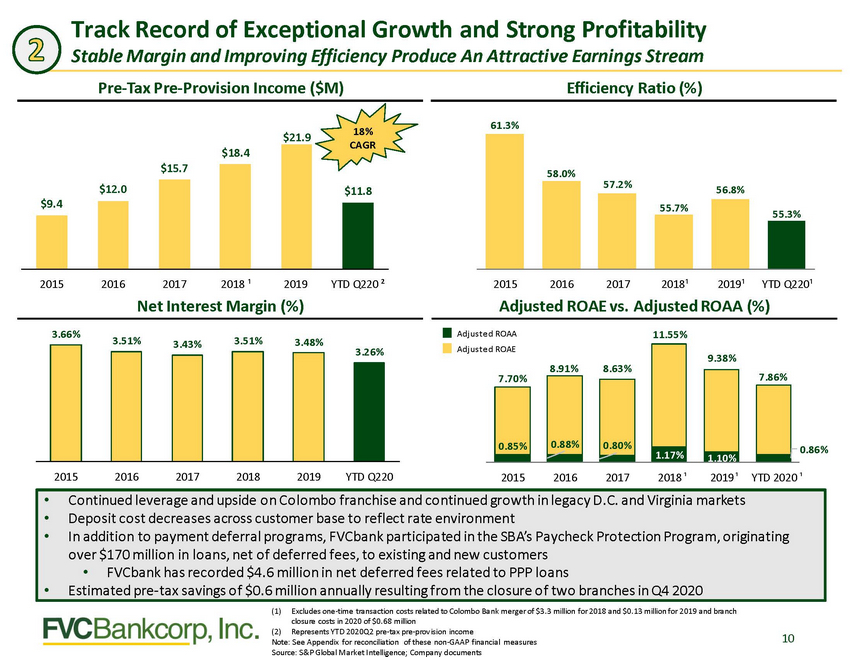

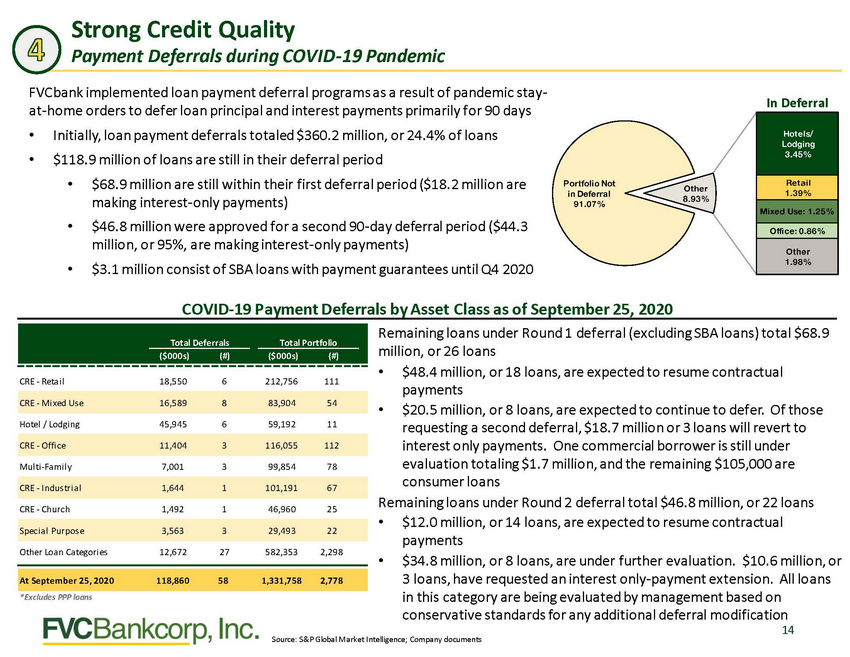

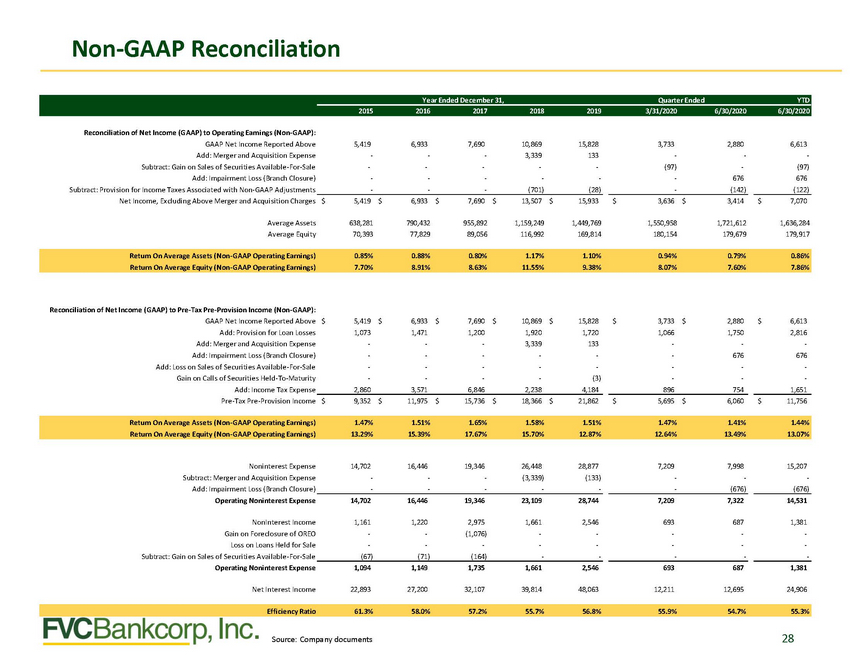

| Non-GAAP Reconciliation Reconciliation of Net Income (GAAP) to Operating Earnings (Non-GAAP): GAAP Net Income Reported Above Add: Merger and Acquisition Expense Subtract: Gain on Sales of Securities Available-For-Sale Add: Impairment Loss (Branch Closure) Subtract: Provision for Income Taxes Associated with Non-GAAP Adjustments Net Income, Excluding Above Merger and Acquisition Charges 5,419 - - - - 6,933 - - - - 7,690 - - - - 10,869 3,339 - - (701) 15,828 133 - - (28) 3,733 - (97) - - 2,880 - - 676 (142) 6,613 - (97) 676 (122) $ 5,419 $ 6,933 $ 7,690 $ 13,507 $ 15,933 $ 3,636 $ 3,414 $ 7,070 Average Assets Average Equity 638,281 70,393 790,432 77,829 955,892 89,056 1,159,249 116,992 1,449,769 169,814 1,550,958 180,154 1,721,612 179,679 1,636,284 179,917 Reconciliation of Net Income (GAAP) to Pre-Tax Pre-Provision Income (Non-GAAP): GAAP Net Income Reported Above Add: Provision for Loan Losses Add: Merger and Acquisition Expense Add: Impairment Loss (Branch Closure) Add: Loss on Sales of Securities Available-For-Sale Gain on Calls of Securities Held-To-Maturity Add: Income Tax Expense Pre-Tax Pre-Provision Income $ 5,419 1,073 - - - - 2,860 $ 6,933 1,471 - - - - 3,571 $ 7,690 1,200 - - - - 6,846 $ 10,869 1,920 3,339 - - - 2,238 $ 15,828 1,720 133 - - (3) 4,184 $ 3,733 1,066 - - - - 896 $ 2,880 1,750 - 676 - - 754 $ 6,613 2,816 - 676 - - 1,651 $ 9,352 $ 11,975 $ 15,736 $ 18,366 $ 21,862 $ 5,695 $ 6,060 $ 11,756 Noninterest Expense Subtract: Merger and Acquisition Expense Add: Impairment Loss (Branch Closure) Operating Noninterest Expense 14,702 - - 16,446 - - 19,346 - - 26,448 (3,339) - 28,877 (133) - 7,209 - - 7,998 - (676) 15,207 - (676) 14,702 16,446 19,346 23,109 28,744 7,209 7,322 14,531 NonInterest Income Gain on Foreclosure of OREO Loss on Loans Held for Sale 1,161 - - 1,220 - - 2,975 (1,076) - 1,661 - - 2,546 - - 693 - - 687 - - 1,381 - - - Subtract: Gain on Sales of Securities Available-For-Sale (67) (71) (164) - - - - Operating Noninterest Expense 1,094 1,149 1,735 1,661 2,546 693 687 1,381 Net Interest Income 22,893 27,200 32,107 39,814 48,063 12,211 12,695 24,906 28 Source: Company documents Efficiency Ratio 61.3% 58.0% 57.2% 55.7% 56.8% 55.9% 54.7% 55.3% Return On Average Assets (Non-GAAP Operating Earnings) 1.47% 1.51% 1.65% 1.58% 1.51% 1.47% 1.41% 1.44% Return On Average Equity (Non-GAAP Operating Earnings) 13.29% 15.39% 17.67% 15.70% 12.87% 12.64% 13.49% 13.07% Return On Average Assets (Non-GAAP Operating Earnings) 0.85% 0.88% 0.80% 1.17% 1.10% 0.94% 0.79% 0.86% Return On Average Equity (Non-GAAP Operating Earnings) 7.70% 8.91% 8.63% 11.55% 9.38% 8.07% 7.60% 7.86% Year Ended December 31, Quarter Ended YTD 2015 2016 2017 2018 2019 3/31/2020 6/30/2020 6/30/2020 |