UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2015 |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 001-36565

INNOCOLL HOLDINGS PUBLIC LIMITED COMPANY

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

Republic of Ireland

(Jurisdiction of incorporation or organization)

Innocoll Holdings plc

Unit 9, Block D

Monksland Business Park

Monksland, Athlone

Ireland

+353 (0) 90 6486834

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Name of each exchange on which

registered |

| | |

| Ordinary Shares, $0.01 par value per share | NASDAQ Global Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

As of December 31, 2015, the Registrant’s predecessor, Innocoll AG, had outstanding 1,837,493 ordinary shares, notional par value €1.00 per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.¨ Yesx No

If the report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.¨ Yesx No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.x Yes¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).x Yes¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ☐ | |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ¨ | International Financial Reporting

Standards as issued by the

International Accounting Standards

Board x | Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.¨ Item 17¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).¨ Yesx No

TABLE OF CONTENTS

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains forward-looking statements that involve substantial risks and uncertainties. All statements, other than statements of historical facts, included in this annual report regarding our strategy, future operations, regulatory process, future financial position, future revenue, projected costs, prospects, plans, objectives of management and expected market growth are forward-looking statements. The words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “project,” “will,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words.

The forward-looking statements in this annual report on Form 20-F include, among other things, statements about:

| · | our plans to develop and manufacture XaraColl, Cogenzia and our other product candidates; |

| · | the results of clinical trials for XaraColl, Cogenzia and our other product candidiates; |

| · | the timing of, and our ability to obtain, regulatory approval of XaraColl, Cogenzia and our other product candidates; |

| · | the timing of our anticipated launches of XaraColl, Cogenzia and our other product candidates; |

| · | the rate and degree of market acceptance of XaraColl, Cogenzia and our other product candidates; |

| · | the size and growth of the potential markets for XaraColl, Cogenzia and our other product candidates and our ability to serve those markets; |

| · | our manufacturing and marketing capabilities; |

| · | the timing of, and our ability to obtain, regulatory approvals for the expansion of our manufacturing facility; |

| · | regulatory developments in the United States and foreign countries; |

| · | our ability to obtain and maintain the scope, duration and protection of our intellectual property rights; |

| · | statements concerning our corporate and tax domiciles and potential changes to them, including potential tax charges; |

| · | the accuracy of our estimates regarding expenses and capital requirements; and |

| · | the loss of key scientific or management personnel. |

We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements, and you should not place undue reliance on our forward-looking statements. Actual results or events could differ materially from the plans, intentions and expectations disclosed in the forward-looking statements we make. We have included important factors in the cautionary statements included in this annual report, particularly the factors described in the “Item 3. Key Information—D. Risk Factors” section of this annual report, that could cause actual results or events to differ materially from the forward-looking statements that we make. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures or investments that we may make.

You should read this annual report and the documents that we have filed as exhibits to this annual report, completely and with the understanding that our actual future results may be materially different from what we expect. We do not assume any obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

SERVICE OF PROCESS AND ENFORCEMENT OF CIVIL LIABILITIES

Innocoll Holdings plc is a public limited company formed under Irish law, and its registered offices and all of its assets are located outside of the United States. In addition, certain members of our board, our senior management and the experts named herein are residents of jurisdictions other than the United States, namely Ireland, the United Kingdom and Germany. As a result, it may not be possible for you to effect service of process within the United States upon Innocoll Holdings plc or these individuals to enforce judgments obtained in U.S. courts based on the civil liability provisions of the U.S. securities laws against Innocoll in the United States.

In addition, it may not be possible to enforce court judgments obtained in the United States against us in Ireland based on the civil liability provisions of the U.S. federal or state securities laws. We have been advised by William Fry, our Irish counsel, that the United States currently does not have a treaty with Ireland providing for the reciprocal recognition and enforcement of judgments in civil and commercial matters.

The following requirements must be met before a judgment of a U.S. court will be deemed to be enforceable in Ireland:

| · | the judgment must be for a definite sum; |

| · | the judgment must be final and conclusive; and |

| · | the judgment must be provided by a court of competent jurisdiction. |

An Irish court may also exercise its right to refuse enforcement if the U.S. judgment was obtained by fraud, if the judgment violates Irish public policy, if the judgment is in breach of natural justice or if it is irreconcilable with an earlier foreign judgment. There is some uncertainty as to whether the courts of Ireland would recognize or enforce judgments of U.S. courts obtained against us or our directors or officers based on the civil liabilities provisions of the U.S. federal or state securities laws or hear actions against us or those persons based on those laws. Therefore, a final judgment for the payment of money rendered by any U.S. federal or state court based on civil liability, whether or not based solely on U.S. federal or state securities laws, would not automatically be enforceable in Ireland.

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

Innocoll AG, a German stock corporation, which had American Depository Shares, or ADSs, listed on the Nasdaq Global Market (“Innocoll Germany”), held an Extraordinary General Meeting of Shareholders in Munich, Germany on January 30, 2016, in which its shareholders considered and approved a proposal for a cross-border merger between Innocoll Germany and Innocoll Holdings plc, a public limited company formed under Irish law (“Innocoll Ireland”), with Innocoll Germany being the disappearing entity and Innocoll Ireland being the surviving entity in a merger by acquisition (the “Merger”).

On March 16, 2016, Innocoll Germany merged with Innocoll Ireland by way of a European cross-border merger with Innocoll Ireland being the surviving company. Upon the effectiveness of the Merger, we terminated Innocoll Germany’s ADS facility and each cancelled ADS effectively became an entitlement to receive one ordinary share of Innocoll Ireland. Holders of Innocoll Germany ordinary shares received 13.25 ordinary shares of Innocoll Ireland in respect of each share held of Innocoll Germany. Simultaneous with this transaction, Innocoll Ireland listed its ordinary shares on the Nasdaq Global Market under the symbol “INNL”, which we previously used for Innocoll Germany’s ADSs. The Merger effectively resulted in Innocoll Ireland becoming the publicly-traded parent of the Innocoll group of companies carrying on the same business as that conducted by Innocoll Germany prior to the Merger.

The financial and other information presented in this annual report as of December 31, 2015, including audited financial information, is the information of Innocoll AG, our predecessor. The audited financial statements of Innocoll AG contained in this annual report were prepared in accordance with IFRS as issued by the IASB, audited in accordance with the standards of the Public Company Accounting Oversight Board and approved by the board of Innocoll AG prior to the Merger. Innocoll Holdings plc intends to prepare its financial information in accordance with US GAAP beginning with the first quarter of 2016. As a result of this transition, the Company may report first quarter results at a later date than it has in the past.

Except where indicated to the contrary, or the context suggests otherwise, all share and per share information: (i) not presented in the financial statements or financial statement data refers to ordinary shares of Innocoll Holdings plc, and (ii) included in the financial statements and financial statement data for Innocoll AG refers to ordinary shares of Innocoll Germany prior to the Merger.

In this annual report, unless the context otherwise indicates, Innocoll Holdings plc, a public limited company formed under Irish law, is referred to as Innocoll. Innocoll together with its direct and indirect wholly owned subsidiaries as of the time relevant to the applicable reference are collectively referred to as the Innocoll Group. Notwithstanding that the historical audited financial statements prepared in accordance with IFRS and presented herein is the information of Innocoll AG, our predecessor, Innocoll and its current direct and indirect wholly owned subsidiaries are collectively referred to as “we,” “us,” “our,” “Innocoll” or the “Company.”

| A. | SELECTED FINANCIAL DATA |

Financial information in this annual report is the information of Innocoll AG, our predecessor. The audited financial statements of Innocoll AG contained in this annual report were prepared in accordance with IFRS. Innocoll Holdings plc intends to prepare its financial information in accordance with US GAAP.

We present below our selected historical financial and operating data as of and for each of the years in the three-year period ended December 31, 2015. The financial data as of December 31, 2015 and 2014 and for the years ended December 31, 2015, 2014 and 2013 have been derived from our audited financial statements and the related notes, which are included elsewhere in this annual report and which have been prepared in accordance with IFRS as issued by the IASB and audited in accordance with the standards of the Public Company Accounting Oversight Board (United States). Pursuant to Section 13(a) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), we are permitted to provide fewer than five years of selected financial data.

