Exhibit 99.1

Creation of a Premier Specialty Materials Company March 29, 2019 Why the Merger of Equals is the Value Maximizing Opportunity

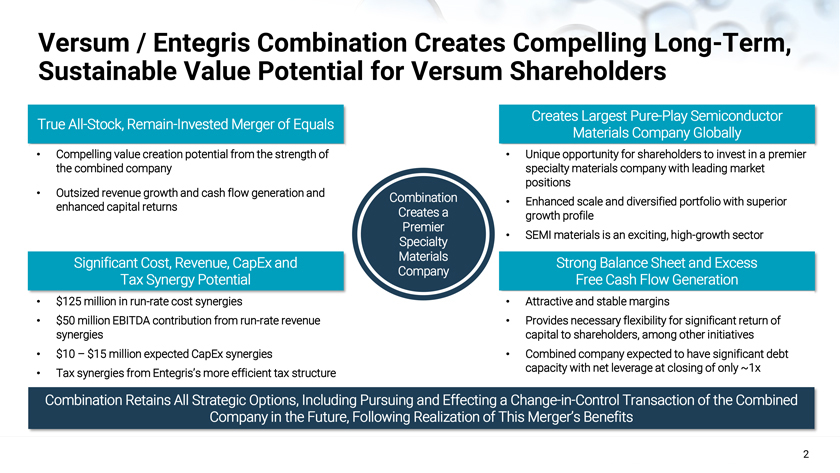

2 Versum / Entegris Combination Creates Compelling Long-Term, Sustainable Value Potential for Versum Shareholders True All-Stock, Remain-Invested Merger of Equals Compelling value creation potential from the strength of the combined company Outsized revenue growth and cash flow generation and enhanced capital returns Creates Largest Pure-Play Semiconductor Materials Company Globally Unique opportunity for shareholders to invest in a premier specialty materials company with leading market positions Enhanced scale and diversified portfolio with superior growth profile SEMI materials is an exciting, high-growth sector $125 million in run-rate cost synergies $50 million EBITDA contribution from run-rate revenue synergies $10 – $15 million expected CapEx synergies Tax synergies from Entegris’s more efficient tax structure Significant Cost, Revenue, CapEx and Tax Synergy Potential Strong Balance Sheet and Excess Free Cash Flow Generation Attractive and stable margins Provides necessary flexibility for significant return of capital to shareholders, among other initiatives Combined company expected to have significant debt capacity with net leverage at closing of only ~1x Combination Creates a Premier Specialty Materials Company Combination Retains All Strategic Options, Including Pursuing and Effecting a Change-in-Control Transaction of the Combined Company in the Future, Following Realization of This Merger’s Benefits

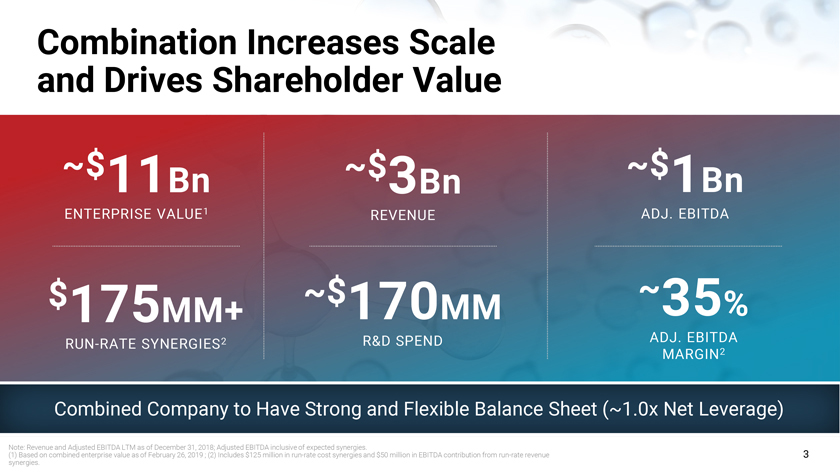

Combination Increases Scale and Drives Shareholder Value 3 Note: Revenue and Adjusted EBITDA LTM as of December 31, 2018; Adjusted EBITDA inclusive of expected synergies. (1) Based on combined enterprise value as of February 26, 2019 ; (2) Includes $125 million in run-rate cost synergies and $50 million in EBITDA contribution from run-rate revenue synergies. ~$3Bn REVENUE $175MM+ RUN-RATE SYNERGIES2 ~$170MM R&D SPEND ~35% ADJ. EBITDA MARGIN2 ~$1Bn ADJ. EBITDA ~$11Bn ENTERPRISE VALUE1 Combined Company to Have Strong and Flexible Balance Sheet (~1.0x Net Leverage)

