As filed with the Securities and Exchange Commission on June 18, 2020.

Registration No.

333-

236956UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO.

3

TO

FORM

S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Albertsons Companies, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 5411 | 47-4376911 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

250 Parkcenter Blvd.

Boise, ID 83706

(208)

395-6200

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Juliette W. Pryor, Esq.

Executive Vice President and General Counsel

Albertsons Companies, Inc.

250 Parkcenter Blvd.

Boise, ID 83706

(208)

395-6200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Stuart D. Freedman, Esq. Antonio L. Diaz-Albertini, Esq. Schulte Roth & Zabel LLP 919 Third Avenue New York, NY 10022 Phone: (212) 756-2000 Fax: (212) 593-5955 | William J. Miller, Esq. Cahill Gordon & Reindel LLP 80 Pine Street New York, NY 10005 Phone: (212) 701-3000 Fax: (212) 378-2500 |

Approximate date of commencement of proposed sale to the public:

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box.

☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule12b-2

of the Exchange Act.Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||

Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

☐

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities to be Registered | Amount to Be Registered | Proposed Maximum Aggregate Offering Price Per Share(2) | Proposed Maximum Aggregate Offering Price | Amount of Registration Fee(3) | ||||

Class A common stock, par value $0.01 per share | 75,670,000(1) | $20.00 | $1,513,400,000 | $196,439.32(4) | ||||

| (1) | Includes shares to be sold upon exercise of the underwriters’ option to purchase additional shares to cover over-allotments, if any. |

| (2) | Estimated solely for the purpose of calculating the registration fee under Rule 457(a) of the Securities Act of 1933, as amended. |

| (3) | An aggregate registration fee of $11,620 in respect of shares of the registrant’s common stock was previously paid on July 8, 2015 in connection with the registration statement on Form S-1 (No. 333-205546). Additionally, an aggregate registration fee of $202,188 in respect of shares of the registrant’s common stock was previously paid on September 25, 2015 in connection withPre-Effective Amendment No. 2 to the registration statement on Form S-1 (No. 333-205546). Additionally, an aggregate registration fee of $13,091 in respect of shares of the registrant’s common stock was previously paid on October 2, 2015 in connection withPre-Effective Amendment No. 3 to the registration statement on Form S-1 (No. 333-205546). Thus, the aggregate filing fee associated with the registrant in connection with the registration statement on Form S-1 (No. 333-205546) was $226,899. The registrant withdrew the registration statement on Form S-1 (No. 333-205546) by filing a Form RW on April 6, 2018. The withdrawn registration statement on Form S-1 (No. 333-205546) was not declared effective, and no securities were sold thereunder. Pursuant to Rule 457(p), the registrant utilized $225,641 previously paid in connection with the withdrawn registration statement on Form S-1 to offset the filing fee in respect of shares of the registrant’s common stock in connection with the registration statement on Form S-4 (No.333-224169) filed with the Securities and Exchange Commission on April 6, 2018. The registrant terminated the offering and, on August 9, 2018, filed a Post-Effective Amendment No. 1 to FormS-4 (No.333-224169), which Post-Effective Amendment No. 1 to Form S-4 was declared effective on August 14, 2018, to deregister any and all securities registered but unsold or otherwise unissued under the registration statement on Form S-4. Pursuant to Rule 457(p), the registrant hereby offsets the filing fee previously paid in connection with the withdrawn registration statement on Form S-1 against the filing fee for this registration statement on Form S-1. |

| (4) | Previously paid. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated June 18, 2020.

65,800,000 Shares

Albertsons Companies, Inc.

Class A Common Stock

This is an initial public offering of shares of Class A common stock, $0.01 par value (“common stock”), of Albertsons Companies, Inc. The selling stockholders named in this prospectus are selling 65,800,000 shares of our common stock. All of the shares of common stock are being sold by the selling stockholders. We will not receive any of the proceeds from the sale of common stock by the selling stockholders.

Prior to this offering, there has been no public market for the common stock. It is currently estimated that the initial public offering price per share will be between $18.00 and $20.00. We have been approved to list our common stock on the New York Stock Exchange, or NYSE, under the symbol “ACI.”

Investing in our common stock involves a high degree of risk. See “Risk Factors” on page 26 to read about factors you should consider before buying shares of the common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Per Share | Total | |||||||

Initial public offering price | $ | $ | ||||||

Underwriting discounts and commissions(1) | $ | $ | ||||||

Proceeds to selling stockholders(1) | $ | $ | ||||||

| (1) | See “Underwriting” for additional information regarding underwriting compensation. |

The underwriters may also purchase up to an additional 9,870,000 shares of common stock from certain of the selling stockholders, at the initial public offering price, less the underwriting discount and commissions, within 30 days from the date of this prospectus. We will not receive any of the proceeds from the sale of common stock by the selling stockholders in this offering, including from any exercise by the underwriters of their option to purchase additional common stock.

The underwriters expect to deliver the shares against payment on or about , 2020.

BofA Securities | Goldman Sachs & Co. LLC | J.P. Morgan | Citigroup |

Credit Suisse | Morgan Stanley | Wells Fargo Securities | Barclays | Deutsche Bank Securities |

BMO Capital Markets | Evercore ISI | Guggenheim Securities | Oppenheimer & Co. | RBC Capital Markets |

Telsey Advisory Group | MUFG | Academy Securities | Blaylock Van, LLC | Drexel Hamilton |

Loop Capital Markets | Penserra Securities LLC | Ramirez & Co., Inc. | Stern | Tigress Financial Partners |

The date of this prospectus is , 2020.

TABLE OF CONTENTS

vi | ||||

1 | ||||

26 | ||||

52 | ||||

54 | ||||

55 | ||||

56 | ||||

58 | ||||

59 | ||||

61 | ||||

83 | ||||

101 | ||||

112 | ||||

137 | ||||

142 | ||||

147 | ||||

154 | ||||

162 | ||||

168 | ||||

176 | ||||

180 | ||||

186 | ||||

186 | ||||

186 | ||||

F- 1 |

Until , 2020 (25 days after the date of this prospectus), all dealers that buy, sell, or trade shares of our common stock, whether or not participating in this initial public offering, may be required to deliver a prospectus. This delivery requirement is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

Unless indicated otherwise, the information included in this prospectus (i) assumes that the shares of common stock to be sold in this offering are sold at $19.00 per share, which is the midpoint of the estimated offering range set forth on the cover page of this prospectus, (ii) assumes that all shares offered by the selling stockholders in this offering are sold (other than pursuant to the underwriters’ option to purchase additional shares described herein) and (iii) reflects a 2.072-for-1 forward stock split of our common stock which was effected on June 18, 2020 and all information related to our common stock and per share common amounts in this prospectus and our consolidated financial statements have been retroactively adjusted to give effect to the stock split.

