| FILED PURSUANT TO RULE 424(h) | ||

| REGISTRATION FILE NO.: 333-207361-07 | ||

The information in this supplement is not complete and may be changed. This supplement is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

The preliminary prospectus to which this is a supplement, dated November 13, 2017,

may be amended or completed prior to time of sale.

SUPPLEMENT

(To Preliminary Prospectus Dated November 13, 2017)

$771,907,000 (Approximate)

CSAIL 2017-CX10 Commercial Mortgage Trust

(Central Index Key Number 0001720474)

as Issuing Entity

Credit Suisse Commercial Mortgage Securities Corp.

(Central Index Key Number 0001654060)

as Depositor

Column Financial, Inc.

(Central Index Key Number 0001628601)

Natixis Real Estate Capital LLC

(Central Index Key Number 0001542256)

BSPRT Finance, LLC

(Central Index Key Number 0001722518)

Benefit Street Partners CRE Finance LLC

(Central Index Key Number 0001632269)

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates, Series 2017-CX10

This is a supplement (“Supplement”) to the prospectus dated November 13, 2017 (the “Preliminary Prospectus”). Capitalized terms used in this supplement but not defined herein have the meanings given to them in the Preliminary Prospectus.

Structural Update

A. Offered Class A-4 and Class A-5 Certificates

| 1. | The Initial Certificate Balance of the Class A-4 Certificates will be decreased to $102,361,000. |

| 2. | The Initial Certificate Balance of the Class A-5 Certificates will be increased to $237,373,000. |

| 3. | The Initial Available Notional Amount of the Class X-A Certificates will be increased to $663,429,000. |

| 4. | The Initial Retained Notional Amount of the Class X-A Certificates will be decreased to $28,294,000. |

| 5. | With respect to the “Offered Certificates”, the relevant portion of the table set forth in “Summary of the Certificates” on page 3 of the Preliminary Prospectus is deleted and replaced with the following: |

| Credit Suisse | NATIXIS |

| Co-Lead Manager and Joint Bookrunner | Co-Lead Manager and Joint Bookrunner |

The date of this Supplement is November 15, 2017

| Class | Approx. Initial Certificate Balance or Notional Amount(1) | Initial Available Certificate Balance or Notional Amount(1) | Initial Retained Certificate Balance or Notional Amount(1)(4) | Approx. Initial Credit Support(2) | Pass-Through Rate Description | Assumed | Initial Approx. Pass-Through Rate | Weighted Average | Expected Principal Window(5) | |||||||||||||||||||||

Offered Certificates | ||||||||||||||||||||||||||||||

| A-1 | $ | 14,888,000 | $ | 14,279,000 | $ | 609,000 | 30.000 | % | (6) | September 2022 | % | 2.71 | 1 – 58 | |||||||||||||||||

| A-2 | $ | 81,680,000 | $ | 78,339,000 | $ | 3,341,000 | 30.000 | % | (6) | October 2022 | % | 4.85 | 58 – 59 | |||||||||||||||||

| A-3 | $ | 143,190,000 | $ | 137,333,000 | $ | 5,857,000 | 30.000 | % | (6) | November 2024 | % | 6.82 | 81 – 84 | |||||||||||||||||

| A-4 | $ | 102,361,000 | $ | 98,174,000 | $ | 4,187,000 | 30.000 | % | (6) | September 2027 | % | 9.46 | 105 – 118 | |||||||||||||||||

| A-5 | $ | 237,373,000 | $ | 227,664,000 | $ | 9,709,000 | 30.000 | % | (6) | November 2027 | % | 9.92 | 118 – 120 | |||||||||||||||||

| A-SB | $ | 19,217,000 | $ | 18,431,000 | $ | 786,000 | 30.000 | % | (6) | August 2026 | % | 6.89 | 59 – 105 | |||||||||||||||||

| X-A | $ | 691,723,000 | (7) | $ | 663,429,000 | (7) | $ | 28,294,000 | (7) | N/A | Variable IO(8) | November 2027 | % | N/A | N/A | |||||||||||||||

| X-B | $ | 80,184,000 | (7) | $ | 76,903,000 | (7) | $ | 3,281,000 | (7) | N/A | Variable IO(8) | November 2027 | % | N/A | N/A | |||||||||||||||

| A-S | $ | 93,014,000 | $ | 89,209,000 | $ | 3,805,000 | 19.125 | % | (6) | November 2027 | % | 9.96 | 120 – 120 | |||||||||||||||||

| B | $ | 49,180,000 | $ | 47,168,000 | $ | 2,012,000 | 13.375 | % | (6) | November 2027 | % | 9.96 | 120 – 120 | |||||||||||||||||

| C | $ | 31,004,000 | $ | 29,735,000 | $ | 1,269,000 | 9.750 | % | (6) | November 2027 | % | 9.96 | 120 – 120 | |||||||||||||||||

| 6. | The table set forth under “Certificate Balances and Notional Amounts” in “Summary of Terms” on page 34 of the Preliminary Prospectus is deleted and replaced with the following: |

Initial Certificate Balance or Notional Amount | Initial Available Certificate Balance or Notional Amount | Initial Retained Certificate Balance or Notional Amount(1) | ||||||||||

| Class A-1 | $ | 14,888,000 | $ | 14,279,000 | $ | 609,000 | ||||||

| Class A-2 | $ | 81,680,000 | $ | 78,339,000 | $ | 3,341,000 | ||||||

| Class A-3 | $ | 143,190,000 | $ | 137,333,000 | $ | 5,857,000 | ||||||

| Class A-4 | $ | 102,361,000 | $ | 98,174,000 | $ | 4,187,000 | ||||||

| Class A-5 | $ | 237,373,000 | $ | 227,664,000 | $ | 9,709,000 | ||||||

| Class A-SB(2) | $ | 19,217,000 | $ | 18,431,000 | $ | 786,000 | ||||||

| Class X-A(3) | $ | 691,723,000 | $ | 663,429,000 | $ | 28,294,000 | ||||||

| Class X-B(3) | $ | 80,184,000 | $ | 76,903,000 | $ | 3,281,000 | ||||||

| Class A-S | $ | 93,014,000 | $ | 89,209,000 | $ | 3,805,000 | ||||||

| Class B | $ | 49,180,000 | $ | 47,168,000 | $ | 2,012,000 | ||||||

| Class C | $ | 31,004,000 | $ | 29,735,000 | $ | 1,269,000 | ||||||

| 7. | The tables with respect to the Class A-4 and Class A-5 Certificates set forth in “Yield and Maturity Considerations—Weighted Average Life” on page 463 of the Preliminary Prospectus are deleted and replaced in their entirety with the following: |

