U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| ☒ QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the quarterly period ended June 30, 2019 |

| | ☐ TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 333-229065

ANDES 7 Inc.

(Exact name of registrant as specified in its charter)

| | Delaware | | 47-4683655 | |

| | | | | |

| | (State or Other Jurisdiction of | | (I.R.S. Employer | |

| | Incorporation or Organization) | | Identification No.) | |

| | | | | |

| | | | | |

| | 424 Clay Street, Lower Level, San Francisco, CA | | 94111 | |

| | | | | |

| | (Address of Principal Executive Offices) | | (Zip Code) | |

| | | | | |

Registrant’s telephone number, including area code: 415 463 7827

N/A

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐No ☒

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Non-accelerated filer ☒ Emerging growth company ☒ | Accelerated filer ☐ Smaller reporting company ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐No ☒

State the number of shares outstanding of each of the issuer’s classes of common equity, as of the latest practicable date: As of August 19, 2019, the issuer had 120,100,000 shares of its common stock issued and outstanding.

TABLE OF CONTENTS

| PART I | | | |

| Item 1. | Unaudited Financial Statements | 3 | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 12 | |

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 20 | |

| Item 4. | Controls and Procedures | 21 | |

| PART II | | | |

| Item 1. | Legal Proceedings | 21 | |

| Item 1A. | Risk Factors | 21 | |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 22 | |

| Item 3. | Defaults Upon Senior Securities | 22 | |

| Item 4. | Mine Safety Disclosures | 22 | |

| Item 5. | Other Information | 22 | |

| Item 6. | Exhibits | 22 | |

| | Signatures | 23 | |

PART I

Item 1. Unaudited Financial Statements

ANDES 7, INC.

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2019

| Consolidated Balance Sheets as of June 30, 2019 (unaudited) and December 31, 2018 | | 4 | |

| | | | |

| Consolidated Statements of Operations for the three and six months ended June 30, 2019 and 2018 (unaudited) | | 5 | |

| | | | |

| Consolidated Statement of Stockholders’ Deficit for the three and six months ended June 30, 2019 and 2018 (unaudited) | | | |

| | | | |

| Consolidated Statements of Cash Flows for the six months ended June 30, 2019 and 2018 (unaudited) | | 6 | |

| | | | |

| Notes to the Financial Statements (unaudited) | | 7 | |

| ANDES 7, INC. and Subsidiary |

| CONSOLIDATED BALANCE SHEETS |

| (Unaudited) |

| | | | June 30, | | | | December 31, | |

| | | 2019 | | | | 2019 | |

| | | | | | | | | |

| ASSETS | | | | | | | | |

| | | | | | | | | |

| Current assets: | | | | | | | | |

| Cash | | $ | 1,988 | | | $ | 2,216 | |

| Accounts receivable | | | 1,500 | | | | 618 | |

| Inventory | | | 82,746 | | | | 81,279 | |

| Other current assets | | | 3,170 | | | | 3,323 | |

| Total current assets | | | 89,404 | | | | 87,436 | |

| Office deposit | | | — | | | | 8,042 | |

| Deposit – land contract | | | 317,238 | | | | 271,110 | |

| Construction in progress | | | 21,791 | | | | 20,646 | |

| ROU asset - operating lease | | | 19,570 | | | | — | |

| Property and equipment, net | | | 244,034 | | | | 245,313 | |

| Total assets | | $ | 692,037 | | | $ | 632,547 | |

| | | | | | | | | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | | | |

| | | | | | | | | |

| Current liabilities: | | | | | | | | |

| Accounts payable and accrued liabilities | | $ | 11,079 | | | $ | 6,751 | |

| Due to a related party | | | 42,730 | | | | 43,720 | |

| Loans from directors | | | 1,411,634 | | | | 1,236,719 | |

| Loans payable, current portion | | | 8,580 | | | | 10,396 | |

| Total current liabilities | | | 1,474,023 | | | | 1,297,586 | |

| | | | | | | | | |

| Long term liabilities: | | | | | | | | |

| Loans payable, non-current | | | 11,174 | | | | 13,538 | |

| Operating lease liability | | | 19,570 | | | | — | |

| Total liabilities | | | 1,504,767 | | | | 1,311,124 | |

| | | | | | | | | |

| Stockholders’ Equity (Deficit): | | | | | | | | |

| Preferred stock, $0.0001 par value, 5,000,000 shares authorized; 500,000 shares issued and outstanding as on June 30, 2019 and December 31, 2018 respectively | | | 50 | | | | 50 | |

| Common stock, $0.0001 par value, 1,000,000,000 shares authorized, 120,100,000 shares issued and outstanding as on June 30, 2019 and December 31, 2018 respectively | | | 12,010 | | | | 12,010 | |

| Additional paid in capital | | | 239,034 | | | | 238,044 | |

| Accumulated deficit | | | (988,550 | ) | | | (891,669 | ) |

| Accumulated other comprehensive loss | | | (75,274 | ) | | | (37,012 | ) |

| Total stockholders’ deficit | | | (812,730 | ) | | | (678,577 | ) |

| | | | | | | | | |

| Total liabilities and stockholders’ deficit | | $ | 692,037 | | | $ | 632,547 | |

| | | | | | | | | |

| The accompanying notes are an integral part of these audited consolidated financial statements. |

| ANDES 7, INC. and Subsidiary |

| CONSOLIDATED STATEMENTS OF OPERATIONS |

| (Unaudited) |

| | | For the Three Months Ended June 30, | | For the Six Months Ended June 30, |

| 2019 | | 2018 | 2019 | | 2018 |

| Revenue | $ | 4,807 | $ | 2,644 | $ | 7,245 | $ | 3,500 |

| Cost of revenue | | 1,993 | | 2,335 | | 2,947 | | 5,226 |

| Gross Margin | | 2,814 | | 309 | | 4,298 | | (1,726) |

| | | | | | | | | |

| Operating expenses: | | | | | | | | |

| General and administrative | | 44,957 | | 74,532 | | 73,091 | | 167,324 |

| Rent expense | | 2,851 | | 2,810 | | 5,698 | | 7,566 |

| Advertising and promotion | | 143 | | 808 | | 848 | | 8,449 |

| Professional fees | | 13,028 | | - | | 20,767 | | - |

| Total operating expenses | | 60,979 | | 78,150 | | 100,404 | | 183,339 |

| Loss from operations | | (58,165) | | (77,841) | | (96,106) | | (185,065) |

| Other income (expense): | | | | | | | | |

| Interest income | | - | | - | | - | | - |

| Interest expense | | (426) | | (415) | | (775) | | (1,767) |

| Total other income (expense) | | (426) | | (415) | | (775) | | (1,767) |

| Loss before income taxes | | (58,591) | | (78,256) | | (96,881) | | (186,832) |