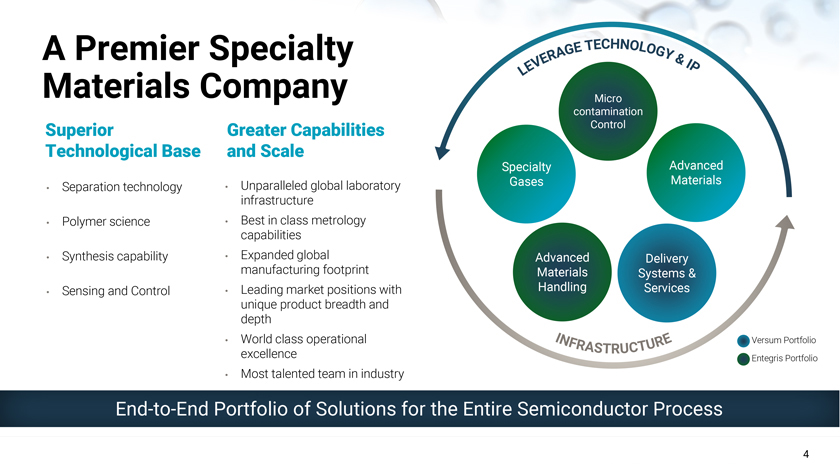

4 A Premier Specialty Materials Company End-to-End Portfolio of Solutions for the Entire Semiconductor Process Specialty Gases Delivery Systems & Services Separation technology Polymer science Synthesis capability Sensing and Control Superior Technological Base Unparalleled global laboratory infrastructure Best in class metrology capabilities Expanded global manufacturing footprint Leading market positions with unique product breadth and depth World class operational excellence Most talented team in industry Greater Capabilities and Scale Advanced Materials Advanced Materials Handling Micro contamination Control Versum Portfolio Entegris Portfolio

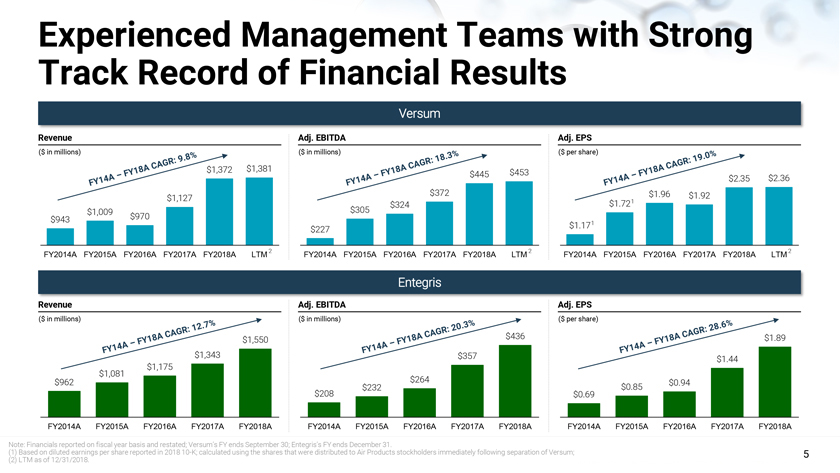

5 Experienced Management Teams with Strong Track Record of Financial Results $943 $1,009 $970 $1,127 $1,372 $1,381 FY2014A FY2015A FY2016A FY2017A FY2018A LTM Revenue $227 $305 $324 $372 $445 $453 FY2014A FY2015A FY2016A FY2017A FY2018A LTM $1.17 $1.72 $1.96 $1.92 $2.35 $2.36 FY2014A FY2015A FY2016A FY2017A FY2018A LTM Adj. EBITDA Adj. EPS $962 $1,081 $1,175 $1,343 $1,550 FY2014A FY2015A FY2016A FY2017A FY2018A $0.69 $0.85 $0.94 $1.44 $1.89 FY2014A FY2015A FY2016A FY2017A FY2018A $208 $232 $264 $357 $436 FY2014A FY2015A FY2016A FY2017A FY2018A Versum Entegris ($ in millions) ($ in millions) ($ per share) Revenue Adj. EBITDA Adj. EPS ($ in millions) ($ in millions) ($ per share) 1 1 Note: Financials reported on fiscal year basis and restated; Versum’s FY ends September 30; Entegris’s FY ends December 31. (1) Based on diluted earnings per share reported in 2018 10-K; calculated using the shares that were distributed to Air Products stockholders immediately following separation of Versum; (2) LTM as of 12/31/2018. 2 2 2