Our historical results are not necessarily indicative of the financial results to be expected in any future periods. You should read this information in conjunction with “Item 5. Operating and Financial Review and Prospects,” and our financial statements and related notes, each included elsewhere in this annual report.

Amounts presented in U.S. dollars are not audited and have been converted from euros to U.S. dollars solely for the convenience of the reader at an exchange rate of $1.0887 per euro, the exchange rate on December 31, 2015. See “Exchange Rate Information” below.

The financial data have been prepared in accordance with IFRS, unless otherwise noted.

| | | | | | Years Ended December 31, | |

| | | 2015 | | | 2015 | | | 2014 | | | 2013 | |

| | | | | | (in thousands, except for per share data) | |

| Consolidated Statement of Comprehensive Income Data: | | | | | | | | | | | | | | | | |

| Revenue | | | | | | | | | | | | | | | | |

| Revenue – continuing operations | | $ | 2,816 | | | € | 2,587 | | | € | 4,497 | | | € | 3,546 | |

| Cost of sales | | | (5,228 | ) | | | (4,802 | ) | | | (5,573 | ) | | | (4,551 | ) |

| Gross loss | | | (2,412 | ) | | | (2,215 | ) | | | (1,076 | ) | | | (1,005 | ) |

| Operating expense | | | | | | | | | | | | | | | | |

| Research and development expenses | | | (29,262 | ) | | | (26,878 | ) | | | (3,252 | ) | | | (1,663 | ) |

| General and administrative expenses | | | (20,667 | ) | | | (18,983 | ) | | | (11,687 | ) | | | (4,121 | ) |

| Other operating income/(expense) – net | | | 4,220 | | | | 3,876 | | | | (39 | ) | | | (154 | ) |

| Total operating expense – net | | | (45,709 | ) | | | (41,985 | ) | | | (14,978 | ) | | | (5,938 | ) |

| Loss from operating activities – continuing operations | | | (48,121 | ) | | | (44,200 | ) | | | (16,054 | ) | | | (6,943 | ) |

| Finance income/(expense) | | | 1,544 | | | | 1,418 | | | | (4,535 | ) | | | (6,949 | ) |

| Other income | | | - | | | | - | | | | 75 | | | | 16,073 | |

| (Loss)/profit before income tax | | | (46,577 | ) | | | (42,782 | ) | | | (20,514 | ) | | | 2,181 | |

| Income tax expense | | | (400 | ) | | | (367 | ) | | | (152 | ) | | | (72 | ) |

| (Loss)/profit for the period – all attributable to equity holders of the company | | | (46,977 | ) | | | (43,149 | ) | | | (20,666 | ) | | | 2,109 | |

| Currency translation adjustment | | | (566 | ) | | | (520 | ) | | | (623 | ) | | | 155 | |

| Total comprehensive (loss)/income | | $ | (47,543 | ) | | € | (43,669 | ) | | € | (21,289 | ) | | € | 2,264 | |

| (Loss)/earnings per share: | | | | | | | | | | | | | | | | |

| Basic | | | (27.9 | ) | | | (25.6 | ) | | | (28.1 | ) | | | 47.0 | |

| Diluted | | | (27.9 | ) | | | (25.6 | ) | | | (28.1 | ) | | | (9.5 | ) |

| Basic (loss) per ADS(1) | | | (2.1 | ) | | | (1.9 | ) | | | (2.1 | ) | | | | |

| Diluted (loss) per ADS(1) | | | (2.1 | ) | | | (1.9 | ) | | | (2.1 | ) | | | | |

(1) For the years ended December 31, 2015 and 2014 we excluded the dilutive effect of potentially exercisable instruments in issue from the computation of the diluted net loss and diluted weighted-average shares outstanding as the effect would be anti-dilutive.

| | | | | | As of December 31, | |

| | | 2015 | | | 2015 | | | 2014 | | | 2013 | |

| | | | | | (in thousands, except per share data) |

| Consolidated Statement of Financial Position Data: | | | | | | | | | | | | | | | | |

| Current assets | | $ | 48,558 | | | € | 44,602 | | | € | 47,495 | | | € | 4,824 | |

| Total assets | | | 56,977 | | | | 52,335 | | | | 48,733 | | | | 5,556 | |

| Current liabilities | | | (16,913 | ) | | | (15,535 | ) | | | (6,899 | ) | | | (9,048 | ) |

| Long term debt | | | (16,400 | ) | | | (15,064 | ) | | | - | | | | (63,026 | ) |

| Other non-current liabilities | | | (11,547 | ) | | | (10,606 | ) | | | (7,300 | ) | | | (1,055 | ) |

| Total equity attributable to equity holders of the company | | | 12,117 | | | | 11,130 | | | | 34,534 | | | | (67,573 | ) |

| Total equity and liabilities | | | 56,977 | | | | 52,335 | | | | 48,733 | | | | 5,556 | |

Other Data:

The tables below include a reconciliation of our GAAP results to non-GAAP results for the years ended December 31, 2015, 2014 and 2013. We define adjusted non-GAAP earnings per share as basic and diluted earnings per share excluding share based payments, fair value expense on warrants and reversal of impairment of property, plant and equipment. We believe adjusted non-GAAP earnings per share is meaningful to our investors to enhance their understanding of our financial condition and results. We believe that non-GAAP earnings per share excluding these non-cash items may provide securities analysts, investors and other interested parties with a useful measure of our operating performance and cash requirements. Disclosure in this annual report of non-GAAP earnings per share, which is a non-IFRS financial measure, is intended as a supplemental measure of our performance that is not required by, or presented in accordance with, IFRS. Non-GAAP earnings per share should not be considered as an alternative to earnings per share, profit (loss) or any other performance measure derived in accordance with IFRS. Our presentation of adjusted earnings per share should not be construed to imply that our future results will be unaffected by unusual non-cash or non-recurring items.

For the year ended December 31, 2015 the reconciliation primarily relates to non-cash expenses in the amount of €4.8 million with respect to share-based compensation, €3.7 million with respect to fair value expense on warrants and (€3.9) million with respect to the reversal of impairment of property, plant and equipment. On a non-GAAP-basis, the net loss for the year ended December 31, 2015 was €38.5 million, or €22.9 per share of Innocoll AG, compared to a net loss of €9.3 million, or €12.6 per share of Innocoll AG for the year ended December 31, 2014.

| | | Years ended December 31, | |

| | | 2015 | | | 2015 | | | 2014 | | | 2013 | |

| | | (in thousands, except for per share data) | |

| Numerator for non-GAAP (loss)/earnings per share: | | | | | | | | | | | | | | | | |

| Net (loss)/earnings – basic | | $ | (46,977 | ) | | € | (43,149 | ) | | € | (20,666 | ) | | € | 2,109 | |

| Share based payments | | | 5,199 | | | | 4,775 | | | | 5,149 | | | | - | |

| Reversal of impairment of property, plant & equipment | | | (4,220 | ) | | | (3,876 | ) | | | - | | | | - | |

| Fair value expense on warrants | | | 4,066 | | | | 3,735 | | | | 6,265 | | | | 205 | |

| Non-GAAP net (loss)/earnings - basic | | | (41,932 | ) | | | (38,515 | ) | | | (9,252 | ) | | | 2,314 | |

| | | | | | | | | | | | | | | | | |

| Adjustment to net earnings for interest on convertible preferred shares | | | - | | | | - | | | | - | | | | 4,728 | |

| Adjustment to net earnings for interest on convertible promissory notes | | | - | | | | - | | | | - | | | | 1,918 | |

| Adjustment for gain on settlement of promissory notes and preferred stock | | | - | | | | - | | | | - | | | | (15,903 | ) |

| Non-GAAP net (loss) – diluted | | | (41,932 | ) | | | (38,515 | ) | | | (9,252 | ) | | | (6,943 | ) |

| | | | | | | | | | | | | | | | | |

| Denominator – number of shares: | | | | | | | | | | | | | | | | |

| Weighted-average shares outstanding – basic | | | 1,685,088 | | | | 1,685,088 | | | | 735,416 | | | | 44,848 | |

