EXHIBIT 99.2

EGNITUS INC.

INDEX TO CONDENSED FINANCIAL STATEMENTS

(UNAUDITED)

| 1 |

CONSOLIDATED BALANCE SHEETS

(Amount expressed in United States Dollars (“US$”), except for number of shares)

| Note | September 30, 2018 (unaudited) | December 31, 2017 (audited) | ||||||||

| ASSETS | ||||||||||

| Current assets: | ||||||||||

| Cash and bank balances | $ | 2,547 | $ | 10,956 | ||||||

| Trade receivables | - | 25,125 | ||||||||

| Other receivables and deposits | 3 | 19,275 | 28,101 | |||||||

| Amount owing by directors | 4 | 17,296 | 22,894 | |||||||

| Total current assets | 39,118 | 87,076 | ||||||||

| Non-current assets: | ||||||||||

| Plant and equipment, net | 5 | 257,780 | 310,455 | |||||||

| Total non-current asset | 257,780 | 310,455 | ||||||||

| TOTAL ASSETS | $ | 296,898 | $ | 397,531 | ||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||||

| Current liabilities: | ||||||||||

| Trade payables | $ | - | $ | 229,599 | ||||||

| Other payables and accrued liabilities | 6 | 384,549 | 2,462 | |||||||

| Deferred income | 3,414 | - | ||||||||

| Amount owing to directors | 7 | 48,381 | 67,938 | |||||||

| Income tax payable | 4,834 | 18,045 | ||||||||

| Total current liabilities | 441,178 | 318,044 | ||||||||

| TOTAL LIABILITIES | $ | 441,178 | $ | 318,044 | ||||||

| Stockholders’ equity: | ||||||||||

| Issued capital, 19,768,800 outstanding as of September 30, 2018, and 19,477,500 outstanding as of December 31, 2017 | 8 | $ | 1,977 | $ | 1,949 | |||||

| Additional paid up share capital | 560,374 | 406,227 | ||||||||

| Accumulated losses | (580,094 | ) | (217,487 | ) | ||||||

| Other comprehensive expense | (125,071 | ) | (111,387 | ) | ||||||

| Total equity attributable to owners of the Company | (142,814 | ) | 79,302 | |||||||

| Non-controlling interests | (1,466 | ) | 185 | |||||||

| Total stockholders’ equity | (144,280 | ) | 79,487 | |||||||

| TOTAL LIABILITIES AND STOCKHOLDERS EQUITY | $ | 296,898 | $ | 397,531 | ||||||

See accompanying notes to financial statements

| 2 |

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

AND COMPREHENSIVE (EXPENSE)/INCOME

(Amount expressed in United States Dollars (“US$”), except for number of shares)

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||

| 2018 (unaudited) | 2017 (unaudited) | 2018 (unaudited) | 2017 (unaudited) | |||||||||||||

| Revenues, net | $ | 18,065 | $ | 26,222 | $ | 63,869 | $ | 214,641 | ||||||||

| Cost of revenues | - | (18,127 | ) | (2,909 | ) | (58,222 | ) | |||||||||

| Gross profit | 18,065 | 8,095 | 60,960 | 156,419 | ||||||||||||

| Operating expenses | (159,966 | ) | (108,733 | ) | (425,077 | ) | (201,193 | ) | ||||||||

| Loss from operations | (141,901 | ) | (100,638 | ) | (364,117 | ) | (44,774 | ) | ||||||||

| Income taxes | - | - | - | (3,644 | ) | |||||||||||

| NET LOSS | $ | (141,901 | ) | $ | (100,638 | ) | $ | (364,117 | ) | $ | (48,418 | ) | ||||

| Net loss attributable to non-controlling interests | 819 | 187 | 1,510 | 367 | ||||||||||||

| NET LOSS ATTRIBUTABLE TO THE COMPANY | (141,082 | ) | (100,451 | ) | (362,607 | ) | (48,051 | ) | ||||||||

| Other comprehensive expense: | ||||||||||||||||

| - Foreign currency translation (loss)/gain | 2,600 | 37,928 | (14,387 | ) | (31,754 | ) | ||||||||||

| COMPREHENSIVE (EXPENSE)/INCOME | $ | (138,482 | ) | $ | (62,523 | ) | $ | (376,994 | ) | $ | (79,805 | ) | ||||

| Other comprehensive gain/(expense) attributable to non-controlling interests | 154 | (273 | ) | 141 | (271 | ) | ||||||||||

| TOTAL COMPREHENSIVE (EXPENSE)/INCOME ATTRIBUTABLE TO THE COMPANY | $ | (138,328 | ) | $ | (62,796 | ) | $ | (376,853 | ) | $ | (80,076 | ) | ||||

