The information in this preliminary pricing supplement is not complete and may be changed. This preliminary pricing supplement is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted

Subject to completion dated July 16, 2021

| Pricing supplement To prospectus dated April 8, 2020, prospectus supplement dated April 8, 2020 and product supplement no. 4-II dated November 4, 2020 | Registration Statement Nos. 333-236659 and 333-236659-01 Rule 424(b)(2)

|

| JPMorgan Chase Financial Company LLC |

| Structured Investments | $ Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks due August 2, 2022 Fully and Unconditionally Guaranteed by JPMorgan Chase & Co. |

General

| · | The notes are designed for investors who seek exposure to the performance of the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks, reduced by the Basket Adjustment Factor. The Basket is comprised of unequally weighted Reference Stocks of 33 U.S.-listed companies that may benefit from a positive performance of the consumer discretionary, infrastructure and financials sectors during the term of the notes. Notwithstanding the name of the Basket, there is no guarantee that the Basket will provide exposure to companies positively impacted by COVID-19 international recovery. If the recovery characteristics of the Basket are a factor in your decision to invest in the notes, you should consult with your legal or other advisers before making an investment in the notes. |

| · | Investors should be willing to forgo interest and dividend payments and, if the Basket declines or if the Ending Basket Level does not exceed the Starting Basket Level by approximately 1.78117%, be willing to lose some or all of their principal amount at maturity. |

| · | The notes are unsecured and unsubordinated obligations of JPMorgan Chase Financial Company LLC, which we refer to as JPMorgan Financial, the payment on which is fully and unconditionally guaranteed by JPMorgan Chase & Co. Any payment on the notes is subject to the credit risk of JPMorgan Financial, as issuer of the notes, and the credit risk of JPMorgan Chase & Co., as guarantor of the notes. |

| · | Minimum denominations of $10,000 and integral multiples of $1,000 in excess thereof |

Key Terms

| Issuer: | JPMorgan Chase Financial Company LLC, an indirect, wholly owned finance subsidiary of JPMorgan Chase & Co. |

| Guarantor: | JPMorgan Chase & Co. |

| Basket: | The Basket is comprised of Reference Stocks of 33 U.S.-listed companies (each, a “Reference Stock” and collectively, the “Reference Stocks”). The Bloomberg ticker symbol, issuers of the Reference Stocks, the relevant exchange on which it is listed, the Stock Weight and the Stock Strike Price of each Reference Stock are set forth under “The Basket” on page PS-1 of this pricing supplement. Despite its name, there is no guarantee that the Basket will actually provide exposure to companies positively impacted by COVID-19 international recovery. |

| Payment at Maturity: | Payment at maturity will reflect the performance of the Basket, subject to the Basket Adjustment Factor. Accordingly, at maturity, you will receive an amount per $1,000 principal amount note calculated as follows: $1,000 × (1 + Basket Return) × Basket Adjustment Factor Because the Basket Adjustment Factor is 98.25%, you will lose some or all of your principal amount at maturity if the Basket Return is less than a positive return of approximately 1.78117%. In no event will the Payment at Maturity be less than zero. For more information on how the Basket Adjustment Factor can impact your payment at maturity, please see “What Is the Total Return on the Notes at Maturity, Assuming a Range of Performances for the Basket?” in this pricing supplement. |

| Basket Return: | (Ending Basket Level – Starting Basket Level) Starting Basket Level |

| Basket Adjustment Factor: | 98.25% |

| Starting Basket Level: | Set equal to 100 on the Strike Date |

| Ending Basket Level: | The arithmetic average of the closing levels of the Basket on the Ending Averaging Dates |

| Closing Level of the Basket: | On any Ending Averaging Date, the closing level of the Basket will be calculated as follows: 100 × [1 + sum of (Stock Return of each Reference Stock × Stock Weight of that Reference Stock)] A level of the Basket may be published on the Bloomberg Professional® service (“Bloomberg”) under the Bloomberg ticker “JPPBKBG4”. Any levels so published are for informational purposes only and are not binding in any way with respect to the notes. Although that level may appear under that Bloomberg ticker during the term of the notes, any such level may not be the same as the closing level of the Basket determined by the calculation agent for each Ending Averaging Date. You will not have any rights or claims, whether legal or otherwise, relating to any information regarding that level (whether displayed on Bloomberg or elsewhere) with respect to the notes. |

| Stock Return: | With respect to each Reference Stock, on each Ending Averaging Date: (Final Stock Price – Stock Strike Price) Stock Strike Price |

| Stock Strike Price: | With respect to each Reference Stock, the closing price of one share of that Reference Stock on the Strike Date, as specified in “The Basket” on page PS-1 of this pricing supplement. |

| Final Stock Price: | With respect to each Reference Stock, on any Ending Averaging Date, the closing price of one share of that Reference Stock on that Ending Averaging Date |

| Stock Adjustment Factor: | With respect to each Reference Stock, the Stock Adjustment Factor is referenced in determining the closing price of one share of that Reference Stock and is set initially at 1.0 on the Strike Date. The Stock Adjustment Factor of each Reference Stock is subject to adjustment upon the occurrence of certain corporate events affecting that Reference Stock. See “The Underlyings — Reference Stocks — Anti-Dilution Adjustments” and “The Underlyings — Reference Stocks — Reorganization Events” in the accompanying product supplement for further information. |

| Strike Date | July 15, 2021 |

| Pricing Date: | On or about July 16, 2021 |

| Original Issue Date: | On or about July 21, 2021 (Settlement Date) |

| Ending Averaging Dates*: | July 22, 2022, July 25, 2022, July 26, 2022, July 27, 2022 and July 28, 2022 |

| Maturity Date*: | August 2, 2022 |

| CUSIP: | 48129KBG4 |

| * | Subject to postponement in the event of certain market disruption events and as described under “General Terms of Notes — Postponement of a Determination Date — Notes Linked to Multiple Underlyings” and “General Terms of Notes — Postponement of a Payment Date” in the accompanying product supplement |

Investing in the notes involves a number of risks. See “Risk Factors” beginning on page PS-12 of the accompanying product supplement and “Selected Risk Considerations” beginning on page PS-5 of this pricing supplement.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of the notes or passed upon the accuracy or the adequacy of this pricing supplement or the accompanying product supplement, prospectus supplement and prospectus. Any representation to the contrary is a criminal offense.

| Price to Public (1) | Fees and Commissions (2) | Proceeds to Issuer | |

| Per note | $1,000 | $ | $ |

| Total | $ | $ | $ |

| (1) | See “Supplemental Use of Proceeds” in this pricing supplement for information about the components of the price to public of the notes. |

| (2) | J.P. Morgan Securities LLC, which we refer to as JPMS, acting as agent for JPMorgan Financial, will pay all of the selling commissions it receives from us to other affiliated or unaffiliated dealers. In no event will these selling commissions exceed $7.50 per $1,000 principal amount note. See “Plan of Distribution (Conflicts of Interest)” in the accompanying product supplement. |

If the notes priced today, the estimated value of the notes would be approximately $985.20 per $1,000 principal amount note. The estimated value of the notes, when the terms of the notes are set, will be provided in the pricing supplement and will not be less than $970.00 per $1,000 principal amount note. See “The Estimated Value of the Notes” in this pricing supplement for additional information.

The notes are not bank deposits, are not insured by the Federal Deposit Insurance Corporation or any other governmental agency and are not obligations of, or guaranteed by, a bank.

Additional Terms Specific to the Notes

You may revoke your offer to purchase the notes at any time prior to the time at which we accept such offer by notifying the applicable agent. We reserve the right to change the terms of, or reject any offer to purchase, the notes prior to their issuance. In the event of any changes to the terms of the notes, we will notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes, in which case we may reject your offer to purchase.

