Exhibit 99.2

Business Combination between Double Eagle and Williams Scotsman August 2017

Disclaimer Important Information About the Transaction and Where to Find It In connection with the proposed transaction described herein (the “Transaction”), Double Eagle intends to file a registration st atement on Form S - 4 (the “Registration Statement”) with the SEC, which will include a proxy statement/prospectus, that will be b oth the proxy statement to be distributed to holders of Double Eagle’s ordinary shares in connection with Double Eagle’s solicitation of proxies for the vote by Double Eagle’s share hol ders with respect to the Transaction and other matters as may be described in the Registration Statement, as well as the pros pec tus relating to the offer and sale of the securities to be issued in the Transaction. After the Registration Statement is declared effective, Double Eagle will mail a definitive proxy sta tement/prospectus and other relevant documents to its shareholders. Double Eagle’s shareholders and other interested persons are advised to read, when available, the preliminary proxy statement/prospectus included in the Registration Statement and the amendments thereto and the definitive p rox y statement/prospectus, as these materials will contain important information about Williams Scotsman International, Inc., Do ubl e Eagle and the Transaction. The definitive proxy statement/prospectus will be mailed to shareholders of Double Eagle as of a record date to be establishe d f or voting on the Transaction. Shareholders will also be able to obtain copies of the proxy statement/prospectus and other doc ume nts filed with the SEC that will be incorporated by reference in the proxy statement/prospectus, without charge, once available, at the SEC’s web site at www.sec.gov, or by dire cti ng a request to: Double Eagle Acquisition Corp., 2121 Avenue of the Stars, Suite 2300, Los Angeles, California, Attention: El i B aker, Vice President, General Counsel and Secretary, (310) 209 - 7280. Participants in the Solicitation Double Eagle and its directors and executive officers may be deemed participants in the solicitation of proxies from Double E agl e’s shareholders with respect to the Transaction. A list of the names of those directors and executive officers and a descrip tio n of their interests in Double Eagle is contained in Double Eagle’s annual report on Form 10 - K for the fiscal year ended December 31, 2016, which was filed with the SEC and is available fr ee of charge at the SEC’s web site at www.sec.gov, or by directing a request to Double Eagle Acquisition Corp., 2121 Avenue o f t he Stars, Suite 2300, Los Angeles, California, Attention: Eli Baker, Vice President, General Counsel and Secretary, (310) 209 - 7280. Additional information regarding the intere sts of such participants will be contained in the proxy statement/prospectus for the Transaction when available. Williams Scotsman International, Inc. and its directors and executive officers may also be deemed to be participants in the s oli citation of proxies from the shareholders of Double Eagle in connection with the Transaction. A list of the names of such dir ect ors and executive officers and information regarding their interests in the Transaction will be included in the proxy statement/prospectus for the Transaction when available. Forward - Looking Statements This presentation includes “forward - looking statements” within the meaning of the “safe harbor ” provisions of the Private Securities Litigation Reform Act of 1995. Double Eagle’s and Williams Scotsman International, Inc .’s actual results may differ from their expectations, estimates and projections and consequently, you should not rely on these forward looking statements as predictions of future events. Words such as “expect, ” “ estimate,” “project,” “budget,” “forecast,” “anticipate,” “intend,” “plan,” “may,” “will,” “could,” “should,” “believes,” “pr edi cts,” “potential,” “continue,” and similar expressions are intended to identify such forward - looking statements. These forward - looking statements include, without limitation, Double Eagle’s, Williams Scotsman International, Inc. ’s and TDR Capital LLP’s (acting in its capacity as investment fund manager, being together with its affiliates “TDR”) expectations with respect to future performance and anticipated financial impacts of the Transaction, the satisfaction of the closing conditions to the Transacti on and the timing of the completion of the Transaction. These forward - looking statements involve significant risks and uncertaintie s that could cause the actual results to differ materially from the expected results. Most of these factors are outside Double Eagle’s, Williams Scotsman International, Inc. ’s and TDR’s control and are difficult to predict. Factors that may cause such differences include, but are not limited to: (1) the occurr enc e of any event, change or other circumstances that could give rise to the termination of the definitive agreement for the Transaction (the “Transaction Agreement”), (2) the outcome of any lega l p roceedings that may be instituted against Double Eagle or Williams Scotsman International, Inc. following the announcement of th e Transaction Agreement and the transactions contemplated therein; (3) the inability to complete the Transaction, including due to failure to obtain approval of the share hol ders of Double Eagle or other conditions to closing in the Transaction Agreement; (4) delays in obtaining, adverse conditions co ntained in, or the inability to obtain necessary regulatory approvals or complete regulator reviews required to complete the transactions contemplated by the Transaction Agreement; (5) the risk that the Transaction disrupts current plans and operations as a result of the announcement and consummation of the Trans ac tion; (6) the ability to recognize the anticipated benefits of the Transaction, which may be affected by, among other things, competition, the ability of the combined company t o g row and manage growth profitably, maintain relationships with suppliers and obtain adequate supply of products and retain its ke y employees; (7) costs related to the Transaction; (8) changes in applicable laws or regulations; (9) the possibility that Williams Scotsman International, Inc. or the combined com pan y may be adversely affected by other economic, business, and/or competitive factors; and (10) other risks and uncertainties i ndi cated from time to time in the proxy statement/prospectus relating to the Transaction, including those under “Risk Factors” therein, and in Double Eagle’s other f ili ngs with the SEC. Double Eagle cautions that the foregoing list of factors is not exclusive. Double Eagle cautions readers no t t o place undue reliance upon any forward - looking statements, which speak only as of the date made. Double Eagle , Williams Scotsman International, Inc . and TDR do not undertake or accept any obligation or undertaking to release publicly any updates or revisions to any forward - looking statements to reflect any change in its expectations or any change in events, conditions or circumstances on which any such statement is based . Any investment made by a fund managed by TDR or any of its affiliates (a “TDR Fund”) will be made solely in accordance with t he legal documents relating to the relevant TDR Fund and not on the basis described in this presentation. Nothing in this presen tat ion gives rise to or is intended to give rise to any legal obligation on behalf of TDR, any TDR Fund, or any of its affiliates. No Offer or Solicitation This presentation shall not constitute a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the Transaction. This presentation shall also not constitute an offer to sell or the solicitation of an offer to b uy any securities, nor shall there be any sale of securities in any states or jurisdictions in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the se cur ities laws of any such jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requ ire ments of section 10 of the Securities Act of 1933, as amended. No Representation or Warranty None of Double Eagle, Williams Scotsman International, Inc. or any of their respective affiliates makes any representation or warranty as to the accuracy or completeness of the information co ntained in this presentation. The sole purpose of the presentation is to assist persons in deciding whether they wish to proceed with a further review of the Transaction and is not intended to be all - inclusive or to contain all the information that a person may desire in considering the Transaction. It is not intended to form the basis of any investment decision or any ot her decision in respect of the Transaction. Financial Information The financial information contained in this presentation has been taken from or prepared based on the historical financial st ate ments of Williams Scotsman International, Inc., without giving effect to the carve - out transaction described herein, for the per iods presented. An audit of these financial statements is in process and will be incorporated in the S - 4 filing. Use of Projections This presentation contains financial forecasts, including with respect to Williams Scotsman International, Inc.’s revenue, EBITDA and Adjusted EBITDA for 2017 and 2018. Neither Double Eagle’s nor Williams Scotsman International, Inc.’s independent auditors have audited, reviewed, compiled or p erf ormed any procedures with respect to the projections for the purpose of their inclusion in this presentation, and accordingly, neither of them expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this presentation. The se projections are for illustrative purposes only and should not be relied upon as being necessarily indicative of future results. In this presentation, certain of the above - mentioned projected information has been provided for purposes of providing compariso ns with historical data. The assumptions and estimates underlying the prospective financial information are inherently uncert ain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those co nta ined in the prospective financial information. Projections are inherently uncertain due to a number of factors outside of Wil lia ms Scotsman International, Inc.’s control. Accordingly, there can be no assurance that the prospective results are indicative of future performance of Williams Scotsman International, Inc . o r the combined company after the Transaction or that actual results will not differ materially from those presented in the pr osp ective financial information. Inclusion of the prospective financial information in this presentation should not be regarded as a representation by any person that the results containe d i n the prospective financial information will be achieved. Industry and Market Data In this presentation, we rely on and refer to information and statistics regarding market participants in the sectors in whic h W illiams Scotsman International, Inc. competes and other industry data. We obtained this information and statistics from third - pa rty sources, including reports by market research firms and company filings . The matters referred to in this presentation may, in whole or in part, constitute inside information for the purposes of the EU Market Abuse Regulation (596/2014) (or equivalent legislation). Being in receipt of the presentation you agree you may be res tri cted from dealing in (or encouraging others to deal in) price sensitive securities. Use of Non - GAAP Financial Measures This presentation includes non - GAAP financial measures, including EBITDA, Adjusted EBITDA, Adjusted EBITDA Margin, Adjusted Gross Profit, Adjusted Operating Income and Operating Free Cash Flo w. Double Eagle, Williams Scotsman International Inc. and TDR believe that these non - GAAP measures are useful to investors for two principal reasons. First, they believe these measures assist investors in comparing performance over various reporting periods on a con sis tent basis by removing from operating results the impact of items that do not reflect core operating performance. Second, the se measures are used by Williams Scotsman’s board of directors and management to assess its performance and may (subject to the limitations descri bed below) enable investors to compare the performance of Williams Scotsman and the combined company to its competitors. Double E ag le, Williams Scotsman International Inc. and TDR believe that the use of these non - GAAP financial measures provides an additional tool for investors to use in evaluating ongoing operating results and trends. These non - GAAP measures should not be considered in isolation from, or as an alternative to, financial measures determined in accordance wit h GAAP. Other companies may calculate EBITDA, Adjusted EBITDA, Adjusted EBITDA Margin, Adjusted Gross Profit, Adjusted Operating Income, Operating Free Cash Flow and other non - GAAP financial measures differently, and therefore Williams Scotsman’s non - GAAP financial measures may not be directly comparable to similarly titled measures of other companies . For reconciliation of the non - GAAP measures used in this presentation, see “Reconciliation of Non - GAAP Measures” in the Append ix at the end of this presentation (the “Appendix”). 2

