UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-23122

American Funds Emerging Markets Bond Fund

(Exact Name of Registrant as Specified in Charter)

6455 Irvine Center Drive

Irvine, California 92618

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (949) 975-5000

Date of fiscal year end: December 31

Date of reporting period: December 31, 2023

Becky L. Park

American Funds Emerging Markets Bond Fund

6455 Irvine Center Drive

Irvine, California 92618

(Name and Address of Agent for Service)

ITEM 1 – Reports to Stockholders

American Funds Emerging

Markets Bond Fund® Annual report

for the year ended

December 31, 2023 |  |

Find compelling

opportunities in

emerging markets

bonds with a

flexible approach

The Securities and Exchange Commission has adopted new regulations that will change the content and design of annual and semi-annual shareholder reports beginning in July 2024. Certain types of information, including investment portfolio and financial statements, will not be included in the shareholder reports but will be available online, delivered free of charge upon request, and filed on a semi-annual basis on Form N-CSR.

If you would like to receive shareholder reports and other communications from the fund electronically, you may update your mailing preferences with your financial intermediary or enroll in e-delivery at capitalgroup.com (for accounts held directly with the fund).

American Funds Emerging Markets Bond Fund seeks to provide a high level of total return over the long term, of which current income is a large component.

This fund is one of more than 40 offered by Capital Group, home of American Funds, one of the nation’s largest mutual fund families. For over 90 years, Capital Group has invested with a long-term focus based on thorough research and attention to risk.

Fund results shown in this report, unless otherwise indicated, are for Class F-2 shares. Class A share results are shown at net asset value unless otherwise indicated. If a sales charge (maximum 3.75%) had been deducted, the results would have been lower. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. For current information and month-end results, refer to capitalgroup.com.

Refer to page 3 for Class F-2 and Class A share results with relevant sales charges deducted. For other share class results, refer to capitalgroup. com and americanfundsretirement.com.

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. The investment adviser is currently reimbursing a portion of other expenses. The reimbursement will be in effect through at least March 1, 2024. The adviser may elect at its discretion to extend, modify or terminate the reimbursement at that time. The investment results shown reflect the reimbursement, without which the results would have been lower. Refer to the fund’s most recent prospectus for details.

The fund’s net 30-day yield as of December 31, 2023, calculated in accordance with the U.S. Securities and Exchange Commission (SEC) formula, was 6.80% for Class F-2 shares and 6.16% for Class A shares. The fund’s gross 30-day yield as of that date was 6.66% for Class F-2 shares and 6.08% for Class A shares. The Class A share results reflect the 3.75% maximum sales charge.

The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings. The use of derivatives involves a variety of risks, which may be different from, or greater than, the risks associated with investing in traditional cash securities, such as stocks and bonds. Lower rated bonds are subject to greater fluctuations in value and risk of loss of income and principal than higher rated bonds. Investing outside the United States involves additional risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries. Refer to the fund prospectus and the Risk Factors section of this report for more information on these and other risks associated with investing in the fund.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Contents

Fellow investors:

Emerging markets bonds rose sharply in 2023 as inflation fell in key Latin American markets and remained well-contained across much of Asia. In our view, central banks in Brazil, Mexico, Colombia and Indonesia (among others) acted effectively to mitigate the post-COVID-19 inflation that affected both developed and emerging markets to varying degrees. Against this backdrop, F-2 shares of American Funds Emerging Markets Bond Fund returned 13.75% in U.S. dollar terms for the 12-month period ended December 31, 2023.

In comparison, the J.P. Morgan Emerging Markets Bond Index (EMBI) Global Diversified* gained 11.09% over the same period. This index measures broad returns across U.S. dollar-denominated emerging markets bonds. The local currency index, the J.P. Morgan Government Bond Index-Emerging Markets (GBI-EM) Global Diversified*, produced a gain of 12.70% in U.S. dollar terms for the 12-month period ended December 31, 2023.

Meanwhile, the J.P. Morgan Index Blend–50% JPM EMBI Global Diversified & 50% JPM GBI-EM Global Diversified*, a 50%/50% blend of the local currency index and the dollar bond market index, returned 11.92% in U.S. dollar terms. This index is more reflective of the fund’s strategy.

The fund paid dividends at each month-end during the period for a total of about $0.55 per share for Class F-2 shares. Fund investors who reinvested their dividends earned an income return of 7.51%, while those who elected to take their dividends in cash received an income return of 7.26%.

Market overview

Emerging markets bonds entered 2023 following a very difficult 2022, in which the J.P. Morgan Index Blend returned –14.75%. While 2023 was certainly volatile, emerging markets bonds ultimately produced strong returns, most notably in Latin America. As financial conditions

Results at a glance

For periods ended December 31, 2023, with all distributions reinvested

| | | | | | | Average annual total returns |

| | | Cumulative

total returns | | | | | | Lifetime (since

Class A inception |

| | | 6 months | | 1 year | | 3 years | | 5 years | | on 4/22/2016) |

| | | | | | | | | | | | | | | | | | | | | |

| American Funds Emerging Markets Bond Fund (Class F-2 shares) | | | 6.01 | % | | | 13.75 | % | | | –1.25 | % | | | 3.45 | % | | | 3.54 | % |

| American Funds Emerging Markets Bond Fund (Class A shares) | | | 5.84 | | | | 13.39 | | | | –1.53 | | | | 3.16 | | | | 3.30 | |

| J.P Morgan Emerging Markets Bond Index (EMBI) Global Diversified* | | | 6.73 | | | | 11.09 | | | | –3.56 | | | | 1.67 | | | | 2.23 | |

| J.P. Morgan Government Bond Index-Emerging Markets (GBI-EM) Global Diversified* | | | 4.55 | | | | 12.70 | | | | –3.16 | | | | 1.14 | | | | 1.52 | |

| Lipper Emerging Markets Hard Currency Debt Funds Average† | | | 6.69 | | | | 11.00 | | | | –2.80 | | | | 1.93 | | | | 2.40 | |

Past results are not predictive of results in future periods.

| * | The J.P. Morgan Emerging Market Bond Index (EMBI) Global Diversified is a uniquely weighted emerging market debt benchmark that tracks total returns for U.S. dollar-denominated bonds issued by emerging market sovereign and quasi-sovereign entities. The J.P. Morgan Government Bond Index-Emerging Markets Global Diversified covers the universe of regularly traded, liquid fixed-rate, domestic currency emerging market government bonds to which international investors can gain exposure. The J.P. Morgan Index Blend-50% JPM EMBI Global Diversified & 50% JPM GBI-EM Global Diversified tracks the universe of regularly traded, liquid fixed-rate local and external sovereign debt issued by emerging markets. 50% of the index covers USD-denominated emerging markets sovereign bonds and the remaining 50% has exposure to local government bonds issued by emerging markets countries except India and China, which have capital controls. The indexes are unmanaged, and their results include reinvested dividends and/or distributions but do not reflect the effect of account fees, expenses or U.S. federal income taxes. Investors cannot invest directly in an index. This report, and any product, index or fund referred to herein, is not sponsored, endorsed or promoted in any way by J.P. Morgan or any of its affiliates who provide no warranties whatsoever, express or implied, and shall have no liability to any prospective investor, in connection with this report. J.P. Morgan disclaimer: https://www.jpmm.com/research/disclosures. |

| † | Lipper averages reflect the current composition of all eligible mutual funds (all share classes) within a given category. Source: Refinitiv Lipper. Lipper categories are dynamic, and averages may have few funds, especially over longer periods. To see the number of funds included in the Lipper category for each fund’s lifetime, refer to the Quarterly Statistical Update, available on our website. |

| American Funds Emerging Markets Bond Fund | 1 |

eased, many distressed credits also posted strong returns in U.S. dollars and euros as investors gained confidence.

Broadly speaking, these returns came as emerging markets central banks took effective action to manage their interest rate cycles following the volatility and economic disruptions caused by the COVID-19 pandemic. As the pandemic receded in late 2022 and early 2023, many emerging markets central banks were well ahead of their developed market counterparts in managing the pandemic’s inflationary effects. As a result, key central banks in Latin America and Asia either kept interest rates on hold or began easing cycles by the third quarter of 2023, which generally aided local currency emerging markets bond returns.

This came as the U.S. Federal Reserve (the Fed) continued its rate-hiking campaign during the year, eventually increasing the federal funds target rate to a multiyear high of 5.25%–5.50%. While broad-based U.S. inflation remained elevated on a historical basis, core inflation fell significantly toward the end of 2023.

Within this environment, the U.S. Dollar Index (DXY)† fell 2.7% over the course of the year, while currencies such as the Colombian peso (+25.2%), the Mexican nuevo peso (+15.1%) and the Brazilian real (+8.7%) rose in U.S. dollar terms. In contrast, currencies such as the Argentine peso (–78.1%) and the Turkish lira (–36.6%) fell sharply in U.S. dollar terms as investors avoided these markets due to their economic and political challenges.

While emerging markets bonds generally rose during the year, individual markets experienced significant duress. In China, for example, economic conditions were challenging as the country’s long-anticipated post-COVID-19 reopening failed to produce the kind of sustained growth for which many investors had hoped. Meanwhile, Russia’s ongoing invasion of Ukraine continued to damage both economies dramatically as the war appeared to fall into a relative stalemate. Still, gains in other emerging bond markets more than offset these macro difficulties during the year as investors remained constructive on the asset class.

Inside the portfolio

As emerging markets bonds rose during the year, the fund’s returns exceeded the J.P. Morgan Index Blend by 1.83 percentage points in U.S. dollar terms, due in part to the portfolio’s currency, yield curve and duration positioning. (The yield curve is defined as the slope of the yield differential between short- and long-term interest rates, while duration in this context is defined as a fund’s sensitivity to changes in interest rates.) Security selection was also a meaningful contributor to relative results. The fund’s greater-than-benchmark positions in Colombia, Argentina, Brazil and Tunisia added to relative returns, while a small off-benchmark holding in Russia and the fund’s less-than-benchmark exposure to Poland both detracted.

In Colombia, political gridlock benefited returns as the lack of a clear mandate for President Gustavo Petro gave the country’s central bank an opportunity to focus squarely on implementing effective monetary policy. Meanwhile, the Brazilian central bank followed a similar course.

Hard currency bonds, and especially corporate credits, aided relative returns as they rose sharply during some of the more volatile months of the year. However, the fund’s underweight position in the U.S. dollar market and the higher yielding part of that universe in the last two months of the year detracted from overall returns. Still, the fund’s local currency positions more than compensated for this underweight exposure.

The fund benefited from its overweight exposures to the Colombian peso, Mexican peso and Brazilian real as compared to the J.P. Morgan Index Blend. The fund’s underweight position in the Czech koruna and its greater-than-benchmark exposure to the Polish zloty both detracted from returns.

Looking ahead

While the global inflation and interest rate environments appear more ambiguous in 2024 than in 2023, we believe that most developed and emerging markets are at or near a peak in both inflation and rates. In fact, broad-based inflation appears to be declining in many markets, including the U.S. Although the strong returns that emerging markets bonds produced in 2023 were on the back of a weak 2022, we believe that 2024 can provide positive returns as well.

In our view, the duration, foreign exchange and starting yield components of emerging bond markets remain very attractive. At this stage of the economic cycle, most local currencies appear reasonably valued versus the U.S. dollar. In addition, we believe emerging markets bonds will likely benefit if global interest rates fall significantly in 2024, given that in that scenario, issuers would be refinancing at lower rates than in the recent past.

Nevertheless, some uncertainty remains within the global economic outlook. While the Fed appears to be leaning toward cutting rates in 2024, that posture may change if U.S. inflation is more persistent than expected. In China, although some degree of economic stimulus seems likely this year, we remain concerned about the country’s political environment and the resilience of Chinese consumers. Taking these factors into account, volatility appears likely to persist during the year. Even in light of this uncertainty, however, we continue to believe that emerging markets bond valuations appear attractive and that economic growth in most emerging markets is likely to be reasonably strong in 2024.

