July 31, 2024

Registration Statement Nos. 333-270004 and 333-270004-01; Rule 424(b)(2)

Pricing supplement to product supplement no. 4-I dated April 13, 2023, underlying supplement no. 1-I dated April 13, 2023, the prospectus and

prospectus supplement, each dated April 13, 2023, and the prospectus addendum dated June 3, 2024

JPMorgan Chase Financial Company LLC

Structured Investments

$4,862,000

Uncapped Dual Directional Buffered Return Enhanced

Notes Linked to the S&P 500

®

Futures Excess Return

Index due August 3, 2028

Fully and Unconditionally Guaranteed by JPMorgan Chase & Co.

● The notes are designed for investors who seek an uncapped return of 1.40 times any appreciation, or a capped,

unleveraged return equal to the absolute value of any depreciation (up to the Buffer Amount of 30.00%), of the S&P 500

®

Futures Excess Return Index at maturity.

● Investors should be willing to forgo interest payments and be willing to lose up to 70.00% of their principal amount at

maturity.

● The notes are unsecured and unsubordinated obligations of JPMorgan Chase Financial Company LLC, which we refer to as

JPMorgan Financial, the payment on which is fully and unconditionally guaranteed by JPMorgan Chase & Co. Any

payment on the notes is subject to the credit risk of JPMorgan Financial, as issuer of the notes, and the credit risk

of JPMorgan Chase & Co., as guarantor of the notes.

● Minimum denominations of $1,000 and integral multiples thereof

● The notes priced on July 31, 2024 and are expected to settle on or about August 5, 2024.

● CUSIP: 48135PUV1

Investing in the notes involves a number of risks. See “Risk Factors” beginning on page S-2 of the accompanying

prospectus supplement, Annex A to the accompanying prospectus addendum, “Risk Factors” beginning on page PS-11 of

the accompanying product supplement and “Selected Risk Considerations” beginning on page PS-5 of this pricing

supplement.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of

the notes or passed upon the accuracy or the adequacy of this pricing supplement or the accompanying product supplement,

underlying supplement, prospectus supplement, prospectus and prospectus addendum. Any representation to the contrary is a

criminal offense.

Price to Public (1)

Fees and Commissions (2)

Proceeds to Issuer

Per note

$1,000

$9.4404

$990.5596

Total

$4,862,000

$45,899

$4,816,101

(1) See “Supplemental Use of Proceeds” in this pricing supplement for information about the components of the price to public of the notes.

(2) J.P. Morgan Securities LLC, which we refer to as JPMS, acting as agent for JPMorgan Financial, will pay all of the selling commissions

it receives from us to other affiliated or unaffiliated dealers. These selling commissions will vary and will be up to $9.50 per $1,000 principal

amount note. See “Plan of Distribution (Conflicts of Interest)” in the accompanying product supplement.

The estimated value of the notes, when the terms of the notes were set, was $986.60 per $1,000 principal amount note. See

“The Estimated Value of the Notes” in this pricing supplement for additional information.

The notes are not bank deposits, are not insured by the Federal Deposit Insurance Corporation or any other governmental agency

and are not obligations of, or guaranteed by, a bank.

PS-1| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

Key Terms

Issuer: JPMorgan Chase Financial Company LLC, a direct,

wholly owned finance subsidiary of JPMorgan Chase & Co.

Guarantor: JPMorgan Chase & Co.

Index: The S&P 500

®

Futures Excess Return Index

(Bloomberg ticker: SPXFP)

Upside Leverage Factor: 1.40

Buffer Amount: 30.00%

Pricing Date: July 31, 2024

Original Issue Date (Settlement Date): On or about August

5, 2024

Observation Date*: July 31, 2028

Maturity Date*: August 3, 2028

* Subject to postponement in the event of a market disruption

event and as described under “General Terms of Notes —

Postponement of a Determination Date — Notes Linked to a

Single Underlying — Notes Linked to a Single Underlying

(Other Than a Commodity Index)” and “General Terms of

Notes — Postponement of a Payment Date” in the

accompanying product supplement

Payment at Maturity:

If the Final Value is greater than the Initial Value, your

payment at maturity per $1,000 principal amount note will be

calculated as follows:

$1,000 + ($1,000 × Index Return × Upside Leverage Factor)

If the Final Value is equal to the Initial Value or is less than

the Initial Value by up to the Buffer Amount, your payment at

maturity per $1,000 principal amount note will be calculated

as follows:

$1,000 + ($1,000 × Absolute Index Return)

This payout formula results in an effective cap of 30.00% on

your return at maturity if the Index Return is negative. Under

these limited circumstances, your maximum payment at

maturity is $1,300.00 per $1,000 principal amount note.

If the Final Value is less than the Initial Value by more than

the Buffer Amount, your payment at maturity per $1,000

principal amount note will be calculated as follows:

$1,000 + [$1,000 × (Index Return + Buffer Amount)]

If the Final Value is less than the Initial Value by more than

the Buffer Amount, you will lose some or most of your

principal amount at maturity.

Absolute Index Return: The absolute value of the Index

Return. For example, if the Index Return is -5%, the Absolute

Index Return will equal 5%.

Index Return:

(Final Value – Initial Value)

Initial Value

Initial Value: The closing level of the Index on the Pricing

Date, which was 476.09

Final Value: The closing level of the Index on the

Observation Date

PS-2| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

Supplemental Terms of the Notes

The notes are not futures contracts or swaps and are not regulated under the Commodity Exchange Act of 1936, as amended

(the “Commodity Exchange Act”). The notes are offered pursuant to an exemption from regulation under the Commodity Exchange

Act, commonly known as the hybrid instrument exemption, that is available to securities that have one or more payments indexed to the

value, level or rate of one or more commodities, as set out in section 2(f) of that statute. Accordingly, you are not afforded any

protection provided by the Commodity Exchange Act or any regulation promulgated by the Commodity Futures Trading Commission.

For purposes of the accompanying product supplement, the Index will be deemed to be an Equity Index, except as provided below, and

any references in the accompanying product supplement to the securities included in an Equity Index (or similar references) should be

read to refer to the securities included in the S&P 500

®

Index, which is the reference index for the futures contracts included in the

Index. Notwithstanding the foregoing, the Index will be deemed to be a Commodity Index for purposes of the section entitled “The

Underlyings — Indices — Discontinuation of an Index; Alteration of Method of Calculation” in the accompanying product supplement.

Notwithstanding anything to the contrary in the accompanying product supplement, if a Determination Date (as defined in the

accompanying product supplement) has been postponed to the applicable Final Disrupted Determination Date (as defined in the

accompanying product supplement) and that day is a Disrupted Day (as defined in the accompanying product supplement), the

calculation agent will determine the closing level of the Index for that Determination Date on that Final Disrupted Determination Date in

accordance with the formula for and method of calculating the closing level of the Index last in effect prior to the commencement of the

market disruption event (or prior to the non-trading day), using the official settlement price (or, if trading in the relevant futures contract

has been materially suspended or materially limited, the calculation agent’s good faith estimate of the applicable settlement price that

would have prevailed but for that suspension or limitation) at the close of the principal trading session on that date of each futures

contract most recently composing the Index, as well as any futures contract required to roll any expiring futures contract in accordance

with the method of calculating the Index.

