UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-23053

American Funds Retirement Income Portfolio Series

(Exact Name of Registrant as Specified in Charter)

6455 Irvine Center Drive

Irvine, California 92618

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (949) 975-5000

Date of fiscal year end: October 31

Date of reporting period: October 31, 2023

Gregory F. Niland

American Funds Retirement Income Portfolio Series

5300 Robin Hood Road

Norfolk, Virginia 23513

(Name and Address of Agent for Service)

ITEM 1 – Reports to Stockholders

American Funds®

Retirement Income

Portfolio Series Annual report

for the year ended

October 31, 2023 |  |

Portfolios designed

to help address

your retirement

income needs

American Funds, by Capital Group, is one of the nation’s largest mutual fund families. For over 90 years, Capital Group has invested with a long-term focus based on thorough research and attention to risk.

American Funds® Retirement Income Portfolio — Conservative strives for the accomplishment of three investment objectives: current income, long-term growth of capital and conservation of capital, with an emphasis on income and conservation of capital.

American Funds® Retirement Income Portfolio — Moderate strives for the balanced accomplishment of three investment objectives: current income, long-term growth of capital and conservation of capital.

American Funds® Retirement Income Portfolio — Enhanced strives for the accomplishment of three investment objectives: current income, long-term growth of capital and conservation of capital, with an emphasis on income and growth of capital.

Fund results shown in this report, unless otherwise indicated, are for Class F-2 shares. Class A share results are shown at net asset value unless otherwise indicated. If a sales charge (maximum 5.75%) had been deducted from Class A shares, the results would have been lower. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. For current information and month-end results, visit capitalgroup.com.

Here are the total returns on a $1,000 investment for periods ended September 30, 2023 (the most recent calendar quarter-end). Class A share returns reflect the maximum 5.75% sales charge. Also shown are the expense ratios as of the series prospectus dated January 1, 2024 (unaudited).

| | | Cumulative

total returns | | Average annual

total returns | | |

| | | 1 year | | 5 years | | Lifetime

(since 8/28/15) | | Expense

ratios |

| | | | | | | | | |

| American Funds Retirement Income Portfolio — Conservative | | | | | | | | | | | | | | | | |

| Class F-2 shares | | | 5.69 | % | | | 3.17 | % | | | 3.95 | % | | | 0.39 | % |

| Class A shares | | | –0.51 | | | | 1.75 | | | | 2.96 | | | | 0.56 | |

| American Funds Retirement Income Portfolio — Moderate | | | | | | | | | | | | | | | | |

| Class F-2 shares | | | 8.88 | | | | 4.01 | | | | 5.02 | | | | 0.41 | |

| Class A shares | | | 2.47 | | | | 2.56 | | | | 4.03 | | | | 0.60 | |

| American Funds Retirement Income Portfolio — Enhanced | | | | | | | | | | | | | | | | |

| Class F-2 shares | | | 11.76 | | | | 4.69 | | | | 5.99 | | | | 0.42 | |

| Class A shares | | | 5.07 | | | | 3.26 | | | | 4.99 | | | | 0.59 | |

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, results reflect fee waivers and/or expense reimbursements, without which they would have been lower. Visit capitalgroup.com for more information.

American Funds Retirement Income Portfolio Series funds invest in Class R-6 shares of the underlying funds.

For other share class results, visit capitalgroup.com and americanfundsretirement.com.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Contents

Fellow investors:

All three portfolios in American Funds Retirement Income Portfolio Series posted positive returns that can help investors to accomplish their retirement income objectives for the fiscal year ended October 31, 2023. All three funds overcame a difficult environment, especially as it relates to the bond market.

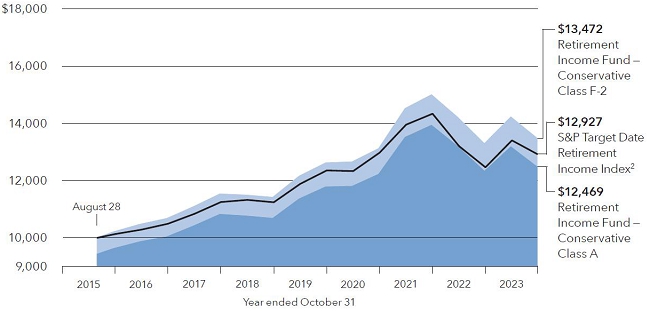

The Conservative portfolio had a total return of 1.37% for the period, which included dividends totaling nearly 39 cents a share. The fund’s income return was 3.67% for those choosing to reinvest dividends and 3.62% for those taking dividends in cash.

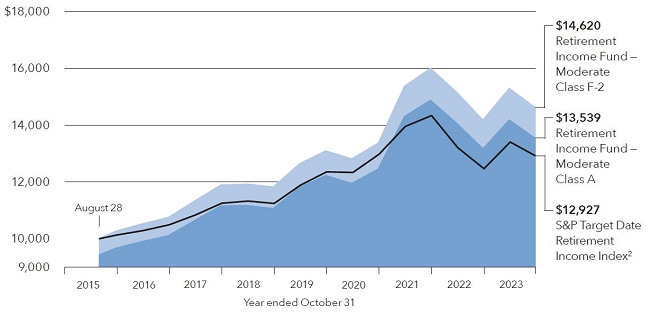

The Moderate portfolio had a total return of 3.07%, which included dividends and capital gains totaling more than 60 cents a share. The fund’s income return was 3.64% with dividends reinvested and 3.60% for those taking dividends in cash.

Finally, the Enhanced portfolio had a total return of 4.61%, including dividends and capital gains of more than 70 cents a share. The fund’s income return was 3.44% with dividends reinvested and 3.39% for investors taking dividends in cash.

By way of comparison, the S&P Target Date Retirement Income Index advanced 3.71% for the 12-month period.

About the series

In creating the series, a mix of individual American Funds was carefully selected through an objective-based process and rigorous analysis. The Portfolio Solutions Committee regularly monitors each fund in the series. Each portfolio is designed to provide retirement income based on an investor’s risk tolerance and withdrawal rates. To learn more about the three portfolios, refer to page 6.

Results at a glance

For periods ended October 31, 2023, with all distributions reinvested

| | | Cumulative

total returns | | Average annual

total returns |

| | | 1 year | | 5 years | | Lifetime

(since 8/28/15) |

| American Funds Retirement Income Portfolio — Conservative | | | | | | | | | | | | |

| Class F-2 shares | | | 1.37 | % | | | 3.37 | % | | | 3.71 | % |

| Class A shares | | | 1.20 | | | | 3.16 | | | | 3.48 | |

| American Funds Retirement Income Portfolio — Moderate | | | | | | | | | | | | |

| Class F-2 shares | | | 3.07 | | | | 4.33 | | | | 4.76 | |

| Class A shares | | | 2.79 | | | | 4.12 | | | | 4.53 | |

| American Funds Retirement Income Portfolio — Enhanced | | | | | | | | | | | | |

| Class F-2 shares | | | 4.61 | | | | 5.17 | | | | 5.70 | |

| Class A shares | | | 4.43 | | | | 4.95 | | | | 5.48 | |

| S&P Target Date Retirement Income Index* | | | 3.71 | | | | 2.83 | | | | 3.19 | |

Past results are not predictive of results in future periods.

| * | The S&P Target Date Retirement Income Index, a component of the S&P Target Date Index Series, has an asset allocation and glide path that represent a market consensus across the universe of target date fund managers. The index is fully investable, with varying levels of exposure to the asset classes determined during an annual survey process of target date funds’ holdings. This index is unmanaged, and its results include reinvested dividends and/or distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes. Investors cannot invest directly in an index. Source: S&P Dow Jones Indices LLC. |

The American Funds Retirement Income Portfolio Series investment allocations may not achieve fund objectives, and adequate income through retirement is not guaranteed. The funds’ risks are directly related to the risks of the underlying funds. Payments consisting of return of capital will result in a decrease in an investor’s fund share balance. Higher rates of withdrawal and withdrawals during declining markets may result in a more rapid decrease in an investor’s fund share balance. Persistent returns of capital could ultimately result in a zero account balance. Refer to the series prospectus and the Risk Factors section of this report for more information on these and other risks associated with investing in the funds.

| American Funds Retirement Income Portfolio Series | 1 |

The economy

The markets began the reporting period optimistic that inflation had peaked, and this helped the economy in general. Inflation has continued to ease since then, more rapidly in the U.S. than in other regions. The consensus a year ago was that the economy was headed for recession. While there is still uncertainty and doubt about the economic outlook, many market analysts and economists now think a recession is not imminent.

U.S. equities rebounded in the fourth quarter of 2022, having finished their worst year since 2008. The rally continued for three consecutive quarters, through the first two quarters of 2023, before reversing by the third quarter over fears that the U.S. Federal Reserve (the Fed) would keep interest rates higher for longer than had previously been expected. This was mirrored by global central banks indicating they may keep monetary policy tight.

