five years6 years0.01

Exhibit 99.1

Unaudited Interim Report

for the

six-month

period ended 30 June 20234

The following is a review of our financial condition and results of operations as of 30 June 2023 and for the

six-month

periods ended 30 June 2023 and 2022, and of the key factors that have affected or are expected to be likely to affect our ongoing and future operations.This document includes information from the previously published results announcement and unaudited interim report of Anheuser-Busch InBev SA/NV for the

six-month

period ended 30 June 2023, as amended to comply with the requirements of Regulation G and Item 10(e) of RegulationS-K

promulgated by the U.S. Securities and Exchange Commission (“SEC”). The purpose of this document is to provide such additional disclosure as may be required by Regulation G and Item 10(e) and to delete certain information not in compliance with SEC regulations. This document does not update or otherwise supplement the information contained in the previously published results announcement and unaudited interim report.Some of the information contained in this discussion, including information with respect to our plans and strategies for our business and our expected sources of financing, contain forward-looking statements that involve risk and uncertainties. You should read “Forward-Looking Statements” below for a discussion of the risks related to those statements. You should also read “Item 3. Key Information—D. Risk Factors” of our Annual Report on Form

20-F

for the year ended 31 December 2022 filed with the SEC on 17 March 2023 (“2022

Annual Report

”) for a discussion of certain factors that may affect our business, financial condition and results of operations. See “Presentation of Financial and Other Data” in our 2022 Annual Report for further information on our presentation of financial information.

We have prepared our interim unaudited condensed consolidated financial statements as of 30 June 2023 and for the

six-month

period ended 30 June 2023 and 2022 in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board and in conformity with International Financial Reporting Standards as adopted by the European Union (“IFRS

”). The financial information and related discussion and analysis contained in this report are presented in U.S. dollars except as otherwise specified. Unless otherwise specified the financial information analysis in this Form

6-K

is based on interim unaudited condensed financial statements as of 30 June 2023 and for thesix-month

period ended 30 June 2023 and 2022. The reported numbers as of 30 June 2023 and for thesix-month

period ended 30 June 2023 and 2022 are unaudited, and in the opinion of management, include all normal adjustments that are necessary to present fairly the results for the interim periods. Due to seasonal fluctuations and other factors, the results of operations for thesix-month

period ended 30 June 2023 and 2022 are not necessarily indicative of the results to be expected for the full year. Certain monetary amounts and other figures included in this report have been subject to rounding adjustments. Accordingly, any discrepancies in any tables between the totals and the sums of amounts listed are due to rounding.Anheuser-Busch InBev is a publicly traded company (Euronext: ABI) based in Leuven, Belgium, with secondary listings on the Mexico (MEXBOL: ANB) and South Africa (JSE: ANH) stock exchanges and with American Depositary Receipts on the New York Stock Exchange (NYSE: BUD). As a company, we dream big to create a future with more cheers. We are always looking to serve up new ways to meet life’s moments, move our industry forward and make a meaningful impact in the world. We are committed to building great brands that stand the test of time and to brewing the best beers using the finest ingredients. Our diverse portfolio of well over 500 beer brands includes global brands Budweiser

®

, Corona®

and Stella Artois®

; multi-country brands Beck’s®

, Hoegaarden®

, Leffe®

and Michelob Ultra®

; and local champions such as Aguila®

, Antarctica®

, Bud Light®

, Brahma®

, Cass®

, Castle®

, Castle Lite®

, Cristal®

, Harbin®

, Jupiler®

, Modelo Especial®

, Quilmes®

, Victoria®

, Sedrin®

and Skol®

. Our brewing heritage dates back more than 600 years, spanning continents and generations. From our European roots at the Den Hoorn brewery in Leuven, Belgium. To the pioneering spirit of the Anheuser & Co brewery in St. Louis, US. To the creation of the Castle Brewery in South Africa during the Johannesburg gold rush. To Bohemia, the first brewery in Brazil. Geographically diversified with a balanced exposure to developed and developing markets, we leverage the collective strengths of approximately 167,000 employees based in nearly 50 countries worldwide. For 2022, AB InBev’s reported revenue was USD 57.8 billion (excluding joint ventures and associates).Capitalized terms used herein and not defined have the meanings given to them in the 2022 Annual Report.

5

Forward-Looking Statements

There are statements in this document, such as statements that include the words or phrases “will likely result,” “are expected to,” “will continue,” “is anticipated,” “anticipate,” “estimate,” “project,” “may,” “might,” “could,” “believe,” “expect,” “plan,” “potential,” “we aim,” “our goal,” “our vision,” “we intend” or similar expressions that are forward-looking statements. These statements are subject to certain risks and uncertainties. Actual results may differ materially from those suggested by these statements due to, among others, the risks or uncertainties listed below. See also “Item 3. Key Information—D. Risk Factors” of our 2022 Annual Report for further discussion of risks and uncertainties that could impact our business.

These forward-looking statements are not guarantees of future performance. Rather, they are based on current views and assumptions and involve known and unknown risks, uncertainties and other factors, many of which are outside our control and are difficult to predict, that may cause actual results or developments to differ materially from any future results or developments expressed or implied by the forward-looking statements. Factors that could cause actual results to differ materially from those contemplated by the forward-looking statements include, among others:

| • | global, regional and local economic weakness and uncertainty, including the risks of an economic downturn, recession and/or inflationary pressures in one or more of our key markets, and the impact they may have on us, our customers and our suppliers and our assessment of that impact; |

| • | continued geopolitical instability (including as a result of the ongoing conflict between Russia and Ukraine), which may have a substantial impact on the economies of one or more of our key markets and may result in, among other things, disruptions to global supply chains, increases in commodity and energy prices with follow-on inflationary impacts, and economic and political sanctions; |

| • | financial risks, such as interest rate risk, foreign exchange rate risk (in particular as against the U.S. dollar, our reporting currency), commodity risk, asset price risk, equity market risk, counterparty risk, sovereign risk, liquidity risk, inflation or deflation, including inability to achieve our optimal net debt level; |

| • | changes in government policies and currency controls; |

| • | continued availability of financing and our ability to achieve our targeted coverage and debt levels and terms, including the risk of constraints on financing in the event of a credit rating downgrade; |

| • | the monetary and interest rate policies of central banks, in particular the European Central Bank, the Board of Governors of the U.S. Federal Reserve System, the Bank of England, Banco Central do Brasil, Banco Central de la República Argentina Banco de la República |

| • | changes in applicable laws, regulations and taxes in jurisdictions in which we operate, including the laws and regulations governing our operations and changes to tax benefit programs, as well as actions or decisions of courts and regulators; |

| • | limitations on our ability to contain costs and expenses or increase our prices to offset increased costs; |

| • | failure to meet our expectations with respect to expansion plans, premium growth, accretion to reported earnings, working capital improvements and investment income or cash flow projections; |

| • | our ability to continue to introduce competitive new products and services on a timely, cost-effective basis; |

| • | the effects of competition and consolidation in the markets in which we operate, which may be influenced by regulation, deregulation or enforcement policies; |

6

| • | changes in consumer spending; |

| • | changes in pricing environments; |

| • | volatility in the availability or prices of raw materials, commodities and energy; |

| • | difficulties in maintaining relationships with employees; |

| • | regional or general changes in asset valuations; |

| • | greater than expected costs (including taxes) and expenses; |

| • | damage to our reputation or brand image; |

| • | climate change and other environmental concerns; |

| • | the risk of unexpected consequences resulting from acquisitions, joint ventures, strategic alliances, corporate reorganizations or divestiture plans, and our ability to successfully and cost-effectively implement these transactions and integrate the operations of businesses or other assets we have acquired; |

| • | the outcome of pending and future litigation, investigations and governmental proceedings; |

| • | natural and other disasters, including widespread health emergencies such as the COVID-19 pandemic, cyberattacks and military conflict and political instability; |

| • | any inability to economically hedge certain risks; |

| • | inadequate impairment provisions and loss reserves; |

| • | technological disruptions, threats to cybersecurity and the risk of loss or misuse of personal data; |

| • | other statements included in this document that are not historical; and |

| • | our success in managing the risks involved in the foregoing. |

Many of these risks and uncertainties are, and will be, exacerbated by the ongoing conflict between Russia and Ukraine and any worsening of the global business and economic environment as a result. Our statements regarding financial risks, including interest rate risk, foreign exchange rate risk, commodity risk, asset price risk, equity market risk, counterparty risk, sovereign risk, inflation and deflation, are subject to uncertainty. For example, certain market and financial risk disclosures are dependent on choices about key model characteristics and assumptions and are subject to various limitations. By their nature, certain of the market or financial risk disclosures are only estimates and,

as

a result, actual future gains and losses could differ materially from those that have been estimated.We caution that the forward-looking statements in this document are further qualified by the risk factors disclosed in “Item 3. Key Information—D. Risk Factors” of our 2022 Annual Report that could cause actual results to differ materially from those in the forward-looking statements. Subject to our obligations under Belgian and U.S. law in relation to disclosure and ongoing information, we undertake no obligation to update publicly or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

