| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-193376-25 | ||

November 2, 2015

FREE WRITING PROSPECTUS

STRUCTURAL AND COLLATERAL TERM SHEET

$960,912,147

(Approximate Total Mortgage Pool Balance)

$828,786,000

(Approximate Offered Certificates)

COMM 2015-LC23 |

Deutsche Mortgage & Asset Receiving Corporation

Depositor

German American Capital Corporation

Ladder Capital Finance LLC

Cantor Commercial Real Estate Lending, L.P.

Jefferies LoanCore LLC

Sponsors and Mortgage Loan Sellers

| Deutsche Bank Securities | Cantor Fitzgerald & Co. | |

| Joint Bookrunning Managers and Co-Lead Managers | ||

| Jefferies | ||

| Co-Manager | ||

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-193376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

COMM 2015-LC23 Mortgage Trust

Capitalized terms used but not defined herein have the meanings assigned to them in the other Free Writing Prospectus expected to be dated November 2, 2015 relating to the offered certificates (hereinafter referred to as the “Free Writing Prospectus”).

|

| KEY FEATURES OF SECURITIZATION |

| Offering Terms: | ||

| Joint Bookrunners & Co-Lead Managers: | Deutsche Bank Securities Inc. and Cantor Fitzgerald & Co. | |

| Co-Manager: | Jefferies LLC | |

| Mortgage Loan Sellers: | German American Capital Corporation* (“GACC”) (41.1%), Ladder Capital Finance LLC (“Ladder”) (30.6%), Cantor Commercial Real Estate Lending, L.P. (“CCRE”) (16.5%) and Jefferies LoanCore LLC (“JLC”) (11.8%). *An indirect wholly owned subsidiary of Deutsche Bank AG. | |

| Master Servicer: | Wells Fargo Bank, National Association | |

| Operating Advisor: | Park Bridge Lender Services LLC | |

| Special Servicer: | LNR Partners, LLC | |

| Trustee: | Wilmington Trust, National Association | |

| Certificate Administrator: | Wells Fargo Bank, National Association | |

| Rating Agencies: | Moody’s Investors Service, Inc., Fitch Ratings, Inc. and Kroll Bond Rating Agency, Inc. | |

| Determination Date: | 6thday of each month, or if such 6th day is not a business day, the following business day, commencing in December 2015. | |

| Distribution Date: | 4thbusiness day following the Determination Date in each month, commencing in December 2015. | |

| Cut-off Date: | Payment Date in November 2015 (or related origination date, if later). Unless otherwise noted, all Mortgage Loan statistics are based on balances as of the Cut-off Date. | |

| Settlement Date: | On or about November 17, 2015 | |

| Settlement Terms: | DTC, Euroclear and Clearstream, same day funds, with accrued interest. | |

| ERISA Eligible: | All of the Offered Certificates are expected to be ERISA eligible. | |

| SMMEA Eligible: | None of the Offered Certificates will be SMMEA eligible. | |

| Day Count: | 30/360 | |

| Tax Treatment: | REMIC | |

| Rated Final Distribution Date: | October 2053 | |

| Minimum Denominations: | $10,000 (or $100,000 with respect to Class XP-A and Class XS-A Certificates) and in each case in multiples of $1 thereafter. | |

| Clean-up Call: | 1% (with certain exceptions described under“The Pooling and Servicing Agreement—Optional Termination” in the Free Writing Prospectus) | |

| Distribution of Collateral by Property Type |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 3 |

COMM 2015-LC23 Mortgage Trust

|

| TRANSACTION HIGHLIGHTS |

| Mortgage Loan Sellers | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Outstanding Pool Balance |

| German American Capital Corporation | 17 | 17 | $362,856,940 | 37.8% |

| Ladder Capital Finance LLC | 25 | 55 | $246,060,185 | 25.6% |

| Cantor Commercial Real Estate Lending, L.P. | 11 | 13 | $158,901,949 | 16.5% |

| Jefferies LoanCore LLC | 8 | 14 | $113,093,073 | 11.8% |

| LCF / GACC(1) | 1 | 21 | $80,000,000 | 8.3% |

| Total: | 62 | 120 | $960,912,147 | 100.0% |

| Pooled Collateral Facts: | |

| Initial Outstanding Pool Balance: | $960,912,147 |

| Number of Mortgage Loans: | 62 |

| Number of Mortgaged Properties: | 120 |

| Average Mortgage Loan Cut-off Date Balance: | $15,498,583 |

| Average Mortgaged Property Cut-off Date Balance: | $8,007,601 |

| Weighted Average Mortgage Rate: | 4.6650% |

| Weighted Average Mortgage Loan Original Term to Maturity Date or ARD (months): | 107 |

| Weighted Average Mortgage Loan Remaining Term to Maturity Date or ARD (months): | 105 |

| Weighted Average Mortgage Loan Seasoning (months): | 1 |

| % of Mortgaged Properties Leased to a Single Tenant: | 12.1% |

Credit Statistics(2): | |

| Weighted Average Mortgage Loan U/W NCF DSCR: | 1.82x |

| Weighted Average Mortgage Loan Cut-off Date LTV(3)(4): | 61.6% |

| Weighted Average Mortgage Loan Maturity Date or ARD LTV(3)(4): | 55.2% |

| Weighted Average U/W NOI Debt Yield: | 10.6% |

Amortization Overview: | |

| % Mortgage Loans with Amortization through Maturity Date or ARD: | 39.4% |

| % Mortgage Loans which pay Interest Only through Maturity Date or ARD: | 38.7% |

| % Mortgage Loans which pay Interest Only followed by Amortization through Maturity Date or ARD: | 21.8% |

| Weighted Average Remaining Amortization Term (months)(5): | 349 |

Loan Structural Features: | |

| % Mortgage Loans with Upfront or Ongoing Tax Reserves: | 81.5% |

| % Mortgage Loans with Upfront or Ongoing Replacement Reserves(6): | 71.4% |

| % Mortgage Loans with Upfront or Ongoing Insurance Reserves: | 54.1% |

| % Mortgage Loans with Upfront or Ongoing TI/LC Reserves(7): | 82.4% |

| % Mortgage Loans with Upfront Engineering Reserves: | 40.1% |

| % Mortgage Loans with Upfront or Ongoing Other Reserves: | 64.5% |

| % Mortgage Loans with In Place Hard Lockboxes: | 56.2% |

| % Mortgage Loans with Cash Traps Triggered at DSCR Levels ≥ 1.05x: | 75.5% |

| % Mortgage Loans with Cash Traps Triggered at Debt Yield ≥ 7.0%: | 8.7% |

| % Mortgage Loans with Defeasance Only After a Lockout Period and Prior to an Open Period(8): | 69.2% |

| % Mortgage Loans with Prepayment Only After a Lockout Period and Prior to an Open Period with a Yield Maintenance Charge: | 30.4% |

| % Mortgage Loans with Prepayment with a Yield Maintenance Charge Prior to an Open Period and also Defeasance or Yield Maintenance After a Lockout Period and Prior to an Open Period: | 0.4% |

| (1) | The Equity Inns Portfolio Mortgage Loan was co-originated by LCF and GACC. LCF will contribute $48.0 million of the Equity Inns Portfolio Mortgage Loan, which represents 60.0% of the Equity Inns Portfolio Mortgage Loan cut-off date balance, and GACC will contribute $32.0 million of the Equity Inns Portfolio Mortgage Loan, which represents 40.0% of Equity Inns Portfolio Mortgage Loan cut-off date balance. |

| (2) | With respect to the Equity Inns Portfolio Mortgage Loan, 32 Avenue of the Americas Mortgage Loan, 11 Madison Avenue Mortgage Loan, Harvey Building Products Portfolio Mortgage Loan, Springfield Mall Mortgage Loan and 40 Wall Street Mortgage Loan, the LTV, DSCR and Debt Yield calculations include the relatedpari passu companion loan(s), but not any related subordinate companion loan(s). |

| (3) | With respect to the Equity Inns Portfolio Mortgage Loan, representing 8.3% of the initial outstanding pool balance, the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated based on the portfolio appraised value, which attributes a premium to the aggregate value of the Equity Inns Portfolio mortgaged properties as a whole. For additional information, see the Footnotes to Annex A-1 in the Free Writing Prospectus. |

