UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2020 |

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO |

Commission File Number: 000-55931

Blackstone Real Estate Income Trust, Inc.

(Exact name of Registrant as specified in its charter)

| |

Maryland | 81-0696966 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

345 Park Avenue

New York, New York 10154

(Address of principal executive offices) (Zip Code)

(212) 583-5000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act:

Title of Each Class

Class S Common Stock, $0.01 par value per share

Class I Common Stock, $0.01 par value per share

Class T Common Stock, $0.01 par value per share

Class D Common Stock, $0.01 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | | Accelerated filer | ☐ |

Non-accelerated filer | ☒ | | Smaller reporting company | ☐ |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Yes ☐ No ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act. Yes ☐ No ☒

The aggregate market value of the common stock held by non-affiliates of the registrant: There is currently no established public market for the Registrant’s shares of common stock.

As of March 17, 2021, the issuer had the following shares outstanding: 783,834,057 shares of Class S common stock, 1,054,300,963 shares of Class I common stock, 47,308,129 shares of Class T common stock, and 146,970,893 shares of Class D common stock.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this annual report on Form 10-K incorporates information by reference from the registrant’s definitive proxy statement with respect to its 2021 annual meeting of stockholders to be filed with the Securities and Exchange Commission within 120 days after the close of the registrant’s fiscal year.

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS; RISK FACTOR SUMMARY

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the federal securities laws and the Private Securities Litigation Reform Act of 1995. These forward-looking statements can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “anticipate,” “estimate,” “believe,” “continue” or other similar words or the negatives thereof. These may include our financial projections and estimates and their underlying assumptions, statements about plans, objectives and expectations with respect to future operations, statements with respect to acquisitions and statements regarding future performance. These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this document (or our prospectus and other filings). Except as otherwise required by federal securities laws, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future developments or otherwise.

Forward-looking statements are inherently uncertain and there are or may be important factors that could cause actual outcomes or results to differ materially from those indicated in such statements. A summary of principal risk factors that make investing in our securities risky and might cause such actual outcomes or results to differ is set forth below.

| • | Since there is no public trading market for shares of our common stock, repurchase of shares by us will likely be the only way to dispose of your shares. Our share repurchase plan provides stockholders with the opportunity to request that we repurchase their shares on a monthly basis, but we are not obligated to repurchase any shares and may choose to repurchase only some, or even none, of the shares that have been requested to be repurchased in any particular month in our discretion. In addition, repurchases will be subject to available liquidity and other significant restrictions. Further, our board of directors may make exceptions to, modify and suspend our share repurchase plan if, in its reasonable judgement, it deems such action to be in our best interest and the best interest of our stockholders. Our board of directors cannot terminate our share repurchase plan absent a liquidity event which results in stockholders receiving cash or securities listed on a national securities exchange or where otherwise required by law. As a result, our shares should be considered as having only limited liquidity and at times may be illiquid. |

| • | We cannot guarantee that we will make distributions, and if we do we may fund such distributions from sources other than cash flow from operations, including, without limitation, the sale of or repayment under our assets, borrowings or offering proceeds (including from sales of our common stock or Operating Partnership units to the Special Limited Partner, an affiliate of Blackstone), and we have no limits on the amounts we may pay from such sources. |

| • | The purchase and repurchase price for shares of our common stock are generally based on our prior month’s and are not based on any public trading market. While there will be independent valuations of our properties from time to time, the valuation of properties is inherently subjective and our NAV may not accurately reflect the actual price at which our properties could be liquidated on any given day. |

| • | We are dependent on the Adviser to conduct our operations. The Adviser will face conflicts of interest as a result of, among other things, the allocation of investment opportunities among us and Other Blackstone Accounts, the allocation of time of its investment professionals and the substantial fees that we will pay to the Adviser. |

| • | Principal and interest payments on any borrowings will reduce the amount of funds available for distribution or investment in additional real estate assets. |

| • | There are limits on the ownership and transferability of our shares. See “Description of Capital Stock—Restrictions on Ownership and Transfer” in the prospectus for the Offering. |

| • | While BREIT’s investment strategy is to invest in stabilized commercial real estate diversified by sector with a focus on providing current income to investors, an investment in BREIT is not an investment in fixed income. Fixed income has material differences from an investment in the Company, including those related to vehicle structure, investment objectives and restrictions, risks, fluctuation of principal, safety, guarantees or insurance, fees and expenses, liquidity and tax treatment. |

| • | We intend to continue to qualify as a REIT for U.S. federal income tax purposes. However, if we fail to qualify as a REIT and no relief provisions apply, our NAV and cash available for distribution to our stockholders could materially decrease. |

| • | The acquisition of investment properties may be financed in substantial part by borrowing, which increases our exposure to loss. The use of leverage involves a high degree of financial risk and will increase the exposure of the investments to adverse economic factors. |

| • | Investing in commercial real estate assets involves certain risks, including but not limited to: tenants’ inability to pay rent; increases in interest rates and lack of availability of financing; tenant turnover and vacancies; and changes in supply of or demand for similar properties in a given market. |

1

| • | The outbreak of the novel coronavirus (“COVID-19”) has had and may in the future have an adverse impact on our NAV, results of operations (including FFO, AFFO and FAD), cash flows and fundraising, and may have an adverse impact on our ability to source new investments, obtain financing, fund distributions to stockholders and satisfy repurchase requests, among other factors. |

| • | Our operating results will be affected by global and national economic and market conditions generally and by the local economic conditions where our properties are located, including changes with respect to rising vacancy rates or decreasing market rental rates; fluctuations in the average occupancy and room rates for hotel properties; inability to lease space on favorable terms; bankruptcies, financial difficulties or lease defaults by our tenants, particularly for our tenants with net leases for large properties; and changes in government rules, regulations and fiscal policies, such as property taxes, zoning laws, limitations on rental rates, and compliance costs with respect to environmental laws. |

| • | Our portfolio is currently concentrated in certain industries and geographies, and, as a consequence, our aggregate return may be substantially affected by adverse economic or business conditions affecting that particular type of asset or geography. |

| • | Competition for investment opportunities may reduce our profitability and the return on your investment. |

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, or achievements. We caution you not to place undue reliance on these forward-looking statements. All written and oral forward-looking statements attributable to us or persons acting on our behalf are qualified in their entirety by these cautionary statements. Moreover, unless we are required by law to update these statements, we will not necessarily update or revise any forward-looking statements included or incorporated by reference in this Annual Report after the date hereof, either to conform them to actual results or to changes in our expectations. We urge you to carefully consider the foregoing summary together with the risks discussed in Part I., Item 1A. “Risk Factors” and Part II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations”.

Website Disclosure

We use our website (www.breit.com) as a channel of distribution of company information. The information we post through this channel may be deemed material. Accordingly, investors should monitor this channel, in addition to following our press releases and SEC filings. The contents of our website are not, however, a part of this report.

2

PART I.

References herein to “Blackstone Real Estate Income Trust,” the “Company,” “BREIT,” “we,” “us,” or “our” refer to Blackstone Real Estate Income Trust, Inc., a Maryland corporation, and its subsidiaries unless the context specifically requires otherwise.

General Description of Business and Operations

BREIT invests primarily in stabilized income-generating commercial real estate in the United States and, to a lesser extent, in real estate debt. Our objective is to bring Blackstone’s leading institutional quality real estate investment platform to income focused investors. We are externally managed by BX REIT Advisors L.L.C. (the “Adviser”), a subsidiary of The Blackstone Group Inc. (“Blackstone”). We were incorporated in Maryland in 2015. We are the sole general partner of BREIT Operating Partnership L.P. (“BREIT OP”), a Delaware limited partnership, and we own substantially all of our assets through BREIT OP. We currently operate our business in eight reportable segments: Multifamily, Industrial, Net Lease, Hotel, Self Storage, Retail, and Office Properties, and Investments in Real Estate Debt. Multifamily includes various forms of rental housing including apartments, student housing and manufactured housing. Net Lease includes the real estate assets of The Bellagio Las Vegas (“Bellagio”) and the unconsolidated interest in the MGM Grand and Mandalay Bay joint venture.