2

Percentages of the Initial Certificate Balance of

the Class A-4 Certificates at the Specified CPYs:

Prepayment Assumption | |||||

Distribution Date | 0% CPY | 25% CPY | 50% CPY | 75% CPY | 100% CPY |

| Closing Date | 100% | 100% | 100% | 100% | 100% |

| November 2018 | 100 | 100 | 100 | 100 | 100 |

| November 2019 | 100 | 100 | 100 | 100 | 100 |

| November 2020 | 100 | 100 | 100 | 100 | 100 |

| November 2021 | 100 | 100 | 100 | 100 | 100 |

| November 2022 | 100 | 100 | 100 | 100 | 100 |

| November 2023 | 100 | 100 | 100 | 100 | 100 |

| November 2024 | 100 | 100 | 100 | 100 | 100 |

| November 2025 | 100 | 100 | 100 | 100 | 100 |

| November 2026 | 76 | 76 | 76 | 76 | 76 |

| November 2027 and thereafter | 0 | 0 | 0 | 0 | 0 |

| Weighted Average Life (in years)(1) | 9.46 | 9.39 | 9.32 | 9.28 | 9.13 |

(1) The weighted average life of the Class A-4 certificates is determined by (a) multiplying the amount of each principal distribution on it by the number of years from the date of issuance of the Class A-4 certificates to the related Distribution Date, (b) summing the results and (c) dividing the sum by the aggregate amount of the reductions in the certificate balance of the Class A-4 certificates.

Percentages of the Initial Certificate Balance of

the Class A-5 Certificates at the Specified CPYs:

Prepayment Assumption | |||||

Distribution Date | 0% CPY | 25% CPY | 50% CPY | 75% CPY | 100% CPY |

| Closing Date | 100% | 100% | 100% | 100% | 100% |

| November 2018 | 100 | 100 | 100 | 100 | 100 |

| November 2019 | 100 | 100 | 100 | 100 | 100 |

| November 2020 | 100 | 100 | 100 | 100 | 100 |

| November 2021 | 100 | 100 | 100 | 100 | 100 |

| November 2022 | 100 | 100 | 100 | 100 | 100 |

| November 2023 | 100 | 100 | 100 | 100 | 100 |

| November 2024 | 100 | 100 | 100 | 100 | 100 |

| November 2025 | 100 | 100 | 100 | 100 | 100 |

| November 2026 | 100 | 100 | 100 | 100 | 100 |

| November 2027 and thereafter | 0 | 0 | 0 | 0 | 0 |

| Weighted Average Life (in years)(1) | 9.92 | 9.89 | 9.84 | 9.76 | 9.47 |

(1) The weighted average life of the Class A-5 certificates is determined by (a) multiplying the amount of each principal distribution on it by the number of years from the date of issuance of the Class A-5 certificates to the related Distribution Date, (b) summing the results and (c) dividing the sum by the aggregate amount of the reductions in the certificate balance of the Class A-5 certificates.

B. NOn-Offered loan-specific Certificates

| 1. | The initial Certificate Balance of the Class UES-A Certificates will be increased to $89,010,000. |

| 2. | The initial Certificate Balance of the Class UES-B Certificates will be decreased to $31,060,000. |

| 3. | The initial Certificate Balance of the Class UES-C Certificates will be increased to $36,840,000. |

| 4. | The initial Certificate Balance of the Class UES-D Certificates will be increased to $43,090,000. |

| 5. | No Class UES-E Certificates will be issued. |

| 6. | With respect to the “Non-Offered Loan-Specific Certificates” the portion of the table relating to the Y&L Towers Trust Subordinate Companion Loan set forth in “Summary of the Certificates” in the Preliminary Prospectus is deleted and replaced with the following: |

3

Non-Offered Loan-Specific Certificates | ||||||||||||||||||||||||||||||||||||

| UES-A(12) | $ | 89,010,000 | $ | 84,559,500 | $ | 4,450,500 | 55.495 | % | (6) | October 2022 | % | 4.88 | 59 – 59 | |||||||||||||||||||||||

| UES-B(12) | $ | 31,060,000 | $ | 29,507,000 | $ | 1,553,000 | 39.965 | % | (6) | October 2022 | % | 4.88 | 59 – 59 | |||||||||||||||||||||||

| UES-C(12) | $ | 36,840,000 | $ | 34,998,000 | $ | 1,842,000 | 21.545 | % | (6) | October 2022 | % | 4.88 | 59 – 59 | |||||||||||||||||||||||

| UES-D(12) | $ | 43,090,000 | $ | 40,935,500 | $ | 2,154,500 | 0.000 | % | (6) | October 2022 | % | 4.88 | 59 – 59 | |||||||||||||||||||||||

| UES-X(12) | $ | 156,910,000 | (7) | $ | 149,064,500 | (7) | $ | 7,845,500 | (7) | N/A | Variable IO(8) | October 2022 | % | N/A | N/A | |||||||||||||||||||||

Collateral UPDATE

A. Benefit Street Partners CRE Finance LLC and BSPRT Finance, LLC

| 1. | The Preliminary Prospectus is updated to include BSPRT Finance, LLC as a sponsor and a mortgage loan seller. |

| 2. | The tables set forth on pages 21 and 141 of the Preliminary Prospectus under the headings “Relevant Parties” in “Summary of Terms” and “Description of the Mortgage Pool—General”, respectively, are deleted and replaced with the following: |