We and the selling stockholders have not, and the underwriters have not, authorized anyone to provide any information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We, the selling stockholders and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. The selling stockholders and the underwriters are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of shares of our common stock.

i

DEFINITIONS

Unless otherwise indicated or as the context otherwise requires, a reference in this prospectus to:

| • | “ACI” refers to Albertsons Companies, Inc., a Delaware corporation; |

| • | “ACI Institutional Investors” refers to Klaff Realty, L.P., Schottenstein Stores Corp., Lubert-Adler Real Estate Management Company, L.P. (“Lubert-Adler Management”) and Kimco Realty Corporation, and each of their respective controlled affiliates and investment funds; |

| • | “Albertsons” refers to Albertson’s LLC, a Delaware limited liability company and a wholly-owned subsidiary of ACI; |

| • | “Cerberus” refers to Cerberus Capital Management, L.P., a Delaware limited partnership, and investment funds and accounts managed by it and its affiliates; |

| • | “Code” refers to the Internal Revenue Code of 1986, as amended; |

| • | “Exchange Act” refers to the U.S. Securities Exchange Act of 1934, as amended; |

| • | “GAAP” refers to accounting principles generally accepted in the United States of America; |

| • | “NALP” refers to New Albertsons L.P., a Delaware limited partnership and a wholly-owned subsidiary of ACI; |

| • | “Safeway” refers to Safeway Inc., a Delaware corporation and a wholly-owned subsidiary of ACI; |

| • | “SEC” refers to the Securities and Exchange Commission; |

| • | “Securities Act” refers to the U.S. Securities Act of 1933, as amended; |

| • | “Sponsors” refers to Cerberus, the ACI Institutional Investors and their respective controlled affiliates and investment funds; and |

| • | “we,” “our” and “us” refers to ACI and its direct or indirect subsidiaries. |

EXPLANATORY NOTE

ACI is a Delaware corporation. AB Acquisition LLC (“AB Acquisition”) is a Delaware limited liability company. ACI was formed for the purpose of reorganizing the organizational structure of AB Acquisition and its direct and indirect consolidated subsidiaries. Prior to December 3, 2017, ACI had no material assets or operations. On December 3, 2017, Albertsons Companies, LLC, a Delaware limited liability company, and its parent, AB Acquisition, completed a reorganization of their legal entity structure whereby the existing equityholders of AB Acquisition each contributed their equity interests in AB Acquisition to Albertsons Investor Holdings LLC (“Albertsons Investor”) or KIM ACI, LLC (“KIM ACI”). In exchange, equityholders received a proportionate share of units in Albertsons Investor and KIM ACI, respectively. Albertsons Investor and KIM ACI then contributed all of the equity interests they received to ACI in exchange for common stock issued by ACI. As a result, Albertsons Investor and KIM ACI became the parents of ACI, owning all of the outstanding common stock of ACI, with AB Acquisition and its subsidiary, Albertsons Companies, LLC, becoming wholly-owned subsidiaries of ACI. On February 25, 2018, Albertsons Companies, LLC, merged with and into ACI, with ACI as the surviving corporation (the “ACI Reorganization Transactions”). Prior to February 25, 2018, substantially all of the assets and operations of ACI were those of its subsidiary, Albertsons Companies, LLC. On June 9, 2020, we used cash in an amount equal to the proceeds from the sale and issuance of our 6.75% Series A-1 convertible preferred stock, $0.01 par value (“Series A-1 preferred stock”), and 6.75% Series A convertible preferred stock, $0.01 par value (“Series A preferred stock” and together with the Series A-1 preferred stock, the “Convertible Preferred Stock”), and the Investor Exchange Right (as defined herein) to repurchase 101,611,736 shares of outstanding common stock from certain Pre-IPO Stockholders (as defined herein) (the “Repurchase”). In connection with, and prior to the closing of,

ii

this offering, Albertsons Investor and KIM ACI will distribute all common stock of ACI held by them to their respective equityholders (the “Distribution”)

.

As a result, following the Repurchase and the Distribution, Albertsons Investor and KIM ACI will no longer be the stockholders of ACI.BASIS OF PRESENTATION

Except as otherwise noted herein, the consolidated financial statements and consolidated financial data included in this prospectus are those of ACI and its consolidated subsidiaries.

We use a 52 or 53 week fiscal year ending on the last Saturday in February each year. Our first quarter consists of 16 weeks, and our second, third and fourth quarters generally consist of 12 weeks. For ease of reference, unless the context otherwise indicates, we identify our fiscal years in this prospectus by reference to the calendar year of the first day of such fiscal year. The fiscal years ended February 23, 2019 (“fiscal 2018”), February 24, 2018 (“fiscal 2017”), February 25, 2017 (“fiscal 2016”) and February 27, 2016 (“fiscal 2015”) included and the fiscal years ending February 27, 2021 (“fiscal 2020”), February 26, 2022 (“fiscal 2021”), February 25, 2023 (“fiscal 2022”) and February 24, 2024 (“fiscal 2023”) will include 52 weeks. The fiscal years ended February 29, 2020 (“fiscal 2019”) and February 28, 2015 (“fiscal 2014”) consisted of 53 weeks.

IDENTICAL SALES

As used in this prospectus, the term “identical sales” includes stores operating during the same period in both the current fiscal year and the prior fiscal year, comparing sales on a daily basis. Direct to consumer internet sales are included in identical sales and fuel sales are excluded from identical sales. Fiscal 2019 is compared with fiscal 2018, fiscal 2018 is compared with fiscal 2017, fiscal 2017 is compared with fiscal 2016, fiscal 2016 is compared with fiscal 2015 and fiscal 2015 is compared with fiscal 2014. On an actual basis, acquired stores become identical on the

one-year

anniversary date of their acquisition. Stores that are open during remodeling are included in identical sales.TRADEMARKS AND TRADE NAMES

This prospectus includes certain of ACI’s trademarks and trade names, which are protected under applicable intellectual property laws and are the property of ACI and its subsidiaries. This prospectus also contains trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective owners. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the

®

or TM symbols. We do not intend our use or display of other parties’ trademarks, trade names or service marks to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of ACI by, these other parties.MARKET, INDUSTRY AND OTHER DATA AND APPRAISALS

This prospectus includes market and industry data and outlook, which are based on publicly available information, reports from government agencies, reports by market research firms and/or our own estimates based on our management’s knowledge of and experience in the markets and businesses in which we operate. We believe this information to be reasonable based on the information available to us as of the date of this prospectus. However, we have not independently verified market and industry data from third-party sources. Historical information regarding supermarket and grocery industry revenues, including online grocery revenues, was obtained from Euromonitor and IBISWorld. Forecasts regarding

Food-at-Home

inflation were obtained from the U.S. Department of Agriculture. Information with respect to our market share was obtained from Nielseniii

ACView All Outlets Combined (Food, Mass and Dollar but excluding Drug). U.S. Gross Domestic Product (GDP) was obtained from the Bureau of Economic Analysis. This information may prove to be inaccurate because of the method by which we obtained some of the data for our estimates or because this information cannot always be verified with complete certainty due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in a survey of market size. In addition, market conditions, customer preferences and the competitive landscape can and do change significantly. As a result, you should be aware that the market and industry data included in this prospectus and our estimates and beliefs based on such data may not be reliable. We have not verified the accuracy of such industry and market data.

In addition, the market value reported in the appraisals of the properties described herein are an estimate of value, as of the date stated in each appraisal. The appraisals were subject to the following assumption: the estimate of market value as is, is based on the assumption that the existing occupant/user remains in occupancy in the foreseeable future, commensurate with the typical tenure of a user of this type, and is paying market rent as of the effective date of appraisal. Changes since the appraisal date in external and market factors or in the property itself can significantly affect the conclusions. As an opinion, the reported values are not necessarily a measure of current market value and may not reflect the amount which would be received if the property were sold today. While we and the underwriters are not aware of any misstatements regarding any appraisals, market, industry or similar data presented herein, such data involves risks and uncertainties and is subject to change based on various factors, including those discussed under the sections entitled “Special Note Regarding Forward-Looking Statements” and “Risk Factors” in this prospectus.