Bond markets also rallied early in the period but stalled in the second quarter of 2023 due to pressure from rising interest rates. However, heading into the third quarter of 2023, the 10-year U.S. Treasury began a slow rise in yield, registering 4.18 on September 1 and 4.99 on October 191 before rallying again in early November. This will be a rate to watch closely as we move into a new reporting period.

Over the period, the world economy continued to show signs of stabilization and growth in some sectors, despite volatility caused by geopolitical strains, notably in energy prices. Key economic considerations in the coming period will include continuing geopolitical conflicts and, over the longer run, climate adaptation along with the evolution and adoption of artificial intelligence (AI).

The AI explosion has been a huge market driver over the period and will likely continue to be a major economic force for years to come. AI is a driver of innovation, and therefore growth, that affects the whole economy, not just the technology sector. It will affect such sectors as health care, food, transportation and more. AI will have significant consequences — as yet unknown — on industries and individuals. This level of change can make investing difficult to navigate. Our position in such an environment is always to first take a long-term view and, using exhaustive research, invest in what makes sense for the long-term well-being of our investors.

The burst of investment in AI mirrors historical surges in investment and productivity, driven by technological innovation: transportation infrastructure in the 19th century, electrification in the early 20th century and the internet in recent decades. Speculative frenzy often fuels such a bubble, which in turn drives up stock prices and lowers the cost of capital. This enables large-scale investment, with wildly varying returns to investors. Sometimes investment returns are spectacular; sometimes investors suffer large losses, even if society as a whole ends up benefiting. So, we use and advise care and caution.

The climate transition is a particular focus in the European Union (EU) now, with a package of measures that target an emissions reduction of at least 55% by 2030 a legal obligation.2 For example, all new cars must have zero CO2emissions starting in 2035.3

Businesses globally are affected by climate policy, as EU countries are working on new legislation to achieve this goal and net zero CO2emissions by 2050.

Changes enacted as a result of the new measures will have far-reaching effects, redirecting trillions of dollars globally. Because the climate transition has such significant impact on the economy and on the credit quality of affected businesses and assets, it will also affect the conduct of monetary policy and regulation aimed at ensuring the stability of the financial system as a whole. The good news is that the European Central Bank (ECB) still views its policy objectives as feasible and sees climate targets as attainable in a way that is politically, economically and socially acceptable.4 In the U.S., the outcomes are more difficult to evaluate because climate discussions continue to be polarized in American politics.

Going forward, as we watch geopolitical forces and crises rising, abating and taking shape, we focus on fundamental research and investor well-being for the long term. To do that, we put tremendous effort into understanding geopolitical risk in different regions and looking at how it affects investment opportunities large and small. Policy and conflict affect everything from supply chains to prices to quality of life for individuals. All of these factors are important to us, and we put these considerations and more into each decision.

Over decades of careful investing, we have learned to avoid quick reactions to headlines. As always, we take our time and dig into what is going on underneath and use the considerable reach of our full global resources as guides.

The stock market

Global stocks rose in the fourth quarter of 2022 and continued through the second quarter of 2023, as investors welcomed signs that inflation may have peaked in

| 1 | CNBC, “U.S. 10 Year Treasury.” |

| 2 | Reuters: “EU countries approve 2035 phaseout of CO2-emitting cars,” by Kate Abnett, March 29, 2023. |

| 3 | European Council/Council of the European Union: “Fit for 55.” |

| 4 | European Central Bank, “CLIMATE-RELATED INDICATORS: Analytical indicators on carbon emissions.” |

| | |

| 2 | American Funds Retirement Income Portfolio Series |

key markets around the world. The rallies were also driven by technology stocks that were lifted by rapid development in generative artificial intelligence. Shares of NVIDIA soared 52% during the second quarter and 190% year to date, as of June 30, 2023. Rival chipmakers Broadcom and Advanced Micro Devices also enjoyed double-digit gains. Apple rose 18%, becoming the world’s first $3 trillion company. Other sectors rallied as well. Pharmaceutical giant Eli Lilly climbed 37% in the second quarter of 2023 over optimism regarding its early-stage Alzheimer’s and obesity drugs.

Markets lost ground in the third quarter of 2023, pressured by rising interest rates, slowing growth in some of the world’s largest economies and renewed fear that the Fed would keep interest rates higher for longer than previously expected. Consumer price increases — while still high on a historical basis — moderated in the U.S., Europe and many other economies.

The bond market

Global fixed income advanced in the early quarters of the reporting period, on adjusted rate expectations by the Fed and European Central Bank. However, bond markets declined in the second quarter of 2023, as the ECB — along with many other central banks around the world — continued to tighten monetary policy. At its July meeting, the Fed boosted its benchmark federal funds rate to a 22-year high. The 11th hike since March 2022 pushed rates to a target range of 5.25% to 5.50%. Although the central bank held rates steady in September, its projections indicated another hike could come by the end of the year.

General expectations are that the Fed could begin cutting rates in 2024, but there are wide discrepancies in predictions about the timing of such rate cuts.

Inside the series

Each portfolio, which focuses on generating income from bonds and dividend-paying stocks, produced positive returns over the past 12 months.

The portfolios benefited from the flexibility to invest in funds investing in both U.S. and international equities. While equities advanced both at home and abroad, international stocks outpaced those in the U.S. by nearly 200 basis points (2%) in the fiscal year, as measured by the MSCI All Country World Index ex USA and S&P 500 Index, respectively.5 As income strategies, the portfolios emphasize dividend-paying stocks, and the picture for these equities has been a split-screen — the top quintile of dividend-paying stocks outpaced the lowest quintile in international markets for the 12 months ended September 30, 2023, but the opposite was true in the U.S. Although dividend-paying stocks tend to trail the broader market during periods of strong growth and market exuberance, we believe they should be an integral part of a retirement income strategy, as these stocks can provide both income and appreciation potential with less volatility than growth-oriented stocks. Bond market returns were muted during the fiscal year, with some bond funds adding to the portfolios’ returns, while others presented setbacks. We continued to manage the portfolios’ bond exposure actively, to provide an appropriate mix of income, inflation protection, capital preservation and diversification from equities.

Looking forward

Our focus continues to be the long-term well-being of our investors. Rapidly changing markets and world circumstances are things we cannot predict. However, through our 90-year history, we have seen that people and markets have shown their ability to endure. Our focus on exhaustive, fundamental research and investor well-being is designed for tough and uncertain times.

Careful securities selection remains at the core of our investment process, whether in times of rapid growth or inevitable decline. We continue to encourage you to take a long-term view on investing.

We thank you for your trust in our efforts and look forward to reporting to you next year.

Cordially,

Andrew B. Suzman

President

December 11, 2023

For current information about the series, visit capitalgroup.com.

| 5 | The S&P 500 Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks. MSCI All Country World ex USA Index is a free float-adjusted market capitalization weighted index that is designed to measure equity market results in the global developed and emerging markets, excluding the United States. The indexes are unmanaged, and their results include reinvested dividends and/or distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes. |

| | |

| American Funds Retirement Income Portfolio Series | 3 |

The value of a $10,000 investment

How a hypothetical $10,000 investment has grown (for periods ended October 31, 2023, with all distributions reinvested)

Fund results shown are for Class F-2 shares and Class A shares. Class A share results reflect deduction of the maximum sales charge of 5.75% on a $10,000 investment.1; thus, the net amount invested was $9,425. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. For current information and month-end results, visit capitalgroup.com.

Conservative portfolio

Average annual total returns3 based on a $1,000 investment

(for periods ended October 31, 2023)

| | | 1 year | | 5 years | | Lifetime

(since 8/28/15) |

| | | | | | | |

| Class F-2 shares | | | 1.37 | % | | | 3.37 | % | | | 3.71 | % |

| Class A shares* | | | –4.61 | | | | 1.94 | | | | 2.74 | |

| | |

| * | Assumes payment of the maximum 5.75% sales charge. |

Moderate portfolio

Average annual total returns3 based on a $1,000 investment

(for periods ended October 31, 2023)

| | | 1 year | | 5 years | | Lifetime

(since 8/28/15) |

| | | | | | | |

| Class F-2 shares | | | 3.07 | % | | | 4.33 | % | | | 4.76 | % |

| Class A shares* | | | –3.13 | | | | 2.90 | | | | 3.78 | |

| | |

| * | Assumes payment of the maximum 5.75% sales charge. |

Refer to page 5 for footnotes.

| 4 | American Funds Retirement Income Portfolio Series |

Enhanced portfolio

Average annual total returns3 based on a $1,000 investment

(for periods ended October 31, 2023)

| | | 1 year | | 5 years | | Lifetime

(since 8/28/15) |

| | | | | | | |

| Class F-2 shares | | | 4.61 | % | | | 5.17 | % | | | 5.70 | % |

| Class A shares* | | | –1.54 | | | | 3.72 | | | | 4.72 | |

| | |

| * | Assumes payment of the maximum 5.75% sales charge. |

| 1 | As outlined in the prospectus, the sales charge is reduced for accounts (and aggregated investments) of $25,000 or more and is eliminated for purchases of $1 million or more. |

| 2 | The S&P Target Date Retirement Income Index, a component of the S&P Target Date Index Series, has an asset allocation and glide path that represent a market consensus across the universe of target date fund managers. The index is fully investable, with varying levels of exposure to the asset classes determined during an annual survey process of target date funds’ holdings. This index is unmanaged, and its results include reinvested dividends and/or distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes. Source: S&P Dow Jones Indices LLC. |

| 3 | Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, results reflect fee waivers and/or expense reimbursements, without which they would have been lower. Visit capitalgroup.com for more information. |

American Funds Retirement Income Portfolio Series funds invest in Class R-6 shares of the underlying funds.