| | | | | | | | | |

| Provision for income taxes | | - | | - | | - | | - |

| Net loss | $ | (58,591) | $ | (78,256) | $ | (96,881) | $ | (186,832) |

| | | | | | | | | |

| Other comprehensive income (loss): | | | | | | | | |

| Foreign currency translation adjustment | | (26,070) | | 26,438 | | (38,262) | | 25,516 |

| Comprehensive loss | $ | (84,661) | $ | (51,818) | $ | (135,143) | $ | (161,316) |

| | | | | | | | | |

| Loss per share basic & diluted | $ | (0.00) | $ | (0.01) | $ | (0.00) | $ | (0.02) |

| | | | | | | | | |

| Weighted average outstanding shares, basic & diluted | | 120,100,000 | | 10,100,000 | | 120,100,000 | | 10,100,000 |

| | | | | | | | | |

| The accompanying notes are an integral part of these audited consolidated financial statements |

| ANDES 7, INC. and Subsidiary |

| CONSOLIDATED STATEMENT OF SHAREHOLDERS' EQUITY |

| (Unaudited) | |

| | | | Preferred Stock | | | | Common Stock | | | | Additional paid | | | | Subscriptions | | | | Accumulated | | | | Other Comprehensive | | | | Total | |

| | | | Shares | | | | Amount | | | | Shares | | | | Amount | | | | in capital | | | | Receivable | | | | Deficit | | | | Income | | | | Total | |

| For the three months ended June 30, 2018 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance, March 31, 2018 | | | — | | | | — | | | | 10,100,000 | | | $ | 1,010 | | | $ | 249,044 | | | $ | — | | | $ | (742,471 | ) | | $ | (51,898 | ) | | $ | (544,315 | ) |

| Foreign currency translation adjustment | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 26,438 | | | | 26,438 | |

| Net loss for the three months ended June 30, 2018 | | | | | | | | | | | | | | | | | | | | | | | | | | | (78,256 | ) | | | | | | | (78,256 | ) |

| Balance, June 30, 2018 | | | — | | | | — | | | | 10,100,000 | | | | 1,010 | | | | 249,044 | | | | — | | | | (820,727 | ) | | | (25,460 | ) | | | (596,133 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| For the three months ended June 30, 2019 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance, March 31, 2019 | | | 500,000 | | | | 50 | | | | 120,100,000 | | | $ | 12,010 | | | $ | 238,044 | | | $ | — | | | $ | (929,959 | ) | | $ | (49,204 | ) | | $ | (729,059 | ) |

| Debt forgiveness | | | — | | | | — | | | | — | | | | — | | | | 990 | | | | — | | | | — | | | | — | | | | 990 | |

| Foreign currency translation adjustment | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | (26,070 | ) | | | (26,070 | ) |

| Net loss for the three months ended June 30, 2019 | | | | | | | | | | | | | | | | | | | | | | | | | | | (58,591 | ) | | | | | | | (58,591 | ) |

| Balance, June 30, 2019 | | | 500,000 | | | | 50 | | | | 120,100,000 | | | | 12,010 | | | | 239,034 | | | | — | | | | (988,550 | ) | | | (75,274 | ) | | | (812,730 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| For the six months ended June 30, 2018 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance, December 31, 2017 | | | — | | | | — | | | | 10,100,000 | | | $ | 1,010 | | | $ | 249,044 | | | $ | — | | | $ | (633,895 | ) | | $ | (50,976 | ) | | $ | (434,817 | ) |

| Foreign currency translation adjustment | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 25,516 | | | | 25,516 | |

| Net loss for the six months ended June 30, 2018 | | | | | | | | | | | | | | | | | | | | | | | | | | | (186,832 | ) | | | | | | | (186,832 | ) |

| Balance, June 30, 2018 | | | — | | | | — | | | | 10,100,000 | | | | 1,010 | | | | 249,044 | | | | — | | | | (820,727 | ) | | | (25,460 | ) | | | (596,133 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| For the six months ended June 30, 2019 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance, December 31, 2018 | | | 500,000 | | | | 50 | | | | 120,100,000 | | | $ | 12,010 | | | $ | 238,044 | | | $ | — | | | $ | (891,669 | ) | | $ | (37,012 | ) | | $ | (678,577 | ) |

| Debt forgiveness | | | — | | | | — | | | | — | | | | — | | | | 990 | | | | — | | | | — | | | | — | | | | 990 | |

| Foreign currency translation adjustment | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | (38,262 | ) | | | (38,262 | ) |

| Net loss for the six months ended June 30, 2019 | | | | | | | | | | | | | | | | | | | | | | | | | | | (96,881 | ) | | | | | | | (96,881 | ) |

| Balance, June 30, 2019 | | | 500,000 | | | | 50 | | | | 120,100,000 | | | | 12,010 | | | | 239,034 | | | | — | | | | (988,550 | ) | | | (75,274 | ) | | | (812,730 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| The accompanying notes are an integral part of these audited consolidated financial statements | |

| ANDES 7, INC. and Subsidiary |

| CONSOLIDATED STATEMENTS OF CASH FLOWS |

| (Unaudited) |

| | | For the Six Months Ended June 30, |

| 2019 | | 2018 |

| Cash flows from operating activities: | | | | |

| Net loss | $ | (96,881) | $ | (186,832) |

| Adjustments to reconcile net loss to net cash used in operating activities: | | | | |