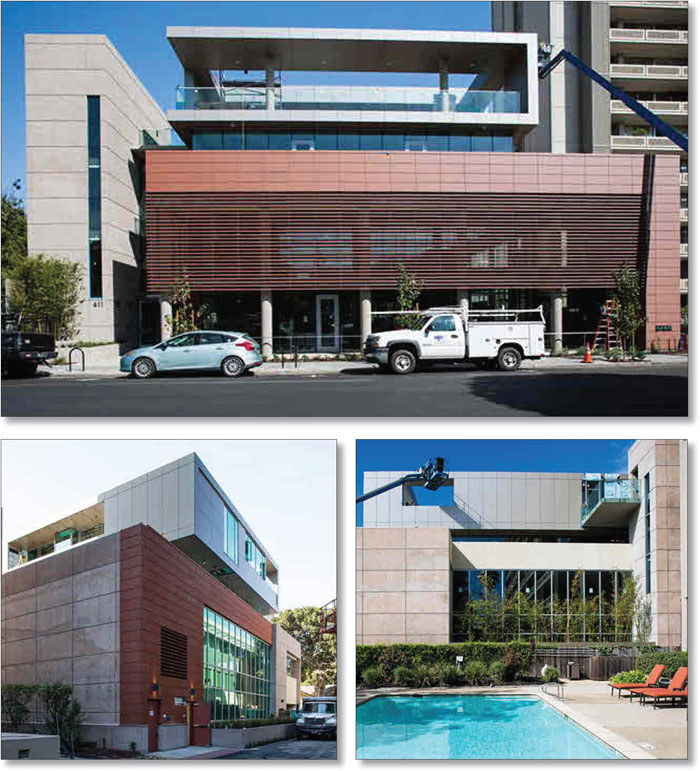

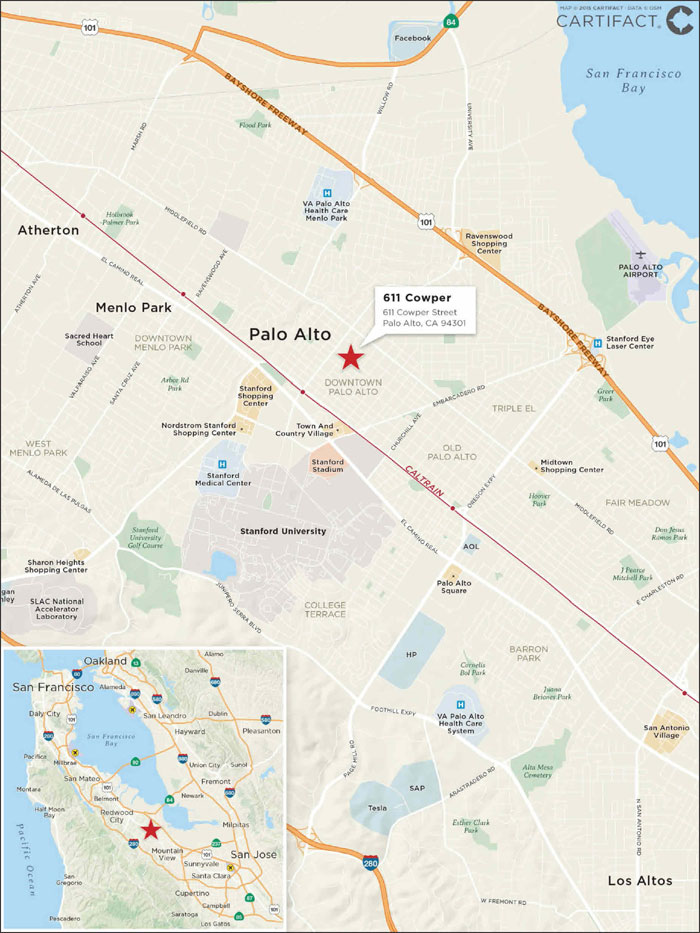

| (4) | With respect to 611 Cowper mortgage loan, representing 3.4% of the initial outstanding pool balance, the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated based on the “as stabilized” value. For additional information, see the Footnotes to Annex A-1 in the Free Writing Prospectus. |

| (5) | Excludes loans which are interest only for the full loan term. |

| (6) | Includes FF&E Reserves. |

| (7) | Represents the percent of the allocated initial outstanding principal balance of retail, office, industrial and mixed use properties only. |

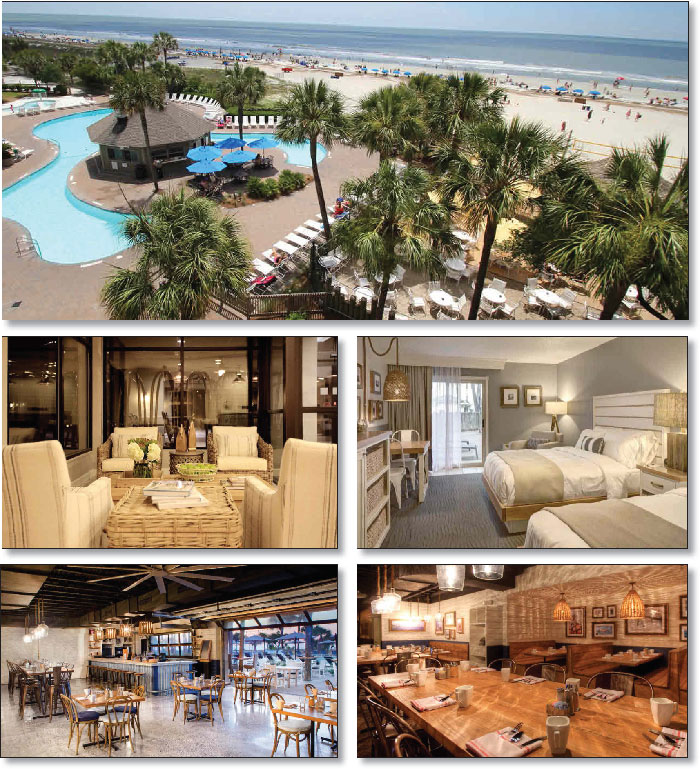

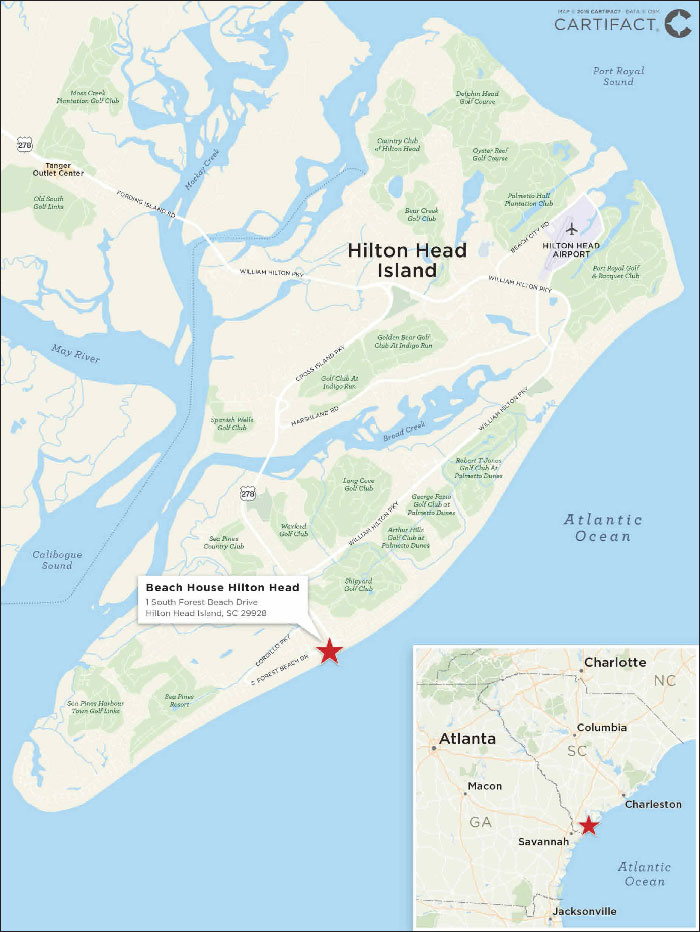

| (8) | With respect to the Beach House Hilton Head mortgage loan, defeasance is permitted for 91 payments after a lockout period. Beginning with the 59th payment after the lockout period, in lieu of defeasance, the borrower may prepay the mortgage loan in full, together with a prepayment penalty equal to (a) 4% if such prepayment is made on or after October 6, 2022 through October 5, 2023, 3% if such prepayment is made on or after October 6, 2023 through October 5, 2024 and 1% if such prepayment is made on or after October 6, 2024 through July 5, 2025. On or after July 6, 2025 through October 6, 2025, the Beach House Hilton Head mortgage loan may be prepaid without penalty. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 4 |

COMM 2015-LC23 Mortgage Trust

|

| STRUCTURE OVERVIEW |

OFFERED CERTIFICATES

| Class(1) | Ratings (Moody’s/Fitch/KBRA) | Initial Certificate Balance or Notional Amount(2) | Initial Subordination | Weighted Average Life | Principal Window (months)(3) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) |

| Class A-1 | Aaa(sf)/AAAsf/AAA(sf) | $39,109,000 | 30.000%(6) | 2.67 | 1 – 58 | 43.1% | 15.1% |

| Class A-2 | Aaa(sf)/AAAsf/AAA(sf) | $210,190,000 | 30.000%(6) | 4.89 | 58 – 59 | 43.1% | 15.1% |

| Class A-SB | Aaa(sf)/AAAsf/AAA(sf) | $53,371,000 | 30.000%(6) | 7.40 | 59 – 116 | 43.1% | 15.1% |

| Class A-3 | Aaa(sf)/AAAsf/AAA(sf) | $125,000,000 | 30.000%(6) | 9.79 | 116 – 118 | 43.1% | 15.1% |

| Class A-4 | Aaa(sf)/AAAsf/AAA(sf) | $244,968,000 | 30.000%(6) | 9.85 | 118 – 119 | 43.1% | 15.1% |

| Class XP-A(7) | Aa1(sf)/AAAsf/AAA(sf) | $733,896,000(8) | N/A | N/A | N/A | N/A | N/A |

| Class XS-A(7) | Aa1(sf)/AAAsf/AAA(sf) | $733,896,000(8) | N/A | N/A | N/A | N/A | N/A |

| Class A-M | Aa2(sf)/AAAsf/AAA(sf) | $61,258,000 | 23.625% | 9.90 | 119 – 119 | 47.0% | 13.9% |

| Class B | A1(sf)/AA-sf/AA(sf) | $51,649,000 | 18.250% | 9.90 | 119 – 119 | 50.4% | 13.0% |

| Class C | NR/A-sf/A(sf) | $43,241,000 | 13.750% | 9.90 | 119 – 119 | 53.1% | 12.3% |

NON-OFFERED CERTIFICATES

| Class(1) | Ratings Moody’s/Fitch/KBRA | Initial Certificate Balance or Notional Amount(2) | Initial Subordination | Weighted Average Life | Principal Window (months)(3) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) |

| Class X-B(7) | NR/A-sf/AAA(sf) | $94,890,000(8) | N/A | N/A | N/A | N/A | N/A |

| Class X-C(7) | NR/BBB-sf/BBB-(sf) | $52,850,000(8) | N/A | N/A | N/A | N/A | N/A |

| Class X-D(7) | NR/BB-sf/BB(sf) | $22,822,000(8) | N/A | N/A | N/A | N/A | N/A |

| Class X-E(7) | NR/NR/B-(sf) | $22,822,000(8) | N/A | N/A | N/A | N/A | N/A |

| Class X-F(7) | NR/NR/NR | $33,632,147(8) | N/A | N/A | N/A | N/A | N/A |

| Class D | NR/BBBsf/BBB+(sf) | $28,828,000 | 10.750% | 9.90 | 119 – 120 | 55.0% | 11.9% |

| Class E | NR/BBB-sf/BBB-(sf) | $24,022,000 | 8.250% | 9.98 | 120 – 120 | 56.5% | 11.6% |

| Class F | NR/BB-sf/BB(sf) | $22,822,000 | 5.875% | 9.98 | 120 – 120 | 58.0% | 11.3% |

| Class G | NR/B-sf/B+(sf) | $10,810,000 | 4.750% | 9.98 | 120 – 120 | 58.7% | 11.1% |

| Class H | NR/NR/B-(sf) | $12,012,000 | 3.500% | 9.98 | 120 – 120 | 59.4% | 11.0% |

| Class J | NR/NR/NR | $33,632,147 | 0.000% | 9.98 | 120 – 120 | 61.6% | 10.6% |

| (1) | The pass-through rates applicable to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G, Class H and Class J Certificates will equal one of: (i) a fixed per annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, (iii) a rate equal to the lesser of a specified pass-through rate and the rate specified in clause (ii) or (iv) the rate specified in clause (ii), less a specified rate. |