During the year, former fund president Robert Neithart retired from Capital Group. I am honored to assume the role of president of the fund in Robert’s stead. We thank you for making American Funds Emerging Markets Bond Fund part of your portfolio and look forward to reporting to you again in six months.

Sincerely,

Kirstie Spence

President

February 9, 2024

For current information about the fund, visit capitalgroup.com.

Past results are not predictive of results in future periods.

| † | The ICE U.S. Dollar Index is a geometrically averaged calculation that measures the value of the U.S. dollar relative to a basket of foreign currencies: the euro, the yen, the British pound, the Canadian dollar, the Swedish krona and the Swiss franc. The U.S. Dollar Index, together with all rights, title and interest in and related to the U.S. Dollar Index, including all content included therein and all related intellectual property and property rights, is the exclusive property of ICE Data Indices, LLC. |

| 2 | American Funds Emerging Markets Bond Fund |

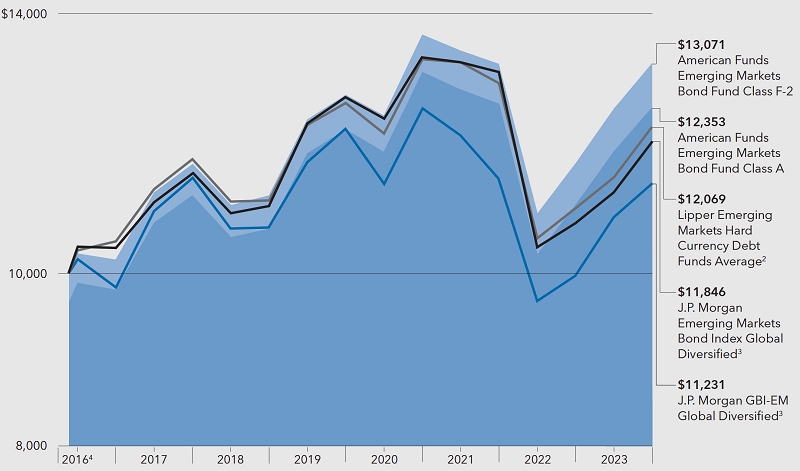

The value of a $10,000 investment

How a hypothetical $10,000 investment has fared for the period April 22, 2016, to December 31, 2023, with all distributions reinvested.

Fund results shown are for Class F-2 and Class A shares. Class A shares reflect deduction of the maximum sales charge of 3.75% on the $10,000 investment.1 Thus, the net amount invested was $9,625.

Past results are not predictive of results for future periods. The results shown are before taxes on fund distributions and sale of fund shares.

| 1 | As outlined in the prospectus, the sales charge is reduced for accounts (and aggregated investments) of $100,000 or more and is eliminated for purchases of $500,000 or more. There is no sales charge on dividends or capital gain distributions that are reinvested in additional shares. |

| 2 | Results of the Lipper Emerging Markets Hard Currency Debt Funds Average do not reflect any sales charges. Lipper averages reflect the current composition of all eligible mutual funds (all share classes) within a given category. Source: Refinitiv Lipper. Lipper categories are dynamic and averages may have few funds, especially over longer periods. For the number of funds included in the Lipper category for each fund’s lifetime, refer to the Quarterly Statistical Update, available on our website. |

| 3 | This report, and any product, index or fund referred to herein, is not sponsored, endorsed or promoted in any way by J.P. Morgan or any of its affiliates who provide no warranties whatsoever, express or implied, and shall have no liability to any prospective investor, in connection with this report. J.P. Morgan disclaimer: https://www.jpmm.com/research/disclosures. |

| 4 | For the period April 22, 2016, commencement of fund operations, through December 31, 2016. |

Total returns based on a $1,000 investment (for the period ended December 31, 2023)

| | | 1 year | | 5 years | | Lifetime (since

Class A inception

on 4/22/16) |

| | | | | | | |

| Class F-2 shares | | | 13.75 | % | | | 3.45 | % | | | 3.54 | % |

| Class A shares* | | | 9.08 | | | | 2.38 | | | | 2.78 | |

| * | Assumes payment of the maximum 3.75% sales charge. |

The total annual fund operating expense ratios are 0.66% for Class F-2 shares and 0.97% for Class A shares as of the prospectus dated March 1, 2024 (unaudited).

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, investment results reflect fee waivers and/or expense reimbursements, without which they would have been lower. Refer to capitalgroup.com for more information.

| American Funds Emerging Markets Bond Fund | 3 |

Investment portfolio December 31, 2023

| Investment mix by security type | Percent of net assets |

| Portfolio quality summary* | | Percent of

net assets |

| U.S. Treasury and agency† | | | 4.62 | % |

| AA/Aa | | | 7.99 | |

| A/A | | | 14.10 | |

| BBB/Baa | | | 30.51 | |

| Below investment grade | | | 35.23 | |

| Short-term securities & other assets less liabilities | | | 7.55 | |

| * | Bond ratings, which typically range from AAA/Aaa (highest) to D (lowest), are assigned by credit rating agencies such as Standard & Poor’s, Moody’s and/or Fitch as an indication of an issuer’s creditworthiness. In assigning a credit rating to a security, the fund looks specifically to the ratings assigned to the issuer of the security by Standard & Poor’s, Moody’s and/or Fitch. If agency ratings differ, the security will be considered to have received the highest of those ratings, consistent with the fund’s investment policies. The ratings are not covered by the Report of Independent Registered Public Accounting Firm. |

| † | These securities are guaranteed by the full faith and credit of the U.S. government. |

| | |

| Bonds, notes & other debt instruments 91.67% | | Principal amount

(000) | | | Value

(000) | |

| Bonds & notes of governments & government agencies outside the U.S. 69.17% | | | | | | | | |

| Abu Dhabi (Emirate of) 2.50% 9/30/20291 | | USD | 1,150 | | | $ | 1,054 | |

| Abu Dhabi (Emirate of) 3.125% 9/30/2049 | | | 2,700 | | | | 1,990 | |

| Albania (Republic of) 5.90% 6/9/2028 | | EUR | 4,140 | | | | 4,682 | |

| Angola (Republic of) 9.50% 11/12/2025 | | USD | 1,280 | | | | 1,260 | |

| Angola (Republic of) 8.00% 11/26/20291 | | | 4,100 | | | | 3,653 | |

| Angola (Republic of) 8.00% 11/26/2029 | | | 2,110 | | | | 1,880 | |

| Angola (Republic of) 8.75% 4/14/2032 | | | 3,000 | | | | 2,647 | |

| Angola (Republic of) 8.75% 4/14/20321 | | | 500 | | | | 441 | |

| Angola (Republic of) 9.125% 11/26/2049 | | | 3,480 | | | | 2,849 | |

| Argentine Republic 0.50% 7/9/2029 | | EUR | 65 | | | | 26 | |

| Argentine Republic 1.00% 7/9/2029 | | USD | 1,290 | | | | 519 | |

| Argentine Republic 0.75% 7/9/2030 (1.75% on 7/9/2027)2 | | | 19,050 | | | | 7,687 | |

| Argentine Republic 3.625% 7/9/2035 (4.125% on 7/9/2024)2 | | | 11,460 | | | | 3,960 | |

| Argentine Republic 0% 12/15/2035 | | | 600 | | | | 21 | |

| Argentine Republic 3.00% 1/9/2038 (3.75% on 7/9/2024)2 | | EUR | 978 | | | | 385 | |

| Azerbaijan (Republic of) 3.50% 9/1/2032 | | USD | 910 | | | | 792 | |

| Brazil (Federative Republic of) 6.00% 8/15/20243 | | BRL | 11,063 | | | | 2,271 | |

| Brazil (Federative Republic of) 10.00% 1/1/2025 | | | 10,600 | | | | 2,184 | |

| Brazil (Federative Republic of) 0% 7/1/2025 | | | 7,123 | | | | 1,277 | |

| Brazil (Federative Republic of) 0% 1/1/2026 | | | 61,600 | | | | 10,543 | |

| Brazil (Federative Republic of) 6.00% 8/15/20263 | | | 12,882 | | | | 2,704 | |

| Brazil (Federative Republic of) 10.00% 1/1/2027 | | | 23,420 | | | | 4,841 | |

| Brazil (Federative Republic of) 10.00% 1/1/2029 | | | 101,081 | | | | 20,768 | |

| Brazil (Federative Republic of) 10.00% 1/1/2031 | | | 52,986 | | | | 10,780 | |

| Brazil (Federative Republic of) 10.00% 1/1/2033 | | | 12,525 | | | | 2,542 | |

| Brazil (Federative Republic of) 6.00% 8/15/20503 | | | 58,322 | | | | 12,926 | |

| Bulgaria (Republic of) 4.375% 5/13/2031 | | EUR | 1,390 | | | | 1,615 | |

| Bulgaria (Republic of) 4.50% 1/27/2033 | | | 1,310 | | | | 1,522 | |

| Chile (Republic of) 5.00% 10/1/2028 | | CLP | 595,000 | | | | 664 | |

| Chile (Republic of) 4.70% 9/1/2030 | | | 1,740,000 | | | | 1,904 | |

| Chile (Republic of) 6.00% 4/1/2033 | | | 340,000 | | | | 406 | |

| | |

| 4 | American Funds Emerging Markets Bond Fund |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Bonds & notes of governments & government agencies outside the U.S. (continued) | | | | | | | | |

| Chile (Republic of) 5.30% 11/1/2037 | | CLP | 2,980,000 | | | $ | 3,407 | |

| Chile (Republic of) 3.10% 5/7/2041 | | USD | 2,150 | | | | 1,642 | |

| Chile (Republic of) 4.34% 3/7/2042 | | | 1,810 | | | | 1,623 | |

| Chile (Republic of) 4.00% 1/31/2052 | | | 200 | | | | 165 | |

| China (People’s Republic of), Series INBK, 2.26% 2/24/2025 | | CNY | 8,650 | | | | 1,221 | |

| China (People’s Republic of), Series INBK, 2.48% 4/15/2027 | | | 3,930 | | | | 556 | |

| China (People’s Republic of), Series INBK, 2.85% 6/4/2027 | | | 1,480 | | | | 212 | |

| China (People’s Republic of), Series INBK, 2.40% 7/15/2028 | | | 4,100 | | | | 579 | |

| China (People’s Republic of), Series INBK, 2.80% 3/24/2029 | | | 25,260 | | | | 3,621 | |

| China (People’s Republic of), Series INBK, 2.68% 5/21/2030 | | | 16,050 | | | | 2,281 | |

| China (People’s Republic of), Series INBK, 2.69% 8/15/2032 | | | 9,450 | | | | 1,343 | |

| China (People’s Republic of), Series 1910, 3.86% 7/22/2049 | | | 15,670 | | | | 2,589 | |

| China (People’s Republic of), Series INBK, 3.39% 3/16/2050 | | | 23,270 | | | | 3,575 | |

| China (People’s Republic of), Series INBK, 3.32% 4/15/2052 | | | 2,070 | | | | 315 | |

| China (People’s Republic of), Series INBK, 3.12% 10/25/2052 | | | 54,400 | | | | 8,001 | |

| China (People’s Republic of), Series INBK, 3.19% 4/15/2053 | | | 5,500 | | | | 829 | |

| China Development Bank Corp., Series 2009, 3.39% 7/10/2027 | | | 6,590 | | | | 958 | |

| China Development Bank Corp., Series 1905, 3.48% 1/8/2029 | | | 8,350 | | | | 1,228 | |

