Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM1-K

| ☒ | ANNUAL REPORT FOR THE FISCAL YEAR ENDED DECEMBER 31, 2018 |

OR

| ☐ | Special Financial report for the fiscal year ended December 31, 2018 |

Cottonwood Multifamily REIT I, Inc.

(Exact name of registrant as specified in its charter)

| Maryland | 36-4812393 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 6340 South 3000 East, Suite 500, Salt Lake City, UT | 84121 | |

| (Address of principal executive offices) | (Zip Code) | |

(801)278-0700

(Registrant’s telephone number, including area code)

Title of each class of securities issued pursuant to Regulation A:

Unclassified Shares of Common Stock

Table of Contents

Cottonwood Multifamily REIT I, Inc.

ANNUAL REPORT ON FORM1-K

For the Year Ended December 31, 2018

| ITEM 1. | BUSINESS | 1 | ||

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 3 | ||

| ITEM 3. | 7 | |||

| ITEM 4. | SECURITY OWNERSHIP OF MANAGEMENT AND CERTAIN SECURITYHOLDERS | 11 | ||

| ITEM 5. | 11 | |||

| ITEM 6. | 11 | |||

| ITEM 7. | F-1 | |||

| ITEM 8. | ||||

Table of Contents

| Item 1. | Business |

The Company

Cottonwood Multifamily REIT I, Inc. is Maryland corporation formed on June 22, 2015 to invest in multifamily apartment communities located throughout the United States. The use of the terms the “Company,” “we,” “us,” or “our” in this annual report refers to Cottonwood Multifamily REIT I, Inc., unless the context indicates otherwise.

We completed our $50,000,000 offering that was qualified as a “Tier 2” offering pursuant to Regulation A promulgated under the Securities Act in April 2017, raising the full offering amount from approximately 1,300 investors. We may pursue additional offerings at the discretion of our board of directors.

We have no employees; we have engaged a subsidiary of Cottonwood Residential O.P., LP (“CROP”) to act as our asset manager and property manager. We rely on our board of directors, and the team of real estate professionals that CROP has assembled for theday-to-day operation of our business. Cottonwood Residential II, Inc. is a general partner of CROP, its operating partnership, and makes all decisions on behalf of CROP.

From the launch of our offering in May 2016 Cottonwood Capital Property Management II, LLC, has acted as our property manager. Additionally, from the launch of our offering through February 28, 2019, it also acted as our asset manager. Effective March 1, 2019, CC Advisors I, LLC (“CC Advisors I”) acts as our asset manager. See “Restructure of Asset Manager” below for additional information regarding the change in our asset manager.

We operate under the direction of our board of directors, the members of which are accountable to us and our shareholders as fiduciaries. Our board of directors is responsible for the management and control of our affairs. We have three members on our board of directors, all of whom are on the board of directors and are officers of Cottonwood Residential II, Inc. As a result, we do not have independent management. Our board of directors is classified into three classes. Each class of directors is elected for successive terms ending at the annual meeting of the shareholders the third year after election and until his or her successor is elected and qualified. The board of directors has the right, with input from our investment committee, to make decisions regarding investments by our operating partnership.

We have elected to be taxed as a REIT under the Internal Revenue Code of 1986, as amended (the “Code”). As of December 31, 2018, our portfolio was comprised of three investments in joint ventures owning Class A multifamily apartment communities in various locations throughout the United States.

Restructure of Asset Manager

As a result of the determination by CROP to restructure the ownership of our asset manager, effective March 1, 2019, our asset management agreement was assigned to a newly formed affiliate of CROP, CC Advisors I. As our new asset manager, CC Advisors I, is responsible for the asset management services rendered to us. Property management services will continue to be provided by Cottonwood Capital Property Management II, LLC.

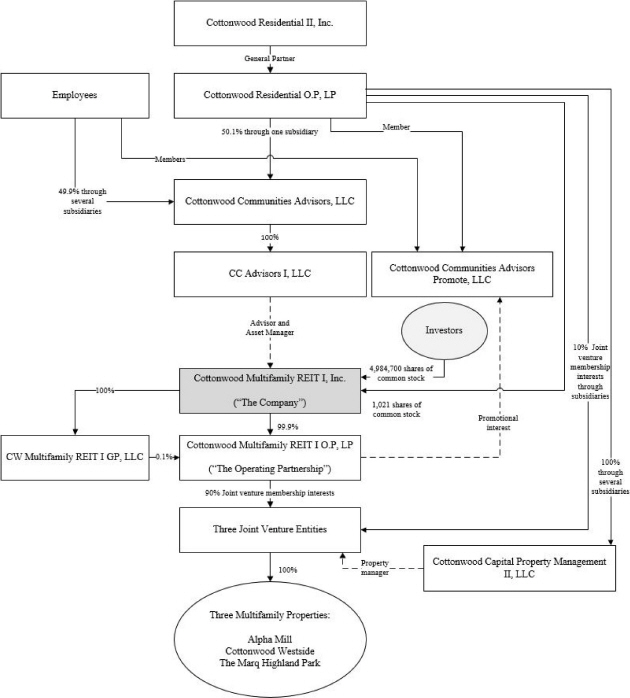

CROP will continue to have an indirect ownership interest in the new asset manager, CC Advisors I; however, two additional entities in which employees of CROP and its affiliates have an ownership interest will also have an indirect ownership interest in our new asset manager. As our asset manager will be an affiliate, our new asset manager will continue to rely on the same expertise and experience to provide our asset management services. In addition, as part of the restructuring, a new entity, Cottonwood Communities Advisors Promote, LLC (“CC Advisors Promote”), owns the promotional interest in our investments previously held by CROP. The fees and services to be provided to us remain unchanged following these changes.

1

Table of Contents

The chart below shows the relationships among our company and its affiliates following the change in our asset manager:

Investment Strategy

All of our investments have been made through joint ventures with CROP. We anticipate holding and managing our investments until December 31, 2023, the termination date. The termination date may be extended by the board for an additional two years, with an additionaltwo-year extension available by a majority vote of the shareholders. If approvals for extension are not met, we will begin an orderly sale of our assets within aone-year period from the date the decision not to extend was made. The termination date may be accelerated in the sole discretion of the board of directors. It is possible that we could merge with entities affiliated with our sponsor, including Cottonwood Residential II, Inc., a general partner of CROP.

2

Table of Contents

In the event that a listing occurs on or before the termination date, we will continue perpetually unless we are dissolved pursuant to a vote of our shareholders and other any applicable statutory provisions. A listing shall mean the commencement of trading of our common stock on any securities exchange registered as a national securities exchange, any over the counter exchange or, as determined in the sole discretion of our board of directors, any similar exchange that offers sufficient trading to offer similar liquidity to our shareholders. A listing shall also be deemed to occur on the effective date of a merger in which the consideration received by our shareholders is securities of another entity that are listed on any securities exchange registered as a national securities exchange, any over the counter exchange or, as determined in the sole discretion of our board of directors, any similar exchange that offers sufficient trading to offer similar liquidity to our shareholders.

Investment Objectives

Our investment objectives are to:

| • | preserve, protect and return invested capital; |

| • | pay stable cash distributions to shareholders; and |

| • | realize capital appreciation in the value of our investments over the long term. |

Our board of directors may revise our investment policies without the approval of our shareholders.

Risk Factors

We face risks and uncertainties that could affect us and our business as well as the real estate industry in general. These risks are outlined under the heading “Risk Factors” contained in our Offering Circular, which may be updated from time to time by our future filings under Regulation A. In addition, new risks may emerge at any time, and we cannot predict such risks or estimate the extent to which they may affect our financial performance. These risks could result in a decrease in the value of our common shares.

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Cautionary Statement Regarding Forward-Looking Statements

This Annual Reporton Form 1-K contains forward-looking statements. You can generally identify forward-looking statements by our use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “anticipate,” “estimate,” “believe,” “continue,” or other similar words. You should not rely on these forward-looking statements because the matters they describe are subject to known and unknown risks, uncertainties and other unpredictable factors, many of which are beyond our control. Our actual results, performance and achievements may be materially different from those expressed or implied by these forward-looking statements.