| Dilutive common stock issuable upon conversion of preferred shares(1) | | | | | | | | | | | - | | | | 547,195 | |

| Dilutive common stock issuable upon conversion of promissory notes (1) | | | - | | | | - | | | | - | | | | 160,246 | |

| Weighted-average shares outstanding – diluted | | | 1,685,088 | | | | 1,685,088 | | | | 735,416 | | | | 752,289 | |

| | | | | | | | | | | | | | | | | |

| Non-GAAP (loss)/earnings per share: | | | | | | | | | | | | | | | | |

| Basic | | | (24.9 | ) | | | (22.9 | ) | | | (12.6 | ) | | | 51.6 | |

| Diluted | | | (24.9 | ) | | | (22.9 | ) | | | (12.6 | ) | | | (9.2 | ) |

| | | | | | | | | | | | | | | | | |

| Non-GAAP (loss)/earnings per ADS(2): | | | | | | | | | | | | | | | | |

| Basic | | | (1.9 | ) | | | (1.7 | ) | | | (1.0 | ) | | | | |

| Diluted | | | (1.9 | ) | | | (1.7 | ) | | | (1.0 | ) | | | | |

(1) For the years ended December 31, 2015 and December 31, 2014, we excluded the dilutive effect of potentially exercisable instruments in issue from the computation of the diluted net loss and diluted weighted-average shares outstanding as the effect would be anti-dilutive.

(2) Prior to the termination of the ADS facility, one ordinary share of Innocoll AG represented 13.25 ADSs. Upon consummation of the Merger, each ADS of Innocoll AG was exchanged for one ordinary share of Innocoll Holdings plc. Going forward, Innocoll Holdings plc’s earnings/(loss) per share calculation will be equivalent to the earnings/(loss) per ADS calculation of Innocoll AG.

Exchange Rate Information

Our business to date has been conducted primarily in the European Union, or EU, and we prepare our consolidated financial statements in euros. All references in this annual report to “U.S. dollars” or “$” are to the legal currency of the United States and all references to “€“or “euro” are to the currency introduced at the start of the third stage of the European economic and monetary union pursuant to the treaty establishing the European Community, as amended. Solely for the convenience of the reader, unless otherwise indicated, all amounts in U.S. dollars have been converted from euros to U.S. dollars at an exchange rate of $1.0887 per euro, the official exchange rate quoted as of December 31, 2015 by the European Central Bank. Such U.S. dollar amounts are not necessarily indicative of the amounts of U.S. dollars that could actually have been purchased upon exchange of euros at the dates indicated. Fluctuations in the exchange rate between the U.S. dollar and the euro will affect the U.S. dollar amounts received by owners of our ordinary shares on conversion of dividends, if any, paid in euros on the ordinary shares and will affect the U.S. dollar price of our ordinary shares on the NASDAQ Global Market. The following table presents information on the exchange rates between the U.S. dollar and the euro for the periods indicated. The rates set forth below are provided solely for your convenience and may differ from the actual rates used in the preparation of the financial statements included in this annual report and other financial data appearing in this annual report.

| Year Ended December 31, | | High | | | Low | | | Average | | | Year end | |

| 2011 | | $ | 1.4882 | | | $ | 1.2889 | | | $ | 1.3920 | | | $ | 1.2939 | |

| 2012 | | $ | 1.3454 | | | $ | 1.2089 | | | $ | 1.2848 | | | $ | 1.3194 | |

| 2013 | | $ | 1.3814 | | | $ | 1.2768 | | | $ | 1.3281 | | | $ | 1.3791 | |

| 2014 | | $ | 1.3953 | | | $ | 1.2141 | | | $ | 1.3285 | | | $ | 1.2141 | |

| 2015 | | $ | 1.2043 | | | $ | 1.0552 | | | $ | 1.1095 | | | $ | 1.0887 | |

| Month Ended | | High | | | Low | | | Average | | | Month end | |

| September 2015 | | $ | 1.1419 | | | $ | 1.1138 | | | $ | 1.1221 | | | $ | 1.1203 | |

| October 2015 | | $ | 1.1439 | | | $ | 1.0930 | | | $ | 1.1235 | | | $ | 1.1017 | |

| November 2015 | | $ | 1.1032 | | | $ | 1.0579 | | | $ | 1.0736 | | | $ | 1.0579 | |

| December 2015 | | $ | 1.0990 | | | $ | 1.0600 | | | $ | 1.0877 | | | $ | 1.0887 | |

| January 2016 | | $ | 1.0920 | | | $ | 1.0742 | | | $ | 1.0860 | | | $ | 1.0920 | |

| February 2016 | | $ | 1.1347 | | | $ | 1.0884 | | | $ | 1.1093 | | | $ | 1.0888 | |

On March 16, 2016, the exchange rate was $[ ] per euro.

| B. | CAPITALIZATION AND INDEBTEDNESS |

Not applicable.

| C. | REASONS FOR THE OFFER AND USE OF PROCEEDS |

Not applicable.

Risks Related to Our Financial Position and Capital Requirements

We have a history of operating losses and anticipate that we will continue to incur operating losses in the future and may never sustain profitability.

We have incurred operating losses in each year since inception because our research and development and general and administrative expenses exceeded our revenue. Our operating loss for the years ended December 31, 2013, 2014 and 2015 was, €6.9 million, €16.1 million and €44.2 million, respectively. As of December 31, 2015, we had an accumulated deficit of €149.9 million and our current assets exceeded our current liabilities by €29.1 million.