| (2) | Approximate; subject to a permitted variance of plus or minus 5%. In addition, the notional amounts of the Class XP-A, Class XS-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates (collectively, the “Class X Certificates”) may vary depending upon the final pricing of the classes of Certificates whose Certificate Balances comprise such notional amounts and, if as a result of such pricing the pass-through rate of any class of Class X Certificates would be equal to zero, such Class X Certificates may not be issued on the settlement date of this securitization. |

| (3) | The weighted average life and principal window during which distributions of principal would be received as set forth in the table with respect to each class of Certificates with a Certificate Balance is based on (i) modeling assumptions described in the Free Writing Prospectus, (ii) assumptions that there are no prepayments, delinquencies or losses on the mortgage loans and (iii) assumptions that there are no extensions of maturity dates and mortgage loans with anticipated repayment dates, if any, are repaid on the respective anticipated repayment dates. |

| (4) | “Certificate Principal to Value Ratio” for any class with a Certificate Balance is calculated as the product of (a) the weighted average Mortgage Loan Cut-off Date LTV of the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of the related class of Certificates and all other classes with a Certificate Balance, if any, that are senior to such class, and the denominator of which is the total initial Certificate Balance of all Certificates. The Certificate Principal to Value Ratios of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are calculated in the aggregate for those classes as if they were a single class. |

| (5) | “Underwritten NOI Debt Yield” for any class with a Certificate Balance is calculated as the product of (a) the weighted average U/W NOI Debt Yield for the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of all Certificates and the denominator of which is the total initial Certificate Balance of the related class of Certificates and all other classes with a Certificate Balance, if any, that are senior to such class. The Underwritten NOI Debt Yields of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are calculated in the aggregate for those classes as if they were a single class. |

| (6) | The initial subordination levels for the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are represented in the aggregate. |

| (7) | As further described in the Free Writing Prospectus, the pass-through rates applicable to the Class XP-A and Class XS-A Certificates are described in “Structure Overview—Interest Payments” herein. In addition, the pass-through rate applicable to the Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates for each Distribution Date will generally be equal to the excess of (i) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360 day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such distribution date occurs over (ii)(A) with respect to the Class X-B Certificates, the weighted average of the pass-through rates of the Class B and Class C Certificates (based on their Certificate Balances), (B) with respect to the Class X-C Certificates, the weighted average of the pass-through rates of the Class D and Class E Certificates (based on their Certificate Balances), (C) with respect to the Class X-D Certificates, the pass-through rate of the Class F Certificates, (D) with respect to the Class X-E Certificates, the weighted average of the pass-through rates of the Class G and Class H Certificates (based on their Certificate Balances) and (E) with respect to the Class X-F Certificates, the pass-through rate of the Class J Certificates. |

| (8) | The Class X Certificates will not have Certificate Balances. None of the Class X Certificates will be entitled to distributions of principal. The interest accrual amounts on the Class XP-A Certificates will be calculated by reference to a notional amount equal to the sum of the component notional amounts of the components of the Class XP-A Certificates, each of which components will relate to one of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M Certificates and, at any time during any of the periods specified on Annex H to the Free Writing Prospectus, will equal the lesser of (a) the amount specified on Annex H to the Free Writing Prospectus, and (b) the then Certificate Balance of the related class of Certificates. The interest accrual amounts on the Class XS-A Certificates will be calculated by reference to a notional amount equal to the sum of the total Certificate Balance of each of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M Certificates. The interest accrual amounts on the Class X-B Certificates will be calculated by reference to a notional amount equal to the sum of the total Certificate Balance of each of the Class B and Class C Certificates. The interest accrual amounts on the Class X-C Certificates will be calculated by reference to a notional amount equal to the sum of the total Certificate Balance of the Class D and Class E Certificates. The interest accrual amounts on the Class X-D Certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class F Certificates. The interest accrual amounts on the Class X-E Certificates will be calculated by reference to a notional amount equal to the sum of the total Certificate Balance of the Class G and Class H Certificates. The interest accrual amounts on the Class X-F Certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class J Certificates. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 5 |

COMM 2015-LC23 Mortgage Trust

|

| STRUCTURE OVERVIEW |

| Class A-2 Principal Paydown(1) |

| Class | Mortgage | Mortgage Loan | Property Type | Cut-off Date Balance | Remaining Term to Maturity (Mos.) | Cut-off Date LTV Ratio | U/W NCF DSCR | U/W NOI Debt Yield | |

| A-2 | JLC | Carrollwood Station | Multifamily | $21,500,000 | 58 | 62.1% | 1.53x | 8.6% | |

| A-2 | CCRE | Warsaw Village | Retail | $3,600,000 | 58 | 73.5% | 1.33x | 10.0% | |

| A-2 | LCF / GACC | Equity Inns Portfolio | Hospitality | $80,000,000 | 59 | 64.4% | 2.35x | 13.3% | |

| A-2 | LCF | 1209 DeKalb | Multifamily | $46,000,000 | 59 | 72.3% | 1.48x | 7.1% | |

| A-2 | LCF | Harvey Building Products Portfolio | Various | $41,953,778 | 59 | 53.5% | 1.96x | 12.8% | |

| A-2 | CCRE | Murrieta Spectrum | Retail | $20,600,000 | 59 | 70.3% | 1.30x | 8.9% | |

| (1) | This table reflects the mortgage loans whose balloon payments will be applied to pay down the Class A-2 Certificates, assuming (i) that none of the mortgage loans experience prepayments, defaults or losses, (ii) there are no extensions of maturity dates and (iii) each mortgage loan is paid in full on its stated maturity date, or in the case of any mortgage loan with an anticipated repayment date, on such repayment date. See “Yield and Maturity Considerations—Yield Considerations” in the Free Writing Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 6 |

COMM 2015-LC23 Mortgage Trust

| STRUCTURE OVERVIEW |

| Principal Payments: | Payments in respect of principal of the Certificates will be distributed,first, to the Class A-SB Certificates, until the Certificate Balance of such Class is reduced to the planned principal balance for the related Distribution Date set forth on Annex A-3 to the Free Writing Prospectus,then, to the Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G, Class H and Class J Certificates, in that order, until the Certificate Balance of each such Class is reduced to zero. Notwithstanding the foregoing, if the total principal balance of the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G, Class H and Class J Certificates have been reduced to zero as a result of loss allocation, payments in respect of principal of the Certificates will be distributed,first, to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates, on apro rata basis, based on the Certificate Balance of each such Class,then, to the extent of any recoveries on realized losses, to the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G, Class H and Class J Certificates, in that order, in each case until the Certificate Balance of each such Class is reduced to zero (or previously allocated realized losses have been fully reimbursed).

Each Class of Class X Certificates will not be entitled to receive distributions of principal; however, (i) the notional amounts of the Class XP-A and Class XS-A Certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to one or more of each of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-M Certificates; (ii) the notional amount of the Class X-B Certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class B and Class C Certificates; (iii) the notional amount of the Class X-C Certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class D and Class E Certificates; (iv) the notional amount of the Class X-D Certificates will be reduced by the principal distributions and realized losses allocated to the Class F Certificates; (v) the notional amount of the Class X-E Certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class G and Class H Certificates; and (vi) the notional amount of the Class X-F Certificates will be reduced by the principal distributions and realized losses allocated to the Class J Certificates.

|

| Interest Payments: | On each Distribution Date, interest accrued for each Class of the Certificates at the applicable pass-through rate will be distributed in the following order of priority, to the extent of available funds:first, to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class XP-A, Class XS-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates, on apro rata basis, based on the accrued and unpaid interest on each such Class andthen, to the Class A-M, Class B, Class C, Class D, Class E, Class F Class G, Class H and Class J Certificates, in that order, in each case until the interest payable to each such Class is paid in full.

The pass-through rates applicable to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G, Class H and Class J Certificates for each Distribution Date will equal one of: (i) a fixedper annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such Distribution Date occurs, (iii) a rate equal to the lesser of a specified pass-through rate and the rate specified in clause (ii) or (iv) the rate specified in clause (ii), less a specified rate.

As further described in the Free Writing Prospectus, the pass-through rate applicable to the Class XP-A Certificates for each Distribution Date will equal the weighted average of the respective strip rates of the related components (the “Class XP-A Components”), which each applicable strip rate will equal the excess, if any, of (a) the lesser of (1) the rateper annum for such Distribution Date set forth on Annex I to the Free Writing Prospectus and (2) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such Distribution Date occurs, over (b) the pass-through rate for such Distribution Date for the related class of Certificates. The pass-through rate applicable to the Class XS-A Certificates for each Distribution Date will equal the weighted average of the respective strip rates of the related components, which each applicable strip rate will equal (A) if any portion of the related component notional amount is also included in the related component of a Class XP-A Component immediately prior to the related Distribution Date, the excess, if any, of (a) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. 7 |

COMM 2015-LC23 Mortgage Trust

| STRUCTURE OVERVIEW |

necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such Distribution Date occurs, over (b) the greater of (1) the rateper annum corresponding to such Distribution Date as set forth on Annex I to the Free Writing Prospectus and (2) the pass-through rate for such Distribution Date for the related class of Certificates, and (B) if any portion of the related component notional amount is not included in the related component of a Class XP-A Component immediately prior to the related Distribution Date, the excess, if any, of (a) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such Distribution Date occurs, over (b) pass-through rate for such Distribution Date for the related class of Certificates.

| |

| In addition, the pass-through rates applicable to the Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates for each Distribution Date will generally be equal to the excess of (i) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such Distribution Date occurs over (ii) (A) with respect to the Class X-B Certificates, the weighted average of the pass-through rates of the Class B and Class C Certificates (based on their Certificate Balances), (B) with respect to the Class X-C Certificates, the weighted average of the pass-through rates of the Class D and Class E Certificates (based on their Certificate Balances), (C) with respect to the Class X-D Certificates, the pass-through rate of the Class F Certificates, (D) with respect to the Class X-E Certificates, the weighted average of the pass-through rates of the Class G and Class H Certificates (based on their Certificate Balances) and (E) with respect to the Class X-F Certificates, the pass-through rate of the Class J Certificates. | |

| Prepayment Interest Shortfalls: | Prepayment interest shortfalls will be allocatedpro rata based on interest entitlements, in reduction of the interest otherwise payable with respect to each of the interest-bearing Classes of Certificates. |

| Loss Allocation: | Losses will be allocated to each Class of Certificates entitled to principal in reverse alphabetical order starting with Class J through and including Class A-M and then to Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates on apro ratabasis based on the Certificate Balance of each such Class. The notional amount of any Class of Class X Certificates will be reduced by the aggregate amount of realized losses allocated to the Certificates that are components of the notional amount of such Class of Class X Certificates.

|

Prepayment Premiums: | A percentage of all prepayment premiums (either fixed prepayment premiums or yield maintenance amounts) collected on the Mortgage Loans will be allocated to each of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D and Class E Certificates (the “YM P&I Certificates”) then entitled to principal distributions, which percentage will be equal to the product of (a) a fraction, not greater than one, the numerator of which is the amount of principal distributed to such Class on such Distribution Date and the denominator of which is the total amount of principal distributed to the holders of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-M, Class B, Class C, Class D and Class E Certificates on such Distribution Date, and (b) a fraction (expressed as a percentage which can be no greater than 100% nor less than 0%), the numerator of which is the excess of the pass-through rate of each such Class of Certificates currently receiving principal over the relevant Discount Rate, and the denominator of which is the excess of the Mortgage Rate of the related Mortgage Loan over the relevant Discount Rate.

