FIRST QUARTER ENDED MARCH 31, 2018

MANAGEMENT’S

DISCUSSION AND ANALYSIS

May 15, 2018

|

| | | |

| Table of Contents | | | |

| | 1 | Management's Discussion and Analysis | |

| | 2 | Business Overview and Segments | |

| | 3 | Recent Events | |

| | 4 | Results of Operations | |

| | 5 | Segment Performance | |

| | 6 | Corporate and Other Costs | |

| | 7 | Selected Quarterly Financial Information | |

| | 8 | Balance Sheet Analysis | |

| | 9 | Liquidity and Capital Realignment | |

| | 10 | Lending Arrangements and Debt | |

| | 11 | Contractual Obligations | |

| | 12 | Related Party Transactions | |

| | 13 | Non-IFRS Financial Measures | |

| | 14 | Critical Accounting Estimates | |

| | 15 | Contingencies | |

| | 16 | Outstanding Share Data | |

| | 17 | Control Environment | |

| | 18 | Forward-looking Statements | |

1 Management Discussion and Analysis

The following Management’s Discussion and Analysis ("MD&A") summarizes Concordia International Corp.’s ("Concordia" or the "Company", or "we" or "us" or "our") consolidated operating results and cash flows for the three month period ended March 31, 2018 with a comparative prior period, and the Company’s balance sheet as at March 31, 2018 with a comparative period to December 31, 2017. The MD&A was prepared as of May 15, 2018 and should be read in conjunction with the unaudited condensed interim consolidated financial statements and the notes thereto as at and for the three month period ended March 31, 2018 and the consolidated financial statements and Management's Discussion and Analysis for the year ended December 31, 2017. Financial information in this MD&A is based on financial statements that have been prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board ("IASB") and amounts are stated in thousands of United States Dollars ("USD"), which is the reporting currency of the Company, unless otherwise noted. The significant exchange rates used in the translation to the reporting currency are:

|

| | |

| | US$ per Great British pound (£) |

| As at, and for the periods ended | Spot | Average |

| January 1, 2016 to March 31, 2016 | 1.4395 | 1.4321 |

| April 1, 2016 to June 30, 2016 | 1.3395 | 1.4354 |

| July 1, 2016 to September 30, 2016 | 1.3008 | 1.3136 |

| October 1, 2016 to December 31, 2016 | 1.2305 | 1.2438 |

| January 1, 2017 to March 31, 2017 | 1.2489 | 1.2387 |

| April 1, 2017 to June 30, 2017 | 1.3004 | 1.2781 |

| July 1, 2017 to September 30, 2017 | 1.3402 | 1.3088 |

| October 1, 2017 to December 31, 2017 | 1.3494 | 1.3276 |

| January 1, 2018 to March 31, 2018 | 1.4037 | 1.3910 |

Certain prior period financial information has been presented to conform to the current period presentation.

Some of the statements contained in this MD&A constitute forward-looking information within the meaning of applicable Canadian securities legislation and forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995 (collectively, "forward-looking statements"), which are based upon the current internal expectations, estimates, projections, assumptions and beliefs of the Company's management ("Management"). Refer to the "Forward-Looking Statements" section of this MD&A for a discussion of certain risks, uncertainties, and assumptions relating to forward-looking statements. Additional information relating to the Company, including the Company’s Annual Report on Form 20-F, is available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov. The results of operations, business prospects and financial condition of Concordia will be affected by, among other things, the "Risk Factors" set out in Concordia’s Annual Report on Form 20-F dated March 8, 2018 and other documents filed with the Canadian Securities Administrators and the United States Securities and Exchange Commission, available on SEDAR at www.sedar.com and EDGAR at www.sec.gov.

Certain measures used in this MD&A do not have any standardized meaning under IFRS. When used, these measures are defined in such terms as to allow the reconciliation to the closest IFRS measure. See "Results of Operations", "Segment Performance", "Selected Quarterly Financial Information", and "Non-IFRS Financial Measures".

|

| |

| Concordia Management's Discussion and Analysis | Page 2 |

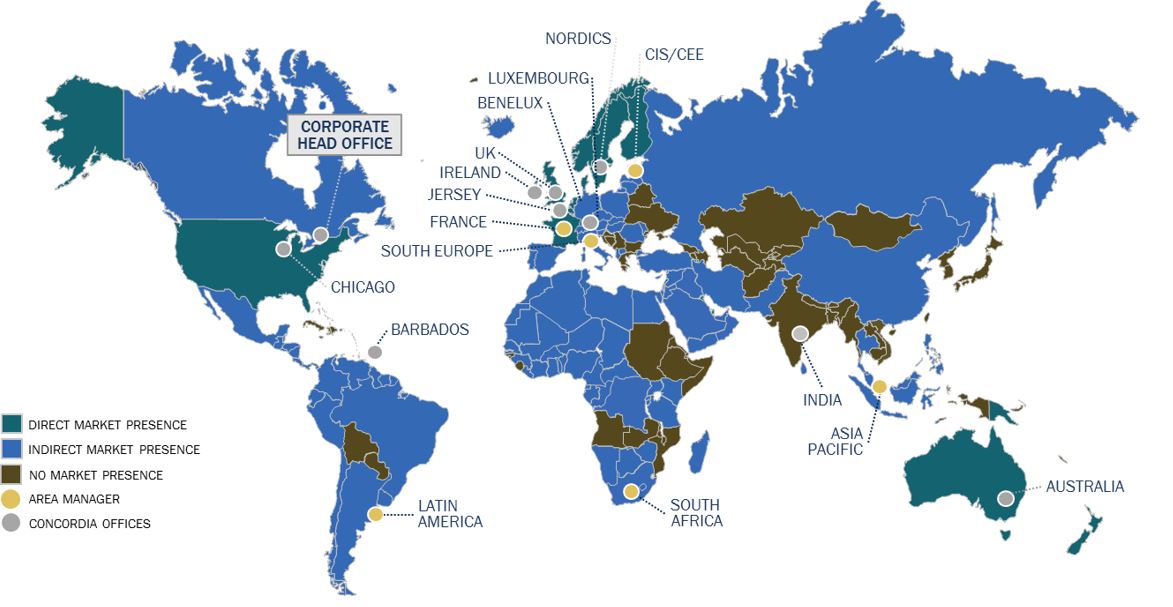

2 Business Overview and Segments

Concordia is an international specialty pharmaceutical company, owning or licensing, through its subsidiaries, a diversified portfolio of branded and generic prescription products. The Company has two reporting segments, which consist of Concordia International and Concordia North America, in addition to its Corporate cost centre.

* In above, “CIS” means the Commonwealth of Independent States and “CEE” means Central and Eastern Europe.

The registered and head office of the Company is located at 277 Lakeshore Rd. East, Suite 302, Oakville, Ontario, L6J 1H9. The Company’s records office is located at 333 Bay St., Suite 2400, Toronto, Ontario, M56 2T6. The Company’s common shares are listed on the Toronto Stock Exchange under the symbol "CXR" and on the NASDAQ under the symbol "CXRX".

Concordia International

The Concordia International segment consists of a diversified portfolio of branded and generic products that are sold to wholesalers, hospitals and pharmacies in over 90 countries. The Concordia International segment specializes in the acquisition, licensing and development of off-patent prescription medicines, which may be niche, hard to make products. The segment’s over 200 products are manufactured and sold through an out-sourced manufacturing network and marketed internationally through a combination of direct sales and local distribution relationships. The Concordia International segment operates primarily outside of the North American marketplace.

Concordia North America

The Concordia North America segment has a diversified product portfolio that focuses primarily on the United States pharmaceutical market. These products include, but are not limited to, Donnatal® for the treatment of irritable bowel syndrome; Zonegran® for the treatment of partial seizures in adults with epilepsy; Nilandron® for the treatment of metastatic prostate cancer; Lanoxin® for the treatment of mild to moderate heart failure and atrial fibrillation; Plaquenil® for the treatment of lupus and rheumatoid arthritis; and Photofrin® for the treatment of certain types of cancer. Concordia North America’s product portfolio consists of branded products and authorized generic contracts. The segment’s products are manufactured through an out-sourced production network and sold primarily through a third party distribution network in the United States.

Corporate

The Corporate cost centre represents certain centralized costs including costs associated with the Company's head office and senior management located in Canada and costs associated with being a public reporting entity.

|

| |

| Concordia Management's Discussion and Analysis | Page 3 |

3 Recent Events

Canada Business Corporations Act (the "CBCA") Proceedings

On October 20, 2017, the Company announced that it and one of its wholly-owned subsidiaries commenced a court proceeding under the CBCA.