NON-GAAP

FINANCIAL MEASURESAs used in this prospectus, (i) EBITDA is defined as GAAP earnings (net income (loss)) before interest, income taxes, depreciation and amortization, (ii) Adjusted EBITDA is defined as GAAP earnings (net income (loss)) before interest, income taxes, depreciation, and amortization, further adjusted to eliminate the effects of items management does not consider in assessing ongoing performance, (iii) Adjusted Net Income is defined as GAAP net income (loss) adjusted to eliminate the effects of items management does not consider in assessing ongoing performance, (iv) Adjusted Free Cash Flow is defined as Adjusted EBITDA less capital expenditures, (v) Net Debt is defined as total debt (which includes finance lease obligations and is net of deferred financing costs and original issue discount) minus unrestricted cash and cash equivalents and (vi) Net Debt Ratio is defined as the ratio of Net Debt to Adjusted EBITDA for the rolling 52 or 53 week period.

EBITDA, Adjusted EBITDA, Adjusted Net Income, Adjusted Free Cash Flow, Net Debt and Net Debt Ratio (collectively, the

“Non-GAAP

Measures”) are performance measures that provide supplemental information management believes is useful to analysts and investors to evaluate ongoing results of operations, when considered alongside other GAAP measures such as net income, operating income and gross profit. TheseNon-GAAP

Measures exclude the financial impact of items management does not consider in assessing our ongoing operating performance, and thereby facilitate review of our operating performance on aperiod-to-period

basis. Other companies may have different capital structures or different lease terms, and comparability to our results of operations may be impacted by the effects of acquisition accounting on our depreciation and amortization. As a result of the effects of these factors and factors specific to other companies, we believe theNon-GAAP

Measures, as applicable, provide helpful information to analysts and investors to facilitate a comparison of our operating performance to that of other companies. We also use Adjusted EBITDA, as further adjusted for additional items defined in our debt instruments, for board of director and bank compliance reporting. For a reconciliation of thesenon-GAAP

financial measures to the most directly comparable GAAP financial measures, see “Prospectus Summary—Summary Consolidated Historical Financial and Other Data.”iv

Non-GAAP

Measures have limitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of our operating results or cash flows as reported under GAAP. Some of these limitations are:| • | Non-GAAP Measures do not reflect certainone-time ornon-recurring cash costs to achieve anticipated synergies; |

| • | Non-GAAP Measures do not reflect changes in, or cash requirements for, our working capital needs; |

| • | EBITDA and Adjusted EBITDA do not reflect the significant interest expense or the cash requirements necessary to service interest or principal payments on our debt; |

| • | EBITDA and Adjusted EBITDA do not reflect income taxes or the cash payments related to income tax obligations; |

| • | Although depreciation and amortization are non-cash charges, the assets being depreciated or amortized may have to be replaced in the future, and EBITDA and Adjusted EBITDA and, with respect to acquired intangible assets, Adjusted Net Income, do not reflect any cash requirements for such replacements; |

| • | Non-GAAP Measures are adjusted for certainnon-recurring andnon-cash income or expense items that are reflected in our statements of operations; |

| • | Non-GAAP Measures do not reflect our cash expenditures or future requirements for capital expenditures or contractual commitments; and |

| • | Other companies in our industry may calculate these measures differently than we do, limiting their usefulness as comparative measures. |

Because of these limitations,

Non-GAAP

Measures should not be considered as measures of discretionary cash available to us to invest in the growth of our business. We compensate for these limitations by relying primarily on our GAAP results and usingNon-GAAP

Measures only for supplemental purposes. See our consolidated financial statements included elsewhere in this prospectus.v

LETTER FROM VIVEK SANKARAN, PRESIDENT & CHIEF EXECUTIVE OFFICER

Dear Prospective Stockholder,

In 1939, Joe Albertson opened the first Albertsons store at 16

th

and State streets in Boise, Idaho. The store featured welcoming associates, great products and great value. Since then, much has changed in the way we shop for and consume food; but at Albertsons, our purpose and values have not wavered. We remain committed to making every day better for our associates, our customers and our communities, never more so than through the unprecedented events of recent months.When I joined Albertsons from PepsiCo in April of 2019, I found a company that was well-positioned to benefit from changes affecting shopping and eating habits. The banners that make up Albertsons have earned customer loyalty over decades. Yet, in many ways, our Company is only a few years old. Since the Safeway merger in 2015, we have successfully completed the integration of our stores, supply chain and technology platforms. We have invested in capabilities allowing us to serve the customer wherever, whenever and however they choose to shop. We now benefit from one of the industry’s largest networks of

First-and-Main,

food retail locations with leading market shares in valuable and growing markets. It allows us to serve our customers locally, while delivering the advantages of national scale.All of these elements have come together in a corporate identity that is customer focused to make the shopping experience,and. We have developed a robust strategic framework to support this identity, resting on the four pillars of,,and. These pillars equip us to win in our sector. I believe we can deliver attractive and improving financial performance, grow market share and increase customer lifetime value through more engaged relationships across our omni-channel platform and loyalty ecosystem.

Easy

Exciting

Friendly

Growth

Productivity

Technology

Talent and

Culture

Our Goal & Identity

Our goal is to drive deep and lasting relationships with our customers. To achieve our goal, we offer a unique customer shopping experience that is,and– in our stores, at curbside, online and on mobile devices.

Easy

Exciting

Friendly

| • | Easy well-thought-out initiatives underway that seek to make the Albertsons shopping experience easier and more convenient for our existing customers and appealing to new customers. We are leveraging our exceptional store footprint to provide a full suite of omni-channel offerings, including Drive Up & Go curbside pickup and home delivery. We are working to make thein-store shopping experience quicker and easier through initiatives such as faster checkout and improvedin-store navigation. These capabilities are further enhanced through targeted technology investments and partnerships like the ones we have announced with Glympse for location sharing of store pickup and home delivery orders and Takeoff Technologies for automated micro-fulfillment to support our eCommerce efforts. We also seek to simplify the many food-related choices our customers face daily by offering efficient, comprehensive solutions such as meal planning, shopping list creation and prepared foods. |

| • | Exciting best-in-class fresh offerings encompass value-added organic, local and seasonal products. Examples include dailyfresh-cut fruit and vegetables, customized meat cuts and seafood varieties, made-from-scratch bakery items, convenient prepared meal solutions, deli offerings and beautiful floral designs. In many locations, we also provide attractive specialty offerings, including curated wine selections and artisan cheese shops. We feature a localized assortment that is customized to individual markets, like our Santa Monica Seafood in Southern California and our Hatch Chile salsa in Arizona. We continue to |

vi

| innovate with our Own Brands Own Brands O Organics Own Brands |

| • | Friendly non-customer-facing areas of our stores, freeing up our associates to do more of what they love: serving shoppers and providing a great customer experience. |

Our Strategic Framework

We support our,andidentity through a strategy that is designed to drive sustainable growth in our business. Our strategic framework rests on four key pillars: (1); (2); (3); and (4). Each of these pillars comprises specific, identified initiatives. We plan to grow ID sales by leveraging our core business–our stores, accelerating incremental eCommerce growth, continuing to increase the penetration of ourportfolio and increasing customer engagement and lifetime value through our extended loyalty ecosystem. We support our growth through a focus on productivity. We are working to optimize procurement and indirect spend. We are focused on delivering operational efficiencies, including shrink management, general and administrative expense discipline and labor and working capital productivity. We are also leveraging the national scale of our organization to “buy better” and create

Easy

Exciting

Friendly

Growth

Productivity

Technology

Talent and

Culture

Own Brands

best-in-class

supplier relationships. Since I joined the Company, we have developed and begun to implement specific productivity initiatives that target $1 billion of annualrun-rate

productivity benefits by the end of fiscal 2022 to help offset cost inflation, fund growth and drive earnings. While certain projects are well underway and contributing as expected, in other cases, we have temporarily paused some of our initiatives to ensure we are first taking care of our customers and our communities, while focusing on the safety of our associates during the coronavirus (COVID-19) pandemic.Technology, talent and culture underpin every strategic decision we make as an organization. They accelerate our,andidentity and the growth and productivity we are striving for. We are modernizing our technology infrastructure to drive enhancements for our customers, store operations, merchandising and our supply chain. Ongoing technology initiatives include digitizing and automating current capabilities, leveraging data science across our merchandising, pricing and promotional strategies and training our team to be more digitally minded. Lastly, our talent and culture remain Albertsons’ greatest resource. Our friendly service, inclusive environment and the deep community ties that we have developed, along with our nationwide loyalty ecosystem, help to drive higher customer lifetime value through increased purchase frequency, basket size, customer satisfaction and retention. We will continue to empower store-level decision makers, encourage frontline ownership and strengthen capabilities so that we remain.