There is no sales charge on dividends or capital gain distributions that are reinvested in additional shares. The results shown are before taxes on fund distributions and sale of fund shares.

| American Funds Retirement Income Portfolio Series | 5 |

About American Funds Retirement Income Portfolio Series

A trio of investments intended to help meet the unique needs of retirees

American Funds Retirement Income Portfolio Series was created to address the real income needs of retirees. In developing the funds, we surveyed hundreds of retirees and found that they were not only worried about paying their bills, but also about maintaining an enjoyable retirement lifestyle. Finding an appropriate balance between asset growth and withdrawals was a priority, but preservation of their original nest egg was a factor as well.

We took their concerns to heart, creating three portfolios designed to meet different income needs and to accommodate varying levels of risk tolerance.

| | • | The Conservative portfolio focuses on capital preservation. That means a higher degree of fixed income investments and a lower recommended withdrawal rate. |

| | | |

| | • | The Moderate portfolio seeks a balance of withdrawals and longevity with a moderate withdrawal rate and moderate risk of loss. |

| | | |

| | • | The Enhanced portfolio targets higher asset growth through a larger allocation of equity investments. While its composition makes it more vulnerable to volatility, it offers the potential for greater withdrawals. |

Income in retirement

When thinking about retirement income, it shouldn’t be confused with income in the traditional sense of bond returns and dividend payments. Rather, it’s about withdrawals taken from the portfolio as a whole which, in some cases, includes drawing on principal. To offset any declines in bond income and dividends, growth is essential. For this reason, each of the three portfolios includes a flexible mix of equity-income funds. As well as offering the potential to grow assets over time, they can help buffer the portfolios in market downturns.

There are no guarantees in investing, but we believe these portfolios can help our investors pursue a successful retirement while seeking to preserve as much of their initial investment as possible.

Experienced oversight and management

The Portfolio Solutions Committee — a group of seven American Funds portfolio managers with an average of 31* years of investment experience between them — is responsible for monitoring the series. They review each portfolio’s holdings, results and distributions to determine they not only remain aligned with their objectives, but that they can support their suggested withdrawal rates now and in the future.

| * | Portfolio manager years of experience as of the prospectus dated January 1, 2024. |

| | |

| 6 | American Funds Retirement Income Portfolio Series |

Portfolios designed to serve the unique needs of retirees

American Funds Retirement Income Portfolio Series was launched in August 2015 to help retirees generate income to fund their lifestyles in retirement. The three funds are designed to provide income in retirement that balances the need for income with an investor’s risk tolerance.

The members of the Portfolio Solutions Committee monitor the series to keep the funds aligned with their objectives and to determine whether any changes to the underlying fund allocations are needed.

American Funds Retirement Income Portfolio — Conservative

With significant allocations to The Bond Fund of America® and U.S. Government Securities Fund®, this portfolio focuses on preservation of capital, while still seeking to provide current income.

Underlying funds:

| 7% | | American Mutual Fund® |

| 14% | | Capital Income Builder® |

| 19% | | The Income Fund of America® |

| 8% | | American Balanced Fund® |

| 4% | | American Funds® Global Balanced Fund |

| 15% | | The Bond Fund of America |

| 7% | | U.S. Government Securities Fund |

| 6% | | American Funds Inflation Linked Bond Fund® |

| 10% | | American Funds® Strategic Bond Fund |

| 5% | | Intermediate Bond Fund of America® |

| 5% | | American Funds® Multi-Sector Income Fund |

American Funds Retirement Income Portfolio — Moderate

The portfolio includes several fixed income funds, but the allocation is weighted toward equity-income funds like Capital Income Builder and The Income Fund of America.

Underlying funds:

| 5% | | American Mutual Fund |

| 7% | | Capital World Growth and Income Fund® |

| 14% | | Capital Income Builder |

| 24% | | The Income Fund of America |

| 15% | | American Balanced Fund |

| 5% | | American Funds Global Balanced Fund |

| 5% | | The Bond Fund of America |

| 5% | | American Funds Inflation Linked Bond Fund |

| 9% | | American Funds® Multi-Sector Income Fund |

| 6% | | American Funds Strategic Bond Fund |

| 5% | | U.S. Government Securities Fund |

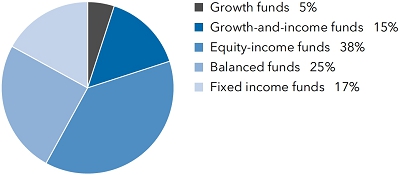

American Funds Retirement Income Portfolio — Enhanced

With larger allocations to income-focused equity funds, the portfolio has greater potential upside over the long term and greater potential for current income, but likely will result in more volatility.

Underlying funds:

| 5% | | AMCAP Fund® |

| 5% | | American Mutual Fund |

| 10% | | Capital World Growth and Income Fund |

| 14% | | Capital Income Builder |

| 24% | | The Income Fund of America |

| 20% | | American Balanced Fund |

| 5% | | American Funds Global Balanced Fund |

| 5% | | American Funds Inflation Linked Bond Fund |

| 7% | | American Funds Multi-Sector Income Fund |

| 5% | | American High-Income Trust® |

AMCAP Fund, a growth-oriented fund, outpaced its respective benchmark index over the fiscal year, as did Capital World Growth and Income Fund, a global growth-and-income-oriented fund. American Mutual Fund, a U.S. growth-and-income-oriented fund, and Capital Income Builder and The Income Fund of America, two other funds focused at least partially on income, all trailed their benchmark indexes. American Balanced Fund, which focuses on U.S. investments, trailed its benchmark, while its globally oriented counterpart, American Funds Global Balanced Fund, outpaced its benchmark. All of the bond funds (except American Funds Multi-Sector Income Fund) also trailed their indexes. Please refer to the funds’ prospectuses for information on their benchmark indexes.

The underlying fund allocations are as of September 30, 2023. American Funds Retirement Income Portfolio Series funds are actively monitored, so allocations may vary over time.

| American Funds Retirement Income Portfolio Series | 7 |

American Funds Conservative Portfolio

Investment portfolio October 31, 2023

| Growth-and-income funds 7% | | Shares | | | Value

(000) | |

| American Mutual Fund, Class R-6 | | | 1,705,110 | | | $ | 80,277 | |

| |

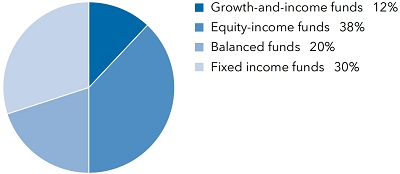

| Equity-income funds 33% | | | | | | | | |

| The Income Fund of America, Class R-6 | | | 10,140,060 | | | | 217,910 | |

| Capital Income Builder, Class R-6 | | | 2,666,145 | | | | 160,875 | |

| | | | | | | | 378,785 | |

| |

| Balanced funds 12% | | | | | | | | |

| American Balanced Fund, Class R-6 | | | 3,152,519 | | | | 91,738 | |

| American Funds Global Balanced Fund, Class R-6 | | | 1,415,780 | | | | 46,098 | |

| | | | | | | | 137,836 | |

| |

| Fixed income funds 48% | | | | | | | | |

| The Bond Fund of America, Class R-6 | | | 16,176,777 | | | | 172,768 | |

| American Funds Strategic Bond Fund, Class R-6 | | | 13,139,635 | | | | 114,578 | |

| U.S. Government Securities Fund, Class R-6 | | | 7,088,370 | | | | 80,807 | |

| American Funds Inflation Linked Bond Fund, Class R-6 | | | 7,780,230 | | | | 68,855 | |

| American Funds Multi-Sector Income Fund, Class R-6 | | | 6,707,341 | | | | 57,817 | |

| Intermediate Bond Fund of America, Class R-6 | | | 4,807,314 | | | | 57,784 | |

| | | | | | | | 552,609 | |

| | | | | | | | | |

| Total investment securities 100% (cost: $1,215,988,000) | | | | | | | 1,149,507 | |

| Other assets less liabilities 0% | | | | | | | (294 | ) |

| | | | | | | | | |

| Net assets 100% | | | | | | $ | 1,149,213 | |

| | |

| 8 | American Funds Retirement Income Portfolio Series |

American Funds Conservative Portfolio (continued)

