| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-193376-24 | ||

October 13, 2015

FREE WRITING PROSPECTUS

STRUCTURAL AND COLLATERAL TERM SHEET

$931,617,393

(Approximate Total Mortgage Pool Balance)

$803,520,000

(Approximate Offered Certificates)

COMM 2015-CCRE27 |

Deutsche Mortgage & Asset Receiving Corporation

Depositor

German American Capital Corporation

The Bank of New York Mellon

KeyBank National Association

Cantor Commercial Real Estate Lending, L.P.

Sponsors and Mortgage Loan Sellers

| Deutsche Bank Securities | Cantor Fitzgerald & Co. | |

| Joint Bookrunning Managers and Co-Lead Managers | ||

| KeyBanc Capital Markets | Goldman, Sachs & Co. | CastleOak Securities, L.P. |

| Co-Managers | ||

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-193376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

COMM 2015-CCRE27 Mortgage Trust

Capitalized terms used but not defined herein have the meanings assigned to them in the other Free Writing Prospectus expected to be dated October 13, 2015, relating to the offered certificates (hereinafter referred to as the “Free Writing Prospectus”).

| KEY FEATURES OF SECURITIZATION |

| Offering Terms: | |

| Joint Bookrunners & Co-Lead Managers: | Deutsche Bank Securities Inc. and Cantor Fitzgerald & Co. |

| Co-Managers: | KeyBanc Capital Markets, CastleOak Securities, L.P. and Goldman, Sachs & Co. |

| Mortgage Loan Sellers: | German American Capital Corporation* (“GACC”) (42.7%), The Bank of New York Mellon (“BNYM”) (21.1%), KeyBank National Association (“KeyBank”) (20.8%) and Cantor Commercial Real Estate Lending, L.P. (“CCRE”) (15.4%). *An indirect wholly owned subsidiary of Deutsche Bank AG. |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

| Operating Advisor: | Park Bridge Lender Services LLC |

| Special Servicer: | Rialto Capital Advisors, LLC |

| Trustee: | Wells Fargo Bank, National Association |

| Rating Agencies: | Moody’s Investors Service, Inc., Fitch Ratings, Inc. and DBRS, Inc. |

| Determination Date: | 6th day of each month, or if such 6th day is not a business day, the following business day, commencing in November 2015. |

| Distribution Date: | 4th business day following the Determination Date in each month, commencing in November 2015. |

| Cut-off Date: | Payment Date in October 2015 (or related origination date, if later). Unless otherwise noted, all Mortgage Loan statistics are based on balances as of the Cut-off Date. |

| Settlement Date: | On or about October 29, 2015 |

| Settlement Terms: | DTC, Euroclear and Clearstream, same day funds, with accrued interest. |

| ERISA Eligible: | All of the Offered Certificates are expected to be ERISA eligible. |

| SMMEA Eligible: | None of the Offered Certificates will be SMMEA eligible. |

| Day Count: | 30/360 |

| Tax Treatment: | REMIC |

| Rated Final Distribution Date: | October 2048 |

| Minimum Denominations: | $10,000 (or $100,000 with respect to Class X-A) and in each case in multiples of $1 thereafter. |

| Clean-up Call: | 1% (with certain exceptions described under“The Pooling and Servicing Agreement—Optional Termination” in the Free Writing Prospectus) |

| Distribution of Collateral by Property Type |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 3 |

COMM 2015-CCRE27 Mortgage Trust

| TRANSACTION HIGHLIGHTS |

| Mortgage Loan Sellers | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Outstanding Pool Balance | ||

| German American Capital Corporation | 20 | 34 | $397,893,862 | 42.7% | ||

| The Bank of New York Mellon | 12 | 16 | $196,225,586 | 21.1% | ||

| KeyBank National Association | 25 | 28 | $194,035,645 | 20.8% | ||

| Cantor Commercial Real Estate Lending, L.P. | 8 | 18 | $143,462,300 | 15.4% | ||

| Total: | 65 | 96 | $931,617,393 | 100.0% | ||

| Pooled Collateral Facts: | |

| Initial Outstanding Pool Balance: | $931,617,393 |

| Number of Mortgage Loans: | 65 |

| Number of Mortgaged Properties: | 96 |

| Average Mortgage Loan Cut-off Date Balance: | $14,332,575 |

| Average Mortgaged Property Cut-off Date Balance: | $9,704,348 |

| Weighted Average Mortgage Rate: | 4.4889% |

| Weighted Average Mortgage Loan Original Term to Maturity Date or ARD (months): | 115 |

| Weighted Average Mortgage Loan Remaining Term to Maturity Date or ARD (months): | 114 |

| Weighted Average Mortgage Loan Seasoning (months): | 1 |

| % of Mortgaged Properties Leased to a Single Tenant: | 3.1% |

| Credit Statistics(1): | |

| Weighted Average Mortgage Loan U/W NCF DSCR(2): | 1.77x |

| Weighted Average Mortgage Loan Cut-off Date LTV(3)(4): | 65.5% |

| Weighted Average Mortgage Loan Maturity Date or ARD LTV(3)(4): | 57.8% |

| Weighted Average U/W NOI Debt Yield: | 10.4% |

| Amortization Overview: | |

| % Mortgage Loans with Amortization through Maturity Date or ARD: | 33.9% |

| % Mortgage Loans which pay Interest Only through Maturity Date or ARD: | 20.6% |

| % Mortgage Loans which pay Interest Only followed by Amortization through Maturity Date or ARD: | 45.5% |

| Weighted Average Remaining Amortization Term (months)(2)(5): | 357 |

| Loan Structural Features: | |

| % Mortgage Loans with Upfront or Ongoing Tax Reserves: | 91.2% |

| % Mortgage Loans with Upfront or Ongoing Replacement Reserves(6): | 87.8% |

| % Mortgage Loans with Upfront or Ongoing Insurance Reserves: | 41.1% |

| % Mortgage Loans with Upfront or Ongoing TI/LC Reserves(7): | 92.1% |

| % Mortgage Loans with Upfront Engineering Reserves: | 49.3% |

| % Mortgage Loans with Upfront or Ongoing Other Reserves: | 38.6% |

| % Mortgage Loans with In Place Hard Lockboxes: | 31.2% |

| % Mortgage Loans with Cash Traps Triggered at DSCR Levels ≥ 1.10x: | 85.7% |

| % Mortgage Loans with Cash Traps Triggered only based on Loan Specific Debt Yield: | 7.5% |

| % Mortgage Loans with Defeasance Only After a Lockout Period and Prior to an Open Period: | 88.5% |

| % Mortgage Loans with Prepayment Only After a Lockout Period and Prior to an Open Period with a Yield Maintenance Charge: | 11.5% |

| (1) | With respect to the 11 Madison Avenue Mortgage Loan and NMS Los Angeles Multifamily Portfolio Mortgage Loan the LTV, DSCR and Debt Yield calculations include the relatedpari passucompanion loan(s), but not any related subordinate companion loan(s). |

| (2) | With respect to the Atlanta Multifamily Portfolio Mortgage Loan, representing approximately 4.8% of the initial outstanding pool balance, following an initial interest only period of 18 months, the mortgage loan amortizes based on a non-standard amortization schedule and the U/W NCF DSCR for such Mortgage Loan was calculated based on the debt service for the first 12 amortizing payments. For additional information, see Annex H to the Free Writing Prospectus. |

| (3) | With respect to two mortgage loans, representing 6.4% of the initial outstanding principal balance, the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated based on the “as complete” or “as renovated” value. For additional information, see the Footnotes to Annex A-1 in the Free Writing Prospectus. |

| (4) | With respect to the NMS Los Angeles Multifamily Portfolio Mortgage Loan, Sandalwood Portfolio Mortgage Loan and the Midwest Shopping Center Portfolio Mortgage Loan, collectively representing 17.8% of the initial outstanding pool balance, the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated based on the “as portfolio” appraised value, which attributes a premium to the aggregate value of the mortgaged properties as a whole. For additional information, see the Footnotes to Annex A-1 in the Free Writing Prospectus. |

| (5) | Excludes loans which are interest only for the full loan term. |

| (6) | Includes FF&E Reserves. |

| (7) | Represents the percent of the allocated initial outstanding principal balance of retail, office, industrial and mixed use properties only. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 4 |

COMM 2015-CCRE27 Mortgage Trust

| STRUCTURE OVERVIEW |

OFFERED CERTIFICATES

| Class(1) | Ratings (Moody’s/Fitch/DBRS) | Initial Certificate Balance or Notional Amount(2) | Initial | Weighted | Principal Window (months)(3) | Certificate Principal to Value Ratio(4) | Underwritten | ||||||||

| Class A-1 | Aaa(sf)/AAAsf/AAA(sf) | $38,731,000 | 30.000%(6) | 2.79 | 1 - 58 | 45.8% | 14.9% | ||||||||

| Class A-2 | Aaa(sf)/AAAsf/AAA(sf) | $72,542,000 | 30.000%(6) | 4.87 | 58 - 60 | 45.8% | 14.9% | ||||||||

| Class A-SB | Aaa(sf)/AAAsf/AAA(sf) | $62,544,000 | 30.000%(6) | 7.47 | 60 - 117 | 45.8% | 14.9% | ||||||||

| Class A-3 | Aaa(sf)/AAAsf/AAA(sf) | $215,000,000 | 30.000%(6) | 9.79 | 117 - 119 | 45.8% | 14.9% | ||||||||

| Class A-4 | Aaa(sf)/AAAsf/AAA(sf) | $263,315,000 | 30.000%(6) | 9.86 | 119 - 119 | 45.8% | 14.9% | ||||||||

| Class X-A(7) | Aa1(sf)/AAAsf/AAA(sf) | $705,700,000 | (8) | N/A | N/A | N/A | N/A | N/A | |||||||

| Class A-M | Aa2(sf)/AAAsf/AAA(sf) | $53,568,000 | 24.250% | 9.86 | 119 - 119 | 49.6% | 13.7% | ||||||||

| Class B | A1(sf)/AA-sf/AA(sf) | $54,732,000 | 18.375% | 9.86 | 119 - 119 | 53.5% | 12.7% | ||||||||

| Class C | NR/A-sf/A(sf) | $43,088,000 | 13.750% | 9.86 | 119 - 119 | 56.5% | 12.1% | ||||||||