See accompanying notes to financial statements

| 3 |

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Amount expressed in United States Dollars (“US$))

| For the Nine Months Ended September 30, | ||||||||

| 2018 (unaudited) | 2017 (unaudited) | |||||||

| Cash flows from operating activities: | ||||||||

| Net loss | $ | (364,117 | ) | $ | (48,418 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Depreciation of plant and equipment | 47,102 | 31,096 | ||||||

| Operating (loss)/profit before working capital changes | (317,015 | ) | (17,322 | ) | ||||

| Changes in operating assets and liabilities: | ||||||||

| Trade and other receivables | 23,451 | (52,935 | ) | |||||

| Trade and other payables | 153,190 | (146,306 | ) | |||||

| Cash used in operating activities | (140,374 | ) | (216,563 | ) | ||||

| Cash flows from investing activities: | ||||||||

| Purchase of plant and equipment | - | (146,953 | ) | |||||

| Net cash used in investing activities | - | (146,953 | ) | |||||

| Cash flows from financing activities: | ||||||||

| Proceed from issued shares | 159,748 | |||||||

| Acquisition of subsidiaries | - | (46,021 | ) | |||||

| (Repayment to)/Advance from Directors | (13,959 | ) | 73,093 | |||||

| Net cash generated from/(used in) financing activities | 145,789 | 27,072 | ||||||

| Foreign currency translation adjustment | (13,824 | ) | 68,582 | |||||

| NET CHANGE IN CASH AND CASH EQUIVALENTS | (8,409 | ) | (267,862 | ) | ||||

| CASH AND CASH EQUIVALENTS, BEGINNING OF FINANCIAL YEAR | 10,956 | 269,991 | ||||||

| CASH AND CASH EQUIVALENTS, END OF FINANCIAL YEAR | $ | 2,547 | 2,129 | |||||

See accompanying notes to financial statements.

| 4 |

EGNITUS INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS (CONT.)

(Amount expressed in United States Dollars (“US$))

| For the Nine Months Ended September 30, | ||||||||

| 2018 (unaudited) | 2017 (unaudited) | |||||||

| CASH AND CASH EQUIVALENTS INFORMATION: | ||||||||

| Cash in hand | $ | 1,119 | $ | 1,307 | ||||

| Cash at bank | 1,428 | 822 | ||||||

| Cash and cash equivalents, end of financial year | 2,547 | 2,129 | ||||||

| For the Nine Months Ended September 30, | ||||||||

| 2018 | 2017 | |||||||

| (unaudited) | (unaudited) | |||||||

| Supplementary cash flows information: | ||||||||

| Income taxes paid | $ | - | $ | 3,644 | ||||

See accompanying notes to financial statements.

| 5 |

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY/(DEFICIT)

(Amount expressed in United States Dollars (“US$))

| Common stock | Additional paid up share | Accumulated | Accumulated other comprehensive | Non-controlling | Total | |||||||||||||||||||||||

| Share capital | capital | Losses | expense | Total | interest | Equity | ||||||||||||||||||||||

| Balance as of December 31, 2017 | $ | 1,949 | $ | 406,227 | $ | (217,487 | ) | $ | (111,387 | ) | $ | 79,301 | $ | 185 | $ | 79,487 | ||||||||||||

| Issued of share capital | 28 | 154,147 | - | - | 154,175 | - | 154,175 | |||||||||||||||||||||

| Net loss | - | - | (362,607 | ) | - | (362,607 | ) | (1,510 | ) | (364,117 | ) | |||||||||||||||||

| Foreign currency translation loss | - | - | - | (14,246 | ) | (14,246 | ) | (141 | ) | (14,387 | ) | |||||||||||||||||

| Balance as of September 30, 2018 | 1,977 | 560,374 | (580,094 | ) | (125,633 | ) | (143,376 | ) | (1,466 | ) | (144,842 | ) | ||||||||||||||||

See accompanying notes to financial statements.

