Table of Contents

As filed with the Securities and Exchange Commission on October 28, 2016

Registration Statement No. 333-206667

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3

to

Form F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

IC POWER PTE. LTD.

(Exact name of registrant as specified in its charter)

| Singapore | (Company Registration No. 201511865D) | Not applicable | ||

| 4911 | ||||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

1 Temasek Avenue

# 36-01

Millenia Tower

Singapore 039192

Telephone: +65 6351 1780

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

C T Corporation System

111 Eighth Avenue

New York, New York 10011

Telephone: + 1 212 894 8940

(Address, including zip code, and telephone number, including area code, of registrant’s agent for service of process)

Copies to:

Scott V. Simpson James A. McDonald Skadden, Arps, Slate, Meagher & Flom (UK) LLP 40 Bank Street London E14 5DS United Kingdom Telephone: +44 20 7519 7000 Facsimile: +44 20 7519 7070 | Mark Bagnall John Vetterli White & Case LLP 200 Biscayne Blvd. Suite 4900 Miami, Florida 33131 Telephone: 305 371 2700 Facsimile: 305 358 5744 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 (the “Securities Act”), check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

| ||||

Title of each class of securities to be registered | Proposed maximum aggregate offering price(1)(2) | Amount of registration fee(3) | ||

Ordinary shares, no par value | $100,000,000 | $11,620 | ||

| ||||

| ||||

| (1) | Includes additional ordinary shares that may be sold upon exercise of a purchase option to be granted to the underwriters. |

| (2) | Estimated solely for the purposes of calculating the registration fee pursuant to Rule 457(o) of the Securities Act of 1933. |

| (3) | Previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus Dated ,2016

PROSPECTUS

Ordinary Shares

This is the initial public offering of ordinary shares, no par value, of IC Power Pte. Ltd., or IC Power, a private company limited by shares incorporated under the laws of Singapore. We expect the public offering price to be between $ and $ per ordinary share.

Prior to this offering, there has been no public market for our ordinary shares. We are in the process of applying to list our ordinary shares on the New York Stock Exchange, or the NYSE, under the symbol “ICP.”

Upon the completion of this offering, and assuming an initial public offering price equal to the mid-point of the price range set forth above, Kenon Holdings Ltd. (NYSE: KEN; TASE: KEN), our current sole shareholder, will continue to control approximately % of the aggregate voting power of our ordinary shares, or approximately % if the underwriters exercise in full their option to purchase up to additional ordinary shares from us. For further information, see “Principal Shareholders.”

Investing in our ordinary shares involves risks. See “Risk Factors” beginning on page 42 to read about certain factors you should consider before purchasing our ordinary shares.

Per Share | Total | |||||||

Initial public offering price | $ | $ | ||||||

Underwriting discounts and commissions(1) | $ | $ | ||||||

Proceeds to us, before expenses | $ | $ | ||||||

| (1) | See “Underwriting” for a description of compensation payable to the underwriters. |

We have agreed to allow the underwriters to purchase up to an additional ordinary shares from us, at the public offering price, less the underwriting discounts and commissions, within days from the date of this prospectus.

The underwriters expect to deliver our ordinary shares to purchasers against payment on or about , 2016.

Neither the U.S. Securities and Exchange Commission, or the SEC, nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| BofA Merrill Lynch | Credit Suisse |

| Goldman, Sachs & Co. | UBS Investment Bank | |

| HSBC | Scotiabank | Credicorp Capital | ||

The date of this prospectus is , 2016.

Table of Contents

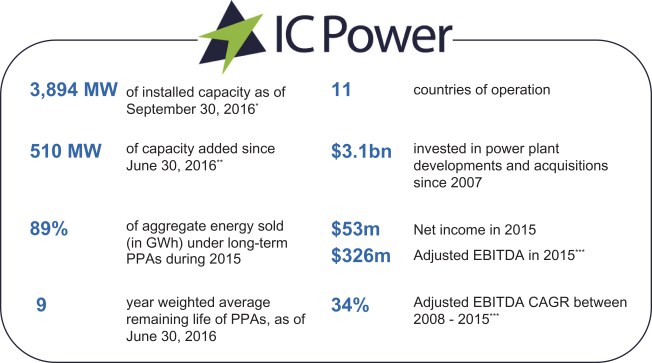

| * | 3,114 MW of proportionate capacity |

| ** | 383 MW of proportionate capacity |

| *** | Adjusted EBITDA in 2015 was $326 million, compared to $41 million in 2008. Adjusted EBITDA is a non-IFRS measure. For a reconciliation of our net income to our Adjusted EBITDA, see “Summary Consolidated Financial and Other Information—Key Financial and Other Operating Information – IC Power and ICP.” |

As of June 30, 2016

| (1) | Includes 193 MW capacity from Las Flores. |

| (2) | Includes 18 MW currently under operation and a cogeneration plant, which is expected to have capacity of 140 MW. |

| (3) | Excludes Agua Clara, a 50 MW wind project, which is expected to commence commercial operations in early 2018. |

Table of Contents

| ii | ||||

| ii | ||||

| iv | ||||

| iv | ||||

| v | ||||

| v | ||||

| v | ||||

| xi | ||||

| 1 | ||||

| 18 | ||||

| 21 | ||||

UNAUDITED PRO FORMA CONDENSED CONSOLIDATED FINANCIAL INFORMATION | 35 | |||

| 42 | ||||

| 80 | ||||

| 83 | ||||

| 84 | ||||

| 84 | ||||

| 86 | ||||

| 87 | ||||

| 88 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 99 | |||

| 169 | ||||

| 183 | ||||

| 278 | ||||

| 285 | ||||

| 286 | ||||

| 288 | ||||

| 308 | ||||

| 310 | ||||

| 315 | ||||

| 326 | ||||

| 326 | ||||

| 326 | ||||

| 327 | ||||

| F-1 |

Neither we nor the underwriters (nor any of our or their respective affiliates) have authorized anyone to provide any information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we may have referred you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. If anyone provides you with additional, different, or inconsistent information, you should not rely on it. Neither we nor the underwriters (nor any of our or their respective affiliates) are making an offer to sell the ordinary shares in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or any sale of the ordinary shares. Our business, financial condition, results of operations and liquidity may have changed since the date on the front cover of this prospectus.

i

Table of Contents

Neither we nor any of the underwriters have taken any action to permit a public offering of the ordinary shares outside the United States or to permit the possession or distribution of this prospectus outside the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about and observe any restrictions relating to the offering of the ordinary shares and the distribution of this prospectus outside the United States.

Until , 2016 (the 25th day after the date of this prospectus), all dealers that buy, sell or trade in our ordinary shares, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealer’s obligation to deliver a prospectus when acting as underwriter and with respect to their unsold allotment or subscription.

As described under “Corporate Formation and Reorganization,” we were formed in May 2015, under the name IC Power Pte. Ltd., or IC Power, to serve as the holding company of I.C. Power Asia Development Ltd. (formerly known as I.C. Power Ltd.), or ICP, and its businesses. On March 17, 2016, Kenon, our current sole shareholder, effected an internal reorganization pursuant to which it transferred all of its equity interests in its wholly-owned subsidiary ICP to us in exchange for (1) 559,309 of our ordinary shares and (2) notes payable by us to Kenon in an aggregate principal amount of $220 million, which transactions we collectively refer to as the Reorganization. Additionally, prior to the completion of this offering, we will be converted into a Singapore public company limited by shares and renamed . Except as otherwise indicated, or unless the context requires otherwise, references to “IC Power,” “the Company,” “we,” “us” and “our” prior to the date of the Reorganization shall refer to ICP and its businesses, and as of the date of the Reorganization and thereafter, to IC Power and its subsidiaries, including ICP.

We present financial statements in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB, and all financial information included in this prospectus is presented in accordance with IFRS as issued by the IASB, except as otherwise indicated. In particular, this prospectus contains certain non-IFRS financial measures which are defined under “Summary Consolidated Financial and Other Information” and“Business.”