NON-OFFERED CERTIFICATES

| Class(1) | Ratings (Moody’s/Fitch/DBRS) | Initial Certificate Balance or Notional Amount(2) | Initial | Weighted | Principal Window (months)(3) | Certificate Principal to Value Ratio(4) | Underwritten | ||||||||

| Class X-B(7) | NR/A-sf/AAA(sf) | $97,820,000 | (8) | N/A | N/A | N/A | N/A | N/A | |||||||

| Class X-C(7) | NR/BBB-sf/AAA(sf) | $51,238,000 | (8) | N/A | N/A | N/A | N/A | N/A | |||||||

| Class X-D(7) | NR/NR/AAA(sf) | $33,772,000 | (8) | N/A | N/A | N/A | N/A | N/A | |||||||

| Class X-E(7) | NR/NR/AAA(sf) | $13,974,000 | (8) | N/A | N/A | N/A | N/A | N/A | |||||||

| Class X-F(7) | NR/NR/AAA(sf) | $29,113,392 | (8) | N/A | N/A | N/A | N/A | N/A | |||||||

| Class D | NR/BBB-sf/BBB(low)(sf) | $51,238,000 | 8.250% | 9.94 | 119 - 120 | 60.1% | 11.3% | ||||||||

| Class E | NR/BB-sf/BB(low)(sf) | $24,455,000 | 5.625% | 9.95 | 120 - 120 | 61.8% | 11.0% | ||||||||

| Class F | NR/B-sf/B(high)(sf) | $9,317,000 | 4.625% | 9.95 | 120 - 120 | 62.5% | 10.9% | ||||||||

| Class G | NR/NR/B(low)(sf) | $13,974,000 | 3.125% | 9.95 | 120 - 120 | 63.5% | 10.7% | ||||||||

| Class H | NR/NR/NR | $29,113,392 | 0.000% | 9.95 | 120 - 120 | 65.5% | 10.4% | ||||||||

| (1) | The pass-through rates applicable to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H Certificates will equal one of: (i) a fixed per annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, (iii) a rate equal to the lesser of a specified pass-through rate and the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs or (iv) the weighted average of the net mortgage rates on the mortgage loans) (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, less a specified rate. |

| (2) | Approximate; subject to a permitted variance of plus or minus 5%. In addition, the notional amounts of the Class X-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates (collectively, the “Class X Certificates”) may vary depending upon the final pricing of the classes of Certificates whose Certificate Balances comprise such notional amounts and, if as a result of such pricing the pass-through rate of any class of Class X Certificates would be equal to zero, such Class X Certificates may not be issued on the settlement date of this securitization. |

| (3) | The weighted average life and principal window during which distributions of principal would be received as set forth in the table with respect to each class of Certificates with a Certificate Balance is based on (i) modeling assumptions described in the Free Writing Prospectus, (ii) assumptions that there are no prepayments, delinquencies or losses on the mortgage loans and (iii) assumptions that there are no extensions of maturity dates and mortgage loans with anticipated repayment dates, if any, are repaid on the respective anticipated repayment dates. |

| (4) | “Certificate Principal to Value Ratio” for any class with a Certificate Balance is calculated as the product of (a) the weighted average Mortgage Loan Cut-off Date LTV of the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of the related class of Certificates and all other classes with a Certificate Balance, if any, that are senior to such class, and the denominator of which is the total initial Certificate Balance of all Certificates. The Certificate Principal to Value Ratios of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are calculated in the aggregate for those classes as if they were a single class. |

| (5) | “Underwritten NOI Debt Yield” for any class with a Certificate Balance is calculated as the product of (a) the weighted average U/W NOI Debt Yield for the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of all Certificates and the denominator of which is the total initial Certificate Balance of the related class of Certificates and all other classes with a Certificate Balance, if any, that are senior to such class. The Underwritten NOI Debt Yields of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are calculated in the aggregate for those classes as if they were a single class. |

| (6) | The initial subordination levels for the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are represented in the aggregate. |

| (7) | As further described in the Free Writing Prospectus, the pass-through rate applicable to the Class X Certificates for each Distribution Date will generally be equal to the excess of (i) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360 day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs over (ii)(A) with respect to the Class X-A Certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M Certificates (based on their Certificate Balances), (B) with respect to the Class X-B Certificates, the weighted average of the pass-through rates of the Class B and Class C Certificates (based on their Certificate Balances), (C) with respect to the Class X-C Certificates, the pass-through rate of the Class D Certificates, (D) with respect to the Class X-D Certificates, the weighted average of the pass-through rates of the Class E and Class F Certificates (based on their Certificate Balances), (E) with respect to the Class X-E Certificates, the pass-through rate of the Class G Certificates and (F) with respect to the Class X-F Certificates, the pass-through rate of the Class H Certificates. |

| (8) | The Class X Certificates will not have Certificate Balances. None of the Class X Certificates will be entitled to distributions of principal. The interest accrual amounts on the Class X-A Certificates will be calculated by reference to a notional amount equal to the sum of the total Certificate Balance of each of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M Certificates. The interest accrual amounts on the Class X-B Certificates will be calculated by reference to a notional amount equal to the sum of the total Certificate Balance of each of the Class B and Class C Certificates. The interest accrual amounts on the Class X-C Certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class D Certificates. The interest accrual amounts on the Class X-D Certificates will be calculated by reference to a notional amount equal to the sum of the total Certificate Balance of each the Class E and Class F Certificates. The interest accrual amounts on the Class X-E Certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class G Certificates. The interest accrual amounts on the Class X-F Certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class H Certificates. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 5 |

COMM 2015-CCRE27 Mortgage Trust

| STRUCTURE OVERVIEW |

| Class A-2 Principal Paydown(1) |

Mortgage | Mortgage Loan | Property Type | Cut-off Date Balance | Remaining Term to Maturity (Mos.) | Cut-off Date LTV Ratio | U/W | U/W NOI | |||||||

| GACC | The Phenix at Infinity Park II | Multifamily | $14,250,000 | 58 | 71.6% | 1.34x | 8.3% | |||||||

| GACC | Atlanta Multifamily Portfolio | Multifamily | $45,000,000 | 59 | 64.9% | 1.30x | 8.3% | |||||||

| BNYM | WHG Extended Stay Portfolio | Hospitality | $15,500,000 | 60 | 70.5% | 1.95x | 13.7% |

| (1) | This table reflects the mortgage loans whose balloon payments will be applied to pay down the Class A-2 Certificates, assuming (i) that none of the mortgage loans experience prepayments, defaults or losses, (ii) there are no extensions of maturity dates and (iii) each mortgage loan is paid in full on its stated maturity date, or in the case of any mortgage loan with an anticipated repayment date, on such repayment date. See “Yield and Maturity Considerations—Yield Considerations” in the Free Writing Prospectus. |

| (2) | With respect to the Atlanta Multifamily Portfolio Mortgage Loan, representing approximately 4.8% of the initial outstanding pool balance, following an initial interest only period of 18 months, the mortgage loan amortizes based on a non-standard amortization schedule and the U/W NCF DSCR for such Mortgage Loan was calculated based on the debt service for the first 12 amortizing payments. For additional information, see Annex H to the Free Writing Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 6 |

COMM 2015-CCRE27 Mortgage Trust

| STRUCTURE OVERVIEW |

| Principal Payments: | Payments in respect of principal of the Certificates will be distributed,first, to the Class A-SB Certificates, until the Certificate Balance of such Class is reduced to the planned principal balance for the related Distribution Date set forth on Annex A-3 to the Free Writing Prospectus,then, to the Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H Certificates, in that order, until the Certificate Balance of each such Class is reduced to zero. Notwithstanding the foregoing, if the total principal balance of the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H Certificates have been reduced to zero as a result of loss allocation, payments in respect of principal of the Certificates will be distributed,first, to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates, on apro rata basis, based on the Certificate Balance of each such Class,then, to the extent of any recoveries on realized losses, to the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H Certificates, in that order, in each case until the Certificate Balance of each such Class is reduced to zero (or previously allocated realized losses have been fully reimbursed). | |

| Each Class of Class X Certificates will not be entitled to receive distributions of principal; however, (i) the notional amount of the Class X-A Certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M Certificates; (ii) the notional amount of the Class X-B Certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class B and Class C Certificates; (iii) the notional amount of the Class X-C Certificates will be reduced by the principal distributions and realized losses allocated to the Class D Certificates; (iv) the notional amount of the Class X-D Certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class E and Class F Certificates; (v) the notional amount of the Class X-E Certificates will be reduced by the principal distributions and realized losses allocated to the Class G Certificates and (vi) the notional amount of the Class X-F Certificates will be reduced by the principal distributions and realized losses allocated to the Class H Certificates. | ||

| Interest Payments: | On each Distribution Date, interest accrued for each Class of the Certificates at the applicable pass-through rate will be distributed in the following order of priority, to the extent of available funds:first, to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class X-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates, on apro rata basis, based on the accrued and unpaid interest on each such Class andthen, to the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H Certificates, in that order, in each case until the interest payable to each such Class is paid in full. | |

| The pass-through rates applicable to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H Certificates for each Distribution Date will equal one of: (i) a fixedper annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, (iii) a rate equal to the lesser of a specified pass-through rate and the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs or (iv) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, less a specified rate. | ||

| As further described in the Free Writing Prospectus, the pass-through rates applicable to the Class X Certificates for each Distribution Date will generally be equal to the excess of (i) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs over (ii) (A) with respect to the Class X-A Certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M Certificates (based on their Certificate Balances), (B) with respect to the Class X-B Certificates, the weighted average of the pass-through rates of the Class B and Class C Certificates (based on their Certificate Balances), (C) with respect to the Class X-C Certificates, the pass-through rate of the Class D Certificates, (D) with respect to the Class X- |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 7 |

COMM 2015-CCRE27 Mortgage Trust

| STRUCTURE OVERVIEW |

| D Certificates, the weighted average of the pass-through rates of the Class E and Class F Certificates (based on their Certificate Balances), (E) with respect to the Class X-E Certificates, the pass-through rate of the Class G Certificates and (F) with respect to the Class X-F Certificates, the pass-through rate of the Class H Certificates. | ||

| Prepayment Interest Shortfalls: | Prepayment interest shortfalls will be allocatedpro rata based on interest entitlements, in reduction of the interest otherwise payable with respect to each of the interest-bearing Classes of Certificates. | |

| Loss Allocation: | Losses will be allocated to each Class of Certificates entitled to principal in reverse alphabetical order starting with Class H through and including Class A-M and then to Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates on apro ratabasis based on the Certificate Balance of each such Class. The notional amount of any Class of Class X Certificates will be reduced by the aggregate amount of realized losses allocated to the Certificates that are components of the notional amount of such Class of Class X Certificates. | |

| Prepayment Premiums: | A percentage of all prepayment premiums (either fixed prepayment premiums or yield maintenance amounts) collected on the Mortgage Loans will be allocated to each of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C and Class D Certificates (the “YM P&I Certificates”) then entitled to principal distributions, which percentage will be equal to the product of (a) a fraction, not greater than one, the numerator of which is the amount of principal distributed to such Class on such Distribution Date and the denominator of which is the total amount of principal distributed to the holders of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H Certificates on such Distribution Date, and (b) a fraction (expressed as a percentage which can be no greater than 100% nor less than 0%), the numerator of which is the excess of the pass-through rate of each such Class of Certificates currently receiving principal over the relevant Discount Rate, and the denominator of which is the excess of the Mortgage Rate of the related Mortgage Loan over the relevant Discount Rate. | |

| Prepayment Premium Allocation Percentage for all YM P&I Certificates = |

| (Pass-Through Rate - Discount Rate) | X | The percentage of the principal distribution amount to such Class as described in (a) above | ||

| (Mortgage Rate - Discount Rate) |

| The remaining percentage of the prepayment premiums will be allocated to the Class X-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates in the manner described in the Free Writing Prospectus. In general, this formula provides for an increase in the percentage of prepayment premiums allocated to the YM P&I Certificates then entitled to principal distributions relative to the Class X-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates as Discount Rates decrease and a decrease in the percentage allocated to such Classes as Discount Rates rise. | ||