Investments in affiliates1

| | | Value at

11/1/2022

(000) | | | Additions

(000) | | | Reductions

(000) | | | Net

realized

gain (loss)

(000) | | | Net

unrealized

appreciation

(depreciation)

(000) | | | Value at

10/31/2023

(000) | | | Dividend

income

(000) | | | Capital gain

distributions

received

(000) | |

| Growth-and-income funds 7% | | | | | | | | | | | | | | | | | | | | | |

| American Mutual Fund, Class R-6 | | $ | 93,446 | | | $ | 4,783 | | | $ | 14,861 | | | $ | 417 | | | $ | (3,508 | ) | | $ | 80,277 | | | $ | 2,087 | | | $ | 2,565 | |

| Equity-income funds 33% | | | | | | | | | | | | | | | |

| The Income Fund of America, Class R-6 | | | 248,769 | | | | 19,464 | | | | 37,545 | | | | (3,619 | ) | | | (9,159 | ) | | | 217,910 | | | | 9,004 | | | | 8,633 | |

| Capital Income Builder, Class R-6 | | | 184,077 | | | | 7,619 | | | | 31,766 | | | | (202 | ) | | | 1,147 | | | | 160,875 | | | | 6,815 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | 378,785 | | | | | | | | | |

| Balanced funds 12% | | | |

| American Balanced Fund, Class R-6 | | | 105,813 | | | | 2,211 | | | | 20,113 | | | | 893 | | | | 2,934 | | | | 91,738 | | | | 2,017 | | | | — | |

| American Funds Global Balanced Fund, Class R-6 | | | 53,027 | | | | 1,058 | | | | 11,056 | | | | (596 | ) | | | 3,665 | | | | 46,098 | | | | 1,019 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | 137,836 | | | | | | | | | |

| Fixed income funds 48% | | | | | | | | | | | | | | | | | | | | | | |

| The Bond Fund of America, Class R-6 | | | 319,206 | | | | 15,349 | | | | 158,990 | | | | (27,318 | ) | | | 24,521 | | | | 172,768 | | | | 10,369 | | | | — | |

| American Funds Strategic Bond Fund, Class R-6 | | | 126,180 | | | | 9,497 | | | | 11,568 | | | | (2,360 | ) | | | (7,171 | ) | | | 114,578 | | | | 7,257 | | | | — | |

| U.S. Government Securities Fund, Class R-6 | | | 87,339 | | | | 5,813 | | | | 7,887 | | | | (1,126 | ) | | | (3,332 | ) | | | 80,807 | | | | 3,206 | | | | — | |

| American Funds Inflation Linked Bond Fund, Class R-6 | | | 76,498 | | | | 7,813 | | | | 9,152 | | | | (2,073 | ) | | | (4,231 | ) | | | 68,855 | | | | 4,791 | | | | — | |

| American Funds Multi-Sector Income Fund, Class R-6 | | | — | | | | 64,760 | | | | 4,133 | | | | (86 | ) | | | (2,724 | ) | | | 57,817 | | | | 1,398 | | | | — | |

| Intermediate Bond Fund of America, Class R-6 | | | — | | | | 64,208 | | | | 4,562 | | | | (96 | ) | | | (1,766 | ) | | | 57,784 | | | | 845 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | 552,609 | | | | | | | | | |

| Total 100% | | | | | | | | | | | | | | $ | (36,166 | ) | | $ | 376 | | | $ | 1,149,507 | | | $ | 48,808 | | | $ | 11,198 | |

| | |

| 1 | Part of the same “group of investment companies” as the fund as defined under the Investment Company Act of 1940, as amended. |

Refer to the notes to financial statements.

| American Funds Retirement Income Portfolio Series | 9 |

American Funds Moderate Portfolio

Investment portfolio October 31, 2023

| Growth-and-income funds 12% | | Shares | | | Value

(000) | |

| Capital World Growth and Income Fund, Class R-6 | | | 1,687,130 | | | $ | 90,869 | |

| American Mutual Fund, Class R-6 | | | 1,384,820 | | | | 65,197 | |

| | | | | | | | 156,066 | |

| |

| Equity-income funds 38% | | | | | | | | |

| The Income Fund of America, Class R-6 | | | 14,535,733 | | | | 312,373 | |

| Capital Income Builder, Class R-6 | | | 3,024,498 | | | | 182,498 | |

| | | | | | | | 494,871 | |

| |

| Balanced funds 20% | | | | | | | | |

| American Balanced Fund, Class R-6 | | | 6,698,929 | | | | 194,939 | |

| American Funds Global Balanced Fund, Class R-6 | | | 2,004,882 | | | | 65,279 | |

| | | | | | | | 260,218 | |

| |

| Fixed income funds 30% | | | | | | | | |

| American Funds Multi-Sector Income Fund, Class R-6 | | | 13,645,818 | | | | 117,627 | |

| American Funds Strategic Bond Fund, Class R-6 | | | 8,958,183 | | | | 78,116 | |

| The Bond Fund of America, Class R-6 | | | 6,133,053 | | | | 65,501 | |

| U.S. Government Securities Fund, Class R-6 | | | 5,745,702 | | | | 65,501 | |

| American Funds Inflation Linked Bond Fund, Class R-6 | | | 7,372,802 | | | | 65,249 | |

| | | | | | | | 391,994 | |

| | | | | | | | | |

| Total investment securities 100% (cost: $1,362,977,000) | | | | | | | 1,303,149 | |

| Other assets less liabilities 0% | | | | | | | (325 | ) |

| | | | | | | | | |

| Net assets 100% | | | | | | $ | 1,302,824 | |

| | |

| 10 | American Funds Retirement Income Portfolio Series |

American Funds Moderate Portfolio (continued)

Investments in affiliates1

| | | Value at

11/1/2022

(000) | | | Additions

(000) | | | Reductions

(000) | | | Net

realized

gain (loss)

(000) | | | Net

unrealized

appreciation

(depreciation)

(000) | | | Value at

10/31/2023

(000) | | | Dividend

income

(000) | | | Capital gain

distributions

received

(000) | |

| Growth-and-income funds 12% | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Capital World Growth and Income Fund, Class R-6 | | $ | 94,463 | | | $ | 3,628 | | | $ | 17,356 | | | $ | (1,936 | ) | | $ | 12,070 | | | $ | 90,869 | | | $ | 2,260 | | | $ | — | |

| American Mutual Fund, Class R-6 | | | 68,816 | | | | 3,906 | | | | 4,934 | | | | 2 | | | | (2,593 | ) | | | 65,197 | | | | 1,616 | | | | 1,936 | |

| | | | | | | | | | | | | | | | | | | | | | | | 156,066 | | | | | | | | | |

| Equity-income funds 38% | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| The Income Fund of America, Class R-6 | | | 323,250 | | | | 32,046 | | | | 24,400 | | | | (1,617 | ) | | | (16,906 | ) | | | 312,373 | | | | 12,300 | | | | 11,456 | |

| Capital Income Builder, Class R-6 | | | 189,062 | | | | 8,847 | | | | 15,408 | | | | (306 | ) | | | 303 | | | | 182,498 | | | | 7,361 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | 494,871 | | | | | | | | | |

| Balanced funds 20% | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| American Balanced Fund, Class R-6 | | | 201,460 | | | | 5,431 | | | | 18,851 | | | | (1,420 | ) | | | 8,319 | | | | 194,939 | | | | 4,068 | | | | — | |

| American Funds Global Balanced Fund, Class R-6 | | 67,315 | | | | 1,379 | | | | 7,102 | | | | (1,058 | ) | | | 4,745 | | | | 65,279 | | | | 1,379 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | 260,218 | | | | | | | | | |

| Fixed income funds 30% | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| American Funds Multi-Sector Income Fund, Class R-6 | | | 117,919 | | | | 13,096 | | | | 11,646 | | | | (982 | ) | | | (760 | ) | | | 117,627 | | | | 7,793 | | | | — | |

| American Funds Strategic Bond Fund, Class R-6 | | | 77,852 | | | | 11,990 | | | | 5,296 | | | | (617 | ) | | | (5,813 | ) | | | 78,116 | | | | 4,628 | | | | — | |

| The Bond Fund of America, Class R-6 | | | 64,765 | | | | 6,537 | | | | 3,171 | | | | (332 | ) | | | (2,298 | ) | | | 65,501 | | | | 2,627 | | | | — | |

| U.S. Government Securities Fund, Class R-6 | | | 64,672 | | | | 8,226 | | | | 3,749 | | | | (579 | ) | | | (3,069 | ) | | | 65,501 | | | | 2,487 | | | | — | |

| American Funds Inflation Linked Bond Fund, Class R-6 | | | 65,617 | | | | 9,644 | | | | 4,332 | | | | (783 | ) | | | (4,897 | ) | | | 65,249 | | | | 4,204 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | 391,994 | | | | | | | | | |

| Total 100% | | | | | | | | | | | | | | $ | (9,628 | ) | | $ | (10,899 | ) | | $ | 1,303,149 | | | $ | 50,723 | | | $ | 13,392 | |

| | |

| 1 | Part of the same “group of investment companies” as the fund as defined under the Investment Company Act of 1940, as amended. |

