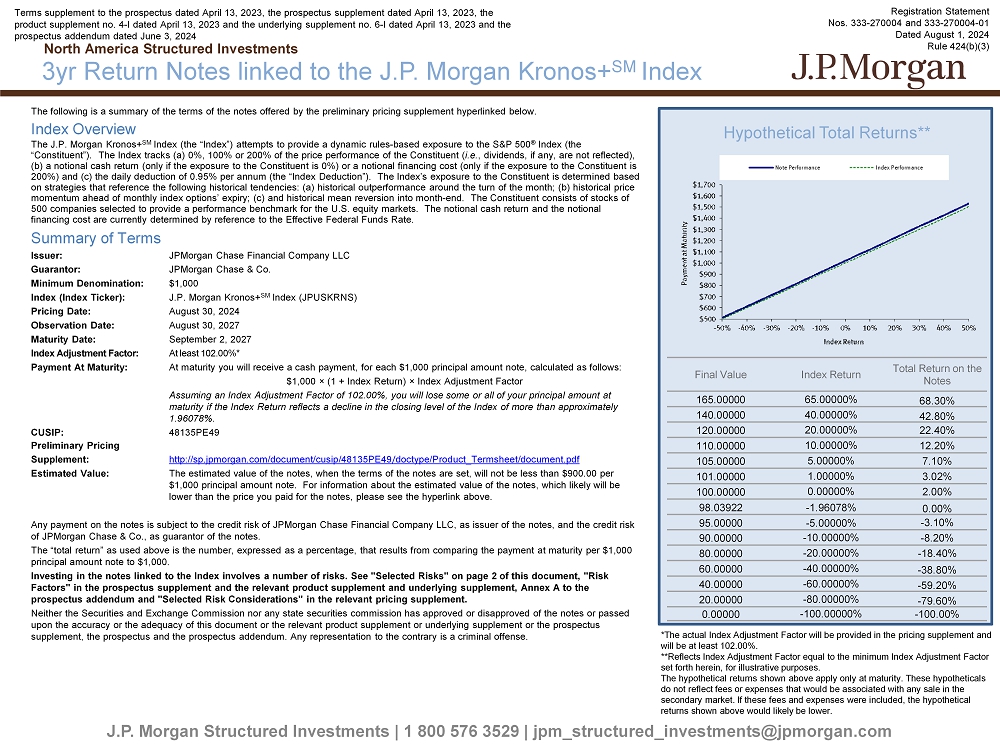

The following is a summary of the terms of the notes offered by the preliminary pricing supplement hyperlinked below. Index Overview The J.P. Morgan Kronos+ SM Index (the “Index”) attempts to provide a dynamic rules - based exposure to the S&P 500 ® Index (the “Constituent”). The Index tracks (a) 0%, 100% or 200% of the price performance of the Constituent ( i.e. , dividends, if any, are not reflected), (b) a notional cash return (only if the exposure to the Constituent is 0%) or a notional financing cost (only if the exposure to the Constituent is 200%) and (c) the daily deduction of 0.95% per annum (the “Index Deduction”). The Index’s exposure to the Constituent is det erm ined based on strategies that reference the following historical tendencies: (a) historical outperformance around the turn of the month; (b ) historical price momentum ahead of monthly index options’ expiry; (c) and historical mean reversion into month - end. The Constituent consists of stocks of 500 companies selected to provide a performance benchmark for the U.S. equity markets. The notional cash return and the noti ona l financing cost are currently determined by reference to the Effective Federal Funds Rate. Summary of Terms Issuer: JPMorgan Chase Financial Company LLC Guarantor: JPMorgan Chase & Co. Minimum Denomination: $1,000 Index (Index Ticker): J.P. Morgan Kronos+ SM Index (JPUSKRNS) Pricing Date: August 30, 2024 Observation Date: August 30, 2027 Maturity Date: September 2, 2027 Index Adjustment Factor: At least 102.00%* Payment At Maturity: At maturity you will receive a cash payment, for each $1,000 principal amount note, calculated as follows: $1,000 î (1 + Index Return) î Index Adjustment Factor Assuming an Index Adjustment Factor of 102.00%, you will lose some or all of your principal amount at maturity if the Index Return reflects a decline in the closing level of the Index of more than approximately 1.96078 %. CUSIP: 48135PE49 Preliminary Pricing Supplement: http://sp.jpmorgan.com/document/cusip/48135PE49 / doctype/Product_Termsheet/document.pdf Estimated Value: The estimated value of the notes, when the terms of the notes are set, will not be less than $900.00 per $1,000 principal amount note. For information about the estimated value of the notes, which likely will be lower than the price you paid for the notes, please see the hyperlink above. Any payment on the notes is subject to the credit risk of JPMorgan Chase Financial