BREIT is a non-listed, perpetual life real estate investment trust (“REIT”). We qualified as a REIT under the Internal Revenue Code of 1986, as amended (the “Code”) for U.S. federal income tax purposes and generally will not be subject to U.S. federal income taxes on our taxable income to the extent we annually distribute all of our net taxable income to stockholders and maintain our qualification as a REIT.

As of March 17, 2021, we had received net proceeds of $24.1 billion from the sale of shares of our Class S, Class I, Class T and Class D common stock. We have contributed the net proceeds to BREIT OP in exchange for a corresponding number of Class S, Class I, Class T, and Class D units. BREIT OP has primarily used the net proceeds to make investments in real estate and real estate debt.

Our Adviser

We are externally managed by our Adviser, and pursuant to the advisory agreement between us and the Adviser (the “Advisory Agreement”), we have delegated to the Adviser the authority to source, evaluate and monitor our investment opportunities and to make decisions related to the acquisition, management, financing and disposition of our assets, in accordance with our investment objectives, guidelines, policies and limitations, as well as provide us with our executive management team. Our board of directors will at all times have oversight and policy-making authority over us, including responsibility for governance, financial controls, compliance and disclosure.

Our Adviser is a part of Blackstone, a leading global investment manager with assets under management of $618.6 billion as of December 31, 2020. Blackstone’s alternative asset management businesses include private equity, real estate, insurance, hedge fund solutions, non-investment grade credit, secondary private equity funds of funds, infrastructure and multi-asset class strategies, all on a global basis.

In connection with the performance of its duties, our Adviser benefits from the resources, relationships, and expertise of the 541 professionals in Blackstone’s global real estate group, which is one of the largest real estate investment managers in the world with $187.2 billion of investor capital under management as of December 31, 2020. Blackstone's real estate group ("Blackstone Real Estate") has one centralized investment committee (the "Investment Committee") that meets weekly to review large new investments around the world. The Investment Committee includes all Senior Managing Directors in Blackstone Real Estate, as well as select senior executives of Blackstone.

Our chief executive officer, chief financial officer, and other executive officers are senior Blackstone real estate professionals. Our Adviser, our executive officers, and other personnel supplied to us by our Adviser are each not obligated to dedicate any specific amount of time to our business. Our Adviser is subject to the supervision and oversight of our board of directors and has only such functions and authority as our board of directors delegates to it. Pursuant to the Advisory Agreement, our Adviser is entitled to receive a base management fee, and expense reimbursements. In addition, BREIT Special Limited Partner L.P. (the “Special Limited Partner”), a wholly-owned subsidiary of Blackstone, is entitled to receive a performance participation allocation. See Note 9 to our consolidated financial statements and Item 13 “Certain Relationships and Related Transactions, and Director Independence” in this Annual Report on Form 10-K for more detail on the terms of the Advisory Agreement.

3

Investment Objectives

Our investment objectives are to invest in assets that will enable us to:

| • | provide attractive current income in the form of regular, stable cash distributions; |

| • | preserve and protect invested capital; |

| • | realize appreciation in net asset value (“NAV”) from proactive investment management and asset management; and |

| • | provide an investment alternative for stockholders seeking to allocate a portion of their long-term investment portfolios to commercial real estate with lower volatility than listed public real estate companies. |

Investment Strategy

Our investment strategy is to acquire primarily stabilized, income-generating commercial real estate in the United States and to a lesser extent, invest in real estate debt and other securities. Our investment strategy capitalizes on Blackstone’s scale and the real-time information provided by its real estate holdings to identify and acquire our target investments at attractive pricing. We also benefit from Blackstone’s reputation and ability to transact in scale with speed and certainty, and its long-standing and extensive relationships in the real estate industry. After acquisition, we leverage Blackstone Real Estate’s established asset management team, which focuses on value creation through the oversight and improvement of the operating performance of Blackstone Real Estate’s portfolio holdings.

Our investments in primarily stabilized, income-generating U.S. commercial real estate focus on a range of asset types. These may include multifamily, industrial, net lease, hotel, retail, and office assets, as well as others, including, without limitation, healthcare, student housing, senior living, data centers, manufactured housing and storage properties. For a breakdown of our portfolio by asset type see the “Investments in Properties” section below.

Our real estate debt strategy is designed to generate current income and contribute to our overall net returns. Alongside our credit facilities and operating cash flow, our real estate debt investments may provide an additional source of liquidity. These liquidity sources are collectively used for cash management, satisfying any stock repurchases under our share repurchase plan and other purposes. We use the Blackstone Real Estate Debt Strategies team to assist in this portion of the portfolio. The Blackstone Real Estate Debt Strategies team leverages the competitive advantages of the broader Blackstone Real Estate platform and its own proprietary investment models to seek attractive real estate debt investment opportunities throughout the capital structure.

We believe that our structure as a perpetual-life REIT will allow us to acquire and manage our investment portfolio in a more active and flexible manner. We are not limited by a pre-determined operational period or the need to provide a “liquidity” event at the end of that period.

Investments in Real Estate

We invest primarily in stabilized, income-generating U.S. commercial real estate. We may invest to a lesser extent in Canadian and European cities and potentially elsewhere and opportunistically in equity of public and private real estate-related companies. We may also acquire assets that require some amount of capital investment in order to be renovated or repositioned. We generally will limit investment in new developments on a standalone basis, but may consider development that is ancillary to an overall investment.

We do not designate specific geography or sector allocations for the portfolio; rather we invest in regions or asset classes where we see the best opportunities that support our investment objectives.