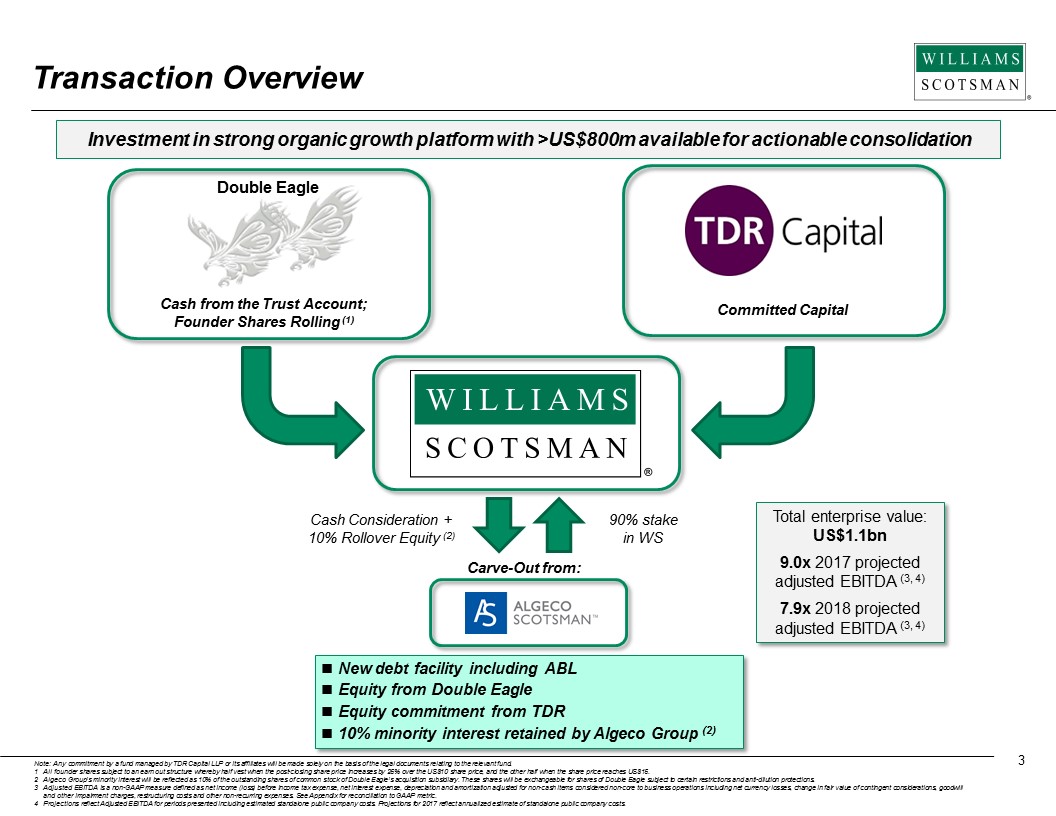

Transaction Overview 3 Investment in strong organic growth platform with >US$800m available for actionable consolidation Double Eagle Carve - Out from: Committed Capital Cash from the Trust Account; Founder Shares Rolling (1) New debt facility including ABL Equity from Double Eagle E quity commitment from TDR 10% minority interest retained by Algeco Group (2) Cash Consideration + 10% Rollover Equity (2) 90% stake in WS Total enterprise value: US$1.1bn 9.0x 2017 projected adjusted EBITDA (3, 4) 7.9x 2018 projected adjusted EBITDA (3, 4) Note : Any commitment by a fund managed by TDR Capital LLP or its affiliates will be made solely on the basis of the legal documents re lating to the relevant fund. 1 All founder shares subject to an earn out structure whereby half vest when the post - closing share price increases by 25% over the US$10 share price, and the other half wh en the share price reaches US$15 . 2 Algeco Group’s minority interest will be reflected as 10% of the outstanding shares of common stock of Double Eagle’s acquisition su bs idiary. These shares will be exchangeable for shares of Double Eagle subject to certain restrictions and anti - dilution protectio ns. 3 Adjusted EBITDA is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change i n fair value of contingent considerations, goodwill and other impairment charges, restructuring costs and other non - recurring expenses. See Appendix for reconciliation to GAAP metr ic. 4 Projections reflect Adjusted EBITDA for periods presented including estimated standalone public company costs. Projections for 2017 reflect annualized estimate of standalone public company costs .

Specialty Rental Services Market Leader in Modular Space & Portable Storage Solutions Compelling growth platform with substantial capital committed to accelerate organic growth and M&A Fast Growing Business with Strong Momentum and Visibility 1 US Adj. EBITDA ( 1) CAGR 2015 - 2018E; current run - rate underpins forecast 14% Share price performance in 21 months when public ( 3 ) 75% of new capital committed by TDR $500m >3x EV / Adj. EBITDA discount to Mobile Mini (1, 4) despite faster Williams Scotsman growth Actionable opportunities to double in size and benefit from highly accretive synergies >2x Platform to Consolidate and Capture Meaningful Synergies 3 Successful Previous Public Company Track Record 4 Robust Balance Sheet to Accelerate Growth 2 Significant Multiple Upside to Key Peer 5 Note : Any commitment by a fund managed by TDR Capital LLP or its affiliates will be made solely on the basis of the legal documents re lating to the relevant fund. 1 Adjusted EBITDA is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of contingent con siderations, goodwill and other impairment charges, restructuring costs and other non - recurring expenses . For a reconciliation of Adjusted EBITDA to net loss, see Appendix. 2 Assumes $490m of total debt and $125m of cash as well as 2017 projected Adjusted EBITDA of $122m . Projections reflect Adjusted EBITDA for periods presented including estimated standalone public company costs. 3 Reflects period from September 2005 to June 2007 without giving effect to changes in company business, strategy, management, general economic or market conditions or oth er factors due to the passage of time. Past performance is not indicative of future results and should not be relied upon as suc h. 4 Source : Bloomberg as of 11 August 2017 . Williams Scotsman multiple reflects implied acquisition multiple (b ased on 2018 projected Adjusted EBITDA of $ 139m) and excludes transaction expenses. 4 3.0x Net debt / 2017 Projected Adj. EBITDA (1, 2)

Experienced media/communications investor and studio/network CEO, incl. Sony Pictures Entertainment and CBS Sponsor and President of Global Eagle and Silver Eagle Serves as Director of the Boards of Scripps Networks Interactive, Global Eagle and Videocon d2h Served as CFO since October 2015; various Business Development roles since joining in 2012 Previously Vice President at Sterling Partners, supporting mid - market PE investments and portfolio company operations Prior to Sterling, Associate at Banc of America Capital Investors Founded TDR Capital with Manjit Dale in 2002 Over 30 years of private equity, mezzanine and leveraged finance experience Previously Chairman of Algeco Europe Joined TDR Capital in June 2008 15 years of private equity and leveraged finance experience Day to day management of Algeco Scotsman investment since 2010 22 years industry experience, including Chairman, President & CEO of Williams Scotsman from 1994 - 2010 Served as Algeco Scotsman Non - Executive Chairman since April 2010 Also Non - Executive Chairman of the FTI Consulting Board, as well as Director of Baker Corp. and Neff Corp. Gerry Holthaus , Chairman Tim Boswell, CFO Jeff Sagansky, CEO of Double Eagle (1) Stephen Robertson, Founding Partner (1) Gary Lindsay, Partner (1) 5 Served as CEO & President of Williams Scotsman since January 2014 Previously Chief Commercial and Strategy Officer of Novelis Held various positions at Cummins in product development, strategy and procurement in North America and Europe Brad Soultz, CEO & President Proven and Experienced Industry Veterans and Investors 1 Individual not expected to hold a significant management role in post - transaction business.

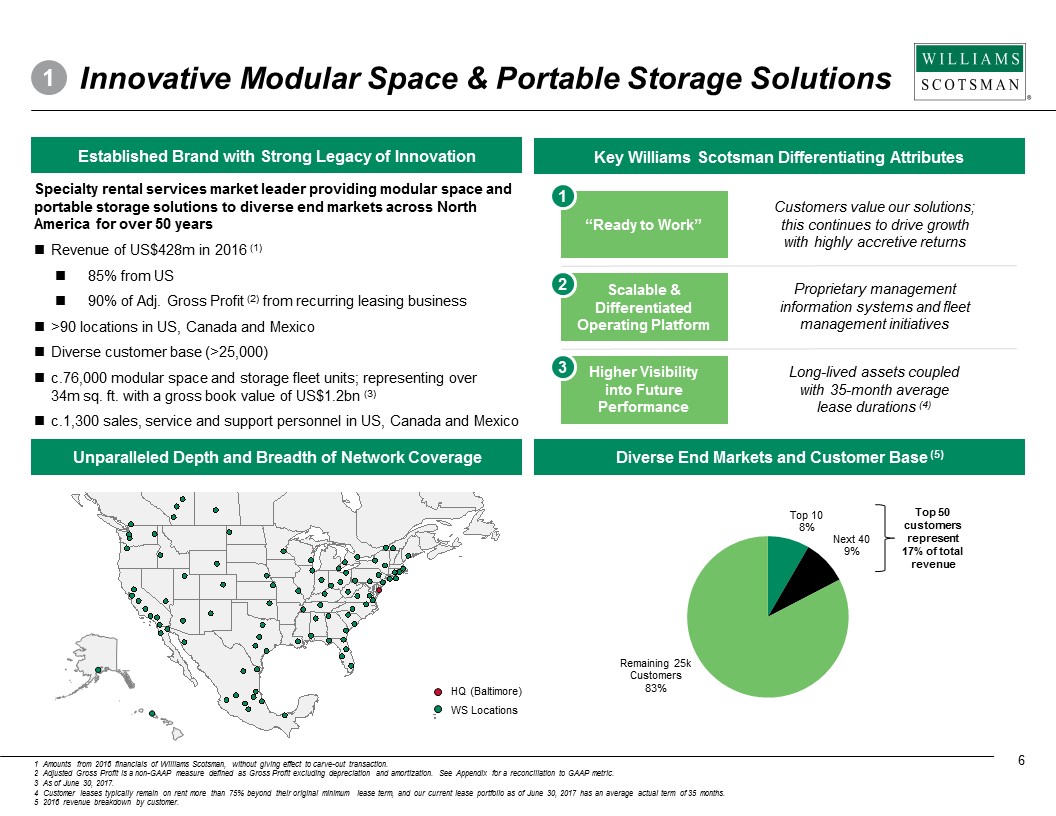

Unparalleled Depth and Breadth of Network Coverage Established Brand with Strong Legacy of Innovation Specialty rental services market leader providing modular space and portable storage solutions to diverse end markets across North America for over 50 years Revenue of US$428m in 2016 (1) 85% from US 90% of Adj. Gross Profit (2) from recurring leasing business > 90 locations in US, Canada and Mexico Diverse customer base (>25,000) c.76,000 modular space and storage fleet units; representing over 34m sq. ft. with a gross book value of US$1.2bn (3) c.1,300 sales, service and support personnel in US, Canada and Mexico 942862_1.wor NY008MZK WS Locations HQ (Baltimore) Key Williams Scotsman Differentiating Attributes “Ready to Work” Scalable & Differentiated Operating Platform Higher Visibility into Future Performance 1 2 3 Customers value our solutions; this continues to drive growth with highly accretive returns Proprietary management information systems and fleet management initiatives Long - lived assets coupled with 35 - month average lease durations (4) Diverse End Markets and Customer Base (5) Innovative Modular Space & Portable Storage Solutions 1 Top 10 8% Next 40 9% Remaining 25k Customers 83% Top 50 customers represent 17% of total revenue 6 1 Amounts from 2016 financials of Williams Scotsman, without giving effect to carve - out transaction. 2 Adjusted Gross Profit is a non - GAAP measure defined as Gross Profit excluding depreciation and amortization. See Appendix for a reconciliation to GAAP metric . 3 As of June 30, 2017. 4 Customer leases typically remain on rent more than 75% beyond their original minimum lease term, and our current lease portfolio as of Ju ne 30, 2017 has an average actual term of 35 months. 5 2016 revenue breakdown by customer.

