| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-193376-19 | ||

June 3, 2015 | |||

FREE WRITING PROSPECTUS STRUCTURAL AND COLLATERAL TERM SHEET $1,321,890,997 (Approximate Total Mortgage Pool Balance) $1,221,096,000 (Approximate Offered Certificates) | |||

| COMM 2015-LC21 | |||

Deutsche Mortgage & Asset Receiving Corporation Depositor German American Capital Corporation Cantor Commercial Real Estate Lending, L.P. Ladder Capital Finance LLC KeyBank National Association Sponsors and Mortgage Loan Sellers | |||

| Deutsche Bank Securities | Cantor Fitzgerald & Co. | ||

| Joint Bookrunning Managers and Co-Lead Managers | |||

| KeyBanc Capital Markets | Goldman, Sachs & Co. | ||

| Co-Managers | |||

| The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-193376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us. | |||

COMM 2015-LC21 Mortgage Trust Capitalized terms used but not defined herein have the meanings assigned to them in the other Free Writing Prospectus expected to be dated June 4, 2015, relating to the offered certificates (hereinafter referred to as the “Free Writing Prospectus”). |

| KEY FEATURES OF SECURITIZATION |

| Offering Terms: | ||

| Joint Bookrunners & Co-Lead Managers: | Deutsche Bank Securities Inc. Cantor Fitzgerald & Co. | |

| Co-Managers: | KeyBanc Capital Markets Inc. and Goldman, Sachs & Co. | |

| Mortgage Loan Sellers: | German American Capital Corporation* (“GACC”) (39.0%), Cantor Commercial Real Estate Lending, L.P. (“CCRE”) (25.1%), Ladder Capital Finance LLC (“LCF”) (21.4%) and KeyBank National Association (“KeyBank”) (14.6%). *An indirect wholly owned subsidiary of Deutsche Bank AG. | |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association | |

| Operating Advisor: | Park Bridge Lender Services LLC | |

| Special Servicer: | Midland Loan Services, a Division of PNC Bank, National Association | |

| Trustee: | Wilmington Trust, National Association | |

| Certificate Administrator: | Deutsche Bank Trust Company Americas | |

| Rating Agencies: | Moody’s Investors Service, Inc., DBRS, Inc. and Kroll Bond Rating Agency, Inc. | |

| Determination Date: | The 6th day of each month, or if such 6th day is not a business day, the following business day, commencing in July 2015. | |

| Distribution Date: | 4th business day following the Determination Date in each month, commencing in July 2015. | |

| Cut-off Date: | Payment Date in June 2015 (or related origination date, if later). Unless otherwise noted, all Mortgage Loan statistics are based on balances as of the Cut-off Date. | |

| Settlement Date: | On or about June 18, 2015 | |

| Settlement Terms: | DTC, Euroclear and Clearstream, same day funds, with accrued interest. | |

| ERISA Eligible: | All of the Offered Certificates are expected to be ERISA eligible. | |

| SMMEA Eligible: | None of the Offered Certificates will be SMMEA eligible. | |

| Day Count: | 30/360 | |

| Tax Treatment: | REMIC | |

| Rated Final Distribution Date: | July 2048 | |

| Minimum Denominations: | $10,000 (or $100,000 with respect to Class X-A) and in each case in multiples of $1 thereafter. | |

| Clean-up Call: | 1% | |

| Distribution of Collateral by Property Type |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 3 |

COMM 2015-LC21 Mortgage Trust

TRANSACTION HIGHLIGHTS |

| Mortgage Loan Sellers | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Outstanding Pool Balance |

| German American Capital Corporation | 22 | 88 | $515,860,000 | 39.0% |

| Cantor Commercial Real Estate Lending, L.P. | 34 | 48 | $331,175,118 | 25.1% |

| Ladder Capital Finance LLC | 27 | 27 | $282,345,116 | 21.4% |

| KeyBank National Association | 20 | 35 | $192,510,764 | 14.6% |

| Total: | 103 | 198 | $1,321,890,997 | 100.0% |

| Pooled Collateral Facts: | ||

| Initial Outstanding Pool Balance: | $1,321,890,997 | |

| Number of Mortgage Loans: | 103 | |

| Number of Mortgaged Properties: | 198 | |

| Average Mortgage Loan Cut-off Date Balance: | $12,833,893 | |

| Average Mortgaged Property Cut-off Date Balance: | $6,676,217 | |

| Weighted Average Mortgage Rate: | 4.3323% | |

| Weighted Average Mortgage Loan Original Term to Maturity Date or ARD (months): | 112 | |

| Weighted Average Mortgage Loan Remaining Term to Maturity Date or ARD (months): | 111 | |

| Weighted Average Mortgage Loan Seasoning (months): | 1 | |

| % of Mortgaged Properties Leased to a Single Tenant: | 12.5% | |

Credit Statistics(1): | ||

| Weighted Average Mortgage Loan U/W NCF DSCR: | 2.01x | |

Weighted Average Mortgage Loan Cut-off Date LTV(2): | 65.5% | |

Weighted Average Mortgage Loan Maturity Date or ARD LTV(2): | 56.9% | |

| Weighted Average U/W NOI Debt Yield: | 11.5% | |

Amortization Overview: | ||

| % Mortgage Loans with Amortization through Maturity Date or ARD: | 40.4% | |

| % Mortgage Loans which pay Interest Only through Maturity Date or ARD: | 36.5% | |

| % Mortgage Loans which pay Interest Only followed by Amortization through Maturity Date or ARD: | 21.9% | |

Weighted Average Remaining Amortization Term (months)(3): | 354 | |

Loan Structural Features: | ||

| % Mortgage Loans with Upfront or Ongoing Tax Reserves: | 88.4% | |

% Mortgage Loans with Upfront or Ongoing Replacement Reserves(4): | 85.1% | |

| % Mortgage Loans with Upfront or Ongoing Insurance Reserves: | 53.5% | |

% Mortgage Loans with Upfront or Ongoing TI/LC Reserves(5): | 80.5% | |

| % Mortgage Loans with Upfront Engineering Reserves: | 50.1% | |

| % Mortgage Loans with Upfront or Ongoing Other Reserves: | 50.8% | |

| % Mortgage Loans with In Place Hard Lockboxes: | 55.8% | |

| % Mortgage Loans with Cash Traps Triggered at DSCR Levels ≥ 1.10x: | 83.6% | |

| % Mortgage Loans with Cash Traps Triggered only based on Loan Specific Debt Yield: | 7.3% | |

| % Mortgage Loans with Defeasance Only After a Lockout Period and Prior to an Open Period: | 89.4% | |

| % Mortgage Loans with Prepayment with a Yield Maintenance Charge Only After a Lockout Period and Prior to an Open Period: | 8.7% | |

| % Mortgage Loans Freely Prepayable Only After a Lockout Period: | 1.5% | |

| % Mortgage Loans with Prepayment with a Yield Maintenance Charge or Defeasance Only After a Lockout Period and Prior to an Open Period: | 0.2% | |

| % Mortgage Loans with Prepayment with a Yield Maintenance Charge Prior to an Open Period and also Defeasance Only After a Yield Maintenance Period and Prior to an Open Period: | 0.1% | |

| (1) | With respect to the Courtyard by Marriott Portfolio Loan, the La Gran Plaza Loan and the Renaissance New Orleans Portfolio Loan, LTV, DSCR and debt yield calculations include the related pari passu companion loan(s). With respect to the one group of three cross-collateralized and cross-defaulted loans, LTV, DSCR and debt yield calculations are calculated on an aggregate basis unless otherwise specifically indicated. |

| (2) | With respect to seven mortgage loans, representing 7.1% of the initial outstanding principal balance, the Cut-off Date LTV and Maturity Date or ARD LTV have in certain cases been calculated based on the “as complete”, “as renovated” or “hypothetical as is” value. For additional information, see the Footnotes to Annex A-1 in the Free Writing Prospectus. |

| (3) | Excludes loans which are interest only for the full loan term or through a related anticipated repayment date. |

| (4) | Includes FF&E Reserves. |

| (5) | Represents the percent of the allocated initial outstanding principal balance of retail, office, industrial and mixed use properties only. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 4 |

COMM 2015-LC21 Mortgage Trust

SUMMARY OF THE CERTIFICATES |

OFFERED CERTIFICATES

Class(1) | Ratings (Moody’s/DBRS/KBRA) | Initial Certificate Balance or Notional Amount(2) | Initial Subordination Levels | Weighted Average Life (years)(3) | Principal Window (months)(3) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) |

| Class A-1 | Aaa(sf)/AAA(sf)/AAA(sf) | $57,900,000 | 30.000%(6) | 2.65 | 1 - 55 | 45.8% | 16.4% |

| Class A-2 | Aaa(sf)/AAA(sf)/AAA(sf) | $181,050,000 | 30.000%(6) | 4.83 | 55 - 60 | 45.8% | 16.4% |

| Class A-SB | Aaa(sf)/AAA(sf)/AAA(sf) | $90,150,000 | 30.000%(6) | 7.38 | 60 - 115 | 45.8% | 16.4% |

| Class A-3 | Aaa(sf)/AAA(sf)/AAA(sf) | $225,000,000 | 30.000%(6) | 9.80 | 115 - 119 | 45.8% | 16.4% |

| Class A-4 | Aaa(sf)/AAA(sf)/AAA(sf) | $371,223,000 | 30.000%(6) | 9.89 | 119 - 119 | 45.8% | 16.4% |

Class X-A(7) | Aa1(sf)/AAA(sf)/AAA(sf) | $1,042,641,000(8) | N/A | N/A | N/A | N/A | N/A |

| Class A-M | Aa2(sf)/AAA(sf)/AAA(sf) | $117,318,000 | 21.125% | 9.97 | 119 - 120 | 51.7% | 14.6% |

| Class B | NR/AA(low)(sf)/AA-(sf) | $67,747,000 | 16.000% | 9.98 | 120 - 120 | 55.0% | 13.7% |

| Class C | NR/A(low)(sf)/A-(sf) | $51,223,000 | 12.125% | 9.98 | 120 - 120 | 57.6% | 13.1% |

| Class D | NR/BBB(low)(sf)/BBB-(sf) | $59,485,000 | 7.625% | 9.98 | 120 - 120 | 60.5% | 12.4% |

