UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-23084

Series Portfolios Trust

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

(Address of principal executive offices) (Zip code)

Ryan L. Roell, President

Series Portfolios Trust

c/o U.S. Bancorp Fund Services, LLC

777 East Wisconsin Ave, 5th Fl

Milwaukee, WI 53202

(Name and address of agent for service)

(Name and address of agent for service)

(414) 516-1709

Registrant's telephone number, including area code

Date of fiscal year end: December 31, 2022

Date of reporting period: December 31, 2022

Item 1. Report to Stockholders.

| (a) |

Palm Valley Capital Fund

Investor Class – PVCMX

ANNUAL REPORT

December 31, 2022

PALM VALLEY CAPITAL FUND

INVESTMENT PERFORMANCE (%) as of December 31, 2022

Total Return | Annualized Return | |||||

Inception | Quarter | YTD | 1 Year | 3 Year | Inception | |

| Palm Valley Capital Fund | 4/30/19 | 3.86% | 3.16% | 3.16% | 8.43% | 7.24% |

| S&P SmallCap 600 Index | 9.19% | -16.10% | -16.10% | 5.80% | 6.36% | |

| Morningstar Small Cap Index | 8.05% | -18.46% | -18.46% | 3.33% | 4.16% | |

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be higher or lower than the performance quoted. Performance of the Fund current to the most recent quarter-end can be obtained by calling 904-747-2345.

As of the most recent prospectus, the Fund’s gross expense ratio is 1.83% and the net expense ratio is 1.30%. Palm Valley Capital Management has contractually agreed to waive its management fees and reimburse Fund operating expenses through at least April 30, 2023.

Courage Under Fire

Kairos (ancient Greek): the opportune and decisive moment

January 1, 2023

Dear Fellow Shareholders,

At daybreak on June 17, 1775, colonial forces under the command of William Prescott gazed over the top of a strong redoubt they had constructed the prior night on Breed’s Hill in Charlestown, Massachusetts. The colonists were vastly outnumbered and short on gunpowder. As the British army advanced on their position, marking the beginning of the Battle of Bunker Hill, legend has it the colonists heard the famous orders: “Don’t fire until you can see the whites of their eyes!” To achieve maximum impact, they would wait until the threat was uncomfortably close before expending scarce resources. Investors take note.

Battle of Bunker Hill by Don Troiani

There are three types of edges in investing: informational, analytical, and behavioral. While there will always be opportunities for enterprising investors to uncover interesting nuggets on public companies, material informational advantages have dwindled due to technological advances and regulatory changes. Today, most active managers

1

PALM VALLEY CAPITAL FUND

attempt to differentiate and market themselves by their analytical approaches. They announce, “We buy undervalued companies with strong competitive advantages” or “Our quant model identifies growth stocks that are likely to continue to outperform.” However, the congruence in outcomes for most mutual funds indicates that advertised differences in investment styles have little practical impact when portfolios are overdiversified and markets are driven by central banks.

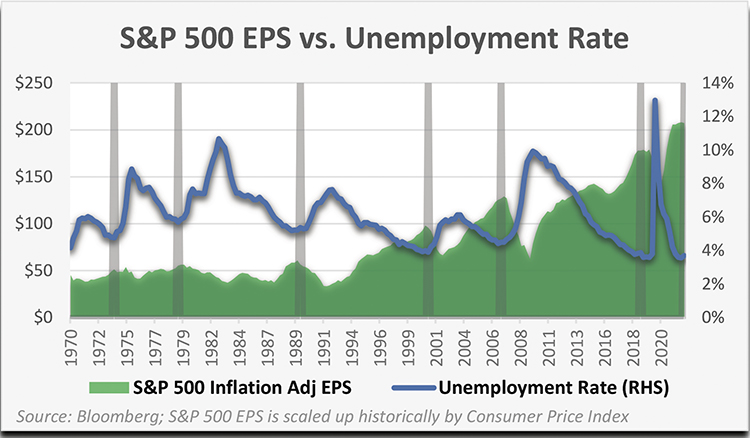

Most investors have abandoned the pursuit of a true analytical edge in favor of primarily analyzing the Federal Reserve’s words and actions. Dovish Fed = wind at our backs. Hawkish Fed = wind in our faces…no, they’ll come around. They always do! Except now, as the Fed attempts to extinguish the inflationary upswell of 2021 and 2022 that they ignored for too long, Fed members are telling investors the rate hikes won’t stop until the inflation genie is back in the bottle. And, they add, it will probably take job losses to achieve that outcome. Naturally, there is a rather strong historical relationship between corporate profits and employment. Right now, both are at a cyclical peak.

There is a growing camp of investors that thinks you’d be an idiot to ignore the Fed’s tough guy act, since it has been supported by consistent rate hikes throughout 2022. The Fed, with egg on their faces, must prove that they aren’t a one trick pony in the Asset Bubble Derby and actually will address inflation persisting above their stated 2% mandate. They’re doing it, belatedly, and with a balance sheet that remains gargantuan by any historical comparison. Still, with all the rate hikes and Fed jawboning, investors haven’t ignored the wink and nod to the Fed put. During the November 2, 2022, FOMC press conference, after repeatedly affirming the Fed’s determination to quell inflation, Chairman Powell made clear: “If we overtighten, then we have the ability with our tools, which are powerful, to, as we showed at the beginning of the pandemic episode, we can support economic activity strongly if that happens, if that’s necessary.”

The S&P 500 finished 2022 down 19% from its all-time high. We do not believe U.S. stocks are pricing in an extended period of higher interest rates or a decline in corporate profits. The 10-year Treasury yield fell over 80 basis points from its October peak to early December before rebounding over the last two weeks. Fed members themselves don’t even know where short-term rates will be in twelve months. A year ago, they were expecting the Fed Funds rate to end 2022 below 1%. We aren’t sure where inflation will settle and how long it will take to get there, but we feel strongly that the Fed will be less resistant to easing than it was to tightening. Pulling the proverbial punch bowl might be a no-brainer with underage guests and police on the scene, but these guys and gals like to party. You don’t make friends by punishing portfolios forever.

2

PALM VALLEY CAPITAL FUND

The finance and real estate sectors are, regrettably, beholden to the Fed. Millions of careers depend on the Fed’s magnanimity to asset owners. Billionaire Starwood Capital CEO Barry Sternlicht bleated on CNBC in December that the Fed’s rate hikes are “an assault on capitalism.” Eradicating the speculative, debt-fueled behavior that formed our modern economy likely involves much heavier lifting than coming off the zero bound for a year or two. But it’s a start. We don’t think the Fed is the shepherd that will lead our economy to a more sustainable place. Eventually, though, we believe we’ll get there, but not before crossing dark valleys of volatility. In our opinion, the key ingredients for future investment success could be very different than what worked the last dozen years.

A behavioral edge is the “je ne sais quoi” of an investment strategy. It’s the consistency of your discipline and ability to control your emotions when investing. If AC/DC had led the undersupplied defense of Breed’s Hill with a battle cry of Shoot to Thrill, we suspect it wouldn’t have worked out as well (“Pull it, pull it, pull the trigger!”). A behavioral edge allows you to exploit others’ haphazard decisions and use Mr. Market to achieve your investment objectives. Instead of using the Fed as a key input in our strategy, we focus on the businesses we would like to own. Do they meet our absolute return hurdles? If not, we’ll wait for the kairotic moment—the elusive fat pitch. For us, the regret associated with losing money on an investment that was never compelling far exceeds the disappointment from missing speculative gains. Some observers may interpret our patience as paralysis or a flawed methodology. Perhaps our low double-digit investment hurdles are now too high, since central banks bastardized investing over the last generation? We would strongly disagree that our strategy is antiquated.

Equity valuations have not reflected the compression seen during prior inflationary periods. In our opinion, average multiples are still hovering at higher-than-normal levels for two reasons: (1) investors do not expect higher interest rates to persist, and (2) they appear to think recent earnings are largely sustainable (with some exceptions).

3

PALM VALLEY CAPITAL FUND

We believe a world where interest rates are manipulated lower by central banks is ultimately self-correcting. Some of that is currently playing out, as the speculative boom of 2021, which was facilitated by the Fed, turned inflationary. This broad inflation was more poignant than the long period of asset inflation that preceded it, prompting a monetary policy reversal. Thinking beyond our current predicament, for extremely low interest rates to endure without kindling inflation would normally suggest a weak, slow growth economy. A stock’s capitalization rate is “k – g” (required return – growth rate), and if both are low, there is no expansion of the justified valuation multiple. The U.S. has been able to enhance its economic growth rate in recent decades from of an accumulation of debt, which will sap future growth.