7

Management Comments

Continued global momentum, partially offset by US performance, delivered high-single digit revenue growth

We delivered a

top-line

increase of 7.2%1

, with revenue growth in more than 85% of our markets in the second quarter of 2023 driven by a revenue per hl increase of 9.0%1

, as a result of pricing actions, ongoing premiumization and other revenue management initiatives. Volumes declined by 1.4%2

in the second quarter of 2023, as growth in the majority of our markets was offset by performance in the US. Normalized EBITDA increased by 5.0%3

in the second quarter of 2023 compared to the same period of 2022, despite anticipated commodity cost headwinds and increased sales and marketing investments. Underlying EPS for the first six months of 2023 was USD 1.374

.Progressing our strategic priorities

We continue to execute on and invest in three key strategic pillars to deliver consistent growth and long-term value creation.

| • | Lead and grow the category : In the first six months of 2023, we invested approximately USD 3.5 billion in sales and marketing, an increase of 12.8% versus the same period in 2022, driving an increase of our portfolio brand power5 in approximately 60% of our key markets. We are executing on five proven and scalable levers to drive category expansion: |

○ | Inclusive Category |

○ | Core Superiority mid-single digit1 revenue increase, as double-digit growth in South Africa and Colombia was partially offset by the revenue decline of Bud Light in the US. Our mainstream brands gained or maintained share of segment in two thirds of our key markets, according to our estimates. |

○ | Occasions Development no-alcohol beer portfolio delivered approximately 30%1 revenue growth in the second quarter of 2023, with our performance driven by Budweiser Zero in Brazil and the growth of Corona Cero in Canada and Europe. Leveraging our digitaldirect-to-consumer |

○ | Premiumization : Our above core beer portfolio grew revenue by more than 10%1 in the second quarter of 2023, led by our global brands and double-digit1 growth of Modelo in Mexico and Spaten in Brazil. Our global brands grew revenue by 18.4%1,6 outside of their home markets in the second quarter of 2023, led by Corona, which was recently recognized by Kantar BrandZ as the #1 fastest growing global beer brand by value, which grew 23.7%1, 6 . Budweiser delivered a revenue increase of 16.9%1,6 with broad-based growth in 25 markets and supported by the return of consumer demand in China. Stella Artois grew by 14.5%1,6. |

○ | Beyond Beer 1 as growth globally was partially offset by a soft malt-based seltzer industry in the US. Global growth was primarily driven by the expansion of Brutal Fruit in Africa and the Vicky portfolio in Mexico. |

| • | Digitize and monetize our ecosystem |

○ | Digitizing our relationships with more than 6 million customers globally |

1

Excluding the effects of the 2022 and 2023 acquisitions and disposals and currency translation effects, see “—Revenue” below.2

Excluding volume changes attributable to the 2022 and 2023 acquisitions and disposals and transfers of businesses, see “—Volumes” below.3

Normalized EBITDA is anon-IFRS

measure. For a discussion of how we use Normalized EBITDA, and its limitations, and a table showing the calculation of our Normalized EBITDA, for the periods shown, see “—Normalized EBITDA” below.4

Underlying EPS is anon-IFRS

measure. For a discussion of how we use Underlying EPS, and its limitations, and a table showing the calculation of our Underlying EPS, for the periods shown, see “—Profit Attributable to our Equity Holders” below.5

The Brand Power of our portfolio of beer and Beyond Beer brands is assessed based on data sourced from reports published by Kantar Worldpanel.6

The growth of our global brands (excluding the effects of the 2022 and 2023 acquisitions and disposals and currency translation effects, see “—Revenue” below), Budweiser, Stella Artois and Corona, excludes exports to Australia for which a perpetual license was granted to a third party upon disposal of the Australia operations in 2020.8

| 2023 captured through B2B digital platforms. In the second quarter of 2023, BEES had 3.3 million monthly active users and captured approximately USD 9.2 billion in gross merchandise value (GMV), growth of 15% and 30% versus the second quarter of 2022 respectively. BEES Marketplace is live in 15 markets with 63% of BEES customers also Marketplace buyers. Marketplace captured approximately USD 340 million in GMV from sales of third-party products in the second quarter of 2023, growth of 41% versus the same period last year. |

○ | Leading the way in DTC solutions : Our omnichanneldirect-to-consumer |

| • | Optimize our business : In the first six months of 2023, disciplined overhead management and efficient allocation of resources across our operations, enabled us to invest approximately USD 2.1 billion in capex and USD 3.5 billion in sales and marketing to drive the organic growth of our business, while managing the continued elevated cost environment. Underlying EPS4 for the first six months of 2023 was USD 1.37, an increase of USD 0.04 per same period of 2022, cycling a USD 0.05 per share net benefit from tax credits in Brazil year-over-year. |

Advancing our sustainability priorities

We continued to innovate and make progress towards our 2025 Sustainability Goals through key local initiatives with the potential to scale globally. For Climate Action, we invested in a biomass processor in our Jupille brewery in Belgium to produce thermal energy from malt husks, which is expected to reduce our gas consumption by more than 15% and lower our carbon emissions. In Sustainable Agriculture, to strengthen local supply chains we provided technical and financial training to over 900 smallholder barley farmers in Uganda. In Water Stewardship, we installed new vacuum pump technology in breweries across several markets to reduce water usage in bottle fillers by approximately 50%. For Circular Packaging, our business in Brazil launched a nationwide returnable bottle campaign to help increase the use of returnable packaging

by

promoting affordability and sustainability.Creating a future with more cheers

In the first six months of 2023, we delivered 10.0%service to our customers, generating value for our stakeholders and delivering on our purpose to create a future with more cheers.

1

revenue growth and 9.1%3,7

Normalized EBITDA growth while continuing to invest for the long-term in our brands, facilities and digital transformation. We remain focused on brewing high quality beer, providingbest-in-class

7

Excluding the effects of the 2022 and 2023 acquisitions and disposals, the 2022 Brazilian tax credits and currency translation, see “—Normalized EBITDA” below.9

Results of Operations for the

Six-Month

Period Ended 30 June 2023 Compared toSix-Month

Period Ended 30 June 2022Effective 1 January 2023,gains/(losses) on derivatives related to the hedging of our share-based payment programs are reported in exceptional net finance income/(cost). As a result, the relevant financial information for the

mark-to-market

six-month

period ended 30 June 2022 has been amended to conform to the basis of presentation for thesix-month

period ended 30 June 2023 to reflect this change in classification.Brazilian tax credits

In the

six-month

period ended 30 June 2023,Ambev, our subsidiary, recognized USD 78 million of interest income in Finance income related to tax credits in Brazil. In the

six-month

period ended 30 June 2022,Ambev, our subsidiary, recognized USD 201 million income in Other operating income and USD 113 million of interest income in Finance income related to tax credits in Brazil.

The table below presents our condensed consolidated results of operations for the

six-month

periods ended 30 June 2023 and 2022.Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | Change | ||||||||||

(USD million, except volumes) | (%) (1) | |||||||||||

Volumes (thousand hectoliters) | 288,131 | 289,074 | (0.3 | ) | ||||||||

Revenue | 29,333 | 28,027 | 4.7 | |||||||||

Cost of sales | (13,536 | ) | (12,784 | ) | (5.9 | ) | ||||||

Gross profit | 15,796 | 15,243 | 3.6 | |||||||||

Selling, General and Administrative expenses | (9,051 | ) | (8,616 | ) | (5.0 | ) | ||||||

Other operating income/(expenses) | 327 | 478 | (31.6 | ) | ||||||||

Exceptional items | (107 | ) | (105 | ) | (1.9 | ) | ||||||

Profit from operations | 6,965 | 7,000 | (0.5 | ) | ||||||||

Normalized EBITDA (²) | 9,668 | 9,583 | 0.9 | |||||||||

Note:

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

| (2) | Normalized EBITDA is a non-IFRS measure. For a discussion of how we use Normalized EBITDA and its limitations, and a table showing the calculation of our Normalized EBITDA, for the periods shown, see “—Normalized EBITDA” below. |

10

Volumes

Our reported volumes include both beer and beyond beer and

non-beer

(primarily carbonated soft drinks) volumes. In addition, volumes include not only brands that we own or license, but also third-party brands that we brew or otherwise produce as a subcontractor and third-party products that we sell through our distribution network, particularly in Europe and Middle Americas. Volumes sold by the Global Export and Holding Companies businesses are shown separately.The table below summarizes the volume evolution by business segment.

Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | Change | ||||||||||

(thousand hectoliters) | (%) (1) | |||||||||||

North America | 47,395 | 51,448 | (7.9 | ) | ||||||||

Middle Americas | 72,164 | 72,024 | 0.2 | |||||||||

South America | 76,023 | 76,815 | (1.0 | ) | ||||||||

EMEA | 42,842 | 42,962 | (0.3 | ) | ||||||||

Asia Pacific | 49,589 | 45,385 | 9.3 | |||||||||

Global Export and Holding Companies | 117 | 440 | (73.4 | ) | ||||||||

Total | 288,131 | 289,074 | (0.3 | ) | ||||||||

Note:

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

Our consolidated volumes for the

six-month

period ended 30 June 2023 decreased by 0.9 million hectoliters, or 0.3%, to 288.1 million hectoliters compared to our consolidated volumes for thesix-month

period ended 30 June 2022, as growth in the majority of our markets in the second quarter of 2023 was offset by performance in the US. The results for thesix-month

period ended 30 June 2023 reflect the performance of our business after the completion of certain acquisitions and disposals we undertook in 2022 and 2023 (collectively, the “2022 and 2023 acquisitions and disposals”).The 2022 and 2023 acquisitions and disposals include acquisitions and disposals which were individually not significant and had no significant impact on our volumes for the

six-month

period ended 30 June 2023 compared to thesix-month

period ended 30 June 2022.Excluding volume changes attributable to the 2022 and 2023 acquisitions and disposals, our own beer volumes decreased 0.8% in the

six-month

period ended 30 June 2023 compared to thesix-month

period ended 30 June 2022. On the same basis, in thesix-month

period ended 30 June 2023, ournon-beer

volumes increased 2.1% compared to the same period in 2022.North America

In the

six-month

period ended 30 June 2023, our volumes in North America decreased by 4.1 million hectoliters, or 7.9%, compared to thesix-month

period ended 30 June 2022. Excluding volume changes attributable to transfers of businesses from the Global Export and Holding Companies, our total volumes decreased by 8.0% in thesix-month

period ended 30 June 2023, compared to the same period last year.In the United States, our(“STWs”) declined by 8.6% and our(“STRs”) declined by 9.2%, underperforming the industry, primarily due to the volume decline of Bud Light. The beer industry continued to demonstrate resilience in the first half of 2023, delivering revenue growth of 2.6%, while volumes declined 2.7% according to Circana. Our total beer industry share declined in the second quarter of 2023, but has been stable since the last week of April through the end of June. Since April, we actively engaged with over 170,000 consumers across the country through a third-party research firm and the data shows that most consumers surveyed are favorable towards the Bud Light brand and approximately 80% are favorable or neutral. As part of our long-term plan, we increased investments in our key brands, invested in measures to support our wholesalers and continued key initiatives such as partnerships with NFL, NBA, Folds of Honor and Farm Rescue.

sales-to-wholesalers

sales-to-retailers

In Canada, volumes declined by

low-single

digits.Middle Americas

In the

six-month

period ended 30 June 2023, our volumesin

Middle Americas increased by 0.2%, compared to thesix-month

period ended 30 June 2022.In Mexico, volumes were flat. Our performance in the first six months of 2023 was driven by ongoing portfolio development and digital transformation. Our above core portfolio continued to outperform, growing revenue by

mid-teens,

led by the strong performance of Modelo, Michelob Ultra and Pacifico. We continued to progress our digital and physical DTC initiatives in the second quarter of 2023 with our digital DTC platform, TaDa, now operating in over 60 major cities and fulfilling on average over 300 000 orders per month and the opening of a further 150 Modelorama stores.11

In Colombia, volumes declined by

low-single

digits and in Peru volumes declined bylow-single

digits.In Ecuador, our volumes increased by low-single digits, supported by continued share of total alcohol gains. Our above core brands continued to lead our growth in the first half of 2023, delivering a double-digit revenue increase.

South America

In the

six-month

period ended 30 June 2023, our volumes in South America decreased by 0.8 million hectoliters, or 1.0%, compared to thesix-month

period ended 30 June 2022, with our beer volumes decreasing 1.7% and soft drinks increasing 0.7%.In Brazil, our total volumes were flat with beer volumes down 0.9% and

non-beer

volumes up 2.5%. Our premium and super premium brands continued to outperform in the first six months of 2023, delivering volume growth in themid-thirties,

led by Original, Spaten and Corona. BEES Marketplace continued to expand, reaching over 700,000 customers, a 29% increase versus the second quarter of 2022, and growing GMV by 64%. Our digital DTC platform, Zé Delivery, reached 4.6 million monthly active users this quarter, a 12% increase versus the second quarter of 2022, and increased GMV by 12%.In Argentina, volumes declined by

mid-single

digits in the first six months of 2023.EMEA

In EMEA, our volumes, including subcontracted volumes, for the

six-month

period ended 30 June 2023 decreased by 0.1 million hectoliters, or 0.3%, with our own beer volumes increasing by 0.9%, compared to thesix-month

period ended 30 June 2022. Excluding volume changes attributable to transfers of businesses from the Global Export and Holding Companies, our total volumes decreased by 0.5% in thesix-month

period ended 30 June 2023, compared to the same period last year.On the same basis, in Europe, our volumes declined by

low-single

digits in the first six months of 2023. We continue to drive premiumization across Europe. Our premium and super premium brands delivered double-digit revenue growth in the first six months of 2023, led by Corona and Budweiser.In South Africa, volumes grew by

mid-single

digits in the first six months of 2023. We continue to see strong consumer demand for our portfolio, gaining share of beer and total alcohol according to our estimates. Carling Black Label, the #1 beer brand in the country, led our performance in thesix-month

period of 2023, withlow-teens

volume growth and our global brands grew volumes by more than 40%, driven by Corona.In Africa excluding South Africa, volumes declined by low teens in Nigeria in the first six months of 2023, driven by a soft industry which was impacted by the continued challenging operating environment. In our other markets, we grew volumes in aggregate by low-single digits in the first six months of 2023, driven primarily by Tanzania, Ghana and Uganda.

Asia Pacific

For the

six-month

period ended 30 June 2023, our volumes increased by 4.2 million hectoliters, or 9.3%, compared to thesix-month

period ended 30 June 2022.In China, volumes grew by 9.4% in the first six months of 2023, outperforming the industry according to our estimates. We delivered volume growth across all segments of our portfolio in the first six months of 2023, led by high-teens volume growth in both our premium and super premium portfolios. The roll out and adoption of the BEES platform continued, with BEES now present in over 220 cities and over 45% of our revenue through digital channels in June.

In South Korea, volumes grew by low single-digits in the first

six

months of 2023.Global Export & Holding Companies

For the

six-month

period ended 30 June 2023, Global Export and Holding Companies volumes decreased by 0.3 million hectoliters, or 73.4% compared to the same period last year.Excluding transfer of businesses mainly to the Europe and North America zone, our total volumes decreased by 58.9% in the

six-month

period ended 30 June 2023, compared to the same period last year.12

Revenue

The following table reflects changes in revenue across our business segments for the

six-month

period ended 30 June 2023 as compared to our revenue for thesix-month

period ended 30 June 2022:Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | Change | ||||||||||

(USD million) | (%) (1) | |||||||||||

North America | 7,926 | 8,192 | (3.2 | ) | ||||||||

Middle Americas | 7,573 | 6,693 | 13.1 | |||||||||

South America | 5,849 | 5,333 | 9.7 | |||||||||

EMEA | 4,070 | 3,940 | 3.3 | |||||||||

Asia Pacific | 3,679 | 3,471 | 6.0 | |||||||||

Global Export & Holding Companies | 236 | 399 | (40.9 | ) | ||||||||

Total | 29,333 | 28,027 | 4.7 | |||||||||

Note:

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

Our consolidated revenue was USD 29,333 million for the

six-month

period ended 30 June 2023. This represented an increase of USD 1,306 million, or 4.7%, compared to our consolidated revenue for thesix-month

period ended 30 June 2022 of USD 28,027 million. The results for thesix-month

period ended 30 June 2023 reflect (i) the performance of our business after the completion of certain acquisitions and disposals we undertook in 2022 and 2023 and (ii) currency translation effects.| · | The 2022 and 2023 acquisitions and disposals had no significant impact on our consolidated revenue for the six-month period ended 30 June 2023 compared to thesix-month period ended 30 June 2022. |

| · | Our consolidated revenue for the six-month period ended 30 June 2023 also reflects a negative currency translation impact of USD 1,459 million mainly arising from currency translation effects in EMEA, South America and Asia Pacific. |