Prepayment Premium Allocation Percentage for all YM P&I Certificates = |

| (Pass-Through Rate - Discount Rate) | The percentage of the principal | |||

| (Mortgage Rate - Discount Rate) | X | distribution amount to such Class as | ||

| described in (a) above |

| The remaining percentage of the prepayment premiums will be allocated to the Class XS-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates in the manner described in the Free Writing Prospectus. In general, this formula provides for an increase in the percentage of prepayment premiums allocated to the YM P&I Certificates then entitled to principal distributions relative to the Class XS-A, Class X-B, Class X-C, Class X-D, Class X-E and Class X-F Certificates as Discount Rates decrease and a decrease in the percentage |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. 8 |

COMM 2015-LC23 Mortgage Trust

| STRUCTURE OVERVIEW |

| allocated to such Classes as Discount Rates rise. | |

| Loan Combinations: | The portfolio of mortgaged properties identified on Annex A–1 to the Free Writing Prospectus as Equity Inns Portfolio secures (i) a Mortgage Loan evidenced by two promissory notes designated as Note A-1-A and Note A-4-A, with an aggregate outstanding principal balance as of the Cut–off Date of $80,000,000 (the “Equity Inns Portfolio Mortgage Loan”), representing approximately 8.3% of the Initial Outstanding Pool Balance, (ii) four promissory notes designated as Note A-1-B, Note A-2-A, Note A-2-B and Note A-3, with an aggregate outstanding principal balance as of the Cut-off Date of $91,200,000, which are currently held by LCF or an affiliate, and (iii) three promissory notes designated as Note A-4-B, Note A-5 and Note A-6 (together with Note A-1-B, Note A-2-A, Note A-2-B and Note A-3, the “Equity Inns Portfolio Companion Loans”), with an aggregate outstanding principal balance as of the Cut-off Date of $60,800,000, which are currently held by GACC or an affiliate. The Equity Inns Portfolio Mortgage Loan and the Equity Inns Portfolio Companion Loans arepari passu in right of payment and are collectively referred to herein as the “The Equity Inns Portfolio Loan Combination”.

The Equity Inns Portfolio Loan Combination will be serviced pursuant to the COMM 2015-LC23 pooling and servicing agreement and the related intercreditor agreement. For additional information regarding the Equity Inns Portfolio Loan Combination, see“Description of the Mortgage Pool—Loan Combinations—Equity Inns Portfolio Loan Combination”in the Free Writing Prospectus.

The Mortgaged Property identified on Annex A-1 to the Free Writing Prospectus as 32 Avenue of the Americas secures (i) a Mortgage Loan evidenced by a promissory note designated as Note A-4, with an outstanding principal balance as of the Cut-off Date of $70,000,000 (the “32 Avenue of the Americas Mortgage Loan”), representing approximately 7.3% of the Initial Outstanding Pool Balance, (ii) three promissory notes designated as Note A-1, Note A-2 and Note A-3, with an aggregate outstanding principal balance as of the Cut-off Date of $297,500,000, which are currently held by JPMorgan Chase Bank, National Association or an affiliate, and (iii) a promissory note designated as Note A-5 (together with the Note A-1, Note A-2 and Note A-3, the “32 Avenue of the Americas Companion Loans”), with an outstanding principal balance as of the Cut-off Date of $57,500,000, which is currently held by GACC or an affiliate. The 32 Avenue of the Americas Mortgage Loan and the 32 Avenue of the Americas Companion Loans arepari passu in right of payment and are collectively referred to herein as the “32 Avenue of the Americas Loan Combination”.

The 32 Avenue of the Americas Loan Combination will be serviced pursuant to the COMM 2015-LC23 pooling and servicing agreement and the related intercreditor agreement. After the 32 Avenue of the Americas Note A-1 Securitization Date (as defined below), the 32 Avenue of the Americas Loan Combination will be serviced pursuant to the 32 Avenue of the Americas pooling and servicing agreement and the related intercreditor agreement. For additional information regarding the 32 Avenue of the Americas Loan Combination, see “Description of the Mortgage Pool—Loan Combinations—32 Avenue of the Americas Loan Combination” in the Free Writing Prospectus.

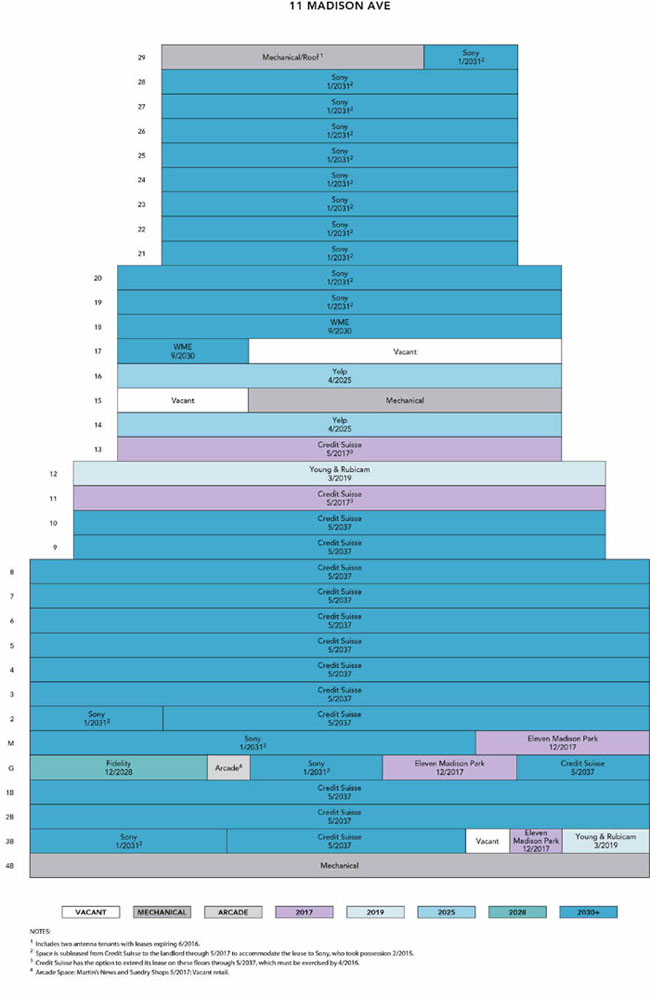

The Mortgaged Property identified on Annex A–1 to the Free Writing Prospectus as 11 Madison Avenue secures (i) a Mortgage Loan evidenced by a promissory note designated as Note A-1-C3, with an outstanding principal balance as of the Cut-off Date of $69,600,000 (the “11 Madison Avenue Mortgage Loan”), representing approximately 7.2% of the Initial Outstanding Pool Balance, (ii) nine pari passu promissory notes designated as Note A-1-S1, Note A-1-S2, Note A-1-S3, Note A-2-S1, Note A-2-S2, Note A-2-S3, Note A-3-S1, Note A-3-S2 and Note A-3-S3, respectively, having an aggregate outstanding principal balance as of the Cut-off Date of $397,530,000 (the “11 Madison Avenue Standalone Pari Passu Companion Loans”), each of which is generally pari passu in right of payment with the 11 Madison Avenue Mortgage Loan and the 11 Madison Avenue Non-Standalone Pari Passu Companion Loans (as defined below); (iii) six pari passu promissory notes designated as Note A-1-C1, Note A-1-C2, Note A-2-C1, Note A-2-C2, Note A-3-C1 and Note A-3-C2, respectively, having an aggregate outstanding principal balance as of the Cut-off Date of $297,200,000 (the “11 Madison Avenue Non-Standalone Pari Passu Companion Loans” and, together with the 11 Madison Avenue Standalone Pari Passu Companion Loans, the “11 Madison Avenue Pari Passu Companion Loans”), each of which is generally pari passu in right of payment with the 11 Madison Avenue Mortgage Loan and the 11 Madison Avenue Standalone Pari Passu Companion Loans; and (iv) three promissory notes designated as Note B-1-S, Note B-2-S and

|

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. 9 |

COMM 2015-LC23 Mortgage Trust

| STRUCTURE OVERVIEW |

Note B-3-S, respectively, with an aggregate outstanding principal balance as of the Cut-off Date of $310,670,000 (collectively, the “11 Madison Avenue Subordinate Companion Loans” and, together with the 11 Madison Avenue Pari Passu Companion Loans, the “11 Madison Avenue Companion Loans”), which are subordinate in right of payment in respect of each of the 11 Madison Avenue Mortgage Loan and the 11 Madison Avenue Pari Passu Companion Loans. The 11 Madison Avenue Standalone Pari Passu Companion Loans and the 11 Madison Avenue Subordinate Companion Loans are collectively referred to as the “11 Madison Avenue Standalone Companion Loans”.

The 11 Madison Avenue Subordinate Companion Loans, together with the 11 Madison Avenue Mortgage Loan and the 11 Madison Avenue Pari Passu Companion Loans, are referred to as the “11 Madison Avenue Loan Combination”. Only the 11 Madison Avenue Mortgage Loan is included in the Issuing Entity. Each of the 11 Madison Avenue Standalone Pari Passu Companion Loans and 11 Madison Avenue Subordinate Companion Loans was included in the MAD 2015-11MD Mortgage Trust. The 11 Madison Avenue Non-Standalone Pari Passu Companion Loans are currently being held as follows: (i) Note A-1-C1 and Note A-1-C2 were included in the COMM 2015-CCRE26 Mortgage Trust and the COMM 2015-CCRE27 Mortgage Trust, respectively, (ii) Note A-2-C1 and Note A-2-C2 are currently being held by Morgan Stanley Bank, N.A., (iii) Note A-3-C1 is included in the WFCM 2015-NXS3 Mortgage Trust and (iv) Note A-3-C2 is currently being held by Wells Fargo Bank, National Association.