Growth accelerating since 2015, driven by strong pricing, delivery volumes / units on rent and VAPS momentum 14% CAGR in Organic US Adj. EBITDA 1 Revenue (1) ( US$m ) Adj. EBITDA (1) ( US$m ) Note: 2015 and 2016 converted at actual rates. 2017 and 2018 at budgeted rates: 1.35 CAD/USD and 20 MXN/USD. VAPS defined as Value Added Products and Services. 1 Based on Williams Scotsman financials, without giving effect to estimated standalone public company costs or the carve - out transaction for 2015 and 2016; 2017 and 2018 projections based on Williams Scotsman financials, without giving effect to the carve - out. Adjusted EBITDA is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of contingent considerations, goodwill and other impairment ch arg es, restructuring costs and other non - recurring expenses. See Appendix for reconciliation to GAAP metric. 2 Other North America includes Canada, Mexico and Alaska. 7 US Other North America (2) ▪ US is contributing ~90% of Adjusted EBITDA and growing organically at 14% CAGR ▪ Growth driven by robust market demand, “Ready To Work” solutions, and pricing and capital management tools ▪ Growth has been achieved despite cash constrained operating environment ▪ Other North America segment offers upside as market recovers ▪ With improved access to capital, WS can accelerate organic growth and pursue highly accretive acquisitions 85 104 112 126 45 24 14 17 131 128 126 143 2015 2016 2017E 2018E 353 365 386 406 101 62 52 57 454 428 438 463 2015 2016 2017E 2018E

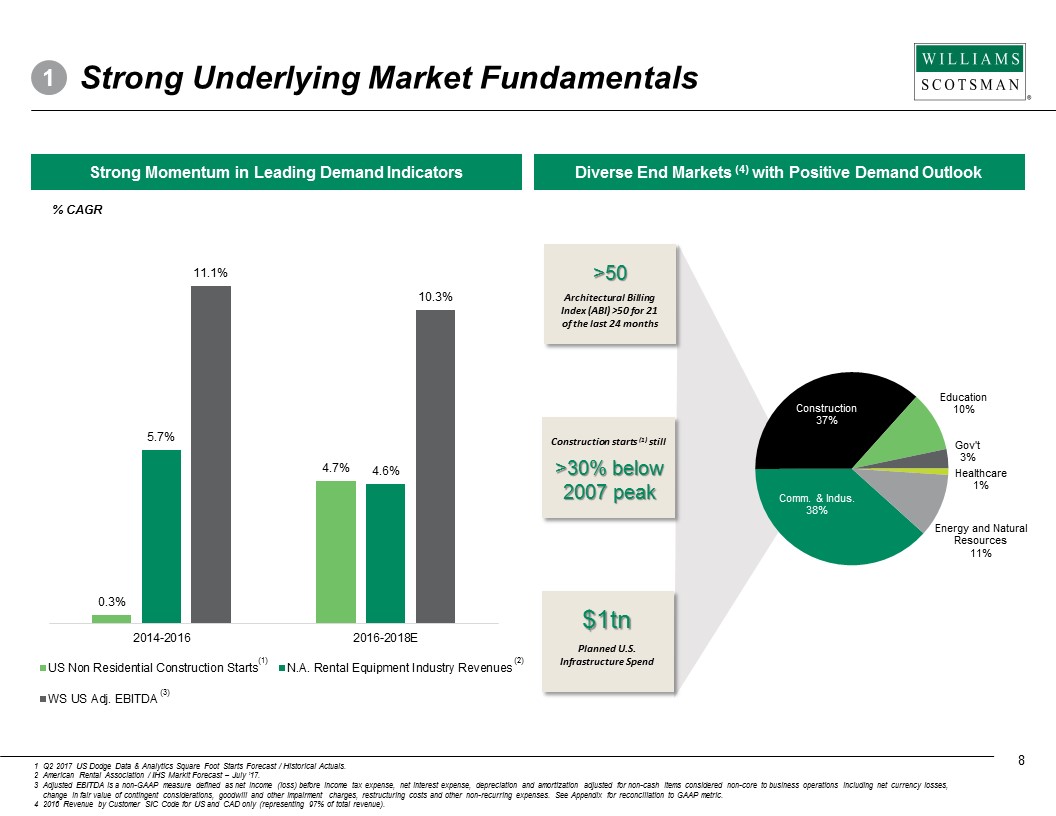

0.3% 4.7% 5.7% 4.6% 11.1% 10.3% 2014-2016 2016-2018E US Non Residential Construction Starts N.A. Rental Equipment Industry Revenues WS US Adj. EBITDA (1) (2) % CAGR (3) Comm. & Indus. 38% Construction 37% Education 10% Gov't 3% Healthcare 1% Energy and Natural Resources 11% $1tn Planned U.S. Infrastructure Spend Construction starts (1) still >30 % below 2007 peak >50 Architectural Billing Index (ABI) >50 for 21 of the last 24 months Strong Underlying Market Fundamentals 1 Strong Momentum in Leading Demand Indicators Diverse End Markets (4) with Positive Demand Outlook 1 Q2 2017 US Dodge Data & Analytics Square Foot Starts Forecast / Historical Actuals. 2 American Rental Association / IHS Markit Forecast – July ’17. 3 Adjusted EBITDA is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of contingent considerations, goodwill and other impairment charges, restructuring costs and other non - recu rring expenses. See Appendix for reconciliation to GAAP metric. 4 2016 Revenue by Customer SIC Code for US and CAD only (representing 97% of total revenue). 8

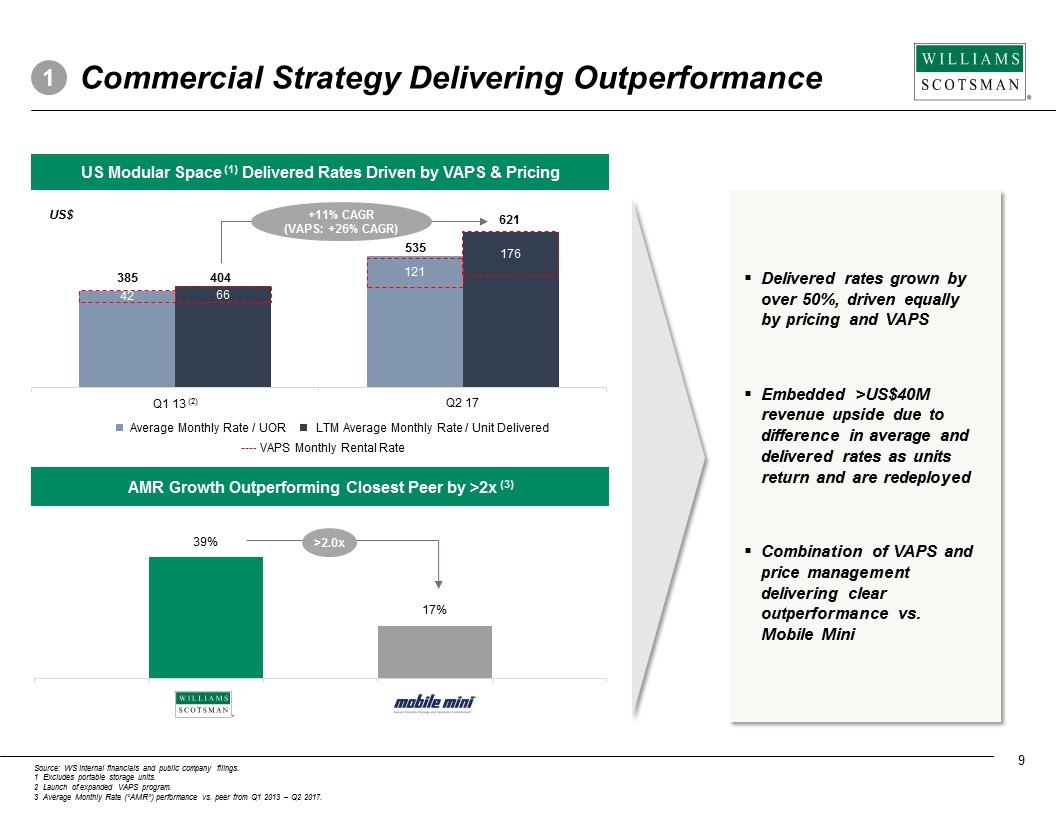

AMR Growth Outperforming Closest Peer by >2x (3) ▪ Delivered rates grown by over 50 %, driven equally by pricing and VAPS ▪ Embedded >US$40M revenue upside due to difference in average and delivered rates as units return and are redeployed ▪ Combination of VAPS and price management delivering clear outperformance vs. Mobile Mini Commercial Strategy Delivering Outperformance 1 US Modular Space (1) Delivered Rates Driven by VAPS & Pricing Source: WS internal financials and public company filings. 1 Excludes portable storage units. 2 L aunch of expanded VAPS program. 3 Average Monthly Rate (“AMR”) performance vs. peer from Q1 2013 – Q2 2017. 9 39% 17% Q1 13 Q1 17 >2.0x Average Monthly Rate / UOR LTM Average Monthly Rate / Unit Delivered VAPS Monthly Rental Rate 42 66 121 176 Q1 13 (2) Q2 17 385 404 535 621 +11% CAGR (VAPS: +26% CAGR) US$