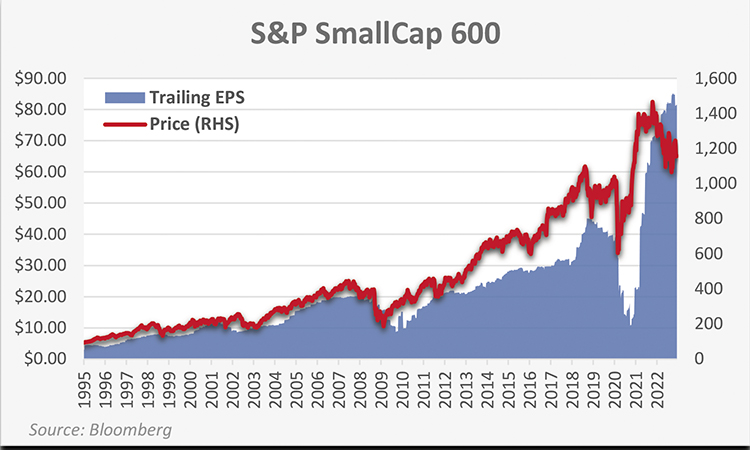

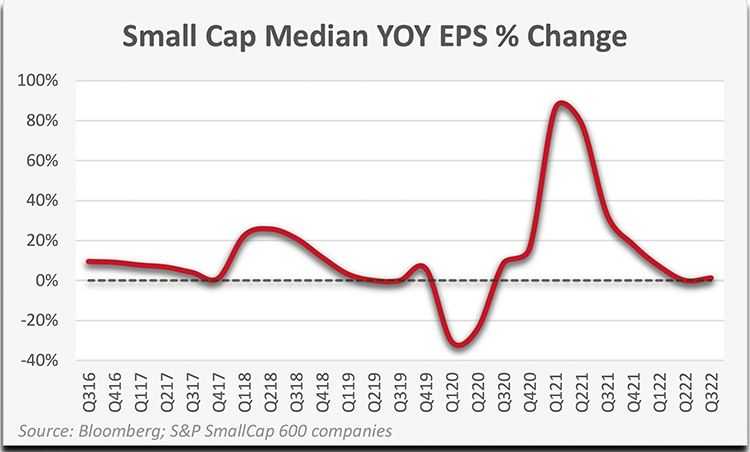

The second leg of support for bloated valuations — earnings — could be the catalyst that finally sends stocks reeling. Earnings for the S&P SmallCap 600 soared 113% from the end of 2019 to their peak in 2022. Margins for profitable small firms hit record levels in the second quarter and decreased slightly in Q3 due to inflation. Profits haven’t broken down broadly yet, as half of small caps still reported year-over-year earnings growth in the third quarter. To return to the average since the turn of the century, small cap margins would need to contract by about 25%.

We think the end draws nigh for the small cap profit cycle. The three sectors contributing most to the astonishing earnings growth of the small cap index (S&P 600) since 2019 are Energy, Financials, and Consumer Discretionary. Energy profits will face difficult comparisons in the coming quarters given the decline in oil prices from a summer peak above $120/bbl to $80/bbl at year end. As far as Financials, small cap banks bulked up on commercial real estate loans after the credit crisis, and we expect delinquencies to rise from very low levels. Key industries that drove Consumer Discretionary EPS expansion during the pandemic were homebuilders, RV manufacturers, and retailers. This sector has already begun to exhibit earnings weakness, with profits for the median company down 20% year-over-year in Q3 (from extremely elevated levels). Rising interest rates have dropkicked the housing market, as well as demand for RVs. The retail industry is mixed, with ongoing strength for some businesses and noticeable weakness for those catering to customers with less discretionary income. The plummeting reported personal savings rate reflects an

4

PALM VALLEY CAPITAL FUND

unwinding of the government’s pandemic transfers. If the job market softens according to the Fed’s plan and stimulus is not renewed, we imagine the retail space will become significantly more pressured. The employment rate took 10 years to fully recover after the 2008 credit crisis. While it may seem harsh, a recession could be needed to rebalance the labor market. It’s a good thing the Bureau of Labor Statistics doesn’t hedonically adjust customer service!

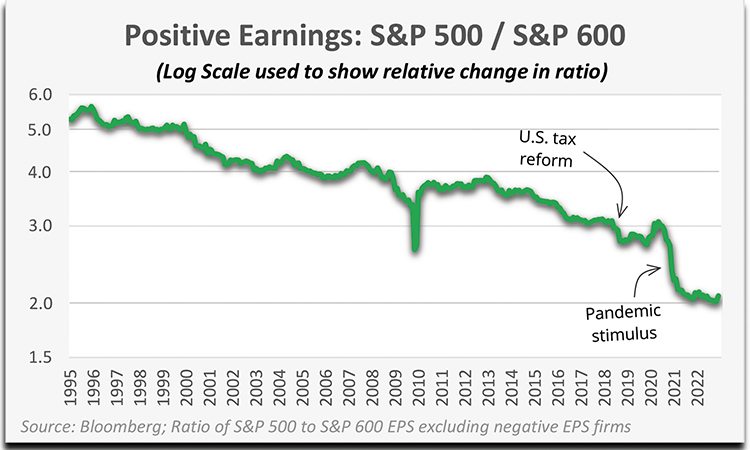

Earnings for profitable small caps compounded at nearly 11% annualized since 1995, exceeding the growth rate for large caps by over 3.5%. Although small firms are generally expected to produce faster growth, the recent boom catapulted small company profits beyond their long-term trend versus bigger firms (chart left), which is surprising considering earnings gushers from Apple, Microsoft, and Google. Tax cuts, share repurchases, falling interest rates, and corporate and federal borrowing were all catalysts that supported rising per share profits. Federal debt grew from $5 trillion in 1995 to $31 trillion today, making the $76 billion in total net income for companies in the S&P SmallCap 600 Index look like a drop in the bucket. Without growing deficits, we believe corporate earnings will lose a major tailwind, and small company profits could be disproportionately impacted.

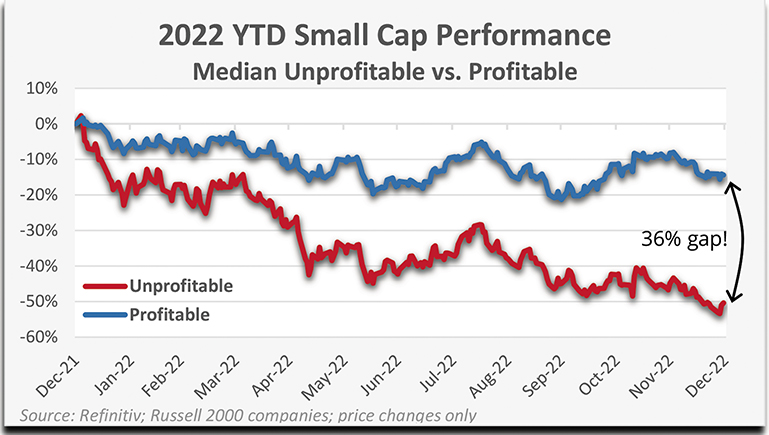

We don’t foresee a happy ending to this story where investors avoid steep losses. We expect there to be opportunities to deploy capital at our return hurdles, and 2022 offered hope that we were approaching those levels. However, the most severe casualties in 2022 were seen in highly speculative investments such as crypto assets and young, unprofitable companies. Money losing businesses in the Russell 2000 fell 50%

5

PALM VALLEY CAPITAL FUND

in 2022 (median), over 4x as much as profitable ones, which had a median loss of 12%, including dividends. Over the last two years, profitable small caps are higher, on average, by over 10%, while unprofitable ones registered more than a 50% median haircut. As far as we’re concerned, let the bodies hit the floor.

Extremely speculative investments generally do not belong in absolute return portfolios, in our opinion. Therefore, the vaporization of previous euphoric gains is primarily relevant to us in whether it is the prologue to a widespread drawdown. The mostly profitable S&P SmallCap 600 has an overall P/E of 15x, which may appear totally acceptable, but the Index multiple on pre-pandemic EPS is 33x. Additionally, the median company P/E based on trailing earnings is 19x. Based on our bottom-up analysis of the companies we follow, we are not seeing many discounts when valuing firms on normalized earnings and insisting on a double digit required return. At Palm Valley, we aren’t trying to time the market. We’re waiting for individual opportunities to come into our sights, and most high-quality small caps just aren’t there yet.

…………………………………………………………………………………………………………………………………………………………………………………………………………

For the quarter ending December 31, 2022, the Palm Valley Capital Fund (“the Fund”) increased 3.86% compared to a rise of 9.19% for the S&P SmallCap 600 Total Return Index and an 8.05% gain for the Morningstar Small Cap Total Return Index. The Fund lagged benchmarks during the fourth quarter due to our large cash position. At the end of the period, the Fund held 78.9% of assets in cash equivalents, which include U.S. Treasuries. The equities within the portfolio increased 15.36% for the three-month period and benefited from our above-average exposure to precious metals.

For the full 2022 year, the Fund rose 3.16%, while the S&P SmallCap 600 dropped 16.10% and the Morningstar Small Cap benchmark decreased 18.46%. The Fund’s equity holdings generally performed better than small cap benchmarks, with our stocks returning 13.04% in 2022. Currently, most of our positions are not included in popular U.S. small cap benchmarks such as the S&P SmallCap 600 and Russell 2000. However, we believe our favorable relative equity performance versus benchmarks was mainly because our companies tend to be mature and profitable, two characteristics that tended to improve 2022 returns.