On May 2, 2018, the Company announced a proposed transaction to realign its capital structure (the “Recapitalization Transaction”).

The proposed Recapitalization Transaction would raise new equity capital of $586.5 million, and to reduce the Company’s total outstanding debt by approximately $2.4 billion.

In connection with the proposed Recapitalization Transaction, the Company entered into a support agreement (the “Support Agreement”) with certain holders of the Company’s existing secured debt (the “Secured Debt”) and certain holders of the Company’s existing unsecured debt (the “Unsecured Debt”) that are subject to confidentiality agreements with Concordia and which hold in the aggregate approximately $1.6 billion in principal amount, or approximately 72%, of the Company’s Secured Debt and approximately $1.0 billion in principal amount, or approximately 64% of the Company’s Unsecured Debt (the “Initial Consenting Debtholders”). The Initial Consenting Debtholders are comprised of an ad hoc committee of holders of Secured Debt and an ad hoc committee of holders of Unsecured Debt. Pursuant to the Support Agreement, the Initial Consenting Debtholders have, among other things, agreed to support the Recapitalization Transaction and vote in favour of the plan of arrangement (the “CBCA Plan”) in Concordia’s previously announced proceedings (the "CBCA Proceedings") under the CBCA pursuant to which the Recapitalization Transaction is expected to be implemented.

In addition, on May 2, 2018 Concordia obtained an interim order (the “Interim Order”) issued by the Ontario Superior Court of Justice (the "Court") in the CBCA Proceedings authorizing, among other things, the holding of the following meetings (the “Meetings”) scheduled for June 19, 2018: (i) a meeting of holders of the Secured Debt (the “Secured Debtholders”); (ii) a meeting of holders of the Unsecured Debt (the “Unsecured Debtholders”); and (iii) a meeting (the "Shareholders' Meeting") of holders of the Company’s common shares (the “Shareholders”), in each case to consider and vote upon, among other things, the CBCA Plan to implement the Recapitalization Transaction.

Certain Key Recapitalization Transaction Terms

The Recapitalization Transaction contemplates the following key terms and conditions:

Secured Debt

| |

| • | The Company’s Secured Debt in the aggregate principal amount of approximately $2.2 billion, plus accrued and unpaid interest, will be exchanged for (i) cash in an amount equal to any outstanding accrued and unpaid interest (at contractual non-default rates) in respect of the Secured Debt, (ii) cash in the amount of $500 million (the “Secured Creditor Cash Pool”), (iii) any Additional Cash Amount (as defined below) and (iv) new secured debt (the “New Secured Debt”) comprised of new senior secured term loans (“New Senior Secured Term Loans”) and new senior secured notes (“New Senior Secured Notes”). The Company expects the aggregate principal amount of the New Secured Debt to be issued to Secured Debtholders pursuant to the Recapitalization Transaction to be approximately $1.4 billion; |

| |

| • | Each Secured Debtholder will receive its pro rata share of the New Secured Debt, in the form of either New Senior Secured Term Loans or New Senior Secured Notes depending on the type of Secured Debt held by such Secured Debtholder, subject to (i) holders of the Company’s existing secured term loans as of the record date of May 9, 2018 (the “Record Date”) having the right to elect to receive their New Secured Debt in the form of New Senior Secured Notes, provided that any such elections may be subject to certain re-allocations pursuant to the terms of the Recapitalization Transaction, and (ii) Secured Debtholders receiving New Senior Secured Term Loans having the right to elect to receive their New Senior Secured Term Loans denominated in USD or Euros, provided that any such elections may be subject to certain re-allocations pursuant to the terms of the Recapitalization Transaction; |

| |

| • | Secured Debtholders as of the Record Date who vote in favour of the CBCA Plan on or prior to the early consent date of June 6, 2018 (the “Early Consent Date”), as it may be extended by Concordia (the “Early Consenting Secured Debtholders”) will be entitled to receive on implementation of the Recapitalization Transaction pursuant to the CBCA Plan early consent consideration in the form of cash equal to 5% of the principal amount of Secured Debt owing to such Early Consenting Secured Debtholder as of the Record Date and voted in favour of the CBCA Plan (the “Secured Debtholder Early Consent Cash Consideration”) as additional consideration in exchange for their Secured Debt; |

| |

| • | If the aggregate amount of Secured Debtholder Early Consent Cash Consideration that becomes payable pursuant to the Recapitalization Transaction is less than $100 million, then an amount equal to the difference between $100 million and the amount of Secured Debtholder Early Consent Cash Consideration that becomes payable (the “Additional Cash Amount”) will be paid on a pro rata basis to each Secured Debtholder as additional consideration in exchange for their Secured Debt; and |

| |

| • | The final principal amount of New Secured Debt to be issued pursuant to the Recapitalization Transaction shall be in such amount that results in the aggregate consideration payable to Secured Debtholders pursuant to the Recapitalization Transaction by way of the Secured Creditor Cash Pool, the New Secured Debt and the Secured Debtholder Early Consent Cash Consideration (but not including the payment of accrued and unpaid interest or the Additional Cash Amount) being equal to 93.3835% of the principal amount of Secured Debt owing to such Secured Debtholders if such Secured Debtholders are Early Consenting Secured Debtholders, |

|

| |

| Concordia Management's Discussion and Analysis | Page 4 |

and approximately 88.3835% of the principal amount of Secured Debt owing to such Secured Debtholders if such Secured Debtholders are not Early Consenting Secured Debtholders.

Unsecured Debt

| |

| • | The Company’s Unsecured Debt in the aggregate principal amount of approximately $1.6 billion, plus accrued and unpaid interest, will be exchanged for (i) new common shares of Concordia representing approximately 8% of the outstanding common shares of Concordia immediately following the implementation of the Recapitalization Transaction (the “Unsecured Debt Exchange Shares”) and (ii) any Reallocated Unsecured Shares (as defined below); |

| |

| • | Unsecured Debtholders as of the Record Date who vote in favour of the CBCA Plan on or prior to the Early Consent Date, as it may be extended by Concordia (the “Early Consenting Unsecured Debtholders”) will be entitled to receive on implementation of the Recapitalization Transaction pursuant to the CBCA Plan early consent consideration in the form of new common shares of Concordia equal to their pro rata share (calculated based on the principal amount of Unsecured Debt held by such Early Consenting Unsecured Debtholders as at the Record Date and voted in favour of the CBCA Plan, divided by the aggregate principal amount of Unsecured Debt outstanding as at the Record Date) of a pool of common shares (the “Unsecured Early Consent Share Pool”) representing approximately 4% of the outstanding common shares of Concordia immediately following implementation of the Recapitalization Transaction pursuant to the CBCA Plan (the “Unsecured Debtholder Early Consent Shares”) as additional consideration in exchange for their Unsecured Debt; and |

| |

| • | If less than 100% of Unsecured Debt is voted in favour of the CBCA Plan by Early Consenting Unsecured Debtholders, any shares remaining in the Unsecured Early Consent Share Pool not issued as Unsecured Debtholder Early Consent Shares (the “Reallocated Unsecured Shares”) will be issued to all holders of Unsecured Debt on a pro rata basis as additional consideration for their Unsecured Debt. |

Private Placement

| |

| • | Approximately $586.5 million (the “Total Offering Size”) in cash will be invested to acquire new common shares of Concordia representing in the aggregate approximately 88% of the outstanding common shares of Concordia immediately following the implementation of the Recapitalization Transaction (the “Private Placement Shares”) by certain parties who executed a subscription agreement with the Company (the “Subscription Agreement”) concurrently with the execution of the Support Agreement (the “Private Placement Parties”) pursuant to a private placement (the “Private Placement”); |

| |

| • | The proceeds of the Private Placement will be used towards paying the Secured Creditor Cash Pool and the Secured Debtholder Early Consent Cash Consideration to be paid as part of the consideration for the exchange of the Secured Debt; |

| |

| • | Each of the Private Placement Parties will be entitled to receive its pro rata share (based on its subscription commitment) of cash consideration in the aggregate amount of $44 million (subject to any corresponding adjustments to the extent the Total Offering Size is reduced pursuant to the terms of the Subscription Agreement) (the “Private Placement Consideration”), which is payable on the terms set out in the Subscription Agreement, including on completion of the Recapitalization Transaction and certain earlier events; and |

| |

| • | Pursuant to the Subscription Agreement, the Private Placement Parties and the Company expect to agree on certain governance terms and registration rights. The governance terms will be described in more detail in the Company’s management information circular to be mailed to Secured Debtholders, Unsecured Debtholders and Shareholders in connection with the various Meetings to be held to approve the CBCA Plan. |