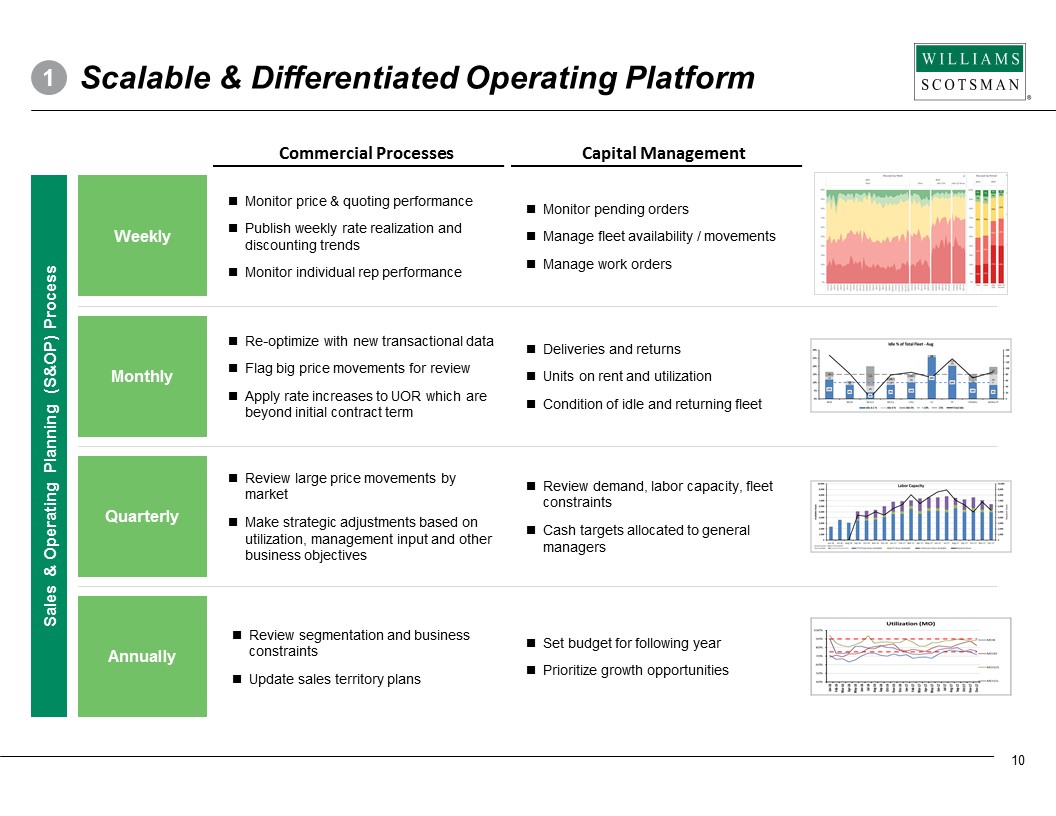

10 Sales & Operating Planning (S&OP) Process Monitor price & quoting performance Publish weekly rate realization and discounting trends Monitor individual rep performance Weekly Re - optimize with new transactional data Flag big price movements for review Apply rate increases to UOR which are beyond initial contract term Monthly Review large price movements by market Make strategic adjustments based on utilization, management input and other business objectives Quarterly Review segmentation and business constraints Update sales territory plans Annually Scalable & Differentiated Operating Platform 1 Monitor pending orders Manage fleet availability / movements Manage work orders Deliveries and returns Units on rent and utilization Condition of idle and returning fleet Review demand, labor capacity, fleet constraints Cash targets allocated to general managers Set budget for following year Prioritize growth opportunities Commercial Processes Capital Management

VAPS Growth Activate surplus rentable idle fleet Activate idle un - rentable fleet through refurbishment Tuck - in M&A or other used fleet purchases VAPS Drive 25% Improvement in Unit IRR Opportunity for Capital Efficient Growth by Returning to Normalized Utilization Rate Highly Accretive Opportunities to Expand Fleet 1 2 3 Purchase new fleet when investment returns support -$40,000 -$20,000 $0 $20,000 $40,000 $60,000 $80,000 $100,000 $120,000 - 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Compelling Specialty Rental Unit Economics 1 IRR > 20% over 20 year unit life, with VAPS penetration lifting IRR to ~25 % (1) Clear Priorities for Capital Allocation with a Focus on Highest Marginal ROI 11 1 Based on illustrative example of specific model type (60ft x 12ft mobile office). Cumulative Cash Flow with VAPS Cumulative Cash Flow with no VAPS Years Capital Investment Acquisition cost of ~$ 30K, incl. VAPS cost to equip unit of $2.4k Maintenance Mid - life refurbishment ~$ 9K Proceeds Realized residual values average 50% of original factory cost Rapid payback of 36 months

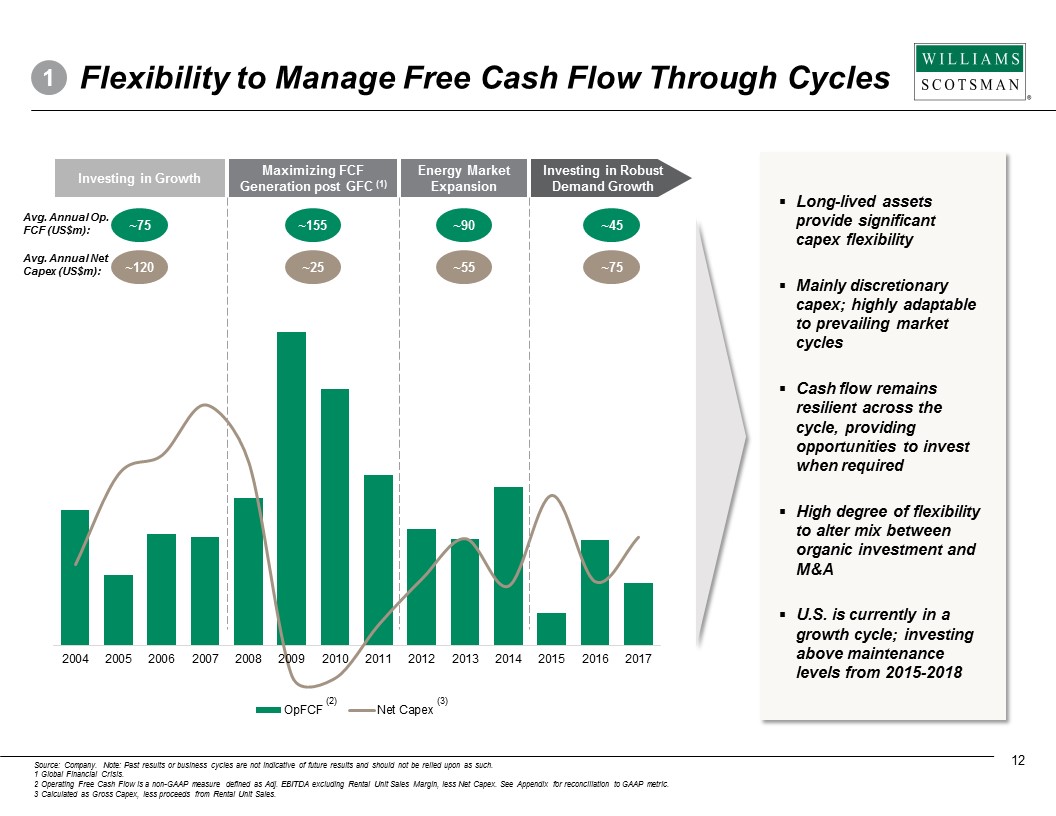

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 OpFCF Net Capex 12 ▪ Long - lived assets provide significant capex flexibility ▪ Mainly discretionary capex; highly adaptable to prevailing market cycles ▪ Cash flow remains resilient across the cycle, providing opportunities to invest when required ▪ High degree of flexibility to alter mix between organic investment and M&A ▪ U.S . is currently in a growth cycle; investing above maintenance levels from 2015 - 2018 (3) Source: Company. Note: Past results or business cycles are not indicative of future results and should not be relied upon as such. 1 Global Financial Crisis. 2 Operating Free Cash Flow is a non - GAAP measure defined as Adj. EBITDA excluding Rental Unit Sales Margin, less Net Capex. See Appendix for reconciliation to GAAP metric. 3 Calculated as Gross Capex, less proceeds from Rental Unit Sales . (2) Flexibility to Manage Free Cash Flow Through Cycles 1 Investing in Growth Maximizing FCF Generation post GFC (1) Energy Market Expansion Investing in Robust Demand Growth ~ 75 ~ 155 ~90 ~45 Avg. Annual Op. FCF (US$m): ~120 ~25 ~55 ~75 Avg. Annual Net Capex (US$m):

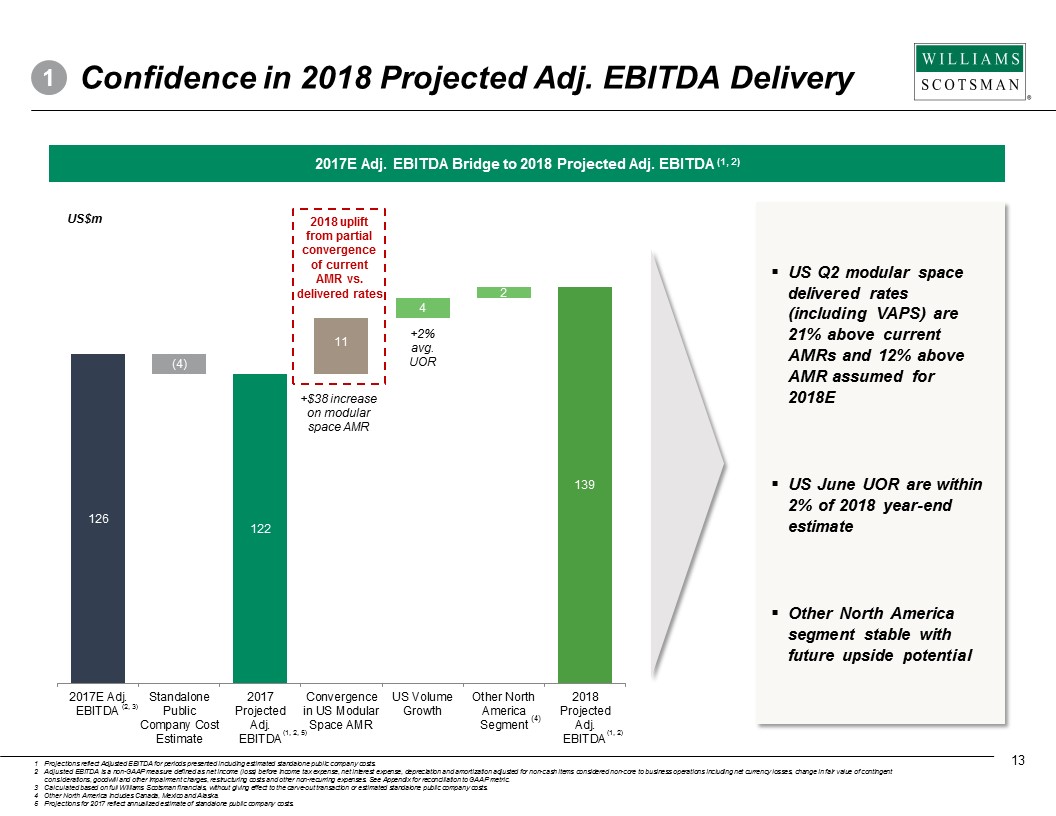

122 126 (4) 11 4 2 139 2017E Adj. EBITDA Standalone Public Company Cost Estimate 2017 Projected Adj. EBITDA Convergence in US Modular Space AMR US Volume Growth Other North America Segment 2018 Projected Adj. EBITDA US$m 2018 uplift from partial convergence of current AMR vs. d elivered rates + 2% avg. UOR +$ 38 increase on modular space AMR (4) (1, 2, 5) 2017E Adj. EBITDA Bridge to 2018 Projected Adj. EBITDA (1, 2) Confidence in 2018 Projected Adj. EBITDA Delivery 1 1 Projections reflect Adjusted EBITDA for periods presented including estimated standalone public company costs. 2 Adjusted EBITDA is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of co ntingent considerations, goodwill and other impairment charges, restructuring costs and other non - recurring expenses. See Appendix for reconciliation to GAAP metric . 3 Calculated based on full Williams Scotsman financials, without giving effect to the carve - out transaction or estimated standalon e public company costs. 4 Other North America includes Canada, Mexico and Alaska. 5 Projections for 2017 reflect annualized estimate of standalone public company costs. 13 ▪ US Q2 modular space delivered rates (including VAPS) are 21% above current AMRs and 12% above AMR assumed for 2018E ▪ US June UOR are within 2% of 2018 year - end estimate ▪ Other North America segment stable with future upside potential (2, 3) (1, 2)