Easy

Exciting

Friendly

Locally Great, Nationally Strong

We are proud of the progress we have made over the past few years. The importance of our role in the communities that we serve has been evident as we strive to meet our customers’ needs during the coronavirus (COVID-19) pandemic. Our highest priority has been ensuring the safety of our associates and customers as we continue to keep America fed. We have taken significant steps to invest in and protect our associates as they serve on the front lines of the public health crisis. They are heroes and I could not be more thankful for their tireless commitment to serving our customers and securing supply of our products to meet unprecedented levels of demand. We also donated $50 million to hunger relief to ensure families in the communities we serve have access to the food they need.

vii

Over the last few weeks, our country has once again confronted racism. At

Albertsons, we categorically and unambiguously condemn racism of any kind. It is a core principle that each person who walks through our doors will be treated with courtesy, dignity and respect. Those principles, which are deeply embedded into our culture, provide a critical touchstone for our team as civil unrest sweeps our country. We are committed to ongoing action to ensure that Albertsons sets an example in promoting equality and inclusion across our team and communities. We hope the coming months will mark the start of a new level of courage and compassion in our communities. We are committed to being a community leader in this effort, starting with the internal conversations that our leaders are having with their teams. We have and will continue to encourage listening with compassion and learning from our team how we can best enact real change in every community we serve. While we know this change cannot happen overnight, we are committed to seeing it through.

The way our Company has come together since the start of 2020 to support our associates, deliver on our commitment to our customers and support our communities gives me greater conviction in our bright future.

At Albertsons, we are just beginning the next chapter in our rich history, and we welcome you to join us on this exciting journey.

Vivek Sankaran

President & Chief Executive Officer

viii

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our common stock, you should carefully read this entire prospectus, including our consolidated financial statements and the related notes included elsewhere in this prospectus. You should also consider the matters described under the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in each case included elsewhere in this prospectus. Unless the context otherwise requires, the terms “ACI,” the “Company,” “we,” “us” and “our” refer to Albertsons Companies, Inc. and its consolidated subsidiaries.

OUR COMPANY

We are one of the largest food retailers in the United States, with 2,252 stores across 34 states and the District of Columbia. We operate 20 iconic banners with on average 85 years of operating history, includingand, with approximately 270,000 talented and dedicated employees, as of February 29, 2020, who serve on average more than 33 million customers each week. Additionally, as of February 29, 2020, we operated 1,290operating structure empowers decision making at the local level, which we believe better serves our customers and communities, while also providing the systems, analytics and buying power afforded by an organization with national scale and $62.5 billion in annual sales. Throughout the coronavirus (COVID-19) pandemic, our highest priorities have been the safety of our associates and customers and maintaining the supply of product. During the first eight weeks of fiscal 2020, we have delivered strong sales growth and increases in market share across our portfolio.

Albertsons, Safeway, Vons, Pavilions, Randalls, Tom Thumb, Carrs, Jewel-Osco, Acme, Shaw’s, Star Market, United Supermarkets, Market Street

Haggen

in-store

branded coffee shops, 402 adjacent fuel centers, 23 dedicated distribution centers, 20 manufacturing facilities and various online platforms. Our stores operate inFirst-and-Main

retail locations and have leading market share within attractive and growing geographies. We hold a #1 or #2 position by market share in 68% of the 121 metropolitan statistical areas (“MSAs”) in which we operate. Our portfolio of well-located, full-service stores provides the foundation of our omni-channel platform, including our rapidly growing Drive Up & Go curbside pickup, home delivery and rush delivery offerings. We seek to tailor our offerings to local demographics and preferences of the markets that we operate in. OurLocally Great, Nationally Strong

We are focused on creating deep and lasting relationships with our customers by offering them an experience that is,and– wherever, whenever and however they choose to shop. We make lifefor our customers through a convenient and consistent shopping experience across our omni-channel network. Merchandising is at our core and we offer anand differentiated product assortment. We believe we are an industry leader in fresh, emphasizing organic, locally sourced and seasonal items as well as value-added services like dailyportfolio, which achieved over $13.1 billion in sales during fiscal 2019 and reached 25.4% sales penetration. Ourservice is embedded in our culture and enables us to build deep ties with our local communities.

Easy

Exciting

Friendly

Easy

Exciting

fresh-cut

fruit and vegetables, customized meat cuts and seafood varieties, made-from-scratch bakery items, prepared foods, deli and floral. We also continue to grow our innovative and distinctiveOwn Brands

Friendly

|  | |||

1

Our,andshopping experience, coupled with our nationwide, grocery and fuel rewards programs and pharmacy services, offers a differentiated value proposition to our customers. Theprogram has 20.7 million registered loyalty households which, we believe, provides us with a comprehensive understanding of our core shoppers. These loyalty programs and our omni-channel offerings combine to form an extended loyalty ecosystem that drives increased customer lifetime value through greater purchase frequency, larger basket size and higher customer retention.

Easy

Exciting

Friendly

just for U

just for U

Our Company has grown through a series of transformational acquisitions over the last six years, including our merger with Safeway in 2015 which gave us the benefits of national scale. While our banners have rich histories, we are in many ways a young company. We have integrated systems and converted stores and distribution centers to create a common platform. We believe our common platform gives us greater transparency and compatibility across our network, allowing us to better serve our customers and employees while enhancing our supply chain.

We continue to sharpen our in-store execution, increase our

Own Brands

penetration and expand our omni-channel and digital capabilities. We have invested substantially in our business, deploying approximately $6.8 billion of capital expenditures beginning with fiscal 2015, including the $1.5 billion we spent in fiscal 2019. We used that capital to remodel existing stores, opportunistically build new stores and enhance our digital capabilities. We have also developed and begun to implement specific productivity initiatives across our business that target $1 billion of annual run-rate productivity benefits by the end of fiscal 2022 to help offset cost inflation, fund growth and drive earnings. While certain projects are well underway and contributing as expected, in other cases, we have temporarily paused some of our initiatives to ensure we are first taking care of our customers and our communities, while focusing on the safety of our associates during the coronavirus (COVID-19) pandemic.We have enhanced our management team, adding executives with complementary backgrounds to position us well for the future, including our President and CEO, Vivek Sankaran, who joined the Company from PepsiCo in April 2019. In fiscal 2019, we also added Chris Rupp as Chief Customer & Digital Officer and Mike Theilmann as Chief Human Resources Officer. In addition, we have internally promoted and expanded the roles of certain key members of our leadership team, including Susan Morris, our Chief Operations Officer, and Geoff White, our Chief Merchandising Officer.