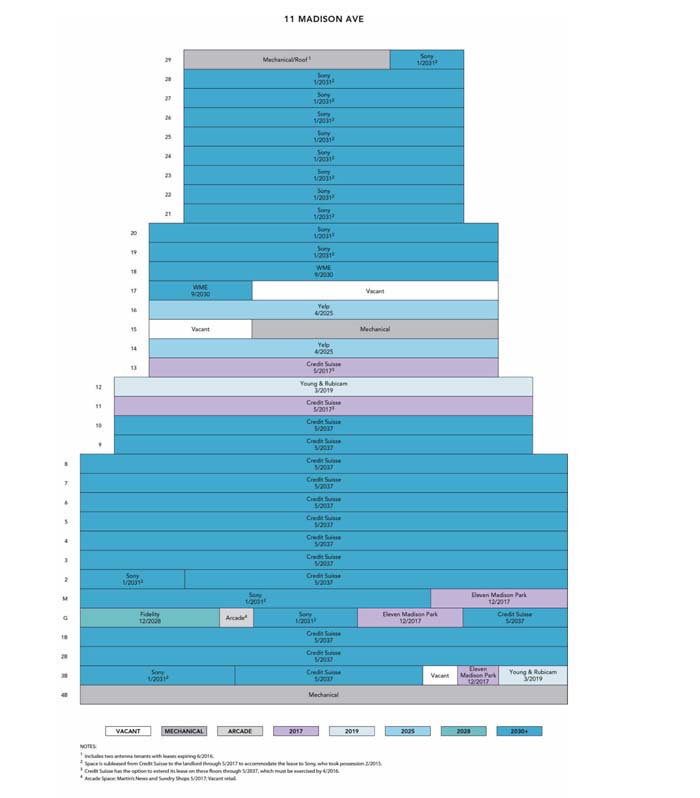

| Loan Combinations: | The Mortgaged Property identified on Annex A–1 to the Free Writing Prospectus as 11 Madison Avenue secures (i) a Mortgage Loan evidenced by a promissory note designated as Note A-1-C2 with an outstanding principal balance as of the Cut-off Date of $70,000,000 (the “11 Madison Avenue Mortgage Loan”), representing approximately 7.5% of the Initial Outstanding Pool Balance. The 11 Madison Avenue Loan Combination (as defined below) is evidenced by: (i) one promissory Note A-1-C2 that evidences the 11 Madison Avenue Mortgage Loan; (ii) ninepari passu promissory notes designated as Note A-1-S1, Note A-1-S2, Note A-1-S3, Note A-2-S1, Note A-2-S2, Note A-2-S3, Note A-3-S1, Note A-3-S2 and Note A-3-S3, respectively, having an aggregate outstanding principal balance as of the Cut-off Date of $397,530,000 (the “11 Madison Avenue StandalonePari Passu Companion Loans”), each of which is generallypari passu in right of payment with the 11 Madison Avenue Mortgage Loan and the 11 Madison Avenue Non-StandalonePari Passu Companion Loans (as defined below); (iii) sixpari passu promissory notes designated as Note A-1-C1, Note A-1-C3, Note A-2-C1, Note A-2-C2, Note A-3-C1 and Note A-3-C2, respectively, having an aggregate outstanding principal balance as of the Cut-off Date of $296,800,000 (the “11 Madison Avenue Non-StandalonePari Passu Companion Loans” and, together with the 11 Madison Avenue StandalonePari Passu Companion Loans, the “11 Madison AvenuePari Passu Companion Loans”), each of which is generallypari passu in right of payment with the 11 Madison Avenue Mortgage Loan and the 11 Madison Avenue StandalonePari Passu Companion Loans; and (iv) three promissory notes designated as Note B-1-S, Note B-2-S and |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 8 |

COMM 2015-CCRE27 Mortgage Trust

| STRUCTURE OVERVIEW |

| Note B-3-S, respectively, with an aggregate outstanding principal balance as of the Cut-off Date of $310,670,000 (together, the “11 Madison Avenue Subordinate Companion Loans” and, together with the 11 Madison AvenuePari Passu Companion Loans, the “11 Madison Avenue Companion Loans”), which are subordinate in right of payment in respect of each of the 11 Madison Avenue Mortgage Loan and the 11 Madison AvenuePari Passu Companion Loans. The 11 Madison Avenue StandalonePari Passu Companion Loans and the 11 Madison Avenue Subordinate Companion Loans are collectively referred to as the “11 Madison Avenue Standalone Companion Loans”) | ||

| The 11 Madison Avenue Subordinate Companion Loans, together with the 11 Madison Avenue Mortgage Loan and the 11 Madison AvenuePari Passu Companion Loans, are referred to as the “11 Madison Avenue Loan Combination”. Only the 11 Madison Avenue Mortgage Loan is included in the Issuing Entity. Each of the 11 Madison Avenue StandalonePari Passu Companion Loans and 11 Madison Avenue Subordinate Companion Loans has been included in the MAD 2015-11MD Mortgage Trust. The 11 Madison Avenue Non-StandalonePari Passu Companion Loans are currently being held as follows: (i) Note A-1-C1 has been contributed by GACC to the COMM 2015-CCRE26 securitization and Note A-1-C3 is currently being held by GACC, (ii) Note A-2-C1 and Note A-2-C2 are currently being held by Morgan Stanley Bank, N.A. and (iii) Note A-3-C1 and Note A-3-C2 are currently being held by Wells Fargo. | ||

| The 11 Madison Avenue Loan Combination will be serviced pursuant to the MAD 2015-11MD pooling and servicing agreement and the related intercreditor agreement. For additional information regarding the 11 Madison Avenue Loan Combination, see“Description of the Mortgage Pool—Loan Combinations—11 Madison Avenue Loan Combination”in the Free Writing Prospectus. | ||

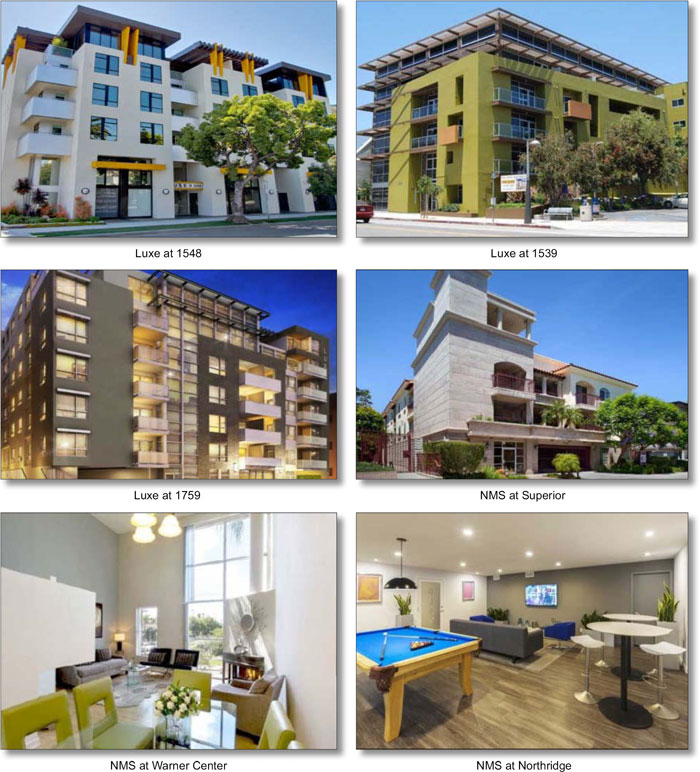

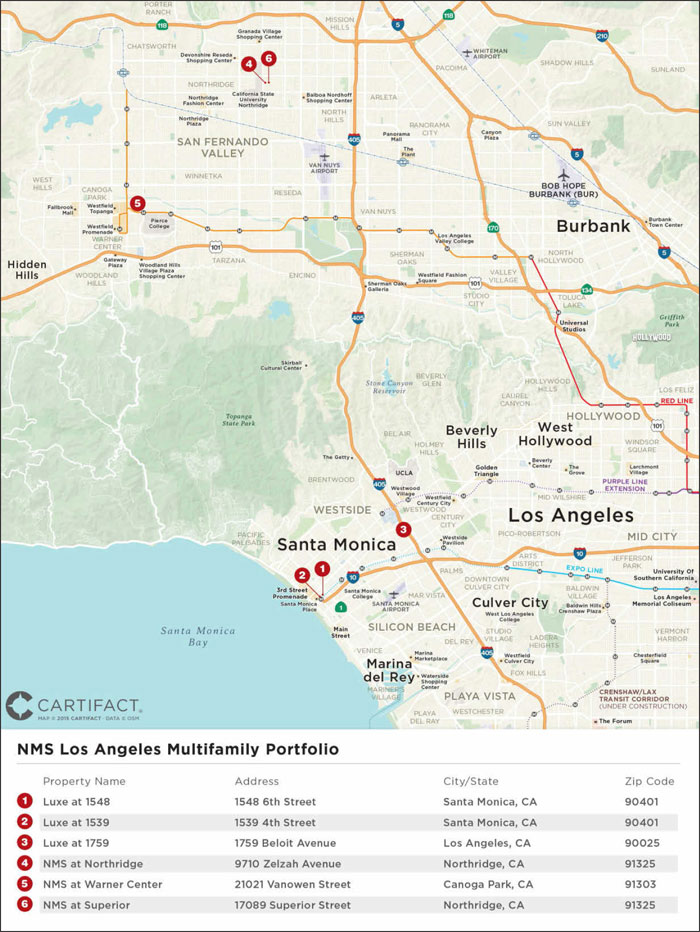

| The portfolio of Mortgaged Properties identified on Annex A–1 to the Free Writing Prospectus as NMS Los Angeles Multifamily Portfolio secures (i) a Mortgage Loan evidenced by a promissory note designated as Note A-1, with an outstanding principal balance as of the Cut–off Date of $65,000,000 (the “NMS Los Angeles Multifamily Portfolio Mortgage Loan”), representing approximately 7.0% of the Initial Outstanding Pool Balance, (ii) a promissory note designated as Note A-2 (the “NMS Los Angeles Multifamily Portfolio Note A-2 Companion Loan”), with an outstanding principal balance as of the Cut-off Date of $30,000,000, which is currently held by CCRE or an affiliate and (iii) a promissory note designated as Note A-3 (together with the NMS Los Angeles Multifamily Portfolio Note A-2 Companion Loan, the “NMS Los Angeles Multifamily Portfolio Companion Loans”), with an outstanding principal balance as of the Cut-off Date of $25,000,000, which is currently held by CCRE or an affiliate. The NMS Los Angeles Multifamily Portfolio Mortgage Loan and the NMS Los Angeles Multifamily Portfolio Companion Loans arepari passu in right of payment and are collectively referred to herein as the “NMS Los Angeles Multifamily Portfolio Loan Combination”. | ||

| The NMS Los Angeles Multifamily Portfolio Loan Combination is being serviced pursuant to the COMM 2015-CCRE27 pooling and servicing agreement and the related intercreditor agreement. For additional information regarding the NMS Los Angeles Multifamily Portfolio Loan Combination, see“Description of the Mortgage Pool—Loan Combinations—NMS Los Angeles Multifamily Portfolio Loan Combination”in the Free Writing Prospectus. | ||

| The 11 Madison Avenue Mortgage Loan is referred to as a “Non-Serviced Mortgage Loan” and the 11 Madison Avenue Loan Combination is referred to as a “Non-Serviced Loan Combination”. The NMS Los Angeles Multifamily Portfolio Loan Combination is referred to as a “Serviced Loan Combination”. | ||

| Control Rights and Directing Holder: | Controlling Class Certificateholders will have certain control rights over servicing matters with respect to each Mortgage Loan (other than Non-Serviced Mortgage Loans) and Serviced Loan Combinations. The majority owner or appointed representative of the Class of Control Eligible Certificates that is the Controlling Class (such owner or representative, the “Directing Holder”), will be entitled to direct the Special Servicer to take, or refrain from taking certain actions with respect to a Mortgage Loan (other than Non-Serviced Mortgage Loans) and Serviced Loan Combinations. Furthermore, the Directing Holder will also have the right to receive notice and consent to certain material actions that the Master Servicer and the Special Servicer proposes to take with respect to such Mortgage Loan (other than Non-Serviced Mortgage Loans) and Serviced Loan Combinations. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 9 |

