Table of Contents

As filed with the Securities and Exchange Commission on January 25, 2017.

Registration No. 333-206235

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 11

to

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Mauser Group B.V.1

(Exact Name of Registrant as Specified in its Charter)

| The Netherlands | 3412 | Not Applicable | ||

| (State or other jurisdiction of incorporation) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

Amstelveenseweg 760

1081 JK Amsterdam

The Netherlands

+31205043800

(Address, including Zip Code, and Telephone Number, including Area Code, of Registrant’s Principal Executive Offices)

Hans-Peter Schaefer

498 E Mac Ewen

Osprey, FL 34229

(941) 966-5294

(Name, Address, including Zip Code, and Telephone Number, including Area Code, of Agent for Service)

With copies to:

| Steven J. Slutzky, Esq. Debevoise & Plimpton LLP 919 Third Avenue New York, New York 10022 (212) 909-6000 | Marc D. Jaffe, Esq. Wesley C. Holmes, Esq. Latham & Watkins LLP 885 Third Avenue New York, New York 10022 (212) 906-1200 |

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ (Do not check if a smaller reporting company) | Smaller reporting company | ☐ | |||

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

| 1 | The registrant is currently named “Mauser Group B.V.” Following the date of this registration statement, but prior to the date of the preliminary prospectus, the registrant will be converted to a Dutch public limited liability company and renamed “Mauser Group N.V.” |

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted

Subject to Completion.

Preliminary Prospectus dated January 25, 2017.

PROSPECTUS

Shares

Mauser Group N.V.

Ordinary Shares

This is Mauser Group N.V’s initial public offering. We are selling of our ordinary shares.

We expect the public offering price to be between $ and $ per share. Currently, no public market exists for the ordinary shares. After pricing of the offering, we expect that the ordinary shares will trade on the New York Stock Exchange under the symbol “MSR.”

Currently, we are named Mauser Group B.V. and are a private company with limited liability (besloten vennootschap met beperkte aansprakelijkheid) incorporated under the laws of the Netherlands. Following the date of the preliminary prospectus, but prior to the completion of this offering, we intend to convert into a public company with limited liability (naamloze vennootschap), and our name will be Mauser Group N.V.

Investing in the ordinary shares involves risks that are described in the“Risk Factors” section beginning on page 23 of this prospectus.

| Per Share | Total | |||||||

Public offering price | $ | $ | ||||||

Underwriting discount(1) | $ | $ | ||||||

Proceeds, before expenses, to us | $ | $ | ||||||

| (1) | See “Underwriting” beginning on page 187 of this prospectus for additional information regarding underwriting compensation. |

The underwriters may also exercise their option to purchase up to an additional ordinary shares from us, at the public offering price, less the underwriting discount, for 30 days after the date of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares will be ready for delivery on or about , 2017.

| BofA Merrill Lynch | Citigroup | |||

| Credit Suisse | ||||

| Baird | Deutsche Bank Securities | Jefferies | ||

| BNP PARIBAS | ING | Natixis | Nomura | |||

The date of this prospectus is , 2017.

Table of Contents

| Page | ||||

| ii | ||||

| ii | ||||

| ii | ||||

| 1 | ||||

| 23 | ||||

Special Note RegardingForward-Looking Statements and Information | 49 | |||

| 51 | ||||

| 52 | ||||

| 53 | ||||

| 55 | ||||

| 56 | ||||

| 57 | ||||

| 58 | ||||

| 60 | ||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 62 | |||

| 122 | ||||

| 139 | ||||

Remuneration of the Members of the Board of Directors and Executive Officers | 148 | |||

| 152 | ||||

| 154 | ||||

| 157 | ||||

| 172 | ||||

| 174 | ||||

| 176 | ||||

| 187 | ||||

| 195 | ||||

| 196 | ||||

| 196 | ||||

| 197 | ||||

| F-1 | ||||

We and the underwriters have not authorized anyone to provide you with additional information or information different from that contained in this prospectus. We are offering to sell, and seeking offers to buy, our ordinary shares only in jurisdictions where offers and sales are permitted.

i

Table of Contents

We operate in an industry in which it is difficult to obtain precise industry and market information. We have obtained certain market and competitive position data in this prospectus directly or indirectly from publicly available information, industry publications and surveys, reports from government agencies, reports by market research firms and our own estimates based on our management’s knowledge of and experience in the market sectors in which we compete. In addition, in many cases we have made statements in this prospectus regarding our industry and our competitive position in this industry based on our experience and our own investigation of market conditions. Our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the captions “Risk Factors,” “Special Note Regarding Forward-Looking Statements and Information” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

TRADEMARKS, SERVICE MARKS AND BRAND NAMES

We use various trademarks, service marks and brand names, such as MAUSER, NCG and INFINITY SERIES that we deem particularly important to the advertising activities and operation of our business, and some of these marks are registered in certain jurisdictions. This prospectus also may refer to the trademarks, service marks and brand names of other companies. All trademarks, service marks and brand names cited in this prospectus are the property of their respective holders.

Unless the context otherwise indicates or requires, as used in this prospectus, (i) the terms “we,” “our,” “us,” “Mauser” and the “Company,” when used in the context of (a) the period before the CD&R Acquisition (as defined herein) refer to Mauser Holding GmbH and its consolidated subsidiaries and (b) the period after the CD&R Acquisition refer to Mauser Group B.V. (or at any time after the conversion into a public company described below, to Mauser Group N.V.) and its consolidated subsidiaries, (ii) the term “issuer” refers to Mauser Group B.V. (or at any time after the conversion into a public company described below, to Mauser Group N.V.) exclusive of its subsidiaries, (iii) the term “Predecessor” refers to Mauser Holding GmbH and its consolidated subsidiaries, (iv) the term “Successor” refers to Mauser Group B.V. (or at any time after the conversion into a public company described below, to Mauser Group N.V.) and its consolidated subsidiaries, (v) the term “First Lien Dollar Credit Facility” refers to our $422 million senior first lien secured dollar denominated term loan facility, (vi) the term “First Lien Euro Credit Facility” refers to our €445 million senior first lien secured euro denominated term loan facility, (vii) the term “First Lien Revolving Credit Facility” refers to our €150 million senior first lien secured revolving facility, (viii) the term “First Lien Capex Credit Facility” refers to our €50 million senior first lien secured initial acquisition/capex loan facility, (ix) the term “Second Lien Credit Facility” refers to our $402 million senior second lien secured term loan facility, (x) the term “First Lien Credit Facility” refers to the First Lien Dollar Credit Facility, the First Lien Euro Credit Facility, the First Lien Revolving Credit Facility and the First Lien Capex Credit Facility, collectively, (xi) the term “Senior Credit Facilities” refers to the First Lien Credit Facility and the Second Lien Credit Facility, collectively, (xi) the term “MEP I” refers to our program established in 2007 for certain employees and members of management to purchase shares in shares in Mauser Holding GmbH, (xii) “MEP II” refers to our program established in 2010 for certain employees and members of management to purchase shares in shares in Mauser Holding GmbH, (xiii) “MPP” refers to our program established in 2014 for certain employees and executives to indirectly purchase shares in CD&R Millennium Holdco 1 S.à r.l. and (xiv) “management equity plans” refers to MEP I, MEP II and MPP, collectively and as in effect from time to time.

ii

Table of Contents

When we refer to our “acquisitions,” we refer to any acquisition of an entity or the entry into new joint ventures where we have a controlling stake.When we refer to our “organic” growth, we refer to our growth (i) excluding the impact of all new acquisitions and dispositions made since the beginning of the prior year period for the periods presented and (ii) assuming a fixed currency exchange rate based on the exchange rate for the earlier period for the periods presented.

We are currently a private company with limited liability (besloten vennootschap met beperkte aansprakelijkheid) incorporated under the laws of the Netherlands named Mauser Group B.V. Following the date of the preliminary prospectus, but prior to the completion of this offering, we intend to convert into a public company with limited liability (naamloze vennootschap), and our name will be Mauser Group N.V.

