Table of Contents

As filed with the Securities and Exchange Commission on October 26, 2021

Registration Statement No. 333-260140

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

Form S-11

FOR REGISTRATION UNDER THE SECURITIES ACT OF 1933

OF SECURITIES OF CERTAIN REAL ESTATE COMPANIES

Claros Mortgage Trust, Inc.

(Exact name of registrant as specified in its governing instruments)

c/o Mack Real Estate Credit Strategies, L.P.

60 Columbus Circle, 20th Floor

New York, NY 10023

(212) 484-0050

(Address, including Zip Code, and Telephone Number, including Area Code, of Registrant’s Principal Executive Offices)

J.D. Siegel, Esq.

c/o Mack Real Estate Credit Strategies, L.P.

60 Columbus Circle, 20th Floor

New York, NY 10023

(212) 484-0050

(Name, Address, including Zip Code, and Telephone Number, including Area Code, of Agent for Service)

Copies to:

William J. Cernius, Esq. Brent T. Epstein, Esq. | Edward F. Petrosky, Esq. James O’Connor, Esq. | |

| Latham & Watkins LLP | Sidley Austin LLP | |

| 650 Town Center Drive, 20th Floor | 787 Seventh Avenue | |

| Costa Mesa, CA 92626 | New York, NY 10019 | |

| Tel (714) 755-8172 | Tel (212) 839-5300 | |

| Fax (714) 755-8290 | Fax (212) 839-5599 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this registration statement.

If any of the Securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

| ||||||||

Title of Each Class of Securities to be Registered | Amount to be Registered(1) | Proposed Maximum Offering Price Per Share(2) | Proposed Maximum Offering Price(1)(2) | Amount of Registration Fee(3) | ||||

Common Stock, $0.01 par value per share | 8,050,000 | $19.65 | $158,182,500 | $14,664 | ||||

| ||||||||

| ||||||||

| (1) | Includes 1,050,000 shares of common stock that the underwriters have the option to purchase. |

| (2) | Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(a) under the Securities Act of 1933, as amended. |

| (3) | $9,270 of the registration fee was paid with the initial filing of the Registration Statement on October 8, 2021. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED OCTOBER 26, 2021

PRELIMINARY PROSPECTUS

7,000,000 Shares

Claros Mortgage Trust, Inc.

Common Stock

Claros Mortgage Trust, Inc., a Maryland corporation, is focused primarily on originating senior and subordinate loans on transitional commercial real estate assets located in major U.S. markets. We are externally managed and advised by Claros REIT Management LP, or our Manager, under the terms of a management agreement.

This is our initial public offering and no public market currently exists for our common stock. We are offering all of the 7,000,000 shares of our common stock as described in this prospectus. We currently anticipate the initial public offering price of our common stock will be between $18.65 and $19.65 per share. We have applied to list our common stock on the New York Stock Exchange, or the NYSE, under the symbol “CMTG.”

We have elected and believe we have qualified to be taxed as a real estate investment trust, or a REIT, for U.S. federal income tax purposes commencing with our taxable year ended December 31, 2015. To assist us in qualifying as a REIT, our charter prohibits, with certain exceptions, the beneficial or constructive ownership by any person of more than 9.6% in value of the aggregate of the outstanding shares of our capital stock or more than 9.6% (in value or in number of shares, whichever is more restrictive) of the aggregate of the outstanding shares of our common stock. In addition, our charter contains various other restrictions on the ownership and transfer of our common stock and capital stock. See “Description of Capital Stock—Restrictions on Ownership and Transfer.”

We are an “emerging growth company” as defined in Section 2(a) of the Securities Act of 1933, as amended, or the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, and, as such, have elected to comply with certain reduced public company reporting requirements for this prospectus and future filings. See “Summary—Implications of Being an Emerging Growth Company.”

Investing in our common stock involves risks. You should read the section entitled “Risk Factors” beginning on page 50 of this prospectus for a discussion of certain risk factors that you should consider before making a decision to invest in our common stock.

| Per Share | Total | |||||||

Initial public offering price | $ | $ | ||||||

Underwriting discount(1) | $ | $ | ||||||

Proceeds, before expenses, to us | $ | $ | ||||||

| (1) | See “Underwriting” for a description of the compensation payable to the underwriters. |

We have granted the underwriters a 30-day option to purchase up to an additional 1,050,000 shares of common stock from us at the initial public offering price less the underwriting discount.

None of the Securities and Exchange Commission, any state securities commission, or any other regulatory body has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares on or about , 2021.

Joint Lead Book-Running Managers

| Morgan Stanley | J.P. Morgan |

Joint Book-Running Managers

| Goldman Sachs & Co. LLC | Deutsche Bank Securities | UBS Investment Bank | Wells Fargo Securities | |||

| JMP Securities | Keefe, Bruyette & Woods A Stifel Company | |

The date of this prospectus is , 2021.

Table of Contents

| Page | ||||

| 1 | ||||

| 50 | ||||

| 114 | ||||

| 116 | ||||

| 117 | ||||

| 119 | ||||

| 121 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 123 | |||

| 177 | ||||

| 217 | ||||

| 232 | ||||

| 241 | ||||

| 244 | ||||

| 251 | ||||

CERTAIN PROVISIONS OF MARYLAND LAW AND OUR CHARTER AND BYLAWS | 257 | |||

| 264 | ||||

| 266 | ||||

| 291 | ||||

| 294 | ||||

| 302 | ||||

| 302 | ||||

| 302 | ||||

| F-1 | ||||

i

Table of Contents

You should rely only on the information contained in this prospectus. We have not, and the underwriters have not, authorized any other person to provide you with different or additional information. If anyone provides you with different or additional information, you should not rely on it. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of its date or on the date or dates which are specified herein. Our business, financial condition, liquidity, results of operations and prospects may have changed since those dates.

MARKET AND OTHER INDUSTRY DATA

This prospectus includes market and other industry data and estimates, as well as estimates that are based on our Manager’s knowledge and experience in the markets in which we operate. The sources of these third-party data and estimates generally state that the information they provide has been obtained from sources they believe to be reliable, but we have not investigated or verified the accuracy and completeness of this information. Our own estimates are based on information obtained from our Manager’s experience in the markets in which we operate and from other contacts in these markets. We are responsible for all of the disclosure in this prospectus, and we believe our estimates to be accurate as of the date of this prospectus or any other date stated in this prospectus. However, this information may prove to be inaccurate because of the method by which we obtained some of the data or estimates or because this information cannot always be verified with complete certainty due to the limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties. As a result, you should be aware that market and other industry data included in this prospectus, and estimates and beliefs based on that data, may not be reliable.

ii

Table of Contents

This summary highlights some of the information in this prospectus. It does not contain all of the information that you should consider before making a decision to invest in our common stock. You should read carefully the more detailed information set forth under “Risk Factors” and the other information included in this prospectus. Except where the context suggests otherwise, the terms the “Company,” “we,” “us,” “our” and “CMTG” refer to Claros Mortgage Trust, Inc., a Maryland corporation, individually and together with its subsidiaries as the context may require; our “Manager” refers to Claros REIT Management LP, a Delaware limited partnership, our external manager and an affiliate of MRECS; and “MRECS” refers to Mack Real Estate Credit Strategies, L.P., the CRE lending and debt investment business affiliated with Mack Real Estate Group, LLC, which we refer to as the “Mack Real Estate Group” or “MREG.” Although MRECS and MREG are distinct legal entities, for convenience, references to our “Sponsor” in this prospectus are deemed to include reference to MRECS and MREG, individually or collectively, as appropriate for the context and unless otherwise indicated. References to “CRE” throughout this prospectus mean commercial real estate.