| 6 |

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENT

(Amount expressed in United States Dollars (“US$”), except for number of shares)

| 1. | ORGANIZATION AND BUSINESS BACKGROUND |

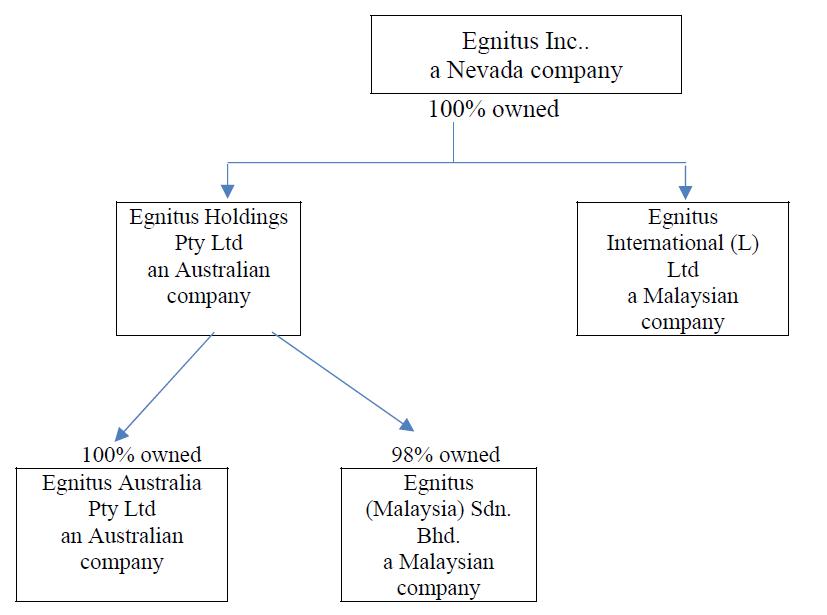

Egnitus Inc. was incorporated in the State of Nevada on June 5, 2017. On December 17, 2017, the Company acquired all of the outstanding capital stock of Egnitus Holding Pty Ltd and Egnitus International (L) Ltd., an Australian and Malaysian corporation (“Subsidiary”) respectively. The Subsidiaries was incorporated in Australia and Malaysian on April 13, 2015 and July 29, 2011 respectively.

The principal office address is 713 Glen Oaks Dr, Thousand Oaks, CA 91360. We also have branch offices which is located at Level 9, 127 Creet St, Brisbane, Australia 4000 and No 34.02 Menara Citibank, 165 Jalan Ampang, 50450 Kuala Lumpur, Malaysia. Our telephone number is (+61) 7-3148-5354 and our website is www.egnatium.com.

The corporate structure is depicted below:

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

| ● | Basis of presentation |

The accompanying unaudited condensed financial statements have been prepared by management in accordance with both accounting principles generally accepted in the United States (“GAAP”), and the instructions to Rule 10-01 of Regulation S-X. Certain information and note disclosures normally included in audited financial statements prepared in accordance with generally accepted accounting principles have been condensed or omitted pursuant to those rules and regulations, although the Company believes that the disclosures made are adequate to make the information not misleading.

| 7 |

| ● | Basis of presentation (continued) |

In the opinion of management, the balance sheet as of December 31, 2017 which has been derived from the audited financial statements and these unaudited condensed financial statements reflect all normal and recurring adjustments considered necessary to state fairly the results for the periods presented. The results for the period ended September 30, 2018 are not necessarily indicative of the results to be expected for the entire fiscal year ending December 31, 2018 or for any future period.

These unaudited financial statements and notes thereto should be read in conjunction with the audited financial statements for the year ended December 31, 2017.

| ● | Going concern |

The Company’s condensed consolidated financial statements are prepared using generally accepted accounting principles in the United States of America applicable to a going concern, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The Company has generated minimal revenue and has sustained operating losses since inception to date and allow it to continue as a going concern. The continuation of the Company as a going concern is dependent upon the continued financial support from its shareholders, the ability of the Company to obtain necessary financing to continue operations, and the attainment of profitable operations. The Company incurred a net loss of $364,117 for the period ended September 30, 2018, incurred a net current liabilities of $402,060 and an accumulated deficit of $580,094 as of September 30, 2018. These factors, among others, raise a substantial doubt regarding the Company’s ability to continue as a going concern. If the Company is unable to obtain adequate capital, it could be forced to cease operations. The accompanying consolidated financial statements do not include any adjustments to reflect the recoverability and classification of recorded asset amounts and classification of liabilities that might be necessary should the Company be unable to continue as a going concern.