Our fiscal year ends on December 31, and references to “fiscal” when used in reference to any twelve-month period ended December 31, refer to our fiscal years ended December 31. Unless otherwise stated or unless the context otherwise requires, all financial and operating measures in this prospectus are presented as of or for the year ended December 31, 2015. Unless otherwise stated or unless the context otherwise requires, all financial and operating measures in this prospectus for the year ended December 31, 2014 reflect our pro forma results for the year ended December 31, 2014. Our pro forma results for the year ended December 31, 2014 give effect to the CD&R Acquisition and the transactions related thereto as if they had been consummated on January 1, 2014. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Pro Forma Adjustments” for additional information.

The term “IFRS” refers to International Financial Reporting Standards as adopted by the International Accounting Standards Board or “IASB”. The financial statements of the Successor and the Predecessor contained in this prospectus have been prepared on the basis of IFRS.

iii

Table of Contents

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information you should consider before investing in our ordinary shares. You should read this entire prospectus, including the sections entitled “Risk Factors,” “—Summary Historical and Pro Forma Financial Information,” “Selected Consolidated Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and the related notes, before making an investment decision.

Our Company

Mauser is a leading global supplier of rigid packaging products and services for industrial use. We believe that we hold the number 1 or number 2 market position in the markets we serve based on revenue or capacity utilization in all of the categories of products and services we offer. The categories of products and services we provide represent an approximately €7 billion global market within the €15 billion global rigid industrial packaging industry, which management expects based on industry data to grow at a compound annual growth rate, or CAGR, of approximately 4.0% from 2014 through 2020. Our comprehensive product and service offering includes plastic, metal and fiber drums, intermediate bulk containers, or IBCs, and the collection, reconditioning and resale of used IBCs and plastic drums. We believe that this combination of products and services represents a differentiated business model and creates a unique value proposition that has allowed us to profitably (as measured by Adjusted EBITDA) grow faster than our end markets while generating significant cash. Our differentiated business model is based on a full lifecycle management approach whereby we develop and produce new containers with machinery that we design and build in-house and collect, recondition and resell used IBCs and plastic drums. Our revenue, consolidated result for the period and Adjusted EBITDA for the year ended December 31, 2015 were €1,371.8 million (representing an increase of 10.3% from the pro forma year ended December 31, 2014), €(13.7) million (representing an improvement of 60.9% from the pro forma year ended December 31, 2014) and €195.2 million (representing an increase of 20.4% from the pro forma year ended December 31, 2014), respectively. Our revenue, consolidated result for the period and Adjusted EBITDA for the nine months ended September 30, 2016 were €1,106.1 million (representing an increase of 5.4% from the nine months ended September 30, 2015), €15.0 million (representing an increase of 400% from the nine months ended September 30, 2015) and €167.3 million (representing an increase of 11.5% from the nine months ended September 30, 2015), respectively. For a reconciliation of Adjusted EBITDA to consolidated result for the period, see note 5 under “—Summary Historical and Pro Forma Financial Information” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Adjusted EBITDA.” As of September 30, 2016 we had €1,321.1 million of total debt outstanding.

We serve over 12,500 customers, including large blue chip companies such as ADM, BASF, Bayer, Brenntag, Cargill, Chevron, Dow Chemical, Evonik, Ecolab, ExxonMobil, Huntsman, Lubrizol, Momentive, Recofarma, Shell and Univar. We have low customer concentration with no single customer representing more than 5% of our revenue for the nine months ended September 30, 2016 and the top 20 customers accounting for only approximately 30% of revenue for the nine months ended September 30, 2016. We enjoy high customer loyalty and have had relationships with our top 20 customers averaging over 40 years with many of these customers purchasing from our entire product and service portfolio and across all of the geographies we serve.

To serve our customers, we currently operate 111 manufacturing facilities in 88 strategic locations across 18 countries. Many of our facilities are close in proximity to the factories of our major clients, enabling fast and cost-effective customer service. We believe that our global footprint, manufacturing expertise and over one hundred year history of innovation allow us to serve global customers on a local basis and produce uniform quality products worldwide that comply with strict regulations.

1

Table of Contents

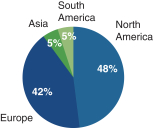

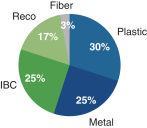

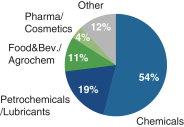

We have a diverse product and service mix measured by geography, product and end market, which is illustrated as a percentage of revenue for the year ended December 31, 2015 in the charts below.

| By Geography | By Product and Service | By End Market | ||

|  |  | ||

2

Table of Contents

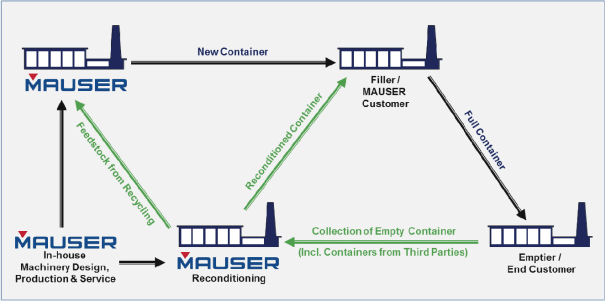

Our Differentiated Business Model and Unique Value Proposition

Our customers value environmentally sustainable products and partners that provide them with cost-effective packaging. Our lifecycle management approach addresses these needs through both the production of new containers as well as our ability to recondition and recycle used packaging. Our differentiated business model has allowed us to profitably (as measured by Adjusted EBITDA) grow our business while increasing our market share.

Our reconditioning services give our customers the option to have us collect used containers from them, including containers that were not produced by us. The used container is either washed or rebottled, depending on the quality of the returned container. In addition, we use recycled post-consumer resin, or PCR, from used containers that cannot be reconditioned as raw materials for our new products, including IBCs and plastic drums, rather than new and more expensive resin, which reduces our costs and drives incremental margin. By bundling new and reconditioned products we are able to offer our customers highly attractive cost alternatives. Our reconditioning business is our fastest growing, highest margin and highest return on capital segment.

We believe that our competitors would have difficulty replicating our full lifecycle management approach because reconditioning requires a large network, a significant number of permits that can be time consuming and expensive to obtain, significant intellectual property and technological expertise.

3

Table of Contents

Our Products and Services

IBC | Reconditioning | Plastic | Metal | Fiber | ||||||

|  |  |  |  | ||||||

2015 Revenue % of total | €364m 25% | €236m 17% | €437m 30% | €360m 25% | €41m 3% | |||||

Historic Mauser Organic Volume Growth 2011—2015 | 7.0% | 6.7% | 3.8% | 2.2% | 4.5% | |||||

Global Positioning | #2 | #1 | #1 | #2 | #2 | |||||

Product Portfolio | • Composite IBCs with HDPE bottle on either wood, plastic or steel composite pallets | • Worldwide network of collection and reconditioning services for IBCs and plastic drums | • Large drums (tight/open head) • Small drums/jerry cans • Specialty products | • Large drums • Small drums • Specialty products | • Fiber drums (lock ring drums, plastic liners for liquids) | |||||

End Markets | • Food and Beverage • Chemicals • Various intermediates for pharma / cosmetics | • Food and Beverage • Chemicals • Various intermediates for pharma / cosmetics | • Chemicals, lubricants, additives • Pharmaceuitical intermediaries • Food and Beverage • Oil derivatives, cleaner • Pesticides, herbicides | • Oil, paints, adhesives, textile colours, coatings, paper chemicals, dyes and pigments • Acids, lubricants, additives, pharma / cosmetics • Agrochemical products | • Chemicals, additives, hygenic markets • Food and Beverage • Pharma, cosmetics, intermediaries • Agriculture • Adhesives & sealants & rubber chemicals | |||||

4

Table of Contents

Our Competitive Strengths

We believe a number of strengths differentiate us from our competitors, including:

Global leader in industrial packaging with broad product and service offering and strategic global footprint

We are a leading supplier of rigid packaging products and services for industrial use. We believe that we hold the number 1 or number 2 market position in the markets we serve based on revenue or capacity utilization in all of the categories of products and services we offer. We believe our leading market positions are a result of our global presence, breadth and standardization of products, value-added service offerings and our differentiated business model. Our product portfolio includes plastic, metal and fiber drums and IBCs. We also operate the world’s largest reconditioning services business for the collection and reconditioning of used IBCs and plastic drums. Further, proximity to customers is important, as we believe delivery and collection of rigid bulk containers beyond a radius of approximately 200 miles significantly increases transportation costs. This limits the ability of smaller competitors to service customers beyond their own regional markets and makes it difficult for them to replicate our global footprint without significant capital expenditures. As a result, we believe our footprint provides us with a significant competitive advantage.