Except as otherwise required by federal securities laws, we do not undertake to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Overview

Cottonwood Multifamily REIT I, Inc. is Maryland corporation formed to acquire and own directly or indirectly multifamily apartment communities located throughout the United States. We completed our $50,000,000 offering that was qualified as a “Tier 2” offering pursuant to Regulation A promulgated under the Securities Act in April 2017 after raising the full offering amount.

Our Investments

Proceeds from our offering were used to acquire 90% membership interests in three joint ventures formed by us and subsidiaries of CROP. Each joint venture acquired one of the properties below:

Property Name | Property Location | Units | Net Rentable Square Feet | Average Unit Size | Year Built | Occupancy at December 31, 2018 | Date Acquired by the Joint Ventures | |||||||||||||

Alpha Mill | Charlotte, NC | 267 | 222,411 | 833 | 2007, 2014 | 96.2% | August 3, 2016 | |||||||||||||

Cottonwood Westside | Atlanta, GA | 197 | 169,223 | 859 | 2015 | 96.4% | August 3, 2016 | |||||||||||||

The Marq Highland Park | Tampa, FL | 243 | 238,748 | 983 | 2015 | 94.1% | August 3, 2016 | |||||||||||||

More information regarding our investments can be foundhere.

3

Table of Contents

Sources of Operating Revenue and Cash Flow

Revenue and cash flow is generated from operations of the properties acquired through our unconsolidated joint venture investments with subsidiaries of CROP.

Profitability and Performance Metrics

We calculate funds from operations (“FFO”) and core funds from operations (“Core FFO”) to evaluate the profitability and performance of our business. See“Non-GAAP Financial Measures” below for a description of these metrics. All of our investing activities relate to commercial real estate and are all considered a single reportable business segment for financial reporting purposes. All of our investments have similar economic characteristics and are evaluated using similar criteria.

Market Outlook and Recent Trends

Overview

We believe that current market dynamics and underlying fundamentals suggest the positive trends in United States multifamily housing will continue. Steady job growth, low unemployment, increased rentership rates, increasing household formation and aligned demographics provide the backdrop for strong renter demand. We believe that other factors impacting the prime United States renter demographic such as delayed major life decisions, increased levels of student debt and tight credit standards in the single-family home mortgage market support the value proposition for owning multifamily apartment communities. Recent updates in the markets where our three properties are located are as follows:

Atlanta, Georgia

Atlanta is recognized as the transportation, communication, industrial, and cultural center of the southeastern United States. Atlanta’s central location within a nine-state region has been a major factor in its economic success. Home to major corporations such as UPS, Delta Airlines and Coco-Cola, Atlanta has remained successful in attracting major corporate expansions and relocations that have brought thousands of new jobs (and major real estate projects) to the region. The city boasts a growing technology sector attracting companies such as Amazon Web Services and Anthem’s IT department. In addition, major infrastructure projects (including a $1 billion roadway improvement and $2.5 billion in funding for MARTA line expansions) are underway and approved by voters. Atlanta has seen continued deliveries of multifamily development projects, particularly in the Downtown/Midtown areas. However, due to Atlanta’s ability to attract migrants from other parts of the country and multiple growth engines, employment growth of 2.4% year-over-year has continued to outpace the national average of 1.7%, thus providing demand to absorb new supply.

Charlotte, North Carolina

Charlotte is one of the fastest-growing markets in the nation in terms of jobs and population and has historically been considered a solid location for industry, with a particular focus on healthcare, FinTech, tech and energy, as of recent. Its competitive strengths include relatively low costs of doing business and living, a strong transportation network (including the recent opening of the LYNX Blue Line metro adjacent to the Alpha Mill property), educated workforce, and being a central location midway between New York and Florida. The region has seen an increase in jobs, building permits, average home sale prices, and infrastructure projects. Wage growth in the region has accelerated in the last two years and is expected to continue over the next several years. Given its positive demographic characteristics and strongin-migration expanding the consumer base and creating demand for additional housing, Charlotte’s growth in employment at a projected 1.5% and income at 3.3% are expected to outpace the U.S. averages over the next five years.

Tampa, Florida

Tampa’s economy is driven by tourism, professional services, back office and call center, with several recent expansions of multinational companies creating relatively high-wage jobs and positive immigration. Many recent corporate expansions are a result of the business-friendly environment with no state income tax and low corporate taxes, as well as the appealing climate and renowned beaches. A $3 billionmixed-use Water Street development adds promise to a rapidly revitalizing downtown area, further promoting the live / work / play environment in the broader metro. Year-over year job growth of 1.9% and rent growth of 3.3% both exceed national averages, while expected job and population growth are anticipated to continue to drive positive multifamily fundamentals in the future.

4

Table of Contents

Critical Accounting Policies

The preparation of financial statements in accordance with GAAP requires us to use judgment in the application of accounting policies, including making estimates and assumptions. Such judgments are based on our experience, the experience of our management, and industry data. We consider these policies critical because we believe understanding these policies is necessary in order to understand and evaluate our reported financial results. These policies may involve significant judgments and assumptions, or require estimates about matters that are inherently uncertain. These judgments will affect the reported amounts of assets, liabilities, revenues, expenses and related disclosures in the financial statements. Additionally, other companies may utilize different estimates that may impact the comparability of our results of operations to those of companies in similar businesses.

We believe the following accounting policy is critical. Please refer to Note 2 included in the financial statements contained in this report for a more thorough discussion of our accounting policies and procedures.

| • | Investments in Joint Ventures |

Results of Operations

During the years ended December 31, 2018 and 2017, we incurred net losses of approximately $1.6 million and $2.8 million, respectively, as follows:

| (Amounts in thousands) | 2018 | 2017 | ||||||

Equity in losses of joint ventures | $ | (385 | ) | $ | (1,365 | ) | ||

Interest expense on bridge loan from CROP | — | (177 | ) | |||||

Asset management fees to our advisor | (934 | ) | (999 | ) | ||||

Other expenses | (292 | ) | (284 | ) | ||||

|

|

|

| |||||

Net loss | $ | (1,611 | ) | $ | (2,825 | ) | ||

|

|

|

| |||||

Net loss per basic and diluted common shares | $ | (0.32 | ) | $ | (0.60 | ) | ||

Weighted average common shares outstanding, basic and diluted | 4,992,167 | 4,721,348 | ||||||

Equity in losses of joint ventures are attributable to our 90% investment in the three properties and comprised of the following:

| 2017 | 2018 | |||||||||||||||||||||||||||||||||||||||||||||||

(Amounts in Thousands) | Q1 | Q2 | Q3 | Q4 | Total | Equity in Earnings (Losses) at 90% | Q1 | Q2 | Q3 | Q4 | Total | Equity in Earnings (Losses) at 90% | ||||||||||||||||||||||||||||||||||||

Revenues | ||||||||||||||||||||||||||||||||||||||||||||||||

Rental and other operating income | $ | 2,876 | $ | 2,979 | $ | 3,053 | $ | 3,067 | $ | 11,975 | $ | 10,778 | $ | 3,097 | $ | 3,160 | $ | 3,199 | $ | 3,216 | $ | 12,672 | $ | 11,405 | ||||||||||||||||||||||||

Operating expenses | ||||||||||||||||||||||||||||||||||||||||||||||||

Rental operations expense | 1,116 | 1,110 | 1,161 | 1,009 | 4,396 | 3,956 | 1,099 | 1,153 | 1,140 | 1,018 | 4,410 | 3,969 | ||||||||||||||||||||||||||||||||||||

General and administrative | 99 | 123 | 120 | 106 | 448 | 403 | 81 | 86 | 101 | 94 | 362 | 326 | ||||||||||||||||||||||||||||||||||||

Property management fees | 102 | 104 | 107 | 106 | 419 | 377 | 109 | 110 | 112 | 113 | 444 | 400 | ||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||

Total operating expenses | 1,317 | 1,337 | 1,388 | 1,221 | 5,263 | 4,736 | 1,289 | 1,349 | 1,353 | 1,225 | 5,216 | 4,695 | ||||||||||||||||||||||||||||||||||||

Net operating income | 1,559 | 1,642 | 1,665 | 1,846 | 6,712 | 6,042 | 1,808 | 1,811 | 1,846 | 1,991 | 7,456 | 6,710 | ||||||||||||||||||||||||||||||||||||

Non operating expenses (income) | ||||||||||||||||||||||||||||||||||||||||||||||||

Interest on Fannie Mae facility | 753 | 781 | 807 | 791 | 3,132 | 2,819 | 821 | 853 | 875 | 931 | 3,480 | 3,132 | ||||||||||||||||||||||||||||||||||||

Depreciation and amortization | 1,618 | 1,142 | 1,150 | 1,159 | 5,069 | 4,562 | 1,162 | 1,165 | 1,175 | 1,178 | 4,680 | 4,212 | ||||||||||||||||||||||||||||||||||||

Other non operating expenses (income) | 30 | 13 | 26 | (40 | ) | 29 | 26 | (154 | ) | (161 | ) | (26 | ) | 64 | (277 | ) | (249 | ) | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||

Net loss | $ | (842 | ) | $ | (294 | ) | $ | (318 | ) | $ | (64 | ) | $ | (1,518 | ) | $ | (1,365 | ) | $ | (21 | ) | $ | (46 | ) | $ | (178 | ) | $ | (182 | ) | $ | (427 | ) | $ | (385 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||

SeeNote 3 to our consolidated financial statements for further details on individual property operating information.

Liquidity and Capital Resources

Our primary sources of liquidity are cash and cash equivalents on hand, lender escrowed reserves, and cash flow generated from operations. Other sources may include additional borrowings from our facility or loans from CROP. CROP may, but is not obligated to, lend us money. All of the terms and conditions of such loans shall be determined by us and CROP; provided however that the interest rate on any such loan shall not exceed the10-year Treasury rate plus 600 basis points.

5

Table of Contents

We intend to strengthen our capital and liquidity positions by continuing to focus on our core fundamentals at the property level. Factors which could increase or decrease our future liquidity include but are not limited to operating performance of our properties, volatility in interest rates, and the satisfaction of REIT dividend requirements.

Cash Flow

The following presents our summarized cash flows information for the years ended December 31, 2018 and 2017:

| (Amounts in Thousands) | 2018 | 2017 | ||||||

Net cash provided by operating activities | $ | (86 | ) | $ | 1,243 | |||

Net cash provided by investing activities | 3,747 | — | ||||||

Net cash used in financing activities | (2,990 | ) | (3,333 | ) | ||||

Net increase (decrease) in cash and cash equivalents | 671 | (2,090 | ) | |||||

Cash and cash equivalents at beginning of period | 291 | 2,381 | ||||||

|

|

|

| |||||

Cash and cash equivalents at end of period | $ | 962 | $ | 291 | ||||

|

|

|

| |||||

Distributions

Our Board of Directors authorized cash distributions equivalent to 5.75% of original purchase price on an annualized basis through December 31, 2018. During 2018 and 2017 distributions of $2,973 and $2,863, respectively, were declared and paid (amounts in thousands).

Non-GAAP Financial Measures

Funds from operations, or FFO, is an additional measure of the operating performance of a REIT and of our company. We compute FFO in accordance with the standards established by the National Association of Real Estate Investment Trusts, or NAREIT, as net income or loss (computed in accordance with GAAP), excluding gains or losses from sales of depreciable properties, the cumulative effect of changes in accounting principles, real estate-related depreciation and amortization, and after adjustments for our share of unconsolidated partnerships and joint ventures.

Our management also uses Core FFO as a measure of our operating performance. Core FFO excludes certainnon-cash ornon-routine items that we do not believe are reflective of our operating performance. Specifically, Core FFO excludes from FFO: amortization of debt issuance costs andmark-to-market adjustments included in net income. Themark-to-market adjustments are fair value adjustments to derivative instruments that are excluded in our calculation of Core FFO to more appropriately reflect core operating performance. Debt issuance costs are amortized over the term of the debt as an interest expense. We have excluded the amortization debt issuance costs in our calculation of Core FFO to more appropriately reflect the impact of these costs on our operating performance as these closing costs are not reflective of charges actually incurred during the period. We believe excluding these items provides investors with a useful supplemental metric that directly addresses core operating performance.

Our calculation of Core FFO may differ from the methodology used for calculating Core FFO by other REITs and, accordingly, our Core FFO may not be comparable. We utilize FFO and Core FFO as measures of our operating performance, and believe these measures are also useful to investors because they facilitate an understanding of our operating performance after adjustingfor certain non-cash expenses and other items not indicative of operating performance.

Neither FFO nor Core FFO is equivalent to net income or cash generated from operating activities determined in accordance with U.S. GAAP. Furthermore, FFO and Core FFO do not represent amounts available for management’s discretionary use because of needed capital replacement or expansion, debt service obligations or other commitments or uncertainties. Neither FFO nor Core FFO should be considered as an alternative to net income as an indicator of our operating performance or as an alternative to cash flow from operating activities as a measure of our liquidity.

6

Table of Contents

Our unaudited Core FFO calculation for the year December 31, 2018 and 2017 is as follows (amounts in thousands, except share data):

| 2018 | 2017 | |||||||

Net loss | $ | (1,611 | ) | $ | (2,825 | ) | ||

Adjustments: | ||||||||

Depreciation and amortization - our share of joint ventures | 4,212 | 4,562 | ||||||

|

|

|

| |||||

FFO | 2,601 | 1,737 | ||||||

Adjustments: | ||||||||

Amortization of our share of debt issuance costs | 87 | 77 | ||||||

Mark to market adjustment on our share of interest rate cap | (250 | ) | (68 | ) | ||||

|

|

|

| |||||

Core FFO | $ | 2,438 | $ | 1,746 | ||||

|

|

|

| |||||

FFO per basic and diluted common shares | $ | 0.52 | $ | 0.37 | ||||

Core FFO per basic and diluted common shares | $ | 0.49 | $ | 0.37 | ||||

Weighted average common shares outstanding, basic and diluted | 4,992,167 | 4,721,348 | ||||||

Related Party Arrangements

SeeNote 7 to our consolidated financial statements for discussion on related party arrangements.

| Item 3. | Directors and Officers |

We operate under the direction of our board of directors. The board of directors is responsible for the management and control of our affairs. The current board members are Daniel Shaeffer (Chairman of the Board), Chad Christensen and Gregg Christensen. The current Chief Executive Officer and President is Enzio Cassinis; the current Chief Financial Officer is Adam Larson; the current Chief Accounting Officer is Susan Hallenberg; the current Chief Investment Officer is Paul Fredenberg; and the current Chief Legal Officer is Gregg Christensen.

Investment Committee

We have established an investment committee that is charged with identifying and investigating potential investment opportunities for us. The investment committee analyzes and approves any investment to be made by us. The investment committee has seven committee members and is currently comprised of Enzio Cassinis, Adam Larson, Susan Hallenberg, Gregg Christensen, Paul Fredenberg, Daniel Shaeffer and Chad Christensen. The investment committee may request information from third parties in making its recommendations.

7

Table of Contents

Executive Officers and Directors

The following table shows the names and ages of our current directors and executive officers and the positions held by each individual:

Name(1) | Positions | Age (2) | Term of Office | |||

| Enzio Cassinis | Chief Executive Officer, President and Investment Committee Member | 41 | October 2018 to Present(3) December 2015 to Present(5) | |||

| Adam Larson | Chief Financial Officer and Investment Committee Member | 37 | October 2018 to Present(3), (6) | |||

| Susan Hallenberg | Chief Accounting Officer and Treasurer and Investment Committee Member | 51 | October 2018 to Present(3), (6) | |||

| Gregg Christensen | Chief Legal Officer, Director and Investment Committee Member | 49 | June 2015 to Present | |||

| Paul Fredenberg | Chief Investment Officer and Investment Committee Member | 41 | October 2018 to Present(3) December 2015 to Present(5) | |||

| Daniel Shaeffer | Chairman of the Board, Director and Investment Committee Member | 48 | June 2015 to Present(4) December 2015 to Present(5) | |||

| Chad Christensen | Director and Investment Committee Member | 45 | June 2015 to Present(4) December 2015 to Present(5) |

| (1) | The address of each director and executive officer listed is 6340 South 3000 East, Suite 500, Salt Lake City, Utah 84121. |

| (2) | As of March 31, 2019. |

| (3) | The current executive officers were appointed in October 2018. |

| (4) | The current directors were appointed in June 2015. |

| (5) | These investment committee members were appointed in December 2015. |

| (6) | These investment committee members were appointed in October 2018. |

Enzio Cassinis has been our Chief Executive Officer since October 2018. In addition to serving as our Chief Executive Officer and President, Mr. Cassinis serves as the Chief Executive Officer and President of Cottonwood Communities, Inc. (“CCI”), a Cottonwood-sponsorednon-traded real estate investment trust conducting an offering of $750 million that is registered under the Securities Acts of 1933, and Cottonwood Multifamily REIT II, Inc. (“CWMF REIT II”), another Cottonwood-sponsored real estate investment trust that raised $50 million in an offering that was qualified as a “Tier 2” offering pursuant to Regulation A promulgated under the Securities Act. He also serves as the Chief Executive Officer for the current asset manager.

