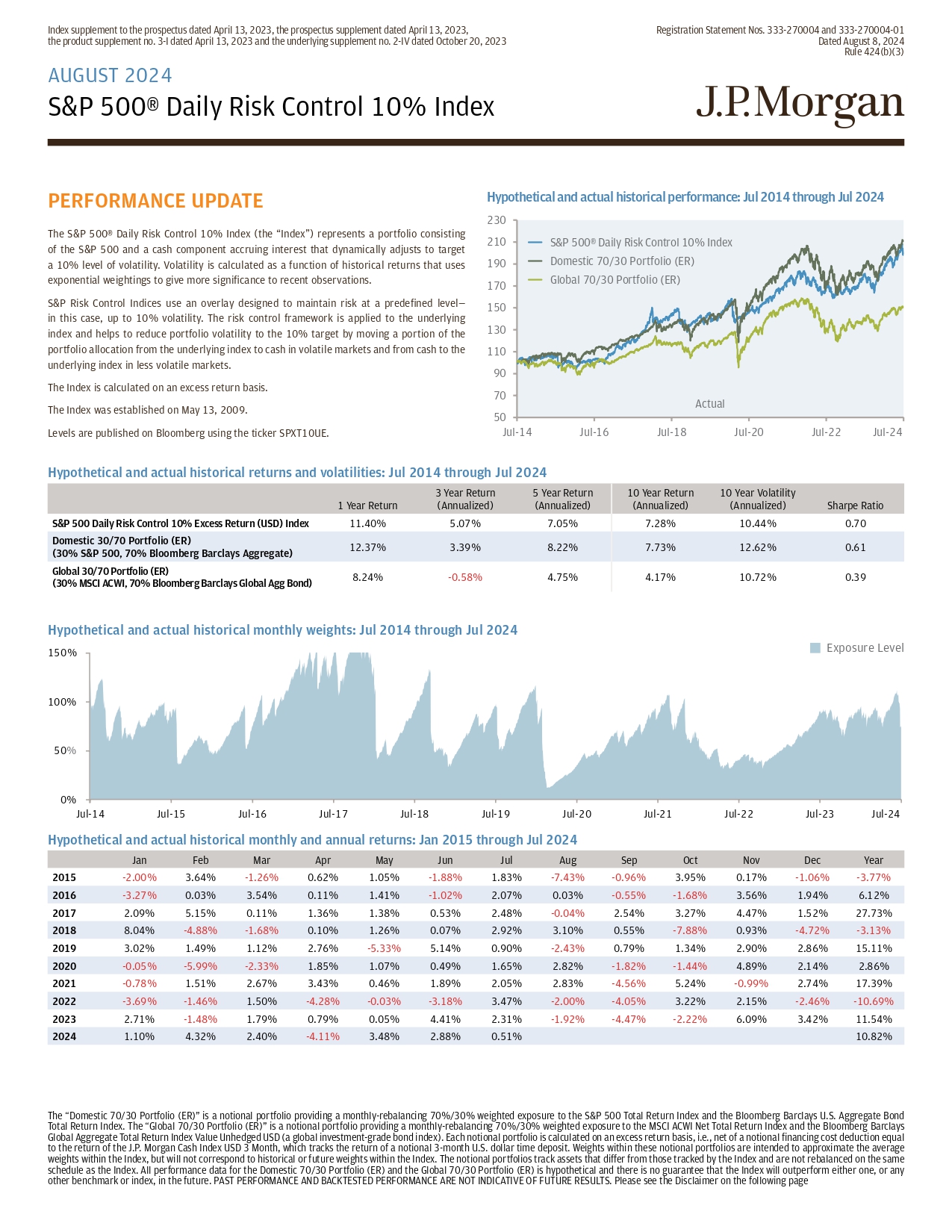

Index supplement to the prospectus dated April 13, 2023, the prospectus supplement dated April 13, 2023, the product supplement no. 3 - I dated April 13, 2023 and the underlying supplement no. 2 - IV dated October 20, 2023 Registration Statement Nos. 333 - 270004 and 333 - 270004 - 01 D ate d A ugus t 8 , 2024 Rul e 424(b)(3) A UGU S T 2024 S&P 500® D aily Risk C o n t r ol 10% Ind e x The “Domestic 70 / 30 Portfolio (ER)” is a notional portfolio providing a monthly - rebalancing 70 % / 30 % weighted exposure to the S&P 500 Total Return Index and the Bloomberg Barclays U . S . Aggregate Bond Total Return Index . The “Global 70 / 30 Portfolio (ER)” is a notional portfolio providing a monthly - rebalancing 70 % / 30 % weighted exposure to the MSCI ACWI Net Total Return Index and the Bloomberg Barclays Global Aggregate Total Return Index Value Unhedged USD (a global investment - grade bond index) . Each notional portfolio is calculated on an excess return basis, i . e . , net of a notional financing cost deduction equal to the return of the J . P . Morgan Cash Index USD 3 Month, which tracks the return of a notional 3 - month U . S . dollar time deposit . Weights within these notional portfolios are intended to approximate the average weights within the Index, but will not correspond to historical or future weights within the Index . The notional portfolios track assets that differ from those tracked by the Index and are not rebalanced on the same schedule as the Index . All performance data for the Domestic 70 / 30 Portfolio (ER) and the Global 70 / 30 Portfolio (ER) is hypothetical and there is no guarantee that the Index will outperform either one, or any other benchmark or index, in the future . PAST PERFORMANCE AND BACKTESTED PERFORMANCE ARE NOT INDICATIVE OF FUTURE RESULTS . Please see the Disclaimer on the following page Hypothetical and actual historical performance: Jul 2014 through Jul 2024 PER F ORMANCE UP D A TE 230 Th e S& P 500 ® D ail y Ris k C o n tr o l 10% Ind ex (th e “Ind e x” ) r ep r ese n t s a po r t f oli o c onsisti n g of the S&P 500 and a cash component accruing interest that dynamically adjusts to target 210 a 10 % level of volatility . Volatility is calculated as a function of historical returns that uses 190 e xpone n tia l w eig h tin g s t o gi v e mo r e significan c e t o r ec e n t obse r v ations . 1 7 0 S&P Risk Control Indices use an overlay designed to maintain risk at a predefined level — 150 in this case, up to 10% volatility. The risk control framework is applied to the underlying index and helps to reduce portfolio volatility to the 10 % target by moving a portion of the 130 portfolio allocation from the underlying index to cash in volatile markets and from cash to the 110 underlyi n g ind e x i n les s v olatil e mar k ets . 