Refer to the notes to financial statements.

| American Funds Retirement Income Portfolio Series | 11 |

American Funds Enhanced Portfolio

Investment portfolio October 31, 2023

| Growth funds 5% | | Shares | | | Value

(000) | |

| AMCAP Fund, Class R-6 | | | 2,139,203 | | | $ | 73,033 | |

| |

| Growth-and-income funds 15% | | | | | | | | |

| Capital World Growth and Income Fund, Class R-6 | | | 2,717,474 | | | | 146,363 | |

| American Mutual Fund, Class R-6 | | | 1,561,723 | | | | 73,526 | |

| | | | | | | | 219,889 | |

| |

| Equity-income funds 38% | | | | | | | | |

| The Income Fund of America, Class R-6 | | | 16,375,923 | | | | 351,919 | |

| Capital Income Builder, Class R-6 | | | 3,402,575 | | | | 205,311 | |

| | | | | | | | 557,230 | |

| |

| Balanced funds 25% | | | | | | | | |

| American Balanced Fund, Class R-6 | | | 10,069,575 | | | | 293,024 | |

| American Funds Global Balanced Fund, Class R-6 | | | 2,253,923 | | | | 73,388 | |

| | | | | | | | 366,412 | |

| |

| Fixed income funds 17% | | | | | | | | |

| American Funds Multi-Sector Income Fund, Class R-6 | | | 11,956,320 | | | | 103,063 | |

| American High-Income Trust, Class R-6 | | | 8,345,120 | | | | 73,938 | |

| American Funds Inflation Linked Bond Fund, Class R-6 | | | 8,254,232 | | | | 73,050 | |

| | | | | | | | 250,051 | |

| | | | | | | | | |

| Total investment securities 100% (cost: $1,493,173,000) | | | | | | | 1,466,615 | |

| Other assets less liabilities 0% | | | | | | | (360 | ) |

| | | | | | | | | |

| Net assets 100% | | | | | | $ | 1,466,255 | |

| | |

| 12 | American Funds Retirement Income Portfolio Series |

American Funds Enhanced Portfolio (continued)

Investments in affiliates1

| | | Value at

11/1/2022

(000) | | | Additions

(000) | | | Reductions

(000) | | | Net

realized

gain (loss)

(000) | | | Net

unrealized

appreciation

(depreciation)

(000) | | | Value at

10/31/2023

(000) | | | Dividend

income

(000) | | | Capital gain

distributions

received (000) | |

| Growth funds 5% | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| AMCAP Fund, Class R-6 | $ | 71,128 | | | $ | 4,890 | | | $ | 11,556 | | | $ | (2,012 | ) | | $ | 10,583 | | | $ | 73,033 | | | $ | 450 | | | $ | — | |

| Growth-and-income funds 15% | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Capital World Growth and Income Fund, Class R-6 | | | 143,934 | | | | 6,275 | | | | 19,037 | | | | (2,047 | ) | | | 17,238 | | | | 146,363 | | | | 3,528 | | | | — | |

| American Mutual Fund, Class R-6 | | | 73,562 | | | | 4,876 | | | | 1,952 | | | | (45 | ) | | | (2,915 | ) | | | 73,526 | | | | 1,760 | | | | 2,078 | |

| | | | | | | | | | | | | | | | | | | | | | | | 219,889 | | | | | | | | | |

| Equity-income funds 38% | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| The Income Fund of America, Class R-6 | | | 347,246 | | | | 36,268 | | | | 10,522 | | | | (701 | ) | | | (20,372 | ) | | | 351,919 | | | | 13,478 | | | | 12,351 | |

| Capital Income Builder, Class R-6 | | | 202,825 | | | | 11,935 | | | | 8,838 | | | | (495 | ) | | | (116 | ) | | | 205,311 | | | | 8,024 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | 557,230 | | | | | | | | | |

| Balanced funds 25% | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| American Balanced Fund, Class R-6 | | | 288,573 | | | | 9,915 | | | | 14,861 | | | | (1,002 | ) | | | 10,399 | | | | 293,024 | | | | 5,929 | | | | — | |

| American Funds Global Balanced Fund, Class R-6 | | | 71,968 | | | | 1,909 | | | | 4,296 | | | | (657 | ) | | | 4,464 | | | | 73,388 | | | | 1,516 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | 366,412 | | | | | | | | | |

| Fixed income funds 17% | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| American Funds Multi-Sector Income Fund, Class R-6 | | | 99,538 | | | | 13,000 | | | | 7,800 | | | | (385 | ) | | | (1,290 | ) | | | 103,063 | | | | 6,657 | | | | — | |

| American High-Income Trust, Class R-6 | | | 70,940 | | | | 8,762 | | | | 4,334 | | | | (152 | ) | | | (1,278 | ) | | | 73,938 | | | | 5,238 | | | | — | |

| American Funds Inflation Linked Bond Fund, Class R-6 | | | 70,188 | | | | 15,626 | | | | 6,511 | | | | (742 | ) | | | (5,511 | ) | | | 73,050 | | | | 4,572 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | 250,051 | | | | | | | | | |

| Total 100% | | | | | | | | | | | | | | $ | (8,238 | ) | | $ | 11,202 | | | $ | 1,466,615 | | | $ | 51,152 | | | $ | 14,429 | |

| | |

| 1 | Part of the same “group of investment companies” as the fund as defined under the Investment Company Act of 1940, as amended. |

Refer to the notes to financial statements.

| American Funds Retirement Income Portfolio Series | 13 |

| Financial statements | |

| | |

Statements of assets and liabilities

at October 31, 2023 | (dollars in thousands) |

| | | Conservative

Portfolio | | | Moderate

Portfolio | | | Enhanced

Portfolio | |

| Assets: | | | | | | | | | |

| Investment securities of affiliated issuers, at value | | $ | 1,149,507 | | | $ | 1,303,149 | | | $ | 1,466,615 | |

| Receivables for: | | | | | | | | | | | | |

| Sales of investments | | | 208 | | | | 708 | | | | — | |

| Sales of fund’s shares | | | 737 | | | | 260 | | | | 1,865 | |

| Dividends | | | 1,567 | | | | 1,228 | | | | 1,101 | |

| Total assets | | | 1,152,019 | | | | 1,305,345 | | | | 1,469,581 | |

| | | | | | | | | | | | | |

| Liabilities: | | | | | | | | | | | | |

| Payables for: | | | | | | | | | | | | |

| Purchases of investments | | | 1,567 | | | | 1,229 | | | | 2,510 | |

| Repurchases of fund’s shares | | | 945 | | | | 968 | | | | 456 | |

| Services provided by related parties | | | 286 | | | | 316 | | | | 352 | |

| Trustees’ deferred compensation | | | 8 | | | | 8 | | | | 8 | |

| Total liabilities | | | 2,806 | | | | 2,521 | | | | 3,326 | |

| Net assets at October 31, 2023 | | $ | 1,149,213 | | | $ | 1,302,824 | | | $ | 1,466,255 | |

| | | | | | | | | | | | | |

| Net assets consist of: | | | | | | | | | | | | |

| Capital paid in on shares of beneficial interest | | $ | 1,240,772 | | | $ | 1,359,898 | | | $ | 1,489,342 | |

| Total accumulated loss | | | (91,559 | ) | | | (57,074 | ) | | | (23,087 | ) |

| Net assets at October 31, 2023 | | $ | 1,149,213 | | | $ | 1,302,824 | | | $ | 1,466,255 | |

| | | | | | | | | | | | | |

| Investment securities of affiliated issuers, at cost | | $ | 1,215,988 | | | $ | 1,362,977 | | | $ | 1,493,173 | |

Refer to the notes to financial statements.