From June 2013 through September 2018, Mr. Cassinis served in various roles at Cottonwood Residential, Inc. Most recently, he served as the Senior Vice President of Corporate Strategy, where he was responsible for financial planning and analysis, balance sheet management and capital and venture formation activity. Prior to joining Cottonwood Residential in June 2013, Mr. Cassinis was Vice President of Investment Management at Archstone, one of the largest apartment operators and developers in the U.S. and Europe. There, he negotiated transactions in both foreign and domestic markets with transaction volume exceeding several billion dollars in total capitalization. Prior to Archstone, Mr. Cassinis worked as an attorney with Krendl, Krendl, Sachnoff & Way, PC (now Kutak Rock LLP) from February 2003 to May 2006, focusing his practice on corporate law and merger and acquisition transactions.

Mr. Cassinis earned a Master of Business Administration and Juris Doctorate (Order of St. Ives) from the University of Denver, and a Bachelor of Science in Business Administration from the University of Colorado at Boulder and is a CFA® charterholder.

Adam Larson has been our Chief Financial Officer since October 2018. In addition to serving as our Chief Financial Officer, Mr. Larson also serves as the Chief Financial Officer of CCI and CWMF REIT II. He also serves as Chief Financial Officer for our current asset manager.

Through September 2018, Mr. Larson was the Senior Vice President of Asset Management of Cottonwood Residential, Inc. In this role he provided strategic guidance with respect to asset management, financial planning and analysis, and property operations. Prior to joining Cottonwood in June 2013, Mr. Larson worked in the Investment Banking Division at Goldman Sachs advising clients on mergers and acquisitions and other capital raising activities in the Real Estate, Consumer/Retail and Healthcare sectors.

8

Table of Contents

Mr. Larson previously worked at Barclays Capital, Bonneville Real Estate Capital and Hitachi Consulting. Mr. Larson holds an MBA from the University of Chicago Booth School Of Business, and a BS in Business Management from Brigham Young University where he also served as Student Body President.

Susan Hallenberg has been an officer of us since December 2015, and served as principal accounting officer and our principal financial officer in her role as Chief Financial Officer from December 2016 through September 2018. Ms. Hallenberg continues to serve as our principal accounting officer in her position as Chief Accounting Officer and Treasurer, which positions she has held since October 2018. Ms. Hallenberg also serves as Chief Accounting Officer and Treasurer of CCI and CWMF REIT II. She is also Chief Financial Officer and Treasurer of Cottonwood Multifamily Opportunity Fund, Inc. (“CWMF Opp Fund”), a Cottonwood-sponsored program conducting a $50 million offering that was qualified as a “Tier 2” offering pursuant to Regulation A promulgated under the Securities Act. Ms. Hallenberg is also the Chief Financial Officer and Treasurer of Cottonwood Residential II, Inc. and its predecessor entity, positions she has held since May 2005.

Prior to joining the Cottonwood, Ms. Hallenberg served as Acquisitions Officer for Phillips Edison & Company, a real estate investment company. She also served as Vice President for Lend Lease Real Estate Investments, where her responsibilities included financial management of a largemixed-use real estate development project and the underwriting, financing and reporting on multifamily housing development opportunities in the Western United States using tax credit,tax-exempt bond, and conventional financing. She also worked for Aldrich Eastman & Waltch for two years as an Assistant Portfolio Controller.

Ms. Hallenberg started her career at Ernst & Young where she worked in the firm’s audit department for four years. Ms. Hallenberg holds a BA in Economics/Accounting from The College of the Holy Cross.

Gregg Christensen has served as our Chief Legal Officer and one of our directors since June 2015. Mr. Christensen also serves as the Executive Vice President, Secretary, General Counsel and a Director of Cottonwood Residential II, Inc. and its predecessor entities since 2007. He holds similar officer positions with CCI, CWMF REIT II and CWMF Opp Fund. In addition, he serves as a director of CWMF Opp Fund and CWMF REIT II. Mr. Christensen oversees and coordinates all legal aspects of Cottonwood Residential II, Inc. and its affiliates, including our company, and is also actively involved in operations, acquisitions, and due diligence activities for us and our affiliates.

Prior to joining Cottonwood Residential, Inc., Mr. Christensen was a principal, managing director and general counsel of Cherokee & Walker, an investment company focused on real estate investments and private equity investments in real estate related companies. Previously, Mr. Christensen practiced law with Nelson & Senior in Salt Lake City. His areas of practice included real estate and corporate law. He is a member of the Utah State Bar, as well as the Bar of the United States District Court for the District of Utah. Mr. Christensen has been involved in real estate development, management, acquisition, disposition and financing for more than 22 years.

Mr. Christensen holds an Honors Bachelor of Arts Degree in English from the University of Utah and a Juris Doctorate Degree from the University of Utah, S.J. Quinney College of Law. Gregg Christensen and Chad Christensen are brothers.

Paul Fredenberg has been our Chief Investment Officer since October 2018. In addition to serving as our Chief Investment Officer, Mr. Fredenberg serves as the Chief Investment Officer of CCI, CWMF REIT II, and our asset manager, positions he has held since October 2018.

Through September 2018, Mr. Fredenberg served as the Senior Vice President of Acquisitions of Cottonwood Residential, Inc. a position he had held since September 2005. As Senior Vice President of Acquisitions, he focused exclusively on sourcing and evaluating new multifamily investment opportunities for Cottonwood Residential, Inc. Prior to joining Cottonwood in 2005, Mr. Fredenberg worked in the Investment Banking division of Wachovia Securities advising clients on mergers and acquisitions activities across multiple industries. He has also held investment banking and management consulting positions at Piper Jaffray and the Arbor Strategy Group.

Mr. Fredenberg holds an MBA from the Wharton School at the University of Pennsylvania, an MA in Latin American Studies from the University of Pennsylvania, and a BA in Economics from the University of Michigan, Ann Arbor.

Daniel Shaeffer has served as one of our Directors since June 2015 and as our Chairman of the Board since October 2018. He was formerly our Chief Executive Officer from June 2015 through September 2018. Mr. Shaeffer also has served as the Chief Executive Officer and a Director of Cottonwood Residential II, Inc. and its predecessor entities since 2004. He is also a director of CCI, CWMF REIT II and CWMF Opp Fund. In addition, he serves as Chief Executive Officer of CWMF Opp Fund. Mr. Shaeffer’s primary responsibilities include overseeing acquisitions, capital markets and strategic planning for Cottonwood Residential II, Inc. and its affiliates.

9

Table of Contents

Before co-founding Cottonwood Capital, LLC, a predecessor to Cottonwood Residential II, Inc., in 2004, Mr. Shaeffer worked as a senior equities analyst with Wasatch Advisors of Salt Lake City. Prior to joining Wasatch Advisors, Mr. Shaeffer was a Vice President of Investment Banking at Morgan Stanley. Mr. Shaeffer began his career with Ernst & Young working in the firm’s audit department. Mr. Shaeffer has been involved in real estate development, management, acquisition, disposition and financing for more than 13 years.

Mr. Shaeffer holds an International MBA from the University of Chicago Graduate School of Business and a BS in Accounting from Brigham Young University and is a Certified Public Accountant.