6

PALM VALLEY CAPITAL FUND

During the year, the average daily yield offered on three-month U.S. Treasury bills was 2%, and it finished at 4.4%. We celebrate higher risk-free yields, and they made a welcome contribution to our performance in 2022. Nevertheless, the rise in short-term rates does not directly impact our equity valuations or timing of investment. We believe this differentiates Palm Valley from most investment managers who use a fluid cost of capital calculation as opposed to a more rigid absolute return hurdle—ours is 10% to 15% for our equities. We are familiar with the consequences of holding zero yielding cash when expensive stocks keep ascending. However, our strategy will accept relative performance shortfalls in an attempt to guard against material drawdowns and preserve our flexibility to act when valuations are ripe. Consider the Fund’s performance (ticker: PVCMX) since inception versus the S&P SmallCap 600 and Russell 2000 Indexes, separated by year (partial year in 2019 from the Fund’s April 30, 2019, launch):

In retrospect, our performance journey may appear mundane in every period except 2020. From our perspective, Spring 2020 was the only time since the Fund’s inception that the small cap market offered a sizeable number of opportunities meeting our required return threshold. Of course, when stocks were on the verge of becoming truly cheap during the beginning of the pandemic, the Fed unleashed its “powerful tools” to reignite the equity bull market. While we will be unsurprised by similar Fed actions in the future, we think the likelihood of an unencumbered rebound in stocks is diminishing, given the threat of inflation and fatigue from wealth inequality.

The Fund’s lower volatility has been primarily due to our cash position. Since inception, the Fund’s annualized standard deviation of returns is 6.6% compared to 29.7% for the S&P SmallCap 600 and Russell 2000. However, the standard deviation of the Fund’s equities is 24.1% since inception. Lower volatility is sometimes a byproduct of our strategy, but it is not something we are specifically targeting. In fact, while we prefer to invest in high quality businesses with predictable cash flows, which are easier to value, we are willing to invest in sectors with greater historical volatility, such as energy and materials (e.g., precious metals). Enduring expensive valuations among higher quality American firms have led us to less popular areas among U.S. investors like commodity-oriented companies and businesses with foreign exposure.

7

PALM VALLEY CAPITAL FUND

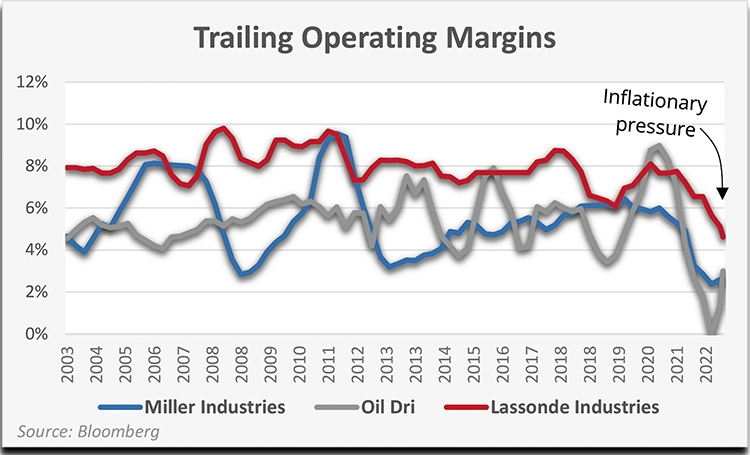

One theme for the Fund during 2022 was our investment in companies exhibiting margins that are below normal levels, generally because of inflationary factors. We believe this contrasts with the overall market’s above-average profitability. Fund holdings that fit this bill include Miller Industries (ticker: MLR), Oil Dri (ticker: ODC), Lassonde Industries (ticker: LAS/A CN), and Hooker Furnishings (ticker: HOFT). In the first three cases, we believe the catalysts for improved profitability are the price increases the companies are currently pushing through to customers. Miller Industries, for example, will have raised its tow truck prices by nearly one-third from the beginning of 2021 through January 2023. Lassonde’s fruit juice prices rose 12% year-over-year in Q3, while Oil Dri’s product pricing was up roughly 20% from the prior year. Hooker Furnishings’ margin problems have been caused by issues besides inflation, and we believe these are resolving; nevertheless, signature Hooker Branded average selling prices are approximately 30% higher over two years. For certain businesses, the lag between cost inflation and price realization presented investment opportunities in 2022, in our judgment.

We did not purchase any new holdings during the fourth quarter. We sold three positions entirely: Heartland Express (ticker: HTLD), Alamos Gold (ticker: AGI), and Smith & Nephew plc (ticker: SNN). Heartland took on leverage for an acquisition, which increased the company’s financial risk. Alamos and Smith & Nephew appreciated quickly after purchase and exceeded our calculated valuations. We also meaningfully reduced our weightings in Amdocs (ticker: DOX), Osisko Gold Royalties (ticker: OR), and Oil Dri (ticker: ODC) as their stock prices approached fair value.

The three positions contributing most to the Fund’s fourth quarter performance were the Sprott Physical Silver Trust (ticker: PSLV), Oil Dri, and Miller Industries. Silver prices gained 26% in the fourth quarter. Medium-term interest rate expectations peaked in mid-October, then began to slide. Investors’ anticipation of a Fed pivot supported precious metals, which held most gains through the end of the quarter, even as equities sold off in December. The silver market has lately demonstrated more strength than gold, a function of its higher volatility and, potentially, suspected shortages in the market for physical silver. Oil Dri’s revenues rose 19% in Q4 due to price increases, fueling expanding gross margins across its product line, which ranges from cat litter to industrial absorbents. Oil Dri may be closer to the finish line in raising prices than some of the Fund’s other positions that were acquired under a similar thesis. Miller Industries, which has also pushed through significant pricing, has seen a partial recovery in margins this year.

8

PALM VALLEY CAPITAL FUND

During the quarter, the only holding negatively impacting the Fund by at least 10 basis points was WH Group (ticker: WHGLY). Strong revenue and profit growth year-to-date have been overshadowed by a more cautious outlook due to cost inflation and the near-term impact of China relaxing its zero-COVID policies. The shares trade for less than 5x trailing operating profit.

For the full calendar year, the Fund’s top performers were Coterra Energy (ticker: CTRA), Amdocs, and Alamos Gold. Coterra’s stock rose sharply along with energy prices at the beginning of 2022. Amdocs delivered record operating results during the year and demonstrated the strength of its market position serving the world’s leading communication service providers. All the Fund’s precious metals holdings, led by Alamos, contributed positively to performance in 2022, with a 1% collective contribution from gold and silver equities. We think this was a good outcome relative to gold and silver prices that ended the year essentially flat, after a summer swoon. Additionally, precious metals miners were down, on average, in 2022.

The Fund’s primary 2022 detractors were Crawford & Co. (tickers: CRD/A, CRD/B) and Lassonde Industries (ticker: LAS/A CN). Crawford’s shares were by far the largest drag on the portfolio during the year, which could reflect an apparent lack of urgency by management to restore profitability in the company’s international operations. Additionally, Crawford’s leverage increased over the past 18 months to fund acquisitions. We think the valuation is attractive at 5-6x normalized EV/EBITA, and potential near-term catalysts include an abatement of tax loss selling, year-end cash collections that will reduce leverage, and a boost in fourth quarter catastrophe-related claims revenue tied to Hurricane Ian.

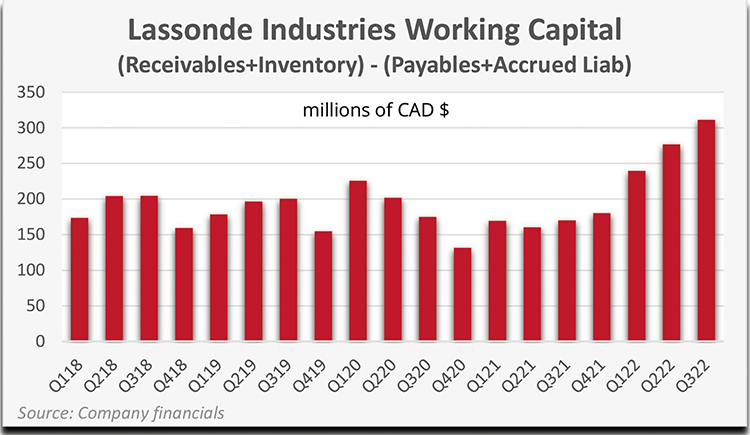

We acquired Lassonde Industries midway through 2022 at a multiyear low, but the Canadian-domiciled company’s stock continued to sink and now trades for 6x our estimate of normalized operating income. Profits have been negatively impacted by inflationary pressures for packaging, apple and orange concentrates, and transportation costs. Management is aggressively raising prices for its branded and private label fruit juice and drink offerings. The company intends to make significant capital investments to improve the performance of its lagging U.S. operations.

9

PALM VALLEY CAPITAL FUND

Management announced that because supply chain challenges were fading, Lassonde is revising its inventory accumulation strategy and expects to reduce inventory levels. Elevated working capital is a common theme among public firms at the moment, and we wonder what the collective impact will be of a synchronized pullback.

