UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report,

Commission file number: 001-37723

ENEL CHILE S.A.

(Exact name of Registrant as specified in its charter)

ENEL CHILE S.A.

(Translation of Registrant’s name into English)

CHILE

(Jurisdiction of incorporation or organization)

Santa Rosa 76, Santiago, Chile

(Address of principal executive offices)

Nicolás Billikopf, phone: (56-2) 2353-4628, nicolas.billikopf@enel.com, Santa Rosa 76, Piso 15, Santiago, Chile

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of Each Class | | Name of Each Exchange on Which Registered |

American Depositary Shares Representing Common Stock | | New York Stock Exchange |

Common Stock, no par value * | | |

* | Listed, not for trading, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission. |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ☐ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☒ | Accelerated filer ☐ | Non-accelerated filer ☐ Emerging growth company ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards † provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).☐ Yes ☒ No

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report

Shares of Common Stock: 49,092,772,762

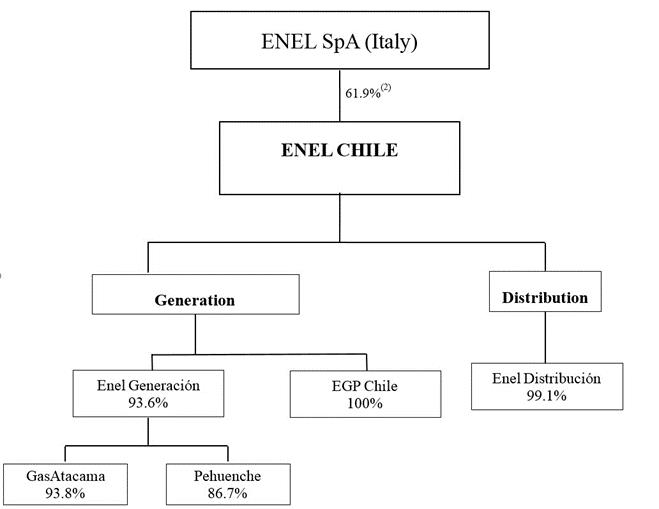

Enel Chile’s Organizational Structure(1)

As of December 31, 2017(2)

| (1) | Only principal operating consolidated entities are presented here. The percentage listed in the box for each of Enel Chile’s consolidated subsidiaries represents its economic interest in such consolidated subsidiary. |

| (2) | Reflects organizational structure prior to giving effect to the 2018 Reorganization, which was completed on April 2, 2018. |

Enel Chile’s Organizational Structure(1)

As of the date of this Report and after giving effect to the 2018 Reorganization

| (1) | Only principal operating consolidated entities are presented here. The percentage listed in the box for each of Enel Chile’s consolidated subsidiaries represents its economic interest in such consolidated subsidiary. |

| (2) | Enel owns 61.9% of our outstanding shares (excluding treasury stock which will be cancelled). |

TABLE OF CONTENTS

1

GLOSSARY

AFP | | Administradora de Fondos de Pensiones | | A legal entity that manages a Chilean pension fund. |

| | | | |

CDEC | | Centro de Despacho Económico de Carga | | The autonomous entity in charge of coordinating the efficient operation and dispatch of generation units to satisfy demand in the SIC and SING that was replaced by the CEN in November 2017. |

| | | | |

Celta | | Compañía Eléctrica Tarapacá S.A. | | Celta was a former Chilean generation subsidiary of Enel Generación that operated plants in the SING and the SIC. Celta merged into GasAtacama in November 2016. |

| | | | |

CEN | | Coordinador Eléctrico Nacional | | An autonomous entity in charge of coordinating the efficient operation of the SEN, dispatching generation units to satisfy demand and known as the National Electricity Coordinator. It replaced the CDEC for both the SIC and SING in November 2017. |

| | | | |

| | | | |

Chilean Stock Exchanges | | Chilean Stock Exchanges | | The three principal stock exchanges located in Chile: the Santiago Stock Exchange, the Electronic Stock Exchange and the Valparaíso Stock Exchange. |

| | | | |

Chilectra Américas | | Chilectra Américas S.A. | | A former electricity distribution company that held minority interests in non-Chilean generation companies. Chilectra Américas was created in the context of the reorganization carried out during 2016 and then merged into Enel Américas in December 2016. |

| | | | |

CMF | | Comisión para el Mercado Financiero | | Chilean Financial Market Commission, the governmental authority that supervises public companies, securities and the insurance business. Formerly the Chilean Superintendence of Securities and Insurance or SVS in its Spanish acronym. |

| | | | |

CNE | | Comisión Nacional de Energía | | Chilean National Energy Commission, governmental entity with responsibilities under the Chilean regulatory framework. |

| | | | |

DCV | | Depósito Central de Valores S.A. | | Chilean Central Securities Depositary. |

| | | | |

Enel | | Enel S.p.A. | | An Italian energy company with multinational operations in the power and gas markets. A 60.6% beneficial owner of us as of December 31, 2017 and 61.9% owner of our voting shares (excluding treasury stock which will be cancelled) as of the date of this Report and after giving effect to the 2018 Reorganization, and our ultimate parent company. |

| | | | |

Enel Américas | | Enel Américas S.A. | | An affiliated publicly held limited liability stock corporation incorporated under the laws of the Republic of Chile headquartered in Chile, with subsidiaries engaged primarily in the generation, transmission and distribution of electricity in Argentina, Brazil, Colombia, and Peru, and which is controlled by Enel. Formerly known on an interim basis as Enersis Américas S.A. and prior to that as Enersis S.A. |

2

| | | | |

Enel Chile | | Enel Chile S.A. | | Our company, a publicly held limited liability stock corporation incorporated under the laws of the Republic of Chile, with subsidiaries engaged primarily in the generation and distribution of electricity in Chile. Registrant of this Report. Formerly known on an interim basis as Enersis Chile S.A. |

| | | | |

Enel Distribución | | Enel Distribución Chile S.A. | | A publicly held limited liability stock corporation incorporated under the laws of the Republic of Chile and our electricity distribution subsidiary operating in the Santiago metropolitan area. Formerly known on an interim basis as Chilectra Chile S.A. and prior to that as Chilectra S.A. |

| | | | |

Enel Generación | | Enel Generación Chile S.A. | | A publicly held limited liability stock corporation incorporated under the laws of the Republic of Chile and our electricity generation subsidiary in Chile. Formerly known as Empresa Nacional de Electricidad S.A. or Endesa Chile. |

| | | | |

EGP Chile | | Enel Green Power Chile Ltda. | | A closely held stock corporation organized under the laws of the Republic of Chile, with non-conventional renewable electricity generation operations and since April 2, 2018, our consolidated subsidiary. |

| | | | |

EGPL | | Enel Green Power Latin América S.A. | | A closely held stock corporation organized under the laws of the Republic of Chile that merged with us on April 2, 2018. As a result, we now consolidate EGP Chile. |

| | | | |

GasAtacama | | GasAtacama Chile S.A. | | A company engaged in gas transportation and electricity generation in northern Chile. A subsidiary of Enel Generación. |

| | | | |

GasAtacama Holding | | Inversiones GasAtacama Holding Ltda. | | A holding company subsidiary of Enel Generación, which previously held GasAtacama. GasAtacama Holding merged into Celta during 2016, which later merged into GasAtacama. |

| | | | |

Gener | | AES Gener S.A. | | A Chilean generation company and one of our competitors in Chile. |

| | | | |

GNL Quintero | | GNL Quintero S.A. | | A company created to develop, build, finance, own and operate a LNG regasification facility at Quintero Bay at which LNG is unloaded, stored and regasified. Enel Generación sold its 20% stake in this company to Enagas Chile S.p.A., an unaffiliated company, in September 2016. |