End markets and products with attractive growth prospects

Since 2009, we estimate that the global market for rigid industrial packaging has consistently grown in excess of addressable market GDP, and we expect this trend to continue. Management estimates based on industry data that sales in the relevant rigid industrial packaging market grew at a CAGR of 4.0% from 2009 to 2014 compared to addressable market GDP growth at a CAGR of 3.0% over the same period. We estimate that our end markets will grow at CAGRs of 2.1% to 4.4% from 2014 to 2020 compared to projected addressable market GDP growth at a CAGR of 3.0%. We believe that our differentiated business model has allowed and will continue to allow us to grow faster than our end markets.

We also believe that our strong position in the IBC and reconditioning markets strategically positions us to take advantage of the relatively higher growth of these product segments. Management estimates based on industry data that IBC and reconditioning products have more than quintupled their share of the rigid industrial packaging market, measured by the volume of chemicals filled, from less than 5% in 1995 to more than 25% today. As a result, we believe that IBC and reconditioning products will continue to outgrow the overall market.

Differentiated business model drives competitive advantage

We believe our differentiated business model and lifecycle management approach provides us with a distinct and sustainable competitive advantage. We were an innovator in creating the reconditioning market and we currently operate the world’s largest reconditioning services network for IBCs with 41 facilities in 12 countries. Our competitors would have difficulty creating a similar network due to the significant time and cost that would be required to build a large network, obtain permits, develop products and services, and obtain intellectual property and technological expertise. In addition, we have acquired a significant number of customer relationships and employee knowledge that are important in the implementation of the lifecycle management approach through our acquisitions and it would be difficult for a competitor to develop similar relationships and knowledge. Accordingly, we believe that our differentiated business model will continue to drive market share gains across our product portfolio and will lead to attractive profit growth.

Longstanding global relationships with large and diversified blue chip customer base

We have a diverse and global customer base, serving over 12,500 customers at approximately 17,000 locations. We have low customer concentration with no single customer representing more than 5% of revenue

5

Table of Contents

for the nine months ended September 30, 2016 and the top 20 customers accounting for only approximately 30% of revenue for the nine months ended September 30, 2016. Our customer base includes many leading global blue chip companies in the chemicals, petrochemicals / lubricants, food & beverage, agrochemicals, pharma / cosmetics and other end markets. We maintain strong relationships with our customers due to our ability to supply consistent, high quality products and services on a global scale. In addition, we believe that our customers appreciate our ability to develop customized products. As a result, we enjoy high customer loyalty and have had relationships with our top 20 customers averaging over 40 years. Many of our customers purchase from our entire product and service portfolio and across all of our geographies.

Focus on operational excellence

We have consistently demonstrated our ability to improve margins in our business through initiatives designed to achieve operational excellence. Since 2012, our management team has implemented several initiatives focused on supply chain improvements, savings on purchases, increased efficiency of our manufacturing process and targeted sales and marketing enhancements. For example, our Margin Acceleration Through Excellence initiative, or MAX, included optimizing raw material pass-through clauses in contracts, moving a substantial portion of our contracts from quarterly to monthly adjustments, optimizing product design and implementing sales initiatives focused on low margin customers. We also have established the Mauser Excellence Program, or MEP, which has included savings initiatives in sales and marketing, operations and purchasing and finance. In addition, our use of PCR from used containers that cannot be reconditioned for IBC pallets and plastic drums reduced our raw material costs for these products by approximately 50%. These operational excellence initiatives have contributed to our consolidated result for the period margin expansion of 0.8% and Adjusted EBITDA margin expansion of 2.6% from the year ended December 31, 2012 to the year ended December 31, 2015.

Strong growth, margin expansion and efficiency generation

From the year ended December 31, 2010 to the year ended December 31, 2015, our revenue has grown organically at a CAGR of 7.4% (8.9% including new acquisitions and dispositions). Since 2007, we have supplemented our organic growth with 33 acquisitions that were accretive to revenue and Adjusted EBITDA. From the year ended December 31, 2010 to the year ended December 31, 2015, consolidated result for the period has grown at a CAGR of 24.1% and Adjusted EBITDA has grown at a CAGR of 11.2%. Our focus on operational excellence, growth in higher margin products, continued sales efforts and disciplined expansion strategy, which is guided by strict near-term profitability and return requirements, has also led to improving profitability with consolidated result for the period going from €(54.3) million in the year ended December 31, 2010 to €(13.7) million in the year ended December 31, 2015. Over the same period, Adjusted EBITDA margins expanded from 11.3% in the year ended December 31, 2010 to 14.2% in the year ended December 31, 2015. See note 5 under “—Summary Historical and Pro Forma Financial Information” for a tabular display of our consolidated result for the years during this period.

We have also put considerable focus on efficient investment of capital, effective working capital control and operational discipline throughout the Company. A large proportion of our contracts include raw material cost pass-through clauses that allow us to pass fluctuations in key raw material prices on to our customers, which we believe helps to mitigate the impact of fluctuating commodity prices on earnings.

Proven track record of accretive acquisitions and disciplined capital deployment

We have a successful track record of identifying and acquiring complementary businesses at attractive valuations, integrating operations as well as customers into our global network and implementing cost savings initiatives. Since 2007, we have invested approximately €254.8 million, completing 33 transactions globally across various product segments, with a focus on the high growth areas of IBC and reconditioning. We believe we have generally been able to acquire smaller competitors at highly attractive pre-synergy valuation multiples and have created significant additional value through synergies from cost savings and cross-selling opportunities.

6

Table of Contents

We are often the partner of choice for smaller companies in the market due to our global market positions and reputation for producing quality products.

Entrepreneurial management team has reshaped the business portfolio and improved profitability

Our seasoned and entrepreneurial senior management team has a proven track record of success at the strategic, financial and operating levels. They average more than 20 years of industry experience and have significant knowledge in operating businesses and integrating acquisitions. Our senior management team has been pivotal in reshaping the business with the introduction of regional strategic business units, or SBUs, and global leadership for key functions such as sales, marketing and procurement.

We are led by our Chief Executive Officer, Hans-Peter Schaefer, who was appointed to his current role in February 2012, after 9 years with us. Mr. Schaefer has 33 years of experience in the chemicals industry, and was previously President and CEO of Schuetz Container Systems, which represents Schuetz’s North American operations, before joining us in 2004 as President and CEO of NCG. Mr. Schaefer is joined by our Chief Financial Officer, Bjoern Kreiter, who has been with us for more than 19 years and was promoted to Chief Financial Officer in November 2012. Our management team also includes five SBU managers as well as Senior Vice Presidents for Global Sales & Marketing, Global Procurement and Technology, each of whom has extensive international operational experience and strong relationships with our customers.

Our Growth Strategies

We believe that we are well positioned to capitalize on our market-leading positions to grow our business, enhance our margins and maximize our cash flows to drive shareholder returns. We seek to achieve this objective by executing on the following strategies:

Continue to drive profitable growth in our core markets

We believe that executing on our business strategy will further enhance our differentiated business model and lead us to achieve strong income and Adjusted EBITDA growth. We actively seek to further develop our existing customer relationships and take advantage of the positive growth dynamics within our highly attractive end markets. Our key end markets, the chemicals, petrochemicals / lubricants, food & beverage, agrochemicals and pharma / cosmetics end markets are expected to grow in excess of addressable market GDP growth, with projected growth at a CAGR of approximately 2.1% to 4.4% through 2020. As one of a small number of companies with a global footprint, we are confident in our ability to capture this growth across markets and geographies by leveraging our strong customer relationships and the breadth and quality of our product and service offerings.

