On or about April 13, 2022, claimants, investors in Funds managed by GPB Capital Holdings, LLC, commenced an arbitration with the American Arbitration Association against GPB Capital Holdings, LLC, GPB Automotive Portfolio, LP, GPB Holdings II, LP, GPB Cold Storage, LP, GPB Holdings, LP, GPB Holdings II, LP, GPB Holdings Qualified, LP, GPB Holdings III, LP, GPB NYC Development, LP, and GPB Waste Management, LP, along with other non-GPB parties. All claimants were customers of Concorde Investment Services, LLC (“Concorde”), and each purchased his or her limited partnership interest in a GPB-managed Fund through Concorde. Claimants asserted claims based on fraud, breach of fiduciary duty, breach of contract, among others, and claimed to have suffered millions of dollars in damages.

GPB contended that the arbitration was improperly filed, and as such commenced a proceeding in New York State Supreme Court (GPB Capital Holdings, LLC et al. v. Tom Alberto et al., Index No. 656432/2022), solely for the purpose of seeking a stay of the arbitration. In July 2022, following the Court’s entry of an Order temporarily staying the arbitration, the parties stipulated and agreed to the entry of a court order entering judgment for GPB and the other petitioners. The arbitration will be permanently stayed upon the Court so-ordering the parties stipulation. In a letter dated December 20, 2022, the American Arbitration Association informed the parties to the arbitration that, as of December 20, 2022, the arbitration was closed.

Michael Peirce, derivatively on behalf of GPB Automotive Portfolio, LP v. GPB Capital Holdings, LLC, Ascendant Capital, LLC, Ascendant Alternative Strategies, LLC, Axiom Capital Management, Inc., Steven Frangioni, David Gentile, William Jacoby, Minchung Kgil, Mark D. Martino and Jeffry Schneider, -and- GPB Automotive Portfolio, LP, Nominal Defendant (New York Supreme Court, New York County, Case No. 652858/2020)

In July 2020, plaintiff filed a derivative action in New York Supreme Court against GPB, Ascendant, AAS, Axiom, Steve Frangioni, David Gentile, William Jacoby, Minchung Kgil, Mark Martino, and Jeffry Schneider. The Complaint alleges various breaches of fiduciary duty and/or aiding and abetting the breaches of fiduciary duty against all defendants, breach of contract against GPB, unjust enrichment, and an equitable accounting. Plaintiffs are seeking declaratory relief, disgorgement, restitution, an equitable accounting, and unspecified damages. Any potential losses associated with this matter cannot be estimated at this time.

Alfredo J. Martinez, et al. v. GPB Capital Holdings, LLC (Delaware Chancery Court, Case No. 2019-1005)

In December 2019, plaintiffs filed a civil action in Delaware Court of Chancery to compel inspection books and records from GPB, as General Partner, and from the Partnership, GPB Holdings I, GPB Automotive Portfolio, LP, and GPB Waste Management. In June 2020, the court dismissed plaintiffs’ books and records request, but allowed a contract claim for specific performance to proceed as a plenary action. The plaintiffs are seeking unspecified damages and penalties. Any potential losses associated with this matter cannot be estimated at this time.

Alfredo J. Martinez and HighTower Advisors v. GPB Capital Holdings, LLC, et al. (Delaware Chancery Court, Case No. 2020-0545)

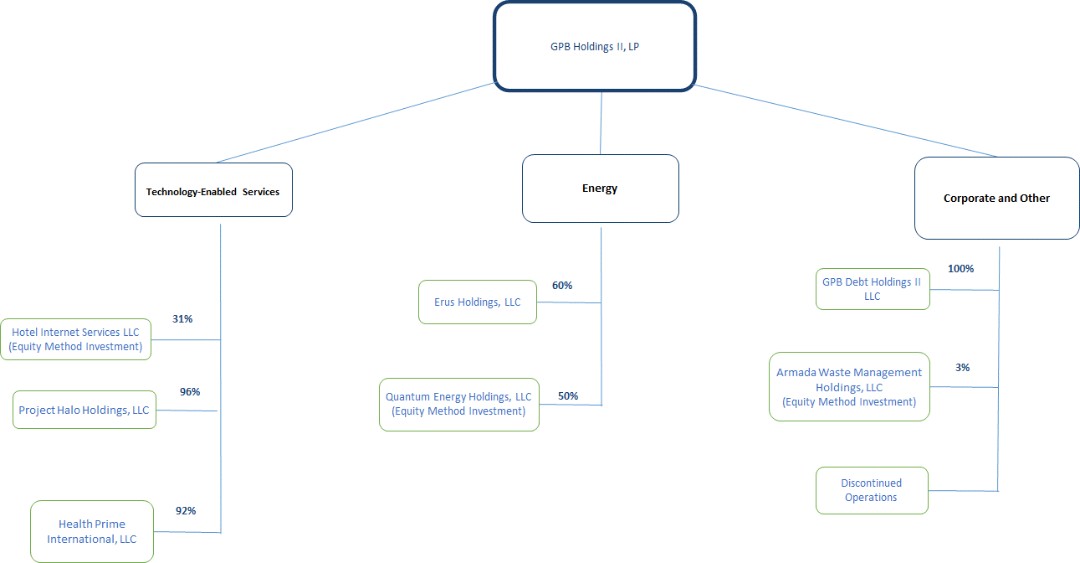

In July 2020, plaintiff filed a complaint against GPB, Armada Waste Management GP, LLC, Armada Waste Management, LP, the Partnership, GPB Automotive Portfolio, LP, and GPB Holdings, LP in the Delaware Court of Chancery to compel inspection of GPB’s books and records based upon specious and unsubstantiated allegations regarding alleged fraudulent activity, mismanagement, and breaches of fiduciary duty. The plaintiffs are seeking an order compelling GPB to permit inspection of documents related to Armada Waste, as well as for costs and fees. Any potential losses associated with this matter cannot be estimated at this time.

Lance Cotten, Alex Vavas and Eric Molbegat v. GPB Capital Holdings, LLC, Automile Holdings LLC D/B/A Prime Automotive Group, David Gentile, David Rosenberg, Philip Delzotta, Joseph Delzotta, and any other related entities (New York Supreme Court, Nassau County, Case No. 604943/2020)

In May 2020, plaintiffs filed a civil action in New York Supreme Court, Nassau County, against GPB, Automile Holdings LLC d/b/a Prime Automotive Group, David Gentile, David Rosenberg, Philip Delzotta, Joseph Delzotta, and other related entities. The complaint alleges that defendants engaged in systematic fraudulent and discriminatory schemes against customers and engaged in retaliatory actions against plaintiffs, who were employed by Garden City Nissan from August until October 2019. The plaintiffs are seeking damages pursuant to New York Labor Law Section 740, which provides for compensation for lost wages, benefits, and other remuneration, and liquidated damages for alleged violations of Executive Law Section 296. No costs associated with the resolution of this matter are expected to be charged to the Partnership.