The 11 Madison Avenue Loan Combination is being serviced pursuant to the MAD 2015-11MD pooling and servicing agreement and the related intercreditor agreement. For additional information regarding the 11 Madison Avenue Loan Combination, see“Description of the Mortgage Pool—Loan Combinations—11 Madison Avenue Loan Combination”in the Free Writing Prospectus.

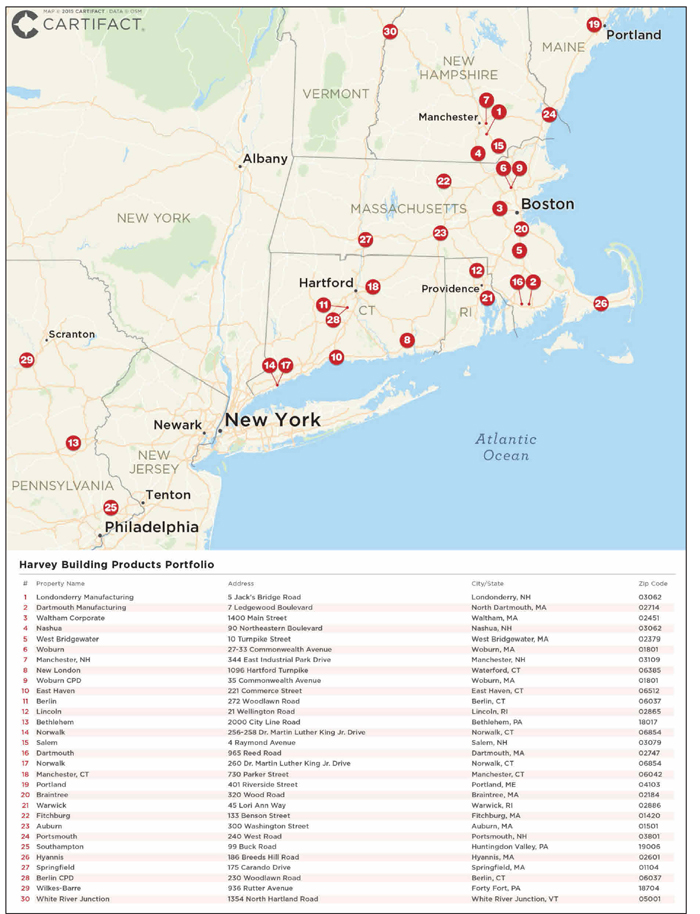

The portfolio of mortgaged properties identified on Annex A-1 to the Free Writing Prospectus as Harvey Building Products Portfolio secures (i) a Mortgage Loan evidenced by a promissory note designated as Note A-1 with an outstanding principal balance as of the Cut-off Date of $41,953,178 (the “Harvey Building Products Portfolio Mortgage Loan”), representing approximately 4.4% of the Initial Outstanding Pool Balance, and (ii) two promissory notes designated as Note A-2 and Note A-3 (collectively, “Harvey Building Products Companion Loans”), with an aggregate outstanding principal balance as of the Cut-off Date of $67,925,164, which are currently held by LCF or an affiliate. The 32 Harvey Building Products Portfolio Mortgage Loan and the Harvey Building Products Portfolio Companion Loans arepari passu in right of payment and are collectively referred to herein as the “Harvey Building Products Portfolio Loan Combination”.

The Harvey Building Products Portfolio Loan Combination will be serviced pursuant to the COMM 2015-LC23 pooling and servicing agreement and the related intercreditor agreement. For additional information regarding the Harvey Building Products Portfolio Loan Combination, see “Description of the Mortgage Pool—Loan Combinations—Harvey Building Products Portfolio Loan Combination” in the Free Writing Prospectus.

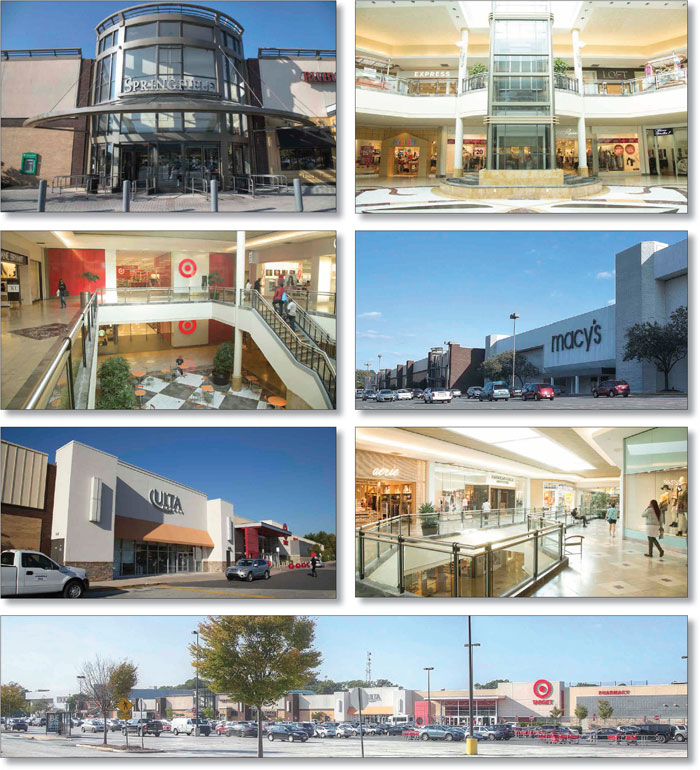

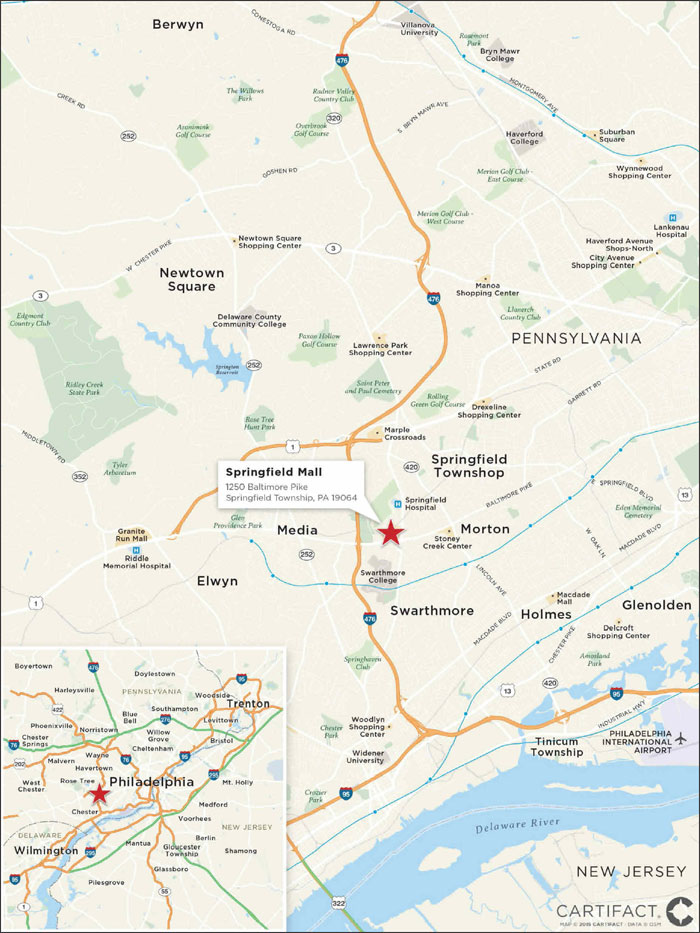

The Mortgaged Property identified on Annex A-1 to the Free Writing Prospectus as Springfield Mall secures (i) a Mortgage Loan evidenced by a promissory note designated as Note A-1 with an outstanding principal balance as of the Cut-off Date of $32,460,817 (the “Springfield Mall Mortgage Loan”), representing approximately 3.4% of the Initial Outstanding Pool Balance and (ii) a promissory note designated as Note A-2 (the “Springfield Mall Companion Loan”), with an outstanding principal balance as of the Cut-off Date of $32,460,817, which is currently held by CCRE or an affiliate. The Springfield Mall Mortgage Loan and the Springfield Mall Companion Loan arepari passu in right of payment and are collectively referred to herein as the “Springfield Mall Loan Combination”.

The Springfield Mall Loan Combination will be serviced pursuant to the COMM 2015-LC23 pooling and servicing agreement and the related intercreditor agreement. For additional information regarding the Springfield Mall Loan Combination, see “Description of the Mortgage Pool—Loan Combinations—Springfield Mall Loan Combination” in the Free Writing Prospectus.

| |

| The Mortgaged Property identified as 40 Wall Street on Annex A-1 to the Free Writing Prospectus secures (i) a promissory note designated as Note A-1-B (the “40 Wall Street |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. 10 |

COMM 2015-LC23 Mortgage Trust

| STRUCTURE OVERVIEW |

| Mortgage Loan”), with an outstanding principal balance as of the Cut-off Date of $4,960,524, representing approximately 0.5% of Initial Outstanding Pool Balance, (ii) two promissory notes designated as Note A-1-A and Note A-2, with an aggregate outstanding principal balance as of the cut-off date of $94,249,948, which is included in the WFCM 2015-LC22 Mortgage Trust, and (iii) a promissory note designated as Note A-3 (together with Note A-1-A and Note A-2, the “40 Wall Street Companion Loans”), with an outstanding principal balance as of the cut-off date of $59,526,283, which is included in the COMM 2015-CCRE24 Mortgage Trust. The 40 Wall Street Mortgage Loan and the 40 Wall Street Companion Loansare pari passu in right of payment and are collectively referred to as the “40 Wall Street Loan Combination”. | |

The 40 Wall Street Loan Combination is being serviced pursuant to the WFCM 2015-LC22 pooling and servicing agreement and the related intercreditor agreement. For additional information regarding the 40 Wall Street loan combination, see “Description of the Mortgage Pool—Loan Combinations—40 Wall Street Loan Combination” in the Free Writing Prospectus.

Each of the Equity Inns Portfolio Loan Combination, the Harvey Building Products Portfolio Loan Combination and the Springfield Mall Loan Combination is referred to as a “Serviced Loan Combination”.