4

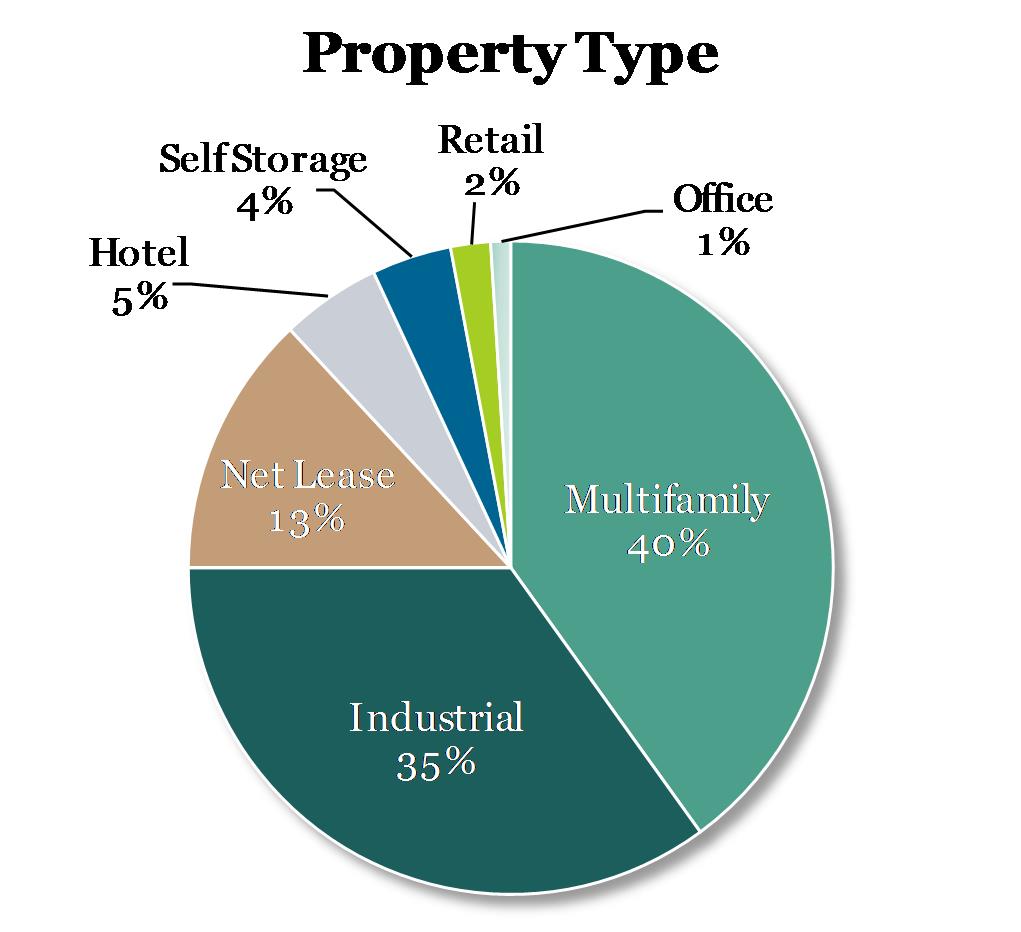

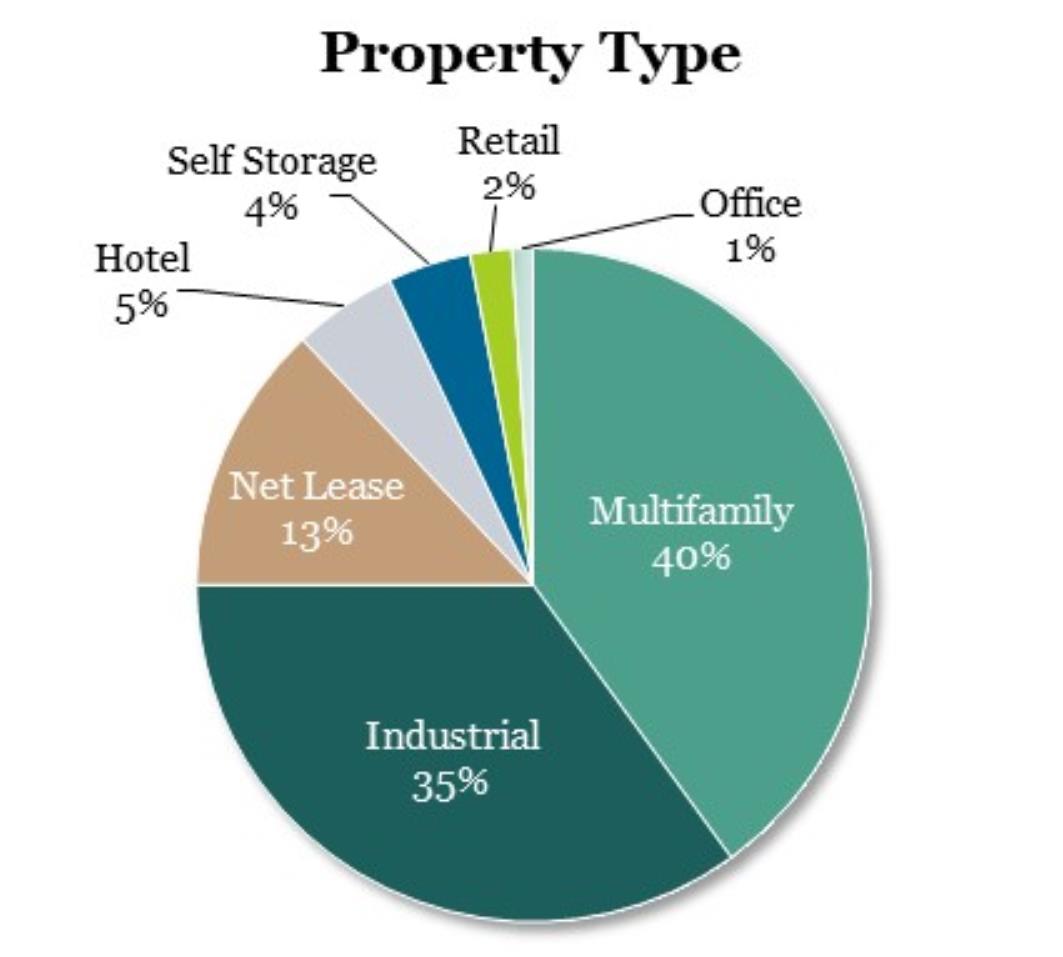

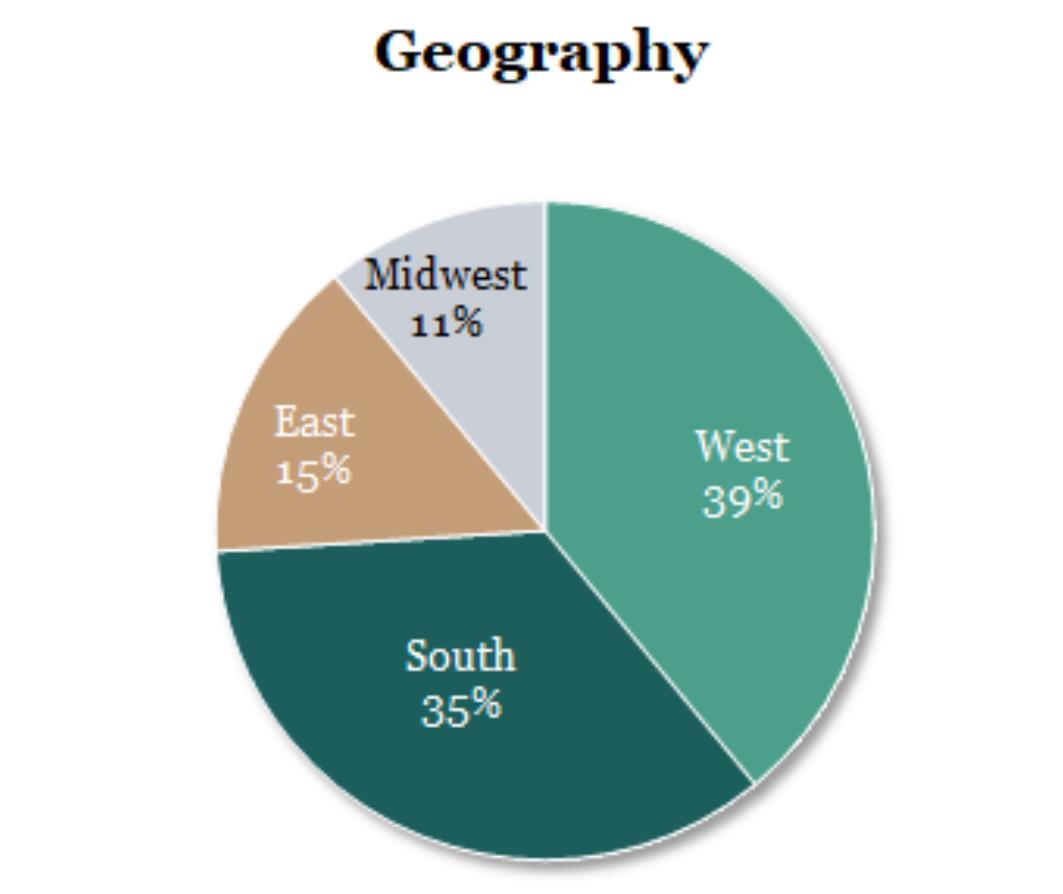

The following charts describe the diversification of our investments in real estate(1) based on fair value as of December 31, 2020:

(1 | ) Investments in real estate includes our direct property investments, unconsolidated investments, and equity in public and private real estate-related companies. “Geography” weighting is measured as the asset value of real estate properties, excluding the value of any third party interests in such real estate properties, and unconsolidated investments for each geographical category (South, East, West, Midwest) against the total asset value of all (i) real estate properties, excluding the value of any third party interests in such real estate properties, and (ii) unconsolidated investments. |

5

The following map identifies the top markets of our portfolio composition in real properties based on fair value as of December 31, 2020:

The select markets that are named represent all metropolitan statistical areas (“MSAs”) in which BREIT has at least a 2% weighting. BREIT is invested in additional MSAs which are not named above. Shading reflects the concentration of all real estate properties and unconsolidated investments in each state. Weighting is measured as the asset value of real estate properties and unconsolidated investments for each market against the total asset value of all (i) real estate properties, excluding the value of any third party interests in such real estate properties, and (ii) unconsolidated investments.

