Wells Fargo Commercial Mortgage Trust 2015-P2

Filed: 2 Dec 15, 12:00am

| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-206677-01 | ||

|  |  |

Free Writing Prospectus

Structural and Collateral Term Sheet

$1,002,201,025

(Approximate Initial Pool Balance)

$860,640,000

(Approximate Aggregate Certificate Principal Balance of Offered Certificates)

Wells Fargo Commercial Mortgage Trust 2015-P2

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

Principal Commercial Capital

Ladder Capital Finance LLC

Citigroup Global Markets Realty Corp.

Wells Fargo Bank, National Association

Société Générale

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2015-P2

December 2, 2015

| WELLS FARGO SECURITIES | CITIGROUP | SOCIETE GENERALE |

| Co-Lead Manager and Joint Bookrunner | Co-Lead Manager and Joint Bookrunner | Co-Lead Manager and Joint Bookrunner |

Deutsche Bank Securities Co-Manager |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-206677) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Directive 2003/71/EC (as amended) and/or Part VI of the Financial Services and Markets Act 2000, as amended, or other offering document.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Wells Fargo Securities, LLC, Citigroup Global Markets Inc., SG Americas Securities, LLC, or Deutsche Bank Securities Inc., or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The information herein is preliminary and may be supplemented or amended prior to the time of sale. Prospective investors should understand that, when considering the purchase of the Offered Certificates, a contract of sale will come into being no sooner than the date on which the relevant class of certificates has been priced and the investor has otherwise taken all actions the investor must take to become committed to purchase the Offered Certificates, and the investor has therefore entered into a contract of sale. Any “indications of interest” expressed by any prospective investor, and any “soft circles” generated by the underwriters, prior to the time of sale, will not create binding contractual obligations for such prospective investors, on the one hand, or the underwriters, the depositor or any of their respective agents or affiliates, on the other hand.

In addition, the Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. As a result of the foregoing, a prospective investor may commit to purchase certificates that have characteristics that may change, and each prospective investor is advised that all or a portion of the certificates referred to in these materials may be issued without all or certain of the characteristics described in these materials. The underwriters’ obligation to sell certificates to any prospective investor is conditioned on the certificates and the transaction having the characteristics described in these materials. If the underwriters determine that a condition is not satisfied in any material respect, such prospective investor will be notified, and neither the depositor nor the underwriters will have any obligation to such prospective investor to deliver any portion of the Offered Certificates which such prospective investor has committed to purchase, and there will be no liability between the underwriters, the depositor or any of their respective agents or affiliates, on the one hand, and such prospective investor, on the other hand, as a consequence of the non-delivery.

The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 2 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Certificate Structure |

| I. | Certificate Structure |

| Class | Expected Ratings (Fitch/KBRA/Moody’s)(1) | Approximate Initial Certificate Principal Balance or Notional Amount(2) |

Approx. | Pass-Through Rate Description | Weighted Average Life (Years)(4) | Expected Principal Window(4) | Certificate Principal to Value Ratio(5) | Certificate Principal U/W NOI Debt Yield(6) | |||

| Offered Certificates | |||||||||||

| A-1 | AAAsf/AAA(sf)/Aaa(sf) | $28,655,000 | 30.000% | (7) | 2.90 | 1/16 – 10/20 | 44.0% | 14.6% | |||

| A-2A | AAAsf/AAA(sf)/Aaa(sf) | $70,000,000 | 30.000% | (7) | 4.86 | 10/20 – 12/20 | 44.0% | 14.6% | |||

| A-2B | AAAsf/AAA(sf)/Aaa(sf) | $82,513,000 | 30.000% | (7) | 4.98 | 12/20 – 12/20 | 44.0% | 14.6% | |||

| A-3 | AAAsf/AAA(sf)/Aaa(sf) | $170,000,000 | 30.000% | (7) | 9.73 | 8/25 – 10/25 | 44.0% | 14.6% | |||

| A-4 | AAAsf/AAA(sf)/Aaa(sf) | $292,790,000 | 30.000% | (7) | 9.90 | 10/25 – 12/25 | 44.0% | 14.6% | |||

| A-SB | AAAsf/AAA(sf)/Aaa(sf) | $57,582,000 | 30.000% | (7) | 7.45 | 12/20 – 8/25 | 44.0% | 14.6% | |||

| A-S | AAAsf/AAA(sf)/Aa1(sf) | $47,605,000 | 25.250% | (7) | 9.98 | 12/25 – 12/25 | 46.9% | 13.7% | |||

| X-A | AAAsf/AAA(sf)/NR | $749,145,000 | (8) | N/A | Variable(9) | N/A | N/A | N/A | N/A | ||

| X-B | AA-sf/AAA(sf)/NR | $61,385,000 | (10) | N/A | Variable(11) | N/A | N/A | N/A | N/A | ||

| B | AA-sf/AA-(sf)/A1(sf) | $61,385,000 | 19.125% | (7) | 9.98 | 12/25 – 12/25 | 50.8% | 12.7% | |||

| C | A-sf/A-(sf)/NR | $50,110,000 | 14.125% | (7) | 9.98 | 12/25 – 12/25 | 53.9% | 11.9% | |||

| Non-Offered Certificates | |||||||||||

| X-D | BBB-sf/BBB-(sf)/NR | $56,373,000 | (12) | N/A | Variable(13) | N/A | N/A | N/A | N/A | ||

| D | BBB-sf/BBB-(sf)/NR | $56,373,000 | 8.500% | (7) | 9.98 | 12/25 – 12/25 | 57.5% | 11.2% | |||

| E | BBsf/BB(sf)/NR | $22,550,000 | 6.250% | (7) | 9.98 | 12/25 – 12/25 | 58.9% | 10.9% | |||

| F | Bsf/B(sf)/NR | $11,275,000 | 5.125% | (7) | 9.98 | 12/25 – 12/25 | 59.6% | 10.8% | |||

| G | NR/NR/NR | $51,363,025 | 0.000% | (7) | 9.98 | 12/25 – 12/25 | 62.8% | 10.2% | |||

| Notes: | |||||||||||||||

| (1) | The expected ratings presented are those of Fitch Ratings, Inc. (“Fitch”), Kroll Bond Rating Agency, Inc. (“KBRA”) and Moody’s Investors Service, Inc. (“Moody’s”) which the depositor hired to rate the offered certificates. One or more other nationally recognized statistical rating organizations that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) or otherwise, to rate or provide market reports and/or published commentary related to the offered certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign or that its reports will not express differing, possibly negative, views of the mortgage loans and/or the offered certificates. The ratings of each class of offered certificates address the likelihood of the timely distribution of interest and, except in the case of the Class X-A and X-B certificates, the ultimate distribution of principal due on those classes on or before the Rated Final Distribution Date. See “Risk Factors—Other Risks Relating to the Certificates—Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded” and “Ratings” in the Preliminary Prospectus, expected to be dated December 2, 2015 (the “Preliminary Prospectus”). Fitch, KBRA and Moody’s have informed us that the “sf” designation in their ratings represents an identifier for structured finance product ratings. |

| (2) | The principal balances and notional amounts set forth in the table are approximate. The actual initial principal balances and notional amounts may be larger or smaller depending on the initial pool balance of the mortgage loans definitively included in the pool of mortgage loans, which aggregate cut-off date principal balance may be as much as 5% larger or smaller than the amount presented in the Preliminary Prospectus. |

| (3) | The approximate initial credit support with respect to the Class A-1, A-2A, A-2B, A-3, A-4 and A-SB Certificates represents the approximate credit enhancement for the Class A-1, A-2A, A-2B, A-3, A-4 and A-SB Certificates in the aggregate. |

| (4) | Weighted Average Lives and Expected Principal Windows are calculated based on an assumed prepayment rate of 0% CPR and the “Structuring Assumptions” described under “Yield and Maturity Considerations—Weighted Average Life” in the Preliminary Prospectus. |

| (5) | The Certificate Principal to Value Ratio for each Class of Certificates (other than the Class A-1, A-2A, A-2B, A-3, A-4 and A-SB Certificates) is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio for the mortgage loans and (b) a fraction, the numerator of which is the total initial Certificate Balance of such Class of Certificates and all Classes of Principal Balance Certificates senior to such Class of Certificates and the denominator of which is the total initial Certificate Balance of all of the Principal Balance Certificates. The Certificate Principal to Value Ratio for each of the Class A-1, A-2A, A-2B, A-3, A-4 and A-SB Certificates is calculated in the aggregate for those Classes as if they were a single Class and is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio for the mortgage loans and (b) a fraction, the numerator of which is the total initial aggregate Certificate Balances of such Classes of Certificates and the denominator of which is the total initial Certificate Balance of all of the Principal Balance Certificates. In any event, however, excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan. |

| (6) | The Certificate Principal U/W NOI Debt Yield for each Class of Certificates (other than the Class A-1, A-2A, A-2B, A-3, A-4 and A-SB Certificates) is calculated as the product of (a) the weighted average U/W NOI Debt Yield for the mortgage loans and (b) a fraction, the numerator of which is the total initial Certificate Balance of all of the Classes of Principal Balance Certificates and the denominator of which is the total initial Certificate Balance for such Class of Certificates and all Classes of Principal Balance Certificates senior to such Class of Certificates. The Certificate Principal U/W NOI Debt Yield for each of the Class A-1, A-2A, A-2B, A-3, A-4 and A-SB Certificates is calculated in the aggregate for those Classes as if they were a single Class and is calculated as the product of (a) the weighted average U/W NOI Debt Yield for the mortgage loans and (b) a fraction, the numerator of which is the total initial Certificate Balance of all of the Classes of Principal Balance Certificates and the denominator of which is the total aggregate initial Certificate Balances for the Class A-1, A-2A, A-2B, A-3, A-4 and A-SB Certificates. In any event, however, cash flow from each mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan. |