NON-OFFERED CERTIFICATES

Class(1) | Ratings (Moody’s/DBRS/KBRA) | Initial Certificate Balance or Notional Amount(2) | Initial Subordination Levels | Weighted Average Life (years)(3) | Principal Window (months)(3) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) |

Class X-B(7) | NR/AAA(sf)/AAA(sf) | $118,970,000(8) | N/A | N/A | N/A | N/A | N/A |

Class X-C(7) | NR/AAA(sf)/BBB-(sf) | $59,485,000(8) | N/A | N/A | N/A | N/A | N/A |

Class X-D(7) | NR/AAA(sf)/NR | $34,700,000(8) | N/A | N/A | N/A | N/A | N/A |

Class X-E(7) | NR/AAA(sf)/NR | $24,785,000(8) | N/A | N/A | N/A | N/A | N/A |

Class X-F(7) | NR/AAA(sf)/NR | $41,309,997(8) | N/A | N/A | N/A | N/A | N/A |

| Class E | NR/BB(low)(sf)/BB-(sf) | $34,700,000 | 5.000% | 9.98 | 120 - 120 | 62.2% | 12.1% |

| Class F | NR/B(low)(sf)/B-(sf) | $24,785,000 | 3.125% | 9.98 | 120 - 120 | 63.5% | 11.9% |

| Class G | NR/NR/NR | $41,309,997 | 0.000% | 10.49 | 120 - 127 | 65.5% | 11.5% |

| (1) | The pass-through rates applicable to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F and Class G Certificates will equal one of: (i) a fixed per annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, (iii) a rate equal to the lesser of a specified pass-through rate and the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, or (iv) the weighted average of the net mortgage rates on the mortgage loans) (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, less a specified rate. |

| (2) | Approximate; subject to a permitted variance of plus or minus 5%. In addition, the notional amounts of the Class X-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates may vary depending upon the final pricing of the classes of certificates and whose Certificate Balances comprise such notional amounts and, if as a result of such pricing the pass-through rate of the Class X-A, Class X-B, Class X-C, Class X-D, Class X-E or Class X-F Certificates, as applicable, would be equal to zero, such class of certificates will not be issued on the settlement date of this securitization. |

| (3) | The weighted average life and principal window during which distributions of principal would be received as set forth in the table with respect to each class of certificates with a Certificate Balance is based on (i) modeling assumptions described in the Free Writing Prospectus, (ii) assumptions that there are no prepayments, delinquencies or losses on the mortgage loans and (iii) assumptions that there are no extensions of maturity dates and mortgage loans with anticipated repayment dates are repaid on the respective anticipated repayment dates. |

| (4) | “Certificate Principal to Value Ratio” for any class with a Certificate Balance is calculated as the product of (a) the weighted average Mortgage Loan Cut-off Date LTV of the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of the related class of Certificates and all other classes, if any, that are senior to such class, and the denominator of which is the total initial Certificate Balance of all Certificates. The Certificate Principal to Value Ratios of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are calculated in the aggregate for those classes as if they were a single class. |

| (5) | “Underwritten NOI Debt Yield” for any class with a Certificate Balance is calculated as the product of (a) the weighted average U/W NOI Debt Yield for the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of all Certificates and the denominator of which is the total initial Certificate Balance of the related class of Certificates and all other classes, if any, that are senior to such class. The Underwritten NOI Debt Yields of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are calculated in the aggregate for those classes as if they were a single class. |

| (6) | The initial subordination levels for the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are represented in the aggregate. |

| (7) | As further described in the Free Writing Prospectus, the pass-through rate applicable to the Class X-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates for each Distribution Date will generally be equal to the excess of (i) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary to accrue on the basis of a 360 day year consisting of twelve 30-day months), over (ii)(A) with respect to the Class X-A Certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M Certificates (based on their Certificate Balances), (B) with respect to the Class X-B Certificates, the weighted average of the pass-through rates of the Class B and Class C Certificates (based on their Certificate Balances), (C) with respect to the Class X-C Certificates, the pass-through rate of the Class D Certificates, (D) with respect to the Class X-D Certificates, the pass-through rate of the Class E Certificates, (E) with respect to the Class X-E Certificates, the pass-through rate of the Class F Certificates and (F) with respect to the Class X-F Certificates, the pass-through rate of the Class G Certificates. |

| (8) | The Class X-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates (the “Class X Certificates”) will not have Certificate Balances. None of the Class X Certificates will be entitled to distributions of principal. The interest accrual amounts on the Class X-A Certificates will be calculated by reference to a notional amount equal to the sum of the total Certificate Balances of each of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M Certificates. The interest accrual amounts on the Class X-B Certificates will be calculated by reference to a notional amount equal to the sum of the total Certificate Balances of each of the Class B and Class C Certificates. The interest accrual amounts on the Class X-C Certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class D Certificates. The interest accrual amounts on the Class X-D Certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class E Certificates. The interest accrual amounts on the Class X-E Certificates will be calculated by reference to a notional amount equal to the Certificate |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 5 |

COMM 2015-LC21 Mortgage Trust

SUMMARY OF THE CERTIFICATES |

Balance of the Class F Certificates. The interest accrual amounts on the Class X-F Certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class G Certificates.

Short-Term Certificate Principal Paydown Summary(1) |

| Class | Mortgage Loan Seller | Mortgage Loan | Property Type | Cut-off Date Balance | Remaining Term to Maturity (Mos.) | Cut-off Date LTV Ratio | U/W NCF DSCR | U/W NOI Debt Yield | |

| A-1 | KeyBank | Renaissance New Orleans Portfolio(2) | Hospitality | $19,458,449 | 55 | 60.6% | 1.54x | 12.9% | |

| A-1/A-2 | GACC | Courtyard by Marriott Portfolio(2) | Hospitality | $97,050,000 | 58 | 28.2% | 7.40x | 32.7% | |

| A-2 | CCRE | 24 Hour Fitness West Covina | Retail | $10,738,548 | 59 | 64.1% | 1.58x | 10.4% | |

| A-2 | GACC | North Stadium Business Center | Industrial | $10,360,000 | 59 | 59.9% | 1.97x | 9.0% | |

| A-2 | LCF | Value Place | Hospitality | $4,738,703 | 59 | 64.3% | 1.56x | 13.8% | |

| A-2/A-SB | KeyBank | Parkdale Shopping Center | Retail | $12,170,000 | 60 | 73.8% | 1.30x | 9.2% | |

| A-2/A-SB | CCRE | Centre Creek Plaza & Wells Fargo Building | Office | $10,650,000 | 60 | 76.3% | 1.35x | 9.5% | |

| A-2/A-SB | CCRE | McDowell Business Park | Industrial | $7,100,000 | 60 | 67.6% | 1.40x | 9.6% | |

| A-2/A-SB | KeyBank | Parkcrest Apartments | Multifamily | $6,150,000 | 60 | 72.4% | 1.39x | 9.9% | |

| (1) | This table identifies loans with balloon payments due during the principal paydown window assuming 0% CPR and no losses or extensions for the indicated Certificates. See “Yield and Maturity Considerations—Yield Considerations” in the Free Writing Prospectus. |

| (2) | With respect to the Courtyard by Marriott Portfolio Loan and Renaissance New Orleans Portfolio Loan LTV, DSCR and debt yield calculations include the related pari passu companion loans. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 6 |

COMM 2015-LC21 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Principal Payments: | Payments in respect of principal of the Certificates will be distributed, first, to the Class A-SB Certificates, until the Certificate Balance of such Class is reduced to the planned principal balance for the related Distribution Date set forth on Annex A-3 to the Free Writing Prospectus, then, to the Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class A-M, Class B, Class C, Class D, Class E, Class F and Class G Certificates, in that order, until the Certificate Balance of each such Class is reduced to zero. Notwithstanding the foregoing, if the total principal balance of the Class A-M, Class B, Class C, Class D, Class E, Class F and Class G Certificates have been reduced to zero as a result of loss allocation, payments in respect of principal of the Certificates will be distributed, first, to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates, on a pro rata basis, based on the Certificate Balance of each such Class, then, to the extent of any recoveries on realized losses, to the Class A-M, Class B, Class C, Class D, Class E, Class F and Class G Certificates, in that order, in each case until the Certificate Balance of each such Class is reduced to zero (or previously allocated realized losses have been fully reimbursed). Each Class of Class X Certificates will not be entitled to receive distributions of principal; however, (i) the notional amount of the Class X-A Certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M Certificates; (ii) the notional amount of the Class X-B Certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class B and Class C Certificates; (iii) the notional amount of the Class X-C Certificates will be reduced by the principal distributions and realized losses allocated to the Class D Certificates; (iv) the notional amount of the Class X-D Certificates will be reduced by the principal distributions and realized losses allocated to the Class E Certificates; (v) the notional amount of the Class X-E Certificates will be reduced by the principal distributions and realized losses allocated to the Class F Certificates; and (vi) the notional amount of the Class X-F Certificates will be reduced by the principal distributions and realized losses allocated to the Class G Certificates. | |

| Interest Payments: | On each Distribution Date, interest accrued for each Class of the Certificates at the applicable pass-through rate will be distributed in the following order of priority, to the extent of available funds: first, to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class X-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates, on a pro rata basis, based on the accrued and unpaid interest on each such Class and then, to the Class A-M, Class B, Class C, Class D, Class E, Class F and Class G Certificates, in that order, in each case until the interest payable to each such Class is paid in full. The pass-through rates applicable to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F and Class G Certificates for each Distribution Date will equal one of: (i) a fixed per annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, (iii) a rate equal to the lesser of a specified pass-through rate and the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, or (iv) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, less a specified rate. As further described in the Free Writing Prospectus, the pass-through rate applicable to the Class X-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates for each Distribution Date will generally be equal to the excess of (i) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months), over (ii) (A) with respect to the Class X-A Certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M Certificates (based on their Certificate Balances), (B) with respect to the Class X-B Certificates, the weighted average of the pass-through rates of the Class B and Class C Certificates (based on their Certificate Balances), (C) with respect to the Class X-C Certificates, the pass-through rate of the Class D Certificates, (D) with respect to the Class X-D Certificates, the pass-through rate of the Class E Certificates, |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 7 |