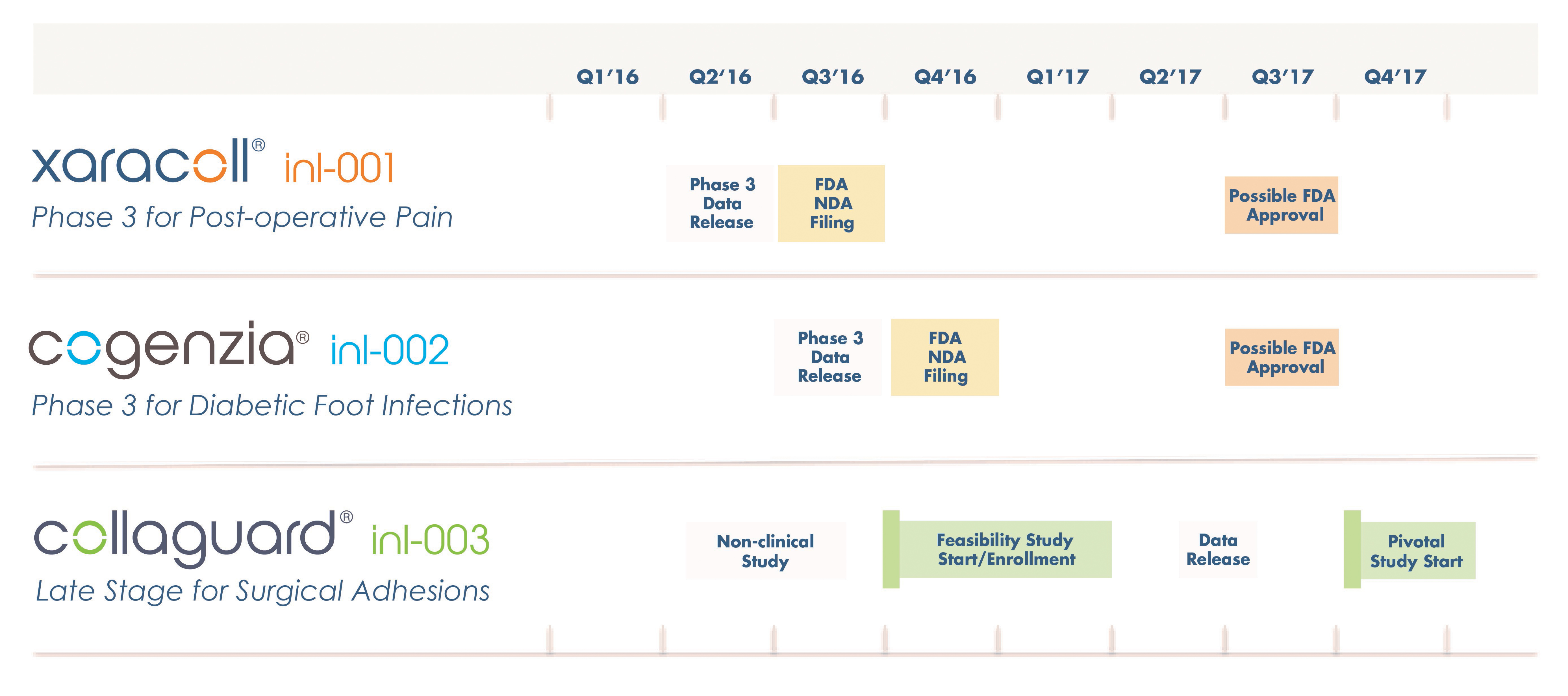

Our ability to become profitable depends on our ability to develop and commercialize our lead product candidates, XaraColl and Cogenzia. Our lead product candidates are not yet approved for commercial sale in the United States or Europe, and we do not know when, or if, we will generate significant revenues from their sale in the future. Cogenzia has been approved in seven countries outside of the United States and Europe but has not yet been commercialized in any of these countries. Our third late-stage product candidate, CollaGUARD, is approved for commercial sale in 12 countries, but not yet approved for commercial sale in the United States and we do not know when, or if, we if will generate significant revenue from its sale in the United States in the future. We do not anticipate generating revenue from sales of XaraColl until at least the end of 2017 and we will never generate revenue from XaraColl if we do not obtain regulatory approval. While we have products approved or commercialized and available for sale in certain markets, including CollatampG, RegenePro and Septocoll, our revenues to date from these products have been limited.

Even if we do generate product sales, we may never achieve or sustain profitability. We anticipate that our operating losses will substantially increase over the next several years as we execute our plan to expand our research, development and commercialization activities, including the clinical development and planned commercialization of our product candidates, and incur the additional costs of operating as a public company. In addition, if we obtain regulatory approval of our product candidates, we may incur significant sales and marketing expenses. Because of the numerous risks and uncertainties associated with developing pharmaceutical products, we are unable to predict the extent of any future losses or when we will become profitable, if ever.

If we fail to obtain additional financing, we may be unable to complete the development and commercialization of our product candidates.

Our operations have consumed substantial amounts of cash since inception. We expect to continue to spend substantial amounts to continue the clinical development of our product candidates, including our Phase 3 clinical trials. If our product candidates are approved, we will require significant additional funds in order to launch and commercialize such product candidates in the United States and potentially in the EU. We will also need to spend substantial amounts to significantly expand our manufacturing infrastructure. Finally, we had trade and other payables of €13.2 million and deferred income of €2.0 million (representing products to be delivered for which payment has already been received) as of December 31, 2015.

Our rate of expenses will continue to increase as we advance our planned clinical trials of XaraColl, Cogenzia and CollaGUARD and expand our manufacturing facility in Saal, Germany. As a result, we will be required to seek additional sources of capital during the next 12 months or restrict certain of our expenditures to conserve capital and extend our resources. Our need for additional capital will depend significantly on the level and timing of regulatory approval and product sales, as well as the extent to which we choose to establish collaboration, co-promotion, distribution or other similar agreements for our products and product candidates. Moreover, changing circumstances may cause us to spend cash significantly faster than we currently anticipate, and we may need to spend more cash than currently expected because of circumstances beyond our control. We expect to continue to incur substantial additional operating losses as we seek regulatory approval for and commercialize XaraColl, Cogenzia and CollaGUARD and develop and seek regulatory approval for our other product candidates. If we obtain FDA approval for our products, we will incur significant sales, marketing and manufacturing expenses. In addition, we expect to incur additional expenses to add operational, financial and information systems and personnel, including personnel to support our planned product commercialization and expanded manufacturing efforts for Xaracoll, Cogenzia and CollaGuard in the United States. We also expect to incur significant costs to continue to comply with corporate governance, internal controls and similar requirements applicable to us as a public company.

Our future funding requirements, both near- and long-term, will depend on many factors, including, but not limited to:

| · | the initiation, progress, timing, costs and results of clinical trials for our product candidates, particularly XaraColl and Cogenzia, and the PMA application for CollaGUARD; |

| · | the clinical development plans we establish for these product candidates; |

| · | the number and characteristics of product candidates that we develop and seek regulatory approval for; |

| · | the outcome, timing and cost of regulatory approvals by the U.S. Food and Drug Administration, or FDA, and comparable foreign regulatory authorities, including the potential for the FDA or comparable foreign regulatory authorities to require that we perform more studies than those that we currently expect; |

| · | the cost of filing, prosecuting, defending and enforcing any patent claims and other intellectual property rights; |

| · | the effects of competing technological and market developments; |

| · | the timing of, and our ability to obtain, regulatory approvals for the expansion of our manufacturing facility |

| · | the cost and timing of completion of commercial-scale manufacturing activities; and |

| · | the cost of establishing sales, marketing and distribution capabilities for any product candidates for which we may receive regulatory approval in regions where we choose to commercialize our products on our own. |

We cannot be certain that additional funding will be available on acceptable terms, or at all. If we are unable to raise additional capital in sufficient amounts or on terms acceptable to us, we may have to significantly delay, scale back or discontinue the development or commercialization of our product candidates or other research and development initiatives. We also could be required to seek collaborators for our product candidates at an earlier stage than would otherwise be desirable or on terms that are less favorable than might otherwise be available or relinquish or license on unfavorable terms our rights to our product candidates in markets in which we would otherwise seek to pursue development or commercialization ourselves.

Any of the above events could significantly harm our business, prospects, financial condition and results of operations and cause the price of our securities to decline.

Our existing and any future indebtedness could adversely affect our ability to operate our business.

Innocoll Germany and our wholly-owned subsidiary, Innocoll Pharmaceuticals Limited, or Innocoll Pharmaceuticals, entered into a Finance Contract with the European Investment Bank, or EIB, in March 2015 whereby the EIB has committed to lend to Innocoll Pharmaceuticals up to €25 million. We drew down €15 million of the loan commitment, and contingent on achieving the primary endpoint on either XaraColl or Cogenzia Phase 3 clinical trials, are entitled to draw down an additional €10 million. We could in the future incur additional debt obligations beyond our borrowings from the EIB. The EIB loan, our existing loan obligations, together with other similar obligations that we may incur in the future, could have significant adverse consequences, including:

| · | requiring us to dedicate a portion of our cash resources to pay for the principal and interest accrued over the 5 years loan payable at the end of the period, which may limit available resource to fund working capital, capital expenditures, product development and other general expenses; |

| · | increasing our vulnerability to adverse changes in general economic, industry and market conditions; |

| · | subjecting us to restrictive covenants that may reduce our ability to take certain corporate actions or obtain further debt or equity financing and could take up management time dealing with any consents required from lenders or other financing sources; |

| · | limiting our flexibility in planning for, or reacting to, changes in our business and the industry in which we compete; and |

| · | placing us at a competitive disadvantage compared to our competitors that have less debt or better debt servicing options. |

We may not have sufficient funds, and may be unable to arrange for additional financing, to pay the amounts due under our existing loan obligations. Failure to make payments or comply with other covenants under our existing debt could result in an event of default and acceleration of amounts due. Under our agreement with the EIB the occurrence of an event which would in the reasonable opinion of EIB have a material adverse effect on our business, operations, property or condition (financial or otherwise) or prospects compared with our condition at the date of the EIB facility agreement is an event of default. If an event of default occurs and the lender accelerates the amounts due, we may not be able to make accelerated payments, and the lender could seek to enforce security interests in the collateral securing such indebtedness, such as the shares in and assets of Innocoll Pharmaceuticals Limited, which include all of our assets. In addition, the covenants under our existing debt, and the pledge of our assets as collateral, could limit our ability to obtain additional debt financing.