| Depreciation expense | | 14,428 | | 13,823 |

| Preferred stock issued | | - | | - |

| Changes in operating assets and liabilities: | | | | |

| Accounts receivable | | (882) | | 2,182 |

| Inventory | | (1,467) | | (7,693) |

| Advanced payments | | - | | - |

| Other assets | | 8,195 | | 1,636 |

| Accounts payable and accrued liabilities | | 4,328 | | (1,106) |

| Deposits | | (46,128) | | (90,879) |

| Net cash used in operating activities | | (118,407) | | (268,869) |

| Cash flows from investing activities: | | | | |

| Construction in progress | | (1,145) | | 1,180 |

| Purchase of property and equipment | | (13,149) | | - |

| Proceeds from sale of property and equipment | | - | | 4,746 |

| Net cash used in investing activities | | (14,294) | | 5,926 |

| | | | | |

| Cash flows from financing activities: | | | | |

| Proceeds from related party debt | | - | | 17,529 |

| Proceeds from the sale of preferred stock | | - | | 50 |

| Net proceeds from Director loans | | 174,915 | | 167,607 |

| Net proceeds (payments) from loans | | (4,180) | | (6,839) |

| Net cash provided by financing activities | | 170,735 | | 178,347 |

| | | | | |

| Net change in cash | | 38,034 | | (84,596) |

| | | | | |

| Effects of currency translation on cash | | �� (38,262) | | 25,516 |

| Cash, beginning of the period | | 2,216 | | 59,935 |

| | | | | |

| Cash, end of the period | $ | 1,988 | $ | 855 |

| | | | | |

| Supplemental disclosures: | | | | |

| Cash paid for interest | $ | - | $ | - |

| Cash paid for taxes | $ | - | $ | - |

| | | | | |

| Non-cash transactions: | | | | |

| Debt forgiveness | $ | 990 | | - |

| | | | | |

| The accompanying notes are an integral part of these audited consolidated financial statements |

ANDES 7, INC. and Subsidiary

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2019

(UNAUDITED)

NOTE 1 - ORGANIZATION AND DESCRIPTION OF BUSINESS

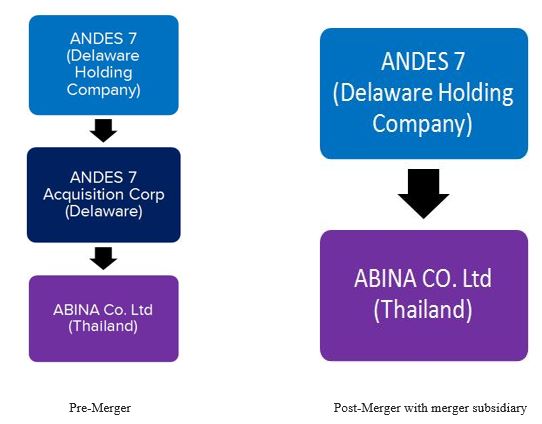

ANDES 7 Inc. (the “Company”) was incorporated in the State of Delaware on July 27, 2015. ANDES 7 Inc. was formed as a vehicle to pursue a business combination with an operating company that would have perceived benefits of becoming a publicly traded corporation.

On February 12, 2016, the Company entered into a Subscription Agreements with three subscribers for the issuance of its restricted common stock – Abina Asean, Co. Ltd., an entity organized under the laws of the Republic of Seychelles (8,000,000 shares), Toh Kean Ban (1,000,000 shares) and Dr. Ir. H.M. Itoc Tochija (1,000,000 shares). Each of the Subscription Agreements were the result of privately negotiated transactions without the use of public dissemination of promotional or sales materials. Each of the buyers represented they were “accredited investors,” and as such could bear the risk of such investment for an indefinite period of time and to afford a complete loss thereof.

On July 2, 2018, the Company entered into an Agreement and Plan of Merger between the Company, ANDES 7 Acquisition Corp, (“Merger Sub”) a Delaware corporation and Abina Co. Ltd. (the “Abina”). Abina is a corporation organized under the Kingdom of Thailand and has operated under the name “Abina Co. Ltd.” since August 3, 2015 and has since then operated a diverse business involved in investments in hotels, resorts, and commercial property. The Agreement and Plan of Merger provided for the acquisition by the Company of all the outstanding shares of Abina through a reverse merger of merger sub into Abina, the surviving corporation. The financial statements have been prepared to retroactively present the reverse merger.

NOTE 2 - GOING CONCERN

The accompanying audited financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The Company’s ability to raise additional capital through debt and/or equity financing is unknown. The obtainment of additional financing and the successful development of the Company’s contemplated plan of operations are necessary for the Company to continue. The ability to successfully resolve these factors raise substantial doubt about the Company’s ability to continue as a going concern. However; management believes that the Company will generate sufficient cash flows to fund its operations and to meet its obligations on a timely basis for the next twelve months. The financial statements of the Company do not include any adjustments that may result from the outcome of these aforementioned uncertainties.

NOTE 3 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The Company’s financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”).

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires the Company to make estimates and judgments that affect the reported amounts of assets and liabilities, revenues and expenses, and related disclosures of contingent assets and liabilities. These estimates and judgments are based on historical information, information that is currently available to the Company and on various other assumptions that the Company believes to be reasonable under the circumstances. Actual results could differ from those estimates.

Principles of Consolidation

The accompanying consolidated financial statements include the accounts of the Company and its wholly-owned subsidiaries, Andes 7 Acquisition Corp and Abina Co, Ltd. All financial information has been prepared in conformity with accounting principles generally accepted in the United States of America. All significant intercompany transactions and balances have been eliminated.

Translation Adjustment

For the periods ended June 30, 2019 and 2018, the accounts of the Company were maintained, and its financial statements were expressed, in BAHT. Such financial statements were translated into USD in accordance with the Foreign Currency Matters Topic of the Codification (ASC 830), with the BAHT as the functional currency. According to the Codification, all assets and liabilities were translated at the current exchange rate at respective balance sheets dates, stockholders’ equity are translated at the historical rates and income statement items are translated at the average exchange rate for the period. The resulting translation adjustments are reported under other comprehensive income in accordance with the Comprehensive Income Topic of the Codification (ASC 220), as a component of members’ capital. Transaction gains and losses are reflected in the income statement.

