UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | | | | |

| ☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended September 30, 2024

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _________ to ___________

Commission file number 001-37884

VALVOLINE INC.

| | | | | |

| Kentucky | 30-0939371 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

100 Valvoline Way, Suite 100

Lexington, Kentucky 40509

Telephone Number (859) 357-7777

Securities registered pursuant to Section 12(b) of the Act: | | | | | | | | |

| Title of each class | Trading Symbol | Name of each exchange on which registered |

| Common stock, par value $0.01 per share | VVV | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | ☑ | Accelerated filer | ☐

|

| Non-accelerated filer | ☐

| Smaller reporting company | ☐

|

| | Emerging growth company | ☐

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statement. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrants’ executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

The aggregate market value of voting common stock held by non-affiliates at March 31, 2024 was approximately $5.7 billion. At November 19, 2024, there were 128,373,010 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for its 2025 Annual Meeting of Shareholders (the “Proxy Statement”) are incorporated by reference into Part III of this Annual Report on Form 10-K and will be filed within 120 days of the registrant’s fiscal year end.

TABLE OF CONTENTS

| | | | | | | | | | | |

| | Page |

| PART I | | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 1C. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | | |

| PART II | | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| | | |

| PART III | | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | | |

| PART IV | | |

| Item 15. | | |

| Item 16. | | |

Forward-Looking Statements

Certain statements in this Annual Report on Form 10-K, other than statements of historical fact, are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements may include, without limitation, executing on the growth strategy to create shareholder value by driving the full potential in the Company’s core business, accelerating network growth and innovating to meet the needs of customers and the evolving car parc; realizing the benefits from the sale of Global Products; and future opportunities for the remaining stand-alone retail business; and any other statements regarding Valvoline's future operations, financial or operating results, capital allocation, debt leverage ratio, anticipated business levels, dividend policy, anticipated growth, market opportunities, strategies, competition, and other expectations and targets for future periods. Valvoline has identified some of these forward-looking statements with words such as “anticipates,” “believes,” “expects,” “estimates,” “is likely,” “predicts,” “projects,” “forecasts,” “may,” “will,” “should,” and “intends,” and the negative of these words or other comparable terminology. These forward-looking statements are based on Valvoline’s current expectations, estimates, projections, and assumptions as of the date such statements are made and are subject to risks and uncertainties that may cause results to differ materially from those expressed or implied in the forward-looking statements. Factors that might cause such differences include, but are not limited to, those discussed under the headings “Risk Factors” in Item 1A of Part I of this Annual Report on Form 10-K, “Management’s Discussion and Analysis of Financial Condition and Results of Operation” in Item 7 of Part II of this Annual Report on Form 10-K and “Quantitative and Qualitative Disclosures about Market Risk” in Item 7A of Part II of this Annual Report on Form 10-K. Valvoline assumes no obligation to update or revise these forward-looking statements for any reason, even if new information becomes available in the future, unless required by law.

PART I

ITEM 1. BUSINESS

Overview

Valvoline Inc. is a leader in automotive preventive maintenance delivering convenient and trusted services in its retail stores throughout the United States (“U.S.”) and Canada. The terms “Valvoline,” the “Company,” “we,” “us,” “management,” and “our” as used herein refer to Valvoline Inc., its predecessors and its consolidated subsidiaries, except where the context indicates otherwise.

As the quick, easy, trusted leader in automotive preventive maintenance, Valvoline is creating shareholder value by driving the full potential of its core business, accelerating network growth and innovating to meet the needs of customers and the evolving car parc. With average customer ratings that indicate high levels of service satisfaction, Valvoline and the Company’s franchise partners keep customers moving with approximately 15-minute stay-in-your-car oil changes; battery, bulb and wiper replacements; tire rotations; and other manufacturer recommended maintenance services. The Company operates and franchises more than 2,000 service center locations through its Valvoline Instant Oil ChangeSM (“VIOC”) and Valvoline Great Canadian Oil Change (“GCOC”) retail locations and supports nearly 270 locations through its Express CareTM platform. For over 15 decades, Valvoline has consistently adapted to address changing technologies and customer needs and is well positioned to service evolving vehicle maintenance needs with its growing network of stores.

Company background

Established in 1866, Valvoline has a history of innovation spanning nearly 160 years when Dr. John Ellis founded Valvoline by discovering the lubricating properties of distilled crude oil and formulated the world's first petroleum-based lubricant. Valvoline was trademarked seven years later in 1873, making it the first trademarked motor oil brand in the U.S. Soon thereafter, as vehicle ownership rapidly grew, Valvoline became widely known in the automotive world through racing victories and as a recommended oil for the iconic Ford Model T, while expanding its product offerings and global reach through its innovative automotive maintenance and heavy-duty engine applications.

Valvoline was acquired by Ashland (currently doing business as Ashland Inc., and together with its predecessors and consolidated subsidiaries, referred to herein as “Ashland”), in 1950 and continued accelerating through the development of all-climate and racing motor oils, in addition to supporting notable automobile racing victories by some of the biggest legends of the sport. By the late 1980s, Valvoline began operating and franchising VIOC service center stores, expanding into consumer-focused automotive preventive maintenance and quick lube services. Valvoline maintained its focus on innovating for evolving vehicle technologies and the needs of customers through the late 1990s and early 2000s by introducing synthetic and high-mileage motor oils.

Valvoline was incorporated in May 2016 as a subsidiary of Ashland, followed by the transfer of the Valvoline business and certain other legacy Ashland assets and liabilities from Ashland to Valvoline. Valvoline completed its initial public offering of common stock in September 2016, and Ashland distributed its remaining ownership interest in Valvoline in May 2017 (the “Distribution”). Today, Valvoline operates as an independent corporation that trades on the New York Stock Exchange (“NYSE”) under the symbol “VVV” as a pure play automotive retail services provider focused on delivering quick, easy, and trusted vehicle maintenance services.

Discontinued operations

On March 1, 2023, Valvoline completed the sale of its former Global Products reportable segment (currently doing business as “Valvoline Global Operations” and referred to herein as “Global Products”) to Aramco Overseas Company B.V. (the “Buyer”) (the “Transaction”). The operating results and cash flows associated with and directly attributed to the Global Products disposal group are reflected as discontinued operations. Refer to Note 3 included within the Notes to Consolidated Financial Statements included in Item 8 of Part II of this Annual Report on Form

10-K for additional information regarding the Global Products business, including income from discontinued operations. Unless otherwise noted, disclosures herein relate solely to the Company’s continuing operations.

Valvoline’s retail services

Valvoline operates and franchises more than 2,000 service center locations through its VIOC and GCOC retail locations and supports nearly 270 locations through its Express Care platform. The Company has built a reputation as the quick, easy, trusted name in automotive preventive maintenance through its full-service oil changes from certified technicians in approximately 15-minutes, including a free 18-point maintenance check. Valvoline continues to build its market share by leveraging its stay-in-your-car service model and providing each customer with service that can be seen by experts they can trust. Valvoline technicians utilize the Company’s proprietary SuperProTM system to deliver a superior customer experience and make timely service recommendations based upon visual inspection, vehicle service history, and original equipment manufacturer (“OEM”) recommendations. The SuperPro system is utilized in both company-operated and franchised service center locations, creating a consistent service experience for customers.

