Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-23155

Ivy NextShares

(Exact name of registrant as specified in charter)

6300 Lamar Avenue, Overland Park, Kansas 66202

(Address of principal executive offices) (Zip code)

Jennifer K. Dulski

6300 Lamar Avenue

Overland Park, Kansas 66202

(Name and address of agent for service)

Registrant’s telephone number, including area code: (913)236-2000

Date of fiscal year end: June 30

Date of reporting period: June 30, 2019

Table of Contents

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

Table of Contents

|

Annual Report

JUNE 30, 2019 |

| Ticker | ||||

IVY NEXTSHARES | ||||

| Ivy Focused Energy NextShares | IVENC | |||

| Ivy Focused Growth NextShares | IVFGC | |||

| Ivy Focused Value NextShares | IVFVC | |||

| Listing Exchange: The NASDAQ Stock Market LLC |

| |||

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission (SEC), paper copies of the Funds’ Annual and Semiannual Shareholder Reports no longer will be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Ivy Investments website (www.ivyinvestments.com), and you will be notified by mail each time a report is posted, and provided with a website link to access the report.

If you have already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically anytime by contacting your financial intermediary (e.g., a broker-dealer or bank) or, if you are a direct investor, by calling1-888-923-3355 or by enrolling at www.ivyinvestments.com.

You may elect to receive all future reports in paper format free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you may call1-888-923-3355 to let the Funds know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper format will apply to all funds held in your account if you invest through your financial intermediary or all funds held with the Fund Complex if you invest directly with the Funds.

IVY INVESTMENTS®refers to the financial services offered by Ivy Distributors, Inc., a FINRA member broker dealer and the distributor of IVY FUNDS® mutual funds, and those financial services offered by its affiliates.

Table of Contents

| CONTENTS | IVY NEXTSHARES |

| 3 | ||||

| 4 | ||||

Management Discussion, Portfolio Highlights and Schedule of Investments: | ||||

| 5 | ||||

| 10 | ||||

| 16 | ||||

| 21 | ||||

| 22 | ||||

| 23 | ||||

| 24 | ||||

| 26 | ||||

| 33 | ||||

| 34 | ||||

| 35 | ||||

| 41 | ||||

| 42 | ||||

| 42 | ||||

| 42 | ||||

| 42 |

This report is submitted for the general information of the shareholders of Ivy NextShares. It is not authorized for distribution to prospective investors in the Funds unless preceded or accompanied by a current Ivy NextShares prospectus, or summary prospectus, and current performance information.

2

Table of Contents

| PRESIDENT’S LETTER | IVY NEXTSHARES |

| JUNE 30, 2019 (UNAUDITED) | |

| Philip J. Sanders, CFA |

Dear Shareholder,

We saw a little bit of everything during the fiscal period. The first quarter of the fiscal year was relatively calm, while we witnessed dramatic market volatility and the worst quarter for U.S. equities since 2011 to end 2018. Equity markets roared back following the sharp correction, with the S&P 500 Index advancing 17% so far in 2019, as of June 30, and every sector posting gains. The rally had apro-cyclical component as information technology, consumer discretionary and industrials delivered the strongest sector returns while energy and health care were the laggards.

The U.S. economy remains relatively healthy and is now in the longest economic expansion in U.S. history despite uncertainty about trade and signs of global weakening. We believe the underlying fundamentals — a robust job market, rising wages and low inflation — support continued growth during the rest of 2019. However, U.S. trade policy remains a wildcard and poses a major threat to the current expansion.

The U.S. Federal Reserve (Fed) has held steady on interest rates thus far in 2019. However, increasing pressures from trade turmoil and uncertainty around the strength of global growth is likely to lead the Fed to become more accommodative, leading to interest rate cuts in the second half of the calendar year.

Emerging markets faced multiple headwinds over the fiscal year, namely a strong dollar, China’s focus on deleveraging and regulation, trade wars, volatile energy prices and increased geopolitical risks. Despite near-term concerns and likely volatility across the global equity market, we believe the long-term fundamentals in emerging markets will continue to offer opportunities. By comparison, U.S. equities broadly have benefitted from a more attractive growth rate, which was the result of tax reform, lower regulatory pressures and repatriation of overseas earnings.

Looking ahead, we believe equities face intensifying headwinds as the pace of global growth slows and trade turmoil lingers. As we examine the investment landscape, we continue to put greater emphasis on the fundamentals and quality of asset classes and sectors. We believe it is important to stay focused on the merits of individual market sectors, industries and companies when making investment decisions. Those fundamentals historically have tended to outweigh external factors such as government policies and regulations. While those can affect

every business and every investor, we think the innovation and management skill within individual companies are the ultimate drivers of long-term stock prices.

Economic Snapshot

| 6/30/2019 | 6/30/2018 | |||||||

S&P 500 Index | 2,941.76 | 2,718.37 | ||||||

MSCI EAFE Index | 1,922.30 | 1,958.64 | ||||||

10-Year Treasury Yield | 2.00% | 2.85% | ||||||

U.S. unemployment rate | 3.7% | 4.0% | ||||||

30-year fixed mortgage rate | 3.73% | 4.55% | ||||||

Oil price per barrel | $ | 58.47 | $ | 74.15 | ||||

Sources: Bloomberg, U.S. Department of Labor, MBA, CME

All government statistics shown are subject to periodic revision. The S&P 500 Index is an unmanaged index that tracks the stocks of 500 primarilylarge-cap U.S. companies. MSCI EAFE Index is an unmanaged index comprised of securities that represent the securities markets in Europe, Australasia and the Far East. It is not possible to invest directly in any of these indexes. Mortgage rates are from BankRate and reflect the overnight national average rate on a conventional30-year fixed loan. Oil prices reflect the market price of West Texas intermediate crude grade.

Respectfully,

Philip J. Sanders, CFA

President

The opinions expressed in this letter are those of the President of the Ivy NextShares Funds and are current only through the end of the period of the report, as stated on the cover. The President’s views are subject to change at any time, based on market and other conditions, and no forecasts can be guaranteed.

| 2019 | ANNUAL REPORT | 3 |

Table of Contents

| ILLUSTRATION OF FUND EXPENSES | IVY NEXTSHARES |

(UNAUDITED)

Expense Example

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including brokerage commissions on purchases and sales of fund shares and (2) ongoing costs, including management fees and other Fund expenses. The following table is intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for thesix-month period ended June 30, 2019.

Actual Expenses

The first section in the following table provides information about actual account values and actual expenses for each Fund. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, a $7,500 account value divided by $1,000 = 7.5), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second section in the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of five percent per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this five percent hypothetical example with the five percent hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as brokerage commissions paid on purchases and sales of fund shares. Therefore, the second section in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Expenses paid may be impacted by expense reduction arrangements. If those arrangements had not been in place, expenses paid would have been higher. See Note 4 in Notes to Financial Statements for further information.

| Actual(1) | Hypothetical(2) | Annualized Expense Ratio Based on the Six-Month Period | ||||||||||||||||||||||||||

| Fund | Beginning Account Value 12-31-18 | Ending Account Value 6-30-19 | Expenses Paid During Period* | Beginning Account Value 12-31-18 | Ending Account Value 6-30-19 | Expenses Paid During Period* | ||||||||||||||||||||||

Ivy Focused Energy NextShares | $ | 1,000 | $ | 1,092.50 | $ | 4.92 | $ | 1,000 | $ | 1,020.09 | $ | 4.75 | 0.95% | |||||||||||||||

Ivy Focused Growth NextShares | $ | 1,000 | $ | 1,249.60 | $ | 4.39 | $ | 1,000 | $ | 1,020.94 | $ | 3.94 | 0.78% | |||||||||||||||

Ivy Focused Value NextShares | $ | 1,000 | $ | 1,088.10 | $ | 4.07 | $ | 1,000 | $ | 1,020.93 | $ | 3.94 | 0.78% | |||||||||||||||

| * | Fund expenses are equal to the Fund’s annualized expense ratio (provided in the table), multiplied by the average account value over the period, multiplied by 181 days in thesix-month period ended June 30, 2019, and divided by 365. |

| (1) | This section uses the Fund’s actual total return and actual Fund expenses. It is a guide to the actual expenses paid by the Fund in the period. The “Ending Account Value” shown is computed using the Fund’s actual return and the “Expenses Paid During Period” column shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. A shareholder may use the information here, together with the dollar amount invested, to estimate the expenses that were paid over the period. For every thousand dollars a shareholder has invested, the expenses are listed in the last column of this section. |

| (2) | This section uses a hypothetical five percent annual return and actual Fund expenses. It helps to compare the Fund’s ongoing costs with other mutual funds. A shareholder can compare the Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other Funds. |

The above illustrations are based on ongoing costs only and do not include any transactional costs, such as brokerage commissions on purchases and sales of fund shares.

| 4 | ANNUAL REPORT | 2019 |

Table of Contents

| MANAGEMENT DISCUSSION | IVY FOCUSED ENERGY NEXTSHARES |

(UNAUDITED)

David P. Ginther

Michael T. Wolverton

Below, David P. Ginther, CPA, and Michael Wolverton, CFA, portfolio managers, discuss positioning, performance and results of Ivy Focused Energy NextShares for the fiscal year ended June 30, 2019. Mr. Ginther and Mr. Wolverton have managed the Fund since its inception in October 2016. Mr. Ginther has 24 years of industry experience and Mr. Wolverton has 15 years of industry experience.