Excluding the effects of the 2022 and 2023 acquisitions and disposals and currency translation, our revenue increased 10.0% and by 10.6% on a per hectoliter basis in the

six-month

period ended 30 June 2023 compared to the same period in 2022. Despite the decrease in volumes discussed above, the increase in our consolidated revenue was driven by the increase in our revenue on a per hectoliter basis, as a result of pricing actions, ongoing premiumization and other revenue management initiatives.The growth in our revenue per hectoliter in the

six-month

period ended 30 June 2023 was most significant in South America, EMEA and Middle Americas.| · | In South America, the growth in the revenue per hectoliter in Argentina was driven primarily by revenue management initiatives in a highly inflationary environment. In Brazil, we reported double-digit revenue per hectoliter growth, driven by revenue management initiatives and continued premiumization. |

| · | In Middle Americas, the growth in the revenue per hectoliter was driven by pricing actions and other revenue management initiatives. |

| · | In EMEA, the growth in the revenue per hectoliter was driven by pricing actions. In Europe, there was also continued momentum of our premium and super premium brands. |

On the same basis, combined revenues of our global brands, Budweiser, Stella Artois and Corona, increased by 16.9% outside their home markets in the

six-month

period ended 30 June 2023 compared to the same period of 2022.We are reporting our Argentinean operation applying hyperinflation accounting under IAS 29, following the categorization of Argentina as a country with a three-year cumulative inflation rate greater than 100%, since 2018. Inflation in Argentina has accelerated over the past 12 months, resulting in a more significant impact on the revenue growth (excluding the effects of the 2022 and 2023 acquisitions and disposals and currency translation effects) of AB InBev than historically. For illustrative purposes, fully excluding the Argentinean operation, the revenue growth (excluding the effects of the 2022 and 2023 acquisitions and disposals and currency translation effects) for AB InBev for

six-month

period ended 30 June 2023 would be 6.7%.13

Cost of Sales

The following table reflects changes in cost of sales across our business segments for the

six-month

period ended 30 June 2023 as compared to thesix-month

period ended 30 June 2022:Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | Change | ||||||||||

(USD million) | (%) (1) | |||||||||||

North America | (3,420 | ) | (3,349 | ) | (2.1 | ) | ||||||

Middle Americas | (2,926 | ) | (2,625 | ) | (11.5 | ) | ||||||

South America | (2,949 | ) | (2,792 | ) | (5.6 | ) | ||||||

EMEA | (2,210 | ) | (2,000 | ) | (10.5 | ) | ||||||

Asia Pacific | (1,750 | ) | (1,655 | ) | (5.7 | ) | ||||||

Global Export & Holding Companies | (281 | ) | (362 | ) | 22.4 | |||||||

Total | (13,536 | ) | (12,784 | ) | (5.9 | ) | ||||||

Note:

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

Our consolidated cost of sales was USD 13,536 million for the

six-month

period ended 30 June 2023. This represented an increase of USD 752 million, or 5.9% compared to our consolidated cost of sales for thesix-month

period ended 30 June 2022. The results for thesix-month

period ended 30 June 2023 reflect (i) the performance of our business after the completion of certain acquisitions and disposals we undertook in 2022 and 2023 and (ii) currency translation effects.| · | The 2022 and 2023 acquisitions and disposals did not have a significant impact on our consolidated cost of sales for the six-month period ended 30 June 2023 compared to thesix-month period ended 30 June 2022. |

| · | Our consolidated cost of sales for the six-month period ended 30 June 2023 also reflects a positive currency translation impact of USD 690 million mainly arising from currency translation effects in South America, EMEA and Asia Pacific. |

Excluding the effects of the 2022 and 2023 acquisitions and disposals and currency translation, our cost of sales increased by USD 1,463 million or 11.5%. Our consolidated cost of sales for the

six-month

period ended 30 June 2023 was partially impacted by decrease in volumes discussed above. On the same basis, our consolidated cost of sales per hectoliter increased by 12.2%. This was primarily driven by anticipated commodity cost headwinds. The increase in cost of sales per hectoliter was most significant in South America, with Argentina in a high inflationary environment, EMEA and North America.14

Operating Expenses

The discussion below relates to our operating expenses, which equal the sum of our distribution, sales and marketing expenses, administrative expenses and other operating income and expenses (net), for the

six-month

period ended 30 June 2023 as compared to thesix-month

period ended 30 June 2022. Our operating expenses do not include exceptional charges, which are reported separately.Our operating expenses for the

six-month

period ended 30 June 2023 were USD 8,724 million, representing an increase of USD 586 million, compared to our operating expenses for the same period in 2022.Six-month periodended 30 June 2023 | Six-month periodended 30 June 2022 | Change | ||||||||||

(USD million) | (%) (1) | |||||||||||

Selling, General and Administrative expenses | (9,051 | ) | (8,616 | ) | (5.0 | ) | ||||||

Other operating income/(expenses) | 327 | 478 | (31.6 | ) | ||||||||

Total Operating Expenses | (8,724 | ) | (8,138 | ) | (7.2 | ) | ||||||

Note:

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

Selling, General and Administrative Expenses

The following table reflects changes in our distribution expenses, sales and marketing expenses and administrative expenses (our “selling, general and administrative expenses”) across our business segments for the

six-month

period ended 30 June 2023 as compared to thesix-month

period ended 30 June 2022:Six-month periodended 30 June 2023 | Six-month periodended 30 June 2022 | Change | ||||||||||

(USD million) | (%) (1) | |||||||||||

North America | (2,354 | ) | (2,279 | ) | (3.3 | ) | ||||||

Middle Americas | (1,863 | ) | (1,631 | ) | (14.2 | ) | ||||||

South America | (1,804 | ) | (1,609 | ) | (12.1 | ) | ||||||

EMEA | (1,307 | ) | (1,341 | ) | 2.5 | |||||||

Asia Pacific | (1,033 | ) | (999 | ) | (3.4 | ) | ||||||

Global Export & Holding Companies | (692 | ) | (756 | ) | 8.5 | |||||||

Total | (9,051 | ) | (8,616 | ) | (5.0 | ) | ||||||

Note:

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

Our consolidated selling, general and administrative expenses were USD 9,051 million for the

six-month

period ended 30 June 2023. This represented an increase of USD 435 million, or 5.0%, as compared to thesix-month

period ended 30 June 2022. The results for thesix-month

period ended 30 June 2023 reflect (i) the performance of our business after the completion of certain acquisitions and disposals we undertook in 2022 and 2023 and (ii) currency translation effects.| • | The 2022 and 2023 acquisitions and disposals had no significant impact on our consolidated selling, general and administrative expenses for the six-month period ended 30 June 2023 compared to thesix-month period ended 30 June 2022. |

| • | Our consolidated selling, general and administrative expenses for the six-month period ended 30 June 2023 also reflects a positive currency translation impact of USD 426 million mainly arising from currency translation effects in South America, EMEA and Asia Pacific. |

15

Excluding the effects of the 2022 and 2023 acquisitions and disposals and currency translation, our consolidated selling, general and administrative expenses increased by 9.8%, due primarily to increased sales and marketing investments.

Other operating income/(expense)

The following table reflects changes in other operating income and expenses across our business segments for the

six-month

period ended 30 June 2023 as compared to thesix-month

period ended 30 June 2022:Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | Change | ||||||||||

(USD million) | (%) (1) | |||||||||||

North America | 18 | 28 | (35.7 | ) | ||||||||

Middle Americas | 8 | (12 | ) | - | ||||||||

South America | 171 | 312 | (45.2 | ) | ||||||||

EMEA | 83 | 88 | (5.7 | ) | ||||||||

Asia Pacific | 53 | 67 | (20.9 | ) | ||||||||

Global Export & Holding Companies | (6 | ) | (5 | ) | (20.0 | ) | ||||||

Total | 327 | 478 | (31.6 | ) | ||||||||

Note:

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

The net positive effect of our consolidated other operating income and expenses for the

six-month

period ended 30 June 2023 was USD 327 million. This represented a decrease of USD 151 million, as compared to thesix-month

period ended 30 June 2022. The results for thesix-month

period ended 30 June 2023 reflect (i) the performance of our business after the completion of certain acquisitions and disposals we undertook in 2022 and 2023, (ii) the tax credits in Brazil recognized by our subsidiary, Ambev in 2022 and (iii) currency translation effects.| • | The 2022 and 2023 acquisitions and disposals and the 2022 Brazilian tax credits negatively impacted our net consolidated other operating income and expenses by USD 204 million on a net basis for the six-month period ended 30 June 2023 compared to thesix-month period ended 30 June 2022. |

| • | Our net consolidated other operating income and expenses for the six-month period ended 30 June 2023 had no significant currency translation impact. |

Excluding the effects of the 2022 and 2023 acquisitions and disposals, Brazilian tax credits and currency translation, our net consolidated other operating income and expenses increased by 26.2%, mainly driven by higher government grants and the impact of disposal of

non-core

assets year-over-year.Exceptional Items

Exceptional items are items which, in our management’s judgment, need to be disclosed separately by virtue of their size and incidence in order to obtain a proper understanding of our financial information. We consider these items to be significant in nature.