Investments in Real Estate Debt

Our real estate debt investments focus on non-distressed public and private real estate debt, including, but not limited to, commercial mortgage-backed securities (“CMBS”), real estate-related corporate credit, mortgages, loans, mezzanine and other forms of debt (including residential mortgage-backed securities (“RMBS”) and other residential credit), interests of collateralized debt obligation and collateralized loan obligation vehicles and equity interests in public and private entities that invest in real estate debt as one of their core businesses, and may also include preferred equity and derivatives. Our investments in real estate debt are focused in the United States, but may also include securities issued or backed by real estate in Europe and certain other countries.

Borrowing Policies

We use financial leverage to provide additional funds to support our investment activities. This allows us to make more investments than would otherwise be possible, resulting in a broader portfolio. Subject to the limitation on indebtedness for money borrowed in our charter described below, our target leverage ratio is in the range of 60%. Our leverage ratio is measured by dividing (i) consolidated

6

property-level and entity-level debt net of cash and loan-related restricted cash, by (ii) the asset value of real estate investments (measured using the greater of fair market value and the cost) plus the equity in our settled real estate debt portfolio. Indebtedness incurred (i) in connection with funding a deposit in advance of the closing of an investment or (ii) as other working capital advances, will not be included as part of the calculation above. The leverage ratio excludes our pro rata share of indebtedness within our unconsolidated investments. Real estate investments include our direct property investments, unconsolidated investments, and equity in public and private real estate-related companies. Our real estate debt portfolio may have embedded leverage, including through the use of reverse repurchase agreements and derivatives, including, but not limited to, total return swaps, securities lending arrangements and credit default swaps. During times of increased investment and capital market activity, but subject to the limitation on indebtedness for money borrowed in our charter described below, we may employ greater leverage in order to build a broader portfolio of assets. We may leverage our portfolio by assuming or incurring secured or unsecured property-level or entity-level debt.

Under our charter, we have a limitation that precludes us from borrowing in excess of 300% of the cost of our net assets, which approximates borrowing 75% of the cost of our investments (unless a majority of our independent directors approves any borrowing in excess of the limit and we disclose the justification for doing so to our stockholders), but such restriction does not restrict the amount of indebtedness we may incur with respect to any single investment.

For an overview of our borrowings, see Item 7 — “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources.”

Taxation of the Company

We elected to be taxed as a REIT, under the Code commencing with our taxable year ended December 31, 2017, the year in which the proceeds from the Initial Offering were released from escrow. We generally must distribute annually at least 90% of our taxable net income, subject to certain adjustments and excluding any net capital gain, in order for U.S. federal income tax not to apply to our earnings that we distribute. To the extent that we satisfy this distribution requirement, but distribute less than 100% of our net taxable income, we will be subject to U.S. federal income tax on our undistributed taxable income. In addition, we will be subject to a 4% nondeductible excise tax if the actual amount that we pay out to our stockholders in a calendar year is less than a minimum amount specified under U.S. federal tax laws.

Our qualification as a REIT also depends on our ability to meet various other requirements imposed by the Code, which relate to organizational structure, diversity of stock ownership, and certain restrictions with regard to the nature of our assets and the sources of our income. Even if we qualify as a REIT, we may be subject to certain U.S. federal income and excise taxes and state and local taxes on our income and assets. If we fail to maintain our qualification as a REIT for any taxable year, we may be subject to material penalties as well as federal, state, and local income tax on our taxable income at regular corporate rates and we would not be able to qualify as a REIT for the subsequent four full taxable years.

Furthermore, we have one or more taxable REIT subsidiaries (“TRSs”) which pay federal, state, and local income tax on their net taxable income. See Item 1A—“Risk Factors—Risks Related to our REIT Status and Certain Other Tax Items” for additional tax status information.

Governmental Regulations

As an owner of real estate, our operations are subject, in certain instances, to supervision and regulation by U.S. and other governmental authorities, and may be subject to various laws and judicial and administrative decisions imposing various requirements and restrictions, which, include among other things: (i) federal and state securities laws and regulations; (ii) federal, state and local tax laws and regulations, (ii) state and local laws relating to real property; (iv) federal, state and local environmental laws, ordinances, and regulations, and (v) various laws relating to housing, including permanent and temporary rent control and stabilization laws, the Americans with Disabilities Act of 1990 and the Fair Housing Amendment Act of 1988, among others.

Compliance with the federal, state and local laws described above has not had a material, adverse effect on our business, assets, results of operations, financial condition and ability to pay distributions, and we do not believe that our existing portfolio will require us to incur material expenditures to comply with these laws and regulations.

Competition

We face competition from various entities for investment opportunities in properties, including other REITs, pension funds, insurance companies, investment funds and companies, partnerships and developers. In addition to third-party competitors, other programs sponsored by the Adviser and its affiliates, particularly those with investment strategies that overlap with ours, will seek investment

7

opportunities under Blackstone’s prevailing policies and procedures. Many of these entities may have greater access to capital to make investments than we have.

In the face of this competition, we have access to our Adviser’s and Blackstone’s professionals and their industry expertise and relationships, which we believe provide us with a competitive advantage and help us source, evaluate and compete for potential investments. We believe these relationships will enable us to compete more effectively for attractive investment opportunities. However, we may not be able to achieve our business goals or expectations due to the competitive risks that we face. For additional information concerning these competitive risks, see Item 1A—“Risk Factors—Risks Related to Our Investment Activities.”

Human Capital

We have no employees other than those employed by Simply Storage Management, which was acquired with the December 2020 acquisition of Simply Storage, none of whom are executive officers of the Company or are involved in the management of the Company. Our operations are conducted by the Adviser.

Conflicts of Interest

We are subject to conflicts of interest arising out of our relationship with Blackstone, including the Adviser and its affiliates. See Item 1A — “Risk Factors — Risks Related to Conflicts of Interest.”

Available Information

Stockholders may obtain copies of our filings with the SEC, free of charge from the website maintained by the SEC at www.sec.gov or from our website at www.breit.com.

We are providing the address to our website solely for the information of investors. The information on our website is not a part of, nor is it incorporated by reference into, this report.

8

You should specifically consider the following material risks in addition to the other information contained in this Annual Report on Form 10-K. The occurrence of any of the following risks might have a material adverse effect on our business and financial condition. The risks and uncertainties discussed below are not the only ones we face, but do represent those risks and uncertainties that we believe are most significant to our business, operating results, financial condition, prospects and forward-looking statements. As used herein, the term “you” refers to our current stockholders or potential investors in our common stock, as applicable.

Risks Related to Our Organizational Structure

We have held most of our current investments for only a limited period of time and you will not have the opportunity to evaluate our future investments before we make them, which makes your investment more speculative.

We have held most of our current investments for a limited period of time and are not able to provide you with information to assist you in evaluating the merits of any specific properties or real estate debt that we may acquire, except for investments that may be described in one or more supplements to the prospectus for the Offering (the “Prospectus”). Because we have not held our current investments for a long period of time, it may be difficult for you to evaluate our success in achieving our investment objectives. We will continue to seek to invest substantially all of the future net offering proceeds from the Offering and certain private offerings, after the payment of fees and expenses, in the acquisition of or investment in interests in properties and real estate debt. However, because you will be unable to evaluate the economic merit of our future investments before we make them, you will have to rely entirely on the ability of the Adviser to select suitable and successful investment opportunities. Furthermore, the Adviser has broad discretion in selecting the types of properties we will invest in and the tenants of those properties, and you will not have the opportunity to evaluate potential investments. These factors increase the risk that your investment may not generate returns comparable to other real estate investment alternatives.