Fiscal Year Performance

For the 12 Months Ended June 30, 2019 | ||||

Ivy Focused Energy NextShares (at net asset value) | -30.59% | |||

Ivy Focused Energy NextShares (at share price) | -30.57% | |||

Benchmark and Morningstar/Lipper Averages | ||||

S&P 1500 Energy Sector Index | -15.66% | |||

(generally reflects the performance of stocks that represent the energy market) | ||||

Morningstar Equity Energy Category Average | -23.59% | |||

(generally reflects the performance of the universe of funds with similar investment objectives) | ||||

Lipper Natural Resources Funds Universe Average | -19.92% | |||

(generally reflects the performance of the universe of funds with similar investment objectives) | ||||

Please note that Fund returns include applicable fees and expenses while index returns do not include any such fees. The performance discussion below is at net asset value.

Global risks mean volatile year

There were dramatic swings in oil prices during the fiscal year, culminating in a decline in the final quarter because of concerns about rising shale oil production, a slowing global economy and escalation of the U.S.-China trade tension.

Because of strong underlying supply/demand fundamentals, the Organization of Petroleum Exporting Countries (OPEC) early in the fiscal year decided to change its production quotas to begin bringing more supply to the market. Another factor in this decision was the resumption by the U.S. of economic sanctions against Iran that were scheduled to take effect in November 2018. Members of OPEC anticipated a significant reduction of supply when oil exports from Iran were phased out. However, OPEC and the rest of the market were surprised when the U.S. granted waivers for recipients of Iranian oil to continue doing so for another six months through the first quarter of 2019. The Trump Administration then did not further extend waivers during the second quarter of 2019, which would have allowed selected countries to continue buying Iranian crude oil. The administration also threatened penalties for any country trading with Iran.

The combination of acceleration in the U.S. oil supply, increased OPEC supply, waivers for Iranian exports and decelerating global demand led to a steep drop in oil prices in the third quarter of the year. Because of the dramatic negative swing in fundamentals, OPEC reversed course in November 2018 and announced a reduction in supply once again. The production cut was a positive stimulus for the oil market as crude oil prices rebounded significantly higher in the first quarter of 2019. West Texas Intermediate — the U.S. benchmark — was up about 30% and Brent crude oil was up slightly more. In addition, global oil inventories declined in the quarter as demand exceeded supply.

Strong economic growth, rationed supply from OPEC and falling global inventories created a positive backdrop for oil prices to move higher. But late in the fiscal year, Brent crude oil — the international benchmark — was in “backwardation,” meaning the current (spot) price was higher than the futures market price. That condition typically suggests a tight physical oil market. Concerns about deteriorating global macroeconomic sentiment versus a tight physical oil market led to a wide price spread between the Brent crude oil futures and spot oil, and crude oil steadily declined.

Geopolitical risks around the world increased in the final quarter of the fiscal year. Tensions between the U.S. and Iran continued to rise after Iran shot down a U.S. military drone and was accused of being behind attacks on oil tankers in the Straits of Hormuz. Roughly 20% of the world oil supply travels through the Straits every day, raising fears of additional disruptions. Geopolitical risks continued to affect production in Iran, Libya and Venezuela. The OPEC member countries plus Russia agreed during the quarter to extend production cuts through the first quarter of 2020. OPEC indicated it will review the cuts and could extend them again through the end of 2020, depending on global economic growth.

Oil prices pressure energy equities

The Fund had a negative return for the fiscal year and underperformed the returns of its benchmark index and category averages.

| 2019 | ANNUAL REPORT | 5 |

Table of Contents

The Fund’s overweight allocations at the end of the fiscal year of more than 38% of its equity assets in Exploration & Production (E&P) companies and 26% in Oil and Gas Equipment and Services companies were factors in the underperformance. The Fund remained underweight to the integrated oil companies compared to the benchmark. The Fund has maintained a high allocation to what we believe to be quality upstream companies in the E&P and Oil Services industry segments. Such companies generally have outperformed energy sector peers when oil prices have risen — which the portfolio managers still expect in the coming year — but that was a factor in underperformance because of the sharp fall in prices late in the fiscal year.

Key detractors from the Fund’s performance relative to its benchmark during the fiscal year included holdings in Enscoplc-Class A, Chevron Corp., Oasis Petroleum, Inc., Transocean Ltd., Superior Energy Services and Halliburton Co. Enscoplc-Class A, Oasis Petroleum, Inc. and Superior Energy Services no longer were holdings in the Fund as of June 30, 2019.

Holdings in Enterprise Products Partners, Anadarko Petroleum Corp. and Propetro Holding Corp. contributed to the Fund’s relative performance. Anadarko Petroleum Corp. no longer was a holding in the Fund as of June 30, 2019. The Fund also benefitted by not holding several underperforming equities that are benchmark components, including ExxonMobil Corp., Occidental Petroleum Corp. and Conocophillips.

The Fund made no use of derivatives during the reporting period.

The focus of the energy strategy remains on investing in companies that we believe can create value over the full course of the energy cycle. We define those as companies that arelow-cost operators, have strong balance sheets, have the ability to grow profitably and have strong return on capital.

Continue tight oil markets

We expect the oil markets to continue to be tight through 2019 because of draws on inventories and the extension of OPEC’s production cuts into 2020. We think growth in U.S. shale oil production is likely to exceed worldwide oil demand growth for 2019.

The worldwide oil demand growth rate continues to be the greatest risk to oil prices. We believe the rate of growth will slow in the second half of 2019. Demand growth still has been better than the market expected despite the increased tension between U.S. and China over trade issues.

We believe price volatility in the oil markets will continue in 2019. We expect geopolitical tensions in the Middle East to remain high and continue to be a factor in the oil market, with no sign of talks in the future. We nevertheless believe oil demand will continue to grow despite slower global economic growth and the production cuts by OPEC and partner states. We also think the reversal of some of the Iran sanction waivers will help rebalance the world oil market and support oil prices in 2019. We believe OPEC took a positive and necessary step toward rebalancing the world oil market with its production cut decision and think the move will help support prices in 2019.

We think that the U.S. oil rig count is likely to remain flat, as producers show spending discipline even with higher oil prices. Exploration and production companies are seeing more pressure from investors to be more prudent in allocating capital in order to generate better investor returns. This discipline could be tested in the second half of 2019 if oil prices remain in the current range or higher.

Past performance is not a guarantee of future results. The value of the Fund’s shares will change and you could lose money on your investment.

Investing in companies involved in one specified sector may be more risky and volatile than an investment with greater sector diversification. Investing in the energy sector can be riskier than other types of investment activities because of a range of factors, including price fluctuation caused by real and perceived inflationary trends and political developments, and the cost assumed by energy companies in complying with environmental safety regulations. These and other risks are more fully described in the Fund’s prospectus.

The opinions expressed in this report are those of the Fund’s portfolio managers and are current only through the end of the period of the report as stated on the cover. The managers’ views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed.

The index noted is unmanaged, includes reinvested dividends and does not include fees. One cannot invest directly in an index, nor is an index representative of Ivy Focused Energy NextShares.

| 6 | ANNUAL REPORT | 2019 |

Table of Contents

| PORTFOLIO HIGHLIGHTS | IVY FOCUSED ENERGY NEXTSHARES |

ALL DATA IS AS OF JUNE 30, 2019 (UNAUDITED)

Asset Allocation

Stocks | 97.0% | |||

Energy | 93.9% | |||

Industrials | 3.1% | |||

Liabilities (Net of Cash and Other Assets), and Cash Equivalents+ | 3.0% |

Country Weightings

North America | 88.6% | |||

United States | 84.6% | |||

Canada | 4.0% | |||

Europe | 8.4% | |||

Liabilities (Net of Cash and Other Assets), and Cash Equivalents+ | 3.0% |

Top 10 Equity Holdings

| Company | Country | Sector | Industry | |||

Pioneer Natural Resources Co. | United States | Energy | Oil & Gas Exploration & Production | |||

Continental Resources, Inc. | United States | Energy | Oil & Gas Exploration & Production | |||

Concho Resources, Inc. | United States | Energy | Oil & Gas Exploration & Production | |||

Chevron Corp. | United States | Energy | Integrated Oil & Gas | |||

Enterprise Products Partners L.P. | United States | Energy | Oil & Gas Storage & Transportation | |||

Marathon Petroleum Corp. | United States | Energy | Oil & Gas Refining & Marketing | |||

Parsley Energy, Inc., Class A | United States | Energy | Oil & Gas Exploration & Production | |||

Schlumberger Ltd. | United States | Energy | Oil & Gas Equipment & Services | |||

ProPetro Holding Corp. | United States | Energy | Oil & Gas Equipment & Services | |||

Valero Energy Corp. | United States | Energy | Oil & Gas Refining & Marketing |

See your advisor or www.ivyinvestments.com for more information on the Fund’s most recently published Top 10 Equity Holdings.