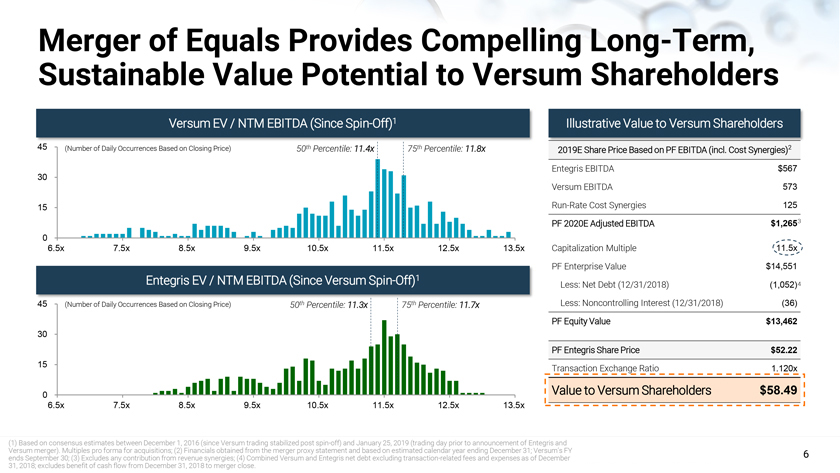

6 Merger of Equals Provides Compelling Long-Term, Sustainable Value Potential to Versum Shareholders VersumEV / NTM EBITDA (Since Spin-Off)1 (1) Based on consensus estimates between December 1, 2016 (since Versum trading stabilized post spin-off) and January 25, 2019 (trading day prior to announcement of Entegris and Versum merger). Multiples pro forma for acquisitions; (2) Financials obtained from the merger proxy statement and based on estimated calendar year ending December 31; Versum’s FY ends September 30; (3) Excludes any contribution from revenue synergies; (4) Combined Versum and Entegris net debt excluding transaction-related fees and expenses as of December 31, 2018; excludes benefit of cash flow from December 31, 2018 to merger close. 2019E Share Price Based on PF EBITDA (incl. Cost Synergies)2 Entegris EBITDA $567 Versum EBITDA 573 Run-Rate Cost Synergies 125 PF 2020E Adjusted EBITDA $1,265 Capitalization Multiple 11.5x PF Enterprise Value $14,551 Less: Net Debt (12/31/2018) (1,052) Less: Noncontrolling Interest (12/31/2018) (36) PF Equity Value $13,462 PF Entegris Share Price $52.22 Transaction Exchange Ratio 1.120x Value to Versum Shareholders $58.49 Illustrative Value to Versum Shareholders 4 3 0 15 30 45 6.5x 7.5x 8.5x 9.5x 10.5x 11.5x 12.5x 13.5x Entegris EV / NTM EBITDA (Since VersumSpin-Off)1 0 15 30 45 6.5x 7.5x 8.5x 9.5x 10.5x 11.5x 12.5x 13.5x (Number of Daily Occurrences Based on Closing Price) (Number of Daily Occurrences Based on Closing Price) 50th Percentile: 11.4x 75th Percentile: 11.8x 50th Percentile: 11.3x 75th Percentile: 11.7x