You should read this pricing supplement together with the accompanying prospectus, as supplemented by the accompanying prospectus supplement relating to our Series A medium-term notes, of which these notes are a part, and the more detailed information contained in the accompanying product supplement. This pricing supplement, together with the documents listed below, contains the terms of the notes and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, fact sheets, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in the “Risk Factors” section of the accompanying product supplement, as the notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisers before you invest in the notes.

You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| · | Product supplement no. 4-II dated November 4, 2020: https://www.sec.gov/Archives/edgar/data/19617/000095010320021467/crt_dp139322-424b2.pdf |

| · | Prospectus supplement and prospectus, each dated April 8, 2020: https://www.sec.gov/Archives/edgar/data/19617/000095010320007214/crt_dp124361-424b2.pdf |

Our Central Index Key, or CIK, on the SEC website is 1665650, and JPMorgan Chase & Co.’s CIK is 19617. As used in this pricing supplement, “we,” “us” and “our” refer to JPMorgan Financial.

The Basket

The issuer of each Reference Stock, Bloomberg ticker symbol and the relevant exchange on which each Reference Stock is listed and the Stock Weight and the Stock Strike Price of each Reference Stock are set forth below.

| Reference Stock Issuer/Reference Stock | Bloomberg Ticker Symbol | Relevant Exchange | Stock Weight | Stock Strike Price | |

| Ford Motor Company | Common stock, par value $0.01 per share | F UN | New York Stock Exchange | 4.265242% | $14.01 |

| Nucor Corporation | Common stock, par value $0.40 per share | NUE UN | New York Stock Exchange | 4.251969% | $95.42 |

| Deere & Company | Common stock, par value $1.00 per share | DE UN | New York Stock Exchange | 4.057435% | $346.10 |

| Expedia Group, Inc. | Common stock, par value $0.0001 per share | EXPE UW | The NASDAQ Global Select Market | 3.901554% | $169.20 |

| The Goldman Sachs Group, Inc. | Common stock, par value $0.01 per share | GS UN | New York Stock Exchange | 3.817183% | $373.35 |

| Morgan Stanley | Common stock, par value $0.01 per share | MS UN | New York Stock Exchange | 3.783175% | $92.63 |

| American Express Company | Common shares, par value $0.20 per share | AXP UN | New York Stock Exchange | 3.714864% | $172.85 |

| Norwegian Cruise Line Holdings LTD. | Ordinary shares, par value $0.001 per share | NCLH UN | The New York Stock Exchange | 3.516522% | $24.45 |

| Eaton Corporation plc | Ordinary shares, par value $0.01 per share | ETN UN | New York Stock Exchange | 3.375718% | $153.87 |

| Delta Air Lines, Inc. | Common stock, par value $0.0001 per share | DAL UN | New York Stock Exchange | 3.298652% | $41.35 |

| Starbucks Corporation | Common stock, par value $0.001 per share | SBUX UW | Nasdaq Global Select Market | 3.232285% | $118.97 |

| The Walt Disney Company | Common stock, par value $0.01 per share | DIS UN | New York Stock Exchange | 3.220580% | $184.15 |

| Caterpillar Inc. | Common stock, par value $1.00 per share | CAT UN | New York Stock Exchange | 3.162162% | $211.41 |

| Wynn Resorts, Limited | Common stock, par value $0.01 per share | WYNN UW | Nasdaq Global Select Market | 3.059754% | $108.23 |

| Dow Inc. | Common stock, par value $0.01 per share | DOW UN | New York Stock Exchange | 3.013571% | $61.91 |

| Royal Caribbean Cruises LTD | Common stock, par value $0.01 per share | RCL UN | New York Stock Exchange | 3.010873% | $74.21 |

| United Airlines Holdings, Inc. | Common stock, par value $0.01 per share | UAL UW | The NASDAQ Global Select Market | 3.004413% | $47.71 |

| JPMorgan Structured Investments — | PS-1 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| Reference Stock Issuer/Reference Stock | Bloomberg Ticker Symbol | Relevant Exchange | Stock Weight | Stock Strike Price | |

| DuPont de Nemours, Inc. | Common stock, par value $0.01 per share | DD UN | New York Stock Exchange | 2.999035% | $79.55 |

| ConocoPhillips | Common stock, par value $0.01 per share | COP UN | New York Stock Exchange | 2.939165% | $57.08 |

| Exxon Mobil Corporation | Common stock, no par value | XOM UN | New York Stock Exchange | 2.814748% | $58.95 |

| CBRE Group, Inc. | Class A common stock, par value $0.01 per share | CBRE UN | New York Stock Exchange | 2.703012% | $83.50 |

| Citigroup Inc. | Common stock, par value $0.01 per share | C UN | New York Stock Exchange | 2.701001% | $68.45 |

| The Boeing Company | Common stock, par value $5.00 per share | BA UN | New York Stock Exchange | 2.643854% | $222.76 |

| MasterCard Incorporated | Class A common stock, par value $0.0001 per share | MA UN | New York Stock Exchange | 2.630019% | $390.23 |

| Booking Holdings Inc. | Common stock, par value $0.008 per share | BKNG UW | The NASDAQ Global Select Market | 2.617530% | $2,169.39 |

| Visa Inc. | Class A common stock, par value $0.0001 per share | V UN | New York Stock Exchange | 2.607061% | $248.55 |

| Iron Mountain Incorporated | Common stock, par value $0.01 per share | IRM | New York Stock Exchange | 2.603626% | $44.05 |

| The Coca-Cola Company | Common stock, par value $0.25 per share | KO UN | New York Stock Exchange | 2.383495% | $144.71 |

| International Flavors & Fragrances Inc. | Common stock, par value $0.125 per share | IFF | New York Stock Exchange | 2.357137% | $144.00 |

| Chevron Corporation | Common stock, par value $0.75 per share | CVX UN | New York Stock Exchange | 2.321514% | $101.30 |

| Las Vegas Sands Corp. | Common stock, par value $0.001 per share | LVS UN | The New York Stock Exchange | 2.300785% | $56.44 |

| Restaurant Brands International Inc. | Common shares, no par value | QSR UN | New York Stock Exchange | 1.853596% | $63.83 |

| Newell Brands Inc. | Common stock, par value $1.00 per share | NWL UW | Nasdaq Stock Market LLC | 1.838470% | $27.05 |

| JPMorgan Structured Investments — | PS-2 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

What Is the Total Return on the Notes at Maturity, Assuming a Range of Performances for the Basket?

The following table and examples illustrate the hypothetical total return or payment at maturity on the notes. The “total return” as used in this pricing supplement is the number, expressed as a percentage, that results from comparing the payment at maturity per $1,000 principal amount note to $1,000. Each hypothetical total return or payment at maturity set forth below reflects the Basket Adjustment Factor of 98.25% and the Starting Basket Level of 100. Each hypothetical total return or payment at maturity set forth below is for illustrative purposes only and may not be the actual total return or payment at maturity applicable to a purchaser of the notes. The numbers appearing in the following table and examples have been rounded for ease of analysis.

| Ending Basket Level | Basket Return | Total Return |

| 200.00000 | 100.00000% | 96.50000% |

| 190.00000 | 90.00000% | 86.67500% |

| 180.00000 | 80.00000% | 76.85000% |

| 170.00000 | 70.00000% | 67.02500% |

| 150.00000 | 50.00000% | 47.37500% |

| 140.00000 | 40.00000% | 37.55000% |

| 130.00000 | 30.00000% | 27.72500% |

| 120.00000 | 20.00000% | 17.90000% |

| 110.00000 | 10.00000% | 8.07500% |

| 105.00000 | 5.00000% | 3.16250% |

| 101.78117 | 1.78117% | 0.00000% |

| 101.00000 | 1.00000% | -0.76750% |

| 100.00000 | 0.00000% | -1.75000% |

| 95.00000 | -5.00000% | -6.66250% |

| 90.00000 | -10.00000% | -11.57500% |

| 80.00000 | -20.00000% | -21.40000% |

| 70.00000 | -30.00000% | -31.22500% |

| 60.00000 | -40.00000% | -41.05000% |

| 50.00000 | -50.00000% | -50.87500% |

| 40.00000 | -60.00000% | -60.70000% |

| 30.00000 | -70.00000% | -70.52500% |

| 20.00000 | -80.00000% | -80.35000% |

| 10.00000 | -90.00000% | -90.17500% |

| 0.00000 | -100.00000% | -100.00000% |

Hypothetical Examples of Amount Payable at Maturity

The following examples illustrate how the payment at maturity in different hypothetical scenarios is calculated.