…………………………………………………………………………………………………………………………………………………………………………………………………………

“The two most powerful warriors are patience and time.”

Leo Tolstoy

On the eleventh hour of the eleventh day of the eleventh month of 1918, fighting in World War I officially ceased after Germany signed an Armistice with the Allied Powers earlier that day. In October, Netflix released a remake of All Quiet on the Western Front (spoilers ahead). The movie follows a young German soldier during WWI and is “possibly one of the most searing and soul-crushing depictions of warfare that has ever muddied the screen,” according to USA Today.

The film opens as young, excited German volunteers are issued uniforms—unaware that these had belonged to dead soldiers. Paul, the protagonist, who lied about his age to serve, is immediately sent to the front line, where his life is saved in the trenches by a veteran comrade. Shellshocked and helpless, Paul is ordered to collect the dog tags of the deceased. What follows is an extreme amount of hunger, death, suffering, and hopelessness that transforms Paul from an eager 17-year-old recruit to a gaunt, desperate warrior fighting to survive another day. Each of his friends is killed, with Paul’s last comrade shot by a farmer’s son after attempting to steal a goose for the second time. Meanwhile, the beleaguered German leadership reluctantly agrees to onerous terms imposed by their French counterparts to stop fighting precisely at 11:00am on November 11, 1918. Nevertheless, the intransigent General Friedrichs orders his remaining, depleted forces to engage in a final battle the morning before the armistice takes effect. Paul is fighting in the trenches again, and it appears he will survive until the clock strikes 11. Sadly, he is critically wounded in the final seconds of the war, and he staggers out of the bunker to catch one last glimpse of daylight and peace.

10

PALM VALLEY CAPITAL FUND

The message of the film is futility. With machine guns and mustard gas, WWI fighting was routinely chaotic— “whites of their eyes” restraint was missing in action. Almost twenty million people died from the war, including three million soldiers on the Western Front, a 400+ mile line of trenches between France and Germany. Despite this enormous toll, neither side gained significant ground at the front lines at any time. Symbolically, the penultimate death among Paul’s crew happened after a literal wild goose chase.

A wild goose chase is the foolish and hopeless pursuit of something unattainable. The consequences of war overshadow anything else, but as far as careers are concerned, modern absolute return investors are accustomed to feelings of despair. It can be argued that since the emergence of the Fed put, it’s a fool’s errand to normalize profits and wait for equity multiples to revert to historical levels before buying. At Palm Valley, we fight this battle daily.

On the other hand, maybe the real wild goose chase is the attempted elimination of the business cycle by the U.S. government and Federal Reserve. While the U.S. was long viewed as the world’s premier free market economy, we’re clearly headed in the other direction with increasing government intervention. For the most part, those complaining now about Fed rate hikes were not bemoaning the rate suppression that came first. Yet, what’s good for the goose is good for the gander. It’s time to clean up the mess.

Fed members blundered in their initial nonreaction to spiking inflation; however, by the end of 2022 they were communicating and delivering a more hawkish monetary policy than we have seen in several years. Stocks fell, but not nearly as much as one who believed we were permanently off the zero bound might expect. At this juncture, you can either invest based on a belief in business cycles and normalization or invest based on faith that the economy can be successfully managed forever.

As for us, like the colonists near Bunker Hill, we’ll wait patiently on higher ground for real opportunities to materialize, instead of hanging out in the trenches on the front lines in the expectation of an eleventh-hour bailout.

11

PALM VALLEY CAPITAL FUND

Thank you for your investment.

Sincerely,

| Jayme Wiggins | Eric Cinnamond |

Mutual fund investing involves risk. Principal loss is possible. The Palm Valley Capital Fund invests in smaller sized companies, which involve additional risks such as limited liquidity and greater volatility than large capitalization companies. The ability of the Fund to meet its investment objective may be limited to the extent it holds assets in cash (or cash equivalents) or is otherwise uninvested.

Before investing in the Palm Valley Capital Fund, you should carefully consider the Fund’s investment objectives, risks, charges, and expenses. The Prospectus contains this and other important information and it may be obtained by calling 904-747-2345. Please read the Prospectus carefully before investing.

Past performance is no guarantee of future results. Dividends are not guaranteed and a company’s future ability to pay dividends may be limited. A company currently paying dividends may cease paying dividends at any time. Fund holdings and sector allocations are subject to change and are not a recommendation to buy or sell any security. Earnings growth for a Fund holding does not guarantee a corresponding increase in the market value of the holding or the Fund.

The S&P SmallCap 600 Total Return Index measures the small cap segment of the U.S. equity market. The index is designed to track companies that meet specific inclusion criteria to ensure that they are liquid and financially viable. The Morningstar Small Cap Total Return Index tracks the performance of U.S. small-cap stocks that fall between 90th and 97th percentile in market capitalization of the investable universe. It is not possible to invest directly in an index.

The Palm Valley Capital Fund is distributed by Quasar Distributors, LLC. Opinions expressed are those of the author, are subject to change at any time, are not guaranteed and should not be considered investment advice.

12

PALM VALLEY CAPITAL FUND

Definitions:

Basis point: One hundredth of a percentage point (0.01%).

bbl: Abbreviation for one barrel of oil (42 U.S. gallons liquid volume).

CAD: Canadian dollar.

CPI (Consumer Price Index): A measure that examines the weighted average of prices of a basket of consumer goods and services.

Dot Plot: Chart that records each Fed member’s projection for the Federal Funds Rate.

EBITA: Earnings Before Interest, Taxes, and Amortization of acquired intangibles (i.e., operating income).

Enterprise Value (EV): Market Cap plus total debt minus cash equivalents, adjusting for noncontrolling interests.

EPS (Earnings per share): Net income divided by shares outstanding.

Federal Funds Rate: The interest rate that banks charge each other for lending money on an overnight basis.

Fed put: A belief that the Federal Reserve will always rescue the financial markets.

FOMC (Federal Open Market Committee): A committee of the Federal Reserve Board that meets regularly to set monetary policy, including the interest rates that are charged to banks.

Free Cash Flow: Free Cash Flow equals Cash from Operating Activities minus Capital Expenditures.

P/E Ratio: A stock’s price divided by its earnings per share.

Russell 2000: The Russell 2000 Index is an American small-cap stock market index based on the market capitalizations of the bottom 2,000 companies in the Russell 3000 Index.

S&P 500: The Standard & Poor’s 500 is an American stock market index based on the market capitalizations of 500 large companies.

Standard deviation: A measure of the dispersion of a dataset around its average.

Working Capital: The difference between a company’s current assets and current liabilities.

YOY (year-over-year): Analysis of results from one time period with those from another time period one year earlier.

Zero Bound: Monetary policy tool where a central bank reduces short-term interest rates to zero to stimulate the economy.

13

PALM VALLEY CAPITAL FUND

Value of $10,000 Investment (Unaudited)

The chart assumes an initial investment of $10,000. Performance reflects waivers of fees and operating expenses in effect. In the absence of such waivers, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate, so that your shares, when redeemed, may be worth more or less than their original cost. Performance assumes the reinvestment of capital gains and income distributions. The performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Rates of Return (%) – As of December 31, 2022

1 Year | 3 Years | Since Inception(1) | |

| Palm Valley Capital Fund | 3.16% | 8.43% | 7.24% |

S&P SmallCap 600 Index(2) | -16.10% | 5.80% | 6.36% |

(1) | Inception date of the Fund was May 1, 2019. |

(2) | The S&P SmallCap 600 Index is a capitalization-weighted index that measures the performance of selected U.S. stocks with small market capitalization. |

14

PALM VALLEY CAPITAL FUND

Expense Example (Unaudited)

December 31, 2022

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including management fees and other Fund specific expenses. The expense example is intended to help the shareholder understand ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the most recent six-month period.

The Actual Expenses comparison provides information about actual account values and actual expenses. A shareholder may use the information in this line, together with the amount invested, to estimate the expenses paid over the period. A shareholder may divide his/her account value by $1,000 (e.g., an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses paid on his/her account during this period.