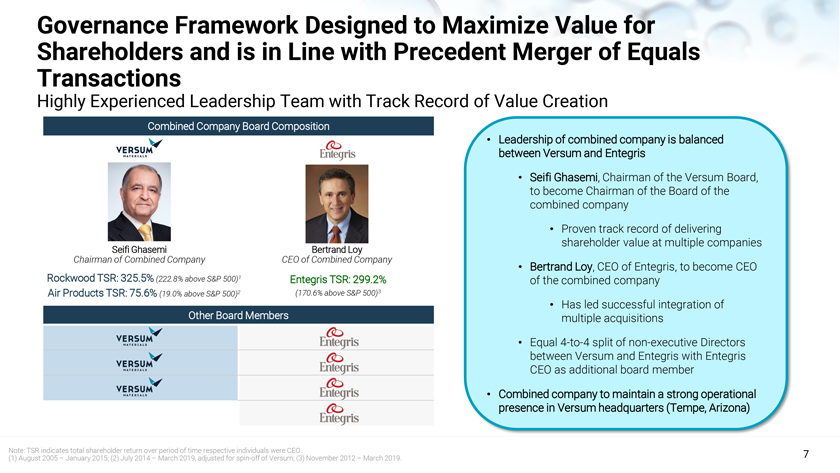

7 Governance Framework Designed to Maximize Value for Shareholders and is in Line with Precedent Merger of Equals Transactions Highly Experienced Leadership Team with Track Record of Value Creation Combined Company Board Composition Other BoardMembers Seifi Ghasemi Chairman of Combined Company Bertrand Loy CEO of Combined Company Leadership of combined company is balanced between Versumand Entegris Seifi Ghasemi, Chairman of the Versum Board, to become Chairman of the Board of the combined company Proven track record of delivering shareholder value at multiple companies Bertrand Loy, CEO of Entegris, to become CEO of the combined company Has led successful integration of multiple acquisitions Equal 4-to-4 split of non-executive Directors between Versum and Entegris with Entegris CEO as additional board member Combined company to maintain a strong operational presence in Versumheadquarters (Tempe, Arizona) Rockwood TSR: 325.5%(222.8% above S&P 500)1 Air Products TSR: 75.6% (19.0% above S&P 500)2 Entegris TSR: 299.2% (170.6% above S&P 500)3 Note: TSR indicates total shareholder return over period of time respective individuals were CEO. (1) August 2005 – January 2015; (2) July 2014 – March 2019;, adjusted for spin-off of Versum; (3) November 2012 – March 2019.

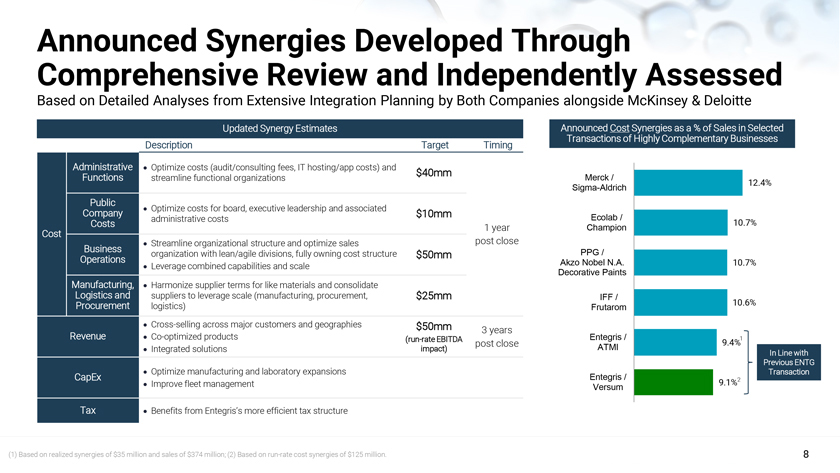

8 Announced Synergies Developed Through Comprehensive Review and Independently Assessed Based on Detailed Analyses from Extensive Integration Planning by Both Companies alongside McKinsey & Deloitte Updated Synergy Estimates Description Target Timing Cost Administrative Functions Optimize costs (audit/consulting fees, IT hosting/app costs) and streamline functional organizations $40mm 1 year post close Public Company Costs Optimize costs for board, executive leadership and associated administrative costs $10mm Business Operations Streamline organizational structure and optimize sales organization with lean/agile divisions, fully owning cost structure Leverage combined capabilities and scale $50mm Manufacturing, Logistics and Procurement Harmonize supplier terms for like materials and consolidate suppliers to leverage scale (manufacturing, procurement, logistics) $25mm Revenue Cross-selling across major customers and geographies Co-optimized products Integrated solutions $50mm (run-rate EBITDA impact) 3 years post close CapEx Optimize manufacturing and laboratory expansions Improve fleet management Tax Benefits from Entegris’s more efficient tax structure Announced Cost Synergies as a % of Sales in Selected Transactions of Highly Complementary Businesses 12.4% 10.7% 10.7% 10.6% 9.4% 9.1% Merck / Sigma-Aldrich Ecolab / Champion PPG / Akzo Nobel N.A. Decorative Paints IFF / Frutarom Entegris / ATMI Entegris / Versum 1 (1) Based on realized synergies of $35 million and sales of $374 million; (2) Based on run-rate cost synergies of $125 million. In Line with Previous ENTG Transaction 2