| Colombia (Republic of) 4.50% 3/15/2029 | | USD | 241 | | | | 226 | |

| Colombia (Republic of) 3.00% 1/30/2030 | | | 278 | | | | 235 | |

| Colombia (Republic of) 7.00% 3/26/2031 | | COP | 5,102,400 | | | | 1,137 | |

| Colombia (Republic of) 3.125% 4/15/2031 | | USD | 1,311 | | | | 1,071 | |

| Colombia (Republic of) 3.25% 4/22/2032 | | | 1,053 | | | | 839 | |

| Colombia (Republic of) 8.00% 4/20/2033 | | | 2,560 | | | | 2,797 | |

| Colombia (Republic of) 7.50% 2/2/2034 | | | 1,720 | | | | 1,820 | |

| Colombia (Republic of) 8.00% 11/14/2035 | | | 1,250 | | | | 1,370 | |

| Colombia (Republic of) 7.375% 9/18/2037 | | | 610 | | | | 635 | |

| Colombia (Republic of) 5.625% 2/26/2044 | | | 261 | | | | 220 | |

| Colombia (Republic of) 5.00% 6/15/2045 | | | 785 | | | | 612 | |

| Colombia (Republic of) 5.20% 5/15/2049 | | | 200 | | | | 157 | |

| Colombia (Republic of) 4.125% 5/15/2051 | | | 4,850 | | | | 3,239 | |

| Colombia (Republic of), Series B, 5.75% 11/3/2027 | | COP | 17,804,900 | | | | 4,073 | |

| Colombia (Republic of), Series B, 7.00% 3/26/2031 | | | 48,378,900 | | | | 10,777 | |

| Colombia (Republic of), Series B, 7.25% 10/18/2034 | | | 6,248,200 | | | | 1,328 | |

| Colombia (Republic of), Series UVR, 3.75% 2/25/20373 | | | 20,000 | | | | 1,770 | |

| Colombia (Republic of), Series B, 9.25% 5/28/2042 | | | 29,273,000 | | | | 6,859 | |

| Colombia (Republic of), Series B, 7.25% 10/26/2050 | | | 3,615,200 | | | | 680 | |

| Cote d’Ivoire (Republic of) 5.25% 3/22/2030 | | EUR | 1,380 | | | | 1,371 | |

| Cote d’Ivoire (Republic of) 5.875% 10/17/2031 | | | 1,745 | | | | 1,732 | |

| Cote d’Ivoire (Republic of) 4.875% 1/30/2032 | | | 970 | | | | 905 | |

| Cote d’Ivoire (Republic of) 6.875% 10/17/2040 | | | 4,000 | | | | 3,707 | |

| Czech Republic 5.70% 5/25/2024 | | CZK | 23,170 | | | | 1,040 | |

| Czech Republic 1.25% 2/14/2025 | | | 61,810 | | | | 2,662 | |

| Czech Republic 2.40% 9/17/2025 | | | 13,000 | | | | 562 | |

| Czech Republic 1.00% 6/26/2026 | | | 9,070 | | | | 376 | |

| Czech Republic 2.50% 8/25/2028 | | | 19,360 | | | | 822 | |

| Czech Republic 0.95% 5/15/2030 | | | 10,520 | | | | 398 | |

| Czech Republic 1.20% 3/13/2031 | | | 30,160 | | | | 1,138 | |

| Czech Republic 4.90% 4/14/2034 | | | 159,600 | | | | 7,838 | |

| Czech Republic 1.95% 7/30/2037 | | | 258,940 | | | | 9,336 | |

| Czech Republic 1.50% 4/24/2040 | | | 53,320 | | | | 1,717 | |

| Development Bank of Kazakhstan JSC 10.75% 2/12/2025 | | KZT | 85,750 | | | | 179 | |

| Development Bank of Kazakhstan JSC 10.95% 5/6/2026 | | | 1,313,500 | | | | 2,595 | |

| Development Bank of Kazakhstan JSC 10.95% 5/6/2026 | | | 218,500 | | | | 432 | |

| Dominican Republic 5.95% 1/25/20271 | | USD | 2,300 | | | | 2,313 | |

| Dominican Republic 5.95% 1/25/2027 | | | 1,700 | | | | 1,710 | |

| Dominican Republic 5.50% 2/22/20291 | | | 1,420 | | | | 1,392 | |

| Dominican Republic 5.50% 2/22/2029 | | | 500 | | | | 490 | |

| Dominican Republic 4.50% 1/30/20301 | | | 4,988 | | | | 4,608 | |

| Dominican Republic 7.05% 2/3/20311 | | | 665 | | | | 700 | |

| Dominican Republic 13.625% 2/3/2033 | | DOP | 49,250 | | | | 1,034 | |

| Dominican Republic 13.625% 2/3/2033 | | | 24,200 | | | | 508 | |

| Dominican Republic 6.00% 2/22/20331 | | USD | 805 | | | | 796 | |

| Dominican Republic 11.25% 9/15/2035 | | DOP | 121,300 | | | | 2,259 | |

| Dominican Republic 11.25% 9/15/2035 | | | 38,450 | | | | 716 | |

| Dominican Republic 5.30% 1/21/2041 | | USD | 1,000 | | | | 867 | |

| Dominican Republic 5.30% 1/21/20411 | | | 887 | | | | 769 | |

| | |

| American Funds Emerging Markets Bond Fund | 5 |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Bonds & notes of governments & government agencies outside the U.S. (continued) | | | | | | | | |

| Dominican Republic 5.875% 1/30/2060 | | USD | 6,365 | | | $ | 5,522 | |

| Dominican Republic 5.875% 1/30/20601 | | | 2,170 | | | | 1,882 | |

| Egypt (Arab Republic of) 6.588% 2/21/20281 | | | 2,528 | | | | 1,946 | |

| Egypt (Arab Republic of) 6.588% 2/21/2028 | | | 1,445 | | | | 1,112 | |

| Egypt (Arab Republic of) 5.625% 4/16/2030 | | EUR | 1,000 | | | | 708 | |

| Egypt (Arab Republic of) 7.053% 1/15/2032 | | USD | 404 | | | | 278 | |

| Egypt (Arab Republic of) 7.625% 5/29/2032 | | | 1,000 | | | | 697 | |

| Egypt (Arab Republic of) 7.625% 5/29/20321 | | | 575 | | | | 401 | |

| Egypt (Arab Republic of) 8.875% 5/29/2050 | | | 660 | | | | 422 | |

| Egypt (Arab Republic of) 8.75% 9/30/2051 | | | 880 | | | | 559 | |

| Egypt (Arab Republic of) 8.15% 11/20/20591 | | | 1,300 | | | | 802 | |

| Ethiopia (Federal Democratic Republic of) 6.625% 12/11/20244 | | | 3,575 | | | | 2,430 | |

| European Bank for Reconstruction & Development 5.15% 2/16/2024 | | INR | 66,300 | | | | 796 | |

| European Bank for Reconstruction & Development 6.30% 10/26/2027 | | | 75,500 | | | | 896 | |

| Export-Import Bank of India 3.25% 1/15/2030 | | USD | 250 | | | | 229 | |

| Export-Import Bank of India 5.50% 1/18/2033 | | | 1,000 | | | | 1,036 | |

| Export-Import Bank of Korea 4.25% 9/15/2027 | | | 805 | | | | 798 | |

| Gabonese Republic 6.95% 6/16/2025 | | | 1,048 | | | | 1,002 | |

| Gabonese Republic 6.625% 2/6/20311 | | | 400 | | | | 335 | |

| Gabonese Republic 7.00% 11/24/20311 | | | 1,820 | | | | 1,522 | |

| Gabonese Republic 7.00% 11/24/2031 | | | 1,710 | | | | 1,430 | |

| Gaci First Investment Co. 5.00% 10/13/2027 | | | 500 | | | | 505 | |

| Georgia (Republic of) 2.75% 4/22/20261 | | | 1,975 | | | | 1,856 | |

| Ghana (Republic of) 7.75% 4/7/20291,4 | | | 1,900 | | | | 835 | |

| Ghana (Republic of) 7.625% 5/16/20294 | | | 490 | | | | 215 | |

| Honduras (Republic of) 6.25% 1/19/2027 | | | 6,610 | | | | 6,362 | |

| Honduras (Republic of) 6.25% 1/19/20271 | | | 263 | | | | 253 | |

| Honduras (Republic of) 5.625% 6/24/2030 | | | 3,806 | | | | 3,402 | |

| Honduras (Republic of) 5.625% 6/24/20301 | | | 2,285 | | | | 2,042 | |

| Hungary (Republic of) 5.00% 2/22/2027 | | EUR | 1,625 | | | | 1,875 | |

| Hungary (Republic of) 6.125% 5/22/20281 | | USD | 3,130 | | | | 3,259 | |

| Hungary (Republic of) 2.00% 5/23/2029 | | HUF | 170,250 | | | | 410 | |

| Hungary (Republic of) 2.125% 9/22/2031 | | USD | 810 | | | | 655 | |

| Hungary (Republic of) 6.25% 9/22/20321 | | | 1,000 | | | | 1,069 | |

| Hungary (Republic of) 5.375% 9/12/2033 | | EUR | 2,000 | | | | 2,365 | |

| Hungary (Republic of), Series B, 3.00% 6/26/2024 | | HUF | 478,930 | | | | 1,356 | |

| Hungary (Republic of), Series B, 5.50% 6/24/2025 | | | 788,900 | | | | 2,249 | |

| Hungary (Republic of), Series A, 6.75% 10/22/2028 | | | 854,520 | | | | 2,560 | |

| Hungary (Republic of), Series A, 3.25% 10/22/2031 | | | 675,650 | | | | 1,659 | |

| Hungary (Republic of), Series 32-A, 4.75% 11/24/2032 | | | 738,200 | | | | 1,967 | |

| Hungary (Republic of), Series 41-A, 3.00% 4/25/2041 | | | 1,200,000 | | | | 2,344 | |

| India (Republic of) 6.54% 1/17/2032 | | INR | 405,000 | | | | 4,680 | |

| Indonesia (Republic of) 4.65% 9/20/2032 | | USD | 2,040 | | | | 2,043 | |

| Indonesia (Republic of) 6.625% 2/15/2034 | | IDR | 2,995,000 | | | | 195 | |

| Indonesia (Republic of) 6.625% 2/17/2037 | | USD | 300 | | | | 352 | |

| Indonesia (Republic of) 5.25% 1/17/2042 | | | 600 | | | | 627 | |

| Indonesia (Republic of), Series 77, 8.125% 5/15/2024 | | IDR | 6,918,000 | | | | 452 | |

| Indonesia (Republic of), Series 59, 7.00% 5/15/2027 | | | 31,785,000 | | | | 2,100 | |

| Indonesia (Republic of), Series 64, 6.125% 5/15/2028 | | | 69,965,000 | | | | 4,489 | |

| Indonesia (Republic of), Series 95, 6.375% 8/15/2028 | | | 29,230,000 | | | | 1,895 | |

| Indonesia (Republic of), Series 71, 9.00% 3/15/2029 | | | 15,635,000 | | | | 1,124 | |

| Indonesia (Republic of), Series 78, 8.25% 5/15/2029 | | | 35,718,000 | | | | 2,502 | |

| Indonesia (Republic of), Series 82, 7.00% 9/15/2030 | | | 100,205,000 | | | | 6,653 | |

| Indonesia (Republic of), Series 87, 6.50% 2/15/2031 | | | 107,654,000 | | | | 6,964 | |

| Indonesia (Republic of), Series 73, 8.75% 5/15/2031 | | | 28,473,000 | | | | 2,070 | |

| Indonesia (Republic of), Series 91, 6.375% 4/15/2032 | | | 154,160,000 | | | | 9,911 | |

| Indonesia (Republic of), Series 58, 8.25% 6/15/2032 | | | 40,712,000 | | | | 2,907 | |

| Indonesia (Republic of), Series 74, 7.50% 8/15/2032 | | | 50,000,000 | | | | 3,441 | |

| Indonesia (Republic of), Series 96, 7.00% 2/15/2033 | | | 97,834,000 | | | | 6,589 | |

| Indonesia (Republic of), Series 65, 6.625% 5/15/2033 | | | 19,400,000 | | | | 1,265 | |

| Indonesia (Republic of), Series 68, 8.375% 3/15/2034 | | | 45,362,000 | | | | 3,295 | |

| Indonesia (Republic of), Series 80, 7.50% 6/15/2035 | | | 33,080,000 | | | | 2,291 | |

| Indonesia (Republic of), Series 72, 8.25% 5/15/2036 | | | 33,753,000 | | | | 2,472 | |

| Indonesia (Republic of), Series 92, 7.125% 6/15/2042 | | | 19,170,000 | | | | 1,292 | |