Example 1: The level of the Basket increases from the Starting Basket Level of 100.00 to an Ending Basket Level of 105.00. Because the Ending Basket Level of 105.00 is greater than the Starting Basket Level of 100.00 and the Basket Return is 5.00%, the investor receives a payment at maturity of $1,031.625 per $1,000 principal amount note, calculated as follows:

$1,000 × (1 + 5.00%) × 98.25% = $1,031.625

Example 2: The level of the Basket increases from the Starting Basket Level of 100.00 to an Ending Basket Level of 101.00. Although the Ending Basket Level of 101.00 is greater than the Starting Basket Level of 100.00 and the Basket Return is 1.00%, because of the negative effect of the Basket Adjustment Factor, the investor receives a payment at maturity of $992.325 per $1,000 principal amount note, calculated as follows:

$1,000 × (1 + 1.00%) × 98.25% = $992.325

Example 3: The level of the Basket decreases from the Starting Basket Level of 100.00 to an Ending Basket Level of 50.00. Because the Ending Basket Level of 50.00 is less than the Starting Basket Level of 100.00 and the Basket Return is

-50.00%, the investor receives a payment at maturity of $491.25 per $1,000 principal amount note, calculated as follows:

$1,000 × (1 + -50.00%) × 98.25% = $491.25

The hypothetical returns and hypothetical payments on the notes shown above apply only if you hold the notes for their entire term. These hypotheticals do not reflect fees or expenses that would be associated with any sale in the secondary market. If these fees and expenses were included, the hypothetical returns and hypothetical payments shown above would likely be lower.

| JPMorgan Structured Investments — | PS-3 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

Selected Purchase Considerations

| · | UNCAPPED INVESTMENT EXPOSURE TO THE PERFORMANCE OF THE BASKET — The notes provide uncapped exposure to the performance of the Basket, subject to the Basket Adjustment Factor. Because the notes are our unsecured and unsubordinated obligations, the payment of which is fully and unconditionally guaranteed by JPMorgan Chase & Co., payment of any amount on the notes is subject to our ability to pay our obligations as they become due and JPMorgan Chase & Co.’s ability to pay its obligations as they become due. |

| · | RETURN LINKED TO AN UNEQUALLY WEIGHTED BASKET OF 33 REFERENCE STOCKS — The return on the notes is linked to the performance of an unequally weighted Basket that consists of 33 Reference Stocks as set forth under “The Basket” on page PS-1 of this pricing supplement. Notwithstanding the name of the Basket, there is no guarantee that the Basket will provide exposure to companies positively impacted by COVID-19 international recovery. If the recovery characteristics of the Basket are a factor in your decision to invest in the notes, you should consult with your legal or other advisers before making an investment in the notes. |

| · | TAX TREATMENT — You should review carefully the section entitled “Material U.S. Federal Income Tax Consequences” in the accompanying product supplement no. 4-II. The following discussion, when read in combination with that section, constitutes the full opinion of our special tax counsel, Latham & Watkins LLP, regarding the material U.S. federal income tax consequences of owning and disposing of notes. |

Based on current market conditions, in the opinion of our special tax counsel it is reasonable to treat the notes as “open transactions” that are not debt instruments for U.S. federal income tax purposes, as more fully described in “Material U.S. Federal Income Tax Consequences — Tax Consequences to U.S. Holders — Notes Treated as Open Transactions That Are Not Debt Instruments” in the accompanying product supplement. Assuming this treatment is respected, the gain or loss on your notes should be treated as long-term capital gain or loss if you hold your notes for more than a year, whether or not you are an initial purchaser of notes at the issue price. However, the IRS or a court may not respect this treatment, in which case the timing and character of any income or loss on the notes could be materially and adversely affected. You should consult your tax advisor as to the possibility and the tax consequences in that event.

In addition, in 2007 Treasury and the IRS released a notice requesting comments on the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments. The notice focuses in particular on whether to require investors in these instruments to accrue income over the term of their investment. It also asks for comments on a number of related topics, including the character of income or loss with respect to these instruments; the relevance of factors such as the nature of the underlying property to which the instruments are linked; the degree, if any, to which income (including any mandated accruals) realized by non-U.S. investors should be subject to withholding tax; and whether these instruments are or should be subject to the “constructive ownership” regime, which very generally can operate to recharacterize certain long-term capital gain as ordinary income and impose a notional interest charge. While the notice requests comments on appropriate transition rules and effective dates, any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the notes, possibly with retroactive effect. You should consult your tax adviser regarding the U.S. federal income tax consequences of an investment in the notes, including possible alternative treatments and the issues presented by this notice. As discussed in the accompanying product supplement, Section 871(m) of the Code and Treasury regulations promulgated thereunder (“Section 871(m)”) generally impose a 30% withholding tax (or a lower rate under an applicable treaty) on dividend equivalents paid or deemed paid to Non-U.S. Holders with respect to certain financial instruments linked to U.S. equities or indices that include U.S. equities, even in cases where the derivatives do not provide for payments explicitly linked to dividends. Each such linked U.S. stock is an “Underlying Security”. Section 871(m) generally applies to notes that substantially replicate the economic performance of one or more Underlying Securities, as determined upon issuance, based on tests set forth in the applicable Treasury regulations (a “Specified Security”). We intend to treat the notes as Specified Securities and therefore as being subject to Section 871(m). Under the applicable Treasury regulations, the dividend equivalent amount is calculated using a formula that is based on the actual dividends paid with respect to the Underlying Securities (subject to certain assumptions), even if these dividends are not explicitly reflected in determining any payment on the note. We have estimated the implicit dividend equivalent amounts relating to all Underlying Securities with respect to a note as 0.94%. We will treat these amounts as payable quarterly on or before September 30, 2021, on December 31, 2021, on March 31, 2022 and on June 30, 2022, respectively. If you are a non-U.S. Holder, you should expect withholding agents to withhold 30% (or a lower rate under the dividend provision of an applicable income tax treaty) of the estimated implicit dividend equivalent amounts from your payment at maturity, if not sooner, based on the payment schedule listed above. Furthermore, if you sell or otherwise dispose of the notes prior to maturity, you should expect withholding agents to withhold 30% (or lower rate under the dividend provision of an applicable income tax treaty) of any estimated implicit dividend equivalent amounts that have accrued on the notes and that have not already been withheld on. We will not provide any further information concerning the actual dividend equivalent amounts, which may differ from our estimated implicit dividend equivalent amounts. You should consult your tax adviser regarding the application of these rules.

Our determinations (including with respect to the dividend equivalent amount) are generally binding on you, but are not binding on the IRS, and the IRS may disagree with our determinations. Section 871(m) is complex and its application may depend on your particular circumstances. You should consult your tax adviser regarding the application of Section 871(m) to the notes.

Withholding under legislation commonly referred to as “FATCA” may (if the notes are recharacterized as debt instruments) apply to amounts treated as interest paid with respect to the notes, as well as to payments of gross

| JPMorgan Structured Investments — | PS-4 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

proceeds of a taxable disposition, including redemption at maturity, of a note although under recently proposed regulations (the preamble to which specifies that taxpayers are permitted to rely on them pending finalization), no withholding will apply to payments of gross proceeds (other than any amount treated as interest). You should consult your tax adviser regarding the potential application of FATCA to the notes.