| + | Cash equivalents are defined as highly liquid securities with maturities of less than three months. Cash equivalents may include U.S. Government Treasury bills, bank certificates of deposit, bankers’ acceptances, corporate commercial paper, short term investment funds and other money market instruments. |

| 2019 | ANNUAL REPORT | 7 |

Table of Contents

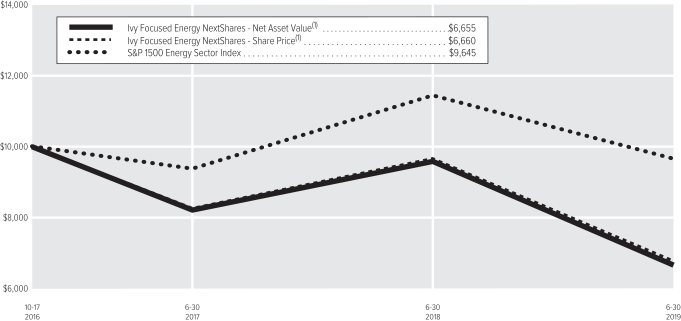

| COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT | IVY FOCUSED ENERGY NEXTSHARES |

(UNAUDITED)

| (1) | The value of the investment in the Fund is impacted by the ongoing expenses of the Fund and assumes reinvestment of dividends and distributions. |

| Average Annual Total Return | ||||||||

| | Net Asset Value | | | Share Price | ||||

1-year period ended6-30-19 | -30.59% | -30.57% | ||||||

5-year period ended6-30-19 | — | — | ||||||

10-year period ended6-30-19 | — | — | ||||||

Since inception of Fund(2) through6-30-19 | -14.00% | -13.97% | ||||||

| (2) | 10-17-16 (the date on which shares were first acquired by shareholders). |

Past performance is not necessarily indicative of future performance. Indexes are unmanaged. The performance graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. Performance results may include the effect of expense reduction arrangements for some or all of the periods shown. If those arrangements had not been in place, the performance results for those periods would have been lower. The Fund’s performance at share price will differ from its results at net asset value (“NAV”). Share price returns are based on the Fund’s price at the close of market trading. If you trade your shares at another time during the day, your return may differ. For performance as of the most recent month end, including historical trading premiums/discounts relative to NAV, please refer to www.ivyinvestments.com.

| 8 | ANNUAL REPORT | 2019 |

Table of Contents

| SCHEDULE OF INVESTMENTS | IVY FOCUSED ENERGY NEXTSHARES (in thousands) |

JUNE 30, 2019

| COMMON STOCKS | Shares | Value | ||||||

Energy |

| |||||||

Integrated Oil & Gas – 9.3% |

| |||||||

Chevron Corp. | 3 | $ | 311 | |||||

Suncor Energy, Inc. | 8 | 238 | ||||||

|

| |||||||

| 549 | ||||||||

|

| |||||||

Oil & Gas Drilling – 5.6% |

| |||||||

Patterson-UTI Energy, Inc. | 13 | 149 | ||||||

Transocean, Inc. (A) | 28 | 182 | ||||||

|

| |||||||

| 331 | ||||||||

|

| |||||||

Oil & Gas Equipment & Services – 25.2% |

| |||||||

Baker Hughes, Inc. | 10 | 235 | ||||||

Cactus, Inc., Class A (A) | 6 | 184 | ||||||

Core Laboratories N.V. | 3 | 136 | ||||||

FMC Technologies, Inc. | 7 | 176 | ||||||

Halliburton Co. | 10 | 228 | ||||||

ProPetro Holding Corp. (A) | 13 | 265 | ||||||

Schlumberger Ltd. | 7 | 266 | ||||||

|

| |||||||

| 1,490 | ||||||||

|

| |||||||

Oil & Gas Exploration & Production – 36.4% |

| |||||||

Concho Resources, Inc. | 3 | 329 | ||||||

Continental Resources, Inc. (A) | 8 | 338 | ||||||

Diamondback Energy, Inc. | 2 | 246 | ||||||

EOG Resources, Inc. | 3 | 252 | ||||||

Parsley Energy, Inc., Class A (A) | 14 | 267 | ||||||

| COMMON STOCKS (Continued) | Shares | Value | ||||||

Oil & Gas Exploration & Production(Continued) |

| |||||||

Pioneer Natural Resources Co. | 2 | $ | 376 | |||||

Whiting Petroleum Corp. (A) | 7 | 122 | ||||||

WPX Energy, Inc. (A) | 20 | 225 | ||||||

|

| |||||||

| 2,155 | ||||||||

|

| |||||||

Oil & Gas Refining & Marketing – 12.6% |

| |||||||

Marathon Petroleum Corp. | 5 | 271 | ||||||

Phillips 66 | 2 | 214 | ||||||

Valero Energy Corp. | 3 | 263 | ||||||

|

| |||||||

| 748 | ||||||||

|

| |||||||

Oil & Gas Storage & Transportation – 4.8% |

| |||||||

Enterprise Products Partners L.P. | 10 | 286 | ||||||

|

| |||||||

Total Energy – 93.9% |

| 5,559 | ||||||

Industrials |

| |||||||

Industrial Machinery – 3.1% |

| |||||||

Apergy Corp. (A) | 5 | 184 | ||||||

|

| |||||||

Total Industrials – 3.1% |

| 184 | ||||||

TOTAL COMMON STOCKS – 97.0% |

| $ | 5,743 | |||||

(Cost: $7,253) |

| |||||||

| SHORT-TERM SECURITIES | Shares | Value | ||||||

Money Market Funds – 3.5% |

| |||||||

State Street Institutional U.S. Government Money Market Fund 2.310% (B) | 209 | $ | 209 | |||||

|

| |||||||

TOTAL SHORT-TERM SECURITIES – 3.5% |

| $ | 209 | |||||

(Cost: $209) |

| |||||||

TOTAL INVESTMENT SECURITIES – 100.5% |

| $ | 5,952 | |||||

(Cost: $7,462) |

| |||||||

LIABILITIES, NET OF CASH AND OTHER ASSETS – (0.5)% |

| (32 | ) | |||||

NET ASSETS – 100.0% |

| $ | 5,920 | |||||

Notes to Schedule of Investments

| (A) | No dividends were paid during the preceding 12 months. |

| (B) | Rate shown is the annualized7-day yield at June 30, 2019. |

The following table is a summary of the valuation of the Fund’s investments by the fair value hierarchy levels as of June 30, 2019. See Note 3 to the Financial Statements for further information regarding fair value measurement.

| Level 1 | Level 2 | Level 3 | ||||||||||

Assets | ||||||||||||

Investments in Securities | ||||||||||||

Common Stocks | $ | 5,743 | $ | — | $ | — | ||||||

Short-Term Securities | 209 | — | — | |||||||||

Total | $ | 5,952 | $ | — | $ | — | ||||||

| Country Diversification | ||||

(as a % of net assets) |

| |||

United States | 84.6% | |||

Canada | 4.0% | |||

Switzerland | 3.1% | |||

United Kingdom | 3.0% | |||

Netherlands | 2.3% | |||

Other+ | 3.0% | |||

| + | Includes liabilities (net of cash and other assets), and cash equivalents |

See Accompanying Notes to Financial Statements.

| 2019 | ANNUAL REPORT | 9 |

Table of Contents

| MANAGEMENT DISCUSSION | IVY FOCUSED GROWTH NEXTSHARES |

(UNAUDITED)

Bradley M. Klapmeyer

Below, Bradley M. Klapmeyer, CFA, portfolio manager of Ivy Focused Growth NextShares, discusses positioning, performance and results for the fiscal year ended June 30, 2019. Mr. Klapmeyer has managed the Fund since inception in October 2016 and has 19 years of industry experience.

Fiscal Year Performance

For the 12 Months Ended June 30, 2019 | ||||

Ivy Focused Growth NextShares (at net asset value) | 16.54% | |||

Ivy Focused Growth NextShares (at share price) | 16.54% | |||

Benchmark and Morningstar/Lipper Averages | ||||

Russell 1000 Growth Index | 11.56% | |||

(generally reflects the performance of securities that represent thelarge-cap growth market) | ||||

Morningstar Large Growth Category Average | 10.02% | |||

(generally reflects the performance of the universe of funds with similar investment objectives) | ||||

LipperLarge-Cap Growth Funds Universe Average | 10.79% | |||

(generally reflects the performance of the universe of funds with similar investment objectives) | ||||

Please note that Fund returns include applicable fees and expenses while index returns do not include any such fees. The performance discussion below is at net asset value.

The Russell 1000 Growth Index, the Fund’s benchmark, gained a solid 11.56% during the measurement period, which would have indicated the possibility of a solid, uneventful prior 12 months. Unfortunately, that assessment was far from correct as the market went through a series of significant reversals during the measurement period. As a timeline, the benchmark posted strong gains from June 30, 2018 through September 30, 2018, up 9.2%. Those gains were reversed in a significantsell-off of nearly 16% in the following three months, only to reverse again with a 21.5% gain during the next six months.

Sentiment evolved notably from the beginning until the end of the measurement period. During the early months of the fiscal year, economic growth remained strong, fueled from the benefits of personal and corporate tax reform in calendar year 2018. Economic growth likely also experienced an uplift. Global businesses began to pull forward export demand from the U.S. to front run tariffs as trade war rhetoric continued to intensify but remained a peripheral threat to overall economic stability. The Federal Reserve (Fed) comfortably moved interest rates higher in June and September 2018, marking the seventh and eighth increases of the cycle. Importantly, inflation remained within reasonable bounds, giving investors comfort that the Fed had plenty of room for patience on interest rates before the economy overheated. Volatility cooled off and market returns were strong.