COMM 2015-LC21 Mortgage Trust |

| STRUCTURE OVERVIEW |

| (E) with respect to the Class X-E Certificates, the pass-through rate of the Class F Certificates and (F) with respect to the Class X-F Certificates, the pass-through rate of the Class G Certificates. | ||

| Prepayment Interest Shortfalls: | Prepayment interest shortfalls will be allocated pro rata based on interest entitlements, in reduction of the interest otherwise payable with respect to each of the interest-bearing certificate classes. | |

| Loss Allocation: | Losses will be allocated to each Class of Certificates entitled to principal in reverse alphabetical order starting with Class G through and including Class A-M and then to Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates on a pro rata basis based on the Certificate Balance of each such class. The notional amount of any Class of Class X Certificates will be reduced by the aggregate amount of realized losses allocated to Certificates that are components of the notional amount of such Class of Class X Certificates. | |

| Prepayment Premiums: | A percentage of all prepayment premiums (either fixed prepayment premiums or yield maintenance amounts) collected on the Mortgage Loans will be allocated to each of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C and Class D Certificates (the “YM P&I Certificates”) then entitled to principal distributions, which percentage will be equal to the product of (a) a fraction, not greater than one, the numerator of which is the amount of principal distributed to such Class on such Distribution Date and the denominator of which is the total amount of principal distributed to the holders of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C and Class D Certificates on such Distribution Date, and (b) a fraction (expressed as a percentage which can be no greater than 100% nor less than 0%), the numerator of which is the excess of the pass-through rate of each such Class of Certificates currently receiving principal over the relevant Discount Rate, and the denominator of which is the excess of the Mortgage Rate of the related Mortgage Loan over the relevant Discount Rate. |

Prepayment Premium Allocation Percentage for all YM P&I Certificates = |

| (Pass-Through Rate - Discount Rate) | X | The percentage of the principal distribution amount to such Class or trust component as described in (a) above | |||

(Mortgage Rate - Discount Rate) |

| The remaining percentage of the prepayment premiums will be allocated to the Class X-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates in the manner described in the Free Writing Prospectus. In general, this formula provides for an increase in the percentage of prepayment premiums allocated to the YM P&I Certificates then entitled to principal distributions relative to the Class X-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates as Discount Rates decrease and a decrease in the percentage allocated to such Classes as Discount Rates rise. | ||

| Loan Combinations: | The portfolio of Mortgaged Properties identified on Annex A–1 to the Free Writing Prospectus as Courtyard by Marriott Portfolio secures a Mortgage Loan with an outstanding principal balance as of the Cut–off Date of $97,050,000, evidenced by Note A-2B (the “Courtyard by Marriott Portfolio Loan”), representing approximately 7.3% of the Initial Outstanding Pool Balance, and also secures (i) three promissory notes (collectively referred to as the “Courtyard by Marriott Portfolio Pari Passu Companion Loans”), which are generally pari passu in right of payment with the Courtyard by Marriott Portfolio Loan, consisting of: (a) one promissory note designated as Note A-1 with an outstanding principal balance as of the Cut-off Date of $33,500,000, which was included in the COMM 2015-CCRE23 Mortgage Trust as a non-pooled mortgage loan, (b) one promissory note designated as Note A-2A with an outstanding principal balance as of the Cut-off Date of $100,000,000, which was included in the COMM 2015-CCRE23 Mortgage Trust and (c) one promissory note designated as Note A-2C with an outstanding principal balance as of the Cut-off Date of $84,450,000, which was included in the GSMS 2015-GC30 Mortgage Trust as a pooled mortgage loan; and (ii) one promissory note designated as Note B (the “Courtyard by Marriott Portfolio Subordinate Companion Loan”) with an outstanding principal balance as of the Cut-off Date of $355,000,000 which is subordinate in right of payment in respect of each of the Courtyard by Marriott Portfolio Loan and the Courtyard by Marriott Portfolio Pari Passu Companion Loans and was included in the COMM 2015-CCRE23 Mortgage Trust as a non-pooled mortgage loan. The Courtyard by Marriott Portfolio Loan, the Courtyard by Marriott Portfolio Pari Passu Companion Loans and |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 8 |

COMM 2015-LC21 Mortgage Trust |

| STRUCTURE OVERVIEW |

| the Courtyard by Marriott Portfolio Subordinate Companion Loan are collectively referred to herein as the “Courtyard by Marriott Portfolio Loan Combination”). The Courtyard by Marriott Portfolio Loan Combination is being serviced pursuant to the COMM 2015-CCRE23 pooling and servicing agreement and the related intercreditor agreement. For additional information regarding the Courtyard by Marriott Portfolio Loan Combination, see “Description of the Mortgage Pool—Loan Combinations—Courtyard by Marriott Portfolio Loan Combination” in the Free Writing Prospectus. The Mortgaged Property identified on Annex A–1 to the Free Writing Prospectus as La Gran Plaza secures a Mortgage Loan with an outstanding principal balance as of the Cut–off Date of $23,969,702, evidenced by Note A-2 (the “La Gran Plaza Loan”), representing approximately 1.8% of the outstanding principal balance, and also secures on a pari passu basis two companion loans that have an aggregate outstanding principal balance as of the Cut-off Date of $51,934,353, evidenced by Note A-1 (the “La Gran Plaza Note A-1 Companion Loan”), which is currently held by LCF, and which may be sold or further divided at any time (subject to compliance with the terms of the related co-lender agreement) and the Note A-3 (together with the La Gran Plaza Note A-1 Companion Loan, the “La Gran Plaza Pari Passu Companion Loans”), which was included in the COMM 2015-CCRE23 Mortgage Trust. The La Gran Plaza Loan and the La Gran Plaza Pari Passu Companion Loans are pari passu in right of payment and are collectively referred to herein as the “La Gran Plaza Loan Combination.” The La Gran Plaza Loan Combination is initially being serviced pursuant to the COMM 2015-CCRE23 pooling and servicing agreement and the related intercreditor agreement. On and after the securitization date of the La Gran Plaza Note A-1 Companion Loan (the “La Gran Plaza Note A-1 Securitization Date”), the servicing of the La Gran Plaza Loan Combination will transfer to the pooling and servicing agreement for that securitization. For additional information regarding the La Gran Plaza Loan Combination, see “Description of the Mortgage Pool—Loan Combinations—La Gran Plaza Loan Combination” in the Free Writing Prospectus. In addition, prior to the La Gran Plaza Note A-1 Securitization Date, CWCapital Asset Management LLC, if necessary, is expected to be the special servicer for the La Gran Plaza Loan Combination. On and after the La Gran Plaza Note A-1 Securitization Date, the special servicer under the pooling and servicing related to such securitization will be the special servicer. The portfolio of Mortgaged Properties identified on Annex A–1 to the Free Writing Prospectus as Renaissance New Orleans Portfolio secures a Mortgage Loan with an outstanding principal balance as of the Cut–off Date of $19,458,449, evidenced by Note A-2 (the “Renaissance New Orleans Portfolio Loan”), representing approximately 1.5% of the Initial Outstanding Pool Balance, and also secures on a pari passu basis one companion loan that has an outstanding principal balance as of the Cut-off Date of $23,782,549, evidenced by Note A-1 (the “Renaissance New Orleans Portfolio Pari Passu Companion Loan”), which was included in the JPMBB 2015-C28 Mortgage Trust. The Renaissance New Orleans Portfolio Loan and the Renaissance New Orleans Portfolio Pari Passu Companion Loan are pari passu in right of payment and are collectively referred to herein as the “Renaissance New Orleans Portfolio Loan Combination.” The Renaissance New Orleans Portfolio Loan Combination is being serviced pursuant to the JPMBB 2015-C28 pooling and servicing agreement and the related intercreditor agreement. For additional information regarding the Renaissance New Orleans Portfolio Loan Combination, see “Description of the Mortgage Pool—Loan Combinations—Renaissance New Orleans Portfolio Loan Combination” in the Free Writing Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 9 |