| (7) | The pass-through rates for the Class A-1, A-2A, A-2B, A-3, A-4, A-SB, A-S, B, C, D, E, F and G Certificates in each case will be one of the following: (i) a fixed rateper annum, (ii) a variable rate per annum equal to the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, (iii) a variable rateper annum equal to the lesser of (a) a fixed rate and (b) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date or (iv) a variable rateper annum equal to the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date minus a specified percentage. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (8) | The Class X-A Certificates are notional amount certificates. The Notional Amount of the Class X-A Certificates will be equal to the aggregate principal balance of the Class A-1, A-2A, A-2B, A-3, A-4, A-SB and A-S Certificates outstanding from time to time. The Class X-A Certificates will not be entitled to distributions of principal. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 3 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Certificate Structure |

| (9) | The pass-through rate for the Class X-A Certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the weighted average of the pass-through rates on the Class A-1, A-2A, A-2B, A-3, A-4, A-SB and A-S Certificates for the related distribution date, weighted on the basis of their respective aggregate principal balances outstanding immediately prior to that distribution date. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (10) | The Class X-B Certificates are notional amount certificates. The Notional Amount of the Class X-B Certificates will be equal to the principal balance of the Class B Certificates outstanding from time to time. The Class X-B Certificates will not be entitled to distributions of principal. |

| (11) | The pass-through rate for the Class X-B Certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the pass-through rate on the Class B Certificates for the related distribution date. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (12) | The Class X-D Certificates are notional amount certificates. The Notional Amount of the Class X-D Certificates will be equal to the principal balance of the Class D Certificates outstanding from time to time. The Class X-D Certificates will not be entitled to distributions of principal. |

| (13) | The pass-through rate for the Class X-D Certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the pass-through rate on the Class D Certificates for the related distribution date. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 4 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Issue Characteristics |

| II. | Transaction Highlights |

Mortgage Loan Sellers:

Mortgage Loan Seller | Number of | Number of | Aggregate Cut-off | % of Initial | ||||

| Principal Commercial Capital(1) | 9 | 22 | $255,000,000 | 25.4% | ||||

| Ladder Capital Finance LLC | 23 | 52 | 243,814,257 | 24.3 | ||||

| Citigroup Global Markets Realty Corp. | 10 | 12 | 208,388,821 | 20.8 | ||||

| Wells Fargo Bank, National Association | 21 | 21 | 167,826,195 | 16.7 | ||||

| Société Générale | 8 | 8 | 127,171,753 | 12.7 | ||||

Total | 71 | 115 | $1,002,201,025 | 100.0% |

| (1) | Principal Commercial Capital is the lending platform jointly formed by Macquarie US Trading LLC and Principal Real Estate Investors, LLC to originate and securitize commercial mortgage loans. The mortgage loans to be transferred to the depositor by Macquarie US Trading LLC d/b/a Principal Commercial Capital were originated by either (i) Macquarie Investments US Inc. d/b/a Principal Commercial Capital, in the case of one mortgage loan, secured by the mortgaged property identified on Annex A 1 to the Preliminary Prospectus as Hawthorne Business Center, representing approximately 1.2% of the Initial Pool Balance, which will transfer such mortgage loan to Macquarie US Trading LLC d/b/a Principal Commercial Capital on or prior to the closing date, or (ii) Macquarie US Trading LLC d/b/a Principal Commercial Capital, in the case of all other mortgage loans to be transferred to the depositor by Macquarie US Trading LLC d/b/a Principal Commercial Capital. |

Loan Pool:

| Initial Pool Balance: | $1,002,201,025 |

| Number of Mortgage Loans: | 71 |

| Average Cut-off Date Balance per Mortgage Loan: | $14,115,507 |

| Number of Mortgaged Properties: | 115 |

| Average Cut-off Date Balance per Mortgaged Property(1): | $8,714,792 |

| Weighted Average Mortgage Interest Rate: | 4.763% |

| Ten Largest Mortgage Loans as % of Initial Pool Balance(2): | 50.4% |

| Weighted Average Original Term to Maturity or ARD (months): | 111 |

| Weighted Average Remaining Term to Maturity or ARD (months): | 110 |

| Weighted Average Original Amortization Term (months)(3): | 359 |

| Weighted Average Remaining Amortization Term (months)(3): | 359 |

| Weighted Average Seasoning (months): | 1 |

| (1) | Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in the related loan documents or such other allocation as the related mortgage loan seller deemed appropriate. |

| (2) | Includes the ten largest mortgage loans or group of cross-collateralized underlying mortgage loans. |

| (3) | Excludes any mortgage loan that does not amortize. |

Credit Statistics:

| Weighted Average U/W Net Cash Flow DSCR(1): | 1.64x |

| Weighted Average U/W Net Operating Income Debt Yield(1): | 10.2% |

| Weighted Average Cut-off Date Loan-to-Value Ratio(1): | 62.8% |

| Weighted Average Balloon or ARD Loan-to-Value Ratio(1): | 56.8% |

| % of Mortgage Loans with Additional Subordinate Debt(2): | 14.3% |

| % of Mortgage Loans with Single Tenants(3): | 11.3% |

| (1) | With respect to the Empire Mall mortgage loan, the Harbor Pointe Apartments mortgage loan, the Heritage Industrial Portfolio mortgage loan, the Anchorage Marriott Downtown mortgage loan, the Harvey Building Products Portfolio mortgage loan and the JW Marriott Santa Monica Le Merigot mortgage loan, each of which is part of a whole loan, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passu companion loan(s) (unless otherwise stated). The debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property), that currently exists or is allowed under the terms of any mortgage loan. The information for each mortgaged property that relates to a mortgage loan that is cross-collateralized or cross-defaulted with one or more other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio, and debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group. On an individual basis, without regard to the cross-collateralization feature, any mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. See “Description of the Mortgage Pool—Mortgage Pool Characteristics—Cross-Collateralized Mortgage Loans; Multi-Property Mortgage Loans and Related Borrower Mortgage Loans” in the Preliminary Prospectus and Annex A-1 to the Preliminary Prospectus. |

| (2) | The percentage figure expressed as “% of Mortgage Loans with Additional Subordinate Debt” is determined as a percentage of the initial pool balance and does not take into account any future subordinate debt (whether or not secured by the mortgaged property), that may be permitted under the terms of any mortgage loan or the pooling and servicing agreement. See “Description of the Mortgage Pool—Additional Indebtedness—Other Secured Indebtedness” and “—Other Unsecured Indebtedness”. |

| (3) | Excludes mortgage loans that are secured by multiple single tenant properties and includes mortgage loans secured by multiple single tenant properties where each property is occupied by the same tenant or tenants that are affiliates of one another. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 5 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Issue Characteristics |

Loan Structural Features:

Amortization:Based on the Initial Pool Balance, 71.6% of the mortgage pool (52 mortgage loans) has scheduled amortization, as follows:

48.0% (27 mortgage loans) provides for an interest-only period followed by an amortization period; and

23.6% (25 mortgage loans) requires amortization during the entire loan term.

Interest-Only:Based on the Initial Pool Balance, 28.4% of the mortgage pool (19 mortgage loans) provides for interest-only payments during the entire loan term. The Weighted Average Cut-off Date Loan-to-Value Ratio and Weighted Average U/W Net Cash Flow DSCR for those mortgage loans are 61.1% and 1.69x, respectively.

Hard Lockboxes: Based on the Initial Pool Balance, 38.7% of the mortgage pool (21 mortgage loans) have hard lockboxes in place.

Reserves:The mortgage loans require amounts to be escrowed monthly as follows (excluding any mortgage loans with springing provisions):

| Real Estate Taxes: | 79.1% of the pool | |

| Insurance: | 60.7% of the pool | |

| Capital Replacements: | 72.9% of the pool | |

| TI/LC: | 56.5% of the pool(1) | |

| (1) The percentage of Initial Pool Balance for mortgage loans with TI/LC reserves is based on the aggregate principal balance allocable to loans that include retail, office, industrial and mixed use properties. | ||

Call Protection/Defeasance: Based on the Initial Pool Balance, the mortgage pool has the following call protection and defeasance features:

81.3% of the mortgage pool (52 mortgage loans) features a lockout period, then defeasance only until an open period;

8.7% of the mortgage pool (six mortgage loans) features a lockout period, then the greater of a prepayment premium or yield maintenance until an open period;

5.3% of the mortgage pool (five mortgage loans) features a lockout period, then the greater of a prepayment premium or yield maintenance or defeasance until an open period;

3.1% of the mortgage pool (one mortgage loan) features a lockout period, then the greater of a prepayment premium or yield maintenance, then the greater of a prepayment premium or yield maintenance or defeasance until an open period; and

1.5% of the mortgage pool (seven mortgage loans) features no lockout period, but requires yield maintenance, then yield maintenance or defeasance until an open period.