Revenue Growth Levers are Highly Accretive to Margin Evolution Significant Projected Adj. EBITDA Margin Expansion Potential 1 ▪ Meaningful margin expansion as units are redeployed at current pricing; ~95% of AMR increases convert to EBITDA (5) ▪ >80% of VAPS revenue growth converts to EBITDA (5) ▪ >70% of revenue from UOR growth converts to EBITDA (5) ▪ M&A synergies highly accretive to margins given embedded operating leverage opportunity 29% 28% (1%) ~200bps ~150bps ~150bps ~33% ~300 - 500bps 2017E Adj. EBITDA Margin Standalone Public Company Cost Estimate 2017 Projected Adj. EBITDA Margin Average Monthly Rental Rate Increases VAPS Rate and Penetration Growth Utilization Gains Potential Projected Adj. EBITDA Margin M&A Opportunity 14 (1, 2, 4) (1 , 2, 4) (2, 3) 1 Projections reflect Adjusted EBITDA for periods presented including estimated standalone public company costs. 2 Adjusted EBITDA Margin is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of contingent considerations, goodwill and other impairment charges, restructuring costs and other non - recurring expenses, divided by Revenue. See Appendix for reconciliation to GAAP metric . 3 Calculated based on full Williams Scotsman financials, without giving effect to the carve - out transaction or estimated standalon e public company costs. 4 Projections for 2017 reflect annualized estimate of standalone public company costs. 5 EBITDA is a non - GAAP financial measure defined as net income (loss) before income tax expense (benefit), interest expense, depreciation and amorti zat ion. See Appendix for reconciliation to GAAP metric.

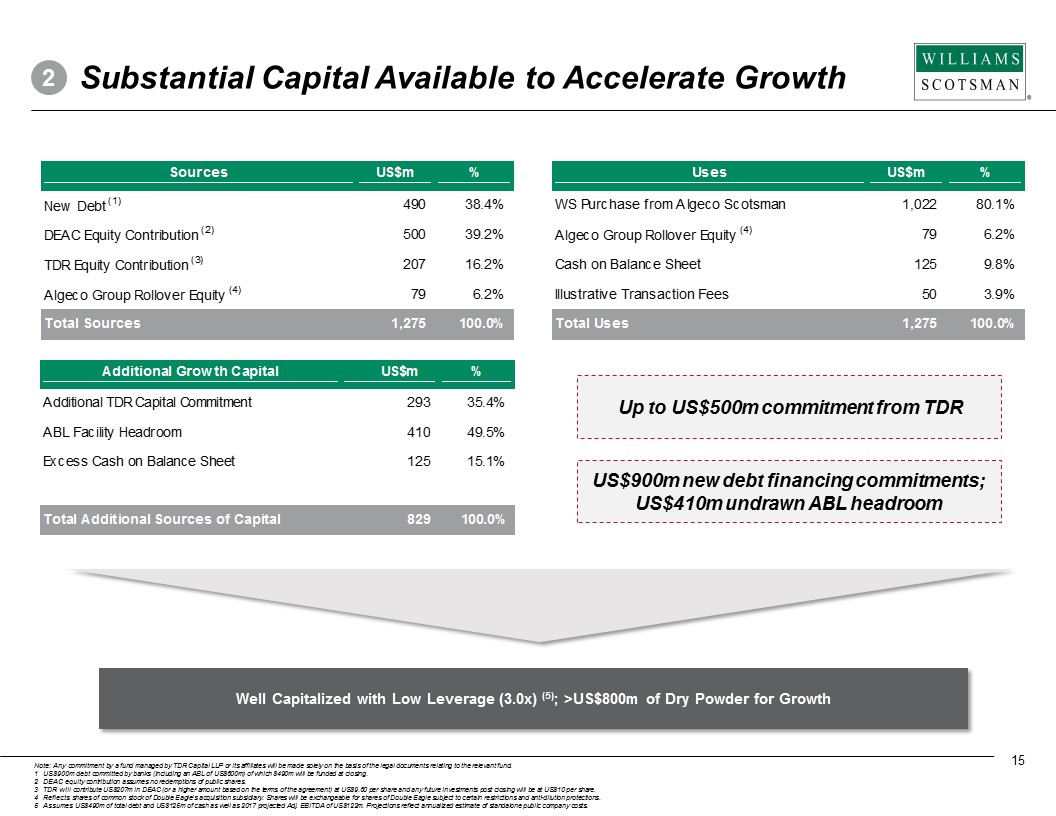

Uses US$m % WS Purchase from Algeco Scotsman 1,022 80.1% Algeco Group Rollover Equity (4) 79 6.2% Cash on Balance Sheet 125 9.8% Illustrative Transaction Fees 50 3.9% Total Uses 1,275 100.0% Well Capitalized with Low Leverage ( 3.0x) (5) ; >US$800m of Dry Powder for Growth Sources US$m % New Debt (1) 490 38.4% DEAC Equity Contribution (2) 500 39.2% TDR Equity Contribution (3) 207 16.2% Algeco Group Rollover Equity (4) 79 6.2% Total Sources 1,275 100.0% Additional Growth Capital US$m % Additional TDR Capital Commitment 293 35.4% ABL Facility Headroom 410 49.5% Excess Cash on Balance Sheet 125 15.1% Total Additional Sources of Capital 829 100.0% Up to US$500m commitment from TDR Substantial Capital Available to Accelerate Growth 2 15 Note: Any commitment by a fund managed by TDR Capital LLP or its affiliates will be made solely on the basis of the legal documents relating to the relevant fund . 1 US$900m debt committed by banks (including an ABL of US$600m ) of which $ 490m will be funded at closing. 2 DEAC equity contribution assumes no redemptions of public shares . 3 TDR will contribute US$207m in DEAC (or a higher amount based on the terms of the agreement) at US$9.60 per share and any future investments post closing will be at US$10 per share. 4 Reflects shares of common stock of Double Eagle’s acquisition subsidiary. Shares will be exchangeable for shares of Double Ea gle subject to certain restrictions and anti - dilution protections. 5 Assumes US$490m of total debt and US$125m of cash as well as 2017 projected Adj. EBITDA of US$122m. Projections reflect annualized estimate of standalone public company costs. US$900m new debt financing commitments; US$410m undrawn ABL headroom

EBITDA Scale Commentary National ▪ WS announced combination with Modspace in 2016 (2) ▪ Modspace subsequently filed for and has emerged from bankruptcy Regional ▪ Next 8 regional players represent ~33% of U.S. market ▪ Multiple private equity and family owned companies Local ▪ Remaining ~33% of U.S. market highly diversified ▪ WS actively tracking 60 local players averaging <1,000 UOR ▪ Typically privately owned Total Addressable Market of over $5bn + ( 1) Market Primed for Consolidation 3 Fragmented Markets Present Multiple Actionable M&A Opportunities WS Platform Capable of Integrating Targets of all Sizes Source: Dodge PIP Data, NA financial data, internal analysis for 2017 budget process. 1 Includes modular office and storage markets. 2 Acquisition agreement was terminated prior to completion. 16 Top 2 Players: c.33% of market Next 8 Players: c.33% of market Remainder: Highly Diversified

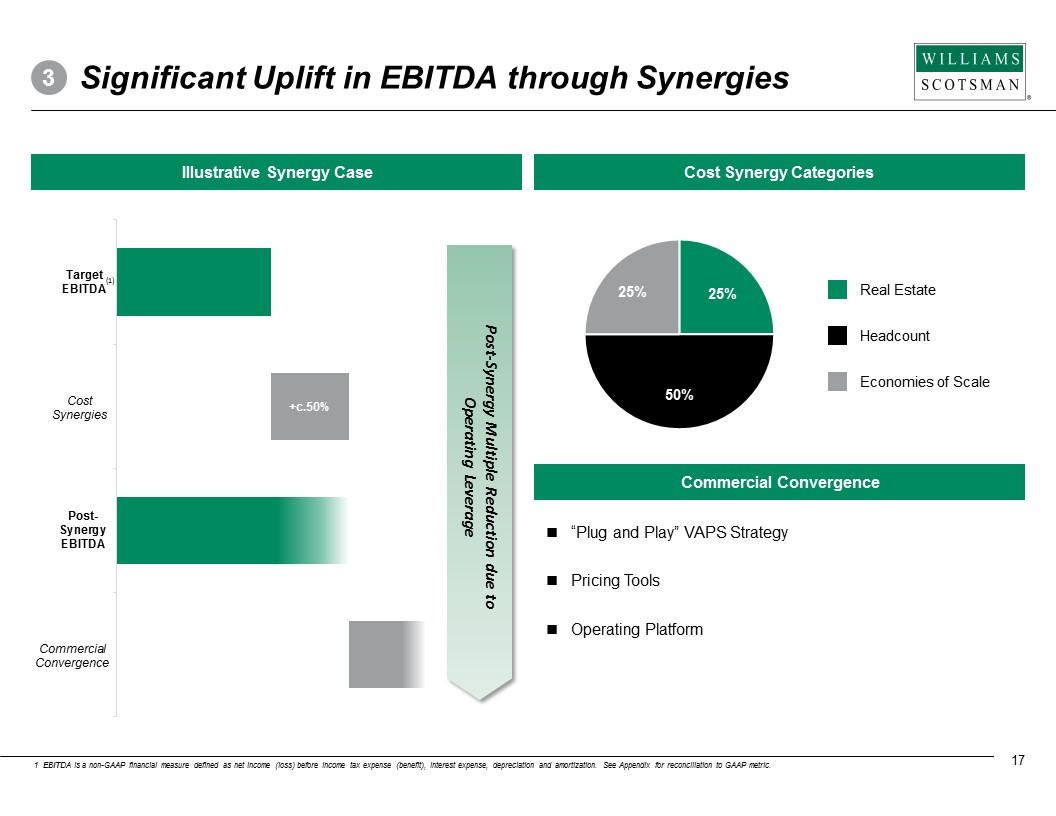

Significant Uplift in EBITDA through Synergies 3 “Plug and Play” VAPS Strategy Pricing Tools Operating Platform Cost Synergy Categories Commercial Convergence 17 Cost Synergies Commercial Convergence Illustrative Synergy Case 25% 50% 25 % Real Estate Headcount Economies of Scale Post - Synergy Multiple Reduction due to Operating Leverage Post- Synergy EBITDA Target EBITDA +c.50% 1 EBITDA is a non - GAAP financial measure defined as net income (loss) before income tax expense (benefit), interest expense, depreciation and amorti zat ion. See Appendix for reconciliation to GAAP metric. (1)

70 90 110 130 150 170 190 Sep-05 Dec-05 Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 +75% +46% Stock price performance prior to Algeco Acquisition Outperform vs S&P 500 Indexed to 100 +27% +46% x2 Revenue Uplift (1) +25% Adjusted EBITDA Uplift ( 1 )( 2 ) +47% Share Price Performance Before Take Private +75% $2.2bn acquisition by Algeco announced 21 Months as a listed company Successful Previous Public Company Track Record 4 18 Source: FactSet. Note: r eflects period from September 2005 to June 2007 without giving effect to changes in company business, strategy, management, general economic or market conditions or other factors due to the passage of time. Past performance is not indicative of future results and should not be relied upon as such . 1 Financial Performance for Period Q3 2005 – Q2 2007. 2 Adjusted EBITDA is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of contingent considerations, goodwill and other impairment charges, restructuring cost s a nd other non - recurring expenses . See Appendix for reconciliation to GAAP metric.