Chad Christensen has served as one of our Directors since June 2015 and was formerly our President and Chairman of the Board from June 2015 through September 2018. Mr. Christensen also has served as the President and a Director of Cottonwood Residential II, Inc. and its predecessor entities since 2004. He is also a director of CCI, CWMF REIT II and CWMF Opp Fund. In addition, he serves as President and Chairman of the Board of CWMF Opp Fund. Mr. Christensen oversees financial and general operations for Cottonwood Residential II, Inc. and its affiliates. Mr. Christensen is also actively involved in acquisitions, marketing and capital raising activities for Cottonwood Residential II, Inc. and its affiliates.

Before co-founding Cottonwood Capital, LLC, a predecessor to Cottonwood Residential II, Inc., in 2004, Mr. Christensen worked with the Stan Johnson Company, a national commercial Real Estate Brokerage firm in Tulsa, Oklahoma. Early in his career, Mr. Christensen founded Paramo Investment Company, a small investment management company. Mr. Christensen has been involved in real estate development, management, acquisition, disposition and financing for more than 15 years.

Mr. Christensen holds a MBA from The Wharton School at the University of Pennsylvania with an emphasis in Finance and Real Estate and a BA in English from the University of Utah. Mr. Christensen also holds an active real estate license. Chad Christensen and Gregg Christensen are brothers.

Compensation of Executive Officers

As described above, certain of the executive officers of Cottonwood Residential II, Inc. and its affiliates also serve as our executive officers. Each of these individuals receive compensation for his or her services, including services performed by CROP for us on behalf of our asset manager and property manager and their affiliates. As executive officers of our asset manager and property manager, these individuals will manageour day-to-day affairs, oversee the review, selection and recommendation of investment opportunities, service acquired investments and monitor the performance of these investments to ensure that they are consistent with our investment objectives. Although we will indirectly bear some of the costs of the compensation paid to these individuals, through fees we pay to our asset manager and property manager, we do not intend to pay any compensation directly to these individuals. More information regarding the compensation of our officers and directors and our asset manager and property manager can be found here.

10

Table of Contents

| Item 4. | Security Ownership of Management and Certain Securityholders |

The following table sets forth the beneficial ownership of our shares of common stock as of April 26, 2019, for each person or group that holds more than 10% of our shares of common stock, for each director, executive officer and for the directors and executive officers as a group. To our knowledge, each person that beneficially owns our shares of common stock has sole voting and disposition power with regards to such shares.

Unless otherwise indicated below, each person or entity has an address in care of our principal executive offices at 6340 South 3000 East, Suite 500, Salt Lake City, Utah 84121.

Name of Beneficial Owner(1) | Number of Shares Beneficially Owned | Percent of All Shares | ||||||

Daniel Shaeffer(2) | 1,021 | * | ||||||

Chad Christensen(2) | 1,021 | * | ||||||

Gregg Christensen(2) | 1,021 | * | ||||||

Enzio Cassinis | — | — | ||||||

Adam Larson | — | — | ||||||

Susan Hallenberg | — | — | ||||||

Paul Fredenberg | — | — | ||||||

All executive officers as a group (7 persons) | 1,021 | * | ||||||

| * | Less than 1% of all shares. |

| (1) | Under SEC rules, a person is deemed to be a “beneficial owner” of a security if that person has or shares “voting power”, which includes the power to dispose of or to direct the disposition of such security. A person also is deemed to be a beneficial owner of any securities which that person has a right to acquire within 60 days. Under these rules, more than one person may be deemed to be a beneficial owner of the same securities and a person may be deemed to be a beneficial owner of securities as to which he or she has no economic or pecuniary interest. |

| (2) | Cottonwood Residential O.P., LP owns 1,021 shares of our common stock. Cottonwood Residential O.P., LP is managed by its general partner, Cottonwood Residential II, Inc. Cottonwood Residential II, Inc. is managed by its board of directors, which currently consists of Daniel Shaeffer, Chad Christensen, Gregg Christensen, Jonathan Gardner and Philip White. The board of directors of Cottonwood Residential II, Inc., as the general partner of Cottonwood Residential O.P., LP, has the voting and investment control of the shares of our common stock held by Cottonwood Residential O.P., LP. Messrs. Shaeffer, C. Christensen and G. Christensen disclaim beneficial ownership of the shares held by Cottonwood Residential O.P., LP. |

| Item 5. | Interest of Management and Others in Certain Transactions |

SeeNote 7 to our financial statements in “Item 7. Financial Statements” for a discussion of related party transactions.

| Item 6. | Other Information |

None.

11

Table of Contents

Cottonwood Multifamily REIT I, Inc.

Consolidated Financial Statements

Years Ended December 31, 2018 and 2017

| F- 1 | ||||

| F- 2 | ||||

Consolidated Financial Statements | ||||

| F- 3 | ||||

| F- 4 | ||||

| F- 5 | ||||

| F- 6 | ||||

| F- 7 | ||||

Table of Contents

Report of Independent Registered Public Accounting Firm

To the Stockholders and Board of Directors

Cottonwood Multifamily REIT I, Inc.

Opinion on the Consolidated Financial Statements

We have audited the accompanying consolidated balance sheet of Cottonwood Multifamily REIT I, Inc. and subsidiaries (the Company) as of December 31, 2018, and the related consolidated statements of operations, equity, and cash flows for the year then ended, and the related notes (collectively, the consolidated financial statements). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2018, and the results of its operations and its cash flows for the year then ended, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement, whether due to error or fraud. Our audit included performing procedures to assess the risks of material misstatement of the consolidated financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that our audit provides a reasonable basis for our opinion

/s/ KPMG LLP

We have served as the Company’s auditor since 2018.

Denver, Colorado

April 29, 2019

F-1

Table of Contents

Report of Independent Auditors

The Board of Directors and Stockholders

Cottonwood Multifamily REIT I, Inc.

We have audited the accompanying consolidated financial statements of Cottonwood Multifamily REIT I, Inc., which comprise the balance sheet as of December 31, 2017, and the related consolidated statements of operations, equity, and cash flows for the year ended December 31, 2017, and the related notes to the consolidated financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in conformity with U.S. generally accepted accounting principles; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of the financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion the financial statements referred to above present fairly, in all material respects, the consolidated financial position of Cottonwood Multifamily REIT I, Inc. at December 31, 2017, and the consolidated results of its operations and its cash flows for the year ended December 31, 2017 in conformity with U.S. generally accepted accounting principles.

/s/ Ernst & Young LLP

Salt Lake City, Utah

April 27, 2018

F-2

Table of Contents

Cottonwood Multifamily REIT I, Inc.

Consolidated Balance Sheets

(Amounts in Thousands, Except Share Data)

| December 31, | ||||||||

| 2018 | 2017 | |||||||

Assets | ||||||||

Investments in joint ventures | $ | 35,810 | $ | 42,818 | ||||

Cash and cash equivalents | 962 | 291 | ||||||

Other assets | 24 | 25 | ||||||

|

|

|

| |||||

Total assets | $ | 36,796 | $ | 43,134 | ||||

|

|

|

| |||||

Liabilities and equity | ||||||||

Liabilities: | ||||||||

Accrued interest on related party bridge loans | $ | — | $ | 756 | ||||

Accounts payable and accrued liabilities | 421 | 1,406 | ||||||

|

|

|

| |||||

Total liabilities | $ | 421 | $ | 2,162 | ||||

|

|

|

| |||||

Commitments and contingencies (Note 8) | ||||||||

Equity: | ||||||||

Preferred stock, $0.01 par value, 100,000,000 shares authorized; no shares issued and outstanding | — | — | ||||||

Common stock, $0.01 par value, 1,000,000,000 shares authorized; 4,984,700 and 4,997,000 shares issued and outstanding at December 31, 2018 and 2017, respectively | 50 | 50 | ||||||

Additional paid in capital | 49,802 | 49,925 | ||||||

Accumulated distributions | (5,836 | ) | (2,973 | ) | ||||

Accumulated deficit | (7,641 | ) | (6,030 | ) | ||||

|

|

|

| |||||

Total equity | 36,375 | 40,972 | ||||||

|

|

|

| |||||

Total liabilities and equity | $ | 36,796 | $ | 43,134 | ||||

|

|

|

| |||||

See accompanying notes to the consolidated financial statements.

F-3

Table of Contents

Cottonwood Multifamily REIT I, Inc.