The Adviser manages our portfolio pursuant to very broad investment guidelines and generally is not required to seek the approval of our board of directors for each investment, financing or asset allocation decision made by it, which may result in our making riskier investments and which could adversely affect our results of operations and financial condition.

Our board of directors approved very broad investment guidelines that delegate to the Adviser the authority to execute acquisitions and dispositions of real estate and real estate debt on our behalf, in each case so long as such investments are consistent with the investment guidelines and our charter. The Adviser will implement on our behalf the strategies and discretionary approaches it believes from time to time may be best suited to prevailing market conditions in furtherance of that purpose, subject to the limitations under our investment guidelines and our charter. There can be no assurance that the Adviser will be successful in implementing any particular strategy or discretionary approach to our investment activities. Furthermore, the diversification and type of investments may differ substantially from our prior investments. For example, future investments may focus on different sectors of real estate or different geographic areas than is the case for our current investment portfolio. Our board of directors reviews our investment guidelines on an annual basis (or more often as it deems appropriate) and reviews our investment portfolio periodically. The prior approval of our board of directors or a committee of independent directors will be required only as set forth in our charter (including for transactions with affiliates of the Adviser) or for the acquisition or disposition of assets that are not in accordance with our investment guidelines. In addition, in conducting periodic reviews, our directors rely primarily on information provided to them by the Adviser. Furthermore, transactions entered into on our behalf by the Adviser may be costly, difficult or impossible to unwind when they are subsequently reviewed by our board of directors.

There is no public trading market for shares of our common stock; therefore, your ability to dispose of your shares will likely be limited to repurchase by us. If you do sell your shares to us, you may receive less than the price you paid.

There is no current public trading market for shares of our common stock, and we do not expect that such a market will ever develop. Therefore, repurchase of shares by us will likely be the only way for you to dispose of your shares. We expect to continue to repurchase shares at a price equal to the transaction price of the class of shares being repurchased on the date of repurchase (which will generally be equal to our prior month’s NAV per share) and not based on the price at which you initially purchased your shares. Subject to limited exceptions, shares repurchased within one year of the date of issuance will be repurchased at 95% of the transaction price. As a result, you may receive less than the price you paid for your shares when you sell them to us pursuant to our share repurchase plan. See Item 5—“Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities—Share Repurchases.”

9

Your ability to have your shares repurchased through our share repurchase plan is limited. We may choose to repurchase fewer shares than have been requested to be repurchased, in our discretion at any time, and the amount of shares we may repurchase is subject to caps. Further, our board of directors may make exceptions to, modify or suspend our share repurchase plan if it deems such action to be in our best interest and the best interest of our stockholders.

We may choose to repurchase fewer shares than have been requested in any particular month to be repurchased under our share repurchase plan, or none at all, in our discretion at any time. We may repurchase fewer shares than have been requested to be repurchased due to lack of readily available funds because of adverse market conditions beyond our control, the need to maintain liquidity for our operations or because we have determined that investing in real property or other illiquid investments is a better use of our capital than repurchasing our shares. In addition, the aggregate NAV of total repurchases (including repurchases at certain non-U.S. investor access funds primarily created to hold shares of our common stock but excluding any Early Repurchase Deduction applicable to the repurchased shares) is limited, in any calendar month, to no more than 2% of our aggregate NAV(measured using the aggregate NAV as of the end of the immediately preceding month) and, in any calendar quarter, to shares whose aggregate value is no more than 5% of our aggregate NAV (measured using the average aggregate NAV at the end of the immediately preceding three months). Further, our board of directors may make exceptions to, modify and suspend our share repurchase plan if, in its reasonable judgment, it deems such action to be in our best interest and the best interest of our stockholders. Our board of directors cannot terminate our share repurchase plan absent a liquidity event which results in stockholders receiving cash or securities listed on a national securities exchange or where otherwise required by law. If the full amount of all shares of our common stock requested to be repurchased in any given month are not repurchased, funds will be allocated pro rata based on the total number of shares of common stock being repurchased without regard to class and subject to the volume limitation. All unsatisfied repurchase requests must be resubmitted after the start of the next month or quarter, or upon the recommencement of the share repurchase plan, as applicable.

The vast majority of our assets consist of properties that cannot generally be readily liquidated without impacting our ability to realize full value upon their disposition. Therefore, we may not always have a sufficient amount of cash to immediately satisfy repurchase requests. Should repurchase requests, in our judgment, place an undue burden on our liquidity, adversely affect our operations or risk having an adverse impact on the Company as a whole, or should we otherwise determine that investing our liquid assets in real properties or other illiquid investments rather than repurchasing our shares is in the best interests of the Company as a whole, then we may choose to repurchase fewer shares than have been requested to be repurchased, or none at all. Upon suspension of our share repurchase plan, our board of directors will be required to consider at least quarterly whether the continued suspension of our share repurchase plan is in the best interests of the Company and our stockholders; however, we are not required to authorize the recommencement of the share repurchase plan within any specified period of time. As a result, your ability to have your shares repurchased by us may be limited and at times you may not be able to liquidate your investment. See Item 5—“Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities—Share Repurchases.”

Economic events that may cause our stockholders to request that we repurchase their shares may materially adversely affect our cash flow and our results of operations and financial condition.

Economic events affecting the U.S. economy, such as the general negative performance of the real estate sector, could cause our stockholders to seek to sell their shares to us pursuant to our share repurchase plan at a time when such events are adversely affecting the performance of our assets. Even if we decide to satisfy all resulting repurchase requests, our cash flow could be materially adversely affected. In addition, if we determine to sell assets to satisfy repurchase requests, we may not be able to realize the return on such assets that we may have been able to achieve had we sold at a more favorable time, and our results of operations and financial condition, including, without limitation, breadth of our portfolio by property type and location, could be materially adversely affected.

We have incurred net losses under GAAP in the past and may incur net losses in the future, and we have an accumulated deficit and may continue to have an accumulated deficit in the future.

For the year ended December 31, 2020 and the year ended December 31, 2019, we had net loss attributable to our stockholders of approximately $853.4 million and $401.8 million, respectively. As of December 31, 2020 and December 31, 2019, we had an accumulated deficit of approximately $1.6 billion and $769.2 million, respectively. These amounts largely reflect the expense of real estate depreciation and amortization in accordance with GAAP, which was $1.4 billion and $824.0 million during these periods. For the year ended December 31, 2020 and the year ended December 31, 2019, our funds available for distribution, or FAD, was $743.7 million and $409.4 million, respectively.

Net loss and accumulated deficit are calculated and presented in accordance with GAAP, which, among other things, requires depreciation of real estate investments to be calculated on a straight-line basis. As a result, our operating results imply that the value of our real estate investments will decrease evenly over a set time period. However, we believe that the value of real estate investments will fluctuate over time based on market conditions. Thus, in addition to GAAP financial metrics, management reviews certain non-GAAP financial metrics that exclude real estate-related depreciation and amortization, including FAD, as an additional meaningful

10

non-GAAP supplemental disclosure to provide information for considering our operating results. See Item 5—“Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities— Funds from Operations, Adjusted Funds from Operations and Funds Available for Distribution” for reconciliations of FAD to GAAP net loss attributable to common stockholders and for considerations on how to review this metric.

We face risks associated with the deployment of our capital.

In light of the nature of our continuous public offering as well as ongoing and periodic private offerings in relation to our investment strategy and the need to be able to deploy potentially large amounts of capital quickly to capitalize on potential investment opportunities, if we have difficulty identifying and purchasing suitable properties on attractive terms, there could be a delay between the time we receive net proceeds from the sale of shares of our common stock in the Offering or any private offering and the time we invest the net proceeds. We may also from time to time hold cash pending deployment into investments or have less than our targeted leverage, which cash or shortfall in target leverage may at times be significant, particularly at times when we are receiving high amounts of offering proceeds and/or times when there are few attractive investment opportunities. Such cash may be held in an account for the benefit of our stockholders that may be invested in money market accounts or other similar temporary investments, each of which are subject to the management fees.