COMM 2015-LC21 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Control Rights and Directing Holder: | Certain Classes of Certificates (the “Control Eligible Certificates”) will have certain control rights over servicing matters with respect to each Mortgage Loan (other than the Courtyard by Marriott Portfolio Loan, the La Gran Plaza Loan and the Renaissance New Orleans Portfolio Loan and any Excluded Mortgage Loan). The majority owner or appointed representative of the Class of Control Eligible Certificates that is the Controlling Class (such owner or representative, the “Directing Holder”), will be entitled to direct the Special Servicer to take, or refrain from taking certain actions with respect to a Mortgage Loan (other than the Courtyard by Marriott Portfolio Loan, the La Gran Plaza Loan and the Renaissance New Orleans Portfolio Loan and any Excluded Mortgage Loan). Furthermore, the Directing Holder will also have the right to receive notice and consent to certain material actions that the Master Servicer and the Special Servicer proposes to take with respect to such Mortgage Loan (other than the Courtyard by Marriott Portfolio Loan, the La Gran Plaza Loan and the Renaissance New Orleans Portfolio Loan and any Excluded Mortgage Loan). It is expected that KKR Securities Holdings LLC or its affiliate will be the initial Directing Holder with respect to each Mortgage Loan (other than the Courtyard by Marriott Portfolio Loan, the La Gran Plaza Loan and the Renaissance New Orleans Portfolio Loan and any Excluded Mortgage Loan). An “Excluded Mortgage Loan” is a mortgage loan or loan combination with respect to which the Controlling Class Representative or any Controlling Class Certificateholder is a “Borrower Party”. A “Borrower Party” is a borrower, a manager of a mortgaged property or an affiliate, principal, partner, member, joint venturer, limited partner, employee, representative, director, advisor or investor in any of the foregoing or an agent of any of the foregoing. For a description of the directing holder for the Courtyard by Marriott Portfolio Loan Combination, the Gateway Business Center Phase II Loan Combination and the Renaissance New Orleans Portfolio Loan Combination see “Description of the Mortgage Pool—Loan Combinations” and “Description of the Pooling and Servicing Agreement—The Directing Holder” in the Free Writing Prospectus. Notwithstanding the foregoing, there will be no Directing Holder with respect to any Excluded Mortgage Loan. | |

| Control Eligible Certificates: | Class E, Class F and Class G Certificates. | |

| Controlling Class: | The Controlling Class will be the most subordinate Class of Control Eligible Certificates then outstanding that has an aggregate Certificate Balance, as notionally reduced by any Appraisal Reduction Amounts allocable to such Class, equal to no less than 25% of the initial Certificate Balance of such Class. The Controlling Class as of the Settlement Date will be the Class G Certificates. | |

| Appraised-Out Class: | Any Class of Control Eligible Certificates that has been determined, as a result of Appraisal Reductions Amounts allocable to such Class, to no longer be the Controlling Class. | |

Remedies Available to Holders of an Appraised-Out Class: | Holders of the majority of any Class of Control Eligible Certificates that is determined at any time of determination to no longer be the Controlling Class as a result of an allocation of an Appraisal Reduction Amounts in respect of such Class will have the right, at their sole expense, to require the Special Servicer to order a second appraisal for any Mortgage Loan (other than Non-Serviced Loans) for which an Appraisal Reduction Event has occurred. Upon receipt of the second appraisal, the Special Servicer will be required to determine, in accordance with the Servicing Standard, whether, based on its assessment of the second appraisal, a recalculation of the Appraisal Reduction Amount is warranted. If warranted, the Special Servicer will direct the Master Servicer to recalculate the Appraisal Reduction Amount based on the second appraisal, and if required by such recalculation, the Special Servicer will reinstate the Appraised-Out Class as the Controlling Class. The Holders of an Appraised-Out Class requesting a second appraisal will not be entitled to exercise any rights of the Controlling Class until such time, if any, as the Class is reinstated as the Controlling Class. | |

| Control Termination Event: | Will occur when no Class of Control Eligible Certificates has an aggregate Certificate Balance (as notionally or actually reduced by any Appraisal Reduction Amounts and Realized Losses) equal to or greater than 25% of the initial Certificate Balance of such Class. | |

| Upon the occurrence and the continuance of a Control Termination Event, the Directing Holder |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 10 |

COMM 2015-LC21 Mortgage Trust |

| STRUCTURE OVERVIEW |

will no longer have any Control Rights. The Directing Holder will no longer have the right to direct certain actions of the Special Servicer and will no longer have consent rights with respect to certain material actions that the Master Servicer or Special Servicer proposes to take with respect to a Mortgage Loan. Upon the occurrence and continuation of a Control Termination Event, the Directing Holder will retain non-binding consultation rights with respect to certain material actions that the Special Servicer proposes to take with respect to a Mortgage Loan. Such consultation rights will continue until the occurrence of a Consultation Termination Event. Notwithstanding the foregoing, a Control Termination Event is deemed to exist with respect to any Excluded Mortgage Loan. | ||

| Consultation Termination Event: | Will occur when, without giving regard to the application of any Appraisal Reduction Amounts (i.e., giving effect to principal reduction through Realized Losses only), there is no Class of Control Eligible Certificates that has an aggregate Certificate Balance equal to 25% or more of the initial Certificate Balance of such Class. Upon the occurrence and continuance of a Consultation Termination Event the Directing Holder will have no rights under the pooling and servicing for this securitization (the “Pooling and Servicing Agreement”) other than those rights that all Certificateholders have. Notwithstanding the foregoing, a Consultation Termination Event is deemed to exist with respect to any Excluded Mortgage Loan. | |

Appointment and Replacement of Special Servicer: | The Directing Holder will appoint the initial Special Servicer as of the Settlement Date. Prior to the occurrence and continuance of a Control Termination Event, the Special Servicer (other than with respect to the Courtyard by Marriott Portfolio Loan Combination, the La Gran Plaza Loan Combination and the Renaissance New Orleans Portfolio Loan Combination and any Excluded Mortgage Loan) may generally be replaced at any time by the Directing Holder. Upon the occurrence and during the continuance of a Control Termination Event, the Directing Holder will no longer have the right to replace the Special Servicer and such replacement (other than with respect to the Courtyard by Marriott Portfolio Loan, the La Gran Plaza Loan and the Renaissance New Orleans Portfolio Loan) will occur based on a vote of holders of all voting eligible Classes of Certificates as described below. See “Description of the Mortgage Pool—Loan Combinations” and “Description of the Pooling and Servicing Agreement” in the Free Writing Prospectus for a description of the special servicer appointment and replacement rights with respect to the Courtyard by Marriott Portfolio Loan Combination, the La Gran Plaza Loan Combination and the Renaissance New Orleans Portfolio Loan Combination. With respect to any Excluded Mortgage Loan, the replacement of the Special Servicer will only occur based on a vote of holders of all voting eligible Classes of Certificates as described below. | |

Replacement of Special Servicer by Vote of Certificateholders: | Other than with respect to the Courtyard by Marriott Portfolio Loan, the La Gran Plaza Loan and the Renaissance New Orleans Portfolio Loan, if a Control Termination Event has occurred and is continuing, upon (i) the written direction of holders of Certificates evidencing not less than 25% of the voting rights of all Classes of Certificates entitled to principal (taking into account the application of Appraisal Reduction Amounts to notionally reduce the Certificate Balances of Classes to which such Appraisal Reduction Amounts are allocable) requesting a vote to replace the Special Servicer with a replacement Special Servicer, (ii) payment by such requesting holders to the Certificate Administrator of all reasonable fees and expenses to be incurred by the Certificate Administrator in connection with administering such vote and (iii) delivery by such holders to the Certificate Administrator of written confirmations from each Rating Agency that the appointment of the replacement Special Servicer will not result in a downgrade of the Certificates, the Certificate Administrator will be required to promptly provide written notice to all certificateholders of such request and conduct the solicitation of votes of all Certificates in such regard. Upon the written direction (within 180 days) of (i) Holders of at least 75% of a Certificateholder Quorum or (ii) the Holders of more than 50% of the voting rights of each Class of Non-Reduced Certificates, the Trustee will immediately replace the Special Servicer with the replacement Special Servicer (other than with respect to the Courtyard by Marriott Portfolio Loan, the La Gran Plaza Loan and the Renaissance New Orleans Portfolio Loan). |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 11 |

COMM 2015-LC21 Mortgage Trust |

| STRUCTURE OVERVIEW |

| “Certificateholder Quorum” means, in connection with any solicitation of votes in connection with the replacement of the Special Servicer as described above, the holders of Certificates evidencing at least 75% of the aggregate voting rights (taking into account Realized Losses and the application of any Appraisal Reduction Amounts to notionally reduce the Certificate Balance of the Certificates) of all classes of Certificates entitled to principal, on an aggregate basis. | ||

| In addition, other than with respect to the Courtyard by Marriott Portfolio Loan, the La Gran Plaza Loan and the Renaissance New Orleans Portfolio Loan, after the occurrence of a Consultation Termination Event, if the Operating Advisor determines that the Special Servicer is not performing its duties in accordance with the Servicing Standard, the Operating Advisor will have the right to recommend the replacement of the Special Servicer (other than with respect to the Courtyard by Marriott Portfolio Loan, the La Gran Plaza Loan and the Renaissance New Orleans Portfolio Loan). The Operating Advisor’s recommendation to replace the Special Servicer (other than with respect to the Courtyard by Marriott Portfolio Loan, the La Gran Plaza Loan and the Renaissance New Orleans Portfolio Loan) must be confirmed by a majority of the voting rights of all Classes of Certificates entitled to principal (taking into account the application of Appraisal Reduction Amounts to notionally reduce the Certificate Balances of Classes to which such Appraisal Reduction Amounts are allocable) within 180 days from the time such recommendation is posted to the Certificate Administrator website and is subject to the receipt of written confirmations from each Rating Agency that the appointment of the replacement Special Servicer will not result in a downgrade of the Certificates. | ||

See“Description of the Mortgage Pool—Loan Combinations”and “Description of the Pooling and Servicing Agreement” in the Free Writing Prospectus for a description of the special servicer appointment and replacement rights with respect to the Courtyard by Marriott Portfolio Loan Combination, the La Gran Plaza Loan Combination and the Renaissance New Orleans Portfolio Loan Combination. | ||