| Indonesia Asahan Aluminium (Persero) PT 4.75% 5/15/2025 | | USD | 1,600 | | | | 1,581 | |

| Indonesia Asahan Aluminium (Persero) PT 6.53% 11/15/2028 | | | 264 | | | | 277 | |

| Indonesia Asahan Aluminium (Persero) PT 5.80% 5/15/2050 | | | 300 | | | | 292 | |

| | |

| 6 | American Funds Emerging Markets Bond Fund |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Bonds & notes of governments & government agencies outside the U.S. (continued) | | | | | | | | |

| International Bank for Reconstruction and Development 6.85% 4/24/2028 | | INR | 316,500 | | | $ | 3,815 | |

| International Finance Corp. 6.30% 11/25/2024 | | | 159,470 | | | | 1,905 | |

| Israel (State of) 2.875% 3/16/2026 | | USD | 373 | | | | 356 | |

| Israel (State of) 2.25% 9/28/2028 | | ILS | 1,750 | | | | 456 | |

| Israel (State of) 2.75% 7/3/2030 | | USD | 4,319 | | | | 3,825 | |

| Israel (State of) 6.50% 11/6/2031 | | | 4,201 | | | | 4,533 | |

| Israel (State of) 1.30% 4/30/2032 | | ILS | 13,390 | | | | 3,013 | |

| Israel (State of) 4.50% 1/17/2033 | | USD | 2,655 | | | | 2,528 | |

| Jordan (Hashemite Kingdom of) 7.50% 1/13/2029 | | | 1,555 | | | | 1,579 | |

| Jordan (Hashemite Kingdom of) 5.85% 7/7/2030 | | | 1,555 | | | | 1,450 | |

| Jordan (Hashemite Kingdom of) 7.375% 10/10/2047 | | | 1,036 | | | | 924 | |

| Kazakhstan (Republic of) 6.50% 7/21/2045 | | | 800 | | | | 917 | |

| Kenya (Republic of) 6.875% 6/24/2024 | | | 775 | | | | 755 | |

| Kenya (Republic of) 7.25% 2/28/20281 | | | 1,725 | | | | 1,582 | |

| Magyar Export-Import Bank 6.00% 5/16/2029 | | EUR | 6,204 | | | | 7,286 | |

| Malaysia (Federation of), Series 0319, 3.478% 6/14/2024 | | MYR | 2,599 | | | | 566 | |

| Malaysia (Federation of), Series 0115, 3.955% 9/15/2025 | | | 5 | | | | 1 | |

| Malaysia (Federation of), Series 0120, 3.422% 9/30/2027 | | | 3,852 | | | | 832 | |

| Malaysia (Federation of), Series 0417, 3.899% 11/16/2027 | | | 1,300 | | | | 286 | |

| Malaysia (Federation of), Series 0513, 3.733% 6/15/2028 | | | 1,870 | | | | 408 | |

| Malaysia (Federation of), Series 0218, 4.369% 10/31/2028 | | | 5,197 | | | | 1,165 | |

| Malaysia (Federation of), Series 0219, 3.885% 8/15/2029 | | | 12,810 | | | | 2,811 | |

| Malaysia (Federation of), Series 0220, 2.632% 4/15/2031 | | | 3,367 | | | | 677 | |

| Malaysia (Federation of), Series 0122, 3.582% 7/15/2032 | | | 2,100 | | | | 449 | |

| Malaysia (Federation of), Series 0419, 3.828% 7/5/2034 | | | 44,230 | | | | 9,567 | |

| Malaysia (Federation of), Series 0415, 4.254% 5/31/2035 | | | 19,350 | | | | 4,320 | |

| Malaysia (Federation of), Series 0615, 4.786% 10/31/2035 | | | 5,925 | | | | 1,392 | |

| Malaysia (Federation of), Series 0317, 4.762% 4/7/2037 | | | 562 | | | | 132 | |

| Malaysia (Federation of), Series 0418, 4.893% 6/8/2038 | | | 44,666 | | | | 10,676 | |

| Malaysia (Federation of), Series 0519, 3.757% 5/22/2040 | | | 2,500 | | | | 521 | |

| Malaysia (Federation of), Series 0221, 4.417% 9/30/2041 | | | 699 | | | | 158 | |

| Malaysia (Federation of), Series 0519, 4.638% 11/15/2049 | | | 2,448 | | | | 559 | |

| Malaysia (Federation of), Series 0120, 4.065% 6/15/2050 | | | 2,594 | | | | 555 | |

| Malaysia (Federation of), Series 022, 5.357% 5/15/2052 | | | 2,352 | | | | 598 | |

| MFB Magyar Fejlesztesi Bank Zartkoruen Mukodo Reszvenytarsasag 6.50% 6/29/2028 | | USD | 2,200 | | | | 2,269 | |

| Mic Capital Management (Rsc) Seven, Ltd. 5.084% 5/22/20531 | | | 200 | | | | 197 | |

| Mongolia (State of) 3.50% 7/7/2027 | | | 200 | | | | 179 | |

| Mongolia (State of) 8.65% 1/19/20281 | | | 1,492 | | | | 1,566 | |

| Mongolia (State of) 8.65% 1/19/2028 | | | 550 | | | | 577 | |

| Morocco (Kingdom of) 1.375% 3/30/2026 | | EUR | 433 | | | | 452 | |

| Morocco (Kingdom of) 5.95% 3/8/20281 | | USD | 1,225 | | | | 1,259 | |

| Mozambique (Republic of) 9.00% 9/15/2031 | | | 4,590 | | | | 3,921 | |

| Namibia (Republic of) 5.25% 10/29/2025 | | | 2,000 | | | | 1,981 | |

| Nigeria (Republic of) 8.375% 3/24/2029 | | | 250 | | | | 241 | |

| Nigeria (Republic of) 7.875% 2/16/2032 | | | 3,030 | | | | 2,732 | |

| Nigeria (Republic of) 8.25% 9/28/2051 | | | 4,585 | | | | 3,776 | |

| Oman (Sultanate of) 5.625% 1/17/2028 | | | 1,000 | | | | 1,021 | |

| Oman (Sultanate of) 4.875% 6/15/20301 | | | 800 | | | | 792 | |

| Oman (Sultanate of) 6.25% 1/25/20311 | | | 2,771 | | | | 2,920 | |

| Oman (Sultanate of) 6.75% 1/17/2048 | | | 3,437 | | | | 3,605 | |

| Oman (Sultanate of) 7.00% 1/25/2051 | | | 279 | | | | 302 | |

| Panama (Republic of) 7.125% 1/29/2026 | | | 710 | | | | 729 | |

| Panama (Republic of) 3.16% 1/23/2030 | | | 830 | | | | 709 | |

| Panama (Republic of) 6.375% 7/25/20331 | | | 5,310 | | | | 4,989 | |

| Panama (Republic of) 6.40% 2/14/2035 | | | 2,560 | | | | 2,505 | |

| Panama (Republic of) 6.875% 1/31/2036 | | | 2,240 | | | | 2,241 | |

| Panama (Republic of) 4.50% 5/15/2047 | | | 1,350 | | | | 962 | |

| Panama (Republic of) 4.50% 4/16/2050 | | | 700 | | | | 487 | |

| Panama (Republic of) 4.30% 4/29/2053 | | | 820 | | | | 551 | |

| Panama (Republic of) 6.853% 3/28/2054 | | | 1,200 | | | | 1,126 | |

| Panama (Republic of) 4.50% 4/1/2056 | | | 673 | | | | 454 | |

| Panama (Republic of) 3.87% 7/23/2060 | | | 1,696 | | | | 1,020 | |

| Panama (Republic of) 4.50% 1/19/2063 | | | 2,704 | | | | 1,776 | |

| Paraguay (Republic of) 5.00% 4/15/2026 | | | 154 | | | | 153 | |

| Paraguay (Republic of) 4.95% 4/28/2031 | | | 430 | | | | 421 | |

| Paraguay (Republic of) 5.60% 3/13/20481 | | | 2,432 | | | | 2,224 | |

| Peru (Republic of) 4.125% 8/25/2027 | | | 1,056 | | | | 1,035 | |

| | |

| American Funds Emerging Markets Bond Fund | 7 |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Bonds & notes of governments & government agencies outside the U.S. (continued) | | | | | | | | |

| Peru (Republic of) 6.95% 8/12/2031 | | PEN | 3,045 | | | $ | 854 | |

| Peru (Republic of) 6.15% 8/12/2032 | | | 6,752 | | | | 1,783 | |

| Peru (Republic of) 3.00% 1/15/2034 | | USD | 840 | | | | 712 | |

| Peru (Republic of) 5.40% 8/12/2034 | | PEN | 14,786 | | | | 3,615 | |

| Peru (Republic of) 5.40% 8/12/2034 | | | 3,039 | | | | 743 | |

| Peru (Republic of) 3.55% 3/10/2051 | | USD | 1,100 | | | | 837 | |

| Peru (Republic of) 2.78% 12/1/2060 | | | 1,615 | | | | 1,011 | |

| PETRONAS Capital, Ltd. 3.50% 4/21/20301 | | | 1,000 | | | | 940 | |

| PETRONAS Capital, Ltd. 3.50% 4/21/2030 | | | 300 | | | | 282 | |

| PETRONAS Capital, Ltd. 4.50% 3/18/2045 | | | 200 | | | | 184 | |

| PETRONAS Capital, Ltd. 3.404% 4/28/2061 | | | 250 | | | | 180 | |

| Philippines (Republic of) 2.95% 5/5/2045 | | | 1,487 | | | | 1,120 | |

| Philippines (Republic of) 5.95% 10/13/2047 | | | 600 | | | | 671 | |

| Poland (Republic of) 7.50% 7/25/2028 | | PLN | 2,825 | | | | 791 | |

| Poland (Republic of) 4.875% 10/4/2033 | | USD | 2,545 | | | | 2,586 | |

| Poland (Republic of) 6.00% 10/25/2033 | | PLN | 7,830 | | | | 2,112 | |

| Poland (Republic of), Series 0726, 2.50% 7/25/2026 | | | 17,700 | | | | 4,238 | |

| Poland (Republic of), Series 5Y, 3.75% 5/25/2027 | | | 36,370 | | | | 8,909 | |

| Poland (Republic of), Series 0727, 2.50% 7/25/2027 | | | 1,754 | | | | 412 | |

| Poland (Republic of), Series 1029, 2.75% 10/25/2029 | | | 1,781 | | | | 404 | |

| Poland (Republic of), Series 1030, 1.25% 10/25/2030 | | | 1,413 | | | | 284 | |

| Poland (Republic of), Series 0432, 1.75% 4/25/2032 | | | 9,044 | | | | 1,789 | |

| Qatar (State of) 4.00% 3/14/2029 | | USD | 2,330 | | | | 2,315 | |

| Qatar (State of) 3.75% 4/16/20301 | | | 1,000 | | | | 978 | |

| Qatar (State of) 4.40% 4/16/20501 | | | 2,300 | | | | 2,125 | |

| Republika Srpska 4.75% 4/27/2026 | | EUR | 959 | | | | 1,014 | |

| Romania 3.65% 7/28/2025 | | RON | 11,410 | | | | 2,454 | |

| Romania 2.50% 10/25/2027 | | | 900 | | | | 175 | |

| Romania 1.75% 7/13/2030 | | EUR | 3,000 | | | | 2,684 | |

| Romania 2.124% 7/16/2031 | | | 1,000 | | | | 883 | |

| Romania 2.00% 4/14/2033 | | | 830 | | | | 688 | |

| Romania 4.75% 10/11/2034 | | RON | 4,515 | | | | 885 | |

| Romania 7.625% 1/17/20531 | | USD | 200 | | | | 225 | |

| Russian Federation 7.00% 1/25/20234,5 | | RUB | 49,732 | | | | — | 6 |

| Saudi Arabia (Kingdom of) 4.75% 1/18/20281 | | USD | 2,600 | | | | 2,630 | |

| Saudi Arabia (Kingdom of) 4.875% 7/18/20331 | | | 3,178 | | | | 3,250 | |

| Saudi Arabia (Kingdom of) 4.625% 10/4/2047 | | | 2,000 | | | | 1,800 | |

| Saudi Arabia (Kingdom of) 5.00% 1/18/20531 | | | 3,005 | | | | 2,837 | |

| Saudi Arabia (Kingdom of) 3.45% 2/2/2061 | | | 1,300 | | | | 917 | |

| Senegal (Republic of) 4.75% 3/13/2028 | | EUR | 2,960 | | | | 3,026 | |

| Senegal (Republic of) 4.75% 3/13/2028 | | | 1,140 | | | | 1,165 | |

| Senegal (Republic of) 5.375% 6/8/2037 | | | 1,000 | | | | 819 | |

| Senegal (Republic of) 6.75% 3/13/2048 | | USD | 4,425 | | | | 3,492 | |

| Serbia (Republic of) 6.50% 9/26/20331 | | | 5,617 | | | | 5,778 | |

| Serbia (Republic of) 6.50% 9/26/2033 | | | 300 | | | | 309 | |

| Sharjah (Emirate of) 6.50% 11/23/20321 | | | 2,405 | | | | 2,530 | |

| South Africa (Republic of), Series R-186, 10.50% 12/21/2026 | | ZAR | 10,900 | | | | 624 | |

