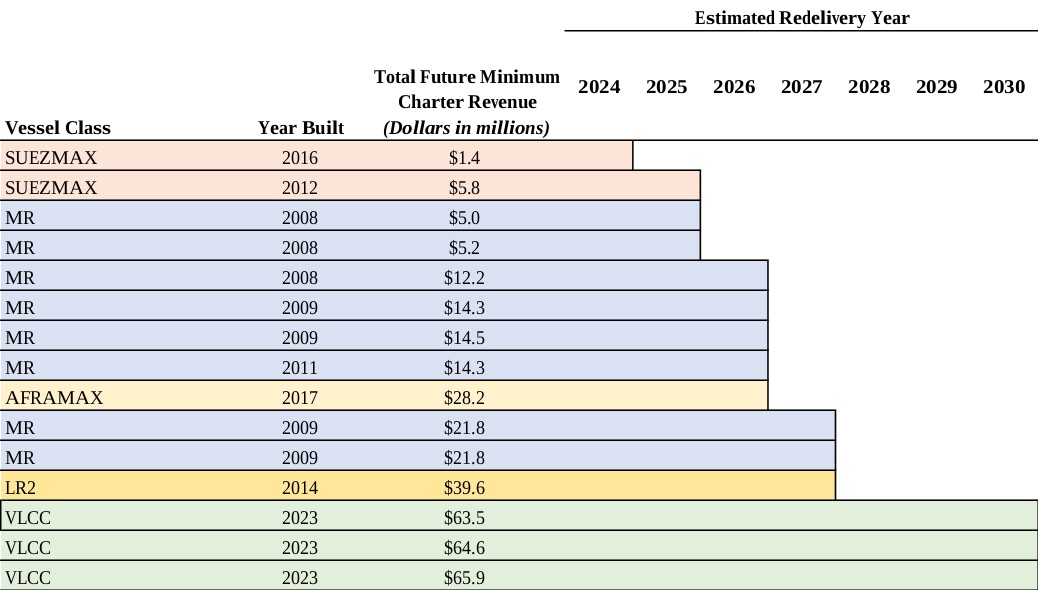

Operations and Oil Tanker Markets:

The International Energy Agency (“IEA”) estimates global oil consumption for the second quarter of 2024 at 102.9 million barrels per day (“b/d”), up 0.7% from the same quarter in 2023. The estimate for global oil consumption for 2024 is 103.1 million b/d, an increase of 1.0% over the 2023 estimate of 102.1 million b/d. OECD demand in 2024 is estimated to decrease 0.2% to 45.6 million b/d, while non-OECD demand is estimated to increase by 2.0% to 57.5 million b/d.

Global oil production in the second quarter of 2024 was 102.2 million b/d, a decrease of 0.3 million b/d from the second quarter of 2023. OPEC crude oil production averaged 26.6 million b/d in the second quarter of 2024, the same level as the first quarter of 2024, and a decrease of 1.7 million b/d from the second quarter of 2023. Non-OPEC production increased by 1.4 million b/d to 70.1 million b/d in the second quarter of 2024 compared with the second quarter of 2023. Oil production in the U.S. in the second quarter of 2024 increased by 5.5% to 13.3 million b/d compared to the first quarter of 2024 and by 4.7% from the second quarter of 2023.

U.S. refinery throughput increased by 0.5 million b/d to 16.4 million b/d in the second quarter of 2024 compared with the first quarter of 2024. U.S. crude oil imports in the second quarter of 2024 increased by 0.4 million b/d to 6.6 million b/d compared with the second quarter of 2023, with imports from OPEC countries remaining flat and imports from non-OPEC countries increasing by 0.4 million b/d.

China’s crude oil imports decreased in June 2024 to 11.3 million b/d, a drop of 11% year-over-year, and first half 2024 crude oil imports were at 11.1 million b/d, down 2.3% year-over-year.

Total OECD commercial inventories ended the second quarter of 2024 down 1.9% or 27 million barrels of crude, and up 1.8% or 26 million barrels of products, respectively, compared with the second quarter of 2023.

During the second quarter of 2024, the tanker fleet of vessels over 10,000 dwt increased, net of vessels recycled, by 0.9 million dwt as the crude fleet increased by 0.5 million dwt, all in the Aframax fleet. The product carrier fleet increased by 0.4 million dwt, all in the MR fleet. Year-over-year, the size of the tanker fleet increased by 6.8 million dwt with the VLCCs, Suezmaxes, Aframaxes, and MRs increasing by 1.5 million dwt, 0.2 million dwt, 3.1 million dwt, and 2.1 million dwt, respectively. The LR1/Panamax fleet remained unchanged.

During the second quarter of 2024, the tanker orderbook increased by 8.4 million dwt overall compared with the first quarter of 2024. The crude tanker orderbook increased by 5.3 million dwt. The VLCC orderbook increased by 3.4 million dwt, while the Suezmax and Aframax orderbooks increased by 0.5 million dwt and 1.5 million dwt, respectively. The product carrier orderbook increased by 3.1 million dwt, with increases in the LR1 and MR sectors of 0.9 million dwt and 2.2 million dwt respectively. Year-over-year, the total tanker orderbook increased by 38.4 million dwt, with increases in VLCC, Suezmaxes, Aframaxes, Panamaxes and LR1s of 15.3 million dwt, 8.2 million dwt, 5.9 million dwt, 2.7 million dwt and 6.4 million dwt, respectively.

Crude tanker rates remained strong in the second quarter of 2024, although VLCC rates were weaker than in the first quarter of 2024, a weakness that is persisting into the third quarter of 2024, on the back of reduced Chinese crude oil imports. Even so, current rates remain significantly over 10-year average rates and cash breakeven levels, reflecting the continuing impact of the disruptions in trade flows on tanker demand. Clean product tanker rates remained strong during the second quarter of 2024, and that strength continues into the third quarter of 2024.

Update on Critical Accounting Estimates and Policies:

The Company’s consolidated financial statements are prepared in accordance with accounting principles generally accepted in the United States, which require the Company to make estimates in the application of its accounting policies based on the best assumptions, judgments and opinions of management. For a description of all of the Company’s material accounting policies, see Note 3, “Summary of Significant Accounting Policies,” to the Company’s consolidated financial statements as of and for the year ended December 31, 2023 included in the Company’s Annual Report on Form 10-K. See Note 2, “Significant Accounting Policies,” to