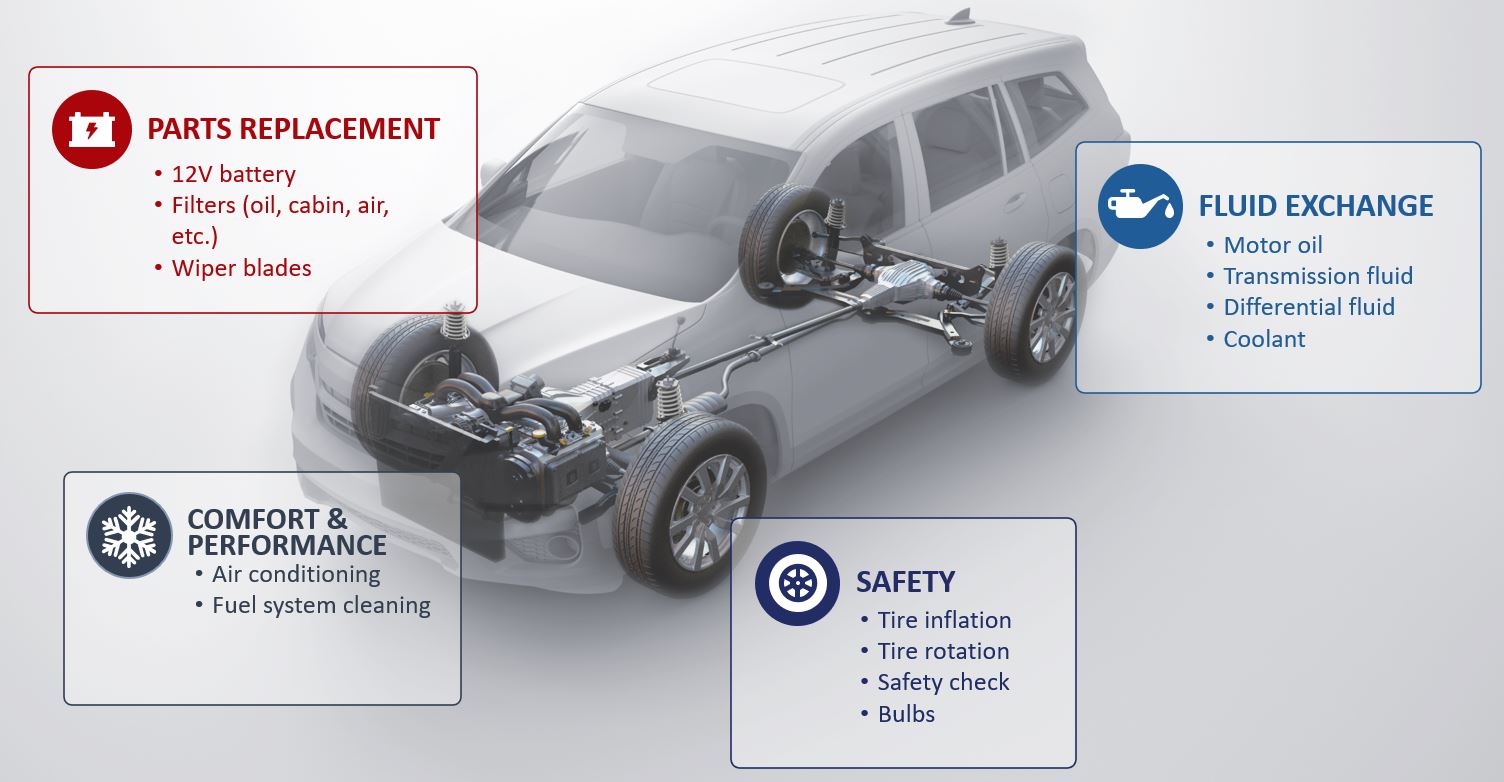

The following summarizes the primary services Valvoline offers at most retail service center stores:

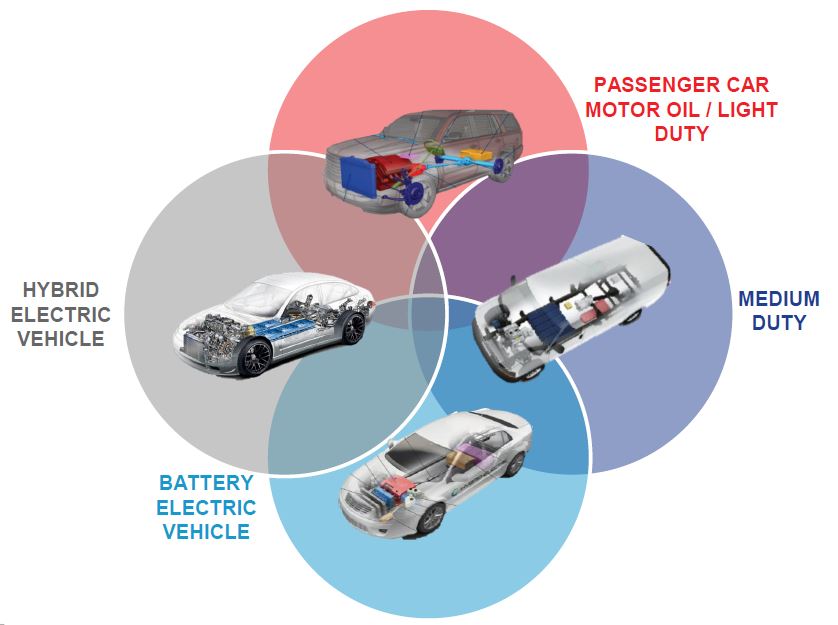

Valvoline’s services are offered to a wide range of vehicle types, including fleets, as shown below:

Industry overview

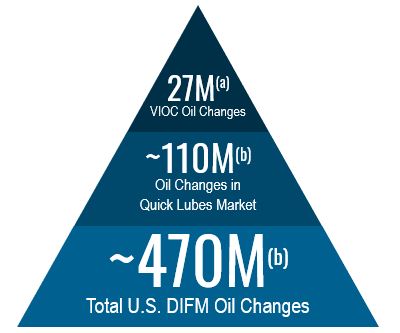

Demand for automotive aftermarket services benefits from the growing number and age of vehicles in operation as well as increasing vehicle complexity and ongoing increases in miles driven. In addition, the resilient North American automotive aftermarket services market is highly fragmented, which creates a significant opportunity for consolidation. Based on industry surveys and management estimates, the U.S. Do It For Me (“DIFM”) total addressable market depicted below demonstrates the magnitude of the opportunity in the U.S. for Valvoline:

| | | | | |

| (a) | VIOC oil changes in fiscal year 2024 (U.S. company-operated and franchised stores) |

| (b) | Management estimates developed utilizing internal and industry data for U.S. passenger car and light truck quick lube and DIFM oil changes |

Business and growth strategies

As a pure play automotive retail services provider and the trusted leader in preventive automotive maintenance, Valvoline is well positioned to create long-term shareholder value through executing the Company’s strategic initiatives, which include:

•Driving the full potential of the core business through increasing market share and improving operational efficiency in existing stores by building on Valvoline’s strong foundation in marketing, technology, and data insights.

•Aggressively growing the retail footprint with company-operated store growth and an increased emphasis on franchisee store growth; and

•Targeting customer and service expansion with a focus on fleet business, driving non-oil change service penetration, and meeting the needs of an evolving car parc.