The positive sentiment changed significantly during the October to December 2018 timeframe and there was carnage in the markets as proof. The list of concerns during this period began to build into a market panic and were plentiful: Weakening growth in the U.S., eurozone and China — likely stemming from the uncertainty created by the trade war; Brexit risk back to a boil; U.S. government shutdown over a border wall funding impasse; presidential attacks on Fed Chairman Jerome Powell, and the realization that the temporary trade truce was anything but clear. The panic attack was further exacerbated by the Fed moving forward with the ninth interest rate hike of the cycle in December 2018, marking the fourth within that past 12 months. As such, the equity market screamed “policy error” and the markets turned to a dark place … the end of an already too long economic cycle.

In the last reversal, the market came roaring back during the second half of the measurement period. It isn’t difficult to find the factors that generated the optimism, which drove the markets higher. Post what was perceived to be a policy error during the prior period, the Fed moved quickly to ease tightening financial conditions. Actions taken included stepping back from material quantitative tightening (balance sheet reduction) and communicating that interest rates will be on hold for the foreseeable future. Interest rates responded as the yield curve moved lower. Investors perceived the reduction in rates as helpful for solving the problem of tightening financial conditions and by the end of the measurement period were pricing in the likelihood of multiple rates cuts during the coming quarters.

Another reversal was the market stress related to escalating trade war rhetoric. There was building consensus during the final quarter of the fiscal year that China and the U.S. were on a path to a real trade agreement. Companies with foreign exposure, which had a difficult year in calendar year 2018, benefited from this more optimistic sentiment. Ultimately at the end of period the U.S. and China agreed to a “trade truce” that paused further tariff action by either country. Investors welcomed this pause in escalation, but it was largely anticipated by the markets and left the existing tariffs in place.

Overall, the fiscal year closed out with an optimistic tone that corrective action being taken in part by U.S. participants, such as the Fed moving more dovish, but also supportive actions from other central banks and governments around the globe, would ultimately lead to improved global growth over the coming12-month measurement period.

| 10 | ANNUAL REPORT | 2019 |

Table of Contents

Looking at the return by the index, factor performance showed that momentum (price returns, relative strength) and quality (Return on Capital and Return on Equity) factors were key variables in driving performance during the fiscal year. Value, risk and cash deployment were the keyout-of-favor factors, with low valuation stocks and high-dividend yielding stocks generally underperforming the benchmark.

Strategies employed, contributors and detractors

In the12-month period ended June 30, 2019, the Fund outperformed relative to its benchmark. Fund performance was mainly driven by information technology, with additional strong positive contributions from industrials and health care. Despite the strong absolute and relative performance, the communications services sector was a notable detractor of performance during the measurement period.

Information technology stocks, especiallymega-cap technology stocks, once again proved to be fuel for the markets for most of the measurement period. The Fund was overweight the sector but the majority of outperformance was driven by stock selection. Individual security overweight positions in PayPal, Inc., MasterCard, Inc., VeriSign, Inc. and Visa, Inc., contributed meaningfully to performance. An overweight position to software stocks, such as Microsoft Corp., Adobe, Inc. and salesforce.com, Inc., also contributed to relative performance. We think investors were attracted to the strongend-markets in technology, such as digital marketing initiatives, cloud computing andsoftware-as-a-service approaches. The payment stocks continued to post solid transaction volume gains and likely benefited from movement during the second half of the measurement period toward higher quality names.

Another notable contributor to the Fund’s strong relative performance was stock selection in the industrials sector. An overweight position in CoStar Group, Inc. contributed to performance as the company continued to post solid growth in both its core commercial real estate analytics business but also in its strong multi-family/commercial real estate listings offering. Defense contractor, Lockheed Martin, Corp., also contributed to relative performance.

Health care contribution was driven by Zoetis, Inc., which continues to benefit from its slow, steady and stable growth in the animal health sector. The Fund also benefited from underweight exposure to thelarge-cap biotechnology and pharmaceutical sectors, both of which performed poorly during the measurement period.

Despite good overall strong absolute and relative performance, the communications services sector was acall-out detractor from Fund performance. The Fund was overweight Alphabet, Inc., which underperformed, and was underweight Facebook, Inc., which outperformed. The Fund also was negatively impacted by lack of exposure to Disney, which was strong in the last quarter of the measurement period due to investor excitement regarding Disney’s new video streaming service.

Outlook and positioning

Exiting the second quarter of 2019, one could easily be drawn back into a narrative that has worked for most of this decade’s long bull market. The narrative takes a very optimist skew on shaky economic data and is something akin to the beliefs, “Don’t sweat these pullbacks, they are typically good buying opportunities, slow growth is good enough, and although global growth has weakened, China is adding economic support and global central bankers will respond.” This narrative may sound familiar and is in fact the narrative we have leaned into over the past decade as well. We took advantage of multiple buying opportunities during many of the “mini-shocks” through the years. And yes, many ultimately proved to be good buying opportunities.

This time around we take issue with returning to this same narrative so quickly. Yes, there are actions in place to address the slowing global growth and address tightening financial conditions in the U.S. However, we believe it is important to take a step back and observe that the slowdowns and subsequent recoveries that occurred during 2013 and 2016 were painted within a backdrop of easy monetary policy conditions and easy global policy. Since then the Fed has instituted nine rate hikes and has stopped the expansion of its balance sheet. These changes are all mechanisms that could lead to tightening conditions, which we believe have yet to be fully digested and should result in continued slowing in the back half of 2019.

We foresee earnings risk and negative revisions ahead. There are some who believe bad economic news is good for the market because it will bring with it central bank intervention. We believe this thinking is a bit premature, so we are positioned more for the slowing than any rebound that might follow. One must stop to consider, “are global rates moving to ‘dovish’ territory to increase the odds of accelerating growth, or have global rates moved ‘dovish’ because the downside risk to growth was materially increasing? Are things likely to accelerate, or just not get as nasty?”

In our view, investors seem comfortable with current trade tensions, believing the disputes will amicably resolve themselves (with time). They seem to have gotten used to the trade war rhetoric and the “on again, off again” threats. And while two large economies threatening each other with growth-halting tariffs is now the new normal, it still worries us. Others believe the Trump administration will seek a resolution to the trade disputes only when the equity market retreats. Whatever the rationale, it seems investors have generally priced in a positive outcome for the trade dispute.

| 2019 | ANNUAL REPORT | 11 |

Table of Contents

Investor complacency is surprising given the economic headwinds. Global manufacturing data, for example, has moved into contraction territory. Companies are reassessing how and when to reposition their assets, leading to slowdown in business investment spending. As we have noted before, companies will likely struggle to build long-range investment plans if the rules of engagement for global trade are in flux and are changed by social posts. We believe this situation will continue to impair corporate investment and challenge the long-term margins of manufacturing companies.

We are eyeing risky assets, as we believe the next round of negative revisions may present opportunities in more risky assets. However, we have a very high hurdle for taking on additional risk, either cyclical or economic. We require companies with higher cyclical risk to have a strong margin profile and outstanding through-cycle cash flow generation. We also require these companies to have strong economic models, as revealed by our proprietary fundamental research, a unique aspect to the businesses that protects their through-cycle competitive position and asset returns. With these riskier assets we also require valuations that offer downside protection.

For the time being, we believe investors will remain favorable to the high-quality growth names and the overall growth category as they find fewer and fewer attractive holdings due to slowing economic growth. Valuation is always a consideration and a risk control mechanism, but during these periods, valuations can take a backseat to demand for the shrinking list of stable, visible growers. Should economic growth reaccelerate, we could see a sharp rotation back to cyclical growth, but for now we believe the growth scarcity narrative has a little more runway.

As of June 30, 2019, the Fund’s largest positions are Microsoft Corp., Alphabet, Inc., MasterCard, Inc., PayPal, Inc., Amazon.com, Inc., Zoetis, Inc., Adobe, Inc., Visa, Inc., Apple, Inc., and CoStar Group, Inc.

Past performance is not a guarantee of future results. As with any mutual fund, the value of the Fund’s shares will change, and you could lose money on your investment.

Prices of growth stocks may be more sensitive to changes in current or expected earnings than the prices of other stocks. Growth stocks may not perform as well as value stocks or the stock market in general. These and other risks are more fully described in the Fund’s prospectus.

The opinions expressed in this report are those of the Fund’s portfolio manager and are current only through the end of the period of the report as stated on the cover. The portfolio manager’s views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed.