| ● | Use of estimates |

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. The Company regularly evaluates estimates and assumptions related to the valuation of accounts receivable, accounts payable, accrued liabilities, payable to related party, valuation of beneficial conversion features in convertible debt, valuation of derivatives, and deferred income tax asset valuation allowances. The Company bases its estimates and assumptions on current facts, historical experience and various other factors that it believes to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities and the accrual of costs and expenses that are not readily apparent from other sources. The actual results experienced by the Company may differ materially and adversely from the Company’s estimates. To the extent there are material differences between the estimates and the actual results, future results of operations will be affected.

| ● | Cash and cash equivalents |

Cash and cash equivalents represent cash on hand, demand deposits placed with banks or other financial institutions and all highly liquid investments with an original maturity of three months or less as of the purchase date of such investments.

| 8 |

| ● | Plant and equipment |

Plant and equipment are stated at cost less accumulated depreciation and accumulated impairment losses, if any. Depreciation is calculated on the straight-line basis to write off the cost over the following expected useful lives of the assets concerned. The principal annual rates used are as follows:

| Categories | Principal Annual Rates/Expected Useful Life | |||

| Computer and software | 20 | % | ||

| Trade mark | 20 | % | ||

| Furniture and fittings | 20 | % | ||

| Renovation | 20 | % | ||

| Motor vehicle | 20 | % | ||

Fully depreciated plant and equipment are retained in the financial statements until they are no longer in use.

| ● | Revenue recognition |

The Company provides vocational training, consulting services for assets and education for construction tradesman that need qualifications for roofing, plumbing, home renovation, electrical and carpentry. The Company’s training packages vary in price according to the different types of vocational training and education programs purchased by the customers. The Company recognizes revenue upon the completion of the vocational training courses and education programs offered to its customers. The Company recognizes as revenue any deposits previously received, as they are non-refundable upon commencement of the vocational training courses.

The Company’s revenue recognition policy is based on the revenue recognition criteria established in accordance with Accounting Standards Codification (ASC) 605. The criteria and how the Company satisfies each element are as follows: (1) persuasive evidence of an arrangement - the Company and the customer enters into a signed contract; (2) delivery has occurred - as noted above, upon the commencement of the training course, the deposit is non-refundable per the terms of the signed contract and upon completion of the course, the Company has provided all services to be delivered to the customer under the contract; (3) the price is fixed and determinable - the signed contract indicates a fixed dollar amount for the training for the courses enrolled by the customer; (4) collectability is reasonable assured - the Company receives as payment a deposit and the balance of the training upon the completion of the training course.

| ● | Comprehensive income |

ASC Topic 220, “Comprehensive Income” establishes standards for reporting and display of comprehensive income, its components and accumulated balances. Comprehensive income as defined includes all changes in equity during a period from non-owner sources. Accumulated other comprehensive income, as presented in the accompanying statements of stockholders’ equity consists of changes in unrealized gains and losses on foreign currency translation and cumulative net change in the fair value of available-for-sale investments held at the balance sheet date. This comprehensive income is not included in the computation of income tax expense or benefit.

| ● | Income tax expense |

Income taxes are determined in accordance with the provisions of ASC Topic 740, “Income Taxes” (“ASC Topic 740”). Under this method, deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax basis. Deferred tax assets and liabilities are measured using enacted income tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. Any effect on deferred tax assets and liabilities of a change in tax rates is recognized in income in the period that includes the enactment date.

| 9 |

| ● | Income tax expense (continued) |

ASC 740 prescribes a comprehensive model for how companies should recognize, measure, present, and disclosed in their financial statements uncertain tax positions taken or expected to be taken on a tax return. Under ASC 740, tax positions must initially be recognized in the financial statements when it is more likely than not the position will be sustained upon examination by the tax authorities. Such tax positions must initially and subsequently be measured as the largest amount of tax benefit that has a greater than 50% likelihood of being realized upon ultimate settlement with the tax authority assuming full knowledge of the position and relevant facts.