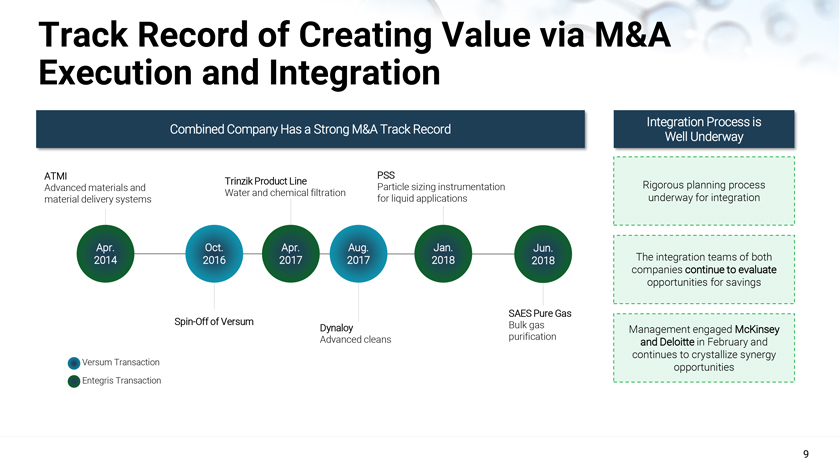

9 Track Record of Creating Value via M&A Execution and Integration Apr. 2014 Oct. 2016 Aug. 2017 Apr. 2017 Jan. 2018 Jun. 2018 ATMI Advanced materials and material delivery systems Spin-Off of Versum Trinzik Product Line Water and chemical filtration Dynaloy Advanced cleans PSS Particle sizing instrumentation for liquid applications SAES Pure Gas Bulk gas purification The integration teams of both companies continue to evaluate opportunities for savings Management engaged McKinsey and Deloitte in February and continues to crystallize synergy opportunities Combined Company Has a Strong M&A Track Record Integration Process is Well Underway Rigorous planning process underway for integration Versum Transaction Entegris Transaction

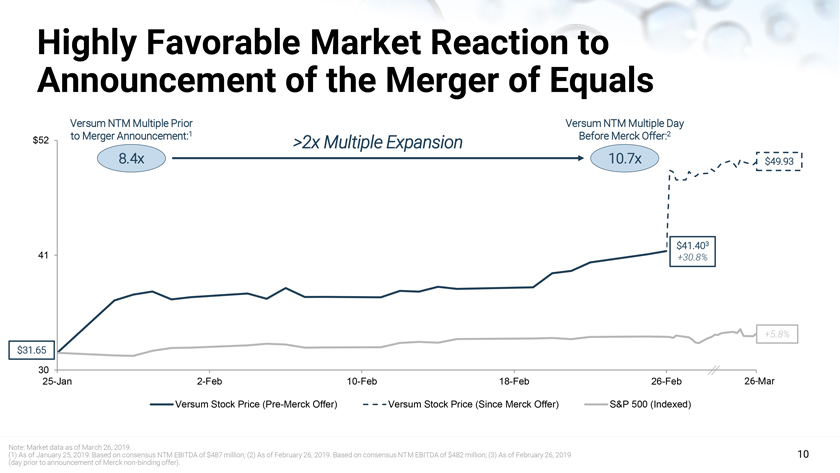

10 Highly Favorable Market Reaction to Announcement of the Merger of Equals 30 41 $52 25-Jan 2-Feb 10-Feb 18-Feb 26-Feb Versum Stock Price (Pre-Merck Offer) Versum Stock Price (Since Merck Offer) S&P 500 (Indexed) $49.93 +5.8% 8.4x Versum NTM Multiple Prior to Merger Announcement:1 10.7x Versum NTM Multiple Day Before Merck Offer:2 >2x Multiple Expansion $31.65 26-Mar $41.403 +30.8% Note: Market data as of March 26, 2019. (1) As of January 25, 2019. Based on consensus NTM EBITDA of $487 million; (2) As of February 26, 2019. Based on consensus NTM EBITDA of $482 million; (3) As of February 26, 2019 (day prior to announcement of Merck non-binding offer).

11 “The merger with Entegris appears to have slightly higher cost synergies and revenue synergies, and our LBO model supports fair value for the new company in 2022 at $73.” (March 4) “If Versummerges with Entegris, we believe it will lock in a leadership position for at least the next cycle; if it merges with Merck, we believe another round of restructuring in electronic chemicals would occur as other companies with electronic chemical portfolios, such as DWDP and 3M, re-assess the competitive landscape.” (March 4) “The combined entity could be worth $12 billion or more in enterprise value (versus the current $9 billion goal), which would make the Versumportion more valuable than the current Merck $48/share all-cash offer.” (March 8) “We would reiterate the merit of the Entegris MOE as having potential for long-term value creation and believe there is likely upside to the current cost and capex synergy targets; note that revenue synergies and favorable tax structures provide additional upside potential.” (March 1) “We believe the key benefits of the transaction are enhanced global scale and a strengthened position as a leading supplier to customers, particularly in a more challenging time in the semi cycle. The merger will create a comprehensive solutions provider across the entire semiconductor manufacturing process. The merger would increase opportunity for increased scale and improved ability to handle process challenges from customers, which want to rely on fewer, more capable suppliers.” (January 28) “We believe this deal is a strong positive as it creates a company of greater scale, with a unique set of product offerings, a more defensive portfolio and a strong B/S supporting organic growth innovation, w/ probable long-term M&A optionality for tuck-in / bolt-on deals.” (January 28) “While the companies have talked about cost synergies, we believe there are significant revenue synergy opportunities that can be created within their respective materials and chemicals technology (that can create new materials for next generation manufacturing).” (March 1) “We also believe the proposed Entegris-Versum combination offers better long-term growth potential given the breadth of products (specialty chemicals, filters, and material handling) the combined company would offer.” (February 28) Analysts Have Endorsed the Benefits from the Merger of Equals