Cap on Workout and Liquidation Fees: | The workout fees and liquidation fees payable to a Special Servicer under the Pooling and Servicing Agreement will be an amount equal to the lesser of: (1) 1.0% of each collection of interest and principal following a workout or liquidation and (2) $1,000,000 per workout or liquidation. All Modification Fees actually paid to the Special Servicer in connection with a workout or liquidation or in connection with any prior workout or partial liquidation that occurred within the prior 18 months will be deducted from the total workout and/or liquidation fees payable (other than Modification Fees earned while the Mortgage Loan was not in special servicing). In addition, the total amount of workout and liquidation fees actually payable by the Trust under the Pooling and Servicing Agreement will be capped in the aggregate at $1,000,000 for each related Mortgage Loan. If a new special servicer begins servicing the related Mortgage Loan, all amounts paid to the prior special servicer will be disregarded for purposes of calculating the cap. | |

| Special Servicer Compensation: | The special servicing fee will equal 0.25% per annum of the stated principal balance of the related specially serviced loan or REO property. The Special Servicer and its affiliates will be prohibited from receiving or retaining any compensation or any other remuneration under the Pooling and Servicing Agreement (including in the form of commissions, brokerage fees, rebates, or as a result of any other fee-sharing arrangement) from any person (including the issuing entity, any borrower, any manager, any guarantor or indemnitor in respect of a Mortgage Loan or Serviced Loan Combination, if any, and any purchaser of any Mortgage Loan, Serviced Companion Loan or REO Property) in connection with the disposition, workout or foreclosure of any Mortgage Loan or Serviced Loan Combination, the management or disposition of any REO Property, or the performance of any other special servicing duties under the Pooling and Servicing Agreement, other than as expressly permitted in the Pooling and Servicing Agreement and other than commercially reasonable treasury management fees, banking fees and insurance commissions or fees received or retained by the Special Servicer or any of its Affiliates in connection with any services performed by such party with respect to any mortgage loan. Subject to certain limited exceptions, the Special Servicer will also be required to report any compensation or other remuneration the Special Servicer or its affiliates have received from any person and such information will be disclosed in the Certificateholders’ monthly distribution date statement. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 12 |

COMM 2015-LC21 Mortgage Trust |

| STRUCTURE OVERVIEW |

Operating Advisor: | With respect to the Mortgage Loans (other than with respect to the Courtyard by Marriott Portfolio Loan Combination, the La Gran Plaza Loan Combination and the Renaissance New Orleans Portfolio Loan Combination) and prior to the occurrence of a Control Termination Event, the Operating Advisor will have access to any final asset status report and all information available with respect to the transaction on the Certificate Administrator’s website but will not have any approval or consultation rights. After the occurrence and during the continuance of a Control Termination Event, the Operating Advisor will have consultation rights with respect to certain major decisions and will have additional monitoring responsibilities on behalf of the entire trust. The Operating Advisor will be subject to termination if holders of at least 15% of the aggregate voting rights of the Certificates (in connection with termination and replacement relating to the Mortgage Loans) vote to terminate and replace the Operating Advisor and such vote is approved by holders of more than 50% of the applicable voting rights that exercise their right to vote, provided that holders of at least 50% of the applicable voting rights have exercised their right to vote. The holders initiating such vote will be responsible for the fees and expenses in connection with the vote and replacement. The Operating Advisor will not have consultation rights in respect of the Courtyard by Marriott Portfolio Loan Combination, the La Gran Plaza Loan Combination and the Renaissance New Orleans Portfolio Loan Combination. | |

| Liquidated Loan Waterfall: | On liquidation of any Mortgage Loan, all net liquidation proceeds will be applied so that amounts allocated as a recovery of accrued and unpaid interest will not, in the first instance, include any amount by which the interest portion of P&I Advances previously made was reduced as a result of Appraisal Reduction Amounts. After the adjusted interest amount is so allocated, any remaining net liquidation proceeds will be allocated to pay principal on the Mortgage Loan until the unpaid principal amount of the Mortgage Loan has been reduced to zero. Any remaining liquidation proceeds would then be allocated as a recovery of accrued and unpaid interest corresponding to the amount by which the interest portion of P&I Advances previously made was reduced as a result of Appraisal Reduction Amounts. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 13 |

COMM 2015-LC21 Mortgage Trust |

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Distribution of Cut-off Date Balances(1) |

Weighted Averages | |||||||||||||||||||||

| Range of Cut-off Date Balances | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut-off Date LTV Ratio(3) | Maturity Date or ARD LTV(3) | |||||||||||||

| $747,500 | - | $7,499,999 | 47 | $214,401,604 | 16.2% | 4.5292% | 115 | 1.51x | 69.2% | 57.2% | |||||||||||

| $7,500,000 | - | $14,999,999 | 25 | $265,091,996 | 20.1% | 4.3208% | 109 | 1.59x | 68.3% | 59.2% | |||||||||||

| $15,000,000 | - | $24,999,999 | 21 | $414,083,722 | 31.3% | 4.4412% | 116 | 1.57x | 68.6% | 58.6% | |||||||||||

| $25,000,000 | - | $49,999,999 | 8 | $257,513,675 | 19.5% | 4.1904% | 120 | 1.63x | 67.0% | 62.5% | |||||||||||

| $50,000,000 | - | $74,999,999 | 1 | $73,750,000 | 5.6% | 4.5300% | 120 | 1.70x | 70.9% | 57.4% | |||||||||||

| $75,000,000 | - | $97,050,000 | 1 | $97,050,000 | 7.3% | 3.6900% | 58 | 7.40x | 28.2% | 28.2% | |||||||||||

| Total/Weighted Average | 103 | $1,321,890,997 | 100.0% | 4.3323% | 111 | 2.01x | 65.5% | 56.9% | |||||||||||||

Distribution of Mortgage Rates(1) |

Weighted Averages | ||||||||||||||||||||||

| Range of Mortgage Rates | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut-off Date LTV Ratio(3) | Maturity Date or ARD LTV(3) | ||||||||||||||

| 3.6900% | - | 3.9999% | 8 | $218,350,000 | 16.5% | 3.8137% | 92 | 4.15x | 52.4% | 47.1% | ||||||||||||

| 4.0000% | - | 4.4999% | 58 | $737,196,787 | 55.8% | 4.2785% | 118 | 1.60x | 68.0% | 59.8% | ||||||||||||

| 4.5000% | - | 4.7499% | 17 | $208,567,816 | 15.8% | 4.5793% | 118 | 1.57x | 69.7% | 57.7% | ||||||||||||

| 4.7500% | - | 5.4640% | 20 | $157,776,394 | 11.9% | 4.9747% | 99 | 1.55x | 66.2% | 56.3% | ||||||||||||

| Total/Weighted Average | 103 | $1,321,890,997 | 100.0% | 4.3323% | 111 | 2.01x | 65.5% | 56.9% | ||||||||||||||

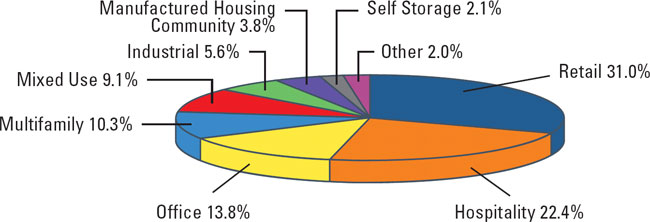

Property Type Distribution(1)(4) |

| Weighted Averages | ||||||||||||||||||||||||

| Property Type | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Number of Units/Rooms/Pads/ NRA/Beds | Cut-off Date Balance per Unit/Room/Pad/ NRA/Bed | Mortgage Rate | Stated Remaining Term (Mos.)(2) | Occupancy | U/W NCF DSCR | Cut-off Date LTV Ratio(3) | Maturity Date or ARD LTV(3) | |||||||||||||

| Retail | 65 | $409,635,830 | 31.0% | 2,674,484 | $484 | 4.4032% | 116 | 97.4% | 1.57x | 68.6% | 60.8% | |||||||||||||

Anchored(5) | 52 | $334,995,477 | 25.3% | 2,237,211 | $508 | 4.4131% | 115 | 97.7% | 1.58x | 68.1% | 61.0% | |||||||||||||

| Unanchored | 13 | $74,640,353 | 5.6% | 437,273 | $372 | 4.3588% | 119 | 95.9% | 1.55x | 70.7% | 60.1% | |||||||||||||

| Hospitality | 77 | $296,340,398 | 22.4% | 11,530 | $116,073 | 4.3641% | 94 | 79.9% | 3.58x | 54.4% | 46.5% | |||||||||||||

| Limited Service | 7 | $134,114,368 | 10.1% | 1,025 | $170,189 | 4.6977% | 120 | 84.9% | 1.72x | 67.4% | 54.8% | |||||||||||||

| Select Service | 65 | $97,050,000 | 7.3% | 9,590 | $42,408 | 3.6900% | 58 | 72.3% | 7.40x | 28.2% | 28.2% | |||||||||||||

| Full Service | 4 | $60,437,327 | 4.6% | 794 | $120,310 | 4.6778% | 99 | 80.5% | 1.73x | 67.1% | 56.7% | |||||||||||||

| Extended Stay | 1 | $4,738,703 | 0.4% | 121 | $39,163 | 4.7300% | 59 | 88.3% | 1.56x | 64.3% | 53.8% | |||||||||||||

| Office | 11 | $182,220,804 | 13.8% | 1,257,460 | $187 | 4.2536% | 116 | 93.1% | 1.65x | 65.6% | 59.3% | |||||||||||||

| Suburban | 7 | $77,650,000 | 5.9% | 583,019 | $144 | 4.1453% | 111 | 94.7% | 1.55x | 69.7% | 61.1% | |||||||||||||

| CBD | 3 | $69,870,804 | 5.3% | 388,054 | $268 | 4.4253% | 119 | 94.8% | 1.63x | 63.0% | 56.1% | |||||||||||||

| Suburban/Flex | 1 | $34,700,000 | 2.6% | 286,387 | $121 | 4.1500% | 119 | 86.3% | 1.91x | 61.5% | 61.5% | |||||||||||||

| Multifamily | 13 | $135,511,880 | 10.3% | 22,453 | $60,927 | 4.3125% | 116 | 95.1% | 1.42x | 72.3% | 63.9% | |||||||||||||

| Mixed Use | 8 | $119,655,853 | 9.1% | 1,496,601 | $22,000 | 4.2351% | 122 | 93.1% | 1.50x | 67.6% | 55.0% | |||||||||||||

| Office/Retail | 4 | $96,305,853 | 7.3% | 1,496,353 | $160 | 4.2338% | 123 | 91.7% | 1.52x | 67.3% | 54.8% | |||||||||||||

| Multifamily/Retail | 4 | $23,350,000 | 1.8% | 248 | $112,080 | 4.2402% | 119 | 98.8% | 1.42x | 68.4% | 55.6% | |||||||||||||

| Industrial | 7 | $74,321,004 | 5.6% | 1,982,231 | $60 | 4.4875% | 106 | 95.3% | 1.66x | 66.1% | 54.4% | |||||||||||||

| Manufactured Housing Community | 7 | $50,245,000 | 3.8% | 1,518 | $35,427 | 4.1640% | 119 | 84.0% | 1.60x | 73.6% | 64.1% | |||||||||||||

| Self Storage | 7 | $27,807,316 | 2.1% | 593,923 | $49 | 4.2468% | 119 | 84.5% | 1.45x | 72.3% | 59.8% | |||||||||||||

| Leased Fee | 3 | $26,152,913 | 2.0% | 423,428 | NAP | 3.9285% | 119 | NAP | 1.43x | 71.3% | 61.7% | |||||||||||||

| Total/Weighted Average | 198 | $1,321,890,997 | 100.0% | 4.3323% | 111 | 91.2% | 2.01x | 65.5% | 56.9% | |||||||||||||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 14 |