The index noted is unmanaged, includes reinvested dividends and does not include fees. One cannot invest directly in an index, nor is an index representative of Ivy Focused Growth NextShares.

| 12 | ANNUAL REPORT | 2019 |

Table of Contents

| PORTFOLIO HIGHLIGHTS | IVY FOCUSED GROWTH NEXTSHARES |

ALL DATA IS AS OF JUNE 30, 2019 (UNAUDITED)

Asset Allocation

Stocks | 98.6% | |||

Information Technology | 43.5% | |||

Consumer Discretionary | 14.5% | |||

Communication Services | 11.9% | |||

Industrials | 11.6% | |||

Health Care | 10.6% | |||

Financials | 4.1% | |||

Real Estate | 2.4% | |||

Liabilities (Net of Cash and Other Assets), and Cash Equivalents+ | 1.4% |

Top 10 Equity Holdings

| Company | Sector | Industry | ||

Microsoft Corp. | Information Technology | Systems Software | ||

Alphabet, Inc., Class C | Communication Services | Interactive Media & Services | ||

MasterCard, Inc., Class A | Information Technology | Data Processing & Outsourced Services | ||

PayPal, Inc. | Information Technology | Data Processing & Outsourced Services | ||

Amazon.com, Inc. | Consumer Discretionary | Internet & Direct Marketing Retail | ||

Zoetis, Inc. | Health Care | Pharmaceuticals | ||

Adobe, Inc. | Information Technology | Application Software | ||

Visa, Inc., Class A | Information Technology | Data Processing & Outsourced Services | ||

Apple, Inc. | Information Technology | Technology Hardware, Storage & Peripherals | ||

CoStar Group, Inc. | Industrials | Research & Consulting Services |

See your advisor or www.ivyinvestments.com for more information on the Fund’s most recently published Top 10 Equity Holdings.

| + | Cash equivalents are defined as highly liquid securities with maturities of less than three months. Cash equivalents may include U.S. Government Treasury bills, bank certificates of deposit, bankers’ acceptances, corporate commercial paper, short term investment funds and other money market instruments. |

| 2019 | ANNUAL REPORT | 13 |

Table of Contents

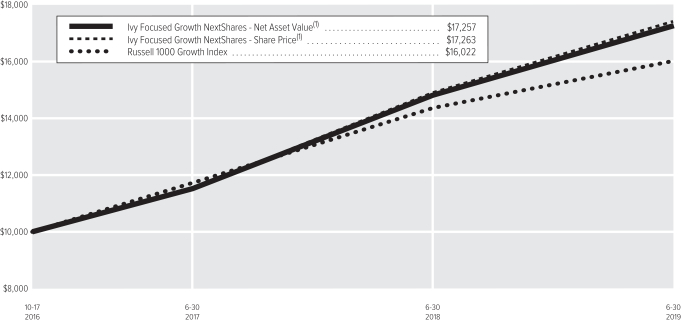

| COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT | IVY FOCUSED GROWTH NEXTSHARES |

(UNAUDITED)

| (1) | The value of the investment in the Fund is impacted by the ongoing expenses of the Fund and assumes reinvestment of dividends and distributions. |

| Average Annual Total Return | ||||||||

| | Net Asset Value | | | Share Price | | |||

1-year period ended6-30-19 | 16.54% | 16.54% | ||||||

5-year period ended6-30-19 | — | — | ||||||

10-year period ended6-30-19 | — | — | ||||||

Since inception of Fund(2) through6-30-19 | 22.38% | 22.40% | ||||||

| (2) | 10-17-16 (the date on which shares were first acquired by shareholders). |

Past performance is not necessarily indicative of future performance. Indexes are unmanaged. The performance graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. Performance results may include the effect of expense reduction arrangements for some or all of the periods shown. If those arrangements had not been in place, the performance results for those periods would have been lower. The Fund’s performance at share price will differ from its results at net asset value (“NAV”). Share price returns are based on the Fund’s price at the close of market trading. If you trade your shares at another time during the day, your return may differ. For performance as of the most recent month end, including historical trading premiums/discounts relative to NAV, please refer to www.ivyinvestments.com.

| 14 | ANNUAL REPORT | 2019 |

Table of Contents

| SCHEDULE OF INVESTMENTS | IVY FOCUSED GROWTH NEXTSHARES (in thousands) |

JUNE 30, 2019

| COMMON STOCKS | Shares | Value | ||||||

Communication Services |

| |||||||

Interactive Home Entertainment – 2.9% |

| |||||||

Electronic Arts, Inc. (A) | 4 | $ | 401 | |||||

|

| |||||||

Interactive Media & Services – 9.0% |

| |||||||

Alphabet, Inc., Class C (A) | 1 | 882 | ||||||

Facebook, Inc., Class A (A) | 2 | 385 | ||||||

|

| |||||||

| 1,267 | ||||||||

|

| |||||||

Total Communication Services – 11.9% |

| 1,668 | ||||||

Consumer Discretionary |

| |||||||

Apparel, Accessories & Luxury Goods – 2.7% |

| |||||||

V.F. Corp. | 4 | 380 | ||||||

|

| |||||||

Automobile Manufacturers – 3.8% |

| |||||||

Ferrari N.V. | 3 | 535 | ||||||

|

| |||||||

Home Improvement Retail – 2.7% |

| |||||||

Home Depot, Inc. (The) | 2 | 373 | ||||||

|

| |||||||

Internet & Direct Marketing Retail – 5.3% |

| |||||||

Amazon.com, Inc. (A) | — | * | 748 | |||||

|

| |||||||

Total Consumer Discretionary – 14.5% |

| 2,036 | ||||||

Financials |

| |||||||

Financial Exchanges & Data – 4.1% |

| |||||||

CME Group, Inc. | 3 | 579 | ||||||

|

| |||||||

Total Financials – 4.1% |

| 579 | ||||||

Health Care |

| |||||||

Managed Health Care – 2.8% |

| |||||||

UnitedHealth Group, Inc. | 2 | 394 | ||||||

|

| |||||||

| COMMON STOCKS (Continued) | Shares | Value | ||||||

Pharmaceuticals – 7.8% |

| |||||||

Pfizer, Inc. | 8 | $ | 361 | |||||

Zoetis, Inc. | 6 | 728 | ||||||

|

| |||||||

| 1,089 | ||||||||

|

| |||||||

Total Health Care – 10.6% |

| 1,483 | ||||||

Industrials |

| |||||||

Aerospace & Defense – 3.5% |

| |||||||

Lockheed Martin Corp. | 1 | 486 | ||||||

|

| |||||||

Construction Machinery & Heavy Trucks – 1.8% |

| |||||||

Caterpillar, Inc. | 2 | 246 | ||||||

|

| |||||||

Railroads – 2.0% |

| |||||||

Union Pacific Corp. | 2 | 288 | ||||||

|

| |||||||

Research & Consulting Services – 4.3% |

| |||||||

CoStar Group, Inc. (A) | 1 | 605 | ||||||

|

| |||||||

Total Industrials – 11.6% |

| 1,625 | ||||||

Information Technology |

| |||||||

Application Software – 11.2% |

| |||||||

Adobe, Inc. (A) | 2 | 708 | ||||||

Intuit, Inc. | 2 | 585 | ||||||

salesforce.com, Inc. (A) | 2 | 276 | ||||||

|

| |||||||

| 1,569 | ||||||||

|

| |||||||

Data Processing & Outsourced Services – 16.3% |

| |||||||

MasterCard, Inc., Class A | 3 | 829 | ||||||

PayPal, Inc. (A) | 7 | 788 | ||||||

Visa, Inc., Class A | 4 | 671 | ||||||

|

| |||||||

| 2,288 | ||||||||

|

| |||||||

| COMMON STOCKS (Continued) | Shares | Value | ||||||

Internet Services & Infrastructure – 2.5% |

| |||||||

VeriSign, Inc. (A) | 2 | $ | 348 | |||||

|

| |||||||

Systems Software – 8.9% |

| |||||||

Microsoft Corp. | 9 | 1,242 | ||||||

|

| |||||||

Technology Hardware, Storage & Peripherals – 4.6% |

| |||||||

Apple, Inc. | 3 | 653 | ||||||

|

| |||||||

Total Information Technology – 43.5% |

| 6,100 | ||||||

Real Estate |

| |||||||

Specialized REITs – 2.4% |

| |||||||

Equinix, Inc. | 1 | 344 | ||||||

|

| |||||||

Total Real Estate – 2.4% |

| 344 | ||||||

TOTAL COMMON STOCKS – 98.6% |

| $ | 13,835 | |||||

(Cost: $9,218) |

| |||||||

| SHORT-TERM SECURITIES | ||||||||

Money Market Funds – 1.6% |

| |||||||

State Street Institutional U.S. Government Money Market Fund 2.310% (B) | 218 | 218 | ||||||

|

| |||||||

TOTAL SHORT-TERM SECURITIES – 1.6% |

| $ | 218 | |||||

(Cost: $218) |

| |||||||

TOTAL INVESTMENT SECURITIES – 100.2% |

| $ | 14,053 | |||||

(Cost: $9,436) |

| |||||||

LIABILITIES, NET OF CASH AND OTHER ASSETS – (0.2)% |

| (33 | ) | |||||

NET ASSETS – 100.0% |

| $ | 14,020 | |||||

Notes to Schedule of Investments

| * | Not shown due to rounding. |

| (A) | No dividends were paid during the preceding 12 months. |

| (B) | Rate shown is the annualized7-day yield at June 30, 2019. |

The following table is a summary of the valuation of the Fund’s investments by the fair value hierarchy levels as of June 30, 2019. See Note 3 to the Financial Statements for further information regarding fair value measurement.

| Level 1 | Level 2 | Level 3 | ||||||||||

Assets | ||||||||||||

Investments in Securities | ||||||||||||

Common Stocks | $ | 13,835 | $ | — | $ | — | ||||||

Short-Term Securities | 218 | — | — | |||||||||

Total | $ | 14,053 | $ | — | $ | — | ||||||

The following acronym is used throughout this schedule:

REIT = Real Estate Investment Trust

See Accompanying Notes to Financial Statements.

| 2019 | ANNUAL REPORT | 15 |

Table of Contents

| MANAGEMENT DISCUSSION | IVY FOCUSED VALUE NEXTSHARES |

(UNAUDITED)

Matthew T. Norris

Below, Matthew T. Norris, CFA, portfolio manager of Ivy Focused Value NextShares, discusses positioning, performance and results for the fiscal year ended June 30, 2019. He has managed the Fund since its inception in October 2016, and has 27 years of industry experience.