Each of the 11 Madison Mortgage Loan and 40 Wall Street Mortgage Loan is referred to as a “Non-Serviced Mortgage Loan”. Each of the 11 Madison Loan Combination and 40 Wall Street Loan Combination is referred to as a “Non-Serviced Loan Combination”.

The 32 Avenue of the Americas Mortgage Loan is referred to as a “Servicing Shift Mortgage Loan”, and the 32 Avenue of the Americas Loan Combination is referred to as a “Servicing Shift Loan Combination”. Prior to the applicable securitization date (the “32 Avenue of the Americas Note A-1 Securitization Date”), the 32 Avenue of the Americas Loan Combination is referred to as a “Serviced Loan Combination”. On and after the 32 Avenue of the Americas Note A-1 Securitization Date, the 32 Avenue of the Americas Mortgage Loan will be a “Non-Serviced Mortgage Loan” and the 32 Avenue of the Americas Loan Combination will be a “Non-Serviced Loan Combination”.

| |

| Control Rights and Directing Holder: | Controlling Class Certificateholders will have certain control rights over servicing matters with respect to each Mortgage Loan (other than Non-Serviced Mortgage Loans and Servicing Shift Mortgage Loans) and Serviced Loan Combinations (other than Servicing Shift Loan Combinations). The majority owner or appointed representative of the Class of Control Eligible Certificates that is the Controlling Class (such owner or representative, the “Directing Holder”), will be entitled to direct the Special Servicer to take, or refrain from taking certain actions with respect to a Mortgage Loan (other than Non-Serviced Mortgage Loans and Servicing Shift Mortgage Loans) and Serviced Loan Combinations (other than Servicing Shift Loan Combinations). Furthermore, the Directing Holder will also have the right to receive notice and consent to certain material actions that the Master Servicer and the Special Servicer proposes to take with respect to such Mortgage Loan (other than Non-Serviced Mortgage Loans and Servicing Shift Mortgage Loans) and Serviced Loan Combinations (other than Servicing Shift Loan Combinations).

It is expected that LNR Securities Holdings, LLC or its affiliate will be the initial Directing Holder with respect to each Mortgage Loan (other than Non-Serviced Mortgage Loans and Servicing Shift Mortgage Loans) and Serviced Loan Combination (other than Servicing Shift Loan Combinations).

For a description of the directing holder for each Non-Serviced Loan Combination and Servicing Shift Loan Combination, see“Description of the Mortgage Pool—Loan Combinations” and “Description of the Pooling and Servicing Agreement—The Directing Holder”in theFree Writing Prospectus.

|

| Control Eligible Certificates: | Class F, Class G, Class H and Class J Certificates.

|

| Controlling Class: | The Controlling Class will be the most subordinate Class of Control Eligible Certificates then outstanding that has an aggregate Certificate Balance, as notionally reduced by any Appraisal Reduction Amounts allocable to such Class, equal to no less than 25% of the initial Certificate Balance of such Class; provided that if at any time the Certificate Balances of the Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class A-M, Class B, Class C, Class D and Class E have been reduced to zero as a result of the allocation of principal payments on the |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. 11 |

COMM 2015-LC23 Mortgage Trust

| STRUCTURE OVERVIEW |

Mortgage Loans, then the “Controlling Class” will be the most subordinate Class of Control Eligible Certificates that has an aggregate Certificate Balance greater than zero without regard to the application of Appraisal Reduction Amounts to notionally reduce the Certificate Balance of such Class.

The Controlling Class as of the Settlement Date will be the Class J Certificates.

| |

| Appraised-Out Class: | Any Class of Control Eligible Certificates that has been determined, as a result of Appraisal Reductions Amounts allocable to such Class, to no longer be the Controlling Class.

|

| Remedies Available to Holders of an Appraised-Out Class: | Holders of the majority of any Class of Control Eligible Certificates that is determined at any time of determination to no longer be the Controlling Class as a result of an allocation of an Appraisal Reduction Amounts in respect of such Class will have the right, at their sole expense, to require the Special Servicer to order a second appraisal for any Mortgage Loan (other than Non-Serviced Mortgage Loans) for which an Appraisal Reduction Event has occurred. Upon receipt of the second appraisal, the Special Servicer will be required to determine, in accordance with the Servicing Standard, whether, based on its assessment of the second appraisal, a recalculation of the Appraisal Reduction Amount is warranted. If warranted, the Special Servicer will direct the Master Servicer to recalculate the Appraisal Reduction Amount based on the second appraisal, and if required by such recalculation, the Special Servicer will reinstate the Appraised-Out Class as the Controlling Class. The Holders of an Appraised-Out Class requesting a second appraisal will not be entitled to exercise any rights of the Controlling Class until such time, if any, as the Class is reinstated as the Controlling Class.

|

| Control Termination Event: | Will occur with respect to any Mortgage Loan (other than the Non-Serviced Mortgage Loans and Servicing Shift Mortgage Loans) or Serviced Loan Combination (other than Servicing Shift Loan Combinations) when no Class of Control Eligible Certificates has an aggregate Certificate Balance (as notionally or actually reduced by any Appraisal Reduction Amounts and Realized Losses) equal to or greater than 25% of the initial Certificate Balance of such Class (subject to “—Controlling Class” above).

Upon the occurrence and the continuance of a Control Termination Event, the Directing Holder will no longer have any Control Rights. The Directing Holder will no longer have the right to direct certain actions of the Special Servicer and will no longer have consent rights with respect to certain material actions that the Master Servicer or Special Servicer proposes to take with respect to a Mortgage Loan (other than the Non-Serviced Mortgage Loans and Servicing Shift Mortgage Loans).

Upon the occurrence and continuation of a Control Termination Event, the Directing Holder will retain non-binding consultation rights with respect to certain material actions that the Special Servicer proposes to take with respect to a Mortgage Loan (other than the Non-Serviced Mortgage Loans and Servicing Shift Mortgage Loans) and Serviced Loan Combinations (other than Servicing Shift Loan Combinations). Such consultation rights will continue until the occurrence of a Consultation Termination Event.

|

| Consultation Termination Event: | Will occur with respect to any Mortgage Loan (other than the Non-Serviced Mortgage Loans and Servicing Shift Mortgage Loans) and Serviced Loan Combinations (other than Servicing Shift Loan Combinations) when, without giving regard to the application of any Appraisal Reduction Amounts (i.e., giving effect to principal reduction through Realized Losses only), there is no Class of Control Eligible Certificates that has an aggregate Certificate Balance equal to 25% or more of the initial Certificate Balance of such Class (subject to “—Controlling Class” above).

Upon the occurrence and continuance of a Consultation Termination Event, the Directing Holder will have no rights under the Pooling and Servicing Agreement other than those rights that all Certificateholders have.

|

| Appointment and Replacement of Special Servicer: | The Directing Holder will appoint the initial Special Servicer with respect to each Mortgage Loan (other than the Non-Serviced Mortgage Loans and Servicing Shift Mortgage Loans) and each Serviced Loan Combination (other than Servicing Shift Loan Combinations) as of the Settlement Date. Prior to the occurrence and continuance of a Control Termination Event, the Directing Holder generally may replace the Special Servicer with respect to each Mortgage Loan (other than the Non-Serviced Mortgage Loans and Servicing Shift Mortgage Loans) and |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. 12 |

COMM 2015-LC23 Mortgage Trust

| STRUCTURE OVERVIEW |

each Serviced Loan Combination (other than Servicing Shift Loan Combinations) with or without cause at any time.

Upon the occurrence and during the continuance of a Control Termination Event, the Directing Holder will no longer have the right to replace the Special Servicer and such replacement (other than with respect to the Non-Serviced Loan Combinations and Servicing Shift Loan Combinations) will occur based on a vote of holders of all voting eligible Classes of Certificates as described below. See“Description of the Mortgage Pool—Loan Combinations” and “Description of the Pooling and Servicing Agreement”in theFree Writing Prospectus for a description of the special servicer appointment and replacement rights with respect to Non-Serviced Loan Combinations and Servicing Shift Loan Combinations. | |

| Replacement of Special Servicer by Vote of Certificateholders: | Other than with respect to Non-Serviced Loan Combinations and Servicing Shift Loan Combinations, if a Control Termination Event has occurred and is continuing, upon (i) the written direction of holders of Certificates evidencing not less than 25% of the voting rights of all Classes of Certificates entitled to principal (taking into account the application of Appraisal Reduction Amounts to notionally reduce the Certificate Balances of Classes to which such Appraisal Reduction Amounts are allocable) requesting a vote to replace the Special Servicer with a replacement Special Servicer, (ii) payment by such requesting holders to the Certificate Administrator of all reasonable fees and expenses to be incurred by the Certificate Administrator in connection with administering such vote and (iii) delivery by such holders to the Certificate Administrator of written confirmations from each Rating Agency that the appointment of the replacement Special Servicer will not result in a downgrade of the Certificates, the Certificate Administrator will be required to promptly provide written notice to all certificateholders of such request and conduct the solicitation of votes of all Certificates in such regard. Upon the written direction (within 180 days) of (i) Holders of at least 75% of a Certificateholder Quorum or (ii) the Holders of more than 50% of the voting rights of each Class of Non-Reduced Certificates, the Trustee will immediately replace the Special Servicer with the replacement Special Servicer (other than with respect to Non-Serviced Loan Combinations and Servicing Shift Loan Combinations).

“Certificateholder Quorum” means, in connection with any solicitation of votes in connection with the replacement of the Special Servicer as described above, the holders of Certificates evidencing at least 75% of the aggregate voting rights (taking into account Realized Losses and the application of any Appraisal Reduction Amounts to notionally reduce the Certificate Balance of the Certificates) of all classes of Certificates entitled to principal, on an aggregate basis.

In addition, after the occurrence of a Consultation Termination Event, if the Operating Advisor determines that the Special Servicer is not performing its duties in accordance with the Servicing Standard, the Operating Advisor will have the right to recommend the replacement of the Special Servicer (other than with respect to Non-Serviced Loan Combinations and Servicing Shift Loan Combinations). The Operating Advisor’s recommendation to replace the Special Servicer (other than with respect Non-Serviced Loan Combinations and Servicing Shift Loan Combinations) must be confirmed by a majority of the voting rights of all Classes of Certificates entitled to principal (taking into account the application of Appraisal Reduction Amounts to notionally reduce the Certificate Balances of Classes to which such Appraisal Reduction Amounts are allocable) within 180 days from the time such recommendation is posted to the Certificate Administrator website and is subject to the receipt of written confirmations from each Rating Agency that the appointment of the replacement Special Servicer will not result in a downgrade of the Certificates.