Any values of the Index, and any values derived therefrom, included in this pricing supplement may be corrected, in the event of

manifest error or inconsistency, by amendment of this pricing supplement and the corresponding terms of the notes. Notwithstanding

anything to the contrary in the indenture governing the notes, that amendment will become effective without consent of the holders of

the notes or any other party.

PS-3| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

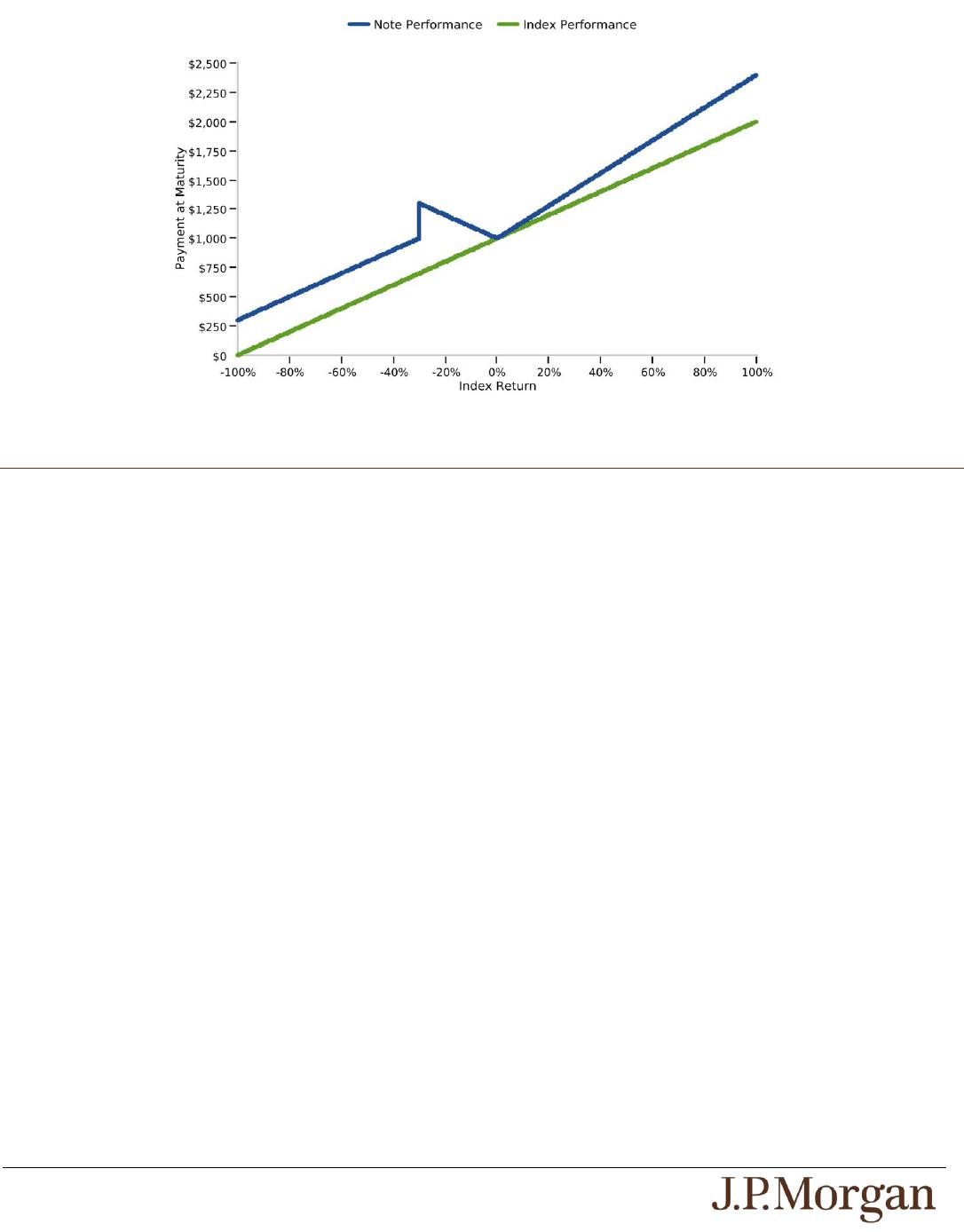

Hypothetical Payout Profile

The following table and graph illustrate the hypothetical total return and payment at maturity on the notes linked to a hypothetical Index.

The “total return” as used in this pricing supplement is the number, expressed as a percentage, that results from comparing the

payment at maturity per $1,000 principal amount note to $1,000. The hypothetical total returns and payments set forth below assume

the following:

● an Initial Value of 100.00;

● an Upside Leverage Factor of 1.40; and

● a Buffer Amount of 30.00%.

The hypothetical Initial Value of 100.00 has been chosen for illustrative purposes only and does not represent the actual Initial Value.

The actual Initial Value is the closing level of the Index on the Pricing Date and is specified under “Key Terms – Initial Value” in this

pricing supplement. For historical data regarding the actual closing levels of the Index, please see the historical information set forth

under “The Index” in this pricing supplement.

Each hypothetical total return or hypothetical payment at maturity set forth below is for illustrative purposes only and may not be the

actual total return or payment at maturity applicable to a purchaser of the notes. The numbers appearing in the following table and

graph have been rounded for ease of analysis.

Final Value

Index Return

Absolute Index Return

Total Return on the

Notes

Payment at Maturity

180.00

80.00%

N/A

112.00%

$2,120.00

165.00

65.00%

N/A

91.00%

$1,910.00

150.00

50.00%

N/A

70.00%

$1,700.00

140.00

40.00%

N/A

56.00%

$1,560.00

130.00

30.00%

N/A

42.00%

$1,420.00

120.00

20.00%

N/A

28.00%

$1,280.00

110.00

10.00%

N/A

14.00%

$1,140.00

105.00

5.00%

N/A

7.00%

$1,070.00

101.00

1.00%

N/A

1.40%

$1,014.00

100.00

0.00%

0.00%

0.00%

$1,000.00

95.00

-5.00%

5.00%

5.00%

$1,050.00

90.00

-10.00%

10.00%

10.00%

$1,100.00

85.00

-15.00%

15.00%

15.00%

$1,150.00

80.00

-20.00%

20.00%

20.00%

$1,200.00

70.00

-30.00%

30.00%

30.00%

$1,300.00

60.00

-40.00%

N/A

-10.00%

$900.00

50.00

-50.00%

N/A

-20.00%

$800.00

40.00

-60.00%

N/A

-30.00%

$700.00

30.00

-70.00%

N/A

-40.00%

$600.00

20.00

-80.00%

N/A

-50.00%

$500.00

10.00

-90.00%

N/A

-60.00%

$400.00

0.00

-100.00%

N/A

-70.00%

$300.00

PS-4| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

The following graph demonstrates the hypothetical payments at maturity on the notes for a range of Index Returns (-100% to 100%).

There can be no assurance that the performance of the Index will result in the return of any of your principal amount in excess of

$300.00 per $1,000.00 principal amount note, subject to the credit risks of JPMorgan Financial and JPMorgan Chase & Co.