Unless we indicate otherwise or the context otherwise requires, all information in this prospectus (i) assumes no exercise of the underwriters’ option to purchase additional shares of our common stock, (ii) reflects a 2-for-1 reverse stock split of our common stock effected on October 6, 2021, and (iii) does not reflect 1,097,293 shares of common stock underlying unvested restricted stock units, or RSUs, that are expected to vest in full as of the date of this prospectus and an additional 8,281,594 shares of our common stock reserved for future grant or issuance under our 2016 Incentive Award Plan, or the 2016 Plan. In addition, unless otherwise indicated or required by context, all references in this prospectus to our “stockholders’ equity” and “common stock” include 7,306,984 shares of our common stock outstanding as of the date of this prospectus that we are currently required to classify as “redeemable common stock” on our balance sheet in accordance with generally accepted accounting principles, or GAAP, because the shares are subject to a stockholder’s contractual redemption right. The stockholder’s contractual redemption right will terminate upon completion of this offering, at which point the shares previously subject to that right will be reclassified as common stock on our balance sheet in accordance with GAAP.

Our Company

We are a CRE finance company focused primarily on originating senior and subordinate loans on transitional CRE assets located in major U.S. markets. Transitional CRE assets are properties that require repositioning, renovation, rehabilitation, leasing, development or redevelopment or other value-added elements in order to maximize value. We believe our Sponsor’s real estate development, ownership and operations experience and infrastructure differentiates us in lending on these transitional CRE assets. Our objective is to be a premier provider of debt capital for transitional CRE assets and, in doing so, to generate attractive risk-adjusted returns for our stockholders over time, primarily through dividends. We strive to create a diversified investment portfolio of CRE loans that we generally intend to hold to maturity.

Upon completion of this offering, we expect to be one of the largest public commercial mortgage real estate investment trusts in the U.S., based on total stockholders’ equity. From our inception in August 2015 through June 30, 2021, we have raised approximately $2.6 billion of equity capital and originated, co-originated or acquired 86 investments consisting of 131 loans on transitional CRE assets with aggregate loan commitments of approximately $11.5 billion. We have raised and invested significant institutional capital from major state and corporate pension funds, global insurance companies and leading investment managers, among others. We believe that these investors have been attracted to us by the experience of our team and our track record of disciplined underwriting and rigorous asset management. From our inception through June 30, 2021, 29 of the investments that we originated, representing aggregate loan commitments of $3.1 billion, have been repaid in full or sold, with no credit losses incurred and a realized gross internal rate of return of 13.2%. As of June 30, 2021,

1

Table of Contents

our loan portfolio was comprised of 56 loan investments consisting of 92 loans, representing aggregate loan commitments of $7.5 billion, remaining loan commitments (representing aggregate loan commitments less repayments received in respect thereof) of $7.3 billion and unpaid principal balance of $6.1 billion, and our stockholders’ equity was $2.5 billion, representing a book value of $18.76 per share of our common stock.

Leveraging our Sponsor’s broad real estate investment, development and management experience, our investment approach employs an ownership mindset. For each investment, we perform a thorough analysis of the underlying asset, the borrower and the borrower’s business plan and evaluate alternative uses of collateral in order to distinguish “execution risk” (i.e., the risk that a borrower will fail to execute its intended business plan) from “basis risk” (i.e., the risk of a material diminution in collateral value, as a result of the borrower over leveraging the collateral for the loan or otherwise). Although our objective is to originate loans for which the borrower will perform as expected and pay as agreed, we believe that in a downside scenario we have the ability to evaluate and mitigate much of the execution risk by utilizing our Sponsor’s broad experience and capabilities in developing, owning and managing real estate equity investments. We believe that this experience of our Sponsor enables our Manager to underwrite, originate and manage loans on transitional CRE assets, with an appropriate level of execution risk and, in its judgment, relatively limited basis risk. We offer bespoke and flexible lending solutions to our borrowers that are designed to both align with their business plans and enable us to protect our capital even in a downside scenario.

We focus primarily on originating loans ranging from $50 million to $300 million on transitional CRE assets located in major U.S. markets with attractive fundamental characteristics supported by macroeconomic tailwinds. As of June 30, 2021, our average loan investment commitment was $134.8 million. The below table summarizes our loan portfolio as of June 30, 2021 (dollars in thousands):

| Weighted Average(4) | ||||||||||||||||||||||||||||||||||||||||

| Number of Investments(1) | Number of Loans(1) | Aggregate Loan Commitment(2) | Remaining Loan Commitment(3) | Unpaid Principal Balance | All-In Yield(5) | Term to Initial Maturity(6) | Term to Fully Extended Maturity(6) | LTV(7) | % Floating Rate | |||||||||||||||||||||||||||||||

Senior loans(8) | 49 | 83 | $ | 6,899,919 | $ | 6,743,983 | $ | 5,640,715 | 6.2 | % | 1.2 | 2.7 | 66.4 | % | 98.5 | % | ||||||||||||||||||||||||

Subordinate loans | 7 | 9 | 649,126 | 524,201 | 488,902 | 11.2 | % | 0.4 | 2.3 | 60.8 | % | 95.8 | % | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Total / Weighted Average | 56 | 92 | $ | 7,549,045 | $ | 7,268,184 | $ | 6,129,617 | 6.6 | % | 1.1 | 2.6 | 65.9 | % | 98.3 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

| (1) | Certain investments include multiple loans for which we made commitments to the same borrower or affiliated borrowers on the same date. The loan portfolio table excludes our one real estate owned investment. |

| (2) | Aggregate loan commitment represents initial loan commitments, as adjusted by commitment reductions, less transfers which qualified for sale accounting under GAAP. |

| (3) | Remaining loan commitment represents the aggregate loan commitment less repayments received in respect thereof. |

| (4) | Weighted averages are based on unpaid principal balance. |

| (5) | All-in yield represents the weighted average annualized yield to initial maturity of each loan within our loan portfolio, inclusive of coupon, origination fees, exit fees, and extension fees received, based on the applicable floating benchmark rate (if applicable), including LIBOR floors (if applicable), as of June 30, 2021. |

| (6) | Term to initial and fully extended maturity are measured in years. Fully extended maturity assumes all extension options are exercised by the borrower upon satisfaction of the applicable conditions. |

| (7) | LTV represents “loan-to-value” or “loan-to-cost”, which is calculated as our total loan commitment from time to time, as if fully funded, plus any financings that are pari passu with or senior to our loan, divided by our estimate of either (1) the value of the underlying real estate, determined in accordance with our underwriting process (typically consistent with, if not less than, the value set forth in a third-party appraisal) or (2) the borrower’s projected, fully funded cost basis in the asset, in each case as we deem appropriate for the relevant loan and other loans with similar characteristics. Underwritten values and projected costs should not be assumed to reflect our judgment of current market values or project costs, which may have changed materially since the date of origination including, without limitation, as a result of the COVID-19 |

2

Table of Contents

| pandemic. LTV is updated only in connection with a partial loan paydown and/or release of collateral, material changes to expected project costs, the receipt of a new appraisal (typically in connection with financing or refinancing activity) or a change in our loan commitment. |

| (8) | Includes contiguous subordinate loans (i.e., loans for which we also hold the mortgage loan) representing aggregate loan commitments of $807.3 million, remaining loan commitments of $796.8 million, and aggregate unpaid principal balance of $645.5 million, in each case as of June 30, 2021. |

In February 2021, we foreclosed on a portfolio of seven limited service hotel properties located in New York, New York that secured a mezzanine loan with an unpaid principal balance of $103.9 million as of February 8, 2021 that we originated in February 2018. Neither the prior mezzanine loan nor the portfolio of hotel properties, which we refer to as our real estate owned investment, is included in the table above. Our real estate owned investment at the time of foreclosure was encumbered by a securitized senior mortgage, which we assumed on February 8, 2021 with a principal balance of $300.0 million. In June 2021, the terms of the securitized senior mortgage were modified, which included the repayment of $10.0 million of principal and extension of its maturity date by an additional three years to February 2024. At June 30, 2021, the outstanding balance of our debt related to real estate owned was $290.0 million.

We were organized as a Maryland corporation on April 29, 2015 and commenced operations on August 25, 2015. We have elected and believe we have qualified to be taxed as a real estate investment trust, or REIT, for U.S. federal income tax purposes commencing with our taxable year ended December 31, 2015. We are externally managed and advised by our Manager, an investment adviser registered with the U.S. Securities and Exchange Commission, or the SEC, pursuant to the Investment Advisers Act of 1940, as amended, or the Advisers Act. We operate our business in a manner that permits us to maintain our exclusion from registration under the Investment Company Act of 1940, as amended, or the 1940 Act.