COMM 2015-LC21 Mortgage Trust |

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Geographic Distribution(1)(4) |

Weighted Averages | ||||||||||||||||||||

| State/Location | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut-off Date LTV Ratio(3) | Maturity Date or ARD LTV(3) | ||||||||||||

| California | 23 | $290,372,363 | 22.0% | 4.2832% | 111 | 2.02x | 63.9% | 55.9% | ||||||||||||

Southern(6) | 18 | $267,682,907 | 20.2% | 4.3121% | 113 | 1.79x | 65.7% | 57.3% | ||||||||||||

Northern(6) | 5 | $22,689,455 | 1.7% | 3.9421% | 88 | 4.71x | 42.5% | 38.8% | ||||||||||||

| Texas | 28 | $180,999,348 | 13.7% | 4.3942% | 110 | 1.64x | 69.5% | 59.8% | ||||||||||||

| Illinois | 14 | $81,165,739 | 6.1% | 4.2269% | 112 | 2.21x | 63.4% | 59.1% | ||||||||||||

| New York | 6 | $80,293,379 | 6.1% | 4.3836% | 117 | 1.86x | 61.7% | 58.3% | ||||||||||||

| New York City | 2 | $58,300,000 | 4.4% | 4.4647% | 119 | 1.70x | 62.7% | 62.7% | ||||||||||||

| Remaining New York State | 4 | $21,993,379 | 1.7% | 4.1685% | 112 | 2.30x | 59.2% | 46.6% | ||||||||||||

| Pennsylvania | 6 | $70,650,000 | 5.3% | 4.2595% | 120 | 1.60x | 69.4% | 54.4% | ||||||||||||

| Other | 121 | $618,410,169 | 46.8% | 4.3527% | 110 | 2.16x | 65.3% | 56.4% | ||||||||||||

| Total/Weighted Average | 198 | $1,321,890,997 | 100.0% | 4.3323% | 111 | 2.01x | 65.5% | 56.9% | ||||||||||||

Distribution of Cut-off Date LTV Ratios(1)(3) |

Weighted Averages | ||||||||||||||||||||||

| Range of Cut-off Date LTV Ratios | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut-off Date LTV Ratio | Maturity Date or ARD LTV | ||||||||||||||

| 28.2% | - | 54.9% | 8 | $174,593,932 | 13.2% | 3.9655% | 85 | 4.94x | 39.3% | 35.2% | ||||||||||||

| 55.0% | - | 59.9% | 6 | $37,053,801 | 2.8% | 4.4187% | 103 | 1.81x | 58.0% | 49.4% | ||||||||||||

| 60.0% | - | 64.9% | 11 | $188,727,985 | 14.3% | 4.4911% | 108 | 1.70x | 62.6% | 58.2% | ||||||||||||

| 65.0% | - | 69.9% | 30 | $306,246,196 | 23.2% | 4.4710% | 118 | 1.63x | 67.3% | 59.6% | ||||||||||||

| 70.0% | - | 74.9% | 32 | $448,244,083 | 33.9% | 4.3005% | 117 | 1.48x | 72.7% | 61.0% | ||||||||||||

| 75.0% | - | 76.3% | 16 | $167,025,000 | 12.6% | 4.3481% | 116 | 1.49x | 75.1% | 64.2% | ||||||||||||

| Total/Weighted Average | 103 | $1,321,890,997 | 100.0% | 4.3323% | 111 | 2.01x | 65.5% | 56.9% | ||||||||||||||

Distribution of Maturity Date or ARD LTV Ratios(1)(3) |

Weighted Averages | ||||||||||||||||||||||

Range of LTV Ratios at Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut-off Date LTV Ratio | Maturity Date or ARD LTV | ||||||||||||||

| 7.6% | - | 49.9% | 10 | $155,687,733 | 11.8% | 3.9903% | 81 | 5.27x | 37.7% | 31.6% | ||||||||||||

| 50.0% | - | 54.9% | 16 | $187,862,132 | 14.2% | 4.4090% | 118 | 1.72x | 62.5% | 53.1% | ||||||||||||

| 55.0% | - | 59.9% | 32 | $342,485,978 | 25.9% | 4.4710% | 112 | 1.60x | 69.6% | 57.9% | ||||||||||||

| 60.0% | - | 64.9% | 30 | $426,658,979 | 32.3% | 4.3190% | 119 | 1.50x | 70.6% | 61.8% | ||||||||||||

| 65.0% | - | 69.9% | 13 | $186,376,175 | 14.1% | 4.2811% | 116 | 1.59x | 71.2% | 67.4% | ||||||||||||

| 70.0% | - | 74.1% | 2 | $22,820,000 | 1.7% | 4.6173% | 60 | 1.32x | 75.0% | 72.0% | ||||||||||||

| Total/Weighted Average | 103 | $1,321,890,997 | 100.0% | 4.3323% | 111 | 2.01x | 65.5% | 56.9% | ||||||||||||||

Distribution of Underwritten NCF Debt Service Coverage Ratios(1) |

Weighted Averages | ||||||||||||||||||||||

| Range of Underwritten NCF Debt Service Coverage Ratios | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut-off Date LTV Ratio(3) | Maturity Date or ARD LTV(3) | ||||||||||||||

| 1.25x | - | 1.39x | 27 | $298,674,665 | 22.6% | 4.3397% | 113 | 1.33x | 72.6% | 62.2% | ||||||||||||

| 1.40x | - | 1.44x | 15 | $182,071,578 | 13.8% | 4.3090% | 119 | 1.42x | 71.9% | 60.2% | ||||||||||||

| 1.45x | - | 1.54x | 12 | $73,032,179 | 5.5% | 4.5555% | 102 | 1.49x | 67.4% | 56.5% | ||||||||||||

| 1.55x | - | 1.74x | 26 | $381,619,809 | 28.9% | 4.4968% | 117 | 1.65x | 67.6% | 58.7% | ||||||||||||

| 1.75x | - | 1.99x | 18 | $251,317,767 | 19.0% | 4.2915% | 116 | 1.84x | 63.9% | 57.0% | ||||||||||||

| 2.00x | - | 2.49x | 4 | $38,125,000 | 2.9% | 4.2144% | 119 | 2.15x | 59.0% | 55.2% | ||||||||||||

| 2.50x | - | 7.40x | 1 | $97,050,000 | 7.3% | 3.6900% | 58 | 7.40x | 28.2% | 28.2% | ||||||||||||

| Total/Weighted Average | 103 | $1,321,890,997 | 100.0% | 4.3323% | 111 | 2.01x | 65.5% | 56.9% | ||||||||||||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 15 |

COMM 2015-LC21 Mortgage Trust |

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Original Terms to Maturity or ARD(1)(2) |

Weighted Averages | ||||||||||||||||||||

Original Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(3) | Maturity Date or ARD LTV(3) | ||||||||||||

| 60 | 9 | $178,415,701 | 13.5% | 4.1686% | 58 | 4.72x | 45.8% | 44.0% | ||||||||||||

| 120 | 93 | $1,101,175,297 | 83.3% | 4.3620% | 119 | 1.60x | 68.4% | 58.9% | ||||||||||||

| 129 | 1 | $42,300,000 | 3.2% | 4.2500% | 127 | 1.42x | 73.2% | 61.7% | ||||||||||||

| Total/Weighted Average | 103 | $1,321,890,997 | 100.0% | 4.3323% | 111 | 2.01x | 65.5% | 56.9% | ||||||||||||

Distribution of Remaining Terms to Maturity or ARD(1)(2) |

Weighted Averages | ||||||||||||||||||||||

Range of Remaining Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(3) | Maturity Date or ARD LTV(3) | ||||||||||||||

| 55 | - | 60 | 9 | $178,415,701 | 13.5% | 4.1686% | 58 | 4.72x | 45.8% | 44.0% | ||||||||||||

| 115 | - | 120 | 93 | $1,101,175,297 | 83.3% | 4.3620% | 119 | 1.60x | 68.4% | 58.9% | ||||||||||||

| 127 | - | 127 | 1 | $42,300,000 | 3.2% | 4.2500% | 127 | 1.42x | 73.2% | 61.7% | ||||||||||||

| Total/Weighted Average | 103 | $1,321,890,997 | 100.0% | 4.3323% | 111 | 2.01x | 65.5% | 56.9% | ||||||||||||||