Sellers of the Mortgage Loans

| Seller | Number of Mortgage Loans | Aggregate Cut-Off Date Balance of Mortgage Loans | Approx.% of Initial Pool Balance | |||

| Column Financial, Inc.(1) | 8 | $387,452,843 | 45.3% | |||

| Natixis Real Estate Capital LLC(2) | 13 | 310,942,664 | 36.4 | |||

| BSPRT Finance, LLC(3) | 9 | 127,570,000 | 14.9 | |||

| Benefit Street Partners CRE Finance LLC | 1 | 29,333,985 | 3.4 | |||

| Total | 31 | $855,299,491 | 100.0% |

| (1) | One (1) of the Column Financial, Inc. Mortgage Loans identified on Annex A-1 as GNL Portfolio, was co-originated with Citi Real Estate Funding Inc. In addition, one (1) of the Column Financial, Inc. Mortgage Loans identified on Annex A-1 as Lehigh Valley Mall, was co-originated with JPMorgan Chase Bank, National Association and Cantor Commercial Real Estate Lending, L.P. |

| (2) | One (1) Natixis Real Estate Capital LLC Mortgage Loan identified on Annex A-1 as Yorkshire & Lexington Towers, was co-originated with UBS AG. |

| (3) | One (1) of the BSPRT Finance, LLC mortgage loans identified on Annex A-1 as Miracle Mile, was co-originated with JPMorgan Chase Bank, National Association. |

With respect to the Mortgage Loans identified in the Preliminary Prospectus as being sold to the Depositor by Benefit Street Partners CRE Finance LLC, (a) one (1) such Mortgage Loan secured by the portfolio of Mortgaged Properties identified on Annex A-1 as Garden Multifamily Portfolio, representing approximately 3.4% of the Initial Pool Balance, will be contributed to the pool of Mortgage Loans by Benefit Street Partners CRE Finance LLC, and (b) nine (9) such Mortgage Loans secured by the Mortgaged Property or portfolio of Mortgaged Properties identified on Annex A-1 as Miracle Mile, Rockside Office Portfolio, 701 East 22nd Street, Mt. Washington Mill, Goldstar Industrial Portfolio, Meadows at June Road, Lakefront I & II, SeaMist RV Park and Southern Woods, representing approximately 14.9% of the Initial Pool Balance, will be contributed to the pool of Mortgage Loans by BSPRT Finance, LLC. Benefit Street Partners CRE Finance LLC and BSPRT Finance, LLC are affiliates.

| 3. | Additionally, the following is inserted on page 245 of the Preliminary Prospectus in the section “Transaction Parties—The Originators and Mortgage Loan Sellers” immediately prior to the heading “Benefit Street Partners CRE Finance LLC”: |

4

BSPRT Finance, LLC

General

BSPRT Finance, LLC (“BSPRT”), is a sponsor of, and a seller of certain mortgage loans (the “BSPRT Mortgage Loans”) into, the securitization described in this prospectus. BSPRT is a limited liability company organized under the laws of the State of Delaware. The primary offices of BSPRT are located at 142 West 57th Street, Suite 1201, New York, New York 10019.

BSPRT’s Loan Origination and Acquisition History

The participation by BSPRT in this securitization will be the first securitization in which it has been involved. BSPRT began originating and acquiring loans in 2017 and has not been involved in the securitization of any other types of financial assets.

BSPRT originates and acquires from unaffiliated third party originators, commercial mortgage loans throughout the United States. The following tables set forth information with respect to originations and acquisitions of fixed rate commercial mortgage loans by BSPRT as of October 31, 2017.

Originations and Acquisitions of Fixed Rate Commercial Mortgage Loans

October 31, 2017 | ||

No. of | Approximate Aggregate | |

| Originations/Acquisitions | 9 | $127,770,000 |

In connection with this commercial mortgage securitization transaction, BSPRT will transfer the BSPRT Mortgage Loans to the depositor, who will then transfer the BSPRT Mortgage Loans to the issuing entity for this securitization. In return for the transfer by the depositor to the issuing entity of the BSPRT Mortgage Loans (together with the other mortgage loans being securitized), the issuing entity will issue commercial mortgage pass-through certificates that are, in whole or in part, backed by, and supported by the cash flows generated by, the mortgage loans being securitized. In coordination with the underwriter or the initial purchaser and the depositor, BSPRT will work with rating agencies, the other loan sellers, servicers and investors and will participate in structuring the securitization transaction to maximize the overall value and capital structure, taking into account numerous factors, including without limitation geographic and property type diversity and rating agency criteria.

Pursuant to a MLPA, BSPRT will make certain representations and warranties, subject to certain exceptions set forth therein, and undertake certain loan document delivery requirements with respect to the BSPRT Mortgage Loans; and, in the event of an uncured material breach of any such representation and warranty or an uncured material document defect or omission, BSPRT will generally be obligated to repurchase or replace the affected mortgage loan or, in some cases, pay an amount estimated to cover the approximate loss associated with such breach, defect or omission. We cannot assure you that BSPRT will repurchase or replace, or make an estimated loss reimbursement payment with respect to, a defective mortgage loan, and no affiliate of BSPRT will be responsible for doing so if BSPRT fails with respect to its obligations.

BSPRT does not act as a servicer of the commercial, multifamily and manufactured housing community mortgage loans that BSPRT originates or acquires and will not act as servicer in this commercial mortgage securitization transaction. Instead, BSPRT sells the right to be appointed servicer of its securitized loans to unaffiliated third party servicers and utilizes unaffiliated third party servicers as interim servicers.

5

Review of BSPRT Mortgage Loans

Overview. BSPRT has conducted a review of the BSPRT Mortgage Loans in connection with the securitization described in this prospectus. The review of the BSPRT Mortgage Loans was performed by a team comprised of real estate and securitization professionals (the “BSPRT Review Team”). The review procedures described below were employed with respect to all of the BSPRT Mortgage Loans, except that certain review procedures may only be relevant to the large loan disclosures, if any, in this prospectus. No sampling procedures were used in the review process.