Please refer to Annex A-1 to the Preliminary Prospectus for further information regarding individual loan call protection.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 6 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Issue Characteristics |

| III. | Issue Characteristics |

| Securities Offered: | $860,640,000 approximate monthly pay, multi-class, commercial mortgage REMIC pass-through certificates consisting of eleven classes (Classes A-1, A-2A, A-2B, A-3, A-4, A-SB, A-S, B, C, X-A and X-B), which are offered pursuant to a registration statement filed with the SEC (such classes of certificates, the “Offered Certificates”). | ||

| Mortgage Loan Sellers: | Macquarie US Trading LLC d/b/a Principal Commercial Capital (“PCC”), Ladder Capital Finance LLC (“LCF”), Citigroup Global Markets Realty Corp. (“CGMRC”), Wells Fargo Bank, National Association (“WFB”) and Société Générale (“SG”). | ||

| Co-Lead Managers and Joint Bookrunners: | Wells Fargo Securities, LLC, Citigroup Global Markets Inc. and SG Americas Securities, LLC | ||

| Co-Managers: | Deutsche Bank Securities Inc. | ||

| Rating Agencies: | Fitch Ratings, Inc., Kroll Bond Rating Agency, Inc. and Moody’s Investors Service, Inc. | ||

| Master Servicer: | Wells Fargo Bank, National Association | ||

| Special Servicer: | C-III Asset Management LLC | ||

| Additional Primary Servicer: | Principal Global Investors, LLC | ||

| Certificate Administrator: | Wells Fargo Bank, National Association | ||

| Trustee: | Wilmington Trust, National Association | ||

| Operating Advisor: | Pentalpha Surveillance LLC | ||

| Asset Representations Reviewer: | Pentalpha Surveillance LLC | ||

| Initial Majority Controlling Class Certificateholder: | Raith Capital Partners, LLC or an affiliate thereof. | ||

| Cut-off Date: | The Cut-off Date with respect to each mortgage loan is the due date for the monthly debt service payment that is due in December 2015 (or, in the case of any mortgage loan that has its first due date in January 2016, the date that would have been its due date in December 2015 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month). | ||

| Expected Closing Date: | On or about December 23, 2015. | ||

| Determination Dates: | The 11th day of each month (or if that day is not a business day, the next succeeding business day), commencing in January 2016. | ||

| Distribution Dates: | The fourth business day following the Determination Date in each month, commencing in January 2016. | ||

| Rated Final Distribution Date: | The Distribution Date in December 2048. | ||

| Interest Accrual Period: | With respect to any Distribution Date, the calendar month immediately preceding the month in which such Distribution Date occurs. | ||

| Day Count: | The Offered Certificates will accrue interest on a 30/360 basis. | ||

| Minimum Denominations: | $10,000 for each Class of Offered Certificates (other than the Class X-A and X-B Certificates) and $1,000,000 for the Class X-A and X-B Certificates. Investments may also be made in any whole dollar denomination in excess of the applicable minimum denomination. | ||

| Clean-up Call: | 1% | ||

| Delivery: | DTC, Euroclear and Clearstream Banking | ||

| ERISA/SMMEA Status: | Each Class of Offered Certificates is expected to be eligible for exemptive relief under ERISA. No Class of Offered Certificates will be SMMEA eligible. | ||

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. SEE THE “RISK FACTORS” SECTION OF THE PRELIMINARY PROSPECTUS. | ||

| Bond Analytics Information: | The Certificate Administrator will be authorized to make distribution date statements, CREFC® reports and certain supplemental reports (other than confidential information) available to certain financial modeling and data provision services, including Bloomberg, L.P., Trepp, LLC, Intex Solutions, Inc., Markit Group Limited, Interactive Data Corp., BlackRock Financial Management, Inc., CMBS.com, Inc. and Thomson Reuters Corporation. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 7 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Characteristics of the Mortgage Pool |

| IV. | Characteristics of the Mortgage Pool(1) |

| A. | Ten Largest Mortgage Loans or Groups of Cross-Collateralized Underlying Mortgage Loans |

| Mortgage Loan Seller | Mortgage Loan Name | City | State | Number of Mortgage Loans / Mortgaged Properties | Mortgage Loan Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Property Type | Number of Units/ SF/ Rooms | Cut-off Date Balance Per Unit/ SF/Room | Cut-off Date LTV Ratio (%) | Balloon or ARD LTV Ratio (%) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | |||||||||||||||||

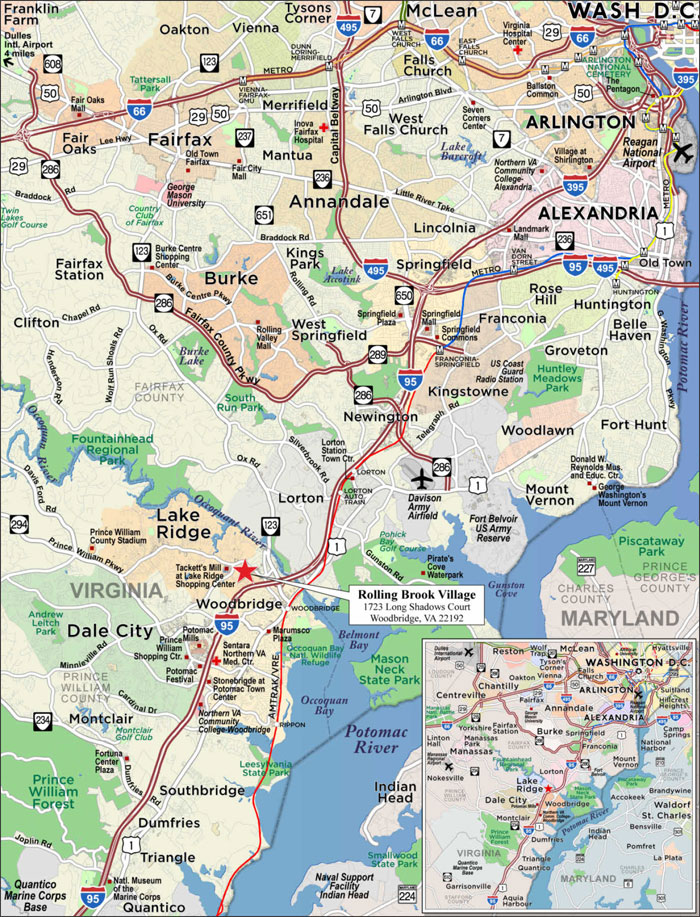

| LCF | Rolling Brook Village | Woodbridge | VA | 1 / 1 | $88,000,000 | 8.8 | % | Multifamily | 732 | $120,219 | 62.0 | % | 62.0 | % | 1.48x | 8.1 | % | |||||||||||||

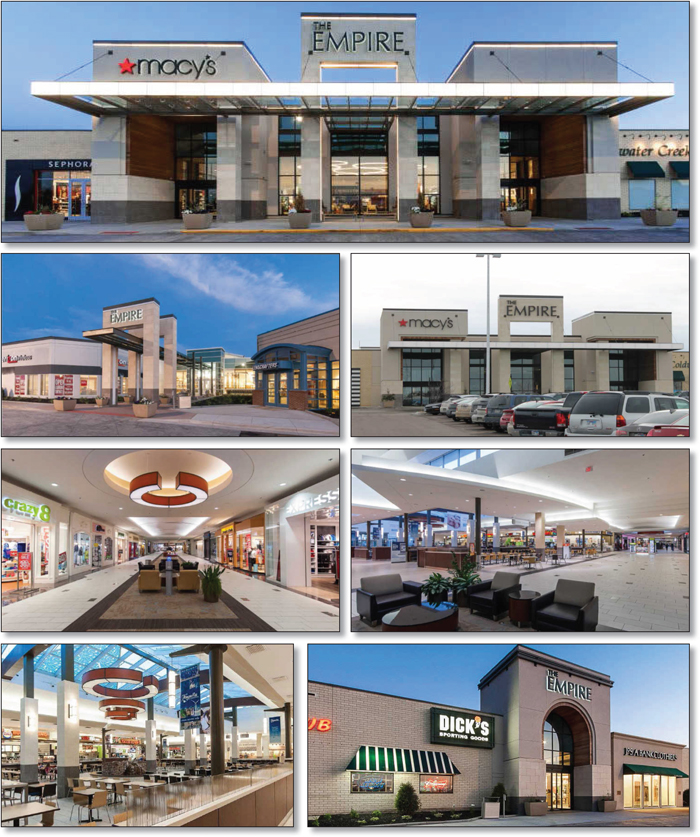

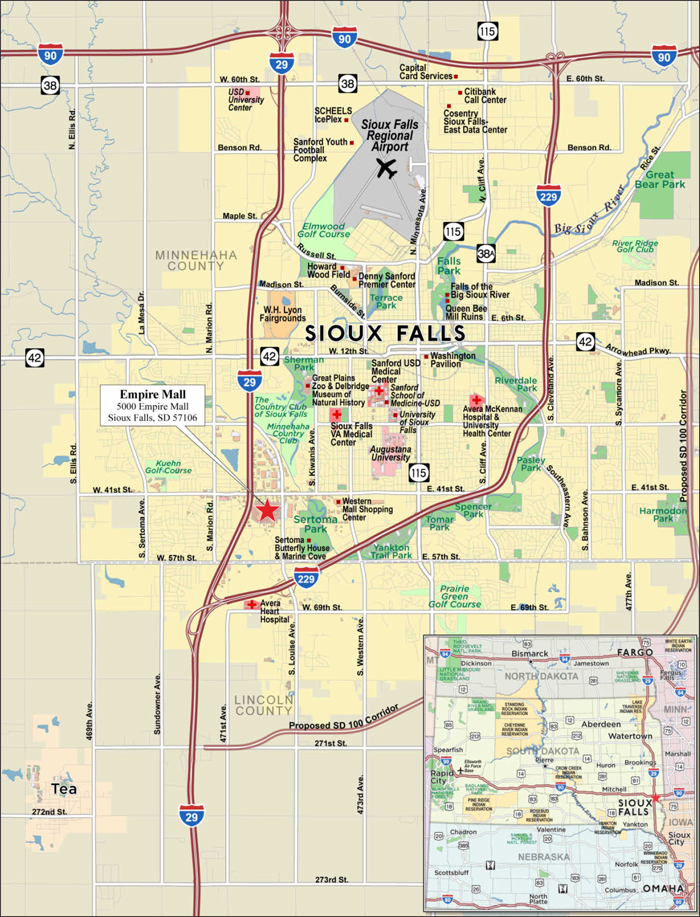

| SG | Empire Mall | Sioux Falls | SD | 1 / 1 | 75,000,000 | 7.5 | Retail | 1,124,451 | 169 | 54.3 | 47.3 | 1.80 | 11.2 | |||||||||||||||||