Existing Shares and Equity Claims

| |

| • | Upon completion of the Recapitalization Transaction, existing Shareholders will retain their existing common shares of Concordia, subject to a share consolidation of one common share in exchange for 300 existing common shares to be implemented as part of the Recapitalization Transaction and the dilution resulting from the issuance of common shares pursuant to the Recapitalization Transaction, such that the existing Shareholders will own approximately 0.35% of the outstanding common shares of Concordia immediately following implementation of the Recapitalization Transaction; and |

| |

| • | All other equity interests in Concordia, including all options, warrants, rights or similar instruments, will be cancelled on implementation of the Recapitalization Transaction pursuant to the CBCA Plan, and all equity claims, other than existing equity class action claims against Concordia (the “Existing Equity Class Action Claims”), will be released pursuant to the CBCA Plan, provided that any recovery in respect of any Existing Equity Class Action Claims will be limited to recovery as against any applicable insurance policies maintained by the Company. |

Share Dilution

| |

| • | The existing common shares retained by the Shareholders upon implementation of the Recapitalization Transaction and the common shares to be issued under the CBCA Plan, including the Unsecured Debt Exchange Shares, the Reallocated Unsecured Shares, the Unsecured Debtholder Early Consent Shares and the Private Placement Shares, shall be subject to dilution following the completion of the Recapitalization Transaction pursuant to the issuance of any new common shares under the management equity incentive plan to be adopted pursuant to the Recapitalization Transaction. |

|

| |

| Concordia Management's Discussion and Analysis | Page 5 |

Subject to the satisfaction or waiver of applicable conditions, the Recapitalization Transaction is expected to be completed by July 31, 2018.

In connection with the Recapitalization Transaction, it is anticipated that Concordia will continue from the Business Corporations Act (Ontario) to the CBCA.

Alternative Implementation Process

The Recapitalization Transaction is being implemented pursuant to the CBCA Plan. The Company is also soliciting votes to advance the Recapitalization Transaction pursuant to insolvency proceedings under Chapter 11 of the United States Bankruptcy Code (a “Chapter 11 Process”), contemporaneously with soliciting votes in respect of the CBCA Plan. Concordia currently intends to complete and implement the CBCA Plan pursuant to the CBCA Proceedings. Contemporaneous solicitation of votes in respect of a Chapter 11 Process ensures that the Company has the future ability to also complete the Recapitalization Transaction under such an alternative implementation process if the Company elects to do so in the future, subject to certain conditions and consent requirements as provided for in the Support Agreement. In addition, in accordance with the terms of the Interim Order, a vote cast in favour of the CBCA Plan at the Meetings may also be counted in favour of implementing a plan of arrangement on substantially similar terms in any insolvency proceedings under the Companies’ Creditors Arrangement Act (Canada) that may be commenced by the Company, to the extent such proceedings are consented to by the majority private placement parties and the majority initial consenting debtholders.

Management and Board of Director Changes

On May 2, 2018, the Company announced that it appointed Graeme Duncan as its interim Chief Executive Officer, and also announced the departure of Allan Oberman, the Company's former Chief Executive Officer and Board Member. The Company paid approximately $7.7 million in severance to the former Chief Executive Officer.

On May 2, 2018, the Company also announced that it appointed Guy Clark as the Company's Chief Corporate Development Officer, and also announced the departure of Sarwar Islam, the Company's former Chief Corporate Development Officer.

Relocation of Corporate Head Office

During the second quarter of 2018, the Company's corporate head office is expected to be relocated to 5770 Hurontario Street, Suite 310, Mississauga, Ontario, L5R 3G5. At the Shareholders' Meeting, Shareholders will be asked to approve a resolution to move the corporate head office to Mississauga, Ontario.

Notification of the termination of the Currency Swaps and termination of Revolving Commitments

On October 20, 2017, the counterparty to the Company's August 17, 2016 cross currency swap agreement ("August Swap Agreement") and November 3, 2016 cross currency swap agreement ("November Swap Agreement", and together with the August Swap Agreement, the "Currency Swaps") notified the Company that it would be terminating the Currency Swaps effective October 23, 2017 due to commencement of the CBCA Proceedings. As part of the Recapitalization Transaction, the Company has agreed to the amount of the Currency Swaps liability ($114,431), which amount will be addressed in the same manner as the Secured Debt under the Recapitalization Transaction. In addition, on October 27, 2017, the Company terminated the revolving commitments under the Company's credit agreement dated October 21, 2015, as amended ("Credit Agreement"). No amounts had been drawn or were outstanding in respect of the revolving commitments at such time.

Rating Agency Changes

On May 7, 2018, Standard & Poors Global Ratings ("S&P") lowered its issue-level ratings on Concordia’s Secured Debt to "CC" from "CCC-". S&P noted that its “SD” corporate credit rating and "D" rating on Concordia’s Unsecured Debt remained unchanged. In addition, on May 8, 2018, Moody’s Investors Service ("Moody’s") placed the Company’s “Ca” Corporate Family Rating and Ca-PD/LD Probability of Default Rating under review for upgrade. Moody’s also affirmed its "Caa2" senior secured ratings and "C" senior unsecured ratings. The SGL-4 Speculative Grade Liquidity Rating was also affirmed. To the extent that the Company intends to complete any future transactions following the Recapitalization Transaction, the Company’s ability to complete any such transactions may be effected by credit rating agency decisions.

Business Impact in Relation to Brexit

On June 23, 2016, the United Kingdom held a referendum and voted to withdraw from the European Union ("Brexit"). On March 29, 2017, the United Kingdom delivered notice to the European Council in accordance with Article 50 of the Treaty on European Union of the United Kingdom’s intention to withdraw from the European Union. The Company understands that the timeframe for the negotiated withdrawal of the United Kingdom from the European Union is approximately two (2) years from the date of the withdrawal notification. However, as no member state has formally withdrawn from the European Union in the past, there is no precedent for the operation of Article 50 and, as a result, the timing and outcome of Brexit continues to be uncertain at this time. The Concordia International segment has significant operations within the United Kingdom and other parts of the European Union, and therefore continues to monitor developments related to Brexit, including the impact resulting from currency market movements.

|

| |

| Concordia Management's Discussion and Analysis | Page 6 |

Business Impact in Relation to the UK Health Service Medical Supplies (Costs) Act 2017 (the "Act")

The Act received Royal Assent on April 27, 2017. The Act introduces provisions in connection with controlling the cost of health service medicines and other medical supplies. The Act also introduces provisions in connection with the provision of pricing and other information by manufacturers, distributors and suppliers of those medicines and medical supplies. The Company continues to monitor the implementation of the Act and its impact on its business. Refer to the "Risk Factors" section of the Company's Annual Report on Form 20-F dated March 8, 2018.

|

| |

| Concordia Management's Discussion and Analysis | Page 7 |

4 Results of Operations

|

| | | | |

| | Three months ended |

| (in $000's, except per share data) | Mar 31, 2018 |

| Mar 31, 2017 |

|

| Revenue | 152,264 |

| 160,557 |

|

| Gross profit | 101,106 |

| 115,415 |

|

| Gross profit % | 66 | % | 72 | % |

| Total operating expenses | 112,345 |

| 97,049 |

|

| Operating income (loss) | (11,239 | ) | 18,366 |

|

| | | |

| Income tax expense (recovery) | 4,704 |

| 4,489 |

|

| Net loss | (55,694 | ) | (78,824 | ) |

| | | |

| Loss per share | | |

| Basic | (1.09 | ) | (1.54 | ) |

| Diluted | (1.09 | ) | (1.54 | ) |

| | | |

EBITDA (1) | 94,503 |

| 56,932 |

|

Adjusted EBITDA (1) | 72,024 |

| 84,242 |

|

Adjusted EPS (1) | (0.19 | ) | 0.22 |

|

Notes:

| |

| (1) | Represents a non-IFRS measure. For the relevant definitions and reconciliation to reported results, see "Non-IFRS Financial Measures" section of this MD&A. Management believes non-IFRS measures, including Adjusted EBITDA, provide supplementary information to IFRS measures used in assessing the performance of the business. |

Revenue

Revenue for the first quarter of 2018 decreased by $8,293, or 5%, compared to the corresponding period in 2017. This decrease was due to lower sales from both segments, partially offset by higher foreign exchange rates impacting translated revenues from the Concordia International segment for the first quarter of 2018 compared to the corresponding period in 2017. Revenues were lower primarily due to lower volumes resulting from competition on a number of the Company's products in both segments. The Concordia International segment revenue for the first quarter of 2018 decreased by $5,779, or 5%, due to $20,463 lower revenue primarily as a result of volume and price declines on key products, including Liothyronine Sodium, Trazodone and Predisolone, partially offset by $14,684 higher revenue as a result of favourable foreign exchange rates positively impacting translated results. The Concordia North America segment revenue for the first quarter of 2018 decreased by 6% when compared to the corresponding period in 2017, mainly as a result of lower volumes on key products, including Donnatal® and Kapvay®. Refer to the "Segment Performance" section of this MD&A for a further discussion on segmental and product specific performance.