| | | | |

HidroAysén | | Centrales Hidroeléctricas de Aysén S.A. | | A company created to develop a hydroelectric project in the Aysén region, southern Chile. Enel Generación owned 51% of HidroAysén and Colbún, an unaffiliated company, owned the remaining 49%. The company terminated its activities in 2017. |

| | | | |

IFRS | | International Financial Reporting Standards | | International Financial Reporting Standards as issued by the International Accounting Standards Board (IASB). |

| | | | |

LNG | | Liquefied Natural Gas. | | Liquefied natural gas. |

| | | | |

3

NCRE | | Non-Conventional Renewable Energy | | Energy sources which are continuously replenished by natural processes, such as wind, biomass, mini-hydro, geothermal, wave, solar or tidal energy. |

| | | | |

OSM | | Ordinary Shareholders’ Meeting | | Ordinary Shareholders’ Meeting. |

| | | | |

Pehuenche | | Empresa Eléctrica Pehuenche S.A. | | A publicly held limited liability Chilean electricity stock corporation, owner of three power stations in the Maule River basin and a subsidiary of Enel Generación. |

| | | | |

SEF | | Superintendencia de Electricidad y Combustible | | Chilean Superintendence of Electricity and Fuels, the governmental authority that supervises the Chilean electricity industry. |

| | | | |

SEN | | Sistema Eléctrico Nacional | | The National Electricity System is the Chilean national interconnected electricity system formed in November 2017 through the integration of the SIC and SING. |

| | | | |

SIC | | Sistema Interconectado Central | | Chilean central interconnected electricity system that was integrated with the SING in November 2017 to form a single interconnected system, the SEN. |

| | | | |

SING | | Sistema Interconectado del Norte Grande | | Chilean interconnected electric system operating in northern Chile that was integrated with the SIC in November 2017 to form a single interconnected system, the SEN. |

| | | | |

UF | | Unidad de Fomento | | Chilean inflation-indexed, Chilean peso-denominated monetary unit, equivalent to Ch$ 26,798.14 as of December 31, 2017. |

| | | | |

UTA | | Unidad Tributaria Anual | | Chilean annual tax unit. One UTA equals 12 Unidad Tributaria Mensual (“UTM”), a Chilean inflation-indexed monthly tax unit used to define fines, among other purposes. For December 2017, one UTM was equivalent to Ch$ 46,972 and one UTA was equivalent to Ch$ 563,664. |

| | | | |

VAD | | Valor Agregado de Distribución | | Value added from distribution of electricity. |

4

INTRODUCTION

As used in this Report on Form 20-F (“Report”), first person personal pronouns such as “we”, “us” or “our”, as well as “Enel Chile” or the “Company”, refer to Enel Chile S.A. and our consolidated subsidiaries unless the context indicates otherwise. Unless otherwise noted, our interest in our principal subsidiaries, and jointly-controlled companies and associates is expressed in terms of our economic interest as of December 31, 2017.

We are a Chilean company engaged in the electricity generation and distribution businesses in Chile through our subsidiaries and affiliates. As of the date of this Report and after giving effect to the 2018 Reorganization (described in “Item 4. Information on the Company ― A. History and Development of the Company ― the 2018 Reorganization”), we own 93.6% of Enel Generación Chile S.A. (“Enel Generación”), a Chilean electricity generation company holding electricity generation operations in Chile, and 99.1% of Enel Distribución Chile S.A. (“Enel Distribución”), a Chilean electricity distribution company with operation in the Santiago Metropolitan Area. On April 2, 2018, Enel Green Power Latin America S.A. (“EGPL”), a Chilean non-conventional electricity generation company holding non-conventional electricity generation operations in Chile, merged with us in connection with the 2018 Reorganization. As a result, we now wholly-own and consolidate Enel Green Power Chile Ltda. (“EGP Chile”).

5

PRESENTATION OF INFORMATION

Financial Information

In this Report, unless otherwise specified, references to “U.S. dollars” or “US$”, are to dollars of the United States of America (“United States”); references to “pesos” or “Ch$” are to Chilean pesos, the legal currency of Chile; and references to “UF” are to Unidades de Fomento. The UF is a Chilean inflation-indexed, peso-denominated monetary unit that is adjusted daily to reflect changes in the official Consumer Price Index (“CPI”) of the Chilean National Institute of Statistics (Instituto Nacional de Estadísticas or “INE”). The UF is adjusted in monthly cycles. Each day in the period beginning on the tenth day of the current month through the ninth day of the succeeding month, the nominal peso value of the UF is indexed in order to reflect a proportionate amount of the change in the Chilean CPI during the prior calendar month. As of December 31, 2017, one UF was equivalent to Ch$ 26,798.14. The U.S. dollar equivalent of one UF was US$ 43.59 as of December 31, 2017, using the Observed Exchange Rate reported by the Central Bank of Chile (Banco Central de Chile) as of December 31, 2017 of Ch$ 614.75 per US$ 1.00. The U.S. dollar observed exchange rate (dólar observado) (the “Observed Exchange Rate”), which is reported by the Central Bank of Chile and published daily on its webpage, is the weighted average exchange rate of the previous business day’s transactions in the Formal Exchange Market. Unless the context specifies otherwise, all amounts translated from Chilean pesos to U.S. dollars or vice versa, or from UF to Chilean pesos, have been carried out at the rates applicable as of December 31, 2017.

The Central Bank of Chile may intervene by buying or selling foreign currency on the Formal Exchange Market to maintain the Observed Exchange Rate within a desired range.

Our consolidated financial statements and, unless otherwise indicated, other financial information concerning us included in this Report are presented in Chilean pesos. We have prepared our consolidated financial statements in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”).

All of our subsidiaries are integrated and all their assets, liabilities, income, expenses and cash flows are included in the consolidated financial statements after making the adjustments and eliminations related to intra-group transactions. Investments in associated companies over which we exercise significant influence are included in our consolidated financial statements using the equity method. For detailed information regarding consolidated entities, jointly-controlled entities and associated companies, see Appendices 1, 2 and 3 to the consolidated financial statements.

Solely for the convenience of the reader, this Report contains translations of certain Chilean peso amounts into U.S. dollars at specified rates. Unless otherwise indicated, the U.S. dollar equivalent for information in Chilean pesos is based on the Observed Exchange Rate for December 31, 2017, as defined in “Item 3. Key Information — A. Selected Financial Data — Exchange Rates”. The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos. No representation is made that the Chilean peso or U.S. dollar amounts shown in this Report could have been or could be converted into U.S. dollars or Chilean pesos, as the case may be, at such rate or at any other rate. See “Item 3. Key Information — A. Selected Financial Data — Exchange Rates”.

Technical Terms

References to “TW” are to terawatts (1012 watts or a trillion watts); references to “GW” and “GWh” are to gigawatts (109 watts or a billion watts) and gigawatt hours, respectively; references to “MW” and “MWh” are to megawatts (106 watts or a million watts) and megawatt hours, respectively; references to “kW” and “kWh” are to kilowatts (103 watts or a thousand watts) and kilowatt hours, respectively; references to “kV” are to kilovolts, and references to “MVA” are to megavolt amperes. References to “BTU” and “MBTU” are to British thermal unit and million British thermal units, respectively. A “BTU” is an energy unit equal to approximately 1,055 joules. References to “Hz” are to hertz; and references to “mtpa” are to metric tons per annum. Unless otherwise indicated, statistics provided in this Report with respect to the installed capacity of electricity generation facilities are expressed in MW. One TW equals 1,000 GW, one GW equals 1,000 MW and one MW equals 1,000 kW. The installed capacity we are presenting in this Report corresponds to the gross installed capacity, without considering the MW that each power plant consumes for its own operation.