Our Sponsor

Mack Real Estate Group, or MREG, was founded in 2013 by William, Richard and Stephen Mack to focus on real estate investments, with an initial emphasis on multifamily development, and has established several affiliates (including MRECS) that invest in and manage real estate debt and equity assets, loans and securities. We believe that the Mack family has developed a first-class reputation dating back to the 1960s as a real estate developer, investor and manager, including through successful prior ventures such as AREA Property Partners (formerly known as Apollo Real Estate Advisors), or AREA, among others. MRECS was founded in 2014 to focus on CRE credit investments as a core business affiliated with the broader MREG platform.

The members of our Sponsor’s senior management team have, on average, more than 25 years of real estate and finance experience. Today, our Sponsor owns, develops, invests in and manages real estate equity, debt and securities on behalf of third-party institutional and high net worth investors. Our Sponsor is headquartered in New York, New York with a team of approximately 60 people dedicated to MREG and MRECS and more than 200 people in total, including those associated with affiliates that provide a variety of services to MREG and MRECS. We believe that this depth of experience and relationships helps position our Sponsor to identify, analyze and execute on attractive lending opportunities on transitional CRE assets.

MREG primarily makes and manages CRE equity investments. It was launched as an opportunistic real estate investor expecting to leverage its founders’ deep experience across multifamily, office, industrial and other asset classes as warranted by market conditions. Initially, MREG invested predominantly in multifamily rental housing in major U.S. urban markets with high barriers to entry, creating a pipeline of more than 5,000 multifamily units in various stages of development and operation (some of which have been sold) with a projected gross development cost of more than $3.0 billion. MREG also invests in industrial properties and pursues other types of CRE equity investments that involve acquisitions of existing investments and ground up

3

Table of Contents

development as it deems desirable based upon prevailing market conditions from time to time. MREG has a development subsidiary with approximately 11 employees based in Los Angeles, Seattle and Phoenix and a property management subsidiary with approximately 130 employees.

MRECS was established to focus primarily on investing in and managing investments in CRE debt, CRE debt securities and highly structured CRE investments (such as preferred equity and mezzanine loans). As MREG’s credit-oriented affiliate, MRECS has assembled a multi-disciplinary team that works closely with other MREG professionals to source, underwrite, structure, execute and manage investments, led by the following professionals:

| • | Richard Mack, our Chief Executive Officer and Chairman, MREG’s and MRECS’ Chief Executive Officer and a Managing Partner of MRECS, co-founded MREG in 2013 and MRECS in 2014 and serves as a member of MRECS’ Investment Committee. Prior to joining MRECS, Mr. Mack joined AREA Property Partners (formerly known as Apollo Real Estate Advisers) in 1993, the year of its formation, as one of the initial employees, where he oversaw ARCap (a subordinate commercial mortgage-backed securities, or CMBS, investor and special servicer), the Claros Real Estate Securities Fund (focused on investments in subordinate CMBS in the U.S. and Europe), the Apollo GMAC Mezzanine Fund and the Apollo Real Estate Finance Corporation, in addition to numerous equity investments; |

| • | Michael McGillis, our President, Chief Financial Officer and Director, MRECS’ Chief Financial Officer, and MREG’s President and Chief Operating Officer, joined MRECS in 2015 and serves as a member of MRECS’ Investment Committee. Prior to joining MRECS, Mr. McGillis was the Managing Director, Head of U.S. Funds and Chief Financial Officer at J.E. Robert Companies, where he was responsible for asset and portfolio management, capital markets, investor relations and financial management activities for a series of private equity real estate funds focused on both CRE debt and equity investments; |

| • | Kevin Cullinan, our Executive Vice President—Originations, also serves as a Managing Director of MRECS and its Head of Originations. Prior to joining MRECS, he worked on the Global Real Assets team at J.P. Morgan Investment Management and at a family office in New York, New York; and |

| • | Priyanka Garg, our Executive Vice President—Portfolio and Asset Management, also serves as a Managing Director of MRECS and its Head of Portfolio and Asset Management. Ms. Garg has more than 20 years of real estate investment management experience, including leadership positions at Treeview Real Estate Advisors and Westbrook Partners. |

We leverage our Sponsor’s platform to originate, underwrite, structure and asset manage a portfolio of loan assets that align with our differentiated investment strategy. In particular, we believe that MREG’s experience and infrastructure in the areas of real estate ownership, development and property management strengthens our ability to lend on transitional CRE assets which involve a level of borrower execution risk that traditional lenders and other debt market participants without our expertise may be unable or unwilling to adequately underwrite.

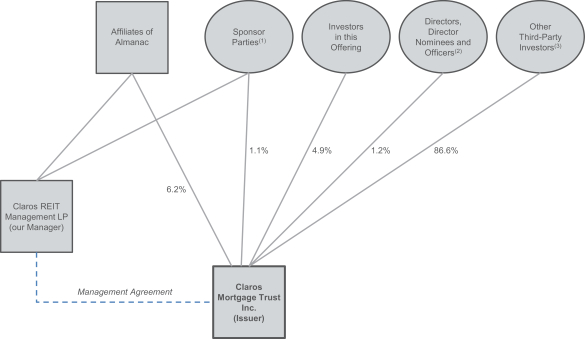

Our Manager

Our Sponsor formed Claros REIT Management LP, or our Manager, concurrently with our inception to pursue what we believe is a compelling market opportunity to invest in our target assets. In performing its duties to us, our Manager benefits from the resources, relationships, fundamental real estate underwriting and management expertise of our Sponsor’s broad group of real estate professionals.

Our Manager is led by Richard Mack, Michael McGillis, Kevin Cullinan, Priyanka Garg and other members of our Sponsor’s senior management team. Pursuant to the terms of the management agreement between us and our Manager, or the Management Agreement, our Manager is responsible for executing our loan origination,

4

Table of Contents

capital markets, portfolio management, asset management and monitoring activities and managing our day-to-day operations. To perform its role in a flexible and efficient manner, our Manager leverages professionals employed by our Sponsor whose services are made available to our Manager and, in turn, to us. Neither we nor our Manager employs personnel directly and any reference herein to our Manager’s officers or employees is a reference to the officers or employees of our Sponsor made available to our Manager. In performing its duties to us, our Manager is at all times subject to the supervision, direction and management of our board of directors, or our Board.

Our Manager has ongoing access to MRECS’ senior management team as part of a services agreement between MRECS and our Manager. In addition, by virtue of the common ownership and control between our Manager and our Sponsor, our Manager also has access to the other personnel of our Sponsor and its affiliates. We believe our Manager benefits from access to individuals with extensive experience in identifying, analyzing, acquiring, financing, hedging, managing and operating real estate investments across investment cycles, geographies, property types, investment types and strategies, including debt and equity interests, controlling and non-controlling investments, corporate and securities investments (including CMBS) and a variety of joint ventures. We believe that this experience of our Sponsor and its affiliates enables our Manager to underwrite, originate and manage loans that facilitate the successful transition of CRE assets, with an appropriate level of execution risk and, in its judgment, relatively limited basis risk.

We believe that access to our Sponsor’s broad group of real estate professionals provides our Manager with the market expertise, strategic relationships and operational experience to allow us to execute on our business plan. For more information regarding our Manager and the Management Agreement, please see “—Management Agreement” below and “Our Manager and the Management Agreement.”