| South Africa (Republic of), Series R-2030, 8.00% 1/31/2030 | | | 253,395 | | | | 12,769 | |

| South Africa (Republic of), Series R-213, 7.00% 2/28/2031 | | | 149,800 | | | | 6,859 | |

| South Africa (Republic of), Series R-2032, 8.25% 3/31/2032 | | | 49,044 | | | | 2,348 | |

| South Africa (Republic of), Series R-2035, 8.875% 2/28/2035 | | | 379,453 | | | | 17,539 | |

| South Africa (Republic of), Series R-2037, 8.50% 1/31/2037 | | | 57,630 | | | | 2,469 | |

| South Africa (Republic of), Series R-2040, 9.00% 1/31/2040 | | | 9,872 | | | | 423 | |

| South Africa (Republic of), Series R-214, 6.50% 2/28/2041 | | | 380,265 | | | | 12,583 | |

| South Africa (Republic of), Series R-2048, 8.75% 2/28/2048 | | | 124,512 | | | | 5,021 | |

| South Korea (Republic of), Series 2709, 3.125% 9/10/2027 | | KRW | 4,650,800 | | | | 3,606 | |

| South Korea (Republic of), Series 3212, 4.25% 12/10/2032 | | | 7,363,100 | | | | 6,180 | |

| South Korea (Republic of), Series 4209, 3.25% 9/10/2042 | | | 940,000 | | | | 743 | |

| Sri Lanka (Democratic Socialist Republic of) 5.75% 4/18/20234 | | USD | 1,282 | | | | 659 | |

| Sri Lanka (Democratic Socialist Republic of) 6.20% 5/11/20271,4 | | | 880 | | | | 447 | |

| Sri Lanka (Democratic Socialist Republic of) 6.75% 4/18/20284 | | | 250 | | | | 126 | |

| Sri Lanka (Democratic Socialist Republic of) 7.55% 3/28/2030 | | | 750 | | | | 379 | |

| Thailand (Kingdom of) 3.85% 12/12/2025 | | THB | 124,390 | | | | 3,719 | |

| Thailand (Kingdom of) 2.25% 3/17/2027 | | | 297,850 | | | | 8,621 | |

| Thailand (Kingdom of) 1.00% 6/17/2027 | | | 126,651 | | | | 3,511 | |

| Thailand (Kingdom of) 2.875% 12/17/2028 | | | 64,850 | | | | 1,922 | |

| Thailand (Kingdom of) 2.00% 12/17/2031 | | | 63,400 | | | | 1,761 | |

| | |

| 8 | American Funds Emerging Markets Bond Fund |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Bonds & notes of governments & government agencies outside the U.S. (continued) | | | | | | | | |

| Thailand (Kingdom of) 1.60% 6/17/2035 | | THB | 6,127 | | | $ | 159 | |

| Thailand (Kingdom of) 3.39% 6/17/2037 | | | 148,774 | | | | 4,581 | |

| Thailand (Kingdom of) 3.30% 6/17/2038 | | | 45,019 | | | | 1,366 | |

| Thailand (Kingdom of) 2.00% 6/17/2042 | | | 54,600 | | | | 1,355 | |

| Thailand (Kingdom of) 2.875% 6/17/2046 | | | 13,000 | | | | 347 | |

| Tunisia (Republic of) 5.625% 2/17/2024 | | EUR | 10,768 | | | | 11,502 | |

| Tunisia (Republic of) 5.75% 1/30/2025 | | USD | 465 | | | | 383 | |

| Tunisia (Republic of) 6.375% 7/15/2026 | | EUR | 1,300 | | | | 1,005 | |

| Tunisia (Republic of) 6.375% 7/15/2026 | | | 550 | | | | 425 | |

| Turkey (Republic of) 6.375% 10/14/2025 | | USD | 1,035 | | | | 1,041 | |

| Turkey (Republic of) 4.25% 4/14/2026 | | | 1,270 | | | | 1,220 | |

| Turkey (Republic of) 4.875% 10/9/2026 | | | 2,000 | | | | 1,934 | |

| Turkey (Republic of) 9.875% 1/15/2028 | | | 1,000 | | | | 1,112 | |

| Turkey (Republic of) 17.30% 7/19/2028 | | TRY | 75,000 | | | | 2,061 | |

| Turkey (Republic of) 17.80% 7/13/2033 | | | 73,372 | | | | 1,954 | |

| Turkey (Republic of) 6.50% 9/20/2033 | | USD | 900 | | | | 863 | |

| Turkey (Republic of) 6.00% 1/14/2041 | | | 400 | | | | 341 | |

| Ukraine 9.99% 5/22/2024 | | UAH | 24,136 | | | | 502 | |

| Ukraine 7.75% 9/1/20244 | | USD | 1,600 | | | | 499 | |

| Ukraine 15.50% 10/2/2024 | | UAH | 15,026 | | | | 323 | |

| Ukraine 12.70% 10/30/2024 | | | 6,612 | | | | 137 | |

| Ukraine 19.50% 1/15/2025 | | | 35,574 | | | | 777 | |

| Ukraine 8.994% 2/1/20264 | | USD | 5,523 | | | | 1,658 | |

| Ukraine 7.75% 9/1/20274 | | | 1,200 | | | | 332 | |

| Ukraine 6.75% 6/20/20284 | | EUR | 2,072 | | | | 565 | |

| Ukraine 6.876% 5/21/20311,4 | | USD | 1,800 | | | | 420 | |

| Ukraine 4.375% 1/27/20324 | | EUR | 700 | | | | 162 | |

| Ukraine 7.253% 3/15/20354 | | USD | 2,012 | | | | 489 | |

| Ukraine 7.253% 3/15/20351,4 | | | 1,700 | | | | 413 | |

| United Mexican States 0% 10/3/2024 | | MXN | 4,200 | | | | 228 | |

| United Mexican States 4.50% 12/4/20253 | | | 69,289 | | | | 3,966 | |

| United Mexican States 8.30% 8/15/2031 | | USD | 1,800 | | | | 2,195 | |

| United Mexican States 4.875% 5/19/2033 | | | 875 | | | | 845 | |

| United Mexican States 4.50% 1/31/2050 | | | 417 | | | | 342 | |

| United Mexican States 6.338% 5/4/2053 | | | 1,792 | | | | 1,829 | |

| United Mexican States 3.771% 5/24/2061 | | | 720 | | | | 490 | |

| United Mexican States 3.75% 4/19/2071 | | | 880 | | | | 590 | |

| United Mexican States, Series M, 7.50% 6/3/2027 | | MXN | 5,355 | | | | 299 | |

| United Mexican States, Series M20, 8.50% 5/31/2029 | | | 127,810 | | | | 7,370 | |

| United Mexican States, Series M, 7.75% 5/29/2031 | | | 166,467 | | | | 9,149 | |

| United Mexican States, Series M, 7.50% 5/26/2033 | | | 56,200 | | | | 3,000 | |

| United Mexican States, Series M, 7.75% 11/23/2034 | | | 5,660 | | | | 305 | |

| United Mexican States, Series M30, 8.50% 11/18/2038 | | | 132,000 | | | | 7,421 | |

| United Mexican States, Series M, 7.75% 11/13/2042 | | | 16,950 | | | | 879 | |

| United Mexican States, Series M, 8.00% 11/7/2047 | | | 16,363 | | | | 862 | |

| United Mexican States, Series M, 8.00% 7/31/2053 | | | 342,940 | | | | 17,938 | |

| Uruguay (Oriental Republic of) 4.375% 12/15/20283 | | UYU | 53 | | | | 1 | |

| Venezuela (Bolivarian Republic of) 7.00% 12/1/20184 | | USD | 155 | | | | 22 | |

| Venezuela (Bolivarian Republic of) 7.75% 10/13/20194 | | | 3,170 | | | | 451 | |

| Venezuela (Bolivarian Republic of) 6.00% 12/9/20204 | | | 2,293 | | | | 321 | |

| Venezuela (Bolivarian Republic of) 9.00% 5/7/20234 | | | 2,257 | | | | 357 | |

| Venezuela (Bolivarian Republic of) 8.25% 10/13/20244 | | | 1,076 | | | | 169 | |

| Venezuela (Bolivarian Republic of) 9.25% 5/7/20284 | | | 562 | | | | 98 | |

| Venezuela (Bolivarian Republic of) 7.00% 3/31/20384 | | | 377 | | | | 58 | |

| | | | | | | | 760,180 | |

| | | | | | | | | |

| Corporate bonds, notes & loans 17.88% | | | | | | | | |

| Energy 4.81% | | | | | | | | |

| Abu Dhabi Crude Oil Pipeline, LLC 4.60% 11/2/2047 | | | 4,950 | | | | 4,558 | |

| AI Candelaria (Spain), SLU 5.75% 6/15/20331 | | | 2,250 | | | | 1,747 | |

| AI Candelaria (Spain), SLU 5.75% 6/15/2033 | | | 250 | | | | 194 | |

| Borr IHC, Ltd. 10.375% 11/15/20301 | | | 2,300 | | | | 2,381 | |

| Cosan Luxembourg SA 7.50% 6/27/20301 | | | 1,200 | | | | 1,254 | |

| Ecopetrol SA 8.625% 1/19/2029 | | | 200 | | | | 213 | |

| Ecopetrol SA 8.875% 1/13/2033 | | | 1,730 | | | | 1,882 | |

| Ecopetrol SA 5.875% 5/28/2045 | | | 457 | | | | 362 | |

| FORESEA Holding SA 7.50% 6/15/2030 | | | 639 | | | | 592 | |

| | |

| American Funds Emerging Markets Bond Fund | 9 |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Corporate bonds, notes & loans (continued) | | | | | | | | |

| Energy (continued) | | | | | | | | |

| Galaxy Pipeline Assets Bidco, Ltd. 2.94% 9/30/2040 | | USD | 980 | | | $ | 809 | |