The Hypothetical Example for Comparison Purposes provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses paid for the period. A shareholder may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, a shareholder would compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

The expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemptions fees or exchange fees. Therefore, the Hypothetical Example for Comparisons Purposes is useful in comparing ongoing costs only and will not help to determine the relevant total costs of owning different funds. In addition, if these transactional costs were included, shareholder costs would have been higher.

| Annualized Net | Beginning | Ending | Expenses Paid | |

| Expense Ratio | Account Value | Account Value | During Period(1) | |

(12/31/2022) | (7/1/2022) | (12/31/2022) | (7/1/2022 to 12/31/2022) | |

| Investor Class | ||||

Actual(2) | 1.25% | $1,000.00 | $1,019.60 | $6.36 |

| Hypothetical | ||||

| (5% annual return before expenses) | 1.25% | $1,000.00 | $1,018.90 | $6.36 |

(1) | Expense are equal to the Fund’s annualized expense ratio for the period multiplied by the average account value over the period, multiplied by 184/365 to reflect its six-month period. |

(2) | Based on the actual returns for the period from July 1, 2022 through December 31, 2022, of 1.96% for Investor Class. |

15

PALM VALLEY CAPITAL FUND

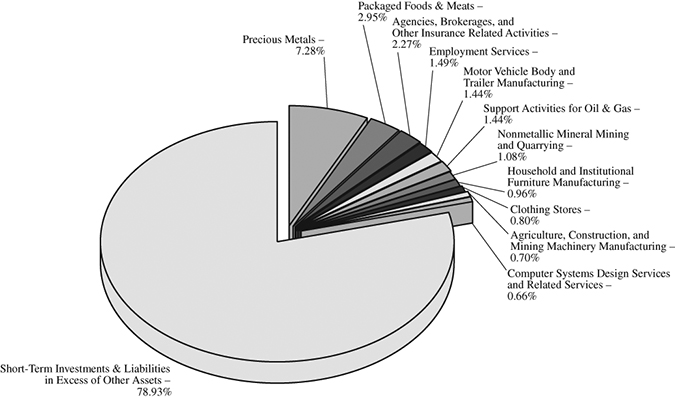

Allocation of Portfolio (Unaudited)

As of December 31, 2022

(% of Net Assets)

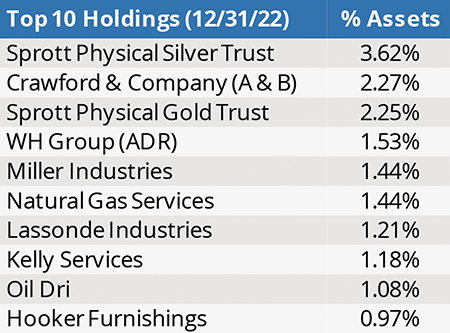

Top 10 Equity Holdings(1) (Unaudited)

As of December 31, 2022

(% of Net Assets)

| Sprott Physical Silver Trust | 3.62% | ||

| Crawford & Co., Class A & Class B | 2.27% | ||

| Sprott Physical Gold Trust | 2.12% | ||

| WH Group Ltd. – ADR | 1.53% | ||

| Miller Industries Inc. | 1.44% | ||

| Natural Gas Services Group, Inc. | 1.44% | ||

| Lassonde Industries, Inc., Class A | 1.22% | ||

| Kelly Services, Inc. | 1.18% | ||

| Oil-Dri Corp. of America | 1.08% | ||

| Hooker Furnishings Corp. | 0.97% |

(1) | Fund Holdings and Sector allocations are subject to change at any time and are not recommendations to buy or sell any security. |

16

PALM VALLEY CAPITAL FUND

Schedule of Investments

December 31, 2022

| Shares | Value | |||||||

| COMMON STOCKS – 21.07% | ||||||||

| Agencies, Brokerages, and Other Insurance Related Activities – 2.27% | ||||||||

| Crawford & Co., Class A | 708,180 | $ | 3,937,481 | |||||

| Crawford & Co., Class B | 52,723 | 279,959 | ||||||

| 4,217,440 | ||||||||

| Agriculture, Construction, and Mining | ||||||||

| Machinery Manufacturing – 0.70% | ||||||||

| Gencor Industries, Inc. (a) | 128,399 | 1,296,830 | ||||||

| Clothing Stores – 0.80% | ||||||||

| Carter’s, Inc. | 19,838 | 1,480,113 | ||||||

| Computer Systems Design Services and Related Services – 0.66% | ||||||||

| Amdocs Ltd. (b) | 13,565 | 1,233,059 | ||||||

| Employment Services – 1.49% | ||||||||

| Kelly Services, Inc. | 130,256 | 2,201,326 | ||||||

| ManpowerGroup, Inc. | 6,939 | 577,394 | ||||||

| 2,778,720 | ||||||||

| Household and Institutional Furniture Manufacturing – 0.96% | ||||||||

| Hooker Furnishings Corp. | 96,017 | 1,795,518 | ||||||

| Motor Vehicle Body and Trailer Manufacturing – 1.44% | ||||||||

| Miller Industries Inc. | 100,479 | 2,678,770 | ||||||

| Packaged Foods & Meats – 2.95% | ||||||||

| Lassonde Industries, Inc., Class A (b) | 27,501 | 2,260,200 | ||||||

| Nathan’s Famous, Inc. | 5,802 | 389,953 | ||||||

| WH Group Ltd. – ADR | 244,353 | 2,841,825 | ||||||

| 5,491,978 | ||||||||

| Nonmetallic Mineral Mining and Quarrying – 1.08% | ||||||||

| Oil-Dri Corp. of America | 59,914 | 2,009,516 | ||||||

| Precious Metals – 7.28% | ||||||||

| Osisko Gold Royalties Ltd. (b) | 103,459 | 1,248,750 | ||||||

| Sprott Physical Gold Trust (a)(b) | 296,769 | 4,184,443 | ||||||

| Sprott Physical Silver Trust (a)(b) | 817,755 | 6,738,301 | ||||||

| SSR Mining, Inc. (b) | 86,941 | 1,362,366 | ||||||

| 13,533,860 | ||||||||

The accompanying notes are an integral part of these financial statements.

17

PALM VALLEY CAPITAL FUND

Schedule of Investments – Continued

December 31, 2022

| Shares | Value | |||||||

| COMMON STOCKS – 21.07% (Continued) | ||||||||

| Support Activities for Oil & Gas – 1.44% | ||||||||

| Natural Gas Services Group, Inc. (a) | 233,524 | $ | 2,676,185 | |||||

| Total Common Stocks | ||||||||

| (Cost $39,345,919) | 39,191,989 | |||||||

| SHORT-TERM INVESTMENTS – 78.94% | ||||||||

| Money Market Fund – 10.63% | ||||||||

| First American Treasury Obligations Fund, Class X, 4.18% (c) | 19,770,746 | 19,770,746 | ||||||

| Principal | ||||||||

| Amount | ||||||||

| US Treasury Bills – 68.31% | ||||||||

| Maturity Date: 1/5/2023, Yield to Maturity: 2.56% | $ | 20,000,000 | 19,995,967 | |||||

| Maturity Date: 1/19/2023, Yield to Maturity: 2.97% | 36,211,000 | 36,152,821 | ||||||

| Maturity Date: 3/2/2023, Yield to Maturity: 3.49% | 23,765,000 | 23,602,893 | ||||||

| Maturity Date: 4/20/2023, Yield to Maturity: 4.45% | 35,439,000 | 34,977,485 | ||||||

| Maturity Date: 6/1/2023, Yield to Maturity: 4.65% | 12,544,000 | 12,310,498 | ||||||

| 127,039,664 | ||||||||

| Total Short-Term Investments | ||||||||

| (Cost $146,837,767) | 146,810,410 | |||||||

| Total Investments | ||||||||

| (Cost $186,183,686) – 100.01% | 186,002,399 | |||||||

| Liabilities in Excess of Other Assets – (0.01)% | (24,051 | ) | ||||||

| Total Net Assets – 100.00% | $ | 185,978,348 | ||||||

| (a) | Non-income producing security. |

| (b) | Foreign security. |

| (c) | The rate quoted is the annualized seven-day effective yield as of December 31, 2022. |

ADR – American Depository Receipt

The accompanying notes are an integral part of these financial statements.

18

PALM VALLEY CAPITAL FUND

Statement of Assets and Liabilities

December 31, 2022

| ASSETS: | ||||

| Investments, at value (Cost $186,183,686) | $ | 186,002,399 | ||

| Receivable for fund shares sold | 230,424 | |||

| Dividends and interest receivable | 70,166 | |||

| Prepaid expenses and other receivables | 35,012 | |||

| Total assets | 186,338,001 | |||

| LIABILITIES: | ||||

| Payable to Adviser | 96,971 | |||

| Distribution fees payable | 82,880 | |||

| Payable for fund shares redeemed | 73,405 | |||

| Payable for fund administration and fund accounting fees | 28,386 | |||

| Payable for audit fees | 17,500 | |||

| Payable for transfer agent fees and expenses | 13,821 | |||

| Payable for custodian fees | 4,704 | |||

| Payable for compliance fees | 2,690 | |||

| Payable for directors fees | 48 | |||

| Accrued expenses and other liabilities | 39,248 | |||

| Total liabilities | 359,653 | |||

| NET ASSETS | $ | 185,978,348 | ||

| NET ASSETS CONSIST OF: | ||||

| Paid-in capital | $ | 185,046,341 | ||

| Total distributable earnings | 932,007 | |||

| Total net assets | $ | 185,978,348 | ||

| Investor Class | ||||

| Shares | ||||

| Net assets | $ | 185,978,348 | ||

Shares issued and outstanding(1) | 15,525,577 | |||

| Net asset value, offering, and redemption price per share | $ | 11.98 | ||

(1) | Unlimited shares authorized without par value. |

The accompanying notes are an integral part of these financial statements.