Market Opportunity

We believe there is an attractive, long-term market opportunity for non-traditional providers of transitional CRE debt financing to originate or acquire loans on transitional CRE assets located primarily in major U.S. markets. In addition, as a result of a fundamental shift in the competitive lending landscape coming out of the global financial crisis of 2008, we believe that a supply-demand disparity for CRE debt capital exists and provides attractive opportunities for non-traditional lenders to finance transitional CRE properties. There are a number of compelling near- and long-term factors that contribute to what we believe to be an attractive market opportunity for non-traditional lenders, including:

| • | High volume of near-term commercial mortgage loan maturities; |

| • | CRE transaction volumes and construction activity over time; |

| • | Significant closed-end private equity real estate fund investable equity capital; |

| • | Limited supply of debt capital for transitional CRE assets relative to demand for such capital; and |

| • | Constructive long-term CRE fundamentals. |

The total outstanding unpaid principal balance on all CRE loans was approximately $5.0 trillion as of June 30, 2021, according to the U.S. Federal Reserve Bank. Although demand for CRE debt financing has generally increased over recent years, we believe the supply of debt capital for transitional CRE assets has remained constrained in large part due to restrictive underwriting standards utilized by conventional financing sources and increased regulatory pressures on traditional bank lenders since the global financial crisis of 2008, even with the recent increase in private equity real estate fund investable debt capital. We believe that one legacy of the credit boom that preceded the global financial crisis of 2008 is that many traditional lenders, primarily banks, have withdrawn or otherwise significantly retrenched from the transitional CRE lending market over the past several years, a trend we believe was exacerbated by the recent economic downturn arising from the COVID-19 pandemic. The withdrawal or other retrenchment of such lenders that historically satisfied much of the demand for transitional CRE debt financing suggests that there may not

5

Table of Contents

be enough providers of the type of financing in which we specialize to meet the expected demand for both the origination of new transitional CRE loans and the refinancing or recapitalization of existing transitional CRE loans. While demand for real estate debt capital generally increased throughout the economic expansion following the global financial crisis, we believe CRE lenders exhibited more discipline, and lending standards were generally more conservative than in the past.

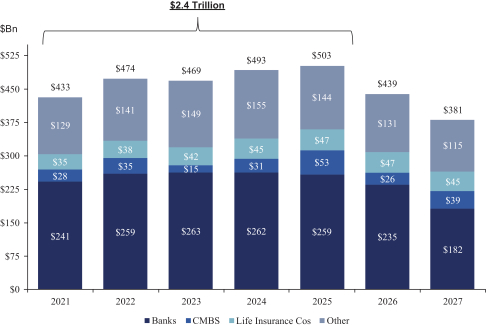

High Volume of Near-Term Commercial Mortgage Loan Maturities

The principal sources of debt investment opportunities are the refinancing of maturing loans and the origination of loans in connection with asset acquisition and development activity. Maturing loans lead to substantial demand for debt capital, as these loans are typically either refinanced or the underlying properties are sold, with buyers often requiring their own new financing. Based on research by Trepp LLC, between 2021 and 2025, commercial mortgage loans with a total outstanding unpaid principal balance of approximately $2.4 trillion will mature, the expected refinancing of some of which we believe will provide opportunities for us to originate new loans.

Commercial Mortgage Loan Maturities (in billions)

Source: Trepp LLC, based on Flow of Funds data, 1Q 2021.

CRE Transaction Volumes and Construction Activity Over Time

CRE transaction and construction activity increased significantly following the global financial crisis of 2008, as many markets benefited from employment gains and historically low interest rates, and consequently experienced increased CRE demand and real estate values. In 2019, acquisition activity surpassed pre-crisis peaks, with annual CRE transaction volume increasing over eight times between 2009 and 2019, from $72 billion to $599 billion, according to Real Capital Analytics, Inc. 2019 was one of the highest years on record for aggregate total CRE transaction volume, and transaction volume during the first quarter of 2020 surpassed that of the first quarter of 2019. While overall 2020 transaction activity was significantly impacted by the COVID-19 pandemic, transaction volume

6

Table of Contents

increased in the second half of the year, with $165 billion of activity in the fourth quarter of 2020 alone. This recovery continued in the second quarter of 2021, with CRE transaction volume up 198% year-over-year, and we expect it will accelerate in parallel with the broader CRE sector recovery.

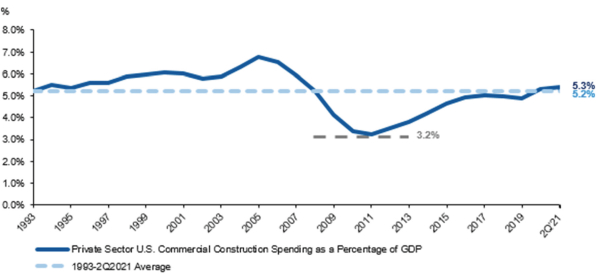

Private sector U.S. commercial construction activity, consisting of construction spending in categories such as retail, wholesale and selected services, healthcare, lodging and residential assets, has generally increased since 2011 into the second quarter of 2021, and, according to data from the U.S. Census Bureau and the U.S. Bureau of Economic Analysis, the amount of private sector U.S. commercial construction spending as a percentage of GDP increased by approximately 65% from 2011 to the end of the second quarter of 2021, representing 5.3% of GDP at June 30, 2021, slightly above 5.2%, the annual average from 1993 through the end of the second quarter of 2021. While construction activity slowed during 2020 in connection with the economic downturn, we expect it will continue to stabilize as economic conditions continue to improve coming out of the COVID-19 pandemic.

CRE Transaction Volume (in billions)

Source: Real Capital Analytics, Inc., August 2021.

7

Table of Contents

Private Sector U.S. Commercial Construction Spending as a Percentage of GDP

Source: Annual private sector commercial construction spending data from U.S. Census Bureau, August 2021. Annual GDP data from U.S. Bureau of Economic Analysis, August 2021.

Note: Reflects private sector commercial construction spending in categories such as retail, wholesale and selected services, healthcare, lodging and residential assets as categorized by the U.S. Census Bureau.

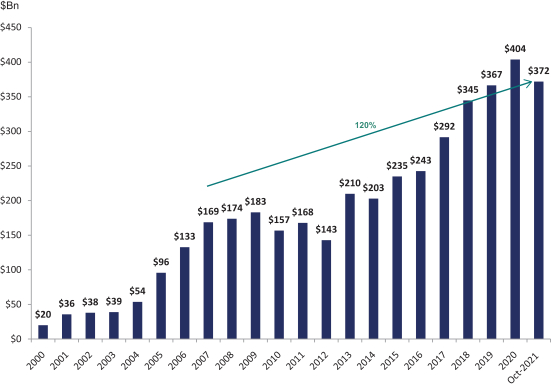

Significant Closed-End Private Equity Real Estate Fund Investable Equity Capital

According to Preqin data as of October 2021, closed-end private equity real estate funds had more than $370 billion of committed investable equity capital that has not yet been called for investment. This represents an increase of 120% from the 2007 level and a return to near pre-pandemic highs. We believe that the deployment of this equity capital may increase CRE transaction activity and, in turn, demand for CRE lending opportunities.

8

Table of Contents

Investable Equity Capital—Closed-End Private Equity Real Estate Funds (in billions)

Source: Preqin, October 2021.

Limited Supply of Debt Capital for Transitional CRE Assets

We believe there is a limited supply of debt capital relative to demand for large balance loans on transitional CRE assets, even with the recent increase in private equity real estate fund investable debt capital. Historically, transitional CRE loans have been funded by U.S. commercial banks, foreign banks, life insurance companies, government sponsored entities, or GSEs, CMBS and other sources of capital, including private debt funds and commercial mortgage REITs. We believe that significant changes have occurred in the regulation of financial institutions, including the rules adopted by the Basel Committee on Banking Supervision, or Basel III, and the Dodd-Frank Wall Street Reform and Consumer Protection Act, or the Dodd-Frank Act, among others, which have caused traditional lenders (such as commercial banks) to be less active in financing transitional CRE assets, creating a lending supply-demand disparity. We believe that this disparity is especially pronounced in the lending market for moderate-to-heavy transitional assets, in which the properties being financed are not yet generating cash flow (or have limited or temporarily diminished cash flows) and require a significant outlay of capital for repositioning, renovation, rehabilitation, leasing, development or redevelopment. Changes in bank regulation resulting from the implementation of Basel III and the Dodd-Frank Act generally increased the capital requirements applicable to banks that have traditionally been a key provider of financing for transitional CRE assets. While the Economic Growth, Regulatory Relief, and Consumer Protection Act, or the EGRRCPA, signed into law on May 24, 2018, amended the approach to certain loans secured by High Volatility Commercial Real Estate, or HVCRE, to relieve some of the burdens on commercial banks, HVCRE and capital requirements still present potential issues for banks financing certain transitional CRE assets. We believe many traditional lenders are now less active in the transitional CRE lending space as they pursue lower leverage loans secured by fully-