Gross Profit and Gross Profit %

Gross profit for the first quarter of 2018 decreased by $14,309, or 12%, compared to the corresponding period in 2017 primarily due to the revenue decreases described above. The decrease in gross profit percentage of 6% for the first quarter of 2018 compared to the corresponding period in 2017, is primarily due to a change in the mix of product sales within both segments. Refer to the "Segment Performance" section of this MD&A for a further discussion on segmental and product specific performance.

Operating Expenses

Operating expenses for the first quarter of 2018 increased by $15,296, or 16%, compared to the corresponding period in 2017. Operating expenses were higher during the first quarter of 2018 primarily due to $10,278 higher restructuring costs arising from the Company's initiative to realign its capital structure and $8,890 higher amortization charges on intangible assets, partially offset by $1,685 lower share based compensation expense and $1,570 lower general and administrative costs. For a further detailed description of operating expenses, refer to the "Corporate and Other Costs" section of this MD&A. For a further detailed description of certain segment operating expenses, refer to "Segment Performance" section of this MD&A.

Operating income (loss) for the first quarter of 2018 decreased by $29,605 compared to the corresponding period in 2017 due to the decrease in gross profit and higher operating expenses as described above.

|

| |

| Concordia Management's Discussion and Analysis | Page 8 |

The current income tax expense recorded for the first quarter of 2018 decreased by $1,296 compared to the corresponding period in 2017. Income taxes were lower primarily due to lower taxable income compared to the corresponding period in 2017, partially offset by the impact of foreign exchange translation of the income tax expense from the Concordia International segment. The deferred income tax expense recorded for the first quarter of 2018 increased by $1,511 and is mainly the result of movements in the foreign exchange rates, partially offset by the reversal of certain temporary differences.

The net loss for the first quarter of 2018 was $55,694 and EPS loss was $1.09 per share. Significant components comprising the net loss for the first quarter of 2018 are interest and accretion expenses of $80,122 and amortization of intangible assets of $65,607 offset by gross profit of $101,106. Refer to the "Corporate and Other Costs" section of this MD&A for further information related to expenses impacting net loss.

EBITDA and Adjusted EBITDA

EBITDA is higher than the net loss as it excludes: interest and accretion expense; interest income; income taxes; depreciation; and amortization of intangible assets. Refer to the "Non-IFRS Financial Measures" section of this MD&A for a full reconciliation. EBITDA for the first quarter of 2018 increased by $37,571 compared to the corresponding period in 2017. The increase in EBITDA was primarily due to $27,314 lower fair value loss on derivative financial instruments and $31,341 higher unrealized foreign exchange gain, partially offset by $14,309 lower gross profit and $10,278 higher acquisition related, restructuring and other costs.

Adjusted EBITDA also includes adjustments for: impairments; fair value adjustments to acquired inventory; acquisition related, restructuring and other costs; share-based compensation; fair value (gain) loss including purchase consideration and derivative financial instruments; foreign exchange (gain) loss; unrealized foreign exchange (gain) loss; and legal settlements and related legal costs (refer to the "Non-IFRS Financial Measures" section of this MD&A for a full reconciliation and description of these expenses). Adjusted EBITDA for the first quarter of 2018 decreased by $12,218, or 15%, compared to the corresponding period in 2017. The decline is primarily due to lower sales and gross margins from both segments, partially offset by higher foreign exchange rates impacting translated results during the first quarter of 2018. Adjusted EBITDA by segment for the three month period ended March 31, 2018 was $51,748 from Concordia International and $24,273 from Concordia North America. Refer to the "Segment Performance" section of this MD&A for a further discussion on segment performance. In addition, during the first quarter of 2018 the Company incurred $3,997 of Corporate costs related to the Corporate Head Office. Corporate expenses decreased by $1,641 compared to the corresponding period in 2017, primarily due to lower general and administrative expenses, including professional fees incurred during the first quarter of 2018.

|

| |

| Concordia Management's Discussion and Analysis | Page 9 |

5 Segment Performance

Concordia International |

| | | | |

| | Three months ended |

| (in $000's) | Mar 31, 2018 |

| Mar 31, 2017 |

|

| Revenue | 112,950 |

| 118,729 |

|

| Cost of sales | 41,673 |

| 37,501 |

|

| Gross profit | 71,277 |

| 81,228 |

|

| Gross profit % | 63 | % | 68 | % |

Adjusted Gross Profit (1) | 71,277 |

| 81,539 |

|

Adjusted Gross Profit %(1) | 63 | % | 69 | % |

| General and Administrative, Selling and Marketing and Research and Development Expenses | 19,529 |

| 18,298 |

|

Adjusted EBITDA(1) | 51,748 |

| 63,241 |

|

Notes:

| |

| (1) | Represents a non-IFRS measure. For the relevant definitions see "Non-IFRS Financial Measures" section of this MD&A. |

Revenue for the first quarter of 2018 decreased by $5,779 or 5%, compared to the corresponding period in 2017. A $20,463 decrease in revenue was partially offset by a $14,684 increase in revenue as a result of the Great British Pound ("GBP") strengthening against the USD, given a significant portion of the segment revenues are earned in GBP. Declines to revenue attributable to key products during the quarter, excluding the impact of foreign currency translation, were: (i) a $9,488 decrease from Liothyronine Sodium; (ii) a $2,384 decrease from Trazodone; (iii) a $2,064 decrease from Prednisolone; (vi) a $1,643 decrease from Biperiden Hydrochloride; and (v) a $1,244 decrease from Prochlorperazine. These lower product volumes and revenues are primarily due to ongoing competitive market pressures resulting in market share erosion. These revenue decreases were partially offset by $2,751 increased revenue from Nitrofurantoin. The remaining decrease was primarily due to general competitive market pressures across the segment's product portfolio.

Cost of sales for the first quarter of 2018 increased by $4,172 or 11%, compared to the corresponding period in 2017. The increase in cost of sales during the first quarter of 2018 is primarily due to the impact of foreign exchange, partially offset by volume declines from products described above.

Gross profit for the first quarter of 2018 decreased by $9,951 primarily due to the factors described above.

Gross profit as a percentage of revenue for the first quarter of 2018 decreased by 5% compared to the corresponding period in 2017. The decrease was primarily due to a shift in product mix, with certain higher margin products experiencing additional market competition, when compared to the first quarter of 2017.

General and administrative, selling and marketing and research and development costs increased by $1,231 primarily due to the impact of foreign exchange. Excluding the $2,249 unfavorable impact of foreign exchange, these costs decreased by $1,018 as a result of lower general and administrative expenses.

|

| |

| Concordia Management's Discussion and Analysis | Page 10 |

Concordia North America |

| | | | |

| | Three months ended |

| (in $000's) | Mar 31, 2018 |

| Mar 31, 2017 |

|

| Revenue | 39,314 |

| 41,828 |

|

| Cost of sales | 9,485 |

| 7,641 |

|

| Gross profit | 29,829 |

| 34,187 |

|

| Gross profit % | 76 | % | 82 | % |

| General and Administrative, Selling and Marketing and Research and Development Expenses | 5,556 |

| 7,548 |

|

Adjusted EBITDA(1) | 24,273 |

| 26,639 |

|

Notes:

| |

| (1) | Represents a non-IFRS measure. For the relevant definitions, see "Non-IFRS Financial Measures" section of this MD&A. |

Revenue for the first quarter of 2018 decreased by $2,514 or 6%, compared to the corresponding period in 2017. The decrease was primarily due to: (i) a $3,533 decrease from Donnatal®, as a result of additional competitive pressures that have resulted in a loss of market share; and (ii) a $2,456 decrease from Kapvay®. In the first quarter of 2018, Donnatal® continued to face pressure from a non-FDA approved product being distributed by a competitor and an additional competitive product launched in the second quarter of 2017. These decreases were partially offset by a $1,516 increase in revenue from Plaquenil® authorized generic. The remaining decrease was primarily due to general competitive market pressures across the segment's product portfolio.

Cost of sales for the first quarter of 2018 increased by $1,844, or 24%, compared to the corresponding period in 2017. The increase in cost of sales when compared with the decrease in revenue is due to a shift in product mix to lower margin products.

Gross profit for the first quarter of 2018 decreased by $4,358, or 13%, primarily due to lower revenue as described above.

Gross profit as a percentage of revenue for the first quarter of 2018 decreased by 6%, compared to the corresponding period in 2017. The decrease was primarily due to a shift in product mix.

General and administrative, selling and marketing and research and development costs decreased by $1,992 primarily due to lower bad debt expenses and a refund of regulatory fees, partially offset by higher selling and marketing costs associated with the co-promotion agreement for sales of Donnatal®.

|

| |

| Concordia Management's Discussion and Analysis | Page 11 |

6 Corporate and Other Costs

The following table details expenses from the Company's Corporate cost centre and other operating expenses from the business segments: |

| | | | |

| | Three months ended |

| (in $000's) | Mar 31, 2018 |

| Mar 31, 2017 |

|

| General and administrative | 12,178 |

| 13,748 |

|

| Selling and marketing | 9,798 |

| 9,752 |

|

| Research and development | 7,106 |

| 7,984 |

|

| Acquisition related, restructuring and other | 15,494 |

| 5,216 |

|

| Share-based compensation | 1,267 |

| 2,952 |

|

| Amortization of intangible assets | 65,607 |

| 56,717 |

|

| Depreciation expense | 470 |

| 488 |

|

| Fair value (gain) loss | 425 |

| 192 |

|

| Interest and accretion expense | 80,122 |

| 92,541 |

|

| Interest income | (706 | ) | (18,479 | ) |

| Fair value (gain) loss on derivative financial instruments | — |

| 27,314 |

|

| Foreign exchange (gain) loss | 1,341 |

| 990 |

|

| Unrealized foreign exchange (gain) loss | (41,006 | ) | (9,665 | ) |

| Total | 152,096 |

| 189,750 |

|

General and Administrative Expenses

General and administrative expenses reflect costs related to salaries and benefits, professional and consulting fees, public company costs, travel, facility leases and other administrative expenditures. General and administrative expenses for the first quarter of 2018 decreased by 11%, compared to the corresponding period in 2017. This decrease is a result of the Company's objective to reduce operating costs across the business.

Selling and Marketing Expenses

Selling and marketing expenses reflect costs incurred by the Company for the marketing, promotion and sale of the Company’s broad portfolio of products across the Company's segments. Selling and marketing costs for the first quarter of 2018 increased by $46 compared to the corresponding period in 2017 primarily as a result of unfavorable foreign exchange rate movements impacting translation.

Research and Development Expenses

Research and development expenses reflect costs for clinical trial activities, product development, professional and consulting fees and services associated with the activities of the medical, clinical and scientific affairs, quality assurance costs, regulatory compliance and drug safety costs (Pharmacovigilence) of the Company. Research and development costs for the first quarter of 2018 decreased by $878, or 11%, compared to the corresponding period in 2017. This decrease is primarily due to a refund of regulatory fees.

Acquisition Related, Restructuring and Other Costs

Acquisition related, restructuring and other costs during the first quarter of 2018 were $15,494. Acquisition related, restructuring and other costs for the first quarter of 2018 increased by 197% primarily due to costs associated with consultants involved in the Company's capital realignment initiative.

Significant costs incurred during the first quarter of 2018 include $8,261 of costs associated with the Company's realignment of its capital structure which include costs of the Company's advisors and advisors of the lending syndicate, $2,326 of management retention costs, $1,931 of costs related to severance, and $2,487 related to ongoing regulatory matters relating to the UK Competition and Markets Authority ("CMA") investigations (refer to the "Litigation and Arbitration" section of this MD&A for further details). The remaining costs relate primarily to costs associated with the ongoing class action lawsuits involving the Company (refer to the "Litigation and Arbitration" section of this MD&A for further details).

|

| |

| Concordia Management's Discussion and Analysis | Page 12 |

Share-Based Compensation

The share based compensation expense relates to the fair value of share-based option, restricted share unit ("RSU") and deferred share unit ("DSU") awards to employees, management and directors of the Company. Share based compensation during the first quarter of 2018 was $1,267. The decrease in the expense of $1,685 for the period is primarily due to no RSUs or DSUs being issued since the second quarter of 2017, and the impact of the staged vesting of the outstanding share-based options and RSUs.

Amortization of Intangible Assets

Amortization of intangible assets was $8,890 higher for the first quarter of 2018 compared to the corresponding period in 2017. The higher expense is due to the Company's change in accounting estimate with respect to amortizing intangible assets in both segments. The expense for the first quarter of 2018 of $65,607 is comprised of the following amounts:

| |

| • | Amortization related to acquired product rights and manufacturing processes for the first quarter of 2018 was $57,255; |

| |

| • | Amortization related to distribution and supplier contracts for the first quarter of 2018 was $7,751. Distribution and supplier contracts are amortized on a straight-line basis over 5 years; and |

| |

| • | Amortization related to other intangibles for the first quarter of 2018 was $601. |

Interest and Accretion

Interest and accretion expenses for the first quarter of 2018 were $80,122 representing a decrease of $12,419 compared to the corresponding period in 2017. The decrease is primarily due to:

| |

| • | The termination of the Currency Swaps during the fourth quarter of 2017 which resulted in $18,303 lower interest expense during the first quarter of 2018 (as well as lower interest income as described below); and |

| |

| • | The acceleration of all deferred financing fees during the fourth quarter of 2017 which resulted in $7,461 lower costs compared to the corresponding period in 2017. |

Offset primarily by:

| |

| • | A $12,230 higher interest expense on the Company's debt agreements as a result of: (i) events of default on certain of the Company's debt agreements; (ii) higher LIBOR rates; and (iii) a change in foreign exchange rates resulting in higher interest expense on the Company's GBP denominated term loan. |

Interest Income

Interest income for the first quarter of 2018 was $706, representing a decrease of $17,773 due to the termination of the Currency Swaps during the fourth quarter of 2017 as a result of the CBCA Proceedings.

Fair value loss on Derivative Contracts

The fair value loss on derivative contracts was $nil for the first quarter of 2018 compared with $27,314 in the corresponding period in 2017 as a result of the termination of the Currency Swaps. On October 20, 2017, the Company was notified by the counterparty to the Currency Swaps that one or more events of default had occurred under the Currency Swaps as a result of the Company obtaining a preliminary interim order from the Court pursuant to the arrangement provisions of the CBCA. As a result of the foregoing, the counterparty designated October 23, 2017 as the early termination date with respect to all transactions under the Currency Swaps. As part of the Recapitalization Transaction, the Company has agreed to the amount of the Currency Swaps liability ($114,431), which amount will be addressed in the same manner as the Secured Debt under the Recapitalization Transaction.

Foreign Exchange (Gain) Loss and Unrealized Foreign Exchange (Gain) Loss

Foreign exchange (gain) loss for the first quarter of 2018 was a loss of $1,341.

Unrealized foreign exchange gain for the first quarter of 2018 was $41,006. The primary component of the unrealized foreign exchange gain is a result of IFRS requiring that inter-company trading balances denominated in a currency other than the functional currency of an entity being retranslated with the exchange differences flowing through the consolidated statement of loss with the off-set within other comprehensive income (loss).

The foreign exchange translation impact of the Concordia International segment is recorded within other comprehensive loss. During the first quarter of 2018, there was a total of $10,569 foreign exchange gains, net of tax, associated with the translation of entities with a different functional currency, primarily within the Concordia International segment, offset by $22,690 of foreign exchange losses associated with the translation of the Company's GBP denominated term loan.