For the

six-month

period ended 30 June 2023, exceptional items included in profit from operations consisted of restructuring charges, business and asset disposal (including impairment losses) and legal costs. Exceptional items were as follows forsix-month

period ended 30 June 2023 and 2022:Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | |||||||

(USD million) | ||||||||

COVID-19 costs | - | (13 | ) | |||||

Restructuring | (50 | ) | (51 | ) | ||||

Business and asset disposal (including impairment losses) | (38 | ) | 6 | |||||

Legal costs | (19 | ) | - | |||||

AB InBev Efes related costs | - | (47 | ) | |||||

Total | (107 | ) | (105 | ) | ||||

16

Restructuring

Exceptional restructuring charges amounted to a net cost of USD 50 million for the

six-month

period ended 30 June 2023 as compared to a net cost of USD 51 million for thesix-month

period ended 30 June 2022. These charges primarily relate to exceptional organizational alignments resulting from improvement in efficiency and aim to eliminate overlapping organizations or duplicated and manual processes, taking into account the right match of employee profiles with the new organizational requirements.Business and assets disposals (including impairment losses)

Business and assets disposals (including impairment losses) amounted to a net cost of USD 38 million for the

six-month

period ended 30 June 2023 mainly comprising impairment of intangible assets and othernon-core

assets sold in the period.Legal costs

The company recorded exceptional legal costs of USD 19 million for the

six-month

period ended 30 June 2023 related to the successful outcome of series of lawsuits regarding Ambev warrants.AB InBev Efes related costs

During the

six-month

period ended 30 June 2022, we incurred exceptional costs of USD 47 million related to AB InBev Efes, following the discontinuation of exports to Russia and our forfeiture of benefits from the operations of the associate.Profit from Operations

The following table reflects changes in profit from operations across our business segments for the

six-month

period ended 30 June 2023 as compared to thesix-month

period ended 30 June 2022:Six-month periodended 30 June 2023 | Six-month periodended 30 June 2022 | Change | ||||||||||

(USD million) | (%) (1) | |||||||||||

North America | 2,131 | 2,570 | (17.1 | ) | ||||||||

Middle Americas | 2,781 | 2,416 | 15.1 | |||||||||

South America | 1,241 | 1,234 | 0.6 | |||||||||

EMEA | 618 | 667 | (7.4 | ) | ||||||||

Asia Pacific | 944 | 879 | 7.4 | |||||||||

Global Export & Holding Companies | (749 | ) | (766 | ) | 2.2 | |||||||

Total | 6,965 | 7,000 | (0.5 | ) | ||||||||

Note:

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

Our profit from operations amounted to USD 6,965 million for the

six-month

period ended 30 June 2023. This represented a decrease of USD 35 million, as compared to our profit from operations for thesix-month

period ended 30 June 2022. The results for thesix-month

period ended 30 June 2023 reflect (i) the performance of our business after the completion of certain acquisitions and disposals we undertook in 2022 and 2023, (ii) the 2022 Brazilian tax credits, (iii) currency translation effects and (iv) the effects of certain exceptional items as described above.| • | The 2022 and 2023 acquisitions and disposals and the Brazilian tax credits negatively impacted our consolidated profit from operations by USD 239 million for the six-month period ended 30 June 2023 compared to thesix-month period ended 30 June 2022. |

| • | Our consolidated profit from operations for the six-month period ended 30 June 2023 also reflects a negative currency translation impact of USD 358 million. |

| • | Our profit from operations for the six-month period ended 30 June 2023 was negatively impacted by USD 107 million of certain exceptional items, as compared to a negative impact of USD 105 million for thesix-month period ended 30 June 2022. See “Exceptional Items” above for a description of exceptional items that impacted our profit from operations for thesix-month period ended 30 June 2023 and 2022. |

Excluding the effects of the 2022 and 2023 acquisitions and disposals, the 2022 Brazilian tax credits and currency translation, our profit from operations increased by 8.3%. This increase was most significant in South America, APAC

17

and Middle Americas, mainly due to revenue growth that was partially offset by anticipated commodity cost headwinds and higher selling, general and administrative expenses due primarily to increased sales and marketing investments.

Normalized EBITDA

The following table reflects changes in our Normalized EBITDA, for the

six-month

period ended 30 June 2023 as compared to thesix-month

period ended 30 June 2022: Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | Change | ||||||||||

(USD million) | (%) (1) | |||||||||||

Profit attributable to equity holders of AB InBev | 1,977 | 1,692 | 16.8 | |||||||||

Profit attributable to non-controlling interests | 678 | 782 | (13.3 | ) | ||||||||

Profit of the period | 2,655 | 2,474 | 7.3 | |||||||||

Net finance cost | 3,223 | 2,268 | (42.1 | ) | ||||||||

Income tax expense | 1,192 | 1,244 | 4.2 | |||||||||

Share of result of associates | (105 | ) | (129 | ) | (18.6 | ) | ||||||

Exceptional share of results of associates | - | 1,143 | - | |||||||||

Profit from operations | 6,965 | 7,000 | (0.5 | ) | ||||||||

Exceptional items | 107 | 105 | (1.9 | ) | ||||||||

Profit from operations, before exceptional items (2) | 7,072 | 7,105 | (0.5 | ) | ||||||||

Depreciation, amortization and impairment | 2,596 | 2,477 | (4.8 | ) | ||||||||

Normalized EBITDA (3) | 9,668 | 9,583 | 0.9 | |||||||||

Note:

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

| (2) | Profit from operations, before exceptional items is a non-IFRS measure. See “Item 5. Operating and Financial Review and Results of Operations—Results of Operations—Year Ended 31 December 2022 Compared to Year Ended 31 December 2021—Normalized EBITDA” of our 2022 Annual Report for additional information on our definition and use of Profit from operations, before exceptional items. |

| (3) | Normalized EBITDA is a non-IFRS measure. See “Item 5. Operating and Financial Review and Results of Operations—Results of Operations—Year Ended 31 December 2022 Compared to Year Ended 31 December 2021—Normalized EBITDA” of our 2022 Annual Report for additional information on our definition and use of Normalized EBITDA. |

Our Normalized EBITDA amounted to USD 9,668 million for the

six-month

period ended 30 June 2023. This represented an increase of USD 85 million, or 0.9%, as compared to our Normalized EBITDA for thesix-month

period ended 30 June 2022. The results for thesix-month

period ended 30 June 2023 reflect (i) the performance of our business after the completion of the acquisitions and disposals we undertook in 2022 and 2023, (ii) the Brazilian tax credits and (iii) currency translation effects. Excluding the effects of the 2022 and 2023 acquisitions and disposals, the 2022 Brazilian tax credits and currency translation, our Normalized EBITDA increased by 9.1%, despite anticipated commodity cost headwinds and increased sales and marketing investments.18

Net Finance Income/(Cost)

Our net finance income/(cost) items were as follows for the

six-month

period ended 30 June 2023 and 30 June 2022:Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | Change | ||||||||||||||

(USD million) | (%) (1) | |||||||||||||||

Net interest expense | (1,630) | (1,683) | 3.1 | |||||||||||||

Net interest on net defined benefit liabilities | (42) | (37) | (13.5) | |||||||||||||

Accretion expense | (385) | (336) | (14.6) | |||||||||||||

Net interest income on Brazilian tax credits | 78 | 113 | (31.0) | |||||||||||||

Other financial results | (540) | (501) | (7.8) | |||||||||||||

Net finance cost before exceptional finance results (2) | (2,520) | (2,444) | (3.1) | |||||||||||||

Mark-to-market (2) | (703) | 296 | - | |||||||||||||

Gain/(loss) on bond redemption and other | - | (120) | - | |||||||||||||

Exceptional net finance income/(cost) (2) | (703) | 176 | - | |||||||||||||

Net finance income/(cost) | (3,223) | (2,268) | (42.1) | |||||||||||||

Note:

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

| (2) | The financial information for the six-month period ended 30 June 2022 has been amended to conform to the basis of presentation for thesix-month period ended 30 June 2023 to reflect the change in classification ofmark-to-market |

Our net finance cost for the

six-month

period ended 30 June 2023 was USD 3,223 million, as compared to a net finance cost of USD 2,268 million for thesix-month

period ended 30 June 2022, representing a cost increase of USD 955 million.The net finance costs before exceptional financial results increased from USD 2,444 million for the

six-month

period ended 30 June 2022 to USD 2,520 million for thesix-month

period ended 30 June 2023.Exceptional net finance income/(cost) includes a negativeadjustment of USD 703 million on derivative instruments related to the hedging of our share-based payment programs and on derivative instruments entered into to hedge the shares issued in relation to the combination with Grupo Modelo and SAB, compared to a positiveadjustment of USD 296 million for the

mark-to-market

mark-to-market

six-month

period ended 30 June 2022.The number of shares covered by the hedging of our share-based payment programs, the deferred share instrument and the restricted shares, together with the opening and closing share prices, are shown below:

Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | |||||||||

Share price at the start of the six-month period (in euro) | 56.27 | 53.17 | ||||||||

Share price at the end of the six-month period (in euro) | 51.83 | 51.36 | ||||||||

Number of derivative equity instruments at the end of the period (in millions) | 100.5 | 100.5 | ||||||||

Share of Results of Associates

Our share of results of associates for the

six-month

period ended 30 June 2023 was USD 105 million as compared to USD 129 million for thesix-month

period ended 30 June 2022.Exceptional Share of Results of Associates

Our exceptional share of results of associates for the

six-month

period ended 30 June 2022 included thenon-cash

impairment of USD 1,143 million we recorded on our investment in AB InBev Efes.19

Income Tax Expense

Our total income tax expense for the

six-month

period ended 30 June 2023 was USD 1,192 million, with an effective tax rate of 31.9%, as compared to an income tax expense of USD 1,244 million and an effective tax rate of 26.3% for thesix-month

period ended 30 June 2022. The effective tax rate for thesix-month

period ended 30 June 2023 was negatively impacted by thenon-deductible

losses from derivatives related to the hedging of our share-based payment programs and hedging of the shares issued in a transaction related to the combination with Grupo Modelo and SAB, while the effective tax rate of 2022 was positively impacted bynon-taxable

gains from these derivatives.The effective tax rate for the

six-month

period ended 30 June 2023 was negatively impacted by country mix.Profit Attributable to

Non-Controlling

InterestsProfit attributable to

non-controlling

interests was USD 678 million for thesix-month

period ended 30 June 2023, a decrease of USD 104 million from USD 782 million for thesix-month

period ended 30 June 2022.Profit Attributable to Our Equity Holders

Profit attributable to our equity holders for the

six-month

period ended 30 June 2023 was USD 1,977 million compared to USD 1,692 million for the same period in 2022. Basic earnings per share of USD 0.98 for thesix-month

period ended 30 June 2023 is based on 2,016 million shares outstanding, representing the weighted average number of ordinary and restricted shares outstanding during this period, where weighted average number of ordinary and restricted shares means, for any period, the number of shares outstanding at the beginning of the period, adjusted by the number of shares canceled, repurchased or issued during the period, including deferred share instruments and stock lending, multiplied by a time-weighting factor.Underlying profit, attributable to equity holders of AB InBev for the

six-month

period ended 30 June 2023 was USD 2,762 million. Items excluded from Underlying profit, attributable to equity holders of AB InBev are theafter-tax

exceptional items discussed above under “—Exceptional Items, “—Net Finance Income/(Cost)” and “—Exceptional Share of Results of Associates” and the impact of hyperinflation accounting.Underlying EPS for the

six-month

period ended 30 June 2023 was USD 1.37. Underlying EPS is basic earnings per share excluding theafter-tax

exceptional items discussed above under “—Exceptional Items, “—Net Finance Income/(Cost)” and “—Exceptional Share of Results of Associates” and the impact of hyperinflation accounting.The increase in profit attributable to our equity holders for the

six-month

period ended 30 June 2023 was primarily due to the exceptional share of results of associates recorded in thesix-month

period ended 30 June 2022, partially offset by the increase in the net finance cost in thesix-month

period ended 30 June 2023 compared to the same period in 2022. Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | |||||||||

(USD million) | ||||||||||

Profit attributable to equity holders of AB InBev | 1,977 | 1,692 | ||||||||

Exceptional items, before taxes | 107 | 105 | ||||||||

Exceptional net finance cost, before taxes (1) | 703 | (176) | ||||||||

Exceptional share of results of associates | - | 1,143 | ||||||||

Exceptional taxes | (51) | (69) | ||||||||

Exceptional non-controlling interest | (9) | 3 | ||||||||

Hyperinflation impacts | 35 | (26) | ||||||||

Underlying profit, attributable to equity holders of AB InBev (2) | 2,762 | 2,672 | ||||||||

Note:

| (1) | The financial information for the six-month period ended 30 June 2022 has been amended to conform to the basis of presentation for thesix-month period ended 30 June 2023 to reflect the change in classification ofmark-to-market |

| (2) | Underlying profit, attributable to equity holders of AB InBev is a non-IFRS measure. See “Item 5. Operating and Financial Review and Results of Operations—Results of Operations—Year Ended 31 December 2022 Compared to Year Ended 31 December 2021—Profit Attributable to Our Equity Holders” of our 2022 Annual Report for additional information on our definition and use of Underlying profit attributable to equity holders of AB InBev. |

20

Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | |||||||||||

(USD per share) | ||||||||||||

Basic earnings per share | 0.98 | 0.84 | ||||||||||

Exceptional items, before taxes | 0.05 | 0.05 | ||||||||||

Exceptional net finance cost, before taxes (1) | 0.35 | (0.09) | ||||||||||

Exceptional share of results of associates | - | 0.57 | ||||||||||

Exceptional taxes | (0.03) | (0.03) | ||||||||||

Hyperinflation accounting impacts in EPS | 0.02 | (0.01) | ||||||||||

Underlying EPS (2) | 1.37 | 1.33 | ||||||||||

Note:

| (1) | The financial information for the six-month period ended 30 June 2022 has been amended to conform to the basis of presentation for thesix-month period ended 30 June 2023 to reflect the change in classification ofmark-to-market |

| (2) | Underlying EPS is a non-IFRS measure. See “Item 5. Operating and Financial Review—E. Results of Operations—Year Ended 31 December 2022 Compared to the Year Ended 31 December 2021—Profit Attributable to Our Equity Holders” of our 2022 Annual Report for additional information on our definition and use of Underlying EPS. |

The calculation of earnings per share is based on 2,016 million shares outstanding, representing the weighted average number of ordinary and restricted shares outstanding during the

six-month

period ended 30 June 2023 (30 June 2022: 2,012 million shares).Impact of Changes in Foreign Exchange Rates

Foreign exchange rates have a significant impact on our consolidated financial statements. The following table sets forth the percentage of our revenue realized by currency for the

six-month

period ended 30 June 2023 and 2022:Six-month period ended | ||||||||||||

30 June 2023 | 30 June 2022 | |||||||||||

U.S. dollar | 27.3% | 29.3% | ||||||||||

Brazilian real | 14.5% | 13.7% | ||||||||||

Mexican peso | 12.3% | 10.3% | ||||||||||

Chinese yuan | 9.6% | 9.4% | ||||||||||

Euro | 5.5% | 5.5% | ||||||||||

Colombian peso | 3.6% | 4.1% | ||||||||||

South African rand | 3.6% | 3.9% | ||||||||||

Argentinean peso (1) | 3.4% | 3.3% | ||||||||||

Canadian dollar | 3.2% | 3.4% | ||||||||||

Peruvian nuevo sol | 3.1% | 2.8% | ||||||||||

Dominican peso | 2.1% | 2.0% | ||||||||||

Pound sterling | 1.9% | 2.1% | ||||||||||

South Korean won | 1.9% | 2.1% | ||||||||||

Other | 7.9% | 8.0% | ||||||||||

Note:

| (1) | Hyperinflation accounting was adopted starting from the September year-to-date |

21

Liquidity and Capital Resources

The following table sets forth our consolidated cash flows for the

six-month

period ended 30 June 2023 and 2022:Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | |||||||||||