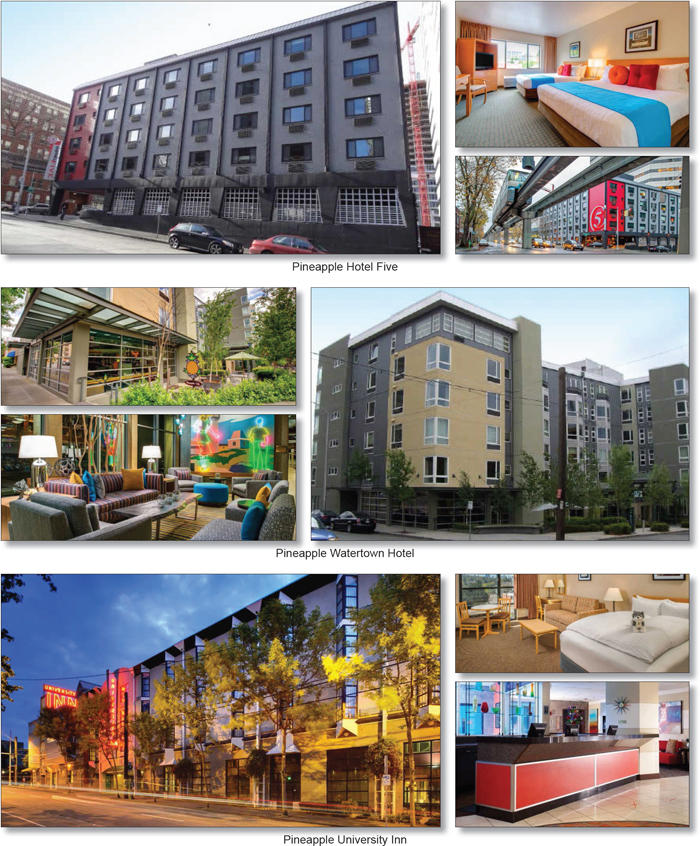

| PCC | Pineapple Hotel Portfolio | Seattle | WA | 1 / 3 | 61,500,000 | 6.1 | Hospitality | 318 | 193,396 | 60.0 | 51.8 | 1.96 | 13.6 | |||||||||||||||||

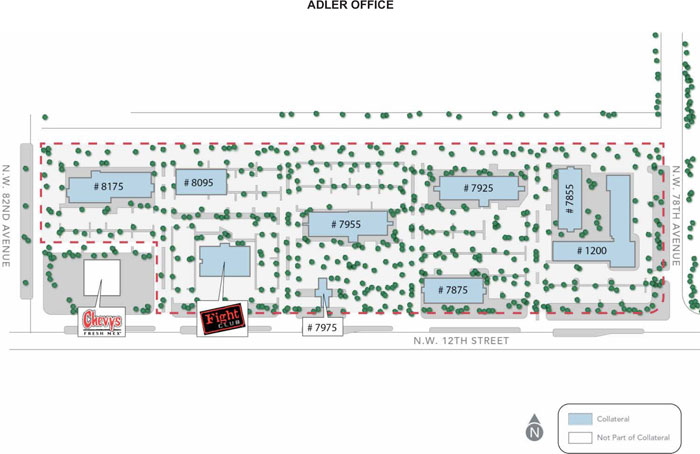

| PCC | Adler Office(2) | Doral | FL | 1 / 1 | 40,200,000 | 4.0 | Office | 388,305 | 98 | 63.3 | 58.3 | 1.29 | 9.0 | |||||||||||||||||

| PCC | Adler Industrial(2) | Doral | FL | 1 / 1 | 16,800,000 | 1.7 | Industrial | 196,267 | 98 | 63.3 | 58.3 | 1.29 | 9.0 | |||||||||||||||||

| CGMRC | Harbor Pointe Apartments | Bayonne | NJ | 1 / 1 | 50,000,000 | 5.0 | Multifamily | 544 | 202,206 | 71.0 | 71.0 | 1.48 | 7.2 | |||||||||||||||||

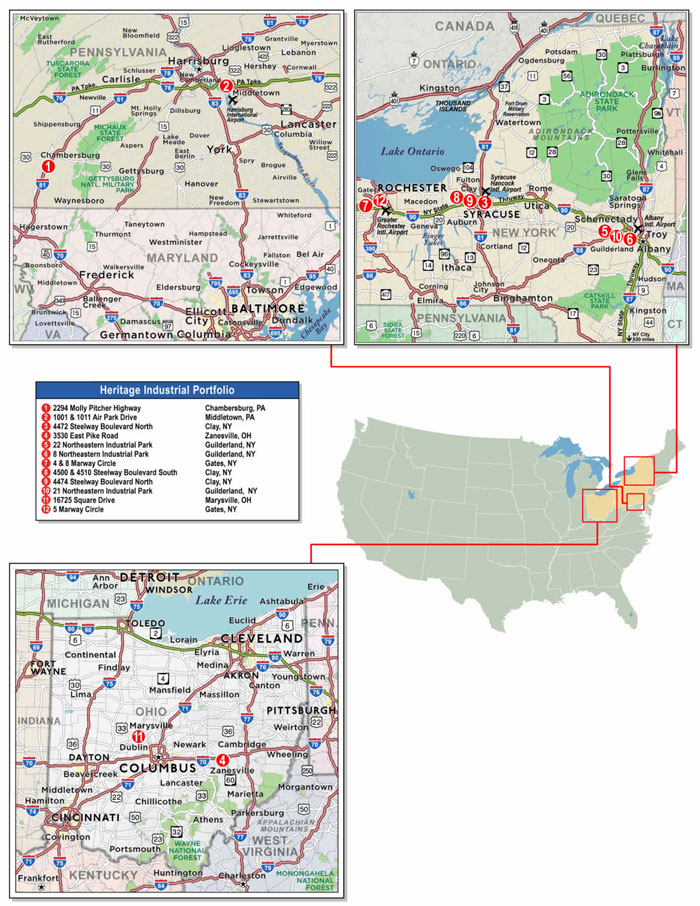

| PCC | Heritage Industrial Portfolio | Various | Various | 1 / 12 | 41,000,000 | 4.1 | Industrial | 2,578,919 | 32 | 69.8 | 61.3 | 1.36 | 9.2 | |||||||||||||||||

| CGMRC | Anchorage Marriott Downtown | Anchorage | AK | 1 / 1 | 37,926,518 | 3.8 | Hospitality | 392 | 193,503 | 69.9 | 51.7 | 1.76 | 12.3 | |||||||||||||||||

| LCF | Harvey Building Products Portfolio | Various | Various | 1 / 30 | 32,922,772 | 3.3 | Various | 2,046,119 | 54 | 53.4 | 49.3 | 1.96 | 12.8 | |||||||||||||||||

| CGMRC | JW Marriott Santa Monica Le Merigot | Santa Monica | CA | 1 / 1 | 31,162,303 | 3.1 | Hospitality | 175 | 356,141 | 59.9 | 55.3 | 1.77 | 13.5 | |||||||||||||||||

| CGMRC | Keeper’s Self Storage Manhattan | New York | NY | 1 / 1 | 31,000,000 | 3.1 | Self Storage | 61,575 | 503 | 57.5 | 57.5 | 1.45 | 7.3 | |||||||||||||||||

| Top Three Total/Weighted Average | 3 / 5 | $224,500,000 | 22.4 | % | 58.9 | % | 54.3 | % | 1.72x | 10.6 | % | |||||||||||||||||||

| Top Five Total/Weighted Average(3) | 6 / 8 | $331,500,000 | 33.1 | % | 61.5 | % | 57.5 | % | 1.61x | 9.8 | % | |||||||||||||||||||

| Top Ten Total/Weighted Average(4) | 11 / 53 | $505,511,593 | 50.4 | % | 61.9 | % | 56.7 | % | 1.62x | 10.2 | % | |||||||||||||||||||

| Non-Top Ten Total/Weighted Average(5) | 60 / 62 | $496,689,432 | 49.6 | % | 63.7 | % | 56.9 | % | 1.66x | 10.2 | % | |||||||||||||||||||

| (1) | With respect to the Empire Mall mortgage loan, the Harbor Pointe Apartments mortgage loan, the Heritage Industrial Portfolio mortgage loan, the Anchorage Marriott Downtown mortgage loan, the Harvey Building Products Portfolio mortgage loan and the JW Marriott Santa Monica Le Merigot mortgage loan, each of which is part of a whole loan, Cut-off Date Balance Per Unit/SF/Room, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passu companion loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account of subordinate debt (whether or not secured by the related mortgaged property), if any, that currently exists or is allowed under the terms of such mortgage loan. |

| (2) | The Adler Office mortgage loan and the Adler Industrial mortgage loan are cross-collateralized and cross-defaulted with one another. With respect to each of the Adler Office and Adler Industrial mortgage loans, the applicable loan-to-value ratios, debt service coverage ratios and debt yields for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by both mortgage loans. On an individual basis, without regard to the cross-collateralization feature, a related mortgage loan may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. |

| (3) | Includes the five largest mortgage loans or group of cross-collateralized underlying mortgage loans. |

| (4) | Includes the ten largest mortgage loans or group of cross-collateralized underlying mortgage loans. |

| (5) | Excludes the ten largest mortgage loans or group of cross-collateralized underlying mortgage loans. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 8 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Characteristics of the Mortgage Pool |