Statistics relating to aggregate annual electricity production are expressed in GWh and based on a year of 8,760 hours, except for leap years, which are based on 8,784 hours. Statistics relating to installed capacity and production of the electricity industry do not include electricity of self-generators.

6

Energy losses experienced by generation companies during transmission are calculated by subtracting the number of GWh of energy sold from the number of GWh of energy generated (excluding their own energy consumption and losses on the part of the power plant), within a given period. Losses are expressed as a percentage of total energy generated.

Energy losses during distribution are calculated as the difference between total energy purchased (GWh of electricity demand, including own generation) and the energy sold excluding tolls and energy consumption not billed (also measured in GWh), within a given period. Distribution losses are expressed as a percentage of total energy purchased. Losses in distribution arise from illegally tapped energy as well as technical losses.

Calculation of Economic Interest

References are made in this Report to the “economic interest” of Enel Chile in its related companies. We could have direct and indirect interest is such companies. In circumstances where we do not directly own an interest in a related company, our economic interest in such ultimate related company is calculated by multiplying the percentage of economic interest in a directly held related company by the percentage of economic interest of any entity in the ownership chain of such related company. For example, if we directly own a 6% equity stake in an associate company and 40% is directly held by our 60%-owned subsidiary, our economic interest in such associate would be 60% times 40% plus 6%, equal to 30%.

Rounding

Certain figures included in this Report have been rounded for ease of presentation. Because of this rounding, it is possible that amounts in tables may not add up to exactly the same amounts as the sum of the entries.

7

FORWARD-LOOKING STATEMENTS

This Report contains statements that are or may constitute forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These statements appear throughout this Report and include statements regarding our intent, belief or current expectations, including but not limited to any statements concerning:

| • | our capital investment program; |

| • | trends affecting our financial condition or results from operations; |

| • | the future impact of competition and regulation; |

| • | political and economic conditions in the countries in which we or our related companies operate or may operate in the future; |

| • | any statements preceded by, followed by or that include the words “believes,” “expects,” “predicts,” “anticipates,” “intends,” “estimates,” “should,” “may” or similar expressions; and |

| • | other statements contained or incorporated by reference in this Report regarding matters that are not historical facts. |

Because such statements are subject to risks and uncertainties, actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to:

| • | demographic developments, political events, economic fluctuations and interventionist measures by authorities in Chile; |

| • | water supply, droughts, flooding and other weather conditions; |

| • | changes in Chilean environmental regulations and the regulatory framework of the electricity industry; |

| • | our ability to implement proposed capital expenditures, including our ability to arrange financing where required; |

| • | the nature and extent of future competition in our principal markets; |

| • | integration of EGPL may not be successful or we may not realize the business growth opportunities, revenue benefits or other benefits; and |

| • | the factors discussed below under “Risk Factors.” |

You should not place undue reliance on such statements, which speak only as of the date that they were made. Our independent registered public accounting firm has not examined or compiled the forward-looking statements and, accordingly, does not provide any assurance with respect to such statements. You should consider these cautionary statements together with any written or oral forward-looking statements that we may issue in the future. We do not undertake any obligation to release publicly any revisions to forward-looking statements contained in this Report to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

For all these forward-looking statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

8

RECENT DEVELOPMENTS

On April 2, 2018, we completed a corporate reorganization to consolidate Enel’s conventional and non-conventional renewable energy businesses in Chile under one company. The corporate reorganization involved a tender offer for all outstanding shares of common stock (including in the form of American Depositary Shares or “ADSs”) of Enel Generación other than shares owned by us (the “Tender Offer”), a capital increase, including a preemptive rights offering, and the merger of Enel Green Power Latin América S.A. (“EGPL”) with and into Enel Chile. For additional information on the corporate reorganization, see “Item 4. Information on the Company – A. History and Development of the Company – The 2018 Reorganization.”

9

PART I

Item 1.Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2.Offer Statistics and Expected Timetable

Not applicable.

Item 3.Key Information

A. Selected Financial Data.

The following selected consolidated financial data should be read in conjunction with our consolidated financial statements included in this Report. The selected consolidated financial data as of December 31, 2017 and 2016 and for each of the years in the three-year period ended December 31, 2017 are derived from our audited consolidated financial statements included in this Report. The selected consolidated financial data as of December 31, 2015, 2014 and 2013, and for the year ended December 31, 2014 and 2013 is derived from our consolidated financial statements not included in this Report. Our consolidated financial statements were prepared in accordance with IFRS, as issued by the IASB.

Amounts in the tables are expressed in millions, except for ratios, operating data and data for shares and American Depositary Shares (“ADS”). For the convenience of the reader, all data presented in U.S. dollars in the following summary, as of and for the year ended December 31, 2017, has been converted at the U.S. dollar Observed Exchange Rate (dólar observado) for that date of Ch$ 614.75 per US$ 1.00. The Observed Exchange Rate, which is reported and published daily on the Central Bank of Chile’s web page, corresponds to the weighted average exchange rate of the previous business day’s transactions in the Formal Exchange Market. For more information concerning historical exchange rates, see “Item 3. Key Information — A. Selected Financial Data— Exchange Rates” below.

10

The following tables set forth our selected consolidated financial data and operating data for the years indicated:

| | As of and for the year ended December 31, | |

| | 2017 (1) | | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 | |

| | (US$ millions) | | | (Ch$ millions) | |

Consolidated Statement of Comprehensive Income Data | | | | | | | | | | | | | | | | | | | | | | | | |

Revenues and other operating income | | | 4,114 | | | | 2,529,347 | | | | 2,541,567 | | | | 2,399,029 | | | | 2,049,065 | | | | 1,738,083 | |

Operating costs (2) | | | (3,173 | ) | | | (1,950,716 | ) | | | (1,973,778 | ) | | | (1,873,540 | ) | | | (1,666,315 | ) | | | (1,346,460 | ) |

Operating income | | | 941 | | | | 578,631 | | | | 567,789 | | | | 525,489 | | | | 382,750 | | | | 391,623 | |

Financial results (3) | | | (36 | ) | | | (22,415 | ) | | | (20,483 | ) | | | (97,869 | ) | | | (67,045 | ) | | | (56,363 | ) |

Other non-operating income | | | 184 | | | | 113,241 | | | | 121,490 | | | | 20,056 | | | | 70,893 | | | | 14,528 | |

Share of profit (loss) of associates and joint ventures accounted for using the equity method | | | (4 | ) | | | (2,697 | ) | | | 7,878 | | | | 8,905 | | | | (54,353 | ) | | | 24,309 | |

Income before income taxes | | | 1,085 | | | | 666,760 | | | | 676,674 | | | | 456,581 | | | | 332,245 | | | | 374,097 | |

Income tax expenses | | | (233 | ) | | | (143,342 | ) | | | (111,403 | ) | | | (109,613 | ) | | | (132,687 | ) | | | (61,712 | ) |

Net income | | | 851 | | | | 523,418 | | | | 565,271 | | | | 346,968 | | | | 199,558 | | | | 312,385 | |

Net income attributable to the parent Company | | | 568 | | | | 349,383 | | | | 384,160 | | | | 251,838 | | | | 162,459 | | | | 229,527 | |

Net income attributable to non-controlling interests | | | 283 | | | | 174,035 | | | | 181,111 | | | | 95,130 | | | | 37,099 | | | | 82,858 | |

Total basic and diluted earnings per average number of shares (Ch$/US$ per share) | | | 0.01 | | | | 7.12 | | | | 7.83 | | | | 5.13 | | | | 3.31 | | | | 5.08 | |

Total basic and diluted earnings per average number of ADSs (Ch$/US$ per ADS) | | | 0.58 | | | | 355.84 | | | | 391.26 | | | | 256.49 | | | | 165.46 | | | | 253.79 | |