9

Table of Contents

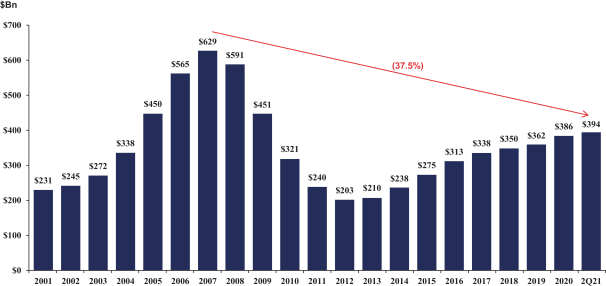

stabilized, prime assets in major markets. Financing transitional CRE assets requires traditional lenders to increase capital reserves and subjects them to greater regulatory scrutiny and administrative burden. The requirement for traditional lenders to maintain greater capital reserves decreases the profitability of these loans to them and we believe this has caused many of those lenders to withdraw or otherwise retrench from the transitional CRE lending market. Not only has the balance of construction loans held by banks dropped 37.5% since 2007, but the balance of construction loans held by banks as a proportion of U.S. CRE debt outstanding also saw a meaningful decline from 19% in 2007 to 8% in the second quarter of 2021, based on total U.S. CRE debt held by banks of $3.3 trillion as of December 31, 2007 and $5.0 trillion as of June 30, 2021, according to data from the Federal Deposit Insurance Corporation, or the FDIC, and the U.S. Federal Reserve Bank.

Construction Loans Held by Banks (in billions)

Source: FDIC, June 30, 2021.

Note: Figures represent construction loans held by FDIC-insured commercial banks and savings institutions at the end of each year, except where noted otherwise.

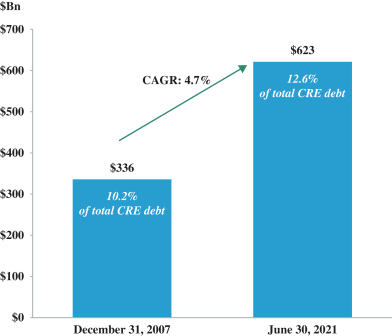

We believe the supply-demand disparity in the transitional CRE lending market will remain significant over the foreseeable future, continuing to create attractive opportunities for transitional CRE lenders. We believe the significant infrastructure-related launch costs of an effective transitional CRE lending platform creates a meaningful barrier to entry for new competitors. Although the balance of construction loans held by banks, both nominally and in proportion to the total amount of outstanding CRE debt, has decreased since 2007, private construction spending simultaneously grew 41% from $859 billion in 2007 to $1,212 billion in the second quarter of 2021 according to private construction spending data collected by the U.S. Census Bureau. We believe that this confluence of factors has resulted in, and will continue to result in, non-traditional lenders, including commercial mortgage REITs, being more active in transitional CRE lending. At the end of the second quarter of 2021, total CRE loans by non-traditional lenders, including commercial mortgage REITs, increased 85.2% in dollar value since December 31, 2007 and comprised $623 billion or 12.6% of the CRE debt market, as compared to $336 billion, or 10.2% of the CRE debt market as of December 31, 2007, according to the U.S. Federal Reserve Bank.

10

Table of Contents

Outstanding U.S. CRE Debt Held By Commercial Mortgage REITS

and Other Non-Traditional Lenders (in billions)

Source: U.S. Federal Reserve Bank—Financial Accounts of the United States, June 30, 2021.

Note: Other Non-Traditional Lenders are defined as all lenders other than U.S. banks and depository institutions, insurance companies, agency and GSEs and asset-backed securitizations.

Constructive Long-Term CRE Fundamentals

We believe that as a result of disciplined lending standards adopted following the global financial crisis of 2008, the CRE market was in a strong position entering the most recent economic downturn arising from the COVID-19 pandemic.

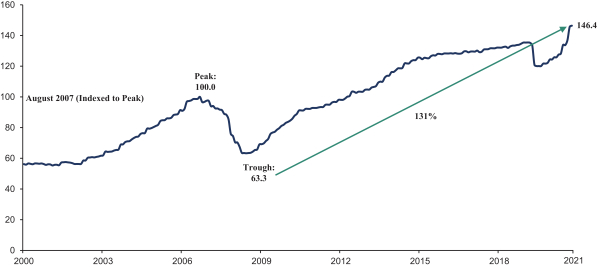

Over the last ten years, CRE property values increased significantly according to Green Street Advisors, or GSA, which helped to drive demand for debt capital within our target assets. During the global financial crisis of 2008, the Commercial Property Price Index, or CPPI, which represents a time series of unleveraged U.S. commercial property values that captures the prices at which CRE transactions are currently being negotiated and contracted, fell 36.7% from its peak in August 2007 to post-global financial crisis lows in May 2009. Since May 2009, the CPPI has increased from 63.3 to 146.4 as of September 1, 2021, representing growth of 131%. No assurance can be given as to the direction, magnitude or timing of future CRE property values. However, we have endeavored to actively limit our basis risk, and our loan portfolio had a weighted average LTV of 65.9% as of June 30, 2021 demonstrating our Manager’s disciplined underwriting standards. We believe that in the current market environment, investing in CRE debt with substantial underlying collateral that is evaluated and underwritten by MRECS’ experienced senior management team provides an attractive opportunity for stable risk-adjusted returns as we believe the basis in our loan portfolio is less exposed to volatility in property prices.

11

Table of Contents

Commercial Property Price Index

Source: GSA, October 2021.

Note: GSA Commercial Property Price Index data indexed to August 2007. Chart illustrates data through September 1, 2021.

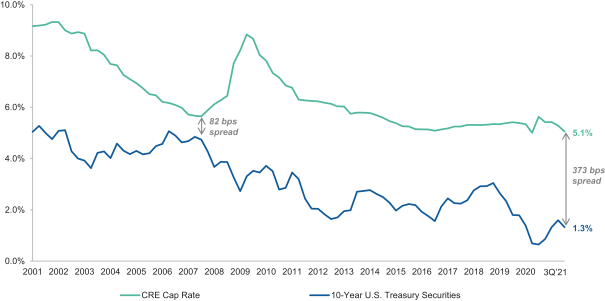

Finally, while U.S. CRE capitalization rates, or cap rates, have compressed since 2009, the rates on 10-year U.S. treasury securities have declined at a greater rate over the same period. We believe there is cushion between CRE cap rates and rates on 10-year U.S. treasury securities to allow for some spread compression if cap rates decline or rates on 10-year U.S. treasury securities increase due to current macroeconomic conditions, including the possibility of near-term inflation. The current spread between CRE cap rates and 10-year U.S. treasury rates of 373 basis points as of September 30, 2021 is 36 basis points wider than the average spread from March 31, 2001 to September 30, 2021 of 337 basis points, as shown in the GSA data.

12

Table of Contents

Historical CRE Cap Rates and 10-year U.S. Treasury Securities Rates

Source: GSA, U.S. Department of the Treasury, October 2021.

Note: Treasury security rates reflect trailing last quarter average. Chart illustrates data through September 30, 2021. CRE cap rate is an average of cap rates for apartment, industrial, mall, office and strip center property types.

Our Investment Approach

We believe that we have a differentiated investment approach, characterized by the following guiding principles:

We Have an Ownership Mindset

We employ an ownership mindset in our origination, underwriting and asset management disciplines, driven by our Sponsor’s real estate investment, development and management expertise. We believe our Sponsor’s experience as a real estate investor and developer helps us better understand borrower needs, and enables us to be a leading solutions provider of loans that are customized to borrowers and their business plans. As part of our ownership mindset, we seek to be patient and prudent, emphasizing long-term borrower relationships rather than short-term one-time investments.