| B. | Summary ofPari PassuWhole Loans |

| Property Name | Mortgage Loan Seller | Related Notes in Loan Group (Original Balance) | Holder of Note | Lead Servicer for Whole loan | Current Master Servicer Under Related Securitization Servicing Agreement | Current Special Servicer Under Related Securitization Servicing Agreement |

| Empire Mall | SG | $75,000,000 | WFCM 2015-P2 | No(2) | Wells Fargo Bank, National Association | C-III Asset Management LLC |

| SG | $40,000,000 | (1) | Yes(2) | TBD | TBD | |

| SG | $40,000,000 | (1) | No(2) | TBD | TBD | |

| SG | $25,000,000 | (1) | No(2) | TBD | TBD | |

| SG | $10,000,000 | (1) | No(2) | TBD | TBD | |

| Harbor Pointe Apartments | CGMRC | $60,000,000 | CGCMT 2015-GC35 | Yes | Midland Loan Services, a Division of PNC Bank, National Association | C-III Asset Management LLC |

| CGMRC | $50,000,000 | WFCM 2015-P2 | No | Wells Fargo Bank, National Association | C-III Asset Management LLC | |

| Heritage Industrial Portfolio | PCC | $41,000,000 | WFCM 2015-P2 | Yes | Wells Fargo Bank, National Association | C-III Asset Management LLC |

| PCC | $40,375,000 | (3) | No | TBD | TBD | |

| Anchorage Marriott Downtown | CGMRC | $37,975,000 | CGCMT 2015-GC35 | Yes | Midland Loan Services, a Division of PNC Bank, National Association | C-III Asset Management LLC |

| CGMRC | $37,975,000 | WFCM 2015-P2 | No | Wells Fargo Bank, National Association | C-III Asset Management LLC | |

| Harvey Building Products Portfolio | LCF | $42,000,000 | COMM 2015-LC23 | Yes | Wells Fargo Bank, National Association | LNR Partners LLC |

| LCF | $33,000,000 | WFCM 2015-P2 | No | Wells Fargo Bank, National Association | C-III Asset Management LLC | |

| LCF | $25,000,000 | (4) | No | TBD | TBD | |

| LCF | $10,000,000 | (4) | No | TBD | TBD | |

| JW Marriott Santa Monica Le Merigot | CGMRC | $31,200,000 | CGCMT 2015-GC35 | Yes | Midland Loan Services, a Division of PNC Bank, National Association | C-III Asset Management LLC |

| CGMRC | $31,200,000 | WFCM 2015-P2 | No | Wells Fargo Bank, National Association | C-III Asset Management LLC | |

| (1) | The relatedpari passu companion loans designated Note A-1, Note A-3, Note A-4 and Note A-5 are currently held by SG or an affiliate. Note A-1 represents the controlling note. Note A-1, Note A-3, Note A-4 and Note A-5 are expected to be contributed to one or more future securitizations. No assurance can be provided that Note A-1, Note A-3, Note A-4 and Note A-5 will not be split further. |

| (2) | The Empire Mall whole loan will be serviced under the WFCM 2015-P2 pooling and servicing agreement until the securitization of the related controllingpari passu companion loan (evidenced by Note A-1), after which the Empire Mall whole loan will be serviced under the pooling and servicing agreement related to the securitization of the related controllingpari passu companion loan. The master servicer and special servicer under that pooling and servicing agreement will be identified in a notice, report or statement to holders of the WFCM 2015-P2 certificates after the securitization of the related controllingpari passu companion loan. |

| (3) | The relatedpari passu companion loan designated Note A-2 is currently held by PCC or an affiliate. Note A-2 represents the non-controlling note and is expected to be contributed to one or more future securitizations. No assurance can be provided that Note A-2 will not be split further. |

| (4) | The relatedpari passu companion loans designated Note A-2-A and Note A-2-B are currently held by LCF or an affiliate. Note A-2-A and Note A-2-B represent non-controlling notes and are expected to be contributed to one or more future securitizations. No assurance can be provided that Note A-2-A and Note A-2-B will not be split further. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 9 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Characteristics of the Mortgage Pool |

| C. | Mortgage Loans with Additional Secured and Mezzanine Financing |

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | Mortgage Loan Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Sub Debt Cut-off Date Balance ($) | Mezzanine Debt Cut-off Date Balance ($) | Total Debt | Mortgage Loan U/W NCF DSCR (x)(2) | Total Debt U/W NCF DSCR (x)(2) | Mortgage Loan Cut-off Date U/W NOI Debt Yield (%)(2) | Total Debt Cut-off Date U/W NOI Debt Yield (%)(2) | Mortgage Loan Cut-off Date LTV Ratio (%)(2) | Total Debt Cut-off Date LTV Ratio (%)(2) | |||||||||||||

| 1 | LCF | Rolling Brook Village | $88,000,000 | 8.8% | $0 | $20,200,000 | 6.018% | 1.48x | 1.05x | 8.1% | 6.6% | 62.0% | 76.2% | |||||||||||||

| 10 | CGMRC | JW Marriott Santa Monica Le Merigot | 31,162,303 | 3.1 | 0 | 17,000,000 | 5.941 | 1.77 | 1.26 | 13.5 | 10.6 | 59.9 | 76.3 | |||||||||||||

| Total/Weighted Average | $119,162,303 | 11.9% | $0 | $37,200,000 | 5.998% | 1.56x | 1.10x | 9.5% | 7.6% | 61.5% | 76.2% | |||||||||||||||

| (1) | Total Debt Interest Rate for any specified mortgage loan reflects the weighted average of the interest rates on the respective components of the total debt. |

| (2) | With respect to the JW Marriott Santa Monica Le Merigot mortgage loan, which is part of a whole loan, debt service coverage ratio, debt yield and loan-to-value ratio calculations include the related pari passu companion loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 10 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Characteristics of the Mortgage Pool |

| D. | Previous Securitization History(1) |

| Loan No. | Mortgage Loan Seller | Mortgage Loan or Mortgaged Property Name | City | State | Property Type | Mortgage Loan or Mortgaged Property Cut- off Date Balance ($) | % of Initial Pool Balance (%) | Previous Securitization | ||||||||

| 2 | SG | Empire Mall | Sioux Falls | SD | Retail | $75,000,000 | 7.5 | % | BACM 2006-6 | |||||||

| 7 | PCC | Heritage Industrial Portfolio | Various | Various | Industrial | 41,000,000 | 4.1 | CD 2007-CD4 | ||||||||

| 8 | CGMRC | Anchorage Marriott Downtown | Anchorage | AK | Hospitality | 37,926,518 | 3.8 | DBUBS 2011-LC3A | ||||||||

| 10 | CGMRC | JW Marriott Santa Monica Le Merigot | Santa Monica | CA | Hospitality | 31,162,303 | 3.1 | DBUBS 2011-LC3A | ||||||||

| 13 | PCC | Home Depot Jamaica | Jamaica | NY | Other | 25,000,000 | 2.5 | MSC 2006-IQ11 | ||||||||

| 16 | CGMRC | Westgate Shopping Center | Ann Arbor | MI | Retail | 22,000,000 | 2.2 | BACM 2006-5 | ||||||||

| 17 | LCF | Green Caye | Dickinson | TX | Mixed Use | 19,000,000 | 1.9 | LBUBS 2006-C3 | ||||||||

| 18 | WFB | Huntington Park Shopping Center | Huntington Park | CA | Retail | 18,500,000 | 1.8 | BSCMS 2006-PW11 | ||||||||

| 20 | WFB | 2200 Harbor Boulevard | Costa Mesa | CA | Retail | 14,000,000 | 1.4 | BSCMS 2005-T20 | ||||||||

| 23 | CGMRC | Amsdell Michigan Pool | Various | MI | Self Storage | 12,500,000 | 1.2 | WFRBS 2011-C5 | ||||||||

| 26 | PCC | Hawthorne Business Center | Hawthorne | CA | Industrial | 11,800,000 | 1.2 | WBCMT 2005-C22 | ||||||||

| 27 | WFB | Valley View Business Center | Las Vegas | NV | Industrial | 11,185,358 | 1.1 | JPMCC 2006-CB14 | ||||||||

| 29 | WFB | Security Public Storage - Salinas | Salinas | CA | Self Storage | 9,925,000 | 1.0 | BSCMS 2006-T22 | ||||||||

| 30 | SG | Dollar Self Storage | Henderson | NV | Self Storage | 9,150,000 | 0.9 | GSMS 2012-GC6 | ||||||||

| 31 | CGMRC | Sunset Plaza | San Angelo | TX | Retail | 9,150,000 | 0.9 | GSMS 2006-GG6 | ||||||||

| 32 | LCF | Tally Ho | Wilmington | DE | Retail | 8,988,677 | 0.9 | CD 2006-CD2 | ||||||||

| 33 | WFB | Parkway Commons | Franklin | TN | Mixed Use | 8,050,000 | 0.8 | LBUBS 2006-C3 | ||||||||

| 36 | WFB | ClimaStor 6 | Baton Rouge | LA | Self Storage | 7,620,134 | 0.8 | BACM 2006-1 | ||||||||

| 37 | WFB | Joiner Parkway Self Storage | Lincoln | CA | Self Storage | 7,350,000 | 0.7 | BSCMS 2006-PW11 | ||||||||

| 38 | LCF | Fairfield Inn & Suites Lumberton | Lumberton | NC | Hospitality | 6,988,368 | 0.7 | CSMC 2006-C1 | ||||||||

| 39 | SG | LA Fitness - Euless | Euless | TX | Retail | 6,700,000 | 0.7 | JPMCC 2007-LD12 | ||||||||

| 41 | CGMRC | CSS Lafayette | Lafayette | CA | Self Storage | 6,300,000 | 0.6 | BACM 2007-3 | ||||||||