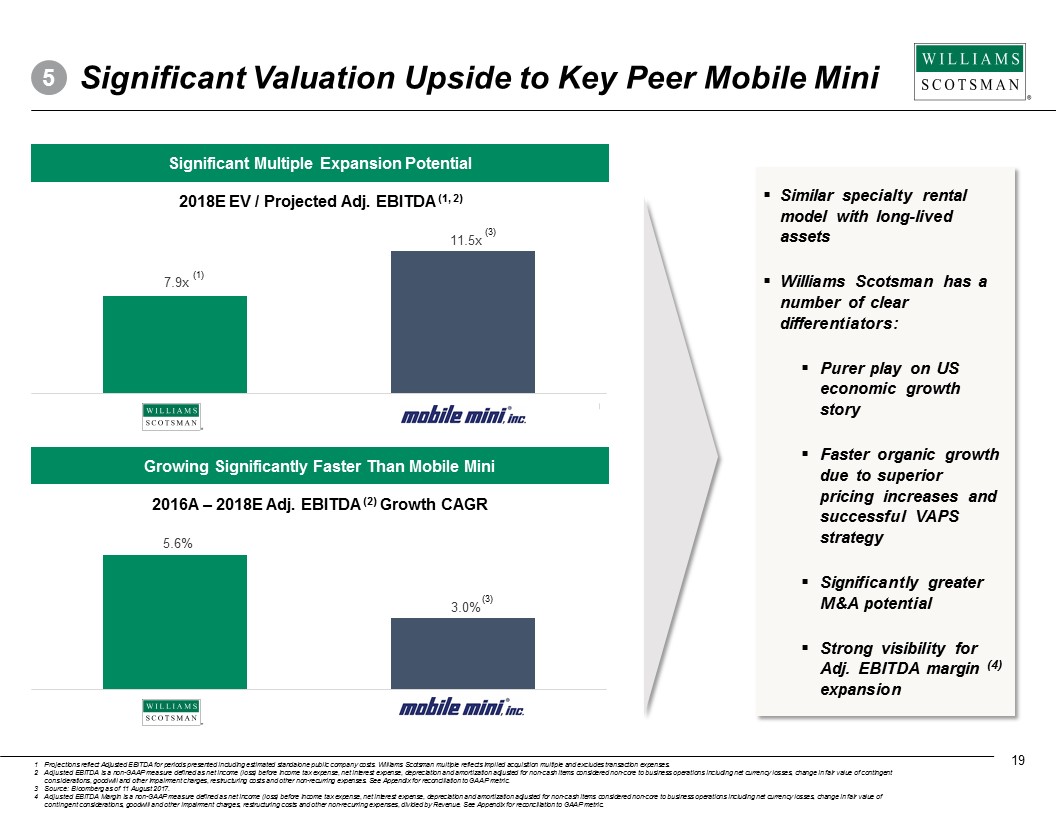

Growing Significantly Faster Than Mobile Mini Significant Valuation Upside to Key Peer Mobile Mini 5 Significant Multiple Expansion Potential 7.9x 11.5x 5.6% 3.0% ( 1) 19 ▪ Similar specialty rental model with long - lived assets ▪ Williams Scotsman has a number of clear differentiators: ▪ Purer play on US economic growth story ▪ Faster organic growth due to superior pricing increases and successful VAPS strategy ▪ Significantly greater M&A potential ▪ Strong visibility for Adj. EBITDA margin (4) expansion 2016A – 2018E Adj. EBITDA (2) Growth CAGR 2018E EV / Projected Adj. EBITDA (1, 2) (3) (3) 1 Projections reflect Adjusted EBITDA for periods presented including estimated standalone public company costs . Williams Scotsman multiple reflects implied acquisition multiple and excludes transaction expenses. 2 Adjusted EBITDA is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of co ntingent considerations, goodwill and other impairment charges, restructuring costs and other non - recurring expenses. See Appendix for reconciliation to GAAP metric . 3 Source: Bloomberg as of 11 August 2017. 4 Adjusted EBITDA Margin is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of contingent considerations, goodwill and other impairment charges, restructuring costs and other non - recurring expenses, divided by Revenue. See Appendix for reconciliation to GAAP metric.

Contracted Revenue with Meaningful Rate Upside x 35 Months Average Duration of Contracts (1) Attractive Returns and Rapid Payback Period x >20% IRR over 20 yr unit life Margin Uplift from Market Leadership and Commercial Excellence x 30% 2018 Projected Adj. EBITDA Margin (3) Robust Cash Generation given High Capex Flexibility x 36 Months Payback period incl. VAPS Strong Momentum in Core US Business x 14% 2015 - 18 Adj. EBITDA (2) CAGR Attractive Model and Compelling Growth Opportunity 20 1 Customer leases typically remain on rent more than 75% beyond their original minimum lease term, and our current lease portfolio as of Ju ne 30, 2017 has an average actual term of 35 months . 2 Adjusted EBITDA is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of contingent considerations, goodwill and other impairment charges, restructuring costs and other non - recurring expenses . See Appendix for reconciliation to GAAP metric. 3 Projections reflect Adjusted EBITDA for periods presented including estimated standalone public company costs. Adjusted EBITDA Margin is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of contingent consider ations, goodwill and other impairment charges, restructuring costs and other non - recurring expenses, divided by Revenue. See App endix for reconciliation to GAAP metric .

Additional Operating and Financial Information

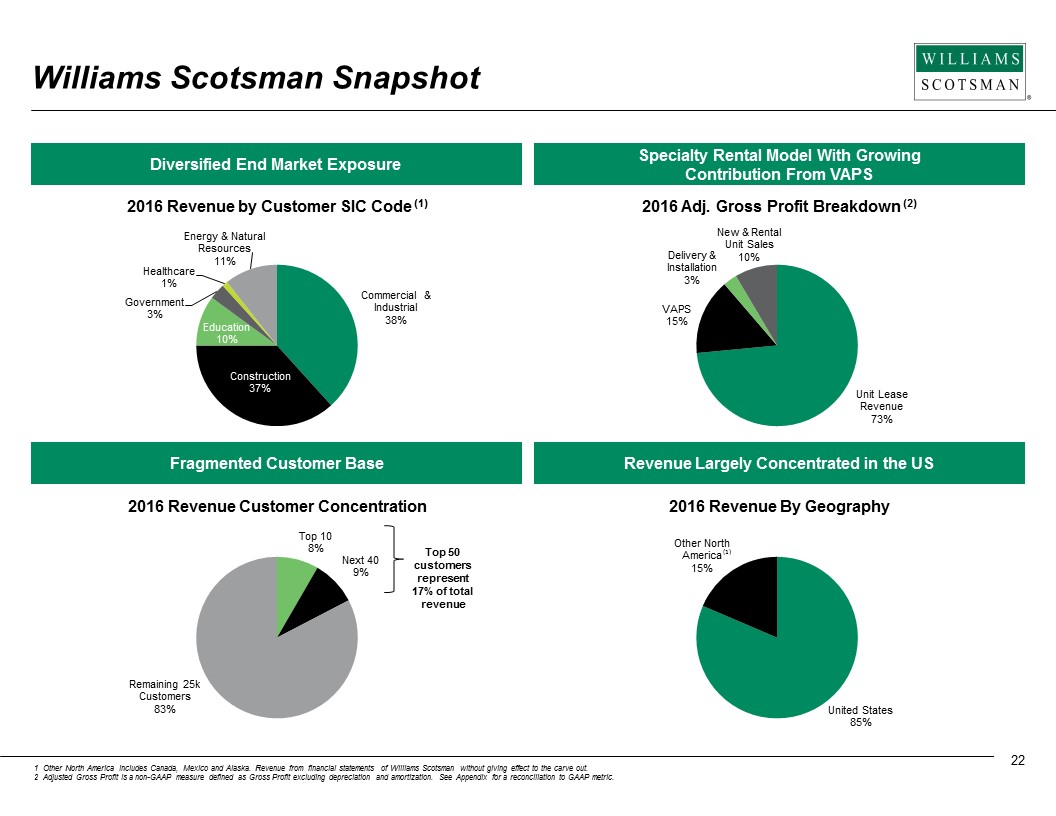

22 Williams Scotsman Snapshot Diversified End Market Exposure Specialty Rental Model With Growing Contribution From VAPS Fragmented Customer Base Revenue Largely Concentrated in the US 2016 Revenue by Customer SIC Code (1) 2016 Adj. Gross Profit Breakdown (2) 2016 Revenue Customer Concentration 2016 Revenue By Geography Commercial & Industrial 38% Construction 37% Education 10% Government 3% Healthcare 1% Energy & Natural Resources 11% Unit Lease Revenue 73% VAPS 15% Delivery & Installation 3% New & Rental Unit Sales 10% Top 10 8% Next 40 9% Remaining 25k Customers 83% United States 85% Other North America 15% Top 50 customers represent 17% of total revenue 1 Other North America includes Canada, Mexico and Alaska. Revenue from financial statements of Williams Scotsman without giving ef fect to the carve out. 2 Adjusted Gross Profit is a non - GAAP measure defined as Gross Profit excluding depreciation and amortization. See Appendix for a reconciliation to GAAP metric. (1)