Growth in excess of our core markets by increasing focus on most attractive product categories

We expect that the IBC and reconditioning markets will grow more rapidly than the overall rigid industrial packaging market in coming years due to increasing customer demand for IBC and reconditioning services. We believe that we are well positioned to take advantage of this growth by continuing to increase our focus on these product categories. We expect that customers will continue to demand integrated service solutions and sustainability, and that the IBC and reconditioning markets will grow as a result of this demand.

Drive market share gains through differentiated business model

We will continue to expand our lifecycle management capabilities which we believe will lead to market share increases across product categories and geographies and further establish our position as the partner of

7

Table of Contents

choice with our customers. Customers are increasingly focused on environmental sustainability and identifying lower cost packaging, and we intend to continue to build upon our lifecycle management offerings to continue to address these requirements. Our attractively priced product bundles combine new and reconditioned containers and we believe they will continue to appeal to cost-conscious customers.

Continue to pursue operational excellence to drive margin and cash flow

Continued operational improvement and excellence in execution is core to our strategy and will continue to be an essential component in further improving our earnings and cash flows. Our global marketing and sales department focuses on securing raw material pass-through clauses in contracts and other profitability enhancements by utilizing a proprietary market database and customer relationship management software to increase our margins. Our global procurement department is focused on continued supply chain improvements and reduction of supply risk across all regions, which we believe will result in increased earnings and cash flow growth.

Pursue acquisition opportunities

We will continue to pursue a disciplined acquisition strategy, targeting value enhancing acquisitions, some of which may be significant, to augment our product portfolio and geographic presence in order to better serve new and existing customers. The global rigid industrial packaging market consists of a small number of global companies and a large number of smaller, local companies and we believe that there is a significant opportunity for further consolidation. We maintain and monitor a list of potential acquisition targets and we believe we will continue to be able to identify and execute acquisitions at attractive valuations. As a result of our management’s experience in the industry, our acquisitions have primarily been identified and initiated by our management team outside of a formal sale processes and we believe we will be able to continue to identify acquisitions internally, benefiting from our strong network of contacts with smaller competitors.

Recent Developments

Acquisition of Total Container Group

On December 2, 2016, we completed the acquisition of Total Container Group Inc., or TCG for a purchase price of €49.1 million. The closing of our acquisition of TCG was conditioned upon TCG’s acquisition of the assets and liabilities of Effective Total Cleaning, LLC, Effective Specialty Transport, LLC, E4 Holdings, Inc. and Advantage IBC, LLC, which we collectively refer to as “Advantage.” After the consummation of the acquisition, TCG is our indirect wholly-owned subsidiary and TCG owns the assets and liabilities of Advantage. Advantage is an independent reconditioner, distributor and service provider of IBCs located in the Southeastern United States.

Repricing of First Lien Credit Facility

On October 5, 2016, we entered into the third amendment to the agreement that governs our First Lien Credit Facility. The third amendment refinanced the existing First Lien Euro Credit Facility, reducing the weighted average interest rate that we pay under the First Lien Credit Facility. As of September 30, 2016, we had approximately €931.3 million of outstanding obligations under our First Lien Credit Facility. Immediately prior to the third amendment, the weighted average interest rate for amounts outstanding under the First Lien Credit Facility was 4.72%, and immediately after the third amendment, it was 4.35%. For a description of the terms of our First Lien Credit Facility, see “Description of Certain Indebtedness—Senior Credit Facilities—First Lien Credit Facility.”

8

Table of Contents

Preliminary Year End Financial Information

Although our financial results for the year ended December 31, 2016 are not yet finalized the following information reflects our preliminary estimates based on information currently available to management:

| • | Our preliminary estimate of revenue for the year ended December 31, 2016 is between € million and € million, an increase of % to % compared to revenue for the year ended December 31, 2015. |

| • | Our preliminary estimate of consolidated result for the year ended December 31, 2016 is between € million and € million, an increase of % to % compared to consolidated result for the year ended December 31, 2015. |

| • | Our preliminary estimate of Adjusted EBITDA for the year ended December 31, 2016 is between € million and € million, an increase of % to % compared to Adjusted EBITDA for the year ended December 31, 2015. |

For a description of management’s use of Adjusted EBITDA, see note 5 under “—Summary Historical and Pro Forma Financial Information.” Below is a reconciliation of consolidated result for the period, the most comparable IFRS measure, to Adjusted EBITDA for the years ended December 31, 2016 and 2015.

| Successor | ||||||||||||

| Year Ended December 31, 2016 (low end of the estimated range) | Year Ended December 31, 2016 (high end of the estimated range) | Year Ended December 31, 2015 (actual) | ||||||||||

Consolidated result for the period | € | € | € | (13.7 | ) | |||||||

Income taxes | 8.6 | |||||||||||

Finance income | (12.3 | ) | ||||||||||

Finance costs | 99.3 | |||||||||||

Share of profit (loss) of investments accounted for using the equity method | (0.2 | ) | ||||||||||

Depreciation/amortization of and impairment losses on property, plant and equipment and intangible assets | 85.6 | |||||||||||

Total other adjustments(a) | 27.5 | |||||||||||

|

|

|

|

|

| |||||||

Adjusted EBITDA | 195.2 | |||||||||||

|

|

|

|

|

| |||||||

9

Table of Contents

| (a) | Total other adjustments relate to certain restructuring, severance and management equity plan costs, start up and acquisition costs, shutdown costs, consulting costs, transaction related costs and other income and expense items. We estimate that we will incur expenses of € million to € million (resulting in a € million to € million adjustment) in the year ended December 31, 2016. We incurred expenses of €28.3 million (resulting in a €27.5 million adjustment) in the year ended December 31, 2015 as a result of €16.5 million of advisor costs related to this offering, €3.5 million of consulting and advisor fees related to the June Dividend Recapitalization (as defined herein) and €2.5 million of service fees paid to CD&R. Below is a table showing our adjustments to calculate Adjusted EBITDA for the periods presented. |

| Successor | ||||||||||||

| Year Ended December 31, 2016 (low end of the estimated range) | Year Ended December 31, 2016 (high end of the estimated range) | Year Ended December 31, 2015 (actual) | ||||||||||

Restructuring, severance and management equity plan cost(i) | € | € | € | (2.5 | ) | |||||||

Start up and acquisition costs(ii) | (1.0 | ) | ||||||||||

Shutdown costs(iii) | (2.3 | ) | ||||||||||

Consulting costs(iv) | (0.2 | ) | ||||||||||

Transaction related costs(v) | (16.5 | ) | ||||||||||

Other expense items(vi) | (5.7 | ) | ||||||||||

Other income items(vii) | 0.8 | |||||||||||

|

|

|

|

|

| |||||||

Total other adjustments | (27.5 | ) | ||||||||||

|

|

|

|

|

| |||||||

| (i) | Restructuring, severance and management participation program costs include estimated costs related to management equity plans of € million to € million for the year ended December 31, 2016 and include costs related to management equity plans of €1.2 million for the year ended December 31, 2015. Other restructuring, severance, and management equity plan costs are related to facility consolidation initiatives and organizational changes, including severance for employees terminated in connection with these initiatives. |

| (ii) | Start up and acquisition costs are related to setting up new operations and joint ventures, including all necessary expenditures prior to the first recognition of revenue at these new operations and joint ventures. Start up and acquisition costs also include costs for due diligence and advisor costs in connection with startup operations. |

| (iii) | Shutdown costs are related to the closing of operations, including book value losses, clean-up initiatives and legacy rent. |

| (iv) | Consulting costs are the costs associated with external advice and expertise, including consultants for organizational improvements, IT optimizations, procurement support and HR support. |

| (v) | Transaction-related costs are primarily related to this offering. |

| (vi) | Other expense items relate to litigation settlements, regulatory cases and other miscellaneous items. |

| (vii) | Other income items are primarily related to book gains resulting from the sale of idle assets, adjustment of pension provisions resulting from legal changes or changes of retirement age, reimbursements and payments from insurance and releases of other provisions. |

10

Table of Contents

The preliminary financial data included in this prospectus has been prepared by, and is the responsibility of, the management of Mauser Group B.V. PricewaterhouseCoopers Aktiengesellschaft Wirtschaftsprüfungsgesellschaft has not audited, reviewed, compiled or performed any procedures with respect to the accompanying preliminary financial data. Accordingly, PricewaterhouseCoopers Aktiengesellschaft Wirtschaftsprüfungsgesellschaft does not express an opinion or any other form of assurance with respect thereto.