As set forth above, except as otherwise indicated, or unless the context requires otherwise, references to “IC Power,” “the Company,” “we,” “us” and “our” prior to the date of the Reorganization shall refer to ICP and its businesses, and, as of the date of the Reorganization and thereafter, to IC Power and its subsidiaries, including ICP. The financial statements we have included in this prospectus consist of: (1) IC Power’s unaudited condensed consolidated interim statements of income, comprehensive income, changes in equity, and cash flows for the six months ended June 30, 2016 and 2015, unaudited condensed consolidated interim statements of financial position as of June 30, 2016 and December 31, 2015, and the notes thereto. As set forth in Note 2 to these financial statements, as a result of the Reorganization, which occurred in March 2016, IC Power restated the information in these financial statements as of December 31, 2015 and for the six months ended June 30, 2015, reflecting the figures from ICP’s financial statements for those periods; (2) IC Power’s audited statement of profit or loss, changes in equity and cash flow for the period from May 4, 2015 (inception) through December 31, 2015, audited statement of financial position as of December 31, 2015, and the notes thereto; and (3) ICP’s audited consolidated statements of income, comprehensive income, changes in equity, and cash flows for the years ended December 31, 2015, 2014 and 2013, audited consolidated statements of financial position as of December 31, 2015 and 2014, and the notes thereto. Each of IC Power and ICP presents its financial statements in U.S. Dollars.

ICP is our predecessor for accounting reporting purposes. During the period from May 4, 2015 (IC Power’s inception) through December 31, 2015, IC Power did not incur any material expenses or recognize any

ii

Table of Contents

material assets or liabilities. Therefore, IC Power’s consolidated financial statements as of and for the year ended December 31, 2015 have not been restated to retroactively reflect the Reorganization, as there would be no material differences between such restated financial statements and ICP’s audited financial statements as of and for the year ended December 31, 2015. IC Power’s condensed consolidated interim financial statements as of and for the six months ended June 30, 2016 include comparative periods against the six months ended June 30, 2015, which have been adjusted to retroactively reflect the completion of the Reorganization and have been presented using the values from the condensed consolidated interim financial statements of ICP (similar to the pooling-of-interest method).

On January 22, 2016, we acquired two Guatemalan electricity distribution businesses (Distribuidora de Electricidad de Oriente, S.A., or DEORSA, and Distribuidora de Electricidad de Occidente, S.A., or DEOCSA), and two, smaller related businesses (Comercializadora Guatemalteca Mayorista de Electricidad, S.A., or Guatemel, and Redes Eléctricas de Centroamérica, S.A., or RECSA). In accordance with Staff Accounting Bulletin 80 (recodified with slight modifications in Staff Accounting Bulletin 103), we have included in this prospectus for each of DEORSA, DEOCSA, Guatemel and RECSA, unaudited condensed interim statements of financial position as of June 30, 2016 and December 31, 2015, unaudited condensed interim statements of profit or loss and other comprehensive income for the three and six months ended June 30, 2016 and 2015, the 21-day period from January 1, 2016 to January 21, 2016 and the 161-day period from January 22, 2016 to June 30, 2016 (the period in the first six months of 2016 from the date of acquisition), unaudited condensed interim statements of changes in shareholders’ equity for the six months ended June 30, 2016 and 2015, unaudited condensed interim statements of cash flows for the six months ended June 30, 2016 and 2015, and the notes thereto. The unaudited condensed interim financial statements referred to above have been prepared in accordance with International Accounting Standard No. 34 “Interim Financial Reporting.”

We have also included (1) for each of DEORSA and DEOCSA, the restated statements of financial position as of December 31, 2015, 2014, 2013 and January 1, 2013, and the related restated statements of profit or loss and other comprehensive income, changes in shareholders’ equity and cash flows for the years ended December 31, 2015, 2014 and 2013, and the notes thereto, (2) for Guatemel, the restated statements of financial position as of December 31, 2015, 2014 and 2013, and the related restated statements of profit or loss and other comprehensive income, changes in shareholders’ equity and cash flows for the years ended December 31, 2015, 2014 and 2013, and the notes thereto, and (3) for RECSA, the restated statements of financial position as of December 31, 2015, 2014 and 2013, and the related restated statements of profit or loss and other comprehensive income, changes in shareholders’ equity and cash flows for the years ended December 31, 2015, 2014 and 2013, and the notes thereto. The foregoing audited financial statements have been audited in accordance with U.S. Generally Accepted Auditing Standards, or U.S. GAAS, and prepared in accordance with IFRS as issued by the IASB.

Finally, this prospectus also includes the following financial statements of Generandes Perú S.A., or Generandes, prepared in accordance with IFRS as issued by the IASB: (1) unaudited consolidated statements of income, comprehensive income, changes in equity and cash flows for the years ended December 31, 2014 and 2013, unaudited consolidated statements of financial position as of December 31, 2014 and 2013, and the notes thereto; and (2) audited consolidated statements of income, comprehensive income, changes in equity and cash flows for the years ended December 31, 2013 and 2012, audited consolidated statements of financial position as of December 31, 2013, 2012 and 2011, and the notes thereto. Through our wholly-owned subsidiary, Inkia Holdings (Acter) Limited, or Acter Holdings, we owned a 39% interest in Generandes (resulting in a 21% indirect interest in Edegel S.A.A., or Edegel), until we sold our interest in Generandes in September 2014. Prior to the execution of our agreement to sell Generandes in April 2014, we accounted for Generandes under the equity method and reflected our proportional share in the net income of Generandes in share in income of associated companies. As a result of our divestment of Generandes, our proportionate share in Generandes’ results of operations is reflected in discontinued operations for all periods discussed in this prospectus. The financial statements of Generandes are included in this prospectus in accordance with Rule 3-09 of RegulationS-X, which does not require the inclusion of interim financial statements. Generandes’ financial statements have been audited in accordance with U.S. GAAS, except for the financial

iii

Table of Contents

statements as of and for the year ended December 31, 2014, which are not required by Rule 3-09 of Regulation S-X to be audited in accordance with U.S. GAAS or Public Company Accounting Oversight Board standards, as Generandes was an investee that would not be considered a “significant subsidiary” of ours as of and for the year ended December 31, 2014 under Rule 3-09 of Regulation S-X.

All references in this prospectus to (1) “U.S. Dollars,” “Dollars,” “$” or “USD” are to U.S. Dollars; (2) “Guatemalan Quetzales” are to the legal currency of the Republic of Guatemala, or Guatemala; (3) “NIS” or “New Israeli Shekels” are to the legal currency of the State of Israel, or Israel; (4) “S/” or “Peruvian Soles” are to the legal currency of the Republic of Peru, or Peru; (5) “Bs” and “Bolivianos” are to the legal currency of the Plurinational State of Bolivia, or Bolivia; (6) “COP” or “Colombian pesos” are to the legal currency of the Republic of Colombia, or Colombia; (7) “Chilean pesos” are to the legal currency of the Republic of Chile, or Chile; and (8) “S$” or “Singapore Dollars” are to the legal currency of the Republic of Singapore, or Singapore. We have made rounding adjustments to reach some of the figures included in this prospectus. Consequently, numerical figures shown as totals in some tables may not be arithmetic aggregations of the figures that precede them. Conversions included in this prospectus are solely illustrative, and you should not expect that any amounts in Guatemalan Quetzales, New Israeli Shekels, Peruvian Soles, Bolivianos, Colombian pesos, Chilean pesos, or Singapore Dollars actually represent a stated U.S. Dollar amount or that it could be converted into U.S. Dollars at the rate suggested.

NON-IFRS FINANCIAL INFORMATION

In this prospectus, we disclose non-IFRS financial measures, namely Adjusted EBITDA and Net Debt, each as defined in “Summary Consolidated Financial and Other Information.” Each of these measures is an important measure used by us, and our businesses, to assess financial performance. These measures are also used by our competitors, ratings agencies, financial analysts and investors to assess the financial performance of companies within our industry . We believe that the disclosure of Adjusted EBITDA and Net Debt provides transparent and useful information to investors and financial analysts in their review of our, or our subsidiaries’ and associated companies’, operating performance and in the comparison of such operating performance to the operating performance of other companies in the same industry or in other industries that have different capital structures, debt levels and/or income tax rates.

Certain information relating to our industry and market position used or referenced in this prospectus was obtained from internal analysis, surveys, market research, publicly available information and industry publications. Unless otherwise indicated, all sources for industry data are estimates or forecasts contained in or derived from internal or industry sources we believe to be reliable. Market and macroeconomic data used throughout this prospectus was obtained from independent industry publications and other publicly available information. Such data, as well as internal surveys, industry forecasts and market research, while believed to be reliable, have not been independently verified. In addition, in certain cases we have made statements in this prospectus regarding our industry and position in the industry based upon our experience and our own investigation of market conditions. We cannot assure you that any of these assumptions are accurate or correctly reflect our position in the industry, and none of our internal surveys or information has been verified by independent sources.