How the Notes Work

Index Appreciation Upside Scenario:

If the Final Value is greater than the Initial Value, investors will receive at maturity the $1,000 principal amount plus a return equal to the

Index Return times the Upside Leverage Factor of 1.40.

● If the closing level of the Index increases 5.00%, investors will receive at maturity a 7.00% return, or $1,070.00 per $1,000 principal

amount note.

Index Par or Index Depreciation Upside Scenario:

If the Final Value is equal to the Initial Value or is less than the Initial Value by up to the Buffer Amount of 30.00%, investors will receive

at maturity the $1,000 principal amount plus a return equal to the Absolute Index Return.

● For example, if the closing level of the Index declines 10.00%, investors will receive at maturity a 10.00% return, or $1,100.00 per

$1,000 principal amount note.

Downside Scenario:

If the Final Value is less than the Initial Value by more than the Buffer Amount of 30.00%, investors will lose 1% of the principal amount

of their notes for every 1% that the Final Value is less than the Initial Value by more than the Buffer Amount.

● For example, if the closing level of the Index declines 60.00%, investors will lose 30.00% of their principal amount and receive only

$700.00 per $1,000 principal amount note at maturity.

The hypothetical returns and hypothetical payments on the notes shown above apply only if you hold the notes for their entire term.

These hypotheticals do not reflect the fees or expenses that would be associated with any sale in the secondary market. If these fees

and expenses were included, the hypothetical returns and hypothetical payments shown above would likely be lower.

PS-5| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

Selected Risk Considerations

An investment in the notes involves significant risks. These risks are explained in more detail in the “Risk Factors” sections of the

accompanying prospectus supplement and product supplement and in Annex A to the accompanying prospectus addendum.

Risks Relating to the Notes Generally

● YOUR INVESTMENT IN THE NOTES MAY RESULT IN A LOSS —

The notes do not guarantee any return of principal. If the Final Value is less than the Initial Value by more than 30.00%, you will

lose 1% of the principal amount of your notes for every 1% that the Final Value is less than the Initial Value by more than 30.00%.

Accordingly, under these circumstances, you will lose up to 70.00% of your principal amount at maturity.

● YOUR MAXIMUM GAIN ON THE NOTES IS LIMITED BY THE BUFFER AMOUNT IF THE INDEX RETURN IS NEGATIVE —

Because the payment at maturity will not reflect the Absolute Index Return if the Final Value is less than the Initial Value by more

than the Buffer Amount, the Buffer Amount is effectively a cap on your return at maturity if the Index Return is negative. The

maximum payment at maturity if the Index Return is negative is $1,300.00 per $1,000 principal amount note.

● CREDIT RISKS OF JPMORGAN FINANCIAL AND JPMORGAN CHASE & CO. —

Investors are dependent on our and JPMorgan Chase & Co.’s ability to pay all amounts due on the notes. Any actual or potential

change in our or JPMorgan Chase & Co.’s creditworthiness or credit spreads, as determined by the market for taking that credit

risk, is likely to adversely affect the value of the notes. If we and JPMorgan Chase & Co. were to default on our payment

obligations, you may not receive any amounts owed to you under the notes and you could lose your entire investment.

● AS A FINANCE SUBSIDIARY, JPMORGAN FINANCIAL HAS NO INDEPENDENT OPERATIONS AND HAS LIMITED ASSETS

—

As a finance subsidiary of JPMorgan Chase & Co., we have no independent operations beyond the issuance and administration of

our securities and the collection of intercompany obligations. Aside from the initial capital contribution from JPMorgan Chase &

Co., substantially all of our assets relate to obligations of JPMorgan Chase & Co. to make payments under loans made by us to

JPMorgan Chase & Co. or under other intercompany agreements. As a result, we are dependent upon payments from JPMorgan

Chase & Co. to meet our obligations under the notes. We are not a key operating subsidiary of JPMorgan Chase & Co. and in a

bankruptcy or resolution of JPMorgan Chase & Co. we are not expected to have sufficient resources to meet our obligations in

respect of the notes as they come due. If JPMorgan Chase & Co. does not make payments to us and we are unable to make

payments on the notes, you may have to seek payment under the related guarantee by JPMorgan Chase & Co., and that

guarantee will rank pari passu with all other unsecured and unsubordinated obligations of JPMorgan Chase & Co. For more

information, see the accompanying prospectus addendum.

● THE NOTES DO NOT PAY INTEREST.

● YOU WILL NOT HAVE ANY RIGHTS WITH RESPECT TO THE E-MINI

®

S&P 500

®

FUTURES CONTRACTS (THE

“UNDERLYING FUTURES CONTRACTS”) OR THE SECURITIES INCLUDED IN THE INDEX UNDERLYING THE

UNDERLYING FUTURES CONTRACTS.

● LACK OF LIQUIDITY—

The notes will not be listed on any securities exchange. Accordingly, the price at which you may be able to trade your notes is likely

to depend on the price, if any, at which JPMS is willing to buy the notes. You may not be able to sell your notes. The notes are not

designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your notes to maturity.

Risks Relating to Conflicts of Interest

● POTENTIAL CONFLICTS —

We and our affiliates play a variety of roles in connection with the notes. In performing these duties, our and JPMorgan Chase &

Co.’s economic interests are potentially adverse to your interests as an investor in the notes. It is possible that hedging or trading

activities of ours or our affiliates in connection with the notes could result in substantial returns for us or our affiliates while the

value of the notes declines. Please refer to “Risk Factors — Risks Relating to Conflicts of Interest” in the accompanying product

supplement.

Risks Relating to the Estimated Value and Secondary Market Prices of the Notes

● THE ESTIMATED VALUE OF THE NOTES IS LOWER THAN THE ORIGINAL ISSUE PRICE (PRICE TO PUBLIC) OF THE

NOTES —

The estimated value of the notes is only an estimate determined by reference to several factors. The original issue price of the

notes exceeds the estimated value of the notes because costs associated with selling, structuring and hedging the notes are

included in the original issue price of the notes. These costs include the selling commissions, the projected profits, if any, that our

affiliates expect to realize for assuming risks inherent in hedging our obligations under the notes and the estimated cost of hedging

our obligations under the notes. See “The Estimated Value of the Notes” in this pricing supplement.

● THE ESTIMATED VALUE OF THE NOTES DOES NOT REPRESENT FUTURE VALUES OF THE NOTES AND MAY DIFFER

FROM OTHERS’ ESTIMATES —

See “The Estimated Value of the Notes” in this pricing supplement.

PS-6| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

● THE ESTIMATED VALUE OF THE NOTES IS DERIVED BY REFERENCE TO AN INTERNAL FUNDING RATE —

The internal funding rate used in the determination of the estimated value of the notes may differ from the market-implied funding

rate for vanilla fixed income instruments of a similar maturity issued by JPMorgan Chase & Co. or its affiliates. Any difference may

be based on, among other things, our and our affiliates’ view of the funding value of the notes as well as the higher issuance,

operational and ongoing liability management costs of the notes in comparison to those costs for the conventional fixed income

instruments of JPMorgan Chase & Co. This internal funding rate is based on certain market inputs and assumptions, which may

prove to be incorrect, and is intended to approximate the prevailing market replacement funding rate for the notes. The use of an

internal funding rate and any potential changes to that rate may have an adverse effect on the terms of the notes and any

secondary market prices of the notes. See “The Estimated Value of the Notes” in this pricing supplement.