Comprehensive Income/(Loss)

The Company uses SFAS 130 “Reporting Comprehensive Income” (ASC Topic 220). Comprehensive income is comprised of net income and all changes to the statements of stockholders’ equity, except those due to investments by stockholders, changes in paid-in capital and distributions to stockholders. Comprehensive loss for the period ended June 30, 2019 and 2018 is included in the statement of operations as a foreign currency translation adjustment.

Cash and Cash Equivalents

Cash and cash equivalents include cash on hand and cash in time deposits, certificates of deposit and all highly liquid instruments with original maturities of three months or less.

Revenue recognition

Revenue is recognized when a customer obtains control of promised goods or services and is recognized in an amount that reflects the consideration that an entity expects to receive in exchange for those goods or services. In addition, the standard requires disclosure of the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. The amount of revenue that is recorded reflects the consideration that the Company expects to receive in exchange for those goods. The Company applies the following five-step model in order to determine this amount: (i) identification of the promised goods in the contract; (ii) determination of whether the promised goods are performance obligations, including whether they are distinct in the context of the contract; (iii) measurement of the transaction price, including the constraint on variable consideration; (iv) allocation of the transaction price to the performance obligations; and (v) recognition of revenue when (or as) the Company satisfies each performance obligation.

The Company only applies the five-step model to contracts when it is probable that the entity will collect the consideration it is entitled to in exchange for the goods or services it transfers to the customer. Once a contract is determined to be within the scope of ASC 606 at contract inception, the Company reviews the contract to determine which performance obligations the Company must deliver and which of these performance obligations are distinct. The Company recognizes as revenues the amount of the transaction price that is allocated to the respective performance obligation when the performance obligation is satisfied or as it is satisfied. Generally, the Company's performance obligations are transferred to customers at a point in time, typically upon delivery.

Inventories

Inventories are valued at the lower of cost or market utilizing the first-in first-out (FIFO) method. Management compares the cost of inventories with the market value and allowance is made for writing down their inventories to market value, if lower.

Fair value of financial instruments

The Company follows paragraph 825-10-50-10 of the FASB Accounting Standards Codification for disclosures about fair value of its financial instruments and paragraph 820-10-35-37 of the FASB Accounting Standards Codification (“Paragraph 820-10-35-37”) to measure the fair value of its financial instruments. Paragraph 820-10-35-37 establishes a framework for measuring fair value in accounting principles generally accepted in the United States of America (U.S. GAAP), and expands disclosures about fair value measurements. To increase consistency and comparability in fair value measurements and related disclosures, Paragraph 820-10-35-37 establishes a fair value hierarchy which prioritizes the inputs to valuation techniques used to measure fair value into three (3) broad levels. The fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities and the lowest priority to unobservable inputs. The three (3) levels of fair value hierarchy defined by Paragraph 820-10-35-37 are described below:

Level 1: Quoted market prices available in active markets for identical assets or liabilities as of the reporting date.

Level 2: Pricing inputs other than quoted prices in active markets included in Level 1, which are either directly or indirectly observable as of the reporting date.

Level 3: Pricing inputs that are generally observable inputs and not corroborated by market data.

The carrying amount of the Company’s financial assets and liabilities, such as cash, prepaid expenses and accounts payable approximate their fair value because of the short maturity of those instruments.

The Company does not have any assets or liabilities measured at fair value on a recurring basis. The Company’s property and equipment is subject to measurement on a non-recurring basis. No fair value adjustments are included in the financial statements.

Income taxes

The Company follows Section 740-10-30 of the FASB Accounting Standards Codification, which requires recognition of deferred tax assets and liabilities for the expected future tax consequences of events that have been included in the financial statements or tax returns. Under this method, deferred tax assets and liabilities are based on the differences between the financial statement and tax bases of assets and liabilities using enacted tax rates in effect for the fiscal year in which the differences are expected to reverse. Deferred tax assets are reduced by a valuation allowance to the extent management concludes it is more likely than not that the assets will not be realized. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the fiscal years in which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in the Statements of Income in the period that includes the enactment date.

The Company adopted section 740-10-25 of the FASB Accounting Standards Codification (“Section 740-10-25”) with regards to uncertainty in income taxes. Section 740-10-25 addresses the determination of whether tax benefits claimed or expected to be claimed on a tax return should be recorded in the financial statements. Under Section 740-10-25, the Company may recognize the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position. The tax benefits recognized in the financial statements from such a position should be measured based on the largest benefit that has a greater than fifty percent (50%) likelihood of being realized upon ultimate settlement. Section 740-10-25 also provides guidance on de-recognition, classification, interest and penalties on income taxes, accounting in interim periods and requires increased disclosures. The Company had no material adjustments to its liabilities for unrecognized income tax benefits according to the provisions of Section 740-10-25.

Adoption of New Accounting Standards

In March 2016, the FASB issued ASU 2016-02,Leases(“ASU 2016-02”), which provides guidance for accounting for leases. ASU 2016-02 requires lessees to classify leases as either finance or operating leases and to record a right-of-use asset and a lease liability for all leases with a term greater than 12 months regardless of the lease classification. The lease classification will determine whether the lease expense is recognized based on effective interest rate method or a straight-line basis over the term of the lease. Accounting for lessors remains largely unchanged from current GAAP. ASU 2016-02 was effective for the Company’s fiscal year beginning after December 15, 2018 and subsequent interim periods. The Company has evaluated the adoption of ASU 2016-02 which was not applicable due to the Company having no leases.

The Company continually assesses any new accounting pronouncements to determine their applicability to the Company. Where it is determined that a new accounting pronouncement affects the Company’s financial reporting, the Company undertakes a study to determine the consequence of the change to its financial statements and assures that there are proper controls in place to ascertain that the Company’s financials properly reflect the change.

NOTE 4 – CONSTRUCTION IN PROGRESS

In 2016 Abina entered into an agreement to purchase land in Chiang Rai, Thailand for 200 million Baht. The Company has paid a $186,654 deposit (5.7 million Baht) as of June 30, 2019 and the balance of 194.3 million Baht is due on December 15, 2019 per the terms of an extension given in an amended agreement. The Company plans on developing the land as a tourist destination and is currently in the process of building a café on the property.