We will not pay any additional amounts with respect to any withholding tax.

Selected Risk Considerations

An investment in the notes involves significant risks. Investing in the notes is not equivalent to investing directly in the Basket or any of the Reference Stocks. These risks are explained in more detail in the “Risk Factors” section of the accompanying product supplement.

Risks Relating to the Notes Generally

| · | YOUR INVESTMENT IN THE NOTES MAY RESULT IN A LOSS — The notes do not guarantee any return of your principal. The amount payable at maturity, if any, will reflect the performance of the Reference Stocks, subject to a reduction by the Basket Adjustment Factor. Because the Basket Adjustment Factor reduces the Basket Return, if the Ending Basket Level does not exceed the Starting Basket Level by at least approximately 1.78117%, you will lose some or all of your principal amount at maturity. |

| · | THE BASKET ADJUSTMENT FACTOR WILL DIMINISH ANY INCREASE IN THE VALUE OF THE BASKET AND MAGNIFY ANY DECLINE IN THE VALUE OF THE BASKET — If the Basket Return is negative or is less than a positive return of approximately 1.78117%, at maturity, you will lose some or all of your principal amount. In addition, the Basket Adjustment Factor will diminish any increase in the value of the Basket and magnify any decline in the value of the Basket. For each 1% that the Ending Basket Level is greater than the Starting Basket Level, the return on your principal amount will increase by less than 1%. In addition, for each 1% that the Ending Basket Level is less than the Starting Basket Level, you will lose more than 1% of your principal amount, provided that the payment at maturity will not be less than zero. |

| · | CREDIT RISKS OF JPMORGAN FINANCIAL AND JPMORGAN CHASE & CO. — The notes are subject to our and JPMorgan Chase & Co.’s credit risks, and our and JPMorgan Chase & Co.’s credit ratings and credit spreads may adversely affect the market value of the notes. Investors are dependent on our and JPMorgan Chase & Co.’s ability to pay all amounts due on the notes. Any actual or potential change in our or JPMorgan Chase & Co.’s creditworthiness or credit spreads, as determined by the market for taking that credit risk, is likely to adversely affect the value of the notes. If we and JPMorgan Chase & Co. were to default on our payment obligations, you may not receive any amounts owed to you under the notes and you could lose your entire investment. |

| · | AS A FINANCE SUBSIDIARY, JPMORGAN FINANCIAL HAS NO INDEPENDENT OPERATIONS AND HAS LIMITED ASSETS — As a finance subsidiary of JPMorgan Chase & Co., we have no independent operations beyond the issuance and administration of our securities. Aside from the initial capital contribution from JPMorgan Chase & Co., substantially all of our assets relate to obligations of our affiliates to make payments under loans made by us or other intercompany agreements. As a result, we are dependent upon payments from our affiliates to meet our obligations under the notes. If these affiliates do not make payments to us and we fail to make payments on the notes, you may have to seek payment under the related guarantee by JPMorgan Chase & Co., and that guarantee will rank pari passu with all other unsecured and unsubordinated obligations of JPMorgan Chase & Co. |

| · | CORRELATION (OR LACK OF CORRELATION) OF THE REFERENCE STOCKS — The notes are linked to an unequally weighted Basket consisting of 33 Reference Stocks. Price movements of the Reference Stocks may or may not be correlated with each other. At a time when the value of one or more of the Reference Stocks increases, the value of the other Reference Stocks may not increase as much or may even decline. Therefore, in calculating the Ending Basket Level, increases in the value of one or more of the Reference Stocks may be moderated, or more than offset, by the lesser increases or declines in the values of the other Reference Stocks. In addition, high correlation of movements in the values of the Reference Stocks during periods of negative returns among the Reference Stocks could have an adverse effect on the payment at maturity on the notes. There can be no assurance that the Ending Basket Level will be higher than the Starting Basket Level. |

| · | NO OWNERSHIP OR DIVIDEND RIGHTS IN THE REFERENCE STOCKS — As a holder of the notes, you will not have any ownership interest or rights in any of the Reference Stocks, such as voting rights or dividend payments. In addition, the issuers of the Reference Stocks will not have any obligation to consider your interests as a holder of the notes in taking any corporate action that might affect the value of the relevant Reference Stocks and the notes. |

| · | NO AFFILIATION WITH THE REFERENCE STOCK ISSUERS — We are not affiliated with the issuers of the Reference Stocks. We assume no responsibility for the adequacy of the information about the Reference Stock issuers contained in this pricing supplement. You should undertake your own investigation into the Reference Stocks and their issuers. We are not responsible for the Reference Stock issuers’ public disclosure of information, whether contained in SEC filings or otherwise. |

| · | LACK OF LIQUIDITY — The notes will not be listed on any securities exchange. JPMS intends to offer to purchase the notes in the secondary market but is not required to do so. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the notes easily. Because other dealers are not likely to make a secondary market for the notes, the price at which you may be able to trade your notes is likely to depend on the price, if any, at which JPMS is willing to buy the notes. |

| · | NO INTEREST PAYMENTS — As a holder of the notes, you will not receive any interest payments. |

| JPMorgan Structured Investments — | PS-5 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| · | THE FINAL TERMS AND VALUATION OF THE NOTES WILL BE PROVIDED IN THE PRICING SUPPLEMENT — The final terms of the notes will be based on relevant market conditions when the terms of the notes are set and will be provided in the pricing supplement. In particular, the estimated value of the notes will be provided in the pricing supplement and may be as low as the minimum for the estimated value of the notes set forth on the cover of this pricing supplement. Accordingly, you should consider your potential investment in the notes based on the minimum for the estimated value of the notes. |

Risks Relating to Conflicts of Interest

| · | POTENTIAL CONFLICTS — We and our affiliates play a variety of roles in connection with the issuance of the notes, including acting as calculation agent and as an agent of the offering of the notes, hedging our obligations under the notes and making the assumptions used to determine the pricing of the notes and the estimated value of the notes when the terms of the notes are set, which we refer to as the estimated value of the notes. In performing these duties, our and JPMorgan Chase & Co.’s economic interests and the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the notes. In addition, our and JPMorgan Chase & Co.’s business activities, including hedging and trading activities, could cause our and JPMorgan Chase & Co.’s economic interests to be adverse to yours and could adversely affect any payment on the notes and the value of the notes. It is possible that hedging or trading activities of ours or our affiliates in connection with the notes could result in substantial returns for us or our affiliates while the value of the notes declines. Please refer to “Risk Factors — Risks Relating to Conflicts of Interest” in the accompanying product supplement for additional information about these risks. |

We and/or our affiliates may also currently or from time to time engage in business with the Reference Stock issuers, including extending loans to, or making equity investments in, the Reference Stock issuers or providing advisory services to the Reference Stock issuers. In addition, one or more of our affiliates may publish research reports or otherwise express opinions with respect to the Reference Stock issuers, and these reports may or may not recommend that investors buy or hold the Reference Stocks. As a prospective purchaser of the notes, you should undertake an independent investigation of the Reference Stock issuers that in your judgment is appropriate to make an informed decision with respect to an investment in the notes.