Market data are inherently predictive and speculative and are not necessarily reflective of actual market conditions. Such statistics are based on market research, which itself is based on sampling and subjective judgments by both the researchers and the respondents, including judgments about what types of products and transactions should be included in the relevant market. In addition, the value of comparisons of statistics for different markets is limited by many factors, including that (1) the markets are defined differently, (2) the underlying information was gathered by different methods and (3) different assumptions were applied in compiling the data. Accordingly, the market statistics included in this prospectus should be viewed with caution.

iv

Table of Contents

REPRESENTATION OF CAPACITY AND PRODUCTION FIGURES

Unless otherwise indicated, statistics provided throughout this prospectus with respect to power generation units are expressed in MW, in the case of the capacity of such power generation units, and in GWh, in the case of the electricity production of such power generation units. Unless otherwise indicated, our capacity figures provided in this prospectus reflect 100% of the capacity of all of our assets, regardless of our ownership interest in the entity that owns each such asset, and our consolidated generation figures provided in this prospectus reflect 100% of the generation figures of our subsidiaries and excludes the generation figures of our associated companies. Excluding the generation figures of AIE (as defined below), whose generation figures are only presented since the date of its acquisition, generation figures for assets acquired during a year are presented for the full year, regardless of the date within the year when the acquisition occurred. As a result, the generation figures provided in this prospectus of Colmito (as defined below), which we acquired in 2013, and ICPNH, Puerto Quetzal, Surpetroil and JPPC (each as defined below), which we acquired in 2014, reflect 100% of the generation figures of these companies for the year ended December 31, 2013 and 2014, respectively, regardless of our date of acquisition of such companies. With respect to capacity figures for the year ended December 31, 2014, and any prior periods thereto, our capacity figures exclude Edegel’s 1,540 MW of capacity, as a result of the sale of our indirect interest in Edegel in September 2014. For information on our ownership interest in each of the operating companies and investments within our generation portfolio, see “Business.”

ENFORCEMENT OF CIVIL LIABILITIES

IC Power is a private company limited by shares incorporated under the laws of Singapore. Some of our directors and officers and certain other persons named in this prospectus reside outside the United States. Additionally, a significant portion of IC Power’s assets and the assets of our directors and officers and certain other persons named in this prospectus are located outside the United States.

As a result, it may not be possible for U.S. investors to effect service of process within the United States upon these persons or to enforce against them or against us in the U.S. courts judgments predicated upon the civil liability provisions of the federal securities laws of the United States. There is doubt as to the enforceability in Singapore, either in original actions or in actions for enforcement of judgments of U.S. courts, of civil liabilities predicated on the U.S. federal securities laws.

CERTAIN TERMS USED IN THIS PROSPECTUS

We have prepared this prospectus using a number of conventions, which you should consider when reading the information contained herein. In this prospectus:

Our Operating Companies and Other Assets

| • | “Agua Clara” means IC Power DR Operations S.A.S., a Dominican Republic corporation; |

| • | “AIE” means Advanced Integrated Energy Ltd., an Israeli corporation; |

| • | “Amayo I” means Consorcio Eólico Amayo S.A., a Panamanian corporation; |

| • | “Amayo II” means Consorcio Eólico Amayo (Fase II) S.A., a Panamanian corporation; |

| • | “CDA” means Cerro del Águila S.A., a Peruvian corporation; |

| • | “Cenérgica” means Compañía de Energía de Centroamérica, S.A. de C.V. (Cenérgica), a Salvadorian corporation; |

| • | “Central Cardones” means Central Cardones S.A., a Chilean corporation; |

v

Table of Contents

| • | “CEPP” means Compañía de Electricidad de Puerto Plata S.A., a Dominican Republic corporation; |

| • | “COBEE” means Compañía Boliviana de Energía Eléctrica S.A., a Canadian corporation; |

| • | “Colmito” means Termoeléctrica Colmito S.A., a Chilean corporation; |

| • | “Corinto” means Empresa Energética Corinto Ltd., a Cayman Islands corporation; |

| • | “DEOCSA” means Distribuidora de Electricidad de Occidente, S.A., a Guatemalan corporation; |

| • | “DEORSA” means Distribuidora de Electricidad de Oriente, S.A., a Guatemalan corporation; |

| • | “Energuate” means DEOCSA and DEORSA, collectively. Energuate is not a legal entity, but serves as the trade name for IC Power’s Guatemalan distribution businesses DEORSA and DEOCSA; |

| • | “Guatemel” means Comercializadora Guatemalteca Mayorista de Electricidad, S.A., a Guatemalan corporation; |

| • | “IC Power” means the registrant, IC Power Pte. Ltd., a Singaporean corporation; |

| • | “ICP” means I.C. Power Asia Development Ltd. (formerly known as I.C. Power Ltd.), an Israeli corporation; |

| • | “ICPDH” means IC Power Distribution Holdings Pte. Ltd., a Singaporean corporation; |

| • | “ICPI” means IC Power Israel Ltd., an Israeli corporation; |

| • | “ICPNH” means IC Power Nicaragua Holdings, a Cayman Islands corporation, formerly known as AEI Nicaragua Holdings Ltd., or AEI Nicaragua; |

| • | “Inkia” means Inkia Energy Limited, a Bermudian corporation; |

| • | “JPPC” means Jamaica Private Power Company Ltd., a Jamaican corporation; |

| • | “Kallpa” means Kallpa Generación S.A., a Peruvian corporation; |

| • | “Kanan” means Kanan Overseas I. Inc., a Panamanian corporation; |

| • | “Nejapa” means Nejapa Power Company S.A., a Panamanian corporation; |

| • | “OIP” means Overseas Investments Peru S.A., a Peruvian corporation; |

| • | “OPC” means OPC Rotem Ltd., an Israeli corporation; |

| • | “Pedregal” means Pedregal Power Company S.de.R.L, a Panamanian corporation; |

| • | “Puerto Quetzal” means Puerto Quetzal Power LLC, a Delaware limited liability company; |

| • | “RECSA” means Redes Eléctricas de Centro América, S.A., a Guatemalan corporation; |

| • | “Samay I” means Samay I S.A., a Peruvian corporation; |

| • | “Surpetroil” means Surpetroil S.A.S., a Colombian corporation; and |

vi

Table of Contents

| • | “Tipitapa Power” means Tipitapa Power Company Ltd., a Cayman Islands corporation. |

Other Relevant Businesses

| • | “Acter Holdings” means Inkia Holdings (Acter) Limited, a Cayman Islands corporation through which we held our interest in Southern Cone; |

| • | “Edegel” means Edegel S.A.A., a Peruvian corporation; |

| • | “Generandes” means Generandes Perú S.A., a Peruvian corporation through which we held our indirect interest in Edegel; |

| • | “Globeleq” means Globeleq Americas Limited, which is the former name of Inkia Americas Limited, a Bermudian corporation; |

| • | “Hadera Paper” means Hadera Paper Ltd., an Israeli corporation; |

| • | “IC” means Israel Corporation Ltd., an Israeli corporation traded on the Tel Aviv Stock Exchange and Kenon’s and ICP’s former parent; |

| • | “Kenon” means Kenon Holdings Ltd., a Singapore company traded on each of the NYSE and the Tel Aviv Stock Exchange; and |

| • | “Southern Cone” means Southern Cone Power Perú S.A., a Peruvian corporation through which we held our interest in Generandes. |