| Galaxy Pipeline Assets Bidco, Ltd. 3.25% 9/30/2040 | | | 1,050 | | | | 826 | |

| GeoPark, Ltd. 5.50% 1/17/2027 | | | 500 | | | | 443 | |

| Guara Norte SARL 5.198% 6/15/20341 | | | 2,406 | | | | 2,194 | |

| Kosmos Energy, Ltd. 7.125% 4/4/20267 | | | 1,684 | | | | 1,603 | |

| Kosmos Energy, Ltd. 7.50% 3/1/20287 | | | 800 | | | | 729 | |

| Modec Finance BV 7.84% 7/15/20265,7 | | | 200 | | | | 201 | |

| MV24 Capital BV 6.748% 6/1/20341 | | | 1,388 | | | | 1,300 | |

| MV24 Capital BV 6.748% 6/1/2034 | | | 887 | | | | 831 | |

| Oleoducto Central SA 4.00% 7/14/20271 | | | 2,495 | | | | 2,321 | |

| Petroleos Mexicanos 7.19% 9/12/2024 | | MXN | 46,570 | | | | 2,623 | |

| Petroleos Mexicanos 7.19% 9/12/2024 | | | 26,639 | | | | 1,500 | |

| Petroleos Mexicanos 6.875% 10/16/2025 | | USD | 730 | | | | 719 | |

| Petroleos Mexicanos 6.875% 8/4/2026 | | | 2,489 | | | | 2,419 | |

| Petroleos Mexicanos 7.47% 11/12/2026 | | MXN | 71,690 | | | | 3,698 | |

| Petroleos Mexicanos 6.70% 2/16/2032 | | USD | 2,141 | | | | 1,779 | |

| Petroleos Mexicanos 6.625% 6/15/2035 | | | 2,182 | | | | 1,676 | |

| Petroleos Mexicanos 7.69% 1/23/2050 | | | 4,250 | | | | 3,028 | |

| Petroleos Mexicanos 6.95% 1/28/2060 | | | 4,265 | | | | 2,814 | |

| Petrorio Luxembourg SARL 6.125% 6/9/20261 | | | 500 | | | | 491 | |

| PTTEP Treasury Center Co., Ltd. 2.587% 6/10/20271 | | | 278 | | | | 258 | |

| PTTEP Treasury Center Co., Ltd. 2.587% 6/10/2027 | | | 200 | | | | 186 | |

| PTTEP Treasury Center Co., Ltd. 2.993% 1/15/2030 | | | 228 | | | | 206 | |

| Qatar Energy 3.125% 7/12/2041 | | | 3,314 | | | | 2,554 | |

| Qatar Energy 3.125% 7/12/20411 | | | 2,995 | | | | 2,309 | |

| Qatar Energy 3.30% 7/12/20511 | | | 2,710 | | | | 1,985 | |

| Tullow Oil PLC 10.25% 5/15/2026 | | | 200 | | | | 179 | |

| | | | | | | | 52,864 | |

| | | | | | | | | |

| Financials 3.52% | | | | | | | | |

| AIA Group, Ltd. 0.88% 9/9/2033 (5-year EUR Mid-Swap + 1.10% on 9/9/2028)2 | | EUR | 2,000 | | | | 1,886 | |

| Banco de Credito del Peru SA 3.25% 9/30/2031 (5-year UST Yield Curve Rate T Note Constant Maturity + 2.45% on 9/30/2026)1,2 | | USD | 2,955 | | | | 2,705 | |

| Banco do Brasil SA 4.625% 1/15/2025 | | | 400 | | | | 395 | |

| Banco do Brasil SA 3.25% 9/30/2026 | | | 850 | | | | 808 | |

| Bangkok Bank Public Co., Ltd. 4.45% 9/19/20281 | | | 900 | | | | 883 | |

| Bangkok Bank Public Co., Ltd. 3.733% 9/25/2034 (5-year UST Yield Curve Rate T Note Constant Maturity + 1.90% on 9/25/2029)2 | | | 2,956 | | | | 2,630 | |

| Bank of East Asia, Ltd. 4.875% 4/22/2032 (5-year UST Yield Curve Rate T Note Constant Maturity + 2.30% on 4/22/2027)2 | | | 1,250 | | | | 1,132 | |

| Bank of East Asia, Ltd. 5.825% junior subordinated perpetual bonds (5-year UST Yield Curve Rate T Note Constant Maturity + 5.527% on 10/21/2025)2 | | | 500 | | | | 437 | |

| BBVA Bancomer SA 5.875% 9/13/2034 (5-year UST Yield Curve Rate T Note Constant Maturity + 4.308% on 9/13/2029)2 | | | 2,200 | | | | 2,079 | |

| BBVA Bancomer SA 8.45% 6/29/2038 (5-year UST Yield Curve Rate T Note Constant Maturity + 4.661% on 6/29/2033)1,2 | | | 1,000 | | | | 1,067 | |

| China Ping An Insurance Overseas (Holdings), Ltd. 2.85% 8/12/2031 | | | 272 | | | | 221 | |

| HDFC Bank, Ltd. 8.10% 3/22/2025 | | INR | 60,000 | | | | 718 | |

| HSBC Holdings PLC 7.39% 11/03/2028 (USD-SOFR + 7.39% on 11/3/2027)2 | | USD | 1,000 | | | | 1,072 | |

| HSBC Holdings PLC 2.206% 8/17/2029 (USD-SOFR + 1.285% on 8/17/2028)2 | | | 1,000 | | | | 874 | |

| HSBC Holdings PLC 8.113% 11/3/2033 (USD-SOFR + 4.25% on 11/3/2032)2 | | | 1,900 | | | | 2,197 | |

| HSBC Holdings PLC 7.399% 11/13/2034 (USD-SOFR + 3.02% on 11/13/2033)2 | | | 500 | | | | 549 | |

| Huarong Finance 2017 Co., Ltd. 4.75% 4/27/2027 | | | 300 | | | | 282 | |

| Itau Unibanco Holding SA 4.50% 11/21/2029 (5-year UST Yield Curve Rate T Note Constant Maturity + 2.822% on 11/21/2024)2 | | | 800 | | | | 786 | |

| Kasikornbank PCL (Hong Kong Branch) 3.343% 10/2/2031 (5-year UST Yield Curve Rate T Note Constant Maturity + 1.70% on 10/2/2026)2 | | | 5,400 | | | | 4,970 | |

| Korea Exchange Bank 3.25% 3/30/20271 | | | 870 | | | | 832 | |

| NongHyup Bank 4.875% 7/3/20281 | | | 3,560 | | | | 3,583 | |

| Power Finance Corp., Ltd. 3.90% 9/16/2029 | | | 500 | | | | 467 | |

| PT Bank Negara Indonesia (Persero) Tbk 4.30% junior subordinated perpetual bonds (5-year UST Yield Curve Rate T Note Constant Maturity + 3.466% on 3/24/2027)2 | | | 3,400 | | | | 3,021 | |

| Shinhan Financial Group Co., Ltd. 5.00% 7/24/20281 | | | 1,600 | | | | 1,600 | |

| Standard Chartered PLC 6.296% 7/6/2034 (1-year UST Yield Curve Rate T Note Constant Maturity + 2.58% on 7/6/2033)1,2 | | | 471 | | | | 495 | |

| Vigorous Champion International, Ltd. 4.25% 5/28/2029 | | | 950 | | | | 875 | |

| Xiaomi Best Time International, Ltd. 2.875% 7/14/2031 | | | 1,000 | | | | 833 | |

| | |

| 10 | American Funds Emerging Markets Bond Fund |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Corporate bonds, notes & loans (continued) | | | | | | | | |

| Financials (continued) | | | | | | | | |

| Xiaomi Best Time International, Ltd. 2.875% 7/14/20311 | | USD | 415 | | | $ | 345 | |

| Xiaomi Best Time International, Ltd. 4.10% 7/14/20511 | | | 1,120 | | | | 797 | |

| Xiaomi Best Time International, Ltd. 4.10% 7/14/2051 | | | 200 | | | | 142 | |

| | | | | | | | 38,681 | |

| | | | | | | | | |

| Materials 2.64% | | | | | | | | |

| Alpek, SAB de CV 3.25% 2/25/20311 | | | 1,285 | | | | 1,102 | |

| Aris Mining Corp. 6.875% 8/9/20261 | | | 1,760 | | | | 1,530 | |

| Braskem Idesa SAPI 7.45% 11/15/20291 | | | 381 | | | | 240 | |

| Braskem Idesa SAPI 7.45% 11/15/2029 | | | 200 | | | | 126 | |

| Braskem Idesa SAPI 6.99% 2/20/20321 | | | 4,230 | | | | 2,480 | |

| Braskem Idesa SAPI 6.99% 2/20/2032 | | | 1,770 | | | | 1,038 | |

| Braskem Netherlands Finance BV 4.50% 1/10/2028 | | | 1,564 | | | | 1,281 | |

| Braskem Netherlands Finance BV 4.50% 1/31/2030 | | | 236 | | | | 184 | |

| Braskem Netherlands Finance BV 8.50% 1/12/20311 | | | 1,005 | | | | 936 | |

| Braskem Netherlands Finance BV 8.50% 1/12/2031 | | | 300 | | | | 279 | |

| Braskem Netherlands Finance BV 7.25% 2/13/20331 | | | 1,250 | | | | 1,054 | |

| Braskem Netherlands Finance BV 7.25% 2/13/2033 | | | 410 | | | | 346 | |

| CAP SA 3.90% 4/27/2031 | | | 200 | | | | 156 | |

| CEMEX, SAB de CV 9.125% senior subordinated perpetual bonds (5-year UST Yield Curve Rate T Note Constant Maturity + 4.907% on 6/14/2028)1,2 | | | 600 | | | | 640 | |

| CSN Inova Ventures 6.75% 1/28/2028 | | | 300 | | | | 293 | |

| CSN Resources SA 8.875% 12/5/20301 | | | 1,100 | | | | 1,147 | |

| CSN Resources SA 5.875% 4/8/20321 | | | 1,610 | | | | 1,402 | |

| Endeavour Mining PLC 5.00% 10/14/2026 | | | 200 | | | | 185 | |

| First Quantum Minerals, Ltd. 8.625% 6/1/20311 | | | 3,750 | | | | 3,183 | |

| Fresnillo PLC 4.25% 10/2/20501 | | | 2,160 | | | | 1,653 | |

| GC Treasury Center Co., Ltd. 2.98% 3/18/20311 | | | 375 | | | | 317 | |

| GC Treasury Center Co., Ltd. 4.40% 3/30/20321 | | | 300 | | | | 274 | |

| Gold Fields Orogen Holding (BVI), Ltd. 6.125% 5/15/2029 | | | 200 | | | | 206 | |

| POSCO 5.75% 1/17/20281 | | | 200 | | | | 205 | |

| Sasol Financing USA, LLC 5.875% 3/27/2024 | | | 400 | | | | 398 | |

| Sasol Financing USA, LLC 4.375% 9/18/2026 | | | 2,410 | | | | 2,247 | |

| Sasol Financing USA, LLC 8.75% 5/3/20291 | | | 2,500 | | | | 2,553 | |

| Sasol Financing USA, LLC 8.75% 5/3/20297 | | | 1,585 | | | | 1,619 | |

| Sasol Financing USA, LLC 5.50% 3/18/2031 | | | 2,250 | | | | 1,898 | |

| | | | | | | | 28,972 | |

| | | | | | | | | |

| Utilities 2.58% | | | | | | | | |

| Aegea Finance SARL 9.00% 1/20/20311 | | | 645 | | | | 686 | |

| AES Panama Generation Holdings SRL 4.375% 5/31/20301 | | | 3,236 | | | | 2,723 | |

| AES Panama Generation Holdings SRL 4.375% 5/31/2030 | | | 196 | | | | 165 | |

| Alfa Desarrollo SpA 4.55% 9/27/20511 | | | 1,113 | | | | 870 | |

| Azure Power Energy, Ltd. 3.575% 8/19/20261 | | | 173 | | | | 153 | |

| Chile Electricity Lux MPC SARL 6.01% 1/20/20331 | | | 2,605 | | | | 2,674 | |

| Empresas Publicas de Medellin ESP 8.375% 11/8/2027 | | COP | 10,000,000 | | | | 2,243 | |

| Empresas Publicas de Medellin ESP 8.375% 11/8/2027 | | | 3,744,000 | | | | 840 | |

| Empresas Publicas de Medellin ESP 4.25% 7/18/20291 | | USD | 1,602 | | | | 1,367 | |

| Empresas Publicas de Medellin ESP 4.375% 2/15/20311 | | | 960 | | | | 786 | |

| Enel Américas SA 4.00% 10/25/2026 | | | 215 | | | | 209 | |

| Enel Chile SA 4.875% 6/12/2028 | | | 1,701 | | | | 1,682 | |

| Enfragen Energia Sur SA 5.375% 12/30/2030 | | | 3,609 | | | | 2,823 | |

| ENN Clean Energy International Investment, Ltd. 3.375% 5/12/20261 | | | 510 | | | | 479 | |