We Leverage our Sponsor’s Real Estate Background and Platform

We believe our Sponsor’s capabilities and infrastructure help us determine potential alternative exit strategies in the event of borrower distress and maintain appropriate ongoing asset management and oversight of our investments. Although our objective is to originate loans for which the borrower will perform as expected and pay as agreed, we believe that in a downside scenario we have the ability to evaluate and mitigate much of the execution risk in borrower business plans by utilizing our Sponsor’s broad experience and capabilities. Our Sponsor has a team of more than 200 people in total, including a development subsidiary with approximately 11 employees based in Los Angeles, Seattle and Phoenix and a property management subsidiary with approximately 130 employees Additionally, approximately 65% of our loan portfolio based on unpaid principal balance as of June 30, 2021 is

13

Table of Contents

located in markets where MREG has its own investments or dedicated development or property management teams. We believe our ability to draw on this expertise enables us to carefully underwrite our loan solutions to our borrowers that may not be available from lenders that lack similar expertise and infrastructure, while selecting and structuring investments so as to limit downside risk for us.

We Underwrite Execution Risk, and Seek to Avoid Basis Risk

We consider execution risk to be the risk that a borrower fails to execute its intended business plan, and we leverage our Sponsor’s real estate platform and infrastructure to carefully underwrite this risk. We consider basis risk to be the risk of a material diminution in collateral value, as a result of the borrower over leveraging the collateral for the loan due to market conditions or other factors. In seeking to limit basis risk, we focus on last-dollar loan basis, as we believe that lower LTVs may provide substantial cushion in the event of declines in the value of our loans’ collateral. Our loan portfolio as of June 30, 2021 had a weighted average LTV of 65.9%, providing substantial subordinate capital to our funded loan amounts. In evaluating basis risk, we consider as-is and (if appropriate) as-stabilized LTV, as well as alternative uses of collateral.

We Offer Bespoke and Flexible Structuring Solutions

We draw on the deep structuring experience of our Manager and its principals to develop lending solutions that are customized to the needs of our borrowers, while protecting our loan basis and emphasizing preservation of capital. For example, a portion of our loans are structured with forward commitments, enabling borrowers to draw additional proceeds as specified milestones are met. We document these loans with structural protections aligned with our borrowers’ business plans designed to enable us to protect our capital even in a downside scenario. Examples of these structural protections include completion guarantees from well capitalized guarantors, among others. Our loans are also typically structured to provide borrowers with loan maturity extension rights, subject to borrowers meeting certain conditions, at agreed upon terms. In addition, under certain market circumstances, we may, in our discretion, negotiate loan amendments or modifications with borrowers where we believe this protects or enhances the value of our investment. Such amendments or modifications may allow the borrower to extend the loan, while we may negotiate a higher spread, loan extension fees, partial loan paydowns or other structural enhancements. Our goal is to be highly responsive to borrowers’ needs, while at the same time hold them accountable for their stated business plan milestones.

Competitive Strengths

We believe that we have the following competitive strengths in originating senior and subordinate loans on transitional CRE assets located primarily in major U.S. markets:

Established and Scaled Platform, Validated by Significant Institutional Capital

Upon completion of this offering, we expect to be one of the largest public commercial mortgage REITs in the U.S., based on total stockholders’ equity. From our inception in August 2015 through June 30, 2021, we have raised approximately $2.6 billion of equity capital and originated, co-originated or acquired 86 investments consisting of 131 loans on transitional CRE assets with aggregate loan commitments of approximately $11.5 billion. We employ a differentiated investment strategy focused on transitional loan opportunities secured by high quality CRE assets, with quality sponsorship, including assets located in major U.S. markets where our Sponsor has infrastructure or experience, at a compelling loan basis. We believe our ownership mindset and our Sponsor’s significant real estate development, ownership and operations experience and infrastructure enable us to underwrite transitional CRE assets, which may require varying degrees of additional capital to maximize their cash flow and value depending on prevailing market conditions, in a way that lenders without such infrastructure or expertise may be unable to do. In general, we choose to focus on fewer, larger loan opportunities representing

14

Table of Contents

what we believe to be the most attractive risk-adjusted returns in the market at any point in time. We have raised and invested significant institutional capital from major state and corporate pension funds, global insurance companies and leading investment managers, among others. We believe that these investors have been attracted to us by the experience of our team and our track record of disciplined underwriting and rigorous asset management. From our inception through June 30, 2021, 29 of the investments that we originated, representing aggregate loan commitments of $3.1 billion, have been repaid in full or sold, with no credit losses incurred and a realized gross internal rate of return of 13.2%. As of June 30, 2021, our loan portfolio was comprised of 56 loan investments consisting of 92 loans, representing aggregate loan commitments of $7.5 billion, remaining loan commitments (representing aggregate loan commitments repayments received in respect thereof) of $7.3 billion, and unpaid principal balance of $6.1 billion, and our stockholders’ equity was $2.5 billion, representing a book value of $18.76 per share of our common stock.

Sponsor with Roots in Real Estate Development and Operations

We believe we have a competitive advantage relative to other market participants with similar investment strategies due to the expertise of the principals and senior management and other personnel of our Sponsor and its affiliates in global real estate investment strategies across the debt and equity spectrum as a developer, owner and operator, as well as a lender. The members of our Sponsor’s senior management team have, on average, more than 25 years of real estate and finance experience. We believe that the Mack family has developed a first-class reputation dating back to the 1960s as a real estate developer, investor and manager, including through successful prior ventures such as AREA, among others.

In particular, our Sponsor’s hands-on real estate investment, development and management capabilities help us evaluate transitional CRE assets, including the feasibility of borrower business plans and potential alternative exit strategies for assets in the event of borrower failure to execute its stated business plan or borrower distress. We leverage our Sponsor’s broad real estate investment, development and management experience to employ an ownership mindset in underwriting our CRE loan originations.

Experienced Cycle-Tested Management and Investment Team

Our management team is made up of seasoned CRE professionals with extensive experience in the CRE equity and debt investment industries. Richard Mack, our Chief Executive Officer and Chairman, joined AREA in 1993, the year of its formation, as one of the initial employees. There, he oversaw ARCap (a subordinate CMBS investor and special servicer), the Claros Real Estate Securities Fund (focused on investments in subordinate CMBS in the U.S. and Europe), the Apollo GMAC Mezzanine Fund and the Apollo Real Estate Finance Corporation, in addition to numerous CRE equity investments. Michael McGillis, our President and Chief Financial Officer, was previously Managing Director, Head of U.S. Funds and Chief Financial Officer at J.E. Robert Companies, where he was responsible for asset and portfolio management, capital markets, investor relations and financial management activities for a series of private equity real estate funds. Kevin Cullinan, our Executive Vice President—Originations, also serves as a Managing Director of MRECS and as its Head of Originations. Prior to joining MRECS, he worked on the Global Real Assets team at J.P. Morgan Investment Management and at a family office in New York, New York. Priyanka Garg, our Executive Vice President—Portfolio and Asset Management, also serves as a Managing Director of MRECS and as its Head of Portfolio and Asset Management. Ms. Garg has more than 20 years of real estate investment management experience, including leadership positions at Treeview Real Estate Advisors and Westbrook Partners. Mr. Cullinan and Ms. Garg are also our Sponsor’s Co-Heads of Credit Strategies.

Messrs. Mack, McGillis and Cullinan and Ms. Garg, among others, lead our multi-disciplinary credit team, which works closely with our Sponsor’s professionals to source, underwrite and structure loans secured by transitional CRE assets. Our Sponsor’s principals and members of senior management have several decades of global real estate investing experience through multiple economic cycles with respect to debt, property and

15

Table of Contents

portfolio investments, mergers and acquisitions and public market transactions. Our Sponsor’s principals seek to focus on opportunities that are overlooked by or not readily executable by other lenders and have demonstrated the discipline to refrain from lending when they believe their targeted returns are unavailable or subject to an undue level of market or financing risk.

Differentiated Investment Strategy Focused on Larger, Transitional Lending Opportunities in Major Markets

We employ a differentiated investment strategy focused on transitional loan opportunities secured by high quality CRE assets, with quality sponsorship, including assets located in major U.S. markets where our Sponsor has infrastructure or experience, at a compelling loan basis. We believe our ownership mindset and our Sponsor’s significant real estate development, ownership and operations experience and infrastructure enable us to underwrite transitional CRE assets, which may require varying degrees of additional capital to maximize their cash flow and value depending on prevailing market conditions, in a way that lenders without such infrastructure or expertise may be unable to do. In general, we choose to focus on fewer, larger loan opportunities representing what we believe to be the most attractive risk-adjusted returns in the market at any point in time.