COMM 2015-CCRE27 Mortgage Trust

| STRUCTURE OVERVIEW |

| It is expected that RREF II CMBS AIV, LP or its affiliate will be the initial Directing Holder with respect to each Mortgage Loan (other than Non-Serviced Mortgage Loans) and Serviced Loan Combination. | ||

| For a description of the directing holder for each Non-Serviced Loan Combination see“Description of the Mortgage Pool—Loan Combinations” and “Description of the Pooling and Servicing Agreement—The Directing Holder”in theFree Writing Prospectus. | ||

| Control Eligible Certificates: | Class E, Class F, Class G and Class H Certificates. | |

| Controlling Class: | The Controlling Class will be the most subordinate Class of Control Eligible Certificates then outstanding that has an aggregate Certificate Balance, as notionally reduced by any Appraisal Reduction Amounts allocable to such Class, equal to no less than 25% of the initial Certificate Balance of such Class. | |

| The Controlling Class as of the Settlement Date will be the Class H Certificates. | ||

| Appraised-Out Class: | Any Class of Control Eligible Certificates that has been determined, as a result of Appraisal Reductions Amounts allocable to such Class, to no longer be the Controlling Class. | |

| Remedies Available to Holders | ||

| of an Appraised-Out Class: | Holders of the majority of any Class of Control Eligible Certificates that is determined at any time of determination to no longer be the Controlling Class as a result of an allocation of an Appraisal Reduction Amounts in respect of such Class will have the right, at their sole expense, to require the Special Servicer to order a second appraisal for any Mortgage Loan (other than Non-Serviced Mortgage Loans) for which an Appraisal Reduction Event has occurred. Upon receipt of the second appraisal, the Special Servicer will be required to determine, in accordance with the Servicing Standard, whether, based on its assessment of the second appraisal, a recalculation of the Appraisal Reduction Amount is warranted. If warranted, the Special Servicer will direct the Master Servicer to recalculate the Appraisal Reduction Amount based on the second appraisal, and if required by such recalculation, the Special Servicer will reinstate the Appraised-Out Class as the Controlling Class. The Holders of an Appraised-Out Class requesting a second appraisal will not be entitled to exercise any rights of the Controlling Class until such time, if any, as the Class is reinstated as the Controlling Class. | |

| Control Termination Event: | Will occur with respect to any Mortgage Loan (other than the Non-Serviced Mortgage Loans) or Serviced Loan Combination when no Class of Control Eligible Certificates has an aggregate Certificate Balance (as notionally or actually reduced by any Appraisal Reduction Amounts and Realized Losses) equal to or greater than 25% of the initial Certificate Balance of such Class. | |

| Upon the occurrence and the continuance of a Control Termination Event, the Directing Holder will no longer have any Control Rights. The Directing Holder will no longer have the right to direct certain actions of the Special Servicer and will no longer have consent rights with respect to certain material actions that the Master Servicer or Special Servicer proposes to take with respect to a Mortgage Loan. | ||

| Upon the occurrence and continuation of a Control Termination Event, the Directing Holder will retain non-binding consultation rights with respect to certain material actions that the Special Servicer proposes to take with respect to a Mortgage Loan (other than Non-Serviced Mortgage Loans) and Serviced Loan Combinations. Such consultation rights will continue until the occurrence of a Consultation Termination Event. | ||

| Consultation Termination Event: | Will occur with respect to any Mortgage Loan (other than Non-Serviced Mortgage Loans) and Serviced Loan Combinations when, without giving regard to the application of any Appraisal Reduction Amounts (i.e., giving effect to principal reduction through Realized Losses only), there is no Class of Control Eligible Certificates that has an aggregate Certificate Balance equal to 25% or more of the initial Certificate Balance of such Class. | |

| Upon the occurrence and continuance of a Consultation Termination Event the Directing Holder will have no rights under the Pooling and Servicing Agreement other than those rights that all Certificateholders have. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 10 |

COMM 2015-CCRE27 Mortgage Trust

| STRUCTURE OVERVIEW |

| Appointment and Replacement | ||

| of Special Servicer: | The Directing Holder will appoint the initial Special Servicer with respect to each Mortgage Loan (other than a Non-Serviced Mortgage Loan) and each Serviced Loan Combination as of the Settlement Date. Prior to the occurrence and continuance of a Control Termination Event, the Directing Holder generally may replace the Special Servicer with respect to each Mortgage Loan (other than a Non-Serviced Mortgage Loan) and each Serviced Loan Combination with or without cause at any time. | |

| Upon the occurrence and during the continuance of a Control Termination Event, the Directing Holder will no longer have the right to replace the Special Servicer and such replacement (other than with respect to the Non-Serviced Loan Combinations) will occur based on a vote of holders of all voting eligible Classes of Certificates as described below. See“Description of the Mortgage Pool—Loan Combinations” and “Description of the Pooling and Servicing Agreement”in theFree Writing Prospectus for a description of the special servicer appointment and replacement rights with respect to Non-Serviced Loan Combinations. | ||

| Replacement of Special Servicer | ||

| by Vote of Certificateholders: | Other than with respect to Non-Serviced Loan Combinations, if a Control Termination Event has occurred and is continuing, upon (i) the written direction of holders of Certificates evidencing not less than 25% of the voting rights of all Classes of Certificates entitled to principal (taking into account the application of Appraisal Reduction Amounts to notionally reduce the Certificate Balances of Classes to which such Appraisal Reduction Amounts are allocable) requesting a vote to replace the Special Servicer with a replacement Special Servicer, (ii) payment by such requesting holders to the Certificate Administrator of all reasonable fees and expenses to be incurred by the Certificate Administrator in connection with administering such vote and (iii) delivery by such holders to the Certificate Administrator of written confirmations from each Rating Agency that the appointment of the replacement Special Servicer will not result in a downgrade of the Certificates, the Certificate Administrator will be required to promptly provide written notice to all certificateholders of such request and conduct the solicitation of votes of all Certificates in such regard. Upon the written direction (within 180 days) of (i) Holders of at least 75% of a Certificateholder Quorum or (ii) the Holders of more than 50% of the voting rights of each Class of Non-Reduced Certificates, the Trustee will immediately replace the Special Servicer with the replacement Special Servicer (other than with respect to Non-Serviced Loan Combinations). | |

| “Certificateholder Quorum” means, in connection with any solicitation of votes in connection with the replacement of the Special Servicer as described above, the holders of Certificates evidencing at least 75% of the aggregate voting rights (taking into account Realized Losses and the application of any Appraisal Reduction Amounts to notionally reduce the Certificate Balance of the Certificates) of all classes of Certificates entitled to principal, on an aggregate basis. | ||

| In addition, after the occurrence of a Consultation Termination Event, if the Operating Advisor determines that the Special Servicer is not performing its duties in accordance with the Servicing Standard, the Operating Advisor will have the right to recommend the replacement of the Special Servicer (other than with respect to Non-Serviced Loan Combinations). The Operating Advisor’s recommendation to replace the Special Servicer (other than with respect Non-Serviced Loan Combinations) must be confirmed by a majority of the voting rights of all Classes of Certificates entitled to principal (taking into account the application of Appraisal Reduction Amounts to notionally reduce the Certificate Balances of Classes to which such Appraisal Reduction Amounts are allocable) within 180 days from the time such recommendation is posted to the Certificate Administrator website and is subject to the receipt of written confirmations from each Rating Agency that the appointment of the replacement Special Servicer will not result in a downgrade of the Certificates. | ||

| See“Description of the Mortgage Pool—Loan Combinations”and “Description of the Poolingand Servicing Agreement”in theFree Writing Prospectus for a description of the special servicer appointment and replacement rights with respect to Non-Serviced Loan Combinations. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 11 |

COMM 2015-CCRE27 Mortgage Trust

| STRUCTURE OVERVIEW |

| Cap on Workout and Liquidation | ||

| Fees: | The workout fees and liquidation fees payable to a Special Servicer under the Pooling and Servicing Agreement will be an amount equal to the lesser of: (1) 1.0% of each collection of interest and principal following a workout or liquidation and (2) $1,000,000 per workout or liquidation. All Modification Fees actually paid to the Special Servicer in connection with a workout or liquidation or in connection with any prior workout or partial liquidation that occurred within the prior 18 months will be deducted from the total workout and/or liquidation fees payable (other than Modification Fees earned while the Mortgage Loan was not in special servicing). In addition, the total amount of workout and liquidation fees actually payable by the Trust under the Pooling and Servicing Agreement will be capped in the aggregate at $1,000,000 for each related Mortgage Loan. If a new special servicer begins servicing the related Mortgage Loan, all amounts paid to the prior special servicer will be disregarded for purposes of calculating the cap. | |

| Special Servicer Compensation: | The special servicing fee will equal 0.25% per annum of the stated principal balance of the related specially serviced loan or REO property, as applicable. The Special Servicer and its affiliates will be prohibited from receiving or retaining any compensation or any other remuneration under the Pooling and Servicing Agreement (including in the form of commissions, brokerage fees, rebates, or as a result of any other fee-sharing arrangement) from any person (including the issuing entity, any borrower, any manager, any guarantor or indemnitor in respect of a Mortgage Loan or Serviced Loan Combination, if any, and any purchaser of any Mortgage Loan, Serviced Companion Loan or REO Property) in connection with the disposition, workout or foreclosure of any Mortgage Loan or Serviced Loan Combination, the management or disposition of any REO Property, or the performance of any other special servicing duties under the Pooling and Servicing Agreement, other than as expressly permitted in the Pooling and Servicing Agreement and other than commercially reasonable treasury management fees, banking fees and insurance commissions or fees received or retained by the Special Servicer or any of its affiliates in connection with any services performed by such party with respect to any mortgage loan. Subject to certain limited exceptions, the Special Servicer will also be required to report any compensation or other remuneration the Special Servicer or its affiliates have received from any person and such information will be disclosed in the Certificateholders’ monthly distribution date statement. | |

| Operating Advisor: | With respect to the Mortgage Loans (other than with respect to Non-Serviced Loan Combinations) and prior to the occurrence of a Control Termination Event, the Operating Advisor will have access to any final asset status report and all information available with respect to the transaction on the Certificate Administrator’s website but will not have any approval or consultation rights. After the occurrence and during the continuance of a Control Termination Event, the Operating Advisor will have consultation rights with respect to certain major decisions and will have additional monitoring responsibilities on behalf of the entire trust. | |

| The Operating Advisor will be subject to termination if holders of at least 15% of the aggregate voting rights of the Certificates (in connection with termination and replacement relating to the Mortgage Loans) vote to terminate and replace the Operating Advisor and such vote is approved by holders of more than 50% of the applicable voting rights that exercise their right to vote, provided that holders of at least 50% of the applicable voting rights have exercised their right to vote. The holders initiating such vote will be responsible for the fees and expenses in connection with the vote and replacement. | ||

| The Operating Advisor will not have consultation rights in respect of Non-Serviced Loan Combinations. | ||

| Liquidated Loan Waterfall: | On liquidation of any Mortgage Loan, all net liquidation proceeds will be applied so that amounts allocated as a recovery of accrued and unpaid interest will not, in the first instance, include any amount by which the interest portion of P&I Advances previously made was reduced as a result of Appraisal Reduction Amounts. After the adjusted interest amount is so allocated, any remaining net liquidation proceeds will be allocated to pay principal on the Mortgage Loan until the unpaid principal amount of the Mortgage Loan has been reduced to zero. Any remaining liquidation proceeds would then be allocated as a recovery of accrued and unpaid interest corresponding to the amount by which the interest portion of P&I Advances previously made was reduced as a result of Appraisal Reduction Amounts. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 12 |