Consolidated Statements of Operations

(Amounts in Thousands)

| Year Ended December 31, | ||||||||

| 2018 | 2017 | |||||||

Equity in losses of joint ventures | $ | (385 | ) | $ | (1,365 | ) | ||

Interest expense on related party bridge loans | — | (177 | ) | |||||

Asset management fee to related party | (934 | ) | (999 | ) | ||||

Other expenses | (292 | ) | (284 | ) | ||||

|

|

|

| |||||

Net loss | $ | (1,611 | ) | $ | (2,825 | ) | ||

|

|

|

| |||||

Net loss per basic and diluted common shares | $ | (0.32 | ) | $ | (0.60 | ) | ||

Weighted average common shares outstanding, basic and diluted | 4,992,167 | 4,721,348 | ||||||

See accompanying notes to the consolidated financial statements.

F-4

Table of Contents

Cottonwood Multifamily REIT I, Inc

Consolidated Statements of Equity

(Amounts in Thousands, Except Share Data)

| Common Stock | ||||||||||||||||||||||||

| Shares | Amount | Additional Paid in Capital | Accumulated Distributions | Accumulated Deficit | Total Equity | |||||||||||||||||||

Balance at December 31, 2016 | 2,780,426 | $ | 28 | $ | 27,776 | $ | (259 | ) | $ | (3,205 | ) | $ | 24,340 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Issuance of common stock | 2,220,574 | 22 | 22,184 | — | — | 22,206 | ||||||||||||||||||

Common stock repurchase | (4,000 | ) | — | (35 | ) | — | — | (35 | ) | |||||||||||||||

Distributions to investors | — | — | — | (2,714 | ) | — | (2,714 | ) | ||||||||||||||||

Net loss | — | — | — | — | (2,825 | ) | (2,825 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Balance at December 31, 2017 | 4,997,000 | $ | 50 | $ | 49,925 | $ | (2,973 | ) | $ | (6,030 | ) | $ | 40,972 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Common stock repurchase | (12,300 | ) | — | (123 | ) | — | — | (123 | ) | |||||||||||||||

Distributions to investors | — | — | — | (2,863 | ) | — | (2,863 | ) | ||||||||||||||||

Net loss | — | — | — | — | (1,611 | ) | (1,611 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Balance at December 31, 2018 | 4,984,700 | $ | 50 | $ | 49,802 | $ | (5,836 | ) | $ | (7,641 | ) | $ | 36,375 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

See accompanying notes to the consolidated financial statements.

F-5

Table of Contents

Cottonwood Multifamily REIT I, Inc

Consolidated Statements of Cash Flows

(Amounts in Thousands)

| Year Ended December 31, | ||||||||

| 2018 | 2017 | |||||||

Operating activities | ||||||||

Net loss | $ | (1,611 | ) | $ | (2,825 | ) | ||

Adjustments to reconcile net loss to net cash provided by operating activities: | ||||||||

Equity in losses of joint ventures | 385 | 1,365 | ||||||

Distributions of capital from joint ventures | 2,875 | 2,220 | ||||||

Changes in operating assets and liabilities: | ||||||||

Other assets | — | (25 | ) | |||||

Accrued interest on related party bridge loan | (756 | ) | (247 | ) | ||||

Accounts payable and accrued liabilities | (979 | ) | 755 | |||||

|

|

|

| |||||

Net cash provided by operating activities | (86 | ) | 1,243 | |||||

|

|

|

| |||||

Investing activities | ||||||||

Distributions of capital from joint ventures related to increased borrowings | 3,747 | — | ||||||

|

|

|

| |||||

Net cash provided by investing activities | 3,747 | — | ||||||

|

|

|

| |||||

Financing activities | ||||||||

Repayment of related party bridge loans | — | (22,920 | ) | |||||

Issuance of common stock | — | 22,206 | ||||||

Common stock repurchase | (123 | ) | (35 | ) | ||||

Distributions to common stockholders | (2,867 | ) | (2,584 | ) | ||||

|

|

|

| |||||

Net cash used in financing activities | (2,990 | ) | (3,333 | ) | ||||

|

|

|

| |||||

Net increase (decrease) in cash and cash equivalents | 671 | (2,090 | ) | |||||

Cash and cash equivalents at beginning of period | 291 | 2,381 | ||||||

|

|

|

| |||||

Cash and cash equivalents at end of period | $ | 962 | $ | 291 | ||||

|

|

|

| |||||

See accompanying notes to the consolidated financial statements.

F-6

Table of Contents

Cottonwood Multifamily REIT I, Inc.

Notes to Consolidated Financial Statements

(Amounts in Thousands, Except Share Data)

Note 1 - Organization and Business

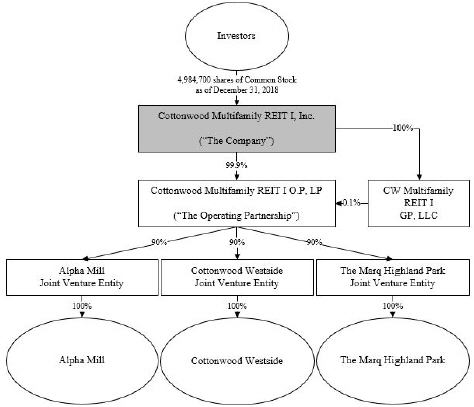

Cottonwood Multifamily REIT I, Inc. (the “Company”) is a Maryland corporation formed on June 22, 2015 to invest in multifamily apartment communities and real estate related assets in the United States primarily through joint ventures with Cottonwood Residential O.P., LP (“CROP”). Substantially all of the Company’s business is conducted through Cottonwood Multifamily REIT I O.P., LP (the “Operating Partnership”), a Delaware limited partnership. The Company is a limited partner and the sole member of the general partner of the Operating Partnership. As used herein, the term “Company”, “we”, “our” or “us” includes the Company, the Operating Partnership and its subsidiaries, unless the context indicates otherwise.

A subsidiary of CROP, Cottonwood Capital Property Management II, LLC (“our sponsor”), sponsored the formation of the Company and the offering of up to $50 million in shares of common stock at a purchase price of $10.00 per share through a Tier 2 Regulation A plus offering with the SEC (“our Offering”). The SEC qualified the offering in May 2016. We completed our Offering in April 2017, raising the full $50 million.

Our sponsor paid all of the selling commissions and managing broker-dealer fees and the organizational and offering expenses related to our Offering. We have an asset management agreement whereby we pay an affiliate of our sponsor an asset management fee. Our sponsor is also the sole property manager for the properties acquired by the joint ventures. Refer toNote 9 for changes related to the organization of our asset manager effective March 1, 2019.

The following chart illustrates our corporate structure and ownership percentages as of December 31, 2018:

The Company is structured as an umbrella partnership REIT and contributed all net proceeds from our Offering to the Operating Partnership. In return for those contributions, the Company received Operating Partnership Units (“OP Units”) in the Operating Partnership equal to the number of shares of common stock (“Common Stock”) the Company issued, maintaining aone-for-one relationship in OP Units issued to the Company and Common Stock issued by the Company. Therefore, holders of Common Stock share in the profits, losses and cash distributions of the Operating Partnership in the same proportion as their ownership in the Company.

F-7

Table of Contents

Cottonwood Multifamily REIT I, Inc.

Notes to Consolidated Financial Statements

(Amounts in Thousands, Except Share Data)

Note 2 - Summary of Significant Accounting Policies

Principles of Consolidation and Basis of Presentation

The consolidated financial statements are presented on the accrual basis of accounting in accordance with U.S. generally accepted accounting principles (“GAAP”) and include the accounts of the Company and its subsidiaries. All intercompany balances and transactions have been eliminated in consolidation.

The joint ventures are variable interest entities (“VIEs”). Generally, VIEs are legal entities in which the equity investors do not have the characteristics of a controlling financial interest or the equity investors lack sufficient equity at risk for the entity to finance its activities without additional subordinated financial support. All VIEs for which we are the primary beneficiary are consolidated. Qualitative and quantitative factors are considered in determining whether we are the primary beneficiary of a VIE, including, but not limited to, which activities most significantly impact economic performance, which party controls such activities, the amount and characteristics of our investments, the obligation or likelihood for us or other investors to provide financial support, and the management relationship of the property.