90 The Index is calculated on an excess return basis. 70 The Index was established on May 13, 2009. 50 Levels are published on Bloomberg using the ticker SPXT10UE. J u l - 14 J u l - 16 J u l - 18 J u l - 20 J u l - 22 J u l - 24 S& P 500 ® Dail y Ris k Contro l 10 % Inde x D o mesti c 70/3 0 P o r t f o lio (ER) G loba l 7 0 /30 P o r t fo l i o (ER) Actual Hypothetical and actual historical returns and volatilities: Jul 2014 through Jul 2024 Sharpe Ratio 10 Y ear V olatili t y (Annualized) 10 Y ear R eturn (Annualized) 5 Y ear R eturn (Annualized) 3 Y ear R eturn (Annualized) 1 Y ear R eturn 0.70 10.44% 7.28% 7.05% 5.07% 11.40% S&P 500 Daily Risk Control 10% Excess Return (USD) Index 0.61 12.62% 7.73% 8.22% 3.39% 12.37% Domestic 30/70 P o r tf olio (ER) (30% S&P 500, 70% Bloombe r g Ba r cl a ys A g g r e ga te) 0.39 10.72% 4.17% 4.75% - 0.58% 8.24% Globa l 30/7 0 Po r tfoli o (ER) (30% MSCI ACWI, 70% Bloomberg Barclays Global Agg Bond) Hypothetical and actual historical monthly weights: Jul 2014 through Jul 2024 J u l - 21 J u l - 22 J u l - 23 J u l - 24 Exposur e Level 0% J u l - 1 4 J u l - 1 5 J u l - 1 6 J u l - 1 7 J u l - 1 8 J u l - 1 9 J u l - 20 Hypothetical and actual historical monthly and annual returns: Jan 2015 through Jul 2024 5 0 % 1 0 0% 150 % Year Dec Nov Oct Sep Aug Jul Jun May Apr Mar Feb Jan - 3.77% - 1.06% 0.17% 3.95% - 0.96% - 7.43% 1.83% - 1.88% 1.05% 0.62% - 1.26% 3.64% - 2.00% 2015 6.12% 1.94% 3.56% - 1.68% - 0.55% 0.03% 2.07% - 1.02% 1.41% 0.11% 3.54% 0.03% - 3.27% 2016 27.73% 1.52% 4.47% 3.27% 2.54% - 0.04% 2.48% 0.53% 1.38% 1.36% 0.11% 5.15% 2.09% 2017 - 3.13% - 4.72% 0.93% - 7.88% 0.55% 3.10% 2.92% 0.07% 1.26% 0.10% - 1.68% - 4.88% 8.04% 2018 15.11% 2.86% 2.90% 1.34% 0.79% - 2.43% 0.90% 5.14% - 5.33% 2.76% 1.12% 1.49% 3.02% 2019 2.86% 2.14% 4.89% - 1.44% - 1.82% 2.82% 1.65% 0.49% 1.07% 1.85% - 2.33% - 5.99% - 0.05% 2020 17.39% 2.74% - 0.99% 5.24% - 4.56% 2.83% 2.05% 1.89% 0.46% 3.43% 2.67% 1.51% - 0.78% 2021 - 10.69% - 2.46% 2.15% 3.22% - 4.05% - 2.00% 3.47% - 3.18% - 0.03% - 4.28% 1.50% - 1.46% - 3.69% 2022 11.54% 3.42% 6.09% - 2.22% - 4.47% - 1.92% 2.31% 4.41% 0.05% 0.79% 1.79% - 1.48% 2.71% 2023 10.82% 0.51% 2.88% 3.48% - 4.11% 2.40% 4.32% 1.10% 2024