The preliminary financial information above is unaudited and may vary materially from our actual financial results for the year ended December 31, 2016. We have provided ranges for the preliminary estimated financial results described above because our financial closing procedures for the year ended December 31, 2016 are not complete. Our closing procedures for the year ended December 31, 2016 will not be complete, and our financial results for the year ended December 31, 2016 will not be publicly available, until after the expected completion of this offering. The preliminary financial information above reflects estimates based only on preliminary information available to us as of the date of this prospectus, has not been subject to our normal quarterly closing procedures and adjustments, which may be material, and is not a comprehensive statement of our financial results for the year ended December 31, 2016. Accordingly, you should not place undue reliance on these preliminary estimates. The preliminary financial information should not be viewed as a substitute for full interim financial statements prepared in accordance with IFRS. The estimates above are not necessarily indicative of any future period or any full fiscal year and should be read together with “Risk Factors,” “Special Note Regarding Forward-Looking Statements and Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “—Summary Historical and Pro Forma Financial Information,” “Selected Consolidated Financial Data” and our audited consolidated financial statements and related notes and unaudited condensed interim consolidated financial statements and related notes included elsewhere in this prospectus.

Conversion to Public Company With Limited Liability

Prior to the date of the preliminary prospectus, we intend to convert to a public company with limited liability (naamloze vennootschap) and rename our company “Mauser Group N.V.” In connection with this conversion, Holdco 2 will be issued of Mauser Group N.V.’s ordinary shares. The issuance of ordinary shares to Holdco 2 is intended to replicate a stock split under local law.

11

Table of Contents

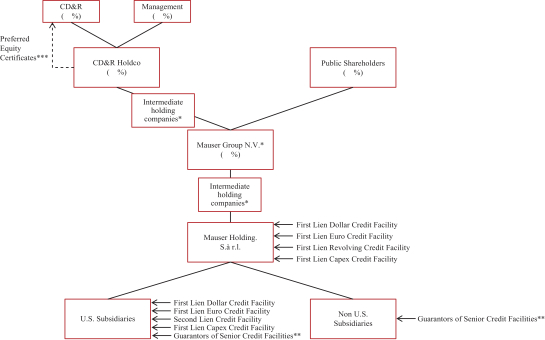

Our Structure

On July 31, 2014, funds managed by Clayton, Dubilier & Rice, LLC, or CD&R, completed the acquisition of all of our then outstanding ordinary shares from Dubai International Capital. We refer to this as the “CD&R Acquisition.”

The following chart reflects our organizational structure immediately following consummation of this offering (assuming no exercise of the underwriters’ option to purchase additional ordinary shares):

| * | Chart does not reflect intermediate holding companies, as inclusion of all intermediate holding companies would make the chart unwieldy and not useful to investors. |

| ** | Not all subsidiaries are guarantors of our Senior Credit Facilities. |

| *** | Through a series of intercompany loans and equity contributions, the proceeds from the issuance of the preferred equity certificates to affiliates of CD&R were transferred to certain of our operating subsidiaries. |

Ownership

Because of our ownership structure, we expect to be a “controlled company” for the purpose of the New York Stock Exchange, or the NYSE, upon the consummation of this offering.

Clayton, Dubilier & Rice, LLC

Founded in 1978, CD&R is a private equity firm composed of a combination of financial and operating executives pursuing an investment strategy predicated on building stronger, more profitable businesses. Since inception, CD&R has managed the investment of more than $21 billion in 65 businesses with an aggregate transaction value of approximately $100 billion.

CD&R has a significant track record of investing in market-leading industrial businesses. For example, CD&R has successfully exited its investment in Culligan, a global leader in water-treatment products and

12

Table of Contents

services for household and commercial applications and Diversey, a leading global manufacturer and distributor of commercial cleaning, sanitation and hygiene solutions. CD&R’s current portfolio includes Atkore International, a leading designer, manufacturer and distributor of electrical and metal products, NCI Building Systems, one of North America’s largest integrated manufacturers of metal products for the nonresidential building industries and Solenis, a specialty chemical supplier serving the paper and water treatment industries.

Risk Factors

An investment in our ordinary shares involves a high degree of risk. Any of the factors set forth under “Risk Factors” may limit our ability to successfully execute our business strategy, and you should carefully consider all of the information set forth in this prospectus in deciding whether to invest in our ordinary shares. These risks are discussed more fully under the caption “Risk Factors” and include, but are not limited to, the following:

| • | general economic conditions, particularly downturns in industrial activity; |

| • | our ability to successfully implement our business strategies, including achieving our growth objectives; |

| • | our dependency on the demand for products made by our customers, including those imported into and exported from Western Europe and the United States and transported in local markets; |

| • | fluctuations in the prices of our raw materials and energy prices; |

| • | our substantial indebtedness; and |

| • | our ability to maintain foreign private issuer status. |

Corporate Information

Mauser Group B.V. was formed as CD&R Millennium Holdco 3 B.V. on April 29, 2014 in connection with CD&R’s acquisition of the Mauser group of companies. On July 29, 2015, CD&R Millennium Holdco 3 B.V. was renamed Mauser Group B.V. We are a private company with limited liability(besloten vennootschap met beperkte aansprakelijkheid)incorporated under the laws of the Netherlands, and prior to the date of the preliminary prospectus, we intend to convert to a public company with limited liability (naamloze vennootschap). Our principal executive offices are located at Amstelveenseweg 760, 1081 JK Amsterdam, The Netherlands and our telephone number at that address is +31205043800. Our website is www.mausergroup.com. Information on, and which can be accessed through, our website is not a part of this prospectus nor is such information incorporated by reference in this prospectus.

13

Table of Contents

The Offering

Issuer | Mauser Group N.V. |

Ordinary shares offered by us | ordinary shares. |

Option to purchase additional ordinary shares from us | ordinary shares. |

Ordinary shares outstanding immediately after the offering | ordinary shares. |

Use of proceeds | We estimate that the net proceeds we will receive from the sale of of our ordinary shares in this offering, after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us, assuming the ordinary shares are sold at the midpoint of the price range set forth on the cover page of this prospectus, will be approximately $ million, or $ million if the underwriters exercise their option to purchase additional ordinary shares in full. |

| As described in “Use of Proceeds,” we intend to use the net proceeds of this offering (i) to redeem, repurchase or otherwise acquire or retire € million principal amount outstanding under our Second Lien Credit Facility plus accrued and unpaid interest of approximately € and a prepayment premium of € , (ii) to pay related fees and expenses, (iii) to pay CD&R a termination fee of € million in connection with the termination of the consulting agreement described under “Related Party Transactions” and (iv) to use the remaining proceeds, if any, for general corporate purposes. |