The Company and the Operating Partnership are consolidated. Control of the joint ventures is shared equally between CROP and us. We are not considered the primary beneficiary of the joint ventures as our sponsor, who is a subsidiary of CROP, is most closely associated with joint venture activities through their asset and property management agreements. As a result, our investments in joint ventures are recorded under the equity method of accounting on the consolidated financial statements.

Use of Estimates

We make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent liabilities at the dates of the consolidated financial statements as well as the amounts of revenues and expenses during the reporting periods. Actual amounts could differ from those estimates.

Organization and Offering Costs

Organization costs include all expenses incurred in connection our formation, including but not limited to legal fees and other costs to incorporate the Company. Offering costs include all expenses incurred in connection with the offering, including managing broker-dealer fees and selling commissions. All organization and offering costs were paid by our sponsor. We will not incur any liability for or reimburse our sponsor for any of these organizational and offering costs. Total offering costs incurred by our sponsor in connection with our Offering were approximately $6,176. Organizational costs incurred by our sponsor were not significant.

Investments in Joint Ventures

Under the equity method of accounting, our investments in joint ventures are stated at cost, adjusted for our share of net earnings or losses and reduced by distributions. Equity in earnings or losses is generally recognized based on our ownership interest in the earnings or losses of the joint ventures. For the purposes of presentation in the consolidated statements of cash flows, we follow the “look through” approach for classification of distributions from unconsolidated real estate assets. Under this approach, distributions are reported under operating cash flow unless the facts and circumstances of a specific distribution clearly indicate that it is a return of capital (e.g., a liquidating dividend or distribution of the proceeds from the entity’s sale of assets), in which case it is reported as an investing activity.

We assess potential impairment of investments in joint ventures whenever events or changes in circumstances indicate that the fair value of the investment is less than its carrying value. To the extent impairment has occurred, and is not considered temporary, the impairment is measured as the excess of the carrying amount of the investment over the fair value of the investment. We have not recognized impairment on any of our joint venture investments.

Cash and Cash Equivalents

We maintain our cash in demand deposit accounts at major commercial banks. Balances in individual accounts at times exceeds FDIC insuredamounts. We have not experienced any losses in such accounts.

F-8

Table of Contents

Cottonwood Multifamily REIT I, Inc.

Notes to Consolidated Financial Statements

(Amounts in Thousands, Except Share Data)

Income Taxes

We elected to be taxed as a REIT as of January 1, 2016. As a REIT, we are not subject to federal income tax with respect to that portion of our income that meet certain criteria and is distributed annually to shareholders. To continue to qualify as a REIT, we must meet certain organizational and operational requirements, including a requirement to distribute at least 90% of our taxable income, excluding net capital gains, to shareholders. We have adhered to, and intend to continue to adhere to, these requirements to maintain REIT status.

If we fail to qualify as a REIT in any taxable year, we will be subject to federal income taxes at regular corporate rates (including any applicable alternative minimum tax) and may not qualify as a REIT for four subsequent taxable years. As a qualified REIT, we are still subject to certain state and local taxes and may be subject to federal income and excise taxes on undistributed taxable income. For the years ended December 31, 2018 and 2017, 100% (unaudited) of all distributions to stockholders qualified as a return of capital.

Recent Accounting Pronouncements

The following table provides a brief description of recent accounting pronouncements that could have a material effect on our consolidated financial statements:

Standard | Description | Required | Effect on the Financial Statements or | |||

| ASU2014-09,Revenue from Contracts with Customers | The ASU establishes principles for recognizing revenue upon the transfer of promised goods or services to customers, in an amount that reflects the expected consideration received in exchange for those goods or services as outlined in a five-step model whereby revenue is recognized as performance obligations within a contract are satisfied. Income from lease contracts is specifically excluded from this ASU. | January 1, 2019 | The ASU may be applied using the full retrospective transition method or by using the modified retrospective transition method with a cumulative effect recognized as of the date of initial application. The majority of our joint venture revenue is derived from real estate lease contracts, which falls outside the scope of the ASU. We have evaluated the impact of adopting the new standard onnon-lease related activity, including other separate resident charges, and do not expect significant adjustments to the consolidated financial statements as a result of adoption of this standard. | |||

| ASU2016-02,Leases | The ASU amends existing accounting standards for lease accounting and establishes the principles for lease accounting for both the lessee and lessor. The amendment requires lessees to recognize aright-of-use asset and lease liability for all leases with terms of more than 12 months. Recognition, measurement and presentation of expenses will depend on classification as a finance or operating lease. The amendment also requires certain quantitative and qualitative disclosures about leasing arrangements. | January 1, 2020 | The standard must be adopted using a modified retrospective transition and provides for certain practical expedients. Transition will require application of the new guidance at the beginning of the earliest comparative period presented. We do not expect adoption to have a significant impact on the consolidated financial statements, as leases are generally 12 months or less with the exception of certain retail leases. | |||

| ASU2016-15,Classification of Certain Cash Receipts and Cash Payments (a consensus of the Emerging Issues Task Force) | The ASU clarifies how several specific cash receipts and cash payments are to be presented and classified on the statement of cash flows, which, among other things, include debt prepayment or debt extinguishment costs, settlement ofzero-coupon debt instruments, insurance settlement proceeds, contingent consideration made after a business combination, distributions received from equity method investees, and separately identifiable cash flows and application of predominance principle. | January 1, 2020 | Each amendment in this standard must be applied prospectively, retrospectively, or as of the beginning of the earliest comparative period presented in the year of adoption, depending on the type of amendment. We do not expect adoption to have a significant impact on the consolidated financial statements. | |||

F-9

Table of Contents

Cottonwood Multifamily REIT I, Inc.

Notes to Consolidated Financial Statements

(Amounts in Thousands, Except Share Data)

Note 3 - Investments in Joint Ventures

Our investment activity in our joint ventures is as follows:

| Alpha Mill | Cottonwood Westside | The Marq Highland Park | Total | |||||||||||||

2016 carrying value | $ | 16,266 | $ | 15,499 | $ | 14,638 | $ | 46,403 | ||||||||

Equity in losses | (475 | ) | (661 | ) | (229 | ) | (1,365 | ) | ||||||||

Distributions | (1,105 | ) | (507 | ) | (608 | ) | (2,220 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

2017 carrying value | 14,686 | 14,331 | 13,801 | 42,818 | ||||||||||||

Equity in losses | (56 | ) | (301 | ) | (28 | ) | (385 | ) | ||||||||

Distributions | (3,225 | ) | (561 | ) | (2,837 | ) | (6,623 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

2018 carrying value | $ | 11,405 | $ | 13,469 | $ | 10,936 | $ | 35,810 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Operational information for the properties owned by our joint ventures for the years ended December 31, 2018 and 2017 is as follows:

Year Ended December 31, 2018 | Alpha Mill | Cottonwood Westside | The Marq Highland Park | Total | Equity in Earnings (Losses) at 90% | |||||||||||||||

Revenues | ||||||||||||||||||||

Rental and other operating income | $ | 4,385 | $ | 3,592 | $ | 4,695 | $ | 12,672 | $ | 11,405 | ||||||||||

Operating expenses | ||||||||||||||||||||

Rental operations expense | 1,233 | 1,477 | 1,700 | 4,410 | 3,969 | |||||||||||||||

General and administrative | 132 | 114 | 116 | 362 | 326 | |||||||||||||||

Property management fees | 153 | 127 | 164 | 444 | 400 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total operating expenses | 1,518 | 1,718 | 1,980 | 5,216 | 4,695 | |||||||||||||||

Net operating income | 2,867 | 1,874 | 2,715 | 7,456 | 6,710 | |||||||||||||||

Interest on Fannie Mae facility | 1,341 | 982 | 1,157 | 3,480 | 3,132 | |||||||||||||||

Depreciation and amortization | 1,680 | 1,342 | 1,658 | 4,680 | 4,212 | |||||||||||||||

Other non operating income | (92 | ) | (114 | ) | (71 | ) | (277 | ) | (249 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net loss | $ | (62 | ) | $ | (336 | ) | $ | (29 | ) | $ | (427 | ) | $ | (385 | ) | |||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Year Ended December 31, 2017 | Alpha Mill | Cottonwood Westside | The Marq Highland Park | Total | Equity in Earnings (Losses) at 90% | |||||||||||||||