In 2016 the Company incurred $79,744 of construction related costs of which approximately $68,000 was for the building of the café and the remaining balance of almost $12,000 primarily consisted of land and site development costs. As of June 30, 2019, the balance in the construction in progress account has increased to $21,791.

NOTE 5 – PROPERTY AND EQUIPMENT

The Company’s property and equipment primarily consists of office furniture and equipment and it is being depreciated using the straight-line method over a period of five years.

| | | June 30,

2019 | | December 31, 2018 |

| Office Equipment | | $ | 63,136 | | | $ | 59,819 | |

| Accounting Software | | | 808 | | | | 766 | |

| Flag Costs | | | 31,866 | | | | 30,192 | |

| Vehicles | | | 90,516 | | | | 85,761 | |

| Buildings and land costs | | | 149,345 | | | | 141,499 | |

| Total property & equipment | | | 335,671 | | | | 318,037 | |

| Less accumulated depreciation | | | (91,637 | ) | | | (72,724 | ) |

| Property & equipment, net | | $ | 244,034 | | | $ | 245,313 | |

Depreciation expense for the three months ended June 30, 2019 and 2018 totaled $7,259 and $6,927 respectively.

Depreciation expense for the six months ended June 30, 2019 and 2018 totaled $14,428 and $13,823 respectively.

NOTE 6 – LOANS PAYABLE

The Company has entered into two financing agreements for its vehicles used in the business. The following is a summary of these loans payable as of June 30, 2019:

| Loan | | Issue Date | | Maturity Date | | Interest Rate | | Beginning Balance | | Payments | | Balance 12/31/18 | | Payments | | Balance

06/30/19 |

| Siam Commercial Bank #1 | | 7/14/2016 | | 7/14/2020 | | | 5.029 | % | | $ | 29,846 | | | | (7,442 | ) | | | 14,438 | | | | (2,574) | | | | 11,864 | |

| Siam Commercial Bank #2 | | 11/29/2016 | | 11/29/2020 | | | 8.98 | % | | | 15,801 | | | | (2,165 | ) | | | 9,496 | | | | (1,606) | | | | 7,890 | |

NOTE 7 – PREFERRED STOCK

The Company is authorized to issue 5,000,000 shares of $0.0001 par value preferred stock.

On March 25, 2018, the Company with the authorization of the board of directors and the majority shareholder adopted a resolution to create 500,000 shares of Series A preferred stock. The Company then filed an amendment to its certificate of incorporation with the State of Delaware on May 10, 2018 to create a certificate of designation for 500,000 shares of Series A preferred stock with each share convertible into 1,000 shares of common stock and with voting rights of 1,000 votes for each share of Series A preferred stock.

On May 10, 2018, Manichan Khor, the wife of Andrew Khor Poh Kiang, the President, CEO and Chairman entered into a stock purchase agreement to purchase 500,000 shares of Series A preferred stock at par value for total proceeds of $50.

NOTE 8 – COMMON STOCK

The Company is authorized to issue 1,000,000,000 shares of $0.0001 par value common stock.

As part of the Agreement and Plan of Merger with Abina Co. Ltd. The Company issued 111,000,000 shares of common stock. In addition, Mr. Khor cancelled 1,000,000 shares of his common stock.

NOTE 9 – RELATED PARTY TRANSACTIONS

During the year ended December 31, 2016, directors of Abina had loaned the Company a total of $655,565. The funds were used to pay for general operating expenses. All loans are unsecured, non-interest bearing and due on demand. As of June 30, 2019, the balance due to was $1,411,634.

Since 2016, a related party had advanced the Company funds to pay for general operating expenses. The funds were unsecured, non-interest bearing and due on demand. During the three months ended June 30, 2019, Mr. Richard Chiang forgave the $990 due to him in connection with the 9,900,000 shares redeemed earlier and recorded $990 as debt forgiveness. As of June 30, 2019, and December 31, 2018, the due to related party balance due is $42,730 and $43,720, respectively.

NOTE 10 – COMMITMENT

In April 2017 Abina entered into a two-year lease for its office facility in Chiang Rai, Thailand which can be further renewed for two years starting April 1, 2019 and it expires on March 31, 2021. The monthly rent obligation is approximately $963 (Thai baht was converted to USD based on average exchange rate). Minimum required rental payments for 2018 and 2019 are approximately $11,556 and $2,889, respectively.

NOTE 11 – ACCUMULATED OTHER COMPREHENSIVE LOSS

The balance of related after-tax components comprising accumulated other comprehensive income included in stockholders’ equity were as follows:

| | | June 30,

2019 | | December 31, 2018 |

| Accumulated other comprehensive loss, beginning of period | | $ | (37,012) | | | $ | (50,976) | |

| Change in cumulative translation adjustment | | | (38,262) | | | | 13,964 | |

| Accumulated other comprehensive loss | | $ | (75,274 | ) | | $ | (37,012 | ) |

NOTE 12 – SUBSEQUENT EVENTS

In accordance with SFAS 165 (ASC 855-10) management has performed an evaluation of subsequent events through the date that the financial statements were issued and has determined that it does not have any material subsequent events to disclose in these financial statements.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The Company

ANDES 7 Inc. was incorporated in the State of Delaware on July 27, 2015. ANDES 7 Inc. was formed as a vehicle to pursue a business combination with an operating company that would have perceived benefits of becoming a publicly traded corporation. Abina Co. Ltd (“Abina”) was incorporated in Thailand on August 3, 2015 and has since then operated a diverse business involved in investments in hotels, resorts, and commercial property. The Company had directed its efforts by the end of 2015 to develop the tallest and largest flagpole in the world in the Chiang Saen District of Chiang Rai, Thailand with measurements of 42 meters in height and 63 meters in length. It was since awarded with the prestigious honor of being the largest flag in Thailand by the Guinness Book of World Records. The flag pole itself is pending development along with a park and concession area for tourists primarily from China.