Cash dividends per share (Ch$/US$ per share)(4) | | | 0.01 | | | | 3.23 | | | | 2.09 | | | | — | | | | — | | | | — | |

Cash dividends per ADS (Ch$/US$ per ADS)(4) | | | 0.26 | | | | 161.72 | | | | 104.65 | | | | — | | | | — | | | | — | |

Weighted average number of shares of common stock (millions) | | | | | | | 49,093 | | | | 49,093 | | | | 49,093 | | | | 49,093 | | | | 45,219 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Consolidated Statement of Financial Position Data | | | | | | | | | | | | | | | | | | | | | | | | |

Total assets | | | 9,264 | | | | 5,694,773 | | | | 5,398,711 | | | | 5,325,469 | | | | 5,126,735 | | | | 4,820,392 | |

Non-current liabilities | | | 1,775 | | | | 1,090,995 | | | | 1,178,471 | | | | 1,270,006 | | | | 1,122,585 | | | | 826,478 | |

Equity attributable to the parent company | | | 4,853 | | | | 2,983,384 | | | | 2,763,391 | | | | 2,592,682 | | | | 2,472,201 | | | | 2,438,837 | |

Equity attributable to non-controlling interests | | | 1,307 | | | | 803,578 | | | | 699,602 | | | | 609,219 | | | | 611,864 | | | | 626,947 | |

Total equity | | | 6,160 | | | | 3,786,962 | | | | 3,462,994 | | | | 3,201,901 | | | | 3,084,066 | | | | 3,065,784 | |

Capital stock | | | 3,626 | | | | 2,229,109 | | | | 2,229,109 | | | | 2,229,109 | | | | 2,229,109 | | | | 2,238,169 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Other Consolidated Financial Data | | | | | | | | | | | | | | | | | | | | | | | | |

Capital expenditures (CAPEX) (5) | | | 433 | | | | 266,030 | | | | 222,386 | | | | 309,503 | | | | 196,932 | | | | 128,239 | |

Depreciation, amortization and impairment losses (6) | | | 261 | | | | 160,622 | | | | 197,587 | | | | 150,147 | | | | 141,623 | | | | 127,720 | |

(1) | Solely for the convenience of the reader, Chilean peso amounts have been converted into U.S. dollars at the exchange rate of Ch$ 614.75 per U.S. dollar, as of December 31, 2017. |

(2) | Operating costs represent raw materials and supplies used, other work performed by the entity, employee benefits expenses, depreciation and amortization expenses, impairment losses recognized in the period’s profit or loss and other expenses. |

(3) | Financial results represent (+) financial income, (-) financial costs, (+/-) foreign currency exchange differences and net gains/losses from indexed assets and liabilities. |

(4) | For 2016, a payout ratio of 50% was used based on annual consolidated net income for our 2016’s annual consolidated net income filed with the CMF, based on 10 months of results starting as of our incorporation on March 1, 2016, and therefore differs from the twelve month net income included in this Report. |

(5) | CAPEX figures represent cash flows used for purchases of property, plant and equipment and intangible assets for each year. |

(6) | For further detail please refer to Note 28 of the Notes to our consolidated financial statements. |

11

| | As of and for the year ended December 31, | |

| | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 | |

OPERATING DATA OF SUBSIDIARIES | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

Enel Distribución | | | | | | | | | | | | | | | | | | | | |

Electricity sold (GWh) | | | 16,438 | | | | 15,924 | | | | 15,893 | | | | 15,690 | | | | 15,140 | |

Number of customers (thousands) | | | 1,882 | | | | 1,826 | | | | 1,781 | | | | 1,737 | | | | 1,694 | |

Total energy losses (%) (1) | | | 5.1 | | | | 5.3 | | | | 5.3 | | | | 5.3 | | | | 5.3 | |

| | | | | | | | | | | | | | | | | | | | |

Enel Generación | | | | | | | | | | | | | | | | | | | | |

Installed capacity (MW) (2) | | | 6,351 | | | | 6,351 | | | | 6,351 | | | | 6,351 | | | | 5,571 | |

Generation (GWh) (2) | | | 17,073 | | | | 17,564 | | | | 18,294 | | | | 18,063 | | | | 19,438 | |

(1) | Energy losses in distribution arise from illegally tapped energy as well as technical losses. They are calculated as the difference between total energy generated and purchased and the energy sold, excluding tolls and energy consumption not billed (GWh), within a given period. Losses are expressed as a percentage of total energy purchased. |

(2) | The 2014 and 2015 data includes the capacity and generation of GasAtacama, as a result of its consolidation. Prior to 2014, our unconsolidated interest in GasAtacama was excluded. |

Exchange Rates

Fluctuations in the exchange rate between the Chilean peso and the U.S. dollar will affect the U.S. dollar equivalent of the peso price of our shares of common stock on the Santiago Stock Exchange (Bolsa de Comercio de Santiago), the Chilean Electronic Stock Exchange (Bolsa Electrónica de Chile) and the Valparaíso Stock Exchange (Bolsa de Corredores de Valparaíso). These exchange rate fluctuations affect the price of our American Depositary Shares (“ADSs”) and the conversion of cash dividends relating to the common shares represented by ADSs from Chilean pesos to U.S. dollars. In addition, to the extent that significant financial liabilities of the Company are denominated in foreign currencies, exchange rate fluctuations may have a significant impact on earnings.

In Chile, there are two currency markets, the Formal Exchange Market (Mercado Cambiario Formal) and the Informal Exchange Market (Mercado Cambiario Informal). The Formal Exchange Market is comprised of banks and other entities authorized by the Central Bank of Chile. The Informal Exchange Market is comprised of entities that are not expressly authorized to operate in the Formal Exchange Market, such as certain foreign currency exchange houses and travel agencies, among others. The Central Bank of Chile has the authority to require that certain purchases and sales of foreign currencies be carried out on the Formal Exchange Market. Both the Formal and Informal Exchange Markets are driven by free market forces. Current regulations require that the Central Bank of Chile be informed of certain transactions that must be carried out through the Formal Exchange Market.

The U.S. dollar Observed Exchange Rate, which is reported by the Central Bank of Chile and published daily on its web page, is the weighted average exchange rate of the previous business day’s transactions in the Formal Exchange Market. Nevertheless, the Central Bank of Chile may intervene by buying or selling foreign currency on the Formal Exchange Market to attempt to maintain the Observed Exchange Rate within a desired range.

The Informal Exchange Market reflects transactions carried out at an informal exchange rate (the “Informal Exchange Rate”). There are no limits imposed on the extent to which the rate of exchange in the Informal Exchange Market can fluctuate above or below the Observed Exchange Rate. Foreign currency for payments and distributions with respect to the ADSs may be purchased either in the Formal or the Informal Exchange Market, but such payments and distributions must be remitted through the Formal Exchange Market.

The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos. As of December 31, 2017, the U.S. dollar Observed Exchange Rate was Ch$ 614.75 per US$ 1.00.