Regulatory Bodies and Electricity System Coordination Entities

| • | “AMM” means Wholesale Market Administrator (Administrador del Mercado Mayorista), a private entity that coordinates the operation of the generation facilities and international interconnections and transmission lines that form the Guatemalan National Electricity System; |

| • | “ANA” means the National Water Authority of Peru(Autoridad Nacional del Agua); |

| • | “CND” means the National Dispatch Center of Panama (Centro Nacional de Despacho); |

| • | “CNDC” means the National Dispatch Committee of Bolivia (Comité Nacional de Despacho de Carga), a governmental entity responsible for planning and coordinating the operation of the generation, transmission and distribution systems that form the SIN in Bolivia; |

| • | “CNEE” means the National Electric Energy Commission of Guatemala (Comisión Nacional de Energía Eléctrica), which was established pursuant to the General Electricity Law of 1996, Decree 93-96, or General Electricity Law (Ley General de Electricidad) and acts as a technical arm of the MEM and which determines the transmission and distribution tariffs and is responsible for ensuring compliance with Guatemalan electricity laws; |

| • | “COES” means the Committee for the Economic Operation of the System (Comité de Operación Económica del Sistema Interconectado Nacional), an independent and private Peruvian entity composed of qualified participants undertaking activities in SEIN which is responsible for planning and coordinating the operation of the generation, transmission and distribution systems that form the SEIN; |

vii

Table of Contents

| • | “CREG” means the Commission for the Regulation of Energy and Gas in Colombia (Comisión de Regulación de Energía y Gas); |

| • | “EA” means the Electricity Authority in Israel, which was established pursuant to the Electricity Sector Law to regulate and supervise, among other things, the provision of essential electric services in Israel and electricity tariffs and, which replaced the previous regulator, Israel’s Public Utilities Authority (Electricity), or the PUAE, on January 1, 2016; |

| • | “Guatemalan National Electricity System” means the Guatemalan national electricity system, which comprises the set of premises, facilities, power plants, transmission lines, substations, distribution grids, electric equipment, loading centers, including all of the electric infrastructure used to supply electricity, whether or not interconnected, within which electric power is transmitted among the country’s several regions; |

| • | “IEC” means Israel Electric Corporation, a government-owned entity, which generates and supplies the majority of electricity in Israel, transmits all of the electricity in Israel, acts as the system operator of Israel’s electricity system, determines the dispatch order of generation units, grants interconnection surveys, and sets spot prices, among other roles; |

| • | “INDECOPI” means the National Institute for the Defense of Competition and Intellectual Property Protection (Instituto Nacional de Defensa de la Competencia y de la Protección de la Propiedad Intelectual), the Peruvian antitrust and intellectual property regulator; |

| • | “INDE” means the National Electrification Institute of Guatemala (Instituto Nacional de Electrificación), a state entity in charge of development of local power production pursuant to the INDE Statutory Law (Ley Orgánica del Instituto Nacional de Electrificación) and consequently in accordance with the General Electricity Law. This entity operates through its three divisions:Empresa de Generación de Energía Eléctrica (EGEE), which is responsible for power generation,Empresa de Transporte y Control de Energía Eléctrica (ETCEE), which is responsible for transmission andEmpresa de Comercialización de Energía (ECOE), which is responsible for trading; |

| • | “MEM” means the Ministry of Energy and Mines of Guatemala (Ministerio de Energía y Minas), which is responsible for enforcing the General Electricity Law and the related regulations and for the coordination of policies between CNEE and the AMM and overseeing energy and mining sectors in Guatemala; |

| • | “MINEM” means the Ministry of Energy and Mines of Peru (Ministerio de Energía y Minas), which is responsible for, among other things, setting national energy policy, proposing and adopting laws and regulations to supervise the energy sector and granting concessions and authorizations to entities who wish to operate in power generation, transmission or distribution in Peru; |

| • | “OC” means the Coordinating Body (Organismo Coordinador), a Dominican governmental authority whose function is to plan and coordinate the operations of the generation, transmission and distribution systems that form the national interconnected electrical system of the Dominican Republic (Sistema Eléctrico Nacional Interconectado); |

| • | “OEFA” means the Organization of Supervision and Environmental Assessment (Organismo de Evaluacióny Fiscalización Ambiental), the Peruvian governmental body responsible for the power plants’ compliance with environmental regulations; |

| • | “OSINERGMIN” means the Supervisory Body of Investment in Energy and Mining (Organismo Supervisor de la Inversión en Energía y Minería), a Peruvian governmental authority which is |

viii

Table of Contents

responsible for, among other things, ensuring that companies comply with the rules and regulations applicable to the energy industry in Peru and for setting the tariffs to be charged to regulated customers; |

| • | “PUAE” means Israel’s Public Utilities Authority (Electricity), which, prior to January 1, 2016, regulated and supervised, among other things, the provision of essential electric services in Israel and electricity tariffs. The PUAE was replaced by the EA on January 1, 2016; |

| • | “Salvadorian CNE” means the National Energy Commission of El Salvador (Comisión Nacional de Energía), a governmental entity which is responsible for proposing and adopting policies and regulations for the Salvadorian energy sector; |

| • | “SEIN” means the national interconnected electrical system of Peru (Sistema Eléctrico Interconectado Nacional); |

| • | “SENACE” means the National Service for Environmental Certification of Sustainable Investments of Peru (Servicio Nacional de Certificación Ambiental para las Inversiones Sostenibles), a Peruvian specialized technical governmental agency in charge of reviewing and approving detailed environmental impact assessments related to projects involving activities, works or services that may cause significant impacts to the environment; |

| • | “SIC” means the national interconnected electrical system of Chile (Sistema Interconectado Central); |

| • | “SIEPAC” means Central American Electrical Interconnection System (Sistema de Interconexión Eléctrica de los Países de América Central) that connects the transmission systems of Nicaragua, Panama, Costa Rica, Honduras, El Salvador and Guatemala through a 230 KW transmission line; |

| • | “SIGET” means the General Superintendency of Electricity and Telecommunications (Superintendencia General de Electricidad y Telecomunicaciones), a Salvadorian entity which is responsible for ensuring that companies comply with the rules and regulations passed by the National Energy Commission of El Salvador (Comisión Nacional de Energía), or Salvadorian CNE, as well as other laws that are applicable to the energy industry in El Salvador; |

| • | “SIN” means a national system formed by generation plants, the interconnected grid, regional transmission lines, distribution lines and consumer loads (Sistema Interconectado Nacional) in each of Bolivia, Colombia and Guatemala; |

| • | “SING” means the Interconnected System of Norte Grande of Chile (Sistema Interconectado Norte Grande); and |

| • | “UPME” means the Mining and Energy Planning Unit (Unidad de Planeación Minero Energética), a special administrative unit of the Ministry of Mines and Energy of Colombia. |

Industry and Other Terms

| • | “availability factor” means the percentage of hours a power generation unit is available for generation of electricity in the relevant period, whether or not the unit is actually dispatched or used for generating power; |

| • | “Btu” means British thermal units; |

| • | “CAGR” means compound annual growth rate; |

ix

Table of Contents

| • | “COD” means the commercial operation date of a development project; |

| • | “distribution” refers to the transfer of electricity from the transmission lines at grid supply points and its delivery to consumers at lower voltages through a distribution system; |

| • | “EPC” means engineering, procurement and construction; |

| • | “firm capacity” means the amount of energy available for production that, pursuant to applicable regulations, must be guaranteed to be available at a given time for injection to a certain power grid; |

| • | “greenfield projects” means projects constructed on unused land with no need to demolish or remodel existing structures; |

| • | “GWh” means gigawatt hours (one GWh is equal to 1,000 MWh); |

| • | “Heat rate” means the number of Btu of energy contained in the fuel required to produce a kWh of energy (Btu/kWh) for thermal plants; |

| • | “HFO” means heavy fuel oil; |

| • | “hydro” means hydroelectric; |

| • | “installed capacity” means the intended full-load sustained output of energy that a generation unit is designed to produce (also referred to as name-plate capacity); |

| • | “IPP” means independent power producer, excluding co-generators and generators for self-consumption; |

| • | “kV” means kilovolt; |

| • | “KWh” means kilowatt hour; |

| • | “MMBtu” means one million metric Btus; |

| • | “MW” means megawatts (one MW is equal to 1,000 Kilowatts or KW); |

| • | “MWh” means megawatt hour; |

| • | “OEM” means original equipment manufacturer; |

| • | “our capacity” or “our installed capacity” means, with respect to each generation asset, 100% of the capacity of such asset, regardless of our ownership interest in the entity that owns such asset; |

| • | “our proportionate capacity” means, with respect to each generation asset, the proportionate capacity of such asset, as determined by our ownership interest in the entity that owns such asset; |

| • | “PPA” means power purchase agreement; |

| • | “transmission” refers to the bulk transfer of electricity from generating facilities to the distribution system at load center station in which the electricity is stabilized by means of the transmission grid; |

| • | “VAD” means the Value Added by Distribution (Valor Agregado de Distribución) charge that is set by the CNEE; |

x

Table of Contents

| • | “VNR” means new replacement value (Valor Nuevo de Reemplazo); |

| • | “VNR of the transmission system” means the estimated cost of replacing a “model” transmission system, including an estimated return on capital; and |

| • | “weighted average availability” refers to the number of hours that a generation facility is available to produce electricity divided by the total number of hours in a year. |

The following tables set forth the historical period-end, average, high and low rates calculated using the daily closing exchange rates, as reported by Bloomberg, for the U.S. Dollar expressed in Peruvian Sol per one U.S. Dollar for the periods indicated:

Peruvian Sol/U.S. Dollar | ||||||||||||||||

Period End(1) | Average(2) | High | Low | |||||||||||||

Year | ||||||||||||||||

2011 | 2.696 | 2.753 | 2.830 | 2.690 | ||||||||||||

2012 | 2.551 | 2.638 | 2.710 | 2.547 | ||||||||||||

2013 | 2.796 | 2.703 | 2.814 | 2.537 | ||||||||||||

2014 | 2.979 | 2.839 | 2.993 | 2.764 | ||||||||||||

2015 | 3.414 | 3.185 | 3.414 | 2.975 | ||||||||||||

| 1. | Represents the closing exchange rate on the last business day of the applicable period. |

| 2. | Represents the average of the closing exchange rates on the last business day of each month during the relevant one-year periods. |

Peruvian Sol/ | ||||||||

High | Low | |||||||

Month | ||||||||

April 2016 | 3.393 | 3.243 | ||||||

May 2016 | 3.377 | 3.304 | ||||||

June 2016 | 3.373 | 3.283 | ||||||

July 2016 | 3.370 | 3.278 | ||||||

August 2016 | 3.398 | 3.302 | ||||||

September 2016 | 3.407 | 3.344 | ||||||

October 2016 (through October 26, 2016) | 3.409 | 3.351 | ||||||

xi

Table of Contents

This summary highlights information presented in greater detail elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before deciding whether to invest in our ordinary shares, you should carefully read this entire prospectus, especially the risks of investing in our ordinary shares discussed under the heading “Risk Factors.”

Overview

We are a leading owner, developer and operator of power generation facilities located in key energy markets in Latin America, the Caribbean and Israel. Additionally, in January 2016, we completed our acquisition of Energuate (comprised of two electricity distribution companies in Guatemala (DEORSA and DEOCSA)), marking our initial entry in the electricity distribution sector.

The power generation companies within our portfolio utilize a range of energy sources, including natural gas, hydroelectric, heavy fuel oil, or HFO, diesel and wind. We principally focus our generation operations in Latin American markets, which typically have higher growth rates of gross domestic product, or GDP, and lower overall and per capita energy consumption, as compared with more developed markets. We believe that economic growth in Latin American markets will drive increases in overall and per capita energy consumption and therefore require significant additional investments in power generation assets in those markets. As of June 30, 2016, our installed capacity and proportionate capacity were 3,384 MW and 2,731 MW, respectively, including Kanan’s 92 MW thermal generation project in Panama, which reached COD in April 2016, and Samay I’s 616 MW cold-reserve thermoelectric project in Peru, which reached COD in May 2016.

We increased our installed capacity by an additional 510 MW, to 3,894 MW (3,114 MW on a proportionate basis), in August 2016 upon the completion of the three generating units of Cerro del Águila S.A.’s, or CDA’s, 510 MW hydroelectric plant located in Peru. In addition, in August 2015, we acquired Advanced Integrated Energy, or AIE, which currently operates an 18 MW plant in Israel and holds a conditional license for the construction of a cogeneration power station in Israel. AIE commenced construction of the plant in June 2016, and the AIE plant, which is expected to have a capacity of 140 MW, is expected to reach its commercial operation date, or COD, by the end of 2018.

ICP’s activities started in 2007 when Inkia Energy Limited, or Inkia, a subsidiary of Israel Corporation Ltd., or IC, an Israeli conglomerate, acquired Globeleq Americas Limited’s, or Globeleq’s, power generation assets in Latin America, which represented 549 MW of installed capacity. In 2010, IC formed ICP and contributed both Inkia and O.P.C. Rotem Ltd., or OPC, to ICP. In January 2015, IC transferred ICP to Kenon (NYSE: KEN; TASE: KEN), our sole shareholder, in connection with IC’s spin-off of Kenon. In March 2016, as more fully described in “Corporate Formation and Reorganization,” Kenon effected an internal reorganization pursuant to which it transferred all of its equity interests in ICP to us.

Between 2007 and June 30, 2016, we invested approximately $3.0 billion in the acquisition, development and expansion of our power generation assets. Of this amount, 80% represented investments in greenfield development (including investments made in CDA, Samay I and Kanan) and 20% represented acquisitions. We have financed our greenfield development using a combination of cash on hand, debt financing and investments by minority shareholders at the asset level, and have financed the acquisitions of our power generation assets using cash on hand. As of June 30, 2016, of the 2,835 MW that we have added to our installed capacity since Inkia’s formation, 72% was derived from greenfield development projects, consisting primarily of our construction of Kallpa Generación S.A.’s, or Kallpa’s, combined cycle plant, Peru’s largest power generation facility, the construction of OPC’s plant, which became Israel’s first independent power producer, or IPP, and the construction of the Samay I project, a cold-reserve thermoelectric plant in Peru. In the same period, we have

1

Table of Contents

acquired businesses with an aggregate installed capacity of 801 MW in Israel and five countries in Latin America. As of the end of August 2016, we had derived 76% of our installed capacity growth since 2007 from greenfield development efforts.

By successfully pursuing growth opportunities, primarily through contracted greenfield development projects in existing markets and acquisitions of anchor investments in new markets, we have expanded our regional presence, diversified our generation portfolio through the addition of various facilities which use a range of energy sources, and significantly increased our cash flows. In 2015, our Adjusted EBITDA was $326 million, as compared to $41 million in 2008, representing a compound annual growth rate, or CAGR, of 34% during this period. Adjusted EBITDA is a non-IFRS measure. For a reconciliation of our net income to our Adjusted EBITDA, see “Summary Consolidated Financial and OtherInformation—Key Financial and Other Operating Information—IC Power and ICP.”

We typically enter into long-term U.S. Dollar-linked power purchase agreements, or PPAs, to sell capacity and/or energy to customers that we believe have strong credit profiles, such as large local distribution companies or non-regulated customers that are subsidiaries of large multinational corporations. As of December 31, 2015, the weighted average remaining life of our PPAs was 10 years (including the remaining life of the PPAs for CDA, Samay I and Kanan). In the year ended December 31, 2015, 89% of our aggregate energy sales (in gigawatt hours, or GWh) were made pursuant to long-term PPAs. We believe this practice limits our exposure to fluctuations in energy spot market rates and helps us to generate strong and predictable margins and cash flows. We seek to enter into PPAs at prices that are equal to, or higher than, the prevailing spot market rates in the countries in which we operate. Additionally, the majority of our PPAs are indexed to the underlying fuel cost of the related long-term supply agreements. Such indexing generally limits our exposure to fuel price fluctuations, including the effect of such fluctuations on our margins. We believe that the stable and predictable margins and cash flows which generally result from such PPAs helps us to successfully secure significant project and bank/bond financing, with no or limited recourse, from a diverse international lender base during the construction of our greenfield projects, which helps us to successfully develop our project pipeline.

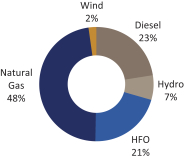

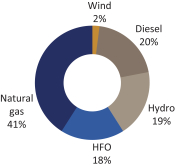

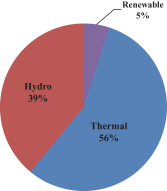

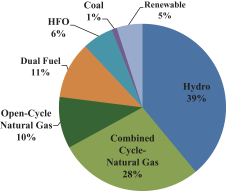

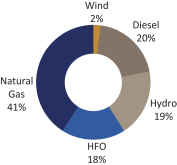

Our power generation portfolio is comprised of facilities located in key power generation markets in Latin America, the Caribbean and Israel, using a range of energy sources. The following charts set forth the relative percentages of our generation business’ installed capacity by energy source as of June 30, 2016, and our generation business’ installed capacity by energy source, as adjusted to reflect the recent completion of the CDA project:

Installed Capacity by Energy Source (as of June 30, 2016)1 | Installed Capacity by Energy Source (September 30, 2016)1 | |

|

| |

| 3,384 MW2 | 3,894 MW2,3,4 |

| 1. | Our dual-fueled assets, COBEE, OPC, Samay I and Termoeléctrica Colmito S.A., or Colmito, are categorized as hydroelectric, natural gas, diesel and natural gas, respectively. |