Fiscal Year Performance

For the 12 Months Ended June 30, 2019 | ||||

Ivy Focused Value NextShares (at net asset value) | 1.62% | |||

Ivy Focused Value NextShares (at share price) | 1.63% | |||

Benchmark and Morningstar/Lipper Averages | ||||

Russell 1000 Value Index | 8.46% | |||

(generally reflects the performance of large-company value style stocks) | ||||

Morningstar Large Value Category Average | 5.79% | |||

(generally reflects the performance of the universe of funds with similar investment objectives) | ||||

LipperMulti-Cap Value Funds Universe Average | 3.20% | |||

(generally reflects the performance of the universe of funds with similar investment objectives) | ||||

Please note that Fund returns include applicable fees and expenses while index returns do not include any such fees. The performance discussion below is at net asset value.

Key drivers

Overall, equity markets were up for the measurement period, but experienced considerable volatility along the way. The broader market fell around 15% in the fourth calendar quarter of 2018, before recovering all of the loss in the first calendar quarter of 2019. There are a number of macro issues contributing to recent increased market volatility. About a year ago, the Federal Reserve (Fed) was on a path of gradually increasing interest rates, while in the past three months this has changed to an expectation of interest rate cuts. The economy, while still growing, has slowed; job growth, while still positive, is more tenuous; and inflation isnon-existent. There is also a feeling that this may be as good as it gets, as many of the tailwinds propelling the market over the past few years will have a difficult time continuing. This has led the Fed to the conclusion that an interest rate cut may improve the economic outlook, with many referring to it as an “insurance” cut against a possible recession.

The trade conflict with China has also contributed to market swings. The news flow during the measurement period swung from good to bad and then back to neutral. Trade wars are not good for either country, and while we have not seen many signs of harm to the U.S. economy so far, we feel they are inevitable if the tariffs continue for a long period.

The12-month measurement period was solid if not spectacular for value stocks as the Russell 1000 Value Index (the Fund’s benchmark) was up 8.46% for the timeframe. The Fund had positive returns for the period, but lagged its benchmark on a number of poor stock selections. Style investing continues to favor growth over value. These trends have been in place for some time and will likely only change with two possible factors: an economic recession, or the return of higher inflation/interest rates. Roughly 10 years post the 2008 recession, it seems possible that we are likely due for another; however, that will be very hard to recognize until it begins.

Contributors and detractors

Large impacts to the Fund’s performance came from several individual stocks. On the negative side, Gap, Inc. (no longer a holding) stock fell 43%, as the strength in its Old Navy division could not offset weakness in the company’s branded retail stores. Although the energy sector was an overall contributor to Fund performance, it did hold one of our negative picks, which was refinery PBF Energy, Inc., which fell 14%. This sector was by far the worst performer in the market, with the sector within the benchmark declining more than 14% — only one other sector, materials, was negative. The Fund still holds PBF Energy.

On the more positive side, our financials and information technology investments added notable performance. Broadcom, Ltd. and KLA Corp., both involved in the semiconductor industry, rose 38% and 31%, respectively. In financials, Synchrony Financial, a provider of store brand and private label credit cards, rose 27%. KLA and Synchrony have both been sold as the stocks appreciated to our estimate of full valuation. The Fund is still invested in Broadcom.

| 16 | ANNUAL REPORT | 2019 |

Table of Contents

Outlook

The rest of 2019 could be interesting for investors. We believe the U.S. economy should continue to plug along, but there are worrisome signs of slowing ahead. We feel corporate earnings estimates are likely too high for the second half of 2019. The outcome of the trade tariffs is difficult to predict, with resolution or escalation having major positive/negative effects on the economy and markets. The tightened job market appears to be stable, but consumers have yet to see significant wage growth. Finally, will the Fed pursue interest rate cuts in an attempt to spur faster gross domestic product growth is the big question. We would expect small positive returns from the overall stock market. However, the risk of a downturn suddenly seems greater than at any time in the past few years.

The aforementioned trends of growth versus value and small cap versus large cap will not alter our investment approach. We seek to find quality, growing companies whose stocks are trading below what we consider their intrinsic values. We seek companies that pay a dividend in the upper deciles of yield, have high returns on capital and strong balance sheets.

The Fund continues to emphasize high current income as an investment goal. During the measurement period, the Fund paid 73.89 cents of income to investors. Based on the measurement period ending net asset value (NAV) of 20.27, this equates to a 3.65% yield. We continue to target a high current yield, with expectations of 3.5% to 4%. We feel the approach of combining dividend, valuation and quality factors gives us a short list of possible investment candidates. This short list enables us to focus on these names in detail. We believe keeping the Fund concentrated will allow our stock picking to show through into the final results.

Past performance is not a guarantee of future results. The value of the Fund’s shares will change, and you could lose money on your investment.

Value stocks are stocks of companies that may have experienced adverse business or industry developments, or may be subject to special risks that have caused the stocks to be out of favor and, in the opinion of the Fund’s manager, undervalued. The value of a security believed by the Fund’s manager to be undervalued may never reach what the manager believes to be its full value, or such security’s value may decrease. These and other risks are more fully described in the Fund’s prospectus.

The opinions expressed in this report are those of the Fund’s portfolio manager and are current only through the end of the period of the report as stated on the cover. The manager’s views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed.

The index noted is unmanaged, includes reinvested dividends and does not include fees. One cannot invest directly in an index, nor is an index representative of the Ivy Focused Value NextShares.

| 2019 | ANNUAL REPORT | 17 |

Table of Contents

| PORTFOLIO HIGHLIGHTS | IVY FOCUSED VALUE NEXTSHARES |

ALL DATA IS AS OF JUNE 30, 2019 (UNAUDITED)

Asset Allocation

Stocks | 99.5% | |||

Financials | 18.5% | |||

Information Technology | 17.3% | |||

Health Care | 17.0% | |||

Energy | 11.0% | |||

Communication Services | 7.8% | |||

Materials | 7.4% | |||

Industrials | 5.1% | |||

Consumer Discretionary | 4.2% | |||

Utilities | 4.1% | |||

Consumer Staples | 4.1% | |||

Real Estate | 3.0% | |||

Liabilities (Net of Cash and Other Assets), and Cash Equivalents+ | 0.5% |

Top 10 Equity Holdings

| Company | Sector | Industry | ||

PBF Energy, Inc., Class A | Energy | Oil & Gas Refining & Marketing | ||

AGNC Investment Corp. | Financials | Mortgage REITs | ||

Broadcom Corp., Class A | Information Technology | Semiconductors | ||

MetLife, Inc. | Financials | Life & Health Insurance | ||

Cummins, Inc. | Industrials | Construction Machinery & Heavy Trucks | ||

Phillips 66 | Energy | Oil & Gas Refining & Marketing | ||

Gilead Sciences, Inc. | Health Care | Biotechnology | ||

General Motors Co. | Consumer Discretionary | Automobile Manufacturers | ||

Walgreen Co. | Consumer Staples | Drug Retail | ||

Cardinal Health, Inc. | Health Care | Health Care Services |

See your advisor or www.ivyinvestments.com for more information on the Fund’s most recently published Top 10 Equity Holdings.

| + | Cash equivalents are defined as highly liquid securities with maturities of less than three months. Cash equivalents may include U.S. Government Treasury bills, bank certificates of deposit, bankers’ acceptances, corporate commercial paper, short term investment funds and other money market instruments. |

| 18 | ANNUAL REPORT | 2019 |

Table of Contents

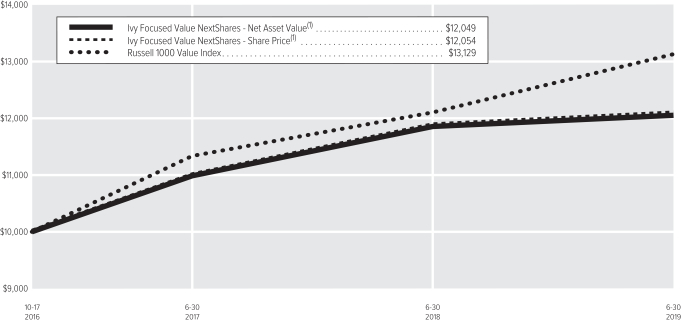

| COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT | IVY FOCUSED VALUE NEXTSHARES |