Risks Related to the Clinical Development and Regulatory Approval of Our Product Candidates

Our business depends substantially on the success of certain of our lead product candidates, XaraColl and Cogenzia, which are still in development. If we are unable to successfully develop and subsequently commercialize XaraColl and Cogenzia, or experience significant delays in doing so, our business will be materially harmed.

We have invested a significant portion of our efforts and financial resources in the development of XaraColl and Cogenzia, our two lead product candidates, which have not yet been approved for commercial sale in the United States or in Europe. There remains a significant risk that we will fail to successfully develop either XaraColl or Cogenzia, or both. We initiated our Phase 3 efficacy trials for Cogenzia in the second quarter of 2015. We recently received topline data from our pivotal pharmacokinetic study in which we tested both a 200 mg and a 300 mg dose versus standard bupivacaine infiltration and commenced our Phase 3 efficacy trials for XaraColl in the third quarter of 2015. We do not expect to have final pivotal data from our XaraColl Phase 3 trials and from our Cogenzia Phase 3 trials available until the first half of and the third quarter of 2016, respectively. Even if we ultimately obtain statistically significant, positive results from our Phase 3 clinical trials, we do not expect to submit applications for marketing approval for XaraColl and Cogenzia until late 2016. The success of our product candidates will depend on several factors, including:

| · | successful completion of clinical trials; |

| · | receipt of regulatory approvals from applicable regulatory authorities; |

| · | maintaining regulatory compliance for our manufacturing facility; |

| · | manufacturing sufficient quantities in acceptable quality; |

| · | achieving meaningful commercial sales of our product candidates, if and when approved; |

| · | obtaining reimbursement from third-party payors for product candidates, if and when approved; |

| · | sourcing sufficient quantities of raw materials used to manufacture our products; |

| · | successfully competing with other products; |

| · | continued acceptable safety and effectiveness profiles for our product candidates following regulatory approval, if and when received; |

| · | obtaining and maintaining patent and trade secret protection and regulatory exclusivity; and |

| · | protecting our intellectual property rights. |

If we do not achieve one or more of these factors in a timely manner, or at all, we could experience significant delays or an inability to successfully commercialize our product candidates, which would materially harm our business and we may not be able to earn sufficient revenues and cash flows to continue our operations.

Our ability to generate future revenues depends heavily on our success in:

| · | developing and securing U.S. and/or foreign regulatory approvals for our product candidates; |

| · | manufacturing commercial quantities of our product candidates at acceptable costs; |

| · | commercializing our product candidates, assuming we receive regulatory approval; |

| · | achieving broad market acceptance of our product candidates in the medical community and with third-party payors and patients; and |

| · | pursuing clinical development of our product candidates for additional indications. |

Clinical drug development is expensive and involves uncertain outcomes, and results of earlier studies and trials may not be predictive of future trial results. If our Phase 3 clinical trials for XaraColl or Cogenzia are unsuccessful, or significantly delayed, we could be required to abandon development and our business will be materially harmed.

Clinical testing is expensive and can take many years to complete, and its outcome is inherently uncertain. Failure can occur at any time during the clinical trial process. The results of our Phase 2 clinical trials for XaraColl and Cogenzia may not be predictive of the results of our planned Phase 3 clinical trials. Adverse events may occur or other risks may be discovered in Phase 3 clinical trials that will cause us to suspend or terminate our clinical trials. In some instances, there can be significant variability in safety and/or efficacy results between different trials of the same product candidate due to numerous factors, including changes in or adherence to trial protocols, differences in the size and type of patient populations and the dropout rates among clinical trial participants. Our future clinical trial results, therefore, may not demonstrate efficacy and safety sufficient to obtain regulatory approval for our product candidates.

Flaws in the design of a clinical trial may not become apparent until the clinical trial is well under way. We have limited experience in designing clinical trials and may be unable to design and execute a clinical trial to support regulatory approval. In addition, clinical trials often reveal that it is not practical or feasible to continue development efforts.

We may voluntarily suspend or terminate our clinical trials if at any time we believe that they present an unacceptable risk to participants. Further, regulatory agencies, institutional review boards or data safety monitoring boards may at any time order the temporary or permanent discontinuation of our clinical trials or request that we cease using certain investigators in the clinical trials if they believe that the clinical trials are not being conducted in accordance with applicable regulatory requirements or that they present an unacceptable safety risk to participants.

If the results of our clinical trials for our current product candidates or clinical trials for any future product candidates do not achieve their primary efficacy endpoints or raise unexpected safety issues, the prospects for approval of our product candidates will be materially adversely affected. Moreover, preclinical and clinical data are often susceptible to varying interpretations and analyses and many companies that believed their product candidates performed satisfactorily in preclinical studies and clinical trials have failed to achieve similar results in later clinical trials, or have ultimately failed to obtain regulatory approval of their product candidates. Many products that initially showed promise in clinical trials or earlier stage testing have later been found to cause undesirable or unexpected adverse effects that have prevented their further development. Our upcoming trials for our primary product candidates, XaraColl and Cogenzia, may not produce the results that we expect.

In addition, we may experience numerous unforeseen events that could cause our clinical trials to be delayed, suspended or terminated, or which could delay or prevent our ability to receive regulatory approval or commercialize our product candidates, including:

| · | delay or failure in reaching agreement with the FDA or comparable foreign regulatory authorities on trial designs that we are able to execute; |

| · | the number of patients required for clinical trials of our product candidates may be larger than we anticipate, enrollment in these clinical trials may be slower than we anticipate or participants may drop out of these clinical trials at a higher rate than we anticipate; |

| · | clinical trials of our product candidates may produce negative, inconclusive or inconsistent results, and we may decide, or regulators may require us, to conduct additional clinical trials or implement a clinical hold; |

| · | we may elect or be required to suspend or terminate clinical trials of our product candidates, including based on a finding that the participants are being exposed to unacceptable health risks; |

| · | regulators or institutional review boards may not authorize us or our investigators to commence or continue a clinical trial, or conduct or continue a clinical trial at a prospective trial site; |

| · | our third-party contractors may fail to comply with regulatory requirements or meet their contractual obligations to us in a timely manner, or at all; |

| · | we may have delays in reaching or fail to reach agreement on acceptable clinical trial contracts or clinical trial protocols with prospective trial sites; |

| · | the cost of clinical trials of our product candidates may be greater than we anticipate; |

| · | changes in government regulation or administrative actions; |

| · | the supply or quality of our product candidates or other materials necessary to conduct clinical trials of our product candidates may be insufficient or inadequate; and |

| · | our product candidates may have undesirable adverse effects or other unexpected characteristics. |

Patient enrollment, a significant factor in the timing of clinical trials, is affected by many factors including the size and nature of the patient population, the proximity of subjects to clinical sites, the eligibility criteria for the trial, the design of the clinical trial, ability to obtain and maintain patient consents, risk that enrolled subjects will drop out before completion, competing clinical trials and clinicians’ and patients’ perceptions of the potential advantages of the drug being studied in relation to other available therapies, including any new drugs that may be approved for the indications we are investigating.

If we experience delays in the completion of, or termination of, any clinical trial of our product candidates, the commercial prospects of our product candidates will be materially harmed, and our ability to generate product revenues from any of these product candidates will cease or be delayed. In addition, any termination of, or delays in completing, our clinical trials will increase our costs, slow down our product candidate development and approval process and jeopardize our ability to commence product sales and generate revenues. Any of these occurrences may significantly harm our business, financial condition and prospects. In addition, many of the factors that cause, or lead to a delay in the commencement or completion of or early termination of, clinical trials may also ultimately lead to the denial of regulatory approval of our product candidates.

We may not receive a general indication of postoperative analgesia for XaraColl, which would have an adverse effect on our ability to market XaraColl for use in surgical procedures other than those studied in our Phase 3 trials and could adversely affect our business and financial results.

The FDA strictly regulates marketing, labeling, advertising and promotion of prescription drugs. These regulations include standards and restrictions for direct-to-consumer advertising, industry-sponsored scientific and educational activities, promotional activities involving the Internet and off-label promotion. The FDA generally does not allow drugs to be promoted for “Off-label” uses — that is, uses that are not described in the product’s labeling and that differ from those that were approved by the FDA. In addition to the FDA approval required for new formulations, any new indication for an approved product also requires FDA approval.