● THE VALUE OF THE NOTES AS PUBLISHED BY JPMS (AND WHICH MAY BE REFLECTED ON CUSTOMER ACCOUNT

STATEMENTS) MAY BE HIGHER THAN THE THEN-CURRENT ESTIMATED VALUE OF THE NOTES FOR A LIMITED TIME

PERIOD —

We generally expect that some of the costs included in the original issue price of the notes will be partially paid back to you in

connection with any repurchases of your notes by JPMS in an amount that will decline to zero over an initial predetermined period.

See “Secondary Market Prices of the Notes” in this pricing supplement for additional information relating to this initial period.

Accordingly, the estimated value of your notes during this initial period may be lower than the value of the notes as published by

JPMS (and which may be shown on your customer account statements).

● SECONDARY MARKET PRICES OF THE NOTES WILL LIKELY BE LOWER THAN THE ORIGINAL ISSUE PRICE OF THE

NOTES —

Any secondary market prices of the notes will likely be lower than the original issue price of the notes because, among other

things, secondary market prices take into account our internal secondary market funding rates for structured debt issuances and,

also, because secondary market prices may exclude selling commissions, projected hedging profits, if any, and estimated hedging

costs that are included in the original issue price of the notes. As a result, the price, if any, at which JPMS will be willing to buy the

notes from you in secondary market transactions, if at all, is likely to be lower than the original issue price. Any sale by you prior to

the Maturity Date could result in a substantial loss to you.

● SECONDARY MARKET PRICES OF THE NOTES WILL BE IMPACTED BY MANY ECONOMIC AND MARKET FACTORS —

The secondary market price of the notes during their term will be impacted by a number of economic and market factors, which

may either offset or magnify each other, aside from the selling commissions, projected hedging profits, if any, estimated hedging

costs and the level of the Index. Additionally, independent pricing vendors and/or third party broker-dealers may publish a price for

the notes, which may also be reflected on customer account statements. This price may be different (higher or lower) than the price

of the notes, if any, at which JPMS may be willing to purchase your notes in the secondary market. See “Risk Factors — Risks

Relating to the Estimated Value and Secondary Market Prices of the Notes — Secondary market prices of the notes will be

impacted by many economic and market factors” in the accompanying product supplement.

Risks Relating to the Index

● JPMORGAN CHASE & CO. IS CURRENTLY ONE OF THE COMPANIES THAT MAKE UP THE S&P 500

®

INDEX, THE INDEX

UNDERLYING THE UNDERLYING FUTURES CONTRACTS OF THE INDEX,

but JPMorgan Chase & Co. will not have any obligation to consider your interests in taking any corporate action that might affect

the level of the Index.

● THE INDEX IS SUBJECT TO SIGNIFICANT RISKS ASSOCIATED WITH THE UNDERLYING FUTURES CONTRACTS —

The Index tracks the excess return of the Underlying Futures Contracts. The price of an Underlying Futures Contract depends not

only on the level of the underlying index referenced by the Underlying Futures Contract, but also on a range of other factors,

including but not limited to the performance and volatility of the U.S. stock market, corporate earnings reports, geopolitical events,

governmental and regulatory policies and the policies of the Chicago Mercantile Exchange (the “Exchange”) on which the

Underlying Futures Contracts trade. In addition, the futures markets are subject to temporary distortions or other disruptions due to

various factors, including the lack of liquidity in the markets, the participation of speculators and government regulation and

intervention. These factors and others can cause the prices of the Underlying Futures Contracts to be volatile and could adversely

affect the level of the Index and any payments on, and the value of, your notes.

● SUSPENSION OR DISRUPTIONS OF MARKET TRADING IN THE UNDERLYING FUTURES CONTRACTS MAY ADVERSELY

AFFECT THE VALUE OF YOUR NOTES —

Futures markets are subject to temporary distortions or other disruptions due to various factors, including lack of liquidity, the

participation of speculators, and government regulation and intervention. In addition, futures exchanges generally have regulations

that limit the amount of the Underlying Futures Contract price fluctuations that may occur in a single day. These limits are

generally referred to as “daily price fluctuation limits” and the maximum or minimum price of a contract on any given day as a result

of those limits is referred to as a “limit price.” Once the limit price has been reached in a particular contract, no trades may be

made at a price beyond the limit, or trading may be limited for a set period of time. Limit prices have the effect of precluding trading

in a particular contract or forcing the liquidation of contracts at potentially disadvantageous times or prices. These circumstances

could delay the calculation of the level of the Index and could adversely affect the level of the Index and any payments on, and the

value of, your notes.

● THE PERFORMANCE OF THE INDEX WILL DIFFER FROM THE PERFORMANCE OF THE INDEX UNDERLYING THE

UNDERLYING FUTURES CONTRACTS —

A variety of factors can lead to a disparity between the performance of a futures contract on an equity index and the performance

of that equity index, including the expected dividend yields of the equity securities included in that equity index, an implicit financing

cost associated with futures contracts and policies of the exchange on which the futures contracts are traded, such as margin

requirements. Thus, a decline in expected dividends yields or an increase in margin requirements may adversely affect the

performance of the Index. In addition, the implicit financing cost will negatively affect the performance of the Index, with a greater

negative effect when market interest rates are higher. During periods of high market interest rates, the Index is likely to

underperform the equity index underlying the Underlying Futures Contracts, perhaps significantly.

PS-7| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

● NEGATIVE ROLL RETURNS ASSOCIATED WITH THE UNDERLYING FUTURES CONTRACTS MAY ADVERSELY AFFECT

THE LEVEL OF THE INDEX AND THE VALUE OF THE NOTES —

The Index tracks the excess return of the Underlying Futures Contracts. Unlike common equity securities, futures contracts, by

their terms, have stated expirations. As the exchange-traded Underlying Futures Contracts approach expiration, they are replaced

by contracts of the same series that have a later expiration. For example, an Underlying Futures Contract notionally purchased

and held in June may specify a September expiration date. As time passes, the contract expiring in September is replaced by a

contract for delivery in December. This is accomplished by notionally selling the September contract and notionally purchasing the

December contract. This process is referred to as “rolling.” Excluding other considerations, if prices are higher in the distant

delivery months than in the nearer delivery months, the notional purchase of the December contract would take place at a price

that is higher than the price of the September contract, thereby creating a negative “roll return.” Negative roll returns adversely

affect the returns of the Underlying Futures Contracts and, therefore, the level of the Index and any payments on, and the value of,

the notes. Because of the potential effects of negative roll returns, it is possible for the level of the Index to decrease significantly

over time, even when the levels of the underlying index referenced by the Underlying Futures Contracts are stable or increasing.

● OTHER KEY RISK:

o THE INDEX COMPRISES NOTIONAL ASSETS AND LIABILITIES. THERE IS NO ACTUAL PORTFOLIO OF ASSETS TO

WHICH ANY PERSON IS ENTITLED OR IN WHICH ANY PERSON HAS ANY OWNERSHIP INTEREST.