Company LLC, as issuer of the notes, and t he credit risk of JPMorgan Chase & Co., as guarantor of the notes. The “total return” as used above is the number, expressed as a percentage, that results from comparing the payment at maturit y p er $1,000 principal amount note to $1,000. Investing in the notes linked to the Index involves a number of risks. See "Selected Risks" on page 2 of this document, "Risk Factors" in the prospectus supplement and the relevant product supplement and underlying supplement, Annex A to the prospectus addendum and "Selected Risk Considerations" in the relevant pricing supplement. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the notes o r p assed upon the accuracy or the adequacy of this document or the relevant product supplement or underlying supplement or the prospec tus supplement, the prospectus and the prospectus addendum. Any representation to the contrary is a criminal offense. J.P. Morgan Structured Investments | 1 800 576 3529 | jpm_structured_investments@jpmorgan.com 3yr Return Notes linked to the J.P. Morgan Kronos+ SM Index H North America Structured Investments Registration Statement Nos. 333 - 270004 and 333 - 270004 - 01 Dated August 1, 2024 Rule 424(b)(3) Terms supplement to the prospectus dated April 13, 2023, the prospectus supplement dated April 13, 2023, the product supplement no. 4 - I dated April 13, 2023 and the underlying supplement no. 6 - I dated April 13, 2023 and the prospectus addendum dated June 3, 2024 Hypothetical Total Returns** Total Return on the Notes Index Return Final Value 68.30% 65.00000% 165.00000 42.80% 40.00000% 140.00000 22.40% 20.00000% 120.00000 12.20% 10.00000% 110.00000 7.10% 5.00000% 105.00000 3.02% 1.00000% 101.00000 2.00 % 0.00000% 100.00000 0.00% - 1.96078% 98.03922 - 3.10% - 5.00000% 95.00000 - 8.20% - 10.00000% 90.00000 - 18.40% - 20.00000% 80.00000 - 38.80% - 40.00000% 60.00000 - 59.20% - 60.00000% 40.00000 - 79.60% - 80.00000% 20.00000 - 100.00% - 100.00000% 0.00000 *The actual Index Adjustment Factor will be provided in the pricing supplement and will be at least 102.00%. **Reflects Index Adjustment Factor equal to the minimum Index Adjustment Factor set forth herein, for illustrative purposes. The hypothetical returns shown above apply only at maturity. These hypotheticals do not reflect fees or expenses that would be associated with any sale in the secondary market. If these fees and expenses were included, the hypothetical returns shown above would likely be lower.