If we are not able to obtain FDA approval for any desired future indications for XaraColl outside of open hernioplasty, our ability to effectively market and sell XaraColl may be limited, and our business may be adversely affected.

While physicians in the United States may choose, and are generally permitted to prescribe drugs for uses that are not described in the product’s labeling, and for uses that differ from those tested in clinical studies and approved by the regulatory authorities, our ability to promote our products is narrowly limited to those indications that are specifically approved by the FDA. “Off-label” uses are common across medical specialties and may constitute an appropriate treatment for some patients in varied circumstances. Regulatory authorities in the United States generally do not regulate the behavior of physicians in their choice of treatments. Regulatory authorities do, however, restrict communications by pharmaceutical companies on the subject of off-label use. Although recent court decisions suggest that certain off-label promotional activities may be protected under the First Amendment, the scope of any such protection is unclear. Moreover, while we intend to promote our products consistent with what we believe to be the approved indication for our drugs, the FDA may disagree. If the FDA determines that our promotional activities fail to comply with the FDA’s regulations or guidelines, we may be subject to warnings from, or enforcement action by, these authorities. In addition, our failure to follow FDA rules and guidelines relating to promotion and advertising may cause the FDA to issue warning letters or untitled letters, bring an enforcement action against us, suspend or withdraw an approved product from the market, require a recall or institute fines or civil fines, or could result in disgorgement of money, operating restrictions, injunctions or criminal prosecution, any of which could harm our reputation and our business.

The results of clinical trials may not support our product candidate claims. Certain of our completed Phase 2 clinical trials failed to meet their primary endpoints and involved small patient populations.

Even if our clinical trials are completed as planned, we cannot be certain that the results will support our product candidate claims or that the FDA or government authorities in other countries will agree with our conclusions regarding such results. Success in preclinical testing and early clinical trials does not ensure that later clinical trials will be successful, and the results of later clinical trials often do not replicate the results of prior clinical trials and preclinical testing.

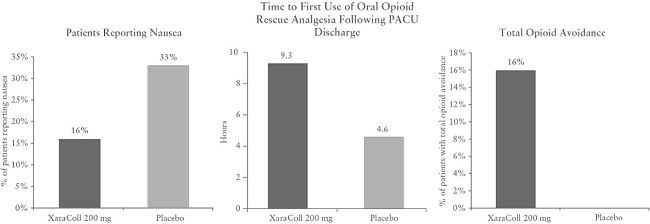

In addition, we were unable to achieve certain primary efficacy endpoints in connection with the Phase 2 clinical studies for our two lead product candidates, XaraColl and Cogenzia. For example, in our two Phase 2 trials for XaraColl, which enrolled 53 and 50 patients, respectively, our primary endpoints were total consumption of opioid analgesia and reduction of pain based on patients’ SPI scores, respectively. Over the first 24 hours post operation, XaraColl-treated patients experienced significantly less pain in study 1 with a XaraColl dose of 100 mg (44% reduction; p = 0.001) but showed merely a trend towards significance for pain reduction in study 2 with a XaraColl dose of 200 mg (22% reduction; p = 0.080). Following a change in guidance we received from the FDA in July 2015, we discontinued the use of integrated endpoints in our Phase 3 trials for XaraColl employing a statistical analysis known as the Silverman Method, and instead chose SPI as our primary endpoint for both XaraColl trials. In addition, we plan to conduct both our Phase 3 trials using a 300 mg dose of XaraColl, a dose that was not tested in our Phase 2 trials. Since bupivacaine is believed to work locally by blocking the generation and the conduction of nerve impulses and it is considered dose dependent, we believe a higher dose should increase the local analgesic effect, even though this dose-related response is not initially supported by the results of our Phase 2 trials, which involved small patient populations. We may fail to reach these endpoints and demonstrate efficacy for XaraColl.

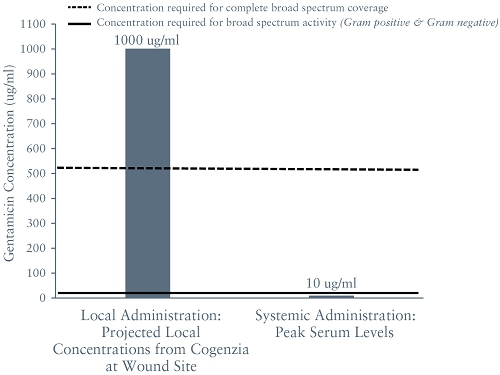

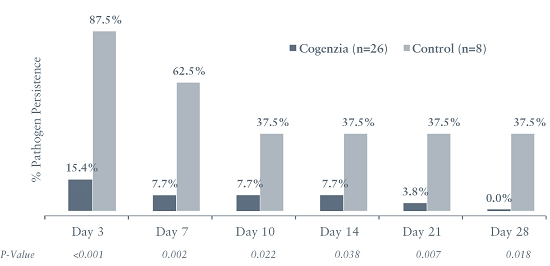

In our Phase 2 trial for Cogenzia involving 56 patients, Cogenzia (50 mg or 200 mg) was applied daily for up to four weeks in combination with systemic antibiotic therapy for the treatment of moderately-infected diabetic foot ulcers with the control group receiving systemic therapy alone. The primary efficacy endpoint was the percentage of patients with a clinical outcome of “clinical cure” on a study visit on day 7 of treatment. Efficacy versus the control group was not achieved. However, based on the modified intent-to-treat population, 100% of the patients who received Cogenzia and who completed the trial achieved a clinical cure two weeks after completion of treatment (test-of-cure date), compared to just 70% of patients who received systemic antibiotic therapy alone, which was a statistically significant difference (p = 0.024). Although we have selected a clinical cure measured 10 – 14 days after the last dose of treatment has been administered as our primary endpoint for our COACT Phase 3 trials for Cogenzia, we may fail to reach these endpoints and demonstrate efficacy for Cogenzia.

In addition, our completed clinical trials involved a small patient population. Because of the small sample size, the results of these clinical trials may not be indicative of future results in a larger and more diverse patient population. The clinical trial process may fail to demonstrate that our product candidates are safe for humans and effective for indicated uses. This failure could cause us to abandon a product candidate and may delay development of other product candidates. Any delay in, or termination of, our clinical trials will delay the filing of our NDAs with the FDA and, ultimately, our ability to commercialize our product candidates and generate product revenues.

If our drug product candidates, such as XaraColl and Cogenzia, receive regulatory approval, we will be subject to ongoing regulatory requirements and we may face future development, manufacturing and regulatory difficulties.

Our drug product candidates, such as XaraColl and Cogenzia, if approved, will be subject to ongoing regulatory requirements for labeling, packaging, storage, advertising, promotion, sampling, record-keeping, submission of safety and other post-market approval information, importation and exportation. In addition, approved products, manufacturers and manufacturers’ facilities are required to comply with extensive FDA and European Medicines Agency, or EMA, requirements and the requirements of other similar agencies, including ensuring that quality control and manufacturing procedures conform to current Good Manufacturing Practices, or cGMP, requirements.

Accordingly, we will be required to expend time, money and effort in all areas of regulatory compliance, including manufacturing, production and quality control. We will also be required to report certain adverse reactions and production problems, if any, to the FDA and EMA and other similar agencies and to comply with certain requirements concerning advertising and promotion for our potential products.