Distributions | We distributed €97.5 million to CD&R Millennium HoldCo 2 B.V., or Holdco 2, our sole shareholder, on June 24, 2015. The proceeds of that distribution were then distributed by Holdco 2 to CD&R Millennium HoldCo 1 S.à r.l, or Holdco 1, our indirect parent company. Holdco 1 used the proceeds of this distribution to (i) repay €16.4 million of preferred equity certificates issued to affiliates of CD&R by Holdco 1 and (ii) distribute €80.6 million to the shareholders of Holdco 1, including CD&R and the participants in the MPP. In addition, we distributed €87.5 million to Holdco 2 on October 29, 2015. The proceeds of this distribution have been distributed by Holdco 2 to Holdco 1. Holdco 1 used the proceeds of this distribution along with €0.5 million remaining from the distribution on June 24, 2015 to (i) repay €16.5 million of preferred equity certificates issued to affiliates of CD&R by Holdco 1 and (ii) distribute €71.5 million to the shareholders of Holdco 1, including CD&R and the participants in the MPP. We currently expect to retain future earnings, if any, for use in the operation and expansion of our business and the repayment of debt. See “Dividend Policy.” |

Proposed NYSE trading symbol | “MSR”. |

14

Table of Contents

Risk Factors | See “Risk Factors” and other information included in this prospectus for a discussion of factors that you should carefully consider before deciding to invest in our ordinary shares. |

The number of our ordinary shares to be outstanding immediately following this offering is based on ordinary shares outstanding as of , 2017 and excludes any ordinary shares to be reserved for issuance under our management benefit plans that may be adopted following the date of this prospectus, but prior to the completion of this offering.

Unless otherwise indicated, all information in this prospectus:

| • | includes ordinary shares of Mauser Group N.V. issued to Holdco 2 in connection with our conversion to a public company with limited liability; |

| • | assumes the issuance of ordinary shares in this offering; |

| • | assumes no exercise by the underwriters of their option to purchase additional ordinary shares; |

| • | assumes that the initial public offering price of our ordinary shares will be $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus; and |

| • | gives effect to the amendment to our articles of association to be adopted upon the completion of this offering. |

15

Table of Contents

Summary Historical and Pro Forma Financial Information

The following table summarizes certain summary historical and pro forma financial data. We have derived the summary statement of operations and cash flow data for the year ended December 31, 2015 (Successor) and the period from April 30, 2014 through December 31, 2014 (Successor) and the balance sheet data as of December 31, 2015 and 2014 (Successor) from the Successor’s audited consolidated financial statements included elsewhere in this prospectus. We have derived the summary statement of operations and cash flow data for the period from January 1, 2014 through July 31, 2014 (predecessor) and the year ended December 31, 2013 (Predecessor) from the Predecessor’s audited financial statements included elsewhere in this prospectus. We have derived the summary statement of operations and cash flow data for the nine months ended September 30, 2016 and 2015 (Successor) and the balance sheet data as of September 30, 2016 (Successor) from the Successor’s unaudited condensed interim consolidated financial statements included elsewhere in this prospectus, which includes all adjustments, consisting of normal recurring adjustments, that management considers necessary for a fair statement of the financial position and the results of operations for such periods. Results for the interim periods are not necessarily indicative of the results for the full year. We prepare our financial statements in accordance with IFRS as adopted by the IASB. Our historical results are not necessarily indicative of the results that should be expected in the future. We have derived the other financial data for the years ended December 31, 2011 and 2010 from the Predecessor’s unaudited financial information which has been prepared in accordance with IFRS as adopted by the IASB.

The summary consolidated financial data set forth below should be read together with our financial statements and the related notes, as well as “Selected Consolidated Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” included elsewhere in this prospectus.

| Successor(1) | Predecessor | |||||||||||||||||||||||||||||||||||

| Year Ended Dec. 31, 2015 | From Apr 30 through Dec. 31, 2014 | Year Ended Dec. 31, 2015 (pro forma)(2) | Nine Months Ended Sep. 30, 2016 | Nine Months Ended Sep. 30, 2015 | Nine Months Ended Sep. 30, 2016 (pro forma)(2) | From Jan 1 through July 31, 2014 | Year Ended Dec. 31, 2013 | |||||||||||||||||||||||||||||

(€ in millions, except share and per share data) | ||||||||||||||||||||||||||||||||||||

Statement of operations data: | ||||||||||||||||||||||||||||||||||||

Revenue | € | 1,371.8 | € | 523.7 | € | € | 1,106.1 | € | 1,049.0 | € | € | 720.0 | € | 1,146.4 | ||||||||||||||||||||||

Cost of sales | (1,136.7 | ) | (449.6 | ) | (896.5 | ) | (867.6 | ) | (601.5 | ) | (976.1 | ) | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Gross profit | 235.1 | 74.1 | 209.6 | 181.4 | 118.5 | 170.3 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Selling, general and administrative expenses | (130.5 | ) | (43.8 | ) | (107.8 | ) | (94.0 | ) | (69.1 | ) | (103.3 | ) | ||||||||||||||||||||||||

Other operating income | 0.4 | 0.2 | 0.1 | 0.1 | 2.0 | 4.0 | ||||||||||||||||||||||||||||||

Other operating expenses | (6.4 | ) | (0.4 | ) | (1.6 | ) | (3.1 | ) | (4.3 | ) | (11.6 | ) | ||||||||||||||||||||||||

Transaction related costs | (16.5 | ) | (27.0 | ) | (7.6 | ) | (10.5 | ) | (12.2 | ) | (2.8 | ) | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Operating result | 82.1 | 3.1 | 92.7 | 73.9 | 34.9 | 56.6 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Finance income | 12.3 | 7.1 | | 10.7 | | | 10.1 | | 6.5 | 18.6 | ||||||||||||||||||||||||||

Finance costs | (99.3 | ) | (38.1 | ) | (75.1 | ) | (68.5 | ) | (47.8 | ) | (76.1 | ) | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

16

Table of Contents

| Successor(1) | Predecessor | |||||||||||||||||||||||||||||||||||

| Year Ended Dec. 31, 2015 | From Apr 30 through Dec. 31, 2014 | Year Ended Dec. 31, 2015 (pro forma)(2) | Nine Months Ended Sep. 30, 2016 | Nine Months Ended Sep. 30, 2015 | Nine Months Ended Sep. 30, 2016 (pro forma)(2) | From Jan 1 through July 31, 2014 | Year Ended Dec. 31, 2013 | |||||||||||||||||||||||||||||

(€ in millions, except share and per share data) | ||||||||||||||||||||||||||||||||||||

Financial result | (87.0 | ) | (31.0 | ) | (64.4 | ) | (58.4 | ) | (41.3 | ) | (57.5 | ) | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Share of profit (loss) of investments accounted for using the equity method | (0.2 | ) | (0.6 | ) | 0.1 | (0.1 | ) | 0.1 | 0.6 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Result before taxes | (5.1 | ) | (28.5 | ) | 28.4 | 15.4 | (6.3 | ) | (0.3 | ) | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Income taxes | (8.6 | ) | (4.6 | ) | (13.4 | ) | (12.4 | ) | (12.7 | ) | (15.4 | ) | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Consolidated result for the period | € | (13.7 | ) | € | (33.1 | ) | € | 15.0 | € | 3.0 | € | (19.0 | ) | € | (15.7 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Thereof attributable to: | ||||||||||||||||||||||||||||||||||||

Owners of the parent | (18.0 | ) | (33.9 | ) | 12.6 | (0.5 | ) | (21.0 | ) | (17.3 | ) | |||||||||||||||||||||||||

Non–controlling interests | 4.3 | 0.8 | 2.4 | 3.5 | 2.0 | 1.6 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

| (13.7 | ) | (33.1 | ) | 15.0 | 3.0 | (19.0 | ) | (15.7 | ) | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Consolidated result for the period per share: | ||||||||||||||||||||||||||||||||||||

Basic and diluted | ||||||||||||||||||||||||||||||||||||

Weighted average ordinary shares used in computing consolidated result for the period per share: | ||||||||||||||||||||||||||||||||||||