COMM 2015-CCRE27 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Distribution of Cut-off Date Balances(1)(2) |

| Range of Cut-off Date Balances | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Pool | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(3) | U/W NCF DSCR | Cut-off Date LTV Ratio(4)(5) | Maturity Date or ARD LTV(4)(5) | ||||||

| $966,058 | - | $7,499,999 | 28 | $118,293,275 | 12.7% | 4.5902% | 119 | 1.64x | 67.8% | 57.4% |

| $7,500,000 | - | $14,999,999 | 18 | $199,823,491 | 21.4% | 4.6004% | 115 | 1.64x | 68.9% | 60.1% |

| $15,000,000 | - | $24,999,999 | 9 | $168,853,099 | 18.1% | 4.5504% | 114 | 1.71x | 69.7% | 61.0% |

| $25,000,000 | - | $49,999,999 | 7 | $246,734,951 | 26.5% | 4.5244% | 108 | 1.52x | 68.0% | 60.0% |

| $50,000,000 | - | $70,000,000 | 3 | $197,912,576 | 21.2% | 4.2193% | 119 | 2.31x | 54.2% | 50.2% |

| Total/Weighted Average | 65 | $931,617,393 | 100.0% | 4.4889% | 114 | 1.77x | 65.5% | 57.8% | ||

Distribution of Mortgage Rates(1)(2) |

| Range of Mortgage Rates | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(3) | U/W NCF DSCR | Cut-off Date LTV Ratio(4)(5) | Maturity Date or ARD LTV(4)(5) | ||||||

| 3.5602% | - | 4.2499% | 6 | $190,965,889 | 20.5% | 3.9706% | 119 | 2.73x | 50.9% | 45.2% |

| 4.2500% | - | 4.4999% | 15 | $214,798,647 | 23.1% | 4.3536% | 115 | 1.44x | 69.2% | 60.1% |

| 4.5000% | - | 4.7499% | 29 | $299,395,996 | 32.1% | 4.6293% | 119 | 1.66x | 69.2% | 59.2% |

| 4.7500% | - | 5.1100% | 15 | $226,456,860 | 24.3% | 4.8688% | 103 | 1.39x | 69.5% | 64.4% |

| Total/Weighted Average | 65 | $931,617,393 | 100.0% | 4.4889% | 114 | 1.77x | 65.5% | 57.8% | ||

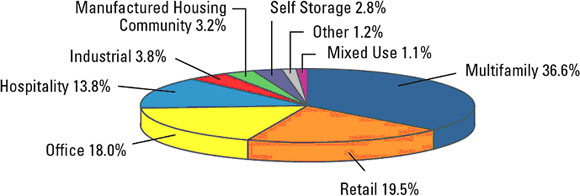

Property Type Distribution(1)(2)(6) |

| Property Type | Number of Mortgaged Properties | Aggregate Date Balance | % of Initial Outstanding Pool Balance | Number of Rooms/ Pads/Units/ NRA/Spaces | Weighted Averages | ||||||

Cut-off Date Unit/NRA/Space | Mortgage Rate | Stated Term | Occupancy | U/W NCF DSCR | Cut-off Ratio(4)(5) | Maturity Date or ARD LTV(4)(5) | |||||

| Multifamily | 29 | $341,141,062 | 36.6% | 5,061 | $138,319 | 4.5950% | 109 | 96.9% | 1.42x | 68.1% | 61.9% |

| Garden | 23 | $224,432,728 | 24.1% | 4,333 | $73,753 | 4.5581% | 103 | 96.1% | 1.49x | 67.3% | 60.2% |

| Mid Rise | 4 | $64,708,333 | 6.9% | 355 | $329,787 | 4.8747% | 119 | 97.6% | 1.30x | 71.4% | 68.2% |

| High Rise | 2 | $52,000,000 | 5.6% | 373 | $178,724 | 4.4062% | 119 | 99.1% | 1.30x | 67.3% | 61.5% |

| Retail | 24 | $181,503,349 | 19.5% | 2,371,940 | $136 | 4.4493% | 119 | 96.0% | 1.52x | 68.3% | 58.0% |

| Anchored(7) | 22 | $161,253,349 | 17.3% | 2,328,842 | $91 | 4.4756% | 119 | 96.1% | 1.50x | 69.0% | 58.2% |

| Unanchored | 2 | $20,250,000 | 2.2% | 43,098 | $496 | 4.2398% | 119 | 94.8% | 1.64x | 62.7% | 56.2% |

| Office | 7 | $167,582,500 | 18.0% | 2,980,966 | $231 | 4.1416% | 119 | 96.3% | 2.56x | 54.0% | 49.2% |

| Suburban | 3 | $87,162,500 | 9.4% | 654,943 | $143 | 4.5307% | 119 | 94.7% | 1.63x | 69.8% | 61.6% |

| CBD | 1 | $70,000,000 | 7.5% | 2,285,043 | $334 | 3.5602% | 119 | 97.8% | 3.89x | 32.5% | 32.5% |

| Medical | 3 | $10,420,000 | 1.1% | 40,980 | $279 | 4.7920% | 119 | 100.0% | 1.41x | 65.7% | 57.7% |

| Hospitality | 14 | $128,579,188 | 13.8% | 1,684 | $126,840 | 4.5320% | 111 | 75.5% | 2.26x | 65.2% | 55.3% |

| Full Service | 3 | $56,924,811 | 6.1% | 467 | $176,805 | 4.5040% | 118 | 77.3% | 2.22x | 64.1% | 52.0% |

| Limited Service | 5 | $37,678,584 | 4.0% | 553 | $76,273 | 4.4790% | 119 | 69.1% | 2.61x | 64.7% | 57.8% |

| Select Service | 1 | $18,475,793 | 2.0% | 117 | $157,913 | 4.5350% | 119 | 85.0% | 1.92x | 64.8% | 52.5% |

| Extended Stay | 5 | $15,500,000 | 1.7% | 547 | $29,220 | 4.7600% | 60 | 73.1% | 1.95x | 70.5% | 64.7% |

| Industrial | 7 | $35,362,500 | 3.8% | 787,462 | $51 | 4.6369% | 119 | 98.8% | 1.38x | 73.2% | 64.4% |

| Manufactured Housing Community | 4 | $30,076,497 | 3.2% | 794 | $39,789 | 4.6637% | 119 | 90.1% | 1.31x | 74.0% | 60.2% |

| Self Storage | 8 | $26,526,010 | 2.8% | 486,075 | $61 | 4.7817% | 119 | 85.3% | 1.49x | 68.8% | 57.8% |

| Parking | 2 | $10,846,286 | 1.2% | 3,189 | $3,544 | 4.7300% | 119 | NAP | 1.99x | 63.2% | 51.6% |

| Mixed Use | 1 | $10,000,000 | 1.1% | 30 | $333,333 | 4.7700% | 120 | 100.0% | 1.50x | 67.6% | 67.6% |

| Total/Weighted Average | 96 | $931,617,393 | 100.0% | 4.4889% | 114 | 93.2% | 1.77x | 65.5% | 57.8% | ||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 13 |

COMM 2015-CCRE27 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Geographic Distribution(1)(2)(6) |

| State/Location | Number of | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||

| Mortgage Rate | Stated | U/W NCF DSCR | Cut-off Date LTV Ratio(4)(5) | Maturity Date or ARD LTV(4)(5) | ||||

| Texas | 12 | $126,118,259 | 13.5% | 4.3827% | 119 | 1.62x | 66.2% | 56.5% |

| Florida | 11 | $115,142,500 | 12.4% | 4.5769% | 119 | 1.69x | 71.4% | 64.0% |

| California | 9 | $92,986,331 | 10.0% | 4.7433% | 119 | 1.39x | 67.2% | 64.7% |

| Southern(8) | 8 | $88,742,134 | 9.5% | 4.7645% | 119 | 1.39x | 66.9% | 65.0% |

| Northern(8) | 1 | $4,244,197 | 0.5% | 4.3000% | 119 | 1.45x | 73.3% | 58.9% |

| New York | 5 | $89,562,262 | 9.6% | 3.8273% | 119 | 3.37x | 39.9% | 37.5% |

| New York City | 1 | $70,000,000 | 7.5% | 3.5602% | 119 | 3.89x | 32.5% | 32.5% |

| Remaining New York State | 4 | $19,562,262 | 2.1% | 4.7829% | 119 | 1.53x | 66.3% | 55.2% |

| Illinois | 8 | $52,493,290 | 5.6% | 4.4503% | 119 | 1.45x | 70.8% | 59.6% |

| Other | 51 | $455,314,751 | 48.9% | 4.5788% | 109 | 1.62x | 68.0% | 59.0% |

| Total/Weighted Average | 96 | $931,617,393 | 100.0% | 4.4889% | 114 | 1.77x | 65.5% | 57.8% |

Distribution of Cut-off Date LTV Ratios(1)(2)(4)(5) |

| Range of Cut-off Date LTV Ratios | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(3) | U/W NCF DSCR | Cut-off Date LTV Ratio | Maturity Date or ARD LTV | ||||||

| 32.5% | - | 54.9% | 2 | $84,280,263 | 9.0% | 3.6754% | 119 | 3.74x | 35.4% | 33.8% |

| 55.0% | - | 59.9% | 4 | $11,865,000 | 1.3% | 4.6124% | 119 | 2.07x | 57.8% | 55.2% |

| 60.0% | - | 64.9% | 15 | $248,471,872 | 26.7% | 4.5023% | 108 | 1.82x | 63.2% | 55.3% |

| 65.0% | - | 69.9% | 17 | $300,503,781 | 32.3% | 4.5511% | 119 | 1.48x | 68.4% | 61.0% |

| 70.0% | - | 74.9% | 20 | $197,577,674 | 21.2% | 4.6262% | 110 | 1.44x | 73.0% | 63.1% |

| 75.0% | - | 77.2% | 7 | $88,918,803 | 9.5% | 4.6913% | 120 | 1.37x | 75.5% | 65.7% |

| Total/Weighted Average | 65 | $931,617,393 | 100.0% | 4.4889% | 114 | 1.77x | 65.5% | 57.8% | ||

Distribution of Maturity Date or ARD LTV Ratios(1)(2)(4)(5) |

| Range of Maturity Date or ARD LTV Ratios | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(3) | U/W NCF DSCR | Cut-off Date LTV Ratio | Maturity Date or ARD LTV | ||||||

| 32.5% | - | 49.9% | 6 | $96,888,859 | 10.4% | 3.8378% | 119 | 3.50x | 38.8% | 35.3% |

| 50.0% | - | 54.9% | 11 | $187,282,616 | 20.1% | 4.4189% | 118 | 1.68x | 64.7% | 52.7% |

| 55.0% | - | 59.9% | 16 | $157,063,898 | 16.9% | 4.4788% | 119 | 1.66x | 67.9% | 57.1% |

| 60.0% | - | 64.9% | 23 | $295,407,020 | 31.7% | 4.5745% | 107 | 1.59x | 69.2% | 62.5% |

| 65.0% | - | 68.8% | 9 | $194,975,000 | 20.9% | 4.7583% | 115 | 1.34x | 72.2% | 67.3% |

| Total/Weighted Average | 65 | $931,617,393 | 100.0% | 4.4889% | 114 | 1.77x | 65.5% | 57.8% | ||