The Index

The Index measures the performance of the nearest maturing quarterly Underlying Futures Contracts trading on the Chicago Mercantile

Exchange (the “Exchange”). The Underlying Futures Contracts are U.S. dollar-denominated futures contracts based on the S&P 500

®

Index. The S&P 500

®

Index consists of stocks of 500 companies selected to provide a performance benchmark for the U.S. equity

markets. For additional information about the Index and the Underlying Futures Contracts, see Annex A in this pricing supplement.

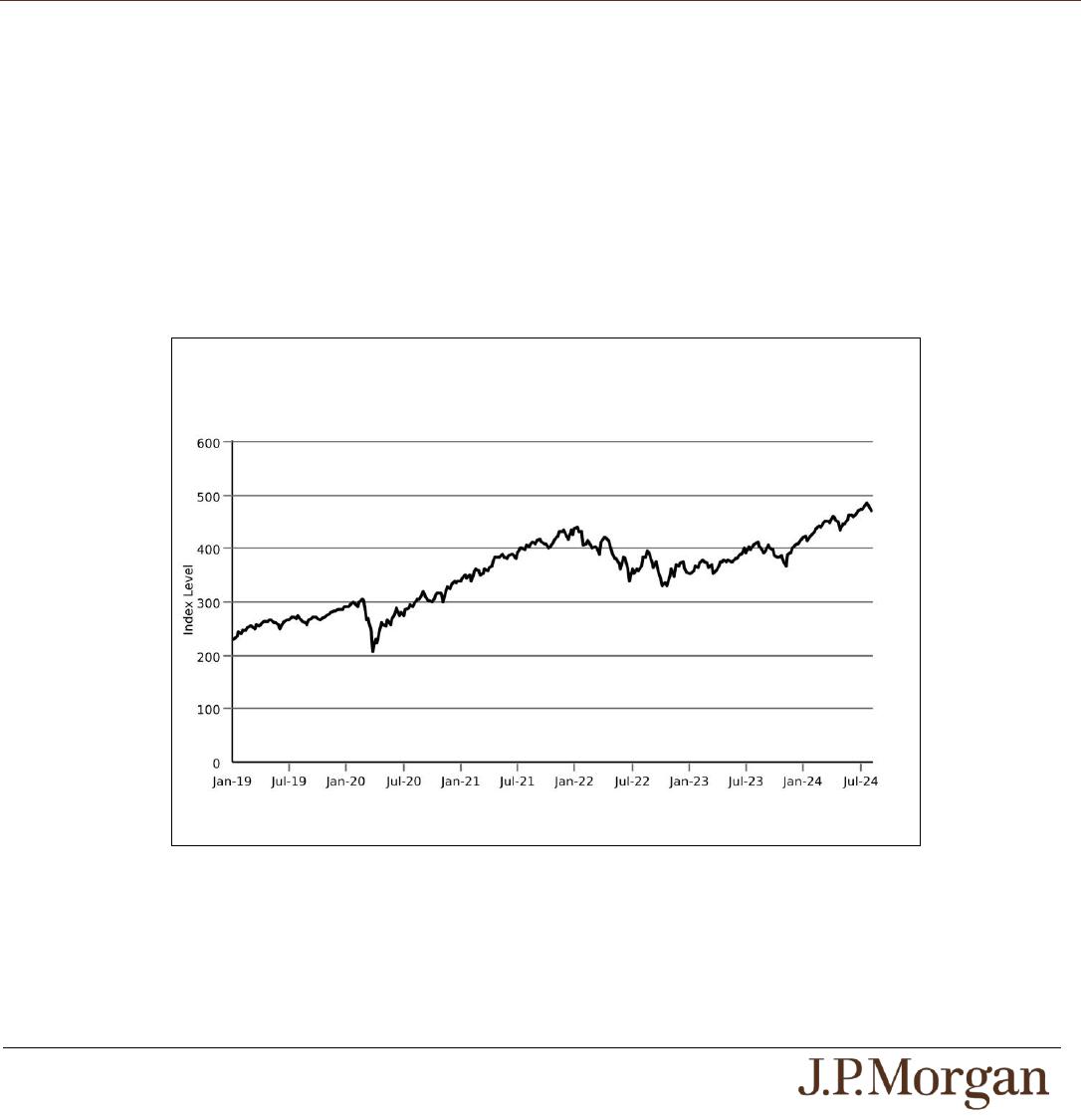

Historical Information

The following graph sets forth the historical performance of the Index based on the weekly historical closing levels of the Index from

January 4, 2019 through July 26, 2024. The closing level of the Index on July 31, 2024 was 476.09. We obtained the closing levels

above and below from the Bloomberg Professional

®

service (“Bloomberg”), without independent verification.

The historical closing levels of the Index should not be taken as an indication of future performance, and no assurance can be given as

to the closing level of the Index on the Observation Date. There can be no assurance that the performance of the Index will result in the

return of any of your principal amount in excess of $300.00 per $1,000.00 principal amount note, subject to the credit risks of JPMorgan

Financial and JPMorgan Chase & Co.

Historical Performance of the S&P 500

®

Futures Excess Return Index

Source: Bloomberg

PS-8| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

Tax Treatment

You should review carefully the section entitled “Material U.S. Federal Income Tax Consequences” in the accompanying product

supplement no. 4-I. The following discussion, when read in combination with that section, constitutes the full opinion of our special tax

counsel, Davis Polk & Wardwell LLP, regarding the material U.S. federal income tax consequences of owning and disposing of notes.

Based on current market conditions, in the opinion of our special tax counsel it is reasonable to treat the notes as “open transactions”

that are not debt instruments for U.S. federal income tax purposes, as more fully described in “Material U.S. Federal Income Tax

Consequences — Tax Consequences to U.S. Holders — Notes Treated as Open Transactions That Are Not Debt Instruments” in the

accompanying product supplement. Assuming this treatment is respected, the gain or loss on your notes should be treated as long-term

capital gain or loss if you hold your notes for more than a year, whether or not you are an initial purchaser of notes at the issue price.

However, the IRS or a court may not respect this treatment, in which case the timing and character of any income or loss on the notes

could be materially and adversely affected. In addition, in 2007 Treasury and the IRS released a notice requesting comments on the

U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments. The notice focuses in particular on whether to

require investors in these instruments to accrue income over the term of their investment. It also asks for comments on a number of

related topics, including the character of income or loss with respect to these instruments; the relevance of factors such as the nature of

the underlying property to which the instruments are linked; the degree, if any, to which income (including any mandated accruals)

realized by non-U.S. investors should be subject to withholding tax; and whether these instruments are or should be subject to the

“constructive ownership” regime, which very generally can operate to recharacterize certain long-term capital gain as ordinary income

and impose a notional interest charge. While the notice requests comments on appropriate transition rules and effective dates, any

Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax

consequences of an investment in the notes, possibly with retroactive effect. You should consult your tax adviser regarding the U.S.

federal income tax consequences of an investment in the notes, including possible alternative treatments and the issues presented by

this notice.

