UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☐

Filed by a Party other than the Registrant ☒

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☒ | Definitive Additional Materials |

| ☐ | Soliciting Material Under § 240.14a-12 |

| MARTIN MIDSTREAM PARTNERS L.P. |

(Name of Registrant as Specified In Its Charter) |

| |

NUT TREE CAPITAL MANAGEMENT L.P. NUT TREE CAPITAL MANAGEMENT GP, LLC JARED R. NUSSBAUM CASPIAN CAPITAL L.P. CASPIAN CAPITAL GP LLC ADAM COHEN DAVID CORLETO |

(Name of Persons(s) Filing Proxy Statement, if other than the Registrant) |

Payment of Filing Fee (Check all boxes that apply):

| ☐ | Fee paid previously with preliminary materials |

| ☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11 |

Nut Tree Capital Management L.P., a Delaware limited partnership (“Nut Tree”), and Caspian Capital L.P., a Delaware limited partnership (“Caspian”), together with the other participants named herein, have filed a definitive proxy statement and accompanying GOLD proxy card with the Securities and Exchange Commission (“SEC”) to be used to solicit votes in connection with their opposition to proposals to be presented at a special meeting of common unitholders (the “Special Meeting”) of Martin Midstream Partners L.P., a Delaware limited partnership (the “Company”), in connection with the Company’s agreement and plan of merger with Martin Resource Management Corporation and certain of its affiliates.

Item 1: On December 2, 2024, Nut Tree and Caspian issued the following press release:

Nut Tree Capital Management and Caspian Capital File Definitive Proxy Materials Opposing Merger Between Martin Midstream Partners and Martin Resource Management Corporation

Nut Tree and Caspian File Definitive Proxy Statement and Send Letter to Unitholders Urging them to Vote “AGAINST” the Merger at MMLP’s Special Meeting to be Held on December 30, 2024

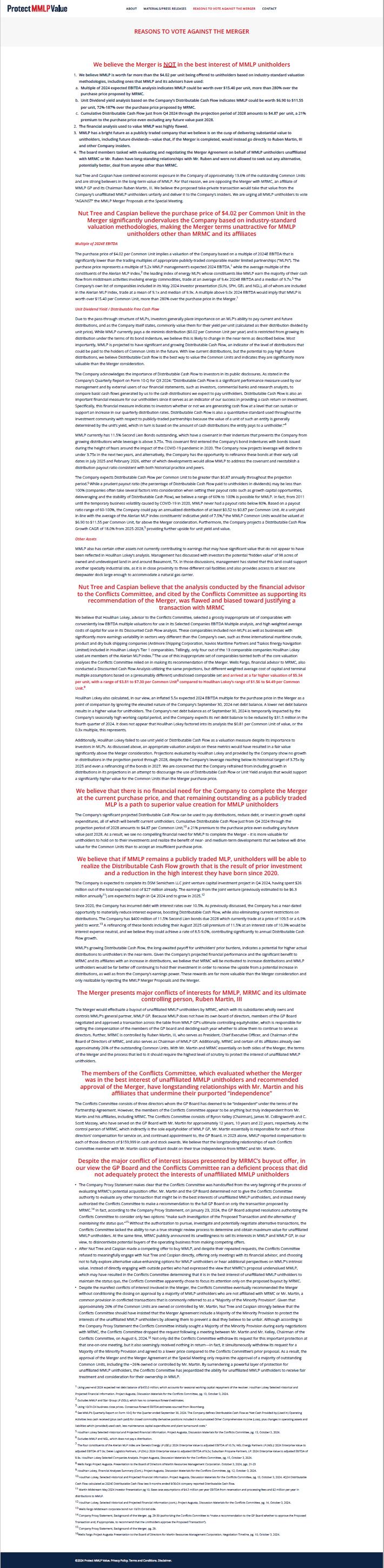

Nut Tree and Caspian Believe MMLP is Worth Far More than the Per Unit Price in the Merger

Merger is Insider Led Deal Presenting Massive Conflicts of Interest and MMLP Approval Was Based on Flawed and Biased Financial Analysis in Nut Tree and Caspian’s View

Nut Tree and Caspian Highlight MMLP’s Bright Future Prospects as a Publicly Traded Company, and Path to Superior Value Creation for Unitholders

New York – December 2, 2024 – Nut Tree Capital Management L.P. (“Nut Tree”) and Caspian Capital L.P. (“Caspian”), which together with their affiliates have combined exposure in Martin Midstream Partners L.P. (NASDAQ: MMLP) (“MMLP” or the “Company”) of approximately 13.6% of the outstanding common units, have filed definitive proxy materials with the Securities and Exchange Commission (“SEC”) opposing the sale of MMLP to Martin Midstream Resource Corporation (“MRMC”) for $4.02 per common unit (the “Merger”) to be voted on during the Company’s upcoming meeting of unitholders scheduled for Monday, December 30, 2024 at 10:00 AM Central time (the “Special Meeting”).

In connection with the filing of the definitive proxy materials, Nut Tree and Caspian have mailed a letter to MMLP’s common unitholders urging them to vote “AGAINST” the Merger at the Special Meeting. As discussed in the definitive proxy materials and the letter, Nut Tree and Caspian oppose the Merger and believe that:

- MMLP’s common units are worth far more than the $4.02 per unit price offered in the Merger;

- The Company relied on a deeply flawed financial analysis used to justify the Merger that ignored the future prospects for MMLP, which stand to create additional value for unitholders; and

- The massive conflicts of interest in the Merger and its negotiation process demand the highest degree of scrutiny and skepticism from MMLP unitholders.

Nut Tree and Caspian stated: “We are opposing this merger because we believe MMLP has a bright future as a publicly traded company and is worth far more than the $4.02 per unit being offered to unitholders. Based on industry-standard valuation methodologies, we believe this is an extremely inadequate price and would unfairly transfer significant value that rightfully belongs to MMLP unitholders to the Company’s insiders, including the ultimate control person of MRMC, Ruben Martin, III. By voting AGAINST the proposed merger with MRMC, MMLP unitholders have an opportunity to protect the value of their investment.”

The full text of the letter can be viewed here and is also available at www.ProtectMMLPValue.com.

Advisors

Olshan Frome Wolosky LLP and Latham & Watkins LLP are serving as legal counsel to Nut Tree and Caspian.

About Caspian Capital LP

Caspian Capital LP’s absolute return strategy was founded in 1997 and is focused on performing, stressed, distressed corporate credit, and value equities. Caspian currently oversees $4.6 billion in assets under management.

About Nut Tree Capital Management LP

Nut Tree Capital, founded in 2015, implements a fundamentals-based strategy focused on distressed credit, stressed/event-driven credit and value equities. Nut Tree currently oversees $4 billion in assets.

Contacts

For Investors:

John Ferguson/Joe Mills

Saratoga Proxy Consulting LLC

(212) 257-1311

info@saratogaproxy.com

For Media:

Jonathan Gasthalter/Nathaniel Garnick

Gasthalter & Co.

(212) 257-4170

Item 2: Also on December 2, 2024, Nut Tree and Caspian posted the following material to www.protectMMLPvalue.com: