FOIA CONFIDENTIAL TREATMENT REQUESTED

PURSUANT TO 17 C.F.R. § 200.83

BY TALEND S.A.: TLND-001

THIS FILING HAS OMITTED CONFIDENTIAL INFORMATION INCLUDED IN AN UNREDACTED VERSION OF THIS LETTER DELIVERED TO THE COMMISSION. OMITTED INFORMATION HAS BEEN REPLACED WITH A PLACEHOLDER IDENTIFIED BY THE MARK “[***]”.

January 24, 2020

Ms. Christine Dietz and Mr. Frank Knapp

United States Securities and Exchange Commission

Division of Corporation Finance

Office of Technology

100 F Street, NE

Washington, DC 20549

Re: Talend S.A.

Form 10-K for the fiscal year ended December 31, 2018

Filed February 28, 2019

File No. 001-37825

Dear Ms. Dietz and Mr. Knapp:

Talend S.A. (the “Company”) respectfully submits this letter to the Securities and Exchange Commission (the “Commission”) via EDGAR in response to the comment letter dated January 8, 2020 relating to the Company’s Annual Report on Form 10-K filed with the Commission on February 28, 2019 (the “Form 10-K”). For the convenience of the Staff, we have reproduced the comments in bold in numerical sequence and the corresponding responses of the Company are shown below each comment. References to page numbers are to the page numbers in the Form 10-K.

Form 10-K for the fiscal year ended December 31, 2018

Note 2. Summary of significant accounting policies

(e) Revenue recognition

Allocation of the transaction price to the performance of obligations in the contract, page 83

1. | We note your response to prior comment 1. Please tell us the specific costs that directly relate to “providing” the IP and tell us what consideration was given to including the costs incurred to develop the IP. As part of your response, tell us what consideration was given to using the “adjusted market assessment approach” to estimate SSP for the performance obligations. Refer to ASC 606-10-32-34a. |

1

Confidential Treatment Requested by Talend S.A.: TLND-001

Response to Comment 1:

The Company respectfully advises the Staff that it has two separately identifiable performance obligations related to its on-premise subscription customers: the right to use the intellectual property (“IP”), including enhanced features, and the right to receive post-contract customer support (“PCS”).

The enhanced features included in the Company’s IP, and provided only to its paying enterprise customers, constitute the Company’s initial performance obligation. The Company’s second performance obligation represents the ongoing obligation to provide PCS over the term of the contract with the customer.

The Company respectfully advises the Staff that the only costs that directly relate to “providing” the IP to its customers are the costs incurred to develop the enhanced features. In the following response, the Company will seek to further explain 1) its business model relative to the broader software market, 2) its rationale for employing a “cost plus margin” approach rather than the “adjusted market assessment approach” and 3) the detailed methodology and analysis used in determining the appropriate allocation of transaction price between the identifiable performance obligations.

Background

Companies in the software market have adopted various strategies for developing and licensing software, with the two most prominent models being 1) open-source licensing and 2) proprietary licensing. The data integration and analytics software market in which the Company operates features this same bifurcation. For example, Cloudera, Inc., Elastic N.V., and MongoDB, Inc. utilize open-source licensing models, while Alteryx, Inc. and Tableau Software, Inc. utilize proprietary licensing models.

Open-Source Licensing Model

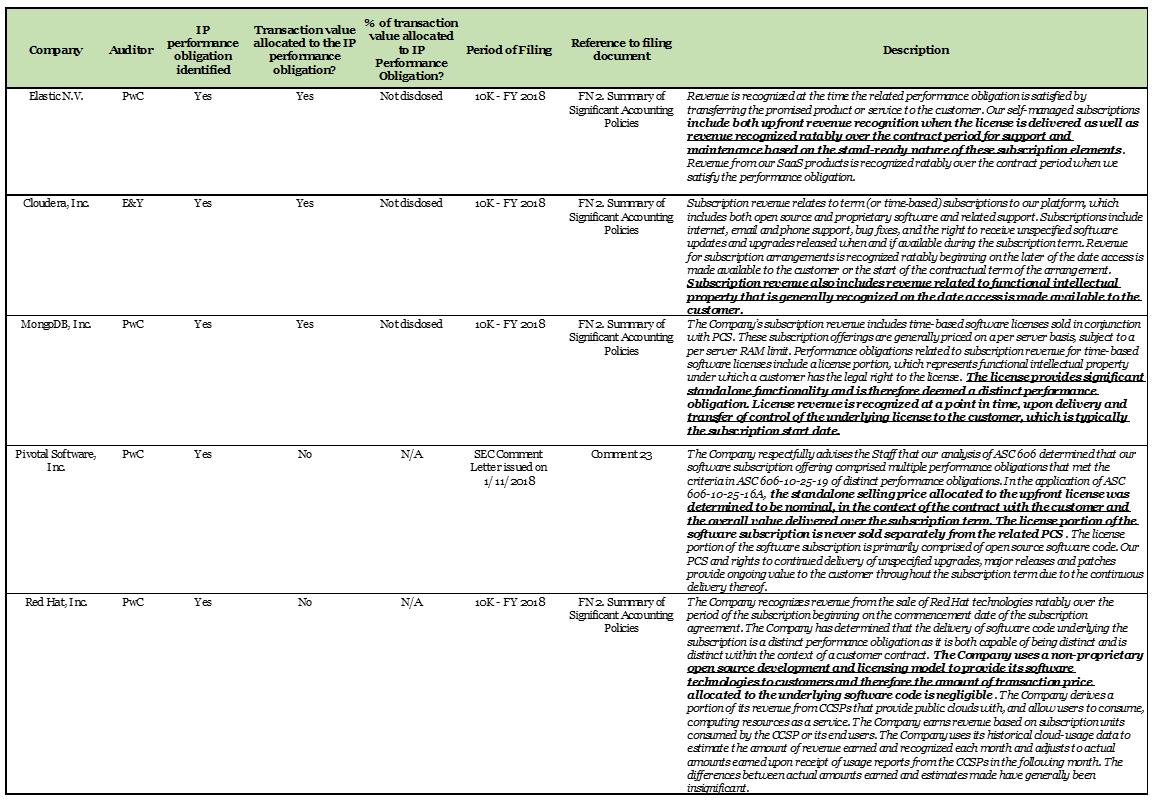

Under the open-source licensing model, companies develop the software and distribute it under an open-source license, such as the GNU General Public License, GNU Lesser General Public License or Apache License. Open-source licenses provide relatively broad rights for recipients of the software to use, copy, modify and redistribute the software. These rights afford significant latitude for recipients to inspect, suggest changes to, customize or enhance the software. Under these open-source licensing models, some companies provide only PCS for commercial purchase and others, like the Company, supplement PCS by providing some enhanced functionality that is only available for commercial purchase as IP. Across both variations, the Company has observed that registrants with open-source licensing models have allocated no value, or a nominal value, to the IP. The Company reviewed the following five registrants with open-source licensing models: Cloudera, Inc., Elastic N.V., MongoDB, Inc., Pivotal Software, Inc., and Red Hat, Inc. (see Appendix A).

2

Confidential Treatment Requested by Talend S.A.: TLND-001

Proprietary Licensing Model

Under the proprietary licensing model, by contrast, a software vendor generally develops the software itself without input from a wider community of participants. Registrants using the proprietary licensing model have allocated a significant portion of the transaction price to the IP. This business model approach, which is more common within the software market, is represented by companies such as Alteryx, Inc., Tableau Software, Inc., Oracle, Inc., and SAP SE.

The Company’s Open-Source Licensing Model

The Company employs an open-source licensing model. As part of its strategy, it offers an open-source solution, which drives awareness and usage amongst its target market, and a paid enterprise solution. The paid enterprise solution includes certain enhanced capabilities and features that are complementary to the core open-source solution, and PCS.

The Company’s open-source solution (“Talend Open Studio”) is designed to meet the requirements of a single user and is unlimited with respect to duration of use, processing volume, number of integration flows that can be designed using the solution and provides connectivity to the most commonly used data sources that can be accessed. The Company’s on-premise enterprise software solution builds on top of the Talend Open Studio applications and provides customers with additional enhanced features, including collaboration (e.g., sharing of data among multiple users), continuous integration, scheduling, monitoring (e.g., the ability to track events), API services and auditing capabilities. These enhanced features, which constituted a minority of total research and development costs for FY 2018, allow multiple users within an enterprise to work more efficiently together. Since the Company’s inception, its open-source applications have been downloaded more than three million times, while the Company has issued only approximately [***] licenses to paying customers.