Database. Members of the BSPRT Review Team maintain a database of loan-level and property-level information, and prepared an asset summary report, relating to each BSPRT Mortgage Loan. The database and the respective asset summary reports were compiled from, among other sources, the related Mortgage Loan documents, appraisals, environmental assessment reports, property condition reports, seismic studies, zoning reports, insurance review summaries, borrower-supplied information (including, but not limited to, rent rolls, leases, operating statements and budgets) and information collected by the BSPRT Team during the underwriting process. The BSPRT Review Team periodically updated the information in the database and the related asset summary report with respect to such BSPRT Mortgage Loan based on updates provided by the related servicer relating to loan payment status and escrows, updated operating statements, rent rolls and leasing activity, and information otherwise brought to the attention of the BSPRT Review Team.

A data tape (the “BSPRT Data Tape”) containing detailed information regarding each BSPRT Mortgage Loan was created from the information in the database referred to in the prior paragraph. The BSPRT Data Tape was used to provide the numerical information regarding the BSPRT Mortgage Loans in this prospectus.

Data Validation and Recalculation. BSPRT engaged a third party accounting firm to perform certain data validation and recalculation procedures designed by BSPRT, relating to information in this prospectus regarding the BSPRT Mortgage Loans. These procedures included:

| ● | comparing the information in the BSPRT Data Tape against various source documents provided by BSPRT that are described under “—Review of BSPRT Mortgage Loans—Database” above; |

| ● | comparing numerical information regarding the BSPRT Mortgage Loans and the related Mortgaged Properties disclosed in this prospectus against the BSPRT Data Tape; and |

| ● | recalculating certain percentages, ratios and other formulae relating to the BSPRT Mortgage Loans disclosed in this prospectus. |

Legal Review. BSPRT engaged various law firms to conduct certain legal reviews of the BSPRT Mortgage Loans for disclosure in this prospectus. In anticipation of the securitization of each BSPRT Mortgage Loan, BSPRT’s origination counsel prepared a due diligence questionnaire that sets forth salient loan terms. In addition, such origination counsel for each BSPRT Mortgage Loan reviewed BSPRT’s representations and warranties set forth on Annex D-1 and, if applicable, identified exceptions to those representations and warranties.

Legal counsel was also engaged in connection with this securitization to assist in the review of the BSPRT Mortgage Loans. Such assistance included, among other things, (i) a review of BSPRT’s asset summary report and its origination counsel’s due diligence questionnaire for each BSPRT Mortgage Loan, (ii) a review of the representations and warranties and exception reports referred to above relating to the BSPRT Mortgage Loans prepared by origination counsel, and (iii) the review of select provisions in certain loan documents with respect to certain of the BSPRT Mortgage Loans.

Other Review Procedures. With respect to any material pending litigation on the underlying Mortgaged Properties of which BSPRT was aware at the origination of any BSPRT Mortgage Loan, the BSPRT Review Team requested updates from the related borrower, origination counsel and/or borrower’s

6

litigation counsel. BSPRT conducted a search with respect to each borrower under the related BSPRT Mortgage Loan to determine whether it filed for bankruptcy. If the BSPRT Review Team became aware of a significant natural disaster in the vicinity of the Mortgaged Property securing any BSPRT Mortgage Loan, the BSPRT Review Team obtained information on the status of the Mortgaged Property from the related borrower to confirm no material damage to the Mortgaged Property.

The BSPRT Review Team, with the assistance of applicable origination counsel, also reviewed the BSPRT Mortgage Loans to determine whether any BSPRT Mortgage Loan materially deviated from the underwriting guidelines set forth under “—BSPRT’s Underwriting Standards” below. See “—BSPRT’s Underwriting Standards—Exceptions” below.

Findings and Conclusions. Based on the foregoing review procedures, the BSPRT Review Team determined that the disclosure regarding the BSPRT Mortgage Loans in this prospectus is accurate in all material respects. The BSPRT Review Team also determined that the BSPRT Mortgage Loans were originated in accordance with BSPRT’s origination procedures and underwriting criteria, except as described under “—BSPRT’s Underwriting Standards—Exceptions” below. BSPRT attributes to itself all findings and conclusions resulting from the foregoing review procedures.

Review Procedures in the Event of a Mortgage Loan Substitution. BSPRT will perform a review of any mortgage loan that it elects to substitute for a Mortgage Loan in the pool in connection with a material breach of a representation or warranty or a material document defect. BSPRT, and, if appropriate, its legal counsel, will review the mortgage loan documents and servicing history of the substitute mortgage loan to confirm it satisfies each of the criteria required under the terms of the related MLPA and the PSA (collectively, the “Qualification Criteria”). BSPRT will engage a third party accounting firm to compare the Qualification Criteria against the underlying source documentation to verify the accuracy of the review by BSPRT and to confirm any numerical and/or statistical information to be disclosed in any required filings under the Exchange Act. Legal counsel will also be engaged by BSPRT to render any tax opinion required in connection with the substitution.

BSPRT’s Underwriting Standards

Each of the BSPRT Mortgage Loans was originated or acquired by BSPRT. Set forth below is a discussion of certain general underwriting guidelines and processes with respect to commercial, multifamily and manufactured housing community mortgage loans originated or acquired by BSPRT.

Notwithstanding the discussion below, given the unique nature of commercial, multifamily and manufactured housing community mortgaged properties, the underwriting and origination procedures and the credit analysis with respect to any particular commercial, multifamily or manufactured housing community mortgage loan may significantly differ from one asset to another, and will be driven by circumstances particular to that property, including, among others, its type, current use, size, location, market conditions, reserve requirements and additional collateral, tenants and leases, borrower identity, sponsorship, performance history and/or other factors. Consequently, we cannot assure you that the underwriting of any particular commercial, multifamily or manufactured housing community mortgage loan originated or acquired by BSPRT will conform to the general guidelines and processes described below. For important information about the circumstances that have affected the underwriting of particular BSPRT Mortgage Loans, see “—BSPRT’s Underwriting Standards—Exceptions” below and “Annex D-2—Exceptions to Mortgage Loan Representations and Warranties”.