If a regulatory agency discovers previously unknown problems with a product, such as adverse events of unanticipated severity or frequency, or problems with the facility where the product is manufactured, or disagrees with the promotion, marketing or labeling of a product, it may impose restrictions on that product or us, including requiring withdrawal of the product from the market. If our potential products fail to comply with applicable regulatory requirements, a regulatory agency may, among other actions:

| · | issue warning letters or untitled letters; |

| · | require product recalls; |

| · | mandate modifications to promotional materials or require us to provide corrective information to healthcare practitioners; |

| · | require us or our potential future collaborators to enter into a consent decree or permanent injunction; |

| · | impose other administrative or judicial civil or criminal actions, including monetary or other penalties, or pursue criminal prosecution; |

| · | withdraw regulatory approval; |

| · | refuse to approve pending applications or supplements to approved applications filed by us or by our potential future collaborators; |

| · | impose restrictions on operations, including costly new manufacturing requirements; or |

| · | seize or detain products. |

Risks Related to Our Business and Strategy

If we fail to manufacture XaraColl, Cogenzia, CollaGUARD or our other marketed products and product candidates in sufficient quantities and at acceptable quality and cost levels, or to fully comply with cGMP or other applicable manufacturing regulations, we may face a bar to, or delays in, the commercialization of our products, breach obligations to our licensing partners or be unable to meet market demand, and lose potential revenues.

The manufacture of our products based on our collagen-based technology platform, including XaraColl and Cogenzia, requires significant expertise and capital investment. Currently, we are manufacturing all commercial and clinical supply for all of our marketed products and product candidates in our sole facility in Saal, Germany without the benefit of any redundant or backup facilities. We need to spend substantial amounts to significantly expand our manufacturing infrastructure in order to satisfy any increases in future demand. Also, substantially all of our inventory of raw material and finished goods is held at this location. We take precautions to safeguard our facility, including acquiring insurance, employing back-up generators, adopting health and safety protocols and utilizing off-site storage of computer data. However, vandalism, terrorism or a natural or other disaster, such as a fire or flood, could damage or destroy our manufacturing equipment or our inventory of raw material or finished goods, cause substantial delays in our operations, result in the loss of key information, and cause us to incur additional expenses. Our insurance may not cover our losses in any particular case. In addition, regardless of the level of insurance coverage, damage to our facilities may have a material adverse effect on our business, financial condition and operating results. In addition, our competitors have substantially greater financial, technical and other resources, such as a larger staff and experienced manufacturing organizations.

We must comply with federal, state and foreign regulations, including FDA regulations governing cGMP enforced by the FDA through its facilities inspection program and by similar regulatory authorities in other jurisdictions where we do business. These requirements include, among other things, quality control, quality assurance and the maintenance of records and documentation. For our medical device products, we are required to comply with the FDA’s Quality System Regulation, or QSR, which covers the methods and documentation of the design, testing, production, control, quality assurance, labeling, packaging, sterilization, storage and shipping of our medical device products.

Our facility has not yet been inspected by the FDA for cGMP compliance. If we do not successfully achieve cGMP compliance for our facility in a timely manner, commercialization of our products could be prohibited or significantly delayed. Even after cGMP compliance has been achieved, the FDA or similar foreign regulatory authorities at any time may implement new standards, or change their interpretation and enforcement of existing standards for manufacture, packaging, testing of or other activities related to our products. For our marketed medical device products, the FDA audits compliance with the QSR through periodic announced and unannounced inspections of manufacturing and other facilities. The FDA may conduct inspections or audits at any time. Similar audit rights exist in Europe and other foreign jurisdictions. Any failure to comply with applicable cGMP, QSR and other regulations may result in fines and civil penalties, suspension of production, product seizure or recall, imposition of a consent decree, or withdrawal of product approval, and would limit the availability of our product. Any manufacturing defect or error discovered after products have been produced and distributed also could result in significant consequences, including adverse health consequences, injury or death to patients, costly recall procedures, re-stocking costs, damage to our reputation and potential for product liability claims. If we are required to find a new manufacturer or supplier, the process would likely require prior FDA and/or equivalent foreign regulatory authority approval, and would be very time consuming. An inability to continue manufacturing adequate supplies of our products at our facility in Saal, Germany, could result in a disruption in the supply of our products. We have licensed the commercial rights in specified foreign territories to market and sell our products. Under those licenses, we have obligations to manufacture commercial product for our commercial partners. If we are unable to fill the orders placed with us by our commercial partners in a timely manner, we may potentially lose revenue and be in breach of our licensing obligations under agreements with them.

We have not obtained regulatory approval for any of our late-stage product candidates in the United States, so we cannot yet generate any revenues from the sales of these products in the United States.

Our late-stage product candidates, XaraColl, Cogenzia and CollaGUARD, have not yet been approved for commercial sale in the United States. We cannot commercialize product candidates in the United States without first obtaining regulatory approval from the FDA to market each product. We initiated our Phase 3 efficacy trials for Cogenzia in the second quarter of 2015. We recently received topline data from our pivotal pharmacokinetic study in which we tested both a 200 mg and a 300 mg dose versus standard bupivacaine infiltration and commenced our Phase 3 efficacy trials for XaraColl in the third quarter of 2015. We do not expect to have final pivotal data from our XaraColl Phase 3 trials and from our Cogenzia Phase 3 trials available until the first half of and the third quarter of 2016, respectively. Even if we ultimately obtain statistically significant, positive results from our Phase 3 clinical trials, we do not expect to submit applications for marketing approval for XaraColl and Cogenzia until late 2016.

Before obtaining regulatory approvals for the commercial sale of any product candidate for a target indication, we must demonstrate in non-clinical, or preclinical, studies and clinical trials, and, with respect to approval in the United States, to the satisfaction of the FDA, that the product candidate is safe and effective for use under the labeled conditions for use and that the manufacturing facilities, processes and controls are adequate. In the United States, we have not submitted an NDA for either XaraColl or Cogenzia. An NDA must include extensive preclinical and clinical data and supporting information to establish the product candidate’s safety and effectiveness for each desired indication. The NDA must also include significant information regarding the chemistry, manufacturing and controls for the product and its components, and draft labeling. Obtaining approval of an NDA is a lengthy, expensive and uncertain process, and approval may not be obtained. If we submit an NDA to the FDA, the FDA must decide whether to accept or reject the submission for filing. We cannot be certain that any of our submissions will be accepted for filing and review by the FDA, or that the FDA will approve the application if it accepts it.

Even though we have a special protocol assessment, or SPA, with the FDA for Cogenzia, the contents of which were fully reaffirmed with the FDA in the fourth quarter of 2014, this SPA is subject to change by the FDA even after we commenced our Phase 3 trials if the FDA determines that a substantial issue essential to determining the safety and effectiveness of the drug was identified after the trial began. Similarly, advice given by the EMA relating to the registrational trial for Cogenzia under the Scientific Advice procedure is only given in the light of the current scientific knowledge, based on the documentation provided by us. The Scientific Advice procedure is designed to avoid major objections regarding the design of the clinical trials being raised during evaluation of the marketing-authorization application but is not legally binding on the EMA.

Regulatory authorities outside of the United States, such as in Europe and in emerging markets, also have requirements for approval of products for commercial sale with which we must comply prior to marketing in those areas. Regulatory requirements can vary widely from country to country and could delay or prevent the introduction of our product candidates. Clinical trials conducted in one country may not be accepted by regulatory authorities in other countries, and obtaining regulatory approval in one country does not mean that regulatory approval will be obtained in any other country. Approval processes vary among countries and can involve additional product testing and validation and additional administrative review periods. Seeking foreign regulatory approval could require additional non-clinical studies or clinical trials, which could be costly and time consuming. The foreign regulatory approval process may include all of the risks associated with obtaining FDA approval, and potentially may include additional risks.

The process to develop, obtain regulatory approval for, and commercialize product candidates is long, complex and costly both inside and outside of the United States, and approval is not guaranteed. Even if we successfully obtain approval from the regulatory authorities for our product candidates, any approval might significantly limit the approved indications for use, or require that precautions, contraindications or warnings be included on the product labeling that limit its commercialization, or limit its commercialization through a Risk Evaluation and Mitigation Strategy, or REMS, that restricts who may prescribe or dispense the product or imposes other significant limits to assure safe use, or require expensive and time-consuming post-approval clinical studies or surveillance as conditions of approval. Following any approval for commercial sale of our product candidates, certain changes to the product, such as changes in manufacturing processes and additional labeling claims, will be subject to additional regulatory review and approval. In addition, regulatory approval for any of our product candidates may be withdrawn. If we are unable to obtain regulatory approval for our product candidates in one or more jurisdictions, or if any approval we do obtain contains significant limitations, our target market will be reduced and our ability to realize the full market potential of our product candidates will be harmed. Furthermore, we may not be able to obtain sufficient funding or generate sufficient revenue and cash flows to continue the development of any other product candidate in the future.