In the event we are unable to find suitable investments such cash may be maintained for longer periods which would be dilutive to overall investment returns. This could cause a substantial delay in the time it takes for your investment to realize its full potential return and could adversely affect our ability to pay regular distributions of cash flow from operations to you. It is not anticipated that the temporary investment of such cash into money market accounts or other similar temporary investments pending deployment into investments will generate significant interest, and investors should understand that such low interest payments on the temporarily invested cash may adversely affect overall returns. In the event we fail to timely invest the net proceeds of sales of our common stock or do not deploy sufficient capital to meet our targeted leverage, our results of operations and financial condition may be adversely affected.

If we are unable to successfully integrate new investments and manage our growth, our results of operations and financial condition may suffer.

We have in the past and may in the future significantly increase the size and/or change the types of investments in our portfolio. We may be unable to successfully and efficiently integrate newly acquired investments into our existing portfolio or otherwise effectively manage our assets or growth. In addition, increases in the size of our investment portfolio and/or changes in our investment focus may place significant demands on our Adviser’s administrative, operational, asset management, financial and other resources which could lead to decreased efficiency. Any failure to effectively manage such growth or increase in scale could adversely affect our results of operations and financial condition.

The amount and source of distributions we may make to our stockholders is uncertain, and we may be unable to generate sufficient cash flows from our operations to make distributions to our stockholders at any time in the future.

We have not established a minimum distribution payment level, and our ability to make distributions to our stockholders may be adversely affected by a number of factors, including the risk factors described in the Prospectus. We have a limited track record and may not generate sufficient income to make distributions to our stockholders. Our board of directors (or a committee of our board of directors) will make determinations regarding distributions based upon, among other factors, our financial performance, debt service obligations, debt covenants, REIT qualification and tax requirements and capital expenditure requirements. Among the factors that could impair our ability to make distributions to our stockholders are:

| • | our inability to invest the proceeds from sales of our shares on a timely basis in income-producing properties; |

| • | our inability to realize attractive risk-adjusted returns on our investments; |

| • | high levels of expenses or reduced revenues that reduce our cash flow or non-cash earnings; and |

| • | defaults in our investment portfolio or decreases in the value of our investments. |

As a result, we may not be able to make distributions to our stockholders at any time in the future, and the level of any distributions we do make to our stockholders may not increase or even be maintained over time, any of which could materially and adversely affect the value of your investment.

11

We may pay distributions from sources other than our cash flow from operations, including, without limitation, the sale of or repayment under our assets, borrowings or offering proceeds, and we have no limits on the amounts we may pay from such sources.

We may not generate sufficient cash flow from operations to fully fund distributions to stockholders. Therefore, we may fund distributions to our stockholders from sources other than cash flow from operations, including, without limitation, the sale of or repayment under our assets, borrowings or offering proceeds (including from sales from our common stock or Operating Partnership units). The extent to which we pay distributions from sources other than cash flow from operations will depend on various factors, including the level of participation in our distribution reinvestment plan, the extent to which the Adviser elects to receive its management fee in Class I shares or Class I units and the Special Limited Partner elects to receive distributions on its performance participation interest in Class I units or Class B units, how quickly we invest the proceeds from this and any future offering and the performance of our investments, including our real estate debt portfolio. Funding distributions from the sale of or repayment under our assets, borrowings or proceeds of the Offering will result in us having less funds available to acquire properties or other real estate-related investments. As a result, the return you realize on your investment may be reduced. Doing so may also negatively impact our ability to generate cash flows. Likewise, funding distributions from the sale of additional securities will dilute your interest in us on a percentage basis and may impact the value of your investment especially if we sell these securities at prices less than the price you paid for your shares. We may be required to continue to fund our regular distributions from a combination of some of these sources if our investments fail to perform, if expenses are greater than our revenues or due to numerous other factors. We have not established a limit on the amount of our distributions that may be paid from any of these sources.

To the extent we borrow funds to pay distributions, we would incur borrowing costs and these borrowings would require a future repayment. The use of these sources for distributions and the ultimate repayment of any liabilities incurred could adversely impact our ability to pay distributions in future periods, decrease our NAV, decrease the amount of cash we have available for operations and new investments and adversely impact the value of your investment.

We may also defer operating expenses or pay expenses (including the fees of the Adviser or distributions to the Special Limited Partner) with shares of our common stock or Operating Partnership units in order to preserve cash flow for the payment of distributions. The ultimate repayment of these deferred expenses could adversely affect our operations and reduce the future return on your investment. We may repurchase shares or redeem Operating Partnership units from the Adviser or the Special Limited Partner shortly after issuing such units or shares as compensation. The payment of expenses in shares of our common stock or with Operating Partnership units will dilute your ownership interest in our portfolio of assets. There is no guarantee any of our operating expenses will be deferred and the Adviser and Special Limited Partner are under no obligation to receive future fees or distributions in shares of our common stock or Operating Partnership units and may elect to receive such amounts in cash.

Payments to the Adviser or the Special Limited Partner in the form of common stock or Operating Partnership units they elect to receive in lieu of fees or distributions will dilute future cash available for distribution to our stockholders.

The Adviser or the Special Limited Partner may choose to receive, and have in the past received, our common stock or Operating Partnership units in lieu of certain fees or distributions. The holders of all Operating Partnership units are entitled to receive cash from operations pro rata with the distributions being paid to us and such distributions to the holder of the Operating Partnership units will reduce the cash available for distribution to us and to our stockholders. Furthermore, under certain circumstances the Operating Partnership units held by the Adviser or the Special Limited Partner are required to be repurchased, in cash at the holder’s election, and there may not be sufficient cash to make such a repurchase payment; therefore, we may need to use cash from operations, borrowings, offering proceeds or other sources to make the payment, which will reduce cash available for distribution to you or for investment in our operations. Repurchases of our shares or Operating Partnership units from the Adviser paid to the Adviser as a management fee are not subject to the monthly and quarterly volume limitations or the Early Purchase Deduction, and such sales receive priority over other shares being put for repurchase during such period. Repurchases of our shares or Operating Partnership units from the Special Limited Partner distributed to the Special Limited Partner with respect to its performance participation interest are not subject to the Early Purchase Deduction, but such repurchases are subject to the monthly and quarterly volume limitations and do not receive priority over other shares being put for repurchase during such period.

Purchases and repurchases of shares of our common stock are not made based on the current NAV per share of our common stock.

Generally, our offering price per share and the price at which we make repurchases of our shares will equal the NAV per share of the applicable class as of the last calendar day of the prior month, plus, in the case of our offering price, applicable upfront selling commissions and dealer manager fees. The NAV per share, if calculated as of the date on which you make your subscription request or repurchase request, may be significantly different than the transaction price you pay or the repurchase price you receive. Certain of our investments or liabilities are subject to high levels of volatility from time to time and could change in value significantly between

12

the end of the prior month as of which our NAV is determined and the date that you acquire or repurchase our shares, however the prior month’s NAV per share will generally continue to be used as the transaction price per share and repurchase price per share. In exceptional circumstances, we may in our sole discretion, but are not obligated to, offer and repurchase shares at a different price that we believe reflects the NAV per share of such stock more appropriately than the prior month’s NAV per share, including by updating a previously disclosed transaction price, in cases where we believe there has been a material change (positive or negative) to our NAV per share since the end of the prior month and we believe an updated price is appropriate. In such exceptional cases, the transaction price and the repurchase price will not equal our NAV per share as of any time.

Valuations and appraisals of our real estate and real estate debt are estimates of fair value and may not necessarily correspond to realizable value.