Risks Relating to the Estimated Value and Secondary Market Prices of the Notes

| · | THE ESTIMATED VALUE OF THE NOTES WILL BE LOWER THAN THE ORIGINAL ISSUE PRICE (PRICE TO PUBLIC) OF THE NOTES — The estimated value of the notes is only an estimate determined by reference to several factors. The original issue price of the notes will exceed the estimated value of the notes because costs associated with selling, structuring and hedging the notes are included in the original issue price of the notes. These costs include the selling commissions, the projected profits, if any, that our affiliates expect to realize for assuming risks inherent in hedging our obligations under the notes and the estimated cost of hedging our obligations under the notes. See “The Estimated Value of the Notes” in this pricing supplement. |

| · | THE ESTIMATED VALUE OF THE NOTES DOES NOT REPRESENT FUTURE VALUES OF THE NOTES AND MAY DIFFER FROM OTHERS’ ESTIMATES — The estimated value of the notes is determined by reference to internal pricing models of our affiliates when the terms of the notes are set. This estimated value of the notes is based on market conditions and other relevant factors existing at that time and assumptions about market parameters, which can include volatility, dividend rates, interest rates and other factors. Different pricing models and assumptions could provide valuations for the notes that are greater than or less than the estimated value of the notes. In addition, market conditions and other relevant factors in the future may change, and any assumptions may prove to be incorrect. On future dates, the value of the notes could change significantly based on, among other things, changes in market conditions, our or JPMorgan Chase & Co.’s creditworthiness, interest rate movements and other relevant factors, which may impact the price, if any, at which JPMS would be willing to buy notes from you in secondary market transactions. See “The Estimated Value of the Notes” in this pricing supplement. |

| · | THE ESTIMATED VALUE OF THE NOTES IS DERIVED BY REFERENCE TO AN INTERNAL FUNDING RATE — The internal funding rate used in the determination of the estimated value of the notes may differ from the market-implied funding rate for vanilla fixed income instruments of a similar maturity issued by JPMorgan Chase & Co. or its affiliates. Any difference may be based on, among other things, our and our affiliates’ view of the funding value of the notes as well as the higher issuance, operational and ongoing liability management costs of the notes in comparison to those costs for the conventional fixed income instruments of JPMorgan Chase & Co. This internal funding rate is based on certain market inputs and assumptions, which may prove to be incorrect, and is intended to approximate the prevailing market replacement funding rate for the notes. The use of an internal funding rate and any potential changes to that rate may have an adverse effect on the terms of the notes and any secondary market prices of the notes. See “The Estimated Value of the Notes” in this pricing supplement. |

| · | THE VALUE OF THE NOTES AS PUBLISHED BY JPMS (AND WHICH MAY BE REFLECTED ON CUSTOMER ACCOUNT STATEMENTS) MAY BE HIGHER THAN THE THEN-CURRENT ESTIMATED VALUE OF THE NOTES FOR A LIMITED TIME PERIOD — We generally expect that some of the costs included in the original issue price of the notes will be partially paid back to you in connection with any repurchases of your notes by JPMS in an amount that will decline to zero over an initial predetermined period. These costs can include selling commissions, projected hedging profits, if any, and, in some circumstances, estimated hedging costs and our internal secondary market funding rates for structured debt issuances. See “Secondary Market Prices of the Notes” in this pricing supplement for additional information relating to this initial period. Accordingly, the estimated value of your notes during this initial period may be lower than the value of |

| JPMorgan Structured Investments — | PS-6 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

the notes as published by JPMS (and which may be shown on your customer account statements).

| · | SECONDARY MARKET PRICES OF THE NOTES WILL LIKELY BE LOWER THAN THE ORIGINAL ISSUE PRICE OF THE NOTES — Any secondary market prices of the notes will likely be lower than the original issue price of the notes because, among other things, secondary market prices take into account our internal secondary market funding rates for structured debt issuances and, also, because secondary market prices may exclude selling commissions, projected hedging profits, if any, and estimated hedging costs that are included in the original issue price of the notes. As a result, the price, if any, at which JPMS will be willing to buy notes from you in secondary market transactions, if at all, is likely to be lower than the original issue price. Any sale by you prior to the Maturity Date could result in a substantial loss to you. See the immediately following risk consideration for information about additional factors that will impact any secondary market prices of the notes. |

The notes are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your notes to maturity. See “— Lack of Liquidity” below.

| · | SECONDARY MARKET PRICES OF THE NOTES WILL BE IMPACTED BY MANY ECONOMIC AND MARKET FACTORS — The secondary market price of the notes during their term will be impacted by a number of economic and market factors, which may either offset or magnify each other, aside from the selling commissions, projected hedging profits, if any, estimated hedging costs and the price of one share of each Reference Stock. |

Additionally, independent pricing vendors and/or third party broker-dealers may publish a price for the notes, which may also be reflected on customer account statements. This price may be different (higher or lower) than the price of the notes, if any, at which JPMS may be willing to purchase your notes in the secondary market. See “Risk Factors — Risks Relating to the Estimated Value and Secondary Market Prices of the Notes — Secondary market prices of the notes will be impacted by many economic and market factors” in the accompanying product supplement.

Risks Relating to the Basket

| · | LIMITED TRADING HISTORY — Certain of the Reference Stocks have limited trading history. On March 20, 2019, The Walt Disney Company acquired all of the outstanding shares of Twenty-First Century Fox, Inc. and TWDC Enterprises 18 Corp. (formerly known as The Walt Disney Company) (“Legacy Disney”), and The Walt Disney Company became the successor SEC registrant to Legacy Disney. On April 1, 2019, DuPont de Nemours, Inc. completed the separation of its materials science business as a result of which Dow Inc. became the parent company of, and the SEC successor registrant to, The Dow Chemical Company. The common stock of Dow Inc. commenced trading on the New York Stock Exchange on April 2, 2019 and therefore has limited historical performance. Accordingly, historical information for each of these Reference Stocks is available only since the applicable date listed above. Past performance should not be considered indicative of future performance. |

| · | THE ANTI-DILUTION PROTECTION FOR THE REFERENCE STOCKS IS LIMITED AND MAY BE DISCRETIONARY — The calculation agent will make adjustments to the Stock Adjustment Factor for each Reference Stock for certain corporate events affecting that Reference Stock. However, the calculation agent will not make an adjustment in response to all events that could affect each Reference Stock. If an event occurs that does not require the calculation agent to make an adjustment, the value of the notes may be materially and adversely affected. You should also be aware that the calculation agent may make adjustments in response to events that are not described in the accompanying product supplement to account for any diluting or concentrative effect, but the calculation agent is under no obligation to do so or to consider your interests as a holder of the notes in making these determinations. |

| · | THE INVESTMENT STRATEGY REPRESENTED BY THE BASKET MAY NOT BE SUCCESSFUL — The Basket is comprised of the Reference Stocks of 33 U.S.-listed companies that may provide exposure to companies positively impacted by COVID-19 international recovery during the term of the note. You should undertake your own investigation into each Reference Stock and its issuer, and you should make your own determination as to the potential performance of the consumer discretionary, infrastructure and financials sectors as represented by the Basket of Reference Stocks during the term of the note. There can be no assurance that the Basket Return will be positive during the term of the notes. It is possible that the investment strategy represented by the Basket will not be successful and that the level of the Basket and the Basket Return will be adversely affected. Moreover, there can be no assurance that the Reference Stocks will outperform other U.S.-listed companies positively impacted by COVID-19 international recovery. |

| · | THE REFERENCE STOCKS ARE CONCENTRATED IN THE CONSUMER DISCRETIONARY, INFRASTRUCTURE AND FINANCIALS SECTORS — A substantial portion of the Reference Stocks has been issued by companies whose business is associated with the consumer discretionary, infrastructure or financials sector. Because the value of the notes is determined by the performance of the Basket consisting of the Reference Stocks, an investment in these notes will be concentrated in these sectors. As a result, the value of the notes may be subject to greater volatility and be more adversely affected by a single positive or negative economic, political or regulatory occurrence affecting these sectors than a different investment linked to securities of a more broadly diversified group of issuers. |