The Company conducts major businesses in Malaysia and is subject to tax in their own jurisdictions. As a result of its business activities, the Company will file separate tax returns that are subject to examination by the foreign tax authorities.

| ● | Foreign currencies translation |

Transactions denominated in currencies other than the functional currency are translated into the functional currency at the exchange rates prevailing at the dates of the transaction. Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional currency using the applicable exchange rates at the balance sheet dates. The resulting exchange differences are recorded in the statement of operations.

The functional currency of the Company is the United States Dollars (“US$”) and the accompanying financial statements have been expressed in US$. In addition, the Company maintains its books and record in a local currency, Malaysian Ringgit (“MYR” or “RM”) and Australian Dollars (“AUD”), which is functional currency as being the primary currency of the economic environment in which the entity operates.

In general, for consolidation purposes, assets and liabilities of its subsidiaries whose functional currency is not US$ are translated into US$, in accordance with ASC Topic 830-30, “Translation of Financial Statement”, using the exchange rate on the balance sheet date. Revenues and expenses are translated at average rates prevailing during the period. The gains and losses resulting from translation of financial statements of foreign subsidiary are recorded as a separate component of accumulated other comprehensive income.

Translation of amounts from the local currency of the Company into US$1 has been made at the following exchange rates for the respective years:

| As of and for the 9 months period ended September 30, | ||||||||

| 2018 | 2017 | |||||||

| Year-end MYR : US$1 exchange rate | 4.1370 | 4.2190 | ||||||

| Yearly average MYR : US$1 exchange rate | 3.9867 | 4.3430 | ||||||

| Year-end AUD : US$1 exchange rate | 0.7238 | 0.7815 | ||||||

| Yearly average AUD : US$1 exchange rate | 0.7579 | 0.7665 | ||||||

| ● | Related parties |

Parties, which can be a corporation or individual, are considered to be related if the Company has the ability, directly or indirectly, to control the other party or exercise significant influence over the other party in making financial and operating decisions. Companies are also considered to be related if they are subject to common control or common significant influence.

| 10 |

| ● | Fair value of financial instruments |

The carrying value of the Company’s financial instruments: cash and cash equivalents, trade receivable, deposits and other receivables, amount due to related parties and other payables approximate at their fair values because of the short-term nature of these financial instruments.

The Company also follows the guidance of the ASC Topic 820-10, “Fair Value Measurements and Disclosures” (“ASC 820-10”), with respect to financial assets and liabilities that are measured at fair value. ASC 820-10 establishes a three-tier fair value hierarchy that prioritizes the inputs used in measuring fair value as follows:

| ● | Level 1: Observable inputs such as quoted prices in active markets; |

| ● | Level 2: Inputs, other than the quoted prices in active markets, that are observable either directly or indirectly; and |

| ● | Level 3: Unobservable inputs in which there is little or no market data, which require the reporting entity to develop its own assumptions |

As of September 30, 2018, and December 31, 2017, the Company did not have any nonfinancial assets and liabilities that are recognized or disclosed at fair value in the financial statements, at least annually, on a recurring basis, nor did the Company have any assets or liabilities measured at fair value on a non-recurring basis.

| ● | Recent accounting pronouncements |

The Company has reviewed all recently issued, but not yet effective, accounting pronouncements and does not believe the future adoption of any such pronouncements may be expected to cause a material impact on its financial condition or the results of its operations.

In May 2014, the FASB issued Accounting Standards Update No. 2014-09, “Revenue from Contracts with Customers” (“ASU 2014-09”). ASU 2014-09 supersedes the revenue recognition requirements in “Revenue Recognition (Topic 605)”, and requires entities to recognize revenue when it transfers promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled to in exchange for those goods or services. ASU 2014-09 is effective for annual reporting periods beginning after December 15, 2016, including interim periods within that reporting period. Early adoption is not permitted. In August 2015, the FASB issued an Accounting Standards Update to defer by one year the effective dates of its new revenue recognition standard until annual reporting periods beginning after December 15, 2017 (2018 for calendar-year public entities) and interim periods therein. This adoption will not have a material impact on our financial statements.

In June 2014, the FASB issued ASU 2014-15, “Presentation of Financial Statements-Going concern (Subtopic 205-40) which provides guidance to an organization’s management, with principles and definitions that are intended to reduce diversity in the timing and content of disclosures that are commonly provided by organizations today in the financial statement footnotes. This guidance in ASU 2014-15 is effective for annual periods ending after December 15, 2016, and interim periods within annual periods beginning after December 15, 2016. Early application is permitted for annual or interim reporting periods for which the financial statements have not previously been issued. This adoption will not have a material impact on our financial statements.