Section 871(m) of the Code and Treasury regulations promulgated thereunder (“Section 871(m)”) generally impose a 30% withholding

tax (unless an income tax treaty applies) on dividend equivalents paid or deemed paid to Non-U.S. Holders with respect to certain

financial instruments linked to U.S. equities or indices that include U.S. equities. Section 871(m) provides certain exceptions to this

withholding regime, including for instruments linked to certain broad-based indices that meet requirements set forth in the applicable

Treasury regulations. Additionally, a recent IRS notice excludes from the scope of Section 871(m) instruments issued prior to January

1, 2027 that do not have a delta of one with respect to underlying securities that could pay U.S.-source dividends for U.S. federal

income tax purposes (each an “Underlying Security”). Based on certain determinations made by us, our special tax counsel is of the

opinion that Section 871(m) should not apply to the notes with regard to Non-U.S. Holders. Our determination is not binding on the IRS,

and the IRS may disagree with this determination. Section 871(m) is complex and its application may depend on your particular

circumstances, including whether you enter into other transactions with respect to an Underlying Security. You should consult your tax

adviser regarding the potential application of Section 871(m) to the notes.

The Estimated Value of the Notes

The estimated value of the notes set forth on the cover of this pricing supplement is equal to the sum of the values of the following

hypothetical components: (1) a fixed-income debt component with the same maturity as the notes, valued using the internal funding

rate described below, and (2) the derivative or derivatives underlying the economic terms of the notes. The estimated value of the notes

does not represent a minimum price at which JPMS would be willing to buy your notes in any secondary market (if any exists) at any

time. The internal funding rate used in the determination of the estimated value of the notes may differ from the market-implied funding

rate for vanilla fixed income instruments of a similar maturity issued by JPMorgan Chase & Co. or its affiliates. Any difference may be

based on, among other things, our and our affiliates’ view of the funding value of the notes as well as the higher issuance, operational

and ongoing liability management costs of the notes in comparison to those costs for the conventional fixed income instruments of

JPMorgan Chase & Co. This internal funding rate is based on certain market inputs and assumptions, which may prove to be incorrect,

and is intended to approximate the prevailing market replacement funding rate for the notes. The use of an internal funding rate and

any potential changes to that rate may have an adverse effect on the terms of the notes and any secondary market prices of the notes.

For additional information, see “Selected Risk Considerations — Risks Relating to the Estimated Value and Secondary Market Prices of

the Notes — The Estimated Value of the Notes Is Derived by Reference to an Internal Funding Rate” in this pricing supplement.

The value of the derivative or derivatives underlying the economic terms of the notes is derived from internal pricing models of our

affiliates. These models are dependent on inputs such as the traded market prices of comparable derivative instruments and on various

other inputs, some of which are market-observable, and which can include volatility, dividend rates, interest rates and other factors, as

well as assumptions about future market events and/or environments. Accordingly, the estimated value of the notes is determined when

the terms of the notes are set based on market conditions and other relevant factors and assumptions existing at that time.

PS-9| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

The estimated value of the notes does not represent future values of the notes and may differ from others’ estimates. Different pricing

models and assumptions could provide valuations for the notes that are greater than or less than the estimated value of the notes. In

addition, market conditions and other relevant factors in the future may change, and any assumptions may prove to be incorrect. On

future dates, the value of the notes could change significantly based on, among other things, changes in market conditions, our or

JPMorgan Chase & Co.’s creditworthiness, interest rate movements and other relevant factors, which may impact the price, if any, at

which JPMS would be willing to buy notes from you in secondary market transactions.

The estimated value of the notes is lower than the original issue price of the notes because costs associated with selling, structuring

and hedging the notes are included in the original issue price of the notes. These costs include the selling commissions paid to JPMS

and other affiliated or unaffiliated dealers, the projected profits, if any, that our affiliates expect to realize for assuming risks inherent in

hedging our obligations under the notes and the estimated cost of hedging our obligations under the notes. Because hedging our

obligations entails risk and may be influenced by market forces beyond our control, this hedging may result in a profit that is more or

less than expected, or it may result in a loss. A portion of the profits, if any, realized in hedging our obligations under the notes may be

allowed to other affiliated or unaffiliated dealers, and we or one or more of our affiliates will retain any remaining hedging profits. See

“Selected Risk Considerations — Risks Relating to the Estimated Value and Secondary Market Prices of the Notes — The Estimated

Value of the Notes Is Lower Than the Original Issue Price (Price to Public) of the Notes” in this pricing supplement.

Secondary Market Prices of the Notes

For information about factors that will impact any secondary market prices of the notes, see “Risk Factors — Risks Relating to the

Estimated Value and Secondary Market Prices of the Notes — Secondary market prices of the notes will be impacted by many

economic and market factors” in the accompanying product supplement. In addition, we generally expect that some of the costs

included in the original issue price of the notes will be partially paid back to you in connection with any repurchases of your notes by

JPMS in an amount that will decline to zero over an initial predetermined period. These costs can include selling commissions,

projected hedging profits, if any, and, in some circumstances, estimated hedging costs and our internal secondary market funding rates

for structured debt issuances. This initial predetermined time period is intended to be the shorter of six months and one-half of the

stated term of the notes. The length of any such initial period reflects the structure of the notes, whether our affiliates expect to earn a

profit in connection with our hedging activities, the estimated costs of hedging the notes and when these costs are incurred, as

determined by our affiliates. See “Selected Risk Considerations — Risks Relating to the Estimated Value and Secondary Market Prices

of the Notes — The Value of the Notes as Published by JPMS (and Which May Be Reflected on Customer Account Statements) May

Be Higher Than the Then-Current Estimated Value of the Notes for a Limited Time Period” in this pricing supplement.

Supplemental Use of Proceeds

The notes are offered to meet investor demand for products that reflect the risk-return profile and market exposure provided by the

notes. See “Hypothetical Payout Profile” and “How the Notes Work” in this pricing supplement for an illustration of the risk-return profile

of the notes and “The Index” in this pricing supplement for a description of the market exposure provided by the notes.

The original issue price of the notes is equal to the estimated value of the notes plus the selling commissions paid to JPMS and other

affiliated or unaffiliated dealers, plus (minus) the projected profits (losses) that our affiliates expect to realize for assuming risks inherent

in hedging our obligations under the notes, plus the estimated cost of hedging our obligations under the notes.

Validity of the Notes and the Guarantee

In the opinion of Davis Polk & Wardwell LLP, as special products counsel to JPMorgan Financial and JPMorgan Chase & Co., when the

notes offered by this pricing supplement have been issued by JPMorgan Financial pursuant to the indenture, the trustee and/or paying

agent has made, in accordance with the instructions from JPMorgan Financial, the appropriate entries or notations in its records relating

to the master global note that represents such notes (the “master note”), and such notes have been delivered against payment as

contemplated herein, such notes will be valid and binding obligations of JPMorgan Financial and the related guarantee will constitute a

valid and binding obligation of JPMorgan Chase & Co., enforceable in accordance with their terms, subject to applicable bankruptcy,

insolvency and similar laws affecting creditors’ rights generally, concepts of reasonableness and equitable principles of general

applicability (including, without limitation, concepts of good faith, fair dealing and the lack of bad faith), provided that such counsel

expresses no opinion as to (i) the effect of fraudulent conveyance, fraudulent transfer or similar provision of applicable law on the

conclusions expressed above or (ii) any provision of the indenture that purports to avoid the effect of fraudulent conveyance, fraudulent

transfer or similar provision of applicable law by limiting the amount of JPMorgan Chase & Co.’s obligation under the related guarantee.