(UNAUDITED)

| (1) | The value of the investment in the Fund is impacted by the ongoing expenses of the Fund and assumes reinvestment of dividends and distributions. |

| Average Annual Total Return | ||||||||

| | Net Asset Value | | | Share Price | ||||

1-year period ended6-30-19 | 1.62% | 1.63% | ||||||

5-year period ended6-30-19 | — | — | ||||||

10-year period ended6-30-19 | — | — | ||||||

Since inception of Fund(2) through6-30-19 | 7.14% | 7.16% | ||||||

| (2) | 10-17-16 (the date on which shares were first acquired by shareholders). |

Past performance is not necessarily indicative of future performance. Indexes are unmanaged. The performance graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. Performance results may include the effect of expense reduction arrangements for some or all of the periods shown. If those arrangements had not been in place, the performance results for those periods would have been lower. The Fund’s performance at share price will differ from its results at net asset value (“NAV”). Share price returns are based on the Fund’s price at the close of market trading. If you trade your shares at another time during the day, your return may differ. For performance as of the most recent month end, including historical trading premiums/discounts relative to NAV, please refer to www.ivyinvestments.com.

| 2019 | ANNUAL REPORT | 19 |

Table of Contents

| SCHEDULE OF INVESTMENTS | IVY FOCUSED VALUE NEXTSHARES (in thousands) |

JUNE 30, 2019

| COMMON STOCKS | Shares | Value | ||||||

Communication Services |

| |||||||

Advertising – 4.0% |

| |||||||

Omnicom Group, Inc. | 4 | $ | 367 | |||||

|

| |||||||

Integrated Telecommunication Services – 3.8% |

| |||||||

Verizon Communications, Inc. | 6 | 348 | ||||||

|

| |||||||

Total Communication Services – 7.8% |

| 715 | ||||||

Consumer Discretionary |

| |||||||

Automobile Manufacturers – 4.2% |

| |||||||

General Motors Co. | 10 | 385 | ||||||

|

| |||||||

Total Consumer Discretionary – 4.2% |

| 385 | ||||||

Consumer Staples |

| |||||||

Drug Retail – 4.1% |

| |||||||

Walgreen Co. | 7 | 378 | ||||||

|

| |||||||

Total Consumer Staples – 4.1% |

| 378 | ||||||

Energy |

| |||||||

Oil & Gas Refining & Marketing – 11.0% |

| |||||||

PBF Energy, Inc., Class A | 18 | 548 | ||||||

Phillips 66 | 5 | 460 | ||||||

|

| |||||||

| 1,008 | ||||||||

|

| |||||||

Total Energy – 11.0% |

| 1,008 | ||||||

Financials |

| |||||||

Life & Health Insurance – 9.1% |

| |||||||

MetLife, Inc. | 9 | 465 | ||||||

Prudential Financial, Inc. | 4 | 364 | ||||||

|

| |||||||

| 829 | ||||||||

|

| |||||||

Mortgage REITs – 5.4% |

| |||||||

AGNC Investment Corp. | 29 | 495 | ||||||

|

| |||||||

| COMMON STOCKS(Continued) | Shares | Value | ||||||

Regional Banks – 4.0% |

| |||||||

Citizens Financial Group, Inc. | 10 | $ | 363 | |||||

|

| |||||||

Total Financials – 18.5% |

| 1,687 | ||||||

Health Care |

| |||||||

Biotechnology – 9.0% |

| |||||||

Amgen, Inc. | 2 | 361 | ||||||

Gilead Sciences, Inc. | 7 | 454 | ||||||

|

| |||||||

| 815 | ||||||||

|

| |||||||

Health Care Services – 4.1% |

| |||||||

Cardinal Health, Inc. | 8 | 374 | ||||||

|

| |||||||

Pharmaceuticals – 3.9% |

| |||||||

Bristol-Myers Squibb Co. | 8 | 359 | ||||||

|

| |||||||

Total Health Care – 17.0% |

| 1,548 | ||||||

Industrials |

| |||||||

Construction Machinery & Heavy Trucks – 5.1% |

| |||||||

Cummins, Inc. | 3 | 463 | ||||||

|

| |||||||

Total Industrials – 5.1% |

| 463 | ||||||

Information Technology |

| |||||||

IT Consulting & Other Services – 4.1% |

| |||||||

International Business Machines Corp. | 3 | 369 | ||||||

|

| |||||||

Semiconductors – 5.3% |

| |||||||

Broadcom Corp., Class A | 2 | 482 | ||||||

|

| |||||||

Technology Hardware, Storage & Peripherals – 7.9% |

| |||||||

Hewlett-Packard Co. | 17 | 360 | ||||||

NetApp, Inc. | 6 | 364 | ||||||

|

| |||||||

| 724 | ||||||||

|

| |||||||

Total Information Technology – 17.3% |

| 1,575 | ||||||

| COMMON STOCKS(Continued) | Shares | Value | ||||||

Materials |

| |||||||

Paper Packaging – 3.8% |

| |||||||

International Paper Co. | 8 | $ | 347 | |||||

|

| |||||||

Specialty Chemicals – 3.6% |

| |||||||

Chemours Co. (The) | 14 | 329 | ||||||

|

| |||||||

Total Materials – 7.4% |

| 676 | ||||||

Real Estate |

| |||||||

Health Care REITs – 3.0% |

| |||||||

Welltower, Inc. | 3 | 271 | ||||||

|

| |||||||

Total Real Estate – 3.0% |

| 271 | ||||||

Utilities |

| |||||||

Independent Power Producers & Energy Traders – 4.1% |

| |||||||

AES Corp. (The) | 22 | 371 | ||||||

|

| |||||||

Total Utilities – 4.1% |

| 371 | ||||||

TOTAL COMMON STOCKS – 99.5% |

| $ | 9,077 | |||||

(Cost: $9,209) | ||||||||

| SHORT-TERM SECURITIES | ||||||||

Money Market Funds – 0.7% |

| |||||||

State Street Institutional U.S. Government Money Market Fund 2.310% (A) | 63 | 63 | ||||||

|

| |||||||

TOTAL SHORT-TERM SECURITIES – 0.7% |

| $ | 63 | |||||

(Cost: $63) | ||||||||

TOTAL INVESTMENT SECURITIES – 100.2% |

| $ | 9,140 | |||||

(Cost: $9,272) | ||||||||

LIABILITIES, NET OF CASH AND OTHER ASSETS – (0.2)% |

| (21 | ) | |||||

NET ASSETS – 100.0% |

| $ | 9,119 | |||||

Notes to Schedule of Investments

| (A) | Rate shown is the annualized7-day yield at June 30, 2019. |

The following table is a summary of the valuation of the Fund’s investments by the fair value hierarchy levels as of June 30, 2019. See Note 3 to the Financial Statements for further information regarding fair value measurement.

| Level 1 | Level 2 | Level 3 | ||||||||||

Assets | ||||||||||||

Investments in Securities | ||||||||||||

Common Stocks | $ | 9,077 | $ | — | $ | — | ||||||

Short-Term Securities | 63 | — | — | |||||||||

Total | $ | 9,140 | $ | — | $ | — | ||||||

The following acronym is used throughout this schedule:

REIT = Real Estate Investment Trust

See Accompanying Notes to Financial Statements.

| 20 | ANNUAL REPORT | 2019 |

Table of Contents

| STATEMENTS OF ASSETS AND LIABILITIES | IVY NEXTSHARES |

AS OF JUNE 30, 2019

| (In thousands, except per share amounts) | Ivy Focused Energy NextShares | Ivy Focused Growth NextShares | Ivy Focused Value NextShares | |||||||||

ASSETS |

| |||||||||||

Investments in unaffiliated securities at value+ | $ | 5,952 | $ | 14,053 | $ | 9,140 | ||||||

Investments at Market Value | 5,952 | 14,053 | 9,140 | |||||||||

Investment securities sold receivable | — | — | 329 | |||||||||

Dividends and interest receivable | 5 | — | * | 22 | ||||||||

Receivable from affiliates | 21 | 27 | 27 | |||||||||

Total Assets | 5,978 | 14,080 | 9,518 | |||||||||

LIABILITIES | ||||||||||||

Investment securities purchased payable | — | — | 340 | |||||||||

Shareholder servicing payable | 2 | 2 | 2 | |||||||||

Accounting services fee payable | 10 | 9 | 10 | |||||||||

Other liabilities | 46 | 49 | 47 | |||||||||

Total Liabilities | 58 | 60 | 399 | |||||||||

Total Net Assets | $ | 5,920 | $ | 14,020 | $ | 9,119 | ||||||

NET ASSETS | ||||||||||||

Capital paid in (shares authorized – unlimited) | $ | 9,333 | $ | 8,854 | $ | 9,513 | ||||||

Accumulated earnings gain (loss) | (3,413 | ) | 5,166 | (394 | ) | |||||||

Total Net Assets | $ | 5,920 | $ | 14,020 | $ | 9,119 | ||||||

CAPITAL SHARES OUTSTANDING | 450 | 430 | 450 | |||||||||

NET ASSET VALUE PER SHARE | $ | 13.16 | $ | 32.60 | $ | 20.27 | ||||||

+COST | ||||||||||||

Investments in unaffiliated securities at cost | $ | 7,462 | $ | 9,436 | $ | 9,272 | ||||||

*Not shown due to rounding.

