States and other international markets. In the future, we expect to seek regulatory approvals in other markets, including but not limited to India, China, the European Union, Brazil, Uruguay and Paraguay. Regulatory and legislative requirements affect the development, production and sale of our products, including the testing, commercializing and planting of seeds containing our biotechnology traits, and the failure to receive these approvals or non-compliance with the applicable regulatory regime could adversely impact our operations and business strategy. Additionally, we may face difficulties in obtaining regulatory approvals in jurisdictions in which we have not previously operated or in which we have limited experience.

In most of our key target markets, including the United States, regulatory approvals must be received prior to the importation and commercialization of transgenic products. These regulatory regimes may be particularly onerous. For example, the U.S. federal government’s regulation of biotechnology is divided among the United States Environmental Protection Agency, which regulates activity related to the invention of plant pesticides and herbicides, the USDA, which regulates the import, field testing and interstate movement of specific technologies that may be used in the creation of transgenic plants, and the United States Food and Drug Administration, which regulates foods derived from new plant varieties. In Argentina, the federal government’s regulation of agricultural biotechnology is handled primarily by two agencies, the National Advisory Commission on Agricultural Biotechnology (Comisión Nacional Asesora de Biotecnología Agropecuaria), or CONABIA, which regulates activity related to biosafety, and the National Food Safety and Quality Service (Servicio Nacional de Sanidad y Calidad Agroalimentaria), or SENASA, which regulates activity related to food and feed safety. Additionally, the National Market Regulator (Dirección Nacional de Mercados) must also conduct an economic evaluation. When products containing our seed traits or other technology reach large scale field trials, bio-safety evaluations and commercial approval stages, if we, our joint ventures or other collaborators are unable to obtain the requisite regulatory approvals or if there is a delay in obtaining such approvals as a result of negative market perception, heightened regulatory standards or unfamiliarity with the applicable regulatory regime, such products will not be commercialized, which would negatively impact our business and results of operations.

17

Our business is dependent in large part on the success of a single technology that we co-own and license and that remains subject to receipt of regulatory approval.

The majority of our commercial technology and biotechnology seed products currently under development incorporates HB4 technology. We and our joint ventures are focusing a significant amount of our resources on commercializing our HB4 technology and expect that the sale of biotech seeds that contain HB4 technology will comprise an increasing and significant portion of our future revenues. As a result, our future growth and financial performance will largely depend on our ability to receive regulatory approval for and commercialize our HB4 technology, and if this effort is unsuccessful we may not have resources to pursue development of our other products and our business could be materially and adversely affected. We also depend on our continued exclusive use of the HB4 technology pursuant to the terms of licensing agreements with CONICET and the National University of the Litoral. We hold an exclusive license with respect to further developments of HB4, which expires when the last of the HB4 patents expire in 2033, unless terminated earlier in accordance with its terms. If this licensing agreement or the pending patent applications were to be declared unenforceable or invalid, we may lose access to one of our principal technologies and could become involved in a costly or time-consuming legal dispute.

We are party to funding agreements that provide certain investors rights to a portion of the payments we might receive in connection with the commercialization of some of our technologies in certain crops.

Between 2005 and 2007, we entered into agreements with various investors in order to obtain funding in the aggregate amount of $1.0 million for research related to early stage development of technology relating to a specific gene from sunflower intended to promote drought tolerance in crops, referred to as Hahb 4. The agreements grant the investors in the aggregate the right to receive 54.4% of the rights and royalties payable to Bioceres S.A. from the successful commercialization of the resulting technology with respect to soybean, wheat and corn. As of the date hereof, a portion of the technology developed in connection with our research and development of Hahb 4 relating to a promoter element is being incorporated into a leading soybean product under development by Verdeca that also incorporates our HB4 technology. In addition, the licenses of our HB4 technology that we have granted to other developers and our joint ventures with respect to wheat and corn include the Hahb 4 promoter element. Accordingly, we may have to pay third parties royalties otherwise due to Bioceres S.A. in the absence of these agreements and we may not receive the full economic benefit of the commercialization of certain of our technologies. Investors party to these arrangements also may claim that they are entitled to payments in addition to the royalties we believe are within the scope of the agreements. The investors may also dispute the allocation of revenue as it relates to the relative importance of our various technologies incorporated into a given product. We cannot be certain how a court would interpret any ambiguities regarding the scope of these agreements or other claims that may be raised by one or more investors. Any dispute regarding these agreements could be costly and divert management’s attention from our operations, and if the investors are deemed to have rights to payments in excess of those we believe are applicable, our business, results of operations, cash flows and prospects would be materially and adversely affected.

There are a limited number of prospective JV partners and collaborators in the markets in which we operate.

Our technology sourcing, product development and commercialization activities are costly, time-intensive and require significant infrastructure and resources. Therefore, our business strategy involves entering into joint venture arrangements with global agricultural firms to leverage their resources, know-how and channels of distribution and into collaborations with research institutions and governmental agencies to facilitate our low cost approach to technology sourcing. The seed biotech and agro-industrial markets are highly consolidated and dominated by a relatively small number of large companies. For example, according to Phillips McDougall’s 2013 Industry Presentation on the Global Seed Market, in 2013 (the latest period for which data is available), six agricultural and seed companies, Monsanto Company, DuPont Pioneer, Syngenta, Vilmorin (Limagrain) and Dow, controlled approximately 64% of market value in the global seed market. Additionally, there are a limited number of researchers and research institutions focused on the technologies that we seek to develop and competition for entry into collaboration arrangements with them can be challenging. Due to the small number of companies in our markets and the small number of potential collaborators, there are limited opportunities for us to pursue additional joint ventures and collaborations

18

with new partners and collaborators. We may cease to be attractive to prospective JV partners or research collaborators if our technology platform or track record is not perceived to be sufficiently developed or successful or if, in the case of prospective JV partners, such prospective partners view us as competitors and choose not to collaborate with us. In addition, if we fail to develop or maintain our relationships with any of our existing JV partners or collaborators, we could lose our opportunity to work with that JV partner or collaborator and suffer a reputational risk that could impact our relationships with other JV partners and collaborators in what is a relatively small industry community. If we are unable to enter into new joint venture agreements or collaborations, we may face higher development costs than anticipated, greater difficulties in achieving commercialization, challenges in expanding our portfolio of technologies and distribution networks and commercial products, or other adverse impacts, which could have a material adverse effect on our business prospects.

The licenses we grant to certain of the joint ventures in which we participate are exclusive with respect to certain territories and/or crops, which limits our ability to use the licensed technology and future technologies either independently or with another partner in the exclusive territories and fields of use.