J.P. Morgan Structured Investments | 1 800 576 3529 | jpm_structured_investments@jpmorgan.com Selected Risks Risks Relating to the Notes Generally • Your investment in the notes may result in a loss. The notes do not guarantee any return of principal. • The level of the Index will include an Index deduction of 0.95% per annum and, in some circumstances, a notional financing cost calculated based on the Effective Federal Funds Rate. • Any payment on the notes is subject to the credit risks of JPMorgan Chase Financial Company LLC and JPMorgan Chase & Co. Therefore the value of the notes prior to maturity will be subject to changes in the market’s view of the creditworthiness of JPMorgan Chase Financial Company LLC or JPMorgan Chase & Co. • As a finance subsidiary, JPMorgan Chase Financial Company LLC has no independent operations and has limited assets. • No interest payments, dividend payments or voting rights. • Lack of liquidity: J.P. Morgan Securities LLC (who we refer to as “JPMS”) intends to offer to purchase the notes in the secondary market but is not required to do so. The price, if any, at which JPMS will be willing to purchase notes from you in the secondary market, if at all, may result in a significant loss of your principal. • The tax consequences of the notes may be uncertain. You should consult your tax adviser regarding the U.S. federal income tax consequences of an investment in the notes. Risks Relating to Conflicts of Interest • Potential conflicts: We and our affiliates play a variety of roles in connection with the issuance of notes, including acting as calculation agent and hedging our obligations under the notes, and making the assumptions used to determine the pricing of the notes and the estimated value of the notes when the terms of the notes are set. It is possible that such hedging or other trading activities of J.P. Morgan or its affiliates could result in substantial returns for J.P. Morgan and its affiliates while the value of the notes declines. Selected Risks (continued) Risks Relating to the Estimated Value and Secondary Market Prices of the Notes • The estimated value of the notes will be lower than the original issue price (price to public) of the notes. • The estimated value of the notes does not represent future values and may differ from others’ estimates. • The estimated value of the notes is determined by reference to an internal funding rate. • The value of the notes, which may be reflected in customer account statements, may be higher than the then current estimated value of the notes for a limited time period. Risks Relating to the Index • JPMorgan Chase & Co. is currently one of the companies that make up the Constituent. • Our affiliate, JPMS, the index sponsor and the index calculation agent of the Index, may have interests that conflict with yours and may adjust the Index in a way that affects its level. • The Index may not be successful or outperform any alternative strategy. • The notes are subject to risks associated with the Index’s turn - of - the - month strategy. • The notes are subject to risks associated with the Index’s options expiry momentum strategy. • The notes are subject to risks associated with the Index’s month - end mean reversion strategy. • The Index’s strategies are applied during only a portion of each month. • The Index may be adversely affected by an overlap between its turn - of - the - month strategy and its month - end mean reversion strategy. • The Index may be uninvested in the Constituent. • The Constituent may be replaced by a substitute index if certain extraordinary events occur. • The notional cash return will be negatively affected if the underlying interest rate is negative. • The Index, which was established on December 22, 2020, has a limited operating history and may perform in unanticipated ways. • The Index comprises notional assets and liabilities. There is no actual portfolio of assets to which any person is entitled or in which any person has any ownership interest. • The Effective Federal Funds Rate is affected by a number of factors and may be volatile. • The method by which the Effective Federal Funds Rate is determined may change, and any such change may adversely affect the value of notes linked to the Index. Additional Information Any information relating to performance contained in these materials is illustrative and no assurance is given that any indic ati ve returns, performance or results, whether historical or hypothetical, will be achieved. These terms are subject to change, and J.P. Morgan undertakes no duty to update this information. This document shall be amended, s upe rseded and replaced in its entirety by a subsequent preliminary pricing supplement and/or pricing supplement, and the documents referred to therein. In the event any inconsistency between the information pres ent ed herein and any such preliminary pricing supplement and/or pricing supplement, such preliminary pricing supplement and/or pricing supplement shall govern. Past performance, and especially hypothetical back - tested performance, is not indicative of future results. Actual performance m ay vary significantly from past performance or any hypothetical back - tested performance. This type of information has inherent limitations and you should carefully consider these limitations before placing reliance on such information. IRS Circular 230 Disclosure: JPMorgan Chase & Co. and its affiliates do not provide tax advice. Accordingly, any discussion o f U .S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with JPMorgan Cha se & Co. of any of the matters addressed herein or for the purpose of avoiding U.S. tax - related penalties. Investment suitability must be determined individually for each investor, and the financial instruments described herein may not be suitable for all investors. This information is not intended to provide and should not be relied upon as providing accounting, legal, regulatory or tax advice. Investors should consult with their own advisers as to the se matters. This material is not a product of J.P. Morgan Research Departments. North America Structured Investments 3yr Return Notes linked to the J.P. Morgan Kronos+ SM Index The risks identified above are not exhaustive. Please see “Risk Factors” in the prospectus supplement and the applicable prod uct supplement and underlying supplement, Annex A to the prospectus addendum and “Selected Risk Considerations” in the applicable preliminary pricing supplement for additional information.