12 Versum Has an Experienced Board and Has Followed Rigorous Governance Process 5 of 7 Directors are Independent1 Seifi Ghasemi, Chairman Chairman, President and CEO, Air Products Former Chairman and CEO, Rockwood Former President and member of Board of Directors, BOC Group Guillermo Novo President and CEO, Versum Former Executive Vice President, Air Products Former Senior Executive, Dow and Rohm & Haas Alejandro Wolff, Lead Director Member of Board of Directors, Rockwood and Albemarle Former U.S. Ambassador to the UN and Chile 33 year career with US Department of State Yi Hyon Paik Former President and Chief Strategy Officer, Samsung SDI Various leadership roles at Samsung Cheil and Dow Chemical Thomas Riordan Former Chief Legal/Administrative Officer, Rockwood Former Vice President, Laporte plc Susan Schnabel Co-Founder and Managing Partner, aPriori Capital Partners Former Managing Director, Credit Suisse and Co-Head of DLJ Merchant Banking Has served on numerous public company boards, including Neiman Marcus and Jacques Croisetière Rockwood Former Senior Vice President and CFO, Bacardi Former CFO, Rohm and Haas (1) Seifi Ghasemi to become independent in October 2019. Regular reviews of various potential financial and strategic opportunities to enhance stockholder value Included possibility of combination with Entegris Following initial conversation between the two CEOs about a possible combination, the Board undertook comprehensive discussions to evaluate the potential merger assisted by financial and legal advisors Combination with Entegris is a merger of equals and not a sale for cash Focus on long-term shareholder value creation Not comparable to a cash offer for the company Board Has Extensive Experience in M&A and Transformational Acquisitions

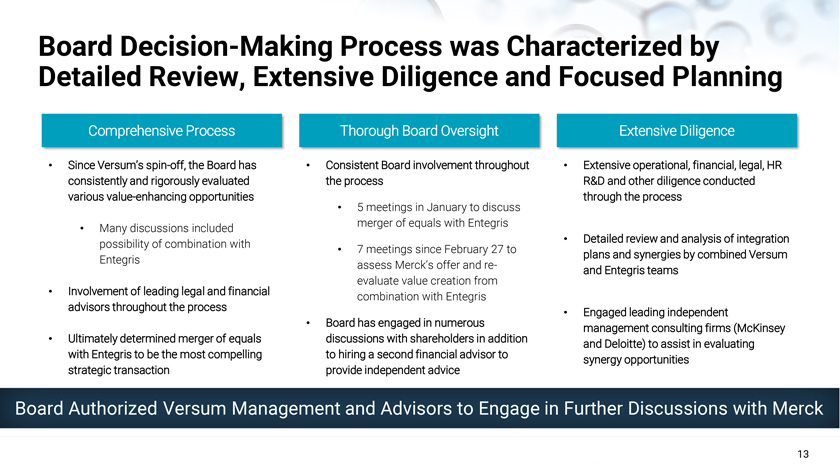

13 Board Decision-Making Process was Characterized by Detailed Review, Extensive Diligence and Focused Planning Comprehensive Process Thorough Board Oversight Extensive Diligence Since Versum’s spin-off, the Board has consistently and rigorously evaluated various value-enhancing opportunities Many discussions included possibility of combination with Entegris Involvement of leading legal and financial advisors throughout the process Ultimately determined merger of equals with Entegris to be the most compelling strategic transaction Consistent Board involvement throughout the process 5 meetings in January to discuss merger of equals with Entegris 7 meetings since February 27 to assess Merck’s offer and reevaluate value creation from combination with Entegris Board has engaged in numerous discussions with shareholders in addition to hiring a second financial advisor to provide independent advice Extensive operational, financial, legal, HR R&D and other diligence conducted through the process Detailed review and analysis of integration plans and synergies by combined Versum and Entegris teams Engaged leading independent management consulting firms (McKinsey and Deloitte) to assist in evaluating synergy opportunities Board Authorized Versum Management and Advisors to Engage in Further Discussions with Merck