These enhanced features represent the initial performance obligation and are immediately available to the Company’s paying enterprise customers. The Company believes that its customers are willing to pay for the enhanced features because of their utility in using the Company’s solution across teams and in production environments. The Company also believes customers see significantly more economic value from the technical support and know-how provided to the customer through PCS to maximize the use of these enhanced features. This is because the problem the Company’s solution solves (developing data analytic work flows and outputs to provide business insight for decision making) generally does not involve standardized business processes or homogenous data sets and requires a relatively higher touch service model to ensure customer success.

The Company’s model differentiates it from companies with proprietary software licensing models, which grant perpetual or term licenses to proprietary software (i.e., software where none of the code is or will be open-source) and provide basic telephone

3

Confidential Treatment Requested by Talend S.A.: TLND-001

support to the customer from their maintenance and support services. For example, the Company’s average enterprise customer with over $100,000 of annual spend submitted two cases per month during the 2018 fiscal year. This population of 472 customers represented approximately two-thirds of total subscription revenue during the 2018 fiscal year. As a data point, the Company considered a public proprietary data analytics software company (different from the Company’s mostly open-source licensing model) that provides significant technical and analytics modeling support to its customers as part of PCS (more consistent with the Company’s own services). This registrant allocates approximately 40-50% of the transaction price to the license, with the remaining transaction value allocated to PCS.

As part of PCS, the Company provides maintenance and support services to its enterprise customers. While the software maintenance services are similar to those provided by other software vendors (e.g., delivering unspecified updates through new releases each year), the support services are more extensive. Specifically, throughout the term of the contract, the support services include typical first line phone support as well as customer success technical consultation. In fact, it is this support that the Company’s customers find of significant economic value during the contract term and differentiates the Company from other software companies that provide only more standard software maintenance – i.e., without ongoing technical consultation. The technical consultation and support provided by the Company cover, and are applicable to, both the enhanced features as well as the open-source features of its solution. The following further details the technical maintenance and support features provided to the Company’s enterprise customers:

Maintenance Services include:

1) | Major updates/upgrades, which deliver major feature development and enhancements to existing features and incorporate applicable defect corrections made in prior major releases. The Company has typically had two major releases per year. |

2) | Minor updates, which deliver minor feature developments and enhancements to existing features and defect corrections. |

3) | Connectivity updates, which ensure the Company’s software is compatible with and supports other applications and systems. The Company constantly releases new or updated integrations into other applications and systems, which are important to the utility of its solutions and to its customers (e.g., if SalesForce.com updates their solution, the Company also updates the connection for the software to continue to work). |

Support Services, which vary depending on the level of customer spend, include:

1) | Technical support, which includes diagnosis and resolution of the product, installation and migration issues, as well as license issues. |

2) | 24/7/365 support for high severity issues. |

4

Confidential Treatment Requested by Talend S.A.: TLND-001

3) | Customer success services, which, among other things, include: |

a. | Providing access to customer success managers, |

b. | Regular case reviews, including for certain customers maintaining a copy of the customer’s environment for easy/quick resolutions of issues. |

c. | Design of integration jobs and data flows. |

d. | Reporting on customers’ operational performance metrics. |

The Company believes the customer success support services described above significantly differentiate the Company’s solution from those offered by proprietary software vendors. Specifically, under the proprietary software model, once the IP has been delivered, the support provided by the vendor is minimal. This differs from the Company’s high level of support, which requires regular interaction with the customer to ensure maximum utilization of the software. Furthermore, when compared to the allocation percentage adopted by the proprietary data analytics software vendor referenced above, which allocates 40-50% of transaction price to PCS, the Company believes its business model (as an open-source licensor, where much of the Company’s software code is available for use for free, but with a similarly high level of support) would suggest it should allocate substantially less of the transaction price to the license of IP than this comparable software vendor and more to the PCS.