Our recent operational initiatives are driving positive financial momentum. We realized strong financial performance in fiscal 2019, generating net sales of $62.5 billion, Adjusted EBITDA of $2.8 billion and Adjusted Free Cash Flow of $1.4 billion. We have achieved nine consecutive quarters of positive identical sales growth. Adjusted EBITDA grew from $2.7 billion in fiscal 2018 to $2.8 billion in fiscal 2019 and we generated a cumulative $6.7 billion in Adjusted Free Cash Flow since the start of fiscal 2015. The momentum we are experiencing gives us confidence that ourandidentity resonates with customers. We believe our strategic framework will enable us to continue delivering profitable growth going forward.

Easy, Exciting

Friendly

Identical Sales | Net Income ($mm) | Adj. EBITDA ($mm) | ||

|  |  | ||

2

Cumulative Adjusted Free Cash Flow (in billions)

DRIVERS OF CURRENT MOMENTUM

We have achieved significant near-term momentum in our business through a number of successful and ongoing initiatives, including the following:

Sharpened In-Store Execution.

in-store

execution and enhancing our customer experience to drive profitable growth. We have simplified our merchandising programs, automated ourfront-end

scheduling processes and expanded self-checkout in 533 additional stores during fiscal 2019. These enhancements have been instrumental in improving store-level productivity, allowing us to increase our focus on the customer. To further enhance the customer experience, we remerchandised over 850 stores since the beginning of fiscal 2017, reallocating space to better accentuate high growth fresh categories like produce, meat and seafood, bakery, prepared foods, deli and floral. This, coupled with our robust remodel program, has also allowed us to optimize store layouts and ease shopping patterns to make things simpler for customers and employees.Increased

Own Brands

Penetration.

Own Brands

Own Brands

Own Brands

Leading Omni-Channel Capabilities.

ready-to-eat

offerings. We now offer home delivery services across more than 2,000 of our stores and 12 of the country’s top 15 MSAs by population. The coronavirus (COVID-19

) pandemic has significantly increased demand for food-at-home, particularly through our eCommerce offerings. As a result we have accelerated our Drive Up & Go build out and have made several enhancements to our eCommerce platform that we believe will meaningfully improve the overall customer experience and enable us to drive growth and market share. |  |  | ||||||||

Investment in Stores and Technology Capabilities.

3

stores, as well as merchandising and maintenance initiatives. We also increased investment in digital and technology projects, including approximately $375 million spent in fiscal 2019. These investments include upgraded pricing and promotional tools and more integrated and

easy-to-use customer-facing digital applications.

Continued Focus on Productivity

.

With the integration of Safeway behind us, we have developed and are in the early stages of implementing a new set of clearly defined productivity initiatives that are underpinned by technology and talent. We are targeting $1 billion of annual run-rate productivity benefits by the end of fiscal 2022 to help offset cost inflation, fund growth and drive earnings. These initiatives include a focus on enhancing store and distribution center operations, leveraging scale to buy better, increasing promotional effectiveness and leveraging general and administrative costs. For example, we implemented a shrink reduction program centered on the use of technology as well as employee and manager education. As a result, we successfully reduced shrink levels by approximately 45 basis points in fiscal 2019 over fiscal 2017. We also believe these productivity initiatives will drive tangible improvements in our customer satisfaction and customer service scores. While certain projects are well underway and contributing as expected, in other cases, we have temporarily paused some of our initiatives to ensure we are first taking care of our customers and our communities, while focusing on the safety of our associates during the coronavirus (COVID-19) pandemic.OUR COMPETITIVE STRENGTHS

We are focused on driving deep and lasting relationships with our customers by delivering an

and

shopping experience. We believe the following competitive strengths will help us to achieve our goal:

Robust Portfolio of Stores and Iconic Banners with Leading Market Shares.

| • | Well-Known Banners |

| • | Prime Locations First-and-Main locations, providing our customers with exceptional convenience. Our owned and ground leased stores and distribution centers, which represent approximately 39% of our store and distribution base, have an aggregate appraised value of $11.2 billion. |

| • | Strong Market Share and Local Market Density coronavirus ( COVID-19) pandemic and the strength of our supply chain. |

| • | Highly Attractive Markets one-third of the U.S. population and approximately 45% of U.S. GDP. In 60% of the 121 MSAs in which we operate, the projected population growth over the next five years, in aggregate, exceeds the national average by over 60%. |

4

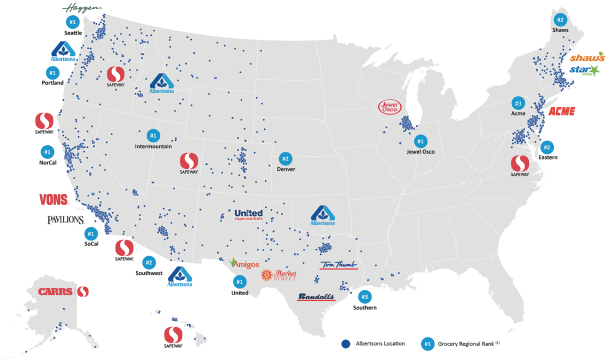

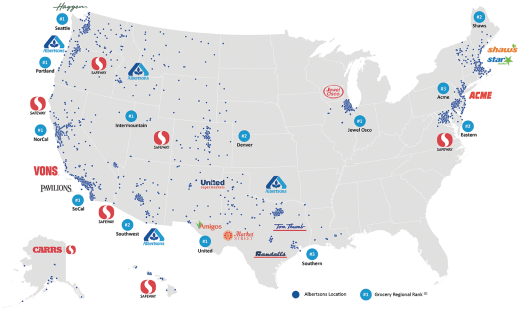

The following illustrative map represents our regional banners and combined store network as of February 29, 2020.

1

Nielsen ACView based on food markets in Company operating geographies as of calendar fourth quarter 2019.Differentiated and Exciting Merchandise Offering.

Exciting

in-store

fresh-cut

fruit,in-store

preparedready-to-cook

vegetables and fresh-made guacamole. In meat and seafood, we featurebest-in-class

full service butcher blocks that highlightcustom-cut

USDA Choice and Prime beef, ground chicken and pork, seasonal smoked meats like sausages and bacon,Open Nature

grass-fed

beef, lamb and wild-caught Alaskan salmon as well as a wide range of responsibly sourced waterfront bistro shrimp. Our bakeries feature scratch-made pastries, artisan breads, and cakesdesigned-to-order

by trained 5 Star decorators. Our prepared foods includeready-to-eat,

ready-to-heat,

andready-to-cook

meal solutions that encompass everything from family favorites to a wide range of world cuisine offerings. Our fresh offerings are complemented by strong specialty assortments. These include our curated wine selections and artisan cheese shops. As our customers demand healthy options and product transparency, we have grown our natural and organic sales nearly twice as fast as the rest of the store during fiscal 2019, with sales penetration of approximately 13% for the same period.5

|  |  |  |  |

High-Quality Own Brands That Deliver Great Value.

Own Brands

Own Brands

Own Brands

Own Brands

Value Corner

Signature Reserve

Own Brands

Lucerne

Signature Select

Signature Café

O Organics

Own Brands

Own Brands

Own Brands

Own Brands

top-line

growth and margin expansion. Sustainability is also a top priority with ourOwn Brands

Own Brands

|

|

Integrated Omni-Channel Solutions.