Retail store development

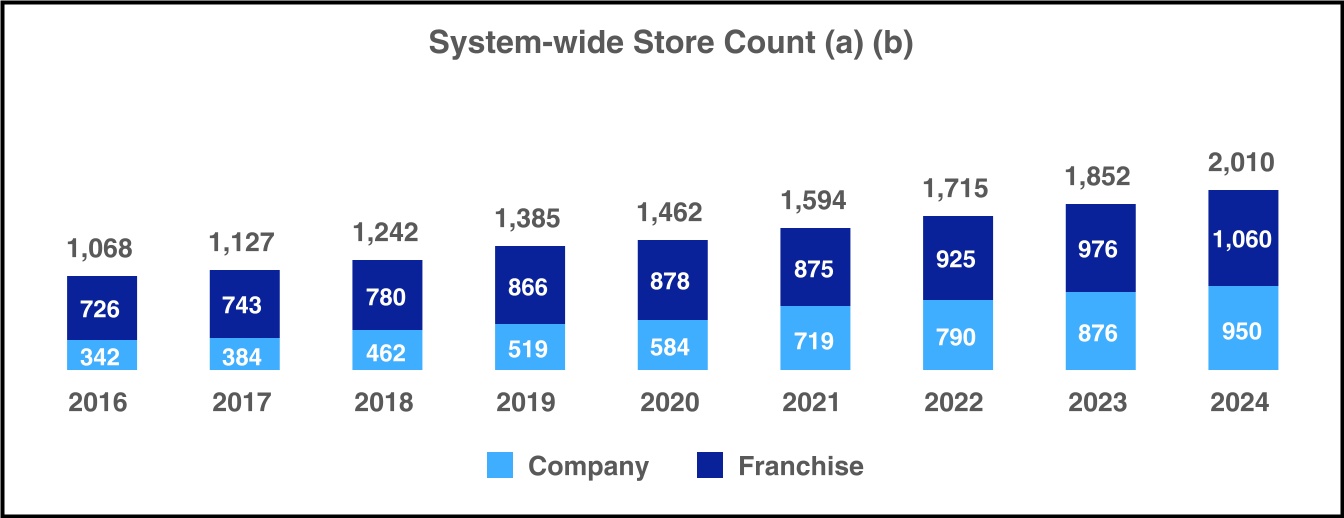

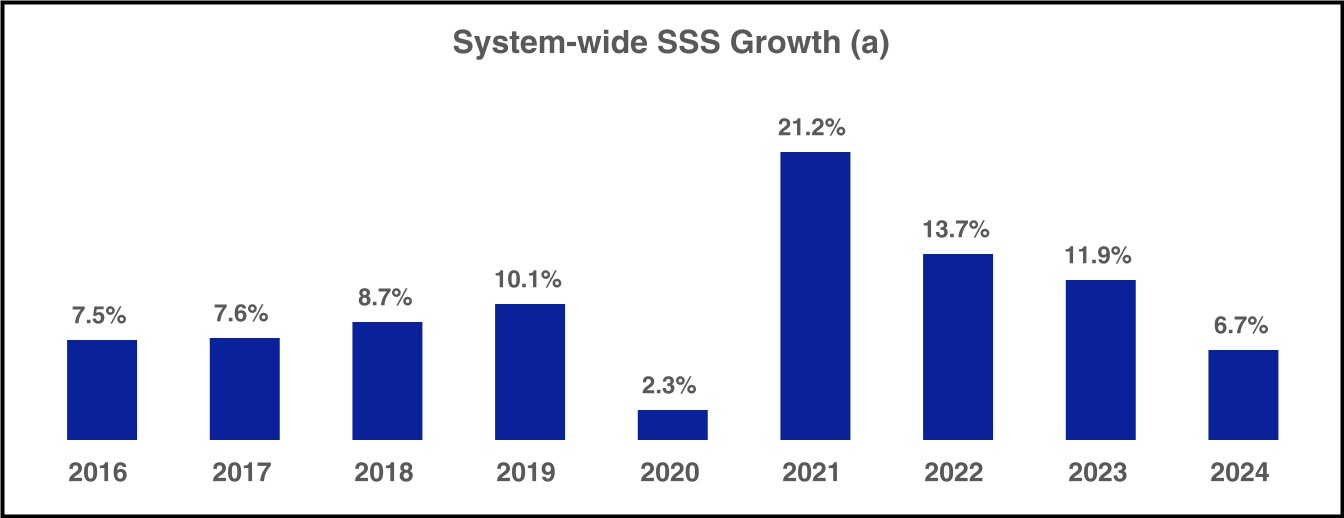

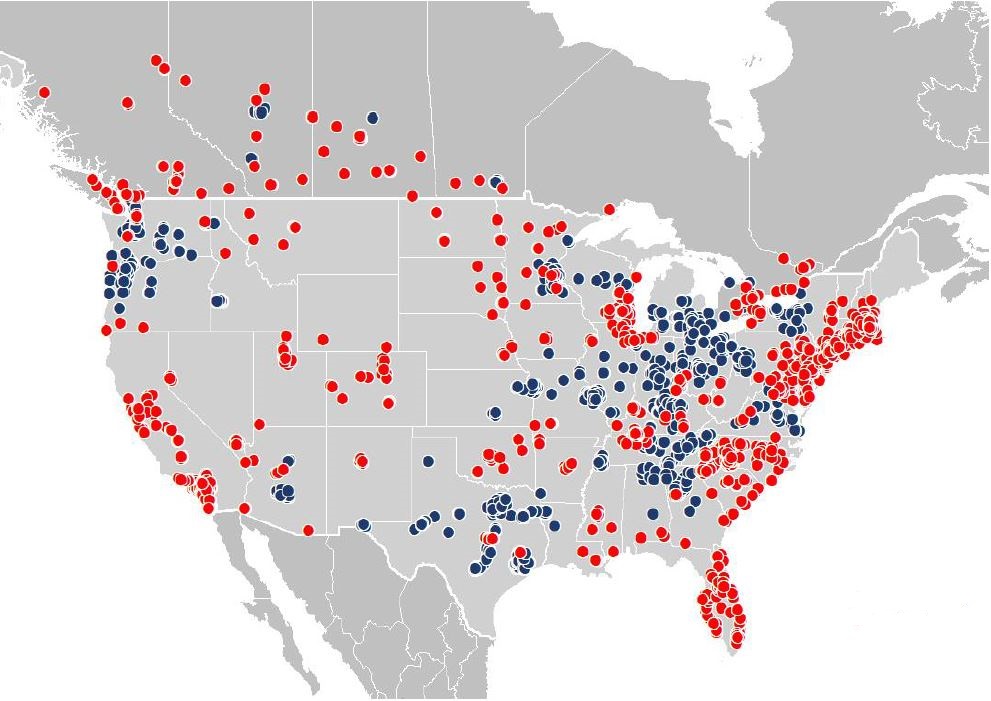

Valvoline’s network of retail service centers delivered its 18th consecutive year of system-wide same-store sales (“SSS”) growth in fiscal 2024, demonstrating the system's operational excellence. As shown below, Valvoline operates, either directly or through its franchisees, 2,010 service center stores across the U.S. and Canada as of September 30, 2024:

| | | | | |

| l | Company-operated |

| l | Franchised |

Valvoline utilizes a three-pronged approach to grow its retail network through 1) franchisee store expansion 2) opportunistic acquisitions, and 3) new store development. This approach drove system-wide store growth of over 45% over the last five years. During this period, Valvoline added 625 net new stores to the system and expanded its service centers internationally into Canada. The retail services store network and its same-store sales growth is summarized below:

| | | | | |

| (a) | Refer to "Key Business Measures" in Item 7 of Part II of this Annual Report on Form 10-K for a description of management's use and determination of key metrics, including store counts and SSS. Measures include franchisees, which are distinct independent legal entities and Valvoline does not consolidate the results of operations of its franchisees. |

| (b) | As of September 30, 2020, one franchised service center store included in the store count was temporarily closed at the discretion of the respective independent operator due to the impacts of COVID-19. |

Competition

Valvoline faces competition across its service offerings based on several key criteria, including brand recognition, product selection, quality of service, price, convenience, speed, location, and customer experience, in addition to the ability to deliver innovative services to meet evolving customer needs. Valvoline competes for customers in the highly fragmented automotive aftermarket service industry with automotive dealerships, automotive repair and maintenance centers, as well as other regional and independent quick lube operators.

Additionally, Valvoline’s retail stores compete for consumers and franchisees with other major franchised brands that offer a turn-key operations management system, such as Jiffy Lube, Grease Monkey, Take 5 Oil Change, Express Oil Change, and Mr. Lube in Canada. Valvoline competes with other franchisors in automotive services and across other industries on the basis of the expected return on investment and the value propositions offered to franchisees.

Valvoline also competes for Express Care operators and customers with national branded companies that offer an independent quick lube platform with a professional signage program and limited business model support.

Marketing and customer experience

Valvoline places a high priority on delivering an in-store customer experience that is quick, easy, and trusted. To both acquire and retain customers, marketing plays an important role in demonstrating the distinct experience that Valvoline offers customers, as well as providing information on locations, promotions, services offered, and wait times.

Techniques utilized by the Company are intended to build awareness of and create demand for its automotive preventive maintenance services. Valvoline markets through search and direct response channels, invests in advertising through social and digital media, and leverages targeted sponsorships to reach specific audiences. The Company’s modeled marketing strategies are efficient and yield strong rates of return.

Valvoline leverages its digital tools to obtain customer feedback across the retail network of stores. Customer feedback is frequently measured and monitored to ensure that any service issues are quickly addressed to maintain high levels of customer satisfaction. Valvoline also utilizes its digital infrastructure and technology to more efficiently interact with customers, driving customer engagement, acquisition and retention, and consistency. The Company's strengths in digital marketing and data analytics are leveraged to attract new and retain existing customers, including tailored marketing campaigns directed to specific customers when they are in the market for their next service.

Intellectual property

Valvoline holds approximately 390 trademarks in more than 70 countries across the world, including the Valvoline and “V” brand logo trademarks. These trademarks have a perpetual life, are generally subject to renewal every ten years, and are among Valvoline's most protected and valuable assets. With the completion of the sale of Global Products, Valvoline owns the Valvoline brand for all global retail services, excluding China and certain countries in the Middle East and North Africa, while Global Products owns the Valvoline brand for all product uses globally. Valvoline partners with Global Products to ensure that Valvoline's iconic brand is managed in a consistent and holistic manner.

Valvoline trade names and service marks used in its business include ValvolineTM and Valvoline Instant Oil ChangeSM, among others. Valvoline is also party to arrangements that license its intellectual property to others in return for revenues. Valvoline owns approximately 700 domain names that are used to promote Valvoline services and provide information about the Company.

Product supply and price

The products used in Valvoline’s retail service delivery are principally sourced from Global Products. In connection with the sale of Global Products, Valvoline entered into a long-term supply agreement for the purchase of substantially all lubricant and certain ancillary products for its stores from Global Products (the “Supply Agreement”).

Valvoline is able to leverage its scale, as well as the scale of its suppliers, for favorable terms in the arrangement of product supply for its store operations across the network. This benefit enhances the value proposition to new and existing independent store operators as well as to the profits of Valvoline’s company store operations. Valvoline’s arrangement of product supply for its independent operators provides recurring fees and margins that benefit ongoing results. As Valvoline continues to grow organically and through acquisitions, the business is well-positioned to continue driving increased benefits to the overall system of retail stores.