Revenues | ||||||||||||||||||||

Rental and other operating income | $ | 4,124 | $ | 3,444 | $ | 4,407 | $ | 11,975 | $ | 10,778 | ||||||||||

Operating expenses | ||||||||||||||||||||

Rental operations expense | 1,239 | 1,456 | 1,701 | 4,396 | 3,956 | |||||||||||||||

General and administrative | 146 | 168 | 134 | 448 | 403 | |||||||||||||||

Property management fees | 144 | 121 | 154 | 419 | 377 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total operating expenses | 1,529 | 1,745 | 1,989 | 5,263 | 4,736 | |||||||||||||||

Net operating income | 2,594 | 1,699 | 2,418 | 6,712 | 6,042 | |||||||||||||||

Interest on Fannie Mae facility | 1,190 | 884 | 1,058 | 3,132 | 2,819 | |||||||||||||||

Depreciation and amortization | 1,930 | 1,504 | 1,635 | 5,069 | 4,562 | |||||||||||||||

Other non operating expenses (income) | 3 | 46 | (20 | ) | 29 | 26 | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net loss | $ | (529 | ) | $ | (735 | ) | $ | (255 | ) | $ | (1,518 | ) | $ | (1,365 | ) | |||||

|

|

|

|

|

|

|

|

|

| |||||||||||

F-10

Table of Contents

Cottonwood Multifamily REIT I, Inc.

Notes to Consolidated Financial Statements

(Amounts in Thousands, Except Share Data)

Summarized balance sheet information for the properties owned by the joint ventures is as follows:

December 31, 2018 | Alpha Mill | Cottonwood Westside | The Marq Highland Park | Total | ||||||||||||

Real estate assets, net | $ | 48,139 | $ | 39,693 | $ | 40,484 | $ | 128,316 | ||||||||

Other assets | 929 | 1,107 | 1,074 | 3,110 | ||||||||||||

Fannie Mae facility | 36,265 | 25,655 | 32,260 | 94,180 | ||||||||||||

Other liabilities | 340 | 268 | 297 | 905 | ||||||||||||

Equity | 12,463 | 14,877 | 9,001 | 36,341 | ||||||||||||

December 31, 2017 | Alpha Mill | Cottonwood Westside | The Marq Highland Park | Total | ||||||||||||

Real estate assets, net | $ | 49,405 | $ | 40,625 | $ | 42,011 | $ | 132,041 | ||||||||

Other assets | 1,188 | 790 | 1,209 | 3,187 | ||||||||||||

Fannie Mae facility | 34,100 | 25,300 | 30,500 | 89,900 | ||||||||||||

Other liabilities | 385 | 281 | 370 | 1,036 | ||||||||||||

Equity | 16,108 | 15,834 | 12,350 | 44,292 | ||||||||||||

The excess of cost over our share of net assets of our investments in joint ventures is $3,103 and $2,955 at December 31, 2018 and 2017, respectively, and relates to acquisition date accounting differences.

Note 4 - Related Party Bridge Loans

We had not issued any shares to investors when the joint ventures acquired the properties on August 3, 2016. To facilitate our required capital contributions CROP provided bridge loans to us in the aggregate amount of $49,050 with $45,886 of the loans secured by our interests in the joint ventures. The loans bore interest at 6% per year and were repaid from offering proceeds. We repaid all of the bridge loans with offering proceeds in 2017 and repaid $756 of accrued interest in 2018.

F-11

Table of Contents

Cottonwood Multifamily REIT I, Inc.

Notes to Consolidated Financial Statements

(Amounts in Thousands, Except Share Data)

Note 5 - Stockholders’ Equity

Our charter authorizes the issuance of up to 1,000,000,000 shares of common stock at $0.01 par value per share and 100,000,000 shares of preferred stock at $0.01 par value per share.

Voting Common Stock

Holders of our common stock are entitled to receive dividends when authorized by the board of directors, subject to any preferential rights of outstanding preferred stock. Holders of common stock are also entitled to one vote per share on all matters submitted to a shareholder vote, including election of directors to the board, subject to certain restrictions. As of December 31, 2018, and 2017, we had outstanding shares of 4,984,700 and 4,997,000 shares, respectively. Our sponsor owns 1,021 shares.

Preferred Stock

The board of directors is authorized, without approval of common shareholders, to provide for the issuance of preferred stock, in one or more classes or series, with such rights, preferences and privileges as the board of directors approves. No preferred stock was issued and outstanding as of December 31, 2018 and 2017.

Distributions

Distributions are determined by the board of directors based on the Company’s financial condition and other relevant factors. Should cash flows from operations not cover distributions, we may look to third party borrowings to fund distributions. We may also use funds from the sale of assets or from the maturity, payoff or settlement of debt investments for distributions not covered by operating cash. Distributions for the years ended December 31, 2018 and 2017 were $2,863 and $2,714, respectively.

Note 6 - Joint Venture Distributions

Cash from operations of the individual joint ventures after payment of property management fees shall be distributed to provide a preferred return of up to 8% on invested capital in the joint venture. Profits will then be allocated 50% to the Operating Partnership and CROP (in proportion to their respective interests in the joint venture) and 50% to CROP until CROP has received an amount equal to 20% of all distributions. Profits after the above distributions will be allocated 80% to the Operating Partnership and CROP (in proportion to their respective interests in the joint venture) and 20% to CROP. Refer toNote 9 for changes in the entities receiving this promote effective March 1, 2019.

Note 7 - Related Party Transactions

Promotional Interest

Some of our directors and officers hold key positions at both CROP and our sponsor. They are not directly compensated by us but are responsible for the management and affairs of the Company. As outlined above, an affiliate of CROP will receive a 20% promotional interest after an 8% preferred return on invested capital. Refer toNote 9 for changes in the entities receiving this promote effective March 1, 2019.

Asset Management Fee

An affiliate of our sponsor provides asset management services for the Company subject to the board of directors’ supervision. As compensation for those services, such affiliate of our sponsor receives a fee of 0.75% of gross assets, defined initially as the gross book value of our assets and subsequently as gross asset value once NAV is established. For the years ended December 31, 2018 and 2017, we incurred asset management fees of $934 and $999, respectively. Refer toNote 9 for changes in the entities receiving these asset management fees effective March 1, 2019.

Property Management Fee

Our sponsor provides property management services for multifamily apartment communities acquired by the joint ventures and receives a fee of 3.5% of gross revenues of each property managed for these services. Our sponsor is also reimbursed for expenses incurred on behalf of their management duties in accordance with the property management agreement. During the years ended December 31, 2018 and 2017, property management fees charged to the three properties were $444 and $419, respectively.

F-12

Table of Contents

Cottonwood Multifamily REIT I, Inc.

Notes to Consolidated Financial Statements

(Amounts in Thousands, Except Share Data)

Construction Management Fee

Our sponsor will receive for its services in supervising any renovation or construction project in excess of $5 in or about each property a construction management fee equal to 5% of the cost of the amount that is expended. No construction management fees were incurred in 2018 or 2017.

Property Management Corporate Service Fee

Our sponsor allocates a flat fee each month to each of the joint ventures which is intended to fairly allocate the overhead costs incurred by our sponsor and its affiliated entities with respect to the management of all assets. This fee may vary depending on the number of assets managed and the actual overhead expenses incurred. Our sponsor will have the right to retain any excess between actual costs and the amount of the fee charged. Property management corporate service fees were not significant for the years ended December 31, 2018 and 2017.

Insurance Fee

Our sponsor through its wholly-owned insurance company, provides insurance for the multifamily apartment communities. They receive a risk management fee equal to 10% of the insurance premium and is entitled to retain in excess of the funded aggregate deductible not used to pay claims. A licensed insurance broker affiliated with our sponsor receives 20% of the brokerage fee charged with respect to the placement of all insurance policies for the multifamily apartment communities. Insurance fees were not significant for the years ended December 31, 2018 and 2017.

Note 8 - Commitments and Contingencies

Economic Dependency

Under various agreements, we have engaged or will engage our sponsor or affiliates of our sponsor to provide certain services that are essential to us, including asset management services and other administrative responsibilities that include accounting services and investor relations. As a result of these relationships, we are dependent upon our sponsor. In the event that our sponsor is unable to provide us with the respective services, we would be required to find alternative providers of these services.

Liquidity Strategy