Basic and diluted | ||||||||||||||||||||||||||||||||||||

| Successor | ||||||||||||

| As of September 30, 2016 | As of December 31, 2015 | As of September 30, 2016 (pro forma)(2) | ||||||||||

| (€ in millions) | ||||||||||||

Balance sheet data: | ||||||||||||

Cash and cash equivalents | € | 92.9 | € | 78.6 | € | |||||||

Total assets | 1,953.0 | 1,828.5 | ||||||||||

Long-term borrowings | 1,254.5 | 1,178.6 | ||||||||||

Total equity | 18.8 | 19.2 | ||||||||||

| Successor(1) | Predecessor | |||||||||||||||||||||||||||

| Year Ended December 31, 2015 | From April 30 through December 31, 2014 | Nine Months Ended September 30, 2016 | Nine Months Ended September 30, 2015 | From January 1 through July 31, 2014 | Year Ended December 31, 2013 | |||||||||||||||||||||||

| (€ in millions) | ||||||||||||||||||||||||||||

Cash flow data:(3) | ||||||||||||||||||||||||||||

Cash generated from operating activities | € | 236.2 | € | 10.9 | € | 101.9 | € | 105.6 | € | 39.7 | € | 83.5 | ||||||||||||||||

Cash generated from (used in) investing activities | (53.7 | ) | (398.4 | ) | (101.6 | ) | (51.0 | ) | (1.6 | ) | (56.4 | ) | ||||||||||||||||

Cash generated from (used in) financing activities | (177.5 | ) | 457.4 | 21.0 | | (71.4 | ) | (49.9 | ) | (33.1 | ) | |||||||||||||||||

17

Table of Contents

| Successor(1) | Predecessor | |||||||||||||||||||||||||||||||||||||

| Year Ended December 31, 2015 | From April 30 through December 31, 2014 | Nine Months Ended September 30, 2016 | Nine Months Ended September 30, 2015 | From January 1 through July 31, 2014 | Year Ended December 31, 2013 | Year Ended December 31, 2012(4) | Year Ended December 31, 2011 | Year Ended December 31, 2010 | ||||||||||||||||||||||||||||||

| (€ in millions) | ||||||||||||||||||||||||||||||||||||||

Other financial | ||||||||||||||||||||||||||||||||||||||

Consolidated result for the period | € | (13.7 | ) | € | (33.1 | ) | € | 15.0 | € | 3.0 | € | (19.0 | ) | € | (15.7 | ) | € | (20.4 | ) | € | (41.1 | ) | € | (57.6 | ) | |||||||||||||

Adjusted EBITDA(5) | € | 195.2 | € | 65.9 | € | 167.3 | € | 150.0 | € | 96.1 | € | 142.4 | € | 133.3 | € | 124.9 | € | 115.0 | ||||||||||||||||||||

Consolidated result for the period margin | (1.0 | %) | (6.3 | %) | 1.4 | % | 0.3 | % | (2.6 | %) | (1.4 | %) | (1.8 | %) | (3.7 | %) | (5.6 | %) | ||||||||||||||||||||

Adjusted EBITDA margin(5) | 14.2 | % | 12.6 | % | 15.1 | % | 14.3 | % | 13.3 | % | 12.4 | % | 11.7 | % | 11.4 | % | 11.3 | % | ||||||||||||||||||||

Capital expenditures | (45.0 | ) | (25.8 | ) | (25.2 | ) | (30.4 | ) | (25.4 | ) | (51.9 | ) | (50.1 | ) | (49.0 | ) | (38.1 | ) | ||||||||||||||||||||

Dispositions of fixed assets | 3.8 | 0.5 | 1.6 | 1.5 | 4.7 | 6.1 | 6.1 | 5.7 | 2.6 | |||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

| (1) | The Successor period started on April 30, 2014 when Mauser Group B.V. was incorporated. For the Successor period from April 30, 2014 to July 31, 2014, there was no operating activity. Operations at the Successor commenced on July 31, 2014 as a result of the CD&R Acquisition. |

| (2) | The statement of operations data for the year ended December 31, 2015 and the nine months ended September 30, 2016 and balance sheet data as of September 30, 2016 are presented on a pro forma basis to give effect to the sale of ordinary shares in this offering assuming no exercise of the underwriters’ option to purchase additional ordinary shares and assuming that the initial public offering price of our ordinary shares will be $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus (and after deducting estimated underwriting discounts and commissions and offering expenses payable by us) and the use of the net proceeds therefrom as described in “Use of Proceeds,” as if each of these transactions occurred on January 1, 2015, in the case of the statements of operations data, or September 30, 2016, in the case of the balance sheet data. |

The statement of operations data presented on a pro forma basis for the year ended December 31, 2015 and the nine months ended September 30, 2016 includes an adjustment in the amount of € million and € million, respectively, to decrease finance costs as a result of the repayment of principal under our Second Lien Credit Facility as described under “Use of Proceeds.” Income taxes have been adjusted for both periods to reflect the above noted statement of operations adjustments.

The balance sheet data presented on a pro forma basis as of September 30, 2016 includes a change of € million in cash and cash equivalents, a change of € million in total assets, a change of € million in long-term borrowings and a change of € million in total equity. An adjustment was recorded to increase cash and cash equivalents in the amount of € million, which reflects the net proceeds from this offering, based on an assumed initial public offering price of $ per share, which is the mid-point of the price range set forth on the cover of this prospectus. An adjustment was recorded to decrease cash and cash equivalents in the amount of € million to reflect (a) the payment of the consulting agreement termination fee to CD&R and (b) the repayment of a portion of principal and the payment of accrued interest and a prepayment premium under the Second Lien Credit Facility. An adjustment was recorded to decrease long-term borrowings in the amount of € million to reflect the repayment of principal and the write-off of a portion of capitalized transaction costs under the Second Lien Credit Facility upon the consummation of this offering, as further described under “Use of Proceeds”.

18

Table of Contents

| For the year ended December 31, 2015 | Offering adjustments | Pro Forma | ||||||||||

(€ in millions, except share and per share data) | ||||||||||||

Operating result | 82.1 | |||||||||||

|

|

|

|

|

| |||||||

Finance income | 12.3 | |||||||||||

Finance costs (a) | (99.3 | ) | ||||||||||

|

|

|

|

|

| |||||||

Financial result | (87.0 | ) | ||||||||||

|

|

|

|

|

| |||||||

Share of profit (loss) of investments accounted for using the equity method | (0.2 | ) | ||||||||||

|

|

|

|

|

| |||||||

Result before taxes | (5.1 | ) | ||||||||||

|

|

|

|

|

| |||||||

Income taxes (b) | (8.6 | ) | ||||||||||

|

|

|

|

|

| |||||||

Consolidated result for the period | (13.7 | ) | ||||||||||

|

|

|

|

|

| |||||||

Thereof attributable to: | ||||||||||||

Owners of the parent | (18.0 | ) | ||||||||||

Non-controlling interests | 4.3 | |||||||||||

|

| |||||||||||

| (13.7 | ) | |||||||||||

|

| |||||||||||

Consolidated result for the period per share: | ||||||||||||

Basic and diluted (c) | ||||||||||||

Weighted average ordinary shares used in computing consolidated result for the period per share: | ||||||||||||

Basic and diluted (c) | ||||||||||||

| For the nine months ended September 30, 2016 | Offering adjustments | Pro Forma | ||||||||||

| (€ in millions, except share and per share data) | ||||||||||||

Operating result | 92.7 | |||||||||||

|

|

|

|

|

| |||||||

Finance income | 10.7 | |||||||||||

Finance costs (a) | (75.1 | ) | ||||||||||

|

|

|

|

|

| |||||||

Financial result | (64.4 | ) | ||||||||||

|

|

|

|

|

| |||||||

Share of profit (loss) of investments accounted for using the equity method | 0.1 | |||||||||||

|

|

|

|

|

| |||||||

Result before taxes | 28.4 | |||||||||||

|

|

|

|

|

| |||||||

Income taxes (b) | (13.4 | ) | ||||||||||

|

|

|

|

|

| |||||||

Consolidated result for the period | 15.0 | |||||||||||

|

|

|

|

|

| |||||||

Thereof attributable to: | ||||||||||||

Owners of the parent | 12.6 | |||||||||||

Non-controlling interests | 2.4 | |||||||||||

| 15.0 | ||||||||||||

Consolidated result for the period per share: | ||||||||||||

Basic and diluted (c) | ||||||||||||

Weighted average ordinary shares used in computing consolidated result for the period per share: | ||||||||||||