| Eskom Holdings SOC, Ltd. 8.45% 8/10/2028 | | | 740 | | | | 752 | |

| Instituto Costarricense de Electricidad 6.75% 10/7/2031 | | | 570 | | | | 576 | |

| Investment Energy Resources, Ltd. 6.25% 4/26/20291 | | | 1,375 | | | | 1,300 | |

| Korea Electric Power Corp. 5.375% 7/31/20261 | | | 2,010 | | | | 2,033 | |

| Korea Electric Power Corp. 4.00% 6/14/2027 | | | 300 | | | | 294 | |

| Korea Electric Power Corp. 4.00% 6/14/20271 | | | 200 | | | | 196 | |

| Light Servicos de Eletricidade SA 4.375% 6/18/20261,4 | | | 1,500 | | | | 700 | |

| Light Servicos de Eletricidade SA 4.375% 6/18/20264 | | | 700 | | | | 327 | |

| Minejesa Capital BV 4.625% 8/10/2030 | | | 1,100 | | | | 1,046 | |

| MVM Energetika Zartkoruen Mukodo Reszvenytarsasag 7.50% 6/9/2028 | | | 2,895 | | | | 3,029 | |

| ReNew Power Pvt., Ltd. 5.875% 3/5/20271 | | | 200 | | | | 191 | |

| ReNew Power Pvt., Ltd. 5.875% 3/5/2027 | | | 200 | | | | 191 | |

| | | | | | | | 28,335 | |

| | |

| American Funds Emerging Markets Bond Fund | 11 |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Corporate bonds, notes & loans (continued) | | | | | | | | |

| Consumer staples 1.14% | | | | | | | | |

| Indofood CBP Sukses Makmur Tbk PT 3.398% 6/9/2031 | | USD | 559 | | | $ | 484 | |

| Indofood CBP Sukses Makmur Tbk PT 3.541% 4/27/2032 | | | 400 | | | | 347 | |

| Indofood CBP Sukses Makmur Tbk PT 4.745% 6/9/2051 | | | 765 | | | | 622 | |

| InRetail Consumer 3.25% 3/22/20281 | | | 2,730 | | | | 2,452 | |

| MARB BondCo PLC 3.95% 1/29/20311 | | | 1,500 | | | | 1,220 | |

| MARB BondCo PLC 3.95% 1/29/2031 | | | 700 | | | | 569 | |

| Minerva Luxembourg SA 4.375% 3/18/20311 | | | 400 | | | | 330 | |

| Minerva Luxembourg SA 8.875% 9/13/20331 | | | 5,168 | | | | 5,473 | |

| Natura Cosmeticos SA 4.125% 5/3/20281 | | | 820 | | | | 742 | |

| NBM US Holdings, Inc. 7.00% 5/14/20267 | | | 250 | | | | 253 | |

| | | | | | | | 12,492 | |

| | | | | | | | | |

| Industrials 0.83% | | | | | | | | |

| Bidvest Group (UK) PLC 3.625% 9/23/2026 | | | 200 | | | | 186 | |

| BOC Aviation, Ltd. 3.00% 9/11/2029 | | | 600 | | | | 540 | |

| BOC Aviation, Ltd. 2.625% 9/17/2030 | | | 200 | | | | 173 | |

| Embraer Netherlands Finance BV 7.00% 7/28/20301 | | | 400 | | | | 420 | |

| Hidrovias International Finance SARL 4.95% 2/8/20311 | | | 2,610 | | | | 2,066 | |

| Lima Metro Line 2 Finance, Ltd. 5.875% 7/5/20341 | | | 489 | | | | 484 | |

| Lima Metro Line 2 Finance, Ltd. 4.35% 4/5/20361 | | | 875 | | | | 803 | |

| Mexico City Airport Trust 4.25% 10/31/2026 | | | 900 | | | | 869 | |

| Mexico City Airport Trust 5.50% 7/31/2047 | | | 1,000 | | | | 864 | |

| MISC Capital Two (Labuan), Ltd. 3.75% 4/6/20271 | | | 1,260 | | | | 1,214 | |

| OCP SA 3.75% 6/23/2031 | | | 200 | | | | 173 | |

| Simpar Europe SA 5.20% 1/26/2031 | | | 200 | | | | 174 | |

| Summit Digitel Infrastructure Pvt, Ltd. 2.875% 8/12/2031 | | | 1,100 | | | | 903 | |

| Summit Digitel Infrastructure Pvt, Ltd. 2.875% 8/12/20311 | | | 300 | | | | 246 | |

| | | | | | | | 9,115 | |

| | | | | | | | | |

| Consumer discretionary 0.77% | | | | | | | | |

| Alibaba Group Holding, Ltd. 4.50% 11/28/2034 | | | 300 | | | | 282 | |

| Arcos Dorados BV 6.125% 5/27/20291 | | | 890 | | | | 889 | |

| Meituan 3.05% 10/28/20301 | | | 250 | | | | 211 | |

| Melco Resorts Finance, Ltd. 4.875% 6/6/20251 | | | 850 | | | | 825 | |

| Melco Resorts Finance, Ltd. 4.875% 6/6/2025 | | | 400 | | | | 389 | |

| Melco Resorts Finance, Ltd. 5.375% 12/4/20291 | | | 1,250 | | | | 1,106 | |

| MercadoLibre, Inc. 3.125% 1/14/2031 | | | 1,142 | | | | 979 | |

| MGM China Holdings, Ltd. 5.375% 5/15/2024 | | | 300 | | | | 299 | |

| Prosus NV 3.68% 1/21/2030 | | | 1,120 | | | | 981 | |

| Sands China, Ltd. 2.55% 3/8/2027 | | | 300 | | | | 273 | |

| Sands China, Ltd. 3.50% 8/8/2031 | | | 532 | | | | 446 | |

| Studio City Finance, Ltd. 6.50% 1/15/2028 | | | 400 | | | | 372 | |

| Studio City Finance, Ltd. 5.00% 1/15/2029 | | | 820 | | | | 690 | |

| Studio City Finance, Ltd. 5.00% 1/15/20291 | | | 800 | | | | 673 | |

| | | | | | | | 8,415 | |

| | | | | | | | | |

| Communication services 0.74% | | | | | | | | |

| América Móvil, SAB de CV, 9.50% 1/27/2031 | | MXN | 80,060 | | | | 4,588 | |

| Axiata SPV5 (Labuan), Ltd. 3.064% 8/19/2050 | | USD | 1,053 | | | | 729 | |

| PLDT, Inc. 2.50% 1/23/2031 | | | 200 | | | | 167 | |

| Tencent Holdings, Ltd. 2.39% 6/3/2030 | | | 500 | | | | 426 | |

| Tencent Holdings, Ltd. 3.68% 4/22/2041 | | | 400 | | | | 315 | |

| Tencent Holdings, Ltd. 3.24% 6/3/20501 | | | 900 | | | | 601 | |

| Tencent Holdings, Ltd. 3.24% 6/3/2050 | | | 400 | | | | 267 | |

| Tencent Holdings, Ltd. 3.84% 4/22/2051 | | | 1,400 | | | | 1,047 | |

| | | | | | | | 8,140 | |

| | | | | | | | | |

| Municipals 0.35% | | | | | | | | |

| Aeropuerto Internacional de Tocumen, SA 4.00% 8/11/20411 | | | 700 | | | | 527 | |

| Aeropuerto Internacional de Tocumen, SA 5.125% 8/11/20611 | | | 1,140 | | | | 870 | |

| Rutas 2 & 7 Finance, Ltd. 0% 9/30/20361 | | | 2,444 | | | | 1,627 | |

| Rutas 2 & 7 Finance, Ltd. 0% 9/30/2036 | | | 1,300 | | | | 865 | |

| | | | | | | | 3,889 | |

| | |

| 12 | American Funds Emerging Markets Bond Fund |

| Bonds, notes & other debt instruments (continued) | | Principal amount

(000) | | | Value

(000) | |

| Corporate bonds, notes & loans (continued) | | | | | | | | |

| Health care 0.22% | | | | | | | | |

| Rede D’Or Finance SARL 4.95% 1/17/2028 | | USD | 205 | | | $ | 195 | |

| Rede D’Or Finance SARL 4.50% 1/22/2030 | | | 2,500 | | | | 2,267 | |

| | | | | | | | 2,462 | |

| | | | | | | | | |

| Real estate 0.15% | | | | | | | | |

| Corp. Inmobiliaria Vesta, SAB de CV 3.625% 5/13/20311 | | | 725 | | | | 623 | |

| FibraSOMA 4.375% 7/22/20311 | | | 1,430 | | | | 1,085 | |

| | | | | | | | 1,708 | |

| | | | | | | | | |

| Information technology 0.13% | | | | | | | | |

| SK hynix, Inc. 6.375% 1/17/20281 | | | 200 | | | | 207 | |

| SK hynix, Inc. 2.375% 1/19/20311 | | | 400 | | | | 325 | |

| SK hynix, Inc. 6.50% 1/17/2033 | | | 650 | | | | 687 | |

| TSMC Global, Ltd. 2.25% 4/23/20311 | | | 200 | | | | 170 | |

| | | | | | | | 1,389 | |

| | | | | | | | | |

| Total corporate bonds, notes & loans | | | | | | | 196,462 | |

| | | | | | | | | |

| U.S. Treasury bonds & notes 4.37% | | | | | | | | |

| U.S. Treasury 4.37% | | | | | | | | |

| U.S. Treasury 4.50% 11/15/20258 | | | 19,200 | | | | 19,271 | |

| U.S. Treasury 3.625% 5/31/2028 | | | 3,358 | | | | 3,324 | |

| U.S. Treasury 4.125% 7/31/2028 | | | 10,000 | | | | 10,104 | |

| U.S. Treasury 4.625% 9/30/2028 | | | 13,100 | | | | 13,526 | |

| U.S. Treasury 3.375% 5/15/20338 | | | 1,920 | | | | 1,844 | |

| | | | | | | | | |

| Total U.S. Treasury bonds & notes | | | | | | | 48,069 | |

| | | | | | | | | |

| Federal agency bonds & notes 0.25% | | | | | | | | |

| Korea Development Bank 4.25% 9/8/2032 | | | 2,070 | | | | 2,016 | |

| Korea National Oil Corp. 4.875% 4/3/20281 | | | 400 | | | | 402 | |

| Korea National Oil Corp. 2.625% 4/18/2032 | | | 200 | | | | 169 | |

| Sinopec Group Overseas Development (2018), Ltd. 2.30% 1/8/20311 | | | 250 | | | | 219 | |

| | | | | | | | 2,806 | |

| | | | | | | | | |

| Total bonds, notes & other debt instruments (cost: $1,007,793,000) | | | | | | | 1,007,517 | |

| | | | | | | | | |

| Convertible bonds & notes 0.64% | | | | | | | | |

| Energy 0.64% | | | | | | | | |

| Abu Dhabi National Oil Co., convertible notes, 0.70% 6/4/2024 | | | 7,200 | | | | 7,037 | |

| | | | | | | | | |

| Total convertible bonds & notes (cost: $7,029,000) | | | | | | | 7,037 | |

| | | | | | | | | |

| | | | Shares | | | | | |

| Common stocks 0.14% | | | | | | | | |

| Energy 0.14% | | | | | | | | |

| FORESEA Holding SA, Class C, nonvoting shares9 | | | 55,880 | | | | 1,369 | |

| FORESEA Holding SA, Class B9 | | | 6,208 | | | | 152 | |

| | | | | | | | | |

| Total common stocks (cost: $1,540,000) | | | | | | | 1,521 | |

| | | | | | | | | |

| Short-term securities 5.69% | | | | | | | | |

| Money market investments 5.63% | | | | | | | | |

| Capital Group Central Cash Fund 5.44%10,11 | | | 618,713 | | | | 61,865 | |

| | |

| American Funds Emerging Markets Bond Fund | 13 |

| Short-term securities (continued) | | Weighted

average yield

at acquisition | | Principal amount

(000) | | Value

(000) | |

| Bills & notes of governments & government agencies outside the U.S. 0.06% | | | |

| Sri Lanka (Democratic Socialist Republic of) 5/10/2024 | | 17.983% | | LKR | 218,000 | | $ | 642 | |