12

The following table sets forth the low, high, average and period-end Observed Exchange Rate for U.S. dollars for the periods set forth below, as reported by the Central Bank of Chile:

| | Daily Observed Exchange Rate (Ch$ per US$)(1) | |

| | Low(2) | | | High(2) | | | Average(3) | | | Period-end | |

Month ended | | | | | | | | | | | | | | | | |

March 2018 | | | 595.93 | | | | 609.58 | | | n.a. | | | | 603.39 | |

February 2018 | | | 588.28 | | | | 603.07 | | | n.a. | | | | 593.61 | |

January 2018 | | | 599.33 | | | | 609.49 | | | n.a. | | | | 603.25 | |

December 2017 | | | 614.75 | | | | 655.74 | | | n.a. | | | | 614.75 | |

November 2017 | | | 629.21 | | | | 645.32 | | | n.a. | | | | 645.32 | |

October 2017 | | | 619.68 | | | | 640.52 | | | n.a. | | | | 636.80 | |

Year ended December 31, | | | | | | | | | | | | | | | | |

2017 | | | 614.75 | | | | 679.05 | | | | 649.11 | | | | 614.75 | |

2016 | | | 645.22 | | | | 730.31 | | | | 676.67 | | | | 669.47 | |

2015 | | | 597.10 | | | | 715.66 | | | | 654.66 | | | | 710.16 | |

2014 | | | 527.53 | | | | 621.41 | | | | 570.34 | | | | 606.75 | |

2013 | | | 466.50 | | | | 533.95 | | | | 498.83 | | | | 524.61 | |

Source: Central Bank of Chile.

(2) | Exchange rates are the actual low and high, on a day-by-day basis for each period. |

(3) | The average of the exchange rates on the last day of each month during the period. |

As of April 24, 2018, the U.S. dollar Observed Exchange Rate was Ch$ 599.84 per US$ 1.00.

Calculation of the appreciation or devaluation of the Chilean peso against the U.S. dollar in any given period is made by determining the percent change between the reciprocals of the Chilean peso equivalent of US$ 1.00 at the end of the preceding period and the end of the period for which the calculation is being made. For example, to calculate the appreciation of the year-end Chilean peso in 2017, one determines the percentage of change between the reciprocal of Ch$ 669.47, the value of one U.S. dollar as of December 31, 2016, or 0.001494, and the reciprocal of Ch$ 614.75, the value of one U.S. dollar as of December 31, 2017, or 0.001627. In this example, the percentage change between the two periods is 8.9%, which represents the 2017 year-end appreciation of the Chilean peso against the 2016 year-end U.S. dollar. A positive percentage change means that the Chilean peso appreciated against the U.S. dollar, while a negative percentage change means that the Chilean peso devaluated against the U.S. dollar.

The following table sets forth the period-end rates for U.S. dollars for the years ended December 31, 2013 through December 31, 2017, based on information published by the Central Bank of Chile.

| | Ch$ per US$(1) | |

| | Period End | | | Appreciation (Devaluation) | |

| | (in Ch$) | | | (in %) | |

Year ended December 31, | | | | | | | | |

2017 | | | 614.8 | | | | 8.9 | |

2016 | | | 669.5 | | | | 6.1 | |

2015 | | | 710.2 | | | | (14.6 | ) |

2014 | | | 606.8 | | | | (13.5 | ) |

2013 | | | 524.6 | | | | (8.5 | ) |

Source: Central Bank of Chile.

(1) | Calculated based on the variation of period-end exchange rates. |

B. | Capitalization and Indebtedness. |

Not applicable.

13

C. | Reasons for the Offer and Use of Proceeds. |

Not applicable.

Chilean economic fluctuations as well as certain economic interventionist measures by governmental authorities may affect our results of operations and financial condition as well as the value of our securities.

All of our operations are located in Chile. Accordingly, our revenues are affected by the performance of the Chilean economy. If local, regional or worldwide economic trends adversely affect the Chilean economy, our financial condition and results from operations could be adversely affected. Moreover, insufficient cash flows for our subsidiaries could result in their inability to meet debt obligations and the need to seek waivers to comply with restrictive debt covenants and increasing costs for subsequent financings.

The Chilean government has exercised in the past, and continues to exercise, a substantial influence over many aspects of the private sector, which may result in changes to economic or other policies.

Future adverse developments in Chile or changes in policies regarding exchange controls, regulations and taxation may impair our ability to execute our strategic plans, which could adversely affect our results of operations and financial condition. Inflation, devaluation, social instability and other political, economic or diplomatic developments, could also reduce our profitability. In addition, Chilean financial and securities markets are influenced by economic and market conditions in other countries and may be affected by events in other countries, which could adversely affect the value of our securities.

Our businesses depend heavily on water supply, and the occurance of droughts, flooding, storms, oceanographic currents and other weather conditions and may adversely affect our operations and profitability.

Approximately 55% of our installed generation capacity in 2017 was hydroelectric. Accordingly, dry hydrological conditions could adversely affect our business, results of operations and financial condition. Our results have been adversely affected when hydrological conditions in Chile have been below their historical average.

While our subsidiary, Enel Generación, has entered into certain agreements with the Chilean government and local irrigators regarding the use of water for hydroelectric generation purposes, during periods of low water levels, if drought conditions persist or become worse, we may face increased pressure by the Chilean government or other third parties to further restrict our water use.

The below-average hydrological conditions not only reduce our ability to operate our hydroelectric plants at full capacity, but also may result in increased water transportation costs for the operation of the San Isidro thermal power plant (778 MW) for cooling purposes. In addition, thermal plant operating costs can be considerably higher than those of hydroelectric plants. Our operating expenses increase during these drought periods when thermal plants are used more frequently. We may need to buy electricity at higher spot prices in order to comply with our contractual supply obligations and the cost of these electricity purchases may exceed our contracted electricity sale prices, thus potentially producing losses from those contracts. For further information with respect to the effect of hydrology on our business and financial results, please refer to “Item 5. Operating and Financial Review and Prospects — A. Operating Results —1. Discussion of Main Factors Affecting Operating Results and Financial Condition of the Company —a. Generation Business.”

Droughts also indirectly affect the operation of our thermal plants, including our facilities that use natural gas, fuel oil or coal, in the following manner:

| • | Our thermal plants require water for cooling and droughts not only reduce the availability of water, but also increase the concentration of chemicals, such as sulfates in the water. The high concentration of chemicals in the water that we use for cooling increases the risk of damaging the equipment at our thermal plants as well as the risk of violating environmental regulations. As a result, we have had to purchase water from agricultural areas that are also experiencing water shortages. These water purchases may increase our operating costs and may require us to negotiate with the local communities. |

| • | Thermal power plants that burn natural gas generate emissions such as nitrogen oxide (NO), carbon dioxide (CO2) and carbon monoxide (CO) gases. When operating with diesel they release NO, sulfur dioxide (SO2) and particulate matter into the atmosphere. Coal fired plants generate emissions of SO2 and NO. Therefore, greater use of thermal plants during periods of drought generally increases the risk of producing a higher level of pollutants, which also would decrease our operating income due to the payment of so called “green taxes” (see “Environmental regulations may cause delays, impede the development of new projects, or increase the costs of operations and capital expenditures” below). |

14

It may take an extended period of time to fully recover from the drought that has been affecting the regions where most of our hydroelectric plants are located and new drought periods may recur in the future. A prolonged drought may exacerbate the risks described above and have a further adverse effect upon our business, results of operations and financial condition.

The distribution business is also affected by weather. Moderate temperatures, for instance, decrease heating in the winter months and air conditioning in the summer months, affecting energy consumption. On the other hand, with extreme temperatures, demand can increase significantly within a very short period of time, which in turn affects service and could result in service disruptions that are potentially subject to fines. Depending on weather conditions, results obtained by our distribution business can vary significantly from year to year. In addition, damage to one or more of our main electricity distribution installations or interruption to service caused by extreme weather events, earthquakes or other natural disasters could have a material adverse effect on our operations. For example, as a result of severe rainstorms in June 2017, with high wind gusts that brought down part of the electric network, 125,000 of our customers, or 7%, were affected adversely. In July 2017, a strong snowstorm that hit the Santiago Metropolitan Region, caused massive damage to the electrical infrastructure, and affected 342,000 of our customers, or 18%, and 17% of our feeders. This was the most damaging snowstorm in Santiago since 1970, and left parts of the capital without power for over a week. These events significantly increased our costs due to emergency responses including payments related to damage compensation, fines, line maintenance and tree trimming programs.