Valvoline works diligently to preserve margins by adjusting its pricing in response to changes in costs. The Company’s customer value proposition focuses on convenience and quality service which provides the ability to leverage pricing power to raise prices while maintaining customer loyalty. Pricing adjustments to products sold to Valvoline's independent operators are made pursuant to their contracts and are generally based on movements in published base oil indices.

Seasonality

Valvoline’s business is moderately impacted by seasonality. Transaction volumes follow driving patterns of consumers, which generally trend with the length of daylight hours, North American holidays, and vacation timing. As a result, the second half of the fiscal year ordinarily is more robust as miles driven tends to be higher. Weather conditions can modestly affect transaction volumes, and geographic variation typically limits weather impacts to specific regions.

Regulatory and environmental matters

Valvoline operates to maintain compliance with various federal, state, local and non-U.S. laws and governmental regulations relating to the operation of its business, including those regarding employment and labor practices; workplace safety; building and zoning requirements; the handling, storage and disposal of hazardous substances contained in the products used in service, including used motor oil and lead-acid batteries; and the ownership, construction and operation of real property, among others. Valvoline maintains policies and procedures to control risks and monitor compliance with applicable laws and regulations. These laws and regulations require Valvoline to obtain and comply with permits, registrations or other authorizations issued by governmental authorities. These authorities can modify or revoke the Company’s permits, registrations or other authorizations and can enforce compliance through fines, sanctions and injunctions. The Company is also subject to regulation by various U.S. federal regulatory agencies and by the applicable regulatory authorities in locations in which Valvoline’s services are offered. Such regulations principally relate to the operation of its service centers, advertising and marketing of Valvoline’s services.

Valvoline inventories lubricating and vehicle maintenance products and handles used automotive oils and filters. Accordingly, Valvoline is subject to numerous federal, state, local and non-U.S. environmental laws including the Comprehensive Environmental Response Compensation and Liability Act. In addition, the U.S. Environmental Protection Agency under the Resource Conservation and Recovery Act, as well as various state and local environmental protection agencies, regulate the handling and disposal of certain waste products and other materials.

As a franchisor, Valvoline is subject to various federal, state, and non-U.S. franchising laws. The Federal Trade Commission (the “FTC”) regulates franchising activities in the U.S. and requires franchisors to make extensive disclosure to prospective franchisees before the execution of a franchise agreement. Certain jurisdictions require registration or specific disclosure in connection with franchise offers and sales, or have laws that limit franchisor rights regarding the termination, renewal or transfer of franchise agreements.

Valvoline is subject to various federal, state, local and non-U.S. laws and regulations relating to information security, privacy, cashless payments and customer credit, protection and fraud. An increasing number of governments and industry groups have established data privacy laws and standards for the protection of personal information, including financial information (e.g., credit card numbers), social security numbers, and health information. The Company is also subject to labor and employment laws, including regulations established by the U.S. Department of Labor and other local regulatory agencies, governing working conditions, paid leave, workplace safety, wage and hour standards, and hiring and employment practices.

Human capital management

"It all starts with our people" is one of Valvoline's core values, and the Company endeavors to create an environment that promotes safety, fosters diversity, encourages creativity, rewards performance, and emphasizes culture and purpose. To recruit and retain the most qualified team members, Valvoline focuses on treating team members well by paying competitive wages, offering an attractive benefit package, and providing robust training and career development opportunities. Valvoline is committed to actively creating an environment where each team member is empowered to learn, grow, and maximize their personal contribution.

Workforce

As of September 30, 2024, Valvoline had approximately 11,500 employees (excluding contract employees) in the U.S. and Canada, including approximately 10,500 full-time employees. Valvoline operates 950 company-owned

retail service center stores throughout the U.S. and Canada and supports its network of more than 2,000 stores through centralized teams.

The table below provides the Company's approximate distribution of employees, which includes its company-operated service center stores, central supporting teams, and excludes independent contractors:

| | | | | |

| Number of employees |

| |

| |

| |

| Company-operated store employees | 10,300 | |

| |

| |

| |

| Central supporting team members | 1,200 | |

| Total employee headcount | 11,500 | |

Valvoline seeks to attract, develop, and retain highly qualified talent as summarized further below.

Talent acquisition

Valvoline strives to foster a workplace culture that attracts and retains top, diverse talent at every level. Valvoline's talent acquisition is based on qualifications and experiences of target employees, including "building block" traits and capabilities that support strong development early in an employee's career with the Company. Valvoline continues to benefit from substantial investment in talent acquisition to ensure the Company has the right skill set to attract and recruit exceptional diverse talent along with supporting technology to increase efficiency in staffing stores. Valvoline utilizes innovative technology and structured processes intended to attract qualified candidates, including engaging job descriptions designed to reach a larger audience, a quick and mobile-friendly application process, online chat features to proactively address applicant questions, and video storytelling that offers a view of Valvoline's culture through the lens of its own employees. These tools have been created to convey what makes Valvoline unique as an employer to better attract diverse and ideal candidates, and these strong branding and sourcing efforts allow Valvoline to select among the very best.

The Company’s focus on aggressive growth, including the addition of 158 net new system-wide stores in fiscal 2024, creates a critical need for talent to operate those stores. Valvoline utilizes its tools and processes to attract qualified candidates, including providing support to franchise sourcing efforts. Franchisees collaborate through periodic sharing of hiring experiences and best practices to ensure company-operated and franchised locations attract and hire the best candidates to deliver consistent and superior service to Valvoline’s customers.

Training and development

The opportunity to develop and advance, regardless of job role or location, is critical to the success of Valvoline. A key component of the Company’s talent development approach is to provide each team member with the necessary tools and training opportunities to develop within their area of subject matter knowledge. Training is tailored to specific job roles and functions incorporating both on-the-job training as well as virtual or in-person classes and e-learning. Valvoline provides new VIOC and GCOC employees 270 hours of training that is generally completed within the first 60 days of employment leading to their first certification and another 240 hours of training in the next 140 days that supports promotability.

Valvoline provides an Introduction to Management program within its VIOC and GCOC stores where assistant managers interact with leadership team members and peers from other stores to learn about Valvoline's culture, share best practices, and receive management training to prepare them for career advancement. The combination of these efforts enable Valvoline to continue a promote-from-within strategy which has led to a majority of service center managers, area managers, and market manager promotions in the last year being earned by team members who started in hourly positions at VIOC. By engaging team members early, Valvoline provides them with the necessary tools to learn and acquire new skills which increases their value as an employee and, most importantly, affords them the opportunity to advance their careers.

VIOC has been presented with Training magazine’s Training APEX Award 11 times, which ranks companies that are unsurpassed in harnessing human capital and reflects the winners’ journey to attain peak performance in employee training and development and organizational success. Additionally, the Company is an eleven-time recipient of the BEST Award from The Association for Talent Development, that recognizes organizations that are

building talent, enterprise-wide and strategically driving a talent development culture that delivers results. As an eleven-time winner of this award, the Company was also named to the association’s Best of the BEST list.

Employee communication and feedback

In an ongoing effort to understand employees’ needs and deliver on the Company’s values of trust, accountability and collaboration, Valvoline remains focused on transparency and employee feedback. The Company regularly hosts company-wide town halls in which Valvoline’s Chief Executive Officer and other members of senior management inform employees about performance, strategic initiatives, activities, and policies along with providing opportunities for them to ask questions. In addition, Valvoline management is focused on listening to understand what is on the minds of employees by regularly surveying team members to gather real-time feedback as well as identifying opportunities for continuous improvement. Valvoline believes employee survey results are important to evaluate areas for improved communication and are meaningful to recruit and retain top talent, believing satisfied employees are more likely to have a positive impact in the workplace and deliver great customer service.