| 14 | American Funds Retirement Income Portfolio Series |

| Financial statements (continued) | |

| | |

Statements of assets and liabilities

at October 31, 2023 (continued) | (dollars and shares in thousands, except per-share amounts) |

| | | | | Conservative

Portfolio | | | Moderate

Portfolio | | | Enhanced

Portfolio | |

| Shares of beneficial interest issued and outstanding (no stated par value) — unlimited shares authorized | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Class A: | | Net assets | | $ | 830,046 | | | $ | 1,028,482 | | | $ | 1,112,601 | |

| | | Shares outstanding | | | 79,537 | | | | 94,732 | | | | 96,409 | |

| | | Net asset value per share | | $ | 10.44 | | | $ | 10.86 | | | $ | 11.54 | |

| Class C: | | Net assets | | $ | 110,624 | | | $ | 88,267 | | | $ | 75,488 | |

| | | Shares outstanding | | | 10,659 | | | | 8,171 | | | | 6,567 | |

| | | Net asset value per share | | $ | 10.38 | | | $ | 10.80 | | | $ | 11.49 | |

| Class T: | | Net assets | | $ | 10 | | | $ | 10 | | | $ | 11 | |

| | | Shares outstanding | | | 1 | | | | 1 | | | | 1 | |

| | | Net asset value per share | | $ | 10.45 | | | $ | 10.86 | | | $ | 11.55 | |

| Class F-1: | | Net assets | | $ | 20,542 | | | $ | 15,648 | | | $ | 17,161 | |

| | | Shares outstanding | | | 1,968 | | | | 1,441 | | | | 1,486 | |

| | | Net asset value per share | | $ | 10.44 | | | $ | 10.86 | | | $ | 11.55 | |

| Class F-2: | | Net assets | | $ | 117,416 | | | $ | 136,545 | | | $ | 205,526 | |

| | | Shares outstanding | | | 11,230 | | | | 12,554 | | | | 17,779 | |

| | | Net asset value per share | | $ | 10.46 | | | $ | 10.88 | | | $ | 11.56 | |

| Class F-3: | | Net assets | | $ | 20,613 | | | $ | 14,249 | | | $ | 29,802 | |

| | | Shares outstanding | | | 1,972 | | | | 1,312 | | | | 2,581 | |

| | | Net asset value per share | | $ | 10.45 | | | $ | 10.86 | | | $ | 11.55 | |

| Class R-1: | | Net assets | | $ | 1,437 | | | $ | 2,197 | | | $ | 1,204 | |

| | | Shares outstanding | | | 138 | | | | 203 | | | | 105 | |

| | | Net asset value per share | | $ | 10.41 | | | $ | 10.81 | | | $ | 11.53 | |

| Class R-2: | | Net assets | | $ | 1,606 | | | $ | 2,088 | | | $ | 4,243 | |

| | | Shares outstanding | | | 154 | | | | 193 | | | | 370 | |

| | | Net asset value per share | | $ | 10.42 | | | $ | 10.82 | | | $ | 11.47 | |

| Class R-2E: | | Net assets | | $ | 124 | | | $ | 64 | | | $ | 559 | |

| | | Shares outstanding | | | 12 | | | | 6 | | | | 48 | |

| | | Net asset value per share | | $ | 10.46 | | | $ | 10.88 | | | $ | 11.54 | |

| Class R-3: | | Net assets | | $ | 2,161 | | | $ | 4,505 | | | $ | 5,298 | |

| | | Shares outstanding | | | 207 | | | | 416 | | | | 460 | |

| | | Net asset value per share | | $ | 10.45 | | | $ | 10.84 | | | $ | 11.51 | |

| Class R-4: | | Net assets | | $ | 6,411 | | | $ | 2,000 | | | $ | 5,967 | |

| | | Shares outstanding | | | 609 | | | | 184 | | | | 517 | |

| | | Net asset value per share | | $ | 10.52 | | | $ | 10.85 | | | $ | 11.55 | |

| Class R-5E: | | Net assets | | $ | 417 | | | $ | 257 | | | $ | 1,140 | |

| | | Shares outstanding | | | 40 | | | | 24 | | | | 99 | |

| | | Net asset value per share | | $ | 10.52 | | | $ | 10.87 | | | $ | 11.55 | |

| Class R-5: | | Net assets | | $ | 353 | | | $ | 462 | | | $ | 12 | |

| | | Shares outstanding | | | 34 | | | | 42 | | | | 1 | |

| | | Net asset value per share | | $ | 10.46 | | | $ | 10.90 | | | $ | 11.57 | |

| Class R-6: | | Net assets | | $ | 37,453 | | | $ | 8,050 | | | $ | 7,243 | |

| | | Shares outstanding | | | 3,580 | | | | 740 | | | | 626 | |

| | | Net asset value per share | | $ | 10.46 | | | $ | 10.89 | | | $ | 11.57 | |

Refer to the notes to financial statements.

| American Funds Retirement Income Portfolio Series | 15 |

| Financial statements (continued) | |

| | |

Statements of operations

for the year ended October 31, 2023 | (dollars in thousands) |

| | | Conservative

Portfolio | | | Moderate

Portfolio | | | Enhanced

Portfolio | |

| Investment income: | | | | | | | | | |

| Income: | | | | | | | | | |

| Dividends from affiliated issuers | | $ | 48,808 | | | $ | 50,723 | | | $ | 51,152 | |

| | | | | | | | | | | | | |

| Fees and expenses*: | | | | | | | | | | | | |

| Distribution services | | | 3,611 | | | | 3,833 | | | | 3,859 | |

| Transfer agent services | | | 532 | | | | 476 | | | | 565 | |

| Reports to shareholders | | | 23 | | | | 24 | | | | 27 | |

| Registration statement and prospectus | | | 189 | | | | 199 | | | | 225 | |

| Trustees’ compensation | | | 5 | | | | 6 | | | | 6 | |

| Auditing and legal | | | 16 | | | | 18 | | | | 19 | |

| Custodian | | | 6 | | | | 6 | | | | 6 | |

| Other | | | 5 | | | | 5 | | | | 5 | |

| Total fees and expenses before reimbursement | | | 4,387 | | | | 4,567 | | | | 4,712 | |

| Less reimbursements of fees and expenses: | | | | | | | | | | | | |

| Transfer agent services reimbursement | | | — | | | | — | | | | — | † |

| Total fees and expenses after reimbursement | | | 4,387 | | | | 4,567 | | | | 4,712 | |

| Net investment income | | | 44,421 | | | | 46,156 | | | | 46,440 | |

| | | | | | | | | | | | |

| Net realized (loss) gain and unrealized (depreciation) appreciation: | | | | | | | | | | | | |

| Net realized loss on sale of investments in affiliated issuers | | | (36,166 | ) | | | (9,628 | ) | | | (8,238 | ) |

| Capital gain distributions received from affiliated issuers | | | 11,198 | | | | 13,392 | | | | 14,429 | |

| | | | (24,968 | ) | | | 3,764 | | | | 6,191 | |

| Net unrealized appreciation (depreciation) on investments in affiliated issuers | | | 376 | | | | (10,899 | ) | | | 11,202 | |

| Net realized (loss) gain and unrealized appreciation (depreciation) | | | (24,592 | ) | | | (7,135 | ) | | | 17,393 | |

| Net increase in net assets resulting from operations | | $ | 19,829 | | | $ | 39,021 | | | $ | 63,833 | |

| * | Additional information related to class-specific fees and expenses is included in the notes to financial statements. |

| † | Amount less than one thousand. |

Refer to the notes to financial statements.

| 16 | American Funds Retirement Income Portfolio Series |

| Financial statements (continued) | |

| | |

| Statements of changes in net assets | (dollars in thousands) |

| | | Conservative

Portfolio | | | Moderate

Portfolio | | | Enhanced

Portfolio | |

| | | Year ended October 31, | | | Year ended October 31, | | | Year ended October 31, | |

| | | 2023 | | | 2022 | | | 2023 | | | 2022 | | | 2023 | | | 2022 | |

| Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | $ | 44,421 | | | $ | 34,938 | | | $ | 46,156 | | | $ | 37,258 | | | $ | 46,440 | | | $ | 37,629 | |

| Net realized (loss) gain | | | (24,968 | ) | | | (554 | ) | | | 3,764 | | | | 27,114 | | | | 6,191 | | | | 40,355 | |

| Net unrealized appreciation (depreciation) | | | 376 | | | | (210,315 | ) | | | (10,899 | ) | | | (243,224 | ) | | | 11,202 | | | | (278,765 | ) |

| Net increase (decrease) in net assets resulting from operations | | | 19,829 | | | | (175,931 | ) | | | 39,021 | | | | (178,852 | ) | | | 63,833 | | | | (200,781 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Distributions paid to shareholders | | | (42,205 | ) | | | (49,295 | ) | | | (69,237 | ) | | | (56,690 | ) | | | (84,271 | ) | | | (69,644 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net capital share transactions | | | (122,545 | ) | | | 88,346 | | | | (1,823 | ) | | | 68,698 | | | | 47,214 | | | | 155,488 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Total (decrease) increase in net assets | | | (144,921 | ) | | | (136,880 | ) | | | (32,039 | ) | | | (166,844 | ) | | | 26,776 | | | | (114,937 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets: | | | | | | | | | | | | | | | | | | | | | | | | |

| Beginning of year | | | 1,294,134 | | | | 1,431,014 | | | | 1,334,863 | | | | 1,501,707 | | | | 1,439,479 | | | | 1,554,416 | |

| End of year | | $ | 1,149,213 | | | $ | 1,294,134 | | | $ | 1,302,824 | | | $ | 1,334,863 | | | $ | 1,466,255 | | | $ | 1,439,479 | |

Refer to the notes to financial statements.

| American Funds Retirement Income Portfolio Series | 17 |

Notes to financial statements

1. Organization

American Funds Retirement Income Portfolio Series (the “series”) is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end, diversified management investment company. The series consists of three funds (the “funds”). The assets of each fund are segregated, with each fund accounted for separately. The funds’ investment objectives are as follows:

| American Funds Conservative Portfolio | | Seeks current income, long-term growth of capital and conservation of capital, with an emphasis on income and conservation of capital. |

| American Funds Moderate Portfolio | | Seeks current income, long-term growth of capital and conservation of capital. |

| American Funds Enhanced Portfolio | | Seeks current income, long-term growth of capital and conservation of capital, with an emphasis on income and growth of capital. |

Each fund will attempt to achieve its investment objectives by investing in a mix of American Funds (the “underlying funds”) in different combinations and weightings. Capital Research and Management Company (“CRMC”), the series’ investment adviser, is also the investment adviser to the underlying funds.