This opinion is given as of the date hereof and is limited to the laws of the State of New York, the General Corporation Law of the State

of Delaware and the Delaware Limited Liability Company Act. In addition, this opinion is subject to customary assumptions about the

trustee’s authorization, execution and delivery of the indenture and its authentication of the master note and the validity, binding nature

and enforceability of the indenture with respect to the trustee, all as stated in the letter of such counsel dated February 24, 2023, which

was filed as an exhibit to the Registration Statement on Form S-3 by JPMorgan Financial and JPMorgan Chase & Co. on February 24,

2023.

PS-10| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

Additional Terms Specific to the Notes

You should read this pricing supplement together with the accompanying prospectus, as supplemented by the accompanying

prospectus supplement relating to our Series A medium-term notes of which these notes are a part, the accompanying prospectus

addendum and the more detailed information contained in the accompanying product supplement and the accompanying underlying

supplement. This pricing supplement, together with the documents listed below, contains the terms of the notes and supersedes all

other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms,

correspondence, trade ideas, structures for implementation, sample structures, fact sheets, brochures or other educational materials of

ours. You should carefully consider, among other things, the matters set forth in the “Risk Factors” sections of the accompanying

prospectus supplement and the accompanying product supplement and in Annex A to the accompanying prospectus addendum, as the

notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and

other advisers before you invest in the notes.

You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by

reviewing our filings for the relevant date on the SEC website):

● Product supplement no. 4-I dated April 13, 2023:

● Underlying supplement no. 1-I dated April 13, 2023:

● Prospectus supplement and prospectus, each dated April 13, 2023:

● Prospectus addendum dated June 3, 2024:

Our Central Index Key, or CIK, on the SEC website is 1665650, and JPMorgan Chase & Co.’s CIK is 19617. As used in this pricing

supplement, “we,” “us” and “our” refer to JPMorgan Financial.

PS-11| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

Annex A

The S&P 500

®

Futures Excess Return Index

All information contained in this pricing supplement regarding the S&P 500

®

Futures Excess Return Index (the “SPX Futures Index”),

including, without limitation, its make-up, method of calculation and changes in its components, has been derived from publicly

available information, without independent verification. This information reflects the policies of, and is subject to change by, S&P Dow

Jones Indices LLC (“S&P Dow Jones”). The SPX Futures Index is calculated, maintained and published by S&P Dow Jones. S&P Dow

Jones has no obligation to continue to publish, and may discontinue the publication of, the SPX Futures Index.

The SPX Futures Index is reported by Bloomberg L.P. under the ticker symbol “SPXFP.”

The SPX Futures Index measures the performance of the nearest maturing quarterly E-mini

®

S&P 500

®

futures contracts (Symbol: ES)

(the “Underlying Futures Contracts”) trading on the Chicago Mercantile Exchange (the “Exchange”). E-mini

®

S&P 500

®

futures

contracts are U.S. dollar-denominated futures contracts based on the S&P 500

®

Index. For additional information about the S&P 500

®

Index, see “Equity Index Descriptions — The S&P U.S. Indices” in the accompanying underlying supplement. The SPX Futures Index

is calculated real-time from the price change of the Underlying Futures Contracts. The SPX Futures Index is an “excess return” index

that is based on price levels of the Underlying Futures Contracts as well as the discount or premium obtained by “rolling” hypothetical

positions in the Underlying Futures Contracts as they approach delivery. The SPX Futures Index does not reflect interest earned on

hypothetical, fully collateralized contract positions.

Index Rolling

As each Underlying Futures Contract approaches maturity, it is replaced by the next maturing Underlying Futures Contract in a process

referred to as “rolling.” The rolling of the SPX Futures Index occurs quarterly over a one-day rolling period (the “roll day”) every March,

June, September and December, effective after the close of trading five business days preceding the last trading date of the maturing

Underlying Futures Contract.

On any scheduled roll day, the occurrence of either of the following circumstances will result in an adjustment of the roll day according

to the procedure set forth in this section:

● An exchange holiday occurs on that scheduled roll day.

● The daily contract price of any Underlying Futures Contract within the index on that scheduled roll day is a limit price.

If either of the above events occur, the relevant roll day will take place on the next designated commodity index business day whereby

none of the circumstances identified take place.

If a disruption is approaching the last trading day of a contract expiration, the Index Committee (defined below) will convene to

determine the appropriate course of action, which may include guidance from the Exchange.

The Index Committee may change the date of a given rebalancing for reasons including market holidays occurring on or around the

scheduled rebalancing date. Any such change will be announced with proper advance notice where possible.

Index Calculations

The closing level of the SPX Futures Index on any trading day reflects the change in the daily contract price of the Underlying Futures

Contract since the immediately preceding trading day. On each quarterly roll day, the closing level of the SPX Futures Index reflects

the change from the daily contract price of the maturing Underlying Futures Contract on the immediately preceding trading day to the

daily contract price of the next maturing Underlying Futures Contract on that roll day.

The daily contract price of an Underlying Futures Contract will be the settlement price reported by the Exchange. If the Exchange fails

to open due to unforeseen circumstances, such as natural disasters, inclement weather, outages, or other events, the SPX Futures

Index uses the prior daily contract prices. In situations where the Exchange is forced to close early due to unforeseen events, such as

computer or electric power failures, weather conditions or other events, S&P Dow Jones calculates the closing level of the SPX Futures

Index based on (1) the daily contract price published by the Exchange, or (2) if no daily contract price is available, the Index Committee

determines the course of action and notifies clients accordingly.

Index Corrections and Recalculations

S&P Dow Jones reserves the right to recalculate an index at its discretion in the event that settlement prices are amended or upon the

occurrence of a missed index methodology event (deviation from what is stated in the methodology document).

PS-12| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

Index Governance

An S&P Dow Jones index committee (the “Index Committee”) maintains the SPX Futures Index. All committee members are full-time

professional members of S&P Dow Jones’ staff. The Index Committee may revise index policy covering rules for including currencies,

the timing of rebalancing or other matters. The Index Committee considers information about changes to the SPX Futures Index and

related matters to be potentially market moving and material. Therefore, all Index Committee discussions are confidential.

The Index Committees reserve the right to make exceptions when applying the methodology of the SPX Futures Index if the need

arises. In any scenario where the treatment differs from the general rules stated in this document or supplemental documents, notice

will be provided, whenever possible.

In addition to the daily governance of the SPX Futures Index and maintenance of its index methodology, at least once within any 12-

month period, the Index Committee reviews the methodology to ensure the SPX Futures Index continues to achieve the stated

objectives, and that the data and methodology remain effective. In certain instances, S&P Dow Jones may publish a consultation

inviting comments from external parties.

License Agreement

JPMorgan Chase & Co. or its affiliate has entered into an agreement with S&P Dow Jones that provides it and certain of its affiliates or

subsidiaries, including JPMorgan Financial, with a non-exclusive license and, for a fee, with the right to use the SPX Futures Index,

which is owned and published by S&P Dow Jones, in connection with certain securities, including the notes.