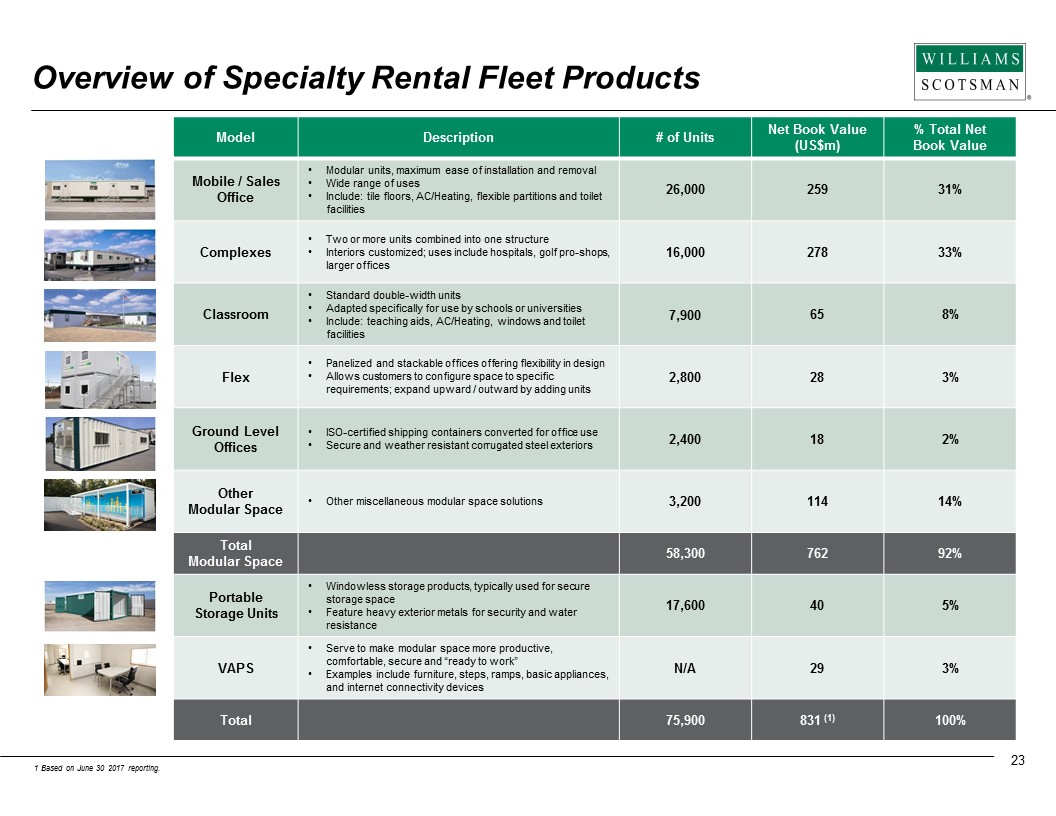

Overview of Specialty Rental Fleet Products Model Description # of Units Net Book Value ( US$m ) % Total Net Book Value Mobile / Sales Office • Modular units, maximum ease of installation and removal • Wide range of uses • Include: tile floors, AC/Heating, flexible partitions and toilet facilities 26,000 259 31% Complexes • Two or more units combined into one structure • Interiors customized; uses include hospitals, golf pro - shops, larger offices 16,000 278 33% Classroom • Standard double - width units • Adapted specifically for use by schools or universities • Include: teaching aids, AC/Heating, windows and toilet facilities 7,900 65 8% Flex • Panelized and stackable offices offering flexibility in design • Allows customers to configure space to specific requirements; expand upward / outward by adding units 2,800 28 3% Ground Level Offices • ISO - certified shipping containers converted for office use • Secure and weather resistant corrugated steel exteriors 2,400 18 2% Other Modular Space • Other miscellaneous modular space solutions 3,200 114 14% Total Modular Space 58,300 762 92% Portable Storage Units • Windowless storage products, typically used for secure storage space • Feature heavy exterior metals for security and water resistance 17,600 40 5% VAPS • Serve to make modular space more productive, comfortable, secure and “ready to work” • Examples include furniture, steps, ramps, basic appliances, and internet connectivity devices N/A 29 3% Total 75,900 831 (1) 100% 1 Based on June 30 2017 reporting. 23

Strong Momentum in Leading Revenue Indicators 1H 2016 1H 2015 Source: Company. Note: Delivery and Net UOR Growth metrics refer to Modular Space only. 1 UOR – Units on Rent. Note: Other North America includes Canada, Mexico and Alaska. US Other North America ▪ US leading revenue indicators are at their strongest levels since 2005 ▪ Other North America indicators denote stabilization of performance; UOR (1) growth of 294 units through June 24 Deliveries Net UOR (1) Growth 1H 2017 11,626 +11% 10,518 10,938 935 754 - 112 +9% 2,497 2,293 2,752 - 417 +683 294 - 389 +1,047

Modular Space Units on Rent and Utilization Rates 25 ▪ Q2 US modular space UOR at highest level in the last three years, highlighting robust demand outlook ▪ Utilization rates increasing but with significant headroom for further growth vs. historical levels ▪ For Other North America segment, Q2 17 was the first quarter to show a sequential Q - o - Q increase in the number of modular space UOR since 2014 Source: Company. Note : Other North America includes Canada, Mexico and Alaska. Modular Space – US Modular Space – Other North America 34,356 34,863 35,568 35,819 35,245 35,205 35,552 35,602 35,074 35,780 Q1 15 Q1 16 Q1 17 Q2 15 Q2 16 Q2 17 Q3 15 Q3 16 Q4 15 Q4 16 70.8% 72.3% 68.7% 71.5% 73.8% 71.7% 72.7% 71.8% 73.1% 7,013 6,846 6,694 6,342 5,844 5,641 5,287 4,972 4,813 4,901 Q1 15 Q1 16 Q1 17 Q2 15 Q2 16 Q2 17 Q3 15 Q3 16 Q4 15 Q4 16 69.5% 58.5% 48.9% 67.8% 56.9% 50.0% 66.4% 53.5% 63.3% 50.4% 67.0% % Utilization (%) Average # Units on Rent Average # Units on Rent

Cost / Profitability Overview 26 ▪ Gross margin in US Leasing and Services positively impacted by strong pricing environment, including VAPS ▪ Gross margin in Other North America seen as stabilizing at a similar level to that of the US ▪ Increase in SG&A as a % of revenue driven by revenue decline in Other North America, partly offset by cost reduction and embedded operating leverage potential SG&A (3) Adj. Gross Profit % (1) by Segment 70% 71% 75% 24% 23% 39% 89% 84% 84% 45% 23% 27% 0% 20% 40% 60% 80% 100% 2014A 2015A 2016A US Leasing & Services US Sales Other North America Leasing & Services Other North America Sales Source: Company. 1 Adjusted Gross Profit is a non - GAAP measure defined as Gross Profit excluding depreciation and amortization. See Appendix for a reconciliation to GAAP metric . 2 Other North America includes Canada, Mexico and Alaska . 3 S elling , general, and administrative (“SG&A”) expense includes all costs associated with selling efforts, including marketing costs and salaries and benefits, including commissions of sales personnel. It also includes overhead costs, such as salaries of administrative and corporate personnel and the leasing of facilities. The company anticipates standalone public company costs going forward of ~US$4m per year, which would increase SG&A as a percentage of revenue by 80 - 100bps . US$m % % Revenue 54% 54% 56% 23% 23% 39% 80% 76% 74% 25% 22% 27% 2014A 2015A 2016A (2) (2) 108 112 110 2014A 2015A 2016A 21.3% 24.6% 25.7%

$35 – $40M Net Maint. Capex 11 47 35 44 39 53 16 28 9 15 14 16 (25) (16) (22) (18) 34 99 42 71 2014 2015 2016 2017E Refurbishments New Fleet VAPS Proceeds from Rental Unit Sales Net Fleet Capex (US$m) 27 Net Fleet Capex (1) Analysis Historical Net Capital Expenditure Evolution ▪ Priority given to VAPS capex given strong growth potential, superior returns and incremental margin delivery ▪ Refurbishment is a key part of fleet management strategy and unique to modular space rental ▪ Highly capital efficient source of growth by extending useful asset lives ▪ Fleet investment above maintenance investment levels driving US modular space UOR growth in 2015 and 2017 Source: Company. Note: Excludes non - fleet capex. 1 Calculated as Gross Capex excluding non - fleet capex, less proceeds from Rental Unit Sales. 34,266 35,269 35,069 35,839 US Modular Space UOR: (1)

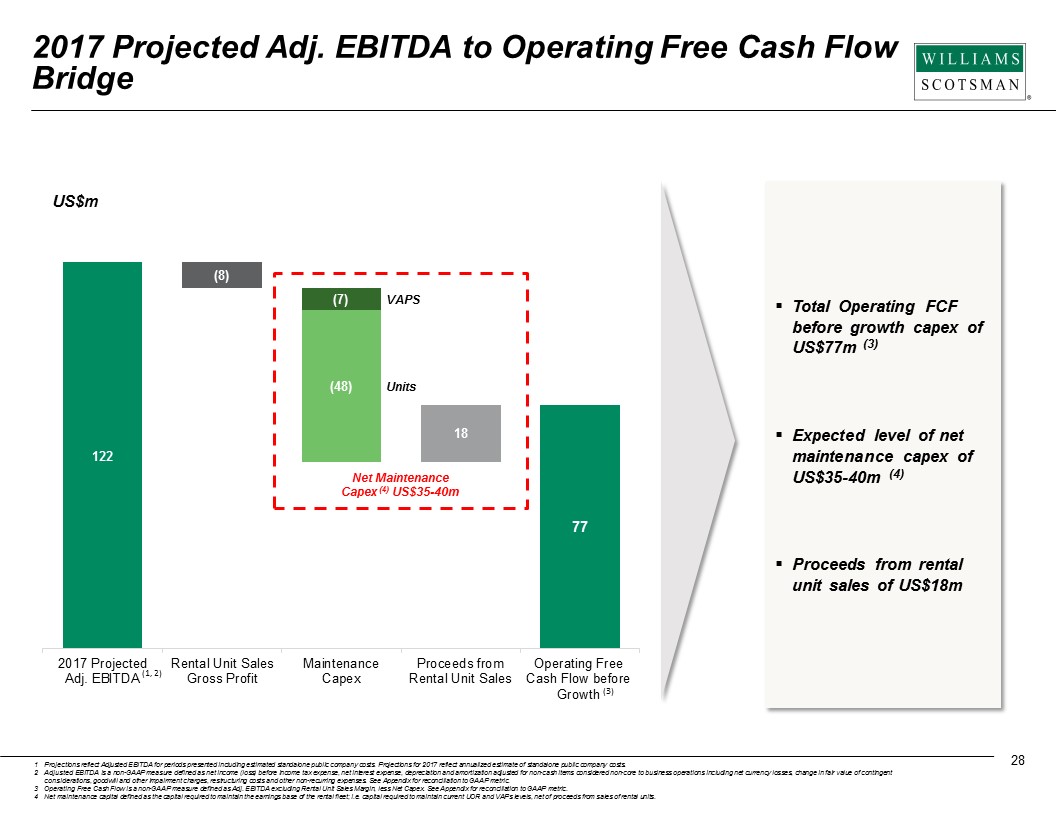

2017 Projected Adj. EBITDA to Operating Free Cash Flow Bridge 28 US$m ▪ Total Operating FCF before growth capex of US$77m (3) ▪ Expected level of net maintenance capex of US$35 - 40m (4) ▪ Proceeds from rental unit sales of US$18m 77 122 (8) ( 48 ) 18 ( 7 ) 2017 Projected Adj. EBITDA Rental Unit Sales Gross Profit Maintenance Capex Proceeds from Rental Unit Sales Operating Free Cash Flow before Growth Net Maintenance Capex (4) US$35 - 40m (3) VAPS Units (1, 2) 1 Projections reflect Adjusted EBITDA for periods presented including estimated standalone public company costs . Projections for 2017 reflect annualized estimate of standalone public company costs. 2 Adjusted EBITDA is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of co ntingent considerations, goodwill and other impairment charges, restructuring costs and other non - recurring expenses. See Appendix for reconciliation to GAAP metric . 3 Operating Free Cash Flow is a non - GAAP measure defined as Adj. EBITDA excluding Rental Unit Sales Margin, less Net Capex. See Appendix for reconciliation to GAAP me tri c. 4 Net maintenance capital defined as the capital required to maintain the earnings base of the rental fleet; i.e. capital required to maintain current UOR and VAPs levels, net of proceeds from sales of rental units.