Distribution of Underwritten NCF Debt Service Coverage Ratios(1)(2) |

| Range of Underwritten NCF Debt Service Coverage Ratios | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(3) | U/W NCF DSCR | Cut-off Date LTV Ratio(4)(5) | Maturity Date or ARD LTV(4)(5) | ||||||

| 1.25x | - | 1.39x | 22 | $364,968,134 | 39.2% | 4.6971% | 109 | 1.31x | 70.7% | 64.0% |

| 1.40x | - | 1.44x | 9 | $85,566,360 | 9.2% | 4.5813% | 119 | 1.43x | 71.0% | 60.9% |

| 1.45x | - | 1.54x | 5 | $81,528,105 | 8.8% | 4.3857% | 118 | 1.52x | 68.6% | 59.4% |

| 1.55x | - | 1.99x | 20 | $251,730,775 | 27.0% | 4.4455% | 115 | 1.75x | 66.2% | 55.2% |

| 2.00x | - | 2.49x | 5 | $40,743,755 | 4.4% | 4.7156% | 119 | 2.22x | 63.0% | 57.5% |

| 2.50x | - | 2.99x | 1 | $3,800,000 | 0.4% | 4.5200% | 120 | 2.57x | 55.9% | 55.9% |

| 3.00x | - | 3.89x | 3 | $103,280,263 | 11.1% | 3.7737% | 119 | 3.67x | 40.2% | 38.8% |

| Total/Weighted Average | 65 | $931,617,393 | 100.0% | 4.4889% | 114 | 1.77x | 65.5% | 57.8% | ||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 14 |

COMM 2015-CCRE27 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Original Terms to Maturity or ARD(1)(2)(3) |

| Original Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(4)(5) | Maturity Date or ARD LTV(4)(5) | ||||

| 60 | 3 | $74,750,000 | 8.0% | 4.7138% | 59 | 1.44x | 67.3% | 63.6% |

| 120 | 62 | $856,867,393 | 92.0% | 4.4693% | 119 | 1.79x | 65.4% | 57.3% |

| Total/Weighted Average | 65 | $931,617,393 | 100.0% | 4.4889% | 114 | 1.77x | 65.5% | 57.8% |

Distribution of Remaining Terms to Maturity or ARD(1)(2)(3) |

| Range of Remaining Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(4)(5) | Maturity Date or ARD LTV(4)(5) | ||||||

| 58 | - | 60 | 3 | $74,750,000 | 8.0% | 4.7138% | 59 | 1.44x | 67.3% | 63.6% |

| 117 | - | 120 | 62 | $856,867,393 | 92.0% | 4.4693% | 119 | 1.79x | 65.4% | 57.3% |

| Total/Weighted Average | 65 | $931,617,393 | 100.0% | 4.4889% | 114 | 1.77x | 65.5% | 57.8% | ||

Distribution of Underwritten NOI Debt Yields(1)(2) |

| Range of Underwritten NOI Debt Yields | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(3) | U/W NCF DSCR | Cut-off Date LTV Ratio(4)(5) | Maturity Date or ARD LTV(4)(5) | ||||||

| 6.7% | - | 8.9% | 18 | $313,908,669 | 33.7% | 4.6917% | 108 | 1.31x | 70.1% | 64.3% |

| 9.0% | - | 9.9% | 16 | $158,099,878 | 17.0% | 4.6100% | 119 | 1.41x | 72.1% | 61.7% |

| 10.0% | - | 12.4% | 18 | $255,005,897 | 27.4% | 4.3865% | 119 | 1.69x | 65.7% | 56.1% |

| 12.5% | - | 14.9% | 8 | $154,131,872 | 16.5% | 4.1473% | 113 | 2.82x | 51.1% | 45.3% |

| 15.0% | - | 20.2% | 5 | $50,471,076 | 5.4% | 4.4095% | 119 | 2.88x | 59.6% | 52.0% |

| Total/Weighted Average | 65 | $931,617,393 | 100.0% | 4.4889% | 114 | 1.77x | 65.5% | 57.8% | ||

Amortization Types(1)(2) |

| Amortization Type | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||

| Mortgage Rate | Stated Remaining Term (Mos.)(3) | U/W NCF DSCR | Cut-off Date LTV Ratio(4)(5) | Maturity Date or ARD LTV(4)(5) | ||||

| Interest Only, then Amortizing | 28 | $403,141,300 | 43.3% | 4.5609% | 110 | 1.43x | 70.1% | 62.5% |

| Amortizing Balloon | 27 | $315,682,093 | 33.9% | 4.5053% | 116 | 1.71x | 66.8% | 54.2% |

| Interest Only | 8 | $192,319,000 | 20.6% | 4.3142% | 119 | 2.60x | 53.5% | 53.5% |

| Interest Only, then Amortizing, ARD | 2 | $20,475,000 | 2.2% | 4.4600% | 120 | 1.36x | 69.3% | 60.6% |

| Total/Weighted Average | 65 | $931,617,393 | 100.0% | 4.4889% | 114 | 1.77x | 65.5% | 57.8% |

Footnotes:

| (1) | With respect to the 11 Madison Avenue Mortgage Loan and NMS Los Angeles Multifamily Portfolio Mortgage Loan, LTV, DSCR, Debt Yield, and Cut-off Date Balance per Room/Pad/Unit/NRA/Space calculations include the relatedpari passu companion loan(s), but not any related subordinate companion loan(s). |

| (2) | With respect to the Atlanta Multifamily Portfolio Mortgage Loan, representing approximately 4.8% of the initial outstanding pool balance, following an initial interest only period of 18 months, the mortgage loan amortizes based on a non-standard amortization schedule and the U/W NCF DSCR for such Mortgage Loan was calculated based on the debt service for the first 12 amortizing payments. For additional information, see Annex H to the Free Writing Prospectus. |

| (3) | In the case of two mortgage loans with an anticipated repayment date, Original Terms to Maturity or ARD and Remaining Terms to Maturity or ARD are through the related anticipated repayment date. |

| (4) | With respect to two mortgage loans, representing 6.4% of the initial outstanding principal balance, the Cut-off Date LTV Ratio and Maturity Date or ARD LTV have been calculated based on the “as complete” or “as renovated” value. For additional information, see the Footnotes to Annex A-1 in the Free Writing Prospectus. |

| (5) | With respect to the NMS Los Angeles Multifamily Portfolio Mortgage Loan, Sandalwood Portfolio Mortgage Loan and the Midwest Shopping Center Portfolio Mortgage Loan, collectively representing 17.8% of the initial outstanding pool balance, the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated based on the “as portfolio” appraised value, which attributes a premium to the aggregate value of the mortgaged properties as a whole. For additional information, see the Footnotes to Annex A-1 in the Free Writing Prospectus. |

| (6) | Reflects allocated loan amount for properties securing multi-property mortgage loans. |

| (7) | Anchored retail includes anchored, shadow anchored and single tenant properties. |

| (8) | Northern California properties have a zip code greater than 93600. Southern California properties have a zip code less than or equal to 93600. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 15 |

COMM 2015-CCRE27 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Ten Largest Mortgage Loans |

Mortgage Loan | Mortgage Loan | City, State | Property Type | Cut-off Date Balance | % of Initial Outstanding Pool Balance | Cut-off Date Balance per Room/Pad/Unit/NRA/ Space(1) | Cut-off Date Ratio(1)(2) | U/W NCF DSCR(1)(3) | U/W NOI Debt Yield(1) |

| 11 Madison Avenue | GACC | New York, NY | Office | $70,000,000 | 7.5% | $334 | 32.5% | 3.89x | 14.3% |

| NMS Los Angeles Multifamily Portfolio | CCRE | Various, CA | Multifamily | 65,000,000 | 7.0% | $312,500 | 68.8% | 1.31x | 6.7% |

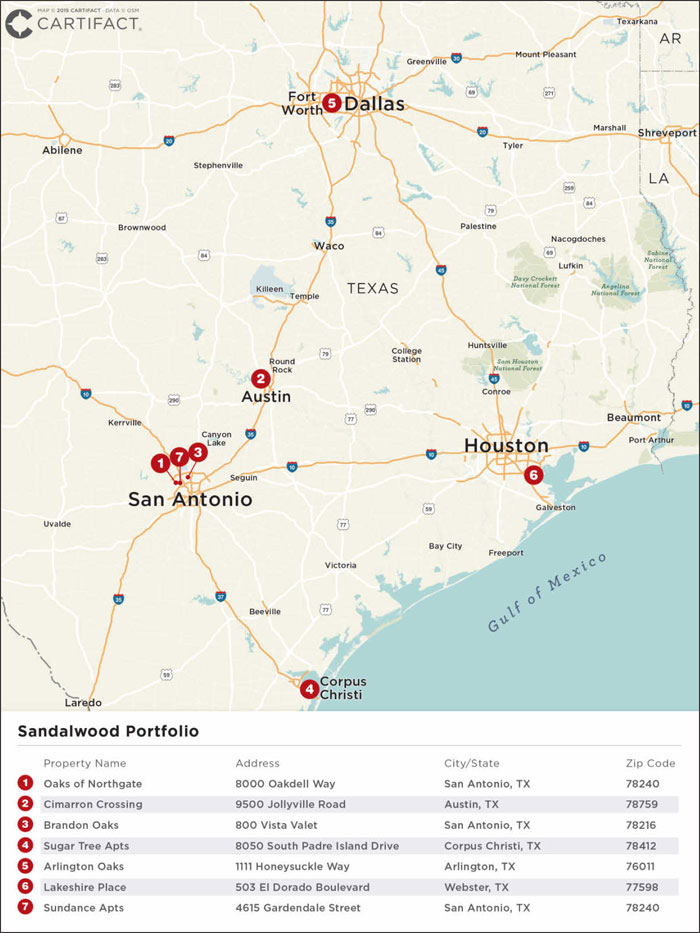

| Sandalwood Portfolio | GACC | Various, TX | Multifamily | 62,912,576 | 6.8% | $38,268 | 63.3% | 1.60x | 10.2% |

| Atlanta Multifamily Portfolio | GACC | Various, GA | Multifamily | 45,000,000 | 4.8% | $76,531 | 64.9% | 1.30x | 8.3% |

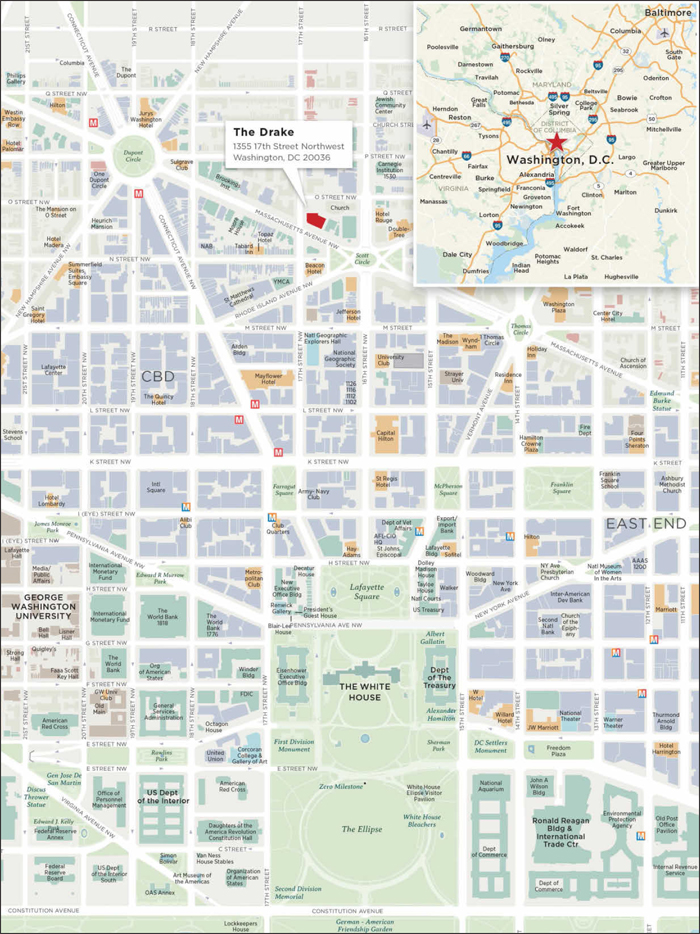

| The Drake | BNYM | Washington, DC | Multifamily | 44,000,000 | 4.7% | $201,835 | 67.4% | 1.28x | 7.7% |