2

Table of Contents

| 2. | Includes 616 MW attributable to Samay I, which reached COD in May 2016. In July 2016, all of the plant’s units were declared unavailable to the system due to damage to the shafts in three of the plant’s four units. We have developed a plan to repair the units, and on August 28, 2016, Kenon announced that we expected all four units to be operational within six months. |

| 3. | Includes 510 MW attributable to CDA, which plant’s three generating units reached COD in August 2016. |

| 4. | Does not include the 140 MW cogeneration power station which AIE began constructing in June 2016 as a greenfield project. Construction of this plant commenced in June 2016 and COD is expected by the end of 2018. |

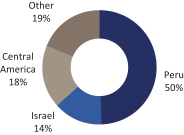

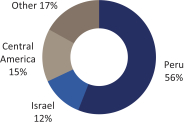

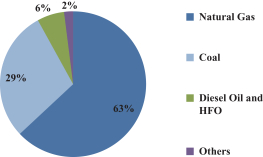

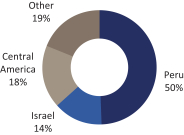

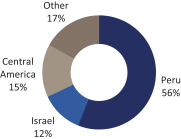

The following charts set forth the relative percentage of our generation business’ installed capacity by segment as of June 30, 2016, and our generation business’ installed capacity by segment, as adjusted to reflect the recent completion of the CDA project:

Installed Capacity by Segment (as of June 30, 2016) | Installed Capacity by Segment (September 30, 2016) | |

|

| |

| 3,384 MW1 | 3,894 MW1,2,3 |

| 1. | Includes 616 MW attributable to Samay I, which reached COD in May 2016. In July 2016, all of the plant’s units were declared unavailable to the system due to damage to the shafts in three of the plant’s four units. We have developed a plan to repair the units, and on August 28, 2016, Kenon announced that we expected all four units to be operational within six months. |

| 2. | Includes 510 MW attributable to CDA, which plant’s three generating units reached COD in August 2016. |

| 3. | Does not include the 140 MW cogeneration power station which AIE began constructing in June 2016 as a greenfield project. Construction of this plant commenced in June 2016 and COD is expected by the end of 2018. |

We are a leader in our largest market, Peru, one of the fastest growing economies in Latin America, with an average GDP growth rate of approximately 4.8% per year from 2010 through 2015 according to the International Monetary Fund, a mature regulatory framework, and a well-run power system. As of and for the year ended December 31, 2015, our operating company in Peru, Kallpa, had an installed capacity of 1,063 MW, representing 11% of Peru’s installed capacity, and generated 12% of the gross energy generated (in GWh) in Peru. Kallpa represented 81% of our net income, 47% of our Adjusted EBITDA, and 40% of our installed capacity as of and for the year ended December 31, 2015. In May 2016, Samay I (our cold-reserve thermoelectric project) reached COD, providing an additional 616 MW of installed capacity to the Peruvian market. In August 2016, we provided an additional 510 MW of installed capacity to the Peruvian market with the completion of the three generating units of CDA. As a result of the completion of this project, our total installed capacity in Peru is 2,189 MW, making us the principal power producer in Peru in terms of installed capacity. Although energy and capacity prices in Peru have recently experienced downward pressure due to oversupply of capacity in the market, we expect demand and spot prices to increase in the medium term as a result of large mining and industrial projects in Peru and sustained growth in underlying demand.

We also operate OPC, the first IPP in Israel, which, in 2013 following decades of state control, opened its electricity market to private power producers. As a result, the electricity market in Israel is still in the early stages of development. Israel’s energy consumption levels have also increased in recent years and are expected to continue to increase in the near-term. As of and for the year ended December 31, 2015, OPC had an installed

3

Table of Contents

capacity of 440 MW, representing approximately 3% of Israel’s installed capacity and 19% of the installed capacity of IPPs, and generated 6% of the gross energy generated (in GWh) in Israel. As of and for the year ended December 31, 2015, OPC represented 38% of our net income, 24% of our Adjusted EBITDA, and 17% of our installed capacity. We believe that OPC’s plant provides us with a strategic advantage as an early entrant to the Israeli electricity market. Additionally, given Israel’s growing economy and the advanced age of its existing state-owned power generation facilities, we believe OPC provides us with the know-how and visibility to pursue additional power project opportunities in Israel, such as the acquisition of AIE, which opportunities may become increasingly available to private sector participants such as us.

In addition to our attractive positions in Peru and Israel, we have also developed an attractive footprint in several markets in Latin America, including Chile and Colombia, and are in the process of opening a development office in Mexico. Additionally, in January 2016, we completed our acquisition of Energuate (comprised of two electricity distribution companies in Guatemala (DEORSA and DEOCSA)), and two smaller, related companies (Guatemel and RECSA). As of December 31, 2015, Energuate provides electric service for approximately 1.6 million regulated customers in Guatemala (representing approximately 55% of Guatemala’s regulated distribution customers in 2015) and distributes energy across approximately 100,000 km2in Guatemala, covering approximately 12 million inhabitants. Energuate operates approximately 34,000 km of distribution lines within Guatemala (representing approximately 70% of Guatemala’s distribution lines) as of December 31, 2015, and holds the non-exclusive right to distribute electricity within its service area until 2048. In the years ended December 31, 2015 and 2014, Energuate sold 2,305 GWh and 2,164 GWh of energy, respectively. We believe that our current platform, coupled with our agile and disciplined decision-making process, enables us to take advantage of opportunities as they arise.

4

Table of Contents

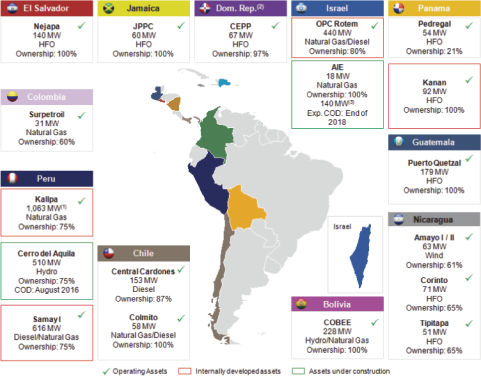

Our Portfolio of Generation Assets

The following table sets forth summary operational information regarding each of our operating companies and associated company in our generation business as of June 30, 2016, according to segment1:

Segment | Country | Entity | Ownership | Fuel | Installed | Proportionate | Type of Asset | Weighted | LTM (GWh)3 | |||||||||||||||||||

Peru | Peru | Kallpa | 75 | % | Natural Gas | 1,063 | 4 | 797 | Greenfield4 | 7 | 6,309 | |||||||||||||||||

| Peru | Samay I | 75 | % | Diesel and Natural Gas | 616 | 462 | Greenfield | 12 | — | |||||||||||||||||||

Israel | Israel | OPC | 80 | % | Natural Gas and Diesel | 440 | 352 | Greenfield | 7 | 5 | 3,929 | |||||||||||||||||

| Israel | AIE | 100 | % | Natural Gas6 | 18 | 18 | Acquired | 15 | 697 | |||||||||||||||||||

Central America | Nicaragua | Corinto | 65 | % | HFO | 71 | 46 | Acquired | 3 | 429 | ||||||||||||||||||

| Nicaragua | Tipitapa Power | 65 | % | HFO | 51 | 33 | Acquired | 3 | 367 | |||||||||||||||||||

| Nicaragua | Amayo I | 61 | % | Wind | 40 | 24 | Acquired | 9 | 159 | |||||||||||||||||||

| Nicaragua | Amayo II | 61 | % | Wind | 23 | 14 | Acquired | 3 | 94 | |||||||||||||||||||

| Guatemala | Puerto Quetzal | 100 | % | HFO | 179 | 179 | Acquired | 1 | 515 | |||||||||||||||||||

| El Salvador | Nejapa | 100 | % | HFO | 140 | 140 | Original Inkia Asset | 1 | 801 | |||||||||||||||||||

| Panama | Kanan | 100 | % | HFO | 92 | 92 | Greenfield | 4 | 269 | |||||||||||||||||||