| · | NON-SECURITIES RISK — Each of the common shares of Restaurant Brands International Inc., the common stock of Royal Caribbean Cruises Ltd. and the ordinary shares of Norwegian Cruise Line Holdings Ltd. and Eaton Corporation plc have been issued by a non-U.S. company. Investments in securities linked to the value of such non-U.S. equity securities involve risks associated with the home countries of the issuers of those non-U.S. equity securities. |

| JPMorgan Structured Investments — | PS-7 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| · | IN SOME CIRCUMSTANCES, THE PAYMENT YOU RECEIVE ON THE NOTES MAY BE BASED ON THE VALUE OF CASH, SECURITIES (INCLUDING SECURITIES OF OTHER ISSUERS) OR OTHER PROPERTY DISTRIBUTED TO HOLDERS OF A REFERENCE STOCK UPON THE OCCURRENCE OF A REORGANIZATION EVENT — Following certain corporate events relating to a Reference Stock where its issuer is not the surviving entity, a liquidation of a Reference Stock issuer or other reorganization events affect a Reference Stock issuer as described in the accompanying product supplement, a portion of any payment on the notes may be based on the common stock (or other security) of a successor to that Reference Stock issuer or any cash or any other assets distributed to holders of that Reference Stock in the relevant corporate event. The occurrence of these corporate events and the consequent adjustments may materially and adversely affect the value of the notes. The specific corporate events that can lead to these adjustments and the procedures for selecting the Exchange Property (as defined in the accompanying product supplement) are described in the accompanying product supplement. |

| JPMorgan Structured Investments — | PS-8 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

The Basket and the Reference Stocks

Public Information

All information contained in this pricing supplement on the Reference Stocks and on the Reference Stock issuers is derived from publicly available sources, without independent verification. Each Reference Stock is registered under the Securities Exchange Act of 1934, as amended, which we refer to as the Exchange Act, and is listed on the exchange provided in the table below, which we refer to as the relevant exchange for purposes of that Reference Stock in the accompanying product supplement. Information provided to or filed with the SEC by a Reference Stock issuer pursuant to the Exchange Act can be located by reference to the SEC file number provided in the table below, and can be accessed through www.sec.gov.

We do not make any representation that these publicly available documents are accurate or complete. We obtained the closing prices below from Bloomberg, without independent verification. The closing prices below may have been adjusted by Bloomberg for corporate actions, such as stock splits, public offerings, mergers and acquisitions, spin-offs, delistings and bankruptcy.

| Bloomberg Ticker Symbol | Reference Stock Issuer/Reference Stock | Relevant Exchange | SEC File Number | Closing Price on July 15, 2021 | |

| AXP UN | American Express Company | Common shares, par value $0.20 per share | New York Stock Exchange | 001-7657 | $172.85 |

| BA UN | The Boeing Company | Common stock, par value $5.00 per share | New York Stock Exchange | 001-442 | $222.76 |

| BKNG UW | Booking Holdings Inc. | Common stock, par value $0.008 per share | The NASDAQ Global Select Market | 001-36691 | $2,169.39 |

| C UN | Citigroup Inc. | Common stock, par value $0.01 per share | New York Stock Exchange | 001-9924 | $68.45 |

| CAT UN | Caterpillar Inc. | Common stock, par value $1.00 per share | New York Stock Exchange | 001-768 | $211.41 |

| CBRE UN | CBRE Group, Inc. | Class A common stock, par value $0.01 per share | New York Stock Exchange | 001-32205 | $83.50 |

| COP UN | ConocoPhillips | Common stock, par value $0.01 per share | New York Stock Exchange | 001-32395 | $57.08 |

| CVX UN | Chevron Corporation | Common stock, par value $0.75 per share | New York Stock Exchange | 001-00368 | $101.30 |

| DAL UN | Delta Air Lines, Inc. | Common stock, par value $0.0001 per share | New York Stock Exchange | 001-5424 | $41.35 |

| DD UN | DuPont de Nemours, Inc. | Common stock, par value $0.01 per share | New York Stock Exchange | 001-38196 | $79.55 |

| DE UN | Deere & Company | Common stock, par value $1.00 per share | New York Stock Exchange | 001-4121 | $346.10 |

| DIS UN | The Walt Disney Company | Common stock, par value $0.01 per share | New York Stock Exchange | 001-38842 | $184.15 |

| DOW UN | Dow Inc. | Common stock, par value $0.01 per share | New York Stock Exchange | 001-38646 | $61.91 |

| ETN UN | Eaton Corporation plc | Ordinary shares, par value $0.01 per share | New York Stock Exchange | 000-54863 | $153.87 |

| EXPE UW | Expedia Group, Inc. | Common stock, par value $0.0001 per share | The NASDAQ Global Select Market | 001-37429 | $169.20 |

| F UN | Ford Motor Company | Common stock, par value $0.01 per share | New York Stock Exchange | 001-3950 | $14.01 |

| GS UN | The Goldman Sachs Group, Inc. | Common stock, par value $0.01 per share | New York Stock Exchange | 001-14965 | $373.35 |

| IFF | International Flavors & Fragrances Inc. | Common stock, par value $0.125 per share | New York Stock Exchange | 001-4858 | $144.00 |

| IRM | Iron Mountain Incorporated | Common stock, par value $0.01 per share | New York Stock Exchange | 001-13045 | $44.05 |

| KO UN | The Coca-Cola Company | Common stock, par value $0.25 per share | New York Stock Exchange | 001-02217 | $144.71 |

| LVS UN | Las Vegas Sands Corp. | Common stock, par value $0.001 per share | The New York Stock Exchange | 001-32373 | $56.44 |

| MA UN | MasterCard Incorporated | Class A common stock, par value $0.0001 per share | New York Stock Exchange | 001-32877 | $390.23 |

| MS UN | Morgan Stanley | Common stock, par value $0.01 per share | New York Stock Exchange | 001-11758 | $92.63 |

| NCLH UN | Norwegian Cruise Line Holdings LTD. | Ordinary shares, par value $0.001 per share | The New York Stock Exchange | 001-35784 | $24.45 |

| NUE UN | Nucor Corporation | Common stock, par value $0.40 per share | New York Stock Exchange | 001-4119 | $95.42 |

| NWL UW | Newell Brands Inc. | Common stock, par value $1.00 per share | Nasdaq Stock Market LLC | 001-9608 | $27.05 |

| JPMorgan Structured Investments — | PS-9 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| Bloomberg Ticker Symbol | Reference Stock Issuer/Reference Stock | Relevant Exchange | SEC File Number | Closing Price on July 15, 2021 | |

| QSR UN | Restaurant Brands International Inc. | Common shares, no par value | New York Stock Exchange | 001-36786 | $63.83 |

| RCL UN | Royal Caribbean Cruises LTD | Common stock, par value $0.01 per share | New York Stock Exchange | 001-11884 | $74.21 |

| SBUX UW | Starbucks Corporation | Common stock, par value $0.001 per share | Nasdaq Global Select Market | 000-20322 | $118.97 |

| UAL UW | United Airlines Holdings, Inc. | Common stock, par value $0.01 per share | The NASDAQ Global Select Market | 001-06033 | $47.71 |

| V UN | Visa Inc. | Class A common stock, par value $0.0001 per share | New York Stock Exchange | 001-33977 | $248.55 |

| WYNN UW | Wynn Resorts, Limited | Common stock, par value $0.01 per share | Nasdaq Global Select Market | 000-50028 | $108.23 |

| XOM UN | Exxon Mobil Corporation | Common stock, no par value | New York Stock Exchange | 001-2256 | $58.95 |