(USD million) | ||||||||||||

Cash flow from operating activities | 1,597 | 2,182 | ||||||||||

Cash flow from/(used in) investing activities | (2,061) | (1,917) | ||||||||||

Cash flow from/(used in) financing activities | (2,823) | (5,392) | ||||||||||

Net increase/(decrease) in cash and cash equivalents | (3,287) | (5,128) | ||||||||||

Cash flow from operating activities

The following table sets forth our cash flow from operating activities for the

six-month

period ended 30 June 2023 and 30 June 2022:Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | |||||||||||

(USD million) | ||||||||||||

Profit | 2,655 | 2,474 | ||||||||||

Interest, taxes and non-cash items included in profit | 7,512 | 7,015 | ||||||||||

Cash flow from operating activities before changes in working capital and provisions | 10,167 | 9,489 | ||||||||||

Change in working capital | (4,615) | (3,339) | ||||||||||

Pension contributions and use of provisions | (192) | (195) | ||||||||||

Interest and taxes (paid)/received | (3,806) | (3,823) | ||||||||||

Dividends received | 43 | 50 | ||||||||||

Cash flow from operating activities | 1,597 | 2,182 | ||||||||||

Cash flow from operating activities was USD 1,597 million for the

six-month

period ended 30 June 2023 compared to USD 2,182 million forsix-month

period ended 30 June 2022. The decrease was primarily driven by changes in working capital for the first six months of 2023 compared to the same period last year as 2022.Changes in working capital in the first half of 2023 and 2022 reflect higher working capital levels at the end of June than at

year-end

as a result of seasonality.Cash flow from investing activities

The following table sets forth our cash flow from investing activities for the

six-month

period ended 30 June 2023 and 2022:Six-month period ended 30 June 2023 | Six-month period ended 30 June 2022 | |||||||||||

(USD million) | ||||||||||||

Net capital expenditure (1) | (2,063) | (1,939) | ||||||||||

Sale/(acquisition) of subsidiaries, net of cash disposed/ acquired of | (8) | (44) | ||||||||||

Proceeds from sale/(acquisition) of other assets | 10 | 66 | ||||||||||

Cash flow from / (used in) investing activities | (2,061) | (1,917) | ||||||||||

Note:

| (1) | Net capital expenditure consists of acquisitions of plant, property and equipment and of intangible assets, minus proceeds from sale. |

22

Cash flow from investing activities was a net cash outflow of USD 2,061 million for the

six-month

period ended 30 June 2023 compared to a net cash outflow of USD 1,917 million for thesix-month

period ended 30 June 2022. The increase in the cash outflow from investing activities was mainly due to higher net capital expenditures in 2023 compared to 2022.Our net capital expenditures were USD 2,063 million for the

six-month

period ended 30 June 2023 and USD 1,939 million for thesix-month

period ended 30 June 2022. Out of the total half-year 2023 capital expenditures approximately 33% was used to improve our production facilities, 49% was used for logistics and commercial investments and 18% was used for improving administrative capabilities and the purchase of hardware and software.Cash flow from financing activities

The following table sets forth our cash flow from financing activities for the

six-month

period ended 30 June 2023 and 2022:Six-month periodended 30 June 2023 | Six-month periodended 30 June 2022 | |||||||||||

(USD million) | ||||||||||||

Dividends paid | (1,923 | ) | (1,276 | ) | ||||||||

Net (payments on)/proceeds from borrowings | 155 | (3,452 | ) | |||||||||

Payments of lease liabilities | (359 | ) | (286 | ) | ||||||||

Other (including purchase of non-controlling interests) | (696 | ) | (378 | ) | ||||||||

Cash flow from / (used in) financing activities | (2,823 | ) | (5,392 | ) | ||||||||

Cash outflow from financing activities was USD 2,823 million for the

six-month

period ended 30 June 2023, compared to a cash outflow of USD 5,392 million for thesix-month

period ended 30 June 2022. The decrease is primarily driven by lower debt redemption in 2023 compared in 2022.As of 30 June 2023, we had total liquidity of USD 16.9 billion, which consisted of USD 10.1 billion available under committed long-term credit facilities and USD 6.8 billion of cash, cash equivalents and short-term investments in debt securities less bank overdrafts. Although we may borrow such amounts to meet our liquidity needs, we principally rely on cash flows from operating activities to fund the company’s operations.

Capital Resources and Equity

Our net debt was USD 73.8 billion as of 30 June 2023 as compared to USD 69.7 billion as of 31 December 2022. See note 17 to our unaudited condensed consolidated interim financial statements as of 30 June 2023 and for the

six-month

period ended 30 June 2023 and 2022 for a discussion of how we use net debt and a table showing the calculation of our net debt as of 30 June 2023. Apart from operating results net of capital expenditures, the net debt was mainly impacted by payments of interests and taxes (USD 3.8 billion increase of net debt), dividend payments to shareholders of AB InBev and Ambev (USD 1.9 billion increase of net debt) and foreign exchange impact on net debt (USD 0.4 billion increase of net debt).96% of our bond portfolio holds a fixed-interest rate, 42% is denominated in currencies other than USD and maturities are well-distributed across the next several years.

Consolidated equity attributable to our equity holders as at 30 June 2023 was USD 77,460 million, compared to USD 73,398 million as at 31 December 2022. The net increase in equity results from the profit attributable to equity shareholders and foreign exchange gains on translation of foreign operations primarily related to the combined effect of the appreciation of the closing rates of the Colombian peso, the Euro, the Mexican peso, the Peruvian sol and the weakening of the closing rate of the South African rand, which resulted in a foreign exchange translation adjustment of USD 3 610 million as of 30 June 2023 (increase of equity). This increase in equity is partially offset by dividends paid.

23

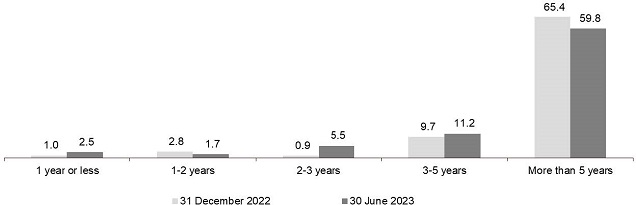

The chart below shows the bond repayment schedule as of 30 June 2023 (figures in USD billion):

Further details on interest bearing loans and borrowings, repayment schedules and liquidity risk are disclosed in notes 17 and 19 to our unaudited condensed consolidated interim financial statements as of 30 June 2023 and for the

six-month

period ended 30 June 2023 and 2022.Adoption of hyperinflation accounting in Argentina

Since 1 January 2018, we have applied hyperinflation accounting as prescribed by IAS 29for our Argentinean subsidiaries.

Financial Reporting in Hyperinflationary Economies

The results for the

six-month

period ended 30 June 2023 were translated at the June 2023 closing rate of 256.71 Argentinean pesos per US dollar. The results for thesix-month

period ended 30 June 2022, were translated at the June 2022 closing rate of 125.21 Argentinean pesos per US dollar.The impact of hyperinflation accounting for the period ended 30 June 2023 amounted to USD 23 million increase in revenue, USD 66 million positive monetary adjustment reported in the finance line and represented USD (0.02) earnings per share excluding exceptional items.

24

Guarantor Financial Information

The debt securities issued by (i) Anheuser-Busch InBev Finance Inc. (“”) under Indentures dated as of January 17, 2013, January 25, 2016 and May 15, 2017, in each case among ABIFI, Anheuser-Busch InBev SA/NV (the “”), the subsidiary guarantors listed therein and the Bank of New York Mellon Trust Company, N.A., as trustee (ii) Anheuser-Busch InBev Worldwide Inc. (“”) under Indentures dated as of October 16, 2009, December 16, 2016 and April 4, 2018, in each case among ABIWW, the Parent Guarantor, the subsidiary guarantors listed therein and the Bank of New York Mellon Trust Company, N.A, as trustee and (iii) Anheuser-Busch Companies, LLC (“”) and ABIWW, as

ABIFI

Parent Guarantor

ABIWW

ABC

co-issuers,

under the Indenture dated as of November 13, 2018, among ABC, ABIWW, the subsidiary guarantors listed therein and the Bank of New York Mellon Trust Company, N.A., as trustee, are, in each case, fully and unconditionally guaranteed by the Parent Guarantor and jointly and severally guaranteed by Brandbrew S.A., Brandbev S.à r.l. and Cobrew NV, and by ABC (in respect of debt issued by ABIFI and/or ABIWW (as sole issuer)), ABIWW (in respect of debt issued by ABIFI) and by ABIFI (in respect of debt issued by ABIWW and/or ABC) on a full and unconditional basis. The Parent Guarantor owns, directly or indirectly, 100% of each of ABIFI, ABIWW, ABC, Brandbrew S.A., Brandbev S.à r.l. and Cobrew NV.Each guarantee provided under the aforementioned indentures is referred to as a “” and collectively, the “”; the subsidiaries of the Parent Guarantor providing Guarantees are referred to as the “” and the Parent Guarantor and Subsidiary Guarantors collectively are referred to as the “”. ABIWW, ABIFI and ABC are collectively referred to as the “”.