AUGUST 2024 | S&P 500® Daily Risk Control 10% Index S electe d Risks JPMorgan Chase & Co. is currently one of the companies that make up the underlying index The Index may not be successful and may not outperform or underperform the underlying index The Index may not approximate its target volatility of 10% The daily adjustment of the exposure of the Index to the underlying index may cause the Index not to reflect fully any appreciation of the underlying index or to magnify any depreciation of the underlying index The Index may be significantly uninvested, which will result in a portion of the Index reflecting no return The level of the Index reflects the deduction of a notional financing cost The Index’s methodology for calculating the notional financing cost was recently changed The risks identified above are not exhaustive. You should also review carefully the related “Risk Factors” section in the prospectus supplement and the relevant product supplement and underlying supplement and the “Selected Risk Considerations” in the relevant pricing supplement. Disclaimer The information contained in this document is for discussion purposes only . Any information relating to performance contained in these materials is illustrative and no assurance is given that any indicative returns, performance or results, whether historical or hypothetical, will be achieved . These terms are subject to change, and J . P . Morgan undertakes no duty to update this information . This document shall be amended, superseded and replaced in its entirety by a subsequent term sheet and/or disclosure supplement, and the documents referred to therein . In the event any inconsistency between the information presented herein and any such term sheet and/or disclosure supplement, such term sheet and/or disclosure supplement shall govern . The 10 Year Volatility (Annualized) on the previous page is a measure of market risk, calculated as of the square root of two hundred and fifty - two ( 252 ) multiplied by the sample standard deviation of the daily logarithmic returns of each applicable index or portfolio (considering only days for which levels are available for all three) over the preceding 10 years . The Sharpe Ratio on the previous page is a measure of risk - adjusted performance, calculated as the 10 Year Return (Annualized) divided by the 10 Year Volatility (Annualized) . Investment suitability must be determined individually for each investor, and CDnotes linked to the Index may not be suitable for all investors . This material is not a product of J . P . Morgan Research Departments . Copyright © 2024 JPMorgan Chase & Co . All rights reserved . For additional regulatory disclosures, please consult : www . jpmorgan . com/disclosures . Information contained on this website is not incorporated by reference in, and should not be considered part of, this document . This monthly update document replaces and supersedes all prior written materials of this type previously provided with respect to the Index .