If we fail to develop and commercialize additional product candidates, we may be unable to grow our business.

If we decide to pursue the development and commercialization of any additional product candidates, we may be required to invest significant resources to acquire or in-license the rights to such product candidates or to conduct product discovery activities. In addition, any other product candidates will require additional, time-consuming development efforts prior to commercial sale, including preclinical studies, extensive clinical trials and approval by the FDA and applicable foreign regulatory authorities. All product candidates are prone to the risk of failure that is inherent in therapeutic product development, including the possibility that the product candidate will not be shown to be sufficiently safe and/or effective for approval by regulatory authorities. In addition, we cannot assure you that we will be able to acquire, discover or develop any additional product candidates, or that any additional product candidates we may develop will be approved, manufactured or produced economically; successfully commercialized; or widely accepted in the marketplace or be more effective than other commercially available alternatives. Research programs to identify new product candidates require substantial technical, financial and human resources whether or not we ultimately identify any candidates. If we are unable to develop or commercialize additional product candidates, our business and prospects will suffer.

We have engaged in only limited sales of our products to date, 87% of which are to one customer for the year ended December 31, 2015.

While we are a global, commercial-stage, specialty pharmaceutical and medical device company, with late-stage development programs targeting areas of significant unmet medical needs, we have engaged in only limited sales of our products to date with approximately 87% of our sales being generated by one customer in the year ended December 31, 2015. Our products may never gain significant acceptance in the marketplace and, therefore, never generate substantial revenue or profits for the company. We must establish a market for our products and build that market through marketing campaigns to increase awareness of, and consumer confidence in, our products. If we are unable to expand our current customer base and obtain market acceptance of our products, our operations could be disrupted and our business may be materially adversely affected. Even if we achieve profitability, we may not be able to sustain or increase profitability.

We face significant competition from other pharmaceutical and medical device companies and our operating results will suffer if we fail to compete effectively.

The pharmaceutical and medical device industry is characterized by intense competition and rapid innovation. Although we believe that we hold a leading position in our understanding of collagen-based therapeutic products, our competitors may be able to develop other products that are able to achieve similar or better results. Our potential competitors include established and emerging pharmaceutical and biotechnology companies and universities and other research institutions. Many of our competitors have substantially greater financial, technical and other resources, such as larger research and development staff and experienced marketing and manufacturing organizations and well-established sales forces. Smaller or early-stage companies may also prove to be significant competitors, particularly through collaborative arrangements with large, established companies. Mergers and acquisitions in the pharmaceutical and biotechnology industries may result in even more resources being concentrated in our competitors. Competition may increase further as a result of advances in the commercial applicability of technologies and greater availability of capital for investment in these industries. Our competitors may succeed in developing, acquiring or licensing on an exclusive basis products that are more effective or less costly than our product candidates. We believe the key competitive factors that will affect the development and commercial success of our product candidates are efficacy, safety and tolerability profile, reliability, price and reimbursement.

We anticipate that XaraColl will compete in the United States with currently marketed bupivacaine and opioid analgesics such as morphine, as well as elastomeric bag/catheter devices intended to provide bupivacaine over several days, which have been marketed by I-FLOW Corporation (owned by Halyard Health) since 2004; and Pacira Pharmaceutical’s Exparel, a liposomal injection of bupivacaine, indicated for single-dose infiltration into the surgical site to produce postsurgical analgesia. While we are not aware of any topically applied antibiotics approved for the treatment of Diabetic Foot Infections, or DFIs, that we anticipate would compete directly with Cogenzia, DFIs are currently treated with systemic antibiotics and physicians may choose not to use Cogenzia in conjunction with these products. Once approved in the United States, CollaGUARD will compete with a number of well-accepted adhesion barriers marketed in the United States and elsewhere by well-established companies, including Sanofi’s Seprafilm®, Baxter’s Adept®, Ethicon’s Interceed® and Mast Biosurgery’s Surgiwrap®.

The financial performance of our medical device products, such as CollaGUARD, may be adversely affected by medical device tax provisions in the healthcare reform laws in the United States.

The the Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act of 2010, or collectively, the Affordable Care Act, imposes, among other things, an annual excise tax of 2.3% on any entity that manufactures or imports medical devices offered for sale in the United States beginning with tax year 2013. Under these provisions, the Congressional Research Service predicts that the total cost to the medical device industry may be up to $20 billion over the next decade. We do not believe that CollaGUARD is currently subject to this tax based on the retail exemption under applicable Treasury Regulations. However, the availability of this exemption is subject to interpretation by the IRS, and the IRS may disagree with our analysis. In addition, future products that we manufacture, produce or import may be subject to this tax. The financial impact this tax may have on our business is unclear and there can be no assurance that our business will not be materially adversely affected by it.

If we face allegations of noncompliance with the law and encounter sanctions, our reputation, revenues and liquidity may suffer, and our products could be subject to restrictions or withdrawal from the market.

Any government investigation of alleged violations of law could require us to expend significant time and resources in response and could generate negative publicity. Any failure to comply with ongoing regulatory requirements may significantly and adversely affect our ability to commercialize and generate revenues from our products. If regulatory sanctions are applied or if regulatory approval is withdrawn, the value of our company and our operating results will be adversely affected. Additionally, if we are unable to generate revenues from our product sales, our potential for achieving profitability will be diminished and the capital necessary to fund our operations will be increased.

Even if we obtain regulatory approval for our product candidates, the products may not gain market acceptance among hospitals, physicians, health care payors, patients and others in the medical community.

Even if we obtain regulatory approval for any of our product candidates that we may develop or acquire in the future, the product may not gain market acceptance among hospitals, physicians, health care payors, patients and others in the medical community. Market acceptance of any of our product candidates for which we receive approval depends on a number of factors, including:

| · | the clinical indications for which they are approved; |

| · | the product labeling, including warnings, precautions, side effects, and contraindications that the FDA approves; |

| · | the potential and perceived advantages of our product candidates over alternative products; |

| · | relative convenience and ease of administration; |

| · | the effectiveness of our sales and marketing efforts; |

| · | acceptance by major operators of hospitals, physicians and patients of the product candidate as a safe and effective treatment; |

| · | the prevalence and severity of any side effects; |

| · | product labeling or product insert requirements of the FDA or other regulatory authorities; |

| · | any REMS that the FDA might require; |

| · | the timing of market introduction of our product candidates as well as competitive products; |

| · | the cost of treatment in relation to alternative products; and |

| · | the availability of adequate reimbursement and pricing by third-party payors and government authorities. |

If our product candidates are approved but fail to achieve market acceptance among physicians, patients, payors, or others in the medical community, we will not be able to generate significant revenues, which would have a material adverse effect on our business, prospects, financial condition and results of operations.

If our product candidates are approved, and with respect to our already approved products, we may be subject to healthcare laws, regulation and enforcement. Our failure to comply with those laws could have a material adverse effect on our results of operations and financial conditions.

Although we currently do not have any of our lead products on the market in the United States and several other key jurisdictions, if our lead-product candidates are approved, once we begin commercializing our product candidates, we may be subject to additional healthcare regulation and enforcement by the U.S. federal government and by authorities in the states and foreign jurisdictions in which we conduct our business. In certain jurisdictions outside of the United States where we currently market certain of our products, we are already subject to such regulation and enforcement. Such laws include, without limitation, state and federal anti-kickback, false claims, privacy, security, “sunshine,” and trade regulation and advertising laws and regulations. If our operations are found to be in violation of any of such laws or any other governmental regulations that apply to us, we may be subject to penalties, including, but not limited to, civil and criminal penalties, damages, fines, the curtailment or restructuring of our operations, the exclusion from participation in federal and state healthcare programs and imprisonment, any of which could adversely affect our ability to operate our business and our financial results.

A recall of our drug or medical device products, or the discovery of serious safety issues with our drug or medical device products, could have a significant negative impact on us.