For the purposes of calculating our monthly NAV, our properties will generally initially be valued at cost, which we expect to represent fair value at that time. Thereafter, valuations of properties will be determined by the Adviser based in part on appraisals of each of our properties by independent third-party appraisal firms reviewed by our independent valuation advisor at least once per year in accordance with valuation guidelines approved by our board of directors. The Adviser will also conduct a monthly valuation of our properties that will be reviewed and confirmed for reasonableness by our independent valuation advisor. Investments in real estate debt and other securities with readily available market quotations will be valued monthly at fair market value. Certain investments, such as mortgages and mezzanine loans, are unlikely to have market quotations. In the case of loans acquired by us, preferred equity and private company investments, such initial value will generally be the acquisition price of such investment. In the case of loans originated by us, such initial value will generally be the par value of such loan. Each such investment will then be valued by the Adviser within the first three full months after we invest in such investment and no less than quarterly thereafter. Additionally, the Adviser may in its discretion consider material market data and other information that becomes available after the end of the applicable month in valuing our assets and liabilities and calculating our NAV for a particular month. For more information regarding our valuation process, see “Net Asset Value Calculation and Valuation Guidelines” in the Prospectus.

Although monthly valuations of each of our real properties will be reviewed and confirmed for reasonableness by our independent valuation advisor, such valuations are based on asset- and portfolio-level information provided by the Adviser, including historical operating revenues and expenses of the properties, lease agreements on the properties, revenues and expenses of the properties, information regarding recent or planned capital expenditures and any other information relevant to valuing the real property, which information will not be independently verified by our independent valuation advisor. Similarly, each month, our independent valuation advisor will review and confirm for reasonableness our quarterly valuations (and our monthly updates of such valuations) of our real estate debt and other securities for which market quotations are not readily available. However, such valuations are based on information provided by the Adviser, which information will not be verified by our independent valuation advisor.

Within the parameters of our valuation guidelines, the valuation methodologies used to value our properties and certain of our investments will involve subjective judgments and projections and may not be accurate. Valuation methodologies will also involve assumptions and opinions about future events, which may or may not turn out to be correct. Valuations and appraisals of our properties and other investments will be only estimates of fair value. Ultimate realization of the value of an asset depends to a great extent on economic, market and other conditions beyond our control and the control of the Adviser and our independent valuation advisor. Further, valuations do not necessarily represent the price at which an asset would sell, since market prices of assets can only be determined by negotiation between a willing buyer and seller. As such, the carrying value of an asset may not reflect the price at which the asset could be sold in the market, and the difference between carrying value and the ultimate sales price could be material. In addition, accurate valuations are more difficult to obtain in times of low transaction volume because there are fewer market transactions that can be considered in the context of the appraisal. There will be no retroactive adjustment in the valuation of such assets, the offering price of our shares of common stock, the price we paid to repurchase shares of our common stock or NAV-based fees we paid to the Adviser and Blackstone Securities Partners L.P. (the “Dealer Manager”), an affiliate of the Adviser, to the extent such valuations prove to not accurately reflect the realizable value of our assets. Because the price you will pay for shares of our common stock in the Offering, and the price at which your shares may be repurchased by us pursuant to our share repurchase plan are generally based on our prior month’s NAV per share, you may pay more than realizable value or receive less than realizable value for your investment.

Our NAV per share amounts may change materially if the appraised values of our properties materially change from prior appraisals or the actual operating results for a particular month differ from what we originally budgeted for that month.

We anticipate that the annual appraisals of our properties will be conducted on a rolling basis, such that properties may be appraised at different times but each property would be appraised at least once per year. When these appraisals are considered by the Adviser for purposes of valuing the relevant property, there may be a material change in our NAV per share amounts for each class of our common stock from those previously reported. In addition, actual operating results for a given month may differ from what we originally budgeted for that month, which may cause a material increase or decrease in the NAV per share amounts. We will not

13

retroactively adjust the NAV per share of each class reported for the previous month. Therefore, because a new annual appraisal may differ materially from the prior appraisal or the actual results from operations may be better or worse than what we previously budgeted for a particular month, the adjustment to take into consideration the new appraisal or actual operating results may cause the NAV per share for each class of our common stock to increase or decrease, and such increase or decrease will occur in the month the adjustment is made.

It may be difficult to reflect, fully and accurately, material events that may impact our monthly NAV.

The Adviser’s determination of our monthly NAV per share will be based in part on appraisals of each of our properties provided annually by independent third-party appraisal firms in individual appraisal reports reviewed by our independent valuation advisor and quarterly valuations of our real estate debt and other securities for which market prices are not readily available provided by the Adviser and reviewed by our independent valuation advisor, each in accordance with valuation guidelines approved by our board of directors. As a result, our published NAV per share in any given month may not fully reflect any or all changes in value that may have occurred since the most recent appraisal or valuation. The Adviser will review appraisal reports and monitor our real estate and real estate debt, and is responsible for notifying the independent valuation advisor of the occurrence of any property-specific or market-driven event it believes may cause a material valuation change in the real estate valuation, but it may be difficult to reflect fully and accurately rapidly changing market conditions or material events that may impact the value of our real estate and real estate debt or liabilities between valuations, or to obtain complete information regarding any such events in a timely manner. For example, an unexpected termination or renewal of a material lease, a material increase or decrease in vacancies or an unanticipated structural or environmental event at a property may cause the value of a property to change materially, yet obtaining sufficient relevant information after the occurrence has come to light and/or analyzing fully the financial impact of such an event may be difficult to do and may require some time. As a result, the NAV per share may not reflect a material event until such time as sufficient information is available and analyzed, and the financial impact is fully evaluated, such that our NAV may be appropriately adjusted in accordance with our valuation guidelines. Depending on the circumstance, the resulting potential disparity in our NAV may be in favor or to the detriment of either stockholders who repurchase their shares, or stockholders who buy new shares, or existing stockholders.

NAV calculations are not governed by governmental or independent securities, financial or accounting rules or standards.

The methods used by our Adviser and State Street to calculate our NAV, including the components used in calculating our NAV, is not prescribed by rules of the SEC or any other regulatory agency. Further, there are no accounting rules or standards that prescribe which components should be used in calculating NAV, and our NAV is not audited by our independent registered public accounting firm. We calculate and publish NAV solely for purposes of establishing the price at which we sell and repurchase shares of our common stock, and you should not view our NAV as a measure of our historical or future financial condition or performance. The components and methodology used in calculating our NAV may differ from those used by other companies now or in the future.

In addition, calculations of our NAV, to the extent that they incorporate valuations of our assets and liabilities, are not prepared in accordance with generally accepted accounting principles. These valuations may differ from liquidation values that could be realized in the event that we were forced to sell assets.

Additionally, errors may occur in calculating our NAV, which could impact the price at which we sell and repurchase shares of our common stock and the amount of the Adviser’s management fee and the Special Limited Partner’s performance participation interest. The Adviser has implemented certain policies and procedures to address such errors in NAV calculations. If such errors were to occur, the Adviser, depending on the circumstances surrounding each error and the extent of any impact the error has on the price at which shares of our common stock were sold or repurchased or on the amount of the Adviser’s management fee or the Special Limited Partner’s performance participation interest, may determine in its sole discretion to take certain corrective actions in response to such errors, including, subject to Blackstone’s policies and procedures, making adjustments to prior NAV calculations. You should carefully review the disclosure of our valuation policies and how NAV will be calculated under “Net Asset Value Calculation and Valuation Guidelines” in the Prospectus.

Our board of directors may, in the future, adopt certain measures under Maryland law without stockholder approval that may have the effect of making it less likely that a stockholder would receive a “control premium” for his or her shares.