Distribution of Underwritten NOI Debt Yields(1) |

Weighted Averages | ||||||||||||||||||||||

| Range of Underwritten NOI Debt Yields | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut-off Date LTV Ratio(3) | Maturity Date or ARD LTV(3) | ||||||||||||||

| 7.3% | - | 7.9% | 9 | $205,163,675 | 15.5% | 4.3176% | 119 | 1.53x | 68.2% | 64.5% | ||||||||||||

| 8.0% | - | 8.9% | 25 | $283,402,408 | 21.4% | 4.2262% | 119 | 1.48x | 69.9% | 61.0% | ||||||||||||

| 9.0% | - | 9.9% | 20 | $238,992,564 | 18.1% | 4.3648% | 109 | 1.48x | 71.0% | 62.0% | ||||||||||||

| 10.0% | - | 12.4% | 35 | $383,098,645 | 29.0% | 4.4549% | 118 | 1.70x | 67.7% | 56.1% | ||||||||||||

| 12.5% | - | 14.9% | 12 | $99,183,705 | 7.5% | 4.6767% | 104 | 1.78x | 63.5% | 52.2% | ||||||||||||

| 15.0% | - | 32.7% | 2 | $112,050,000 | 8.5% | 3.8338% | 66 | 6.64x | 31.7% | 29.0% | ||||||||||||

| Total/Weighted Average | 103 | $1,321,890,997 | 100.0% | 4.3323% | 111 | 2.01x | 65.5% | 56.9% | ||||||||||||||

Amortization Types(1) |

Weighted Averages | ||||||||||||||||||||

| Amortization Type | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut-off Date LTV Ratio(3) | Maturity Date or ARD LTV(3) | ||||||||||||

| Amortizing Balloon | 48 | $497,681,274 | 37.6% | 4.5060% | 116 | 1.58x | 68.4% | 55.0% | ||||||||||||

| Interest Only, then Amortizing | 39 | $461,170,000 | 34.9% | 4.2896% | 116 | 1.50x | 71.2% | 62.1% | ||||||||||||

| Interest Only | 10 | $289,310,000 | 21.9% | 4.1276% | 97 | 3.66x | 50.5% | 50.5% | ||||||||||||

| Interest Only, ARD | 3 | $35,491,175 | 2.7% | 4.2635% | 115 | 1.81x | 69.7% | 69.7% | ||||||||||||

| Interest Only, then Amortizing, ARD | 1 | $21,500,000 | 1.6% | 3.8100% | 119 | 1.38x | 72.6% | 60.9% | ||||||||||||

| Amortizing Balloon, ARD | 2 | $16,738,548 | 1.3% | 4.6983% | 81 | 1.57x | 61.3% | 50.3% | ||||||||||||

| Total/Weighted Average | 103 | $1,321,890,997 | 100.0% | 4.3323% | 111 | 2.01x | 65.5% | 56.9% | ||||||||||||

Footnotes:

| (1) | With respect to the Courtyard by Marriott Portfolio Loan, the La Gran Plaza Loan and the Renaissance New Orleans Portfolio Loan, LTV, DSCR, debt yield, and cut-off date balance per Unit/Room/Pad/NRA/Bed calculations include the related pari passu companion loan(s). With respect to one group of three cross-collateralized and cross-defaulted mortgage loans, LTV, DSCR and debt yield calculations for such group of mortgage loans have been calculated on an aggregate basis. |

| (2) | In the case of the six mortgage loans with anticipated repayment dates, Original Terms to Maturity or ARD and Remaining Terms to Maturity or ARD is through the related anticipated repayment date. |

| (3) | With respect to seven mortgage loans, representing approximately 7.1% of the initial outstanding principal balance, the Cut-off Date LTV Ratio and Maturity Date or ARD LTV have in certain cases been calculated based on the “as complete”, “as renovated” or “hypothetical as is” value. For additional information, see the Footnotes to Annex A-1 in the Free Writing Prospectus. |

| (4) | Reflects allocated loan amount for properties securing multi-property mortgage loans. |

| (5) | Anchored retail includes anchored, single tenant, shadow anchored and other properties. |

| (6) | Northern California properties have a zip code greater than 93600. Southern California properties have a zip code less than or equal to 93600. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 16 |

COMM 2015-LC21 Mortgage Trust |

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Ten Largest Mortgage Loans |

Mortgage Loan | Mortgage Loan Seller | City, State | Property Type | Cut-off Date Balance | % of Initial Outstanding Pool Balance | Cut-off Date Balance per Room/NRA/Bed(1) | Cut-off Date LTV Ratio(1)(2) | U/W NCF DSCR(1) | U/W NOI Debt Yield(1) | ||||||||||

| Courtyard by Marriott Portfolio | GACC | Various, Various | Hospitality | $97,050,000 | 7.3% | $32,847 | 28.2% | 7.40x | 32.7% | ||||||||||

| Courtyard by Marriott Pasadena | GACC | Pasadena, CA | Hospitality | 73,750,000 | 5.6% | $234,873 | 70.9% | 1.70x | 11.4% | ||||||||||

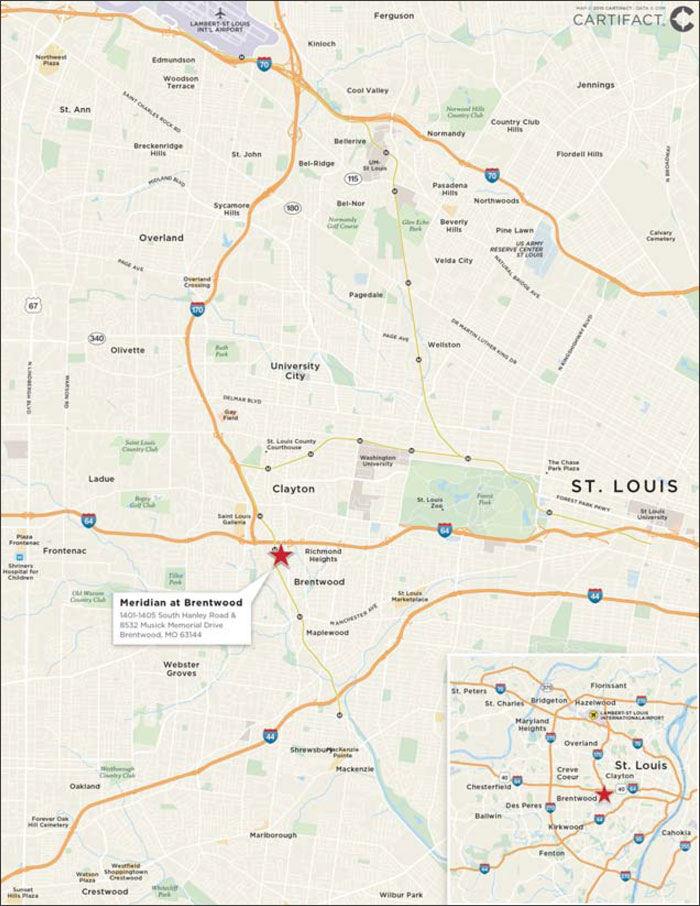

| Meridian at Brentwood | GACC | Brentwood, MO | Mixed Use | 42,300,000 | 3.2% | $175 | 73.2% | 1.42x | 9.2% | ||||||||||

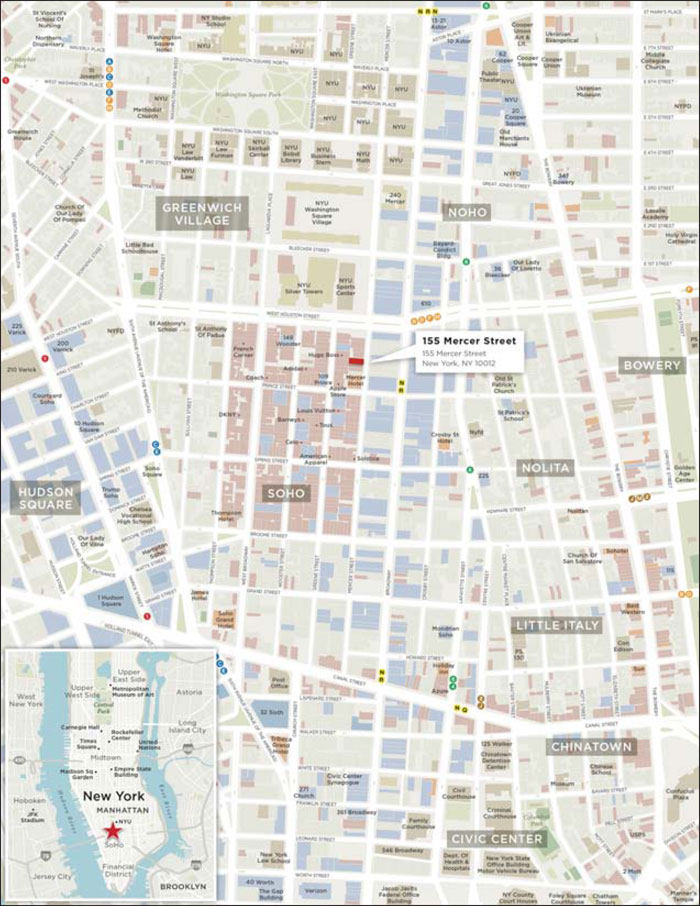

| 155 Mercer Street | CCRE | New York, NY | Retail | 41,000,000 | 3.1% | $2,810 | 63.1% | 1.57x | 7.3% | ||||||||||