Abina has secured the exclusive right and license with the local and state government of Thailand for the development of the “tallest flagpole and largest flag” in the world to be a landmark destination in Thailand and to attract, promote local and foreign tourism primarily from China. Having a long history of being ruled by kings, Abina believes that Thailand is a country deep rooted with patriotism and loyalty to their king and national flag. With this belief, under Abina’s license, the Thai government mandated that each citizen must purchase a flag and or souvenirs from the collection of ANDES 7 souvenirs. ANDES 7 intend to promote and sell its souvenir products and flags through souvenir shops and cafes in major cities throughout Thailand.

Following the merger, the Company is planning a full leisure and tourist destination in Chiang Rai, Thailand with agreements with the Thai government as its exclusive authorized merchandising, souvenir and collectables retailer for the Thai flag, and to offer religious merchandise, retail shops, cafes, and build other real estate projects. The Company is seeking to develop a fully integrated hotel and entertainment center in the Chiang Saen District of Chiang Rai, Thailand that will include souvenir shops, a hotel, office buildings, several malls, and a resort entertainment center catering to both local and foreign tourists primarily from China.

The Company seeks to acquire full rights and ownership in 126 hectares of land in the Chiang Saen District of Chiang Rai, Thailand within a Free Trade Zone designated area to develop a leisure and tourist destination designed for both local and foreign tourists. The Company believes that this area holds beneficial value based on the “One Belt, One Road” initiative or “OBOR”. Announced by the Chinese government in 2013, OBOR is a development strategy by the Chinese government which focuses on connectivity and cooperation between Europe, Africa, China and Southeast Asia. The OBOR initiative is designed to increase the flow of trade, aimed at building new infrastructure, and increasing cultural exchanges.

The project and acquisition costs are expected to cost over an estimated $6 million USD, while the construction of the flagpole, mall, office building complex, hotel, spiritual center and shops are expected to cost $120 million USD. As of the date of this Form 10-Q, the Company has paid 5 million Thai Baht, or $159,000 in US dollars and owes a balance of 195 million Thai Baht, or $6,228,300 in US dollars (at today’s exchange rates) for the land in Chiang Rai, Thailand and received another extension for the amount due by December 15, 2019.The Company seeks to develop a destination site for locals and foreign tourists by establishing a “100 Years Café” coffee shop and souvenir shops that celebrate over 100 years of the Thai flag.

The Company has secured an exclusive license by the government of Thailand to promote, market, and sell souvenirs and collectable products based on the Thai largest flag in Chiang Rai, Thailand. Currently, the Company has created the flag portion of the tallest flagpole and largest flag project but not the flagpole itself. The flagpole is currently under production by an American company and expected to be delivered by 2019. The flag portion measuring 42 meters in height and 63 meters in length was given honors and recognition by the Guinness Book of World Records on November 30, 2016.

The Project

The Company seeks to acquire full rights and ownership in 126 hectares of land in the Chiang Saen District of Chiang Rai, Thailand within a Free Trade Zone designated area to develop a leisure and tourist destination designed for both local and foreign tourists. The Company believes that this area holds beneficial value based on the “One Belt, One Road” initiative or “OBOR”. Announced by the Chinese government in 2013, OBOR is a development strategy by the Chinese government which focuses on connectivity and cooperation between Europe, Africa, China and Southeast Asia. The OBOR initiative is designed to increase the flow of trade, aimed at building new infrastructure, and increasing cultural exchanges.

The project and acquisition costs are expected to cost over an estimated $6 million USD, while the construction of the flagpole, mall, office building complex, hotel, spiritual center and shops are expected to cost $120 million USD. As of the date of this Form 10-Q, the Company has paid 5 million Thai Baht, or $159,000 in US dollars and owes a balance of 195 million Thai Baht, or $6,228,300 in US dollars (at today’s exchange rates) for the land in Chiang Rai, Thailand and received another extension for the amount due by December 15, 2019.The Company seeks to develop a destination site for locals and foreign tourists by establishing a “100 Years Café” coffee shop and souvenir shops that celebrate over 100 years of the Thai flag.

The Company has secured an exclusive license by the government of Thailand to promote, market, and sell souvenirs and collectable products based on the Thai largest flag in Chiang Rai, Thailand. Currently, the Company has created the flag portion of the tallest flagpole and largest flag project but not the flagpole itself. The flagpole is currently underproduction by an American company and expected to be delivered by 2019. The flag portion measuring 42 meters in height and 63 meters in length was given honors and recognition by the Guinness Book of World Records on November 30, 2016.

The Area

The Company is seeking to fully acquire and develop 126 hectares of land in the Chiang Saen District of Chiang Rai, Thailand. Chiang Rai is located in northern Thailand near the borders of Laos and Myanmar (formerly Burma). The area is known as a cultural center with attractions and parks with night bazaar markets and many Buddhist temples. In previous years, Chiang Rai has been known as the “Golden Triangle” which it is still called. The Golden Triangle is the area which meaning comes from the proximity to Laos, Myanmar and Thailand.

(Project land site view from road)

(View of project and surrounding land area)

(Map of project site and proximity to the Mekong River)

Other notable tourist attractions in the area are royal temples that once housed the Emerald Buddha, a jade structure which was replaced with a replica. There are also 100 Khmer (Cambodian) style pillars and temples. In addition, there are historic museums and cultural parks in the area.

The Thai Flag

The Company had directed its efforts by the end of 2015 to develop the tallest and largest flagpole in the world in the Chiang Saen District of Chiang Rai, Thailand. It was since awarded with the prestigious honor of being the largest flag in Thailand by the Guinness Book of World Records. The flag pole itself is pending development along with a park and concession area for tourists primarily from China.

The flag of Thailand plays a significant role in the Company’s plans to expand its business plan. The flag of Thailand has been the same without change from September 28, 1917 to present, or for over 100 years. To celebrate this fact, the Company has merchandise with the “100 Years” labeling on t-shirts, banners, flags, and other collectables. The people of Thailand are strongly supportive and proud of their country and flag. The national flag is seen on display in many places within the country. The colors of the flag represent three important items to the Thai people, red is said to represent the people and the blood which was shed to keep the country independent, the white represents religion or the purity of Buddhism and the blue represents the monarchy in Thailand.