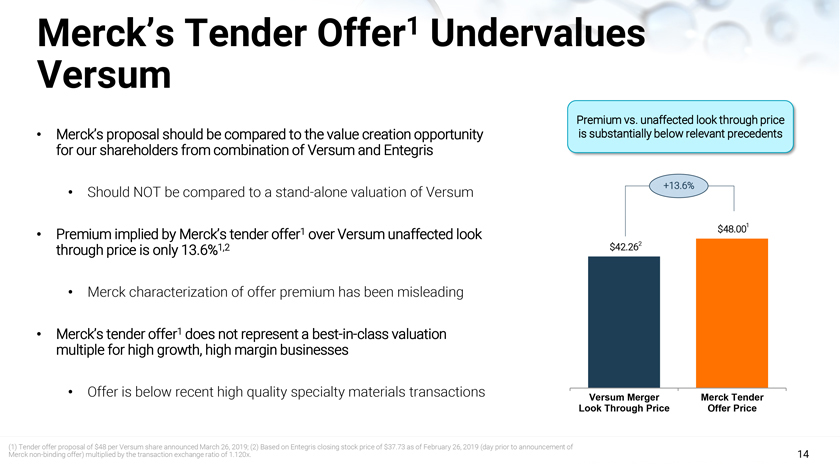

14 Merck’s proposal should be compared to the value creation opportunity for our shareholders from combination of Versum and Entegris Should NOT be compared to a stand-alone valuation of Versum Premium implied by Merck’s tender offer1 over Versum unaffected look through price is only 13.6%1,2 Merck characterization of offer premium has been misleading Merck’s tender offer1 does not represent a best-in-class valuation multiple for high growth, high margin businesses Offer is below recent high quality specialty materials transactions $42.26 $48.00 Versum Merger Look Through Price Merck Tender Offer Price +13.6% Merck’s Tender Offer1 Undervalues Versum 2 Premium vs. unaffected look through price is substantially below relevant precedents (1) Tender offer proposal of $48 per Versum share announced March 26, 2019; (2) Based on Entegris closing stock price of $37.73 as of February 26, 2019 (day prior to announcement of Merck non-binding offer) multiplied by the transaction exchange ratio of 1.120x. 1

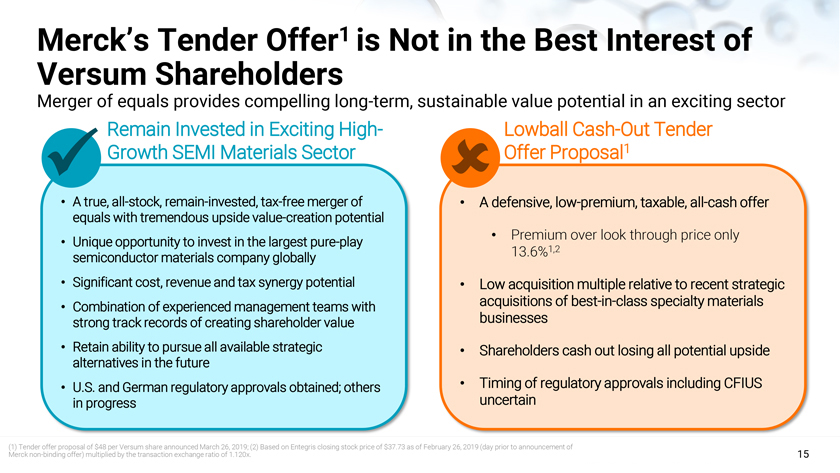

15 Merck’s Tender Offer1 is Not in the Best Interest of Versum Shareholders Merger of equals provides compelling long-term, sustainable value potential in an exciting sector A true, all-stock, remain-invested, tax-free merger of equals with tremendous upside value-creation potential Unique opportunity to invest in the largest pure-play semiconductor materials company globally Significant cost, revenue and tax synergy potential Combination of experienced management teams with strong track records of creating shareholder value Retain ability to pursue all available strategic alternatives in the future U.S. and German regulatory approvals obtained; others in progress A defensive, low-premium, taxable, all-cash offer Premium over look through price only 13.6%1,2 Low acquisition multiple relative to recent strategic acquisitions of best-in-class specialty materials businesses Shareholders cash out losing all potential upside Timing of regulatory approvals including CFIUS uncertain Remain Invested in Exciting High- Growth SEMI Materials Sector Lowball Cash-Out Tender Offer Proposal1 (1) Tender offer proposal of $48 per Versum share announced March 26, 2019; (2) Based on Entegris closing stock price of $37.73 as of February 26, 2019 (day prior to announcement of Merck non-binding offer) multiplied by the transaction exchange ratio of 1.120x.