Loan Analysis. Generally both a credit analysis and a collateral analysis are conducted with respect to each commercial, multifamily and manufactured housing community mortgage loan. The credit analysis of the borrower generally includes a review of third party credit reports and/or judgment, lien, bankruptcy and pending litigation searches. The collateral analysis generally includes a review of, in each case to the extent available and applicable, the historical property operating statements, rent rolls and certain significant tenant leases. The credit underwriting also generally includes a review of third party appraisals, as well as environmental reports, engineering assessments and seismic reports, if applicable and obtained. Generally, BSPRT also conducts or causes a third party to conduct a site inspection to ascertain the overall quality, functionality and competitiveness of the property, including its

7

neighborhood and market, accessibility and visibility, and to assess the tenancy of the property. The submarket in which the property is located is assessed to evaluate competitive or comparable properties as well as market trends.

Loan Approval. Prior to commitment, each commercial, multifamily and manufactured housing community mortgage loan to be originated or acquired must be approved by a loan committee that includes senior personnel from BSPRT. The committee may approve a mortgage loan as recommended, request additional due diligence, modify the loan terms or decline a loan transaction.

Debt Service Coverage Ratio and Loan-to-Value Ratio. The underwriting includes a calculation of the debt service coverage ratio and loan-to-value ratio. BSPRT’s underwriting standards generally require, without regard to any other debt, a debt service coverage ratio of not less than 1.20x and a loan-to-value ratio of not more than 75.0%.

A debt service coverage ratio will generally be calculated based on the underwritten net cash flow from the property in question as determined by BSPRT and payments on the loan based on actual (or, in some cases, assumed) principal and/or interest due on the loan. However, underwritten net cash flow is often a highly subjective number based on a variety of assumptions regarding, and adjustments to, revenues and expenses with respect to the related real property collateral. For example, when calculating the debt service coverage ratio for a commercial, multifamily or manufactured housing community mortgage loan, annual net cash flow that was calculated based on assumptions regarding projected future rental income, expenses and/or occupancy may be utilized. There is no assurance that the foregoing assumptions made with respect to any prospective commercial, multifamily or manufactured housing community mortgage loan will, in fact, be consistent with actual property performance. Such underwritten net cash flow may be higher than historical net cash flow reflected in recent financial statements. Additionally, certain mortgage loans may provide for only interest payments prior to maturity, or for an interest-only period during a portion of the term of the mortgage loan.

A loan-to-value ratio, in general, is the ratio, expressed as a percentage, of the then-outstanding principal balance of the mortgage loan divided by the estimated value of the related property based on an appraisal.

Additional Debt. Certain mortgage loans may have or permit in the future certain subordinate debt, whether secured or unsecured, and/or mezzanine debt. It is possible that BSPRT or an affiliate may be the lender on that subordinate debt and/or mezzanine debt.

The debt service coverage ratios described above will be lower based on the inclusion of the payments related to such additional debt and the loan-to-value ratios described above will be higher based on the inclusion of the amount of any such subordinate debt and/or mezzanine debt.

Assessments of Property Condition. As part of the underwriting process, the property assessments and reports described below will typically be obtained:

| ● | Appraisals. Independent appraisals or an update of an independent appraisal will generally be required in connection with the origination or acquisition of each mortgage loan that meets the requirements of the “Uniform Standards of Professional Appraisal Practice” as adopted by the Appraisal Standards Board of the Appraisal Foundation, or the guidelines in Title XI of the Financial Institutions Reform, Recovery and Enforcement Act of 1989. In some cases, however, the value of the subject real property collateral may be established based on a cash flow analysis, a recent sales price or another method or benchmark of valuation. |

| ● | Environmental Assessment. In most cases, a Phase I environmental assessment will be required with respect to the real property collateral for a prospective commercial, multifamily or manufactured housing community mortgage loan. However, when circumstances warrant, an update of a prior environmental assessment, a transaction screen or a desktop review may be utilized. Alternatively, in limited circumstances, an environmental assessment may not be required, such as when the benefits of an environmental insurance policy or an environmental |

8

| guarantee have been obtained. It should be noted that an environmental assessment conducted at any particular real property collateral will not necessarily cover all potential environmental issues. For example, an analysis for radon, lead-based paint, mold and lead in drinking water will usually be conducted only at multifamily rental properties and only if it is believed that such an analysis is warranted under the circumstances. Depending on the findings of the initial environmental assessment, any of the following may be required: additional environmental testing, such as a Phase II environmental assessment with respect to the subject real property collateral; an environmental insurance policy; that the borrower conduct remediation activities or establish an operations and maintenance plan; and/or a guaranty or reserve with respect to environmental matters. |

| ● | Engineering Assessment. In connection with the origination/acquisition process, in most cases, it will be required that an engineering firm inspect the real property collateral for any prospective commercial, multifamily or manufactured housing community mortgage loan to assess the structure, exterior walls, roofing, interior structure and/or mechanical and electrical systems. Based on the resulting report, the appropriate response will be determined to any recommended repairs, corrections or replacements and any identified deferred maintenance. |

| ● | Seismic Report. Generally, a seismic report is required for all properties located in seismic zones 3 or 4. |

Title Insurance. The borrower is required to provide a title insurance policy for each property. The title insurance policies provided typically must meet the following requirements: (i) written by a title insurer licensed to do business in the jurisdiction where the mortgaged property is located, (ii) in an amount at least equal to the original principal balance of the mortgage loan, (iii) protection and benefits run to the mortgagee and its successors and assigns, (iv) written on an American Land Title Association form or equivalent policy promulgated in the jurisdiction where the mortgaged property is located and (v) if a survey was prepared, the legal description of the mortgaged property in the title policy conforms to that shown on the survey.

Casualty Insurance. Except in certain instances where sole or significant tenants (which may include ground tenants) are required to obtain insurance or may self-insure, BSPRT typically requires that the related mortgaged property be insured by a hazard insurance policy with a customary deductible and in an amount at least equal to the lesser of the outstanding principal balance of the mortgage loan and 100% of the full insurable replacement cost of the improvements located on the property. If applicable, the policy must contain appropriate endorsements to avoid the application of coinsurance and not permit reduction in insurance proceeds for depreciation, except that the policy may permit a deduction for depreciation in connection with a cash settlement after a casualty if the insurance proceeds are not being applied to rebuild or repair the damaged improvements.