See“Description of the Mortgage Pool—Loan Combinations”and “Description of the Pooling and Servicing Agreement”in theFree Writing Prospectus for a description of the special servicer appointment and replacement rights with respect to Non-Serviced Loan Combinations and Servicing Shift Loan Combinations.

|

| Cap on Workout and Liquidation Fees: | The workout fees and liquidation fees payable to a Special Servicer under the Pooling and Servicing Agreement will be an amount equal to the lesser of: (1) 1.0% of each collection of interest and principal following a workout or liquidation and (2) $1,000,000 per workout or liquidation. All Modification Fees actually paid to the Special Servicer in connection with a workout or liquidation or in connection with any prior workout or partial liquidation that occurred within the prior 18 months will be deducted from the total workout and/or liquidation fees payable (other than Modification Fees earned while the Mortgage Loan was not in special |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. 13 |

COMM 2015-LC23 Mortgage Trust

| STRUCTURE OVERVIEW |

| servicing). In addition, the total amount of workout and liquidation fees actually payable by the Trust under the Pooling and Servicing Agreement will be capped in the aggregate at $1,000,000 for each related Mortgage Loan. If a new special servicer begins servicing the related Mortgage Loan, all amounts paid to the prior special servicer will be disregarded for purposes of calculating the cap. | |

| Special Servicer Compensation: | The special servicing fee will equal the greater of (i) 0.25%per annum and (ii) the rate that would result in a special servicing fee of $1,000 for the related month of the stated principal balance of the related specially serviced loan or REO property, as applicable. The Special Servicer and its affiliates will be prohibited from receiving or retaining any compensation or any other remuneration under the Pooling and Servicing Agreement (including in the form of commissions, brokerage fees, rebates, or as a result of any other fee-sharing arrangement) from any person (including the issuing entity, any borrower, any manager, any guarantor or indemnitor in respect of a Mortgage Loan or Serviced Loan Combination, if any, and any purchaser of any Mortgage Loan, Serviced Companion Loan or REO Property) in connection with the disposition, workout or foreclosure of any Mortgage Loan or Serviced Loan Combination, the management or disposition of any REO Property, or the performance of any other special servicing duties under the Pooling and Servicing Agreement, other than as expressly permitted in the Pooling and Servicing Agreement and other than commercially reasonable treasury management fees, banking fees and insurance commissions or fees received or retained by the Special Servicer or any of its Affiliates in connection with any services performed by such party with respect to any mortgage loan. Subject to certain limited exceptions, the Special Servicer will also be required to report any compensation or other remuneration the Special Servicer or its affiliates have received from any person and such information will be disclosed in the Certificateholders’ monthly distribution date statement. |

| Operating Advisor: | With respect to the Mortgage Loans (other than with respect to Non-Serviced Loan Combinations and Servicing Shift Loan Combinations) and prior to the occurrence of a Control Termination Event, the Operating Advisor will have access to any final asset status report and all information available with respect to the transaction on the Certificate Administrator’s website but will not have any approval or consultation rights. After the occurrence and during the continuance of a Control Termination Event, the Operating Advisor will have consultation rights with respect to certain major decisions and will have additional monitoring responsibilities on behalf of the entire trust. |

| The Operating Advisor will be subject to termination if holders of at least 15% of the aggregate voting rights of the Certificates (in connection with termination and replacement relating to the Mortgage Loans) vote to terminate and replace the Operating Advisor and such vote is approved by holders of more than 50% of the applicable voting rights that exercise their right to vote, provided that holders of at least 50% of the applicable voting rights have exercised their right to vote. The holders initiating such vote will be responsible for the fees and expenses in connection with the vote and replacement. | |

| The Operating Advisor will not have consultation rights in respect of Non-Serviced Loan Combinations and Servicing Shift Loan Combinations. | |

| Liquidated Loan Waterfall: | On liquidation of any Mortgage Loan, all net liquidation proceeds will be applied so that amounts allocated as a recovery of accrued and unpaid interest will not, in the first instance, include any amount by which the interest portion of P&I Advances previously made was reduced as a result of Appraisal Reduction Amounts. After the adjusted interest amount is so allocated, any remaining net liquidation proceeds will be allocated to pay principal on the Mortgage Loan until the unpaid principal amount of the Mortgage Loan has been reduced to zero. Any remaining liquidation proceeds would then be allocated as a recovery of accrued and unpaid interest corresponding to the amount by which the interest portion of P&I Advances previously made was reduced as a result of Appraisal Reduction Amounts. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. 14 |

COMM 2015-LC23 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Distribution of Cut-off Date Balances(1) |

| Range of Cut-off Date Balances | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Pool | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(2)(3) | Maturity Date or ARD LTV(2)(3) | ||||||

| $702,000 | - | $7,499,999 | 28 | $111,472,819 | 11.6% | 4.7221% | 117 | 1.54x | 65.3% | 51.6% |

| $7,500,000 | - | $14,999,999 | 14 | $149,198,164 | 15.5% | 4.6503% | 119 | 1.51x | 65.7% | 57.2% |

| $15,000,000 | - | $24,999,999 | 9 | $182,233,997 | 19.0% | 4.8435% | 105 | 1.46x | 68.0% | 61.1% |

| $25,000,000 | - | $49,999,999 | 8 | $298,407,168 | 31.1% | 4.6816% | 101 | 1.67x | 61.8% | 54.8% |

| $50,000,000 | - | $74,999,999 | 2 | $139,600,000 | 14.5% | 4.1979% | 119 | 2.88x | 43.9% | 43.9% |

| $75,000,000 | - | $80,000,000 | 1 | $80,000,000 | 8.3% | 4.9600% | 59 | 2.35x | 64.4% | 64.4% |

| Total/Weighted Average | 62 | $960,912,147 | 100.0% | 4.6650% | 105 | 1.82x | 61.6% | 55.2% | ||

Distribution of Mortgage Rates(1) |

| Range of Mortgage Rates | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(2)(3) | Maturity Date or ARD LTV(2)(3) | ||||||

| 3.5602% | - | 4.4999% | 13 | $235,547,156 | 24.5% | 4.1204% | 118 | 2.37x | 51.4% | 45.3% |

| 4.5000% | - | 4.7499% | 18 | $231,989,828 | 24.1% | 4.6214% | 107 | 1.51x | 66.8% | 59.7% |

| 4.7500% | - | 5.3380% | 31 | $493,375,163 | 51.3% | 4.9456% | 99 | 1.70x | 64.0% | 57.8% |

| Total/Weighted Average | 62 | $960,912,147 | 100.0% | 4.6650% | 105 | 1.82x | 61.6% | 55.2% | ||

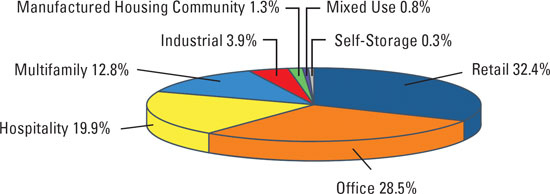

Property Type Distribution(1)(4) |

| Property Type | Number of Mortgaged Properties | Aggregate Date Balance | % of Initial Outstanding Pool Balance | Number of Beds/Rooms/ Pads/Units/ NRA | Weighted Averages | ||||||

Cut-off Date Unit/NRA | Mortgage Rate | Stated Term | Occupancy | U/W NCF DSCR | Cut-off Ratio(2)(3) | Maturity Date or ARD LTV(2)(3) | |||||

| Retail | 30 | $311,283,850 | 32.4% | 2,040,752 | $253 | 4.6312% | 114 | 94.8% | 1.51x | 65.4% | 56.2% |

| Anchored(5) | 21 | $225,381,127 | 23.5% | 1,662,992 | $244 | 4.7197% | 113 | 94.6% | 1.48x | 67.1% | 58.6% |

| Unanchored | 9 | $85,902,723 | 8.9% | 377,760 | $278 | 4.3990% | 118 | 95.2% | 1.57x | 61.1% | 49.9% |

| Office | 18 | $273,595,382 | 28.5% | 5,219,507 | $391 | 4.3636% | 118 | 96.9% | 2.30x | 52.7% | 49.0% |

| CBD | 4 | $163,539,209 | 17.0% | 4,696,306 | $329 | 4.2478% | 119 | 98.7% | 2.67x | 46.2% | 44.5% |

| Suburban | 12 | $64,696,510 | 6.7% | 364,747 | $621 | 4.5143% | 114 | 96.6% | 1.61x | 61.8% | 50.6% |

| Medical | 2 | $45,359,663 | 4.7% | 158,454 | $288 | 4.5663% | 118 | 91.0% | 1.92x | 63.5% | 62.7% |

| Hospitality | 27 | $191,255,094 | 19.9% | 3,553 | $135,410 | 4.9807% | 94 | 75.2% | 1.91x | 64.3% | 57.4% |

| Full Service | 3 | $95,944,447 | 10.0% | 676 | $159,758 | 4.9837% | 119 | 73.0% | 1.55x | 64.5% | 53.8% |

| Limited Service | 13 | $45,845,129 | 4.8% | 1,438 | $84,992 | 4.9967% | 79 | 76.2% | 2.18x | 63.9% | 57.4% |

| Extended Stay | 6 | $31,310,345 | 3.3% | 784 | $164,105 | 4.9600% | 59 | 83.6% | 2.35x | 64.4% | 64.4% |

| Select Service | 5 | $18,155,172 | 1.9% | 655 | $84,564 | 4.9600% | 59 | 70.1% | 2.35x | 64.4% | 64.4% |

| Multifamily | 9 | $123,068,650 | 12.8% | 1,661 | $175,575 | 4.8713% | 86 | 97.7% | 1.44x | 68.8% | 64.5% |

| Industrial | 29 | $37,804,168 | 3.9% | 1,991,719 | $51 | 4.8500% | 59 | 100.0% | 1.96x | 53.5% | 49.3% |

| Manufactured Housing Community | 4 | $12,955,800 | 1.3% | 341 | $40,152 | 4.4831% | 119 | 98.1% | 1.74x | 64.4% | 57.1% |

| Mixed Use | 2 | $7,949,204 | 0.8% | 87,664 | $128 | 4.8385% | 119 | 86.5% | 1.31x | 68.0% | 55.7% |

| Office/Retail | 2 | $7,949,204 | 0.8% | 87,664 | $128 | 4.8385% | 119 | 86.5% | 1.31x | 68.0% | 55.7% |

| Self-Storage | 1 | $3,000,000 | 0.3% | 12,060 | $249 | 5.0800% | 119 | 85.6% | 1.57x | 73.2% | 63.4% |

| Total/Weighted Average | 120 | $960,912,147 | 100.0% | 4.6650% | 105 | 92.0% | 1.82x | 61.6% | 55.2% | ||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 15 |