Other | Bolivia | COBEE | 100 | % | Hydroelectric, Natural Gas | 228 | 228 | Original Inkia Asset | 1 | 277 | ||||||||||||||||||

| Chile | Central Cardones | 87 | % | Diesel | 153 | 133 | Acquired | — | — | |||||||||||||||||||

| Chile | Colmito | 100 | % | Natural Gas and Diesel | 58 | 58 | Acquired | 3 | 263 | |||||||||||||||||||

| Dominican Republic | CEPP | 97 | % | HFO | 67 | 65 | Original Inkia Asset | — | 8 | |||||||||||||||||||

| Jamaica | JPPC | 100 | % | HFO | 60 | 60 | Original Inkia Asset | 2 | 382 | |||||||||||||||||||

| Colombia | Surpetroil | 60 | % | Natural Gas | 31 | 19 | Acquired / Greenfield8 | 1 | 52 | |||||||||||||||||||

| Panama | Pedregal9 | 21 | %10 | HFO | 54 | 11 | Original Inkia Asset | 2 | 298 | |||||||||||||||||||

| Total Operating Capacity | 3,384 | 2,731 | ||||||||||||||||||||||||||

|

|

|

| |||||||||||||||||||||||||

| 1. | Reflects 100% of the capacity of each of our assets, regardless of our ownership interest in the entity that owns each such asset. |

| 2. | Reflects the proportionate capacity of each of our assets, as determined by our ownership interest in the entity that owns each such asset. |

| 3. | Reflects energy sales under PPAs for the 12 months ended June 30, 2016. |

| 4. | Kallpa’s plants were developed as projects constructed on unused land with no need to demolish or remodel existing structures, or greenfield projects, in four different stages between 2005 and 2012, resulting in 870 MW of installed capacity. In addition, Kallpa acquired Las Flores’ power plant in 2014, adding 193 MW to Kallpa’s capacity. |

| 5. | Reflects the weighted average remaining life of OPC’s PPAs with end users based on OPC’s firm capacity. The PPA between OPC and IEC, the government-owned electricity generation, transmission and distribution company in Israel, or the IEC PPA, which extends for |

5

Table of Contents

| an 18-year term and covers OPC’s entire firm capacity, provides OPC with the option to allocate and sell the generated electricity of the power station directly to end users. OPC has exercised this option and sells all of its energy and capacity directly to 20 end users, as of June 30, 2016. For further information on the IEC PPA, see “Business—Regulatory, Environmental and Compliance Matters—Regulation of the Israeli Electricity Sector.” |

| 6. | AIE also holds a conditional license for the construction of a cogeneration power station in Israel. This station will be developed as a greenfield project (at an expected cost of $250 million, including the acquisition price of AIE), based upon a plant with 140 MW of capacity. Construction commenced in June 2016 and COD is expected by the end of 2018. |

| 7. | Reflects energy sales under PPAs since we acquired AIE in August 2015. |

| 8. | When initially acquired by us, Surpetroil had a capacity of 15 MW. As of June 30, 2016, Surpetroil’s capacity has increased to 31 MW as a result of our completion of various greenfield projects. |

| 9. | Although Pedregal is located in Central America, it is a minority investment. Therefore, from an income statement perspective, it is not part of the Central America segment and Pedregal is only reflected in our share in income of associated companies. |

| 10. | Although we have a non-controlling interest in Pedregal, we were party to a management services agreement, which designated us as the administrator responsible for the day-to-day management of Pedregal until the agreement expired in October 2016. We expect to renew the management services agreement in November 2016. However, we may be unable to do so. |

The following table sets forth summary operational information regarding our generation asset in advanced stages of construction as of June 30, 2016.

Country | Entity | Ownership | Fuel | Installed Capacity (MW)1 | Proportionate Capacity2 | Expected | Percentage Developed | Expected Cost | Amount Invested | |||||||||||||||||||||

Peru | CDA | 75% | Hydroelectric | 510 | 383 | August 2016 |

| 98%—Overall completion 99%—Dam construction 100%—Tunnel drilling |

| $959 million | $907 million | 3 | ||||||||||||||||||

|

|

|

|

| ||||||||||||||||||||||||||

Total Capacity of Asset in Advanced Stages of Construction | 510 | 383 | $959 million | $907 million | ||||||||||||||||||||||||||

|

|

|

|

| ||||||||||||||||||||||||||

| 1. | Reflects 100% of the expected capacity, regardless of our ownership interest in the entity that owns the asset. |

| 2. | Reflects the proportionate capacity, as determined by our ownership interest in the entity that owns the asset. |

| 3. | Includes $8 million of intercompany expenses related to services rendered by Kallpa pursuant to a management agreement. |

In April and May 2016, Kanan’s 92 MW thermal generation project and Samay I’s 616 MW cold-reserve thermoelectric project reached their COD, at an aggregate cost of $87 million and $379 million (excluding $26 million of diesel fuel inventory), respectively. In July 2016, all four of Samay I’s units were declared unavailable to the system due to damage to the shafts in three of the plant’s four units. We have developed a plan to repair the units, and on August 28, 2016, Kenon announced that we expected all four units to be operational within six months. We intend to seek coverage for the costs of the outage, including repair costs and loss of profits, as appropriate, from the EPC contractor, equipment manufacturer and/or the insurance coverage (subject to deductibles), and believe we have a reasonable basis to recover these costs, including for loss of profits. For further information on Samay I’s unavailability, see “Business—Generation Segment—Peru— SamayI.” For further information on Samay I’s insurance, see “Business—Insurance.” In August 2016, the three generating units of CDA’s 510 MW run-of-the-river hydroelectric plant in Peru reached their COD, at an estimated cost of approximately $959 million.

6

Table of Contents

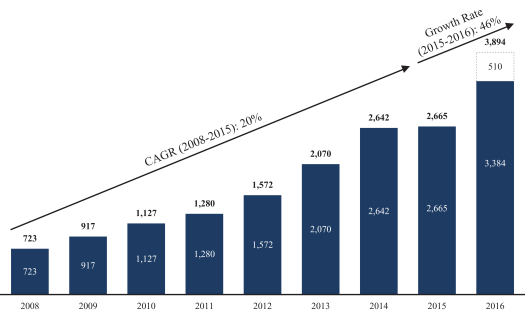

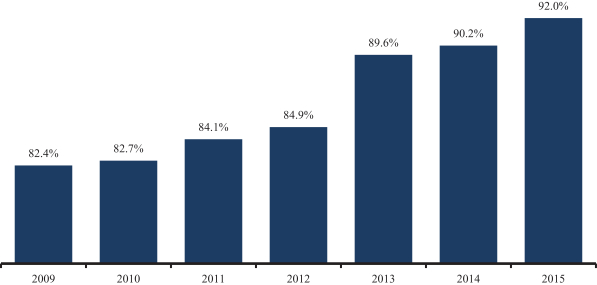

As illustrated below, between 2008 and 2015, we have increased our installed capacity at a CAGR of 20%, and our installed capacity has grown 46% during 2016 as a result of the recentcompletion of the Kanan, Samay I and CDA projects. As of the end of August 2016, we had derived 76% of our installed capacity growth since 2007 from our greenfield development efforts.

Installed Capacity (MW)1

(as of June 30, 2016)2

| 1. | Figures for 2008 and 2009 reflect Inkia’s capacity. |

| 2. | Since June 30, 2016, 510 MW have come on line as a result of the completion of the development of CDA’s three generating units. |

The following table sets forth certain consolidated financial and operational data as of the dates and for the periods set forth below:

Six Months | Year Ended December 31, | |||||||||||||||||||

2016 | 2015 | 2015 | 2014 | 2013 | ||||||||||||||||

| ($ millions, except as otherwise indicated) | ||||||||||||||||||||

Sales from continuing operations | $ | 881 | $ | 655 | $ | 1,289 | $ | 1,372 | $ | 873 | ||||||||||

Net income from continuing operations | 16 | 35 | 49 | 128 | 46 | |||||||||||||||

Net income | 16 | 39 | 53 | 256 | 74 | |||||||||||||||

Adjusted EBITDA1 | 188 | 175 | 326 | 395 | 247 | |||||||||||||||

Installed capacity at end of period (in MW)2 | 3,384 | 2,642 | 2,665 | 2,642 | 2,070 | |||||||||||||||

Proportionate capacity at end of period (in MW)3 | 2,731 | 2,149 | 2,170 | 2,108 | 1,608 | |||||||||||||||

| 1. | Adjusted EBITDA is a non-IFRS measure. For a reconciliation of our net income to our Adjusted EBITDA, see “Summary Consolidated Financial and Other Information.” |

| 2. | Reflects 100% of the capacity of each of our assets, regardless of our ownership interest in the entity that owns each such asset. |

| 3. | Reflects the proportionate capacity of each of our assets, as determined by our ownership interest in the entity that owns each such asset. |

7

Table of Contents

Potential Projects

We are constantly monitoring and considering development and acquisition opportunities and are currently assessing projects in Israel and various Latin American countries, such as Argentina, Chile, Colombia, Panama, Peru, the Dominican Republic, Mexico, Nicaragua, El Salvador and Puerto Rico relating to generation or distribution projects or companies. For example, we are starting development of Agua Clara, a 50 MW wind project in the Dominican Republic, which is expected to commence commercial operations in early 2018. With respect to our potential generation projects, such projects range in size from small-scale power facilities (e.g., less than 40 MW) to large-scale power facilities (e.g., approximately 750 MW) and utilize different fuels and technologies, including natural gas, hydroelectric, wind, solar and stranded gas. In some instances, we have acquired land, secured necessary licenses or rights, including temporary concessions and water rights, commissioned studies, made bids, or initiated similar actions, in connection with our assessment of the viability of the relevant project.