Drive Up & Go

| • Currently available in approximately 650 locations, with plans to grow to 1,600 locations in the next two years• Easy-to-use mobile app• Convenient, well-signed, curbside pickup |

6

Home Delivery

| • First launched home delivery services in 2001• Provide home delivery using our own “white glove” delivery service in approximately 60% of our stores• Operate over 1,000 multi-temperature delivery trucks to support home delivery growth• Successful roll out of new eCommerce website and mobile applications to all divisions |

Rush Delivery

| • Launched rush delivery in 2017 with Instacart• Delivery within one to two hours in all divisions and covering over 2,000, or nearly 90%, of our stores offered in collaboration with third parties• Partnership with Grubhub and Uber Eats adds delivery offerings for our prepared andready-to-eat options from our stores |

Strong Relationships with Loyal Customers.

just for U

just for U

just for U

Engagement in Enhanced Loyalty Ecosystem Increases Customer Lifetime Value

Note: Charts above based on data from a single market division and reflect indexed annual grocery spend and lifetime value versus store-only shoppers who do not participate in our loyalty ecosystem.

1

Programs are just for U, grocery and fuel rewards, pharmacy services, Drive Up & Go and home delivery.2

Defined as annual average gross profit multiplied by average years shopping.Disciplined Approach to Capital Investment and Strong Adjusted Free Cash Flow and Balance Sheet.

7

$3.8 billion of capital expenditures on remodels, upgrades, new stores and merchandising initiatives during this period. We have also invested to enhance our digital and technology assets. We believe these investments have been instrumental in maintaining our position as a leader in the food retail industry. Our strong Adjusted Free Cash Flow profile allows us the flexibility to invest in our business. Beginning with fiscal 2015, the first year after our merger with Safeway, we have generated cumulative Adjusted Free Cash Flow of $6.7 billion through the end of fiscal 2019. We have also reduced our outstanding Net Debt by approximately $3.0 billion since the end of fiscal 2017, decreasing our Net Debt Ratio from 4.7x to 2.9x as of the end of fiscal 2019.

New Best-In-Class Leadership with a Fresh Perspective.

Own Brands

Our team believes in the power of ourapproach. We empower our operators to take ownership of local merchandising and

Locally Great, Nationally Strong

in-store

execution. This enables our local managers to select the best product assortments for their communities, provide a heightened level of customer service and drive improved store performance. This localized approach has been such an important part of our heritage and success.OUR STRATEGIC FRAMEWORK

We are focused on providing our customers with an

and

shopping experience. We support our identity through a strategic framework that rests on four key pillars:

,

,

and

.

Growth:

| • | Achieve More Identical Sales Growth From Our Stores |

| • | Merchandising Excellence Exciting re-merchandised more than 850 stores and plan to expand this successful program. |

| • | Pricing and Promotions |

8

| • | Operating Excellence in-store efficiency by using technology to optimize labor and improvein-stock and display execution, resulting in enhanced store productivity and customer satisfaction. A number of these initiatives are already underway. In stores where we have introduced computer-assisted ordering and production systems, for example, we have seen a meaningful uplift in sales and improved levels ofin-stocks, inventory and shrink. |

| • | Culture of Exceptional Service in-store technology to achieve labor efficiencies through the automation ofnon-customer-facing tasks. We expect this effort to provide our associates more time to better serve customers, enhancing the shopping experience and driving purchase frequency, larger basket size, customer satisfaction and retention. |

| • | Targeted Store Remodels Easy Exciting Friendly |

| • | Drive Incremental eCommerce Growth: a strong growth engine that drives incremental sales. We plan to sustain our eCommerce growth through a number of initiatives. First, we will extend our Drive Up & Go pickup service to approximately 1,600 locations in the next two years. The coronavirus (COVID-19) pandemic has driven significant eCommerce volumes that have caused us to accelerate our omni-channel investments and our Drive up & Go build out. Additionally, we are refreshing our entire digital interface to create a more personalized, easy-to-use and fully-integrated digital experience. We are improving our mobile applications to enable more personalized rewards and services like advanced basket-building tools and product, meal and recipe recommendations. We are further integrating our digital andin-store models to better drive existing customer engagement and new customer trial for our own and third-party delivery. |

| • | Accelerate Own Brand Penetration Own Brands Own Brands Own Brands |

| • | Increase Customer Engagement and Lifetime Value: just for U just for U |

Productivity:

run-rate

productivity benefits by the end of fiscal 2022. This will help us to offset cost inflation, fund growth and drive earnings. Our initiatives include the following:| • | Enhancing Store and DC Operations: non-customer-facing tasks and drive labor productivity. For example, we are working to roll out enhanced demand forecasting and replenishment systems to improve operating efficiency, reduce product waste and optimize labor and inventory levels. We expect to scale these opportunities across the business quickly and efficiently. |

9

| • | Leveraging Scale to Buy Better: |

| • | Increasing Promotional Effectiveness: |

| • | Leveraging G&A: . |

While certain projects are well underway and contributing as expected, in other cases, we have temporarily paused some of our initiatives to ensure we are first taking care of our customers and our communities, while focusing on the safety of our associates during the coronavirus (COVID-19) pandemic.

Technology:

| • | Customers: check-out processes and improve ourat-store pickup experience. For example, we are partnering with Adobe to provide an artificial intelligence-powered solution to personalize the website and mobile application experience. This will enable the customer to see personalized products and information as they browse homepages, categories and product detail pages. |

| • | Store Operations: forecasting and replenishment tools such as computer-assisted ordering and production systems should sharpen our ability to predict store demand and track perpetual inventory, helping us to reduce out-of-stocks, inventory, and shrink. |

10

Additionally, we have begun to introduce

in-store

micro-fulfilment centers (MFCs) to provide enhanced capabilities for last-mile delivery that leverage our well-located store base as the distribution point for online orders. Early learnings from our partnership with Takeoff Technologies indicate improved picking efficiency by more than seven times compared toin-store

services as well as better inventory management andon-time

delivery. We plan to have 10 more MFCs operating within the next two years, in addition to the two operating today. |  |

| • | Merchandising |

| • | Supply Chain: |

Talent and Culture:

11

Across all segments of our business, our associates seek to deliver for our customers, our community, and our Company through their sales and service focus. We seek to celebrate the diversity and inclusiveness of our workforce and focus on improving our communities through sustainability and charitable activities that are an essential part of our business. As we leverage our national scale for efficiencies, we will continue to empower store-level decision makers to take care of our customers and encourage frontline responsibility. We will also continue to nurture an ownership mindset in our stores and ensure that the interests of those who directly manage our customer relationships on a daily basis are aligned with those of our stockholders.

|  |

12

RISKS RELATED TO OUR BUSINESS AND THIS OFFERING

An investment in our common stock involves a high degree of risk. You should carefully consider the risks highlighted in the section entitled “Risk Factors” following this prospectus summary before making an investment decision. These risks include, among others, the following:

| • | coronavirus ( COVID-19 ) related factors, risks and challenges, including among others, the length of time that the pandemic continues, the temporary inability of customers to shop due to illness, quarantine, or other travel restrictions or financial hardship, shifts in demand away from discretionary or higher priced products to lower priced products, or stockpiling or similar pantry-filling activities, reduced workforces which may be caused by, but not limited to, the temporary inability of the workforce to work due to illness, quarantine, or government mandates, potential shortages in supply, or temporary store closures due to reduced workforces or government mandates; |

| • | the competitive nature of the industry in which we conduct our business; |

| • | general business and economic conditions, including the rate of inflation or deflation, consumer spending levels, population, employment and job growth and/or losses in our market; |

| • | our ability to increase identical sales, expand our Own Brands |

| • | our ability to expand or grow our home delivery network and Drive Up & Go curbside pickup services; |

| • | pricing pressures and competitive factors, which could include pricing strategies, store openings, remodels or acquisitions by our competitors; |

| • | labor costs, including benefit plan costs and severance payments, or labor disputes that may arise from time to time and work stoppages that could occur in areas where certain collective bargaining agreements have expired or are on indefinite extensions or are scheduled to expire in the near future; |