Governmental regulations may adversely affect our businesses.

Our businesses and the tariffs that we charge to our customers are subject to extensive regulation and these regulations may adversely affect our profitability. For example, governmental authorities might impose material rationing policies during droughts or prolonged failures of power facilities, which may adversely affect our business, results of operations and financial condition.

Governmental authorities may also delay the distribution tariff review process, or tariff adjustments may be insufficient to pass through all of our costs to customers. Similarly, electricity regulations issued by governmental authorities in Chile may affect the ability of our generation companies to collect revenues sufficient to cover their operating costs.

The inability of any company in our consolidated group to collect revenues sufficient to cover operating costs may affect the ability of that company to operate as a going concern and may otherwise have an adverse effect on our business, financial results and operations.

In 2014, the Chilean government implemented the Energy Agenda, with an emphasis on promoting non-conventional renewable energy (“NCRE”) sources aimed at diversifying conventional energy sources and reducing the cost of electricity. Solar and wind sources are the NCRE technologies most widely used. NCRE facilities dispatch energy at very low marginal costs, and substitute expensive sources, such as conventional thermal plants. However, wind and solar sources have higher intermittency since they can only generate electricity when the wind blows or the sun shines. Handling this intermittency requires integration and flexibility from the rest of the grid’s power plants. The National Electricity Coordinator (“CEN”) coordinates dispatch from all sources. The balance of production not supplied by hydro and NCRE plants comes from thermal plants, which are among the most expensive producers, and in some cases, are subject to operating restrictions. Authorities sometimes request that thermal generators reduce their “technical minimum power capacity,” the minimum capacity at which a power plant should be safely and permanently operated, and its “minimum operating time” as specified by the turbine manufacturer. A turbine that operates for less than the manufacturers’ recommended minimum time, or at less than the technical minimum power capacity, is subject to higher maintenance costs, which are not always recognized by the CEN. Generation below the technical minimum power capacity may also have adverse environmental effects. The CEN has the authority to audit power plant technical parameters, and impose fines or request injunctions.

Changes in the regulatory framework are often submitted to the legislators and administrative authorities and, some of these changes could have a material adverse impact on our business, results of operations and financial condition.

Regulatory authorities may impose fines on our subsidiaries due to operational failures or any breach of regulations.

Our electricity businesses are subject to regulatory fines for any breach of current regulations, including energy supply failures. Such fines may be imposed for a maximum of 10,000 Annual Tax Units (“UTA” in its Spanish acronym), or Ch$ 5.6 billion using the UTA as of December 31, 2017. Our electricity generation subsidiaries are supervised by local regulatory authorities and are subject to fines in cases where, in the opinion of the regulatory authority, operational failures affecting the regular energy supply to the system, including coordination issues, are the fault of the generator. Regulations establish a compensation fee to end customers when energy is interrupted more than the standard allowed time due to events or failures affecting transmission facilities. Compensation is a proportion of the energy not supplied with a minimum value between 20,000 UTA (Ch$ 11.3 billion) and the previous year's energy

15

sales revenues in the case of generators. Due to the consequences of electricity interruptions caused by extreme 2017 weather events, we paid Ch$ 2 billion in legal and Ch$ 3.4 billion in voluntary compensations to distribution customers without electricity for more than 24 hours, with a maximum of Ch$ 25,000 per customer, equivalent to customers’ average monthly consumption (240 kWh/month).

In 2015, the CDEC-SING audited GasAtacama’s thermal plant and reported its findings to the the Superintendence of Electricity and Fuels (“SEF”), which in August 2016 fined GasAtacama 10,000 UTA (Ch$ 5.6 billion as of December 31, 2017) for allegedly providing inaccurate information to the CDEC-SING. In 2017, Gener, a competitor, requested Enel Generación to pay US$ 65.8 million as compensation for their alleged overpayments to GasAtacama associated with the technical minimum power capacity reported by GasAtacama at 310 MW with a 30‑hour minimum operating time that was later estimated by the CEN at only 118 MW and just a 2‑hour minimum time. Further compensation claims from other market players may arise in the future and further fines to any of our plants could adversely affect our business, results of operations and financial condition.

In 2017, Enel Distribución was fined by the SEF for a total amount of 15,000 UTA (Ch$ 8.5 billion) due to various claims of infractions related to the extreme weather in June and July 2017. For further information on fines, please refer to Note 35 of the Notes to our consolidated financial statements.

We depend on payments from our subsidiaries to meet our payment obligations.

In order to pay our obligations, we rely on cash from dividends, loans, interest payments, capital reductions and other distributions from our subsidiaries. The ability of our subsidiaries to pay dividends, interest payments, loans and other distributions to us is subject to legal constraints such as dividend restrictions, fiduciary duties and limitations that may be imposed by local authorities, except for legal minimums.

Contractual Constraints. Distribution restrictions included in certain credit agreements of our subsidiaries may prevent dividends and other distributions to shareholders if they are not in compliance with certain financial ratios. Generally, our credit agreements prohibit any type of distribution if there is an ongoing default.

Operating Results of Our Subsidiaries. The ability of our subsidiaries to pay dividends or make loan payments or other distributions to us is limited by their operating results. To the extent that the cash requirements of any of our subsidiaries exceed their available cash, the subsidiary will not be able to make cash available to us.

Any of the situations described above could adversely affect our business, results of operations and financial condition.

We are involved in litigation proceedings.

We are involved in various litigation proceedings, which could result in unfavorable decisions or financial penalties against us. We will continue to be subject to future litigation proceedings, which could cause material adverse consequences to our business. Our financial condition or results of operations could be adversely affected if we are unsuccessful in defending lawsuits and proceedings against us. For further information on litigation proceedings, please see Note 33.3 of the Notes to our consolidated financial statements.

Environmental regulations may cause delays, impede the development of new projects, or increase the costs of operations and capital expenditures.

Our operating subsidiaries are subject to environmental regulations which, among other things, require us to perform environmental impact studies for future projects and obtain construction and operating permits from both local and national regulators. The approval of these environmental impact studies may be withheld by governmental authorities and therefore their processing time may be longer than expected.

Environmental regulations for existing and future generation capacity have become stricter and now require increased capital investments. For example, we performed improvements to our Tarapacá power plant for which the estimated total investment in reducing and monitoring emissions is Ch$ 68,240 million. Any delay in meeting the standards constitutes a violation of the regulations. Failure to certify the original implementation and ongoing emission standard requirements of such monitoring system may result in significant penalties and sanctions or legal claims for damages. We expect that even more restrictive emission limits will be established in the future. Between 2016 and 2017, Enel Generación paid fines amounting to Ch$ 4.9 billion for non-

16

compliance with environmental license requirements and failure to submit the monitoring reports for our Bocamina, Huasco and Diego de Almagro thermal plants in past years.

The 2014 tax reform law established an annual green tax on stationary power generators, such as thermal generators, based on their emission of pollutants in the previous year. This green tax is payable in 2018 and is applicable to all our thermal facilities. Our plants have reported their emissions during 2017, recognizing a tax liability as of December 31, 2017 in the amount of Ch$ 17.3 billion by Enel Generación, which was paid in April 2018. Tax expense may continue to increase in the future, and discourage thermal electricity generation.

Our power plants, both in operation and under development, may encounter significant opposition from different groups that may delay their development, increase costs, damage our reputation and potentially result in impairment of our goodwill with stakeholders.

Our reputation is the foundation of our relationship with key stakeholders. If we are unable to effectively manage real or perceived issues that could impact us negatively, our business, results of operations and financial condition could be adversely affected.