Corporations organized under Maryland law with a class of registered securities and at least three independent directors are permitted to elect to be subject, by a charter or bylaw provision or a resolution of its board of directors and notwithstanding any contrary charter or bylaw provision, to any or all of five provisions:

| • | staggering the board of directors into three classes; |

| • | requiring a two-thirds vote of stockholders to remove directors; |

14

| • | providing that only the board of directors can fix the size of the board; |

| • | providing that all vacancies on the board, regardless of how the vacancy was created, may be filled only by the affirmative vote of a majority of the remaining directors in office and for the remainder of the full term of the class of directors in which the vacancy occurred; and |

| • | providing for a majority requirement for the calling by stockholders of a special meeting of stockholders. |

These provisions may discourage an extraordinary transaction, such as a merger, tender offer or sale of all or substantially all of our assets, all of which might provide a premium price for stockholders’ shares. In our charter, we have elected that vacancies on our board of directors be filled only by the remaining directors and for the remainder of the full term of the directorship in which the vacancy occurred. Through other provisions in our charter and bylaws, we vest in our board of directors the exclusive power to fix the number of directorships, provided that the number is not less than three. We have not elected to be subject to any of the other provisions described above, but our charter does not prohibit our board of directors from opting into any of these provisions in the future.

Further, under the Maryland Business Combination Act, we may not engage in any merger or other business combination with an “interested stockholder” (which is defined as (1) any person who beneficially owns, directly or indirectly, 10% or more of the voting power of our outstanding voting stock and (2) an affiliate or associate of ours who, at any time within the two-year period prior to the date in question, was the beneficial owner, directly or indirectly, of 10% or more of the voting power of our then outstanding stock) or any affiliate of that interested stockholder for a period of five years after the most recent date on which the interested stockholder became an interested stockholder. A person is not an interested stockholder if our board of directors approved in advance the transaction by which he would otherwise have become an interested stockholder. In approving a transaction, our board of directors may provide that its approval is subject to compliance, at or after the time of approval, with any terms or conditions determined by our board of directors. After the five-year period ends, any merger or other business combination with the interested stockholder or any affiliate of the interested stockholder must be recommended by our board of directors and approved by the affirmative vote of at least:

| • | 80% of all votes entitled to be cast by holders of outstanding shares of our voting stock; and |

| • | two-thirds of all of the votes entitled to be cast by holders of outstanding shares of our voting stock other than those shares owned or held by the interested stockholder with whom or with whose affiliate the business combination is to be effected or held by an affiliate or associate of the interested stockholder. |

These supermajority voting provisions do not apply if, among other things, our stockholders receive a minimum price (as defined in the Maryland General Corporation Law (the “MGCL”)) for their common stock and the consideration is received in cash or in the same form as previously paid by the interested stockholder.

The statute permits various exemptions from its provisions, including business combinations that are exempted by our board of directors prior to the time the interested stockholder becomes an interested stockholder. Our board of directors has adopted a resolution exempting any business combination involving us and any person, including Blackstone, the Dealer Manager and the Adviser, from the provisions of this law, provided that such business combination is first approved by our board of directors.

Our charter permits our board of directors to authorize us to issue preferred stock on terms that may subordinate the rights of the holders of our current common stock or discourage a third party from acquiring us.

Our board of directors is permitted, subject to certain restrictions set forth in our charter, to authorize the issuance of shares of preferred stock without stockholder approval. Further, our board of directors may classify or reclassify any unissued shares of common or preferred stock into other classes or series of stock and establish the preferences, conversion or other rights, voting powers, restrictions, limitations as to dividends and other distributions, qualifications, and terms or conditions of redemption of the stock and may amend our charter from time to time to increase or decrease the aggregate number of shares or the number of shares of any class or series that we have authority to issue without stockholder approval. Thus, our board of directors could authorize us to issue shares of preferred stock with terms and conditions that could subordinate the rights of the holders of our common stock or have the effect of delaying, deferring or preventing a change in control of us, including an extraordinary transaction such as a merger, tender offer or sale of all or substantially all of our assets, that might provide a premium price for holders of our common stock.

Maryland law limits, in some cases, the ability of a third party to vote shares acquired in a “control share acquisition.”

The Maryland Control Share Acquisition Act provides that “control shares” of a Maryland corporation acquired in a “control share acquisition” have no voting rights except to the extent approved by stockholders by a vote of two-thirds of the votes entitled to be cast on the matter. Shares of stock owned by the acquirer, by officers or by employees who are directors of the corporation, are excluded

15

from shares entitled to vote on the matter. “Control shares” are voting shares of stock which, if aggregated with all other shares of stock owned by the acquirer or in respect of which the acquirer can exercise or direct the exercise of voting power (except solely by virtue of a revocable proxy), would entitle the acquirer to exercise voting power in electing directors within specified ranges of voting power. Control shares do not include shares the acquiring person is then entitled to vote as a result of having previously obtained stockholder approval or shares acquired directly from the corporation. A “control share acquisition” means the acquisition of issued and outstanding control shares. The control share acquisition statute does not apply: (1) to shares acquired in a merger, consolidation or statutory share exchange if the Maryland corporation is a party to the transaction; or (2) to acquisitions approved or exempted by the charter or bylaws of the Maryland corporation. Our bylaws contain a provision exempting from the Control Share Acquisition Act any and all acquisitions of our stock by any person. There can be no assurance that this provision will not be amended or eliminated at any time in the future. For a more detailed discussion on the Maryland laws governing control share acquisitions, see “Certain Provisions of Maryland Corporate Law and Our Charter and Bylaws—Control Share Acquisition” in the Prospectus.

Maryland law and our organizational documents limit our rights and the rights of our stockholders to recover claims against our directors and officers, which could reduce your and our recovery against them if they cause us to incur losses.

Maryland law provides that a director will not have any liability as a director so long as he or she performs his or her duties in accordance with the applicable standard of conduct. In addition, our charter generally limits the personal liability of our directors and officers for monetary damages subject to the limitations of the North American Securities Administrators Association’s Statement of Policy Regarding Real Estate Investment Trusts, as revised and adopted on May 7, 2007 (the “NASAA REIT Guidelines”) and Maryland law. Maryland law and our charter provide that no director or officer shall be liable to us or our stockholders for monetary damages unless the director or officer (1) actually received an improper benefit or profit in money, property or services or (2) was actively and deliberately dishonest as established by a final judgment as material to the cause of action. Moreover, our charter generally requires us to indemnify and advance expenses to our directors and officers for losses they may incur by reason of their service in those capacities unless their act or omission was material to the matter giving rise to the proceeding and was committed in bad faith or was the result of active and deliberate dishonesty, they actually received an improper personal benefit in money, property or services or, in the case of any criminal proceeding, they had reasonable cause to believe the act or omission was unlawful. Further, we have entered into separate indemnification agreements with each of our officers and directors. As a result, you and we may have more limited rights against our directors or officers than might otherwise exist under common law, which could reduce your and our recovery from these persons if they act in a manner that causes us to incur losses. In addition, we are obligated to fund the defense costs incurred by these persons in some cases. However, our charter provides that we may not indemnify our directors or officers, or the Adviser and its affiliates, for any liability or loss suffered by them or hold our directors or officers, the Adviser and its affiliates harmless for any liability or loss suffered by us, unless they have determined, in good faith, that the course of conduct that caused the loss or liability was in our best interests, they were acting on our behalf or performing services for us, the liability or loss was not the result of negligence or misconduct by our non-independent directors, the Adviser and its affiliates, or gross negligence or willful misconduct by our independent directors, and the indemnification or agreement to hold harmless is recoverable only out of our net assets or the proceeds of insurance and not from the stockholders. See “Management—Limited Liability and Indemnification of Directors, Officers, the Adviser and Other Agents” in the Prospectus.

Maryland law limits our stockholders’ ability to amend our charter or dissolve us without the approval of our board of directors.

Although the NASAA REIT Guidelines indicate that stockholders are permitted to amend our charter or terminate us without the necessity for concurrence by our board of directors, we are required to comply with the MGCL, which provides that any amendment to our charter or any dissolution of our company must first be declared advisable by our board of directors. Therefore, our stockholders may vote to authorize the amendment of our charter or the dissolution of our company, but only after such action has been declared advisable by our board of directors. Accordingly, the only proposals to amend our charter or to dissolve our company that will be presented to our stockholders will be those that have been declared advisable by our board of directors and also require approval by our stockholders.

You may experience dilution. Your interest in our assets will also be diluted if the Operating Partnership issues additional units.