Flood insurance, if available, must be in effect for any mortgaged property that at the time of origination or acquisition included material improvements in any area identified in the Federal Register by the Federal Emergency Management Agency a special flood hazard area. The flood insurance policy must meet the requirements of the then-current guidelines of the Federal Insurance Administration, be provided by a generally acceptable insurance carrier and be in an amount representing coverage not less than the least of (i) the outstanding principal balance of the mortgage loan, (ii) the full insurable value of the property or, in cases where only a portion of the property is in the flood zone, the full insurable value of the portion of the property contained therein, and (iii) the maximum amount of insurance available under the National Flood Insurance Program Act of 1968, except in some cases where self-insurance was permitted.

The standard form of hazard insurance policy typically covers physical damage or destruction of the improvements on the mortgaged property caused by fire, lightning, explosion, smoke, windstorm and hail, riot or strike and civil commotion. The policies may contain some conditions and exclusions to coverage, including exclusions related to acts of terrorism. Generally, each of the mortgage loans requires that the related property have coverage for terrorism or terrorist acts, if such coverage is available at commercially

9

reasonable rates. In many cases, there is a cap on the amount that the related borrower will be required to expend on terrorism insurance.

Each mortgage instrument typically also requires the borrower to maintain comprehensive general liability insurance against claims for personal and bodily injury, death or property damage occurring on, in or about the property in an amount customarily required by institutional lenders.

Each mortgage instrument typically further requires the related borrower to maintain business interruption or rent loss insurance in an amount not less than 100% of the projected rental income from the related property for not less than twelve months.

Although properties are typically not insured for earthquake risk, a borrower will be required to obtain earthquake insurance if the property has material improvements and the seismic report indicates that the PML or the scenario expected loss (“SEL”) is greater than 20%.

Zoning and Building Code Compliance. In connection with the origination or acquisition of a commercial, multifamily or manufactured housing community mortgage loan, BSPRT will generally examine whether the use and occupancy and construction of the related real property collateral is in material compliance with zoning, land-use, building rules, regulations and orders then applicable to that property. Evidence of this compliance may be in the form of one or more of the following: legal opinions, surveys, recorded documents, temporary or permanent certificates of occupancy, letters from government officials or agencies, title insurance endorsements, engineering or consulting reports, zoning reports and/or representations by the related borrower.

In some cases, a mortgaged property may constitute a legal non-conforming use or structure. In such cases, BSPRT may require an endorsement to the title insurance policy or the acquisition of law and ordinance insurance with respect to the particular non-conformity unless it determines that: (i) the non-conformity should not have a material adverse effect on the ability of the borrower to rebuild; (ii) if the improvements are rebuilt in accordance with currently applicable law, the value and performance of the property would be acceptable; (iii) any major casualty that would prevent rebuilding has a sufficiently remote likelihood of occurring or BSPRT has a reasonable likelihood of recovering approximately 75% of proceeds from the casualty; or (iv) a cash reserve, a letter of credit or an agreement from a principal of the borrower is provided to cover losses.

If a material violation exists with respect to a mortgaged property, BSPRT may require the borrower to remediate such violation and, subject to the discussion under “—BSPRT’s Underwriting Standards —Escrow Requirements” below, to establish a reserve to cover the cost of such remediation, unless a cash reserve, a letter of credit or an agreement from a principal of the borrower is provided to cover losses.

Escrow Requirements. Based on BSPRT’s analysis of the real property collateral, the borrower and the principals of the borrower, a borrower under a commercial, multifamily or manufactured housing community mortgage loan may be required to fund various escrows for taxes, insurance, replacement reserves, tenant improvements/leasing commissions, deferred maintenance and/or environmental remediation. A case-by-case analysis will be conducted to determine the need for a particular escrow or reserve. Consequently, the aforementioned escrows and reserves are not established for every commercial, multifamily and manufactured housing community mortgage loan. Furthermore, BSPRT may accept an alternative to a cash escrow or reserve from a borrower, such as a letter of credit or a guarantee from the borrower or an affiliate of the borrower or periodic evidence that the items for which the escrow or reserve would have been established are being paid or addressed. In some cases, BSPRT may determine that establishing an escrow or reserve is not warranted given the amounts that would be involved and BSPRT’s evaluation of the ability of the property, the borrower or a holder of direct or indirect ownership interests in the borrower to bear the subject expense or cost absent creation of an escrow or reserve. In some cases, BSPRT may determine that establishing an escrow or reserve is not warranted because a tenant or other third party has agreed to pay the subject cost or expense for which the escrow or reserve would otherwise have been established.

10

Generally, subject to the discussion in the prior paragraph, the required escrows for commercial, multifamily and manufactured housing community mortgage loans originated or acquired by BSPRT are as follows:

| ● | Taxes—Monthly escrow deposits equal to 1/12th of the annual property taxes (based on the most recent property assessment and the current millage rate) are typically required to satisfy real estate taxes and assessments, except that such escrows may not be required in certain circumstances, including, but not limited to, (i) if there is an institutional property sponsor or high net worth individual property sponsor, or (ii) if and to the extent that a sole or major tenant (which may include a ground tenant) at the related mortgaged property is required to pay, or there is sufficient evidence that such sole or major tenant is paying, taxes directly. |

| ● | Insurance—Monthly escrow deposits equal to 1/12th of the annual property insurance premium are typically required to pay insurance premiums, except that such escrows may not be required in certain circumstances, including, but not limited to, (i) if there is an institutional property sponsor or high net worth individual property sponsor, (ii) if the related borrower maintains a blanket insurance policy, or (iii) if and to the extent that a sole or major tenant (which may include a ground tenant) at the related mortgaged property is obligated to maintain, or there is sufficient evidence that such sole or major tenant is maintaining, the insurance or is permitted to self-insure. |

| ● | Replacement Reserves—Replacement reserves are generally calculated in accordance with the expected useful life of the components of the property during the term of the mortgage loan. Annual replacement reserves are generally underwritten to the suggested replacement reserve amount from an independent, third-party property condition or engineering report, or to certain minimum requirements by property type, except that such escrows are not required in certain circumstances, including, but not limited to, (i) if a tenant (which may include a ground tenant) at the related mortgaged property or other third party is responsible for all repairs and maintenance, or (ii) if BSPRT determines that establishing an escrow or reserve is not warranted given the amounts that would be involved and BSPRT’s evaluation of the ability of the property, the borrower or a holder of direct or indirect ownership interests in the borrower to bear the cost of repairs and maintenance absent creation of an escrow or reserve. |