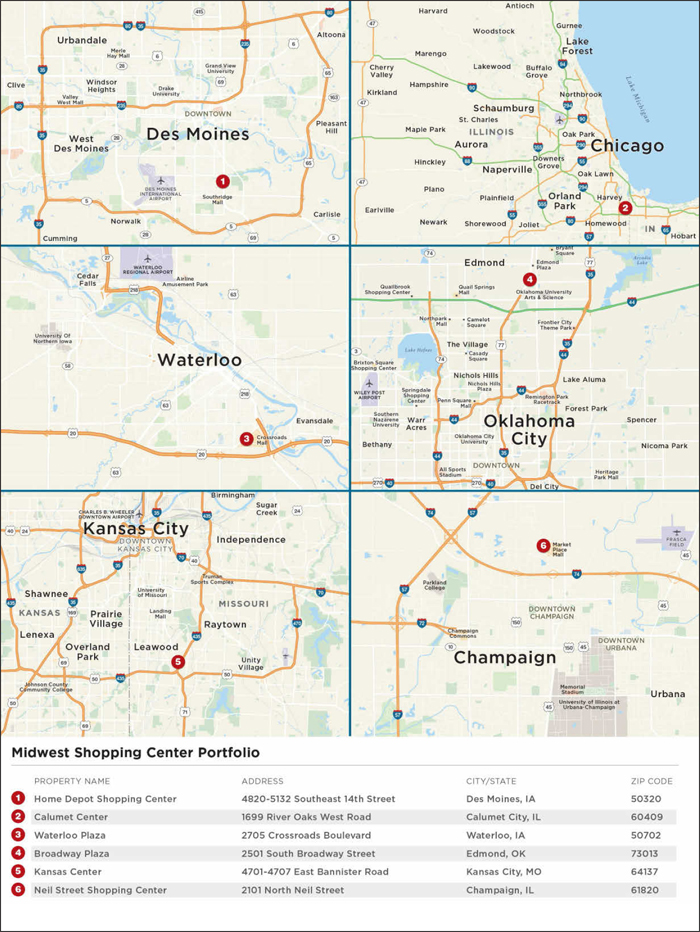

| Midwest Shopping Center Portfolio | GACC | Various, Various | Retail | 38,152,658 | 4.1% | $43 | 67.4% | 1.53x | 10.3% |

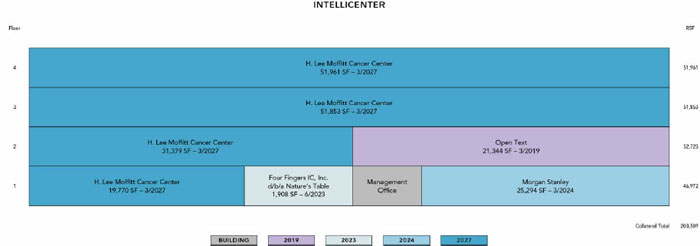

| Intellicenter | KeyBank | Tampa, FL | Office | 33,562,500 | 3.6% | $165 | 75.0% | 1.44x | 9.3% |

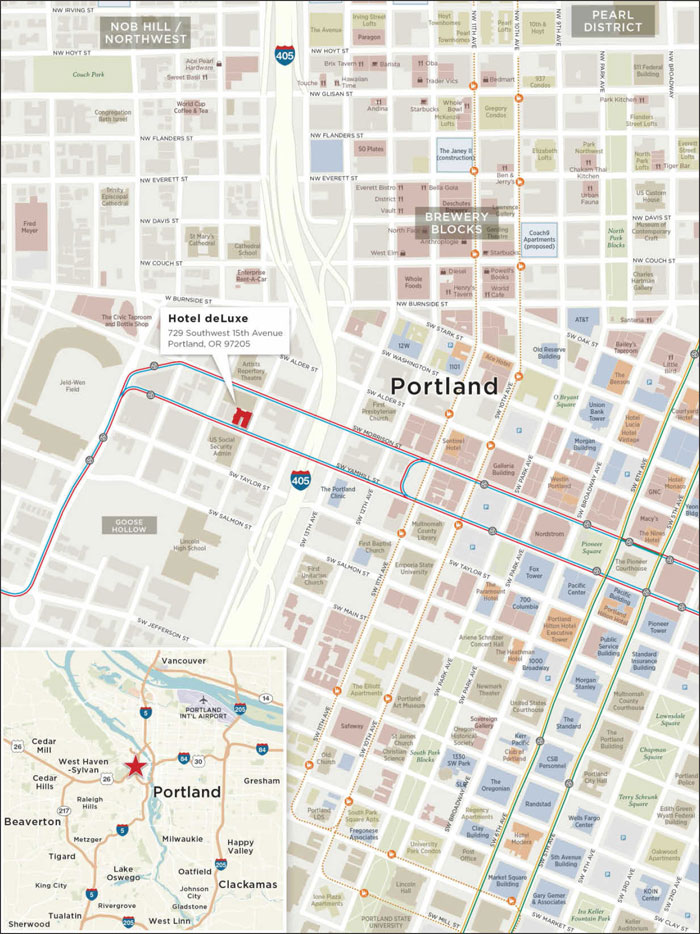

| Hotel deLuxe | BNYM | Portland, OR | Hospitality | 32,419,793 | 3.5% | $249,383 | 68.7% | 1.85x | 12.8% |

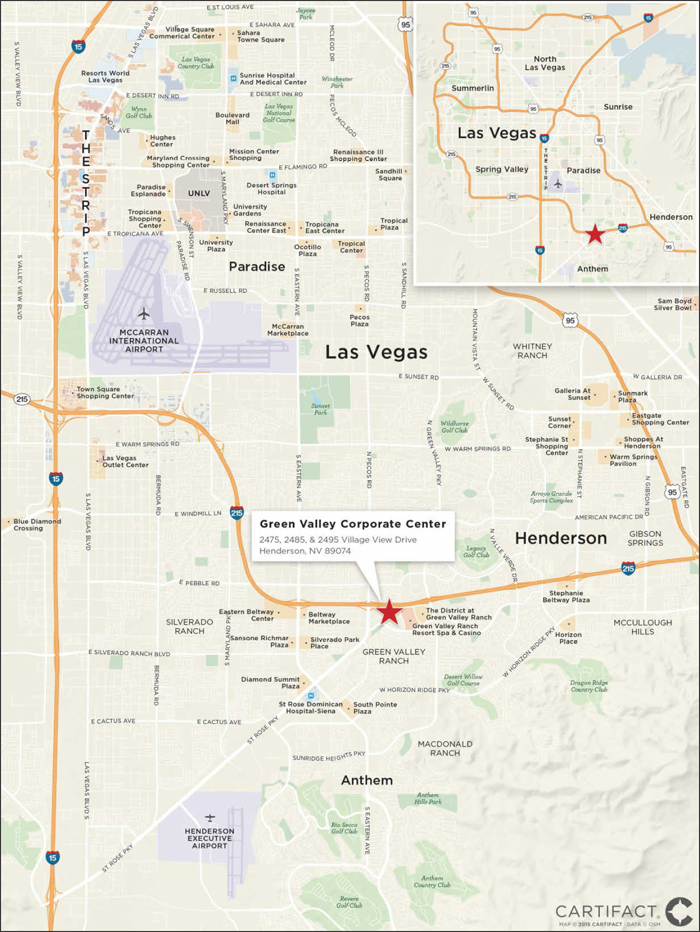

| Green Valley Corporate Center | BNYM | Henderson, NV | Office | 27,000,000 | 2.9% | $166 | 63.9% | 1.96x | 12.4% |

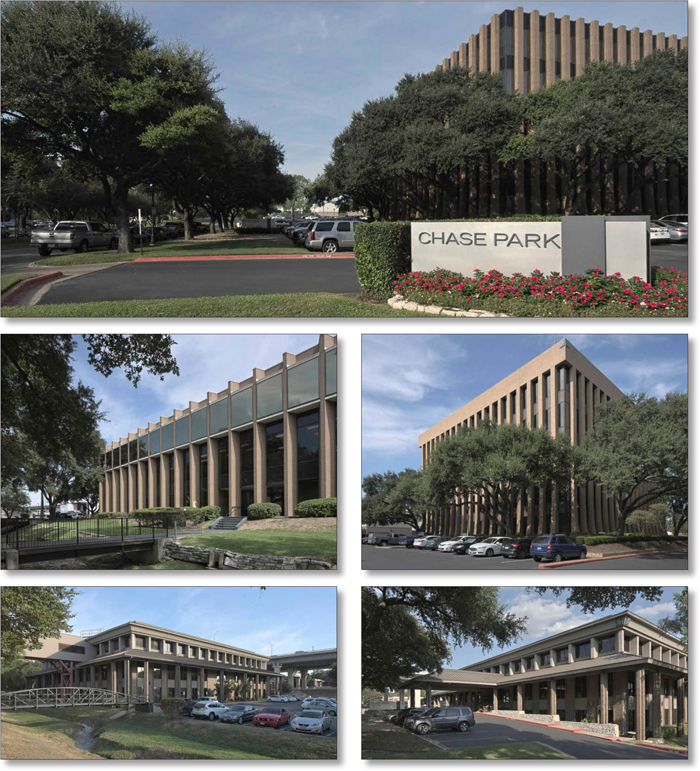

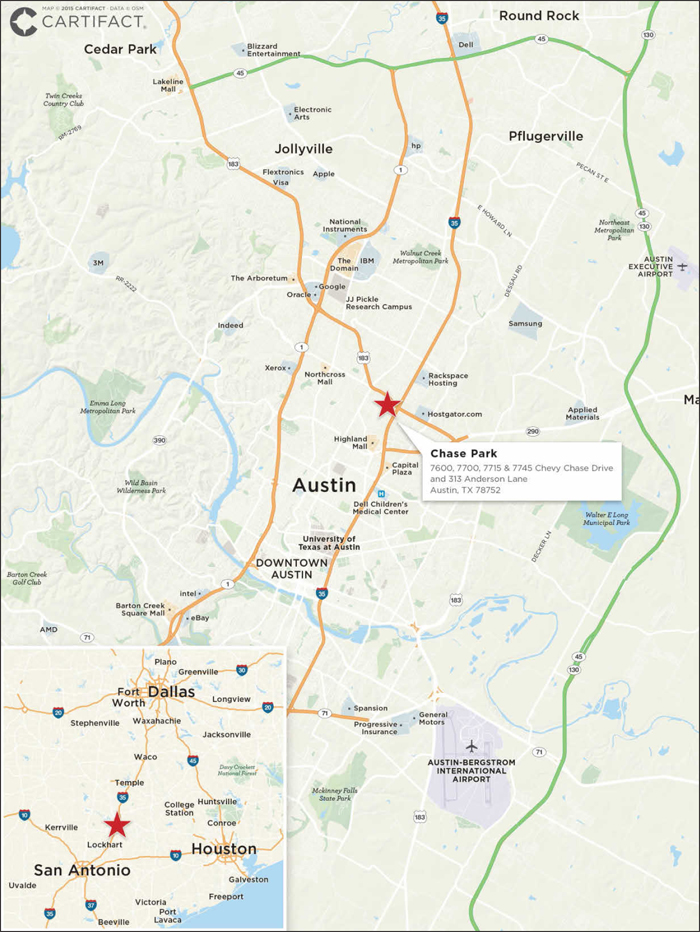

| Chase Park | GACC | Austin, TX | Office | 26,600,000 | 2.9% | $92 | 69.3% | 1.54x | 10.5% |