|

| |

| Concordia Management's Discussion and Analysis | Page 13 |

7 Selected Quarterly Financial Information

|

| | | | | | | | | | | | | | | | |

| For the three months ended (in $000’s, except per share amounts) | Q1-2018 |

| Q4-2017 |

| Q3-2017 |

| Q2-2017 |

| Q1-2017 |

| Q4-2016 |

| Q3-2016 |

| Q2-2016 |

|

| Revenue | 152,264 |

| 150,205 |

| 154,622 |

| 160,785 |

| 160,557 |

| 170,408 |

| 185,504 |

| 231,712 |

|

| Gross profit | 101,106 |

| 100,200 |

| 108,610 |

| 111,312 |

| 115,415 |

| 120,464 |

| 137,034 |

| 177,607 |

|

Adjusted Gross profit (1) | 101,106 |

| 100,200 |

| 108,610 |

| 111,312 |

| 115,726 |

| 120,858 |

| 138,540 |

| 178,476 |

|

| Operating income (loss) | (11,239 | ) | (211,648 | ) | 9,589 |

| (981,255 | ) | 18,366 |

| (524,962 | ) | 42,636 |

| (514,931 | ) |

| Net income (loss), continuing operations | (55,694 | ) | (431,773 | ) | (69,485 | ) | (1,010,653 | ) | (78,824 | ) | (663,761 | ) | (75,147 | ) | (570,384 | ) |

| | | | | | |

|

| | |

| Cash | 343,834 |

| 327,030 |

| 341,303 |

| 301,782 |

| 336,156 |

| 397,917 |

| 162,616 |

| 145,341 |

|

| Total assets | 2,324,626 |

| 2,322,335 |

| 2,651,844 |

| 2,611,489 |

| 3,619,665 |

| 3,731,574 |

| 4,229,695 |

| 4,349,554 |

|

| Total liabilities | 4,301,682 |

| 4,232,848 |

| 4,128,960 |

| 4,022,218 |

| 4,058,725 |

| 4,109,147 |

| 3,928,646 |

| 3,982,125 |

|

| | | | | | |

|

| | |

EBITDA (1) | 94,503 |

| (170,126 | ) | 63,144 |

| (903,563 | ) | 56,932 |

| (569,997 | ) | 30,213 |

| (454,285 | ) |

Adjusted EBITDA (1) | 72,024 |

| 70,778 |

| 78,582 |

| 81,808 |

| 84,242 |

| 80,508 |

| 104,444 |

| 142,344 |

|

| | | | | | |

|

| | |

| Earnings (Loss) per share | | | | | |

|

| | |

| Basic | (1.09 | ) | (8.42 | ) | (1.36 | ) | (19.78 | ) | (1.54 | ) | (13.00 | ) | (1.47 | ) | (11.18 | ) |

| Diluted | (1.09 | ) | (8.42 | ) | (1.36 | ) | (19.78 | ) | (1.54 | ) | (13.00 | ) | (1.47 | ) | (11.18 | ) |

Adjusted (1) | (0.19 | ) | (0.28 | ) | 0.06 |

| 0.19 |

| 0.22 |

| 0.13 |

| 0.69 |

| 1.38 |

|

Amounts shown above are results from continuing operations, excluding discontinued operations, except for total assets and liabilities amounts.

Notes:

(1) Represents a non-IFRS measure. For the relevant definitions see the "Non-IFRS Financial Measures" section of this MD&A. For the relevant reconciliation to reported results, see the "Non-IFRS Financial Measures" section of this MD&A for the first quarter of 2018 and corresponding period in 2017, and for other periods presented, refer to previous publicly filed MD&As.

During the quarterly periods presented above, the Company has experienced a declining trend in operating results. Subsequent to the second quarter of 2016, the business experienced greater than expected market competition on certain products and industry specific environmental changes, which together have resulted in the Company recording a significant amount of impairment charges with respect to acquired intangible assets from its acquisitions, including intellectual property rights and goodwill. Management has focused the discussion and analysis below on comparing to the most recent quarters presented above in order to describe the most current business trends that have occurred in the first quarter of 2018.

Revenues in the first quarter of 2018 were $152,264 which consisted of $112,950 from the Concordia International segment, and $39,314 from the Concordia North America segment. Revenues during the fourth quarter of 2017 were $150,205 which consisted of $113,663 from the Concordia International segment, and $36,542 from the Concordia North America segment. Revenue from the Concordia International segment decreased by $713, or 1%, primarily due to the impact of: (i) $1,992 lower revenue from Fusidic Acid; (ii) $1,355 lower revenue from Carbimazole; and (iii) $1,188 lower revenue from Hydralazine Hcl, partially offset by: (i) a $5,492 increase in revenue as a result of the GBP strengthening against the USD; (ii) $1,505 higher revenue from Nitrofurantoin; and (iii) $1,442 higher revenue from Agripressin. The remaining decrease was primarily due to general competitive market pressures across the Concordia International segment's product portfolio. The Concordia North America segment revenue increase of $2,772 is primarily due to $3,737 higher revenue from the Plaquenil® authorized generic product. Donnatal® continues to experience competitive pressure from a non-FDA approved product being distributed by a third party and most recently the launch of an additional competitive product in the second quarter of 2017. Refer to the "Litigation and Arbitration" section of this MD&A.

Gross profit and adjusted gross profit in the first quarter of 2018 increased by $906 compared to the fourth quarter of 2017. Gross profit as a percentage of revenue in the first quarter of 2018 was 66% compared with the fourth quarter of 2017 of 67%. The decrease in gross profit as a percentage of revenue is primarily due to the shift in product mix within the Concordia North America segment as gross profit as a percentage of revenue within the Concordia International segment was flat.

Net loss from continuing operations during the first quarter of 2018 compared to the fourth quarter of 2017, decreased by $376,079. The decrease in net loss is primarily due to the fourth quarter of 2017 including impairment charges totaling $207,662, and $143,969 higher accretion expenses as a result of accelerating the accretion of deferred financing costs.

|

| |

| Concordia Management's Discussion and Analysis | Page 14 |

Adjusted EBITDA in the first quarter of 2018 of $72,024 consisted of $51,748 related to Concordia International, $24,273 related to Concordia North America, offset by $3,997 related to Corporate expenses. This is compared with fourth quarter 2017 Adjusted EBITDA of $70,778, which consisted of $56,116 related to Concordia International, $19,880 related to North America, offset by $5,218 related to Corporate expenses. Adjusted EBITDA for the first quarter of 2018 was $1,246 higher than the fourth quarter of 2017. The net increase of total adjusted EBITDA of $1,246 is primarily due to favourable foreign exchange rate movements of $2,680 and $1,221 lower Corporate expenses, partially offset by net product declines as described above.

|

| |

| Concordia Management's Discussion and Analysis | Page 15 |

8 Balance Sheet Analysis

|

| | | | | | | | |

| As at (in $000's) | Mar 31, 2018 |

| Dec 31, 2017 |

| Change |

| $ | % |

| Working capital | 243,277 |

| 281,288 |

| (38,011 | ) | (14 | )% |

| Long-lived assets | 1,740,063 |

| 1,752,261 |

| (12,198 | ) | (1 | )% |

| Other current liabilities | 3,824,774 |

| 3,804,684 |

| 20,090 |

| 1 | % |

| Long-term liabilities | 138,597 |

| 141,844 |

| (3,247 | ) | (2 | )% |

| Shareholder's deficit | (1,977,056 | ) | (1,910,513 | ) | (66,543 | ) | 3 | % |

Working capital

Concordia defines working capital as total current assets less accounts payable and accrued liabilities, income taxes payable and provisions. The $38,011 decrease in working capital from December 31, 2017 to March 31, 2018 is primarily due to the following factors:

| |

| • | Inventory decreased by $6,236 primarily due to $2,390 and $3,846 lower inventory on hand within the Concordia International and Concordia North America segments, respectively. These decreases are primarily due to product sales during the first quarter of 2018; |

| |

| • | Accounts payable and accrued liabilities increased by $53,993. The increase in accounts payable and accrued liabilities is primarily due to an increase in interest payable on the Company's debt of $52,563. Interest payments on Unsecured Debt have not been paid as a result of the CBCA Proceedings resulting in a stay of interest and principal payments on these facilities; and |

| |

| • | Provisions decreased by $1,875. The decrease is primarily due to lower expected returns within the Concordia North America segment. |

Offset primarily by:

| |

| • | Cash and cash equivalents increased by $16,804 primarily due to cash from operating activities of $50,558, primarily offset by debt amortization and interest payments of $38,859, as further discussed in the "Liquidity and Capital Realignment" section of this MD&A; and |

| |

| • | Accounts receivable increased by $2,054. Concordia International segment accounts receivable increased by $3,173 primarily as a result of foreign exchange rate movements. Concordia North America accounts receivable decreased by $1,119 primarily due to the timing of receipts from customers. |

Long-lived assets

Long-lived assets consist of fixed assets, intangible assets and goodwill. The $12,198 decrease in long-lived assets from December 31, 2017 to March 31, 2018 is primarily due to intangible asset amortization recorded during the first quarter of 2018 of $65,607, partially offset by a $52,015 increase due to foreign exchange translation. This increase from foreign exchange translation is a result of the movement in the GBP/USD period end exchange rates from 1.3494 as at December 31, 2017 to 1.4037 as at March 31, 2018.

Other current liabilities

Other current liabilities consist of the current portion of long-term debt, purchase consideration payable and cross currency swap liability. The $20,090 increase from December 31, 2017 to March 31, 2018 is primarily due to the increase in the current portion of long-term debt of $14,939 as a result of $26,221 foreign exchange rate movement from December 31, 2017 to March 31, 2018, partially offset by $11,282 of principal repayments.