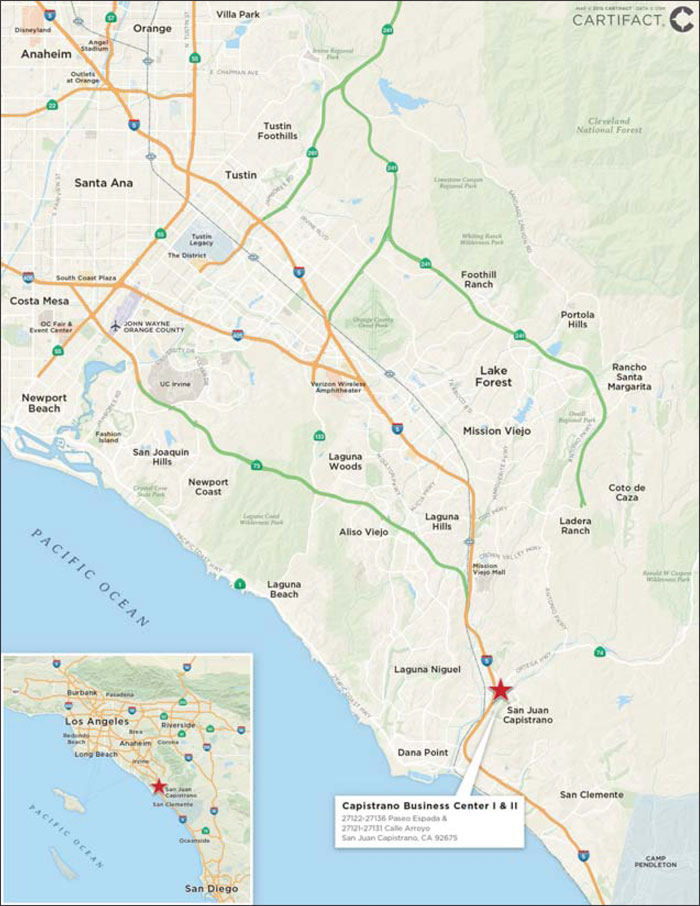

| Capistrano Business Center I & II | GACC | San Juan Capistrano, CA | Office | 34,700,000 | 2.6% | $121 | 61.5% | 1.91x | 8.9% | ||||||||||

| Walgreens Net Lease Portfolio V | KeyBank | Various, Various | Retail | 33,963,675 | 2.6% | $287 | 69.9% | 1.81x | 7.8% | ||||||||||

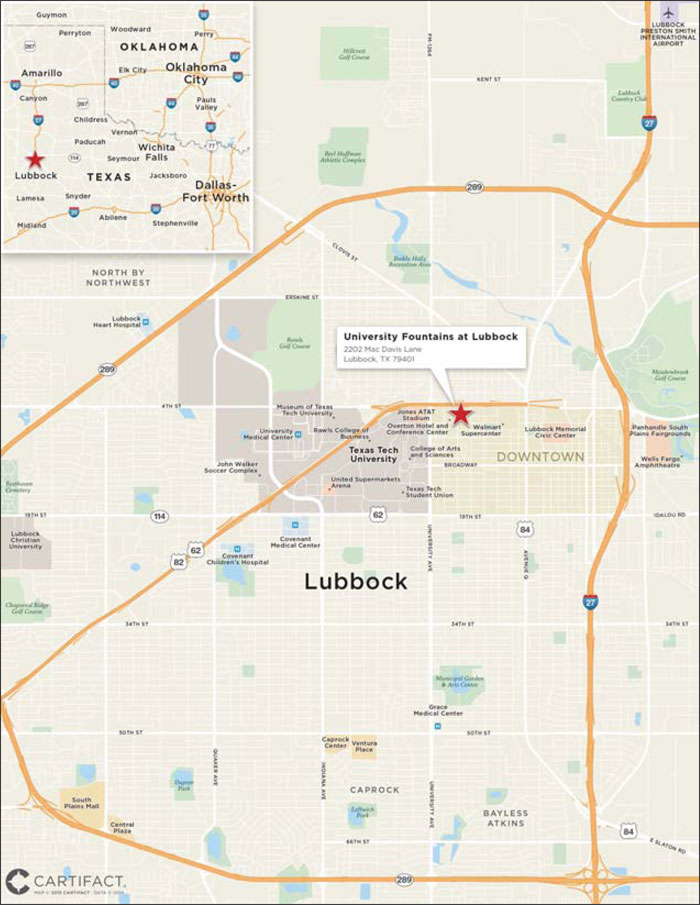

| University Fountains at Lubbock | KeyBank | Lubbock, TX | Multifamily | 27,400,000 | 2.1% | $40,117 | 75.1% | 1.38x | 8.3% | ||||||||||

| Santa Monica Clock Tower | GACC | Santa Monica, CA | Office | 26,700,000 | 2.0% | $490 | 54.5% | 1.80x | 8.2% | ||||||||||

| Delaware Corporate Center I & II | LCF | Wilmington, DE | Office | 26,450,000 | 2.0% | $132 | 67.3% | 1.75x | 10.9% | ||||||||||

| Ortega Ranch | GACC | San Juan Capistrano, CA | Office | 25,000,000 | 1.9% | $174 | 70.4% | 1.42x | 8.6% | ||||||||||

| Total/Weighted Average | $428,313,675 | 32.4% | 58.9% | 2.95x | 14.5% | ||||||||||||||

| (1) | With respect to the Courtyard by Marriott Portfolio Loan, the numerical and statistical information related to the LTV, DSCR, debt yield and cut-off date balances per Room includes the Courtyard by Marriott Portfolio Pari Passu Companion Loans, but does not include the Courtyard by Marriott Portfolio Subordinate Companion Loan unless otherwise specified. |

| (2) | With respect to the University Fountains at Lubbock Loan, the Cut-off Date LTV Ratio has been calculated using the “as renovated” value. The “as renovated” appraised value takes into account capital expenditures at the property, for which $1.8 million was reserved at closing. The “as is” appraised value Cut-off Date LTV Ratio is 79.4%. |

| Pari Passu Companion Loan Summary |

| Mortgage Loan | Mortgage Loan Cut-off Date Balance | Companion Loans Cut-off Date Balance | Loan Combination Cut-off Date Balance | Pooling & Servicing Agreement | Master Servicer | Special Servicer | Voting Rights | ||||||||

| Courtyard by Marriott Portfolio | $97,050,000 | $572,950,000(1) | $670,000,000 | (1) | COMM 2015-CCRE23 | Midland Loan Services | CWCapital Asset Management, LLC | COMM 2015-CCRE23 | |||||||

| La Gran Plaza | $23,969,702 | $51,934,353 | $75,904,055 | See (2) below | See (2) below | See (2) below | See (2) below | ||||||||

| Renaissance New Orleans Portfolio | $19,458,449 | $23,782,549 | $43,240,998 | JPMBB 2015-C28 | Wells Fargo Bank, National Association | Torchlight Loan Services, LLC | JPMBB 2015-C28 | ||||||||

| (1) | The Courtyard by Marriott Portfolio Companion Loans Cut-off Date Balance and Loan Combination Cut-off Date Balance is comprised of the three pari passu companion loans and a B-Note in the amount of $355,000,000. |

| (2) | Prior to the securitization of the La Gran Plaza pari passu companion loan designated as Note A-1, the La Gran Plaza Loan Combination will be serviced under the COMM 2015-CCRE23 pooling and servicing agreement and the related intercreditor agreement, and the directing holder will be the holder of such Note A-1, which initially is expected to be LCF or an affiliate thereof. After the securitization of the La Gran Plaza pari passu companion loan designated as Note A-1, it is expected that the La Gran Plaza Loan Combination will be serviced under the pooling and servicing agreement entered into in connection with that securitization and the related intercreditor agreement, and it is expected that the directing holder of the La Gran Plaza Loan Combination will be the directing holder or its equivalent under that securitization. See “Description of the Mortgage Pool—Loan Combinations—The La Gran Plaza Loan Combination” in the Free Writing Prospectus. |

| Existing Mezzanine Debt Summary |

| Mortgage Loan | Mortgage Loan Cut-off Date Balance | Mezzanine Debt Cut-off Date Balance | Trust U/W NCF DSCR | Total Debt U/W NCF DSCR | Trust Cut-off Date LTV Ratio | Total Debt Cut-off Date LTV Ratio | Trust U/W NOI Debt Yield | Total Debt U/W NOI Debt Yield | ||||||||||||

Walgreens Net Lease Portfolio V(1) | $33,963,675 | $9,694,360 | 1.81x | 1.55x | 69.9% | 89.9% | 7.8% | 6.1% | ||||||||||||

| Komar Desert Center | $17,055,000 | $1,221,427 | 1.38x | 1.19x | 71.1% | 76.2% | 9.0% | 8.4% | ||||||||||||

| aLoft Hotel Minneapolis | $16,000,000 | $1,750,000 | 1.58x | 1.33x | 65.3% | 72.4% | 12.0% | 10.8% | ||||||||||||

| Hilton Garden Inn – Phoenix Airport North | $15,900,000 | $2,639,200 | 1.70x | 1.30x | 67.4% | 78.6% | 13.1% | 11.2% | ||||||||||||

| 24 Hour Fitness West Covina | $10,738,548 | $1,833,894 | 1.58x | 1.15x | 64.1% | 75.1% | 10.4% | 8.9% | ||||||||||||

| Golfsmith Richmond | $3,900,000 | $700,000 | 1.56x | 1.09x | 66.1% | 78.0% | 9.8% | 8.3% | ||||||||||||

| (1) | With respect to the Walgreens Net Lease Portfolio V Loan, the lender allocated $9,694,360 of mezzanine proceeds for illustration of combined debt metrics. See Collateral Asset Summary – Loan No. 6, herein. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 17 |

COMM 2015-LC21 Mortgage Trust |

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Previous Securitization History(1) |

| Mortgage Loan | Mortgage Loan Seller | City, State | Property Type | Cut-off Date Balance | % of Initial Outstanding Pool Balance | Previous Securitization | |||||||

| Courtyard by Marriott Portfolio | GACC | Various, Various | Hospitality | $97,050,000 | 7.3% | Various(2) | |||||||

| Courtyard by Marriott Pasadena | GACC | Pasadena, CA | Hospitality | $73,750,000 | 5.6% | CGCMT 2007-C6 | |||||||

| Capistrano Business Center I & II | GACC | San Juan Capistrano, CA | Office | $34,700,000 | 2.6% | Various(3) | |||||||

| Santa Monica Clock Tower | GACC | Santa Monica, CA | Office | $26,700,000 | 2.0% | MSC 2006-HQ10 | |||||||

| 26-34 South State Street | GACC | Chicago, IL | Retail | $24,000,000 | 1.8% | MLCFC 2006-3 | |||||||