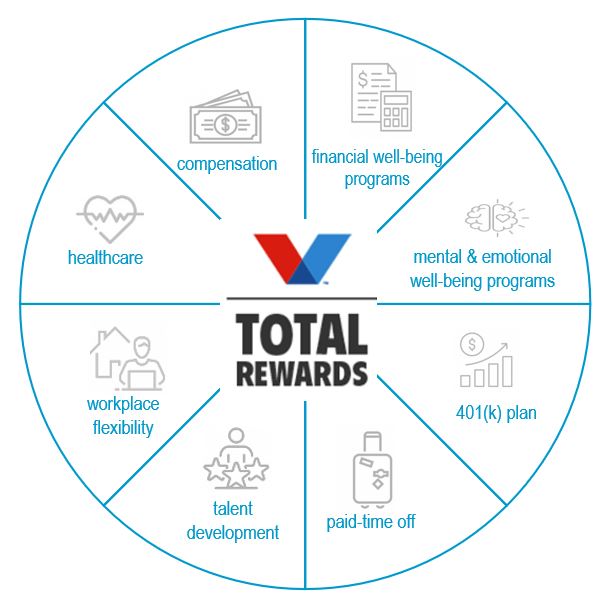

Total rewards

Valvoline’s total rewards philosophy is to help attract, motivate, develop and retain a qualified and diverse workforce. The Company offers competitive, comprehensive compensation and benefits programs designed to care for the physical, mental, emotional, social and financial well-being of its employees. The Company’s objective is to base compensation on employee position, experience, location, performance, and the labor market in order to not be influenced by factors such as gender, race, or ethnicity. Additionally, the Compensation Committee of the Board of Directors (the “Board”) and senior management are actively involved in determining the Company’s total rewards strategy to help Valvoline provide a positive employee experience.

The Company provides a wide variety of benefits to eligible full-time and part-time employees. Valvoline’s strategy is to provide competitive benefit programs which align to the competitive business environment and meet the needs of employees through all stages of life. These include:

•Affordable healthcare plans (medical, prescription, dental, vision, maternity, fertility, adoption and telehealth)

•Life, disability, and accident insurance coverage

•Health savings account (HSA) with company contributions

•401(k) retirement savings plan with generous company basic and matching contributions

•Personalized employee well-being programs to support taking care of the whole employee and family

•Tuition reimbursement

•Paid time off, plus holiday pay, paid disability, paid maternity and family leave, and other leave programs.

Health and safety

The Company designs, builds and operates its facilities to promote and protect the health and safety of its employees, known as its "Vamily." Valvoline strives to create a safe and secure environment for every employee and customer and fosters a sense of belonging to promote emotional well-being that enables employees to deliver “V-Class” service to customers. To help reduce the number of incidents at the Company, Valvoline employs safety-specific education as part of its training programs for all employees. Employees begin this training on day one to instill safety precautions and best practices. As part of the broader training curriculum, team members are required to successfully complete execution reports confirming a strong understanding of Valvoline safety measures.

Diversity, equity and inclusion (“DEI”)

Valvoline is committed to creating an inclusive and welcoming environment for its employees and customers by fostering a strong sense of belonging, where diverse backgrounds are represented, engaged and empowered to inspire innovative ideas and decisions. Valvoline’s goal is for the Company’s workforce to represent the diverse communities served.

The Company is committed to the inclusion of federally-insured minority depository institutions (“MDIs”) alongside larger banks and financial institutions as part of its overall cash management strategy and has $2.6 million of its cash equivalents as of September 30, 2024 with MDIs.

The Company also supports employee-led networking groups (Employee Resource Groups or “ERGs”), which are open to all employees. These ERGs provide a forum to communicate and exchange ideas, build a network of relationships across the Company and pursue personal and professional development. The Company also actively sponsors events that promote diversity and inclusion across the business and its operations.

Citizenship

Valvoline’s citizenship efforts support social and educational needs within the communities the Company serves. Throughout the year, Valvoline supports its employees in volunteering their time and talents to give back to their communities. Valvoline employees support the United Way, Red Cross, Children’s Miracle Network, Habitat for Humanity, Big Brothers Big Sisters, and many more national and local organizations.

Valvoline's Charitable Giving Program encourages its team members to support the communities in which they live and in which the Company operates, through hands-on service, focused generosity and the continuous pursuit of innovative and sustainable solutions. A major focus of Valvoline’s charitable giving programs is the annual employee giving campaign where employees are encouraged to donate to the charity of their choice. Valvoline’s matching program will match the donations given to the organizations that align with at least one of the Company’s fiscal 2024 giving pillars: (1) disadvantaged families and children, (2) education, (3) environment, (4) health care, and/or (5) diversity, equity and inclusion.

Additionally, Valvoline employees support a program that assists Company employees during times of personal hardship by providing short-term financial assistance to eligible service center and corporate employees in immediate financial need because of an accident, illness, injury, death, natural disaster, or other catastrophic event or emergency.

Available information

More information about Valvoline is available on the Company’s website at http://investors.valvoline.com. On this website, Valvoline makes available, free of charge, its Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports, as well as any beneficial ownership

reports of officers and directors filed on Forms 3, 4 and 5. All such reports are available as soon as reasonably practicable after they are electronically filed with, or electronically furnished to, the U.S. Securities and Exchange Commission (the “SEC"). Valvoline also makes available, free of charge on its website, its Amended and Restated Articles of Incorporation, By-Laws, Corporate Governance Guidelines, Board Committee Charters, Director Independence Standards, and Code of Conduct that apply to Valvoline’s directors, officers and employees. These documents are also available in print to any shareholder who requests them. The information contained on Valvoline’s website is not part of this Annual Report on Form 10-K and is not incorporated by reference in this document. References to website addresses are provided as inactive textual references only. The SEC also maintains a website (http://www.sec.gov) that contains reports, proxy and other information and statements regarding issuers, including Valvoline, that file electronically with the SEC.

Executive officers of Valvoline

The following table sets forth information concerning Valvoline's executive officers as of November 19, 2024:

| | | | | | | | |

| Name | Age | Title |

| Lori A. Flees | 54 | President and Chief Executive Officer and Director |

| Mary E. Meixelsperger | 64 | Chief Financial Officer |

| Julie M. O’Daniel | 57 | Senior Vice President, Chief Legal Officer and Corporate Secretary |

| Jonathan L. Caldwell | 47 | Senior Vice President and Chief People Officer |

| R. Travis Dobbins | 52 | Senior Vice President and Chief Technology Officer |

| Linwood R. Fulcher | 53 | Senior Vice President and Chief Operating Officer |

| Dione R. Sturgeon | 47 | Vice President, Chief Accounting Officer and Controller |

Lori A. Flees has served as a director and President and Chief Executive Officer of Valvoline since October 2023. Ms. Flees served as President, Retail Services of Valvoline from April 2022 to September 2023. Prior to joining Valvoline, Ms. Flees held various leadership positions at Walmart Inc., serving as Senior Vice President and Chief Operating Officer of Health & Wellness from August 2020 to March 2022; Senior Vice President and General Merchandising Manager, Sam’s Club Health & Wellness from June 2018 to August 2020; and Senior Vice President, Next Generation Retail and Principal Store No.8 from September 2017 to June 2019.

Mary E. Meixelsperger has served as Valvoline's Chief Financial Officer since June 2016. Prior to joining Valvoline, Ms. Meixelsperger was Senior Vice President and Chief Financial Officer of DSW Inc. from April 2014 to June 2016. In October 2024, Ms. Meixelsperger announced her plans to retire. Ms. Meixelsperger will continue as Chief Financial Officer until a successor is hired and will remain with the Company through a subsequent transition period.

Julie M. O’Daniel has served as Valvoline’s Senior Vice President, Chief Legal Officer and Corporate Secretary since January 2017. Ms. O’Daniel served as General Counsel and Corporate Secretary of Valvoline from September 2016 to January 2017 and as Lead Commercial Counsel of Valvoline from April 2014 to September 2016.

Jonathan L. Caldwell has served as Valvoline's Senior Vice President and Chief People Officer since April 2020. Mr. Caldwell served as Senior Director, Human Resources of Valvoline from March 2018 to April 2020 and as Senior Director, Global Talent Management of Valvoline from October 2016 to March 2018.

R. Travis Dobbins has served as Valvoline's Senior Vice President and Chief Technology Officer since March 2023. Mr. Dobbins served as Vice President of Information Technology of Valvoline from January 2019 to February 2023 and as Information Technology Director, Commercial Solutions from September 2016 to January 2019.

Linwood R. Fulcher has served as Valvoline's Senior Vice President and Chief Operating Officer since October 2023. Mr. Fulcher served as Vice President, Central Operations and Customer Experience Optimization from August 2022 to September 2023. Prior to joining Valvoline, Mr. Fulcher held various leadership positions at Walmart Inc., serving as Vice President Customer Strategy, Science and Journeys from October 2019 to August 2021; and Vice President Returns from February 2017 to October 2019.

Dione R. Sturgeon has served as Valvoline's Vice President, Chief Accounting Officer and Controller since March 2023. Ms. Sturgeon served as Vice President, Corporate Controller from March 2022 to February 2023; as Senior Director, Global Accounting, Reporting & Controls from October 2020 to March 2022; and as Director, Corporate Accounting of Valvoline from August 2016 to October 2020.