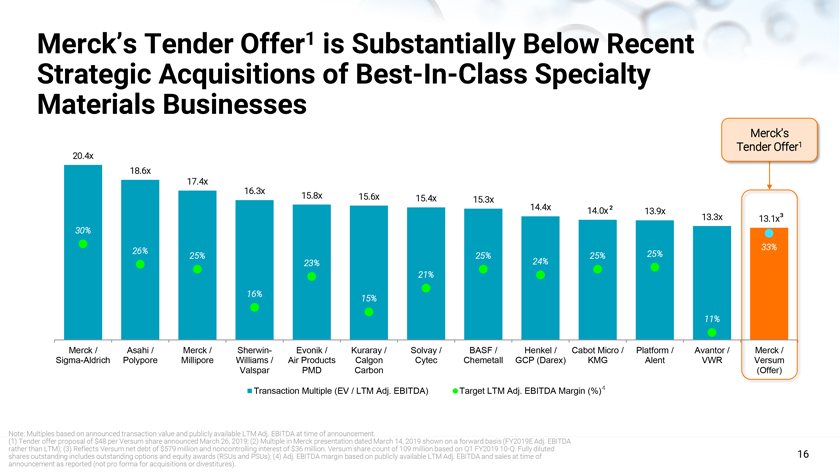

16 20.4x 18.6x 17.4x 16.3x 15.8x 15.6x 15.4x 15.3x 14.4x 14.0x 13.9x 13.3x 13.1x 30% 26% 25% 16% 23% 15% 21% 25% 24% 25% 25% 11% 33% Merck / Sigma-Aldrich Asahi / Polypore Merck / Millipore Sherwin- Williams / Valspar Evonik / Air Products PMD Kuraray / Calgon Carbon Solvay / Cytec BASF / Chemetall Henkel / GCP (Darex) Cabot Micro / KMG Platform / Alent Avantor / VWR Merck / Versum (Offer) Transaction Multiple (EV / LTM Adj. EBITDA) Target LTM Adj. EBITDA Margin (%) Merck’s Tender Offer1 is Substantially Below Recent Strategic Acquisitions of Best-In-Class Specialty Materials Businesses 2 3 Merck’s Tender Offer1 Note: Multiples based on announced transaction value and publicly available LTM Adj. EBITDA at time of announcement. (1) Tender offer proposal of $48 per Versum share announced March 26, 2019; (2) Multiple in Merck presentation dated March 14, 2019 shown on a forward basis (FY2019E Adj. EBITDA rather than LTM); (3) Reflects Versumnet debt of $579 million and noncontrolling interest of $36 million. Versum share count of 109 million based on Q1 FY2019 10-Q. Fully diluted shares outstanding includes outstanding options and equity awards (RSUs and PSUs); (4) Adj. EBITDA margin based on publicly available LTM Adj. EBITDA and sales at time of announcement as reported (not pro forma for acquisitions or divestitures). 4

17 Versum / Entegris Combination Creates Compelling Long-Term, Sustainable Value Potential for Versum Shareholders True All-Stock, Remain-Invested Merger of Equals Compelling value creation potential from the strength of the combined company Outsized revenue growth and cash flow generation and enhanced capital returns Creates Largest Pure-Play Semiconductor Materials Company Globally Unique opportunity for shareholders to invest in a premier specialty materials company with leading market positions Enhanced scale and diversified portfolio with superior growth profile SEMI materials is an exciting, high-growth sector $125 million in run-rate cost synergies $50 million EBITDA contribution from run-rate revenue synergies $10 – $15 million expected CapEx synergies Tax synergies from Entegris’s more efficient tax structure Significant Cost, Revenue, CapEx and Tax Synergy Potential Strong Balance Sheet and Excess Free Cash Flow Generation Attractive and stable margins Provides necessary flexibility for significant return of capital to shareholders, among other initiatives Combined company expected to have significant debt capacity with net leverage at closing of only ~1x Combination Creates a Premier Specialty Materials Company Combination Retains All Strategic Options, Including Pursuing and Effecting a Change-in-Control Transaction of the Combined Company in the Future, Following Realization of This Merger’s Benefits