| 42 | SG | LA Fitness - Grand Prairie | Grand Prairie | TX | Retail | 6,300,000 | 0.6 | JPMCC 2007-LDPX | ||||||||

| 43 | SG | LA Fitness - Pearland | Pearland | TX | Retail | 6,125,000 | 0.6 | MSC 2007-HQ13 | ||||||||

| 44 | WFB | Security Public Storage - Pittsburg | Pittsburg | CA | Self Storage | 6,050,000 | 0.6 | MSC 2006-T23 | ||||||||

| 49 | LCF | Dover Downs | Dover | DE | Retail | 4,993,835 | 0.5 | CSMC 2006-C1 | ||||||||

| 54 | WFB | Security Public Storage - Manteca | Manteca | CA | Self Storage | 4,225,000 | 0.4 | BSCMS 2006-T22 | ||||||||

| 55 | WFB | Storage Depot Fossil Creek | Fort Worth | TX | Self Storage | 4,015,000 | 0.4 | BACM 2006-1 | ||||||||

| 56 | WFB | ClimaStor 7 | Baton Rouge | LA | Self Storage | 3,795,086 | 0.4 | JPMCC 2006-LDP9 | ||||||||

| 60 | WFB | University Center South | Jacksonville | FL | Retail | 3,080,983 | 0.3 | MLMT 2005-CIP1 | ||||||||

| 63 | WFB | Security Public Storage - Sacramento III | Sacramento | CA | Self Storage | 2,600,000 | 0.3 | BSCMS 2006-PW11 | ||||||||

| Total | $440,481,261 | 44.0 | % | |||||||||||||

| (1) | The table above represents the most recent securitization with respect to the mortgaged property securing the related mortgage loan, based on information provided by the related borrower or obtained through searches of a third-party database. While loans secured by the above mortgaged properties may have been securitized multiple times in prior transactions, mortgage loans in this securitization are only listed in the above chart if the mortgage loan paid off a loan in another securitization. The information has not otherwise been confirmed by the mortgage loan sellers. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 11 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Characteristics of the Mortgage Pool |

| E. | Mortgage Loans with Scheduled Balloon Payments and Related Classes |

| Class A-2A and Class A-2B(1) |

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Balloon Balance ($) | % of Class A-2A and A-2B Certificate Principal Balance (%)(2) | Units/ SF/ Rooms | Loan per Unit/SF/ Room ($) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | Cut-off Date LTV Ratio (%) | Balloon or ARD LTV Ratio (%) | Rem. IO Period (mos.) | Rem. Term to Maturity (mos.) | |||||||||||||||||||

| 1 | LCF | Rolling Brook Village | VA | Multifamily | $88,000,000 | 8.8 | % | $88,000,000 | 57.7 | % | 732 | $120,219 | 1.48x | 8.1 | % | 62.0 | % | 62.0% | 60 | 60 | |||||||||||||||

| 9 | LCF | Harvey Building Products Portfolio | Various | Various | 32,922,772 | 3.3 | 30,369,128 | 19.9 | 2,046,119 | 54 | 1.96 | 12.8 | 53.4 | 49.3 | 0 | 58 | |||||||||||||||||||

| 10 | CGMRC | JW Marriott Santa Monica Le Merigot | CA | Hospitality | 31,162,303 | 3.1 | 28,764,615 | 18.9 | 175 | 356,141 | 1.77 | 13.5 | 59.9 | 55.3 | 0 | 59 | |||||||||||||||||||

| 61 | SG | Baymont Inn & Suites Las Vegas | NV | Hospitality | 2,946,753 | 0.3 | 2,739,852 | 1.8 | 111 | 26,547 | 1.69 | 13.9 | 54.6 | 50.7 | 0 | 59 | |||||||||||||||||||

| Total/Weighted Average | $155,031,828 | 15.5 | % | $149,873,595 | 98.3 | % | 1.64x | 10.3 | % | 59.6 | % | 57.7% | 34 | 59 | |||||||||||||||||||||

| (1) | The table above presents the mortgage loan(s) whose balloon payments would be applied to pay down the principal balance of the Class A-2A and A-2B Certificates, assuming a 0% CPR and applying the “Structuring Assumptions” described in the Preliminary Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments prior to maturity (or, in the case of an ARD loan, its anticipated repayment date), defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date (or, in the case of an ARD loan, its anticipated repayment date). Each Class of Certificates, including the Class A-2A and A-2B Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account subordinate debt (whether or not secured by the related mortgaged property), if any, that currently exists or is allowed under the terms of any mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

| (2) | Reflects the percentage equal to the Balloon Balance divided by the initial Class A-2A and A-2B Certificate Principal Balance. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 12 |

(THIS PAGE INTENTIONALLY LEFT BLANK)

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 13 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Characteristics of the Mortgage Pool |

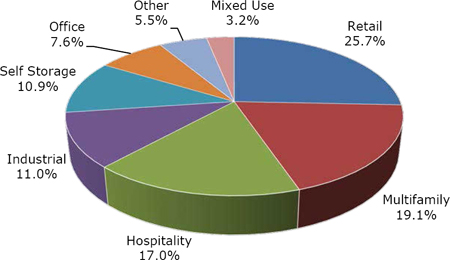

| F. | Property Type Distribution(1) |

| Property Type | Number of Mortgaged Properties | Aggregate Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon or ARD LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) | |||||||||||

| Retail | 27 | $257,287,731 | 25.7% | 62.4% | 55.2% | 1.61x | 10.3% | 9.7% | 4.672 | % | ||||||||||

| Anchored | 8 | 107,132,512 | 10.7 | 65.7 | 57.6 | 1.51 | 10.3 | 9.5 | 4.764 | |||||||||||

| Regional Mall | 1 | 75,000,000 | 7.5 | 54.3 | 47.3 | 1.80 | 11.2 | 10.7 | 4.314 | |||||||||||

| Single Tenant | 14 | 54,907,000 | 5.5 | 64.9 | 59.5 | 1.53 | 9.1 | 8.8 | 4.921 | |||||||||||

| Unanchored | 3 | 11,098,220 | 1.1 | 63.3 | 57.7 | 1.86 | 10.6 | 9.8 | 4.664 | |||||||||||

| Shadow Anchored | 1 | 9,150,000 | 0.9 | 75.0 | 61.7 | 1.43 | 9.9 | 9.3 | 5.040 | |||||||||||

| Multifamily | 9 | 191,325,000 | 19.1 | 65.5 | 63.8 | 1.53 | 8.4 | 8.1 | 4.938 | |||||||||||

| Garden | 7 | 127,775,000 | 12.7 | 62.4 | 60.9 | 1.58 | 8.9 | 8.5 | 5.028 | |||||||||||

| High Rise | 1 | 13,550,000 | 1.4 | 75.3 | 64.7 | 1.28 | 8.2 | 8.0 | 4.750 | |||||||||||

| Mid Rise | 1 | 50,000,000 | 5.0 | 71.0 | 71.0 | 1.48 | 7.2 | 7.1 | 4.760 | |||||||||||

| Hospitality | 9 | 170,615,310 | 17.0 | 61.8 | 52.1 | 1.87 | 13.4 | 11.9 | 4.884 | |||||||||||

| Limited Service | 6 | 96,035,120 | 9.6 | 59.3 | 51.6 | 1.96 | 13.8 | 12.5 | 4.908 | |||||||||||

| Full Service | 2 | 69,088,821 | 6.9 | 65.4 | 53.3 | 1.76 | 12.8 | 11.1 | 4.805 | |||||||||||

| Extended Stay | 1 | 5,491,368 | 0.5 | 59.0 | 44.9 | 1.59 | 14.0 | 11.6 | 5.450 | |||||||||||

| Industrial | 44 | 110,451,769 | 11.0 | 62.1 | 55.8 | 1.63 | 10.5 | 9.8 | 4.710 | |||||||||||

| Warehouse | 38 | 60,474,908 | 6.0 | 64.3 | 57.3 | 1.56 | 10.4 | 9.8 | 4.710 | |||||||||||

| Light Industrial | 2 | 28,600,000 | 2.9 | 58.8 | 55.9 | 1.67 | 9.8 | 9.0 | 4.732 | |||||||||||

| Flex | 2 | 11,978,906 | 1.2 | 65.3 | 53.3 | 1.63 | 10.7 | 10.0 | 4.547 | |||||||||||

| Manufacturing | 2 | 9,397,955 | 0.9 | 53.4 | 49.3 | 1.96 | 12.8 | 12.5 | 4.850 | |||||||||||

| Self Storage | 16 | 109,226,854 | 10.9 | 63.7 | 56.4 | 1.49 | 8.9 | 8.7 | 4.731 | |||||||||||

| Self Storage | 16 | 109,226,854 | 10.9 | 63.7 | 56.4 | 1.49 | 8.9 | 8.7 | 4.731 | |||||||||||

| Office | 5 | 76,644,361 | 7.6 | 64.0 | 60.0 | 1.50 | 9.5 | 8.5 | 4.741 | |||||||||||

| Suburban | 4 | 61,144,361 | 6.1 | 65.2 | 60.2 | 1.36 | 9.3 | 8.4 | 4.850 | |||||||||||

| CBD | 1 | 15,500,000 | 1.5 | 59.2 | 59.2 | 2.06 | 10.3 | 9.0 | 4.310 | |||||||||||

| Other | 2 | 55,000,000 | 5.5 | 57.1 | 54.5 | 1.73 | 9.1 | 9.1 | 4.482 | |||||||||||

| Leased Fee | 2 | 55,000,000 | 5.5 | 57.1 | 54.5 | 1.73 | 9.1 | 9.1 | 4.482 | |||||||||||