(ANDES 7 produced the largest Flag in Thailand in connection with the 100 Year’s Anniversary of the flag)

The Tourism Industry

According to the World Travel & Tourism Council, 20.6% of the GDP, (or $82.5 billion USD) of Thailand in 2016 was from tourism. The World Travel & Tourism Council anticipates that by 2027, 31.7% (or $169.9 billion USD) of GDP will be from tourism. The majority of tourists are from other South East Asian countries or ASEAN (Association of South East Nations), followed by China and Europe. The Company believes that with new infrastructure being commissioned and built by both the Thai government and China through its OBOR initiative, is likely to have an impact on tourism in Thailand. In early 2018, the Thai government approved a high speed rail project that would connect major cities in southern Thailand to the north. According to Reuters, in 2016, Thailand had 33 million foreign tourists visiting Thailand, and Bangkok in particular with Chinese tourists comprising over 26% of that figure. Additionally, according to Mastercard Index of Global Destination Cities, in 2016, Bangkok was the world’s top destination beating 132 cities worldwide, such as London, Paris and Dubai. Thailand earned $71.4 billion in 2017 from tourist revenue which was higher by 11% percent from 2015. The Tourism Authority of Thailand attributes the increase in travel to Thailand to the increased demand from short haul markets during school holidays, heavy interest from the China market, and continued development of long haul markets in Europe, the United States and Russia.

Employees

As of the date of this Form 10-Q quarterly report, ANDES 7 Inc. employed a staff of 6 people of which are in management and administration located at 333, Village 6, Amphur Wiang, Chiang Rai, Thailand 57150. The Company considers its relationship with its employees to be favorable.

Facilities and Logistics

The Company maintains a virtual office in San Francisco, California, in the United States at 424 Clay Street, Lower Level, San Francisco, CA 94111. Its headquarters are located at 333, Village 6, Amphur Wiang, Chiang Rai, Thailand.

| | | |

| Location | Address | Size |

| San Francisco, California | 424 Clay Street, Lower Level

San Francisco, CA 94111 | n/a (virtual office) |

| | | |

| Chiang Rai, Thailand | 333, Village 6, Amphur Wiang

Chiang Rai, Thailand 57150 | 16,000 square meters |

Involvement in Certain Legal Proceedings

None of our officers or directors, promoters or control persons have been involved in the past ten years of any of the following:

(1) Any bankruptcy petition filed by or against any business of which such person was a general partner or executive officer either at the time of the bankruptcy or within two years prior to that time;

(2) Any conviction in a criminal proceeding or being subject to a pending criminal proceeding (excluding traffic violations and other minor offenses);

(3) Being subject to any order, judgment or decree, not subsequently reversed, suspended or vacated, or any court of competent jurisdiction, permanently or temporarily enjoining, barring, suspending or otherwise limiting his involvement in any type of business, securities or banking activities; or

(4) Being found by a court of competent jurisdiction (in a civil action), the Commission or the Commodity Futures Trading Commission to have violated a federal or state securities or commodities law, and the judgment has not been reversed, suspended, or vacated.

Patents

The Company has no patents and no intentions at this time to apply for any patents. The Company however, may choose to file for trademarks upon development of its project in the Chiang Saen District of Chiang Raito to protect its intellectual property.

Results of Operations

Results of Operations for the Three Months Ended June 30, 2019, compared to the Three Months Ended June 30, 2018

Revenues

Sales revenue for the three months ended June 30, 2019 was $4,807, compared to $2,644 for the three months ended June 30, 2018.

Cost of Goods Sold

Cost of revenue for the three months ended June 30, 2019, was $1,993, compared to $2,335 for the three months ended June 30, 2018, a decrease of $342. This decrease was due to the existing inventory held and limited new designs for our t-shirts and souvenirs that were purchased during the period.

Operating Expenses

General and administrative expense was $44,957 for the three months ended June 30, 2019, compared to $74,532 for the three months ended June 30, 2018, a decrease of $29,575.

Rent expense was $2,851 for the three months ended June 30, 2019, compared to $2,810 for the three months ended June 30, 2018, an increase of $41.

Advertising and promotion expenses were $143 for the three months ended June 30, 2019, compared to $808 for the three months ended June 30, 2018, a decrease of $665. Advertising and promotion expense consists of advertising in magazines and promotional product giveaways of t-shirts and other souvenirs.

Professional fees were $13,028 for the three months ended June 30, 2019, compared to $0 for the three months ended June 30, 2018.

Other Income (Expenses)

Interest income for the three months ended June 30, 2019 and June 30, 2018, was $0.

Interest expense for the three months ended June 30, 2019 was $426, compared to $415 for the three months ended June 30, 2018.

Net Loss

Net loss for the for the three months ended June 30, 2019 was $58,591, compared to $78,256 for the three months ended June 30, 2018.

Results of Operations for the Six Months Ended June 30, 2019, compared to the Six Months Ended June 30, 2018

Revenues

Sales revenue for the six months ended June 30, 2019 was $7,245, compared to $3,500 for the six months ended June 30, 2018.

Cost of Goods Sold

Cost of revenue for the six months ended June 30, 2019, was $2,947, compared to $5,226 for the six months ended June 30, 2018, a decrease of $2,279. This decrease was due to the existing inventory held and limited new designs for our t-shirts and souvenirs that were purchased during the period.

Operating Expenses

General and administrative expense was $73,091 for the six months ended June 30, 2019, compared to $167,324 for the six months ended June 30, 2018, a decrease of $94,233.

Rent expense was $5,698 for the six months ended June 30, 2019, compared to $7,566 for the six months ended June 30, 2018, a decrease of $1,868.

Advertising and promotion expenses were $848 for the six months ended June 30, 2019, compared to $8,449 for the six months ended June 30, 2018, a decrease of $7,601. Advertising and promotion expense consists of advertising in magazines and promotional product giveaways of t-shirts and other souvenirs.

Professional fees were $20,767 for the six months ended June 30, 2019, compared to $0 for the six months ended June 30, 2018.

Other Income (Expenses)

Interest income for the six months ended June 30, 2019 and June 30, 2018, was $0.

Interest expense for the six months ended June 30, 2019 was $775, compared to $1,767 for the six months ended June 30, 2018.

Net Loss

Net loss for the for the six months ended June 30, 2019 was $96,881, compared to $186,832 for the six months ended June 30, 2018.