COMM 2015-LC23 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Geographic Distribution(1)(4) |

| State/Location | Number of Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||

| Mortgage Rate | Stated Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(2)(3) | Maturity Date or ARD LTV(2)(3) | ||||

| California | 14 | $254,575,194 | 26.5% | 4.5703% | 112 | 1.59x | 62.8% | 55.9% |

| Southern(6) | 12 | $197,660,680 | 20.6% | 4.6167% | 111 | 1.56x | 64.0% | 56.9% |

| Northern(6) | 2 | $56,914,514 | 5.9% | 4.4092% | 119 | 1.69x | 58.6% | 52.4% |

| New York | 7 | $199,074,357 | 20.7% | 4.3316% | 105 | 2.48x | 51.3% | 50.4% |

| New York City | 4 | $190,560,524 | 19.8% | 4.3113% | 104 | 2.52x | 50.4% | 50.1% |

| Remaining New York State | 3 | $8,513,833 | 0.9% | 4.7875% | 119 | 1.43x | 71.2% | 56.0% |

| Texas | 11 | $85,658,646 | 8.9% | 4.7394% | 110 | 1.67x | 66.7% | 55.1% |

| Illinois | 12 | $65,871,854 | 6.9% | 4.8663% | 112 | 1.58x | 61.9% | 50.2% |

| Pennsylvania | 6 | $64,902,201 | 6.8% | 4.7012% | 117 | 1.54x | 64.0% | 54.4% |

| Other | 70 | $290,829,896 | 30.3% | 4.9006% | 94 | 1.74x | 65.5% | 59.2% |

| Total/Weighted Average | 120 | $960,912,147 | 100.0% | 4.6650% | 105 | 1.82x | 61.6% | 55.2% |

Distribution of Cut-off Date LTV Ratios(1)(2)(3) |

| Range of Cut-off Date LTV Ratios | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term(Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio | Maturity Date or ARD LTV | ||||||

| 29.4% | - | 54.9% | 6 | $168,455,190 | 17.5% | 4.2414% | 103 | 2.69x | 43.5% | 38.9% |

| 55.0% | - | 59.9% | 9 | $183,970,181 | 19.1% | 4.6143% | 119 | 1.74x | 56.7% | 51.1% |

| 60.0% | - | 64.9% | 8 | $212,257,755 | 22.1% | 4.7763% | 90 | 1.94x | 63.2% | 60.6% |

| 65.0% | - | 69.9% | 15 | $142,823,344 | 14.9% | 4.8186% | 119 | 1.41x | 67.6% | 55.8% |

| 70.0% | - | 74.9% | 23 | $241,780,678 | 25.2% | 4.8044% | 101 | 1.45x | 72.3% | 64.1% |

| 75.0% | - | 75.0% | 1 | $11,625,000 | 1.2% | 4.7905% | 119 | 1.36x | 75.0% | 66.1% |

| Total/Weighted Average | 62 | $960,912,147 | 100.0% | 4.6650% | 105 | 1.82x | 61.6% | 55.2% | ||

Distribution of Maturity Date or ARD LTV Ratios(1)(2)(3) |

Range of LTV Ratios at Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | StatedRemaining Term(Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio | Maturity Date or ARD LTV | ||||||

| 21.1% | - | 49.9% | 18 | $295,899,190 | 30.8% | 4.3613% | 110 | 2.21x | 50.5% | 41.8% |

| 50.0% | - | 54.9% | 4 | $31,218,715 | 3.2% | 4.4033% | 118 | 1.58x | 61.4% | 53.3% |

| 55.0% | - | 59.9% | 18 | $261,914,921 | 27.3% | 4.7547% | 119 | 1.54x | 64.9% | 56.7% |

| 60.0% | - | 64.9% | 10 | $252,210,821 | 26.2% | 4.8793% | 95 | 1.88x | 66.2% | 62.9% |

| 65.0% | - | 72.3% | 12 | $119,668,500 | 12.5% | 4.8367% | 84 | 1.41x | 72.1% | 69.3% |

| Total/Weighted Average | 62 | $960,912,147 | 100.0% | 4.6650% | 105 | 1.82x | 61.6% | 55.2% | ||

Distribution of Underwritten NCF Debt Service Coverage Ratios(1) |

| Range of Underwritten NCF Debt Service Coverage Ratios | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(2)(3) | Maturity Date or ARD LTV(2)(3) | ||||||

| 1.13x | - | 1.39x | 23 | $232,088,778 | 24.2% | 4.7874% | 112 | 1.30x | 68.9% | 58.0% |

| 1.40x | - | 1.44x | 2 | $27,231,741 | 2.8% | 4.8125% | 119 | 1.42x | 67.3% | 57.4% |

| 1.45x | - | 1.54x | 8 | $131,926,281 | 13.7% | 4.8885% | 88 | 1.50x | 64.9% | 58.0% |

| 1.55x | - | 1.99x | 24 | $397,116,433 | 41.3% | 4.6743% | 113 | 1.77x | 61.4% | 55.7% |

| 2.00x | - | 2.49x | 4 | $102,948,914 | 10.7% | 4.7752% | 72 | 2.32x | 59.9% | 58.0% |

| 2.50x | - | 3.89x | 1 | $69,600,000 | 7.2% | 3.5602% | 118 | 3.89x | 32.5% | 32.5% |

| Total/Weighted Average | 62 | $960,912,147 | 100.0% | 4.6650% | 105 | 1.82x | 61.6% | 55.2% | ||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 16 |

COMM 2015-LC23 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Original Terms to Maturity or ARD(1) |

| Original Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||

| Mortgage Rate | Stated Remaining Term(Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(2)(3) | Maturity Date or ARD LTV(2)(3) | ||||

| 60 | 6 | $213,653,778 | 22.2% | 4.9297% | 59 | 1.89x | 64.5% | 63.3% |

| 120 | 56 | $747,258,370 | 77.8% | 4.5894% | 119 | 1.80x | 60.8% | 52.9% |

| Total/Weighted Average | 62 | $960,912,147 | 100.0% | 4.6650% | 105 | 1.82x | 61.6% | 55.2% |

Distribution of Remaining Terms to Maturity or ARD(1) |

| Range of Remaining Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | StatedRemaining Term(Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(2)(3) | Maturity Date or ARD LTV(2)(3) | ||||||

| 58 | - | 60 | 6 | $213,653,778 | 22.2% | 4.9297% | 59 | 1.89x | 64.5% | 63.3% |

| 112 | - | 117 | 4 | $30,818,002 | 3.2% | 4.2493% | 117 | 1.67x | 58.3% | 49.5% |

| 118 | - | 120 | 52 | $716,440,367 | 74.6% | 4.6040% | 119 | 1.81x | 60.9% | 53.0% |

| Total/Weighted Average | 62 | $960,912,147 | 100.0% | 4.6650% | 105 | 1.82x | 61.6% | 55.2% | ||

Distribution of Underwritten NOI Debt Yields(1) |

| Range of Underwritten NOI Debt Yields | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | StatedRemaining Term(Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(2)(3) | Maturity Date or ARD LTV(2)(3) | ||||||

| 7.1% | - | 8.9% | 23 | $290,963,657 | 30.3% | 4.7809% | 101 | 1.42x | 67.6% | 61.7% |

| 9.0% | - | 9.9% | 12 | $199,872,235 | 20.8% | 4.7444% | 119 | 1.68x | 63.3% | 57.7% |

| 10.0% | - | 12.4% | 18 | $238,886,538 | 24.9% | 4.6758% | 118 | 1.60x | 62.8% | 52.0% |

| 12.5% | - | 14.9% | 8 | $226,201,328 | 23.5% | 4.4291% | 86 | 2.70x | 51.1% | 48.5% |

| 15.0% | - | 18.4% | 1 | $4,988,391 | 0.5% | 4.9100% | 119 | 2.12x | 56.0% | 35.3% |

| Total/Weighted Average | 62 | $960,912,147 | 100.0% | 4.6650% | 105 | 1.82x | 61.6% | 55.2% | ||

Amortization Types(1) |

| Amortization Type | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||

| Mortgage Rate | StatedRemaining Term(Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(2)(3) | Maturity Date or ARD LTV(2)(3) | ||||

| Amortizing Balloon | 33 | $378,778,647 | 39.4% | 4.7003% | 112 | 1.53x | 62.5% | 50.2% |

| Interest Only | 9 | $367,990,000 | 38.3% | 4.5690% | 95 | 2.29x | 57.1% | 57.1% |

| Interest Only, then Amortizing | 15 | $209,840,000 | 21.8% | 4.7632% | 112 | 1.53x | 67.7% | 60.6% |

| Interest Only, ARD | 5 | $4,303,500 | 0.4% | 4.9840% | 119 | 1.73x | 69.2% | 69.2% |

| Total/Weighted Average | 62 | $960,912,147 | 100.0% | 4.6650% | 105 | 1.82x | 61.6% | 55.2% |

Footnotes:

| (1) | With respect to the Equity Inns Portfolio Mortgage Loan, 32 Avenue of Americas Mortgage Loan, 11 Madison Avenue Mortgage Loan, Harvey Building Products Portfolio Mortgage Loan, Springfield Mall Mortgage Loan and 40 Wall Street Mortgage Loan, the LTV, DSCR, Debt Yield and Cut-off Date Balance per Bed/Room/Pad/Unit/NRA calculations include the related pari passu companion loan(s), but not any related subordinate companion loan(s). |

| (2) | With respect to the Equity Inns Portfolio Mortgage Loan, representing 8.3% of the initial outstanding pool balance, the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated based on the portfolio appraised value, which attributes a premium to the aggregate value of the Equity Inns Portfolio Mortgaged Properties as a whole. For additional information, see the Footnotes to Annex A-1 in the Free Writing Prospectus. |

| (3) | With respect to 611 Cowper Mortgage Loan, representing 3.4% of the initial outstanding principal balance, the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated based on the “as stabilized” value. For additional information, see the Footnotes to Annex A-1 in the Free Writing Prospectus. |

| (4) | Reflects allocated loan amount for properties securing multi-property mortgage loans. |

| (5) | Anchored retail includes anchored, single tenant and urban properties. |

| (6) | Northern California properties have a zip code greater than 93600. Southern California properties have a zip code less than or equal to 93600. |