Guarantee

Guarantees

Subsidiary Guarantors

Guarantors

Issuers

For disclosure required by Rule

13-01

of RegulationS-X

of certain terms and conditions of the guarantees and how the issuer and guarantor structure and other factors may affect payments to the holder of the debt securities see “Item 5. Operating and Financial Review—G. Liquidity and Capital Resources—Guarantor Financial Information” of our 2022 Annual Report.Summarized financial information is presented below for Anheuser-Busch InBev SA/NV, the Issuers and the Subsidiary Guarantors on a combined basis after elimination of intercompany transactions and balances among them and does not include investments in and equity in the earnings of

non-guarantor

subsidiaries. The intercompany balances withNon-Guarantor

Subsidiaries have been presented separately. This summarized financial information is not intended to present the financial position or results of operations of Anheuser-Busch InBev SA/NV, the Issuers and the Subsidiary Guarantors in accordance with IFRS.Six-month periodended 30 June 2023¹ | Year ended 31 December 2022² | |||||||||||

USD million | USD million | |||||||||||

Income Statement Data | ||||||||||||

Revenue | 7,198 | 15,231 | ||||||||||

Gross profit | 3,675 | 8,183 | ||||||||||

Profit for the period | 66 | 975 | ||||||||||

Six-month periodended 30 June 2023 | Year ended 31 December 2022 | |||||||||||

USD million | USD million | |||||||||||

Statement of Financial Position Data | ||||||||||||

Due from non-guarantor subsidiaries | 95,048 | 99,031 | ||||||||||

Other non-current assets | 62,182 | 61,978 | ||||||||||

Non-current assets | 157,230 | 161,009 | ||||||||||

Due from non-guarantor subsidiaries | 10,064 | 3,595 | ||||||||||

Other current assets | 7,044 | 13,367 | ||||||||||

Current assets | 17,108 | 16,962 | ||||||||||

Due to non-guarantor subsidiaries | 23,547 | 24,657 | ||||||||||

Other non-current liabilities | 83,889 | 84,502 | ||||||||||

Non-current liabilities | 107,435 | 109,159 | ||||||||||

Due to non-guarantor subsidiaries | 10,824 | 12,894 | ||||||||||

Other current liabilities | 20,031 | 22,668 | ||||||||||

Current liabilities | 30,855 | 35,562 | ||||||||||

Notes:

| (1) | For the six-month period ended 30 June 2023, revenue, gross profit and profit of the period includes USD 104 million, USD (225) million and USD 1,130 million of intercompany transactions withnon-guarantor subsidiaries and related parties, respectively. |

25

| (2) | For the year ended 31 December 2022, revenue, gross profit and profit of the period includes USD 299 million, USD (439) million and USD 25 million of intercompany transactions with non-guarantor subsidiaries and related parties, respectively. |

2023 OUTLOOK

We expect our revenue to grow from a healthy combination of volume and price.

Net pension interest expenses and accretion expenses are expected to be in the range of USD 200 to 230 million per quarter, depending on currency and interest rate fluctuations. We expect the average gross debt coupon in 2023 to be approximately 4.0%.

We expect net capital expenditure of between USD 4.5 and 5.0 billion in 2023.

26

Index

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 4 | ||||

| 5 | ||||

| 6 |

Unaudited condensed consolidated interim income statement

For the six-month period ended 30 June | ||||||||||

Million US dollar, except earnings per shares in US dollar | No tes | 20 23 | 2022¹ | |||||||

Revenue | 29 333 | 28 027 | ||||||||

Cost of sales | (13 536) | (12 784) | ||||||||

Gross profit | 15 796 | 15 243 | ||||||||

Distribution expenses | (3 183) | (3 076) | ||||||||

Sales and marketing expenses | (3 518) | (3 304) | ||||||||

Administrative expenses | (2 350) | (2 237) | ||||||||

Other operating income/(expenses) | 327 | 478 | ||||||||

Exceptional costs above profit from operations | 7 | (107) | (105) | |||||||

Profit from operations | 6 965 | 7 000 | ||||||||

Finance cost | 8 | (3 608) | (2 962) | |||||||

Finance income | 8 | 385 | 694 | |||||||

Net finance income/(cost) | (3 223) | (2 268) | ||||||||

Share of result of associates | 13 | 105 | 129 | |||||||

Exceptional share of results of associates | 7 / 13 | - | (1 143) | |||||||

Profit before tax | 3 847 | 3 718 | ||||||||

Income tax expense | 9 | (1 192) | (1 244) | |||||||

Profit of the period | 2 655 | 2 474 | ||||||||

Profit of the period attributable to: | ||||||||||

Equity holders of AB InBev | 1 977 | 1 692 | ||||||||

Non-controlling interest | 678 | 782 | ||||||||

Basic earnings per share | 16 | 0.98 | 0.84 | |||||||

Diluted earnings per share | 16 | 0.96 | 0.83 | |||||||

The accompanying notes are an integral part of these consolidated financial statements.

1

As from 1 January 2023, mark-to-market gains/(losses) on derivatives related to the hedging of the share-based payment programs are reported in the exceptional net finance income/(cost). The 2022 presentation was amended to conform to the 2023 presentation.1

Unaudited condensed consolidated interim statement of comprehensive income/(loss)

For the six-month period ended 30 June | ||||||||||

Million US dollar | Notes | 2023 | 2022 | |||||||

Profit of the period | 2 655 | 2 474 | ||||||||

Other comprehensive income/(loss): items that will not be reclassified to profit or loss: | ||||||||||

Re-measurements of post-employment benefits | 16 | 3 | 1 | |||||||

3 | 1 | |||||||||

Other comprehensive income/(loss): items that may be reclassified subsequently to profit or loss: | ||||||||||

Exchange differences on translation of foreign operations | 16 | 3 574 | 2 412 | |||||||

Effective portion of changes in fair value of net investment hedges | (95) | (417) | ||||||||

Cash flow hedges recognized in equity | (497) | 189 | ||||||||

Cash flow hedges reclassified from equity to profit or loss | (103) | (451) | ||||||||

2 879 | 1 733 | |||||||||

Other comprehensive income/(loss), net of tax | 2 882 | 1 734 | ||||||||

Total comprehensive income/(loss) | 5 538 | 4 208 | ||||||||

Attributable to: | ||||||||||

Equity holders of AB InBev | 5 049 | 3 584 | ||||||||

Non-controlling interest | 488 | 624 | ||||||||

The accompanying notes are an integral part of these consolidated financial statements.

2

Unaudited condensed consolidated interim statement of financial position

Million US dollar | Notes | 30 June 2023 | 31 December 2022 | |||||||

ASSETS | ||||||||||

Non-current assets | ||||||||||

Property, plant and equipment | 10 | 27 181 | 26 671 | |||||||

Goodwill | 11 | 116 168 | 113 010 | |||||||

Intangible assets | 12 | 40 973 | 40 209 | |||||||

Investments in associates | 13 | 4 728 | 4 656 | |||||||

Investment securities | 15 | 179 | 175 | |||||||

Deferred tax assets | 2 836 | 2 300 | ||||||||

Employee benefits | 11 | 11 | ||||||||

Income tax receivables | 835 | 883 | ||||||||

Derivatives | 19 | 62 | 60 | |||||||

Trade and other receivables | 14 | 1 895 | 1 782 | |||||||

Total non-current assets | 194 868 | 189 757 | ||||||||

Current assets | ||||||||||

Investment securities | 15 | 85 | 97 | |||||||

Inventories | 6 839 | 6 612 | ||||||||

Income tax receivables | 912 | 813 | ||||||||

Derivatives | 19 | 157 | 331 | |||||||

Trade and other receivables | 14 | 6 609 | 5 330 | |||||||

Cash and cash equivalents | 15 | 6 848 | 9 973 | |||||||

Assets classified as held for sale | 35 | 30 | ||||||||

Total current assets | 21 483 | 23 186 | ||||||||

Total assets | 216 352 | 212 943 | ||||||||

EQUITY AND LIABILITIES | ||||||||||

Equity | ||||||||||

Issued capital | 16 | 1 736 | 1 736 | |||||||

Share premium | 17 620 | 17 620 | ||||||||

Reserves | 18 835 | 15 218 | ||||||||