In 2015, Chilean governmental authorities established procedures that require all stakeholders to participate in the preliminary phase of the evaluation process. Plants built before the adoption of these rules that were not submitted to local consultation may face opposition from several stakeholders, such as ethnic groups, environmental groups, land owners, farmers, local communities and political parties, among others, any of whom may impact the sponsoring company’s reputation and goodwill. The projects that require consultation with local stakeholders in their evaluation process may be rejected or their development may be impeded or slowed down. Our stakeholders may also seek injunctive or other relief, which could negatively impact us if they are successful. Moreover, projects that do not require consultation with local stakeholders may be subject to intervention or suffer continuous resistance, delaying their approval process or development. In 2013‑2016, the Bocamina II power plant encountered substantial opposition from local fishermen’s unions that claimed that our facility negatively affected marine life and caused pollution, which resulted in the interruption of the operation of the power plant for over a year. In July 2015, the Bocamina II power plant resumed operations but then a second group of fishermen illegally occupied a high-voltage pylon which supports the transmission lines owned by Transelec S.A. and serve our power plants. As a consequence, both Bocamina I and II plants were temporarily shut down. The financial effects of this illegal occupation and electricity transmission interruption amounted to a Ch$ 2.8 billion reduction in operating income. Such groups may have the ability to block our power plants and directly affect our results.

The operation of our thermal power plants, especially coal power plants, may also affect our goodwill with stakeholders, due to greenhouse gas emissions, which could adversely affect the environment.

Damage to our reputation may exert considerable pressure on regulators, creditors, and other stakeholders and ultimately lead to projects and operations that may be abandoned, causing our share prices to drop and hindering our ability to attract and retain valuable employees, any of which could result in an impairment of our goodwill with stakeholders.

Power plant construction may encounter delays and significant cost over-runs.

Our power plant projects may be delayed in obtaining regulatory approvals, or may face shortages and increases in the price of equipment, materials or labor, and they may be subject to construction delays, strikes, adverse weather conditions, natural disasters, civil unrest, accidents, and human error. Any such event could adversely impact our results of operations and financial condition.

Market conditions at the time when the projects are initially approved may significantly differ from those that prevail when the projects are completed, which in some cases make such projects commercially unfeasible. This has been the case of many of our former projects, which were initially planned under completely different market conditions with higher energy prices prevailing in the market and less competition than currently exists, especially with the growth of NCRE sources. Deviations in these assumptions, including the estimation of the timing and expenditures related to these projects, may lead to cost over-runs and a completion time widely exceeding our initial estimates, which in turn may have a material adverse effect on our business, results of operation and financial condition. In 2016‑2017, we recorded over Ch$ 90 billion in impairment losses and write-offs due to the abandonment of such projects.

We are currently constructing the Los Cóndores project, a 150 MW run-of-the-river hydroelectric plant. We began the initial evaluation of Los Cóndores, which also includes a transmission line, in 1991, and we originally expected to begin operations in 2012. The project has been delayed for many reasons, including its redesign due to a technological construction change, which required a

17

new emviromental approval. Finally, construction began during 2014 and the project’s commercial start-up has now been deferred until 2020, with an estimated aggregate investment of US$ 940 million, significantly greater than the initial project, although the two are not completely comparable because of the different design and the higher standards employed today.

The locations where we may develop new projects are also sometimes highly challenging in terms of geographical topography, in some cases in mountain slopes with very limited access. These factors may also lead to significant delays and cost overruns.

Political events or financial or other crises in any region worldwide can have a significant impact in Chile, and consequently, may adversely affect our operations as well as our liquidity.

Chile is vulnerable to external shocks, including financial and political events, which could cause significant economic difficulties and affect growth. For example, the 2016 U.S. presidential election considerably increased the volatility of financial markets worldwide due to the uncertainty of political decisions. New policies adopted by the U.S. could affect world markets and global trade and result in renewed volatility, especially in commodity prices. Instability in the Middle East or in any other major oil producing region could also result in higher fuel prices worldwide, which in turn could increase the cost of fuel for our thermal generation plants and adversely affect our results of operations and financial condition. Even temporary or threatened U.S. government shut‑downs, such as those of early 2018, can have a very adverse effect on the timing, execution and increased expense associated with our major transactions and reorganizations.

An international financial crisis and its disruptive effects on the financial industry could adversely impact our ability to obtain new financings on the same historical terms and conditions that we have benefited from to date. Political events or financial or other crises could also diminish our ability to access the Chilean and international capital markets or increase the interest rates available to us. Reduced liquidity could, in turn, adversely affect our capital expenditures, our long term investments and acquisitions, our growth prospects and our dividend payout policy.

We may be unable to enter into suitable acquisitions or successfully integrate businesses that we acquire.

On an ongoing basis, we review acquisition prospects that may increase our market coverage or supplement our existing businesses, though there can be no assurance that we will be able to identify and consummate suitable acquisition transactions in the future. The acquisition and integration of independent companies that we do not control is generally a complex, costly and time-consuming process and requires significant efforts and expenditures. If we consummate an acquisition, it could result in the incurrence of substantial debt and assumption of unknown liabilities, the potential loss of key employees, amortization expenses related to tangible assets and the diversion of management’s attention from other business concerns. In addition, any delays or difficulties encountered in connection with acquisitions and the integration of multiple businesses could have a material adverse effect on our business, financial condition or results of operations.

For example, our integration with EGPL may be difficult and expensive. The merger with EGPL involves the integration of a mature business, as is the case of our conventional energy business, which we develop through Enel Generación, with EGPL’s non-conventional renewable energy business. Our goal in integrating the operations is to increase the revenues and earnings of the combined businesses and, as a combined company, to increase our ability to satisfy the demands of our customers. In so doing, we may encounter substantial difficulties in integrating our operations, and could incur substantial costs as a result of, among other things:

| • | inconsistencies in standards, controls, procedures and policies, business cultures and compensation structures between us and EGPL and the need to implement, integrate and harmonize various business-specific operating procedures and systems, as well as our financial, accounting, information and other systems and those of EGPL; |

| • | diversion of management’s attention from their other responsibilities as a result of the need to deal with integration issues; |

| • | failure to retain our customers and suppliers and those of EGPL; |

| • | difficulties in achieving full utilization of our assets and resources and those of EGPL; and |

| • | complications in retaining key employees (who may depart because of issues relating to the uncertainty and difficulty of integration or general discontent) or in efficiently managing the larger and broader organization. |

18

Under any of these circumstances, the business growth opportunities, revenue benefits and other benefits anticipated by us to result from the completion of the 2018 Reorganization may not be achieved as expected. To the extent that we incur higher integration costs or achieve lower revenue benefits than expected, our results of operations and financial condition may suffer. In addition, the diversion of management attention and any difficulties encountered from this merger could also increase costs or reduce our revenues, earnings and operating results. Any delays encountered in the integration process could have an adverse effect on our revenues, level of expenses, operating results and financial condition, which may adversely affect the value of our securities.

Our business and profitability could be adversely affected if water rights are denied or if water concessions are granted with limited duration.

We own water rights granted by the Chilean Water Authority (Dirección General de Aguas) for the supply of water from rivers and lakes near our production facilities. Under current law, these water rights are (i) for unlimited duration, (ii) absolute and unconditional property rights and (iii) not subject to further challenge. Chilean generation companies must pay an annual license fee for unused water rights. New hydroelectric facilities are required to obtain water rights, the conditions of which may impact design, timing or profitability of a project.