In February 2015, the FASB issued ASU 2015-02 “Consolidation (Topic 810): Amendments to the Consolidation Analysis.” ASU 2015-02 changes the analysis that a reporting entity must perform to determine whether it should consolidate certain types of legal entities. It is effective for annual reporting periods, and interim periods within those years, beginning after December 15, 2015. Early adoption is permitted, including adoption in an interim period. This adoption will not have a material impact on our financial statements.

| 11 |

| ● | Recent accounting pronouncements (continued) |

In July 2015, the FASB issued ASU 2015-11, Inventory, which requires an entity to measure inventory within the scope at the lower of cost and net realizable value. Net realizable value is the estimated selling prices in the ordinary course of

business, less reasonably predictable costs of completion, disposal, and transportation. The effective date for the standard is for fiscal years beginning after December 15, 2016. Early adoption is permitted. We will recognize our inventories at cost or net realizable value, whichever lower.

In February 2016, the Financial Accounting Standards Board (the “FASB”) issued Accounting Standards Update (“ASU”) No. 2016-02, Leases (Topic 842). Under the new guidance, lessees will be required recognize the following for all leases (with the exception of short-term leases) at the commencement date: 1) A lease liability, which is a lessee’s obligation to make lease payments arising from a lease, measured on a discounted basis; and 2) A right-of-use asset, which is an asset that represents the lessee’s right to use, or control the use of, a specified asset for the lease term. The new lease guidance simplified the accounting for sale and leaseback transactions primarily because lessees must recognize lease assets and lease liabilities. Lessees will no longer be provided with a source of off-balance sheet financing. The amendments in this ASU are effective for fiscal years beginning after December 15, 2019, including interim periods within those years. The Company is evaluating this ASU and has not determined the effect of this standard on its ongoing financial reporting.

In January 2017, the FASB issued Accounting Standards Update No. 2017-01, Business Combinations (Topic 805): Clarifying the Definition of a Business (ASU 2017-01), which revises the definition of a business and provides new guidance in evaluating when a set of transferred assets and activities is a business. We will adopt the new standard effective January 1, 2018, on a prospective basis and do not expect the standard to have a material impact on our consolidated financial statements.

| 3 | OTHER RECEIVABLES AND DEPOSITS |

| As of, | ||||||||

| September 30, 2018 | December 31, 2017 | |||||||

| Other receivables | $ | 19,275 | $ | 6,093 | ||||

| Amount owing by related parties | - | 22,008 | ||||||

| $ | 19,275 | $ | 28,101 | |||||

The amount owing by related parties is unsecured, interest-free with no fixed repayment term.

| 4. | AMOUNT OWING BY DIRECTORS |

The amount owing by directors is unsecured, interest-free with no fixed repayment term.

| 12 |

| 5. | PLANT AND EQUIPMENT, NET |

Plant and equipment consisted of the following:

| As of, | ||||||||

| September 30, 2018 | December 31, 2017 | |||||||

| Computer and software | $ | 345,637 | $ | 329,924 | ||||

| Trade mark | 12,205 | 12,205 | ||||||

| Furniture and fittings | 1,091 | 1,091 | ||||||

| Renovation | 1,403 | 1,403 | ||||||

| Motor vehicle | 6,290 | 6,290 | ||||||

| 366,626 | 350,913 | |||||||

| (Less): Accumulated depreciation | (87,559 | ) | (56,114 | ) | ||||

| Add: Foreign translation differences | (21,287 | ) | 15,656 | |||||

| Property, plant and equipment, net | $ | 257,780 | $ | 310,455 | ||||

Depreciation expense for the period ended September 30, 2018 and for the year ended September 30, 2017 were $47,102 and $30,878, respectively.

| 6. | OTHER PAYABLES AND ACCRUED LIABILITIES |

| As of, | ||||||||

| September 30, 2018 | December 31, 2017 | |||||||

| Amount owing to related parties | $ | 112,524 | $ | 2,462 | ||||

| Accrued other expenses | 272,025 | - | ||||||

| $ | 384,549 | $ | 2,462 | |||||

The amount owing by related parties is unsecured, interest-free with no fixed repayment term.