These assets may require light-to-heavy development, redevelopment, renovation, rehabilitation, repositioning or leasing. In light transitional lending, the properties being financed are generating cash flow, but typically require funding for value-added elements such as a new marketing or leasing program or other changes in business plan intended to maximize operating income, which in turn should increase value. In heavy transitional lending, which primarily consists of land and construction loans, the properties being financed are not yet generating operating cash flow and require a significant outlay of capital. In general, investments on properties that require less capital expenditures on a relative basis and/or have a smaller difference between their in-place operating income and projected stabilized operating income are considered “lighter” transition, while investments on properties that are expected to require more capital expenditures on a relative basis and/or have a more significant difference between their in-place operating income (if any) and projected stabilized operating income are considered “heavier” transition. We seek to construct a portfolio that has an attractive and carefully underwritten risk-adjusted return across the light-to-heavy transitional continuum as we deem appropriate for market conditions.

Certain of the transitional CRE assets that we seek to lend against involve a level of borrower execution risk that we believe is difficult for traditional lenders and other debt market participants to appropriately underwrite if they lack comparable real estate development, ownership and operations experience and infrastructure. In addition, we believe that there is inherently less competition in the market for larger CRE loans having a moderate-to-heavy transitional profile, potentially resulting in more attractive pricing to us. Traditional lenders became less active in the transitional CRE lending space following the global financial crisis of 2008 due in part to the adverse capital treatment applicable to them with respect to these loans stemming from post-crisis banking regulations. Our target loan profile is also challenging for many non-traditional lenders that do not have the experience or resources to originate, manage and monitor loans that fit our loan portfolio objectives. In particular, many traditional and non-traditional lenders do not have the broader real estate platform resources to draw upon to manage these loans, which we believe is especially important when borrower performance deviates (or is anticipated to deviate) from underwritten business plans. We expect land and construction loans to represent as much as 20% to 40% of our loan portfolio at any time, subject to our view of market conditions.

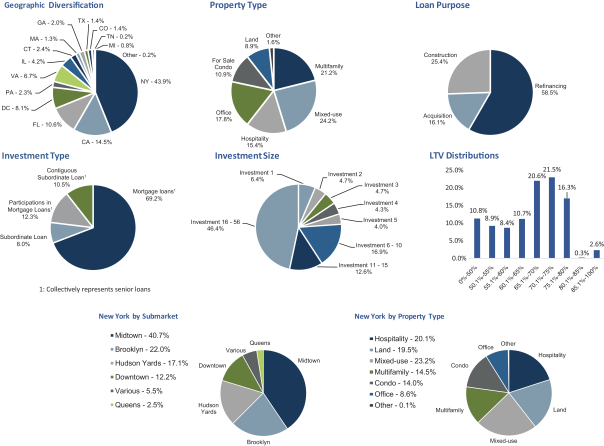

High Quality, Diversified Loan Portfolio with Stable, Attractive Yields

As of June 30, 2021, we had a $6.1 billion loan portfolio (based on unpaid principal balance) on transitional CRE assets, summarized as follows:

| • | 43.9% of our loans are secured by real estate (or equity interests relating thereto) located in the New York metropolitan area with an average remaining loan commitment of approximately $128.9 million, and no other metropolitan area represents more than 14.5% of our loan portfolio. |

16

Table of Contents

| • | Our loans are diversified across property types, with no property type representing more than 24.2% of our loan portfolio. We had no loans secured solely by retail real estate and a relatively small portion of the collateral value underlying our loans on mixed-use properties was related to retail components therein. |

| • | No individual investment exceeded 6.4% of our loan portfolio, our five largest investments represented 24.1% of our loan portfolio, and our 15 largest investments represented 53.6% of our loan portfolio. |

| • | 98.3% of our loans based on unpaid principal balance were floating rate and 94.5% of our floating rate loans based on unpaid principal balance (and 99.7% of our floating rate loans based on unfunded loan commitments (which represents remaining loan commitments less unpaid principal balance of our loans)) had interest rate floors tied to market-standard floating rates, such as LIBOR, providing protection against certain decreases in prevailing interest rates. |

| • | The weighted average one-month LIBOR floor of our loans based on unpaid principal balance was 1.47%. The LIBOR floor on all of our floating rate loans which had a LIBOR floor was in excess of one-month LIBOR of 0.10% as of June 30, 2021. |

| • | Our loan portfolio’s weighted average all-in yield was 6.6%, with a weighted average term to initial and fully extended maturity of 1.1 years and 2.6 years, respectively, providing significant contractual cash flow visibility. |

| • | We had $1.1 billion in unfunded loan commitments outstanding across 24 investments, the funding of which remains subject to satisfactory completion of specified borrower conditions, all of which were floating rate loan commitments with the exception of $23.2 million in fixed rate loan commitments. Of the $1.1 billion in unfunded floating rate loan commitments, the weighted average coupon was one-month LIBOR + 4.48% (subject to weighted average LIBOR floors of 1.65%). |

| • | Our loan portfolio’s weighted average LTV was 65.9%, providing substantial subordinate capital to our funded loan amounts. |

In addition, for each quarter from the quarter ended March 31, 2020 to the quarter ended June 30, 2021, we have paid dividends representing a yield of 7.7% to 9.1% on our book value per share, while maintaining conservative leverage with a Net Debt-to-Equity Ratio of 1.4x at December 31, 2019, 1.5x at December 31, 2020, and 1.5x at June 30, 2021.

We believe our current loan portfolio demonstrates our ability to deliver on our investment strategy.

In February 2021, we foreclosed on a portfolio of seven limited service hotel properties located in New York, New York that secured a mezzanine loan with an unpaid principal balance of $103.9 million as of February 8, 2021 that we originated in February 2018. Our real estate owned investment at the time of foreclosure was encumbered by a securitized senior mortgage, which we assumed on February 8, 2021 with a principal balance of $300.0 million. In June 2021 the terms of the securitized senior mortgage were modified, which included the repayment of $10.0 million of principal, and extension of its maturity date by an additional three years to February 2024. At June 30, 2021, the outstanding balance of our debt related to real estate owned was $290.0 million.

Established Sourcing and Origination Relationships

Our long-standing industry relationships provide us with valuable sources of investment opportunities and market insights that we believe allow us to selectively originate loans which best fit our loan portfolio objectives and investment criteria. Our Sponsor has cultivated extensive relationships in the real estate investment, development, lending and brokerage communities as well as with the executives and professionals of real estate operating companies and other companies that derive significant value from real estate investment activity. As a

17

Table of Contents

result of our Sponsor’s strong industry presence and deal flow, we have reviewed over 1,200 potential CRE lending opportunities totaling approximately $185.4 billion since our inception through June 30, 2021, of which 82%, 15% and 3% were sourced from brokers, existing borrowers and lenders, respectively. Of the transactions we have ultimately executed, 54%, 34% and 11% were sourced from brokers, existing borrowers and lenders, respectively. We believe our relationships with brokers, existing borrowers and lenders demonstrate the advantages of our platform, process and reputation in offering bespoke and flexible financing solutions. These factors have also enabled us to establish new client relationships with consistently high retention rates as repeat borrowers. Borrowers that were or became repeat borrowers or their affiliates comprised 57% of the total number of investments that we have originated as of June 30, 2021. Historically, our Sponsor has not competed with our borrowers to acquire the assets we finance, positioning us as a preferred lender against competitors who may also manage equity funds who compete with our borrowers.

The strength of our origination relationships and expertise is demonstrated by the growth in our origination volume and portfolio size over a relatively short time since our formation. We have originated aggregate loan commitments of approximately $11.5 billion since inception, including originating and increasing existing aggregate loan commitments of $235.3 million and $450.3 million, respectively, during the six months ended June 30, 2021 and 2020, and $513.1 million and $4.0 billion, respectively, during the years ended December 31, 2020 and 2019. Origination volume during the year ended December 31, 2020 was limited due to the COVID-19 pandemic, which we expect to return to normalized levels as the economy continues to improve.