In addition, Chilean Congress has discussed amendments to the Water Code since 2014 in order to prioritize the use of water by defining its access as a basic human need that must be guaranteed by the State. The amendment will establish that water use for human consumption, domestic subsistence and sanitation will always take precedence, in both the granting and limiting the exercise of rights of exploitation. Under the proposal: (i) new water use concessions would be limited to 30 years, which would be extendable with respect to water rights actually used during the 30-year period, unless the Chilean Water Authority demonstrates the water rights have not been used effectively; (ii) new non-consumptive water rights would expire if the holder does not exercise the rights within eight years; (iii) existing non-consumptive water rights which have not been used would expire within eight years from the date of enactment of the new Water Code; and (iv) the preservation of water environmental flows to protect the ecosystem was added for both consumptive and non-consumptive water use and empowers the Chilean Water Authority to mandate an environmental flow requirement for existing water rights. Restrictions enacted to preserve environmental flows would reduce water availability for generation purposes.

Any limitations on our water rights, our need for additional water rights, or our unlimited duration of water concessions could have a material adverse effect on our hydroelectric development projects and our profitability.

Foreign exchange risks may adversely affect our results and the U.S. dollar value of dividends payable to ADS holders.

The Chilean peso has been subject to devaluations and appreciations against the U.S. dollar and may be subject to significant fluctuations in the future. Historically, a significant portion of our consolidated indebtedness has been denominated in U.S. dollars. Although a substantial portion of our operating cash flows is linked to U.S. dollars (primarily coming from the generation business), we generally have been and will continue to be exposed to fluctuations of the Chilean peso against the U.S. dollar because of time lags and other limitations to peg our tariffs to the U.S. dollar and the potential difficulty of obtaining loans in the same currency as our operating cash flow.

Because of this exposure, the U.S. dollar value of cash generated by our subsidiaries can decrease substantially due to peso devaluations against the U.S. dollar. Future volatility in the exchange rate of the currency in which we receive revenues or incur expenditures may adversely affect our business, results of operations and financial condition.

Our long-term electricity sale contracts are subject to fluctuations in the market prices of certain commodities, energy and other factors.

In our generation business, we have economic exposure to fluctuations in the market prices of certain commodities as a result of the long term electricity sales contracts into which we have entered, and the fact that currently 97% of our expected annual generation is sold under contracts with terms of at least five years. We have material obligations as selling parties under long term fixed-price electricity sales contracts. Prices in these contracts are indexed according to different commodities, exchange rates, inflation, and the market price of electricity. Adverse changes to these indices would reduce the rates we charge under our long term fixed-price electricity sales contracts, which could adversely affect our business, results of operations and financial condition.

In our distribution business, we are also exposed to fluctuations in electricity prices. Since 2016, some customers who had freely chosen to be subject to regulated tariffs have now been switching to the unregulated tariff regime instead due to the lower prices. These customers are tendering their electricity needs, either directly or in association with other customers, because regulated tariffs

19

are currently higher than unregulated prices, given that the former are based on contracts tendered in the past at higher prices. Lower market prices might reduce the number of customers that choose regulated tariffs, and customers may choose an alternative energy provider, reducing our number of customers, which could adversely affect our business, results of operations and financial condition.

Our controlling shareholder may exert influence over us and may have a different strategic view for our development than that of our minority shareholders.

Enel owns 61.9% of our voting shares as of the date of this Report and after giving effect to the 2018 Reorganization (and excluding treasury stock which will be cancelled). Enel, our controlling shareholder, has the power to determine the outcome of substantially all material matters that require shareholder votes in accordance with Chilean corporate law, such as the election of the majority of our board members and, subject to contractual and legal restrictions, the adoption of our dividend policy. Enel also exercises significant influence over our business strategy and operations. Its interests may, in some cases, differ from those of our minority shareholders. Certain conflicts of interest affecting Enel in these matters may be resolved in a manner that is different from interests of our company or our minority shareholders.

Our electricity business is subject to risks arising from natural disasters, catastrophic accidents and acts of terrorism, which could adversely affect our operations, earnings and cash flow.

Our primary facilities include power plants and distribution assets. Our facilities may be damaged by earthquakes, flooding, fires, and other catastrophic disasters arising from natural or accidental human causes, as well as acts of protest, vandalism, riot, and terrorism. A catastrophic event could cause disruptions in our business, significant decreases in revenues due to lower demand or significant additional costs to us not covered by our business interruption insurance. There may be lags between a major accident or catastrophic event and the final reimbursement from our insurance policies, which typically carry a deductible and are subject to per event policy maximum amounts.

We are subject to financing risks, such as those associated with funding our new projects and capital expenditures, and risks related to refinancing our maturing debt; we are also subject to debt covenant compliance, all of which could adversely affect our liquidity.

As of December 31, 2017, our consolidated interest-bearing debt totaled Ch$ 778 billion.

Our consolidated interest-bearing debt had the following maturity profile:

| • | Ch$ 15 billion in 2019-2020; |

| • | Ch$ 16 billion in 2021‑2022; and |

| • | Ch$ 730 billion thereafter. |

Some of our debt agreements are subject to (1) financial covenants, (2) affirmative and negative covenants, (3) events of default and (4) mandatory prepayments for contractual breaches, among other provisions. A significant portion of our subsidiaries’ financial indebtedness is subject to cross default provisions, which have varying definitions, criteria, materiality thresholds and applicability with respect to subsidiaries that could give rise to such a cross default. We incurred debt in connection with the 2018 Reorganization, primarily to finance the Tender Offer. As a result, we have recently entered into a debt agreement that is subject to cross default provisions.

In the event that we or our subsidiaries breach any of these contractual provisions, our debtholders may demand immediate repayment, and a significant portion of our indebtedness could become due and payable. We may be unable to refinance our indebtedness or obtain such refinancing on terms acceptable to us. In the absence of such refinancing, we could be forced to dispose of assets in order to make the payments due on our indebtedness under circumstances that might not be favorable to obtaining the best price for such assets. Furthermore, we may be unable to sell our assets quickly enough, or at sufficiently high prices, to enable us to make such payments.

We may also be unable to raise the necessary funds required to finish our projects under development or under construction. Market conditions prevailing at the moment we require these funds or other unforeseen project costs can compromise our ability to finance these projects and expenditures.

20

Our inability to finance new projects or capital expenditures or to refinance our existing debt could adversely affect our results of operation and financial condition.

We rely on electricity transmission facilities that we do not own or control. If these facilities do not provide us with an adequate transmission service, we may not be able to deliver the power we sell to our final customers.

We depend on transmission facilities owned and operated by other unaffiliated power companies to deliver the electricity we sell. This dependence exposes us to several risks. If transmission is disrupted, or transmission capacity is inadequate, we may be unable to sell and deliver our electricity. If a region’s power transmission infrastructure is inadequate, our recovery of sales costs and profits may be insufficient. If restrictive transmission price regulation is imposed, transmission companies upon whom we rely may not have sufficient incentives to invest in expansion of their transmission infrastructure, which could adversely affect our operations and financial results. The construction of new transmission lines may take longer than in the past, mainly because of social and environmental requirements that are creating uncertainty on the probability of completing the projects.

There have been blackout events in the past due to the failure of transmission lines, which exposed weaknesses in the transmission grid and its need for expansion and technological improvements to increase its reliability. Additional failures of transmission lines may occur in the future.

Any such disruption or failure of transmission facilities could interrupt our business, which could adversely affect our results of operations and financial condition.

Our business may experience adverse consequences if we are unable to reach satisfactory collective bargaining agreements with our unionized employees.

A large percentage of our employees are members of unions and have collective bargaining agreements that must be renewed on a regular basis. Our business, financial condition and results of operations could be adversely affected by a failure to reach agreement with any labor union representing such employees or by an agreement with a labor union that contains terms we view as unfavorable. Chilean law provides legal mechanisms for judicial authorities to impose a collective agreement if the parties are unable to come to an agreement, which may increase our costs beyond what we have budgeted.