Basic and diluted (c) | ||||||||||||

The statement of operations data presented on a pro forma basis for the year ended December 31, 2015 and the nine months ended September 30, 2016 includes the following:

| (a) | An adjustment to finance costs in the amount of € million and € million, respectively, to reflect the repayment of principal under our Senior Credit Facilities as if such repayment had occurred on January 1, 2015. This assumed interest rates for the First Lien Dollar Credit Facility (USD) (4.5%), (initial) First Lien Euro Credit Facility (EUR) (4.75%), (amended) First Lien Euro Credit Facility (EUR) (5.50%) and Second Lien Credit Facility (USD) (8.75%). |

19

Table of Contents

| (b) | An adjustment to income tax expense for the items noted above, calculated at a weighted statutory tax rate of 30%. |

| (c) | An adjustment to the weighted average shares outstanding used to compute basic and diluted consolidated result for the period per share to give effect to the following, as if such issuances had occurred on January 1, 2015: |

| • | ordinary shares issued to the public in connection with the consummation of the offering; and |

| • | reflects the ordinary shares issued to Holdco 2 in connection with this offering as described in “—Conversion to Public Company with Limited Liability.” |

| (3) | Our historical statements of cash flows have been significantly impacted by certain restructuring, severance and management equity plan costs, startup costs, acquisition costs, shutdown costs, consulting costs and other income and expense items. For a discussion of these items see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Cash Flows” elsewhere in this prospectus. |

| (4) | The Predecessor’s statement of operations data for the year ended December 31, 2012 includes revenue and related expenses from the disposition of the assets related to the steel reconditioning activities of Mauser Holding USA, LLC, National Container Group, LLC, American Container Net, LLC, ACN-Pittsburgh, LLC, ACN-Providence, LLC, ACN-Logistics, LLC, ACNBurbank, LLC, and ACN-Richmond, LLC that were disposed of during the year ended December 31, 2012. As a result, €11.4 million was recognized in the Predecessor’s operating result for the year ended December 31, 2012, which may not be comparable to the other periods presented. |

| (5) | Adjusted EBITDA and Adjusted EBITDA margin are financial metrics that are not calculated in accordance with IFRS. These non-IFRS metrics should not be considered as alternatives to consolidated result for the period, operating result, revenue, cash generated from operating activities or any other performance measures derived in accordance with IFRS as measures of operating performance or operating cash flows or liquidity. We believe that these non-IFRS metrics are metrics commonly used by investors to evaluate our performance and that of our competitors. We further believe that the disclosure of these non-IFRS metrics is useful to investors, as these non-IFRS metrics form the basis of how our executive team and board of directors evaluate our performance. By disclosing these non-IFRS metrics, we believe that we create for investors a greater understanding of, and an enhanced level of transparency into, some of the means by which our management team operates and evaluates us and facilitates comparisons of the current period’s results with prior periods. |

Our management uses Adjusted EBITDA and Adjusted EBITDA margin as measures of operating performance and in communications with our board of directors concerning our financial performance. Adjusted EBITDA and Adjusted EBITDA margin eliminate items that, management believes, have less bearing on our operating performance, thereby highlighting trends in our core business which may not otherwise be apparent. Management believes that Adjusted EBITDA and Adjusted EBITDA margin also include certain items that are expected to have an impact on our financial position and results of operations in the future. We also present Adjusted EBITDA and Adjusted EBITDA margin in this prospectus as supplemental performance measures because we believe that these measures provide investors and securities analysts with important supplemental information with which to evaluate our performance and to enable them to assess our performance on the same basis as management.

Although these non-IFRS metrics are measurements frequently used by investors and securities analysts in their evaluations of companies, each of these non-IFRS metrics has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for, or more meaningful than, amounts determined in accordance with IFRS.

Some of these limitations are that Adjusted EBITDA and Adjusted EBITDA margin do not reflect income taxes, finance income, finance costs, share of profit (loss) of investments accounted for using the equity method, depreciation and amortization of and impairment losses on property, plant and equipment and intangible assets, certain restructuring, severance and management equity plan costs, start up and acquisition costs, shutdown costs, consulting costs, transaction related costs and other income and expense items. In addition, other companies in our or related industries may calculate these measures differently from the way we do, limiting their usefulness as comparative measures.

Management compensates for the inherent limitations associated with these non-IFRS metrics through disclosure of such limitations, presentation of our financial statements in accordance with IFRS and a reconciliation of Adjusted EBITDA to the most directly comparable IFRS measure, consolidated result for the period.

Adjusted EBITDA represents consolidated result for the period before income taxes, finance income, finance costs, share of profit (loss) of investments accounted for using the equity method, depreciation and amortization of and impairment losses on property, plant and equipment and intangible assets, certain restructuring, severance and management equity plan costs, start up and acquisition costs, shutdown costs, consulting costs, transaction related costs and other income and expense items. Adjusted EBITDA margin represents Adjusted EBITDA as a percentage of revenue.

Each of the periods presented may include the impact of new acquisitions or dispositions during the period. As a result, each period may not be comparable to the other periods presented.

20

Table of Contents

The following table presents a reconciliation of consolidated result for the period, the most comparable IFRS measure, to Adjusted EBITDA for the periods presented:

| Successor(1) | Predecessor | |||||||||||||||||||||||||||||||||||||||||||

| Year Ended Dec. 31, 2015 | From Apr. 30 through Dec. 31, 2014 | Nine Months Ended Sep. 30, 2016 | Nine Months Ended Sep. 30, 2015 | From Jan. 1 through July 31, 2014 | Year Ended Dec. 31, 2013 | Year Ended Dec. 31, 2012 | Year Ended Dec. 31, 2011 | Year Ended Dec. 31, 2010 | ||||||||||||||||||||||||||||||||||||

(€ in millions) | ||||||||||||||||||||||||||||||||||||||||||||

Consolidated result for the period | € | (13.7 | ) | € | (33.1 | ) | € | 15.0 | € | 3.0 | € | (19.0 | ) | € | (15.7 | ) | € | (20.4 | ) | € | (41.1 | ) | € | (54.3 | ) | |||||||||||||||||||

Income taxes | 8.6 | 4.6 | 13.4 | 12.4 | 12.7 | 15.4 | 14.4 | 5.3 | 5.2 | |||||||||||||||||||||||||||||||||||

Finance income | (12.3 | ) | (7.1 | ) | (10.7 | ) | (10.1 | ) | (6.5 | ) | (18.6 | ) | (14.8 | ) | (39.1 | ) | (30.3 | ) | ||||||||||||||||||||||||||

Finance costs | 99.3 | 38.1 | 75.1 | 68.5 | 47.8 | 76.1 | 81.3 | 118.7 | 107.0 | |||||||||||||||||||||||||||||||||||

Share of (profit) loss of investments accounted for using the equity method | 0.2 | 0.6 | (0.1 | ) | 0.1 | (0.1 | ) | (0.6 | ) | 0.7 | (0.1 | ) | (0.2 | ) | ||||||||||||||||||||||||||||||

Depreciation/amortization of and impairment losses on property, plant and equipment and intangible assets | 85.6 | 29.5 | 60.2 | 59.8 | 33.9 | 60.8 | 63.1 | 61.4 | 62.5 | |||||||||||||||||||||||||||||||||||

Total other adjustments(a) | 27.5 | 33.3 | 14.4 | 16.3 | 27.3 | 25.0 | 9.0 | 19.8 | 25.1 | |||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||

Adjusted EBITDA | 195.2 | 65.9 | 167.3 | 150.0 | 96.1 | 142.4 | 133.3 | 124.9 | 115.0 | |||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||

21

Table of Contents