19

PALM VALLEY CAPITAL FUND

Statement of Operations

For the Year Ended December 31, 2022

| INVESTMENT INCOME: | ||||

| Dividend income (net of foreign taxes of $9,869) | $ | 622,899 | ||

| Interest income | 2,045,465 | |||

| Total investment income | 2,668,364 | |||

| EXPENSES: | ||||

| Investment advisory fees (See Note 3) | 1,365,914 | |||

| Distribution fees (See Note 5) | 379,420 | |||

| Fund administration and fund accounting fees (See Note 3) | 146,696 | |||

| Transfer agent fees (See Note 3) | 100,924 | |||

| Sub-transfer agent fees | 85,698 | |||

| Federal and state registration fees | 58,967 | |||

| Legal fees | 33,831 | |||

| Custodian fees (See Note 3) | 24,026 | |||

| Audit fees | 17,500 | |||

| Compliance fees (See Note 3) | 15,017 | |||

| Trustees’ fees (See Note 3) | 14,188 | |||

| Reports to shareholders | 13,377 | |||

| Other | 13,425 | |||

| Total expenses before waiver/reimbursement | 2,268,983 | |||

| Less: Expense waiver/reimbursement by Adviser (See Note 3) | (371,880 | ) | ||

| Net expenses | 1,897,103 | |||

| NET INVESTMENT INCOME | 771,261 | |||

| REALIZED AND CHANGE IN UNREALIZED GAIN (LOSS) ON INVESTMENTS: | ||||

| Net realized gain (loss) on: | ||||

| Investments | 4,261,746 | |||

| Foreign currency transactions | (3,981 | ) | ||

| Net realized gain | 4,257,765 | |||

| Net change in unrealized depreciation on investments | ||||

| Investments | (489,593 | ) | ||

| Foreign currency translation | (28 | ) | ||

| Net change in unrealized depreciation | (489,621 | ) | ||

| Net realized and change in unrealized gain on investments | 3,768,144 | |||

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 4,539,405 | ||

The accompanying notes are an integral part of these financial statements.

20

PALM VALLEY CAPITAL FUND

Statements of Changes in Net Assets

| For the | For the | |||||||

| Year Ended | Year Ended | |||||||

| December 31, 2022 | December 31, 2021 | |||||||

| OPERATIONS: | ||||||||

| Net investment income | $ | 771,261 | $ | (443,269 | ) | |||

| Net realized gain on investments and foreign currency transactions | 4,257,765 | 1,831,627 | ||||||

| Change in unrealized depreciation on investments | ||||||||

| and foreign currency translation | (489,621 | ) | (562,225 | ) | ||||

| Net increase in net assets resulting from operations | 4,539,405 | 826,133 | ||||||

| DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||

| From distributable earnings | (4,199,296 | ) | (1,535,165 | ) | ||||

| CAPITAL SHARE TRANSACTIONS: | ||||||||

Net increase in net assets resulting from capital share transactions(1) | 106,117,894 | 55,626,816 | ||||||

| NET INCREASE IN NET ASSETS | 106,458,003 | 54,917,784 | ||||||

| NET ASSETS: | ||||||||

| Beginning of year | 79,520,345 | 24,602,561 | ||||||

| End of year | $ | 185,978,348 | $ | 79,520,345 | ||||

(1) | A summary of capital shares is as follows: |

| For the Year Ended | For the Year Ended | |||||||||||||||

| December 31, 2022 | December 31, 2021 | |||||||||||||||

| SHARE TRANSACTIONS: | ||||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||

| Issued | 11,481,821 | $ | 138,071,659 | 5,333,242 | $ | 64,697,067 | ||||||||||

| Issued to holders in | ||||||||||||||||

| reinvestment of dividends | 345,482 | 4,131,972 | 109,635 | 1,302,461 | ||||||||||||

| Redeemed | (2,994,607 | ) | (36,087,734 | ) | (855,621 | ) | (10,377,709 | ) | ||||||||

| Redemption fees | — | 1,997 | — | 4,997 | ||||||||||||

| Net increase in shares outstanding | 8,832,696 | $ | 106,117,894 | 4,587,256 | $ | 55,626,816 | ||||||||||

The accompanying notes are an integral part of these financial statements.

21

PALM VALLEY CAPITAL FUND

Financial Highlights

| For the | For the | For the | For the | |||||||||||||

| Year Ended | Year Ended | Year Ended | Year Ended | |||||||||||||

| December 31, 2022 | December 31, 2021 | December 31, 2020 | December 31, 2019(1) | |||||||||||||

| Investor Class | ||||||||||||||||

PER SHARE DATA(2): | ||||||||||||||||

| Net asset value, beginning of period | $ | 11.88 | $ | 11.68 | $ | 10.07 | $ | 10.00 | ||||||||

| INVESTMENT OPERATIONS: | ||||||||||||||||

Net investment income (loss)(3) | 0.06 | (0.11 | ) | (0.06 | ) | 0.05 | ||||||||||

| Net realized and unrealized | ||||||||||||||||

| gain on investments | 0.31 | 0.54 | 1.99 | 0.09 | ||||||||||||

| Total from investment operations | 0.37 | 0.43 | 1.93 | 0.14 | ||||||||||||

| LESS DISTRIBUTIONS FROM: | ||||||||||||||||

| Net investment income | (0.05 | ) | — | — | (0.04 | ) | ||||||||||

| Net realized gains | (0.22 | ) | (0.23 | ) | (0.32 | ) | (0.03 | ) | ||||||||

| Total distributions | (0.27 | ) | (0.23 | ) | (0.32 | ) | (0.07 | ) | ||||||||

| Redemption fees | 0.00 | (4) | 0.00(4 | ) | 0.00 | (4) | — | |||||||||

| Net asset value, end of period | $ | 11.98 | $ | 11.88 | $ | 11.68 | $ | 10.07 | ||||||||

TOTAL RETURN(5) | 3.16 | % | 3.72 | % | 19.12 | % | 1.42 | % | ||||||||

| SUPPLEMENTAL DATA AND RATIOS: | ||||||||||||||||

| Net assets, end of | ||||||||||||||||

| period (in thousands) | $ | 185,978 | $ | 79,520 | $ | 24,603 | $ | 4,652 | ||||||||

| Ratio of gross expenses | ||||||||||||||||

| to average net assets: | ||||||||||||||||

Before expense reimbursement(6) | 1.50 | % | 1.78 | % | 3.38 | % | 7.25 | % | ||||||||

After expense reimbursement(6) | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | ||||||||

| Ratio of net investment income (loss) | ||||||||||||||||

| to average net assets | 0.51 | % | -0.89 | % | -0.51 | % | 0.79 | % | ||||||||

Portfolio turnover rate(5)(7) | 72 | % | 82 | % | 196 | % | 128 | % | ||||||||

(1) | Inception date of the Fund was May 1, 2019. |

(2) | For an Investor share outstanding for the period. |

(3) | Calculated based on average shares outstanding during the period. |

(4) | Amount per share is less than $0.005. |

(5) | Not annualized for periods less than one year. |

(6) | Annualized for periods less than one year. |

(7) | The portfolio turnover disclosed is for the Fund as a whole. The numerator for the portfolio turnover rate includes the lesser of purchases or sales (excluding short-term investments). The denominator includes the average fair value of long positions throughout the period. |

The accompanying notes are an integral part of these financial statements.

22

PALM VALLEY CAPITAL FUND

Notes to the Financial Statements

December 31, 2022

1. ORGANIZATION

Series Portfolios Trust (the “Trust”) is a Delaware statutory trust organized on July 27, 2015, and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Palm Valley Capital Fund (the “Fund”) is a diversified series with its own investment objectives and policies within the Trust. The Fund’s investment adviser, Palm Valley Capital Management LLC (the “Adviser”), is responsible for investment advisory services, day-to-day management of the Fund’s assets, as well as compliance, sales, marketing, and operation services to the Fund. The Fund invests primarily in a portfolio of U.S. common stocks of small-cap companies that offer attractive risk-adjusted returns. The Fund considers small-cap companies to be those that, at the time of investment, have a market capitalization of less than $10 billion. Under normal circumstances, the Fund will hold common stocks of fewer than 40 different companies.

The Fund commenced operations on May 1, 2019. The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (the “Codification”) Topic 946 Financial Services – Investment Companies. The Fund does not hold itself out as related to any other series of the Trust for purposes of investment and investor services, nor does it share the same investment adviser with any other series of the Trust.

The Fund offers a single share class, an Investor Class. The Investor Class does not have front end sales loads or deferred sales charges. The Fund is subject to a distribution fee of up to 0.25% of average daily net assets.

The Fund may issue an unlimited number of shares of beneficial interest, with no par value.

2. SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”).

A. Investment Valuation – The following is a summary of the Fund’s pricing procedures. It is intended to be a general discussion and may not necessarily reflect all the pricing procedures followed by the Fund. Equity securities, including common stocks, preferred stocks, and real estate investment trusts (“REITS”) that are traded on a national securities exchange, except those listed on the Nasdaq Global Market®, Nasdaq Global Select Market® and the Nasdaq Capital Market® exchanges (collectively “Nasdaq”), are valued at the last reported sale price on that exchange on which the security is principally traded. Securities traded on Nasdaq will be valued at the Nasdaq Official Closing Price (“NOCP”). If, on a particular day, an exchange traded or Nasdaq security does not trade, then the mean between the most recent quoted bid and asked prices will be used. All equity securities that are not traded on a listed exchange are valued at the last sale price in the over-the-counter (“OTC”) market. If a non-exchanged traded equity security does not trade on a particular day, then the mean between the last quoted closing bid and asked price will be used. To the extent these securities are actively traded, and valuation adjustments are not applied, they are categorized in Level 1 of the fair value hierarchy.

Fixed income securities, including short-term debt instruments having a maturity less than 60 days, are valued at the evaluated mean price supplied by an approved independent third-party pricing service (“Pricing Service”). These securities are categorized in Level 2 of the fair value hierarchy.

23

PALM VALLEY CAPITAL FUND

Notes to the Financial Statements – Continued

December 31, 2022

In the case of foreign securities, the occurrence of events after the close of foreign markets, but prior to the time the Fund’s net asset value (“NAV”) is calculated will result in an adjustment to the trading prices of foreign securities when foreign markets open on the following business day. The Fund will value foreign securities at fair value, taking into account such events in calculating the NAV. In such cases, use of fair valuation can reduce an investor’s ability to seek profit by estimating the Fund’s NAV in advance of the time the NAV is calculated. These securities are categorized in Level 2 of the fair value hierarchy.

Exchange traded funds and closed-end funds are valued at the last reported sale price on the exchange on which the security is principally traded. If, on a particular day, an exchange traded fund does not trade, then the mean between the most recent quoted bid and asked prices will be used. To the extent these securities are actively traded, and valuation adjustments are not applied, they are categorized in Level 1 of the fair value hierarchy.

Investments in registered open-end investment companies (including money market funds), other than exchange traded funds, are valued at their reported NAV per share. To the extent these securities are valued at their NAV per share, they are categorized in Level 1 of the fair value hierarchy.

The Board of Trustees (the “Board”) has adopted a pricing and valuation policy for use by the Fund and its Valuation Designee (as defined below) in calculating the Fund’s NAV. Pursuant to Rule 2a-5 under the 1940 Act, the Fund has designated the Adviser as its “Valuation Designee” to perform all of the fair value determinations as well as to perform all of the responsibilities that may be performed by the Valuation Designee in accordance with Rule 2a-5. The Valuation Designee is authorized to make all necessary determinations of the fair values of the portfolio securities and other assets for which market quotations are not readily available or if it is deemed that the prices obtained from brokers and dealers, or independent pricing services are unreliable.

The Fund has adopted authoritative fair value accounting standards which establish an authoritative definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value, a discussion in changes in valuation techniques and related inputs during the year and expanded disclosure of valuation levels for major security types. These inputs are summarized in the three broad levels listed below:

| Level 1 – | Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access. |

| Level 2 – | Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

| Level 3 – | Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities.

24

PALM VALLEY CAPITAL FUND

Notes to the Financial Statements – Continued

December 31, 2022

The following table is a summary of the inputs used to value the Fund’s securities by level within the fair value hierarchy as of December 31, 2022:

Investments at Fair Value | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Assets | ||||||||||||||||

Common Stocks(1) | $ | 39,191,989 | $ | — | $ | — | $ | 39,191,989 | ||||||||

| Short-Term Investments | ||||||||||||||||

| Money Market Fund | 19,770,746 | — | — | 19,770,746 | ||||||||||||

| U.S. Treasury Bills | — | 127,039,664 | — | 127,039,664 | ||||||||||||

| Total Short-Term Investments | 19,770,746 | 127,039,664 | — | 146,810,410 | ||||||||||||

| $ | 58,962,735 | $ | 127,039,664 | $ | — | $ | 186,002,399 | |||||||||

(1) | Please refer to the Schedules of Investments to view Common Stocks segregated by industry type. |

During the year ended December 31, 2022, the Fund did not hold any Level 3 securities, nor were there any transfers into or out of Level 3.

B. Foreign Securities and Currency Translation – Investment securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollar amounts at the date of valuation. Purchases and sales of investment securities and income and expense items denominated in foreign currencies are translated into U.S. dollar amounts on the respective dates of such transactions. The Fund does not isolate the portion of the results of operations from changes in foreign exchange rates on investments from the fluctuations arising from changes in market prices of securities held. Reported net realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions, and the difference between the amounts of dividends, interest, and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in the fair values of assets and liabilities, other than investments in securities at fiscal year-end, resulting from changes in exchange rates.

Investments in foreign securities entail certain risks. There may be a possibility of nationalization or expropriation of assets, confiscatory taxation, political or financial instability, and diplomatic developments that could affect the value of the Fund’s investments in certain foreign countries. Since foreign securities normally are denominated and traded in foreign currencies, the value of the Fund’s assets may be affected favorably or unfavorably by currency exchange rates, currency exchange control regulations, foreign withholding taxes, and restrictions or prohibitions on the repatriation of foreign currencies. There may be less information publicly available about a foreign issuer than about a U.S. issuer, and foreign issuers are not generally subject to accounting, auditing, and financial reporting standards, and practices comparable to those in the United States. The securities of some foreign issuers are less liquid and at times more volatile than securities of comparable U.S. issuers.

C. Cash and Cash Equivalents – The Fund considers highly liquid short-term fixed income investments purchased with an original maturity of less than three months to be cash equivalents. Cash equivalents are included in short-term investments on the Schedule of Investments as well as in investments on the Statement of Assets and Liabilities.

D. Guarantees and Indemnifications – In the normal course of business, the Fund enters into contracts with service providers that contain general indemnification clauses. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred.

25

PALM VALLEY CAPITAL FUND

Notes to the Financial Statements – Continued

December 31, 2022

E. Security Transactions, Income and Expenses – The Fund follows industry practice and records security transactions on the trade date. Realized gains and losses on sales of securities are calculated on the basis of identified cost. Dividend income is recorded on the ex-dividend date and interest income and expense is recorded on an accrual basis. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and regulations. Discounts and premiums on securities purchased are amortized over the expected life of the respective securities. Interest income is accounted for on the accrual basis and includes amortization of premiums and accretion of discounts using the effective interest method.

F. Allocation of Income, Expenses and Gains/Losses – Income, expenses (other than those deemed attributable to a specific share class), and gains and losses of the Fund are allocated daily to each class of shares based upon the ratio of net assets represented by each class as a percentage of the net assets of the Fund. Expenses deemed directly attributable to a class of shares are recorded by the specific class. Most Fund expenses are allocated by class based on relative net assets. 12b-1 fees are expensed up to 0.25% of average daily net assets of Investor Class shares (See Note 5).

G. Share Valuation – The NAV per share of the Fund is calculated by dividing the sum of the value of the securities held by the Fund, plus cash or other assets, minus all liabilities (including estimated accrued expenses) by the total number of shares outstanding for the Fund, rounded to the nearest cent. The Fund’s shares will not be priced on days which the New York Stock Exchange (“NYSE”) is closed for trading.

H. Use of Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

I. Statement of Cash Flows – Pursuant to the Cash Flows Topic of the Codification, the Fund qualifies for an exemption from the requirement to provide a statement of cash flows and has elected not to provide a statement of cash flows.

3. RELATED PARTY TRANSACTIONS

The Trust has an agreement with the Adviser to furnish investment advisory services to the Fund. Pursuant to an Investment Advisory Agreement between the Trust and the Adviser, the Adviser is entitled to receive, on a monthly basis, an annual advisory fee equal to 0.90% of the Fund’s average daily net assets.

The Adviser has contractually agreed to reduce its management fees and/or absorb expenses of the Fund to ensure that total annual operating expenses after fee waiver and/or expense reimbursement (excluding Rule 12b-1 fees – Investor Class (see Note 5), shareholder servicing fees, acquired fund fees and expenses, redemption fees, dividends and interest on short positions, taxes, leverage interest, brokerage fees (including commissions, mark-ups and mark- downs), other transactional expenses, annual account fees for margin accounts, expenses incurred in connection with any merger or reorganization, or extraordinary expenses such as litigation) do not exceed 1.00% of the Fund’s average daily net asset value. The Adviser may request recoupment of previously waived fees and reimbursed Fund expenses from the Fund for three years from the date they were waived or reimbursed, provided that, after payment of the recoupment, the Total Annual Fund Operating Expenses do not exceed the lesser of the Expense Cap: (i) in effect at the time of the waiver or reimbursement; or (ii) in effect at the time of recoupment. The Operating Expense Limitation Agreement is intended to be continual in nature and cannot be terminated within one year after the effective date of

26

PALM VALLEY CAPITAL FUND

Notes to the Financial Statements – Continued

December 31, 2022

the Fund’s prospectus and subject thereafter to termination at any time upon 60 days written notice and approval by the Board or the Adviser. Waived fees and reimbursed expenses subject to potential recovery by year of expiration are as follows:

Expiration | Amount | |

| January 2025 – December 2025 | $371,880 | |

| January 2024 – December 2024 | $264,206 | |

| June 2023 – December 2023 | $241,983 |

U.S. Bancorp Fund Services, LLC, doing business as U.S. Bank Global Fund Services (“Fund Services” or the “Administrator”) acts as the Fund’s Administrator, transfer agent, and fund accountant. U.S. Bank N.A. (the “Custodian”) serves as the custodian to the Fund. The Custodian is an affiliate of the Administrator. The Administrator performs various administrative and accounting services for the Fund. The Administrator prepares various federal and state regulatory filings, reports and returns for the Fund; prepares reports and materials to be supplied to the Trustees; monitors the activities of the Fund’s custodian; coordinates the payment of the Fund’s expenses and reviews the Fund’s expense accruals. The officers of the Trust, including the Chief Compliance Officer, are employees of the Administrator. A trustee of the Trust is an officer of the Administrator. As compensation for its services, the Administrator is entitled to a monthly fee at an annual rate based upon the average daily net assets of the Fund, subject to annual minimums. Fees paid by the Fund for administration and accounting, transfer agency, custody and compliance services for the year ended December 31, 2022, are disclosed in the Statement of Operations.