| • | disruptions in our manufacturing facilities’ or distribution centers’ operations, disruption of significant supplier relationships, or disruptions to our produce or product supply chains; |

| • | results of any ongoing litigation in which we are involved or any litigation in which we may become involved; |

| • | data privacy and security, the failure of our IT systems, or maintaining, expanding or upgrading existing systems or implementing new systems; |

| • | the effects of government regulation and legislation, including healthcare reform; |

| • | our ability to raise additional capital to finance the growth of our business, including to fund acquisitions; |

| • | our ability to service our debt obligations, and restrictions in our debt agreements; |

| • | risks related to the Convertible Preferred Stock, the Investor Exchange Right and the impact it may have on our common stock; |

| • | the impact of private and public third-party payers’ continued reduction in prescription drug reimbursements and the ongoing efforts to limit participation in payor networks, including through mail order; |

| • | plans for future growth and other business development activities; |

| • | our ability to realize anticipated savings from our implementation of cost reduction and productivity initiatives; |

| • | changes in tax laws or interpretations that could increase our consolidated tax liabilities; and |

| • | competitive pressures in all markets in which we operate. |

13

CORONAVIRUS (

COVID-19

) Related DEVELOPMENTSSince the beginning of the coronavirus (

COVID-19

) pandemic, we have acted swiftly to prioritize the safety of our front-line associates and customers, while delivering the essential services we provide in our communities. In responding to the pandemic, we have taken a number ofpro-active

steps. Among other steps, we have:| • | Increased the frequency of how often we clean and disinfect all departments, restrooms, and other high-touch points of our stores, including check stands and service counters, and hourly disinfecting of high-touch areas. This is in addition to our rigorous food safety and sanitations programs already in place. |

| • | Installed cart wipes and hand sanitizer stations in key locations within stores. |

| • | Adjusted store hours in certain stores to give store teams the time they need to rest, restock shelves and clean and disinfect. |

| • | Reserved special times for seniors and other vulnerable shoppers who must leave home to obtain their groceries. |

| • | Installed plexiglass in our checkout lanes in all stores to serve as a protective barrier at the check stand. |

| • | Secured masks and gloves for our front-line employees. |

| • | Limited store occupancy to ensure proper social distancing during all hours, and further limited occupancy during times reserved for our most vulnerable customers to improve safety. |

| • | Responded to increased demand for our eCommerce offerings by hiring additional pickers and drivers, and also simplified eCommerce offerings to focus on the products that are most in demand. |

| • | Instituted “contact-free” delivery procedures for home delivery and Drive Up & Go. |

| • | Announced a temporary increase in pay for all front-line associates of $2 per hour for every hour that they work beginning March 15, 2020 through June 13, 2020 in recognition of their significant efforts. In addition, we are making a final weekly reward payment to front-line associates during the week ended June 20, 2020 of $4 per hour based upon the average weekly hours associates worked during the period from March 15, 2020 through June 13, 2020. |

| • | Increased hiring since the beginning of fiscal 2020, partnering with more than 35 companies to help keep Americans working, and now have approximately 310,000 associates. |

| • | Announced a commitment of $50 million to hunger relief and previously launched a major fundraiser to help feed families in need during the coronavirus ( COVID-19 ) pandemic and to help ensure that they get the food they need. |

On March 12, 2020, we provided notice to the lenders to borrow $2.0 billion under our ABL Facility (as defined herein) (such borrowing, the “ABL Borrowing”), so that a total of $2.0 billion (excluding $454.5 million in letters of credit) was outstanding immediately following the borrowing. We increased our borrowings under the ABL Facility as a precautionary measure in order to increase our cash position and preserve financial flexibility in light of current uncertainty in the global markets resulting from the coronavirus (COVID-19) pandemic. We have not needed to use the proceeds of the ABL Borrowing and have provided notice and will repay the ABL Borrowing in full on June 19, 2020. For more information on our existing indebtedness, see “Description of Indebtedness.”

Since the beginning of fiscal 2020, we have experienced significant increases in customer traffic, product demand and overall basket size in stores and in our eCommerce business as customers adjust to the circumstances around coronavirus (COVID-19). As a result, identical sales increased 47% during the first four weeks of fiscal 2020 (ending March 28, 2020), increased 21% during the second four weeks of fiscal 2020 (ending April 25, 2020), and increased 21% during the third four weeks of fiscal 2020 (ending May 23, 2020), compared to 0.5%, 3.6% and 0.5% increases in identical sales in the first four weeks of fiscal 2019, second four weeks of fiscal 2019 and third four weeks of fiscal 2019, respectively. Identical sales for the first 12 weeks of

fiscal 2020 increased 30% compared to 1.5% in the first 12 weeks of fiscal 2019. In addition, our cash balance as14

of

May 23, 2020 was approximately $4.0 billion, which includes the proceeds from the ABL Borrowing, and our Net Debt as of May 23, 2020 was approximately $6.7 billion. Our cash balance and Net Debt at the end of the comparable period in fiscal 2019 was approximately $1.1 billion and $9.4 billion, respectively, and at the end of fiscal 2019 was $471 million and $8.2 billion, respectively. The increase in cash balance as of May 23, 2020, after adjusting for the ABL Borrowing, is primarily attributable to incremental operating cash flows driven by the increased sales performance and from changes in inventory and accounts payable working capital. We spent $311 million on capital expenditures in the first 12 weeks of fiscal 2020 compared to $293 million in the first 12 weeks of fiscal 2019. On June 19, 2020, the ABL Borrowing will be repaid in full without having been used.

Since the end of fiscal 2019, we have experienced an increase in overall flow from our increased sales performance as our gross margin rate was approximately 30.4% for the first 12 weeks of fiscal 2020 compared to 27.9% for the first 12 weeks of fiscal 2019. Excluding fuel sales, our gross margin rate increased 140 basis points in the first 12 weeks of fiscal 2020 compared to the first 12 weeks of fiscal 2019. Selling and administrative expenses as a percent of net sales was 24.5% for the first 12 weeks of fiscal 2020 compared to 25.3% for the first 12 weeks of fiscal 2019. Excluding fuel sales, our selling and administrative expenses as a percent of net sales decreased 160 basis points in the first 12 weeks of fiscal 2020 compared to the first 12 weeks of fiscal 2019. The improved gross margin rate and selling and administrative rate were primarily the result of increased leveraging of our costs, partially offset by increased expenses related to our response to the coronavirus (COVID-19) pandemic.

Subject to opportunistic investments, we currently expect our Net Debt at the end of fiscal 2020 will be approximately $6.7 billion as we anticipate that incremental cash flow from our business will, subject to seasonal fluctuations, fund capital expenditures, debt service, working capital replenishment, dividends and other operating needs. It is too early to predict the permanent impact the coronavirus (COVID-19) pandemic will have on our industry or food-at-home consumption or what the impact on sales will be going forward.