| 7. | AMOUNT OWING TO DIRECTORS |

The amount owing to directors is unsecured, interest-free with no fixed repayment term.

| 8. | INCOME TAX |

Provision for income taxes consisted of the following:

| For the 9 months period ended September 30, | ||||||||

| 2018 | 2017 | |||||||

| Current: | ||||||||

| Local | $ | - | $ | - | ||||

| Foreign | - | 3,644 | ||||||

| - | 3,644 | |||||||

| Deferred tax | ||||||||

| Local | $ | - | $ | - | ||||

| Foreign | - | - | ||||||

| - | 3,644 | |||||||

| 13 |

United States of America

The Company is registered in the State of Nevada and is subject to the tax laws of the United States of America.

Malaysia

Egnitus (Malaysia) Sdn. Bhd. are subject to Malaysia Corporate Tax, which is charged at the statutory income tax rate of 24% on its assessable income.

Labuan

Egnitus International (L) Ltd are subject to Labuan Corporate Tax, which is charged at the statutory income tax rate of 3% on its assessable income.

Australia

Egnitus Holdings Pty Ltd and Egnitus Australia Pty Ltd are subject to Australian current tax law.

| As of, | ||||||||

| September 30, 2018 | December 31, 2017 | |||||||

| Income tax payable: | $ | 4,834 | $ | 18,045 | ||||

| Deferred tax liabilities: | ||||||||

| Plant and equipment | ||||||||

| Local | $ | - | $ | - | ||||

| Foreign | ||||||||

| Deferred tax liabilities | - | - | ||||||

| 9. | FOREIGN CURRENCY EXCHANGE RATE |

The Company cannot guarantee that the current exchange rate will remain stable, therefore there is a possibility that the Company could post the same amount of income for two comparable periods and because of the fluctuating exchange rate post higher or lower income depending on exchange rate converted into US$ at the end of the financial year. The exchange rate could fluctuate depending on changes in political and economic environments without notice.

| 10. | RELATED PARTY TRANSACTIONS |

| For the 9 months period ended September 30, 2018 | For the 9 months period ended September 30, 2017 | |||||||

| Purchased plant and equipment from: | ||||||||

| - Related party A | $ | - | $ | 89,673 | ||||

| - Related party B | - | 6,285 | ||||||

| - | 95,958 | |||||||

Related party A and B are the fellow companies in which common control through key shareholder of the Company.

The related party transactions are generally transacted in an arm-length basis at the current market value in the normal course of business.

| 14 |

| 11. | SUBSEQUENT EVENTS |

In accordance with ASC Topic 855, “Subsequent Events”, which establishes general standards of accounting for and disclosure of events that occur after the balance sheet date but before financial statements are issued, the Management has evaluated subsequent events noting the following transactions that would impact the accounting for events or transactions in the current period or require additional disclosures.

In October 23, 2018, Anvia Holdings Corporation entered into an acquisition agreement to acquire 100% of Entrepreneur Culture Ins Sdn. Bhd. shares for consideration of $60,074 and 65,455 shares of Anvia Holdings Corporation common stock.

In November 29, 2018, Anvia (Australia) Pty Ltd acquired 100% of shares issued and outstanding common shares from the shareholders of Eagle Academy Australia for consideration of $950,820.

In November 30, 2018, Anvia (Australia) Pty Ltd acquired 51% of the shares issued and outstanding common shares from shareholders of Jamiesons Accounting Pty Ltd for consideration of $696,129.

In December 10, 2018, Anvia Holdings Corporation acquired 100% of shares issued and outstanding common shares from shareholders of Doubleline Capital Sdn. Bhd. in exchange with 52,300 shares of Anvia Holdings Corporation common stock.

In December 28, 2018, Anvia Holdings Corporation acquired 100% of shares issued and outstanding common shares from shareholders of Blue Pacific English Academy Inc. for consideration of $27,110.

In December 28, 2018, Doubleline Capital Sdn. Bhd. acquired 100% of shares issued and outstanding common shares from shareholders of All Crescent Sdn. Bhd. for consideration of $130,166 and 200,000 shares of Doubleline Capital Sdn. Bhd. common stock

In December 31, 2018, Anvia (Australia) Pty Ltd acquired 100% of shares issued and outstanding common shares from shareholders of Workstar Technologies Pty Ltd for consideration of $211,380.

| 15 |