Off-Balance Sheet Arrangements

The Company does not have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on the Company’s financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that is material to investors

Liquidity

The accompanying unaudited financial statements have been prepared in conformity with generally accepted accounting principles, which contemplate continuation of the Company as a going concern. As of June 30, 2019, we had cash of $1,988and total liabilities of $1,485,197. We used $118,407 of cash flows in operating activities for the six months ended June 30, 2019. Our current cash balance and cash flow from operating activities will not be sufficient to fund our operations.

Over the next 12 months we expect to expend approximately $30,000 in cash for legal, accounting and related services. Cash used for other expenditures is expected to be minimal. We hope to be able to attract suitable investors for our business plan, which will not require us to use our cash, although there can be no assurances that we will be successful in these efforts.

We expect to be able to secure capital through advances from our Chief Executive Officer, shareholders and others in order to pay expenses such as organizational costs, filing fees, accounting fees and legal fees. We believe it will be difficult to secure capital in the future because we have no assets to secure debt and there is currently no trading market for our securities. We will need additional capital in the next twelve months and if we cannot raise such capital on acceptable terms, we may have to curtail our operations or terminate our business entirely.

The inability to obtain financing or generate sufficient cash from operations could require us to reduce or eliminate expenditures for acquiring suitable partners or otherwise curtail or discontinue our operations, which could have a material adverse effect on our business, financial condition and results of operations. Furthermore, to the extent that we raise additional capital through the sale of equity or convertible debt securities, the issuance of such securities may result in dilution to existing stockholders. If we raise additional funds through the issuance of debt securities, these securities may have rights, preferences and privileges senior to holders of our common stock and the terms of such debt could impose restrictions on our operations. Regardless of whether our cash assets prove to be inadequate to meet our operational needs, we may seek to compensate providers of services by issuing stock in lieu of cash, which may also result in dilution to existing stockholders.

Operating Capital and Capital Expenditure Requirements

Our controlling shareholders expect to advance us additional funding for operating costs in order to implement our business plan. The funds are loaned to the Company as required to pay amounts owed by the Company. As such, our operating capital is currently limited to the resources of our controlling shareholders. The loans from our controlling shareholders are unsecured and non-interest bearing and have no set terms of repayment. We anticipate receiving additional capital once we are able to have our securities actively trading on a public exchange. There is no guarantee our stock will develop a market on that public exchange.

Item 3. Quantitative and Qualitative Disclosures About Market Risk.

None.

Item 4. Controls and Procedures.

Evaluation of Disclosure Controls and Procedures

As required by Rule 13a-15 under the Securities Exchange Act of 1934, we have carried out an evaluation of the effectiveness of our disclosure controls and procedures as of the end of the period covered by this quarterly report, June 30, 2019. This evaluation was carried out under the supervision and with the participation of our management, including our Chief Executive Officer and Chief Financial Officer.

Disclosure controls and procedures are controls and other procedures that are designed to ensure that information required to be disclosed in our reports filed or submitted under the Securities Exchange Act of 1934 is recorded, processed, summarized and reported, within the time periods specified in the Securities and Exchange Commission’s rules and forms. Disclosure controls and procedures include controls and procedures designed to ensure that information required to be disclosed in our company’s reports filed under the Securities Exchange Act of 1934 is accumulated and communicated to management, including our Chief Executive Officer and Chief Financial Officer, to allow timely decisions regarding required disclosure.

Based upon that evaluation, including our Chief Executive Officer and Chief Financial Officer, we have concluded that our disclosure controls and procedures were ineffective as of the end of the period covered by this report due to a material weakness in our internal control over financial reporting, which is described below.

Management’s Report on Internal Control over Financial Reporting

Our management is responsible for establishing and maintaining adequate internal control over financial reporting (as defined in Rule 13a-15(f) under the Securities Exchange Act of 1934). Management has assessed the effectiveness of our internal control over financial reporting as of June 30, 2019, based on criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission. As a result of this assessment, management concluded that, as of June 30, 2019, our internal control over financial reporting was not effective. Our management identified the following material weaknesses in our internal control over financial reporting, which are indicative of many small companies with small staff: (i) inadequate segregation of duties and effective risk assessment; and (ii) insufficient written policies and procedures for accounting and financial reporting with respect to the requirements and application of both US GAAP and SEC guidelines.

We plan to take steps to enhance and improve the design of our internal control over financial reporting. During the period covered by this quarterly report on Form 10-Q, we have not been able to remediate the material weaknesses identified above. To remediate such weaknesses, we hope to implement the following changes during our fiscal year ending December 31, 2019: (i) appoint additional qualified personnel to address inadequate segregation of duties and ineffective risk management; and (ii) adopt sufficient written policies and procedures for accounting and financial reporting. The remediation efforts set out in (i) and (ii) are largely dependent upon our securing additional financing to cover the costs of implementing the changes required. If we are unsuccessful in securing such funds, remediation efforts may be adversely affected in a material manner.

Changes in Internal Control over Financial Reporting

There were no changes in our internal control over financial reporting during the quarter ended June 30, 2019 have materially affected or are reasonably likely to materially affect, our internal control over financial reporting.

PART II - OTHER INFORMATION

Item 1. Legal Proceedings.

There are not presently any material pending legal proceedings to which the Registrant is a party or as to which any of its property is subject, and no such proceedings are known to the Registrant to be threatened or contemplated against it.

Item 1A. Risk Factors

A smaller reporting company is not required to provide the information required by this Item.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds.

None.

Item 3. Defaults Upon Senior Securities.

None.

Item 4. Mine Safety Disclosures

Not applicable.

Item 5. Other Information.

None.

Item 6. Exhibits

SIGNATURES

In accordance with the requirements of the Exchange Act, the Registrant caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| | ANDES 7 Inc. |

| | | |

| | By: | /s/ Andrew Khor Poh Kiang |

| | | Andrew Khor Poh Kiang President, Chief Executive Officer, Chairman of the Board of Directors |

| | | |

| | By: | /s/ Lee Kok Keing |

| | | Lee Kok Keing Chief Financial Officer |

Dated: August 19, 2019