Long term liabilities

Long-term obligations consist of purchase consideration payable, other liabilities and deferred income tax liabilities. The $3,247 decrease in long term liabilities from December 31, 2017 to March 31, 2018 is primarily due to the decrease in deferred tax liabilities of $1,491 due to the reversal of certain deferred tax liabilities in respect of assets recorded as a result of purchase price accounting and changes to the carrying value of certain assets due to their impairment and/or changes in the applicable foreign exchange rate.

|

| |

| Concordia Management's Discussion and Analysis | Page 16 |

Shareholders’ deficit

Shareholders’ deficit increased by $66,543 from December 31, 2017 to March 31, 2018. The increase is primarily related to:

| |

| • | A net loss for the first quarter of 2018 of $55,694; and |

| |

| • | A net foreign exchange impact of $12,121 from the translation of the Concordia International segment, the Currency Swaps and the GBP denominated term loan. |

Offset primarily by:

| |

| • | A $1,272 net change in equity for share based compensation expense, issuance of options, vesting of RSUs and related reversal of deferred income tax assets. |

|

| |

| Concordia Management's Discussion and Analysis | Page 17 |

9 Liquidity and Capital Realignment

Realignment of Capital Structure and Going Concern

During the 2017 fiscal year, the Company announced as part of its long-term strategy an objective to realign its capital structure, which includes an intention to significantly reduce the Company’s existing secured and unsecured debt obligations. On October 20, 2017, as part of the Company’s efforts to realign its capital structure, the Company and one of its wholly-owned direct subsidiaries commenced a court proceeding under the CBCA. The CBCA is a Canadian corporate statute that includes provisions that allow Canadian corporations to restructure certain debt obligations, and is not a bankruptcy or insolvency statute. The preliminary interim order issued by the Court provides a stay of proceedings, which continues to be effective, against any third party that is party to, or a beneficiary of, any loan, note, commitment, contract or other agreement with the Company or any of its subsidiaries, including the Company's debtholders, from exercising any rights or remedy or any proceeding, including, without limitation, terminating, demanding, accelerating, setting-off, amending, declaring in default or taking any other action under or in connection with any loan, note, commitment, contract, or other agreement of the Company and its subsidiaries on the terms set out in the Court order.

In connection with the Company's efforts to realign its capital structure and as contemplated by the CBCA Proceedings, the Company has elected to not make scheduled payments on the following debt obligations: payments under its 7% unsecured senior notes; payments under its 9.5% unsecured senior notes; and payments under its unsecured extended equity bridge facility. During the CBCA Proceedings, the Company has been, and intends to, continue to make scheduled ordinary course interest and principal payments under its secured debt facilities, as applicable. The commencement of the CBCA Proceedings and non-payment of the scheduled payments noted above resulted in events of default under the Company's credit facilities and the Company's Currency Swaps, and therefore the outstanding debt and cross currency swap liabilities have been presented as current liabilities. Refer to the "Lending Arrangements and Debt" section of this MD&A for additional details associated with events of default applicable under certain of the Company's credit facilities and Currency Swaps.

Proposed Recapitalization Transaction

On May 2, 2018, the Company announced a proposed Recapitalization Transaction to realign its capital structure. The details of the Recapitalization Transaction are described within the "Recent Events" section of this MD&A, and in the Company's term sheet dated as of May 1, 2018, the support agreement between the Company, certain subsidiaries of the Company and certain holders of the Company’s secured debt and unsecured debt dated as of May 1, 2018, and the subscription agreement between the Company, certain subsidiaries of the Company, and certain holders of the Company’s secured debt and unsecured debt dated as of May 1, 2018. A management information circular outlining all key terms of the Recapitalization Transaction is expected to be mailed to relevant stakeholders prior to the scheduled June 19, 2018 Meetings where secured and unsecured debtholders and shareholders will vote on the approval of, among other things, the Company's CBCA Plan. The Company believes the Recapitalization Transaction, once completed, will realign the Company's capital structure, and significantly reduce the Company's outstanding debt.

Upon completion of the Recapitalization Transaction, the Company expects to have New Secured Debt of approximately $1.4 billion and cash on hand in excess of $200 million, after payment of related advisor fees and recapitalization transaction costs.

Going Concern

Future liquidity and operations of the Company are dependent on the ability of the Company to restructure its debt obligations and to generate sufficient operating cash flows to fund its on-going operations. If the Company does not complete the realignment of its capital structure through the CBCA Plan described in the "Recent Events" section of this MD&A, it will be necessary to pursue other restructuring strategies, which may include, among other alternatives, proceedings under the Companies Creditors Arrangement Act and / or a filing under the United States Bankruptcy Code. The Company may not be able to restructure and reduce its debt obligations and this results in a material uncertainty that may cast significant doubt upon the Company’s ability to continue as a going concern.

The Company had approximately $344 million of cash on hand as of March 31, 2018 (December 31, 2017 - $327 million) and believes it has sufficient liquidity in the near term to operate its business and meet its ordinary course financial commitments while it works toward implementing the Recapitalization Transaction.

|

| |

| Concordia Management's Discussion and Analysis | Page 18 |

Sources and Uses of Cash |

| | | | |

| | Three months ended |

| (in $000’s) | Mar 31, 2018 |

| Mar 31, 2017 |

|

| Cash flow from Operating Activities | 50,558 |

| 86,204 |

|

| Cash flow used in Investing Activities | (1,583 | ) | (317 | ) |

| Cash flow used in Financing Activities | (38,859 | ) | (151,515 | ) |

| Total | 10,116 |

| (65,628 | ) |

The Company's business continues to generate cash flow from operating activities. Cash flows from operations represent net income adjusted for changes in working capital, non-cash items and excludes interest paid as this is recorded within cash used in financing activities.

Cash flow from operating activities for the first quarter of 2018 decreased by $35,646 compared to the corresponding period in 2017. The decrease is primarily due to $14,309 lower gross profit from both segments, $10,278 higher acquisition related, restructuring and other costs primarily as a result of the Company's capital realignment initiative and $13,546 lower favourable working capital movements.

Cash flow used in financing activities during the three months ended March 31, 2018 is comprised of: $27,577 of contractual interest payments; and $11,282 of scheduled long-term debt principal repayments.

Cash and Capital Management

The purpose of cash and capital management is to ensure that there is sufficient cash to meet all the financial commitments and obligations of the Company as they come due. Since inception, the Company has financed its cash requirements primarily through the issuances of securities, short-term borrowings, long-term debt as well as cash flows generated from operations.

Liquidity risk is the risk that the Company may encounter difficulty meeting obligations associated with financial liabilities. The Company manages liquidity risk through the management of its capital structure.

As described above and in the "Recent Events" section of this MD&A, the Company's capital management plan was to enter into the CBCA Proceedings to realign its capital structure. During this period, the Company has been, and intends to, continue to make scheduled ordinary course interest and principal payments under its Secured Debt facilities, as applicable. The Company has not made scheduled payments under its Unsecured Debt facilities As a result of certain events associated with the CBCA Proceedings, the Company may not have the ability to transfer certain funds, which could have an impact on the Company's liquidity.

In managing the Company’s capital, Management estimates future cash requirements by preparing annual financial forecasts for review and approval by the Board. The financial forecasts are reviewed and updated periodically and establish approved activities for the year and estimates the costs associated with those activities. Forecast to actual variances are prepared and reviewed by Management and are presented regularly to the Board.

|

| |

| Concordia Management's Discussion and Analysis | Page 19 |

10 Lending Arrangements and Debt

|

| | | | |

| As at (in $000’s) | Mar 31, 2018 |

| Dec 31, 2017 |

|

| Term Loan | | |

| - USD term loan | 1,054,625 |

| 1,061,500 |

|

| - GBP term loan | 672,900 |

| 651,086 |

|

| Extended Bridge Facility | 100,832 |

| 100,832 |

|

| 9.5% Senior Notes | 790,000 |

| 790,000 |

|

| 7% Senior Notes | 735,000 |

| 735,000 |

|

| 9% Secured Notes | 350,000 |

| 350,000 |

|

| Total Debt | 3,703,357 |

| 3,688,418 |

|

| Less: Current Portion | 3,703,357 |

| 3,688,418 |

|

| Long-Term Debt | — |

| — |

|

As at March 31, 2018, approximately 82% of total long term debt was denominated in USD (December 31, 2017 - 82%) and 18% denominated in GBP (December 31, 2017 - 18%).