| ● | Tenant Improvements / Leasing Commissions—In the case of retail, office and industrial properties, a tenant improvements / leasing commissions reserve may be required to be funded either at loan origination and/or during the related mortgage loan term to cover certain anticipated leasing commissions or tenant improvement costs which might be associated with re-leasing the space occupied by significant tenants, except that such escrows may not be required in certain circumstances, including, but not limited to, (i) if the related tenant’s lease extends beyond the loan term, (ii) if the rent for the space in question is considered below market, or (iii) if BSPRT determines that establishing an escrow or reserve is not warranted given the amounts that would be involved and BSPRT’s evaluation of the ability of the property, the borrower or a holder of direct or indirect ownership interests in the borrower to bear the anticipated leasing commissions or tenant improvement costs absent creation of an escrow or reserve. |

| ● | Deferred Maintenance—A deferred maintenance reserve may be required to be funded at loan origination or acquisition in an amount typically equal to 100% to 125% of the estimated cost of material immediate repairs or replacements identified in the property condition or engineering report, except that such escrows may not be required in certain circumstances, including, but not limited to, (i) if the sponsor of the borrower delivers a guarantee to complete the immediate repairs in a specified amount of time, (ii) if the deferred maintenance amount does not materially impact the function, performance or value of the property, (iii) if a tenant (which may include a ground tenant) at the related mortgaged property or other third party is responsible for the repairs, or (iv) if BSPRT determines that establishing an escrow or reserve is not warranted given the amounts that would be involved and BSPRT’s evaluation of the ability of the property, the |

11

borrower or a holder of direct or indirect ownership interests in the borrower to bear the cost of repairs absent creation of an escrow or reserve.

| ● | Environmental Remediation—An environmental remediation reserve may be required at loan origination or acquisition in an amount equal to 100% to 125% of the estimated remediation cost identified in the environmental report, except that such escrows may not be required in certain circumstances, including, but not limited to, (i) if the sponsor of the borrower delivers a guarantee agreeing to take responsibility and pay for the identified environmental issues, (ii) if environmental insurance is obtained or already in place, (iii) if a third party unrelated to the borrower is identified as the responsible party or (iv) if BSPRT determines that establishing an escrow or reserve is not warranted given the amounts that would be involved and BSPRT’s evaluation of the ability of the property, the borrower or a holder of direct or indirect ownership interests in the borrower to bear the cost of remediation absent creation of an escrow or reserve. |

For a description of the escrows collected with respect to the BSPRT Mortgage Loans, see Annex A-1.

Exceptions. The BSPRT Mortgage Loans were originated in accordance with the underwriting standards set forth above.

Compliance with Rule 15Ga-1 under the Exchange Act

BSPRT has no prior history as a securitizer and therefore has not filed a Form ABS-15G. BSPRT has no demand, repurchase or replacement history to report as required by Rule 15Ga-1.

Retained Interests in This Securitization

As of the date hereof, neither BSPRT nor any of its affiliates intends to retain any certificates issued by the issuing entity or any other economic interest in this securitization. However, BSPRT and its affiliates, are not restricted from retaining any of such certificates and may, prior to the Closing Date, determine that they wish to retain certain certificates. In addition, BSPRT and its affiliates may acquire certificates in the secondary market. Any such party will have the right to dispose of any such certificates at any time.

The information set forth under “—BSPRT Finance, LLC” has been provided by BSPRT.

| 4. | The first sentence in “Credit Risk Retention—Representations and Warranties” on page 278 of the Preliminary Prospectus is deleted and replaced with the following: |

Each of Column, NREC, BSPRT and BSP will make the representations and warranties identified on Annex D-1 to this prospectus with respect to the Mortgage Loan that it is contributing to this transaction, subject to certain exceptions to such representations and warranties set forth on Annex D-2 to this prospectus.

Additionally, the last paragraph of the same section on page 279 of the Preliminary Prospectus is also deleted and replaced with the following

At the time of its decision to include the BSPRT Mortgage Loans and the BSP Mortgage Loan, as applicable, in this transaction, each of BSPRT and BSP determined either that the risks associated with the matters giving rise to each exception set forth on Annex D-2 to this prospectus were not material or were mitigated by one or more compensating factors, including without limitation, reserves, title insurance or other relevant insurance, opinions of legal counsel, letters of credit, a full or partial recourse guaranty from the borrower sponsor, a full or partial cash sweep, positive credit metrics (such as a low loan-to-value ratio, high debt service coverage ratio or debt yield, or any combination of such factors), or by other circumstances, such as strong sponsorship, a desirable property type, strong tenancy at the related Mortgaged Property, the

12

likelihood that the related mortgage loan borrower or a third party may (and/or, in the case of the mortgage loan borrower, is required to under the related loan documents) resolve the matter soon, any requirements to obtain rating agency confirmation prior to taking an action related to such exception, a determination by BSPRT or BSP, as applicable, that the acceptance of the related fact or circumstance by the related originator was prudent and consistent with market standards after consultation with appropriate industry experts or a determination by BSPRT or BSP, as applicable, that the circumstances that gave rise to such exception should not have a material adverse effect on the use, operation or value of the related Mortgaged Property or on any related lender’s security interest in such Mortgaged Property. However, there can be no assurance that the compensating factors or other circumstances upon which BSPRT or BSP, as applicable, based its decisions will in fact sufficiently mitigate those risks. In particular, we note that an evaluation of the risks presented by such exceptions, including whether any mitigating factors or circumstances are sufficient, may necessarily involve an assessment as to the likelihood of future events as to which no assurance can be given. Additional information regarding the applicable BSPRT Mortgage Loans or BSP Mortgage Loan, including the risks related thereto, is described under “Risk Factors” and “Description of the Mortgage Pool”.