See Accompanying Notes to Financial Statements.

| 2019 | ANNUAL REPORT | 21 |

Table of Contents

| STATEMENTS OF OPERATIONS | IVY NEXTSHARES |

FOR THE YEAR ENDED JUNE 30, 2019

| (In thousands) | Ivy Focused Energy NextShares | Ivy Focused Growth NextShares | Ivy Focused Value NextShares | |||||||||

INVESTMENT INCOME |

| |||||||||||

Dividends from unaffiliated securities | $ | 92 | $ | 127 | $ | 376 | ||||||

Foreign dividend withholding tax | (2 | ) | — | * | — | |||||||

Interest and amortization from unaffiliated securities | 3 | 6 | 1 | |||||||||

Total Investment Income | 93 | 133 | 377 | |||||||||

EXPENSES | ||||||||||||

Investment management fee | 58 | 96 | 72 | |||||||||

Service fee | 25 | 25 | 25 | |||||||||

Custodian fees | 1 | 2 | 2 | |||||||||

Independent Trustees and Chief Compliance Officer fees | 1 | 1 | 1 | |||||||||

Accounting services fee | 115 | 115 | 115 | |||||||||

Professional fees | 45 | 53 | 49 | |||||||||

Intraday pricing fees | 6 | 6 | 6 | |||||||||

Listing fees | 11 | 11 | 11 | |||||||||

Printing fees | 10 | 11 | 10 | |||||||||

Transfer and dividend disbursing agent fees | 14 | 13 | 14 | |||||||||

Other | 4 | 4 | 4 | |||||||||

Total Expenses | 290 | 337 | 309 | |||||||||

Less: | ||||||||||||

Expenses in excess of limit | (224 | ) | (237 | ) | (233 | ) | ||||||

Total Net Expenses | 66 | 100 | 76 | |||||||||

Net Investment Income | 27 | 33 | 301 | |||||||||

REALIZED AND UNREALIZED GAIN (LOSS) | ||||||||||||

Net realized gain (loss) on: | ||||||||||||

Investments in unaffiliated securities | (1,034 | ) | 865 | (251 | ) | |||||||

Foreign currency exchange transactions | — | * | — | — | ||||||||

Net change in unrealized appreciation (depreciation) on: | ||||||||||||

Investments in unaffiliated securities | (1,603 | ) | 1,082 | 60 | ||||||||

Net Realized and Unrealized Gain (Loss) | (2,637 | ) | 1,947 | (191 | ) | |||||||

Net Increase (Decrease) in Net Assets Resulting from Operations | $ | (2,610 | ) | $ | 1,980 | $ | 110 | |||||

*Not shown due to rounding.

See Accompanying Notes to Financial Statements.

| 22 | ANNUAL REPORT | 2019 |

Table of Contents

| STATEMENTS OF CHANGES IN NET ASSETS | IVY NEXTSHARES |

| Ivy Focused Energy NextShares | Ivy Focused Growth NextShares | Ivy Focused Value NextShares | ||||||||||||||||||||||

| (In thousands) | Year ended 6-30-19 | Year ended 6-30-18 | Year ended 6-30-19 | Year ended 6-30-18 | Year ended 6-30-19 | Year ended 6-30-18 | ||||||||||||||||||

INCREASE (DECREASE) IN NET ASSETS | ||||||||||||||||||||||||

Operations: | ||||||||||||||||||||||||

Net investment income | $ | 27 | $ | 81 | $ | 33 | $ | 26 | $ | 301 | $ | 209 | ||||||||||||

Net realized gain (loss) on investments | (1,034 | ) | (831 | ) | 865 | 397 | (251 | ) | 815 | |||||||||||||||

Net change in unrealized appreciation (depreciation) | (1,603 | ) | 1,973 | 1,082 | 2,391 | 60 | (318 | ) | ||||||||||||||||

Net Increase (Decrease) in Net Assets Resulting from Operations | (2,610 | ) | 1,223 | 1,980 | 2,814 | 110 | 706 | |||||||||||||||||

Distributions to Shareholders From: | ||||||||||||||||||||||||

Net investment income | (82 | ) | (30 | ) | (183 | ) | ||||||||||||||||||

Net realized gains | — | (19 | ) | (114 | ) | |||||||||||||||||||

Accumulated earnings | (3 | ) | (614 | ) | (1,177 | ) | ||||||||||||||||||

(combined net investment income and net realized gains) | ||||||||||||||||||||||||

Total Distributions to Shareholders | (3 | ) | (82 | ) | (614 | ) | (49 | ) | (1,177 | ) | (297 | ) | ||||||||||||

Capital Share Transactions | — | 413 | — | — | — | 582 | ||||||||||||||||||

Net Increase (Decrease) in Net Assets | (2,613 | ) | 1,554 | 1,366 | 2,765 | (1,067 | ) | 991 | ||||||||||||||||

Net Assets, Beginning of Period | 8,533 | 6,979 | 12,654 | 9,889 | 10,186 | 9,195 | ||||||||||||||||||

Net Assets, End of Period | $ | 5,920 | $ | 8,533 | $ | 14,020 | $ | 12,654 | $ | 9,119 | $ | 10,186 | ||||||||||||

Undistributed net investment income | $ | 1 | $ | 13 | $ | 44 | ||||||||||||||||||

See Accompanying Notes to Financial Statements.

| 2019 | ANNUAL REPORT | 23 |

Table of Contents

| FINANCIAL HIGHLIGHTS | IVY NEXTSHARES |

FOR A SHARE OF CAPITAL STOCK OUTSTANDING THROUGHOUT EACH PERIOD

| Net Asset Value, Beginning of Period | Net Investment Income (Loss)(1) | Net Realized and Unrealized Gain (Loss) on Investments | Total from Investment Operations | Distributions From Net Investment Income | Distributions From Net Realized Gains | Total Distributions | ||||||||||||||||||||||

Ivy Focused Energy NextShares |

| |||||||||||||||||||||||||||

Year ended6-30-2019 | $ | 18.96 | $ | 0.07 | $ | (5.86 | ) | $ | (5.79 | ) | $ | (0.01 | ) | $ | — | $ | (0.01 | ) | ||||||||||

Year ended6-30-2018 | 16.42 | 0.19 | 2.54 | 2.73 | (0.19 | ) | — | (0.19 | ) | |||||||||||||||||||

Year ended6-30-2017(4) | 20.00 | (0.01 | ) | (3.57 | ) | (3.58 | ) | — | — | — | ||||||||||||||||||

Ivy Focused Growth NextShares |

| |||||||||||||||||||||||||||

Year ended6-30-2019 | 29.43 | 0.08 | 4.52 | 4.60 | (0.06 | ) | (1.37 | ) | (1.43 | ) | ||||||||||||||||||

Year ended6-30-2018 | 23.00 | 0.07 | 6.48 | 6.55 | (0.07 | ) | (0.05 | ) | (0.12 | ) | ||||||||||||||||||

Year ended6-30-2017(4) | 20.00 | 0.07 | 2.97 | 3.04 | (0.04 | ) | — | (0.04 | ) | |||||||||||||||||||

Ivy Focused Value NextShares |

| |||||||||||||||||||||||||||

Year ended6-30-2019 | 22.64 | 0.67 | (0.42 | ) | 0.25 | (0.74 | ) | (1.88 | ) | (2.62 | ) | |||||||||||||||||

Year ended6-30-2018 | 21.64 | 0.48 | 1.21 | 1.69 | (0.42 | ) | (0.27 | ) | (0.69 | ) | ||||||||||||||||||

Year ended6-30-2017(4) | 20.00 | 0.44 | 1.53 | 1.97 | (0.33 | ) | — | (0.33 | ) | |||||||||||||||||||

| (1) | Based on average weekly shares outstanding. |

| (2) | Based on net asset value. Total returns for periods less than one year are not annualized. |

| (3) | Ratios excluding expense waivers are included only for periods in which the Fund had waived or reimbursed expenses. |

| (4) | For the period from October 17, 2016 (commencement of operations of the Fund) through June 30, 2017. |

| (5) | Annualized. |

| 24 | ANNUAL REPORT | 2019 |

Table of Contents

| Net Asset Value, End of Period | Total Return(2) | Net Assets, End of Period (in millions) | Ratio of Expenses to Average Net Assets Including Expense Waiver | Ratio of Net Investment Income (Loss) to Average Net Assets Including Expense Waiver | Ratio of Expenses to Average Net Assets Excluding Expense Waiver(3) | Ratio of Net Investment Income (Loss) to Average Net Assets Excluding Expense Waiver(3) | Portfolio Turnover Rate | |||||||||||||||||||||||||

Ivy Focused Energy NextShares |

| |||||||||||||||||||||||||||||||

Year ended6-30-2019 | $ | 13.16 | -30.59 | % | $ | 6 | 0.95 | % | 0.41 | % | 4.21 | % | -2.85 | % | 29 | % | ||||||||||||||||

Year ended6-30-2018 | 18.96 | 16.76 | 9 | 0.95 | 1.06 | 3.62 | -1.61 | 44 | ||||||||||||||||||||||||

Year ended6-30-2017(4) | 16.42 | -17.89 | 7 | 0.95 | (5) | -0.09 | (5) | 4.16 | (5) | -3.30 | (5) | 18 | ||||||||||||||||||||