According to publicly available filings of the relevant Reference Stock issuer with the SEC:

| · | American Express Company is a globally integrated payments company whose principal products and services are credit and charge card products, along with travel and lifestyle related services, offered to customers and businesses around the world.. |

| · | The Boeing Company is a major aerospace firm. |

| · | Booking Holdings Inc. connects consumers wishing to make travel reservations with providers of travel services around the world through its online platforms. |

| · | Citigroup Inc. is a global diversified financial services holding company whose businesses provide consumers, corporations, governments and institutions with a broad, yet focused, range of financial products and services, including consumer banking and credit, corporate and investment banking, securities brokerage, trade and securities services and wealth management. |

| · | Caterpillar is a manufacturer of construction and mining equipment, diesel and natural gas engines, industrial gas turbines and diesel-electric locomotives. The company principally operates through its three primary segments - Construction Industries, Resource Industries and Energy & Transportation - and also provides financing and related services through its Financial Products segment. |

| · | CBRE Group, Inc. is a commercial real estate services and investment firm. |

| · | ConocoPhillips is an independent E&P company. |

| · | Chevron Corporation manages its investments in subsidiaries and affiliates and provides administrative, financial, management and technology support to U.S. and international subsidiaries that engage in integrated energy and chemicals operations. |

| · | Delta Air Lines, Inc. provides scheduled air transportation for passengers and cargo throughout the United States and around the world. |

| · | DuPont de Nemours, Inc. is a global innovation company with technology-based materials and solutions that help transform industries and everyday life by applying diverse science and expertise to help customers advance their best ideas and deliver essential innovations in key markets including electronics, transportation, building and construction, healthcare and worker safety. |

| · | Deere & Company manufactures and distributes a line of agriculture and turf equipment and related service parts and a range of machines and service parts used in construction, earthmoving, road building, material handling and timber harvesting. In addition, Deere & Company finances sales and leases by dealers of new and used agriculture and turf equipment and construction and forestry equipment, provides wholesale financing to dealers of the foregoing equipment, finances retail revolving charge accounts and offers extended equipment warranties. |

| · | The Walt Disney Company is an entertainment company with operations in media networks; parks, experiences and products; studio entertainment; and direct-to-consumer and international products. On March 20, 2019, The Walt Disney Company acquired all of the outstanding shares of Twenty-First Century Fox, Inc. and TWDC Enterprises 18 Corp. (formerly known as The Walt Disney Company) (“Legacy Disney”), and The Walt Disney Company became the successor SEC registrant to Legacy Disney. |

| · | Dow Inc. combines global breadth, asset integration and scale, focused innovation and leading business positions to achieve profitable growth. |

| · | Eaton Corporation plc is a power management company. They provide sustainable solutions that help their customers effectively manage electrical, hydraulic and mechanical power. |

| · | Expedia Group, Inc. is an online travel company that provides travel products and services to leisure and corporate travelers in the United States and abroad as well as various media and advertising offerings to travel and non-travel advertisers. |

| · | Ford Motor Company designs, manufactures, markets and services a line of Ford cars, trucks, sport utility vehicles, electrified vehicles and Lincoln luxury vehicles, provides financial services through Ford Motor Credit Company LLC, and is pursuing positions in electrification; mobility solutions, including self-driving services; and connected vehicle services. |

| · | The Goldman Sachs Group, Inc. is a financial institution that delivers a broad range of financial services across investment banking, securities, investment management and consumer banking to a large and diversified client base that includes corporations, financial institutions, governments and individuals. |

| · | International Flavors & Fragrances Inc. is a creator and manufacturer of taste, scent and complementary adjacent products, including cosmetic active and natural health ingredients, which are used in a variety of consumer products. |

| · | Iron Mountain Incorporated helps organizations around the world protect their information, reduce storage costs, comply with regulations, facilitate corporate disaster recovery, and better use their information and IT infrastructure for business advantages, regardless of its format, location or life cycle stage. |

| · | The Coca-Cola Company is a total beverage company with products sold in more than 200 countries and territories. |

| · | Las Vegas Sands Corp. is a global developer of destination properties that feature premium accommodations, world-class gaming, entertainment and retail malls, convention and exhibition facilities, celebrity chef restaurants and other amenities. |

| JPMorgan Structured Investments — | PS-10 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| · | MasterCard Incorporated is a technology company in the global payments industry that connects consumers, financial institutions, merchants, governments, digital partners, businesses and other organizations worldwide, enabling them to use electronic forms of payment instead of cash and checks. |

| · | Morgan Stanley is a global financial services firm that, through their subsidiaries and affiliates, advises, and originates, trades, manages and distributes capital for, governments, institutions and individuals. |

| · | Norwegian Cruise Line Holdings LTD., a Bermudan company, is a global cruise company that operates the Norwegian Cruise Line, Oceania Cruises and Regent Seven Seas Cruises brands. |

| · | Nucor Corporation and its subsidiaries manufacture and sell steel and steel products. Nucor Corporation is also a United States recycler, using scrap steel as the primary material in producing its products. |

| · | Newell Brands Inc. is a consumer goods company with a portfolio of brands, including Rubbermaid®, Paper Mate®, Sharpie®, Dymo®, EXPO®, Parker®, Elmer’s®, Coleman®, Marmot®, Oster®, Sunbeam®, FoodSaver®, Mr. Coffee®, Rubbermaid Commercial Products®, Graco®, Baby Jogger®, NUK®, Calphalon®, Contigo®, First Alert®, Mapa®, Spontex® and Yankee Candle®. |

| · | Restaurant Brands International Inc., a Canadian company, is a quick service restaurant company that franchises or owns restaurants. |

| · | Royal Caribbean Cruises LTD., a Liberian company, is a cruise company that controls and operates four global cruise brands: Royal Caribbean International, Celebrity Cruises, Azamara and Silversea Cruises. |

| · | Starbucks Corporation is a roaster, marketer and retailer of specialty coffee. |

| · | United Airlines Holdings, Inc. (formerly known as United Continental Holdings, Inc.) transports people and cargo through its mainline and regional operations. |

| · | Visa Inc. facilitates digital payments across more than 200 countries and territories among a global set of consumers, merchants, financial institutions, businesses, strategic partners and government entities through innovative technologies. |

| · | Wynn Resorts, Limited is a designer, developer and operator of integrated resorts featuring hotel rooms, retail space, dining and entertainment options, meeting and convention facilities and gaming. |

| · | Exxon Mobil Corporation's principal business involves exploration for, and production of, crude oil and natural gas and manufacture, trade, transport and sale of crude oil, natural gas, petroleum products, petrochemicals and a wide variety of specialty products. |

| JPMorgan Structured Investments — | PS-11 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

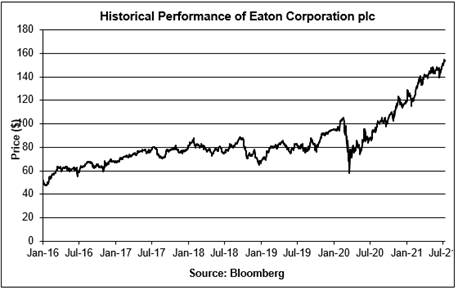

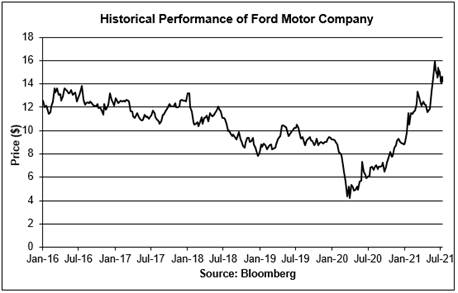

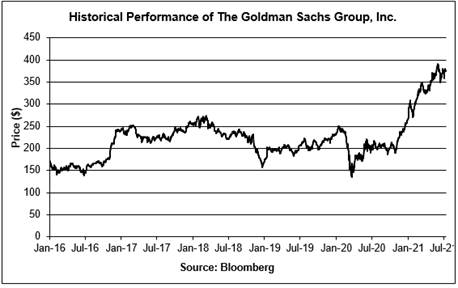

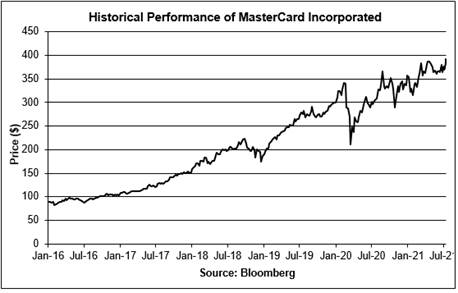

Historical Information Regarding the Basket and the Reference Stocks

The following graphs show the historical weekly performance of the Basket as a whole from April 2, 2019 through July 9, 2021, as well as the Reference Stocks (other than the common stock of Dow Inc.) from January 4, 2016 through July 9, 2021 and the common stock of Dow Inc. from April 2, 2019 through July 9, 2021. The graph of the historical Basket performance assumes the closing level of the Basket on April 2, 2019 was 100 and the Stock Weights were as specified under “The Basket” in this pricing supplement.