B. ADDITIONAL COLLATERAL UPDATES

| 1. | Footnote 1 to the table set forth in “Description of the Mortgage Pool—Additional Indebtedness—Mezzanine Indebtedness” on page 187 of the Preliminary Prospectus; Page A-2-67 of Annex A-2 of the Preliminary Prospectus and exception to representation #9 on page D-2-5 of Annex D of the Preliminary Prospectus is updated by the following information: |

The Yorkshire & Lexington Towers mezzanine lenders have informed the Depositor that they intend to reallocate the principal balance of the two mezzanine loans across three tranches of mezzanine loans, a most senior mezzanine loan, a next most senior mezzanine loan and a junior mezzanine loan. The aggregate principal balance of the mezzanine loans and the weighted average interest rate will not change.

| 2. | With respect to the table set forth on page A-2-12 of Annex A-2 to the Preliminary Prospectus under the heading “Amortization Types”, the fourth row titled “IO-Balloon, ARD” under the column headed “Amortization Types” is deleted and replaced with the title “ARD Interest-only”. |

| 3. | With respect to page A-2-49 of Annex A-2 to the Preliminary Prospectus, the photographs relating to Mortgage Loan No. 2 – GNL Portfolio are deleted and replaced with Exhibit A. |

| 4. | With respect to page A-2-80 of Annex A-2 to the Preliminary Prospectus, the paragraphs titled “The Borrower”, “The Sponsor” and “Affiliated Ground Lessee” are deleted and replaced with the following: |

The Borrower. The borrowing entity for the loan is THR 43 Land LLC, a Delaware limited liability company and special purpose entity. The borrowing entity is controlled by Tishman Hotel & Realty LP, a joint venture between affiliates of Tishman Equities LP, comprising approximately 75.8% ownership, and MetLife, Inc., comprising approximately 24.2% ownership.

The Sponsor. The loan’s sponsor and nonrecourse carve-out guarantor is Tishman Hotel & Realty LP. The Tishman organization is a vertically integrated real estate owner, developer, operator and advisor. With roots dating back to 1898, Tishman is comprised of a diversified staff of experienced real estate, financial and hotel management specialists, and is complemented by a technical staff of architects, engineers and construction management professionals. According to the sponsor, over the last 30 years, Tishman has owned and developed roughly 10 million SF for its own account and has sourced and structured nearly $8.0 billion of debt and equity for its projects. Tishman has managed a total of over 50 hotels including over 20,000 rooms and has acted as a third-party advisor to other hotel stakeholders as well. Tishman’s wide range of hospitality services include: hotel management, hotel asset management, immediate

13

management takeover and operations & market analysis. Current assets under management exceed $4.0 billion in real estate and other asset classes. Unlike traditional real estate investment managers, Tishman’s own account represents nearly $3.0 billion, or roughly 75% of its assets under management.

Affiliated Ground Lessee. The Lessee, THR Times Square, LLC, is affiliated with the borrower and guarantor. The Westin Times Square Fee loan will become full recourse to Tishman if the Ground Lease is amended, modified, terminated, cancelled, surrendered, expires or otherwise ceases to be in full force and effect, in each case without the prior written consent of the lender.

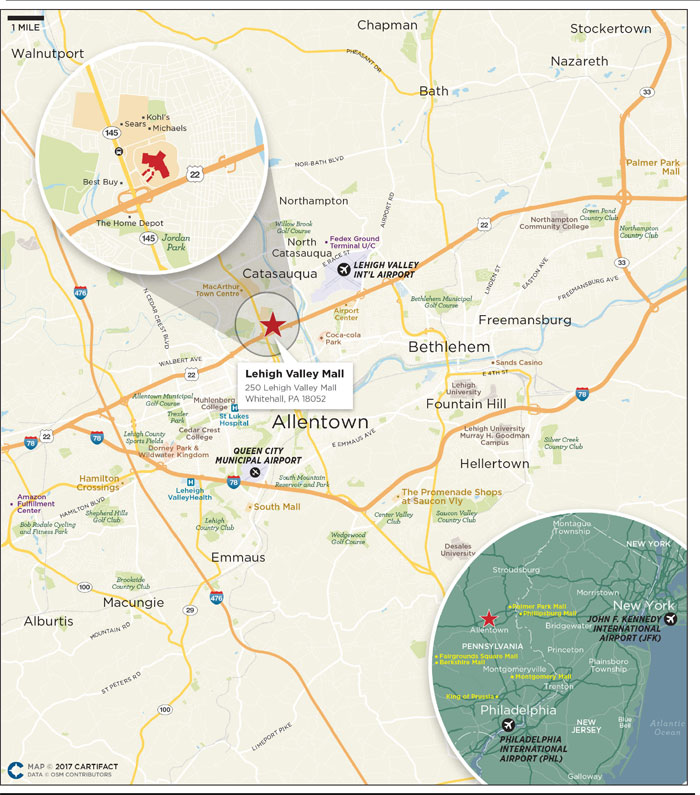

| 5. | With respect to page A-2-99 of Annex A-2 to the Preliminary Prospectus, the map relating to Mortgage Loan No. 6 – Lehigh Valley Mall is deleted and replaced with Exhibit B. |

| 6. | With respect to the table set forth on page A-2-104 of Annex A-2 to the Preliminary Prospectus under the heading “Competitive Set Summary” relating to Mortgage Loan No. 6 – Lehigh Valley Mall, the value in the row titled “Montgomery Mall” under the column headed “Proximity (miles)” is hereby revised to reflect that the Montgomery Mall is 40.0 miles away from the subject property. |

| 7. | With respect to the table set forth on page A-2-104 of Annex A-2 to the Preliminary Prospectus under the heading “Top Tenant Summary” relating to Mortgage Loan No. 6 – Lehigh Valley Mall, the value in the row titled “New York & Company” under the column headed “Occupancy Cost %” is updated to reflect an anchor to the following additional footnote: |

| (6) | The New York & Company lease was recently amended, reducing the annual payment obligations (including a base rent reduction) to $25.72 PSF. As amended, the estimated occupancy cost is 27.3% based on projected 2017 annual sales as of August 2017. |

14

Exhibit A

15

Exhibit B

16