| Mixed Use | 3 | 31,650,000 | 3.2 | 61.6 | 54.6 | 2.02 | 11.4 | 10.9 | 4.616 | |||||||||||

| Manufactured Housing Community/Multifamily/Self Storage | 1 | 19,000,000 | 1.9 | 63.3 | 51.6 | 1.71 | 11.1 | 10.7 | 4.751 | |||||||||||

| Retail/Office | 1 | 8,050,000 | 0.8 | 64.4 | 64.4 | 2.03 | 10.1 | 9.3 | 4.490 | |||||||||||

| Office/Retail | 1 | 4,600,000 | 0.5 | 50.0 | 50.0 | 3.28 | 15.2 | 14.3 | 4.280 | |||||||||||

| Total/Weighted Average: | 115 | $1,002,201,025 | 100.0% | 62.8% | 56.8% | 1.64x | 10.2% | 9.6% | 4.763 | % | ||||||||||

| (1) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, (a) the information for mortgage loans secured by more than one mortgaged property (other than through cross-collateralization with other mortgage loans) is based on allocated amounts (allocating the mortgage loan principal balance to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate), and (b) the information for each mortgaged property that relates to a mortgage loan that is cross-collateralized or cross-defaulted with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio and debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group. On an individual basis, without regard to the cross-collateralization feature, any mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. With respect to the Empire Mall mortgage loan, the Harbor Pointe Apartments mortgage loan, the Heritage Industrial Portfolio mortgage loan, the Anchorage Marriott Downtown mortgage loan, the Harvey Building Products Portfolio mortgage loan and the JW Marriott Santa Monica Le Merigot mortgage loan, each of which is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passu companion loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account of any subordinate debt (whether or not secured by the related mortgaged property) that currently exists or is allowed under the terms of such mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 14 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Characteristics of the Mortgage Pool |

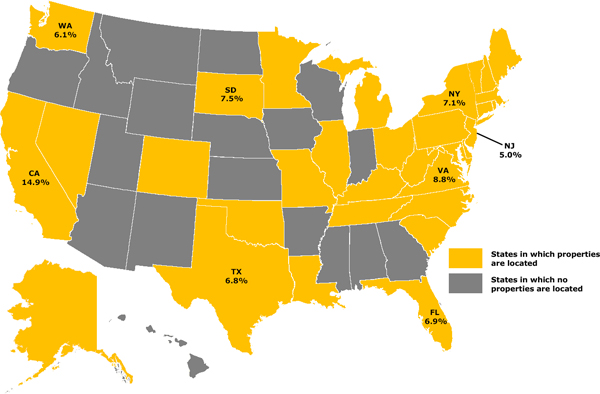

G. Geographic Distribution(1)(2)

| Location | Number of Mortgaged Properties | Aggregate Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon or ARD LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) | |||||||||||

| California | 12 | $149,562,303 | 14.9% | 56.9% | 52.8% | 1.75x | 10.7% | 10.0% | 4.683 | % | ||||||||||

| Southern California(3) | 5 | 105,462,303 | 10.5 | 55.9 | 53.1 | 1.79 | 11.1 | 10.1 | 4.737 | |||||||||||

| Northern California(3) | 7 | 44,100,000 | 4.4 | 59.3 | 52.1 | 1.65 | 9.8 | 9.6 | 4.554 | |||||||||||

| Virginia | 1 | 88,000,000 | 8.8 | 62.0 | 62.0 | 1.48 | 8.1 | 7.9 | 5.247 | |||||||||||

| South Dakota | 1 | 75,000,000 | 7.5 | 54.3 | 47.3 | 1.80 | 11.2 | 10.7 | 4.314 | |||||||||||

| New York | 10 | 70,964,055 | 7.1 | 62.4 | 58.6 | 1.50 | 8.6 | 8.4 | 4.627 | |||||||||||

| Florida | 5 | 69,580,983 | 6.9 | 62.7 | 58.1 | 1.47 | 9.6 | 8.7 | 4.809 | |||||||||||

| Texas | 9 | 67,986,634 | 6.8 | 62.7 | 54.4 | 1.63 | 10.0 | 9.6 | 4.752 | |||||||||||

| Washington | 3 | 61,500,000 | 6.1 | 60.0 | 51.8 | 1.96 | 13.6 | 12.5 | 4.950 | |||||||||||

| New Jersey | 1 | 50,000,000 | 5.0 | 71.0 | 71.0 | 1.48 | 7.2 | 7.1 | 4.760 | |||||||||||

| Other(4) | 73 | 369,607,049 | 36.9 | 66.6 | 57.9 | 1.63 | 10.7 | 9.9 | 4.759 | |||||||||||

| Total/Weighted Average | 115 | $1,002,201,025 | 100.0% | 62.8% | 56.8% | 1.64x | 10.2% | 9.6% | 4.763 | % | ||||||||||

| (1) | The mortgaged properties are located in 32 states. |

| (2) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, (a) the information for mortgage loans secured by more than one mortgaged property (other than through cross-collateralization with other mortgage loans) is based on allocated amounts (allocating the mortgage loan principal balance to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate), and (b) the information for each mortgaged property that relates to a mortgage loan that is cross-collateralized or cross-defaulted with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio and debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group. On an individual basis, without regard to the cross-collateralization feature, any mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. With respect to the Empire Mall mortgage loan, the Harbor Pointe Apartments mortgage loan, the Heritage Industrial Portfolio mortgage loan, the Anchorage Marriott Downtown mortgage loan, the Harvey Building Products Portfolio mortgage loan and the JW Marriott Santa Monica Le Merigot mortgage loan, each of which is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passu companion loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account of any subordinate debt (whether or not secured by the related mortgaged property) that currently exists or is allowed under the terms of such mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

| (3) | For purposes of determining whether a mortgaged property is in Northern California or Southern California, Northern California includes areas with zip codes above 93600 and Southern California includes areas with zip codes of 93600 and below. |

| (4) | Includes 24 other states. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 15 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Characteristics of the Mortgage Pool |

| H. | Characteristics of the Mortgage Pool(1) |

| CUT-OFF DATE BALANCE | |||

| Range of Cut-off Date Balances ($) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance |

| 734,500 - 1,000,000 | 5 | $4,017,000 | 0.4% |

| 1,000,001 - 2,000,000 | 1 | 1,375,000 | 0.1 |

| 2,000,001 - 3,000,000 | 5 | 12,440,623 | 1.2 |

| 3,000,001 - 4,000,000 | 5 | 17,381,070 | 1.7 |

| 4,000,001 - 5,000,000 | 7 | 32,183,835 | 3.2 |

| 5,000,001 - 6,000,000 | 4 | 21,861,368 | 2.2 |

| 6,000,001 - 7,000,000 | 7 | 44,963,368 | 4.5 |

| 7,000,001 - 8,000,000 | 4 | 30,530,134 | 3.0 |

| 8,000,001 - 9,000,000 | 2 | 17,038,677 | 1.7 |

| 9,000,001 - 10,000,000 | 3 | 28,225,000 | 2.8 |

| 10,000,001 - 15,000,000 | 9 | 110,073,358 | 11.0 |

| 15,000,001 - 20,000,000 | 4 | 69,800,000 | 7.0 |

| 20,000,001 - 30,000,000 | 5 | 123,600,000 | 12.3 |

| 30,000,001 - 50,000,000 | 7 | 264,211,593 | 26.4 |

| 50,000,001 - 70,000,000 | 1 | 61,500,000 | 6.1 |

| 70,000,001 - 80,000,000 | 1 | 75,000,000 | 7.5 |

| 80,000,001 - 88,000,000 | 1 | 88,000,000 | 8.8 |

| Total: | 71 | $1,002,201,025 | 100.0% |

| Weighted Average: | $14,115,507 | ||

| UNDERWRITTEN NOI DEBT SERVICE COVERAGE RATIO | |||

| Range of U/W NOI DSCRs (x) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance |

| 1.27 - 1.30 | 1 | $4,970,000 | 0.5% |

| 1.31 - 1.40 | 9 | 63,797,322 | 6.4 |

| 1.41 - 1.50 | 15 | 286,019,768 | 28.5 |

| 1.51 - 1.60 | 5 | 120,950,000 | 12.1 |

| 1.61 - 1.70 | 7 | 59,735,000 | 6.0 |

| 1.71 - 1.80 | 8 | 88,385,018 | 8.8 |

| 1.81 - 1.90 | 9 | 99,146,736 | 9.9 |

| 1.91 - 2.00 | 1 | 37,926,518 | 3.8 |

| 2.01 - 2.50 | 14 | 231,570,664 | 23.1 |

| 2.51 - 3.00 | 1 | 5,100,000 | 0.5 |

| 3.01 - 3.50 | 1 | 4,600,000 | 0.5 |

| Total: | 71 | $1,002,201,025 | 100.0% |

| Weighted Average: | 1.75x | ||

| UNDERWRITTEN NCF DEBT SERVICE COVERAGE RATIO | |||

| Range of U/W NCF DSCRs (x) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance |

| 1.27 - 1.30 | 6 | $106,808,000 | 10.7% |

| 1.31 - 1.40 | 15 | 157,672,322 | 15.7 |

| 1.41 - 1.50 | 11 | 221,506,768 | 22.1 |

| 1.51 - 1.60 | 3 | 14,872,352 | 1.5 |

| 1.61 - 1.70 | 10 | 85,819,155 | 8.6 |

| 1.71 - 1.80 | 8 | 206,587,656 | 20.6 |

| 1.81 - 1.90 | 6 | 11,667,000 | 1.2 |

| 1.91 - 2.00 | 2 | 94,422,772 | 9.4 |

| 2.01 - 2.25 | 8 | 93,145,000 | 9.3 |

| 2.26 - 2.75 | 1 | 5,100,000 | 0.5 |

| 2.76 - 3.28 | 1 | 4,600,000 | 0.5 |

| Total: | 71 | $1,002,201,025 | 100.0% |

| Weighted Average: | 1.64x | ||

| LOAN PURPOSE | |||

| Loan Purpose | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance |

| Refinance | 55 | $751,908,253 | 75.0% |

| Acquisition | 16 | 250,292,772 | 25.0 |

| Total: | 71 | $1,002,201,025 | 100.0% |

| MORTGAGE RATE | |||

| Range of Mortgage Rates (%) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance |

| 4.220 - 4.250 | 1 | $5,100,000 | 0.5% |

| 4.251 - 4.500 | 8 | 164,075,000 | 16.4 |

| 4.501 - 4.750 | 24 | 291,935,772 | 29.1 |

| 4.751 - 5.000 | 25 | 409,231,764 | 40.8 |

| 5.001 - 5.250 | 9 | 111,905,368 | 11.2 |

| 5.251 - 5.470 | 4 | 19,953,121 | 2.0 |

| Total: | 71 | $1,002,201,025 | 100.0% |

| Weighted Average: | 4.763% | ||

| UNDERWRITTEN NOI DEBT YIELD | |||

| Range of U/W NOI Debt Yields (%) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance |

| 7.2 - 8.0 | 2 | $81,000,000 | 8.1% |

| 8.1 - 9.0 | 16 | 260,567,322 | 26.0 |

| 9.1 - 10.0 | 24 | 223,551,768 | 22.3 |

| 10.1 - 11.0 | 13 | 106,394,035 | 10.6 |

| 11.1 - 12.0 | 3 | 97,080,983 | 9.7 |

| 12.1 - 13.0 | 4 | 82,831,493 | 8.3 |

| 13.1 - 14.0 | 5 | 102,475,424 | 10.2 |

| 14.1 - 15.0 | 2 | 38,600,000 | 3.9 |

| 15.1 - 17.0 | 1 | 4,600,000 | 0.5 |

| 17.1 - 17.4 | 1 | 5,100,000 | 0.5 |

| Total: | 71 | $1,002,201,025 | 100.0% |

| Weighted Average: | 10.2% | ||

| UNDERWRITTEN NCF DEBT YIELD | |||

| Range of U/W NCF Debt Yields (%) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance |

| 7.1 - 8.0 | 6 | $206,020,000 | 20.6% |

| 8.1 - 9.0 | 26 | 312,877,090 | 31.2 |

| 9.1 - 10.0 | 16 | 96,247,000 | 9.6 |

| 10.1 - 11.0 | 11 | 191,376,536 | 19.1 |

| 11.1 - 12.0 | 5 | 51,582,627 | 5.1 |

| 12.1 - 13.0 | 4 | 120,397,772 | 12.0 |

| 13.1 - 14.0 | 1 | 14,000,000 | 1.4 |

| 14.1 - 15.0 | 1 | 4,600,000 | 0.5 |

| 15.1 - 15.9 | 1 | 5,100,000 | 0.5 |

| Total: | 71 | $1,002,201,025 | 100.0% |

| Weighted Average: | 9.6% | ||

| (1) | Information regarding mortgage loans that are cross-collateralized or cross-defaulted with other mortgage loans is based upon the individual loan balances, except that the applicable loan-to-value ratio, debt service coverage ratio and debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group. On an individual basis, without regard to the cross-collateralization feature, any mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. With respect to the Empire Mall mortgage loan, the Harbor Pointe Apartments mortgage loan, the Heritage Industrial Portfolio mortgage loan, the Anchorage Marriott Downtown mortgage loan, the Harvey Building Products Portfolio mortgage loan and the JW Marriott Santa Monica Le Merigot mortgage loan, each of which is part of apari passu whole loan, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passu companion loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property), that currently exists or is allowed under the terms of such mortgage loan. See Annex A-1 to the Preliminary Prospectus. Prepayment provisions for each mortgage loan reflects the entire life of the loan (from origination to maturity or ARD). |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 16 |

| Wells Fargo Commercial Mortgage Trust 2015-P2 | Characteristics of the Mortgage Pool |

| ORIGINAL TERM TO MATURITY OR ARD | ||||

| Original Terms to Maturity or ARD (months) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | |

| 60 | 4 | $155,031,828 | 15.5% | |

| 120 | 67 | 847,169,197 | 84.5 | |

| Total: | 71 | $1,002,201,025 | 100.0% | |

| Weighted Average: | 111 months | |||

| REMAINING TERM TO MATURITY OR ARD | ||||

| Range of Remaining Terms to Maturity or ARD (months) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | |

| 58 - 60 | 4 | $155,031,828 | 15.5% | |

| 102 - 120 | 67 | 847,169,197 | 84.5 | |

| Total: | 71 | $1,002,201,025 | 100.0% | |

| Weighted Average: | 110 months | |||

| ORIGINAL AMORTIZATION TERM(2) | ||||

| Original Amortization Terms (months) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | |

| Non-Amortizing | 19 | $284,852,000 | 28.4% | |

| 300 | 2 | 12,479,736 | 1.2 | |

| 360 | 50 | 704,869,289 | 70.3 | |

| Total: | 71 | $1,002,201,025 | 100.0% | |

| Weighted Average(3): | 359 months | |||

(2) The original amortization term shown for any mortgage loan that is interest-only for part of its term does not include the number of months in its interest-only period and reflects only the number of months as of the commencement of amortization remaining from the end of such interest-only period. (3) Excludes the non-amortizing mortgage loans.

| ||||

| REMAINING AMORTIZATION TERM(4) | ||||

| Range of Remaining Amortization Terms (months) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | |

| Non-Amortizing | 19 | $284,852,000 | 28.4% | |

| 299 | 2 | 12,479,736 | 1.2 | |

| 342 - 360 | 50 | 704,869,289 | 70.3 | |

| Total: | 71 | $1,002,201,025 | 100.0% | |

| Weighted Average(5): | 359 months | |||

(4) The remaining amortization term shown for any mortgage loan that is interest-only for part of its term does not include the number of months in its interest-only period and reflects only the number of months as of the commencement of amortization remaining from the end of such interest-only period. (5) Excludes the non-amortizing mortgage loans.

| ||||

| LOCKBOXES | ||||

| Type of Lockbox | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | |

| Springing | 33 | $419,448,106 | 41.9% | |

| Hard/Springing Cash Management | 12 | 308,103,006 | 30.7 | |

| Soft/Upfront Cash Management | 1 | 88,000,000 | 8.8 | |

| Hard/Upfront Cash Management | 9 | 79,617,076 | 7.9 | |

| None | 15 | 77,032,837 | 7.7 | |

| Soft/Springing Cash Management | 1 | 30,000,000 | 3.0 | |

| Total: | 71 | $1,002,201,025 | 100.0% | |

| PREPAYMENT PROVISION SUMMARY | ||||

| Prepayment Provision | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | |

| Lockout / Def / Open | 52 | $815,081,722 | 81.3% | |

| Lockout / GRTR 1% or YM / Open | 6 | 87,625,000 | 8.7 | |

| Lockout / GRTR 1% or YM or Def / Open | 5 | 52,800,000 | 5.3 | |

| Lockout / GRTR 1% or YM / GRTR 1% or YM or Def / Open | 1 | 31,162,303 | 3.1 | |

| YM / YM or Def / Open | 7 | 15,532,000 | 1.5 | |

| Total: | 71 | $1,002,201,025 | 100.0% | |

| CUT-OFF DATE LOAN-TO-VALUE RATIO | ||||

| Range of Cut-off Date LTV Ratios (%) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | |

| 42.4 - 45.0 | 1 | $14,000,000 | 1.4% | |

| 45.1 - 50.0 | 3 | 11,075,000 | 1.1 | |

| 50.1 - 55.0 | 8 | 175,713,360 | 17.5 | |

| 55.1 - 60.0 | 12 | 202,622,348 | 20.2 | |

| 60.1 - 65.0 | 20 | 261,792,358 | 26.1 | |

| 65.1 - 70.0 | 13 | 142,994,739 | 14.3 | |

| 70.1 - 75.0 | 12 | 170,303,220 | 17.0 | |

| 75.1 - 75.5 | 2 | 23,700,000 | 2.4 | |

| Total: | 71 | $1,002,201,025 | 100.0% | |

| Weighted Average: | 62.8% | |||

| BALLOON OR ARD LOAN-TO-VALUE RATIO | |||

| Range of Balloon or ARD LTV Ratios (%) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance |

| 38.8 - 40.0 | 2 | $15,375,000 | 1.5% |

| 40.1 - 45.0 | 4 | 21,635,203 | 2.2 |

| 45.1 - 50.0 | 6 | 131,099,817 | 13.1 |

| 50.1 - 55.0 | 17 | 249,570,263 | 24.9 |

| 55.1 - 60.0 | 16 | 214,535,523 | 21.4 |

| 60.1 - 65.0 | 19 | 267,332,220 | 26.7 |

| 65.1 - 70.0 | 6 | 52,653,000 | 5.3 |

| 70.1 - 71.0 | 1 | 50,000,000 | 5.0 |

| Total: | 71 | $1,002,201,025 | 100.0% |

| Weighted Average: | 56.8% | ||

| AMORTIZATION TYPE | |||||

| Type of Amortization | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | ||

| Interest-only, Amortizing Balloon | 27 | $481,288,000 | 48.0% | ||

| Interest-only, Balloon | 12 | 269,320,000 | 26.9 | ||

| Amortizing Balloon | 25 | 236,061,025 | 23.6 | ||

| Interest-only, ARD | 7 | 15,532,000 | 1.5 | ||