Each fund in the series has 14 share classes consisting of six retail share classes (Classes A, C, T, F-1, F-2 and F-3) and eight retirement plan share classes (Classes R-1, R-2, R-2E, R-3, R-4, R-5E, R-5 and R-6). The eight retirement plan share classes are generally offered only through eligible employer-sponsored retirement plans. The funds’ share classes are described further in the following table:

| Share class | | Initial sales charge | | Contingent deferred sales charge

upon redemption | | Conversion feature |

| Class A | | Up to 5.75% | | None (except 1.00% for certain redemptions within 18 months of purchase without an initial sales charge) | | None |

| Class C | | None | | 1.00% for redemptions within one year of purchase | | Class C converts to Class A after eight years |

| Class T* | | Up to 2.50% | | None | | None |

| Classes F-1, F-2 and F-3 | | None | | None | | None |

Classes R-1, R-2, R-2E, R-3,

R-4, R-5E, R-5 and R-6 | | None | | None | | None |

| * | Class T shares of each fund are not available for purchase. |

Holders of all share classes of each fund have equal pro rata rights to the assets, dividends and liquidation proceeds of each fund held. Each share class of each fund has identical voting rights, except for the exclusive right to vote on matters affecting only its class. Share classes have different fees and expenses (“class-specific fees and expenses”), primarily due to different arrangements for distribution and transfer agent services. Differences in class-specific fees and expenses will result in differences in net investment income and, therefore, the payment of different per-share dividends by each share class of each fund.

2. Significant accounting policies

Each fund in the series is an investment company that applies the accounting and reporting guidance issued in Topic 946 by the U.S. Financial Accounting Standards Board. Each fund’s financial statements have been prepared to comply with U.S. generally accepted accounting principles (“U.S. GAAP”). These principles require the series’ investment adviser to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates. Subsequent events, if any, have been evaluated through the date of issuance in the preparation of the financial statements. The funds follow the significant accounting policies in this section, as well as the valuation policies described in the next section on valuation.

Security transactions and related investment income — Security transactions are recorded by the funds as of the date the trades are executed. Realized gains and losses from security transactions are determined based on the specific identified cost of the securities. Dividend income is recognized on the ex-dividend date.

| 18 | American Funds Retirement Income Portfolio Series |

Fees and expenses — The fees and expenses of the underlying funds are not included in the fees and expenses reported for each of the funds; however, they are indirectly reflected in the valuation of each of the underlying funds. These fees are included in the net effective expense ratios that are provided as supplementary information in the financial highlights tables.

Class allocations — Income, fees and expenses (other than class-specific fees and expenses), realized gains and losses and unrealized appreciation and depreciation are allocated daily among the various share classes of each fund based on their relative net assets. Class-specific fees and expenses, such as distribution and transfer agent services, are charged directly to the respective share class of each fund.

Distributions paid to shareholders — Income dividends and capital gain distributions are recorded on each fund’s ex-dividend date.

3. Valuation

Security valuation — The net asset value per share of each fund is calculated once daily as of the close of regular trading on the New York Stock Exchange, normally 4 p.m. New York time, each day the New York Stock Exchange is open. The net asset value of each share class of each fund is calculated based on the reported net asset values of the underlying funds in which each fund invests. The net asset value of each underlying fund is calculated based on the policies and procedures of the underlying fund contained in each underlying fund’s statement of additional information.

Processes and structure — The series’ board of trustees has designated the series’ investment adviser to make fair value determinations, subject to board oversight. The investment adviser has established a Joint Fair Valuation Committee (the “Committee”) to administer, implement and oversee the fair valuation process, and to make fair value decisions. The Committee regularly reviews its own fair value decisions, as well as decisions made under its standing instructions to the investment adviser’s valuation team. The Committee reviews changes in fair value measurements from period to period, pricing vendor information and market data, and may, as deemed appropriate, update the fair valuation guidelines to better reflect the results of back testing and address new or evolving issues. Pricing decisions, processes and controls over security valuation are also subject to additional internal reviews facilitated by the investment adviser’s global risk management group. The Committee reports changes to the fair valuation guidelines to the board of trustees. The series’ board and audit committee also regularly review reports that describe fair value determinations and methods.

Classifications — The series’ investment adviser classifies each fund’s assets and liabilities into three levels based on the method used to value the assets or liabilities. Level 1 values are based on quoted prices in active markets for identical securities. Level 2 values are based on significant observable market inputs, such as quoted prices for similar securities and quoted prices in inactive markets. Level 3 values are based on significant unobservable inputs that reflect the investment adviser’s determination of assumptions that market participants might reasonably use in valuing the securities. The valuation levels are not necessarily an indication of the risk or liquidity associated with the underlying investment. As of October 31, 2023, all of the investment securities held by each fund were classified as Level 1.

4. Risk factors

Investing in the funds may involve certain risks including, but not limited to, those described below.

Periodic withdrawal risks — There is no guarantee that any of the funds will provide adequate income through retirement. These funds are not designed to, and are not expected to, generate distributions that equal a fixed percentage of each fund’s current net asset value per share. An investor taking periodic withdrawals from any of the funds should not assume that the source of a distribution is dividend or interest income or capital gains; rather, all or a portion of a distribution from any of the funds may consist of a return of capital. A return of capital is a return of all or part of an investor’s original investment in each fund. Each fund’s ability to preserve capital while making periodic distributions to investors is subject to market conditions at the time an investor invests in each fund and during the length of time such investor holds shares of each fund. Even if each fund’s portfolio value grows over time, such growth may be insufficient to enable each fund to make periodic distributions to investors without returning capital to shareholders. Payments consisting of return of capital will result in a decrease in an investor’s fund share balance. Higher rates of withdrawal and withdrawals during declining markets may result in a more rapid decrease in an investor’s fund share balance. Persistent returns of capital could ultimately result in a zero account balance.

Additionally, as periodic withdrawals by investors will be made from each fund’s assets and investors are generally not expected to reinvest such distributions in additional fund shares, distributions to investors will reduce the amount of assets available for investment by each fund. Each fund may suffer substantial investment losses and simultaneously experience additional asset reductions as a result of its distributions to shareholders.

| American Funds Retirement Income Portfolio Series | 19 |

Allocation risk — Investments in each fund are subject to risks related to the investment adviser’s allocation choices. The selection of the underlying funds and the allocation of each fund’s assets could cause the funds to lose value or their results to lag relevant benchmarks or other funds with similar objectives.

Fund structure — Each fund invests in underlying funds and incurs expenses related to the underlying funds. In addition, investors in each fund will incur fees to pay for certain expenses related to the operations of the fund. An investor holding the underlying funds directly and in the same proportions as each fund would incur lower overall expenses but would not receive the benefit of the portfolio management and other services provided by each fund. Additionally, in accordance with an exemption under the Investment Company Act of 1940, as amended, the investment adviser considers only proprietary funds when selecting underlying investment options and allocations. This means that each fund’s investment adviser does not, nor does it expect to, consider any unaffiliated funds as underlying investment options for the funds. This strategy could raise certain conflicts of interest when determining the overall asset allocation of the fund or choosing underlying investments for the fund, including the selection of funds that result in greater compensation to the adviser or funds with relatively lower historical investment results. The investment adviser has policies and procedures designed to mitigate material conflicts of interest that may arise in connection with its management of each fund.

Underlying fund risks — Because each fund’s investments consist of underlying funds, each fund’s risks are directly related to the risks of the underlying funds. For this reason, it is important to understand the risks associated with investing in the underlying funds, as described below.

Market conditions — The prices of, and the income generated by, the common stocks, bonds and other securities held by the underlying funds may decline — sometimes rapidly or unpredictably — due to various factors, including events or conditions affecting the general economy or particular industries or companies; overall market changes; local, regional or global political, social or economic instability; governmental, governmental agency or central bank responses to economic conditions; changes in inflation rates; and currency exchange rate, interest rate and commodity price fluctuations.