Rigorous Underwriting Process and Proactive Asset Management

We leverage our Sponsor’s broad real estate investment, development and management experience to employ “ownership-like” underwriting methods. On each loan, we conduct a thorough analysis of the underlying asset, the borrower and the borrower’s business plan and evaluate alternative uses of collateral in order to distinguish execution risk from basis risk. Although our objective is to originate loans for which the borrower will perform as expected and pay as agreed, we believe that in a downside scenario, we have the ability to evaluate and mitigate much of the execution risk by utilizing our Sponsor’s broad experience and capabilities in developing, owning and managing real estate equity investments. In our view, options are limited to mitigate the basis risk taken by lenders who extend excess financing for a particular asset or property in light of unpredictable future market developments. Accordingly, our Manager is focused on creating a portfolio with an appropriate level of execution risk based on our Sponsor’s experience and capabilities and, in its judgment, relatively limited basis risk. We believe that the performance of certain of our loans since the COVID-19 pandemic demonstrates the strength of our underwriting, asset selection and asset management processes.

One example of how our underwriting and proactive management were employed to address a particular challenge was our recent experience with our mezzanine loan secured by seven limited service hotel properties. In February 2018, we originated a mezzanine loan with an initial principal balance of $85.0 million secured by a portfolio of seven limited service hotel properties located in New York, New York. Following the onset of the COVID-19 pandemic, the hotels were forced to close, causing the borrower to experience financial difficulty, which resulted in the borrower not paying debt service on our mezzanine loan and the securitized senior mortgage. Beginning in June 2020, we began funding debt service on a $300.0 million securitized senior mortgage encumbering the portfolio as protective advances on our loan, which totaled $18.9 million through February 8, 2021. In February 2021, we foreclosed on the portfolio of hotel properties through a Uniform Commercial Code foreclosure and in June 2021 we modified the securitized senior mortgage by extending its maturity date for an additional three years to February 2024 and repaying $10.0 million of principal. Given our Sponsor’s experience and capabilities in real estate ownership and management, we believe we are well-positioned to own this real estate investment through what we expect to be improved operating performance as the New York City hotel market recovers. We believe we were able to foreclose on these assets at an attractive basis and can leverage our Sponsor’s deep experience and capabilities to ultimately achieve favorable risk-adjusted returns on this investment.

18

Table of Contents

From the closing of an investment through its realization, we leverage our Sponsor’s personnel and resources to remain in regular contact with borrowers, servicers and local market experts to actively monitor borrower progress against approved business plans, assess compliance with other loan terms, anticipate property and market issues and, when appropriate and necessary, enforce our rights and remedies. Our asset management team provides weekly updates on our loan portfolio and oversees a rigorous quarterly credit risk review and rating process for each loan in our loan portfolio.

Prudent Balance Sheet Management with Access to Diverse Financing Sources

As part of our financing strategy, we seek to diversify our financing sources and employ prudent levels of leverage, targeting a Total Leverage Ratio between 2.0x and 3.0x. Leveraging the experience of our Sponsor, we maintain relationships with diverse debt financing sources, with an emphasis on match-term financing for our loans. As of June 30, 2021, we had $4.4 billion in outstanding indebtedness, of which $1.5 billion, or 33.0% of all outstanding financings, was recourse to us. As of June 30, 2021, we had repurchase facilities with five counterparties representing a total financing capacity of up to $4.0 billion, of which $1.3 billion was undrawn, as well as asset-specific financing structures representing $762.0 million of total financing capacity, of which $112.9 million was undrawn, a $764.7 million secured term loan, or our Secured Term Loan, and a $290.0 million securitized senior mortgage on our one real estate owned investment. We actively evaluate financing alternatives for each investment, resulting in a leverage profile that we believe to be optimal for each investment and appropriate for our loan portfolio. As we continue to grow our platform, we expect to continue to employ conservative amounts of leverage and diversify our financing strategy from both a counterparty and financing-type standpoint.

Strong Alignment of Interest

At our inception, the Mack family, our Sponsor’s principals and senior management and other related parties, which we refer to as the Sponsor Parties, indirectly invested $30.0 million into the Company. We believe that the significant early-stage investment by these persons aligns our Sponsor’s interests with ours and creates an incentive to protect capital and maximize risk-adjusted returns for our stockholders over time.

In connection with the formation of MREG and MRECS, the Mack family invested significant capital to ensure that our Manager has a highly skilled team and the necessary infrastructure to execute our investment strategy with a long-term view of the opportunities within the transitional CRE lending space.

We do not lend to our Sponsor or its controlled affiliates.

Our Investment Strategy

We seek primarily to originate senior and subordinate loans on transitional CRE assets located in major U.S. markets and generally intend to hold our loans to maturity. Our investments typically have the following characteristics:

| • | investment size of $50 million to $300 million; |

| • | secured by transitional CRE assets (or equity interests relating thereto) in diverse property types; |

| • | located primarily within major U.S. markets with attractive fundamental characteristics supported by macroeconomic tailwinds; |

| • | coupon rates that are determined periodically on the basis of a floating base lending rate plus a credit spread; |

| • | no more than 80% LTV on an individual investment basis and no more than 75% LTV across the portfolio, in each case, at the time of origination or acquisition; |

19

Table of Contents

| • | two- to four-year initial terms with one to three six-month or one-year borrower extension options that are subject to the borrower satisfying certain conditions precedent; |

| • | borrowers with substantial operating experience in the particular property type and geographic market being evaluated, a track record of executing a similar business plan, a strong reputation and substantial equity capital invested in the property being financed; and |

| • | performance covenants on future funding and natural person non-recourse carve-out guarantors and completion guarantors, where appropriate. |

In addition to our primary focus on major U.S. markets, we are also seeking to originate senior and subordinate loans on transitional CRE assets located in other markets that we be believe demonstrate favorable demographic trends as a result of, among other factors, de-urbanization, migration to states with lower tax rates and perceived higher quality of life. We believe that our investment strategy currently provides significant opportunities for us to generate attractive risk-adjusted returns over time for our stockholders. However, to capitalize on the investment opportunities at different points in the economic and real estate investment cycle, we may modify or expand our investment strategy without our stockholders’ consent. We believe that the flexibility of our strategy supported by our Sponsor’s significant CRE experience and its extensive resources will allow us to take advantage of changing market conditions to maximize total returns for our stockholders.

Our Target Assets

We originate, co-originate and acquire senior and subordinate loans on transitional CRE assets located primarily in major U.S. markets. Together, we refer to the following types of investments as our target assets:

Senior Loans: We focus primarily on originating senior loans on transitional CRE assets, including:

| • | Mortgage Loans. Mortgage loans secured by a first priority or subordinate mortgage on transitional CRE assets. These loans are non-amortizing, require a balloon payment of principal at maturity (and in some cases, earlier pay downs in the case of loans that provide for partial releases of collateral upon the occurrence of specified events, such as the sale of condominium units) and are typically structured to be floating rate. Some of our loan commitments include a mixture of up-front and future funding obligations, with future fundings subject to the borrower achieving conditions precedent specified in the loan documents, such as meeting certain construction milestones and leasing thresholds. |

| • | Participations in Mortgage Loans. Participations in the mortgage loans we co-originate or acquire, for which other participations have been or are expected to be syndicated to other investors. |

| • | Contiguous Subordinate Loans. Under certain circumstances, we may structure our investment on a property to include both a senior mortgage and a subordinate loan component, which we refer to as a contiguous subordinate loan. In these cases, we believe the subordinate loan component of the investment, when taken together with its related senior mortgage loan component, renders the entire investment most similar to our other senior loans in comparison to other loan types given its overall credit quality and risk profile. |

Subordinate Loans: We also invest in mezzanine loans, which are primarily originated or co-originated by us, and are usually secured by a pledge of equity ownership interests in the direct or indirect property owner rather than directly by the underlying commercial properties. These loans are subordinate to a mortgage loan but senior to the property owner’s equity ownership interests. These loans may be tranched into senior and junior mezzanine loans. Rights under these loans are generally governed by intercreditor agreements which typically include the right to cure defaults under senior loans. Subordinate loans may also include subordinated mortgage interests, which are mortgage loan interests that are subordinate to senior mortgage loans but senior to the property owner’s equity interests.

20

Table of Contents