| Total/Weighted Average | $444,647,528 | 47.7% | 61.8% | 1.87x | 10.2% | ||||

| (1) | With respect to the 11 Madison Avenue Mortgage Loan and the NMS Los Angeles Multifamily Portfolio Mortgage Loan, LTV, DSCR, Debt Yield and Cut-off Date Balance per Room/Pad/Unit/NRA/Space calculations include the relatedpari passu companion loan(s) but not any related subordinate companion loan(s). |

| (2) | With respect to the NMS Multifamily Portfolio Mortgage Loan, Sandalwood Portfolio Mortgage Loan and the Midwest Shopping Center Portfolio Mortgage Loan, the Cut-off Date LTV Ratio has been calculated based on the “as portfolio” appraised value, which attributes a premium to the aggregate value of the mortgaged properties as a whole. With respect to the Atlanta Multifamily Portfolio Mortgage Loan, the Cut-off Date LTV Ratio has been calculated based on the “as renovated” appraised value, which takes into account renovations being performed at the mortgaged properties. |

| (3) | With respect to the Atlanta Multifamily Portfolio Mortgage Loan, representing approximately 4.8% of the initial outstanding pool balance, following an initial interest only period of 18 months, the mortgage loan amortizes based on a non-standard amortization schedule and the U/W NCF DSCR for such Mortgage Loan was calculated based on the debt service for the first 12 amortizing payments. For additional information, see Annex H to the Free Writing Prospectus. |

Pari Passu Companion Loan Summary |

| Mortgage Loan | Mortgage Loan Cut-off Date | Companion Cut-off Date | Loan Combination Cut-off Date Balance |

Pooling & Servicing Agreement | Master Servicer | Special Servicer | Control Rights |

| 11 Madison Avenue(1) | $70,000,000 | $694,330,000 | $764,330,000 | MAD 2015-11MD | KeyBank National Association | KeyBank National Association | NAP |

| NMS Los Angeles Multifamily Portfolio | $65,000,000 | $55,000,000 | $120,000,000 | COMM 2015-CCRE27 | Midland Loan Services | Rialto Capital Advisors, LLC | COMM 2015-CCRE27 |

| (1) | The Loan Combination Cut-off Date Balance excludes three subordinate companion loans in the aggregate original amount of $310.67 million as well as two mezzanine loans in the aggregate original balance of $325.0 million. |

Existing Mezzanine Debt Summary |

| Mortgage Loan | Mortgage Loan Cut-off Date Balance | Mezzanine Debt Cut-off Date Balance | Trust U/W NCF DSCR(1) | Total Debt U/W NCF DSCR(1) | Trust Cut-off Date LTV Ratio(2) | Total Debt Cut-off Date LTV Ratio(2) | Trust U/W NOI Debt Yield | Total Debt U/W NOI Debt Yield |

| 11 Madison Avenue(3)(4) | $70,000,000 | $325,000,000 | 3.89x | 1.97x | 32.5% | 59.6% | 14.3% | 7.8% |

| Atlanta Multifamily Portfolio | $45,000,000 | $5,000,000 | 1.30x | 1.04x | 64.9% | 72.2% | 8.3% | 7.5% |

| Midwest Shopping Center Portfolio | $38,152,658 | $5,500,000 | 1.53x | 1.21x | 67.4% | 77.1% | 10.3% | 9.0% |

| CSRA Food Lion Portfolio II | $6,500,000 | $780,000 | 1.40x | 1.10x | 67.9% | 76.0% | 10.6% | 9.4% |

| (1) | With respect to the Atlanta Multifamily Portfolio Mortgage Loan, representing approximately 4.8% of the initial outstanding pool balance, following an initial interest only period of 18 months, the mortgage loan amortizes based on a non-standard amortization schedule and the U/W NCF DSCR for such Mortgage Loan was calculated based on the debt service for the first 12 amortizing payments. For additional information, see Annex H to the Free Writing Prospectus. |

| (2) | With respect to the Atlanta Multifamily Portfolio Mortgage Loan, the Cut-off Date LTV Ratio has been calculated based on the “as renovated” appraised value, which takes into account renovations being performed at the mortgaged properties. With respect to the Midwest Shopping Center Portfolio Mortgage Loan, the Cut-off Date LTV Ratio has been calculated based on the “as portfolio” appraised value, which attributes a premium to the aggregate value of the mortgaged properties as a whole. |

| (3) | Consists of two mezzanine loans, a $150,000,000 mezzanine A loan, which is coterminous with the 11 Madison Avenue Mortgage Loan, accrues interest at a fixed per annum rate equal to 4.6500% and a $175,000,000 mezzanine B loan, which is coterminous with the 11 Madison Avenue Mortgage Loan, accrues interest at a fixed per annum rate equal to 4.8500%. |

| (4) | The Total Debt U/W NCF DSCR, Total Debt Cut-off Date LTV Ratio and the Total Debt U/W NOI Debt Yield were calculated based on the total debt amount of $1.4 billion, which includes the 11 Madison Avenue Mortgage Loan and 15 seniorpari passu companion loans in the aggregate original amount $694.33 million, three subordinate companion loans in the aggregate original amount of $310.67 million and two mezzanine loans in the aggregate original amount of $325.0 million. |

Subordinate Debt Summary |

| Mortgage Loan | Mortgage Loan Cut-off Date Balance | Pari Passu Companion | Subordinate Debt Cut-off Date Balance | Trust U/W NCF DSCR | Total Debt U/W NCF DSCR | Trust Cut-off Date LTV Ratio | Total Debt Cut-off Date LTV Ratio | Trust U/W NOI Debt Yield | Total Debt U/W NOI Debt Yield |

| 11 Madison Avenue(1) | $70,000,000 | $694,330,000 | $310,670,000 | 3.89x | 1.97x | 32.5% | 59.6% | 14.3% | 7.8% |

| (1) | The Total Debt U/W NCF DSCR, Total Debt Cut-off Date LTV Ratio and the Total Debt U/W NOI Debt Yield were calculated based on the total debt amount of $1.4 billion, which includes the 11 Madison Avenue Mortgage Loan and 15 seniorpari passu companion loans in the aggregate original amount $694.33 million, three subordinate companion loans in the aggregate original amount of $310.67 million and two mezzanine loans in the aggregate original amount of $325.0 million. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 16 |

(THIS PAGE INTENTIONALLY LEFT BLANK)

| 17 |

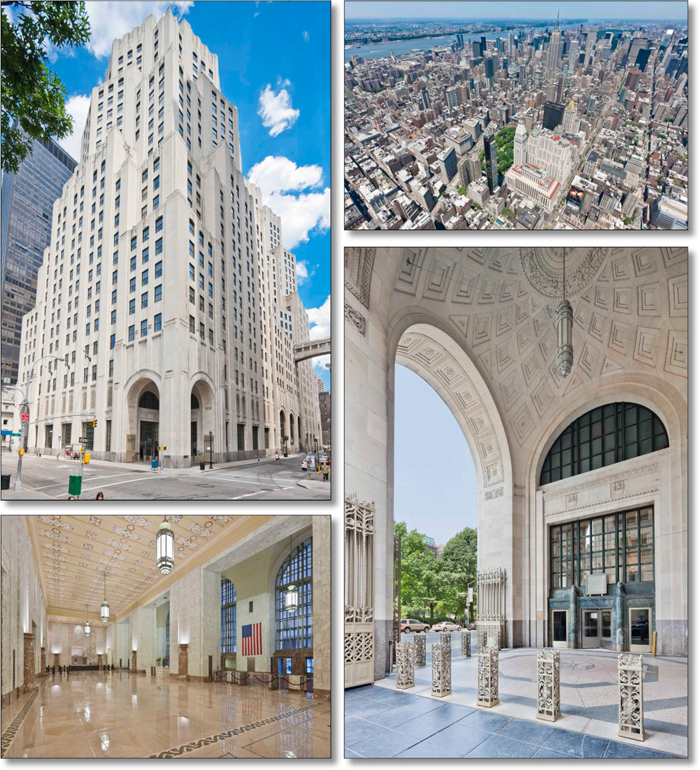

| 11 Madison Avenue New York, NY 10010 | Collateral Asset Summary – Loan No. 1 11 Madison Avenue | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $70,000,000 3.89x 14.3% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 18 |

| 11 Madison Avenue New York, NY 10010 | Collateral Asset Summary – Loan No. 1 11 Madison Avenue | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $70,000,000 3.89x 14.3% |

| Mortgage Loan Information | |

| Loan Seller: | GACC |

| Loan Purpose: | Acquisition |

Credit Assessment (Fitch/DBRS/Moody’s): | AAA/AA(low)/A2 |

| Sponsor: | SL Green Realty Corp. |

| Borrower: | 11 Madison Avenue Owner LLC; 11 Madison Avenue Owner 2 LLC; 11 Madison Avenue Owner 3 LLC; 11 Madison Avenue Owner 4 LLC; 11 Madison Avenue Owner 5 LLC; 11 Madison Avenue Owner 6 LLC; 11 Madison EAT Lender LLC |

| Original Balance(1): | $70,000,000 |

| Cut-off Date Balance(1): | $70,000,000 |

| % by Initial UPB: | 7.5% |

| Interest Rate: | 3.5602% |

| Payment Date: | 6thof each month |

| First Payment Date: | October 6, 2015 |

| Maturity Date: | September 6, 2025 |

| Amortization: | Interest Only |

| Additional Debt(1): | $694,330,000Pari Passu Debt; $310,670,000 Subordinate Secured Debt; $325,000,000 Mezzanine Debt |

| Call Protection(2): | L(25), D(88), O(7) |

| Lockbox / Cash Management: | Hard / Springing |

| Reserves(3) | ||

| Initial | Monthly | |

| Taxes: | $0 | Springing |

| Insurance: | $0 | Springing |

| Replacement: | $0 | Springing |

| TI/LC: | $81,152,102 | Springing |

| Credit Suisse Sublease(4): | $36,500,000 | $0 |

| Sony Free Rent: | $18,847,898 | $0 |

| Endorsement: | $1,000 | $0 |

| Financial Information | ||

| Senior Notes(5) | Total Debt(6) | |

| Cut-off Date Balance / Sq. Ft.: | $334 | $613 |

| Balloon Balance / Sq. Ft.: | $334 | $613 |

| Cut-off Date LTV: | 32.5% | 59.6% |

| Balloon LTV: | 32.5% | 59.6% |

| Underwritten NOI DSCR: | 3.97x | 2.01x |

| Underwritten NCF DSCR: | 3.89x | 1.97x |

| Underwritten NOI Debt Yield: | 14.3% | 7.8% |