| | | | | | | | | | |

| Total short-term securities (cost: $62,527,000) | | | | | | | | 62,507 | |

| Total investment securities 98.14% (cost: $1,078,889,000) | | | | | 1,078,582 | |

| Other assets less liabilities 1.86% | | | | | | | | 20,440 | |

| | | | | | | | | | |

| Net assets 100.00% | | | | | | | $ | 1,099,022 | |

Futures contracts

| Contracts | | Type | | Number of

contracts | | Expiration

date | | Notional

amount

(000) | | | Value and

unrealized

appreciation

(depreciation)

at 12/31/2023

(000) | |

| 2 Year U.S. Treasury Note Futures | | Long | | 632 | | 4/3/2024 | | | USD | 130,138 | | | | $ | 1,284 | |

| 5 Year Euro-Bobl Futures | | Short | | 13 | | 3/11/2024 | | | (1,712 | ) | | | | (23 | ) |

| 5 Year U.S. Treasury Note Futures | | Long | | 33 | | 4/3/2024 | | | 3,590 | | | | | 82 | |

| 10 Year Euro-Bund Futures | | Short | | 14 | | 3/11/2024 | | | (2,121 | ) | | | | (62 | ) |

| 10 Year U.S. Treasury Note Futures | | Long | | 4 | | 3/28/2024 | | | 452 | | | | | 1 | |

| 10 Year Ultra U.S. Treasury Note Futures | | Short | | 97 | | 3/28/2024 | | | (11,448 | ) | | | | (513 | ) |

| 20 Year U.S. Treasury Bond Futures | | Long | | 8 | | 3/28/2024 | | | 999 | | | | | 76 | |

| 30 Year Ultra U.S. Treasury Bond Futures | | Long | | 37 | | 3/28/2024 | | | 4,943 | | | | | 458 | |

| | | | | | | | | | | | | | $ | 1,303 | |

Forward currency contracts

| Contract amount | | | | | | Unrealized

appreciation

(depreciation) | |

Currency purchased

(000) | | Currency sold

(000) | | Counterparty | | Settlement

date | | at 12/31/2023

(000) | |

| EUR | | 840 | | USD | | 912 | | Morgan Stanley | | 1/8/2024 | | | $ | 16 | |

| CZK | | 72,840 | | USD | | 3,245 | | JPMorgan Chase | | 1/8/2024 | | | | 11 | |

| PLN | | 1,150 | | USD | | 287 | | UBS AG | | 1/8/2024 | | | | 5 | |

| USD | | 386 | | CZK | | 8,637 | | Bank of New York Mellon | | 1/8/2024 | | | | — | 6 |

| USD | | 143 | | ZAR | | 2,700 | | UBS AG | | 1/8/2024 | | | | (4 | ) |

| USD | | 22,678 | | EUR | | 20,898 | | Morgan Stanley | | 1/8/2024 | | | | (402 | ) |

| ZAR | | 10,923 | | USD | | 577 | | UBS AG | | 1/9/2024 | | | | 19 | |

| HUF | | 265,180 | | USD | | 751 | | UBS AG | | 1/9/2024 | | | | 13 | |

| PLN | | 757 | | USD | | 188 | | JPMorgan Chase | | 1/9/2024 | | | | 4 | |

| USD | | 1,642 | | CNH | | 11,755 | | BNP Paribas | | 1/9/2024 | | | | (9 | ) |

| USD | | 1,501 | | EUR | | 1,390 | | Citibank | | 1/9/2024 | | | | (34 | ) |

| USD | | 2,578 | | ZAR | | 48,789 | | UBS AG | | 1/9/2024 | | | | (86 | ) |

| THB | | 13,253 | | USD | | 376 | | Citibank | | 1/11/2024 | | | | 10 | |

| THB | | 13,557 | | USD | | 392 | | Citibank | | 1/11/2024 | | | | 3 | |

| USD | | 387 | | CZK | | 8,735 | | Goldman Sachs | | 1/11/2024 | | | | (4 | ) |

| USD | | 24,720 | | EUR | | 22,890 | | Morgan Stanley | | 1/11/2024 | | | | (563 | ) |

| USD | | 17,246 | | KRW | | 22,167,205 | | Citibank | | 1/12/2024 | | | | 135 | |

| KRW | | 9,000,000 | | USD | | 6,939 | | Standard Chartered Bank | | 1/12/2024 | | | | 8 | |

| BRL | | 1,909 | | USD | | 386 | | JPMorgan Chase | | 1/12/2024 | | | | 6 | |

| BRL | | 1,919 | | USD | | 391 | | JPMorgan Chase | | 1/12/2024 | | | | 4 | |

| INR | | 194,000 | | USD | | 2,326 | | Citibank | | 1/12/2024 | | | | 3 | |

| PEN | | 113 | | USD | | 30 | | JPMorgan Chase | | 1/12/2024 | | | | — | 6 |

| BRL | | 1,595 | | USD | | 328 | | JPMorgan Chase | | 1/12/2024 | | | | — | 6 |

| USD | | 162 | | BRL | | 796 | | Citibank | | 1/12/2024 | | | | (2 | ) |

| USD | | 1,079 | | IDR | | 16,660,952 | | Citibank | | 1/12/2024 | | | | (3 | ) |

| USD | | 386 | | BRL | | 1,895 | | Standard Chartered Bank | | 1/12/2024 | | | | (4 | ) |

| USD | | 555 | | BRL | | 2,728 | | Citibank | | 1/12/2024 | | | | (6 | ) |

| USD | | 541 | | PLN | | 2,181 | | Goldman Sachs | | 1/12/2024 | | | | (14 | ) |

| USD | | 604 | | ZAR | | 11,403 | | Citibank | | 1/12/2024 | | | | (19 | ) |

| 14 | American Funds Emerging Markets Bond Fund |

Forward currency contracts (continued)

| Contract amount | | | | | | Unrealized

appreciation | |

Currency

purchased

(000) | | Currency sold

(000) | | Counterparty | | Settlement

date | | (depreciation)

at 12/31/2023

(000) | |

| CLP | | 1,540,825 | | USD | | 1,768 | | Morgan Stanley | | 1/12/2024 | | | $ | (20 | ) |

| USD | | 2,766 | | PEN | | 10,335 | | JPMorgan Chase | | 1/12/2024 | | | | (26 | ) |

| USD | | 2,020 | | EUR | | 1,877 | | Goldman Sachs | | 1/12/2024 | | | | (53 | ) |

| PLN | | 2,320 | | USD | | 586 | | Bank of New York Mellon | | 1/16/2024 | | | | 4 | |

| HUF | | 150,473 | | USD | | 431 | | Goldman Sachs | | 1/16/2024 | | | | 1 | |

| HUF | | 1,603,400 | | USD | | 4,514 | | JPMorgan Chase | | 1/18/2024 | | | | 94 | |

| HUF | | 1,097,000 | | USD | | 3,075 | | BNP Paribas | | 1/18/2024 | | | | 78 | |

| PLN | | 6,225 | | USD | | 1,547 | | Goldman Sachs | | 1/18/2024 | | | | 35 | |

| PLN | | 5,759 | | USD | | 1,428 | | JPMorgan Chase | | 1/18/2024 | | | | 35 | |

| CZK | | 46,500 | | USD | | 2,056 | | Barclays Bank PLC | | 1/18/2024 | | | | 22 | |

| HUF | | 255,050 | | EUR | | 664 | | Goldman Sachs | | 1/18/2024 | | | | — | 6 |

| USD | | 103 | | CZK | | 2,330 | | Standard Chartered Bank | | 1/18/2024 | | | | (1 | ) |

| USD | | 734 | | CZK | | 16,601 | | Barclays Bank PLC | | 1/18/2024 | | | | (8 | ) |

| USD | | 386 | | PLN | | 1,557 | | Goldman Sachs | | 1/18/2024 | | | | (10 | ) |

| CZK | | 57,008 | | USD | | 2,571 | | UBS AG | | 1/18/2024 | | | | (24 | ) |

| THB | | 146,300 | | USD | | 4,100 | | Citibank | | 1/19/2024 | | | | 160 | |

| THB | | 115,000 | | USD | | 3,223 | | Citibank | | 1/19/2024 | | | | 127 | |

| THB | | 111,000 | | USD | | 3,111 | | Citibank | | 1/19/2024 | | | | 123 | |

| THB | | 25,120 | | USD | | 704 | | Citibank | | 1/19/2024 | | | | 28 | |

| MYR | | 6,340 | | USD | | 1,361 | | HSBC Bank | | 1/19/2024 | | | | 24 | |

| CNH | | 6,520 | | USD | | 908 | | HSBC Bank | | 1/19/2024 | | | | 8 | |

| THB | | 13,520 | | USD | | 389 | | Citibank | | 1/19/2024 | | | | 5 | |

| TRY | | 61,000 | | USD | | 2,041 | | Goldman Sachs | | 1/19/2024 | | | | (11 | ) |

| USD | | 9,612 | | MYR | | 44,774 | | HSBC Bank | | 1/19/2024 | | | | (166 | ) |

| PLN | | 35,486 | | USD | | 8,968 | | Citibank | | 1/22/2024 | | | | 47 | |

| PLN | | 4,070 | | USD | | 1,029 | | HSBC Bank | | 1/22/2024 | | | | 5 | |

| CLP | | 330,680 | | USD | | 378 | | JPMorgan Chase | | 1/22/2024 | | | | (3 | ) |

| USD | | 494 | | EUR | | 450 | | Standard Chartered Bank | | 1/22/2024 | | | | (3 | ) |

| USD | | 502 | | ZAR | | 9,355 | | Goldman Sachs | | 1/22/2024 | | | | (9 | ) |

| THB | | 52,060 | | USD | | 1,490 | | UBS AG | | 1/23/2024 | | | | 27 | |

| HUF | | 112,153 | | USD | | 318 | | BNP Paribas | | 1/23/2024 | | | | 4 | |

| USD | | 1,853 | | CNH | | 13,200 | | Morgan Stanley | | 1/23/2024 | | | | (3 | ) |

| BRL | | 5,000 | | USD | | 1,019 | | Morgan Stanley | | 2/9/2024 | | | | 7 | |

| USD | | 900 | | BRL | | 5,000 | | BNP Paribas | | 2/9/2024 | | | | (125 | ) |

| USD | | 1,134 | | ILS | | 4,303 | | JPMorgan Chase | | 2/16/2024 | | | | (56 | ) |

| USD | | 3,565 | | BRL | | 17,500 | | Morgan Stanley | | 2/20/2024 | | | | (20 | ) |

| TRY | | 58,000 | | USD | | 1,853 | | Barclays Bank PLC | | 3/5/2024 | | | | (5 | ) |

| TRY | | 50,000 | | USD | | 1,605 | | BNP Paribas | | 3/5/2024 | | | | (12 | ) |

| TRY | | 84,000 | | USD | | 2,677 | | Barclays Bank PLC | | 3/7/2024 | | | | (6 | ) |

| USD | | 1,560 | | ILS | | 6,260 | | Morgan Stanley | | 4/24/2024 | | | | (176 | ) |

| CZK | | 50,190 | | USD | | 2,220 | | Barclays Bank PLC | | 6/10/2024 | | | | 18 | |

| TRY | | 6,652 | | USD | | 196 | | BNP Paribas | | 6/10/2024 | | | | (3 | ) |

| TRY | | 13,483 | | USD | | 398 | | Morgan Stanley | | 6/10/2024 | | | | (7 | ) |

| BRL | | 10,000 | | USD | | 1,874 | | Morgan Stanley | | 10/2/2024 | | | | 124 | |

| USD | | 3,791 | | BRL | | 20,000 | | JPMorgan Chase | | 10/2/2024 | | | | (204 | ) |

| USD | | 432 | | ILS | | 1,675 | | BNP Paribas | | 10/18/2024 | | | | (36 | ) |

| | | | | | | | | | | | | | $ | (924 | ) |

| American Funds Emerging Markets Bond Fund | 15 |

Swap contracts

Interest rate swaps

Centrally cleared interest rate swaps