Summary P&L, Balance Sheet & Cash Flow Items 29 Key Profit & Loss Items (US$m) (1) 2014 2015 2016 1H 2016 1H 2017 Leasing and Services Modular Leasing 309 301 284 143 142 Modular Delivery and Installation 83 83 82 40 42 Sales New Units 88 54 39 19 15 Rental Units 25 16 22 11 11 Total Revenues 505 454 428 213 210 Gross Profit 200 164 169 88 78 Adjusted EBITDA (2) 159 131 128 67 56 D&A (74) (86) (76) (38) (37) Adjusted Operating Income (3) 85 45 52 29 18 Key Cash Flow & Balance Sheet Items (US$m) Capex for Rental Fleet 59 114 64 28 50 Net Book Value (4) 840 833 815 826 831 1 Based on financial statements of Williams Scotsman, without giving effect to the carve - out. 2 Adjusted EBITDA is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of contingent considerations, goodwill and other impairment charges, restructuring cost s a nd other non - recurring expenses . See Appendix for reconciliation to GAAP metric. 3 Adjusted Operating Income is a non - GAAP measure defined as Adjusted EBITDA less depreciation and amortization . See Appendix for reconciliation to GAAP metric. 4 Reflects Net Rental Equipment. Following the carve - out from Algeco Scotsman, WS will retain approximately $500m of tax assets with which to offset future US cash taxes. Assets are subject to Section 382 limitations but are expected to result in no material U.S. Federal income cash taxes in the mid - term

Summary P&L & Cash Flow Items: Modular – US 30 Key Profit & Loss Items (US$m) (1) 2014 2015 2016 1H 2016 1H 2017 Leasing and Services Modular Leasing 211 225 238 117 126 Modular Delivery and Installation 70 72 74 36 38 Sales New Units 59 43 35 17 13 Rental Units 19 12 18 9 9 Total Revenues 358 353 365 180 186 Gross Profit 115 108 139 70 70 Adjusted EBITDA (2) 84 85 104 52 50 D&A (59) (71) (63) (31) (31) Adjusted Operating Income (3) 25 14 41 21 19 Key Cash Flow Items (US$m) Capex for Rental Fleet 22 98 60 26 48 1 Based on financial statements of Williams Scotsman, without giving effect to the carve - out . 2 Adjusted EBITDA is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of contingent considerations, goodwill and other impairment charges, restructuring cost s a nd other non - recurring expenses. See Appendix for reconciliation to GAAP metric. 3 Adjusted Operating Income is a non - GAAP measure defined as Adjusted EBITDA less depreciation and amortization. See Appendix for reconciliation to GAAP metric.

Summary P&L & Cash Flow Items: Modular – Other North America 31 Key Profit & Loss Items (US$m) (1) 2014 2015 2016 1H 2016 1H 2017 Leasing and Services Modular Leasing 98 76 46 26 16 Modular Delivery and Installation 13 11 8 4 4 Sales New Units 29 11 4 2 2 Rental Units 6 3 4 2 2 Total Revenues 147 101 62 34 24 Gross Profit 85 56 30 18 8 Adjusted EBITDA (2) 75 45 24 15 6 D&A (15) (14) (13) (7) (6) Adjusted Operating Income (3) 60 31 11 8 (1) Key Cash Flow Items (US$m) Capex for Rental Fleet 38 16 4 2 2 1 Based on financial statements of Williams Scotsman, without giving effect to the carve - out . 2 Adjusted EBITDA is a non - GAAP measure defined as net income (loss) before income tax expense, net interest expense, depreciation and amortization adjusted for non - cash items considered non - core to business operations including net currency losses, change in fair value of contingent considerations, goodwill and other impairment charges, restructuring cost s a nd other non - recurring expenses. See Appendix for reconciliation to GAAP metric. 3 Adjusted Operating Income is a non - GAAP measure defined as Adjusted EBITDA less depreciation and amortization. See Appendix for reconciliation to GAAP metric.

Appendix: Reconciliation of Non - GAAP Measures 32 2014 A 2015 A 2016 A 2017E 2018E US$m Modular - US Modular - Other North America Total WS Modular - US Modular - Other North America Total WS Modular - US Modular - Other North America Total WS Modular - US Modular - Other North America Total WS Modular - US Modular - Other North America Total WS Non-GAAP Measures Reconciliation Gross profit (loss) 115 85 200 108 56 164 139 30 169 151 18 169 161 22 183 Depreciation of rental equipment 53 14 67 65 13 78 57 12 69 57 12 69 62 12 74 Adjusted Gross Profit 168 98 267 173 69 242 196 42 238 208 29 238 224 33 257 Selling, general and administrative expense 84 24 108 88 24 112 92 18 110 96 16 112 97 17 114 Depreciation and amortization 59 15 74 71 14 86 63 13 76 63 12 75 68 13 80 Adjusted Operating Income 25 60 85 14 31 45 41 11 52 49 1 51 59 4 63 Depreciation and amortization 59 15 74 71 14 86 63 13 76 63 12 75 68 13 80 EBITDA 84 75 159 85 45 130 104 24 128 112 14 126 126 17 143 Adjustments: Non-recurring Professional Fees 0 (0) (0) 0 0 1 0 0 0 0 0 0 0 0 0 Other (0) 0 0 (0) 0 0 0 0 0 0 0 0 0 0 0 Adjusted EBITDA 84 75 159 85 45 131 104 24 128 112 14 126 126 17 143 Gross Profit on Sale of Rental Units (6) (2) (8) (4) (1) (5) (10) (1) (11) (7) (1) (8) (5) (1) (6) Total Capex (26) (39) (65) (103) (17) (120) (62) (4) (66) (89) (4) (93) (81) (4) (85) Proceeds from Rental Unit Sales 19 6 25 12 3 16 18 4 22 15 4 18 13 3 16 Net Capex (8) (33) (41) (90) (14) (104) (44) 0 (44) (74) (0) (75) (68) (1) (69) Operating Free Cash Flow (OpFCF) 70 40 110 (9) 31 22 49 24 73 31 12 43 54 15 68 Adjusted EBITDA (A) 84 75 159 85 45 131 104 24 128 112 14 126 126 17 143 Total Revenue (B) 358 147 505 353 101 454 365 62 428 386 52 438 406 57 463 Adjusted EBITDA Margin % (=A/B) 23% 51% 31% 24% 45% 29% 28% 39% 30% 29% 26% 29% 31% 29% 31% Projected Items Adjusted EBITDA 84 75 159 85 45 131 104 24 128 112 14 126 126 17 143 Standalone public company costs 4 - 4 4 - 4 Projected Adj EBITDA (C) 108 14 122 122 17 139 Projected Adjusted EBITDA Margin % (=C/B) 28% 26% 28% 30% 29% 30%

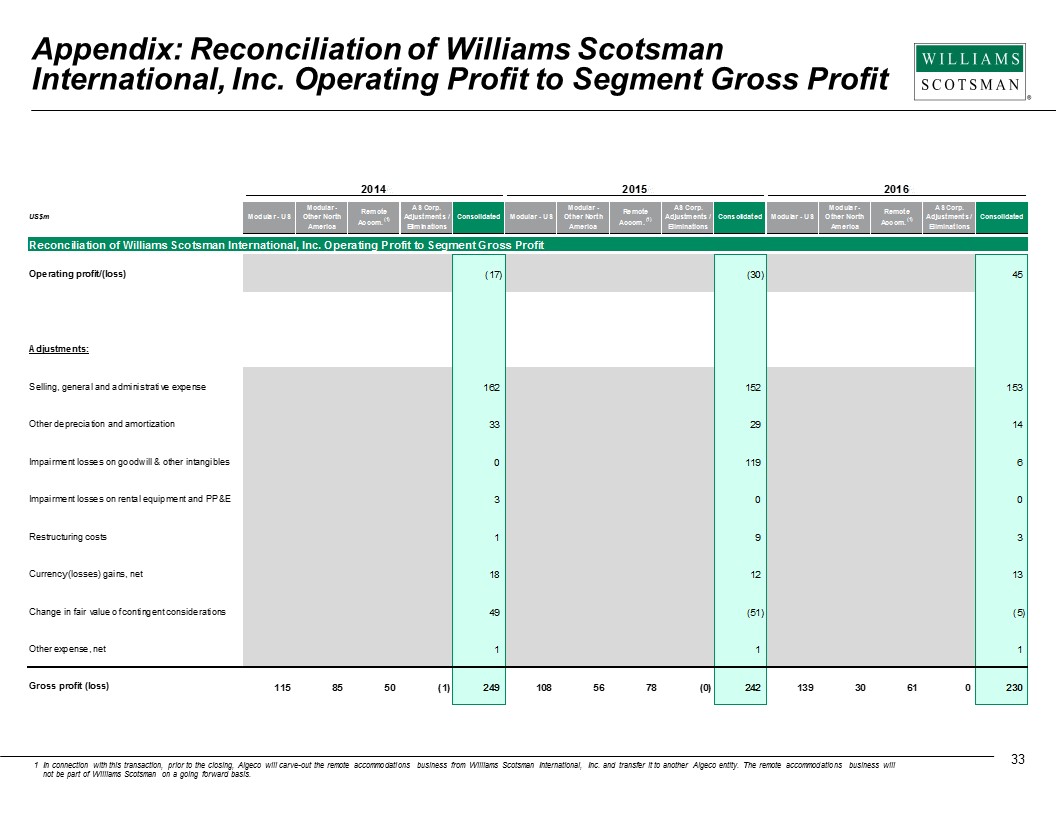

Appendix : Reconciliation of Williams Scotsman International, Inc. Operating Profit to Segment Gross Profit 33 1 In connection with this transaction, prior to the closing, Algeco will carve - out the remote accommodations business from Williams Scotsman International, Inc. and transfer it to another Algeco entity. The remote accommodations business will not be part of Williams Scotsman on a going forward basis. 2014 A 2015 A 2016 A US$m Modular - US Modular - Other North America Remote Accom. (1) AS Corp. Adjustments / Eliminations Consolidated Modular - US Modular - Other North America Remote Accom. (1) AS Corp. Adjustments / Eliminations Consolidated Modular - US Modular - Other North America Remote Accom. (1) AS Corp. Adjustments / Eliminations Consolidated Reconciliation of Williams Scotsman International, Inc. Operating Profit to Segment Gross Profit Operating profit/(loss) (17) (30) 45 Adjustments: Selling, general and administrative expense 162 152 153 Other depreciation and amortization 33 29 14 Impairment losses on goodwill & other intangibles 0 119 6 Impairment losses on rental equipment and PP&E 3 0 0 Restructuring costs 1 9 3 Currency (losses) gains, net 18 12 13 Change in fair value of contingent considerations 49 (51) (5) Other expense, net 1 1 1 Gross profit (loss) 115 85 50 (1) 249 108 56 78 (0) 242 139 30 61 0 230