PRIVATE PLACEMENT OF CONVERTIBLE PREFERRED STOCK

On May 20, 2020, we entered into an investment agreement which was amended and restated on June 9, 2020 (the “Investment Agreement”) with certain investors (collectively, the “Preferred Investors”) led by funds managed, advised or controlled by affiliates of Apollo Global Management, Inc. (“Apollo”), relating to the sale and issuance of $1.75 billion aggregate liquidation preference of Convertible Preferred Stock with an initial dividend rate of 6.75%. On June 9, 2020 (the “Preferred Closing Date”), we sold and issued, (i) an aggregate of 1,410,000 shares of Series A-1 preferred stock, and (ii) an aggregate of 340,000 shares of Series A preferred stock. The Convertible Preferred Stock is convertible into common stock based on an initial conversion price of $17.22 per share. Based on the 580,638,489 shares of common stock outstanding as of May 20, 2020, the date we entered into the Investment Agreement, if the Preferred Investors converted all $1.75 billion of the aggregate liquidation preference of the Convertible Preferred Stock, the Preferred Investors would hold 17.5% of outstanding common stock. The Convertible Preferred Stock has certain voting rights and is subject to, commencing on the third anniversary of the date of the closing of an initial public offering that generates gross cash proceeds to us and/or selling stockholders of at least $1 billion in the aggregate (“Qualified IPO”), subject to certain limitations, mandatory conversion if the trading price of our common stock has equaled or exceeded $20.50 per share (a 19% premium to the conversion price). The Convertible Preferred Stock is subject to redemption at our option following the sixth anniversary of the Preferred Closing Date and under certain other circumstances, as described below.

In addition, on May 20, 2020, ACI Real Estate Company LLC, a Delaware limited liability company, that is a subsidiary of Safeway and our indirect subsidiary (“RE LLC”), and AL RE Investor Holdings, LLC, a

15

Delaware limited liability company (“RE Investor”), entered into a real estate agreement which was amended and restated on June 9, 2020 (the “Real Estate Agreement”), pursuant to which, on the Preferred Closing Date, RE Investor purchased the right, upon certain specified triggering events and to the extent that any shares of Convertible Preferred Stock then remain outstanding, to exchange all of the outstanding Convertible Preferred Stock for equity interests in certain newly-formed subsidiaries of RE LLC (such subsidiaries, the “SPEs”) or the real property assets (“Real Estate Assets”) held by the SPEs (such right to exchange, the “Investor Exchange Right”). The triggering events are the occurrence of any of the following: (i) the seventh anniversary of the Preferred Closing Date, so long as any shares of Convertible Preferred Stock are outstanding, (ii) the fourth anniversary of an initial public offering, if a Fundamental Change (as defined herein, but which includes, among others, certain changes of control and, following a Qualified IPO, a delisting of our common stock) occurs and the related Fundamental Change Stock Price (as defined in the Certificate of Designations (as defined herein)) is less than the conversion price, (iii) a downgrade by one or more gradations (including gradations within ratings categories as well as between ratings categories) or withdrawal of our credit rating by both Moody’s Investors Service, Inc. (“Moody’s”) and Standard & Poor’s Ratings Services (“S&P” and together with Moody’s, the “Rating Agencies”), as a result of which our credit rating is B- (or Moody’s equivalent) or lower, (iv) the failure by us to pay a dividend on the Convertible Preferred Stock, which failure continues for 30 days after such dividend’s due date, or (v) a Bankruptcy Filing (as defined in the Real Estate Agreement).

The aggregate purchase price paid by the Preferred Investors under the Investment Agreement and RE Investor under the Real Estate Agreement was $1.68 billion. We used cash in an amount equal to the proceeds from the sale and issuance of the Convertible Preferred Stock and the Investor Exchange Right for the Repurchase.

STOCK SPLIT

On June 18, 2020, our board of directors and stockholders approved, and we effected, a 2.072-for-1 forward stock split of our common stock.

Corporate Information

Our principal executive offices are located at 250 Parkcenter Blvd., Boise, ID 83706. Our telephone number is (208)

395-6200

and our internet address is www.albertsonscompanies.com.Our website and the information contained thereon are not part of this prospectus and should not be relied upon by prospective investors in connection with any decision to purchase the common stock offered hereby.

Our Sponsors

We believe that one of our strengths is our relationship with our Sponsors. We believe we will benefit from our Sponsors’ experience in the retail industry, their expertise in mergers and acquisitions and real estate, and their support on various near-term and long-term strategic initiatives.

Cerberus

16

Kimco Realty Corporation

Klaff Realty, L.P.

Lubert-Adler

Management

.co-founded

in 1997 by Ira Lubert and Dean Adler, who collectively have over 65 years of experience in underwriting, acquiring, repositioning, refinancing and disposing of real estate assets. Lubert-Adler has more than 20 investment professionals and has invested $7.8 billion of equity into assets valued at $20 billion.Schottenstein Stores Corp.

Our Sponsors control us and will continue to be able to control the election of our directors, determine our corporate and management policies and determine, without the consent of our other stockholders, the outcome of any corporate transaction or other matter submitted to our stockholders for approval, including potential mergers or acquisitions, asset sales and other significant corporate transactions. Following the Repurchase and the completion of the Distribution and this offering, Cerberus will own approximately 31.9% of our common stock, Kimco will own approximately 8.0% of our common stock, Klaff Realty will own approximately 11.7% of our common stock, Lubert-Adler will own approximately 11.7% of our common stock and Schottenstein will own approximately 11.7% of our common stock and our Sponsors will own in the aggregate approximately 75.0% of our common stock, or 73.0% if the underwriters exercise their option to purchase additional shares in full. Our Sponsors will enter into a Stockholders’ Agreement (as defined herein), pursuant to which they will agree to act in concert and vote together on certain matters. As a result, we expect to be a “controlled company” within the meaning of the corporate governance standards of the NYSE on which we will apply to list our shares and, as a result, will qualify for, and intend to rely on, exemptions from certain corporate governance requirements. As a result, our stockholders will not have the same protections afforded to stockholders of companies that are subject to such requirements.

Following the completion of the Distribution and this offering, we will be required to appoint to our board of directors individuals designated by and voted for by our Sponsors. In connection with this offering, we will enter into a stockholders agreement with our Sponsors (the “Stockholders’ Agreement”). If Cerberus (or a permitted transferee or assignee) has beneficial ownership of at least 20% of our then-outstanding common stock, it shall have the right to designate four directors to our board of directors. If Cerberus (or a permitted transferee or assignee) owns less than 20% but at least 10% of our then-outstanding common stock, it shall have the right to designate two directors to our board of directors. If Cerberus (or a permitted transferee or assignee) owns less than 10% but at least 5% of our then-outstanding common stock, it shall have the right to designate one director to our board of directors. If Klaff Realty (or a permitted transferee or assignee) owns at least 5% of our then-outstanding common stock, it shall have the right to designate one director to our board of directors. If

17

Schottenstein Stores (or a permitted transferee or assignee) owns at least 5% of our then-outstanding common stock, it shall have the right to designate one director to our board of directors.

The interests of our Sponsors may not coincide with the interests of other holders of our common stock. Additionally, our Sponsors are in the business of making investments in companies and may, from time to time, acquire and hold interests in businesses that compete directly or indirectly with us. Our Sponsors may also pursue acquisition opportunities that may be complementary to our business, and as a result, those acquisition opportunities may not be available to us. So long as our Sponsors continue to own a significant amount of the outstanding shares of our common stock, they will continue to be able to strongly influence or effectively control our decisions, including potential mergers or acquisitions, asset sales and other significant transactions.

See “Risk Factors—Risks Related to This Offering and Owning Our Common Stock.”

18

THE OFFERING

| Common stock outstanding | 479,026,753 shares (excluding 101,612,000 shares initially issuable upon conversion of the Convertible Preferred Stock) |

| Common stock offered by the selling stockholders | 65,800,000 shares |

| Option to purchase additional shares of common stock | Certain of the selling stockholders have granted to the underwriters a 30-day option to purchase up to 9,870,000 additional shares of our common stock at the initial public offering price less the underwriting discount and commissions. |

| Use of proceeds | We will not receive any net proceeds from the sale of common stock by the selling stockholders, including from any exercise by the underwriters of their option to purchase additional shares of our common stock from the selling stockholders. |