In addition to the Latin American opportunities that we are currently considering, we also monitor opportunities in other markets. For example, in August 2015, we acquired 100% of the shares of AIE from Hadera Paper Ltd., or Hadera Paper, for NIS 60 million (approximately $16 million). AIE currently operates an 18 MW plant and also holds a conditional license for the construction of a cogeneration power station in Israel. AIE commenced construction of the plant in June 2016, and the AIE plant is expected to reach its COD by the end of 2018. We expect that the total cost of completing the AIE plant (including the consideration for the acquisition of AIE) will be approximately $250 million.

8

Table of Contents

Set forth below is a map summarizing certain of the markets and projects that we have identified for potential expansion. Development projects imply a high degree of uncertainty, and there is no guarantee that we will proceed with these projects. Ultimately, notwithstanding the number of opportunities that we may consider over the long- and short-terms, we will only pursue those projects that we believe will generate attractive, risk-adjusted returns over the long-term and which we believe we have the management capacity to build and operate. The summary below sets forth projects developed and owned by us, as well as projects owned by third parties, as well as projects that we may be able to acquire by direct negotiations or through tender processes. This summary is not exhaustive, is only provided to show projects which we are evaluating, and should not serve as an indication of any expectation regarding any final outcome. Numerous conditions will need to be met before we can develop or acquire any of the projects listed below:

Competitive Strengths

Strong track record inproject development, with a disciplined approach to capital structure—We leverage our core competencies—project identification, evaluation, development, construction and operation—to develop power generation facilities using various technologies in attractive markets that typically have relatively high GDP growth rates and relatively low levels of per capita energy consumption. For example, in 2012, we completed our third expansion of Kallpa’s gas-powered plant, which is the largest power generation facility in Peru in terms of capacity, by converting it into a combined cycle facility and thereby adding an additional 292 MW to the facility’s capacity. This expansion was completed on time and below budget. Additionally, in 2013, OPC became the first IPP in Israel when we completed the construction of its 440 MW combined cycle power plant. In April, May and August 2016, we also completed the development of Kanan’s 92 MW thermal

9

Table of Contents

generation project in Panama, the development of Samay I’s 616 MW cold-reserve thermoelectric project in Peru and the development of the three generating units of CDA’s 510 MW run-of-the-river hydroelectric plant in Peru, respectively.

Our projects have been developed with a disciplined capital structure, which reflects our commitment to develop projects in accordance with three key fundamental principles. First, we endeavor to construct projects by entering into turnkey engineering, procurement and construction, or EPC, agreements that define the total project cost and transfer most of the risks of construction delays and cost overruns to our EPC contractors. For example, we constructed Samay I and CDA pursuant to EPC contracts. Second, we seek to secure a revenue stream prior to the construction of our plants by sourcing and entering into long-term PPAs, which provide our development projects with predictable projected margins and cash flows, before construction has commenced. Finally, we leverage our EPC contracts and PPAs to secure long-term project financing agreements which are generally stand-alone, secured, project-specific, and with no or limited recourse. Over the course of our history, we have secured different types of financings (e.g., leases, local and international bonds, syndicated loans, etc.) during times of changing financial markets and in connection with our construction of various projects using a range of energy sources.

Long-term PPAs and supply agreements that limit exposure to market fluctuations—Most of our generation subsidiaries typically enter into long-term PPAs, which generally limits their exposure to fluctuations in energy spot market rates, generates stable and predictable margins, and helps to create stability and predictability in our cash flows. In the year ended December 31, 2015, we made 89% of our aggregate energy sales (in GWh) pursuant to long-term PPAs. As of December 31, 2015, the weighted average remaining life of our PPAs was 10 years (including the remaining life of the PPAs for CDA, Samay I and Kanan) and we have historically sought, and will continue to seek, to renew our long-term PPAs as they expire.

As of December 31, 2015, the majority of our PPAs were indexed to the price of the corresponding power plant’s operating fuel prices in U.S. Dollars (for plants that use fuel), and many of our PPAs provided for payment in, or were linked to, the U.S. Dollar, thereby mitigating such plant’s exposure to fuel price and exchange rate fluctuations. Additionally, the counterparties to our long-term PPAs are typically large local distribution companies or non-regulated customers, including subsidiaries of large multi-national corporations, which we believe have strong credit profiles, mitigating the risk of customer default. Some of our major non-regulated customers within Peru and Israel include Southern Peru Copper Corporation, Sociedad Minera Cerro Verde S.A.A. (a subsidiary of Freeport-McMoRan), Compañía Minera Antapaccay S.A. (a subsidiary of Glencore Xstrata) and Oil Refineries Limited, as well as governments and quasi-governmental entities.

As our power facilities utilize and are dependent upon natural gas, hydroelectric, HFO, diesel, wind, or a combination of these energy sources, we seek to enter into long-term supply and transportation agreements to acquire the necessary fuel for our facilities. For example, Kallpa, Samay I and OPC, which own and operate our largest plants, are party to long-term supply agreements, including natural gas supply agreements and transportation services agreements, that are material to their operations.

Attractive footprint in high growth markets—Currently, our principal focus is on Latin American markets, which typically have higher growth rates of GDP and lower overall and per capita energy consumption, as compared with more developed markets. We expect continued growth in these key markets, providing us with the opportunity to generate attractive, risk-adjusted returns through additional investments in power generation assets in those countries.

We are a leader, and the principal power producer, in our largest market, Peru, one of the fastest growing economies in Latin America, with an average GDP growth of approximately 4.8% per year from 2010 through 2015, according to the International Monetary Fund, a mature regulatory framework, and a well-run power system. As of and for the year ended December 31, 2015, our operating company in Peru, Kallpa, had an

10

Table of Contents

installed capacity of 1,063 MW, representing 11% of Peru’s installed capacity, and generated 12% of the gross energy generated (in GWh) in Peru. Kallpa represented 81% of our net income, 47% of our Adjusted EBITDA, and 40% of our installed capacity as of and for the year ended December 31, 2015. In May 2016, Samay I (our cold-reserve thermoelectric project) reached its COD on schedule, providing an additional 616 MW of installed capacity to the Peruvian market. In August 2016, we provided an additional 510 MW of installed capacity to the Peruvian market with the completion of the three generating units of CDA. As a result of the completion of this project, our total installed capacity in Peru is 2,189 MW, making us the principal power producer in Peru in terms of installed capacity. Although energy and capacity prices in Peru have recently experienced downward pressure due to oversupply of capacity in the market, we expect demand and spot prices to increase in the medium term as a result of large mining and industrial projects in Peru and sustained growth in underlying demand.

We also operate OPC, the first IPP in Israel, which, in 2013 following decades of state control, opened its electricity market to private power producers. As a result, the electricity market in Israel is still in the early stages of development. Israel’s energy consumption levels have also increased in recent years and are expected to continue to increase in the near-term. As of and for the year ended December 31, 2015, OPC had an installed capacity of 440 MW, representing approximately 3% of Israel’s installed capacity and 19% of the installed capacity of IPPs, and generated 6% of the gross energy generated (in GWh) in Israel. As of and for the year ended December 31, 2015, OPC represented 38% of our net income, 24% of our Adjusted EBITDA, and 17% of our installed capacity. We believe that OPC’s plant provides us with a strategic advantage as an early entrant to the Israeli electricity market. Additionally, given Israel’s growing economy and the advanced age of its existing state-owned power generation facilities, we believe OPC provides us with the know-how and visibility to pursue additional power project opportunities in Israel, such as the acquisition of AIE, which opportunities may become increasingly available to private sector participants such as us.

In addition to our attractive positions in Peru and Israel, we have also developed an attractive footprint in several markets in Latin America, including Chile and Colombia, and are in the process of opening a development office in Mexico. We believe that our current platform, coupled with our agile and disciplined decision-making process, enables us to take advantage of opportunities as they arise.