Quasar Distributors, LLC, is the Fund’s distributor (the “Distributor”). The Distributor is not affiliated with the Adviser, Fund Services, or its affiliated companies.

4. TAX FOOTNOTE

Federal Income Taxes – The Fund intends to comply with the requirements of Subchapter M of the Internal Revenue Code of 1986, as amended, necessary to qualify as a regulated investment company and distributes substantially all net taxable investment income and net realized gains to shareholders in a manner which results in no tax cost to the Fund. Therefore, no federal income or excise tax provision is required. As of and during the year ended December 31, 2022, the Fund did not have any tax positions that did not meet the “more-likely-than-not” threshold of being sustained by the applicable tax authority and did not have liabilities for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits on uncertain tax positions as income tax expense in the Statement of Operations. The Fund is subject to examination by taxing authorities for the tax years since the commencement of operations.

As of December 31, 2022, the components of distributable earnings on a tax basis were:

| Tax cost of Investments* | $ | 186,285,057 | ||

| Gross unrealized appreciation | $ | 2,946,197 | ||

| Gross unrealized depreciation | (3,228,855 | ) | ||

| Net unrealized depreciation | (282,658 | ) | ||

| Undistributed ordinary income | 1,189,348 | |||

| Undistributed long-term capital gains | 25,297 | |||

| Other accumulated gains | 20 | |||

| Total distributable earnings | $ | 932,007 |

| * | Represents cost for federal income tax purposes and differs from the cost for financial reporting purposes due to wash sales. |

27

PALM VALLEY CAPITAL FUND

Notes to the Financial Statements – Continued

December 31, 2022

As of December 31, 2022, the Fund did not have any capital loss carryovers. A regulated investment company may elect for any taxable year to treat any portion of any qualified late year loss as arising on the first day of the next taxable year. Qualified late year losses are certain capital, and ordinary losses which occur during the portion of the Fund’s taxable period subsequent to October 31. For the taxable year ended December 31, 2022, the Fund does not plan to defer any qualified late year losses.

Distributions to Shareholders – The Fund distributes substantially all net investment income, if any, and net realized capital gains, if any, annually. Distributions to shareholders are recorded on the ex-dividend date. The treatment for financial reporting purposes of distributions made to shareholders during the year from net investment income or net realized capital gains may differ from their treatment for federal income tax purposes. These differences are caused primarily by differences in the timing of the recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, GAAP requires that they be reclassified in the components of the net assets based on their ultimate characterization for federal income tax purposes. Any such reclassifications will have no effect on net assets, results of operations or net asset values per share of the Fund. For the year ended December 31, 2022, no such reclassifications were made between distributable earnings and paid-in capital.

The tax character of distributions paid for the year ended December 31, 2022, and December 31, 2021, were as follows:

| Ordinary | Long-Term | ||

Income* | Capital Gain | Total | |

| 2022 | $3,479,141 | $720,155 | $4,199,296 |

| 2021 | $1,317,449 | $217,716 | $1,535,165 |

| * | For federal income tax purposes, distributions of short-term capital gains are treated as ordinary income distributions. |

5. DISTRIBUTION FEES

The Fund has adopted a Distribution Plan pursuant to Rule 12b-1 (the “Plan”) for the Investor Class. The Plan permits the Fund to pay for distribution and related expenses at an annual rate up to 0.25% average daily net assets of the Investor Class. Amounts paid under the Plan are paid to the Distributor to compensate it for costs of the services it provides to Investor Class shares of the Fund and the expenses it bears in the distribution of the Fund’s Investor Class shares, including overhead and telephone expenses; printing and distribution of prospectuses and reports used in connection with the offering of the Fund’s Investor class shares to prospective investors; and preparation, printing, payments to intermediaries and distribution of sales literature and advertising materials.

Under the Plan, the Trustees will be furnished quarterly with information detailing the amount of expenses paid under the Plan and the purposes for which payments were made. The Plan may be terminated at any time by vote of a majority of the Trustees of the Trust who are not interested persons. Continuation of the Plan is considered by the Board no less frequently than annually. For the year ended December 31, 2022, the Investor Class incurred expenses of $379,420 pursuant to the Plan.

Distribution fees are not subject to the Operating Expense Limitation Agreement (see Note 3) to reduce management fees and/or absorb Fund expenses by the Adviser. Distribution fees will increase the expenses beyond the Operating Expense Limitation Agreement rate of 1.00% for the Investor Class shares.

28

PALM VALLEY CAPITAL FUND

Notes to the Financial Statements – Continued

December 31, 2022

6. INVESTMENT TRANSACTIONS

The aggregate purchases and sales, excluding short-term investments, by the Fund for the year ended December 31, 2022, were as follows:

Purchases | Sales | |

| U.S. Government | $ — | $ — |

| Other | 42,645,822 | 23,831,253 |

7. BENEFICIAL OWNERSHIP

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of a fund creates a presumption of control of the fund, under Section 2(a)(9) of the Investment Company Act of 1940. As of December 31, 2022, Charles Schwab, for the benefit of its customers, owned more than 25% of the outstanding shares of the Fund. As of December 31, 2022, affiliates of the Advisor held 3.92% of the Fund.

8. RECENT MARKET RISKS

The U.S. and international markets have experienced significant periods of volatility in recent years and months due to a number of economic, political and global macro factors including the impact of COVID-19 as a global pandemic, which has resulted in a public health crisis, disruptions to business operations and supply chains, stress on the global healthcare system, growth concerns in the U.S. and overseas, staffing shortages and the inability to meet consumer demand, and widespread concern and uncertainty. The global recovery from COVID-19 is proceeding at slower than expected rates due to the emergence of variant strains and may last for an extended period of time. Continuing uncertainties regarding interest rates, rising inflation, political events, rising government debt in the U.S. and trade tensions also contribute to market volatility. As a result of continuing political tensions and armed conflicts, including the war between Ukraine and Russia, the U.S. and the European Union imposed sanctions on certain Russian individuals and companies, including certain financial institutions, and have limited certain exports and imports to and from Russia. The war has contributed to recent market volatility and may continue to do so.

9. SUBSEQUENT EVENTS

Management has evaluated events and transactions for potential recognition or disclosure through the date the financial statements were issued and has determined that no items require recognition or disclosure.

29

PALM VALLEY CAPITAL FUND

Report of Independent Registered Public Accounting Firm

To the Shareholders of Palm Valley Capital Fund and

Board of Trustees of Series Portfolios Trust

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Palm Valley Capital Fund (the “Fund”), a series of Series Portfolios Trust, as of December 31, 2022, the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, the related notes, and the financial highlights for each of the four periods in the period then ended (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of December 31, 2022, the results of its operations for the year then ended, the changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the four periods in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2022, by correspondence with the custodian. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the Fund’s auditor since 2019.

COHEN & COMPANY, LTD.

Milwaukee, Wisconsin

March 1, 2023

30

PALM VALLEY CAPITAL FUND

Board Consideration of Investment Advisory Agreement (Unaudited)

December 31, 2022

Under Section 15 of the Investment Company Act of 1940 (the “1940 Act”), the Board of Trustees (the “Board” or the “Trustees”) of Series Portfolios Trust (the “Trust”), including a majority of the Trustees who have no direct or indirect interest in the investment advisory agreement and who are not “interested persons” of the Trust, as defined in the 1940 Act (the “Independent Trustees”), must determine annually whether to approve the continuation of the Trust’s investment advisory agreements.

At a meeting held on July 28, 2022 (the “Meeting”), the Board, including the Independent Trustees, considered and approved the continuance of the advisory agreement (the “Advisory Agreement”) between the Trust, on behalf of the Palm Valley Capital Fund (the “Fund”), and Palm Valley Capital Management, LLC (“Palm Valley”), for an additional one-year term. At the Meeting, the Board considered the factors and reached the conclusions described below in reviewing and approving Palm Valley to continue serving as the Fund’s investment adviser for another year.