We obtained the various closing prices below from the Bloomberg Professional® service (“Bloomberg”), without independent verification. The closing prices may have been adjusted by Bloomberg for corporate actions such as stock splits, public offerings, mergers and acquisitions, spin-offs, delistings and bankruptcy.

Since the commencement of trading of each Reference Stock, the price of that Reference Stock has experienced significant fluctuations. The historical performance of each Reference Stock and the historical performance of the Basket should not be taken as an indication of future performance, and no assurance can be given as to the closing prices of each Reference Stock or the levels of the Basket on the Strike Date, the Pricing Date or any Ending Averaging Date. There can be no assurance that the performance of the Basket will result in the return of any of your principal amount.

| JPMorgan Structured Investments — | PS-12 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| JPMorgan Structured Investments — | PS-13 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| JPMorgan Structured Investments — | PS-14 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| JPMorgan Structured Investments — | PS-15 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

†The vertical dotted line in the graph indicates March 20, 2019. In the graph, the performance to the left of the vertical dotted line reflects the common stock of legacy Disney and the performance to the right of the vertical dotted line reflects the common stock of The Walt Disney Company.

| JPMorgan Structured Investments — | PS-16 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| JPMorgan Structured Investments — | PS-17 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| JPMorgan Structured Investments — | PS-18 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| JPMorgan Structured Investments — | PS-19 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| JPMorgan Structured Investments — | PS-20 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| JPMorgan Structured Investments — | PS-21 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| JPMorgan Structured Investments — | PS-22 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

| JPMorgan Structured Investments — | PS-23 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

The Estimated Value of the Notes

The estimated value of the notes set forth on the cover of this pricing supplement is equal to the sum of the values of the following hypothetical components: (1) a fixed-income debt component with the same maturity as the notes, valued using the internal funding rate described below, and (2) the derivative or derivatives underlying the economic terms of the notes. The estimated value of the notes does not represent a minimum price at which JPMS would be willing to buy your notes in any secondary market (if any exists) at any time. The internal funding rate used in the determination of the estimated value of the notes may differ from the market-implied funding rate for vanilla fixed income instruments of a similar maturity issued by JPMorgan Chase & Co. or its affiliates. Any difference may be based on, among other things, our and our affiliates’ view of the funding value of the notes as well as the higher issuance, operational and ongoing liability management costs of the notes in comparison to those costs for the conventional fixed income instruments of JPMorgan Chase & Co. This internal funding rate is based on certain market inputs and assumptions, which may prove to be incorrect, and is intended to approximate the prevailing market replacement funding rate for the notes. The use of an internal funding rate and any potential changes to that rate may have an adverse effect on the terms of the notes and any secondary market prices of the notes. For additional information, see “Selected Risk Considerations — The Estimated Value of the Notes Is Derived by Reference to an Internal Funding Rate” in this pricing supplement. The value of the derivative or derivatives underlying the economic terms of the notes is derived from internal pricing models of our affiliates. These models are dependent on inputs such as the traded market prices of comparable derivative instruments and on various other inputs, some of which are market-observable, and which can include volatility, dividend rates, interest rates and other factors, as well as assumptions about future market events and/or environments. Accordingly, the estimated value of the notes is determined when the terms of the notes are set based on market conditions and other relevant factors and assumptions existing at that time. See “Selected Risk Considerations — The Estimated Value of the Notes Does Not Represent Future Values of the Notes and May Differ from Others’ Estimates” in this pricing supplement.

The estimated value of the notes will be lower than the original issue price of the notes because costs associated with selling, structuring and hedging the notes are included in the original issue price of the notes. These costs include the selling commissions paid to JPMS and other affiliated or unaffiliated dealers, the projected profits, if any, that our affiliates expect to realize for assuming risks inherent in hedging our obligations under the notes and the estimated cost of hedging our obligations under the notes. Because hedging our obligations entails risk and may be influenced by market forces beyond our control, this hedging may result in a profit that is more or less than expected, or it may result in a loss. We or one or more of our affiliates will retain any profits realized in hedging our obligations under the notes. See “Selected Risk Considerations — The Estimated Value of the Notes Will Be Lower Than the Original Issue Price (Price to Public) of the Notes” in this pricing supplement.

Secondary Market Prices of the Notes

For information about factors that will impact any secondary market prices of the notes, see “Risk Factors — Risks Relating to the Estimated Value and Secondary Market Prices of the Notes — Secondary market prices of the notes will be impacted by many economic and market factors” in the accompanying product supplement. In addition, we generally expect that some of the costs included in the original issue price of the notes will be partially paid back to you in connection with any repurchases of your notes by JPMS in an amount that will decline to zero over an initial predetermined period. These costs can include selling commissions, projected hedging profits, if any, and, in some circumstances, estimated hedging costs and our internal secondary market funding rates for structured debt issuances. This initial predetermined time period is intended to be the shorter of six months and one-half of the stated term of the notes. The length of any such initial period reflects the structure of the notes, whether our affiliates expect to earn a profit in connection with our hedging activities, the estimated costs of hedging the notes and when these costs are incurred, as determined by our affiliates. See “Selected Risk Considerations — The Value of the Notes as Published by JPMS (and Which May Be Reflected on Customer Account Statements) May Be Higher Than the Then-Current Estimated Value of the Notes for a Limited Time Period” in this pricing supplement.

Supplemental Use of Proceeds

The notes are offered to meet investor demand for products that reflect the risk-return profile and market exposure provided by the notes. See “What Is the Total Return on the Notes at Maturity, Assuming a Range of Performances for the Basket?” and “Hypothetical Examples of Amount Payable at Maturity” in this pricing supplement for an illustration of the risk-return profile of the notes and “The Basket and the Reference Stocks” in this pricing supplement for a description of the market exposure provided by the notes.

The original issue price of the notes is equal to the estimated value of the notes plus the selling commissions paid to JPMS and other affiliated or unaffiliated dealers, plus (minus) the projected profits (losses) that our affiliates expect to realize for assuming risks inherent in hedging our obligations under the notes, plus the estimated cost of hedging our obligations under the notes.

| JPMorgan Structured Investments — | PS-24 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |

Supplemental Plan of Distribution

We expect that delivery of the notes will be made against payment for the notes on or about the Original Issue Date set forth on the front cover of this pricing supplement, which will be the third business day following the Pricing Date of the notes (this settlement cycle being referred to as “T+3”). Under Rule 15c6-1 of the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in two business days, unless the parties to that trade expressly agree otherwise. Accordingly, purchasers who wish to trade notes on any date prior to two business days before delivery will be required to specify an alternate settlement cycle at the time of any such trade to prevent a failed settlement and should consult their own advisors.

| JPMorgan Structured Investments — | PS-25 |

| Return Notes Linked to the J.P. Morgan COVID-19 International Recovery Basket of 33 Reference Stocks |