ITEM 1A. RISK FACTORS

The following risks could materially and adversely affect Valvoline’s business, operations, financial position or future financial performance. This information should be considered when reviewing this Annual Report on Form 10-K, including Management’s Discussion and Analysis of Financial Condition and Results of Operations, in addition to the consolidated financial statements and related notes thereto. These risk factors could cause future results to differ from those in forward-looking statements and from historical trends. These risks are not the only risks that Valvoline faces. Additional risks and uncertainties that are not presently known, or that Valvoline currently believes are not material, may also become meaningful and adversely affect Valvoline’s business.

Risks related to the industries in which Valvoline operates

Valvoline faces significant competition from other companies, which places downward pressure on prices and margins and may adversely affect Valvoline’s business and results of operations.

Valvoline operates in a highly competitive market, competing against a wide variety of companies across the automotive services industry. Competition is based on several key criteria, including brand recognition, quality, price, customer service, and the ability to bring innovative services to the marketplace. Competitors include international, national, regional and local automotive repair and maintenance shops, automobile dealerships, and oil change shops. Certain competitors are larger than Valvoline and have greater financial resources and more diversified portfolios, leading to greater operating and financial flexibility. As a result, these competitors may be better able to withstand adverse changes in conditions within the industry, market dynamics, the price of supplies or general economic conditions. In addition, competitors’ pricing decisions could compel Valvoline to decrease its prices, which could negatively affect Valvoline’s margins and profitability.

Rising and volatile supply costs and supply chain constraints or disruptions could adversely affect Valvoline’s results of operations.

Valvoline’s service center locations require large quantities of automotive products and supplies. The Company’s success depends in part on the ability to anticipate and react to changes in supply costs, and the Company is susceptible to increases in primary and secondary supply costs as a result of factors beyond its control. These factors include general economic conditions, including recessions, significant variations in supply and demand, potential increases in taxes and tariffs, pandemics, armed conflicts, war, weather conditions, currency fluctuations where Valvoline operates, commodity market speculation, labor strikes, including rail strikes, and government regulations. For example, Valvoline’s supplier for air filters experienced supply constraints in fiscal 2024 leading to delivery delays to Valvoline until the supplier was able to diversify its supply chain, which impacted non-oil change revenue in the first half of fiscal 2024. Additionally, the International Longshoreman’s Association (“ILA”) union of maritime workers contract expired on September 30, 2024 without a renewed contract negotiated until early October 2024, resulting in a brief labor strike. A more lengthy strike from the ILA could have had a negative impact on Valvoline’s suppliers resulting in an unfavorable impact to product availability and cost and negatively impacted the Company’s consolidated results of operations. Higher product and supply costs could reduce the Company’s profits, which in turn may adversely affect the business and results of operations for both company-operated and franchised stores.

Additionally, should conditions such as supply chain congestion or availability related to severe weather or climate conditions become severe or last for an extended period of time, Valvoline's inventory of supplies may not be sufficient to meet customer demands. Government regulations related to the manufacture or transport of products provided by the supplier may also impede Valvoline’s ability to obtain those supplies on commercially reasonable terms. If Valvoline is unable to obtain and retain product supply under commercially acceptable terms, its ability to deliver services in a competitive and profitable manner or grow its business successfully could be adversely affected.

Demand for Valvoline’s services could be adversely affected by spending trends, declining economic conditions, industry trends and a number of other factors, all of which are beyond its control.

Demand for Valvoline’s services may be affected by a number of factors it cannot control, including the number and age of vehicles in current service, regulation and legislation, technological advances in the automotive industry and changes in engine technology, including the adoption rate of electric or other alternative engine technologies, changing automotive OEM specifications and longer recommended intervals between services. In addition, during periods of declining economic conditions, including recessions, customers may defer vehicle maintenance. Similarly, increases in energy prices or other factors may cause miles driven to decline, resulting in less vehicle wear and tear and reducing demand for maintenance, which may lead to customers deferring or foregoing Valvoline’s services. All of these factors, which impact metrics such as drain intervals and vehicles served per day, could result in a decline in the demand for Valvoline’s services and adversely affect its sales, cash flows and overall financial condition.

Failure to develop and market new services and technologies could impact Valvoline’s competitive position and have an adverse effect on its business and results of operations.

Valvoline’s efforts to respond to changes in customer demand in a timely and cost-efficient manner to drive growth could be adversely affected by difficulties or delays in service innovation, including the inability to identify or gain market acceptance of new service techniques. Due to the rigorous development process and intense competition, there can be no assurance that any of the services Valvoline is currently developing, or could develop in the future, will achieve substantial commercial success. Moreover, Valvoline may experience operating losses for new services after they are introduced and commercialized because of start-up costs or lack of demand.

The automotive maintenance service industry is subject to periodic technological change and ongoing product improvements. The adoption of electric vehicles is increasing, which reduces demand for lubricant services, but expands the opportunity for other services required by electric vehicles, including coolants, fluids and greases. If Valvoline is unable to develop and market services for electric vehicles, its business and results of operations could be adversely impacted. As automotive technologies evolve, Valvoline could be required to comply with any new or stricter laws or regulations, which could require additional expenditures by Valvoline that could adversely impact business results.

Damage to Valvoline’s brand and reputation could have an adverse effect on its business.

Maintaining Valvoline’s strong reputation with customers is a key component of its business. Liability claims, false advertising claims, service complaints, and governmental investigations could result in substantial and unexpected expenditures and affect consumer or customer confidence in Valvoline's services, which may materially and adversely affect its business operations, decrease sales and increase costs. Additionally, as customers are shifting to more environmentally-conscious electric and hybrid vehicles, the inability of Valvoline to continue its development of new services to adapt to those changing demands could affect the Company's reputation as an environmentally friendly choice for vehicle care and could reduce demand for its services. Further, legislators, customers, investors and other stakeholders are increasingly focusing on environmental, social and governance policies of companies. This focus could result in new or increased legislation or disclosure requirements. In the event that such requirements result in increased costs or a negative perception of the Company, there could be an adverse effect on the business or its results of operations.

If allegations are made that Valvoline’s automotive maintenance services were not provided in a manner consistent with its vision and values, the public may develop a negative perception of Valvoline, its brands, image and reputation. In addition, if Valvoline’s franchise or Express Care operators experience service failures or do not successfully operate their service centers in a manner consistent with Valvoline’s standards, its brand, image and reputation could be harmed, which in turn could negatively impact its business and operating results. A negative public perception of Valvoline’s brands, whether justified or not, could impair its reputation, involve it in litigation, damage its brand equity and have a material adverse effect on its business. In addition, damage to the reputation of Valvoline’s competitors or others in the automotive maintenance services industry could negatively impact Valvoline’s reputation and business.

In connection with the sale of Global Products, the parties entered into a brand agreement (the “Brand Agreement”). Pursuant to the Brand Agreement, Valvoline retains ownership of the Valvoline brand for generally all retail services purposes, and Global Products owns the brand for all product uses. The brand sharing arrangement may increase the risk of inconsistency in its use, messaging, or overall damage to the brand, which could have an adverse impact on Valvoline’s reputation and business and result in lengthy and expensive litigation or settlements.

Risks related to executing Valvoline’s strategy

Valvoline has set aggressive growth goals for its business, including increasing sales, cash flow, market share, margins and number of service center stores, to achieve its long-term strategic objectives. Execution of Valvoline’s growth strategies and business plans to facilitate that growth involves a number of risks.

Valvoline has set aggressive growth goals for its business to meet its long-term strategic objectives and improve shareholder value by aggressively growing through new store development, opportunistic acquisitions and increased emphasis on franchise development. Valvoline’s failure to meet one or more of these goals or objectives could negatively impact its business. Aspects of that risk include, among others, changes to the global economy, availability of or failure to identify acquisition targets or real estate for new stores to grow the Company’s network of retail service center stores, real estate and construction costs or delays limiting new store growth, changes to the competitive landscape, including those related to automotive maintenance recommendations and customer preferences, entry of new competitors, attraction and retention of skilled employees, failure to successfully develop and implement digital platforms to support the Company’s growth initiatives, failure to comply with existing or new regulatory requirements, failure to maintain a competitive cost structure and other risks outlined in greater detail in this “Risk Factors” section.

Another component of the Company’s network growth strategy is dependent on the success of recent refranchising activities taken during fiscal 2024 and planned for early fiscal 2025. Failure to achieve the expected benefits of the refranchising transactions could negatively impact the Company’s operating results and its overall long-term strategic growth objectives, including accelerating franchise store growth. In addition, if the Company’s franchise partners are unsuccessful in continuing productivity and growth objectives within their respective markets, the Company’s business results could be adversely affected. Valvoline has also guaranteed future lease commitments related to certain refranchised stores and the Company’s operating results could be negatively impacted by any increased rent obligations to the extent the franchisees default on such lease agreements.