Economies and financial markets throughout the world are highly interconnected. Economic, financial or political events, trading and tariff arrangements, wars, terrorism, cybersecurity events, natural disasters, public health emergencies (such as the spread of infectious disease), bank failures and other circumstances in one country or region, including actions taken by governmental or quasi-governmental authorities in response to any of the foregoing, could have impacts on global economies or markets. As a result, whether or not the underlying funds invest in securities of issuers located in or with significant exposure to the countries affected, the value and liquidity of the underlying funds’ investments may be negatively affected by developments in other countries and regions.

Issuer risks — The prices of, and the income generated by, securities held by the underlying funds may decline in response to various factors directly related to the issuers of such securities, including reduced demand for an issuer’s goods or services, poor management performance, major litigation, investigations or other controversies related to the issuer, changes in the issuer’s financial condition or credit rating, changes in government regulations affecting the issuer or its competitive environment and strategic initiatives such as mergers, acquisitions or dispositions and the market response to any such initiatives. An individual security may also be affected by factors relating to the industry or sector of the issuer or the securities markets as a whole, and conversely an industry or sector or the securities markets may be affected by a change in financial condition or other event affecting a single issuer.

Investing in debt instruments — The prices of, and the income generated by, bonds and other debt securities held by an underlying fund may be affected by factors such as the interest rates, maturities and credit quality of these securities.

Rising interest rates will generally cause the prices of bonds and other debt securities to fall. Also, when interest rates rise, issuers of debt securities which may be prepaid at any time, such as mortgage- or other asset-backed securities, are less likely to refinance existing debt securities, causing the average life of such securities to extend. A general change in interest rates may cause investors to sell debt securities on a large scale, which could also adversely affect the price and liquidity of debt securities and could also result in increased redemptions from the fund. Falling interest rates may cause an issuer to redeem, call or refinance a debt security before its stated maturity, which may result in the fund having to reinvest the proceeds in lower yielding securities. Longer maturity debt securities generally have greater sensitivity to changes in interest rates and may be subject to greater price fluctuations than shorter maturity debt securities.

| 20 | American Funds Retirement Income Portfolio Series |

Bonds and other debt securities are also subject to credit risk, which is the possibility that the credit strength of an issuer or guarantor will weaken or be perceived to be weaker, and/or an issuer of a debt security will fail to make timely payments of principal or interest and the security will go into default. Changes in actual or perceived creditworthiness may occur quickly. A downgrade or default affecting any of the underlying funds’ securities could cause the value of the underlying funds’ shares to decrease. Credit risk is gauged, in part, by the credit ratings of the debt securities in which the underlying fund invests. However, ratings are only the opinions of the rating agencies issuing them and are not guarantees as to credit quality or an evaluation of market risk. The underlying funds’ investment adviser relies on its own credit analysts to research issuers and issues in assessing credit and default risks.

Investing in securities backed by the U.S. government — Securities backed by the U.S. Treasury or the full faith and credit of the U.S. government are guaranteed only as to the timely payment of interest and principal when held to maturity. Accordingly, the current market values for these securities will fluctuate with changes in interest rates and the credit rating of the U.S. government. Notwithstanding that these securities are backed by the full faith and credit of the U.S. government, circumstances could arise that would prevent or delay the payment of interest or principal on these securities, which could adversely affect their value and cause the fund to suffer losses. Such an event could lead to significant disruptions in U.S. and global markets. Securities issued by U.S. government-sponsored entities and federal agencies and instrumentalities that are not backed by the full faith and credit of the U.S. government are neither issued nor guaranteed by the U.S. government. U.S. government securities are subject to market risk, interest rate risk and credit risk.

Investing in mortgage-related and other asset-backed securities — Mortgage-related securities, such as mortgage-backed securities, and other asset-backed securities, include debt obligations that represent interests in pools of mortgages or other income-bearing assets, such as consumer loans or receivables. While such securities are subject to the risks associated with investments in debt instruments generally (for example, credit, extension and interest rate risks), they are also subject to other and different risks. Mortgage-backed and other asset-backed securities are subject to changes in the payment patterns of borrowers of the underlying debt, potentially increasing the volatility of the securities and an underlying fund’s net asset value. When interest rates fall, borrowers are more likely to refinance or prepay their debt before its stated maturity. This may result in an underlying fund having to reinvest the proceeds in lower yielding securities, effectively reducing the underlying fund’s income. Conversely, if interest rates rise and borrowers repay their debt more slowly than expected, the time in which the mortgage-backed and other asset-backed securities are paid off could be extended, reducing an underlying fund’s cash available for reinvestment in higher yielding securities. Mortgage-backed securities are also subject to the risk that underlying borrowers will be unable to meet their obligations and the value of property that secures the mortgages may decline in value and be insufficient, upon foreclosure, to repay the associated loans. Investments in asset-backed securities are subject to similar risks.

Investing in inflation-linked bonds — The values of inflation-linked bonds generally fluctuate in response to changes in real interest rates — i.e., rates of interest after factoring in inflation. A rise in real interest rates may cause the prices of inflation-linked securities to fall, while a decline in real interest rates may cause the prices to increase. Inflation-linked bonds may experience greater losses than other debt securities with similar durations when real interest rates rise faster than nominal interest rates. There can be no assurance that the value of an inflation-linked security will be directly correlated to changes in interest rates; for example, if interest rates rise for reasons other than inflation, the increase may not be reflected in the security’s inflation measure.

Investing in inflation-linked bonds may also reduce an underlying fund’s distributable income during periods of deflation. If prices for goods and services decline throughout the economy, the principal and income on inflation-linked securities may decline and result in losses to the underlying fund.

Interest rate risk — The values and liquidity of the securities held by the underlying fund may be affected by changing interest rates. For example, the values of these securities may decline when interest rates rise and increase when interest rates fall. Longer maturity debt securities generally have greater sensitivity to changes in interest rates and may be subject to greater price fluctuations than shorter maturity debt securities. The underlying fund may invest in variable and floating rate securities. When the underlying fund holds variable or floating rate securities, a decrease in market interest rates will adversely affect the income received from such securities and the net asset value of the fund’s shares. Although the values of such securities are generally less sensitive to interest rate changes than those of other debt securities, the value of variable and floating rate securities may decline if their interest rates do not rise as quickly, or as much, as market interest rates. Conversely, floating rate securities will not generally increase in value if interest rates decline. During periods of extremely low short-term interest rates, the underlying fund may not be able to maintain a positive yield and, in relatively low interest rate environments, there are heightened risks associated with rising interest rates.

| American Funds Retirement Income Portfolio Series | 21 |

Liquidity risk — Certain underlying fund holdings may be or may become difficult or impossible to sell, particularly during times of market turmoil. Liquidity may be impacted by the lack of an active market for a holding, legal or contractual restrictions on resale, or the reduced number and capacity of market participants to make a market in such holding. Market prices for less liquid or illiquid holdings may be volatile or difficult to determine, and reduced liquidity may have an adverse impact on the market price of such holdings. Additionally, the sale of less liquid or illiquid holdings may involve substantial delays (including delays in settlement) and additional costs and the underlying fund may be unable to sell such holdings when necessary to meet its liquidity needs or to try to limit losses, or may be forced to sell at a loss.

Investing in derivatives— The use of derivatives involves a variety of risks, which may be different from, or greater than, the risks associated with investing in traditional securities, such as stocks and bonds. Changes in the value of a derivative may not correlate perfectly with, and may be more sensitive to market events than, the underlying asset, rate or index, and a derivative instrument may cause the underlying fund to lose significantly more than its initial investment. Derivatives may be difficult to value, difficult for the underlying fund to buy or sell at an opportune time or price and difficult, or even impossible, to terminate or otherwise offset. The underlying fund’s use of derivatives may result in losses to the underlying fund, and investing in derivatives may reduce the underlying fund’s returns and increase the underlying fund’s price volatility. The underlying fund’s counterparty to a derivative transaction (including, if applicable, the underlying fund’s clearing broker, the derivatives exchange or the clearinghouse) may be unable or unwilling to honor its financial obligations in respect of the transaction. In certain cases, the underlying fund may be hindered or delayed in exercising remedies against or closing out derivative instruments with a counterparty, which may result in additional losses. Derivatives are also subject to operational risk (such as documentation issues, settlement issues and systems failures) and legal risk (such as insufficient documentation, insufficient capacity or authority of a counterparty, and issues with the legality or enforceability of a contract).

Investing in stocks — Investing in stocks may involve larger price swings and greater potential for loss than other types of investments. As a result, the value of the underlying funds may be subject to sharp declines in value. Income provided by an underlying fund may be reduced by changes in the dividend policies of, and the capital resources available at, the companies in which the underlying fund invests. These risks may be even greater in the case of smaller capitalization stocks.