The commencement of the CBCA Proceedings on October 20, 2017 resulted in an event of default under the Credit Agreement, indentures governing the Company's 9% senior secured notes and 9.5% unsecured notes and the Currency Swaps, which defaults are subject to the stay of proceedings granted by the Court. As a result of the foregoing events of default, a cross default was triggered under the indenture governing the 7% unsecured senior notes and the unsecured extended equity bridge facility, however any demand for payment of this debt has been stayed by the preliminary interim order granted by the Court in the CBCA Proceedings. As a result of these events all debt arrangements are presented as current liabilities. On October 20, 2017, the Company was notified by the counterparty to the Currency Swaps that one or more events of default occurred under the swap agreements as a result of the Company obtaining a preliminary interim order from the Court pursuant to the arrangement provisions of the CBCA. As a result of the foregoing, the counterparty to the Currency Swaps designated October 23, 2017 as the early termination date with respect to all transactions under the Currency Swaps. As part of the Recapitalization Transaction, the Company has agreed to the amount of the Currency Swaps liability ($114,431), which amount will be addressed in the same manner as the Secured Debt under the Recapitalization Transaction.

During the three months ended March 31, 2018, the Company made $11,282 of principal repayments and paid $27,577 of cash interest expense on its secured debt facilities, including the Currency Swaps, as applicable.

Details of the Company's lending arrangements are further disclosed in the notes to the consolidated financial statements for the first quarter of 2018.

The following table presents repayments of long-term debt principal, interest payments on long-term debt, payments on cross currency swap liability and purchase consideration on an undiscounted basis:

|

| | | | | | | | | | | | | | |

| (in $000's) | < 3 months |

| 3 to 6 months |

| 6 months to 1 year |

| 1 to 2 years |

| 2 to 5 years |

| Thereafter |

| Total |

|

| | | | | | | | |

Long-term debt (1) | 3,703,357 |

| — |

| — |

| — |

| — |

| — |

| 3,703,357 |

|

Interest on long-term debt(2) | 159,131 |

| — |

| — |

| — |

| — |

| — |

| 159,131 |

|

| Cross currency swap liability | 114,431 |

| — |

| — |

| — |

| — |

| — |

| 114,431 |

|

Purchase consideration(3) | 6,986 |

| — |

| — |

| — |

| 3,770 |

| — |

| 10,756 |

|

| Total | 3,983,905 |

| — |

| — |

| — |

| 3,770 |

| — |

| 3,987,675 |

|

| |

| (1) | All long-term debt as at March 31, 2018 has been presented as a current liability. Refer to the discussion above on long-term debt classification and the CBCA Proceedings. |

| |

| (2) | The contractual interest amount as at March 31, 2018 reflects the accrued interest payable on long-term debt. |

| |

| (3) | Refer to the "Contractual Obligations" section of this MD&A for further information. |

|

| |

| Concordia Management's Discussion and Analysis | Page 20 |

11 Contractual Obligations

Contractual Obligations

The Company enters into contractual obligations in the normal course of business. There have been no significant changes to the specified contractual obligations during the three months ended March 31, 2018. Details of the contractual obligations are further disclosed in the notes to the consolidated financial statements for the three months ended March 31, 2018.

During the three months ended March 31, 2018, the Company did not engage in any off-balance sheet financing transactions.

|

| |

| Concordia Management's Discussion and Analysis | Page 21 |

12 Related Party Transactions

Compensation for directors and key management, consisting of salaries, performance and retention bonuses, other benefits, severance and director fees for the first quarter of 2018 amounted to $1,946 (2017 - $1,315).

Share based compensation expense recorded for key management and directors, for the first quarter of 2018 amounted to $494 (2017 - $1,883).

Certain current employees of the Concordia International segment had an equity interest in the Concordia International segment at the time of its sale to the Company. As a result, pursuant to the share purchase agreement entered into by the Company in connection with the acquisition of the Concordia International segment, these employees received a portion of the consideration paid by the Company to the vendors of the Concordia International segment (including the earn-out consideration paid in December 2016 and February 2017, respectively).

|

| |

| Concordia Management's Discussion and Analysis | Page 22 |

13 Non-IFRS Financial Measures

This MD&A makes reference to certain non-IFRS measures. These non-IFRS measures are not recognized measures under IFRS and do not have a standardized meaning prescribed by IFRS, and are therefore unlikely to be comparable to similar measures presented by other companies. When used, these measures are defined in such terms as to allow the reconciliation to the closest IFRS measure. These measures are provided as additional information to complement those IFRS measures by providing further understanding of the Company’s results of operations from Management’s perspective. Accordingly, they should not be considered in isolation nor as a substitute to the Company’s financial information reported under IFRS. Management uses non-IFRS measures such as EBITDA, Adjusted EBITDA, Adjusted Gross Profit, Adjusted Net Income and Adjusted EPS to provide investors with supplemental information of the Company’s operating performance and thus highlight trends in the Company’s core business that may not otherwise be apparent when relying solely on IFRS financial measures. Securities analysts, investors and other interested parties frequently use non-IFRS measures in the evaluation of issuers. Management also uses non-IFRS measures in order to facilitate operating performance comparisons from period to period, prepare annual operating budgets, and to assess its ability to meet future debt service requirements, in making capital expenditures, and to consider the business's working capital requirements.

The definition and reconciliation of Adjusted Gross Profit, EBITDA, Adjusted EBITDA, Adjusted Net Income and Adjusted EPS used and presented by the Company to the most directly comparable IFRS measures follows below.

Adjusted Gross Profit

Adjusted Gross Profit is defined as gross profit adjusted for non-cash fair value increases to the cost of acquired inventory from a business combination. Under IFRS, acquired inventory is required to be written-up to fair value at the date of acquisition. As this inventory is sold the fair value adjustment represents a non-cash cost of sale amount that has been excluded in adjusted gross profit in order to normalize gross profit for this non-cash component.

|

| | | | |

| | Three months ended |

| (in $000’s) | Mar 31, 2018 |

| Mar 31, 2017 |

|

| Gross profit per financial statements | 101,106 |

| 115,415 |

|

| Add back: Fair value adjustment to acquired inventory | — |

| 311 |

|

| Adjusted Gross profit | 101,106 |

| 115,726 |

|

EBITDA

EBITDA is defined as net income / loss adjusted for interest and accretion expense, interest income, income taxes, depreciation and amortization. Management uses EBITDA to assess the Company’s operating performance.

Adjusted EBITDA

Adjusted EBITDA is defined as EBITDA adjusted for certain charges including costs associated with acquisitions, restructuring initiatives, and other costs (which includes onerous contract costs and direct costs associated with contractual terminations), management retention costs, non-operating gains / losses, integration costs, legal settlements (net of insurance recoveries) and related legal costs, non-cash items such as unrealized gains / losses on derivative instruments, share based compensation, fair value changes including purchase consideration and derivative financial instruments, asset impairments, fair value increases to inventory arising from purchased inventory from a business combination, gains / losses from the sale of assets and unrealized gains / losses related to foreign exchange. Management uses Adjusted EBITDA, among other Non-IFRS financial measures, as the key metric in assessing business performance when comparing actual results to budgets and forecasts. Management believes Adjusted EBITDA is an important measure of operating performance and cash flow, and provides useful information to investors because it highlights trends in the underlying business that may not otherwise be apparent when relying solely on IFRS measures.

|

| |

| Concordia Management's Discussion and Analysis | Page 23 |

|

| | | | |

| | Three months ended |

| (in $000’s) | Mar 31, 2018 |

| Mar 31, 2017 |

|

| Net loss | (55,694 | ) | (78,824 | ) |

| | | |

| Interest and accretion expense | 80,122 |

| 92,541 |

|

| Interest income | (706 | ) | (18,479 | ) |

| Income taxes | 4,704 |

| 4,489 |

|

| Depreciation | 470 |

| 488 |

|

| Amortization of intangible assets | 65,607 |

| 56,717 |

|

| EBITDA | 94,503 |

| 56,932 |

|

| Fair value adjustment to acquired inventory | — |

| 311 |

|

| Acquisition related, restructuring and other | 15,494 |

| 5,216 |

|

| Share-based compensation | 1,267 |

| 2,952 |

|

| Fair value (gain) loss on purchase consideration and derivatives | 425 |

| 27,506 |

|

| Foreign exchange (gain) loss | 1,341 |

| 990 |

|

| Unrealized foreign exchange (gain) loss | (41,006 | ) | (9,665 | ) |

| Adjusted EBITDA | 72,024 |

| 84,242 |

|

|

| |

| Concordia Management's Discussion and Analysis | Page 24 |

Adjusted Net Income and Adjusted EPS