Valvoline's performance is also highly dependent on attracting and retaining appropriately qualified employees in its service center stores and supporting and corporate teams. A tight labor market in recent years has led to challenges in staffing service center stores due to labor shortages as a number of trends conflate reflecting changing demographics, governmental policies, employee sentiment, and technological change. In response, Valvoline made labor investments and enhanced its recruiting programs to attract new employees. As trends in the labor market evolve, the Company may experience future challenges in recruiting and retaining talent in various locations. Valvoline operates in a competitive labor market, and failure to recruit or retain qualified employees in the future, or the Company's inability to implement corresponding adjustments to its labor model, including compensation and benefit packages, could impair the Company's ability to grow and meet its strategic goals.

Valvoline may be unable to execute its growth strategy, and acquisitions, investments and strategic partnerships could result in operating difficulties, dilution and other harmful consequences that may adversely impact Valvoline’s business and results of operations.

Acquisitions are an important element of Valvoline’s overall growth strategy. Valvoline has completed a significant number of acquisitions in recent years and has developed a pipeline of future viable targets expected to complement the Company’s growth initiatives. An insufficient quantity of strategic acquisition targets in the marketplace with limited targets remaining, or the inability of Valvoline to successfully acquire those targets, may have a negative impact on Valvoline's ability to achieve its future growth projections. Valvoline expects to continue to evaluate and enter into discussions regarding a wide array of potential strategic transactions and to continue to grow organically and through acquisitions. An inability to execute these plans could have an adverse impact on Valvoline’s financial condition and results of operations. In addition, the anticipated benefits of Valvoline’s acquisitions may not be realized and the process of integrating an acquired company, business, or product may create unforeseen operating difficulties or expenditures.

Valvoline’s acquisitions, investments and strategic partnerships could also result in dilutive issuances of its equity securities, the incurrence of debt, contingent liabilities or amortization expenses, impairment of goodwill or purchased long-lived assets and restructuring charges, any of which could harm its financial condition, results of operations and cash flows.

The business model for Valvoline is affected by the financial results of its franchisees.

Valvoline’s business is made up of a network of both company-operated and franchised stores. Valvoline’s success relies in part on the operational and financial success, as well as the cooperation of, its franchisees to implement the Company’s growth strategy, which may be dependent upon their ability to secure adequate financing to meet store development requirements. However, Valvoline has limited influence over its franchisees’ operations and the quality of franchised store operations may be diminished by a number of factors beyond the Company’s control. Valvoline’s franchisees manage their businesses independently and are responsible for the day-to-day operations of 53% of the Company’s system-wide service center stores as of September 30, 2024. Valvoline’s royalty, product, and other revenues from franchised stores are largely dependent on franchisee sales and compliance with franchise agreements. Valvoline’s revenues and margins could be negatively affected should franchisees experience limited or no sales growth, or if the franchisee fails to renew its franchise agreements or otherwise fulfill its obligations under negotiated business development, franchise, or supply agreements with Valvoline. Additionally, if the franchisees are impacted by weak economic conditions and are unable to secure adequate sources of financing, their financial health may worsen, and Valvoline’s revenues may decline. If sales or business performance trends worsen for franchisees, their financial results may deteriorate, which could result in, among other things, store closures, delayed or reduced royalties and purchases and reduced growth in the number of service center stores.

Valvoline’s success also depends on the willingness and ability of its independent franchisees to implement major initiatives, which may require additional investment by them, and to remain aligned with Valvoline on operating, promotional and capital-intensive reinvestment plans. The ability of Valvoline’s franchisees to contribute to the achievement of Valvoline’s overall plans is dependent in large part on the availability of financing to its franchisees at reasonable interest rates and may be negatively impacted by the financial markets in general or the creditworthiness of individual franchisees. The size of Valvoline’s largest franchisees creates additional risk due to their importance to the Company’s growth strategy, requiring their cooperation and alignment with Valvoline’s initiatives. Furthermore, if the franchisees are not able to obtain the financing necessary to complete planned remodel and construction projects, they may be forced to postpone or cancel such projects, impacting the Company’s ability to grow and expand the Valvoline retail footprint.

Risks related to operating Valvoline's business

The Company’s recently implemented enterprise resource planning (“ERP”) system has adversely impacted Valvoline’s internal controls and could continue to negatively impact the business if remedial efforts are not timely and effective.

Valvoline relies upon its ERP application to assist in managing certain business processes and summarizing operational and financial results. Following the sale of the former Global Products reportable segment in fiscal 2023, and as part of Valvoline’s continued evolution to a standalone retail business, the Company has been in the process of separating certain business processes, information systems and applications that were previously shared to support both businesses. On January 1, 2024, Valvoline implemented a new ERP application intended to better accommodate the retail business model and support the Company’s continued growth.

A material weakness in internal control over financial reporting arose in connection with the Company’s implementation of the new ERP system and its related impact on IT general controls, which included deficiencies related to certain business processes that were not adequately designed at the time of system implementation. While the ERP system is intended to ultimately improve and enhance business processes, its implementation resulted in disruptions to maintaining an effective internal control environment and the timely processing of invoices and billings to franchisee, independent operator and fleet customers. Although the new ERP application is not currently utilized in the day-to-day operations of Valvoline’s retail stores and there have been no material impacts on its ability to serve customers to-date, the conversion to any new IT system, including the planned implementation of a human resources information system expected in fiscal 2025, exposes the Company to additional risks and

possible continued disruptions. This includes the loss of information, unauthorized access and systematic changes, disruption to normal operations, and risks associated with integrations with other applications and processes.

Implementing the new ERP system has required, and the efforts associated with mitigation, remediation, and enhancements will continue to require, the investment of significant personnel and financial resources. Failure to adequately and timely address any known or potential issues to ensure the new ERP system operates as intended could result in unexpected incremental costs and diversion of management’s attention and resources, further interruptions or delays in processes and challenges with vendor and customer relationships, difficulty in achieving and maintaining effective internal controls and issuing timely and accurate financial results. Valvoline management has implemented a remedial plan, as described in Item 9A, Controls and Procedures, which substantial progress has been made during fiscal 2024. However, management cannot provide any assurance that such remedial measures, or any other remedial measures taken, will be effective and identify or address all inherent risks from implementing an ERP system. If this remediation fails or other material weaknesses arise, it may adversely affect operating results, the trading price of Valvoline’s common stock, internal control over financial reporting, or the ability to effectively manage the business.

Changes in economic conditions that impact customer spending could harm Valvoline’s business.

Economic downturns, including a recession, may reduce customer demand or inhibit Valvoline’s ability to provide its services. Valvoline’s business and operating results are sensitive to declining economic conditions, credit market tightness, declining customer and business confidence, volatile exchange and interest rates, continuing inflation and other challenges, including those related to acts of aggression or threatened aggression that can affect the economy and financial markets. In the event of adverse developments or stagnation in the economy or financial markets, Valvoline’s customers may defer vehicle maintenance, oil changes, or other services, may repair and maintain their vehicles themselves or be unable to obtain credit reducing their ability to spend.

In a prolonged economic downturn or recession, these risks and uncertainties could have a material negative impact on Valvoline’s business, financial condition and results of operations. The severity and duration of a downturn in economic and financial market conditions, as well as the timing, strength, and sustainability of a recovery, are unknown and are not within the Company’s control. If the U.S. economy were to enter a recession, the recessionary risks discussed above and elsewhere within these risk factors could be more pronounced in such an economic climate.

Economic weakness and uncertainty may cause changes in customer preferences and habits, and if such economic conditions persist for an extended period of time, this may result in customers making long-lasting changes to their spending behaviors, which could unfavorably impact Valvoline’s business, its results of operations and cash flows. Additionally, during periods of favorable economic conditions, customers may be more likely to purchase new vehicles rather than maintaining and servicing older vehicles, which could also have an adverse impact on Valvoline’s business, results of operations, cash flows and strategic objectives.

If Valvoline does not attract, train and retain quality employees in appropriate numbers, including key employees and management, performance could be adversely affected.

Valvoline’s performance is dependent on recruiting, developing, training, and retaining quality and diverse service center employees in large numbers. Valvoline’s service centers positions are subject to high rates of turnover. Valvoline’s ability to meet labor needs while controlling costs is subject to external factors, such as unemployment levels, prevailing wage rates, wage legislation, and changes in rules governing eligibility for overtime and changing demographics. In the event of increasing wage rates, if Valvoline does not increase wages competitively, staffing levels and customer service could suffer because of declining workforce quality. Valvoline’s earnings could decrease if wage rates increase, whether in response to market demands or new wage legislation, and Valvoline is unable to adjust pricing to offset the additional costs. In addition, inflation and economic uncertainty may negatively impact Valvoline’s ability to attract and retain employees.