The notes are not sponsored, endorsed, sold or promoted by S&P Dow Jones or its third-party licensors. Neither S&P Dow Jones nor

its third-party licensors make any representation or warranty, express or implied, to the owners of the notes or any member of the public

regarding the advisability of investing in securities generally or in the notes particularly or the ability of the SPX Futures Index to track

general stock market performance. S&P Dow Jones’ and its third-party licensors’ only relationship to JPMorgan Financial or JPMorgan

Chase & Co. is the licensing of certain trademarks and trade names of S&P Dow Jones and the third-party licensors and of the SPX

Futures Index which is determined, composed and calculated by S&P Dow Jones or its third-party licensors without regard to JPMorgan

Financial or JPMorgan Chase & Co. or the notes. S&P Dow Jones and its third-party licensors have no obligation to take the needs of

JPMorgan Financial or JPMorgan Chase & Co. or the owners of the notes into consideration in determining, composing or calculating

the SPX Futures Index. Neither S&P Dow Jones nor its third-party licensors are responsible for and has not participated in the

determination of the prices and amount of the notes or the timing of the issuance or sale of the notes or in the determination or

calculation of the equation by which the notes are to be converted into cash. S&P Dow Jones has no obligation or liability in connection

with the administration, marketing or trading of the notes.

NEITHER S&P DOW JONES, ITS AFFILIATES NOR THEIR THIRD-PARTY LICENSORS GUARANTEE THE ADEQUACY,

ACCURACY, TIMELINESS OR COMPLETENESS OF THE SPX FUTURES INDEX OR ANY DATA INCLUDED THEREIN OR ANY

COMMUNICATIONS, INCLUDING BUT NOT LIMITED TO, ORAL OR WRITTEN COMMUNICATIONS (INCLUDING ELECTRONIC

COMMUNICATIONS) WITH RESPECT THERETO. S&P DOW JONES, ITS AFFILIATES AND THEIR THIRD-PARTY LICENSORS

SHALL NOT BE SUBJECT TO ANY DAMAGES OR LIABILITY FOR ANY ERRORS, OMISSIONS OR DELAYS THEREIN. S&P DOW

JONES MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF

MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE WITH RESPECT TO THE MARKS, THE SPX

FUTURES INDEX OR ANY DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT

WHATSOEVER SHALL S&P DOW JONES, ITS AFFILIATES OR THEIR THIRD-PARTY LICENSORS BE LIABLE FOR ANY

INDIRECT, SPECIAL, INCIDENTAL, PUNITIVE OR CONSEQUENTIAL DAMAGES, INCLUDING BUT NOT LIMITED TO, LOSS OF

PROFITS, TRADING LOSSES, LOST TIME OR GOODWILL, EVEN IF THEY HAVE BEEN ADVISED OF THE POSSIBILITY OF

SUCH DAMAGES, WHETHER IN CONTRACT, TORT, STRICT LIABILITY OR OTHERWISE.

“S&P

®

” and “S&P 500

®

” are trademarks of S&P Global, Inc. or its affiliates and have been licensed for use by JPMorgan Chase & Co.

and its affiliates, including JPMorgan Financial.

Background on Futures Contracts

Overview of Futures Markets

Futures contracts are contracts that legally obligate the holder to buy or sell an asset at a predetermined delivery price during a

specified future time period. Futures contracts are traded on regulated futures exchanges, in the over-the-counter market and on

various types of physical and electronic trading facilities and markets. An exchange-traded futures contract provides for the purchase

and sale of a specified type and quantity of an underlying asset or financial instrument during a stated delivery month for a fixed price.

A futures contract provides for a specified settlement month in which the cash settlement is made or in which the underlying asset or

financial instrument is to be delivered by the seller (whose position is therefore described as “short”) and acquired by the purchaser

(whose position is therefore described as “long”).

No purchase price is paid or received on the purchase or sale of a futures contract. Instead, an amount of cash or cash equivalents

must be deposited with the broker as “initial margin.” This amount varies based on the requirements imposed by the exchange clearing

PS-13| Structured Investments

Uncapped Dual Directional Buffered Return Enhanced Notes Linked to the S&P 500

®

Futures Excess Return Index

houses, but it may be lower than 5% of the notional value of the contract. This margin deposit provides collateral for the obligations of

the parties to the futures contract.

By depositing margin, which may vary in form depending on the exchange, with the clearing house or broker involved, a market

participant may be able to earn interest on its margin funds, thereby increasing the total return that it may realize from an investment in

futures contracts.

In the United States, futures contracts are traded on designated contract markets. At any time prior to the expiration of a futures

contract, a trader may elect to close out its position by taking an opposite position on the exchange on which the trader obtained the

position, subject to the availability of a liquid secondary market. This operates to terminate the position and fix the trader’s profit or loss.

Futures contracts are cleared through the facilities of a centralized clearing house and a brokerage firm, referred to as a “futures

commission merchant,” which is a member of the clearing house.

Unlike common equity securities, futures contracts, by their terms, have stated expirations. At a specific point in time prior to expiration,

trading in a futures contract for the current delivery month will cease. As a result, a market participant wishing to maintain its exposure

to a futures contract on a particular asset or financial instrument with the nearest expiration must close out its position in the expiring

contract and establish a new position in the contract for the next delivery month, a process referred to as “rolling.” For example, a

market participant with a long position in a futures contract expiring in November who wishes to maintain a position in the nearest

delivery month will, as the November contract nears expiration, sell the November contract, which serves to close out the existing long

position, and buy a futures contract expiring in December. This will “roll” the November position into a December position, and, when

the November contract expires, the market participant will still have a long position in the nearest delivery month.

Futures exchanges and clearing houses in the United States are subject to regulation by the Commodity Futures Trading Commission

(the “CFTC”). Exchanges may adopt rules and take other actions that affect trading, including imposing speculative position limits,

maximum price fluctuations and trading halts and suspensions and requiring liquidation of contracts in certain circumstances. Futures

markets outside the United States are generally subject to regulation by foreign regulatory authorities comparable to the CFTC. The

structure and nature of trading on non-U.S. exchanges, however, may differ from the above description.

Underlying Futures Contracts

E-mini

®

S&P 500

®

futures contracts are U.S. dollar-denominated futures contracts, based on the S&P 500

®

Index, traded on the

Exchange, representing a contract unit of $50 multiplied by the S&P 500

®

Index, measured in cents per index point.

E-mini

®

S&P 500

®

futures contracts listed for the nearest nine quarters, for each March, June, September and December, and the

nearest three Decembers are available for trading. Trading of the E-mini

®

S&P 500

®

futures contracts will terminate at 9:30 A.M.

Eastern time on the third Friday of the contract month.

The daily settlement prices of the E-mini

®

S&P 500

®

futures contracts are based on trading activity in the relevant contract (and in the

case of a lead month also being the expiry month, together with trading activity on lead month-second month spread contracts) on the

Exchange during a specified settlement period. The final settlement price of E-mini

®

S&P 500

®

futures contracts is based on the

opening prices of the component stocks in the S&P 500

®

Index, determined on the third Friday of the contract month.