Consideration of ASC 606, Revenue from Contracts with Customers

As discussed above, the Company’s open-source licensing model differs from certain other open-source companies, as it provides paying customers with enhanced features. Additionally, the Company’s business model differs significantly from the proprietary model as it provides much of its IP at no cost. Therefore, the value allocated to the initial performance obligation would be more than zero value allocated in certain open-source models, but significantly less than a proprietary company’s model (e.g., 70-80%).

As part of the initial adoption and ongoing review of its stand-alone selling price analysis, the Company noted: i) the absence of directly referenceable benchmarks due to few open-source companies with similar business models upon which to develop a precise market assessment approach and ii) the absence of observable prices as the Company’s products are sold as a bundle, including the license and PCS. Therefore, the Company concluded that it was appropriate to use a cost plus margin approach (see ASC 606-10-32-34(b)) to estimate stand-alone selling prices for each performance obligation.

Since its inception, the Company has incurred costs to develop the Talend Open Studio consisting of (i) costs incurred by its software engineering team to develop the architecture of the open-source solution, develop components and connectors, test various versions of the software and identify and deploy enhancements, (ii) sub-contractors engaged in the development process and (iii) operational costs such as amortization expense from intangible assets, facility costs and IT-related costs incurred

5

Confidential Treatment Requested by Talend S.A.: TLND-001

to support these operations. Additionally, the Company has incurred incremental cost to develop and deploy the enterprise enhanced features. These costs, which primarily consist of employee-related expenses, are incurred by the engineering team. The Company respectfully advises the Staff that the only costs considered in “providing” the IP to its customers are the cost incurred to develop the enhanced features.

As part of adopting of ASC 606 on January 1, 2018, the Company developed an SSP allocation model using actual financial data through June 2017 and estimated financial results for the remainder of 2017 and for future periods. The initial assessment resulted in 10% of total transaction value allocated to the IP performance obligation, with the remaining 90% allocated to the support performance obligation. Additionally, the Company refreshed the analysis using final financial data through December 31, 2018 noting the allocation percentages did not change materially from those determined at the ASC 606 adoption time.

The following steps summarize the initial analysis, which were replicated when performing the updated analysis using the actual results. Please refer to Appendix B for the summary of the model.

Step I: Determine the License Revenue

A. | Identify total R&D costs incurred during the respective period |

B. | Based on the work management and ticketing software, allocate R&D cost to the following: |

1. | Support development efforts |

2. | Open-source development efforts |

C. | Calculate the annual amortization expense related to the adjusted R&D cost (e.g., enhanced features) using the estimated useful life |

D. | Apply the desired margin to the annual cost of the IP to arrive at total License annual revenue |

Step II: Determine the Support Revenue

A. | Identify the following costs: |

1. | R&D costs incurred in FY 2018 to support development efforts |

2. | Other support cost incurred during the period to service current period contracts |

B. | Adjust total support cost by removing support costs related to Cloud solutions |

C. | Apply the desired margin to the annual cost of Support to arrive at total Support annual revenue |

Step III: Allocate revenue to each performance obligation

The Company has concluded that the costs incurred to develop the IP for the enterprise enhanced features, both historical and current, should be considered in the Company’s model to determine standalone selling price as it represents a meaningful amount of the total cost incurred necessary to fulfill the performance obligations. Based

6

Confidential Treatment Requested by Talend S.A.: TLND-001

on the model used, the Company has concluded that approximately 10% of the contract value should be allocated to the IP, with the remaining 90% of the contract value be allocated to PCS.

* * * * *

We hope the foregoing has been responsive to the Staff’s inquiry, and greatly appreciate the Staff’s expeditious review of this matter. If you should have any questions about this letter or require any further information, please call the undersigned at (650) 539-3189.

Very truly yours,

/s/ Adam Meister

Adam Meister

Chief Financial Officer

cc: Christal Bemont, Chief Executive Officer

Aaron Ross, General Counsel

Jacques Pierre, KPMG S.A.

Mark B. Baudler, Wilson Sonsini Goodrich & Rosati PC

Andrew D. Hoffman, Wilson Sonsini Goodrich & Rosati PC

7

Confidential Treatment Requested by Talend S.A.: TLND-001

APPENDIX A

8

Confidential Treatment Requested by Talend S.A.: TLND-001

APPENDIX B

[***]

9