Valvoline’s success also depends on the efforts of key management personnel. Valvoline’s failure to develop an adequate succession plan for one or more of these key positions could reduce Valvoline’s institutional knowledge base and competitive advantage during a transition. The loss or limited availability of the services of one or more key management personnel, or Valvoline’s inability to recruit and retain qualified diverse candidates in the future,

could, at least temporarily, have an adverse effect on Valvoline’s operating results and financial condition. Additionally, turnover in other key positions can disrupt progress in implementing business strategies, result in a loss of institutional knowledge, cause greater workload demands for remaining team members and divert attention away from key areas of the business, or otherwise negatively impact the Company’s growth prospects or future operating results.

Valvoline uses information technology systems to conduct business, and a cybersecurity threat, data breach, security incident, failure of a key information technology system, or inability to enhance its capabilities could adversely affect Valvoline’s business and reputation.

Valvoline relies on its information technology systems, including systems which are managed or provided by third-party service providers, to conduct its business. The Company’s point-of-sale platforms for company-operated and franchisee retail stores could be subject to cybersecurity threats, service outages, or data breaches, such as the July 2024 software update by CrowdStrike Holdings, Inc., a cybersecurity technology company, which caused a global information technology outage. This incident required temporary manual processes to maintain operations. Although it was brief and did not have a material impact to business, Valvoline’s business was adversely impacted by the outage and slowed service. Similar software-induced interruptions or any security breach involving the point-of-sale or other systems within the Valvoline network could harm business operations, result in a loss of consumer confidence, or cause costs to be incurred associated with data recovery, investigation, remediation, and data breach notification obligations required under data privacy laws, which can be significant and vary by jurisdiction.

Despite employee training and other measures to mitigate them, cybersecurity threats to its information technology systems, and those of its third-party service providers, are increasing and becoming more advanced and cyber incidents have occurred and could occur as a result of unauthorized access, business email compromise, viruses, malicious code, ransomware, phishing, organized cyber-attacks, social engineering, break-ins, and security breaches due to error or misconduct by its employees, contractors or third-party service providers. The cyber incidents that have occurred have not resulted in a material loss to Valvoline; however, a material breach of or failure of Valvoline’s information technology systems, including systems in which data is stored or may be transferred across third-party platforms, could lead to the loss and destruction of trade secrets, confidential information, proprietary data, intellectual property, customer and supplier data, and employee personal information, and could disrupt business operations which could adversely affect Valvoline’s relationships with business partners and harm its brands, reputation and financial results.

Valvoline’s customer and vendor data may include names, addresses, phone numbers, email addresses and payment account information, among other information. Depending on the nature of the data that is compromised, Valvoline may also have obligations to notify individuals, regulators, law enforcement or payment companies about the incident and may need to provide some form of remedy. Valvoline could also face fines and penalties should it fail to adequately notify affected parties pursuant to new and evolving privacy laws in various jurisdictions in which it does business, as outlined in greater detail in the "Regulatory, legal, and financial risks" section below.

Valvoline is continuing to expand, upgrade and develop its information technology capabilities, including, the Company’s core ERP system. If the Company is unable to adequately transition its information technology organization’s skills and capabilities rapidly enough, including the ability to capitalize on the advancements in Artificial Intelligence software and platforms, it may not effectively support the modernization of Valvoline’s technology architecture and environment. This could hinder Valvoline’s ability to keep pace with its growth and digital initiatives for the consumer-oriented, data driven, mobility enabled nature of the business. Consequently, this might inhibit Valvoline’s ability to meet stakeholder needs and preferences.

Business disruptions from natural, operational and other catastrophic risks could seriously harm Valvoline’s operations and financial performance. In addition, a catastrophic event at one of Valvoline’s service center stores or involving its services or employees could lead to liabilities that could further impair its operations and financial performance.

Business disruptions, including those related to operating hazards inherent in servicing vehicles, natural disasters, severe weather conditions, climate change, supply or logistics disruptions, increasing costs for energy, temporary store and/or power outages, information technology systems and network disruptions, cybersecurity breaches, terrorist attacks, armed conflicts, war, pandemic diseases, fires, floods or other catastrophic events, could harm Valvoline’s operations as well as the operations of Valvoline’s customers and suppliers, and may adversely impact Valvoline’s financial performance. Although the impact to the Company’s results of operations and financial

condition were not material, the recent hurricanes Beryl, Helene and Milton caused certain company-operated and franchised service center stores to temporarily pause operations for a period of time for safety and evacuations, in addition to being impacted by intermittent connectivity issues and limited damage to stores. In these cases when the stores remain open, they often rely upon manual processes which can slow service times and minimize transactions, or in the cases where the stores have to close for a period of time, the inability to service customers until the stores are safe to operate. Although it is impossible to predict the occurrence or consequences of any such events, they could result in reduced demand for Valvoline’s services or make it difficult or impossible for Valvoline to deliver services to its customers. In addition to leading to a disruption of Valvoline’s businesses, a catastrophic event at one of Valvoline’s service center stores or involving its employees could lead to substantial legal liability to or claims by parties allegedly harmed by the event.

While Valvoline maintains business continuity plans that are intended to allow it to continue operations or mitigate the effects of events that could disrupt its business, Valvoline cannot provide assurances that its plans would fully protect it from all such events. In addition, insurance maintained by Valvoline to protect against property damage, loss of business and other related consequences resulting from catastrophic events is subject to significant retentions and coverage limitations, depending on the nature of the risk insured. This insurance may not be sufficient to cover all of Valvoline’s damages or damages to others in the event of a catastrophe. In addition, insurance related to these types of risks may not be available now or, if available, may not be available in the future at commercially reasonable rates.

Pandemics, epidemics or disease outbreaks may disrupt Valvoline’s business and operations, which could materially affect Valvoline’s financial condition, results of operations and forward-looking expectations.

Disruptions caused by pandemics, epidemics or disease outbreaks, such as COVID-19, in the United States or Canada, could materially affect Valvoline's results of operations, financial condition and forward-looking expectations. These events could impact Valvoline's business, particularly as it relates to congestion in the supply chain and related cost, as well as disruptions in the labor market. The Company could experience reduced traffic and sales volume due to changes in customer behavior as individuals may decrease automobile use and practice social distancing and other behavioral changes which may be mandated by governmental authorities or independently undertaken out of an abundance of caution. The extent to which these events could impact Valvoline's business results and operations depends upon the duration and severity, emerging variants, vaccine and booster effectiveness, public acceptance of safety protocols, and governmental measures, including vaccine mandates, among others.

Worsening conditions in the severity and spread of pandemics, epidemics, or disease outbreaks, could result in the resurgence of lockdowns or stay-at-home guidelines which could adversely affect Valvoline’s ability to implement its growth plans, including, without limitation, delay the construction or acquisition of service center stores, or negatively impact Valvoline’s ability to successfully execute plans to enter into new markets; reduce demand for Valvoline’s services; affect the ability and cost to attract and retain talent within the labor market; reduce sales or profitability; negatively impact Valvoline’s ability to maintain operations; or lead to significant disruption of financial markets in which the Company operates, and may reduce Valvoline’s ability to access capital and, in the future, negatively affect the Company’s liquidity.

The limited diversification of Valvoline’s operations subjects it to risks.

Historically, Valvoline has been able to take advantage of its size and global reach as a combined products and services company. The sale of Global Products reportable segment during fiscal 2023 resulted in Valvoline being a smaller, less diversified company, potentially making it more vulnerable to changing market, regulatory and economic conditions. Following completion of the sale of Global Products, Valvoline is more concentrated geographically in the U.S. and Canada and in serving the automotive aftermarket through company-operated, independent franchise and Express Care stores that service vehicles with Valvoline products. In addition, as a smaller company, Valvoline may be unable to obtain goods or services at prices or on terms that are as favorable as those obtained by Valvoline prior to the sale of Global Products, and Valvoline’s ability to absorb costs or unexpected expenses whether due to contingencies or other risks as described herein, may be negatively impacted. Any of these factors could have an adverse effect on Valvoline’s business, financial condition, results of operations, or cash flows.

Operating in numerous locations in the U.S. and Canada increases the scrutiny on Valvoline’s reputation for safety, quality, friendliness, trustworthy service, integrity and business ethics. Any negative publicity about these or other areas involving the business, including Valvoline’s response or lack thereof to external events involving civil unrest, social justice, and political issues, whether or not based in fact, could damage Valvoline’s reputation and the value of the brand.

Regulatory, legal, and financial risks

Data protection requirements could increase operating costs and requirements and a breach in information privacy or other related risks could negatively impact operations.